Abstract

This paper examines the restructuring of the Spanish financial system. This study is justified by the massive economic and social impact of this process in Spain. Based on the annual accounts and the annual reports of Spanish credit institutions, a model was created to predict the possibility of bank failure or bailout. The variables were selected following a review of the literature. They included the legal form of the credit institution (savings bank versus bank), leverage, real estate investment, gross operating margin, staff costs and non-performing loans. Two variables that had not previously been used in studies of this type were also included in the model: risk-weighted assets and coverage (as part of the provisions for non-performing loans). Fuzzy-set qualitative comparative analysis (fsQCA) was used for the analysis. Use of fsQCA is another novel aspect of this study. This technique has never been used to predict corporate bankruptcy or the failure of credit institutions. Proposals were made and tested using data on Spanish banks and savings banks for the year 2010, a critical year for the Spanish financial system. The results yield several interesting conclusions. First, greater leverage increases the probability of survival, contrary to the opinion of most scholars. This result shows that the problem facing Spanish credit institutions was the closure of international markets, not the level of debt. Another key conclusion is that financial institutions with higher staff costs have a greater chance of survival. Therefore, the widespread policy of reducing human resource costs should be reconsidered. Finally, the risk-weighted assets measure offers an excellent predictor of failure of credit institutions, as well as providing other benefits, which substantially increase the value of this measure.

JEL CLASSIFICATIONS:

1. Introduction

One of the most important results of the international economic and financial crisis of 2007 was the need to intervene by bailing out numerous credit institutions. Without these bailouts, the failure of these institutions would have been inevitable. These bailouts were the consequence of the difficulties faced by these entities, and the aim of these bailouts was to avoid the severe problems that the collapse of the financial system might have caused. The International Monetary Fund (IMF) estimates that the losses by credit institutions due to this crisis amounted to 2.5 trillion USD (Guindos et al., Citation2009), which indicates the enormous burden that such a situation can place on public funds.

This study is the first in a series of studies of bailouts in Europe. Despite this study’s European scope, a study of all European credit institutions would be too expansive for two reasons. First, each country applies its own regulations to credit institutions. This regulatory variation is reflected by, for example, differences in balance sheet structures. Second, the crisis did not affect all countries at the same time, so there were time lags in the intensity of the crisis in each country. Both reasons make it substantially more difficult to analyse the failure of credit institutions in several countries. Accordingly, this paper focuses on credit institutions in Spain.

Other scholars have adopted a similar approach. Davidovic et al. (Citation2019) focused on the efficiency of Romania’s banks after accession to the European Union. Fitri Sulaeman et al. (Citation2019) also studied the efficiency of banks in Indonesia, which follow an Islamic banking model. The case study by Costa-Climent and Martínez-Climent (Citation2018) also examined banks that have designed their activities and investments to contribute to sustainability through social and environmental responsibility and corporate social responsibility, with a special focus on Banco Santander in Spain.

The Spanish economic and financial crisis differs from that of other countries in two main ways. First, the crisis hit Spain later than it did elsewhere (Carbó Valverde & Maudos Villarroya, Citation2010; González Pascual & González González, Citation2012; Ontiveros & Berges, Citation2010). Second, a further crucial difference was the excess of real estate investment. With the introduction of the single currency, a new European capital market was formed. This new market encouraged the application of interest rates well below those that had existed previously (Sudrià, Citation2014), leading to an increase in credit. This increase in credit and the opening up of international financial markets increased the leverage of Spanish credit institutions, which had ratios of over 100. Moreover, the subprime mortgage crisis in 2007 triggered the closure of capital markets worldwide, just when Spanish credit institutions needed foreign financing the most to meet their short-term refinancing obligations. Finally, an added differentiating feature is the high degree of politicisation of savings banks (Azofra & Santamaría, Citation2004; Gutiérrez Fernández et al., Citation2013; Pérez-Ruiz & Rodríguez-Bosque, Citation2012). The idiosyncrasy of the Spanish crisis was aggravated by the questionable management by the Bank of Spain, the National Securities Market Commission and the Ministry of Economy (Ekaizer, Citation2018), as well as the European Banking Authority (EBA) and the presidents of the Spanish government (Climent-Serrano & Pavía, Citation2015). This management resulted in a cost to the Spanish public treasury of 64.349 billion euros, according to 2018 data from the Bank of Spain. This amount represented the largest public expenditure in developed countries. In macroeconomic terms, it equated to 6.5% of Spain’s GDP.

This serious situation led to a restructuring of the Spanish financial sector. Of the 45 savings banks that existed in 2009, only two remained in 2019, holding just 0.01% of the assets that were held by this group of institutions in 2009. Six of the savings banks that disappeared became banks, whilst the rest were either merged with or acquired by other credit institutions. Of the banks, only Banco Popular was acquired (by Banco Santander).Footnote1

Given the serious impact of the economic and financial crisis, particularly in Spain, this paper presents a model to predict bank failure and the consequent bailout of credit institutions. The justification for this choice of topic is the sheer size of the financial and social cost and the depth of the links with the entire global economy.

Fuzzy-set qualitative comparative analysis (fsQCA) was used to design the model to predict bank failure. The contribution of this study to the literature is twofold. First, although many studies have attempted to predict corporate bankruptcy (McKee & Lensberg, Citation2002), very few have tried to do so for credit institutions. The study by Serrano-Cinca and Gutiérrez-Nieto (Citation2013) is the only study that has examined crises faced by organisations in this sector. However, the study was conducted for the USA. No such study has been carried out for Spain. Second, no study has used fsQCA to predict the bankruptcy of any type of business. Thus, this study makes an interesting contribution to the literature.

Some of the results obtained are consistent with those presented by other authors in previous studies, namely the politicisation of the savings banks, problems due to real estate investment and defaults. However, other results differ from those found in the literature. Specifically, leverage and excess staff costs are found be advantages, not causes. In addition to these results, this study offers other new findings. For example, credit institutions with higher interest margins and higher fees and commissions have a better chance of survival. The same is true for well-prepared institutions with strong impairment provisions for non-payment.

In section 2, the propositions derived from the literature review are stated. Section 3 describes the method. Section 4 presents the results. Section 5 provides the conclusions. Section 6 outlines the limitations of this study.

2. Literature review

2.1. Studies of bankruptcy prediction

A thorough review of the literature reveals only one article (Serrano-Cinca & Gutiérrez-Nieto, Citation2013) that defines a model to predict the failure of financial institutions (in the United States) using partial least squares discriminant analysis (PLS-DA). Without actually predicting bank failure, Chabot et al. (Citation2019) identified the banks and groups of banks that could disrupt the UK financial system as a result of Brexit. In another context, Angori et al. (Citation2019) analysed the factors that determine margin, which was taken as an indicator of the health and stability of financial institutions. Since the outbreak of the global economic and financial crisis, difficulties in achieving sustainable profitability levels given banks’ interest margins have substantially increased the fragility of the European banking system. Meanwhile, Ji et al. (Citation2019) found that better credit supervision and a change in the market-based financial structure can reduce systemic risk in the banking sector.

Some studies have used fsQCA to study certain aspects of the financial sector. For example, Pinto and Picoto (Citation2018) analysed the effects of the 2008 economic and financial crisis and the sovereign debt crisis on the quality of financial information in European banks. A review of the literature on studies using fsQCA is provided by Roig-Tierno et al. (Citation2017).

Regarding companies in general, various theoretical models have been proposed to predict corporate bankruptcy. A notable model is the Altman Z-Score model, which uses the multiple discriminant analysis described by Postolov et al. (Citation2016).

McKee and Lensberg (Citation2002) applied a genetic programming algorithm to predict business failure, achieving 80% accuracy. The same method was used by Lensberg et al. (Citation2006) to study 28 significant bankruptcy variables with an accuracy of 81%. With the same objective, Alfaro et al. (Citation2008) compared two models: artificial neural networks and the AdaBoost algorithm.

Premachandra et al. (Citation2009) used non-parametric data envelopment analysis (DEA) to study business failure. Drawing upon research by De Andrés et al. (Citation2011), they used a hybrid system that combines fuzzy clustering and MARS.

Returning to the Altman Z-Score model, Altman et al. (Citation2014) reviewed the literature on the importance and effectiveness of the Altman Z-Score bankruptcy prediction model worldwide and explored its applications in finance and related areas. In a similar context, Ravi Kumar and Ravi (Citation2007) studied different techniques for predicting business failure. These techniques can be grouped as follows: (i) statistical techniques, (ii) neural networks, (iii) case-based reasoning, (iv) decision trees, (iv) operational research, (v) evolutionary approaches, (vi) rough set-based techniques, (vii) other techniques subsuming fuzzy logic, support vector machines and isotonic separation, and (viii) soft computing subsuming seamless hybridisation of all of these techniques.

This review of the different techniques used to predict business failure reveals an absence of studies using fsQCA. Therefore, the use of this technique in this study of bankruptcy is considered an interesting way to contribute to the literature.

2.2. Conditions

A literature review was performed to identify the main problems facing the Spanish financial system. Proposals were then developed to build the fsQCA model.

There are three types of credit institutions in Spain: banks, savings banks and credit cooperatives. This study focuses on the two most important types, namely banks and savings banks, which account for more than 90% of the market. Banks are private limited companies and can therefore issue shares to raise capital and increase their equity. In contrast, savings banks are non-profit foundations that are publicly owned and, consequently, cannot issue shares. Therefore, the only way to grow is by reinvesting their profits (Carbó Valverde, Citation2010).

From the end of the 20th century to the end of the 2010s, Spanish credit institutions, especially savings banks, grew considerably (Martín et al., Citation2018). This growth was unchecked, especially the growth of savings banks, which, in addition to growing internally, also expanded in areas of Spain where they had not previously operated. This growth was driven by the real estate bubble. Most financing came from the international wholesale markets, where there was excess liquidity and low prices. The way to meet the requirements of the Basel Accords was by issuing hybrid assets, such as subordinated debt and preference shares, because they counted as requirements in the Basel I and Basel II Accords. The international subprime mortgage crisis led to mistrust in international markets, so Spanish credit institutions, especially savings banks, had major difficulties in covering the short-term financing of long-term loans. This excessive growth also substantially weakened the core capital of savings banks. In addition, financing with hybrid assets led to other difficulties in both the wholesale and retail markets. Small investors panicked, and besides being unable to place any more debt, they demanded repayment of the principal, claiming that they had been misled into confusing perpetual debt with fixed terms. The supervisor, regulator and rating agencies failed to act appropriately. They were unable to assess the risk of the new financial products, and they offered misleading information to small investors, bringing into question their independence from the institutions whose issues they were rating (Calvo & Mingorance, Citation2012).

These factors were detrimental to the financial system in general but especially to the savings banks, which were forced to pay a high price to cover their resource needs. Thanks to their international presence, the large banks were able to diversify their risk and were affected to a lesser extent (Álvarez, Citation2008). The interest the credit institutions paid to meet their long-term commitments to finance property developers and mortgage customers was higher than the interest they received on those investments.

The problems were exacerbated by failures in the real estate sector. From 1994 onwards, Spain built 800,000 houses per year, primarily for speculation, because the actual demand was one third that amount (Berges & García Mora, Citation2009). The expansive monetary policy imposed by the other EU member states, the boost due to the adoption of the euro and confidence that the stable downward trend in interest rates would continue led to favourable expectations that caused a rise in house prices. Thus, the increase in credit was focused on the real estate sector, creating a wealth effect amongst the public and further inflating the housing bubble (Salas & Saurina, Citation2002).

Mortgages were granted with a loan-to-value (LTV) ratio above the appraised value of the mortgaged property. These mortgages violated the mortgage legislation, which sets the loan limit at 80% of the appraised value. This overreaching was observed passively by the Bank of Spain, which, as the supervisor, failed to take preventive measures. The credit institutions thus took on an excess of risk in their investments.

In addition, however, banks’ eagerness to beat the fierce competition led them to cut their interest margins to amongst the lowest in the eurozone. To increase their profits, they were forced to increase their turnover (García Montalvo, Citation2006; Keys et al., Citation2010), further raising their credit risk.

These actions, which were aimed at short-term profit without considering the long-term effects on institutional stability, led in part to the bailout of the Spanish financial institutions. Furthermore, the passive stance adopted by the Bank of Spain and the regulatory bodies meant that they were unable to adapt their control and supervision measures to avoid or at least minimise the impact of the crisis and reduce the size of the real estate bubble in a controlled manner. It is also important to recall that the European Central Bank, under the recommendations of the German institutions, was implementing an expansive monetary policy, with low interest rates and high liquidity.

Sevilla Jiménez et al. (Citation2017) linked the crisis to the housing bubble, highlighting the links between excessive economic and financial growth and the relaxing of controls in loan provision. According to García Montalvo and Raya, one cause of the relaxation in loan provision might be that the branch managers were receiving variable salaries that depended on the number of mortgages they sold. In addition, they had considerable discretion in decisions to grant loans, so only large requests were handled by the central committee of the financial institution.

When the real estate bubble burst, it proved particularly serious in Spain. Comparatively speaking, the number of risky investments was higher than in other countries. It did not occur at the same time either. In addition, the crisis in the financial sector was aggravated by the credit institutions, which, trusting that it would be a temporary situation, refinanced for three years the loans of property developers with a lack of capital and interest. In doing so, they avoided customer default whilst recording the interest that had been accrued but not paid as income in their accounts.

Growth financed with external resources significantly increased leverage, which became greater than 100%, lasted for more than a decade (Carbó Valverde et al., 2010) and caused imbalances, leading to losses in the value of banking assets (Maudos & Vives, Citation2016). This high leverage caused major problems, to such an extent that Miralles-Marcelo and Daza Izquierdo (Citation2011) reported that the Spanish banking system was undergoing a restructuring process as a result of the lack of liquidity in international markets because it could not finance the leverage. However, leverage, which most scholars criticise, is not in itself harmful. Using non-linear regression, Climent-Serrano (Citation2019) showed that leverage in the Spanish financial system can encourage the solid growth of credit institutions because, during periods of stability when access to financing is not a problem, non-performing loans do not grow, whilst credit institutions grow steadily.

The large number of loans to the real estate sector, with a high rate of default, had a major influence on income statements, which were further damaged by the spread of the crisis to almost all sectors (Álvarez, Citation2008). Between 2008 and 2012, losses before taxes amounted to 87.024 billion euros (almost 9% of Spanish GDP), and losses due to bad debts amounted to 240.483 billion euros (25% of Spanish GDP).

The non-performing loans ratio has evolved from historical lows to historical highs. shows the non-performing loans ratio for all Spanish credit institutions since 2000. From a long period of default rates of less than 2%, a sharp increase led to default rates of 14%. In addition, credit institutions were trying to reduce default in a variety of ways such as refinancing with several years’ grace for interest and capital. Other institutions were selling portfolios with high levels of default at the end of the year with a commitment to repurchase them at the beginning of the new year so that the annual accounts would show an artificially low rate of default.

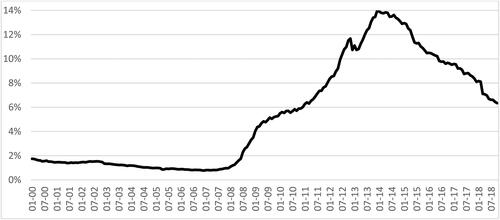

Figure 1. Non-performing loans ratio for Spanish credit institutions since 2000.

Source: Prepared by the authors.

Coverage is defined as the percentage of non-performing loans that are covered by provisions for impairment. This variable is so scarcely studied in the literature that no other studies were found to have examined this variable. Provisions for impairment when loans show signs that they may not be repaid is a guarantee for when default occurs. If the default is well covered, the credit institution will experience few problems in its annual accounts when the default occurs. Therefore, the higher these provisions are as a percentage of non-performing loans, the greater the guarantee will be that the credit institution can cover the defaults, and there will be a better chance of survival. In addition, Spain introduced generic provisions in July 2000. These provisions are made when the economy is performing well to create a cushion for when credit institutions are in poor health. These provisions are similar to the anti-cyclical buffers introduced in the third version of the Basel Accords. Therefore, in theory, Spanish credit institutions should have been better prepared than credit institutions in other countries. This was the case with some Spanish credit institutions. However, under the approval of the Bank of Spain, other institutions engaged in ill-advised and, moreover, illegal practices. These practices are colloquially known as pepas, or specific provisions pending assignment (Ekaizer, Citation2018). These pepas consist of reporting at book price the real estate classified as having non-payment issues, and then accounting for the difference between the book value and the amount actually paid, which is always lower, as provisions for impairment.

At the same time as the expansion of real estate credit, the branch network and the number of employees experienced rapid growth (Maudos & Vives, Citation2016), and the branch network became overstretched. Banks had major difficulties obtaining resources because of their exposure to real estate credit, and they faced considerable pressure on their income statements because of credit default (Gutiérrez Fernández et al., Citation2012). However, staff costs could affect the ability to raise funds at a better price through more personalised service for clients, as well as asset allocation by credit institutions at better returns. Clients that are used to personal treatment might accept a loan at a higher cost if they receive satisfactory personal service. A similar situation could arise with deposits or fixed-term investments at a lower cost if customers feel satisfied with the personal service they receive. Thus, even if staff costs are high, the savings in attracting debt and asset allocation could offset these costs or even lead to a higher return from greater investment in human resources.

The risk-weighted assets measure is the sum of each asset multiplied by its risk coefficient. In assets with low risk, the coefficient is less than 1, whereas in those with high risk, it is greater than 1. This measure is used to calculate the own funds required to cover the solvency ratio. However, including this variable in the model to forecast the survival of credit institutions is useful not because of its primary function but because it indirectly measures the quality of assets. A lower ratio means that the assets are of a higher quality. This feature makes this condition useful to predict the survival of credit institutions. Another valuable feature is that there are two ways of calculating risk-weighted assets. The first is to use the ratings of the rating agencies and the indications of the supervisor. The second is to use the internal ratings-based (IRB) system, which, as its name suggests, is based on the internal ratings that each credit institution calculates for each of its customers, subject to approval by the Bank of Spain. This form of calculation has another advantage because information on the quality (creditworthiness) of customers can provide a source of income through the trading of financial information on customers. Again, no study has been found to have used this variable to estimate the probability of survival of credit institutions.

Based on the review the literature, the proposal in this study is to forecast the survival of credit institutions. This outcome is expected to depend on the presence or absence of several conditions, which are described below.

Type of credit institution is operationalised as a dichotomous variable, where 0 indicates that the institution is a savings bank, and 1 indicates that it is a bank. As per the literature review, the presence of banks (i.e., the absence of savings banks) is expected to be associated with survival.

Leverage is operationalised as the ratio of loans to deposits. Higher ratios indicate greater external financing (international, wholesale, etc.). An absence of leverage is expected. However, given that greater investments mean greater returns, this situation depends on the ease of attracting financing in the wholesale markets.

Real estate investment is operationalised as real estate assets (property, land, etc.) owned by the credit institution (excluding loans to property developers and mortgages to customers) divided by assets. This condition is expected to be absent in surviving institutions.

Gross margin is the gross margin of the credit institution divided by its assets. This condition is expected to be present in surviving institutions.

The staff costs condition is operationalised as staff costs divided by assets. There are arguments for and against the absence of this condition in institutions that survive. On the one hand, absence might be expected because of the cost savings made by having low staff costs. On the other hand, presence might be expected if the productivity of human resources is higher than their cost.

Default is operationalised as doubtful assets divided by total credits. This condition is expected to be absent in surviving institutions.

The condition of risk-weighted assets is operationalised using data declared by each institution in its annual report or reports on prudential requirements. This condition is expected to be absent amongst surviving banks because lower ratios indicate higher quality assets.

Coverage is operationalised as the allowance for doubtful debts divided by doubtful receivables. This condition is expected to be present in surviving banks.

lists the fuzzy-set name assigned to each condition as per its code in the data set. A short description of each condition is also given.

Table 1. Description of conditions.

3. Sample and method

3.1. Sample

A data set was built using economic and financial information from the annual accounts and annual reports of Spanish banks and savings banks for the year 2010. The outcome and conditions are described in the previous section.

3.2. Method

Fuzzy-set qualitative comparative analysis (fsQCA) was used for the analysis. This technique tackles problems from the perspective of complex causality (Woodside, Citation2013). This is a novel approach in the prediction of bankruptcy, particularly for credit institutions. This method has several advantages over traditional techniques such as multiple linear regression analysis because not all real-world relationships between factors are simple, linear and complementary (Fiss, Citation2011; Ragin, Citation2008). The fsQCA method tackles problems from a complex causal perspective by considering the asymmetric relationships between observations. Thus, the combinations of conditions that lead to a given outcome (which may be thought of as the dependent variable) can be identified. The outcome here is the survival of credit institutions that have not been bailed out, acquired or merged with other institutions. The results of the analysis are expressed as a series of combinations known as configurations (Longest & Vaisey, Citation2008).

According to Huarng et al. (Citation2018), one of the key features of this method is the calibration of data to values between 0 and 1 (where 0 denotes full non-membership and 1 denotes full membership) to enable analysis of causal complexity. This method uses configurations of conditions, whereas conventional methods use independent variables. Finally, this method is based on set theory, whereas conventional methods are based on correlations.

Configurations are combinations of factors (or ‘conditions’ in the fsQCA terminology) that are minimally necessary or sufficient to obtain the desired outcome (Meyer et al., Citation1993), namely the survival of credit institutions. Necessary conditions are always present when this outcome occurs, and a condition is sufficient if the outcome occurs whenever that condition is present. However, with sufficient conditions, the outcome may also occur in the presence of other conditions (Woodside, Citation2013).

These qualitative comparative methods are designed to give meaningful results in studies that use small samples. Fiss (Citation2007, p. 1194) indicated that fsQCA is suitable for samples of 10 to 50 cases. The sample in this study contained 36 Spanish credit institutions. According to Huarng et al. (Citation2018), fsQCA successfully forecasts seasonal time series, despite the use of small data sets.

The following steps are followed to conduct fsQCA. First, calibration is carried out. The original variables are grouped according to their degree of membership to a certain condition set (Ragin, Citation2008). A score of 1 indicates full membership, and 0 indicates full non-membership. The cut-off point of 0.5 denotes ambiguous cases that have neither full membership nor non-membership.

Next, the truth table is produced to show all logically possible combinations of conditions or structural configurations (Fiss, Citation2011). From this table, the cases are assigned to the combinations according to their scores. Cases with a score of more than 0.5 are assigned to the corresponding combination, and Boolean logic is used to reduce and identify the combinations associated with the outcome (here, survival of credit institutions). Two parameters must be considered at this stage: coverage and consistency. Coverage indicates the empirical relevance of a solution (higher is better); consistency quantifies the degree to which cases that share conditions lead to the same outcome. Ragin (Citation2008) recommends a minimum consistency of 0.7 to be considered sufficient to indicate goodness of fit.

4. Analysis and results

FsQCA 3.0 software was used to carry out the analysis. First, the truth table was produced for the outcome (survival of the credit institution) based on the sample data. The conditions and the outcome were calibrated using three cut-off points at the 90th, 50th and 10th percentiles (Climent-Serrano et al., Citation2018) for each condition and the outcome. The 10th percentile indicates non-membership to the set; the 50th percentile indicates that the case is neither inside nor outside the set (i.e., it is ambiguous); and the 90th percentile reflects full membership to the set. Subsequently, the data were calibrated following Ragin’s (Citation2008) indications. The results of the calibration appear in .

Table 2. Calibration of conditions.

The analyses of necessity and sufficiency were then performed (). These concepts were introduced in the previous section. The necessity analysis shows whether necessary conditions exist. According to Schneider et al. (Citation2010), for a condition or combination of conditions to be necessary, it must have a consistency score of more than 0.9.

Table 3. Analysis of necessity for presence and absence of outcome.

The necessity analysis shows that there is no necessary condition. Therefore, bailouts or mergers and acquisitions, which were coded as lack of survival or ‘∼Survival’ (i.e., failure of the credit institution), do not occur because of any one single condition. A broad set of conditions must be present for the absence of survival.

Analysis of the reasons for the financial bailout of Spanish credit institutions shows that the condition with the highest consistency is being a savings bank (i.e., not being a bank). This condition has a coefficient of 0.80, which is close to the minimum required value of 0.9 (Schneider et al., Citation2010). In addition, the coverage of this condition is 0.73.

Other conditions also have high coefficients. Some of these are expected, such as the presence of default (coefficient = 0.66) and the absence of gross margin (coefficient = 0.63). However, the results for other conditions are unexpected. The absence of staff costs is relevant because the current policy of credit institutions is to reduce staff.

Another important observation regarding one of the conditions considered here for the first time is the role of risk-weighted assets. This condition is an excellent indicator for the prediction of the failure of credit institutions, whilst it also adds value and provides extra income.

Finally, leverage is a critical factor because of the high burden of responsibility that is attributed to this factor in relation to what has happened in the Spanish financial system. However, the results indicate that greater leverage means greater chances of survival. The reason Spanish credit institutions had to be bailed out was not leverage but the closure of international markets, which occurred outside the Spanish economy because it was an internal problem in the United States.

The causal relationships obtained in the different models of equifinality are shown below. There is more than one combination. The combinations that lead to bailout or mergers and acquisitions are shown. and present the combinations leading to the absence of survival (i.e., the combinations that mean that credit institutions must be bailed out or forcibly acquired).

Table 4. Details of the intermediate solution.

Table 5. Visual representation of the intermediate solution.

Default is a sufficient condition in all configurations that lead to the need for a bailout. Being a savings bank (i.e., not being a bank) is another condition that occurs in seven of the nine combinations for being bailed out. It is neither present nor absent in the other two. Absence of coverage is also a condition for being bailed out in six of the nine combinations. It is neither present nor absent in the other three. The other commonly occurring condition for being bailed out is the absence of a gross margin. The same applies to real estate investment, which is a condition for receiving a bailout.

There are three further conditions. These conditions provide additional value to this study. First, the absence of leverage is a condition for receiving a bailout. An entity must have high leverage not to be bailed out, contrary to what is indicated in the literature. The absence of staff costs is a condition for the bank to be bailed out. Institutions that invest in human resources are less likely to be bailed out. Finally, the risk-weighted assets measure, which is required by the Basel Accords, has many more applications, including offering a good indicator of the insolvency of credit institutions. Like certain other conditions, this measure appears in all three solutions.

The other two solutions, which are not shown, have similar parameters and robustness. The complex solution has a coverage of 0.579 and a consistency of 0.886, and the parsimonious solution has a coverage of 0.707 and a consistency of 0.825.

5. Conclusions

According to the International Monetary Fund, the recent profound financial and economic crisis has cost 2.5 trillion euros (Guindos et al., Citation2009) owing to the bailout of numerous credit institutions that governments have been forced to supply with funds to avoid a massive collapse of the financial system. This major setback justifies analysis of the causes of the crisis in a bid to prevent a repeat of a similar incident of the same or greater magnitude in the future.

However, despite abundant research devoted to predicting business failure, studies of how to predict the failure of credit institutions are virtually non-existent. Furthermore, none of these studies has used fsQCA to predict the failure of credit institutions or indeed any other kind of company.

The fsQCA results can be divided into three groups. The first consists of traditional variables that have played the role that was expected. The second is made up of variables that have recently appeared in the study of credit institutions. The third is the most interesting, consisting of variables that contradict the expected results according to what is reported in the literature.

The outcome (which can be thought of as the dependent variable) was the survival of credit institutions. This was defined as the absence of failure, which in turn was operationalised as the likelihood of receiving a bailout. The conditions considered in this study were type of credit institution (i.e., bank or savings bank), leverage (i.e., ratio of loans to deposits), investment in real estate and land acquisition, operating profit, staff costs, non-performing loans, risk-weighted assets, and coverage ratio.

The expected results include the finding that most combinations indicate that the absence of being a bank (i.e., being a savings bank) leads to the absence of survival (i.e., the bailout of the credit institution). This finding supports the literature, which shows the inadequate management of Spanish savings banks, especially due to the politicisation of the governing agencies.

The other three results that echo the conclusions reported in the literature are that non-performing loans, investment in real estate, and gross income play a role in bank failure or survival. The higher the rate of default is, the higher the probability of having to be bailed out will be. The same is true for investment in real estate and land acquisition. Finally, a higher gross margin is associated with a lower possibility of bailout.

The second block consists of the new variables: the coverage ratio and risk-weighted assets. The results indicate that credit institutions with a high coverage of doubtful assets are less likely to have to be bailed out. The risk-weighted assets measure is also an excellent predictor of the failure of credit institutions. Lower values of this ratio (i.e., poorer asset quality) mean that it is more likely that the credit institution will have higher quality assets. This variable, which is a requirement under the Basel Accords to estimate regulatory capital, is valuable for other reasons. For example, by studying the quality of customers to evaluate their investments, a large amount of valuable information can be obtained to be sold and to earn additional income.

Finally, two variables did not behave as expected according to the literature. The first is leverage, with results suggesting that credit institutions with higher leverage have a lower probability of needing to be bailed out. The evidence shows that over-leveraged banks have had more problems. However, this situation is not due to the leverage itself but rather to the abrupt closure of markets, which meant that banks with open positions faced major problems. Because leverage is advantageous for any entity, there are two possible solutions. The first is to develop mechanisms to ensure that the international financial markets function correctly, and the second is to require credit institutions to close their risk positions using hedging instruments such as swaps, fixed rate/adjustable preferreds (FRAPs) and options. The last condition is staff costs. The results show that credit institutions that invest more in human resources have less chance of being bailed out. These last two findings contradict the views of both the credit institutions and the European banking authorities, but it would be useful to reflect further on them.

The results may help prevent future bailouts such as those that have taken place in recent years. Above all, they can also help ensure that the countries that still have savings banks, such as Germany or Austria, do not fall victim to the same errors as those committed in Spain.

6. Limitations and future research

The lack of uniformity in different regulations, the intensity and temporality of the crisis, the variety in the structure of annual accounts, and the lack of an exhaustive, high-quality database prevent studies such as the present one from considering more than one country at a time. However, by applying the same method, scholars can perform similar studies with credit institutions from different countries so that the results might be compared. This is the first such study, but the intention is to replicate the research with credit institutions in other countries.

Disclosure statement

No potential conflict of interest was reported by the authors.

Notes

1 Banco de Valencia and Banco Pastor were considered savings banks because they belonged to and were run by savings banks and had consolidated accounts in the savings bank group.

References

- Alfaro, E., García, N., Matías Gámez, M., & Elizondo, D. (2008). Bankruptcy forecasting: An empirical comparison of AdaBoost and neural networks. Decision Support Systems, 45(1), 110–122. https://doi.org/https://doi.org/10.1016/j.dss.2007.12.002

- Altman, E. I., Iwanicz-Drozdowska, M., Laitinen, E. K., Suvas, A. (2014). Distressed firm and bankruptcy prediction in an international context: A review and empirical analysis of Altman’s Z-Score Model. Available at SSRN 2536340, https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2536340

- Álvarez, J. A. (2008). La banca española ante la crisis financiera. Estabilidad Financiera, 15, 21–38.

- Angori, G., Aristei, D., & Gallo, M. (2019). Determinants of banks’ net interest margin: Evidence from the Euro Area during the crisis and post-crisis period. Sustainability, 11(14), 3785. https://doi.org/https://doi.org/10.3390/su11143785

- Azofra, V., & Santamaría, M. (2004). El gobierno de las cajas de ahorro españolas [The governance of Spanish savings banks]. Universia Business Review, 2, 48–60.

- Berges, A., & García Mora, A. (2009). Las entidades de crédito ante la crisis. Economistas, 119, 139–150.

- Calvo, A., & Mingorance, A. C. (2012). Por una reforma ética del sistema financiero. Revista de Fomento Social, 266, 277–305.

- Carbó Valverde, S., & Maudos Villarroya, J. (2010). Diez interrogantes del sector bancario español. Cuadernos De Información Económica, 215, 80–105.

- Carbó Valverde, S. (2010). Presente y futuro del modelo de cajas de ahorros en España. CIRIEC-España, Revista de economía pública. Social y Cooperativa, 68, 167–182.

- Chabot, M., Bertrand, J. L., & Thorez, E. (2019). Resilience of United Kingdom financial institutions to major uncertainty: A network analysis related to the Credit Default Swaps market. Journal of Business Research, 101, 70–82. https://doi.org/https://doi.org/10.1016/j.jbusres.2019.04.003

- Climent-Serrano, S. (2019). Effects of economic variables on NPLs depending on the economic cycle. Empirical Economics, 56(1), 325–340. https://doi.org/https://doi.org/10.1007/s00181-017-1362-y

- Climent-Serrano, S., Bustos-Contell, E., Labatut-Serer, G., & Rey-Martí, A. (2018). Low-cost trends in audit fees and their impact on service quality. Journal of Business Research, 89, 345–350. https://doi.org/https://doi.org/10.1016/j.jbusres.2017.11.020

- Climent-Serrano, S., & Pavía, J. (2015). Determinants of profitability in Spanish Financial Institutions. Comparing aided and non-aided entities. Journal of Business Economics and Management, 16(6), 1170–1184. https://doi.org/https://doi.org/10.3846/16111699.2013.801881

- Costa-Climent, R., & Martínez-Climent, C. (2018). Sustainable profitability of ethical and conventional banking original article. Contemporary Economics, 12(4), 519–530. https://doi.org/https://doi.org/10.5709/ce.1897-9254.294

- Davidovic, M., Uzelac, O., & Zelenovic, V. (2019). Efficiency dynamics of the Croatian banking industry: DEA investigation. Economic Research-Ekonomska Istraživanja, 32(1), 33–49. https://doi.org/https://doi.org/10.1080/1331677X.2018.1545596

- De Andrés, J., Lorca, P., De Cos Juez, F. J., & Sánchez-Lasheras, F. (2011). Bankruptcy forecasting: A hybrid approach using Fuzzy c-means clustering and Multivariate Adaptive Regression Splines (MARS). Expert Systems with Applications, 38(3), 1866–1875. https://doi.org/https://doi.org/10.1016/j.eswa.2010.07.117

- Ekaizer, E. (2018). El libro negro. Espasa.

- Fiss, P. C. (2007). A set-theoretic approach to organizational configurations. Academy of Management Review, 32(4), 1180–1198. https://doi.org/https://doi.org/10.5465/amr.2007.26586092

- Fiss, P. C. (2011). Building better causal theories: A fuzzy set approach to typologies in organization research. Academy of Management Journal, 54(2), 393–420. https://doi.org/https://doi.org/10.5465/amj.2011.60263120

- Fitri Sulaeman, H. S., Mulyantini Moelyono, S., & Jubaedah, N. (2019). Determinants of banking efficiency for commercial banks in Indonesia. Contemporary Economics, 13(2), 205–218. https://doi.org/https://doi.org/10.5709/ce.1897-9254.308

- García Montalvo, J. (2006). Deconstruyendo la Burbuja: Expectativas de Revalorización y Precio de la Vivienda en España. Papeles de Economia Española, 109, 44–75.

- González Pascual, J., & González González, J. P. (2012). Las Cajas de Ahorros en el Sistema Financiero Español. Información Comercial Española, ICE Tribuna de Economía, 867, 141–157.

- Guindos, L., Martinez Pujalte, V., & Sevilla, J. (2009). Pasado, presente y futuro de las cajas de ahorro. Thomson Reuters.

- Gutiérrez Fernández, M., Palomo Zurdo, R., & Romero Cuadrado, M. (2012). La Expansión Territorial Como Factor Motivador de la Reestructuración del Sistema Financiero Español: El Caso de las Cajas de Ahorros y Las Cooperativas de Crédito Revesco. REVESCO. Revista de Estudios Cooperativos, 107, 7–34. https://doi.org/https://doi.org/10.5209/rev_REVE.2012.v107.38746

- Gutiérrez Fernández, M., Palomo Zurdo, R. J., & Fernández Barberís, G. (2013). Cajas de ahorros españolas: ¿una pretendida reordenación bajo criterios de racionalidad económica y social. Cuadernos de Economía y Dirección de la Empresa, 16(4), 250–258. https://doi.org/https://doi.org/10.1016/j.cede.2012.12.001

- Huarng, K. H., Rey-Martí, A., & Miquel-Romero, M. J. (2018). Quantitative and qualitative comparative analysis in business. Journal of Business Research, 89, 171–174. https://doi.org/https://doi.org/10.1016/j.jbusres.2018.02.032

- Ji, G., Kim, D. S., & Ahn, K. (2019). Financial structure and systemic risk of banks: Evidence from Chinese reform. Sustainability, 11(13), 3721. https://doi.org/https://doi.org/10.3390/su11133721

- Keys, B., Tanmoy, M., Amit, S., & Vikrant, V. (2010). Did securitization lead to Lax screening? Evidence from subprime loans. Quarterly Journal of Economics, 125(1), 307–362. https://doi.org/https://doi.org/10.1162/qjec.2010.125.1.307

- Lensberg, T., Eilifsen, A., & McKee, T. E. (2006). Bankruptcy theory development and classification via genetic programming. European Journal of Operational Research, 169(2), 677–697. https://doi.org/https://doi.org/10.1016/j.ejor.2004.06.013

- Longest, K. C., & Vaisey, S. (2008). Fuzzy: A program for performing qualitative comparative analyses (QCA) in Stata. The Stata Journal: Promoting Communications on Statistics and Stata, 8(1), 79–104. https://doi.org/https://doi.org/10.1177/1536867X0800800106

- Martín, E., Bachiller, A., & Bachiller, P. (2018). The restructuring of the Spanish banking system: Analysis of the efficiency of financial entities. Management Decision, 56(2), 474–487. https://doi.org/https://doi.org/10.1108/MD-04-2017-0292

- Maudos, J., & Vives, X. (2016). Banking in Spain. In T. Beck & B. Casu (Eds.), The Palgrave handbook of European banking (pp. 1–35). Palgrave Macmillan. https://doi.org/https://doi.org/10.1057/978-1-137-52144-6_22

- McKee, T. E., & Lensberg, T. (2002). Genetic programming and rough sets: A hybrid approach to bankruptcy classification. European Journal of Operational Research, 138(2), 436–451. https://doi.org/https://doi.org/10.1016/S0377-2217(01)00130-8

- Meyer, A. D., Tsui, A. S., & Hinings, C. R. (1993). Configurational approaches to organizational analysis. Academy of Management Journal, 36(6), 1175–1195. https://doi.org/https://doi.org/10.2307/256809

- Miralles-Marcelo, J. L., & Daza Izquierdo, J. (2011). La reestructuración de las Cajas de Ahorro en el Sistema Bancario español. Boletín de la Real Academia de Extremadura de Las Letras y Las Artes, 19, 507–557.

- Ontiveros, E. A. & Berges, (2010). Cajas y bancos la gestión de la crisis. Economía Exterior, 54, 28–29.

- Pérez-Ruiz, A., & Rodríguez-Bosque, I. (2012). La imagen de Responsabilidad Social Corporativa en un contexto de crisis económica: el caso del sector financiero español. Universia Business Review, 33, 14–29.

- Pinto, I., & Picoto, W. N. (2018). Earnings and capital management in European banks - Combining a multivariate regression with a qualitative comparative analysis. Journal of Business Research, 89, 258–264. https://doi.org/https://doi.org/10.1016/j.jbusres.2017.12.034

- Postolov, K., Milenkovic, I., Milenkovic, D., & Iliev, A. J. (2016). Influence of market values of enterprise on objectivity of the Altman Z-model in the period 2006-2012: Case of the Republic of Macedonia and Republic of Serbia. Journal of Central Banking Theory and Practice, 5(3), 47–59. https://doi.org/https://doi.org/10.1515/jcbtp-2016-0019

- Premachandra, I. M., Bhabra, G. M., & Sueyoshi, T. (2009). DEA as a tool for bankruptcy assessment: A comparative study with logistic regression technique. European Journal of Operational Research, 193(2), 412–424. https://doi.org/https://doi.org/10.1016/j.ejor.2007.11.036

- Ragin, C. C. (2008). Redesigning social inquiry: Fuzzy sets and beyond. University of Chicago Press.

- Ravi Kumar, P., & Ravi, V. (2007). Bankruptcy prediction in banks and firms via statistical and intelligent techniques – A review. European Journal of Operational Research, 180(1), 1–28. https://doi.org/https://doi.org/10.1016/j.ejor.2006.08.043

- Roig-Tierno, N., Gonzalez-Cruz, T. F., & Llopis-Martinez, J. (2017). An overview of qualitative comparative analysis: A bibliometric analysis. Journal of Innovation & Knowledge, 2(1), 15–23. https://doi.org/https://doi.org/10.1016/j.jik.2016.12.002

- Salas, V., & Saurina, D. (2002). Credit risk in two institutional settings: Spanish commercial and saving banks. Journal of Financial Services Research, 22(3), 203–224. https://doi.org/https://doi.org/10.1023/A:1019781109676

- Schneider, M. R., Schulze-Bentrop, C., & Paunescu, M. (2010). Mapping the institutional capital of high-tech firms: A fuzzy-set analysis of capitalist variety and export performance. Journal of International Business Studies, 41(2), 246–266. https://doi.org/https://doi.org/10.1057/jibs.2009.36

- Serrano-Cinca, C., & Gutiérrez-Nieto, B. (2013). Partial least square discriminant analysis for bankruptcy prediction. Decision Support Systems, 54(3), 1245–1255. https://doi.org/https://doi.org/10.1016/j.dss.2012.11.015

- Sevilla Jiménez, M., Torregrosa Martí, T., & Núñez Romero, M. (2017). La información financiera y bancaria oficial y la última crisis económica (1999-2012). El Caso Del Banco de España. Estudios de Economía Aplicada, 35(3), 583–610.

- Sudrià, C. (2014). Las crisis bancarias en España: Una perspectiva histórica. Estudios de Economía Aplicada, 32(2), 473–496.

- Woodside, A. G. (2013). Moving beyond multiple regression analysis to algorithms: Calling for adoption of a paradigm shift from symmetric to asymmetric thinking in data analysis and crafting theory. Journal of Business Research, 66(4), 463–472. https://doi.org/https://doi.org/10.1016/j.jbusres.2012.12.021