?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study examines the impact of rule of law and government size under the dimensions of economic freedom to the social and financial efficiency of microfinance institutions (MFIs) from Thailand, Philippines, Malaysia, Indonesia, and Cambodia 2011 to 2018. The Data Envelopment Analysis (DEA) approach has been applied to identify the efficiency level of MFIs. At the same time, the Pooled Ordinary Least Square (PoOLS) and Generalized Least Square (GeLS) methods comprising the Fixed Effect (FEMod) and Random Effect (REMod) models are used to examine the impact of dimensions of economic freedom and potential determinants on the efficiency level of MFIs. Overall, the results revealed that the technical efficiencies for both social and financial efficiency are contaminated by managerial inefficiency, which is measured by pure technical efficiency. This indicates, although the MFIs had been operating on a relatively optimal scale, they were facing the inefficiency from the managerial side. Besides, the results from the panel regression analysis have implied that both property rights and government integrity under the measurement of rule of law positively influence the MFIs’ financial efficiency. Meanwhile, the impact of government size shows both tax burden and government spending are significantly positive to the social efficiency of MFIs. As the policy implication, the information provides suggestion to the government on how its role can help in improving the efficiency level of MFIs and implements some useful initiatives to help MFIs to sustain in the long term. In addition to that policymakers can identify the relevant inputs of MFIs and thus revise the policy accordingly and design new policies and regulations based on different economic freedom dimensions. The results of the present study provide a reference to guide them in decision making on their investments. For academicians or researchers, they can obtain more information regarding the efficiency of MFIs that is valuable for further research or study.

1. Introduction

Microfinance institutions (MFIs) play an important role in providing financial needs to those who cannot get financial services from the financial institutions since their main objective is to serve and deliver any financial needs to low-income groups (Shu & Oney, Citation2014). Nevertheless, there is a significant shift in emphasis from the social objective of poverty alleviation towards the economic objective to maximize the profit to ensure their sustainability (Khan et al., Citation2017; Rauf & Mahmood, Citation2009). The huge transformation on social to economic objective accelerated due to the changing on the current scenario since priory MFIs were being sponsored and financed by donors, but due to reducing the number of donors leads to the limited financial sources, and it creates difficulties to them to sustain and provide services (Kovacova et al., Citation2019; Wagner & Winkler, Citation2013). Therefore, MFIs now have to carry out the mission of poverty alleviation and economic growth on their basis, and they should have a wise balance between these two.

Nowadays, the MFIs are unique in the financial world with double line bottom impact, which refers to social benefits and financial performance (Widiarto & Emrouznejad, Citation2015). The efficiency of MFIs is the measurement of how well the inputs are allocated to produce optimal inputs (Bassem, Citation2008). MFIs consist of two types of efficiencies, which are social and financial efficiency. Social efficiency refers to the effectiveness of MFIs in providing loan portfolio to outreach the society and help to minimize poverty. Meanwhile, financial efficiency refers to the ability of MFIs in generating revenue and profit from their financial activities so that they can maintain their operations.

Some reasons argue that MFIs should be efficient in their operations. The presence of other organizations creates strong competition and some challenges to MFIs. Variety of choice, high performance and quality services will be the primary considerations for people. Hence, MFIs must possess efficiency in both financial and social so that they can compete with commercial banks. Besides, the assets of MFIs are mainly from the donations. The limited resources of MFIs will affect their ability to reach and serve more people. Thus, MFIs must be able to cover the costs incurred for ensuring their sustainability. Therefore, the linkage of financial sustainability and achievement for social objectives are very strong as MFIs must be efficient in social and financial dimensions.

Nowadays, many countries concern about their economic freedom index in their country because it consists of different dimensions or factors that will impact the social and economic growth of a country. Those who lack financial freedom will mostly condemn to poverty. This will indirectly link the operations of MFIs with the activities of society. Besides, economic freedom also contributes to the effort of reducing the poverty of a country that is the primary objective of MFIs, and it also reduces poverty. Hence, there will be a unique association of MFIs with economic freedom.

Besides, different factors will impact on the performance of microfinance. In many studies, economic and organizational indicators such as MFIs’ legal status, regulation and corporate governance are used to explain the microfinance performances (Cull et al., Citation2011). Another study by Akhter (Citation2018) found out that loan lending system, motivation of employee, proper management system, effective risk management technique and government regulatory framework can affect to the MFIs as well. Effect of economic freedom on these various factors will change the ways where they affect MFIs as well.

The rule of law in a country is important to the contribution of economic growth. Regulations and policies by the government may impact the operations of different institutions as well as MFIs. The development of microfinance institutions depends on a regulatory framework as a supportive factor (Boateng & Agyei, Citation2013). According to Cull et al. (Citation2011), the rapid growth of MFIs has urged to the calls for regulations. Regulation can enable MFIs to take deposits like commercial banks and expand their banking functions. However, compliance with regulation is seen to be a higher cost to MFIs.

According to Afonso and Jalles (Citation2011) and Bilan et al. (Citation2020), government can affect the economic development of a country. The size of government can be measured from different views such as in term of government spending and tax burden (Androniceanu et al., Citation2019; Ginevicius, Citation2019; Ślusarczyk, Citation2018). The activities of government can heavily influence the economic growth of the country. The effect of big government could be reduced through economic openness and sound economic policies. Some of the banking institutions will also affect if the tax exerted by the government is increased.

For MFIs to sustain in a country, many factors need to be considered wisely. Many issues could have different challenges for MFIs to operate efficiently. However, there are limited studies on the impact of economic freedom on the efficiency of MFIs. Due to the limitations, this study aims to contribute useful findings on the efficiency of MFIs operating in the selected countries such as Thailand, Philippines, Malaysia, Indonesia and Cambodia, and it obtains new empirical findings from the impact of rule of law and government size.

Therefore, the contribution of this study can be divided into two parts, theoretical and practical significance. In theoretical part, this study can extend the knowledge on the impact of economic freedom indicators on the efficiency of MFIs. Besides, the Cobb Douglas Production Theory, Laissez-Faire Economic Theory and Agency Theory can improve the understanding of different factors toward the efficiency of MFIs. Meanwhile, for the practical contribution, the empirical findings of this study will give a better figure about the impact of MFIs specific determinants, macroeconomic determinants and economic freedom indicators on the efficiency of MFIs. The findings can provide information that can benefit different parties such as MFIs, government, policymakers, investors and academicians. The results from this study can set the benchmark for MFIs on how to increase the efficiency level. The study indicates what factors should MFIs focus while delivering on their functions, thus, it can ensure their efficiency in terms of financial and social. The government will be beneficial as more suggestions can be obtained on how its role will affect the efficiency of MFIs and help to increase the sustainability of MFIs in the long term. Moreover, policymakers can identify what inputs will relevant to the efficiency and thus, they can revise the policy based on appropriate inputs. The results can serve as a reference to guide the investors in decision making on their investments. For academicians or researchers, they can obtain more information regarding the efficiency of MFIs that is valuable for further research or study

To do so, this study gathers and analyses data on a total of 167 MFIs operating in both countries, and the study period is from 2011 to 2018. The study consists of two main stages. In the first stage, this study identifies both social and financial efficiency of MFIs using the Data Envelopment Analysis. In the second stage, this study adopts a multiple panel regression analysis frameworks based on the Pooled Ordinary Least Square (PoOLS) and Generalized Least Square (GeLS) methods comprising the Fixed Effect (FEMod) and Random Effect (REmod) models to examine the impact of rule of law and government size to the social and financial efficiency of MFIs

The paper is arranged as follows: In the section 2, this study provides some reviews of the related literature. Section 3 explains the methods used and variables included in this study. The findings of this study will be presented in section 4. Lastly, section 5, the paper concludes the findings and provides discussions on the limitations and implications of the study.

2. Literature reviews

Numerous of studies stated the MFIs role is focusing on the social performance by alleviating the poverty via assisting the poor people by providing them a platform for the financial service since they are not entitled or do not have access to deal with the financial institutions (Rauf & Mahmood, Citation2009).

Hussain et al. (Citation2020) examine the MFIs social and financial efficiency with the impact of the competition freedom in Cambodia, Malaysia, Indonesia, Thailand and Philippines over the years from 2011 to 2017. The findings conclude that the overall social efficiency of MFIs is significantly less efficient than financial efficiency except for the MFIs in Thailand. Furthermore, the inefficiencies of both MFIs social and financial efficiency are contributed by the managerial inefficiency that measured by pure technical inefficiency. It indicates that the managements of MFIs do not fully utilize the resources and effect to the wastage.

The similar result on social and financial efficiency also discovered by Zainal et al. (Citation2020). They investigate the efficiency of the 168 MFIs from Southeast Asian Countries with the impact of banking regulation and supervision. In general, they find that the level of financial efficiency in the MFIs is significantly higher than social efficiency, and this indicates that the MFIs prefer and more concern on pursuing financial stability.

The study by Zainal et al. (Citation2019) examines the efficiency of the MFIs in five selected ASEAN countries, and they concluded the overall years from 2011 to 2017. The social efficiency of MFIs is relatively low due to the managerial inefficiency, and they need to focus more on the managerial side to improve the performance.

The research of Wagner and Winkler (Citation2013) indicates that the MFIs are no longer depending on the subsidized and donors to finance the financial service activities that lead them to generate their revenue income via offering various banking products. In fact, MFIs, nowadays, require running the model of dual characteristics focusing on social outreach to reduce poverty and financial stability to ensure sustainability in providing financial services to poor people.

Widiarto and Emrouznejad (Citation2015) assert the MFIs undertake the dual role on alleviating the poverty and to have financial sustainability to ensure the going concern on providing financial services to the poorest. They study the social and financial performance between Islamic and conventional MFIs in Middle East, North Africa, East Asia, South Asia and Pacific. The results show that the conventional MFIs outperform rather than Islamic MFIs where the financial efficiency is higher than social efficiency. This indicates that the conventional MFIs have seriously moved forward to give more priority on generating the revenue and profit to ensure that, they may sustain and capable of providing sufficient financial sources efficiently to the poorest.

Khan et al. (Citation2017) examine the contemporary controversies related to the practices of the dominant of MFIs that are focusing on the alleviation of poverty in the developing areas by using the primary data from respondents in North-Western Pakistan. The findings revealed that the current MFIs have shifted their main focus from poverty reduction to the more secure and profitability advance that indicates the MFIs are now trying to give priority on financial rather than social efficiency. The research by Lebovics et al. (Citation2016) also found that financial efficiency is higher than social efficiency in the Vietnamese MFIs that has been measured by the technical efficiency. They also show that the financial and social efficiency of Vietnamese MFIs are not mutually exclusive in view of implicit subsidies by the state and international donors. However, the higher financial efficiency could facilitate the MFIs to achieve and attain the social goals.

Tahir and Tahrim (Citation2013) reported the efficiency analysis of MFIs in five countries in ASEAN, which are Indonesia, Philippines, Vietnam, Cambodia and Laos. MFIs in Indonesia, Cambodia, Philippines and Vietnam have low managerial efficiency than scale efficiency. This indicates that they are inefficient in controlling costs rather than operating at the wrong scale. In contrast, Laos shows a higher managerial efficiency rather than scale efficiency, which means it is operating at the wrong scale rather than producing below the production frontier.

Previous studies also examine the impact of MFIs specific characteristics on the efficiency of MFIs. In the study of Mia and Soltane (Citation2016), the result of the finding has shown that there is a statically significant positive relationship between the profitability (ROA) and efficiency of MFIs. The result is similar to the findings of Iqbal et al. (Citation2019), which also support that there is a highly significant positive relationship in ROA and efficiency of MFIs due to greater facilities provided to customers, efficient in management and advanced technologies in operation. The MFIs could give facilities to attract more customers into the business by using the advanced technology in their operations such as the latest technology from physical to digital payment using the mobile wallet approaches (Alaeddin et al., Citation2018).

Ayayi and Sene (Citation2010) found that there was a positive and significant relationship between the age and efficiency of MFIs. This indicates that the mature and experienced institutions in the microfinance sector will increase the efficiency of MFIs by using efficient management tools such as efficient loan delivery implementation and good credit risk management. This result was supported by the study of Lebovics et al. (Citation2016), which showed that the age of MFI is positively associated with the financial efficiency of MFIs.

Qayyum and Ahmed (Citation2006) identified the impact of size (measured by total assets) on the efficiency of MFIs. From the result of the study, it indicates that the size of institutions has a positive relationship with efficiency in terms of both technical and pure technical efficiencies. They concluded that the size is an important determinant of efficiency of MFIs. However, the study of Bibi et al. (Citation2018) has shown that the size of MFIs is negatively associated with social performance. This is because as the MFIs getting bigger, they have shifted their objectives towards commercialization instead of focusing on helping the poor. Efendic and Hadziahmetovic (Citation2017) also found out that small MFIs have achieved better social and financial efficiencies than large and medium MFIs. This is because small MFIs can monitor well their small number of clients.

The impact of macroeconomics to MFIs efficiency has been conducted by Bibi et al. (Citation2018). The study shows a positive and significant relationship between inflation rate and the performance of MFIs as more borrowers still can be reached even in a high inflationary environment. In the study of Kamarudin et al. (Citation2016), they also found that inflation rate has a positive relationship with the profitability of both small and big banks. When the inflation rate is increased, banks will impose high servicing charges on their customers. The research of Zamore (Citation2018) stated that the GDP indicator shows a positive and significant relationship to the efficiency of MFIs. Besides, the result of Mia and Soltane (Citation2016) also reported that the relationship between the GDP and the productivity of MFIs is positive and significant. This implied that the efficiency level of MFIs increased due to the high demand for microfinance products and services such as deposits, the lower the probability of loan default and lower rates of inflation and unemployment.

Meanwhile, several studies have examined the impact of rule of law and government size under the dimensions of economic freedom to the MFIs’ efficiency. Aghion and Morduch (Citation2004) reported that MFIs can only provide effective financial intermediation through the present of well-functioning regulatory framework. Besides, the improvement of policy environment will lead to overall performance of institutions itself. The rule of law can be measured by components of property right and government integrity, while the government size can be measured by components of government spending and tax burden (Sufian & Shah Habibullah, Citation2014).

A study on property right by Akhter (Citation2018) mentioned that the government regulatory framework represents the extent to which a country’s legal framework allows individuals to acquire, hold, and utilize private property, secured by clear laws that the government enforces effectively to measure the property right. This study showed a significance relationship between the government regulatory framework performances of MFIs. Meinzen-Dick et al. (Citation2009) also suggest that legislation could alleviate poverty by providing the security of property owns by the poor people. In the study of Chortareas et al. (Citation2016), they have also examined on effect of property rights under economic freedom components towards the efficiency of bank. From the study, it shows a positive and significant relationship between property rights and bank efficiency. They claimed that the protection of property rights could contribute to higher openness level, which would lead to higher efficiency levels.

Several studies examine the impact of government integrity to MFIs efficiency. Majumdar and Marcus (Citation2001) stated that the well-designed regulations used for government integrity have a positive impact with productivity while less well-designed regulations have a negative impact and the similar results found by Akhter (Citation2018), Boateng and Agyei (Citation2013), Chortareas et al. (Citation2012) and Aghion and Morduch (Citation2004). They used the regulation variable as the proxy of systemic corruption of government institutions and decision-making by such practices as bribery, extortion, nepotism, cronyism, patronage, embezzlement, and graft to measure the government integrity. The results indicate that the higher government integrity will ensure greater transparency and free from the corruption that contributes to the higher MFIs efficiency.

In the study of Chortareas et al. (Citation2016), they examined the effect of government size that can be measured by government spending and tax burden under economic freedom towards the bank efficiency in US state banking. The result has shown a negative and significant relationship between government size and bank efficiency. Chortareas et al. (Citation2016) reported that inefficiency would be occurred due to excessive government spending. Therefore, the efficient spending by the government could improve the MFIs efficiency since huge financial allocation can be grant and subsidize to the MFIs. The spending of governments is not equally harmful to economic freedom; still, it gives the benefits to the community by providing the infrastructure and public goods, funding research or improving human capital, which is considered as the investment. Generally, most of the government spending will be financed by a higher tax rate and occurred an opportunity cost.

In the study of Carlos Díaz-Casero et al. (Citation2012), the finding showed that the government size is positive and significantly associate with the index of entrepreneurial activity. The tax burden and efficiency claim a positive relationship because the government taxes on income of both an individual and business level are lower and the percentage of GDP from the tax revenue would be smaller. Thus, the efficiency level of MFIs increased as the index of entrepreneurial activity of a country increased due to the lower tax imposed. Besides, the study reported that a tax regulation with the provision of exemptions of tax, incentives of tax, free registration of tax and tax rates reduction can improve the efficiency and sustainability of MFIs (Duve et al., Citation2017). The researchers suggested not to tax heavily on the MFIs due to the primary objective of MFIs that is to alleviate poverty, and the government should provide a less tax burden to the MFIs.

Thus, there are some research gaps revealed from the above literature. Therefore, this study is carried out with the purpose to fill up the research gaps. Firstly, there is little study on the comparison between social and financial efficiency. This study tries to compare both the social and financial efficiency in terms of technical efficiency, pure technical efficiency and scale efficiency. For the specific characteristics determinants of MFIs and macroeconomic determinants, most of the studies only focus on banking sector, but this study tries to focus on the MFIs sector. The main core of this study is on the impact of rule of law and government size under the economic freedom on the efficiency of MFIs. Although there are few studies discuss the economic freedom, it is focussed on the overall impact of economy that discusses without specific on each component.

3. Methodology

This study gathers data from a total of 167 MFIs from Thailand, Philippines, Malaysia, Indonesia and Cambodia over the period from 2011 to 2018. The financial data used in this study is obtained from MIX (Microfinance Information Exchange), a non-profit organization, web-based microfinance information platform, which provides reliable and timely performance information on MFIs (https://www.themix.org/). MIX market offers instant access to financial and social performance information of around 2000 MFIs around the world. The data for macroeconomic determinants is obtained from International Monetary Fund (IMF), an international organization of 189 countries (https://www.imf.org/external/). Besides, the data for economy freedom components are gathered from Heritage Foundation’s Index of Economic Freedom, an annual index and ranking of 186 countries published by the Heritage Foundation (https://www.heritage.org/index/), which created in year 1995.

3.1. Data envelopment analysis approach in 1st stage analysis

The non-parametric Data Envelopment Analysis (DEA) method was used in the first stage of analysis in this study. It is a mathematical-based programming model developed by Charnes et al. (Citation1978). It is known as CCR model, which is the extension of a single input-output production efficiency model (Farell, 1957). Banker et al. (Citation1984) then extend the CCR model to BCC model characterized by variable returns to scale (VRS).

CCR model can measure the overall efficiency or technical efficiency (TecE) of a DMU under Constant Return to Scale that represents as managerial efficiency. After all, the BCC model introduced by altering the CCR model by applying more realistic assumptions of Variable Return to Scale (VRS) Model. Therefore, BCC model using VRS is much suitable to measure the efficiency as different size of MFIs may have different efficiency (Widiarto & Emrouznejad, Citation2015). Pure technical efficiency (PTecE) and scale efficiency (ScaE) are the two decompositions of TecE under BCC model. PTecE measures purely managerial of MFIS without contamination of scale or size. On the other hand, ScaE is the measurement of efficiency on the impact of scale size of MFIs

VRS model:

(1)

(1)

where N1 is an N × 1 vector of ones.

3.2. Inputs and outputs variables under DEA

As discussed in the previous part, MFIs are considered efficient if it can produce a higher level of output with the usage of few inputs. The selection of appropriate inputs and outputs is significant in determining the efficiency of MFIs (Chortareas et al., Citation2012). For this analysis, under the social efficiency, two outputs consist of a number of borrowers (y1), which includes a number of actual borrowers; loan balance (y2), which consists of the average loan balance per borrower over the gross national income per capita. Meanwhile, for the financial efficiency, single-output used which is revenue (y1) measured by the total revenue generated from gross loan portfolio, including margin charge for a loan.

However, same four inputs selections used for both social and financial efficiency namely total assets (x1), which include fixed and current assets available to MFIs from capital or borrowings; operating expenditure (x2), which includes all operating expenses; labour (x3) consists of total labours’ salaries and leverage (x4) that include and the last is deposit (x2) include deposit from customer and the other banks.

Two approaches can be employed while assessing the efficiency of MFIs, and they are intermediation and production approaches. The selection of approach depends on the views towards MFIs (Berger & Humphrey, Citation1997; Sufian & Kamarudin, Citation2014). For intermediation approach, MFIs are considered as intermediaries who collect deposits and make loans to the poor or deficit units. It can also be defined as an intermediary between surplus units and deficit units. For production approach, MFIs are considered as producers of deposits, and they make loans to the poor or deficit units. The MFIs use their assets to generate deposits or loans. Several studies have adopted production approach in their research (Bassem, Citation2008; Kamarudin et al., Citation2017; Tahir & Tahrim, Citation2013). For this study, the intermediation approach is adopted. This is because MFIs are much suitable to classified as an intermediary where they obtain deposits and funds from others and give out as loans to the poor.

3.3. Multiple panel regression in 2nd stage analysis

This study employed the Pooled Ordinary Least Square (PoOLS) and Generalized Least Square (GeLS) methods comprising of Fixed Effect (FEMod) and Random Effect (REMod) in second stage analysis to examine the determinants of MFIs specific characteristics, macroeconomic conditions and the impact of economic freedom components. The decision is made following Gujarati’s (Citation2002) suggestion that GeLS as the robustness check since this estimation method may overcome the heteroscedasticity, resulted from utilising financial data with differences in sizes. Since the sample employed in this study consists of small and large MFIs, differences in sizes of the observations are expected to be observed. The regression model is estimated by using the White (Citation1980) transformation, which is robust to heteroskedasticity and the distribution of disturbances in the second stage regression analysis where involving DEA efficiency scores as the dependent variable. Thus, the baseline regression model is generated as below:

(2)

(2)

where the social (lnSocE) and financial (lnFinE) efficiency scores derived from the DEA method, MFIs specific characteristics (lnROAA, lnAGE, lnTOA), Macroeconomics (lnINF, lnGDP) a set of rule of law (lnPR, lnGI), government size (lnGS, lnTB), ε the error term, and subscripts,

j and

represent individual MFIs, country and period, respectively.

Step-wise multiple regression analysis is adopted in the second stage to avoid the problem of multicollinearity (Hussain et al., Citation2019, Citation2020). Moreover, the log-linear form is performed to reduce simultaneity bias and improve the goodness of fit. Breusch and Pagan Lagrangian Multiplier test is conducted before the results are based on any models to identify either the data appropriate to be pooled or panel. Furthermore, the selection of estimation method of FEMod and REMod regression is determined based on Hausman test.

3.4. Description of variables used in multiple panel regression analysis

In the panel regression model, this study includes four MFI specific, two macroeconomic determinants variables and two dimensions of economic freedom that consists of a total of four components. Each of economy freedom components is measured by the score graded from 0 to 100 where higher value associated with higher freedom in economic. Details of descriptions of all variables used in the regression model are shown in .

Table 1. Descriptions of MFIs specific, macroeconomic and economic freedom variables.

Two dimensions of economic freedom are introduced, which are rule of law and government size. Under rule of law, it consists of property rights and government integrity. Meanwhile, under government size, it consists of government spending and tax burden.

4. Results and discussion

4.1. Social and financial efficiencies of MFIs

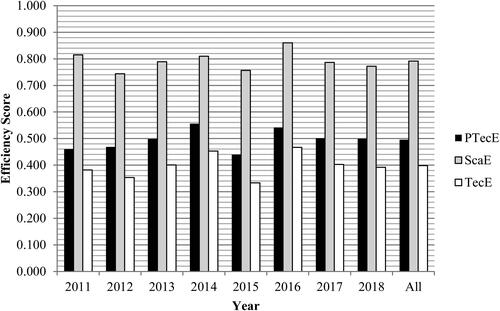

shows the descriptive statistics of MFIs social and financial efficiency for all five countries from 2011 to 2018, including the all years analysis. For the overall efficiency or technical efficiency (TecE) of social efficiency (SocE), the average shows a fluctuation score over the years from 2011 to 2018 ( and ). The highest TecE score recorded in 2016 (46.7%) and the lowest at 33.3% during 2015. The results suggested that for the SocE, the MFIs’ average TecE had a decreasing trend from 38.2% to 35.3% from 2011 to 2012, and then recorded an increase to 40.1% (2013) and 45.3% (2014). Further, it decreased to 33.3% (2015) and recorded an increase in 2016 to 46.7%. However, the trend followed by a continuous decreasing trend for the next two consecutive years, 40.2% in 2017 and 39.1% in 2018, respectively.

Figure 1. Trend of social efficiency score in 2011–2018. Source: Microfinance Information Exchange (MIX), and authors’ own calculations.

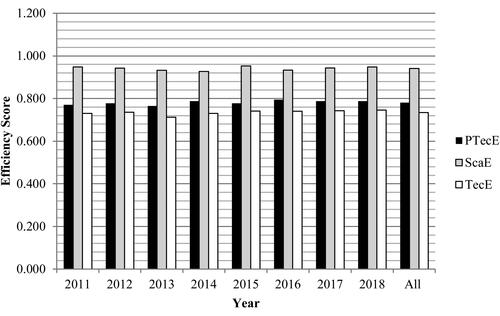

Figure 2. Trend of financial efficiency score in 2011–2018. Source: Microfinance Information Exchange (MIX), and authors’ own calculations.

Table 2. Descriptive statistics of MFIs social and financial efficiency.

Meanwhile, for the financial efficiency (FinE), the MFIs’ average TecE had almost consistent and slightly changed over the years from 2011 to 2018 since the level of the efficiencies are within the small range of changes 71%-75%. The trend shows only two years recorded as decreasing on changes in efficiency levels at 73.6% (2012) and 74% (2016). The maximum TecE score presented in 2018 (74.5%) and the lowest in 2013 (71.2%).

The results for all MFIs in all years confirmed that the pure managerial (PTecE) is the dominant factor in influencing MFIs’ efficiency. In general, the decomposition of TecE into its ScaE and PTecE components suggested that Pure Technical Inefficiency (PTecIE) dominates Scale Inefficiency (ScaIE) for over the years for both of MFIs’ SocE and FinE.

From 2011 to 2018, the results SocE suggested that MFIs exhibited an average TecE of 39.8%, with input waste of 60.2%. The decomposition of the TecE into its PTecE (49.6%) and ScaE (79.1%) components suggested that the inefficiency could be attributed mainly due to PTecIE (50.4%), rather than ScaIE (20.9%). Thus, the results indicate that MFIs could have produced the same amount of outputs by utilizing only 39.8% or reduced by 60.2% of inputs to maximize the outputs.

Furthermore, the FinE results suggested that MFIs exhibited an average TecE of 73.5%, with input waste of 26.5%. The decomposition PTecE (78.1%) and ScaE (94.1%) components suggested that the inefficiency could also be attributed mainly due to PTecIE (21.9%), rather than ScaIE (5.9%). Thus, the results imply that MFIs could have produced the same amount of outputs by using only 73.5% of the amount of inputs used. In other words, MFIs could save their inputs by 26.5% to produce the same amount of outputs.

Overall, the results revealed that the TecE for both SocE and FinE are contaminated by purely managerial efficiency (PTecE). This indicates, although the MFIs have been operating on a relatively optimal scale, they are facing the inefficiency from the managerial side. Therefore, the component of PTecE represents as the main factors in this analysis that need to focus more since the inefficiency of the overall efficiency (TecE), MFIs contributed from PTecIE

In addition, the results also show that the average of all years of PTecE for FinE (49.6%) is higher than SocE (78.1%) and this may indicate that the MFIs from these countries are more focusing on the sustainability of their services.

After examining the descriptive results derived from the DEA method, the issue of interest now is whether the difference in the PTecE, ScaE and TecE. The social and financial efficiency is statistically significant. This study is followed by performing a series of robustness checks, including parametric (t-test) and non-parametric (Mann-Whitney and Kruskall-Wallis) to obtain more robust results.

shows the results from parametric and non-parametric on the social and financial efficiency score on all countries over the years from 2011 to 2018. From 2011 to 2018 (Panels A to H), the specific countries results reported that only MFIs in Thailand show the average and average rank of social efficiency are higher than financial efficiency, but the differences are insignificant under both parametric and non-parametric test. Whereas, the countries, Philippines, Malaysia, Indonesia and Cambodia, show that the MFIs’ financial efficiency is greater than social efficiency and the most of the average and average rank score differences are significant from 5% to 1% level.

Table 3. Parametric and non-parametric robustness test for social and financial efficiency scores.

For the overall years and countries analysis in Panel I, the results from the parametric t-test shows that the average for the PTecE under the financial efficiency is higher than social efficiency (difference average value financial vs. social efficiency = 0.286) and significant at 1% level. Likewise, the financial efficiency has also exhibited a significantly higher average ScaE while comparing with social efficiency ScaE (average difference value financial vs. social efficiency = 0.149). The similar findings also reported for the TecE of financial efficiency is significantly higher rather than social efficiency (average difference value financial vs. social efficiency = 0.337). The results from the parametric t-test are further confirmed by the non-parametric Mann-Whitney and Kruskall-Wallis test.

In conclusion, the results in Panel I (all years) show that the MFIs from all countries over the years are more focused on financial efficiency to maximize the profit rather than reaching out the poorest of the poor citizens since the average and rank average of financial are higher than social efficiency under both parametric and non-parametric tests. This result is consistent with the studies that conducted by Hussain et al. (Citation2020), Zainal et al. (Citation2019, Citation2020), Widiarto and Emrouznejad (Citation2015) and Lebovics et al. (Citation2016). This result shows that MFIs are more concern on pursuing financial stability to ensure they can meet the social needs by granting more loans to the poor consumers with the profit of MFIs to enhance the social efficiency.

4.2. Determinants of efficiency level in MFIs

and present the Model 1 – baseline regression model, which includes MFIs specific determinant variables (lnROAA, lnAGE, lnTOA), Model 2 includes the macroeconomics (lnINF and lnGDP). Model 3 to 6 include all four economic freedom dimensions variables, which are property rights (lnPR) in Model 3, government integrity (lnGI) in Model 4, government spending (lnGS) in Model 5 and tax burden (lnTB) in Model 6. The estimated models enable this study to identify potential determinants and the impact of rule of law and government size under the dimensions of economic freedom on the social and financial efficiency of MFIs.

Table 4. Regression result on the social efficiency of microfinance institutions.

Table 5. Regression result on the financial efficiency of microfinance institutions.

In the preliminary stage, the results from and show that the panel data is most suitable to be used since the p-value of the Breusch and Pagan Lagrangian Multiplier (B and PLM) Chi-Square (X2) test are significant at 1% level in all models (Models 1 to 6) for both social and financial efficiency of MFIs in this study. Furthermore, all the justification on the preliminary results is based on the Fixed Effect Model (FEMod) regression analysis for all models since the Chi-Square (X2) of Hausman test are significant at 1%.

With regards to the impact of the probability (lnROAA), it can be observed from and that the coefficient exhibits a positive relationship with social and financial efficiency at a significant level of 1% levels in all models. This shows that the higher (lower) the profitability (lnROA) might lead to the higher (lower) the social and financial efficiency of MFIs. The MFIs could generate more profit and hence to improve financial efficiency by offering more products and services. The MFIs with low profitability in terms of return on assets might be less efficient due to lack of facilities provided to customers, inefficient in management and lack of advanced technologies in operation. This argument is supported by several studies (Iqbal et al., Citation2019; Mia & Soltane, Citation2016).

The findings suggest that the total number of operational years of MFIs (lnAGE) is significantly negative only to the social efficiency at 1% level (Model 5). This shows that the longer of MFIs operation may affect to the lower repayment loan by a poor borrower, it will lead to the short financial source to the MFIs, and it reduces the capability to outreach the other poor people. The MFIs will not really focus on the poor people since most of the MFIs transform their function more similar to conventional banks that offering more products and services that less focusing on the poor target. Meanwhile, the new MFIs might perform in better social efficiency, because they can learn the existing knowledge provided by the mature MFIs. The new MFIs might be more innovative to solve the problems, increase outreach to the poor and improve social efficiency (Bibi et al., Citation2018; Wagner & Winkler, Citation2013).

In , the findings report that the total asset (lnTOA) has a negative relationship with social efficiency of MFIs at the significant level of 1% (Model 5). also shows that this lnTOA has also significantly reported a negative to the financial efficiency in all models (except Models 1 and 5). This result implies that the larger (smaller) size MFIs tend to exhibit lower (higher) social and financial efficiency. The large MFIs do not utilize efficiently the benefits from large economies of scale, which enable them to generate increased revenues. They fail to utilize their high amount of resources available in maximizing both social and financial efficiency. Besides, large MFIs are unable to monitor well all their clients because the MFIs getting bigger. They have shifted their objectives towards commercialization instead of focusing on helping poor (Bibi et al., Citation2018; Efendic & Hadziahmetovic, Citation2017; Khan et al., Citation2017).

The impacts of inflation rate (lnINF) are significantly positive at 1% level for social efficiency in all models, and Model 4 is specifically for financial efficiency. The number of borrowers increases even though the interest rate is higher because they anticipate much higher inflation in future that will lead to much higher interest rates (Bibi et al., Citation2018; Kamarudin et al., Citation2016). Besides, the higher interest rate during inflation may impact borrower’s incentives to default. Thus, MFIs manage to reach more borrowers even in a high inflationary environment as they can achieve high-efficiency level by maximizing their outputs.

The empirical findings show the positive and significant at 1% level of economic growth (lnGDP) variable with social and financial efficiency of MFIs. When economic growth is high, MFIs will beneficial from the higher demand for their financial services and the probabilities of loan defaults tend to be lower during high economic growth. Profitability is low during recessions due to the increasing default rate and worst credit qualities. Thus, MFIs are encouraged to provide more lending during high economic growth. MFIs tend to maximize their outputs when the number of active borrowers increases as more lendings are given out. The findings support the study by Zamore (Citation2018).

4.3. Do rule of law and government size foster the MFIs efficiency?

The next part will discuss the findings of the impact of rule of law and government size under the dimension of economic freedom on the efficiency levels of MFIs. Based on the findings, and , the rule of law’s component (lnPR and lnGI) only effects to the MFIs’ financial efficiency, while the government size that consists of lnGS, and lnTB components only significantly effect to the social efficiency of MFIs. The empirical findings suggest that property rights (lnPR) have a positive relationship with financial efficiency of MFIs significantly at 1% level (, Model 3). The more effective legal protection of property under the country’s legal framework is higher than the financial efficiency of MFIs. According to Laissez-Faire Economic Theory, the economy will be strong if government protects the individual’s rights. The legal framework allows individual to acquire, hold and utilize their private property. The enforcement by government is important to secure the laws that protect the property rights of individuals. Legislation can reduce poverty by providing the security of property owns by the poor people (Meinzen-Dick et al., Citation2009). When the people can control on their properties, they manage to generate income or make investments and this will encourage the borrowers to have extra financial sources from MFIs to funding their activities. The demand for loans will be increased when more people need financial support. Therefore, MFIs have higher financial efficiency when the legal protection of the property is high. The findings are consistent with studies conducted by Akhter (Citation2018) and Chortareas et al. (Citation2016) since they have discovered government regulatory framework that can also affect the performance of MFIs as well.

With respect to the impact of government integrity (lnGI), the empirical findings are represented in (Model 4) that suggests that the coefficient of lnGI is positive and statistically significant at 1% level to the financial efficiency. The positive sign implies that high government integrity contributes towards higher financial efficiency. High government integrity means the practices of government that always free from corruption. The government will enforce well-structured policies and regulations to supervise on any private and public institutions. The development of MFIs depends on regulatory framework as a supportive factor (Boateng & Agyei, Citation2013). For example, all institutions include MFIs, and they will be monitored and disciplined to ensure free of corruption. Chortareas et al. (Citation2012) also found that regulatory and supervisory policies by government can contribute to higher efficiency. Thus, it can ensure that MFIs also operate in a high transparency and free from corruption. More people will trust the operation of MFIs and increase their borrowings from MFIs. As such, the financial efficiency of MFIs can be increased as they manage to reach more active borrowers and generate more revenue and profit. The findings are in line with studies of Akhter (Citation2018), Boateng and Agyei (Citation2013) and Aghion and Morduch (Citation2004) and define in general, the integrity of the government and the well regulatory framework could also significantly affect the financial efficiency of the MFIs.

Moreover, the coefficient of government spending (lnGS) shows a positive and significance at 5% level with social efficiency of MFIs in (Model 5). This implies that higher government spending leads to the higher social efficiency of MFIs. The spending of governments is not equally harmful to economic freedom but gives the benefits to the community by providing the infrastructure and public goods, funding research or improving human capital, which considered as the investment. Thus, the results show that the government has properly and efficiently spent to lead to efficient institutions. The study finding is similar to the study of Chortareas et al. (Citation2016), because efficient government spending will generate budget surplus and reducing of public debt. In this situation, people will spend more rather than save their money because of the affordable cost of living, and this will encourage the poor people to run the small business by borrowing more money from MFIs to simulate their living economics. As such, it increases the borrowers of MFIs, and thus, the social efficiency of MFIs will be reduced.

Finally, the findings show that the impact of tax burden (lnTB) is significantly positive at 5% level on the social efficiency of MFIs in (Model 6). The positive relationship indicates that higher tax burden tends to improve the social efficiency of MFIs. When the high corporate tax charged by the government to MFIs, it will lead to a higher interest rate charged on loans that need to be paid by the borrowers. Although the high interest rate may reduce the number of borrowers, this will contribute to the high government revenue collection since the MFIs need to high tax from their business activities. In fact, the government may use this collection to provide more financial allocation, such as offering the grant or subsidies to the MFIs in order to improve their operation by providing more loan and service to outreach. In this way, all the poor people use the benefits and they can also increase the MFIs social efficiency. The higher the marginal tax rate on the individual income will contribute to the higher the percentage of GDP of the countries. Therefore, when the percentage of GDP increases, the government size will be increased and the efficiency of MFIs in terms of social outreach will also be improved. Thus, the value of the Total Entrepreneurial Activity (TEA) Index will be increased, and more poor people may start their small business and get loans from MFIs, this finding is in the line of the study of Carlos Díaz-Casero et al. (Citation2012).

5. Conclusion

The main purpose of this study is to investigate the impact of rule of law and government size based on the economic freedom components on the social and financial efficiency of MFIs. Moreover, this study also examines the effect of MFIs specific characteristics and macroeconomic determinants on the efficiency of MFIs. This study examines a total 167 MFIs in Thailand, Philippines, Malaysia, Indonesia and Cambodia from 2011 to 2018. Overall, the finding of first stage analysis reveals that the level of financial efficiency is significantly higher than the social efficiency of MFIs in the all the selected countries, and this indicates that the MFIs are focusing more on generating revenue and profit from their financial activities so that they can maintain their operations.

The results of second stage analysis, the panel regression analysis, show that for the MFIs specifics determinants, the profitability (lnROAA) positively influences the social and financial efficiency of MFIs. The size (lnTOA) affects the MFIs significantly, and it is negative to both social and financial efficiency. However, the total number of MFIs’ operational years (lnAGE) presented is negative, and it is significant only to the MFIs’ financial efficiency. For macroeconomic variables, the inflation rate (lnINF) and economic growth (lnGDP) exhibit a significant positive relationship with social and financial efficiency of MFIs.

With regards to the impact of the rule of law on MFIs efficiency, this study has reported the property rights (lnPR) and government integrity (lnGI), and it positively influences only to the financial efficiency. Meanwhile, for the government size factor, the results indicate that the government spending (lnGS) and tax burden (lnTB) are significantly negative to the financial efficiency.

The findings can provide useful information and several implications for different parties. Firstly, the results could be useful to government regulators and policymakers. For government, the information provides suggestion on how its role can help in improving the efficiency level of MFIs. The government can implement some useful initiatives to help MFIs in the country to sustain in the long term. Moreover, policymakers can identify the relevant inputs that may influence the efficiency level of MFIs. Thus, it paves ways to revise the policy based on it. The policymakers also can design new policies and regulations based on different economic freedom variables, which could enhance the efficiency level of MFIs.

In addition, government and the policymakers could secure the property of owners under the property right and the poor people can alleviate poverty. This protection can contribute to higher openness level, which would lead to higher efficiency levels of MFIs since it will increase the numbers of capable borrowers. Besides, the government must ensure to practice the high integrity that always free from any unethical behaviour such as corruption. The government will enforce well-structured policies and regulations to supervise any private and public institutions. The development of MFIs depends on regulatory framework as supportive factor. The government also needs to spend more on the infrastructure and public goods, funding research and grant to the MFIs or improving human capital, which is considered as the investment to improve social efficiency. Lastly, the higher tax should be practiced by the government since it will improve the social efficiency of the MFIs. While imposing high tax burden on the income of both an individual and business, the countries’ GDP will be increased, and this will provide more capabilities to the government to provide more funding or grant to the MFIs to improve their operation.

Meanwhile, the management teams of MFIs can use this information to improve their efficiency level and create a more sustainable and competitive environment in the future. Moreover, it provides a direction for MFIs on the factors that should be looked for to increase their overall efficiency levels in future planning. The MFIs may also consult the government to provide the property right for the borrower to ensure the protection of poor peoples’ property. The borrower will feel more safety and confidence to make more loans, and this will enhance the financial efficiency of the MFIs. Furthermore, MFIs should be monitored and disciplined to ensure the free of corruption because regulatory and supervisory policies by government can contribute to higher efficiency due to the high transparency environment. This will attract more new borrower since more people will have a trust on MFIs operation. The MFIs also need to utilize the obtained grant or subsidize efficiently for spending to improve the social efficiency by outreach more poor people.

Besides, the information of this study could guide investors in decision making on their investments. It can help the investors to generate higher profits from their investments. The investors can determine which MFIs is safe to invest based on their efficiency level. This can ensure investors to make a wise decision for higher expected return in the future.

Finally, the studies on the efficiency level of MFIs are limited. Hence, the empirical results of this study are valuable to academicians or researchers by helping them to fill up scholarly gaps. Academicians or researches can use the information as a guide to continue to explore and obtain new findings in further study. Moreover, the impact of economic freedom on the efficiency level of MFIs also contributes to new dimensions in the literature.

Acknowledgements

We would like to give thanks to the editors and the anonymous referees of the journal for constructive comments and suggestions, which have significantly helped to improve the contents of the paper. Furthermore, special thanks to (1) Universiti Putra Malaysia Grant Putra Vot No 9632100 sponsored by Universiti Putra Malaysia; (2) Fundamental Research Grant Scheme (FRGS) Vot No FRGS/1/2015/SS01/UPM/02/1 5524716 sponsored by Malaysian Ministry of Higher Education; (3) Universiti Putra Malaysia Grant IPM Vot No 9473700 sponsored by Universiti Putra Malaysia; and (4) Universiti Putra Malaysia Grant IPS Vot No. 9651500 sponsored by Universiti Putra Malaysia as an organizations that funded our research. The usual caveats apply.

References

- Afonso, A., & Jalles, J. T. (2011). Economic performance and government size. European Central Bank Working Paper Series, No. 1399.

- Aghion, B. A. D., & Morduch, J. (2004). Microfinance: Where do we stand? In Goodhart C.A.E. (Eds.), Financial development and economic growth. British association for the advancement of science. Palgrave Macmillan.

- Akhter, P. (2018). A study on the factors affecting the performance of microfinance institutions in Bangladesh. Pacific Business Review International, 10(11), 124–132.

- Alaeddin, O., Altounjy, R., Zainudin, Z., & Kamarudin, F. (2018). From physical to digital: investigating consumer behaviour of switching to mobile wallet. Polish Journal of Management Studies, 17(2), 18–30. https://doi.org/https://doi.org/10.17512/pjms.2018.17.2.02

- Androniceanu, A., Gherghina, R., & Ciobănaşu, M. (2019). The interdependence between fiscal public policies and tax evasion. Administratie si Management Public, 32, 32–41.

- Ayayi, A. G., & Sene, M. (2010). What drives microfinance institution’s financial sustainability. The Journal of Developing Areas, 44(1), 303–324. https://doi.org/https://doi.org/10.1353/jda.0.0093

- Banker, R. D., Charnes, A., & Cooper, W. W. (1984). Some models for estimating technical and scale inefficiencies in data envelopment analysis. Management Science, 30, 1078–1092. https://doi.org/https://doi.org/10.1287/mnsc.30.9.1078

- Bassem, B. S. (2008). Efficiency of microfinance institutions in the Mediterranean: An application of DEA. Transition Studies Review, 15(2), 343–354. https://doi.org/https://doi.org/10.1007/s11300-008-0012-7

- Berger, A. N., & Humphrey, D. B. (1997). Efficiency of financial institutions: International survey and directions for future research. European Journal of Operational Research, 98(2), 175–212. https://doi.org/https://doi.org/10.1016/S0377-2217(96)00342-6

- Bibi, U., Balli, H. O., Matthews, C. D., & Tripe, D. W. (2018). New approaches to measure the social performance of microfinance institutions (MFIs). International Review of Economics & Finance, 53, 88–97.

- Bilan, Y., Mishchuk, H., Roshchyk, I., & Kmecova, I. (2020). An analysis of intellecutal potential and its impact on the social and economic development of European countries. Journal of Competitiveness, 12(1), 22–38. https://doi.org/https://doi.org/10.7441/joc.2020.01.02

- Boateng, I. A., & Agyei, A. (2013). Microfinance in Ghana: Development, success factors and challenges. International Journal of Academic Research in Accounting, Finance and Management Sciences, 3(4), 153–160.

- Carlos Díaz-Casero, J., Ángel Manuel Díaz-Aunión, D., Cruz Sanchez-Escobedo, M., Coduras, A., & Hernández-Mogollón, R. (2012). Economic freedom and entrepreneurial activity. Management Decision, 50(9), 1686–1711.

- Charnes, A., Cooper, W. W., & Rhodes, E. (1978). Measuring the efficiency of decision-making units. European Journal of Operational Research, 2(6), 429–444. https://doi.org/https://doi.org/10.1016/0377-2217(78)90138-8

- Chortareas, G. E., Girardone, C., & Ventouri, A. (2012). Bank supervision, regulation, and efficiency: Evidence from the European Union. Journal of Financial Stability, 8(4), 292–302. https://doi.org/https://doi.org/10.1016/j.jfs.2011.12.001

- Chortareas, G., Kapetanios, G., & Ventouri, A. (2016). Credit market freedom and cost efficiency in US state banking. Journal of Empirical Finance, 37, 173–185. https://doi.org/https://doi.org/10.1016/j.jempfin.2016.03.002

- Cull, R., Demirguc-Kunt, A., & Morduch, J. (2011). Does regulatory supervision curtail microfinance profitability and outreach? World Development, 39(6), 949–965. https://doi.org/https://doi.org/10.1016/j.worlddev.2009.10.016

- Duve, M., Mandizvidza, R., Chibaya, T., & Nyakuwanika, M. (2017). Tax regulation and sustainability of microfinance institutions in Masvingo Urban, Zimbabwe. IRA-International Journal of Management & Social Sciences, 6(3), 429–439. https://doi.org/https://doi.org/10.21013/jmss.v6.n3.p9

- Efendic, V., & Hadziahmetovic, N. (2017). The social and financial efficiency of microfinance institutions: the case of Bosnia and Herzegovina. South East European Journal of Economics and Business, 12(2), 85–101. https://doi.org/https://doi.org/10.1515/jeb-2017-0018

- Ginevicius, R. (2019). Quantitative assessment of the compatibility of the development of socioeconomic systems. Journal of Competitiveness, 11(2), 36–50. https://doi.org/https://doi.org/10.7441/joc.2019.02.03

- Gujarati, D. (2002). Basic econometric (6th ed.). McGraw Hill.

- Hussain, H. I., Kamarudin, F., Thaker, H. M. T., & Salem, M. A. (2019). Artificial neural network to model managerial timing decision: Non-linear evidence of deviation from target leverage. International Journal of Computational Intelligence Systems, 12(2), 1282–1294.

- Hussain, H. I., Kot, S., Kamarudin, F., & Mun, W. C. (2020). The Nexus of competition freedom and the efficiency of microfinance institutions. Journal of Competitiveness, 12(2), 67–89. https://doi.org/https://doi.org/10.7441/joc.2020.02.05

- Iqbal, S., Nawaz, A., & Ehsan, S. (2019). Financial performance and corporate governance in microfinance: Evidence from Asia. Journal of Asian Economics, 60, 1–13. https://doi.org/https://doi.org/10.1016/j.asieco.2018.10.002

- Kamarudin, F., Sufian, F., & Nassir, A. M. (2016). Global financial crisis, ownership and bank profit efficiency in the Bangladesh’s state owned and private commercial banks. Contaduría y Administración, 61(4), 705–745. https://doi.org/https://doi.org/10.1016/j.cya.2016.07.006

- Kamarudin, F., Zack, H. C., Sufian, F., & Anwar, N. A. M. (2017). Does productivity of Islamic banks endure progress or regress? Empirical evidence using data envelopment analysis based Malmquist productivity index. Humanomics, 33(1), 84–118. https://doi.org/https://doi.org/10.1108/H-08-2016-0059

- Khan, W., Shaorong, S., & Ullah, I. (2017). Doing business with the poor: The rules and impact of the microfinance institutions. Economic Research-Ekonomska Istraživanja, 30(1), 951–963. https://doi.org/https://doi.org/10.1080/1331677X.2017.1314790

- Kovacova, M., Kliestik, T., Valaskova, K., Durana, P., & Juhaszova, Z. (2019). Systematic review of variables applied in bankruptcy prediction models of Visegrad group countries. Oeconomia Copernicana, 10(4), 743–772. https://doi.org/https://doi.org/10.24136/oc.2019.034

- Lebovics, M., Hermes, N., & Hudon, M. (2016). Are financial and social efficiency mutually exclusive? A case study of Vietnamese microfinance institutions. Annals of Public and Cooperative Economics, 87(1), 55–77. https://doi.org/https://doi.org/10.1111/apce.12085

- Majumdar, S. K., & Marcus, A. A. (2001). Rules versus discretion: The productivity consequences of flexible regulation. Academy of Management Journal, 44(1), 170–179.

- Meinzen-Dick, R., Kameri-Mbote, P., & Markelova, H. (2009). Property rights for poverty reduction? New York, NY.

- Mia, M. A., & Soltane, B. I. B. (2016). Productivity and its determinants in microfinance institutions (Mfis): Evidence from South Asian countries. Economic Analysis and Policy, 51, 32–45. https://doi.org/https://doi.org/10.1016/j.eap.2016.05.003

- Qayyum, A., & Ahmed, M. (2006). Efficiency and sustainability of micro finance institutions in South Asia.

- Rauf, S. A., & Mahmood, T. (2009). Growth and performance of microfinance in Pakistan. Pakistan Economic and Social Review, 47, 99–122.

- Shu, C. A., & Oney, B. (2014). Outreach and performance analysis of microfinance institutions in Cameroon. Economic Research-Ekonomska Istraživanja, 27(1), 107–119. https://doi.org/https://doi.org/10.1080/1331677X.2014.947108

- Ślusarczyk, B. (2018). Tax incentives as a main factor to attract foreign direct investments in Poland. Administratie SI Management Public, 30, 67–81. https://doi.org/https://doi.org/10.24818/amp/2018.30-05

- Sufian, F., & Kamarudin, F. (2014). The impact of ownership structure on bank productivity and efficiency: Evidence from semi-parametric Malmquist productivity index. Cogent Economics and Finance, 2(1), 1–27. https://doi.org/https://doi.org/10.1080/23322039.2014.932700

- Sufian, F., & Shah Habibullah, M. (2014). Economic freedom and bank efficiency: Does ownership and origins matter? Journal of Financial Regulation and Compliance, 22(3), 174–207. https://doi.org/https://doi.org/10.1108/JFRC-01-2013-0001

- Tahir, I. M., & Tahrim, S. N. C. (2013). Efficiency analysis of microfinance institutions in ASEAN: A DEA approach. Business Management Dynamics, 3(4), 13.

- Wagner, C., & Winkler, A. (2013). The vulnerability of microfinance to financial turmoil - evidence from the global financial crisis. World Development, 51, 71–90. https://doi.org/https://doi.org/10.1016/j.worlddev.2013.05.008

- White, H. (1980). A heteroskedasticity-consistent covariance matrix estimator and a direct test for heteroskedasticity. Econometrica, 48(4), 817–838. https://doi.org/https://doi.org/10.2307/1912934

- Widiarto, I., & Emrouznejad, A. (2015). Social and financial efficiency of Islamic microfinance institutions: A data envelopment analysis application. Socio-Economic Planning Sciences, 50, 1–17. https://doi.org/https://doi.org/10.1016/j.seps.2014.12.001

- Zainal, N., Nassir, A. M., Kamarudin, F., & Law, S. H. (2020). Does bank regulation and supervision impedes the efficiency of microfinance institutions to eradicate poverty? Evidence from ASEAN-5 countries. Studies in Economics and Finance. Forthcoming. https://doi.org/https://doi.org/10.1108/SEF-10-2019-0414

- Zainal, N., Nassir, A. M., Kamarudin, F., Siong Hook, L. S., Sufian, F., & Hussain, H. I. (2019). Social role of microfinance institutions in poverty eradication: Evidence from ASEAN-5 countries. International Journal of Innovation, Creativity and Change, 5(2), 1551–1576.

- Zamore, S. (2018). Should microfinance institutions diversify or focus? A global analysis. Research in International Business and Finance, 46, 105–119. https://doi.org/https://doi.org/10.1016/j.ribaf.2017.12.001