?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study aims to improve the existing problems of intellectual capital (IC) measurement methods including those with unclear and unspecific calculation details and the inability to valuate the influences between IC measures and between IC components, which is a fundamental characteristic of IC. To address the fundamental issues of past methods, this study integrates two multi-criteria decision-making (MCDM) methods: the analytic network process (ANP) and the simple additive weighting (SAW) method, both of which provide specific and clear calculation procedures. ANP is adopted to manage the valuation of influences between IC elements, while SAW is used to solve incommensurable units of IC performance indicators and different concentrations on IC measures and components. Implementation of the method revealed a clear and systematic measurement procedure. The proposed method could consider the relationships among IC measures as well as among IC components and presented calculated results in the form of the weights of IC measurement compositions. Furthermore, the method maintained the crucial characteristics of IC measurement: the ability to standardise units of measure and the capability to valuate the performance of IC for the appropriate measure, component, and holism level.

1. Introduction

Performance measurement has been acknowledged to be one of the most critical processes in the management field. In the past, the measurement of a firm’s performance was concentrated on financial capital that only represented lagging performances. This process brings delayed responses as well as solutions to organisations and, critically, leads to a lack of sustainable development (Gross-Gołacka et al., Citation2020). Therefore, it is widely acknowledged that the measurement of traditional or financial performance is inadequate in the present competitive market. Regarding the above-mentioned flaw, the concentration on performance measurement has been broadly extended to intellectual capital (IC) since the valuation of IC can beneficially introduce leading signals of performance at an early time (Kianto et al., Citation2020). Therefore, firms can adapt or improve themselves when they cannot achieve their goals and objectives.

Basically, most IC measurement methods are created from different interpretations of management perspectives. However, generally, IC is categorised into three major dimensions. Nevertheless, some methods categorise IC either less than or higher than three components. The classifications of IC are applied as fundamental for developing IC measurement methods. Although there are several classifications of IC concepts as previously mentioned, methods of IC measurement are generally classified into two major categories: monetary valuation and non-monetary valuation. Each group of methods offers different advantages. The non-financial classification models provide multidimensional consideration of IC details, while the financial valuation methods are known for standard measurements and ease of verification. Despite key claims of distinctive benefits for each type of measurement method, most measurement models are still unable to properly deal with the basic characteristics of IC measurement: comparability of performance between firms, identification of weights of IC elements and their performance measures, and consideration of the influences between IC components.

From various IC performance measurement methods, there is one similar approach from four non-monetary valuation methods: the IC-Index, value creation index (VCI), holistic approach value, and inclusive valuation methodology (IVM), which could better cope with the fundamental characteristics and the issues related to IC measurement than other performance valuation methods. The distinction of these indices derives from their advanced improvement on several critical deficiencies of IC measurement methods. These developments make these non-financial valuation approaches differ from and better than other measurement concepts in several dimensions. Although these improved methods could resolve several fundamental issues of IC measurement, they still have two remaining weaknesses. The first and the most problematic deficiency is an unclear computation reference (Deventer & Johanna, Citation2002), which could potentially lead to improper measurements and the inability to be compared as well as unreasonable results. Another major problem is the neglect of the computation of influences between intangible assets (Dinçer et al., Citation2017). From these issues, the formerly improved methods are still unable to provide a proper measurement system, and also to deliver reliable as well as comparable performance values (Lu et al., Citation2018). Hence, from the existing problems of past works, a good measurement and interpretation of organisational performance still depends on the experience and competence of executives. Therefore, applying existing measurement methods but lacking professional competence as well as enough management experience possibly leads to incorrect decisions and the mismanagement of organisations.

Even though the formerly improved measurement approaches have several essential advantages over other traditional measurement methods, their existing weaknesses deliver calculated results that still could not properly present a reliable, and comparable performance. This untrustworthy information directly affects the decision-making of executives, especially for inexperienced managers. Therefore, regarding the aforementioned problems, this research aims to propose an improved IC measurement approach by mainly addressing the existing deficiencies of current methods. To improve the existing gaps, proper multiple criteria decision-making methods are elaborately selected and integrated into the core valuable concept of currently improved methods. Since the selected MCDM methods provide a systematic process and a clear calculation reference, this improvement can support inexperienced executives to follow identified processes and deal with the issues of relational consideration and management of incommensurable units, which are found in other existing methods. Finally, to validate the usability of the proposed method, a case study of higher education is conducted. To provide all the necessary information about this study, this article is further presented in five major sections. The next section reviews and highlights gaps in the current IC measurement methods. With regard to the improvement opportunity stated in Section 2, Section 3 proposes a novel framework and computation details of the developed method. Thereafter, to exemplify the proposed evaluation, Section 4 presents an application of the method with a real case study. Finally, the discussion of the findings and the conclusion of the study are presented in Sections 5 and 6, respectively.

2. Literature review

2.1. IC measurement methods

Several IC measurement methods were proposed over several past decades. A content analysis of various theoretical, review, and empirical studies (e.g., Bontis, Citation2001; Nazari, Citation2015; Nimtrakoon, Citation2015; Ramanauskaitė & Rudžionienė, Citation2013; Sveiby, Citation2010) was carried out. The generalised data of widely applied and well-known methods and also their important findings related to the measurement are shown in .

Table 1. Classifications and scopes of IC measurement methods.

Three essential parts of measurement of methods are presented in including a scope of measurement, a level of guidance as well as reference, and method capability; and each method provides dissimilar scope. Nevertheless, most methods in the same category provide several common characteristics. For example, EVA™ and MVA could evaluate performance in the holistic level and provide clear calculation reference as well as three similar measurement capabilities (DEP, STA, and WEI). Only significant findings and gaps of measurement methods are discussed in the next paragraphs.

Generally, IC performance measurement methods can be classified into two categories: monetary and non-monetary valuation methods. The monetary valuation method is a measurement approach that converts the values of a firm’s intangible assets into a monetary term. Most methods under this category are based on the fundamental platform of the traditional accounting concept. Therefore, similar to the basis feature of the accounting principle, monetary valuation methods have a distinctive strength conforming to a measurement concept with high comparability of the computed results among organisations. Nevertheless, most methods in this group can provide a holistic performance of IC as shown in . Although the holistic result is able to present the overall IC performance and improvement opportunities for organisations, it is still unable to provide details and information about IC components. Therefore, companies manage and improve IC without clear direction.

However, regarding , three financial methods (VAIC™, technology broker, and KPMG value explorer™) were found to provide values of IC elements concurrently with aggregated or overall performance. Although these concepts can better deliver the firm’s intangible values, the monetary valuation method still has several weaknesses. As shown in , the weakness of the financial methods, except for the VAIC, is a standard and a systematic conversion from qualitative results to monetary values; additionally, details of the calculation are not clearly presented (Bontis, Citation2001). While the VAIC has clear and well-defined calculation details and processes, it is still critically critiqued for misuse of the fundamental IC concept by including in the calculations some financial values that are not parts of the IC. The financial methods are not only critiqued for the aforementioned issues, but they also have other crucial flaws that neglect the consideration of some fundamental characteristics of IC that influence IC elements as well as differences in the importance of IC components. Based on several crucial issues, the monetary valuation method seems to be less desirable and proper for measuring IC performance. Therefore, another type of method, the non-monetary valuation, is proposed to address the flaws found in the financial technique.

The non-monetary valuation method does not valuate IC into a monetary value. Similar to the monetary valuation concept, the non-monetary valuation method has measurement approaches that one could consider specific components, more than one element, or the holistic performance of IC. Nevertheless, most of the non-financial methods can better manage information than the financial concept. As depicted in , all methods in this category excluding the citation-weighted patents and human capital intelligence could measure more than one IC component. Moreover, there are four distinctive methods: the IC-Index, value creation index, holistic approach value, and IVM, which could handle both the component and the holistic level. These four methods are designed from the same basic concepts that can address both critical issues found in the monetary valuation methods and some basic characteristics of IC measurement. Regarding their advantages over financial valuation methods, these four non-financial methods have explicit approaches that could similarly measure both the qualitative and quantitative performance of all IC elements. Moreover, in contrast to other non-monetary methods, these methods could also solve the incommensurable unit, which is a fundamental issue of IC measurement. Then, beyond the monetary valuation method, these unitless values could be assigned weights to represent differences in importance or impacts of IC components, and furthermore, weighted results could be combined into a single index reflecting the holistic performance of the organisation. Although most issues of IC measurement are addressed by the aforementioned non-monetary valuation method, two previously reported issues persist and remain unsolved.

The first problem is that the past methods do not provide a clear and specific procedure to normalise or standardise performance values, or to quantify weights of IC elements and their related performance indicators. Therefore, due to this unclear issue, applications of methods published in the academic literature are very limited. There is an identification highlighting the lack of academic articles applying the IC-index after its first publication (Deventer & Johanna, Citation2002) due to the unclear reference of the procedure and method.

Another crucial issue found in the available IC measurement methods is a neglect of consideration as well as a valuation of the dependence of IC components and their performance measures. This omission violates a basic characteristic of IC, which is an interrelationship between IC components. This issue is distinctive and also ignored in financial methods, while some non-monetary methods attempt to solve this problem by including a consideration of dependence into the methods (e.g., BSC and IVM). Nevertheless, these proposed approaches still do not include the relationship of IC elements in the measurement and the valuation of performance.

From the aforementioned issues, there is an important opportunity for an improved measurement method that could both provide a clear and systematic procedure to valuate IC performance and also solve issues associated with traditional IC measurement methods and their improved forms. To address these problems, some improvement approaches found in other domains can be used, and the related studies will be reviewed in the next section.

2.2. Improvement of strategic measurement methods using multi-criteria decision making (MCDM)

Regarding the limited resources of an organisation, identifying weights of indicators is one key focus of the performance measurement concept. The ability to perceive importance and priority of measures could support firms to efficiently manage resources and plans that significantly affect the competitive capabilities, ultimate goals, and sustainability of companies. Therefore, with the current high competition, it is obvious that a concentration on weights and priorities assignment is crucial for organisations.

In comparison to IC classified as a method for strategic management, other measurement methods for the top management level generally do not provide weights and priorities of performance indicators. This gap of methods is widely criticised and subsequently improved by several studies. One method that is applied often and properly handled with both the weighting issue and characteristics of measurement methods is the MCDM method. Based on an intensive literature review, there is no consensus or obvious identification concerning the selection and adoption of MCDM methods for improving these performance measurement issues. The MCDM methods are selected and used in accordance with the characteristics of related problems or the direct intentions of authors.

Although, fundamentally, MCDM methods can be used for prioritizing attributes or determining weights of performance measures, these methods still have different advantages and disadvantages. Each method can improve one or more specific issues of the performance measurement concept. Therefore, from various MCDM methods, very limited models can simultaneously handle several problems of either the IC or non-IC performance measurement concept. Therefore, to solve the complex or integrated issues, an approach that is widely applied is the integration of two or more MCDM methods. To the best of the author’s knowledge and available literature, studies specifically related to the improvement of performance measurements by integrating MCDM methods can be determined and are presented in .

Table 2. Improvement of measurement methods by integrating more than one MCDM method.

From , it is apparent that most of the improved approaches integrated two MCDM methods together. There have been fewer attempts applying either less than or more than two methods because fewer methods are used and less flaws are solved. If more methods are integrated, more time and resources are consumed, and more errors related to decisions and fatigue of participants can occur. also highlights that studies specifically improving performance measurement methods are mostly executed in the scope of non-IC (eight articles) than IC (five articles). Interestingly, more than half of the improvements in the IC measurement method have been published in the last 5 years. This concentration on IC measurements within the recent time periods conforms to the latest findings in the literature (Wudhikarn et al., Citation2018).

Furthermore, five studies on IC developments, surprisingly make the improved method capable of valuating IC performance at the holistic level only. The flaw in incommensurability between both IC components and performance measures remains unsolved. In addition to not only improvements in the IC but also the non-IC scope, all improved approaches could solve several flaws of performance measurement methods, but they still only either provide the holistic performance of performers or prioritise the best player in decision problems. The issue about the comparability of either criteria or groups of criteria persist. However, from the various proposed methods, there is one approach, the integration of AHP and SAW, which could mostly cope with unsolved problems of traditional IC measurement methods. In this approach, AHP is applied to identify the weights of IC measures, and the obtained results were subsequently used with the SAW method. Distinctively, SAW can deal with incommensurable units of measures, and moreover, the calculated results can be aggregated to assess the IC component performance and holistic performance, respectively.

Even though the integration of AHP in the proposed approach could provide an ability to assign weights to relative indicators, the AHP was still unable to handle the consideration of relationships between attributes or performance measures that are a basic characteristic of IC. Therefore, this pitfall causes a valuation of performance that is unsound, especially for the IC measurement. Therefore, to solve the relational issue, some other approaches integrate ANP with measurement concepts. Regarding the advantages of ANP, this MCDM method can cope with the relationships of IC and the comprehensive consideration of both qualitative and quantitative data (Saaty, Citation2004). Nevertheless, similar to other previously improved approaches as mentioned previously, the adoption of ANP with other MCDM methods still could not provide comparable performance for both the indicator and group for the measure level. Therefore, considering the specific advantages of ANP as well as SAW, and the improvement opportunities highlighted previously, there is a new improvement opportunity by integrating these two distinctive MCDM methods with the mature non-monetary valuation concept to solve existing flaws of IC performance measurement. The computation and evaluation procedures of this proposed method are presented in the following section.

3. The proposed IC measurement model

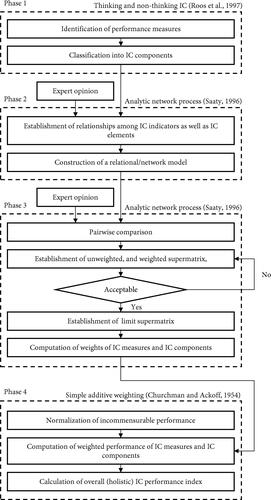

In light of improvement opportunities and advantages of related methods highlighted in the previous section, this study aims to propose a new hybrid approach, which combines two major different concepts: the IC measurement and MCDM methods. The hybrid model integrates different methods to address various and distinct issues of existing traditional methods, since one method could not overcome all the crucial problems of past IC measurement. In this study, the IC measurement concept adopted as a core procedure for the proposed measurement method comes from the major similar frameworks of the IC-Index, VCI, holistic approach value, and IVM, while the two MCDM methods are used to solve different weaknesses of IC measurement methods. ANP is employed to valuate important weights of performance measures by addressing the problem of relationships among IC components and their measurement indicators. Finally, SAW is combined to solve the issue of incommensurable units of indicators and to valuate IC performance at the IC indicator level, and also at the holistic level. The following subsections present the processes underlying the newly integrated IC measurement model, and the overall procedure can be concluded and is shown in .

Figure 1. The procedure for the proposed IC performance measurement model. Source: The Authors.

3.1. Phase 1: Identification of performance measures and classification into IC components

In the first step, IC performance indicators are established regarding visions, goals, missions, strategies, or objectives of organisations. Thus, the obtained measures are classified into four major IC components, including human capital (HC), relationships capital (RC), organisation capital (OC), and renewal and development capital (RDC) mainly following classifications of IC regarding the thinking and non-thinking IC concept (Roos et al., Citation1997). The wide ranges of IC categories regarding this method could support organisations to consider comprehensive managerial and operational activities. This broad range of attention on IC is crucial for the current competitive market (Wu & Chou, Citation2007).

3.2. Phase 2: Establishment of relationships among IC indicators as well as IC elements

The consideration and valuation of relationships between IC compositions is one of the required abilities for the proposed method. Therefore, to handle this requirement, a relational model must first be constructed. Both intra and inter-relationships between IC performance measures and between IC components must be identified by an expert or experienced management. The indicated relationships are then applied to create and visualised through a network model or matrix, which is further used for valuating weights by ANP.

3.3. Phase 3: Application of the ANP method for computing weights of IC indicators and IC components

In this section, only major procedures and necessary information for ANP are provided. In-depth details and computations can be further studied from a book of the original author (Saaty, Citation1996). The major steps of ANP can be described as follows:

3.3.1. Pairwise comparisons

In this step, related performance measures and IC components identified in the former step are compared in a pairwise manner according to the 1-to-9 discrete scales of comparisons (Saaty, Citation1996).

3.3.2 Establishment of weights of IC measures and IC elements

The matrix is computed to a principal eigenvector and priority vector, respectively, for both the IC measure level (called the node level by the ANP concept) and the IC component level (cluster level). The results from pairwise comparisons are used for constructing a supermatrix.

In the ANP procedure, to examine the reliability of the obtained answers, all pairwise comparison results are checked for consistency by the consistency ratio (CR). Whenever the CR is higher than 0.10, the comparisons must be re-evaluated until the ratio is lower than this level. From the reliable results, calculated priority vectors are assembled to the unweighted supermatrix and cluster weight matrix. The weighted supermatrix is constructed by multiplying each segment of the unweighted supermatrix by the corresponding weight from the cluster weight matrix. Finally, the supermatrix limit is computed by raising the powers of the weighted supermatrix until all values in each column are similar. The obtained values from the columns represent the weights of corresponding performance measures, while the weight of the IC component can be calculated by aggregating all weights of related measures in this group. These weights are calculated by considering the basic characteristics of IC and relationships among IC, and they are further used with the SAW method to evaluate IC performance in the next step.

3.4. Phase 4: Application of the SAW method for valuating IC performance

To capably valuate IC performance at the measure, component, and holistic level, the SAW method is integrated in the proposed approach. Following the procedure used for this MCDM method, to first allow a comparable scale, the incommensurable performance is addressed by the normalisation process. A benefit attribute and cost attribute can be normalised using EquationEquations (1)(1)

(1) and Equation(2)

(2)

(2) , respectively.

(1)

(1)

(2)

(2)

where

= 1, 2, 3, …,

= 1, 2, 3, …,

is the normalised performance rating of organisation

with respect to measure

This standardisation process transforms all performance ratings to a similar rating scale that is a proportion value (0 ≤

≤ 1). Using normalised values, the performance of each IC component and overall can be calculated using EquationEquations (3)

(3)

(3) and Equation(4)

(4)

(4) , respectively.

(3)

(3)

(4)

(4)

where

is a synthesizing performance rating of IC component

of the organisation

is a holistic IC performance of the organisation

is a weight of performance measure

is a normalised value of organisation

with respect to measure

under IC component

where

= 1, 2, 3, …,

denotes the set of IC component; and

is the performance measure under IC component

Regarding the and

results, the greater the synthesizing values, the higher is the IC performance. Several past findings for SAW have highlighted the distinctive advantages in which the linear function of trade-offs by SAW could deliver close estimations to complex nonlinear functions while providing improved simplicity of the application and calculation (Hwang & Yoon, Citation1981).

4. A case study of higher education

To exemplify the applicability, the proposed method was implemented in an empirical case with engineering and information technology-related faculty or college from the following four high-ranked universities in Thailand; Mahidol University (MU), Chiang Mai University (CMU), Kasetsart University (KU) and Chulalongkorn University (CU). The study was carried out using partial performance data for the fiscal and academic year 2016 provided by the Commission on the Higher Education Quality Assessment (CHEQA) online system, quality assurance reports and yearly reports of organisations. The details of the applications are demonstrated as follows.

4.1. Phase 1: Identification of performance measures and classification into IC components

In this study, performance indicators and measured results of academic institutions were applied to the proposed method. Regarding the IC classifications stated in the previous section, eight performance measures were classified in the related category, as concluded in .

Table 3. Performance indicators of a case study.

4.2. Phase 2: Establishment of relationships among IC indicators and IC elements

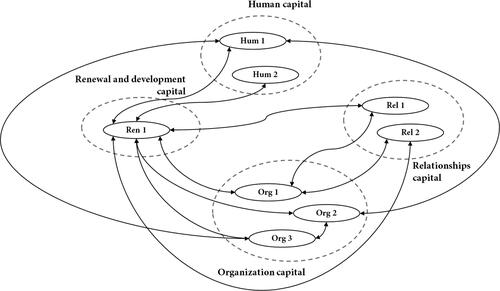

Regarding the ANP procedure, the performance measures depicted in are identified for relationships by an experienced expert at high-level management (vice dean of administrative affairs) of an academic institution. The identified relationships for both the cluster and node level obtained from the answered questionnaire were included as a network model, as shown in .

Figure 2. A relational model of the case study. Source: The Authors.

The network model demonstrates the influences of relationships between performance measures and also between IC components. A plain line ending with an arrowhead represents the starting node influences on the ending node, while the line with a two-way arrowhead indicates two-way influences between the two compared nodes. In this case study, there are only two-way relationships.

The interrelationships between IC components can refer to the influences of indicators. If there is any measure under the IC component influencing other measures in another IC cluster, this implies that the starting IC component affects another related IC element. For example, Hum 1 influences Org 3, implying that human capital also affects organisation capital.

4.3. Phase 3: Application of the ANP method for computing the weights of IC indicators and IC components

The identified relationships and constructed network model in the previous step were inputted in the Super Decisions software. This ANP solver programme automatically generated entire pairwise comparison questions. All the compared IC measures and IC components were then sent and evaluated by the same expert again through the constructed questionnaire. The results from the answered questionnaires were then entered into the Super Decisions programme to calculate the unweighted supermatrix, weighted supermatrix, and limit supermatrix, respectively.

The importance weights of performance measures and IC components (presented in ) were calculated from the pairwise comparisons, which were formerly evaluated by an expert at the beginning of this phase. The presented results were the latest version in which the CRs were already improved (two rounds of enquiries for this case study) until they met an acceptable level (final CRs are 0.0987 and 0.0785 for the node and cluster level, respectively). Finally, the weights of measures were further applied using the SAW method to calculate the IC performance of the organisations in the next step.

Table 4. The weights of IC elements and measures.

4.4. Phase 4: Application of the SAW method for valuating IC performance

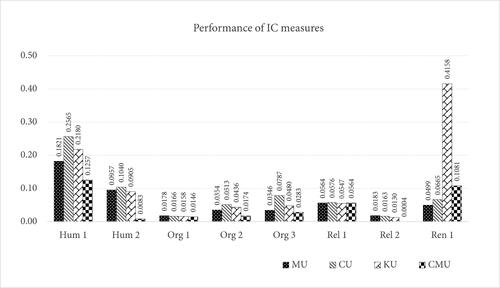

In the last step, the institutional performance data (presented in the performance value columns of ) obtained from the CHEQA system, quality assurance reports and annual reports of organisations were normalised by the best performance values of measures (depicted in the last column of ).

Table 5. Performance values of focused organisations and classifications of performance measures.

The unstandardised performance values from four different institutions were resolved by the normalisation calculation using the EquationEquation (1)(1)

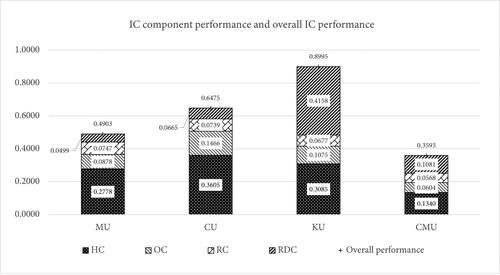

(1) . This mathematics equation converted various and different performance measurement units to a similar, comparable, and unitless scale as shown in . Then, the normalised values were multiplied by the corresponding weights which previously computed and are presented in . The results of multiplications are depicted in . The IC component weight could be summed up from weighted values of all measures in a group using EquationEquation (3)

(3)

(3) , while the holistic performance was calculated by the summation of all values for that organisation or summation of values for all IC components using EquationEquation (4)

(4)

(4) . The valuation of IC performance by different perspectives can be concluded and is shown in , and .

Figure 3. Performance of IC measures. Source: The Authors.

Figure 4. IC component performance and overall IC performance. Source: The Authors.

Table 6. Normalised values for performance.

Table 7. Weighted performance and components as well as holistic performance of IC.

As shown above, the method could be used to calculate the performance of IC and present results on comparable scales and in several presented perspectives: indicator, IC component, and holistic level. Regarding core improvements of the proposed method, the differences in weight assigned to each IC component could affect the overall performance of organisations. For instance, KU was the best performer compared with other competitors. The highest performance of this academic institute derived solely from one outstanding performance of the component RDC. This top weight of the RDC component (measure Ren 1) resulted from its strong influential effect over other IC components that were identified from the integration of ANP in the proposed model, while the weighted and commensurable performance was obtained from the SAW method. The integration of these two MCDM methods could solve the flaws of past methods and serve the purposes of the study.

Although the proposed approach could be successfully developed in accordance with motivation and significance, as well as introduce new abilities and success in the IC measurement method, some conditions are required for its achievement. Additionally, the obtained advantages must also be compensated with some other limitations and weaknesses. Therefore, in the following section, all the crucial issues mentioned before will be analysed and discussed.

5. Discussion

5.1. Significance, motivation and practical implication

Regarding the calculated results and information presented in the previous section, the proposed method could valuate IC performance in various dimensions: indicator level, IC component level, and holistic level. Although the multidimensional results could be discovered in some other IC measurement methods, previous methods still failed to properly cope with some basic characteristics of IC, while the proposed method could better handle this crucial issue.

Rather than being limited by the traditional measurement methods and their improved models, this study proposes an improved measurement method, which provides a more comprehensive and more reliable method. The clearly proposed procedures and computations could provide an explicitly propitious approach that is expected to support the wide application of IC measurements both for academic and practitioner purposes. Furthermore, to accurately reflect the IC performance of organisations, this study resolves the key problems of past IC measurement methods, which mainly rely on the experiences and competence of practitioners or executives, with systematic and reliable decision methods by including ANP and SAW methods. By applying ANP, executives could consider influences and importance weights of the IC components and their measures. This inclusion better provides harmonic magnitude and significance for the IC performance of organisations. Meanwhile, the adoption of SAW could support the standardisation of measurement units, and the calculation of both holistic and atomistic performance. Based on this hybrid method, without much experience in the IC measurement and management, executives could follow a clear systematic process to deal with basic characteristics of IC measurement, as well as crucial issues found in past methods. By using the method, executives would measure more reliable IC performance than the existing IC measurement methods. Ultimately, investors and shareholders would receive measurement results of organisations that correctly reflect IC capabilities of firms.

5.2. Conditions and limitations of the application

Not only is the new integrating approach suggested in this research, but the application of the proposed method was carried out to clearly exemplify its real usage and to examine the applicability and limitations of the method. Therefore, based on the application, some issues arose that should be noted so it can be prevented, and moreover could be improved upon in future work. All major points and conditions are listed as follows:

The addition of the ANP approach to the proposed method increases the processes and complexities of measurements than other methods. Therefore, regarding the complicated procedures and calculations that can possibly lead to inaccurate valuation or other mistakes, a user or person who is in charge must have knowledge and experience with ANP to capably and correctly adopt the proposed method under the limitations of the organisations. Therefore, to facilitate the application of ANP, there are software applications that can support the adoption and calculation of the ANP approach. The software that can fully support all ANP processes is Super Decisions, whereas other tools that mainly facilitate only the computational part are the ANP Solver (add-in tool for Microsoft Excel) and Microsoft Excel. The adoption of these tools could support the success of the practical application of ANP.

Regarding the SAW method, only quantitative performance data can be applied. Moreover, the normalisation process requires the best performance values (maximum or minimum values) of all measures for further calculations of unitless performance. Hence, the method requires comparative performance values from other companies to identify the best performance values. Therefore, to find benchmarking data from other comparable companies, this process adds more complicated tasks to the proposed method. However, if a user wants to avoid the usage of external data sets, another method is available to normalise the performance values. The comparative data for the external companies can be replaced with the best ideal and nadir values following the normalisation approach suggested by Diaz-Balteiro and Romero (Citation2004).

Even though the integration of ANP and SAW could significantly resolve crucial flaws of well-developed IC measurement methods in the past, the advantages of the proposed approach must be exchanged with the possibility of a higher error calculation rate and more time as well as resource consumption. To cope with these issues, a user who has experience, skill, and knowledge regarding the integrated methods is highly recommended; moreover, an organisation should provide additional time and resources for the application of this proposed measurement approach.

In this study, regarding a limited scope as well as number of case studies, it is hard to compare the capability of the proposed approach to other existing methods. Therefore, to prove the better advantage of the proposed approach, a comparative study and more additional applications of the method are highly recommended. Sufficient results of applications as well as opinions of participants from diverse cases are needed for further comparative analysis.

6. Conclusions

In this study, an improved IC performance measurement method is proposed, and the author has decided to name it “the hybrid IC valuation method”. Based on the development and implementation of the method, there are four major suggestions of crucial information and issues, which are the following:

First, even though the proposed hybrid method could resolve crucial flaws of past IC measurement methods, its strength must still be compensated for by the complex procedure, additional time and greater resource consumption. Although many tools are currently available that can improve and alleviate the aforementioned issues, the method still has more complex processes and computations than other widely applied IC measurement methods. Therefore, since the proposed method has both pros and cons, practitioners and academics must realise its strengths and weaknesses before its application.

Second, to improve the ease of use of the method especially for practitioners, the set of applied methods can be changed in other forms that could provide less complex processes as well as computations (e.g., BSC, AHP, and SAW). However, it should be noted that some of the improvement capabilities and strengths from the proposed method will be reduced with respect to substitute methods.

Third, to avoid incorrect measurement and inefficient resource consumption, either academics or practitioners should possess knowledge, skills, and experience with all the applied methods as well as the related calculation tools. Therefore, to successfully implement the method, it is necessary to evaluate the competence of the researchers or practitioners. If they do not have sufficient abilities before implementing the method, related training courses should be provided.

Fourth, to investigate the measuring capability of a method, there needs to be additional empirical studies. Adequate results from various case studies are required for further empirical research focused on the dependence between the results of the method and the ultimate goal of organisations (e.g., financial performance). The significant and strong relationships between these two components would be a critical driver for supporting the establishment of IC measurement standards for organisations and academics.

In conclusion, this research proposes an improved IC measurement approach that aims to solve the weaknesses of existing methods. Although methodological improvement could achieve the objectives of this study, some different issues and limitations were noted. Therefore, to maximise efficiency and effectiveness, academics or practitioners must prudently consider the trade-offs between the proposed method and other existing methods in order to select and use the best measurement approach for their requirements and situation.

Ethical statement

This study was conducted in accordance with the Declaration of Helsinki, International Conference in Harmonization in Good Clinical Practice (ICH-GCP) and the Belmont Report, and the research protocol was approved by the Chiang Mai University Research Ethics Committee (CMUREC No. 62/156 and COE No. 001/63).

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

References

- Bontis, N. (2001). Assessing knowledge assets: A review of the models used to measure intellectual capital. International Journal of Management Reviews, 3(1), 41–60. https://doi.org/https://doi.org/10.1111/1468-2370.00053

- Chang, Y. (2013). Performance measurement of the fourth party logistics providers. iBusiness, 05(02), 7–10. https://doi.org/https://doi.org/10.4236/ib.2013.52B002

- Dash, M. (2016). Banking performance measurement using multi-criteria decision models ELECTRE and PROMETHEE: The case of Indian banks. International Journal of Operations and Quantitative Management, 22(1), 29–37.

- Deventer, V. & Johanna, M. (2002). Introducing intellectual capital management in an information support services environment: Measuring intellectual capital [Doctoral dissertation]. Retrieved from http://upetd.up.ac.za/thesis/available/etd-08012003-162454/unrestricted/04chapter4.pdf

- Diaz-Balteiro, L., & Romero, C. (2004). Sustainability of forest management plans: A discrete goal programming approach. Journal of Environmental Management, 71(4), 351–359. https://doi.org/https://doi.org/10.1016/j.jenvman.2004.04.001

- Dinçer, H., Hacıoğlu, Ü., & Yüksel, S. (2017). Balanced scorecard based performance measurement of European airlines using a hybrid multicriteria decision making approach under the fuzzy environment. Journal of Air Transport Management, 63(1), 17–33. https://doi.org/https://doi.org/10.1016/j.jairtraman.2017.05.005

- Gross-Gołacka, E., Kusterka-Jefmańska, M., & Jefmański, B. (2020). Can elements of intellectual capital improve business sustainability?-The perspective of managers of SMEs in Poland. Sustainability, 12(4), 1545. https://doi.org/https://doi.org/10.3390/su12041545

- Hwang, K., & Yoon, K. (1981). Multiple attribute decision making: Methods and applications. Springer.

- Karadayi, M., & Karsak, E. (2014). Fuzzy MCDM approach for health-care performance assessment. In N. Callaos, S. Hashimoto, A. V. Rutkauskas, B. Sánchez, & C. D. Zinn (Eds.), WMSCI 2014. Proceedings of 18th World Multi-Conference on Systemics, Cybernetics and Informatics (pp. 228–233). International Institute of Informatics and Systemics.

- Kianto, A., Ritala, P., Vanhala, M., & Hussinki, H. (2020). Reflections on the criteria for the sound measurement of intellectual capital: A knowledge-based perspective. Critical Perspectives on Accounting, 70(1), 102046–102015. https://doi.org/https://doi.org/10.1016/j.cpa.2018.05.002

- Lee, Y., Chung, P., & Shyu, J. (2017). Performance evaluation of medical device manufacturers using a hybrid fuzzy MCDM. Journal of Scientific & Industrial Research, 76(1), 28–31.

- Lu, M., Hsu, C., Liou, J., & Lo, H. (2018). A hybrid MCDM and sustainability-balanced scorecard model to establish sustainable performance evaluation for international airports. Journal of Air Transport Management, 71(1), 9–19. https://doi.org/https://doi.org/10.1016/j.jairtraman.2018.05.008

- Nazari, J. (2015). Intellectual capital measurement and reporting models. In P., Ordoñezde Pablos, L. J., Turró, R. D. Tennyson & J., Zhao (Eds.), Knowledge Management for Competitive Advantage During Economic Crisis (pp. 117–139). IGI Global. https://doi.org/10.4018/978-1-4666-6457-9.ch008

- Nimtrakoon, S. (2015). The relationship between intellectual capital, firms’ market value and financial performance: Empirical evidence from the ASEAN. Journal of Intellectual Capital, 16(3), 587–618. https://doi.org/https://doi.org/10.1108/JIC-09-2014-0104

- Marsetio, S., Octavian, A., Sumantri, S., Ahmadi, R., Ritonga, R. & Supartono, (2017). The combination of DEMATEL, ANP, and IPMS methods for performance measurement system design: A case study in KOLAT KOARMATIM. International Journal of Control and Automation, 10(8), 155–170.

- Medel-González, F., Salomon, V., & García-Ávila, L. (2015). Multi-criteria sustainability performance measurement: An application in Cuba. International Journal of Business and Systems Research, 9(4), 394–411. https://doi.org/https://doi.org/10.1504/IJBSR.2015.072586

- Rabbani, A., Zamani, M., Yazdani-Chamzini, A., & Zavadskas, E. (2014). Proposing a new integrated model based on sustainability balanced scorecard (SBSC) and MCDM approaches by using linguistic variables for the performance evaluation of oil producing companies. Expert Systems with Applications, 41(16), 7316–7327. https://doi.org/https://doi.org/10.1016/j.eswa.2014.05.023

- Ramanauskaitė, A., & Rudžionienė, K. (2013). Intellectual capital valuation: methods and their classification. Ekonomika, 93(2), 79–92.

- Roos, J., Roos, G., Dragonetti, N., & Edvinsson, L. (1997). Intellectual capital: Navigating in the new business landscape. New York University Press.

- Saaty, T. (1996). The analytic network process. RWS Publications.

- Saaty, T. (2004). Decision making-the analytic hierarchy and network processes (AHP/ANP). Journal of Systems Science and Systems Engineering, 13(1), 1–35. https://doi.org/https://doi.org/10.1007/s11518-006-0151-5

- Senvar, O., Tuzkaya, U., & Kahraman, C. (2014). Supply chain performance measurement: an integrated DEMATEL and fuzzy-ANP approach. In C. Kahraman & B. Öztayşi (Eds.), Supply chain management under fuzziness (pp. 143–165). Springer.

- Shaik, M., & Abdul-Kader, W. (2018). A hybrid multiple criteria decision making approach for measuring comprehensive performance of reverse logistics enterprises. Computers & Industrial Engineering, 123(1), 9–25.

- Sveiby, K. E. (2010). Methods for measuring intangible assets. Retrieved from http://www.sveiby.com

- Visalakshmi, S., Lakshmi, P., Shama, M. S., & Vijayakumar, K. (2015). An integrated fuzzy DEMATEL-TOPSIS approach for financial performance evaluation of GREENEX industries. International Journal of Operational Research, 23(3), 340–362. https://doi.org/https://doi.org/10.1504/IJOR.2015.069626

- Wu, Y., & Chou, Y. (2007). A new look at logistics business performance: intellectual capital perspective. International Journal of Logistics Management, 18(1), 41–63.

- Wudhikarn, R., Chakpitak, N., & Neubert, G. (2018). A literature review on performance measures of logistics management: An intellectual capital perspective. International Journal of Production Research, 56(13), 4490–4520. https://doi.org/https://doi.org/10.1080/00207543.2018.1431414

- Yurdakul, M., & İç, Y. (2009). Analysis of the benefit generated by using fuzzy numbers in a TOPSIS model developed for machine tool selection problems. Journal of Materials Processing Technology, 209(1), 310–317. https://doi.org/https://doi.org/10.1016/j.jmatprotec.2008.02.006