?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The Chinese government has increased its emphasis on ‘green GDP’ and restricted bank lending to polluting firms. However, government interference may distort bank credit allocation and worsen the external financing environment of polluting firms. Bank competition as a market-based mechanism may play a role in pollution abatement. By matching the Annual Surveys of Industrial Firms dataset with the Ministry of Environmental Protection survey data and the city-level bank competition data, this article explores the effects of banking sector structure on firm-level pollution emissions under the context of bank deregulation. The findings of this study are mainly in four aspects. First, more bank competition can reduce pollution emissions per unit output value. Second, bank competition affects enterprise pollution emissions through alleviating financial constraints. To be more specific, credit availability, credit amount as well as credit cost are the channels for bank competition to affect enterprise pollution emissions. Third, strict environment regulation strengthens the negative effect of bank competition on pollution emissions. Fourth, the mandatory administrative means of impeding banks from lending to polluters did not achieve the aim of pollution reduction. This study provides evidence that the financial system of banks can have a material impact on firms’ pollution emissions.

1. Introduction

The ecological environment problem has become increasingly serious around the world, especially in developing and transitional countries. Pollution can do great harm to human health, such as increasing the incidence of numerous diseases (e.g., cardiorespiratory, cancer, salmonella, typhoid, skin infections, trachoma, cholera and polio), decreasing subjective well-being (Welsch, Citation2006) and shortening human lives (Chen et al., Citation2013; Dominici et al., Citation2014; Ebenstein et al., Citation2015, Citation2017; Lu et al., Citation2015; Pope et al., Citation2009). As the largest developing country, China has experienced rapid economic growth through urbanisation and industrialisation in the past few decades (Wu et al., Citation2019). However, industrialisation and urbanisation have brought a lot of environmental pollution while promoting economic growth (Yang et al., Citation2013). Industrial enterprises should be responsible for more than 90% of the air pollution and 50% of the river pollution in China.Footnote1 The Chinese government now has recognised the importance of environmental protection to sustainable growth and promulgated a series of environmental regulations. Since industrial firms are the major contributors to harmful pollutants (Levine et al., Citation2019), it is fundamental to decrease environmental pollution by reducing firm-level pollutant emissions.

Many factors influence corporate environmental behaviour such as government regulations, community groups, capital market stakeholders, market stakeholders and individual corporation characteristics (He et al., Citation2016; Henriques & Sadorsky, Citation1996; Stafford, Citation2002; Wahba, Citation2008). However, the effect of the financial system on corporate environmental behaviour has been overlooked in previous studies. The Chinese government regards the financial system as an important means to promote environmental protection and restricts banks from lending to polluting firms to inhibit their development.Footnote2 The original intention of this policy is to reduce pollution by worsening the external financing environment and increasing financing constraints faced by the polluters. However, some scholars suggest that more financial constraints not only fail to reduce pollution emissions but also hinder firms from effective pollution abatement (Zhang & Zheng, Citation2019; Zhang, Du, Zhuge, et al., Citation2019). Given the discrepancy between policies and literature findings as well as the lack of studies directly examine the effects of the banking sector on corporate environmental behaviour, this article tries to explore how the development of banking industry measured by bank competition affects the pollution reduction of enterprises.

China’s financial industry is dominated by banks. Bank loans are the primary external financing method, and the equity financing lags far behind the bank-dominated debt financing (Allen et al., Citation2005; Jiang et al., Citation2017). In 2012, the corporate bond market in China provided 8.16% of the total capital raised by corporates in China, whereas banks provided 68.65%. China’s economy has experienced rapid growth, and the banking sector has also experienced unprecedented development, especially after China’s accession to the WTO. Banking competition enables the credit market to play a more effective role, which may affect emissions reduction behaviour of firms. The impact of external credit market conditions on firms’ pollution emissions is less studied, and this study, thus, fills the above gap in the literature.

Bank competition may alleviate credit constraints faced by firms. Easy credit may promote polluters to expand production, thus, increasing emissions. However, there may be countervailing influences. Easy credit may enable firms to invest more in pollution control with the strict environmental regulatory system, thereby reducing emissions per unit output value. By matching the Annual Surveys of Industrial Firms dataset with the Ministry of Environmental Protection survey data and the city-level bank competition data in China, this study provides some evidence that the degree of competition between banks exerts a substantial impact on firms’ pollutants releases. First, we estimate the impact of bank competition on pollution emissions of enterprises and analyze the underlying mechanisms. The results suggest a significant negative relation between bank competition and firms’ pollution emissions. Mechanisms test shows that bank competition first eases financial constraints then reduces pollution emissions of firms. Increasing credit availability and amounts and lowering the credit cost are the specific channels. Second, this article uses the threshold model to examine the heterogeneous influence of bank competition on firms’ pollution emissions under different environmental regulation levels. The results indicate that a single-threshold effect exists in the impact of bank competition on firm pollution reduction. Bank competition has a greater inhibiting effect on firms’ pollution emissions when the government implements more strict environmental regulations. Finally, we divide the whole sample into polluting industries and nonpolluting industries as well as before 2007 and after 2007 to explore the substantial effect of the financial repression policies against non-green enterprises in 2007. The results show that not allowing banks to lend to non-green enterprises cannot reduce the pollution emissions per unit output value.

The main contribution of this study to the literature is threefold. First and foremost, this study provides the first direct empirical evidence on the impact of bank competition on individual firms’ pollution reduction. While there exists a large empirical literature on how bank competition affects firms’ access to finance (Beck et al., Citation2004; Petersen & Rajan, Citation1995) and financial constraints (Chong et al., Citation2013; Zhang, Zhang, et al., Citation2019), how bank competition impacts individual firms’ pollution emissions has not been studied by scholars. To fill in this gap, we investigate the relationship between bank competition and firms’ pollution emissions in the context of China, the world’s largest developing and transitional country. In addition, we provide evidence on the mechanisms to explain our findings. To our best knowledge, no similar researches have been published so far. Second, this study is the first to include bank competition, government environmental regulation and individual firms’ pollution reduction in the same analytical framework. A threshold effect of environmental regulation in the bank competition-pollution emissions relation has been found in this study, suggesting that some degree of environmental regulation is necessary. Third, the results demonstrate that impeding banks from lending to polluters by mandatory administrative means hinders bank competition from playing a role in firms’ pollution reduction. Therefore, the findings of this article are vitally important not only for academics but also for policymakers.

The remainder of this study is organised as follows. Section 2 introduces China’s deregulation in the banking system. Section 3 reviews related literature. Section 4 describes the methodology and data. Section 5 presents and discusses the empirical results. Section 6 concludes this study.

2. China’s deregulation in the banking system

The development of the banking system in China can be divided into three stages. The first stage is from the founding of the People’s Republic of China in 1949 to the implementation of the reform and open-door policy in 1978. The second stage is from 1978 to 2001, the year China entered WTO. The third stage is from 2001 to now.

China’s banking system originated from 1949. Because China’s banking system has not been completed, the People’s Bank of China (PBC) had to act not only as the central bank but also the commercial banks from 1949 to 1978. Before the reform and open-door policy in 1978, China operated under a centralised system that all industries have been firmly controlled by the government. Bank competition actually was virtually nonexistent in that conditions of China (Jiang et al., Citation2017).

After the economic opening policies in 1978, the banking system has been reformed continually as well. In 1983, the ‘Big Four’ banksFootnote3 (i.e., BOC, ABC, CCB and ICBC) took over the commercial bank business from PBC. From 1987 to 2005, twelve shareholding commercial banks were established in succession. These shareholding commercial banks dramatically increased competition among banks (Chemmanur et al., Citation2019). In 1995, the Commercial Bank Law was officially promulgated to guide banks to become more market-oriented. The first mostly privately owned bank Minsheng Bank was established in 1996. Since 1996, regional commercial banks began to emerge. These regional commercial banks primarily contribute to their local economies. In summary, China had already established a complete banking system with the ‘Big Four’ banks dominated, as well as 12 shareholding commercial banks and regional commercial banks as a supplementary before 2001.

China’s banking system reforms had turned into a new phase after entering WTO. The China Banking Regulatory Commission (CBRC) was established in 2003 to supervise and administer banks as well as maintain the legal and steady operation of the banking industry. The ‘Big Four’ were transformed from fully state-owned to shareholding banks through recapitalisation and IPOs. After 2003, CBRC released some reforms to ease restrictions on the banking system, such as allowing foreign banks to operate in ChinaFootnote4, allowing shareholding commercial banks to setup branches in some countiesFootnote5 and removing entry restrictions on opening new branches in a city where a shareholding commercial bank had already setup branches inFootnote6.

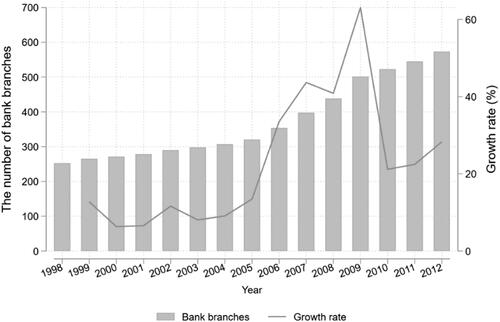

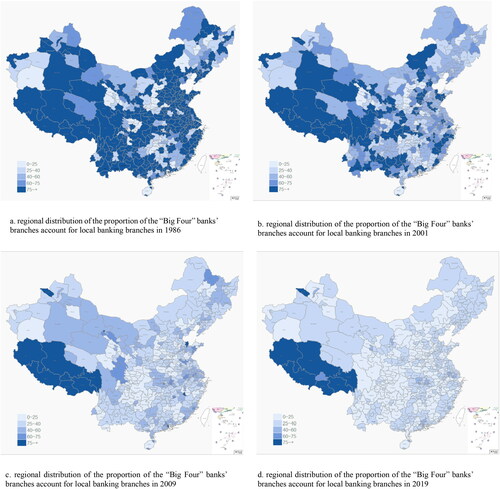

After these reforms, the number of bank branches has increased significantly, and the competition among banks has become increasingly fierce. plots the variation trend of the average number of bank branches at the city-level. As shows, the city-level bank branches rose sharply in 2006, 2007 and 2009 because of the implementation of deregulation policies regarding the banking system. presents the regional distribution of the proportion of the ‘Big Four’ banks’ branches account for local banking branches in 1986, 2001, 2009 and 2019. From , the proportion of the ‘Big Four’ banks’ branches has been declining gradually.

Figure 1. The average number and growth rate of city-level bank branches.

Data Source: China Banking and Insurance Regulatory Commission (CBRC) website.

Source: this study.

Figure 2. The regional distribution of the proportion of the ‘Big Four’ banks’ branches account for local banking branches in 1986, 2001, 2009 and 2019.

Data Source: China Banking and Insurance Regulatory Commission (CBRC) website.

Source: this study.

3. Literature review

This study aims to investigate the real effects of changes in bank competition on the pollution reduction of firms. Although this is one of the first papers trying to investigate the link and mechanisms between bank competition and pollution abatement at firm-level, previous studies have greatly enhanced our understanding of this topic.

3.1. The effects of bank competition on financial constraints faced by firms

Because the financial system of China is dominated by banks, changes in the structure of the banking industry could influence the external financing environment of firms, and further change their financial conditions. There are two opposing views regarding the effects of bank competition on credit constraints. Information hypothesis predicts that high bank concentration (i.e., low bank competition) conducive to the formation of lending relationships between firms and specific creditors resulting in more credits for firms (Petersen & Rajan, Citation1995). In contrast, the market power hypothesis argues that greater bank competition can reduce firms’ financing costs and increase credit availability and amount (Beck et al., Citation2004). More competition increases banks’ willingness to lend to firms at a lower cost, and thus, firms can borrow more for the same costs (Boyd & Nicoló, Citation2005; Guzman, Citation2000; Pagano, Citation1993). Rice and Strahan (Citation2010) and Love and Martínez Pería (Citation2015) also suggest that greater bank competition increases firms’ availability to finance. Along with increases in bank competition, the bargaining power over the loan price shifts from banks to firms, the costs of bank loans will decrease (Jiang et al., Citation2017; Liu et al., Citation2018). Chong et al. (Citation2013) and Zhang, Zhang, et al. (Citation2019) find that growing bank competition reduces firms’ financing constraints, based on data of private and listed Chinese companies, respectively.

In summary, bank competition may impact firms’ financial constraints by changing their external financing environment. Changing firms’ availability to finance, loans amount and costs are the specific channels that the banking sector affects firms’ financial constraints.

3.2. Financial constraints of firms and their pollution reduction

Financial constraints play an important role in firms’ pollution control because pollution abatement investment depends largely on financial conditions (Andersen, Citation2017). Intuitively, exerting financial constraints on polluters, on the one hand, may make them cut down production, thereby reducing total pollution emissions; on the other hand, it may prevent firms from investing in pollution control, consequently increasing pollutants emissions. Therefore, the intuitive effect of financial constraints on pollution reduction is uncertain.

Recently, some studies analyze the effect of financial constraints faced by firms on their pollution reduction. Through combining theoretical model with empirical analysis, Andersen (Citation2017) demonstrates that credit constraints significantly increase firms’ pollution emissions in the United States. The findings of Zhang and Zheng (Citation2019) support the negative effect of financial constraints on pollution reduction by using Chinese data. Using data from Chinese manufacturers, Zhang, Du, Zhuge, et al. (Citation2019) suggest that financial constraints suppress firms’ efforts to reduce waste gas emission. Mitigating the financial constraints of polluters could allow them to equip cleaning equipment so that decrease pollutants emissions per unit of output value (Hao et al., Citation2020). Therefore, existing studies support that financial constraints hinder firms’ pollution reduction actions.

In conclusion, the previous related literature from the above twofold implies a chain that the competition level of banking sector first changes the availability, amount and costs of bank credit, then influences the financial constraints faced by firms and finally acts on firms’ pollution abatement. The present study aims to identify this complex chain from the banking competition to individual firms’ pollution reduction.

3.3. Environmental regulation and pollution reduction

Research about environmental regulation and pollution reduction has reached controversial conclusions. Some scholars believe that environmental regulation can reduce pollution emissions. Porter and Claas (Citation1995) proposed the well-known ‘Porter hypothesis’ which suggests that well-designed environmental regulations can promote corporate innovation activities that offset the costs of complying with environmental regulations. Such ‘innovation offsets’ is based on the fact that reducing pollution is often coincident with improving the utilisation efficiency of resources. Some scholars find that environmental R&D subsidy can promote corporate green innovation and reduce pollutants emissions (Ouchida & Goto, Citation2014; Xing et al., Citation2019). The ‘Porter hypothesis’ has been supported by some empirical studies, such as Laplante and Rilstone (Citation1996) and Cole et al. (Citation2005), which find that environmental regulation reduces firms’ pollution emissions successfully. However, Lanoie et al. (Citation2008) argue that the lagged impact of environmental regulation on productivity is consistent with ‘Porter hypothesis’, while the contemporaneous impact is contrary to ‘Porter hypothesis’. Based on Canada joined and then withdrew from the Kyoto Protocol in 2002 and 2012, respectively, Lv et al. (Citation2020) assess the impact of strict and loose environmental policy on the innovation of oil and gas firms. Their results suggest that strict policies promote firm innovation while loose policies reduce firm innovation. On the contrary, some studies believe that environmental regulation may not promote pollution reduction. The so-called ‘green paradox’ implies that environmental regulation not only cannot slow down but also speed up global warming. Because resource owners may have an incentive to extract the resources earlier under the pressure of environmental regulation (Ritter & Schopf, Citation2014; Sinn, Citation2008). Moreover, some studies find that the ‘Porter hypothesis’ and ‘green paradox’ of environmental regulation exists simultaneously. To be more specific, an inverted-U shaped relationship between environmental regulation and pollution emissions. Before the turning point, environmental regulation shows ‘green paradox’ effect and increase pollution emissions; while after the turning point, it consistent with ‘Porter hypothesis’ and reduce pollution emissions (Zhang & Wei, Citation2014).

With the above related studies in mind, we find that there are still some limitations in this field. First, existing studies on bank competition mainly concerning the impact on financing constraints faced by firms, no study has looked at the effects of bank competition on pollution reduction of enterprises. This research aims to fill this gap by using Chinese data. Second, in the past, the literature did not include bank competition, environmental regulation and pollution reduction in the same analytical framework for theoretical and empirical research. Third, previous studies did not consider the relationship between bank competition and firms’ pollution reduction under different levels of environmental regulation stringency. Therefore, this article detailedly explores how bank competition affects firms’ pollution reduction and the threshold effect of environmental regulation in the bank competition–pollution reduction relationship.

4. Methodology and data

4.1. Empirical methodology

The objective of this study is to analyze the effects of banking deregulation and environmental regulation on firms’ pollution reduction. We build the models from three aspects: (1) the model to assess the impact of bank competition on pollution reduction; (2) the model to explore underlying mechanisms through which banking competition affects pollution reduction; (3) the model to test the threshold effect of environmental regulation in the bank competition–pollution reduction relationship.

4.1.1. The basic model of assessing the impact of bank competition on pollution reduction

To assess the effect of bank competition on firms’ pollution reduction, we estimate the following empirical model:

(1)

(1)

where i, j, c and t indicate firm, industry, city and year, respectively. LnEmission denotes the emissions intensity and is calculated as the natural logarithm of one plus pollution emission per unit output value. We adopted chemical oxygen demand and sulfur dioxide (SO2) emissions to calculate LnEmission. BankCompetition is the independent variable in this study. The value of BankCompetition ranges from zero to one with zero indicating the most regulation and one indicating the most deregulation.

is a vector of controls of firm characteristics that include firm size (Size), the square of firm size (Sizesq), firm age (Age), Leverage, Fixed asset, profitability (ROA), ownership (SOE) and export dummy (Export).

and

capture year, industry and city fixed effects, respectively.

is the random disturbance term.

is the primary interest of EquationEq. (1)

(1)

(1) . A negative

represents that growing competition in banking industry reduces firms’ pollution emissions, and vice verse. Considering the potential endogeneity problem, we use one year lagged independent variables. All continuous variables are winsorized at 1st and 99th percentiles to reduce the effect of outliers. Our results are robust to winsorization. Standard errors are clustered at the firm level. Variable definitions are given in .

Table 1. Variable definitions.

4.1.2. The model to explore underlying mechanisms through which bank competition affects pollution reduction

The four following models are put forward to examine whether financial constraints, availability to finance, credit amount and credit cost are the possible mechanisms through which bank competition affects pollution reduction:

(2)

(2)

(3)

(3)

(4)

(4)

(5)

(5)

where SAindex is the proxy variable of financial constraints. SAindex is measured as the absolute value of −0.737*firm size + 0.043*firm size2 − 0.040*firm age (Hadlock & Pierce, Citation2010). The greater the value of SAindex, the stronger the financing constraints faced by enterprises. Availability is a dummy variable that measures whether a firm receives bank credit. Amount is the amount of bank loan received by a firm. Cost is the total cost associated with per unit of bank credit. The definitions of variables used in these models are given in . We de-mean both variables of the interaction term for ease of the interpretation of

Existing studies suggest that easing financial constraints conducive to pollution reduction of individual enterprises (Andersen, Citation2017; Zhang & Zheng, Citation2019; Zhang, Du, Zhuge, et al., Citation2019). Therefore, if bank competition affects corporate pollution emissions through alleviating their financial constraints, we should expect that the negative effect of bank competition on corporate pollution emissions is more pronounced for firms with stronger financial constraints. If our conjecture is correct, a negative and significant coefficient estimate of

should be observed in EquationEq. (2)

(2)

(2) . If bank competition expands availability to finance and if firms use it to finance their pollution control, then the pollution emissions for companies received bank credit should decrease following increases of bank competition. If the data support our conjecture, then we expect

to be negative and significant in EquationEq. (3)

(3)

(3) . Similarly, if firms get larger amounts of bank credit with increasing bank competition and invest more in pollution control, then, the negative effect of bank competition on pollution emissions should be more pronounced for firms that got larger credit amounts. Therefore, a negative and significant

is expected to be observed in EquationEq. (4)

(4)

(4) . If firms finance at a lower cost with increasing bank competition and fund more in pollution control, the magnitude of the negative effect of bank competition on pollution emissions is larger for firms with lower credit cost. Therefore, we expect to observe a positive and significant coefficient estimate of

in EquationEq. (5)

(5)

(5) .

4.1.3. The panel threshold model to test the threshold effect of environmental regulation in the bank competition–pollution reduction relationship

Under different levels of environmental regulation, the impact of bank competition on firms’ pollution reduction may be different. Therefore, the panel threshold model developed by Hansen (Citation1999) is used to test the impact of bank competition on firms’ pollution reduction under different levels of environmental regulation. The panel threshold model utilised is as follows:

(6)

(6)

where ER is the threshold variable, which is measured by the level of environmental regulation in province p.

is the threshold value of the threshold variable.

in the models is an indicator function indicating the regime defined by the threshold variable (

) and the unknown threshold level (C) and takes a value of 1 or 0 depending on whether the threshold variable is greater or less than the threshold level.

and

are slope parameters of regressors associated with two different regimes.

4.2. Variable measurement

4.2.1. Pollution reduction

In our dataset, there are two water pollution indicators of chemical oxygen demand (COD) and ammonia nitrogen (AN), and three air pollution indicators of SO2, dust and nitrogen oxide (NOx). Because COD and SO2 are the main targets of the Chinese government to reduce emissionsFootnote7, we construct the dependent variable based on emissions of COD and SO2. The dependent variable, emissions intensity, is measured in two ways. The first proxy is the natural logarithm of one plus the ratio of COD emissions to the total industrial output value. The second proxy is defined as the natural logarithm of one plus the ratio of SO2 emissions to the total industrial output value. Detailed definitions are provided in . From the summary statistics in , the mean of COD emissions is 0.251 and the mean of SO2 emissions is 0.514. More directly, the mean of COD emissions per unit output value is 0.778 kg/thousand-yuan, and the mean of SO2 emissions per unit output value is 1.766 kg/thousand-yuanFootnote8.

Table 2. Summary statistics.

4.2.2. Bank deregulation

Along with bank deregulation, the competition among banks will increase. Therefore, in this article, bank competition is used to measure the level of bank deregulation. Traditionally, bank concentration has been widely used as an inverse indicator to measure the level of competition among banks. We use three methods to measure city-level bank competition based on the banks’ market shares in the local city market in the number of branches.

First, we use the Herfindahl–Hirschman Index (HHI) as a proxy for the level of bank competition. This measure is widely used to describe competition in the banking system in previous literature (Alegria & Schaeck, Citation2008; Mercieca et al., Citation2009). HHI is obtained from the following EquationEq. (7)(7)

(7) :

(7)

(7)

where Branchk is the number of the kth bank branches. TotalBranch is the total number of bank branches. c and t denote city and year, respectively.

Second, following Beck et al. (Citation2004), we employ the concentration ratio for the largest three banks (CR3) to bank concentration measures. We calculate the CR3 of each city for each year with EquationEq. (8)(8)

(8) :

(8)

(8)

where Branch1th, Branch2th and Branch3th represent the number of branches of first, second and third largest banks, respectively. is the concentration ratio of city c in year t, that is, the share of the three largest number of branches to the total number of bank branches (TotalBranch).

Third, China’s banking system is dominated by the large and inefficient, state-owned banks, especially colloquially known as the ‘Big Four’ (Allen et al., Citation2008), which includes the Bank of China (BOC), Agricultural Bank of China (ABC), China Construction Bank (CCB) and Industrial and Commercial Bank of China (ICBC). During our research sample period, the ‘Big Four’ is by far the primary external financing source in China while their loan concentration declines significantly throughout our entire sample period (Jiang et al., Citation2017). Therefore, we also calculate the concentration ratio for the ‘Big Four’ banks to measure bank competition using the following EquationEq. (9)(9)

(9) :

(9)

(9)

where BranchBOC, BranchICBC, BranchCCB, BranchABC represent the number of branches of banks of BOC, ICBC, CCB and ABC, respectively. is the concentration ratio for the ‘Big Four’ banks of city c in year t.

Given the three methods of computing bank competition, we do the following transformation to make it a little easier to interpret.

(10)

(10)

(11)

(11)

(12)

(12)

and

range from zero to one with zero indicating the most stringent regulation and one indicating the most deregulation. The empirical regressions based on

and

Using three methods to construct the independent variable can check the reliability and robustness of empirical results. presents the summary statistics. As shown in , on the average, the HHI, the largest three bank concentration (CR3) and the ‘Big Four’ bank concentration (CRbigfour) of the banking system are 0.153 (1–0.847), 0.557 (1–0.443) and 0.514 (1–0.486), respectively. HHI ranges from 0.034 to 0.378; CR3 ranges from 0.255 to 0.906 and CRbigfour ranges from 0.079 to 1. These statistics mean that a huge difference in bank competition exists in different cities and years in China. The ‘Big Four’ still dominates the banking market in terms of these banks’ branch reach.

4.2.3. Environmental regulation

Under different intensity of government environmental regulation, bank competition may have different influence on firms’ pollution emissions behaviour. Therefore, in this study, the environmental regulation is measured from macrolevel rather than firm-level. There are two main methods to measure the intensity of environmental regulation, namely, cost-based environmental regulation indexes and performance-based environmental regulation indexes. The cost-based index measures the level of environmental regulation from the perspective of the input of pollution control. The performance-based index measures the level of environmental regulation from the perspective of the removal rate and utilisation rate of different pollutants. Using the cost-based index may lead to serious endogenous problems because the expenditure of pollution control is usually correlated with the level of regional industrial development and the government’s preference for pollution control. Furthermore, the performance-based index can directly reflect the effectiveness of government environmental regulation (Wu et al., Citation2020). Therefore, this study measures environmental regulation from the perspective of performance-based. The performance-based index is calculated according to the method in Wu et al. (Citation2020). Three indicators of industrial wastewater compliance rate, industrial SO2 removal rate and industrial solid waste comprehensive utilisation rate were adopted to construct the performance-based environmental regulation index. The process can be divided into three steps as follows.

Step 1: Standardise the indicators.

(13)

(13)

where is the standardised value of indicator k of province p in year t; PIp,k,t is the indicator k of province p in year t; min(PIk,t) and max(PIk,t) represent the minimum and maximum values of indicator k at year t in all province in China, respectively.

Step 2: Calculate the adjustment coefficient.

(14)

(14)

where

is the adjustment coefficient of indicator k in province p at year t;

represents the emissions of pollutant k in province p at year t. The pollutant emissions used to calculate this adjustment coefficient include industrial sulfur dioxide emissions, industrial wastewater discharge and industrial solid waste emissions.

is the gross production value of province p in year t. If the emission of pollutant k in the province p at year t is relatively high, thus, the weight given is greater as well.

Step 3: Calculate the performance-based environmental regulation index.

(15)

(15)

where ERp,t is the environmental regulation of province p in year t. The comprehensive indicator represents environmental regulation in this study is obtained hereto. One point should be explained why we employ province level rather than city level environmental regulation. The main reason is that the data at city level has not provided the emissions of industrial solid waste, thus, makes it impossible to calculate the adjustment coefficient. The central government first allocate abatement requirements to each province, and the provincial government further assign abatement mandates to cities and counties (He et al., Citation2020). Therefore, environmental regulation at the province level can reflect the intensity of city environmental regulation to some extent. The summary statistics in show that the environmental regulation index ranges from 1.242 to 22.688, with an average of 6.780.

4.2.4. Control variables

In this article, firms’ specific variables have been controlled to mitigate the omitted variable bias. Specifically, the control variables contain firm size, the square of firm size, firm age, firm leverage, firm fixed asset, ROA, SOE dummy and products exported dummy. Their detail definitions are reported in , and their summary statistics are provided in .

4.3. Data sources

To assess the impacts of banking competition and environmental regulation on firms’ pollution reduction, we construct a comprehensive dataset on firm-level pollutants emissions, city-level bank competition and province-level environmental regulation. Our data mainly come from four datasets. (1) The data of firms’ pollution emission came from the survey conducted by the Ministry of Environmental Protection from 1998 to 2012. (2) The basic firm characteristics were obtained from the Annual Surveys of Industrial Firms dataset (ASIF)Footnote9 spanning from 1998 to 2012Footnote10. (3) The data of city-level bank competition measured by bank concentration were collected from China Banking and Insurance Regulatory Commission (CBRC) website. (4) The province-level environmental regulation data from 1999 to 2010 were extracted from the Ministry of Environmental Protection and the National Bureau of Statistics. Due to the limited access to data, we only obtain the sample before 2013Footnote11. We match them by using firm-level, city-level and province-level identifier, respectively. Considering the availability and comparability of data, we have excluded Hong Kong, Macao and Taiwan from China’s 34 provincial administrative regions. Our final data cover more than 530,000 firm-year observations.

5. Empirical results

5.1. Estimation results of the basic model

5.1.1. Basic regression results

In , we estimate EquationEq. (1)(1)

(1) with COD emissions and SO2 emissions as the dependent variable, respectively. The independent variable is measured through three methods. For each specification, the random effect model (RE) and the fixed effect model (FE) are estimated. Year fixed effects, industry fixed effects and city fixed effects are included in all the models to strip out any persistent differences across years, industries and cities, respectively. When COD emissions are taken as the dependent variable, the coefficients of

are negative and significantly different from zero. Although the RE model of

is not significant, the FE model of

is significant. When SO2 emissions are taken as the dependent variable, the coefficients of bank competition are negative and statistically significant. These results show that increasing competition in the banking system can reduce firms’ pollution emissions.

Table 3. Estimation results of the basic regression model to test the impact of bank competition on firms’ pollution reduction.

5.1.2. Endogeneity concerns

Because firms’ pollution emissions seem unlikely to affect the city-level bank competition, therefore, we suppose that reverse causality is small in this study. However, there may exist omitted variables bias that may lead to endogeneity problems. To deal with this possible endogeneity concerns, we instrument the bank concentration with one-year lagged values of the average value of the concentration indices of the other cities in the same province (Fisman & Svensson, Citation2007). Instrumental variable (IV) must meet two conditions of correlated with the explanatory variable and uncorrelated with the error term. Banks may consider building new branches in other cities of the same province when too much competition in the banking sector in one city. Meanwhile, there exists a clear business segmentation among cities of branches of the same banks which makes it hard for firms to obtain cross-city loans in China (Chong et al., Citation2013). Therefore, the concentration indices of other cities in the same province are not likely to affect firms’ pollution emissions level of one city. The 2SLS estimation results of the instrumental variable (IV) regressions are reported in . The first-stage estimation results of two-stage-least-squares (2SLS) in columns (1), (4) and (7) show that the IV is strongly related to the independent variable. The second-stage estimation results in columns (2), (3), (5), (6), (8) and (9) suggest that the three measurements of bank competition are negatively and significantly associated with firms’ pollutants emissions, meaning that increasing bank competition contributes to firms’ pollution reduction. Therefore, the results of IV regressions support our basic regression results.

Table 4. Estimation results of instrumental variable (IV) regressions.

Our results are consistent with Levine et al. (Citation2019), which found that positive shocks to the credit conditions faced by firms reduced toxic pollutants emissions while credit tightening triggered by the global financial crisis in 2008 increased toxic pollutants emissions. The Chinese banking sector experienced many reforms after the Open and Reform Policy, especially after accession to the WTO. The competition in China’s banking industry has changed dramatically. At the same time, environmental pollution along with China’s economic development became more and more serious. These two changes may be linked to each other. However, most of the available literature focused on the impact of bank competition on corporate credit availability, credit amount and costs, financial constraints as well as corporate innovation and overlooked the possible linkage between these two (Beck et al., Citation2004; Benfratello et al., Citation2008; Chava et al., Citation2013; Chong et al., Citation2013; Cornaggia et al., Citation2015; Petersen & Rajan, Citation1995; Zhang, Zhang, et al., Citation2019). Under such a background, this article provided evidence that increasing competition in the Chinese banking sector did not increase and instead decreased firms’ pollution emissions actions. The findings of this article may address the government’s concern that market-oriented banking system reforms may promote firms’ pollution emissions. Moreover, the findings also extend the role of banks in environmental governance.

5.2. Estimation results of mechanisms test

We have shown that bank competition leads to a negative and significant decrease in corporate pollution emissions. In this section, we explore financial constraints, credit availability, loan amounts and credit costs as four potential channels through which bank competition affects firms’ pollution emissions.

5.2.1. Financial constraints channel

Many previous studies find that increasing bank competition can alleviate the financial constraints faced by firms (Chemmanur et al., 2019; Chong et al., Citation2013; Zhang, Zhang, et al., Citation2019). Other newly published studies which focus on the impact of financing constraints on firms’ pollution emissions suggest that easing a firm’s credit constraints can reduce its pollution emissions (Andersen, Citation2017; Levine et al., Citation2019; Zhang & Zheng, Citation2019; Zhang, Du, Zhuge, et al., Citation2019). Therefore, we expect that bank competition reduces firms’ pollution emissions through easing financial constraints faced by firms seems to be a rational chain. We estimate the financial constraints channel using EquationEq. (2)(2)

(2) . The estimation results are provided in . SAindex is the index of measuring financial constraints faced by firms. If the financial constraints are great faced by a firm, the value of SAindex is greater as well. Both variables of the interaction term have been mean-centered for ease of the interpretation of

Table 5. Estimation results of mechanisms test of financial constraints channel.

As shown in , the coefficient estimates of the interaction terms are all negative and significant, except for column (1). For example, in column (2), the marginal effect of bank competition on corporate pollution emissions is −0.017 if a corporation’s financial constraint (SAindex) is at the sample mean. If a corporation’s financial constraint is above the sample mean by one standard deviation (0.642), then the marginal effect of bank competition on corporate pollution emissions is −0.030 (–0.017–0.02 × 0.642≈–0.030, p-value = .024), revealing that the negative effect of bank competition on corporate pollution emissions is more pronounced for firms with stronger financial constraints. These results suggest that bank competition contributes to firms’ pollution reduction by relieving their financial constraints.

5.2.2. Specific channels of credit availability, amount and cost

In terms of the specific ways in which banking system competition eases firms’ financial constraints, credit availability, credit amount and debt costs have been widespread concerned (Beck et al., Citation2004; Ogura, Citation2012; Petersen & Rajan, Citation1995). To verify these ways, we carry out empirical estimation by employing EquationEqs. (3)–(5), respectively. The empirical estimation results are presented in .

Table 6. Estimation results of mechanisms test of specific ways.

In Panel A, we use COD emissions as the dependent variable. Columns (1), (2) and (3) are for testing credit availability channel. The coefficients of availability are negative and significant meaning that firms which received bank credit discharge less pollutant than that which did not receive bank credit. The interaction terms between bank competition and availability are negatively and significantly associated with COD emissions, suggesting that the negative effects of bank competition on pollution emissions are larger for firms which get bank credit than their counterparts. Based on the coefficient estimate of the interaction term reported in column (1), the marginal effect of bank competition on pollution emissions for firms which received bank credit is −0.109 (–0.07–0.039 × 1= −0.109, p-value = .000), while this magnitude is −0.070 for firms which did not receive bank credit. This result suggests that bank competition decreases firms’ pollution emissions by increasing their credit availability. The empirical results reported in columns (4)–(6) are for testing credit amount channel. The coefficient estimates of the interaction terms are negative and significant, suggesting that the negative effects of bank competition on firms’ pollution emissions are more pronounced for firms that get larger credit amounts. For example, based on the coefficient estimate reported in column (4), the marginal effect of bank competition on firms’ pollution emissions is −0.087 when a firm’s credit amount is equal to the mean of Amount. When adding one standard deviation (3.838) to the mean of a firm’s credit amount, the marginal effect of bank competition on firms’ pollution emissions is −0.141 (–0.087–0.014 × 3.838= −0.141, p-value = .000). Columns (7)–(9) are the tests for credit cost channel. However, the coefficients of interaction terms between bank competition and credit cost are insignificant, suggesting that it fails to support our conjecture of credit cost channel.

Panel B of reports estimation results of mechanisms test for SO2 emissions as the dependent variable. Columns (10)–(12) in Panel B test the credit availability channel. The negative and significant coefficient estimates of interaction terms between bank competition and credit availability support that credit availability can serve as one of the mechanisms through which bank competition decreases firms’ pollution emissions. The tests for credit amount channel are shown in columns (13)–(15). The interaction terms are negatively and significantly associated with SO2 emissions, implying that the negative effects of bank competition on corporate pollution emissions are larger for corporations which received more credit amounts. These results demonstrate that the credit amount is one of the channels through which bank competition affects corporate pollution emissions. The results for testing the borrowing costs channel are exhibited in columns (16)–(18). The coefficient estimates of the interaction terms between bank competition and credit cost are positive and significant, suggesting that the negative effects of bank competition on corporate pollution emissions are more pronounced for corporations with lower credit cost. For example, based on the coefficient estimates reported in column (16), the marginal effect of bank competition on pollution emissions is −0.099 if a firm’s credit cost is at the sample mean. If a firm’s credit cost is below the sample mean by one standard deviation (0.053), then, the marginal effect of bank competition on pollution emissions is −0.140 (–0.099–0.777 × 0.053= −0.140, p-value = .000). These results indicate that firms with lower credit cost experience a bigger decrease in their pollution emissions following increases in banking competition, which suggests that credit cost is one of the channels through which bank competition affects firms’ pollution emissions.

The results of reveal that city level bank competition can promote firms to reduce pollutant emissions by alleviating their financial constraints. Moreover, increasing credit availability and credit amount, and decreasing borrowing costs are the specific channels through which bank competition affects firms’ pollution emissions. These findings are very helpful for us to understand the complex channels through which banking sector structure affects firms’ pollution emissions behaviour.

5.3. Estimation results of the panel threshold model

As the Chinese government realised the importance of environmental protection, a series of environmental protection policies have been promulgated. Under different degrees of environmental regulation stringency, the impact of bank competition on pollution reduction might be different. We use the panel threshold model of EquationEq. (6)(6)

(6) to examine this conjecture. The important feature of this panel threshold model is that it captures the impact of bank competition on firms’ pollution reduction on two different regimes. This study employs the estimation method proposed by Wang (Citation2015) to estimate the fixed effect panel threshold model. The threshold test shows that a single-threshold effect exists in the impact of bank competition on firm pollution reduction. reports the threshold values of environmental regulation under different combinations of independent variables and dependent variables. When SO2 emissions are taken as the dependent variable, the threshold value of environmental regulation is 5.6150 regardless of measurements of the independent variable. In other words, more than 50% of our sample is below the threshold value of environmental regulation stringency. When COD emissions are taken as the dependent variable and BankHHI or

as the independent variable, the threshold value of environmental regulation is 5.3022, but the threshold value is 9.3220 under

serves as the independent variable. Therefore, the impact of bank competition on firms’ emission abatement actions might be nonlinear due to the different environmental regulation stringency. Given this consideration, it is necessary to introduce threshold panel models to explore the impact of bank competition on firm-level pollutants discharge reduction.

Table 7. The threshold value of environmental regulation.

The threshold estimation results are shown in . The dependent variable in columns (1)–(3) is COD emissions and in columns (4)–(6) is SO2 emissions. If the environmental regulation is higher than the threshold value, then the samples are within the regulation stringency interval; otherwise, they are within the regulation loosening interval. No matter which interval environmental regulation is in, the coefficients of bank competition are negative and statistically significant at the 1% level. Although column (2) is an exception, it is noteworthy that within the regulation stringency interval, the coefficients of independent variable are greater than their counterparts within the regulation loosening interval, suggesting that bank competition has a greater inhibiting effect on firm pollution emissions when the government implements more strict environmental regulations. Therefore, the conjecture of the nonlinear impact of bank competition on firm pollution emissions under different government environmental regulation stringency has been confirmed. These results mean that as a market-oriented mechanism to solve the pollution problems of enterprises, bank competition needs to be combined with environmental regulation policies to amplify the inhibiting effect of bank competition on firms’ pollution emissions.

Table 8. Regression results of panel threshold models.

5.4. Industry heterogeneity discussion

This section investigates the heterogeneous effects of bank competition on firms’ pollution emissions based on several subsamples. We discuss the heterogeneous effects in terms of industries and years. First, we classify the whole sample into firms in polluting industries (PI) and nonpolluting industries (NPI). Because polluting industries firms produce most of the pollutants, it is important to concern the effects of bank competition on firms’ pollution emissions in polluting industries. The division of polluting industries and nonpolluting industries follows He et al. (Citation2020). China’s 11th Five-Year Plan (2006–2010) targeting sustainable and green growth, and it affirmed that financial institutions are responsible for supporting pollution reduction (Zhang, Du, et al., Citation2019). CBRC released a series of relevant policies and regulations to restrict banks from lending to non-green companiesFootnote12 in 2007, and the external financing environment of polluting industries has changed completely after 2007. Zhang, Du, et al. (Citation2019) found that 2007 marks a turning point in terms of the leverage, investment and profitability of highly polluting firms. Therefore, we also group the whole sample into before 2007 and after 2007 subsamples to investigate whether the effects of bank competition on pollution emissions for the polluting industrial and nonpolluting industrial firms are influenced by banks regulation enforcement.

The regression analyses of different industries and years are shown in . All sample regression results in columns (1)–(4) suggest that bank competition only reduces pollution emissions of firms in nonpolluting industries. Columns (5)–(8) indicate that bank competition mainly makes the pollution reduction for firms in polluting industries before CBRC restricted banks from lending to polluting firms. However, Columns (9)–(12) show that bank competition primarily affects emission abatement of firms in nonpolluting industries rather than in polluting industries after banks have been restricted to lend to polluting firms. In this regard, the well-intended policies issued by CBRC might reduce the production of total pollutants by cutting down output value of polluting firms; however, it seems unable to make polluting firms reduce pollutants emissions per unit output value. These limited policies seriously affect polluters’ sources of funds, aggravate financing constraints faced by polluters and encourage highly polluting firms to shut down (Hao et al., Citation2020). However, if many polluters close down simultaneously, it may lead to a lot of people lost jobs, industry development retrogression, social instability and some other problems. Therefore, simply cut off the external source of funds for polluting firms to aggravate their situation may not achieve the aim of pollution reduction.

Table 9. Regression analyses of different industries and years.

6. Conclusions and policy implications

Over the past four decades, the Chinese banking sector has been characterised by the rapid expansion of bank branches as well as sharply increased competition among banks. Whether this phenomenon increases individual firms’ pollution emissions as it may allow polluters to obtain more external funds? Is it useful to limit the external financing sources of polluters to reduce their pollution emissions? What is the role of environmental regulations? This article first studies the linkage between bank competition and firms’ pollution emissions, then, explores the specific channels through which bank competition affects individual firms’ pollution emissions. Furthermore, we investigate the threshold effect of environmental regulation on the relationship between bank competition and firms’ pollution emissions. Finally, we discuss the effectiveness of the 2007 environmental regulation policies by using subsamples sorted by industries and years.

The results show that bank deregulation measured by bank competition can reduce firms’ pollution emissions, and it still holds after considering the potential endogeneity problems. Mechanisms test shows that financing constraints, credit availability, credit amount and credit cost are the channels through which bank competition affects individual firms’ pollution emissions. The magnitude of bank competition on firms’ pollution emissions is bigger in regions with strict environmental regulation than that in regions with loose environmental regulation. Our results suggest that directly prevent banks from lending to polluting firms by administrative means cannot reduce the pollution emissions per unit output value of polluting enterprises.

We propose a series of policy implications based on these test results, which may encourage the government to implement better environmental protection policies.

First, the significant negative impact of bank competition on firms’ pollution emissions suggests that the government should not need to worry that more competition in the banking sector may lead to more emissions by polluters. Instead, to address the environmental pollution caused by industrial firms, the government should continue to promote the banking industry market-oriented reform. On the one hand, the government should remove many restrictions which had imposed on the establishment of bank branches and foreign banks to encourage banks to act more effectively in supporting the development of the real economy. On the other hand, the government should treat state-owned banks and non-state-owned banks equally. Most of the small and medium banks are non-state-owned banks, and they mainly provide external financing sources for small- and medium-sized enterprises. Therefore, encouraging the development of small and medium banks can facilitate the development of small- and medium-sized enterprises.

Second, the mechanisms test suggests that alleviating financing constraints, increasing the availability of bank financing, obtaining more credit amount and lowering the cost of financing are the channels through which bank competition affects pollution reduction. In addition, the industry heterogeneity discussion points out that limiting banks to lending to polluting firms by administrative means harms the pollution reduction effect of bank competition. Therefore, the government should not cut off bank loans or forcibly reduce the loan amounts and increase the financing costs of polluting enterprises.

Third, as the threshold effect of the environmental regulation indicating that the inhibiting effect of bank competition on firms’ pollution emissions is greater under stricter environmental regulation, the government should implement strict environmental regulations. For example, the government can set strict pollutants emission standards and punish polluters who violate environmental policies.

However, there are some deficiencies in the research process. First, although we used three methods to measure the competition among banks, however, both three measures are based on the number of branches that cannot accurately measure the market share of each bank. Therefore, the follow-up studies could try to employ other measurements to measure the bank competition, such as the number of deposits and loans of each bank. Second, although we employ the instrumental variable approach to address the endogeneity issue, there may still exist endogeneity issues. The further studies could try to exploit exogenous shocks of bank deregulation to solve the endogeneity. In addition, due to the limited access, the period of this study is from 1998 to 2012. A more precise relationship between bank competition and pollution reduction may be obtained with more recent data in the future.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

Notes

1 The speech of Pan Yue, deputy director of the State Environmental Protection Administration, at the first National Conference on Environmental Policy and Legal Affairs. Available at https://www.douban.com/note/144679418/.

2 For details of these policies, please visit https://www.banklaw.com/laws/bd52106a99ee11e89b644ccc6a5a6fc1.html, http://zfs.mee.gov.cn/hjjj/gjfbdjjzcx/lsxdzc/201502/t20150209_295658.shtml and http://www.gov.cn/banshi/2007-07/31/content_701623.htm.

3 The big four state-owned banks are the Bank of China (BOC), the Agricultural Bank of China (ABC), the China Construction Bank (CCB), the Industrial and Commercial Bank of China (ICBC).

4 This policy was issued in 2006, and the full text of this administrative rule can be referred at http://www.gov.cn/ziliao/flfg/2006-11/15/content_443807.htm.

5 This policy was issued in 2007, and the full text of this administrative rule can be referred at http://www.gov.cn/gzdt/2007-04/06/content_574161.htm.

6 This policy was issued in 2009, and the full text of this administrative rule can be referred at http://www.gov.cn/gzdt/2009-04/30/content_1301338.htm.

7 Please refer to http://www.china.com.cn/environment/2007-06/14/content_8385588.htm for more information.

8 The means of COD emissions per unit output value and SO2 emissions per unit output value were calculated based on the research data directly and are not reported in Table 2.

9 ASIF is an annual survey conducted by China’s National Bureau of Statistics. The survey covers all state-owned and non-state-owned manufacturing enterprises with annual sales above 5 million yuan or 20 million yuan (after 2011). ASIF offers detailed firm-level accounting information and other firm characteristics of listed and unlisted companies.

10 Although using listed Chinese companies database can provide more recent empirical evidence, study databased solely on listed firms may lead to biased results, and thus, unable to find the pollution reduction effect of bank competition.

11 Some studies used a more recent cross-sectional data of year 2013 (Zhang & Zheng, Citation2019; Zhang, Du, Zhuge, et al., Citation2019). Although the data of this study is not up-to-date, the construction of panel data of 1998–2012 can resolve many deficiencies of cross-sectional data, such as controlling for firm and year fixed effects. Therefore, this paper promotes the research on Chinese firms’ pollution reduction by using a more representative panel data.

12 The relevant policies and regulations can be referred at http://zfs.mee.gov.cn/hjjj/gjfbdjjzcx/lsxdzc/201502/t20150209_295658.shtml, http://www.gov.cn/banshi/2007-07/31/content_701623.htm, https://www.banklaw.com/laws/bd52106a99ee11e89b644ccc6a5a6fc1.html, http://www.fsou.com/html/text/chl/1546/154663.html and http://futures.money.hexun.com/2349097.shtml.

References

- Alegria, C., & Schaeck, K. (2008). On measuring concentration in banking systems. Finance Research Letters, 5(1), 59–67. https://doi.org/https://doi.org/10.1016/j.frl.2007.12.001

- Allen, F., Qian, J., & Qian, M. (2005). Law, finance, and economic growth in China. Journal of Financial Economics, 77(1), 57–116. https://doi.org/https://doi.org/10.1016/j.jfineco.2004.06.010

- Allen, F., Qian, J., & Qian, M. (2008). China's financial system: Past, present, and future (pp. 506–568). Cambridge University Press. https://doi.org/https://doi.org/10.1017/CBO9780511754234.015

- Andersen, D. C. (2017). Do credit constraints favor dirty production? Theory and plant-level evidence. Journal of Environmental Economics and Management, 84, 189–208. https://doi.org/https://doi.org/10.1016/j.jeem.2017.04.002

- Beck, T., Demirguc-Kunt, A., & Maksimovic, V. (2004). Bank competition and access to finance: International evidence. Journal of Money, Credit, and Banking, 36(3b), 627–648. https://doi.org/https://doi.org/10.1353/mcb.2004.0039

- Benfratello, L., Schiantarelli, F., & Sembenelli, A. (2008). Banks and innovation: Microeconometric evidence on Italian firms. Journal of Financial Economics, 90(2), 197–217. https://doi.org/https://doi.org/10.1016/j.jfineco.2008.01.001

- Boyd, J. H., & Nicoló, G. D. (2005). The theory of bank risk taking and competition revisited. The Journal of Finance, 60(3), 1329–1343. https://doi.org/https://doi.org/10.1111/j.1540-6261.2005.00763.x

- Chava, S., Oettl, A., Subramanian, A., & Subramanian, K. V. (2013). Banking deregulation and innovation. Journal of Financial Economics, 109(3), 759–774. https://doi.org/https://doi.org/10.1016/j.jfineco.2013.03.015

- Chemmanur, T. J., Qin, J., Sun, Y., Yu, Q., & Zheng, X. (2020). How does greater bank competition affect borrower screening? Evidence from China's WTO entry. Journal of Corporate Finance, 65, 101776. https://doi.org/https://doi.org/10.1016/j.jcorpfin.2020.101776

- Chen, Y., Ebenstein, A., Greenstone, M., & Li, H. (2013). Evidence on the impact of sustained exposure to air pollution on life expectancy from China's Huai River policy. Proceedings of the National Academy of Sciences of the United States of America, 110(32), 12936–12941. https://doi.org/https://doi.org/10.1073/pnas.1300018110

- Chong, T. T., Lu, L., & Ongena, S. (2013). Does banking competition alleviate or worsen credit constraints faced by small- and medium-sized enterprises? Evidence from China. Journal of Banking & Finance, 37(9), 3412–3424. https://doi.org/https://doi.org/10.1016/j.jbankfin.2013.05.006

- Cole, M. A., Elliott, R. J. R., & Shimamoto, K. (2005). Industrial characteristics, environmental regulations and air pollution: An analysis of the UK manufacturing sector. Journal of Environmental Economics and Management, 50(1), 121–143. https://doi.org/https://doi.org/10.1016/j.jeem.2004.08.001

- Cornaggia, J., Mao, Y., Tian, X., & Wolfe, B. (2015). Does banking competition affect innovation? Journal of Financial Economics, 115(1), 189–209. https://doi.org/https://doi.org/10.1016/j.jfineco.2014.09.001

- Dominici, F., Greenstone, M., & Sunstein, C. R. (2014). Science and regulation. Particulate matter matters. Science (New York, N.Y.), 344(6181), 257–259. https://doi.org/https://doi.org/10.1126/science.1247348

- Ebenstein, A., Fan, M., Greenstone, M., He, G., Yin, P., & Zhou, M. (2015). Growth, pollution, and life expectancy: China from 1991–2012. American Economic Review, 105(5), 226–231. https://doi.org/https://doi.org/10.1257/aer.p20151094

- Ebenstein, A., Fan, M., Greenstone, M., He, G., & Zhou, M. (2017). New evidence on the impact of sustained exposure to air pollution on life expectancy from China's Huai River Policy. Proceedings of the National Academy of Sciences of the United States of America, 114(39), 10384–10389. https://doi.org/https://doi.org/10.1073/pnas.1616784114

- Fisman, R., & Svensson, J. (2007). Are corruption and taxation really harmful to growth? Firm level evidence. Journal of Development Economics, 83(1), 63–75. https://doi.org/https://doi.org/10.1016/j.jdeveco.2005.09.009

- Guzman, M. G. (2000). Bank structure, capital accumulation and growth: A simple macroeconomic model. Economic Theory, 16(2), 421–455. https://doi.org/https://doi.org/10.1007/PL00004091

- Hadlock, C. J., & Pierce, J. R. (2010). New evidence on measuring financial constraints: Moving beyond the KZ index. Review of Financial Studies, 23(5), 1909–1940. https://doi.org/https://doi.org/10.1093/rfs/hhq009

- Hansen, B. E. (1999). Threshold effects in non-dynamic panels: Estimation, testing, and inference. Journal of Econometrics, 93(2), 345–368. https://doi.org/https://doi.org/10.1016/S0304-4076(99)00025-1

- Hao, Y., Ye, B., Gao, M., Wang, Z., Chen, W., Xiao, Z., & Wu, H. (2020). How does ecology of finance affect financial constraints? Empirical evidence from Chinese listed energy- and pollution-intensive companies. Journal of Cleaner Production, 246, 119061. https://doi.org/https://doi.org/10.1016/j.jclepro.2019.119061

- He, G., Wang, S., & Zhang, B. (2020). Watering down environmental regulation in China. The Quarterly Journal of Economics, 135(4), 2135–2185. https://doi.org/https://doi.org/10.1093/qje/qjaa024(qjaa024)

- He, Z., Xu, S., Shen, W., Long, R., & Chen, H. (2016). Factors that influence corporate environmental behavior: Empirical analysis based on panel data in China. Journal of Cleaner Production, 133, 531–543. https://doi.org/https://doi.org/10.1016/j.jclepro.2016.05.164

- Henriques, I., & Sadorsky, P. (1996). The determinants of an environmentally responsive firm: An empirical approach. Journal of Environmental Economics and Management, 30(3), 381–395. https://doi.org/https://doi.org/10.1006/jeem.1996.0026

- Jiang, F., Jiang, Z., Huang, J., Kim, K. A., & Nofsinger, J. R. (2017). Bank competition and leverage adjustments. Financial Management, 46(4), 995–1022. https://doi.org/https://doi.org/10.1111/fima.12174

- Lanoie, P., Patry, M., & Lajeunesse, R. (2008). Environmental regulation and productivity: Testing the porter hypothesis. Journal of Productivity Analysis, 30(2), 121–128. https://doi.org/https://doi.org/10.1007/s11123-008-0108-4

- Laplante, B., & Rilstone, P. (1996). Environmental inspections and emissions of the pulp and paper industry in Quebec. Journal of Environmental Economics and Management, 31(1), 19–36. https://doi.org/https://doi.org/10.1006/jeem.1996.0029

- Levine, R., Lin, C., Wang, Z., & Xie, W. (2019). Finance and Pollution: Do Credit Conditions Affect Toxic Emissions?. Working Paper. http://faculty.haas.berkeley.edu/ross_levine/Papers/FinanceandPollution-12062019.pdf

- Liu, P., Li, H., & Huang, S. (2018). Bank competition and the cost of debt: The role of state ownership and firm size. Applied Economics Letters, 25(13), 951–957. https://doi.org/https://doi.org/10.1080/13504851.2017.1388903

- Love, I., & Martínez Pería, M. S. (2015). How bank competition affects firms' access to finance. The World Bank Economic Review, 29(3), 413–448. https://doi.org/https://doi.org/10.1093/wber/lhu003

- Lu, Y., Song, S., Wang, R., Liu, Z., Meng, J., Sweetman, A. J., Jenkins, A., Ferrier, R. C., Li, H., Luo, W., & Wang, T. (2015). Impacts of soil and water pollution on food safety and health risks in China. Environment International, 77, 5–15. https://doi.org/https://doi.org/10.1016/j.envint.2014.12.010

- Lv, X., Qi, Y., & Dong, W. (2020). Dynamics of environmental policy and firm innovation: Asymmetric effects in Canada's oil and gas industries. The Science of the Total Environment, 712, 136371. https://doi.org/https://doi.org/10.1016/j.scitotenv.2019.136371

- Mercieca, S., Schaeck, K., & Wolfe, S. (2009). Bank market structure, competition, and SME financing relationships in European regions. Journal of Financial Services Research, 36(2–3), 137–155. https://doi.org/https://doi.org/10.1007/s10693-009-0060-0

- Ogura, Y. (2012). Lending competition and credit availability for new firms: Empirical study with the price cost margin in regional loan markets. Journal of Banking & Finance, 36(6), 1822–1838. https://doi.org/https://doi.org/10.1016/j.jbankfin.2012.02.006

- Ouchida, Y., & Goto, D. (2014). Do emission subsidies reduce emission? In the context of environmental R&D organization. Economic Modelling, 36, 511–516. https://doi.org/https://doi.org/10.1016/j.econmod.2013.10.009

- Pagano, M. (1993). Financial markets and growth: An overview. European Economic Review, 37(2–3), 613–622. https://doi.org/https://doi.org/10.1016/0014-2921(93)90051-B

- Petersen, M. A., & Rajan, R. G. (1995). The effect of credit market competition on lending relationships. The Quarterly Journal of Economics, 110(2), 407–443. https://doi.org/https://doi.org/10.2307/2118445

- Pope, C. A., Ezzati, M., & Dockery, D. W. (2009). Fine-particulate air pollution and life expectancy in the United States. The New England Journal of Medicine, 360(4), 376–386. https://doi.org/https://doi.org/10.1056/NEJMsa0805646

- Porter, M. E., & Claas, V. D. L. (1995). Toward a new conception of the environment-competitiveness relationship. Journal of Economic Perspectives, 9(4), 97–118. https://doi.org/https://doi.org/10.1257/jep.9.4.97

- Rice, T., & Strahan, P. (2010). Does credit competition affect small-firm finance? The Journal of Finance, 65(3), 861–889. https://doi.org/https://doi.org/10.1111/j.1540-6261.2010.01555.x

- Ritter, H., & Schopf, M. (2014). Unilateral climate policy: Harmful or even disastrous? Environmental and Resource Economics, 58(1), 155–178. https://doi.org/https://doi.org/10.1007/s10640-013-9697-0

- Sinn, H. (2008). Public policies against global warming: A supply side approach. International Tax and Public Finance, 15(4), 360–394. https://doi.org/https://doi.org/10.1007/s10797-008-9082-z

- Stafford, S. L. (2002). The effect of punishment on firm compliance with hazardous waste regulations. Journal of Environmental Economics and Management, 44(2), 290–308. https://doi.org/https://doi.org/10.1006/jeem.2001.1204

- Wahba, H. (2008). Does the market value corporate environmental responsibility? An empirical examination. Corporate Social Responsibility and Environmental Management, 15(2), 89–99. https://doi.org/https://doi.org/10.1002/csr.153

- Wang, Q. (2015). Fixed-effect panel threshold model using stata. The Stata Journal: Promoting Communications on Statistics and Stata, 15(1), 121–134. https://doi.org/https://doi.org/10.1177/1536867X1501500108

- Welsch, H. (2006). Environment and happiness: Valuation of air pollution using life satisfaction data. Ecological Economics, 58(4), 801–813. https://doi.org/https://doi.org/10.1016/j.ecolecon.2005.09.006

- Wu, H., Hao, Y., & Weng, J. (2019). How does energy consumption affect China's urbanization? New evidence from dynamic threshold panel models. Energy Policy, 127, 24–38. https://doi.org/https://doi.org/10.1016/j.enpol.2018.11.057

- Wu, H., Xu, L., Ren, S., Hao, Y., & Yan, G. (2020). How do energy consumption and environmental regulation affect carbon emissions in China? New evidence from a dynamic threshold panel model. Resources Policy, 67, 101678. https://doi.org/https://doi.org/10.1016/j.resourpol.2020.101678

- Xing, M., Tan, T., & Wang, X. (2019). Environmental R&D subsidy, spillovers and privatization in a mixed duopoly. Economic research-Ekonomska Istraživanja, 32(1), 2995–3021. https://doi.org/https://doi.org/10.1080/1331677x.2019.1658530

- Yang, G., Wang, Y., Zeng, Y., Gao, G. F., Liang, X., Zhou, M., Wan, X., Yu, S., Jiang, Y., Naghavi, M., Vos, T., Wang, H., Lopez, A. D., & Murray, C. J. L. (2013). Rapid health transition in China, 1990-2010: Findings from the Global Burden of Disease Study 2010. Lancet (London, England), 381(9882), 1987–2015. https://doi.org/https://doi.org/10.1016/S0140-6736(13)61097-1

- Zhang, D., Du, P., & Chen, Y. (2019). Can designed financial systems drive out highly polluting firms? An evaluation of an experimental economic policy. Finance Research Letters, 31, 218–224. https://doi.org/https://doi.org/10.1016/j.frl.2019.08.032

- Zhang, D., Du, W., Zhuge, L., Tong, Z., & Freeman, R. B. (2019). Do financial constraints curb firms' efforts to control pollution? Evidence from Chinese manufacturing firms. Journal of Cleaner Production, 215, 1052–1058. https://doi.org/https://doi.org/10.1016/j.jclepro.2019.01.112

- Zhang, D., & Zheng, W. (2019). Less financial constraints, more clean production? New evidence from China. Economics Letters, 175, 80–83. https://doi.org/https://doi.org/10.1016/j.econlet.2018.12.032

- Zhang, H., & Wei, X. P. (2014). Green paradox or forced emission-reduction: Dual effect of environmental regulation on carbon emissions. China Population, Resources and Environment, 24(09), 21–29.

- Zhang, Z., Zhang, D., Brada, J. C., & Kutan, A. M. (2019). Does bank competition alleviate financing constraints in China? Further evidence from listed firms. Emerging Markets Finance and Trade, 55(9), 2124–2145. https://doi.org/https://doi.org/10.1080/1540496X.2018.1564905