?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Based on the current context of DE-Capacity in China, this article explores the impact of the merger of public and private firms on capacity and social welfare, with the aim of giving theoretical support to the current practice of mergers and acquisitions in China. With a mixed oligopoly model and Cournot-Nash equilibrium, we conclude that the merger of firms can achieve the goal of DE-Capacity in the market environment dominated by public firms, and that at the same time the social welfare will increase. We also find that if the modest privatisation is considered in the merger then the ultimate social welfare can also obtain further growth with DE-Capacity. In particular, according to the goal of welfare maximisation under different efficiency, we give the optimal privatisation ratio for the merger of public and private firms. However, in the market environment dominated by private firms, the merger of public and private firms cannot achieve the result of increasing social welfare along with DE-Capacity.

1. Introduction

In November 2008, in order to cope with the global financial crisis and stabilise the economy, China government implemented a series of fiscal and monetary policies. The total investment scale of these policies is about RMB 4 trillion, known as the ‘4 trillion’ investment plan in history. Most of the 10 industrial revitalisation plans supported by the ‘four trillion’ investment plan are old industries such as steel, shipbuilding, textile, nonferrous metals, and light industry. In 2007, the output of iron and steel was 480 million tons, which is already the first in the world. After 3 years of implementation of the plan, the number soared to 710 million tons in 2012, nearly half of the world. In the following years, China’s economy once appeared overheated, high inflation and other side effects. In order to solve the problem of overcapacity caused by excessive investment, on 31 December 2015, the central economic work conference proposed that ‘DE-Capacity’ should be listed as the first of the five major tasks of structural reform in 2016, and the idea of ‘more mergers and acquisitions (M&A), less bankruptcy liquidation’ was defined.

In the past few years, China has been implementing M&A to achieve the goal of DE-Capacity. In 2016, China became an important part of the global M&A market, accounting for 15% of the global M&A market, ranking second in the world after the United States. With the gradual realisation of the goal of ‘DE-Capacity’, Chinese M&A market has gradually slowed down. On 20 February 2020, ‘Review of China’s M&A market in 2019 and outlook for 2020’ released by PWC showed that the transaction volume of Chinese firms in 2019 dropped to $558.7 billion, the lowest since 2014, and the transaction volume and number decreased by 14% and 13% respectively compared with 2018.

The scale of China’s M&A is large, even if the value of Chinese M&A transactions declined in 2019, it reached $558.7 billion. Generally, there are ‘big eat small’ and ‘strong-strong alliance’ models in M&A. ‘Big eat small’ model, Alibaba Group announced the wholly owned acquisition of China’s independent embedded CPU IP Core company Zhongtian Microsystems Co., Ltd. The ‘strong-strong combination’ model includes the mergers of CSR Corp and China CNR Corp, China Power Investment Corporation and State Nuclear Power, and Baosteel Group and Wuhan Iron and Steel Group. Advantageous firms are integrated through horizontal mergers, and the ‘big eat small’ model performs better than the ‘strong-strong combination’ model. Studies have shown that during the mergers and acquisitions of domestic listed companies in China, the company’s performance before the merger has stabilised, and the performance of the year after the merger has basically been improved.

Merrill and Schneider (Citation1966) divide firms into these categories: complete private ownership and control, complete government ownership and control, and private ownership restricted by close government supervision in the form of regulation (such as public utilities) and anti-trust laws. Many subsequent studies are also based on such a classification, but there are differences between the micro welfare and the social welfare in terms of the objective function of firms. For example, Hart and Zingales (Citation2017) believe a public company should maximise shareholder welfare not market value, which focuses on the micro welfare. There are also studies on ‘mixed markets’ involving private and public companies, which focus on social welfare, such as Vickers and Yarrow (Citation1988); Matsumura (Citation1998); Hirose and Matsumura (Citation2019). All these literatures assume that the public firm maximises social welfare (the sum of consumer’s surplus and profits by firms) while the private firm maximises its own profits. Following this classification and similar analysis, this article focuses on the theoretical study of M&A from the perspective of social welfare (macro approach) in order to better guide the practice of M&A in China.Footnote1

A large number of scholars have focused on mergers and their impacts. A great deal of literature has been produced. Salant et al. (Citation1983) use the Cournot-Nash model to analyse firms producing a homogeneous good, and find that if all firms have the same constant marginal cost, most horizontal mergers tend to be unprofitable. However, Perry and Porter (Citation1985) show that horizontal mergers of homogeneous firms are profitable using the quadratic cost model. Farrell and Shapiro (Citation1990) and McAfee and Williams (Citation1992) indicate that mergers may have significant impacts on the social welfare. Huck et al. (Citation2004) think merged firms are typically rather complex organisations. Merger has a more profound effect on the structure of a market than simply reducing the number of competitors. They show that this may render horizontal mergers profitable and welfare-improving. Chao et al. (Citation2018) find that for the dual developing economy with public firms in the urban sector, mergers via a reduction in the number of the urban public firms can reduce the cost of capital. In addition, the reduction in the number of the urban public firms can yield a scale effect to the urban public firms. The beneficial effects on higher urban output and less urban unemployment improve social welfare of the developing economy. Haraguchi and Matsumura (Citation2016) adopt a standard differentiated oligopoly with a linear demand in a mixed oligopoly and find that regardless of the number of firms, price competition yields higher welfare.

Based on the theoretical literature that mergers increase social welfare, and taking into account the Chinese practice of DE-Capacity, we propose the main hypothesis of this article.

Hypothesis 1: Merger can increase social welfare while achieving DE-Capacity.

Next, we will verify this hypothesis by constructing a suitable model. For the sake of rigor of the analysis, let us make another hypothesis.

Hypothesis 2: Under the market mechanism, the market behavior of firms in different market environments is consistent - whether public firms dominate or private firms dominate.

In analysing the effects of the merger on the profit and the social welfare, the method of equilibrium analysis is usually adopted, the commonly used models are oligopoly and mixed oligopoly models, and sometimes the level of privatisation of public firms is also considered. Up until now, the literature on oligopoly and mixed oligopoly models is sizable, including Hsu and Wang (Citation2005), Inoue and Nakamura (Citation2007), Liu et al. (Citation2012), Tao et al. (Citation2013), and Chao et al. (Citation2018). Some studies cover special topics. Matsumura (Citation1998), Fujiwara (Citation2015), and Ouattara (Citation2016, Citation2017) consider the optimal level of privatisation for a public firm. In addition, Ouattara (Citation2015) analyses incentives of mergers in an asymmetric mixed oligopoly consisting of two identical private firms and one public firm. However, our research focuses on investigating the reduction in the total output resulting from mergers and the increase in total social welfare as well as the determination of the optimal privatisation ratio of public firm in the merger. Hamada (Citation2020) examines a mixed duopoly in differentiated products and finds that social welfare in Cournot equilibrium is equal to that in the Stackelberg equilibrium when a partially privatised firm is the leader and social welfare is the largest in the Stackelberg equilibrium when a partially privatised firm is the follower.

What these studies have in common is that they are based on firms’ own motivations and behaviour. However, mergers of Chinese firms are more often subject to the government’s intentions. China’s state-owned (public) firms refer to state-owned and state-owned holding firms, and other types of firms are private firms. They are the two most important components of the socialist market economy. Not only can the state-owned firms realise the national social and economic development strategy within a period of time, or the effective means to improve the competitive position of the country in the international market, but also it can solve the imbalance of the economic structure at a certain point, promote the rationalisation and optimisation of the economic structure, and stabilise the ups and downs of the economic cycle. Private firms can optimise the allocation of resources, increase domestic demand, solve employment, and stimulate consumption growth. This article follows Ouattara (Citation2015) which researches the incentives to merge. However, our analytical perspective is different from his article. We analyse mergers under the views on DE-Capacity and find a merger of public and private firms which can reduce the total capacity and increase the social welfare in the market environment dominated by public firms, and the ultimate social welfare can also obtain further growth with DE-Capacity if the modest privatisation is considered in the merger. In particular, according to the goal of welfare maximisation, we give the optimal privatisation ratio for the merger of public and private firms under different efficiency of firms. However, the merger of public and private firms cannot achieve increasing the social welfare with DE-Capacity in the market environment dominated by private firms. This is a major contribution of this article to the literature on mergers.

The article is organised as follows. Section 2 sets up the model. In section 3, we explore the equilibriums of different scenarios. Section 4 provides comparative analysis of the equilibriums. Conclusions are drawn in section 5.

2. The model setup

We consider a market composed of three firms producing a single homogeneous product and analyse the equilibriums according to two different market environments. In the market environment where public firms are dominant, there are two public firms and one private firm. One of the firms is a profit-maximising private firm (demoted by index 0), and the other two are welfare-maximising public firms (denoted by 1 and 2). The quantities of the public firms and private firm are

and

respectively. In the case of no merger, we assume

without loss of generality. In this case, public firms occupy the dominant position in the market, similar to the current market environment in China. The other type of market environment is dominated by private firms. There are two private firms and one public firm in the market. The goal of each private firm is profit maximisation. The goal of the public firm is welfare-maximising. This is more in line with western market conditions. In the two different market environments, we analyse the merger of public firm and private firm respectively and consider the impact of privatisation on the output and the social welfare.

2.1. The market environment dominated by public firms

The inverse demand function is given by

where

is the total output of the good (

). The cost function of firm

is given as follows:

where

This form of the cost functions allows firms to have different technologies. However, we assume that the public firms have identical technologies (

).

When firms and

merge, the merged firm (

) retains two plants, one possessed by firm (

) and the other by firm (

) after the merger. We assume that the merged entity may allocate its production between its two plants in order to minimise its total production cost. Here, we use the same cost function as Ouattara (Citation2015).

where

is the total quantity of the merged firm (

). We define the indicator

given by

to reflect technology differences between the public firms and the private firm. Without loss of generality, we normalise

to 1, so

and

It follows that

and

We assume that

which shows that the efficiency level of private firm is at least as high as the public firms.

The profit of firm is expressed as:

(1)

(1)

where

The social welfare is represented by the sum of consumer surplus (denoted by

) and profits of all firms and given as follows:

(2)

(2)

where

Since the two public firms are identical, without loss of generality, we only analyse the merger of the private firm and public firm 1. The profit function of the merged firm is

(3)

(3)

The social welfare function here is

(4)

(4)

where

Following Matsumura (Citation1998), we assume that when public firm 1 and the private firm decide to merge, the merged firm (01) is partially owned by both the private and the public owners. If we denote as the public owner’s shareholding proportion in the merged firm, then the objective function of the merged firm is given by

(5)

(5)

2.2. The market environment dominated by private firms

For the market environment dominated by private firms, we use a similar setting and get the corresponding results of the formulae (1) to (5) respectively.

The profit of firm is expressed as:

(6)

(6)

where

The social welfare is represented by the sum of consumer surplus (denoted by ) and profits of all firms, given as follows:

(7)

(7)

where

Since the two private firms are identical, without loss of generality, we only analyse the merger of the private firm 1 and public firm. The profit function of the merged firm is

(8)

(8)

The social welfare function here is

(9)

(9)

where

The objective function of the merged firm is given by

(10)

(10)

3. Equilibriums

3.1. The market environment dominated by public firms

3.1.1. Equilibrium before the merger

Assuming that the merger has not yet occurred, we consider a mixed triopoly. The private firm chooses to maximise profit (1), while the public firm

(

) chooses

to maximise social welfare (2). Solving these maximisation problems simultaneously and assuming symmetry between two public firms, we obtain the Nash equilibrium values as given by

3.1.2. Equilibrium after the merger

Public firm 2 chooses to maximise formula (2) and the merged firm chooses

to maximise formula (5). Solving these maximisation problems simultaneously, we obtain the following Nash equilibrium values:

3.2. The market environment dominated by private firms

3.2.1. Equilibrium before the merger

The public firm chooses to maximise formula (7), while the private firm

(

) chooses

to maximise formula (6). Assuming symmetry between two private firms and solving these maximisation problems simultaneously, we obtain the Nash equilibrium values as given by

3.2.2. Equilibrium after the merger

Private firm 2 chooses to maximise formula (6) and the merged firm chooses

to maximise formula (10), then Nash equilibrium values obtained are as following:

4. Comparative analysis

4.1. The market environment dominated by public firms

4.1.1. Comparison of the total output before and after the merger

The difference of the total output before and after the merger is

(11)

(11)

Because the denominator of formula (11) is positive, we just have to examine the sign of the numerator.

Defining then we can conclude the following results.

if

4.1.2. Comparison of the social welfare before and after the merger

The difference between social welfare after and before merger is

Because the denominator of formula (12) is positive, the sign of this formula depends on the sign of the numerator which is a quadratic convex function of since

For the values of

between 0 and 1, we can get the solution for

as

According to the previous analysis, we know the total output of before and after the merger is equal if Substituting

into the numerator of formula (12), we can get the following result:

Thus, we have

To sum up, we come to the following conclusions:

When

When

When

These results mean that the social welfare after the merger is lower than before the merger if the social welfare after the merger is higher than before the merger if

especially, not only is the social welfare higher after the merger than before the merger but also the total output after the merger is not higher than before the merger if

4.1.3. Determination of the optimal privatisation ratio

According to the analysis of the previous section, we get a more useful result. When the merger of considering modest privatisation can produce a relatively low output, but with a higher social welfare. It is very useful to solve the problem of Chinese current ‘overcapacity’.

In this section, we further analyse the results above. We expect to find the optimal proportion of privatisation when public and private firms merge (according to the hypothesis, is the share of public firm,

is the share of private firm).

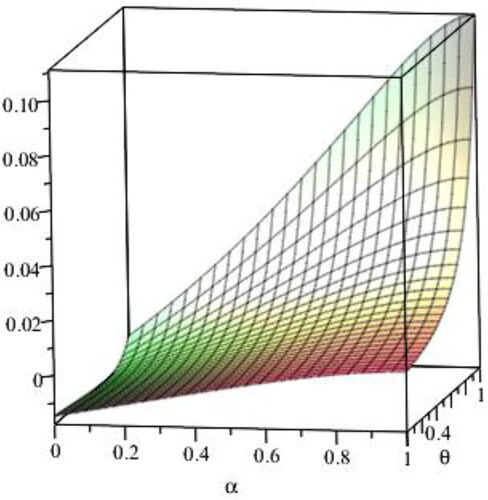

shows the relation of the difference of the social welfare after and before the merger with and

It is obvious that this difference depends on α and θ.

Figure 1. The relation of the difference of the social welfare with and

Source: The Authors.

For different values of we are unable to get the analytical solution

about

to maximise the social welfare, so we use numerical calculation method to solve the optimal proportion of privatisation

for different

values.

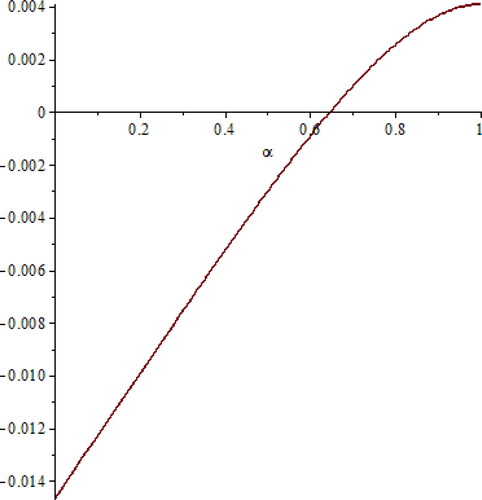

When we get

and

At this point, the relationship between the difference of the social welfare with α is shown in . It is easy to obtain that the output after the merger remains the same, but the difference of the social welfare is maximum when

so the optimal proportion of privatisation

is 0.2, or 20%.

Figure 2. The relationship between the difference of social welfare with α at Source: The Authors.

Similarly, we can calculate the optimal proportion of privatisation at other values of

The results are given in .

Table 1. The optimal proportion of privatisation.

From , we can get that the optimal proportion of privatisation () in the merger will increase with the increase of

The interval

has gradually widened trend, which means that with the increase of the efficiency of private firm, the scope of the proportion of privatisation in the merger that makes less the total output and more the social welfare will increase. With the increase of the efficiency of private firm, the growth rate of privatisation ratio will gradually accelerate.

In practice, we can estimate the value of by combining the efficiency of public firm and private firm, so that we can get the optimal proportion of privatisation in the merger. Therefore, the modest privatisation in the time of the merger can not only achieve the goal of DE-Capacity but also obtain higher social welfare.

4.2. The market environment dominated by private firms

4.2.1. Comparison of total output before and after the merger

The difference of the total output before and after the merger is

(13)

(13)

The sign of the denominator and in the numerator are positive, so we only consider the sign of

in the numerator.

Let we get the following results.

When

When

When

4.2.2. Comparison of the social welfare before and after the merger

The difference of the social welfare before and after the merger is

where the denominator is positive. The sign of the formula (14) depends on the sign of numerator. When

as

the numerator of (14) is the quadratic convex function of

For the values of

between 0 and 1, if

the value of

needs to meet:

Based on the previous analysis, we know that the total output before and after the merger are equal. Substitute into the welfare difference formula above, we get that

To sum up, we come to the following conclusion:

When

When

When

Combining with the previous output comparison, when the private and public firm merge in a market environment dominated by private firms, we cannot increase the social welfare while reducing the total output.

5. Conclusion

According to the analysis of the micro-market mechanism of the merger, we can get that: in the market environment dominated by public firms, the merger of public and private firms will not only reduce the total output but also bring higher the social welfare. Moreover, combining the efficiency of public firm and private firm, the maximum privatisation ratio can also be obtained from the perspective of maximising the social welfare. However, in the market environment dominated by private firms, the merger of public and private firms cannot achieve DE-Capacity and increase the social welfare synchronously.

Based on the analysis results, China can make full use of its institutional advantages and market environment advantages to carry out the merger. At the same time, it is suggested that the government should reasonably introduce private capital in considering the merger to optimise the proportion of public firm, so as to achieve the goal of DE-Capacity and increase the social welfare.

The article explains that firm mergers can achieve the goal of DE-Capacity and increase social welfare by building the suitable models. The contribution of this article is that the horizonal merger of firms in China can achieve the goal of ‘DE-Capacity’ and increase social welfare in theory. In future research, we will expand our model into vertical merger. At the same time, we will collect relevant data and carry out empirical analysis to verify the results of our theoretical analysis. This model of the article can be applied to different industries. These different industries constitute China’s economy entity. Therefore, it is suitable to use this model to illustrate the reduction of overcapacity in different industries. For the product market of an industry, if private firms can enter this market, then the competition between private firms and public firms can still adopt equilibrium analysis, so that our model is applicable even in the transition economies. In addition, for the product market of an industry, if private firms can enter this market, then the competition between private firms and public firms can still adopt equilibrium analysis, so that our model is applicable even in the transition economies.

Disclosure statement

No potential conflict of interest was reported by the authors.

Notes

1 Under World Trade Organisation rules, China will automatically be granted full market economy status in 2016, 15 years after its accession to the WTO. According to the statistics of The Ministry of Commerce of China, up to now, 81 countries in the world have recognised China’s market economy status. Therefore, Current welfare theory in China also inherits the Western theories and standards. There are some differences between Chinese and Western economic theories [refer to Hämäläinen et al. (Citation2019), Zhang et al. (Citation2020), Zhou et al. (Citation2015), Bruton and Ahlstrom (Citation2003), Liu et al. (Citation2019)], but we think China has opened up its economy for decades, so there has been a convergence of Western and Chinese views on welfare due to Chinese pragmatism. Thank the reviewers for their Suggestions.

References

- Bruton, G. D., & Ahlstrom, D. (2003). An institutional view of China’s venture capital industry: Explaining the differences between China and the West. Journal of Business Venturing, 18(2), 233–259. https://doi.org/https://doi.org/10.1016/S0883-9026(02)00079-4

- Chao, C. C., Ee, M., & Wang, L. (2018). Public firms' merger, employment, and welfare in developing countries: A general equilibrium analysis. Review of Development Economics, 22(2), 727–735. https://doi.org/https://doi.org/10.1111/rode.12364

- Farrell, J., & Shapiro, C. (1990). Horizontal mergers: An equilibrium analysis. American Economic Review, 80(1), 107–126.

- Fujiwara, K. (2015). Mixed oligopoly and privatization in general equilibrium. Discussion Paper Series 137, School of Economics, Kwansei Gakuin University, Nishinomiya, Japan.

- Hamada, K. (2020). Mixed duopoly in quantity competition under the optimal privatization rate. Economics Bulletin, 40(1), 689–698.

- Hämäläinen, J., Chen, H., & Zhao, F. (2019). The Chinese welfare philosophy in light of the traditional concept of family. International Social Work, 62(1), 224–239. https://doi.org/https://doi.org/10.1177/0020872817721736

- Haraguchi, J., & Matsumura, T. (2016). Cournot–Bertrand comparison in a mixed oligopoly. Journal of Economics, 117(2), 117–136. https://doi.org/https://doi.org/10.1007/s00712-015-0452-6

- Hart, O., & Zingales, L. (2017). Companies should maximize shareholder welfare not market value. Journal of Law, Finance, and Accounting, 2(2), 247–275.

- Hirose, K., & Matsumura, T. (2019). Comparing welfare and profit in quantity and price competition within Stackelberg mixed duopolies. Journal of Economics, 126(1), 75–93. https://doi.org/https://doi.org/10.1007/s00712-018-0603-7

- Hsu, J., & Wang, X. H. (2005). On welfare under Cournot and Bertrand competition in differentiated oligopolies. Review of Industrial Organization, 27(2), 185–191. https://doi.org/https://doi.org/10.1007/s11151-005-1753-7

- Huck, S., Konrad, K. A., & Müller, W. (2004). Profitable horizontal mergers without cost advantages: The role of internal organization, information and market structure. Economica, 71(284), 575–587. https://doi.org/https://doi.org/10.1111/j.0013-0427.2004.00389.x

- Inoue, T., & Nakamura, Y. (2007). Endogenous timing in a mixed duopoly: The managerial delegation case. Economics Bulletin, 12(27), 1–7.

- Liu, L., Wang, X. H., & Yang, B. Z. (2012). Strategic choice of channel structure in an oligopoly. Managerial and Decision Economics, 33(7–8), 565–574. https://doi.org/https://doi.org/10.1002/mde.2568

- Liu, Q., Luo, T., & Tian, G. G. (2019). How do political connections cause SOEs and non-SOEs to make different M&A decisions/performance? Evidence from China. Accounting & Finance, 59(4), 2579–2619.

- Matsumura, T. (1998). Partial privatization in mixed duopoly. Journal of Public Economics, 70(3), 473–483. https://doi.org/https://doi.org/10.1016/S0047-2727(98)00051-6

- Mcafee, R. P., & Williams, M. A. (1992). Horizontal mergers and antitrust policy. The Journal of Industrial Economics, 40(2), 181–187. https://doi.org/https://doi.org/10.2307/2950509

- Merrill, W. C., & Schneider, N. (1966). Government firms in oligopoly industries: A short-run analysis. The Quarterly Journal of Economics, 80(3), 400–412. https://doi.org/https://doi.org/10.2307/1880727

- Ouattara, K. S. (2015). Incentives to merge in asymmetric mixed oligopoly. Economics Bulletin, 35(2), 885–895.

- Ouattara, K. S. (2016). How privatization affects the strategic choice of managerial incentives: The case of international mixed duopoly. Economics Bulletin, 36(2), 1038–1045.

- Ouattara, K. S. (2017). Strategic privatization in a mixed duopoly with a socially responsible firm. Economics Bulletin, 37(3), 2067–2075.

- Perry, M. K., & Porter, R. H. (1985). Oligopoly and the incentive for horizontal merger. American Economic Review, 75(1), 219–227.

- Salant, S., Switzer, S., & Reynolds, R. (1983). Losses due to Merger: The effects of an exogenous change in industry structure on Coumot-Nash equilibrium. The Quarterly Journal of Economics, 98(2), 185–199. https://doi.org/https://doi.org/10.2307/1885620

- Tao, A., Zhu, Y., & Zou, X. (2013). Welfare comparison of leader-follower models in a mixed duopoly. Journal of Applied Mathematics, 2013(3), 1–7. https://doi.org/https://doi.org/10.1155/2013/320712

- Vickers, J., & Yarrow, G. (1988). Regulation of privatised firms in Britain. European Economic Review, 32(2–3), 465–472. https://doi.org/https://doi.org/10.1016/0014-2921(88)90192-4

- Zhang, X., Liu, Y., Tarba, S. Y., & Giuice, M. D. (2020). The micro-foundations of strategic ambidexterity: Chinese cross-border M&As, mid-view thinking and integration. International Business Review, 29(6), 101710.

- Zhou, B., Guo, J., Hua, J., & Doukas, A. J. (2015). Does state ownership drive M&A performance? Evidence from China. European Financial Management, 21(1), 79–105.