?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The understanding of family businesses from the family side is still in its infancy. This is especially true in relation to how family members manage their relationships with one another and with the firm. Family growth and evolution are usually accompanied by a reduction in shared family meaning and purpose and greater divergence in the form of factional interests and intentions that harm the family and the firm. To counterbalance this negative impact, scholars generally advocate a set of corporate governance practices. However, few papers have analysed how family regulatory frameworks and family governance institutions affect family firm performance. To the best of our knowledge, no paper has analysed the complementary role of family rules and family governance institutions or their relationship with business performance. To fill this gap, we examine how family rules and family governance institutions affect firm performance. Drawing upon the concept of fit from organisation design, this paper shows the complementary role of family rules and family institutions, as well as the need for fit with family complexity. Analysis of a sample of family businesses shows that when family governance fits with family complexity, the relationship with firm performance is positive; any misfit leads to negative consequences.

JEL CLASSIFICATION CODE:

1. Introduction

Two decades ago, Lansberg (Citation1999) reported the negative role of family complexity in family and business outcomes. Since then, considerable research has focused on documenting the consequences of and providing practices to deal with the complexity derived from the evolution of the owner family. Lansberg (Citation1999) observed that family businesses evolve over time and through succession processes. This evolution leads to increasingly complex systems. Lansberg (Citation1999) proposed the concept of family complexity. This concept is defined as the number of family members and the kind of relationships amongst them, as well as the number of generations involved in the family business. Subsequently, Gimeno-Sandig et al. (Citation2006) and Gimeno-Sandig et al. (Citation2010) established a clear differentiation between business complexity and family complexity and proposed a model of fit to manage the risk resulting from each kind of complexity.

With regard to the consequences of family complexity, studies have shown that diluted ownership and low emotional commitment to the business (Vilaseca, Citation2002) cause divergence and reduce cohesion (Montemerlo, Citation2005). Moreover, research on the relationship between levels of family complexity and financial and non-financial performance has revealed a negative and significant impact (De Massis et al., Citation2013; Citation2014; Mazzola et al., Citation2013; Miller et al., Citation2013).

As a way of managing the risk resulting from this kind of complexity, the literature proposes that a normative framework should be developed and formalised to regulate the relationship between the family and the business. The most popular form is the family constitution. The literature also highlights a structure of institutional mechanisms, such as family assemblies and family councils, as a way of promoting family communication and interaction (Aronoff & Ward, Citation2016; Gimeno-Sandig et al., Citation2006, Citation2010; Montemerlo, Citation2005; Mühlebach, Citation2005).

However, the dominant logic in the mainstream literature is a corporate governance approach, proposing a set of institutions and practices aimed at managing and reducing agency costs and blockholder conflicts (Carney et al., Citation2014; Zellweger & Kammerlander, Citation2015). Surprisingly, some of the family business literature presents a paradox: on the one hand, it proposes the management of family conflict by adopting a purely corporate governance logic, whilst on the other, it states that family businesses are driven by a different mindset as regards intention, vision, decision making and performance assessment criteria (Gómez-Mejía et al., Citation2007; Kotlar & De Massis, Citation2013). A consequence is scant research that assesses the impact of family regulatory frameworks (e.g. the family constitution) or family governance institutions (e.g. a family assembly or a family council) on family business performance (Li & Daspit, Citation2016; Suess, Citation2014). In fact, few studies have considered how proper systems of family governance can counterbalance the negative effects of family complexity (Lambrecht & Lievens, Citation2008) and take advantage of the resources provided by a wide and diverse family group (González-Cruz & Cruz-Ros, Citation2016).

To address this gap, this paper analyses the impact of family rules and family governance institutions on family business performance, considering the degree of family complexity. The analysis focuses on the family and on how family governance affects business performance. The paper draws on the concept of fit, a key concept in organisation design, and builds on the contingent model of fit proposed by Gimeno-Sandig et al. (Citation2006, Citation2010). Based on this approach, it tests the proposition that the impact of the family governance system on business performance depends on the internal fit of the elements that make up the family governance system and on the external fit with the contingency of family complexity. Any misfit is expected to lead to negative effects on performance. The analysis is based on a sample of 378 Spanish family businesses in the tourism industry.

The rest of the paper has the following structure. Section 2 succinctly presents the theoretical framework that supports the hypotheses. Section 3 describes the fieldwork, sample and operationalisation of the research variables. Section 4 presents the method and results based on panel regressions. Finally, Section 5 offers conclusions and recommendations.

2. Theoretical framework and hypotheses

As noted by Jaskiewicz and Dyer (Citation2017), there is a need to consider the stages, features and challenges of the evolution of the owner family from the family side, not only from a managerial point of view. Since Lansberg (Citation1999) identified the concept of family complexity, the family business literature has focused on managing family complexity using a corporate governance approach, which relies on two main streams of research. First, exponents of agency theory propose how to protect the firm from owner family faultlines and conflicts (Zellweger & Kammerlander, Citation2015). Second, adherents of stewardship theory and socioemotional wealth theory focus on how to channel the family logic and its specific goals into the business project (Madison et al., Citation2016; Vandekerkhof et al., Citation2018; Villalonga et al., Citation2015).

Surprisingly, research from the perspective of family logic (i.e. focusing on family governance) is less developed than research from a corporate governance approach. Similarly, the literature on family governance frequently focuses on specific events, mainly CEO succession (Brenes et al., Citation2006; Breton-Miller et al., Citation2004; Gilding et al., Citation2015). To the best of our knowledge, few papers have analysed how to manage family complexity through a family governance system, which is understood here as a complementary set of rules and institutions. Similarly, few papers have studied the impact of family governance on firm performance (Arteaga & Menéndez-Requejo, Citation2017).

To fill this gap, we first present the concepts that support the underlying theoretical framework of this paper, namely the model of fit proposed by Gimeno-Sandig et al. (Citation2006, Citation2010). The concept of fit comes from information processing theory (Burton et al., Citation2002, Citation2003; Egelhoff, Citation1991; Galbraith, Citation1974; Keller, Citation1994; Tushman & Nadler, Citation1978), a cornerstone of organisation design. Over the next few pages, we present the literature on family business complexity. Our aim is to state and support a set of hypotheses that link the development of the family governance system to family firm performance. We also distinguish between the two main spheres of the family governance system: the family regulatory framework and the family governance structure. We show the systemic interdependence of these two spheres.

2.1. Family complexity from the approach of fit

According to organisation design theorists, fit refers to the alignment of the organisation’s features to address a contingency factor such as uncertainty (Burns & Stalker, Citation1961; Lawrence & Lorsch, Citation1967) or size (Child, Citation1975). The resulting organisation design is the most suitable one in the sense that it enables the organisation to meet its goals and achieve high performance.

The theoretical foundation of this conceptualisation of fit is based on information processing theory (Galbraith, Citation1974). According to information processing theory, contingencies are an information processing requirement, with organisational structure providing the information processing capacity to meet that requirement (Burton et al., Citation2002, Citation2003; Egelhoff, Citation1991; Keller, Citation1994; Tushman & Nadler, Citation1978). A fit occurs when the information processing capacity matches the information processing requirement. If the information processing capacity is not equal to the information processing requirement, there is a misfit, which leads to underperformance. Later, organisation scholars coined two types of misfit: over-fit and under-fit (Klaas et al., Citation2006; Klaas & Donaldson, Citation2009; Naman & Slevin, Citation1993). Over-fit happens when the structural development is greater than the amount required by the contingency variable, so it is essentially a waste of resources. On the contrary, under-fit occurs when the level of structural development is lower than the amount required by the contingency variable, which causes organisational disability. The same scholars state that both over-fit and under-fit negatively affect performance.

In relation to family businesses, Gimeno-Sandig et al. (Citation2006, Citation2010) proposed a model of fit where the resulting variable is the level of structural risk of the family business and where the amount of risk depends on the misfit between the accumulated level of business and family complexity and the level of structural development. This structural development depends on institutionalisation, appropriate family and business separation, best practices (including formalisation and explicit rules), communication practices and succession management.

Recent research (González-Cruz & Cruz-Ros, Citation2016) has provided empirical evidence supporting the utility of the model of fit proposed by Gimeno-Sandig et al. (Citation2006, Citation2010) in managing structural risk. However, these results are based solely on the business side of the model, and those scholars have called for future research to shed light on the consequences of over-fit.

To help fill this gap, this research looks to the family side of the model. From this approach, we analyse the misfit between family complexity and the structural development specifically aimed at dealing with this complexity, and we examine its effect on performance. The family business literature proposes managing family complexity by developing specific structural artefacts. Examples include the formalisation of a normative framework that regulates the relationship between the family and the business. The literature also proposes the use of a set of institutional mechanisms, such as family assemblies and family councils, that promote family communication and interaction (Montemerlo, Citation2005; Mühlebach, Citation2005). The next sub-section briefly presents the contingency considered in this study (i.e. family complexity) and its consequences.

2.2. Family complexity

Early research on family businesses showed that families evolve over time and through succession processes to develop into increasingly complex systems (Lansberg, Citation1999). This evolution raises new challenges such as ownership dilution, a reduction in commitment to the business, divergence, invisible but deep faultlines and blockholder conflicts (Montemerlo, Citation2005; Vilaseca, Citation2002). These conflicts deplete the firm’s ability to compete and undertake new projects (De Massis et al., Citation2013, Citation2014; Mazzola et al., Citation2013; Miller et al., Citation2013), exerting a negative effect on firm performance, which Dyer (Citation2006) calls the ‘family effect’.

The literature reports that, to a certain point, ownership dilution (i.e. a limited number of family factions with a high proportion of wealth tied up in the business) is detrimental to firm performance (De Massis et al., Citation2013; Mazzola et al., Citation2013; Miller, Le Breton, & Lester, 2011). Similarly, having more generations means greater and more improper involvement of family members in management, as well as deeper family embeddedness (Miller et al., Citation2011) and pay dispersion amongst non-CEO top managers (Jaskiewicz et al., Citation2017). Considering these arguments, Hypothesis 1 is proposed as follows:

Hypothesis 1: There is a negative relationship between family complexity (measured as the number of generations and number of stakeholders) and firm performance.

To manage the risk associated with family complexity, Gimeno-Sandig et al. (Citation2006, Citation2010) proposed a model of fit that links the degree of family complexity to the development of a family regulatory framework and a family institutional structure (Berent-Braun & Uhlaner, Citation2012; Suess, Citation2014). When both of these mechanisms fit with the level of family complexity, the level of structural risk of the family business drops.

2.3. Family regulatory framework

The creation and deployment of rules regulating ownership and work in relation to the family business are well-known ways of managing the owner family. These rules provide protection against owner-owner agency costs (Arteaga & Menéndez-Requejo, Citation2017), develop and protect ‘familiness’ (Minichilli et al., Citation2010; Suess, Citation2014), regulate ownership transmission without draining financial resources or reducing family control (Neubauer & Lank, Citation2016), formalise communication processes, strengthen a shared commitment to norms and values (Neubauer & Lank, Citation2016), shape the owner’s mindset, and provide institutional legitimacy to the family and the business (Reay et al., Citation2015).

These rules cover three main areas: human resource policies for family members (Kidwell et al., Citation2018), the presence of family members in managerial positions and CEO succession (Chittoor & Das, Citation2007), and the valuation and transmission of stakes (Villalonga et al., Citation2015). These family regulatory frameworks generally enhance corporate governance and rules regarding the inclusion of family members in the company. This effect limits family managers’ opportunism and promotes professionalisation, which in turn improves performance. In addition, a suitable family regulatory framework increases feelings of procedural justice between family members (Berghe & Carchon, Citation2003) and increases socioemotional wealth (SEW), which positively influences performance (Hernández-Perlines et al., Citation2020). Accordingly, Hypothesis 2 is proposed as follows:

Hypothesis 2: There is a positive relationship between the family regulatory framework and firm performance.

With regard to family complexity, multiple family owners from different generations are likely to differ in their financial and non-financial interests. This discrepancy potentially leads to family feuds and conflicts (Bertrand et al., Citation2008; Eddleston & Kellermanns, Citation2007; Zellweger & Kammerlander, Citation2015) that can harm firm performance. However, owner family agreements that are formalised as rules prevent blockholder conflicts. Therefore, we expect family complexity to have a less negative effect on performance when the family regulatory framework is stronger. Consequently, Hypothesis 3 is stated as follows:

Hypothesis 3: The negative relationship between family complexity and firm performance is weaker when the family regulatory framework is stronger.

However not all family issues and challenges can be managed using a set of rules. Certain matters need a family governance structure.

2.4. Family governance structure

The family governance structure refers to institutional arrangements to manage family identity, harmony and wealth. The family governance structure is clearly separate from the corporate governance and management of the family-owned firm (Aronoff & Ward, Citation2016; Eckrich & McClure, Citation2012).

The literature identifies two core dimensions of the family governance structure. The first dimension is wealth. A family office is a structure designed to professionalise wealth management and optimise profitability whilst reducing the financial risk and tax burden (Naldi et al., Citation2015; Rivo-López et al., Citation2017). The family office separates the family from its wealth, reducing the risk of irresponsible altruistic tendencies or wasteful financial behaviours (Miller et al., Citation2017).

The second family governance structure dimension has to do with family harmony and unity of purpose. Institutional mechanisms such as the family assembly and the family council are devoted to ensuring regular meetings between family members (Gersick et al., Citation1997; Suess, Citation2014). The main function of these meetings is ‘to achieve, maintain, and increase family members’ unity both among themselves and with their family business’ (Gallo & Kenyon-Rouvinez, Citation2005, p. 53). The purpose of the family assembly and family council has to do with cultivating trust and a shared vision amongst family members (Gnan & Montemerlo, Citation2006) to enhance their emotional commitment to and identification with the family and the firm (Björnberg & Nicholson, Citation2012). Similarly, the family assembly and family council improve family communication (Labaki, Citation2011; Suess, Citation2014) and offer an orderly and structured vehicle to convey the needs and expectations of the family with respect to the firm (Aronoff & Ward, Citation2016; Eckrich & McClure, Citation2012; Nordqvist & Melin, Citation2010).

The family council should be a clearly differentiated family governance institution whose aim is to preserve and enhance family harmony and unity of purpose (Poza, Citation2013). The function of a family council has to do with family unity and harmony (Aronoff & Ward, Citation2016; Eckrich & McClure, Citation2012; Poza, Citation2013). From this perspective, the family council is the formal forum where the family builds an explicit set of common values (Aronoff & Ward, Citation2016; Tàpies & Fernandez-Moya, Citation2012) and principles (Sundaramurthy, Citation2008) that govern intra-family interactions and family-firm relationships. Trust, commitment, harmony, common intention and unity of purpose form the foundations of a functional family that contributes to the firm (Aronoff & Ward, Citation2016; Chittoor & Das, Citation2007; Eckrich & McClure, Citation2012; Gnan & Montemerlo, Citation2006; Sundaramurthy, Citation2008; Vilaseca, Citation2002). Other authors have underlined the role of the family council as a channel for the transfer of family values, mindset, identity and intention towards the firm (Aronoff & Ward, Citation2016; Craig et al., Citation2008; Eckrich & McClure, Citation2012; Nordqvist & Melin, Citation2010; Tàpies & Fernandez-Moya, Citation2012).

With regard to the impact of family governance structure institutions on performance, the results are inconclusive. Some studies (e.g. De Massis et al., Citation2015) have shown a negative but non-significant relationship between the family council and gross profit margin. However, most of the evidence supports the positive effect between family governance structure and firm success (Brenes et al., Citation2011) or financial performance (Arteaga & Menéndez-Requejo, Citation2014, Suess-Reyes, Citation2017). Therefore, the following hypothesis is proposed:

Hypothesis 4: There is a positive relationship between the family governance structure and firm performance.

With regard to the interaction between the family governance structure and family complexity, the family office and, especially, the family council minimise potential conflicts due to family complexity (Arteaga & Menéndez-Requejo, Citation2017; Cruz et al., Citation2014; Vardaman & Gondo, Citation2014). The family governance structure promotes family cohesion, which also minimises the negative effects of family problems on family firm reputation (Arteaga & Menéndez-Requejo, Citation2017; Vardaman & Gondo, Citation2014). Furthermore, The family governance structure enhances stewardship behaviour by promoting cohesion, values and open communication between family members (Gallo & Kenyon-Rouvinez, Citation2005; Suess, Citation2014). The family governance structure contributes to creating a favourable organisational environment (Chirico et al., Citation2011; Sirmon et al., Citation2008). In such an environment, the family business can benefit from the interactions and ties between family members that are necessary to take advantage of the rich, diverse endowment of knowledge, relationships and competencies that a complex family offers (Brenes et al., Citation2011; Umans et al., Citation2020). Considering these findings, Hypothesis 5 is proposed as follows:

Hypothesis 5: The negative relationship between family complexity and firm performance is weaker when the family governance structure is stronger.

2.5. Family governance as a system

Aronoff and Ward (Citation2016, p. 6) define family governance simply but forcefully: ‘effective governance can be defined as creating processes that make revolution unnecessary’. Thus, family governance should not only prevent and manage conflicts today but also enable the smooth transition from generation to generation and through the different stages of the family in the future.

The research underlines the role of the family regulatory framework, especially the family constitution, as a safeguard against conflicts, harmful decisions and destructive behaviours. This approach emphasises the concept of mutual accountability but overlooks others that are equally important, such as understanding, acceptance and adherence. These concepts provide the required sense of shared principles and aspirations amongst family members, as well as a sense of consistency and fairness. Therefore, a family regulatory framework requires a set of institutions and processes for interpretation, amendment and adaptation to new realities and family members’ aspirations. Without the support of this family governance structure, family constitutions become a ‘blue law’ – a ‘monument’ to the founder generation (Tait, Citation2019, p. 15).

Alderson (Citation2015) reports the complementary functions of the family regulatory framework and the family governance structure. The latter offers the appropriate forum to interpret, develop and update the rules that regulate the relationship between the family and the business. Similarly, the former is necessary to enable the mechanism of the family governance structure (i.e. family meetings, assemblies, councils, committees and task forces) to operate smoothly and correctly. As Aronoff and Ward (Citation2011, p. 26) explain, ‘[o]nce family businesses make a positive transition to organized governance procedures, governance has a way of taking care of itself’.

In terms of information processing theory, the family regulatory framework and the family governance structure are complementary but non-substitutive structural solutions to deal with family complexity. A family regulatory framework provides adequate structural mechanisms to manage limited uncertainty and routine challenges (Luo & Donaldsen, Citation2013). It works on the premise that there is an agreement about core issues – or at least an acceptance of a basic set of shared beliefs, values and principles – between key family members to deal with a set of possible future events. In parallel, the family governance structure is based on an institutional framework suitable for managing high uncertainty and non-routine challenges (Luo & Donaldsen, Citation2013). Therefore, it is a necessary structural capability to build basic agreements and develop a set of core beliefs, values and principles that the family group must adhere to, or at least accept, to achieve a unity of purpose. Accordingly, the family regulatory framework and the family governance structure complement each other but are not substitutive structural mechanisms. Hence, an effective family governance system requires both internal fit between the family regulatory framework and the family governance structure and external fit with contingency (in this case, family complexity). In accordance with these arguments, Hypotheses 6 and 7 are proposed as follows:

Hypothesis 6: There is a positive and complementary relationship of the family regulatory framework and the family governance structure with firm performance.

Hypothesis 7: The positive and complementary relationship of the family regulatory framework and the family governance structure with firm performance is stronger when family complexity is higher.

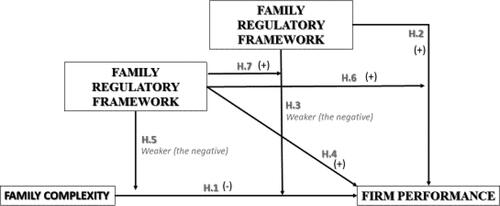

In summary, graphically illustrates the research model and the proposed hypotheses.

Figure 1. Research model and hypotheses. Source: own research.

3. Data and variables

3.1. Databases

We used a database from a primary study of the Spanish tourism industry. The economic activity of tourism is defined by the Spanish Institute of Tourism Studies (Instituto de Estudios Turísticos) in their analysis of the Spanish Labour Force Survey (Encuesta de Población Activa – EPA). The sample was selected from the entire population of Spanish tourism companies appearing in the 2008 Central Companies Directory (DIRCE) compiled by the Spanish National Institute of Statistics (INE). From a population of approximately 140,900 firms, we selected a sample of 8,148 companies. We used stratified random sampling with proportional allocation to ensure the representativeness of the sample in terms of activity (considering five groups), size (taking number of employees as a proxy of the size of the company) and location. After various data cleansing processes, the fieldwork provided a sample of 1,019 companies, with a confidence level of 95% and an error interval of ± 3.1%. The resulting sample represented a response rate of 25.6%.

The research team gathered data through personal interviews with the firms’ CEO or general manager. To address possible difficulties regarding surveys as a data collection method, we followed a set of recommended methods based on Dillman’s (Citation1978) Total Design Method for questionnaire-based research. The fieldwork lasted from December 2009 to March 2010. The sample consisted of 271 non-family businesses and 748 family businesses.

We gathered data on firm performance from 2008 to 2016 using the Sistema de Análisis de Balances Ibéricos (SABI), a database managed by Bureau Van Dijk and Informa D&B, S.A. Because SABI does not offer complete financial information on all interviewed companies, our final data set comprised 543 companies, of which 165 were non-family businesses and 378 were family businesses. This sample offered a reasonable overall representation of the Spanish tourism sector. The sample covered five tourism sub-sectors: accommodation, catering, intermediaries, transport and complementary offer ().

Table 1. Tourism activity.

3.2. Variables

In this section, we describe the variables used in the research model. To mitigate the effect of outliers, we winsorised all variables at 0.5% of each tail of the distribution.

3.2.1. Dependent variable

Return on assets (ROA). The dependent variable, ROA, was defined as EBIT (earnings before interest and taxes) divided by the book value of total assets (Amore, Garofalo & Minchilli, 2014; Anderson & Reeb, Citation2003; Andres, Citation2008; Bouzgarrou & Navatte, Citation2013; Molly et al., Citation2010). Papers published in top academic journals propose ROA as a reliable indicator to assess the impact of action by the owner family on the firm’s capacity to generate economic performance.

3.2.2. Independent variables

Our independent variables were operationalised as indices based on proxies. These were taken from data gathered in the 2009 survey. As in prior studies, our indices were estimated by adding scores for every feature that was present in the surveyed company (Ben-Amar et al., Citation2013; Gompers et al., Citation2003). Higher scores denote a higher level of the index (Black et al., Citation2006).

Family complexity

The family complexity index was based on three proxies from our survey. The first proxy was the percentage of equity held by the largest shareholder. Following Ben-Amar et al. (Citation2013), we divided the sample by the median of this proxy. The variable took the value of 1 if the percentage of equity held by the largest shareholder was below the median, and 0 otherwise. The second proxy was the dominant generation. If the founder had the decision-making power, then the proxy took the value 0. If it was the second generation, then it took the value 1. If it was beyond the second generation, then it took the value 2. The third proxy was the number of family shareholders in the company. Since this index refers to ownership dispersion, we followed the indications provided by De Massis et al. (Citation2013) and Wiklund et al. (Citation2013), who report an inverted U-shaped effect of ownership dispersion. In other words, ownership concentration generates a positive effect on performance (Hoopes & Miller, Citation2006). However, to some extent, property dispersion is harmful to business performance. Beyond this point, additional dispersion has a positive impact on firm performance, given that shareholders’ behaviour is similar to that of shareholders in listed firms. Accordingly, if the number of family shareholders was 1, then the proxy took the value 0. If the number was between 2 and 5, then it took the value 2. If the number was between 6 and 20, then it took the value 1. Finally, if the number of family shareholders was greater than 20, then it took the value 0.

Family regulatory framework

This variable depended on the number of agreements, provisions and rules that the owner family had put in place. Examples include a family constitution, rules for new family members to join the firm or board, rules regarding the family members’ duties in the company, rules for top manager succession, agreements related to power distribution amongst different branches of the family, liquidity policies, rules for stake transmission, and rules to transfer ownership to the next generation. The index was designed as follows: if there was a formal rule, then the index took the value 1; if there was a verbal agreement, then it took the value 0.5.

Family governance structure

As with the preceding independent variable, this third variable reflected the presence of family governance mechanisms such as structures to organise family wealth, a family assembly, a family council and so on. If there was an institutionalised device, the index took the value 1; if there was an informal structure, then the index took the value 0.5. Additionally, we added a proxy to capture how often the family assembly and the family council met. If they met two or more times over the course of the year, then it took the value 1. Finally, we used a proxy to assess the family council usefulness. We considered whether it allowed the exchange of opinions, avoided conflicts, fostered family commitment with the company, worked as a channel of information on the company for the family, organised joint leisure activities, revised the family protocol, defined the rules for family members to join the company, and set the financial policies to manage family wealth. The sample was divided into terciles (Francoeur et al., Citation2008). If the family council assessment fell into the first or second tercile, then the proxy variable took the value 1.

3.2.3. Control variables

The control variables in this study were size (natural logarithm of number of employees), age (natural logarithm of number of years since the creation of the firm), leverage (long-term plus short-term debt divided by the book value of equity), the firm’s risk in terms of the Altman (Citation1968) Z-Score, and investment (capital expenditure divided by plant property and equipment). These control variables were considered in accordance with previous research on family business performance (Andres, Citation2008; Miller et al., Citation2007; Citation2011; Poutziouris et al., Citation2015).

and show the descriptive statistics and correlation matrix, respectively. The data show a significant correlation between age, size and family complexity. As time passes, firm and family complexity grows. In any other case, when there is an imbalance between firm and family complexity (‘too much family for so little company’), firm survival is probably at risk. Similarly, the family regulatory framework and the family governance structure have a high correlation, suggesting the complementarity of these two elements.

Table 2. Descriptive statistics.

Table 3. Correlation matrix and variance inflation factors.

A multicollinearity test was performed using the variance inflation factor (VIF). Low VIF values in suggest no collinearity between the variables. The multivariate analysis provides a more robust explanation of these correlations.

4. Method and results

To test the hypotheses, we used random effects generalised least squares (GLS) panel regression based on the following model:

In this model, FVit is the vector that includes the first, second and third order moderations of the independent variables. The vector CONit represents the control variables. The vector SECit represents the sector control variable. The term YEARit denotes the year dummies. Finally, µi captures the individual random effect.

Given the stability of the family firm variables, random effects GLS is an appropriate approach (Andres, Citation2008; Miller et al., Citation2011). We used robust Huber-White standard errors to account for unobserved firm fixed effects and firm-specific autocorrelation (Miller et al., Citation2011).

4.1. Empirical results

shows the results of the random effects GLS panel regression for the dependent variable (ROA). As shown by the results for Model II, neither family complexity nor family governance structure has a direct and significant impact on firm performance (ROA). Thus, Hypotheses 1 and 4 are not supported. For Hypothesis 4, the results are in line with those reported by De Massis et al. (Citation2015).

Table 4. Estimation results of the random effects GLS panel regression for the dependent variable (ROA).

Model II shows that a well-developed family regulatory framework has a positive and significant impact on firm performance (ROA). Thus, Hypothesis 2 is supported.

Model III shows that managing an increasing level of family complexity through a complex set of family rules (i.e. the family regulatory framework) has a negative and significant impact on firm performance. However, when family complexity is non-existent or low, a more complex set of family rules (i.e. the family regulatory framework) has a positive and significant impact on ROA, in line with Hypothesis 2. These results lead to the rejection of Hypothesis 3. The results reveal a significant relationship but with the opposite sign to that proposed by this hypothesis.

Likewise, Model V shows that an increasing level of family complexity, along with more complex family governance structures, has a negative but non-significant effect on firm performance. Thus, Hypothesis 5 receives no support.

Model IV also shows that an increasing number of rules that regulate the family-firm relationship, along with more developed and intensive use of family governance structures, has a negative and significant relationship with firm performance. Therefore, Hypothesis 6 is rejected.

Finally, Model VI shows that, when the family business has increasing levels of family complexity, an adequate combination of family governance structures and rules that regulate the family-firm relationship (i.e. the family regulatory framework) has a positive and significant impact on firm performance (ROA). Thus, Hypothesis 7 is supported.

Similarly, Model VI shows that a complete set of family rules (i.e. the family regulatory framework), together with a fully developed family governance structure, has a negative and significant impact on ROA when family complexity is low. This situation is a typical case of over-fit. Therefore, the results for Model VI reinforce the findings of Gimeno-Sandig et al. (Citation2010) regarding the need for fit between family complexity and the family governance system and the negative consequences of any misfit, be it under-fit or over-fit.

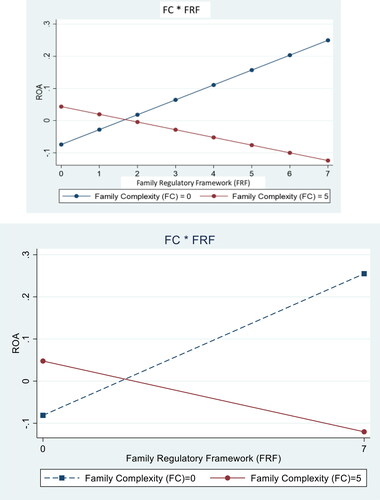

The analysis of the coefficients in regarding the interaction effects requires the interpretation of the related plots (Cohen et al., Citation2003; Miller et al., Citation2013). The first plot shows the interaction between family complexity and the family regulatory framework (see ).

Figure 2. Plots of significant interaction effects between family complexity and family regulatory framework. Source: own research

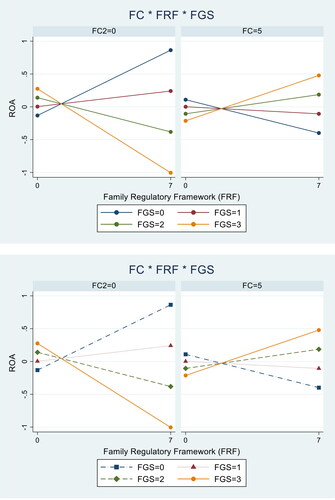

The second plot shows the interaction between family complexity, the family regulatory framework and the family governance structure (see and ).

Figure 3. Plots of significant interaction effects: interaction of family complexity, family regulatory framework and family governance structures. Source: own research.

As the first plot shows, when family complexity is low, a complete set of family rules (i.e. the family regulatory framework) has a positive impact on ROA. Because uncertainty about the adherence to, or at least acceptance of, basic family principles is low or non-existent, rules offer the right structural device to deal with a set of foreseen family issues. On the contrary, when family complexity is high, an increasing number of rules (i.e. the family regulatory framework) to manage family-firm relationships is not enough ().

The second plot (see and ) shows that when family complexity is high, a family regulatory framework without the right family governance structure has a negative effect on firm performance. Because family complexity is high, basic principles cannot be taken for granted. Therefore, a family governance structure is necessary to communicate and discuss the letter and the spirit of the family laws, interpreting and updating the family regulatory framework to adapt to new family realities. Similarly, high family complexity requires an increasingly high degree of institutionalisation in the form of a set of rules that regulate the operation of such family governance mechanisms. Without this complementarity between the family regulatory framework and the family governance structure, families cannot manage high family complexity. Similarly, when family complexity is low, an excess of institutionalisation (i.e. over-fit) in family governance structures has negative consequences. Thus, the results show that any kind of misfit – be it over-fit or under-fit – is detrimental to firm performance.

4.2. Robustness of results

To check the robustness of our results, we performed several tests. First, we used EBITDA (earnings before interest, taxes, depreciation and amortisation) divided by total assets as an alternative dependent variable (Bouzgarrou & Navatte, Citation2013). The results in confirm our previous findings.

Table 5. Estimation results of the random effects GLS panel regression for the dependent variable (EBITDA).

Second, to control for industry trends, we used a new dependent variable, which was calculated as ROA minus the annual mean industry ROA (Amore et al., Citation2014). shows similar results to those reported previously.

Table 6. Estimation results of the random effects GLS panel regression for the dependent variable (ROA - mean industry ROA).

Finally, to test whether our results might be biased by endogeneity in the family governance variables, we ran instrumental variable regressions (Andres, Citation2008, Bouzgarrou & Navatte, Citation2013). As instruments, we used variables that have commonly been used in the related literature (Bouzgarrou & Navatte, Citation2013, Miller et al., Citation2007; Miller et al., Citation2013; Pindado et al., Citation2011; Schmid, Citation2013; Villalonga & Amit, Citation2006). Specifically, we used sales growth (current sales less sales from the previous year, divided by sales from the previous year), cash holdings (cash holdings divided by total assets), and the average age of directors and outside blockholders (ownership percentage of all major non-family members with a holding of more than 5%). Hansen’s test for overidentifying restrictions confirmed the validity of our instruments. The results in are similar to those in .

Table 7. Estimation results.

In line with the related literature (Anderson & Reeb, Citation2003, Andres, Citation2008), the results of the instrumental variables method in confirm our main findings when controlling for the potential endogeneity of family governance variables.

5. Discussion and conclusions

The effect of family complexity on family firm performance has been the target of study for the last decade. However, scant research has considered the direct impact of rules that govern family-firm relationships and family governance structures on family firm performance.

To fill this gap, the present study examined the impact of the family governance framework and the family governance structure on performance. The study also examined the complementarity between family rules and family institutions. This research draws upon the concept of fit from organisation design and builds on the model of fit proposed by Gimeno-Sandig et al. (Citation2006, Citation2010). The analysis sheds light on the consequences of fit and misfit – be it under-fit or over-fit – between family governance and family complexity.

The results show that the relationship of family rules and institutions (i.e. the family regulatory framework and the family governance structure) with family firm performance (ROA) is contingent on family complexity. In other words, the level of structural complexity of the regulatory framework and the institutions that govern the family should fit the level of complexity of the owner family. Any misfit will lead to a non-significant effect or, worse, a negative impact on firm performance (ROA).

When family complexity is low, a complete set of rules and agreements that regulate the relationship between the family and the firm (i.e. the family regulatory framework) seems to be an adequate way of managing the preferences and aspirations of the family group to improve firm performance (ROA). However, when the level of family complexity is high, a complex set of rules (i.e. a complex family regulatory framework) is not enough and may even be counterproductive. High family complexity requires a well-developed regulatory framework supported by the right family governance structure. These results show the complementary role and systemic interdependence of family rules and family institutions. The family regulatory framework provides obsolete laws without the family governance structure, whilst this structure causes complete confusion without the right regulations.

Finally, this research shows that both under- and over-fit are detrimental to family firm performance. These results bring to the fore the need for family business research to provide a better understanding of the range and diversity of family firms and to show that family firms require suitable management and governance set-ups. New research is also needed to identify the most suitable point in the family firm life cycle at which to develop and deploy the family regulatory framework and family governance structure. For this reason, consultancy and case-based research offer a good starting point to support additional research.

This study is not without limitations. First, it focuses on a single industry and country, so further research should seek to confirm the universal validity of our results. Second, although the sample was large enough in statistical terms, its size was still limited. Therefore, additional research with larger samples is required. Third, the operationalisation of variables using indices creates an opportunity for future research to look for methodological triangulation with new, alternative and more accurate indices. Finally, dynamic studies based on panel data are also recommended.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

References

- Alderson, K. (2015). Conflict management and resolution in family-owned businesses: A practitioner focused review. Journal of Family Business Management, 5(2), 140–156. https://doi.org/https://doi.org/10.1108/JFBM-08-2015-0030

- Altman, E. (1968). Financial ratios, discriminant analysis, and the prediction of corporate bankruptcy. The Journal of Finance, 23(4), 589–609. https://doi.org/https://doi.org/10.1111/j.1540-6261.1968.tb00843.x

- Amore, M. D., Garofalo, O., & Minichilli, A. (2014). Gender interactions within the family firm. Management Science, 60(5), 1083–1097. https://doi.org/https://doi.org/10.1287/mnsc.2013.1824

- Anderson, R. C., & Reeb, D. M. (2003). Founding-family ownership, corporate diversification, and firm leverage. Journal of Law & Economics, 46, 653–684.

- Andres, C. (2008). Large shareholders and firm performance. An empirical examination of founding-family ownership. Journal of Corporate Finance, 14(4), 431–445. https://doi.org/https://doi.org/10.1016/j.jcorpfin.2008.05.003

- Aronoff, C. E., & Ward, J. L. (2011). Family business values: How to assure a legacy of continuity and success. Palgrave Macmillan.

- Aronoff, C., & Ward, J. (2016). Family business governance: Maximizing family and business potential. Palgrave Macmillan.

- Arteaga, R., & Menéndez-Requejo, S. (2014). Influencia Del Protocolo Familiar En Los Resultados De Las Empresas Familiares (Family Protocol Influence on the Family Businesses Results). Available at SSRN 2518938.

- Arteaga, R., & Menéndez-Requejo, S. (2017). Family constitution and business performance: Moderating factors. Family Business Review, 30(4), 320–338. https://doi.org/https://doi.org/10.1177/0894486517732438

- Ben-Amar, W., Francoeur, C., Hafsi, T., & Labelle, R. (2013). What makes better boards? A closer look at diversity and ownership. British Journal of Management, 24(1), 85–101. https://doi.org/https://doi.org/10.1111/j.1467-8551.2011.00789.x

- Berent-Braun, M. M., & Uhlaner, L. M. (2012). Family governance practices and teambuilding: paradox of the enterprising family. Small Business Economics, 38(1), 103–119. https://doi.org/https://doi.org/10.1007/s11187-010-9269-4

- Bertrand, M., Johnson, S., Samphantharak, K., & Schoar, A. (2008). Mixing family with business: A study of Thai business groups and the families behind them. Journal of Financial Economics, 88(3), 466–498. https://doi.org/https://doi.org/10.1016/j.jfineco.2008.04.002

- Björnberg, Å., & Nicholson, N. (2012). Emotional ownership: The next generation’s relationship with the family firm. Family Business Review, 25(4), 374–390. https://doi.org/https://doi.org/10.1177/0894486511432471

- Black, B. S., Jang, H., & Kim, W. (2006). Does corporate governance predict firms’ market values? Evidence from Korea. Journal of Law, Economics, and Organization, 22(2), 366–413. https://doi.org/https://doi.org/10.1093/jleo/ewj018

- Bouzgarrou, H., & Navatte, P. (2013). Ownership structure and acquirers performance: Family vs. non-family firms. International Review of Financial Analysis, 27, 123–134. https://doi.org/https://doi.org/10.1016/j.irfa.2013.01.002

- Brenes, E. R., Madrigal, K., & Molina-Navarro, G. E. (2006). Family business structure and succession: Critical topics in Latin American experience. Journal of Business Research, 59(3), 372–374. https://doi.org/https://doi.org/10.1016/j.jbusres.2005.09.011

- Brenes, E. R., Madrigal, K., & Requena, B. (2011). Corporate governance and family business performance. Journal of Business Research, 64(3), 280–285. https://doi.org/https://doi.org/10.1016/j.jbusres.2009.11.013

- Breton-Miller, I. L., Miller, D., & Steier, L. P. (2004). Toward an integrative model of effective FOB succession. Entrepreneurship Theory and Practice, 28(4), 305–328. https://doi.org/https://doi.org/10.1111/j.1540-6520.2004.00047.x

- Burns, T., & Stalker, G. M. (1961). The Management of Innovation. Tavistock.

- Burton, R. M., Lauridsen, J., & Obel, B. (2002). Return on assets loss from situational and contingency misfits. Management Science, 48(11), 1461–1485. https://doi.org/https://doi.org/10.1287/mnsc.48.11.1461.262

- Burton, R. M., Lauridsen, J., & Obel, B. (2003). Erratum: Return on assets loss from situational and contingency misfits. Management Science, 49(8), 1119–1119. https://doi.org/https://doi.org/10.1287/mnsc.49.8.1119.16404

- Carney, M., Gedajlovic, E., & Strike, V. M. (2014). Dead money: Inheritance law and the longevity of family firms. Entrepreneurship Theory and Practice, 38(6), 1261–1283.

- Child, J. (1975). Managerial and organizational factors associated with company performance, part 2: A contingency analysis. Journal of Management Studies, 12(1-2), 12–27. https://doi.org/https://doi.org/10.1111/j.1467-6486.1975.tb00884.x

- Chirico, F., Sirmon, D. G., Sciascia, S., & Mazzola, P. (2011). Resource orchestration in family firms: Investigating how entrepreneurial orientation, generational involvement, and participative strategy affect performance. Strategic Entrepreneurship Journal, 5(4), 307–326. https://doi.org/https://doi.org/10.1002/sej.121

- Chittoor, R., & Das, R. (2007). Professionalization of management and succession performance-A vital linkage. Family Business Review, 20(1), 65–79. https://doi.org/https://doi.org/10.1111/j.1741-6248.2007.00084.x

- Cohen, J., Cohen, P., West, S. G., & Aiken, L. S. (2003). Applied Multiple Regression/Correlation Analysis for the Behavioral Sciences. Lawrence Erlbaum Associates, Inc.

- Craig, J. B., Dibrell, C., & Davis, P. S. (2008). Leveraging family-based brand identity to enhance firm competitiveness and performance in family businesses. Journal of Small Business Management, 46(3), 351–371. https://doi.org/https://doi.org/10.1111/j.1540-627X.2008.00248.x

- Cruz, C., Larraza-Kintana, M., Garcés-Galdeano, L., & Berrone, P. (2014). Are family firms really more socially responsible? Entrepreneurship Theory and Practice, 38(6), 1295–1316.

- De Massis, A., Kotlar, J., Campopiano, G., & Cassia, L. (2013). Dispersion of family ownership and the performance of small-to-medium size private family firms. Journal of Family Business Strategy, 4(3), 166–175. https://doi.org/https://doi.org/10.1016/j.jfbs.2013.05.001

- De Massis, A., Kotlar, J., Campopiano, G., & Cassia, L. (2015). The impact of family involvement on SMEs’ performance: Theory and evidence. Journal of Small Business Management, 53(4), 924–948. https://doi.org/https://doi.org/10.1111/jsbm.12093

- De Massis, A., Kotlar, J., Chua, J. H., & Chrisman, J. J. (2014). Ability and willingness as sufficiency conditions for family‐oriented particularistic behavior: implications for theory and empirical studies. Journal of Small Business Management, 52(2), 344–364. https://doi.org/https://doi.org/10.1111/jsbm.12102

- Dillman, D. A. (1978). 1978 Mail and Telephone Surveys: The Total Design Method. John Wiley.

- Dyer, W., Jr. (2006). Examining the “family effect” on firm performance. Family Business Review, 19(4), 253–273.

- Eckrich, C. J., & McClure, S. L. (2012). The Family Council Handbook: How to Create, Run, and Maintain a Successful Family Business Council. Palgrave Macmillan.

- Eddleston, K. A., & Kellermanns, F. W. (2007). Destructive and productive family relationships: A stewardship theory perspective. Journal of Business Venturing, 22(4), 545–565. https://doi.org/https://doi.org/10.1016/j.jbusvent.2006.06.004

- Egelhoff, W. G. (1991). Information-processing theory and the multinational enterprise. Journal of International Business Studies, 22(3), 341–368. https://doi.org/https://doi.org/10.1057/palgrave.jibs.8490306

- Francoeur, C., Labelle, R., & Sinclair-Desgagné, B. (2008). Gender diversity in corporate governance and top management. Journal of Business Ethics, 81(1), 83–95. https://doi.org/https://doi.org/10.1007/s10551-007-9482-5

- Galbraith, J. R. (1974). Organization design: An information processing view. Interfaces, 4(3), 28–36. https://doi.org/https://doi.org/10.1287/inte.4.3.28

- Gallo, M. A., & Kenyon-Rouvinez, D. (2005). The importance of family and business governance. In Family Business. (pp. 45–57). Palgrave Macmillan.

- Gersick, K. E., Davis, J. A., Hampton, M. M., & Lansberg, I. (1997). Generation to generation: Life cycles of the family business. Harvard Business Press.

- Gilding, M., Gregory, S., & Cosson, B. (2015). Motives and outcomes in family business succession planning. Entrepreneurship Theory and Practice, 39(2), 299–312. https://doi.org/https://doi.org/10.1111/etap.12040

- Gimeno-Sandig, A. G., Labadie, G. J., Saris, W., & Mayordomo, X. M. (2006). Internal factors of family business performance: An integrated theoretical model. In Handbook of research on family business (pp. 145–166).

- Gimeno-Sandig, A., Baulenas, G., & Coma-Cros, J. (2010). Family business models. In Family business models (pp. 57–77). Palgrave Macmillan.

- Gnan, L., & Montemerlo, D. (2006). Family-firm relationships in Italian SMEs: Ownership and governance issues in a double-fold theoretical perspective. In Handbook of research on family business (pp. 501–516).

- Gómez-Mejía, L. R., Haynes, K. T., Núñez-Nickel, M., Jacobson, K. J., & Moyano-Fuentes, J. (2007). Socioemotional wealth and business risks in family-controlled firms: Evidence from Spanish olive oil mills. Administrative Science Quarterly, 52(1), 106–137. https://doi.org/https://doi.org/10.2189/asqu.52.1.106

- Gompers, P., Ishii, J., & Metrick, A. (2003). Corporate governance and equity prices. The Quarterly Journal of Economics, 118(1), 107–155. https://doi.org/https://doi.org/10.1162/00335530360535162

- González-Cruz, T. F., & Cruz-Ros, S. (2016). When does family involvement produce superior performance in SME family business? Journal of Business Research, 69(4), 1452–1457. https://doi.org/https://doi.org/10.1016/j.jbusres.2015.10.124

- Hernández-Perlines, F., Ariza-Montes, A., & Araya-Castillo, L. (2020). Socioemotional wealth, entrepreneurial orientation and international performance of family firms. Economic Research-Ekonomska Istraživanja, 33(1), 3125–3145. https://doi.org/https://doi.org/10.1080/1331677X.2019.1685398

- Hoopes, D. G., & Miller, D. (2006). Owner preferences, competitive heterogeneity and strategic capabilities. Family Business Review, 19(2), 89–101. https://doi.org/https://doi.org/10.1111/j.1741-6248.2006.00064.x

- Jaskiewicz, P., & Dyer, W. G. (2017). Addressing the elephant in the room: Disentangling family heterogeneity to advance family business research. Family Business Review, 30(2), 111–118. https://doi.org/https://doi.org/10.1177/0894486517700469

- Jaskiewicz, P., Block, J. H., Miller, D., & Combs, J. G. (2017). Founder versus family owners’ impact on pay dispersion among non-CEO top managers: Implications for firm performance. Journal of Management, 43(5), 1524–1552. https://doi.org/https://doi.org/10.1177/0149206314558487

- Keller, R. T. (1994). Technology-information processing fit and the performance of R&D project groups: A test of contingency theory. Academy of Management Journal, 37(1), 167–179.

- Kidwell, R. E., Eddleston, K. A., & Kellermanns, F. W. (2018). Learning bad habits across generations: How negative imprints affect human resource management in the family firm. Human Resource Management Review, 28(1), 5–17. https://doi.org/https://doi.org/10.1016/j.hrmr.2017.05.002

- Klaas, P., & Donaldson, L. (2009). Underfits versus overfits in the contingency theory of organizational design: Asymmetric effects of misfits on performance. In A. Bøllingtoft, D. D. Håkonsson, J. F. Nielsen, C. C. Snow, & J. Ulhoi (Eds.), New Approaches to Organization Design. (pp. 147–168). Springer.

- Klaas, P., Lauridsen, J., & Håkonsson, D. D. (2006). New developments in contingency fit theory. In R. M. Burton, B. Eriksen, D. D. Håkonsson, & C. C. Snow (Eds.), Organizational design: The evolving state-of-the-art (pp. 143–164). Springer.

- Kotlar, J., & De Massis, A. (2013). Goal setting in family firms: Goal diversity, social interactions, and collective commitment to family–centered goals. Entrepreneurship Theory and Practice, 37(6), 1263–1288. https://doi.org/https://doi.org/10.1111/etap.12065

- Labaki, R. (2011). The Nova Group case study: family dynamics in a multigenerational French family business. International Journal of Management Cases, 13(1), 27–42. https://doi.org/https://doi.org/10.5848/APBJ.2011.00020

- Lambrecht, J., & Lievens, J. (2008). Pruning the family tree: An unexplored path to family business continuity and family harmony. Family Business Review, 21(4), 295–313. https://doi.org/https://doi.org/10.1177/08944865080210040103

- Lansberg, I. (1999). Succeeding generations: Realizing the dream of families in business. Harvard Business Review Press.

- Lawrence, P. R., & Lorsch, J. W. (1967). Differentiation and integration in complex organizations. Administrative Science Quarterly, 12(1), 1–47. https://doi.org/https://doi.org/10.2307/2391211

- Li, Z., & Daspit, J. J. (2016). Understanding family firm innovation heterogeneity: A typology of family governance and socioemotional wealth intentions. Journal of Family Business Management, 6(2), 103–121. https://doi.org/https://doi.org/10.1108/JFBM-02-2015-0010

- Luo, B. N., & Donaldsen, L. (2013). Misfits in organization design: information processing as a compensatory mechanism. Journal of Organization Design, 2(1), 2–10. https://doi.org/https://doi.org/10.7146/jod.7359

- Madison, K., Holt, D. T., Kellermanns, F. W., & Ranft, A. L. (2016). Viewing family firm behavior and governance through the lens of agency and stewardship theories. Family Business Review, 29(1), 65–93. https://doi.org/https://doi.org/10.1177/0894486515594292

- Mazzola, P., Sciascia, S., & Kellermanns, F. W. (2013). Non-linear effects of family sources of power on performance. Journal of Business Research, 66(4), 568–574. https://doi.org/https://doi.org/10.1016/j.jbusres.2012.01.005

- Miller, D., Le Breton-Miller, I. L., & Lester, R. H. (2013). Family firm governance, strategic conformity, and performance: Institutional vs. strategic perspectives. Organization Science, 24(1), 189–209. https://doi.org/https://doi.org/10.1287/orsc.1110.0728

- Miller, D., Le Breton-Miller, I., & Lester, R. (2011). Family and Lone Founder Ownership and Strategic Behaviour: Social Context, Identity, and Institutional Logics. Journal of Management Studies, 48(1), 1–25. https://doi.org/https://doi.org/10.1111/j.1467-6486.2009.00896.x

- Miller, D., Le Breton-Miller, I., Lester, R., & Cannella, A. (2007). Are family firms really superior performers? Journal of Corporate Finance, 13(5), 829–858. [Database] https://doi.org/https://doi.org/10.1016/j.jcorpfin.2007.03.004

- Miller, D., Le Breton-Miller, I., Amore, M. D., Minichilli, A., & Corbetta, G. (2017). Institutional logics, family firm governance and performance. Journal of Business Venturing, 32(6), 674–693. https://doi.org/https://doi.org/10.1016/j.jbusvent.2017.08.001

- Miller, D., Minichilli, A., & Corbetta, G. (2013). Is family leadership always beneficial? Strategic Management Journal, 34(5), 553–571. https://doi.org/https://doi.org/10.1002/smj.2024

- Minichilli, A., Corbetta, G., & MacMillan, I. C. (2010). Top management teams in family-controlled companies: ‘familiness’, ‘faultlines’, and their impact on financial performance. Journal of Management Studies, 47(2), 205–222. https://doi.org/https://doi.org/10.1111/j.1467-6486.2009.00888.x

- Molly, V., Laveren, E., & Deloof, M. (2010). Family business succession and its impact on financial structure and performance. Family Business Review, 23(2), 131–147. https://doi.org/https://doi.org/10.1177/089448651002300203

- Montemerlo, D. (2005). Family ownership: Boost or obstacle to growth. In FBN-IFERA World Academic Research Forum. EHSAL.

- Mühlebach, C. (2005). Familyness as a Competitive Advantage. Haupt Berne.

- Naldi, L., Chirico, F., Kellermanns, F. W., & Campopiano, G. (2015). All in the family? An exploratory study of family member advisors and firm performance. Family Business Review, 28(3), 227–242. https://doi.org/https://doi.org/10.1177/0894486515581951

- Naman, J. L., & Slevin, D. P. (1993). Entrepreneurship and the concept of fit: A model and empirical tests. Strategic Management Journal, 14(2), 137–153. https://doi.org/https://doi.org/10.1002/smj.4250140205

- Neubauer, F., & Lank, A. G. (2016). The family business: Its governance for sustainability. Springer.

- Nordqvist, M., & Melin, L. (2010). The promise of the strategy as practice perspective for family business strategy research. Journal of Family Business Strategy, 1(1), 15–25. https://doi.org/https://doi.org/10.1016/j.jfbs.2009.12.001

- Pindado, J., Requejo, J., & de la Torre, C. (2011). Family control and investment-cash flow sensitivity: empirical evidence from the Euro zone. Journal of Corporate Finance, 17(5), 1389–1409. https://doi.org/https://doi.org/10.1016/j.jcorpfin.2011.07.003

- Poutziouris, Savva, C., & Hadjielias, E. (2015). Family involvement and firm performance: Evidence from UK listed firms. Journal of Family Business Strategy, 6(1), 14–32. https://doi.org/https://doi.org/10.1016/j.jfbs.2014.12.001

- Poza, E. J. (2013). Family business. Cengage Learning.

- Reay, T., Jaskiewicz, P., & Hinings, C. R. (2015). How family, business, and community logics shape family firm behavior and “rules of the game” in an organizational field. Family Business Review, 28(4), 292–311. https://doi.org/https://doi.org/10.1177/0894486515577513

- Rivo-López, E., Villanueva-Villar, M., Vaquero-García, A., & Lago-Peñas, S. (2017). Family offices: What, why and what for. Organizational Dynamics, 66(4), 262–270.

- Schmid, T. (2013). Control considerations, creditor monitoring, and the capital structure of family firms. Journal of Banking & Finance, 37(2), 257–272.

- Sirmon, D. G., Arregle, J. L., Hitt, M. A., & Webb, J. W. (2008). The role of family influence in firms’ strategic responses to threat of imitation. Entrepreneurship Theory and Practice, 32(6), 979–998. https://doi.org/https://doi.org/10.1111/j.1540-6520.2008.00267.x

- Suess, J. (2014). Family governance–Literature review and the development of a conceptual model. Journal of Family Business Strategy, 5(2), 138–155. https://doi.org/https://doi.org/10.1016/j.jfbs.2014.02.001

- Suess-Reyes, J. (2017). Understanding the transgenerational orientation of family businesses: the role of family governance and business family identity. Journal of Business Economics, 87(6), 749–777. https://doi.org/https://doi.org/10.1007/s11573-016-0835-3

- Sundaramurthy, C. (2008). Sustaining trust within family businesses. Family Business Review, 21(1), 89–102. https://doi.org/https://doi.org/10.1111/j.1741-6248.2007.00110.x

- Tait, A. A. (2019). Is My Family Constitution Unconstitutional?. Law & Inequality. (Sua Sponte, online publication)., Spring.

- Tàpies, J., & Fernandez-Moya, M. (2012). Values and longevity in family business: evidence from a cross-cultural analysis. Journal of Family Business Management, 2(2), 130–146. https://doi.org/https://doi.org/10.1108/20436231211261871

- Tushman, M. L., & Nadler, D. A. (1978). Information processing as an integrating concept in organizational design. Academy of Management Review, 3(3), 613–624.

- Umans, I., Lybaert, N., Steijvers, T., & Voordeckers, W. (2020). Succession planning in family firms: family governance practices, board of directors, and emotions. Small Business Economics, 54(1), 189–207. https://doi.org/https://doi.org/10.1007/s11187-018-0078-5

- Berghe, L. A. A., & Carchon, S. (2003). Agency relations within the family business system: An exploratory approach. Corporate Governance, 11(3), 171–179. https://doi.org/https://doi.org/10.1111/1467-8683.00316

- Vandekerkhof, P., Steijvers, T., Hendriks, W., & Voordeckers, W. (2018). Socio-emotional wealth separation and decision-making quality in family firm TMTs: The moderating role of psychological safety. Journal of Management Studies, 55(4), 648–676. https://doi.org/https://doi.org/10.1111/joms.12277

- Vardaman, J. M., & Gondo, M. B. (2014). Socioemotional wealth conflict in family firms. Entrepreneurship Theory and Practice, 38(6), 1317–1322.

- Vilaseca, A. (2002). The shareholder role in the family business: Conflict of interests and objectives between nonemployed shareholders and top management team. Family Business Review, 15(4), 299–320. https://doi.org/https://doi.org/10.1111/j.1741-6248.2002.00299.x

- Villalonga, B., & Amit, R. (2006). How do family ownership, control and management affect firm value? Journal of Financial Economics, 80(2), 385–417. https://doi.org/https://doi.org/10.1016/j.jfineco.2004.12.005

- Villalonga, B., Amit, R., Trujillo, M. A., & Guzmán, A. (2015). Governance of family firms. Annual Review of Financial Economics, 7(1), 635–654. https://doi.org/https://doi.org/10.1146/annurev-financial-110613-034357

- Wiklund, J., Nordqvist, M., Hellerstedt, K., & Bird, M. (2013). Internal versus external ownership transition in family firms: An embeddedness perspective. Entrepreneurship Theory and Practice, 37(6), 1319–1340. https://doi.org/https://doi.org/10.1111/etap.12068

- Zellweger, T., & Kammerlander, N. (2015). Article Commentary: Family, Wealth, and Governance: An Agency Account. Entrepreneurship Theory and Practice, 39(6), 1281–1303. https://doi.org/https://doi.org/10.1111/etap.12182