?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This paper analyses the impact of corporate board structure on default risk of European banking firms. We focus on four core aspects of boards that have been addressed in Directive 2013/36/EU to strengthen the corporate governance of banks: the size of boards, their independence, the participation of female directors and CEO duality. We employ panel data analysis to study the 109 European listed banks between 2002 and 2019. Default risk is estimated by Merton’s (Citation1974) distance to default. We take into account the presence of unobservable heterogeneity, simultaneity and dynamic endogeneity and estimate the model using the dynamic difference and dynamic system GMM methodologies. The results show that the size of the board influences banks’ default risk. Furthermore, bank size, firm profitability and GDP also exert a considerable influence.

1. Introduction

Firms’ risk-taking policies ultimately depend on the corporate board. For this reason, studies on the relationship between corporate governance mechanisms and default risk have multiplied in recent years (Habib et al., Citation2020; Liang et al., Citation2016). Although the number of academic studies on the relationship between corporate governance mechanisms and default risk in non-financial companies is large, financial companies have often been excluded from the analysis. Moreover, the conclusions reached have not been conclusive nor identical for both types of company, so this is an open question.

Financial firms have special features and are subject to a strong regulatory framework, which may mean that the mechanisms of internal corporate governance are conditioned by this external regulation (Andries & Brown, Citation2017) and may give rise to different relationships than those obtained for non-financial companies. All this, together with the impact that financial firms’ failure may have on the whole financial system, has increased the need to deepen the relationship between the internal corporate governance mechanisms of financial companies and risk taking.

The 2007–2008 crisis highlighted the lack of stability of the financial system at the global level. While the causes of the crisis were mainly of a macroeconomic nature (Erkens et al., Citation2012, among others; United Nations, Citation2010), at the global level, there was a collapse of financial institutions which led to failures and several provisional bailouts of the banking system. In Europe, banks in danger of bankruptcy were rescued, putting the stability of the financial system at risk. Moreover, banks, especially the largest ones, are supported by the system when they fail. they benefit from state guarantees, which can lead them to take excessive risks, with the consequent impact on financial stability (Anginer et al., Citation2018).

The boards of directors of financial firms, as those responsible for supervising business management as well as providing advice, have since been severely challenged. Some studies argue that part of the problems can be attributed to weaknesses in corporate governance structures that have a lack of oversight against risk-taking by financial institutions. Moreover, European regulators have focused on the risks assumed by the banking sector. The global financial crisis highlighted the need to improve and strengthen the regulation and supervision of the financial system. This is all in the interest of creating a strong financial system that guarantees financial stability and protects customers of financial services (Parenti, Citation2020). At European Union (EU) level, concern about this situation was expressed in Directive 2013/36/EU (European Commission, Citation2013)Footnote1, which establishes a series of recommendations related to the internal corporate governance of financial institutions, and in the creation of a Single Supervisory Mechanism (SSM) in 2014. Its main objectives are to guarantee the security and solidity of the European banking system and to increase financial integration and stability in Europe.

For these reasons, analysing the role that corporate board composition may have in preventing default risk or its possible responsibility for financial failure is a subject of maximum interest for the institutions themselves, as well as for policy makers, regulators and society in general. The aim of this paper is to analyse how certain characteristics of the board of directors affect the risk of default of financial firms in the EU during the period 2002 to 2019.

This paper, through empirical research, aims to contribute to an emerging literature examining the impact of corporate governance on banks’ risk-taking. In particular, we analyse the association that relates banks’ risks of default to characteristics of corporate governance in terms of size, independence, the duality of the Chief Executive Officer (CEO) and gender diversity. These board components have been identified by the previous literature, both at a theoretical and empirical level, as determinants of company credit risk (see Ballester et al. (Citation2020) and Fernandes et al. (Citation2018) for a full compilation of the scarce research on the relationship between board characteristics and bank failures). The default risk measure we employ is Merton’s (Citation1974) distance to default (DD) measure.

To address our goal, we need annual information regarding the characteristics of the board analysed, data on its financial statements and daily trading prices for the period 2002–2019. Therefore, the sample analysed was reduced to 109 European banks from 19 countries belonging to the EU (including the UK). In summary, we have an unbalanced panel of 980 company-year observations. Finally, we address endogeneity concern using the dynamic panel and generalised method of moments (GMM) methodology (Arellano & Bover, Citation1995; Blundell & Bond, Citation1998).

The relationship found between board size and distance to default suggests that the risk of bankruptcy is positively and significantly related to the size of the board of directors. This result is in line with the work of Switzer et al. (Citation2018), Felício et al. (Citation2018), John and Ogechukwu (Citation2018) and Baklouti et al. (Citation2016). All other board-related variables do not show a significant relationship to the risk of default.

This study makes important contributions to the literature. First, most studies usually focus on the United States; with this paper we aim to expand research on risk-taking of European financial firms by presenting a multi-country study of how corporate board features influence default risk. Second, the analysis of the participation of female directors on corporate boards completes a gap that has existed up to now in the study of the default risk of European firms. This is particularly relevant as the Directive 2013/36/EU recommends a balance between men and women in corporate governance bodies, and several EU countries have imposed mandatory quotas or recommended an increase in women’s participation in leadership positions. Third, as a measure of default risk we employ a continuous measure, Merton’s (Citation1974) distance to default, which, unlike discrete measures, allows for differences between companies.

The rest of the paper is structured as follows: Section 2 presents the literature review and hypotheses; Section 3 describes the sample and explains the method; we discuss the empirical results in Section 4; Section 5 concludes.

2. Literature review and hypotheses development

As a core element of internal corporate governance, the board performs two basic functions: the monitoring and advising of managers; and the influencing of agency costs and responsibility for reporting high-quality accounting information reducing information asymmetries. Through its functions, the board of directors supports decision-making processes, as well as other areas, such as risk taking or financial stability.

Although the number of corporate governance studies on the subject in non-financial companies is huge, financial firms have tended to be excluded from the analysis. Some traits differentiate the corporate governance of financial and non-financial firms. Stančić et al. (Citation2014) and Switzer et al. (Citation2018) point out an important difference between financial and non-financial companies, such as the nature of the financial business, which Morgan (Citation2002) defines as more complex, opaque, and subject to rapid changes. Furthermore, banks have a financial safety net that supports them when they are bankrupt, as demonstrated in the 2007–2008 crisis when different banks worldwide were bailed out (Anginer et al., Citation2018). Likewise, Andries and Brown (Citation2017) highlight that financial companies are subject to external governance mechanisms by states and regulators that can limit risk-taking even if internal governance mechanisms are weak. Felício et al. (Citation2018) highlights that in financial firms the agency problem is different from that in non-financial firms. Good corporate governance measures that align the objectives of shareholders and managers may not mean a reduction in risk-taking by financial firms, due to shareholders’ preference for risk. Also, Anginer et al. (Citation2018) provide evidence that shareholder-friendly boards are associated with greater risk for financial firms than non-financial firms.

For all these reasons, it is necessary to detect which structures of the corporate board can prevent or mitigate the default risk of financial firms by promoting a better development of the board’s functions and risk-taking behaviour.

We focus on the characteristics of the board of directors that can prevent or reduce the default risk of financial firms. Following previous literature, we consider four mechanisms related to board composition that measure board effectiveness or the ability of the board to perform its monitoring and advisory functions. These characteristics are the size of the board, the percentage of independent directors, CEO duality and the percentage of female directors.

2.1. Board size

There is no consensus on the impact of board size on firms’ financial distress, neither at the theoretical nor empirical level.

The agency theory has linked larger boards with higher agency costs, coordination and communication problems that lead to less efficient and slower decision making (Jensen, Citation1993). From this perspective, small boards are preferable. In this regard, some authors show that large boards of directors may be characterised by delay in the implementation of mechanisms to overcome critical financial situations (Goodstein et al., Citation1994). On the contrary, according to the resource dependence theory the board provides resources to the firm by bringing directors’ human capital and relational capital. Coles et al. (Citation2008) obtain that complex firms benefit from a larger board of directors and García and Herrero (Citation2018), among others, confirm this result empirically for European firms. From this point of view, large boards, which capture more capabilities, more diverse knowledge and greater volumes of information, are preferable and might be critical to avoid financial distress (Pfeffer, Citation1973).

Likewise, the empirical evidence on the effect of board size on default risk for financial firms is mixed. Switzer et al. (Citation2018), Felício et al. (Citation2018), John and Ogechukwu (Citation2018) and Baklouti et al. (Citation2016) find a positive effect; Andries and Brown (Citation2017) and Akwaa-Sekyi and Moreno (Citation2017) find no effect; while a negative effect is found by Lu and Boateng (Citation2018) and Fields et al. (Citation2012).

Following the above arguments and the recommendations of European authorities in relation to increasing the experience of board members through diversification rather than by board size, we expect that smaller boards improve risk-taking decisions. Thus, the following hypothesis is formulated:

H1: Board size is positively related to default risk in European financial firms.

2.2. Board independence

Independent directors fulfil the role of monitoring and advising executives. Independent directors are also related to an increase in the volume and quality of the information disclosed which leads to a reduction of informational asymmetries and mitigates agency costs (Kanagaretnam et al., Citation2007; Klein, Citation2002). Under this perspective there seems to be a consensus that a greater percentage of independent directors enhances the decision-making process and should lead to less risk-taking. Moreover, independent directors provide the firm with different skills and perspectives to solve financial distress. Fich and Slezak (Citation2008) obtain that boards with a higher proportion of independent directors are less likely to fail because they are more efficient at making adjustments to avoid bankruptcy.

Most of the empirical evidence shows a negative relationship between the percentage of independent directors in financial firms and credit risk (Fields et al., Citation2012; Switzer et al., Citation2018). However, other authors obtain a positive effect (Lu & Boateng, Citation2018) or even a null effect (Andries & Brown, Citation2017; Anginer et al., Citation2018; Simpson & Gleason, Citation1999). We formulate the following hypothesis:

H2: Board independence is negatively related to default risk in European financial firms.

2.3. CEO duality

CEO duality refers to the coincidence of the CEO and the chairperson of the board in the same individual. This accumulation of power in one person may lead to less board independence, making the supervision and monitoring of executive directors more complex (Jensen, Citation1993). Also, firms with CEO duality are exposed to greater information asymmetries (Gul & Leung, Citation2004). Nevertheless, a few studies have shown that this confluence of power in one person may result in stronger leadership and better strategic vision (Simpson & Gleason, Citation1999).

Most empirical evidence shows a positive effect of duality on the risk of default (Baklouti et al., Citation2016; Lu & Boateng, Citation2018; Switzer et al., Citation2018). Felício et al. (Citation2018) do not observe a significant effect.

Following the agency theory, we posit the following hypothesis:

H3: CEO duality size is positively related to default risk in European financial firms.

2.4. Gender diversity

In recent years, a growing body of studies has analysed the impact of the incorporation of women on the corporate board. Most of them have shown that greater gender diversity can enhance the monitoring process by reducing agency costs (Adams & Ferreira, Citation2009) and allowing greater transparency in financial and accounting information (Armstrong et al., Citation2014). In the context of risk-taking, some authors have argued that female directors are more risk-averse than men (Croson & Gneezy, Citation2009; Faccio et al., Citation2016) and less overconfident than men (Huang & Kisgen, Citation2013; La Rocca et al., Citation2019). Although the empirical evidence on this matter is scarce, Lu and Boateng (Citation2018) obtain a negative influence of gender diversity on credit risk.

From this perspective, female participation on the board should influence financial decisions by the firm and thus the likelihood of financial distress. Thus, we formulate the following hypothesis:

H4: Gender diversity is negatively related to default risk in European financial firms.

3. Sample selection and research methods

3.1. Sample and descriptive analysis

The objective of our study was to analyse whether the composition and characteristics of corporate directors (size of board, percentage of independents, percentage of women and CEO duality) affect financial firms’ default risk. We sourced the data for the study from the Thomson Reuters Eikon database for the period 2002 to 2019. We selected financial companies headquartered in an EU country (including the UK). We required annual data on the characteristics of the board of directors analysed. In addition, we required annual data on the companies’ financial statements and daily trading prices. The absence of data for any of the mentioned fields leaves us with an unbalanced panel data structure of 980 company-year observations corresponding to a sample of 109 European banks of 19 countries belonging to the EU during the period 2002–2019.Footnote2

The default risk measure we employ is Merton’s distance to default (DD) measure (Merton, Citation1974). This variable, unlike traditional risk approaches based on accounting data, is based on option pricing theory, and uses information on stock returns, leverage and volatility to measure the difference between the value of the firm’s assets and the nominal value of its default point. Merton's model compared to models based on accounting information can provide different advantages. For example, accounting data reflect a company's past situation, assets may not be correctly valued and, among other aspects, do not take into account the volatility of assets. Likewise, Hillegeist et al. (Citation2004) argue that the Merton model contains more information on the probability of bankruptcy than models based on accounting information.

The calculation of DD under the risk-neutral probability measure is:

(1)

(1)

and the probability of default (PD) is:

(2)

(2)

where

denotes the cumulative standard normal distribution, VA is the current value of the asset of the company, D is the face value of the debt (default point), r is the risk-free rate, σA is the annualized company value volatility and T is the length of the horizon (1 year). VA y σA are difficult to measure and can be calculated from the firm’s equity value (Et) and its volatility (σE).Footnote3

A higher value of DD implies a greater distance to default and therefore, lower default risk. Both measures, DD and PD, move in the opposite direction, the higher the distance to default, the lower the probability of insolvency.

Following the literature in corporate governance, we considered several control variables in the analysis (e.g. Andries & Brown, Citation2017; Felício et al., Citation2018, Lu & Boateng, Citation2018; Switzer et al., Citation2018). We included company attributes: firm size, firm’s profitability (ROA) and leverage. We also used some variables dummy for time: CRISIS and SSM_EURO and country GDP and PIIGS.

Larger banks may be associated with lower default risk because they are more likely to be diversified and allocate resources to search for information about their customers (Lu & Boateng, Citation2018). However, Felício et al. (Citation2018) point out that larger banks have a greater capacity to absorb and assume greater risks because of their ability to establish mechanisms that protect and confer security and also greater size allows greater diversification of assets implying a positive relationship between size and risk taking. Better performing firms are less likely to default, so it is expected a negative relationship between ROA and the likelihood of default (Ertugrul & Hedge, Citation2008). However, Lu and Boateng (Citation2018) indicate that a higher ROA may lead to higher risk-taking and consequently to higher credit risk. Lee and Yeh (Citation2004) showed a significant and direct relationship between the leverage ratio and the probability of financial distress. Also, Liang et al. (Citation2016) observed that solvency ratios are important features to predict bankruptcy.

GDP is an economic activity indicator based on the production developing. The GDP is naturally assumed to be negatively related to the likelihood of default, however, Felício et al. (Citation2018) obtain a positive relationship between economic development and risk, which is explained by the fact that the development is broadly associated with market sophistication and a greater capacity to take risks. Respect to the dummy variables PIIGS and CRISIS are expected to have a positive relationship with default risk. SSM_EURO is expected to have a negative relationship with default risk.

The variables used and their explanations are shown in .

Table 1. Variable definitions.

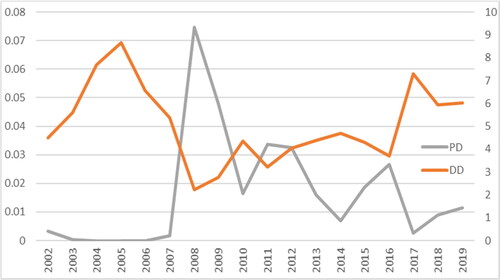

Before presenting the way in which we address the possible relationship between the possibility of bankruptcy and the characteristics of the board of directors, we present some relevant aspects of the sample. shows the time profile for the DD variable and the probability of default for the final sample. As can be seen in , both the subprime crisis in the USA (2008) and the EU sovereign debt crisis (2011) have an effect on the distance to default (probability of default) of financial institutions. As expected, a reduction (increase) in the distance to failure (probability of failure) is observed.

Figure 1. Time profile of distance to default (DD) and probability of default (PD).

Source: Authors

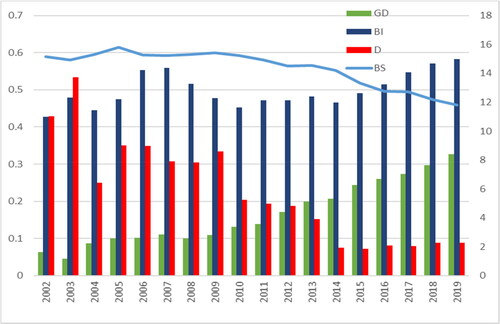

shows how the composition of boards of directors has evolved. One of the priorities of the SSM is the composition of the board of directors. In particular, the SSM advocates smaller and more independent boards, reflecting gender diversity and a non-executive chairmanship. As can be seen, these recommendations have had their impact, highlighting the evolution of gender diversity and the separation between the figure of the board Chairperson and the CEO.

Figure 2. Time profile of corporate board variables.

Source: Authors

presents the descriptive statistics for the sample banks grouped according to the country in which their headquarters is located and shows the correlation matrix and descriptive statistics for the full sample.

Table 2. Descriptive statistics of board variables by country.

Table 3. Descriptive statistics and matrix correlations of final sample.

As we can see in , the Eastern EU countries analysed – Hungary, Poland, Romania and the Czech Republic – show the highest values for the DD measure. For the rest of the countries in the sample (including the PIIGS), the value achieved for this measure is similar. This result is in line with that of Mirzaei et al. (Citation2013), although these authors use the Z-score as an indicator of stability.

Another aspect that we believe is worth highlighting is the result achieved for the gender diversity (GD) variable. In particular, Denmark, Finland and Sweden, countries without a mandatory quota, have the highest levels of women’s participation on boards.

Examining , the descriptive statistics for board characteristic variables revealed that the average board size was 13.98 members. Of these members, 20% were women and 51% were independent directors. In approximately 18% of cases, the CEO was the same as the board Chairperson. However, these results should be treated with caution since, as mentioned above, in recent years, regulations and recommendations on board composition in Europe have led to substantial changes in board composition.

The correlation analysis tested the relationships between all the variables in the analysis. According to Hair et al. (Citation2010), there is a multicollinearity problem when the independent variables show correlations higher than 0.8 or 0.9. In any case, the absolute values of the coefficients are lower than these values, indicating no multicollinearity problems in the regression analysis.

3.2. Research methods

Our main objective is to explore the association between corporate board characteristics and the distance to default. The general model is presented in Equationequation (3)(3)

(3) .

(3)

(3)

Studies have shown that corporate board characteristics are endogenous (e.g. Adams & Ferreira, Citation2009; Huang & Kisgen, Citation2013; La Rocca et al., 2020). Usually, this problem is ignored or corrected using fixed effects; we employed a more advanced method, namely dynamic panel data estimation using two-step system GMM with robust standard errors. This approach controls for the correlation of errors over time, heteroscedasticity across firms, simultaneity and measurement errors due to the use of orthogonal conditions on the variance-covariance matrix (Arellano & Bover, Citation1995; Blundell & Bond, Citation1998) to avoid significantly biased estimates.

However, we also present results obtained with other methodologies that do not explicitly correct for the endogeneity problem to facilitate the comparison of our results with those in the existing literature (Fich & Slezak, Citation2008; Lu & Boateng, Citation2018; Switzer et al., Citation2018). Thus, we estimate expression (3) assuming that all regressors are strictly exogenous (OLS); with fixed effects panel data methodology (FE), we consider unobserved heterogeneity at the firm level. Prior to the application of the GMM methodology, since it is plausible that past shocks to the probability of firm failure contain persistent characteristics over time, we incorporate in previous methodologies the lagged dependent variable to account for the presence of possible dynamic endogeneity. Finally, the presence of unobservable heterogeneity, simultaneity and dynamic endogeneity is considered jointly using the dynamic difference and dynamic system GMM methodologiesFootnote4 developed by Arellano and Bover (Citation1995) and Blundell and Bond (Citation1998).

4. Results and discussion

shows the results obtained by the different techniques used. We observe that, in general, the conclusions are maintained regardless of the estimation method used. Our comments will focus on GMM because we can keep in mind dynamic endogeneity, i.e. a persistent effect on the dependent variable over time, or heterogeneity, i.e. fixed effects (Roodman, Citation2009; Wintoki et al.,Citation2012). The exogeneity assumption is not fulfilled in OLS or FE and only the dynamic estimates of the GMM will produce consistent estimates, as they are robust in the presence of heterogeneity, simultaneity and dynamic endogeneity unobservable in the corporate governance-distance to default relationship.

Table 4. The corporate board and distance to default relation.

Regarding the existence of a significant relationship between board characteristics and financial distress in European banking systems, we find that the only board characteristic that is significantly related to the distance to default is board size. Moreover, this relationship is negative, indicating that if a financial firm has a large board, its distance to failure will be smaller and, therefore, its default risk higher. The use of different credit risk measures or the analysis of different time periods makes it difficult to compare results with previous studies. However, our result for board size is consistent with the findings of Switzer et al. (Citation2018), Felício et al. (Citation2018) or Altunbaş et al. (Citation2020) but differs from those of Lu and Boateng (Citation2018) and Fields et al. (Citation2012).

The rest of the variables related to board characteristics are not statistically significant, indicating that neither independence of the board, gender diversity nor CEO duality have any influence on the probability of bankruptcy of European banks.

In summary, for the sample analysed and the time period studied, our results only confirm hypothesis 1 and may help to understand why European authorities recommend reducing the size of the boards of directors of financial institutions.

Although it is not the main objective of the paper, we believe it is interesting to dedicate a few lines to comment on the results achieved for the variables considered as control variables.

Regarding the control variables, our regression results indicate that GDP variable has a positive and statistically significant effect with distance to default. The results are coincident with previous evidence, such as Felício et al. (Citation2018) among others. With respect to the firm-specific factors, we obtain that for banking firms, larger firms’ size and higher ROA are associated with higher distance to default. Finally, the variable CRISIS, which includes the two major financial crisis suffered in the period analysed, is associated with shorter distance to default and therefore with higher credit risk. The rest of the control variables are not significant.

5. Conclusions

The 2007–2008 financial crisis brought the debate on the corporate governance of European banks to the forefront. It highlighted the responsibility of corporate boards directly in decision-making and risk management and led to the implementation of a series of regulatory measures aimed at ensuring the stability of the financial system.

The results achieved indicate that there is an inverse relationship between bankruptcy distance and the size of the board of directors. Within an agency theory framework, this result suggests that small boards are more agile in making decisions and implementing measures to overcome default risk. However, neither the percentage of independent directors or women on the board nor CEO duality affects the number of acquisitions by a given default risk. The result regarding female representation on boards is especially relevant today, at a time when some countries are imposing mandatory board gender quotas.

The results also support previous evidence regarding credit risk in that larger and more profitable firms are subject to less credit risk. Furthermore, banks headquartered in countries with higher GDP are associated with less credit risk.

These results support the existence of a significant relationship between corporate governance arrangements and stress in the European banking system.

Our findings have several implications. First, they support efforts by policymakers to promote effective boards in terms of size. Second, although our evidence fails to support the notion of different behaviour across gender diverse boards, this should not prevent policies to encourage the hiring of women in leadership positions.

Given the value of our results and the recommendations of European authorities, we believe that this line of research should be extended to investigate in more detail how the diversity of knowledge and previous experience, either via independent directors or via integration of managers with diversity of gender, ethnicity, age, etc., can improve banking companies’ risk-taking decisions.

The study also has some limitations that could be addressed in future research. It might be interesting to analyse the changes that have taken place in boards to adapt to the European regulations after the crisis. Unfortunately, this implies having information on director (who enters and leaves the board, as well as their characteristics) that we do not have at the moment.

Future studies could also include more variables than our study did, in particular variables referring to the remuneration of directors and ownership structure. In addition, the results may lead researchers to analyse in depth the role of independent directors and the time devoted to the exercise of their duties.

Another interesting line of research is the analysis in depth of the presence of women on corporate boards due its scarce evidence in previous studies. There is a need for more studies on the effect on default risk of the female CEO and analysis of the differences between independent and non-independent female directors.

Likewise, due to the importance of the firm’s characteristics in the results, it would be useful to extend the sample to incorporate non-listed firms or to split the sample into family and non-family firms.

Disclosure statement

No potential conflict of interest was provided by the author(s).

Notes

1 This directive is amending Directive 2002/87/EC and repealing Directive 2006/48/EC and 2006/49/EC. Their main objective and subject-matter is to coordinate and to ensure a coherent application of national provisions concerning access to the activity of credit institutions and investment firms, the modalities for their governance, and their supervisory framework.

2 The beginning of the study period is conditioned by the availability of information on the composition of the corporate boards, which begins in 2002.

3 These values correspond to market capitalisation and standard deviation of return in that year.

4 When the correlations between the regressors and the firm fixed-effects are constant throughout the period analysed, the dynamic system GMM estimates produce more efficient estimates than dynamic difference GMM.

References

- Adams, R. B., & Ferreira, D. (2009). Women in the boardroom and their impact on governance and performance. Journal of Financial Economics, 94(2), 291–309. https://doi.org/10.1016/j.jfineco.2008.10.007

- Akwaa-Sekyi, E. K., & Moreno, J. (2017). Internal controls and credit risk relationship among banks in Europe. Intangible Capital, 13 (1), 25–50. https://doi.org/10.3926/ic.911

- Altunbaş, Y., Thornton, J., & Uymaz, Y. (2020). The effect of CEO power on bank risk: Do boards and institutional investors matter? Finance Research Letters, 33, 101202. https://doi.org/10.1016/j.frl.2019.05.020

- Andries, A. M., & Brown, M. (2017). Credit booms and busts in emerging markets: The role of bank governance and risk management. Economics of Transition, 25(3), 377–437. https://doi.org/10.1111/ecot.12127

- Anginer, D., Demirguc-Kunt, A., Huizinga, H., & Ma, K. (2018). Corporate governance of banks and financial stability. Journal of Financial Economics, 130(2), 327–346. https://doi.org/10.1016/j.jfineco.2018.06.011

- Arellano, M., & Bover, O. (1995). Another look at the instrumental variable estimation of error-components models. Journal of Econometrics, 68(1), 29–51. https://doi.org/10.1016/0304-4076(94)01642-D

- Armstrong, C. S., Core, J. E., & Guay, W. R. (2014). Do independent directors cause improvements in firm transparency? Journal of Financial Economics, 113(3), 383–403. https://doi.org/10.1016/j.jfineco.2014.05.009

- Baklouti, N., Gautier, F., & Affes, H. (2016). Corporate governance and financial distress of European commercial banks. Journal of Business Studies Quarterly, 7(3), 75. https://search.proquest.com/docview/1779192283?pq-origsite=gscholar&fromopenview=true

- Ballester, L., González-Urteaga, A., & Martínez, B. (2020). The role of internal corporate governance mechanisms on default risk: A systematic review for different institutional settings. Research in International Business and Finance, 54, 101293. https://doi.org/10.1016/j.ribaf.2020.101293

- Blundell, R., & Bond, S. (1998). Initial conditions and moment restrictions in dynamic panel data models. Journal of Econometrics, 87(1), 115–143. https://doi.org/10.1016/S0304-4076(98)00009-8

- Coles, J. L., Daniel, N. D., & Naveen, L. (2008). Boards: Does one size fit all? Journal of Financial Economics, 87(2), 329–356. https://doi.org/10.1016/j.jfineco.2006.08.008

- Croson, R., & Gneezy, U. (2009). Gender differences in preferences. Journal of Economic Literature, 47(2), 448–474. https://doi.org/10.1257/jel.47.2.448

- Erkens, D. H., Hung, M., & Matos, P. (2012). Corporate governance in the 2007–2008 financial crisis: Evidence from financial institutions worldwide. Journal of Corporate Finance, 18(2), 389–411. https://doi.org/10.1016/j.jcorpfin.2012.01.005

- Ertugrul, M., & Hegde, S. (2008). Board compensation practices and agency costs of debt. Journal of Corporate Finance, 14(5), 512–531. https://doi.org/10.1016/j.jcorpfin.2008.09.004

- European Commission, (2013). Directive 2013/36/EU of the European Parliament and of the Council of 26 June 2013 on access to the activity of credit institutions and the prudential supervision of credit institutions and investment firms. Official Journal of the European Union, 176, 338–436.

- Faccio, M., Marchica, M. T., & Mura, R. (2016). CEO gender, corporate risk-taking, and the efficiency of capital allocation. Journal of Corporate Finance, 39, 193–209. https://doi.org/10.1016/j.jcorpfin.2016.02.008

- Felício, J. A., Rodrigues, R., Grove, H., & Greiner, A. (2018). The influence of corporate governance on bank risk during a financial crisis. Economic research-Ekonomska Istraživanja, 31(1), 1078–1090. https://doi.org/10.1080/1331677X.2018.1436457

- Fernandes, C., Farinha, J., Martins, F. V., & Mateus, C. (2018). Bank governance and performance: A survey of the literature. Journal of Banking Regulation, 19(3), 236–256. https://doi.org/10.1057/s41261-017-0045-0

- Fich, E. M., & Slezak, S. L. (2008). Can corporate governance save distressed firms from bankruptcy? An empirical analysis. Review of Quantitative Finance and Accounting, 30(2), 225–251. https://doi.org/10.1007/s11156-007-0048-5

- Fields, L. P., Fraser, D. R., & Subrahmanyam, A. (2012). Board quality and the cost of debt capital: The case of bank loans. Journal of Banking & Finance, 36(5), 1536–1547. https://doi.org/10.1016/j.jbankfin.2011.12.016

- García, C., & Herrero, B. (2018). Boards of directors: composition and effects on the performance of the firm. Economic Research-Ekonomska Istraživanja, 31(1), 1015–1041. https://doi.org/10.1080/1331677X.2018.1436454

- Goodstein, J., Gautam, K., & Boeker, W. (1994). The effects of board size and diversity on strategic change. Strategic Management Journal, 15(3), 241–250. https://doi.org/10.1002/smj.4250150305

- Gul, F. A., & Leung, S. (2004). Board leadership, outside directors’ expertise and voluntary corporate disclosures. Journal of Accounting and Public Policy, 23(5), 351–379. https://doi.org/10.1016/j.jaccpubpol.2004.07.001

- Habib, A., Costa, M. D., Huang, H. J., Bhuiyan, M. B. U., & Sun, L. (2020). Determinants and consequences of financial distress: review of the empirical literature. Accounting & Finance, 60(S1), 1023–1075. https://doi.org/10.1111/acfi.12400

- Hair, J. F., Black, J. W., Babin, B. J., & Anderson, E. R. (2010). Multivariate data analysis. (7th ed.). Pearson Education Limited.

- Hillegeist, S. A., Keating, E. K., Cram, D. P., & Lundstedt, K. G. (2004). Assessing the probability of bankruptcy. Review of Accounting Studies, 9(1), 5–34. https://doi.org/10.1023/B:RAST.0000013627.90884.b7

- Huang, J., & Kisgen, D. J. (2013). Gender and corporate finance: Are male executives overconfident relative to female executives. ? Journal of Financial Economics, 108(3), 822–839. https://doi.org/10.1016/j.jfineco.2012.12.005

- Jensen, M. C. (1993). The modern industrial revolution, exit, and the failure of internal control systems. The Journal of Finance, 48(3), 831–880. https://doi.org/10.1111/j.1540-6261.1993.tb04022.x

- John, A. T., & Ogechukwu, O. L. (2018). Corporate governance and financial distress in the banking industry: Nigerian experience. Journal of Economics and Behavioral Studies, 10(1(J), 182–193. https://doi.org/10.22610/jebs.v10i1(J).2101

- Kanagaretnam, K., Lobo, G. J., & Whalen, D. J. (2007). Does good corporate governance reduce information asymmetry around quarterly earnings announcements? Journal of Accounting and Public Policy, 26(4), 497–522. https://doi.org/10.1016/j.jaccpubpol.2007.05.003

- Klein, A. (2002). Audit committee, board of director characteristics, and earnings management. Journal of Accounting and Economics, 33(3), 375–400. https://doi.org/10.1016/S0165-4101(02)00059-9

- La Rocca, M., Neha, N., & La Rocca, T. (2019). Female management, overconfidence and debt maturity: European evidence. Journal of Management and Governance, (24), 713–747. https://doi.org/10.1007/s10997-019-09479-9

- Lee, T. S., & Yeh, Y. H. (2004). Corporate governance and financial distress: Evidence from Taiwan. Corporate Governance: An International Review, 12(3), 378–388. https://doi.org/10.1111/j.1467-8683.2004.00379.x

- Liang, D., Lu, C. C., Tsai, C. F., & Shih, G. A. (2016). Financial ratios and corporate governance indicators in bankruptcy prediction: A comprehensive study. European Journal of Operational Research, 252(2), 561–572. https://doi.org/10.1016/j.ejor.2016.01.012

- Lu, J., & Boateng, A. (2018). Board composition, monitoring and credit risk: evidence from the UK banking industry. Review of Quantitative Finance and Accounting, 51(4), 1107–1128. https://doi.org/10.1007/s11156-017-0698-x

- Merton, R. C. (1974). On the pricing of corporate debt: The risk structure of interest rates. The Journal of Finance, 29(2), 449–470.

- Mirzaei, A., Moore, T., & Liu, G. (2013). Does market structure matter on banks’ profitability and stability? Emerging vs. advanced economies. Journal of Banking & Finance, 37(8), 2920–2937. https://doi.org/10.1016/j.jbankfin.2013.04.031

- Morgan, D. P. (2002). Rating banks: Risk and uncertainty in an opaque industry. American Economic Review, 92(4), 874–888. https://doi.org/10.1257/00028280260344506

- Parenti, R. (2020). https://www.europarl.europa.eu/ftu/pdf/en/FTU_2.6.14.pdf. European System of Financial Supervision (ESFS). Fact Sheets on the European Union: Economic and monetary union, taxation and competition policies. https://www.europarl.europa.eu/. On line [2021.03.10]

- Pfeffer, J. (1973). Size, composition, and function of hospital boards of directors: A study of organization-environment linkage. Administrative Science Quarterly, 18(3), 349–364. https://doi.org/10.2307/2391668

- Roodman, D. (2009). How to do xtabond2: An introduction to difference and system GMM in Stata. The Stata Journal, 9(1), 86–136. https://doi.org/10.1177/1536867X0900900106

- Simpson, W. G., & Gleason, A. E. (1999). Board structure, ownership, and financial distress in banking firms. International Review of Economics & Finance, 8(3), 281–292. https://doi.org/10.1016/S1059-0560(99)00026-X

- Stančić, P., Čupić, M., & Obradović, V. (2014). Influence of board and ownership structure on bank profitability: evidence from South East Europe. Economic Research-Ekonomska Istraživanja, 27(1), 573–589. https://doi.org/10.1080/1331677X.2014.970450

- Switzer, L. N., Tu, Q., & Wang, J. (2018). Corporate governance and default risk in financial firms over the post-financial crisis period: International evidence. Journal of International Financial Markets, Institutions and Money, 52, 196–210. https://doi.org/10.1016/j.intfin.2017.09.023

- United Nations (2010). Corporate governance in the wake of the financial crisis. Selected international views. United Nations.

- Wintoki, M. B., Linck, J. S., & Netter, J. M. (2012). Endogeneity and the dynamics of internal corporate governance. Journal of Financial Economics, 105(3), 581–606. https://doi.org/10.1016/j.jfineco.2012.03.005