?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The pandemic crisis, responsible for increased levels of financing with public debt and contingent liabilities, may trigger another debt crisis across the European Union. Our research indicates that member states are increasingly willing to use public guarantees and other off-budget instruments, which are classified as "hidden debt" or "hidden expenditure". Simulations have shown that if public guarantees have to be covered by the budget, an unprecedented increase in a public debt may occur across the euro area countries and the entire EU as a whole. Therefore, the authors recommend the introduction of uniform rules for estimating fiscal risk due to contingent liabilities, as well as standards for their reporting, allowing for their constant monitoring at the EU level.

1. Introduction

Contingent liabilities are defined as a possible obligation arising from past events, the outcome of which will be confirmed only on the occurrence or non-occurrence of one or more uncertain future events not wholly within the organization's control; or as a present obligation arising from past events, which is not recognized either because it is not probable that an outflow of resources will be required to settle an obligation, or the amount of the obligation cannot be reliably measured (IPSAS 2004; GAAP 2005). Based on the Eurostat (Citation2021), contingent liabilities are by nature only potential and not actual liabilities, so they are not included in public debt but “they are important for policy and analysis, and information on them needs to be collected and presented as supplementary data. Even though no payments may turn out to be due for contingent assets and contingent liabilities, a high level of contingencies may indicate an undesirable level of risk on the part of the units offering them'' (ESA 2010, paragraph 5.11). According to the breakdown used by Eurostat, contingent liabilities are divided into: government guarantees, liabilities related to public-private partnerships (PPPs) recorded off-government-balance-sheet and liabilities of government controlled entities (public corporations) classified outside the general government (Eurostat, Citation2021).

However, contemporary international organizations increasingly often emphasize the need for scenario modelling to increase decision makers’ awareness and understanding of the potential impact exerted by the materialization of contingent liabilities (most of them being represented by government guarantees) on public finances and economic fundamentals. A recent note published by IMF’s Fiscal Affairs Department (2020) warns that realizations of existing contingent liabilities can be large, thus each government needs to particularly assess and quantify the impact of servicing its explicit and implicit guarantees. It is argued that off-budget measures, such as contingent liabilities, trigger significant fiscal risks which are still insufficiently understood and measured. In a complementary fashion, the scenario-based assessment of the public debt sustainability in European Union countries carried out by the European Commission (2020) revealed the presence of contingent liabilities, notably related to government guarantees to the private sector, as a major source of vulnerability that may generate upward pressures to the debt-to-GDP ratio. OECD (Citation2020b) adds that assessment methods and stress scenarios should aim to analyze various fiscal risks, such as contingent liabilities, and their potential impact on public finances. A persistent bottleneck identified by the IMF (Citation2016, p. 21) is that contingent liabilities are included in countries’ fiscal risk statements, but “the analysis frequently lacks any quantification of the size or probability of realization”.

Against the background of the COVID-19 pandemic, this issue becomes of utmost importance due to large government fiscal support programmes implemented by many European countries, which also include a state guarantee component as a part of the COVID-19 response. Uncertainty related to the duration of the pandemic and the prospects for economic recovery, overlapping upward pressures on public debt are fuelling countries’ exposure to fiscal risks. OECD (Citation2020b, p.3) outlines the increased importance gained by the fiscal risk management during the COVID-19 pandemic, “as the understanding of past and new fiscal risks and mitigation of their potential impact on the economy and society will be crucial for increasing the resilience of public finances going forward”. Additionally, the last research on the COVID-19 crisis indicates that in the case of extreme revenue shocks, it can be also expected solvency to deteriorate and the probability of default of firms to increase significantly what will compromise the financial flexibility of corporates across Europe and put business continuity under lots of stress. Moreover the policy interventions will further strain the tightening economic conditions due to rising healthcare costs and unemployment (Mirza et al., Citation2020).

The outbreak of the pandemic has put to the forefront of decision makers’ concerns a specific type of fiscal risk, represented by the realization of contingent liabilities, as uncertain budgetary claims. There is not only the risk that new COVID-19 guarantees will be triggered; pre-existing guarantees may also be called due to the significant distress generated by the pandemic outbreak into all the economic sectors of activity.

Therefore, the paper’s aim is to build an empirical deterministic and semi-parametric framework for testing the resilience of public finances across European countries, in relation to a specific fiscal risk which is greatly exacerbated by the COVID-19 pandemic outbreak. The paper focuses exclusively on an individual category of fiscal risks, represented by contingent liabilities risks.

Our contribution to existing literature is novel and manifold. First, the paper fills a literature gap and in a comprehensive way assesses the potential impact to be exerted by contingent liabilities realization, in the context of COVID-19, on both public budget and economic fundamentals. Second, to achieve this goal, we use a mix of baseline scenarios, deterministic and semi-parametric methods to estimate the likelihood of contingent liabilities realization, the amounts realized (payouts) and their further impact on public budget and public debt.

Third, we consider detailed, comprehensive contingent liability structure, with particular emphasis on government guarantees as part of the COVID-19 response. This approach is seldom used in the existing literature, which usually addresses either the total amount of contingent liabilities or financial sector related contingent liability (Amaglobeli et al., Citation2015; Bresciani & Cossaro, Citation2016; Singh et al., Citation2019; Weber, Citation2012). Our choice is also substantiated by some recent international opinions which support the novelty and timeliness of our research. For instance, the IMF. (Citation2020) advocates considering both explicit and implicit contingent liabilities when evaluating the impact on state budget and the probability of realization, while the OECD (Citation2020b) adds that governments are also expected to act as insurers of last resort during the pandemic crisis, and hence both categories of contingent liabilities should require attention. Consequently, the paper aims to fill the gap identified by international authorities through the inclusion the empirical analysis of both implicit and explicit contingent liabilities. To our knowledge, only one paper (Bova et al., Citation2019) followed a similar granular approach, by applying the logit model and targeting advanced and emerging countries.

Fourth, to alleviate a major drawback related to data availability, we developed a new, comprehensive database of more than 100 contingent liability realizations in European countries for the period 1990–2019. The database combines information taken from Bova et al. (Citation2019) dataset with novel data, collected manually from the IMF country-specific Staff Reports, and Eurostat data on government interventions to support financial institutions.

The remaining part of the paper is structured as follows: the first part of the paper reviews the world literature presenting the most important studies on the role of contingent liabilities in generating fiscal risk, with particular emphasis on crisis situations. In the next part of the article, empirical research was conducted into the impact of contingent liabilities on the fiscal situation in the European Union countries, using simulation and scenario analyses and regression models. In the final part of the article, the most important conclusions and assessments in the context of the ongoing pandemic crisis were made.

2. Literature

In a pioneering study on public debt management, Tobin (Citation1963) distinguished five basic items comprising liabilities towards the federal government, i.e. transferable demand obligations, marketable short- and long-term securities, non-marketable government securities and other liabilities. Within the last category, the author identified liabilities which are difficult to calculate in terms of their volume and maturity, and which may impose a greater burden on the future budget than conventional public debt.

One of the first studies on the issue of the diverse approaches to estimating budget deficit and the implications of its interpretation was published in 1984 by Eisner (Citation1984). Apart from the oft-quoted, in a way correct, statement that "the budget deficit is like a sin. For most of the society it is morally wrong, very difficult to avoid, not always easy to identify and prone to change in estimation", this author then also presented a proposal for the construction of an annual budget on "contingency expenditures" and the corresponding revenues. He believed that this would be a useful exercise, providing a basis for measuring the impact of net contingency liabilities on the growth of the current budget deficit.

Intensive research on contingent liabilities began in the mid-1990s based on the experience of many countries from the so-called emerging markets, in which the resulting financial crises (currency or banking crises) were also contributed to by poorly conducted budgetary policies for generating potential liabilities, including, above all, a bad policy of providing guarantees (both in terms of subject and object). Kharas and Mishra (Citation2001), analysing the practical budgetary implications of contingent liabilities in the light of the experience of countries undergoing currency crises, introduce the definition of "hidden deficit". They draw attention to the necessity of switching from the cash principle of deficit calculation to the accrual method, additionally including the central bank and state-owned enterprises into the government sector. Studying the causes of currency crises in Asian countries, these authors have shown that the sudden increase in budget deficits was due to the need to finance potential liabilities and risks associated with the conventional debt portfolio of these countries (primarily exchange rate risk, affecting external debt).

Similar conclusions were also reached by Buiter (Citation1997), who deals with the issue of measuring the financial balance of the public sector. Postulating the necessity of taking into account in the budget deficit indicator, in terms of entities, the so-called broad government sector and the central bank, he also introduces the term "contingent deferred fiscal deficit" which is mainly generated by sovereign guarantees, usually granted by the government or the central bank to state-owned enterprises or commercial banks.

A dramatic increase in the conventional deficit caused by the need to finance previously publicly guaranteed debt was addressed by Blejer (Citation1991). According to this author, in contrast to the private sector, governments usually avoid making reserves related to the above liabilities. Thus, the costs of risk carried by potential debt are not spread over their "lifetime", but are accumulated when they have to be incurred. Blejer also drew attention to the problems of estimating contingent liabilities due to the related phenomenon of “moral hazard”, i.e. a change in private sector behaviour induced by the state's securing the solvency of financial liabilities.

The first solutions for estimating the value of state guarantees were proposed in the 1970s by R. Merton, who modified the original Black-Scholes formula for an option pricing model in relation to the value of state deposit insurance guarantees in the United States (Merton, Citation1977). Continuers in this area of potential liability research included Cooperstein et al. (1995).

The problem of moral hazard revealed in the activity of commercial banks in the case of state deposit guarantees was also emphasised by Easterly (Citation1999). Listing a number of adjustment factors causing the so-called "fiscal illusion", he also takes into account the issue of potential debt (especially the system of state guarantees and security of pension funds).

However, the most thorough and comprehensive analysis of the issue of potential liabilities and fiscal risk management was initiated by two researchers: Polackova Brixi and Schick.

In 1998, Hana Polackova proposed the first integrated classification of on-balance sheet and off-balance sheet liabilities of central government (the Fiscal Risk Matrix) and analysed the issue of factors that increase fiscal risk (especially for countries in the group of the so-called emerging markets). Among the most important of these she included (Polackova, 1998):

the change in the role assumed by the state - from financing and direct provision of services to guaranteeing them, so that the private sector could make certain revenues,

the adopted policy of generating off-budget liabilities, the incurrence of which increases risk but does not require immediate financing, especially in the context of the need to meet top-down imposed constraints such as the Maastricht fiscal criteria or IMF adjustment programmes,

potential liabilities are regarded as a "hedge" against various market failures (deficiencies); however, they generate the serious phenomenon of moral hazard in the market.

In turn, Schick was one of the first theorists to put forward proposals for fiscal risk management. In one of the first studies on the principles and sense of budgeting, the author points out that the principles of including potential liabilities in the budget of various countries will become standardised (Citation2003). Studying a group of a dozen or so countries, he concluded that audited financial statements are currently the most commonly used information document in this respect. However, this solution will evolve towards reporting instruments that specifically include an assessment of contingent debt servicing costs. Schick (Citation2004) was the first to propose standards of good practice for fiscal risk management in a detailed and comprehensive manner. On the basis of these proposals and analyses in various documents, the World Bank and the IMF (2002), the OECD (Citation2005), and the INTOSAI Public Debt Committee (2003) formulated guidelines for appropriate policies to manage risks and potential liabilities and recommendations on best practices for fiscal transparency. In the second part of the article, on the basis of the above guidelines, the authors will present recommendations addressed to public authorities concerning government contingent liabilities management in terms of reducing fiscal risk in EU countries.

Although the pandemic crisis will increase the fiscal burden on public budgets in most countries due to government interventions, there is currently little research focusing on the possible impact of government guarantees and more broadly contingent liabilities on the budgetary effects of COVID-19. These findings mainly relate to the overall assessment of the budgetary results of the fiscal respond to the pandemic crisis (Heald & Hodges, 2020). The preliminary analyzes are more widely available in the international studies issued mainly by the IMF, the OECD and the BIS (IMF, Citation2020, OECD, Citation2020a, Citation2020b, BIS 2020). The results of these studies indicate the growing demand for fiscal risk management.

3. Modelling the expected impact of contingent liabilities on fiscal indicators

This section aims at investigating the fiscal and economic impact of contingent liabilities in European countries, by focusing on key fiscal variables such as budget deficit and government debt. The empirical approach is three-fold. First, we perform a scenario analysis based on the recommendations made by the International Monetary Fund on the treatment of contingent liabilities. As the recommended realization rates are quite high, this initial analysis can be viewed as a worst-case, low frequency of occurrence scenario. Second, we conduct an empirical investigation based on the previously observed data related to the dynamics of contingent liabilities. Third, we complement this analytical framework with the Monte Carlo simulation that estimates the expected realizations (payouts) of contingent liabilities and their fiscal impact based on past observations. Methodological details, variables employed, as well as results obtained are presented in the following sections.

3.1. Scenario analysis

As mentioned above, scientists and international organizations commonly agree that public debt sustainability could weaken due to the realization of contingent liabilities. To uncover the extent to which the potential realization of contingent liabilities could worsen the public debt dynamics we follow a scenario approach similar with the one regularly conducted by the IMF in its country-level debt sustainability analyses. The most commonly considered contingent liability shock in IMF’s analyses is related to the realization of the overall government-guaranteed debt of about 40% of GDP (high fiscal risk). Our analysis considers this benchmark level, as well as other potential levels with various degrees of severity. It should also be added that international accounting standards (such as GAAP, IPSAS 19) recommend the inclusion of contingent liabilities to conventional debt when their risk of being covered by public funds increases to more than 50%. This study therefore adopts two additional thresholds: 20% of GDP as an acceptable level of risk (in EU practice, for most member states a level so far not yet exceeded) and 50% of GDP as a threshold which, if exceeded, may result in a fiscal crisis.

In order to account for the government guarantees provided as a response to the COVID-19 crisis, we rely on manually collected data from the Stability and Convergence Programmes and compute the total stock of government guarantees in 2020, by adding existing non-claimed guarantees with the newly issued COVID-19 ones. We further define three realization scenarios (), based on international best-practice thresholds, and compute the potential level to be recorded by debt-to-GDP ratio conditioned by the realization of a given percentage of the government guarantees accumulated since the outbreak of the pandemic. Specifically, we started from the nominal value of the total stock of government guarantees in 2020 (including the COVID-19 ones) and weighted it with the corresponding threshold. The resulting amount, representing the realization of government guarantees, is further cumulated with the government consolidated gross debt. Finally, this total debt expressed in million euros is divided by nominal GDP, to obtain the projected debt-to-GDP under each of the three scenarios.

Table 1. Projected debt-to-GDP (%) for various levels of CL realizations.

summarizes the final output of this computation, by indicating the potential debt-to-GDP value (for each of the three adverse scenarios) in comparison with the actual level reported by Eurostat, in the second quarter of 2020. Thus, the severity of the impact to be exerted on public finances may be comparatively assessed with the situation when no contingent liabilities realization occurs.

In the second quarter of 2020, i.e. at the beginning of the pandemic crisis, 15 EU countries (out of 28 surveyed) exceeded the maximum level of public debt allowed, i.e. 60% of GDP, with two countries (Greece and Italy) reaching a level twice as high. Thus, the results of the study indicate that after taking into account the risks associated with servicing contingent liabilities (including mainly government guarantees), the number of countries failing to meet the EU fiscal criterion would increase to 22 (first threshold) and 23 (second and third thresholds). In each of the analysed scenarios the situation would be dramatic for the two most indebted countries, whose public debt level would exceed 200% of GDP (in the case of Greece even as much as 270% of GDP). It should also be noted that the burden of contingent liabilities significantly increases the risk also for Belgium, Cyprus, France, Portugal, Spain and the UK. In turn, for countries that have not yet exceeded 60% of GDP in the second quarter of 2020, the fiscal risk associated with the budgetary financing of contingent liabilities may trigger an increase in public debt by up to 20-30% of GDP (Lithuania, Latvia, Malta, the Netherlands, Poland, and Romania).

It should therefore be stressed that the pandemic crisis may contribute to accelerating the onset of another debt crisis across the European Union. As studies conducted on the onset of the pandemic indicate, fiscal risk will continue to increase, requiring constant monitoring by governments not only in the area of government debt management, but also in that of contingent liability management. The lack of uniform management and reporting standards in the area of fiscal risk assessment for the entire European Union may cause difficulties in managing and controlling this fiscal area at the supranational level.

3.2. Dynamic regression models

One way to evaluate the economic influence of contingent liabilities is to directly model their impact on a selection of relevant economic variables. Following the recently revived literature on fiscal research (Ramey, Citation2019), we consider the Panel Structural Vector Autoregression (PSVAR) model (Abrigo & Love, Citation2016; Sigmund & Ferstl, 2021) that alongside contingent liabilities incorporates fiscal and macroeconomic variables, such as GDP, interest rates, inflation, government expenses (or budget deficits), and public debt. However, all attempts at estimating such a model–with different variables, lag lengths, and identification schemes–are unsuccessful, only resulting in models that do not meet the PSVAR stability conditions. We attribute this unsuccessful finding to the limited data sample, which only consists of yearly observations from 2010 to 2019. The root of the problem lies in the reporting standards for contingent liabilities, which are relatively limited and only require annual reports. Therefore, we decide to estimate limited-specification, straightforward Linear Dynamic Panel (LDP) models that allow the fitting of the impact exerted by lagged levels of contingent liabilities on specific variables of interest.

We consider eight alternative dependent variables, for which we estimate the following LDP model:

where

and

are indexes for countries and years, respectively,

is the dependent variable,

is the independent variable, which is always the level of contingent liabilities (proxied by government guarantees),

is a vector of country fixed effects, and

are idiosyncratic shocks. The dependent variables (

) are listed and described in . Because we have 28 countries and only 10 years of data, we are in a situation of small T, large N panel. Thus, we estimate coefficients

and

using the two-step difference GMM initially developed by Arellano and Bond (Citation1991). However, we improve on this by using the forward orthogonal deviations transformation (Arellano & Bover, Citation1995) to remove the dynamic panel bias and also implement small-sample corrections to the covariance matrix estimate, resulting in t-tests instead of z-tests, to evaluate the statistical significance for the coefficients. This GMM version first removes the fixed effects by transforming the data, i.e. by subtracting from all variables the average of all future available observations. Specifically, for every variable

in the equation, it replaces it with its transformed version

that is derived as:

where

are scale factors conveniently chosen to assure that

retains the statistical properties of

Second, it eliminates potential residual endogeneity by instrumenting the differenced variables

on the right-hand side with the second-order lags of the untransformed variable. Blundell and Bond (Citation1998) show that the difference GMM performs poorly for close to random walk variables because past levels convey little information about future changes. However, we still prefer this specification here to their system GMM because the latter complicates the model by additionally assuming that the moments are time-invariant, i.e.

for all

and

This may be questionable in our case and is certainly not necessary, given the characteristics of the (macroeconomic) variables that we investigate, which are obviously not close to random walks.

Table 2. List of variables.

The results of fitting the LDP models are reported in . Regarding econometric validity, all models meet the difference GMM model assumptions, with one exception. Specifically, the Sargan (Citation1958) and Hansen (Citation1982) test results imply that the instruments used in all models are valid, while the Arellano and Bond (Citation1991) tests show the absence of second-order serial correlation in disturbances for all models, except the one estimated for the real exchange rate. Moving on to economic inferences, we focus on the coefficient, which provides an estimate of how sensitive is, on average, each economic variable to the lagged level of contingent liabilities (in European countries). The results show that contingent liabilities do have a significant impact on macroeconomic conditions, and especially on fiscal-related variables. In particular, we find that an increase in contingent liabilities leads to higher levels of government debt in the following year. However, the results also show that contingent liabilities have a positive impact on a country’s fiscal position, as it reduces expenditures and the fiscal deficit of the general government. This seems to indicate that contingent liabilities are used by governments as hidden expenditures, substituting regular expenditures to avoid a direct, observable deterioration of the fiscal position. However, in the long run, contingent liabilities do increase a country’s overall debt and constitute a source of sovereign risk.

Table 3. Estimation results of LDP models.

3.3. Monte Carlo simulation

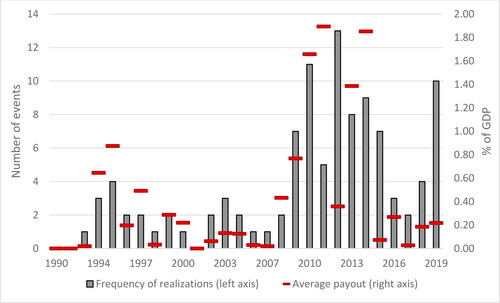

In this section, our goal is to perform the Monte Carlo simulation and estimate the empirical distribution of contingent liability realizations, commonly denoted as “payouts”, for each country in our sample. This, in turn, would provide an alternative way to estimate the expected fiscal impact of contingent liabilities. We implement a semi-parametric approach that relies on observed, historical realizations, which have been recently catalogued by Bova et al. (Citation2019) for 80 countries around the world in a time period ranging from 1990 to 2014. We use from their datasetFootnote1 the payouts recorded for the European economies in our sample (67 observations), but update the sample using more recent realizations that span the period until the end of 2019 (we add 41 observations).Footnote2 In total, we use 108 realizations of contingent liability, which have a mean payout of 3.548 percent of GDP. shows that both the frequency of realizations and the average payout significantly increased after 2009, in the aftermath of the financial crisis.

Figure 1. Payout frequency by year.

Source: own computation.

The simulation is performed with Matlab software and proceeds in two stages. In the first stage, we model contingent liability realizations as a collection of correlated Bernoulli random variables. The unconditional probability of a payout occurring for each country and the system covariance matrix are estimated from the panel of historical realizations spanning 30 years and 28 countries.Footnote3 From the resulting multivariate Bernoulli distribution we draw 1,000,000 sets of values representative of possible payout events.

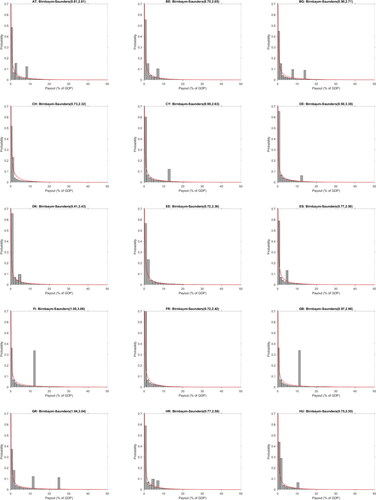

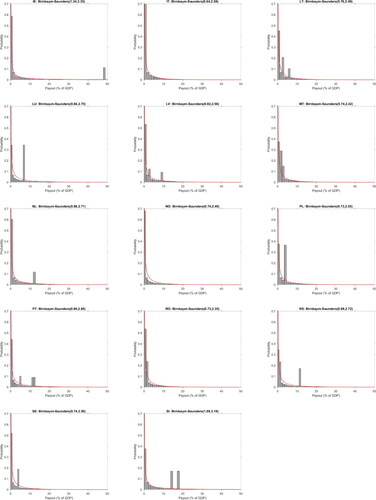

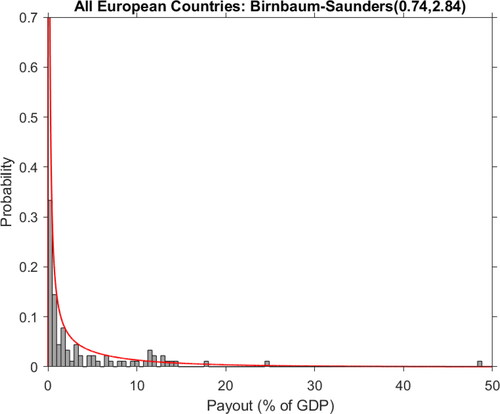

In the second stage, we attribute all positive payout events a value representing the expected payout expressed as a percentage of GDP. In order to do this, we first search for the probability distribution that best fits the historical data on payouts (with Easy Fit software). We consider 56 possible probability density functions and rank each fit with their Kolmogorov-Smirnov, Anderson-Darling, and Chi-Squared statistics, respectively. After computing the average rank and considering the minimum, we find that the Birnbaum and Saunders (Citation1969) “Fatigue Life” distribution with parameters and

is the one that best fits the data (see Appendix A). plots the histogram of empirical payouts and the associated fitted distribution.

Figure 2. Distribution of historical payouts from contingent liabilities for European countries.

Source: own computation.

Using this result, we set payout values as follows. Each time a payout event occurs for a country, we generate a random payout value from the fitted “Fatigue Life” distribution, but also extract another random payout value,

from the set of historical payouts available for that country. The actual payout value is set as either

with a probability of 2/3, or

with a probability of 1/3. This procedure assures that the simulated payout distribution takes advantage of the information contained in the full set of historical data but also preserves heterogeneous, country-specific characteristics.

The simulations enable us to estimate individual expected payouts for each country and also for the entire set of countries. Figures in Appendix B show the simulated payout distribution for each country. A summary of the results obtained in the simulation exercise and the associated expected impact of contingent liabilities on budget deficits and public debt are presented in .

Table 4. Expected impact of contingent liabilities.

The probability that contingent liabilities are realized, in a time frame of one year, records a peak for Italy (25%), followed by Germany and Hungary (21.43%). Most countries in the sample exhibit an occurrence probability ranging between 10 − 18%, while ten countries show probability levels between 3-7%. By looking at the amount of the expected payout, as % of GDP, the higher level is witnessed by Ireland (0.85%), followed by Hungary and Greece. However, in nominal terms, the largest expected payout is to be borne by Germany and amounts to around 17 billion euro. The lowest fiscal burden to be supported by the government belongs to Poland (0.13%), Luxembourg and Czech Republic; at the same time, these countries additionally exhibit a small likelihood for contingent liabilities’ realization.

In terms of the expected impact on budget deficit, the realization of contingent liabilities triggers increased fiscal stress for Estonia and Portugal. By comparing the impact on both state budget and public debt, the findings indicate that the former is more affected by the realization of contingent liabilities. Our findings are confirmed by Bova et al. (Citation2019), who explain that contingent liability realizations are associated with both a significant worsening in the overall fiscal balance and a large increase in debt-to-GDP ratio, having the potential to amplify the existing economic stress.

4. EU policy recommendations

As the empirical analysis shows, the period of the pandemic crisis will significantly affect changes in the level of public debt, which, depending on the solvency risk of the beneficiaries of public guarantees, can translate into much higher fiscal effects and risks.

The previous experience of economic and financial crises has already made it necessary to undertake research, which resulted in international guidelines in the field of contingent liabilities recommended by Schick and international economic and financial institutions. As mentioned at the beginning of the article, the most active in this area were the IMF, the World Bank, the OECD and the INTOSAI Public Debt Committee. However, most recommendations of these institutions were related to broader issues such as government debt management and fiscal transparency.

The current pandemic crisis, which may be the cause of unprecedented use of government guarantees, should also be an opportunity to develop common standards for EU countries in the area of contingent liabilities management. It is worth noting that government guarantees of EU Member States are used both at the national and international levels in terms of a number of EU financial initiatives launched in response to the recent crises (such as the European Stability Mechanism - ESM or Support to Mitigate Unemployment Risks in an Emergency - SURE). This is therefore a case of double guarantee of financial mechanisms from national budgets.

The following are the ten European standards for contingent liabilities management, as recommended by the authors, based on existing international guidelines and postulates and the presented research results ().

Table 5. Proposed European guidelines for government contingent liabilities management.

5. Conclusions

The study indicates that the pandemic crisis could undoubtedly lead to another phase of the debt crisis. As indicated by EU governments in their 2020 Stability and Convergence Programmes, the need to counteract the effects of the pandemic will be directly linked to the activation of many fiscal instruments, financed through public debt or guaranteed by public institutions (including state banks).

Our research therefore draws the following conclusions:

the current level of reporting on contingent liabilities in the EU is insufficient and significantly delayed, making it impossible to monitor the level of contingent instruments used on an ongoing basis,

simulations indicate that the impact of contingent liabilities could result in an unprecedented increase in public debt, especially in euro area countries, while exceeding the 60% of GDP limit could also occur in most EU countries,

EU countries are increasingly inclined to use contingent liabilities as "hidden expenditure" or "hidden debt", which reduces fiscal transparency and may in the future undermine the effectiveness of the assessment of the EU fiscal criteria,

In relation to the above, it seems reasonable to recommend the introduction of EU standards concerning contingent liability management, both in terms of the methodology for estimating fiscal risk, including the creation of appropriate budgetary guarantee reserves, and in terms of detailed and current reporting at both national and EU levels.

Our paper shows that the recent increase in the level of contingent liabilities can be associated with significant fiscal risks for national governments in the European Union. The risks may further be exacerbated in the context of unexpected Black Swan events that have large consequences, such as the recent COVID-19 pandemic. This implies that governments should start thinking about prophylaxis when deciding on policies about the structure of national debt, which would help mitigate an unwanted future deterioration of the fiscal position due to unexpected payouts from contingent liabilities. Therefore, our paper aims at warning governments about these risks and providing some guidelines about adequate policies.

Disclosure statement

No potential conflict of interest was reported by the authors.

Notes

1 This is available as an online appendix on the journal’s website.

2 Bova et al. (Citation2019) database was updated with data collected from: 1) IMF country-level Staff Reports for all types of CL realizations for the period 2016-2019; 2) Eurostat, in terms of financial sector CLs (country-level data on government interventions to support financial institutions - https://ec.europa.eu/eurostat/web/government-finance-statistics/excessive-deficit/supplemtary-tables-financial-crisis).

3 For each country and each year, the value of 1 is used to denote that at least one payout has occurred, and 0 otherwise.

References

- Abrigo, M. R., & Love, I. (2016). Estimation of panel vector autoregression in Stata. The Stata Journal: Promoting Communications on Statistics and Stata, 16(3), 778–804. https://doi.org/10.1177/1536867X1601600314

- Alberola, E., Arslan, Y., Cheng, G., & Moessner, R. (2020). The fiscal response to the Covid-19 crisis in advanced and emerging market economies. BIS Bulletin, No 23.

- Amaglobeli, D., End, N., Jarmuzek, M., & Palomba, G. (2015). From systemic banking crises to fiscal costs: Risk factors. IMF Working Papers, 15(166), 1. https://doi.org/10.5089/9781513529356.001

- Arellano, M., & Bond, S. (1991). Some tests of specification for panel data: Monte Carlo evidence and an application to employment equations. The Review of Economic Studies, 58(2), 277–297. https://doi.org/10.2307/2297968

- Arellano, M., & Bover, O. (1995). Another look at the instrumental variable estimation of error-components models. Journal of Econometrics, 68(1), 29–51. https://doi.org/10.1016/0304-4076(94)01642-D

- Birnbaum, Z. W., & Saunders, S. C. (1969). A new family of life distributions. Journal of Applied Probability, 6(2), 319–327. https://doi.org/10.2307/3212003

- Blejer, M. I. (1991). The measurement of fiscal deficits: Analytical and methodological issues. Journal of Economic Literature, 29, 1644–1678.

- Blundell, R., & Bond, S. (1998). Initial conditions and moment restrictions in dynamic panel data models. Journal of Econometrics, 87(1), 115–143. https://doi.org/10.1016/S0304-4076(98)00009-8

- Bova, E., Ruiz-Arranz, M., Toscani, F. G., & Ture, H. E. (2019). The impact of contingent liability realizations on public finances. International Tax and Public Finance, 26(2), 381–417. https://doi.org/10.1007/s10797-018-9496-1

- Bresciani, M. V., & Cossaro, L. (2016). A balance sheet approach to general government finance: The legacy of the crisis in selected euro area countries. Paper presented at the 13th Euroframe Conference on Economic Policy Issues in the European Union, The Netherlands.

- Buiter, W. H. (1997). Aspects of fiscal performance in some transition economics under fund-supported programs. IMF Working Papers, 97(31), 1. nohttps://doi.org/10.5089/9781451980073.001

- Cooperstein, R. F., Pennacchi, G., & I Redburn, F. S. (1995). The aggregate cost of deposit insurance: A multi – period analysis. Journal of Financial Intermediation, 4(3), 242–271. https://doi.org/10.1006/jfin.1995.1011

- Easterly, W. (1999, April). When is fiscal adjustment an illusion? Economic Policy.

- Eisner, R. (1984). Which budget deficit? Some issues of measurement and their implications. American Economic Review, 74 (2), 138–143.

- ESA. (2010). European system of accounts. pp. 125–126.

- European Commission. (2020). Assessment of public debt sustainability and COVID-related financing needs of euro area member states. https://ec.europa.eu/info/sites/info/files/economy-finance/annex_2_debt_sustainability.pdf

- Eurostat. (2021). https://ec.europa.eu/eurostat/web/government-finance-statistics/contingent-liabilities

- GAAP. (2005). Generally Accepted Accounting Practice.

- Hansen, L. P. (1982). Large sample properties of generalized method of moments estimators. Econometrica, 50(4), 1029–1054. https://doi.org/10.2307/1912775

- Heald, D., & Hodges, R. (2020). The accounting, budgeting and fiscal impact of COVID-19 on the United Kingdom. Journal of Public Budgeting, Accounting & Financial Management, 32(5), 785–795. Volume Issue https://doi.org/10.1108/JPBAFM-07-2020-0121

- IMF & the World Bank. (2002). Guidelines for public debt management.

- IMF. (2016). Fiscal monitor. Acting now, acting together.

- IMF. (2020). Managing fiscal risks under fiscal stress, special series on fiscal policies to respond to COVID-19, fiscal affairs department.

- INTOSAI Public Debt Committee. (2003, February). Fiscal exposures: Implications for debt management and the role for SAIs.

- IPSAS. (2004). International Accounting Standards Board.

- Kharas, H., & Mishra, D. (2001). Hidden deficits and currency crises. World Bank Economists Forum, World Bank.

- Makin, A. J., & Layton, A. (2021, March). The global fiscal response to COVID-19: Risks and repercussions. Economic Analysis and Policy, 69, 340–349. https://doi.org/10.1016/j.eap.2020.12.016

- Merton, R. (1977). An analytical derivation of the cost of deposit insurance and loan guarantees. An application of modern option pricing theory. Journal of Banking and Finance, 1.

- Mirza, N., Rahat, B., Naqvi, B., & Rizvi, S. K. A. (2020). Impact of Covid19 on corporate solvency and possible policy responses in the EU. The Quarterly Review of Economics and Finance. https://doi.org/10.1016/j.qref.2020.09.002

- OECD. (2005). Advances in Risk Management of Government Debt.

- OECD. (2020a). Managing fiscal risks: Lessons from case studies of selected OECD countries. OECD Journal on Budgeting, 21(1). https://doi.org/10.1787/16812336

- OECD. (2020b). OECD best practices for managing fiscal risks. Lessons from Case Studies of Selected OECD Countries and Next Steps Post COVID-19, GOV/PGC/SBO(2020)6, June.

- Polackova, H. (1998). Contingent government liabilities. A Hidden Risk for Fiscal Stability, Policy Research Working Paper, the World Bank, No 1989.

- Ramey, V. A. (2019). Ten years after the financial crisis: What have we learned from the renaissance in fiscal research? Journal of Economic Perspectives, 33(2), 89–114. https://doi.org/10.1257/jep.33.2.89

- Sargan, J. D. (1958). The estimation of economic relationships using instrumental variables. Econometrica, 26(3), 393–415. https://doi.org/10.2307/1907619

- Schick, A. (2004). Budgeting for fiscal risk. In H. Polackova Brixi & A. Schick (Eds.), Government at risk: Contingent liabilities and fiscal risk. The World Bank and Oxford University Press.

- Schick, A. (2003). Does budgeting have a future? OECD Journal on Budgeting, 2(2), 7–48.

- Sigmund, M., & Ferstl, R. (2021). Panel Vector Autoregression in R with the package panelvar. The Quarterly Review of Economics and Finance, 80, 693–720. https://doi.org/10.1016/j.qref.2019.01.001

- Singh, M., Gómez-Puig, M., & Sosvilla-Rivero, S. (2019). Increasing contingent guarantees: The asymmetrical effect on sovereign risk of different government interventions. Research Institute of Applied Economics Working Paper, No 14.

- Tobin, J. (1963). An essay on principles of debt management, Fiscal and Debt Management Policies, Commission on Money and Credit, Cowles Foundation Paper 195.

- Weber, A. (2012). Stock flow adjustments and fiscal transparency: A cross country comparison. IMF Working Papers, 12(39), 1. https://doi.org/10.5089/9781463933821.001

Appendix A.

Appendix A. Distribution fit results for payout events.

Appendix B.