Abstract

This study aims to explore the differing online banking adoption in Spanish cities and towns through Technology Acceptance Model (TAM). This paper is the first to unveil such differences between cities and towns. Data was collected from the Centre for Sociological Research and analyzed with PLS-SEM through SmartPLS. The analyzed model comprised perceived ease of use (PEOU), perceived usefulness (PU), and online banking use behaviour (UB) as variables directly associated. Perceived security (PS) was included as a mediator of the effects in UB. Multi-group analysis (MGA) and Importance-Performance Map Analysis (IPMA) were implemented. Most of the hypothesised direct and indirect effects were statistically significant and found support for both cities’ and towns’ populations. PEOU did not present a statistically significant influence over PS. The direct effects expected were found to be different in cities and towns, although differences were minimal. The study makes an outstanding contribution regarding the banking sector’s social responsibility, which may be further studied to mirror inclusive practices. It also corroborates the importance of PS as a mediator that influences online banking services use.

1. Introduction

In the last decade, online services have flourished, key among those being the banking sector. The internet has changed the way services are provided by financial institutions and customers’ banking activities (Eriksson et al., Citation2008). Banks are betting on a profound digital transformation that is promoted by the rapid spread of online applications. This situation has radically changed the banking industry and the channels they use to get to their clients (Al-Somali et al., Citation2009), that is to say, internet services have become the most effective channel to offer banking products and services (Muñoz-Leiva et al., Citation2017). In the end, unlike traditional banking activities, online banking offers more qualities and functionalities at a lower cost (Laukkanen, Citation2007).

There is no standard form of the term in the literature; it can be referred to as internet banking, online banking, or electronic banking (e-banking). According to Grabner‐Kräuter and Faullant, (Citation2008), ‘internet banking allows customers to conduct a wide range of banking transactions electronically via the bank’s web site – anytime and anywhere, faster, and with lower fees compared to using traditional, real-world bank branches’ (p. 483). Online banking offers an online transaction platform to support several e-commerce applications such as online shopping, online bill payments, online auction, internet stock trading, and so forth (Blut et al., Citation2016).

Information and Communication Technologies (ICT) for finance transactions can yield noteworthy benefits for both the service supplier and the customer (Banu et al. (Citation2019) point out that online banking was essentially designed to increase the convenience for the customer by fulfilling their requirements, with account viewing, money transfer, account application, bill payments, loan payment, and so on. At the same time, banks may also benefit from a reduction in the cost of operation (e.g. labour and service cost), an updated and synchronised dataset of their customers, and so forth (Montazemi & Qahri-Saremi, Citation2015). In other words, benefits provided by online banking are significant to ease financial services use for both parties. Nonetheless, despite the apparent advantages of internet banking for customers and the increasing number of internet users, in many countries the growth rate of internet consumers who adopt internet banking has not risen as sharply as expected until recent years (White & Nteli, Citation2004).

Although online banking has not been an appealing prospect for some users, to curb the spread of Covid-19 during the global pandemic, the lockdown imposed in several countries limited or nullified in-person services. This led to demands for the improvement of online services such as internet banking and promoted the use of online services to become more prominent within financial activities. The American Banker found that approximately 35% of clients were using their online banking service more frequently (Crosman, Citation2020) and a greater average perception of satisfaction with online banking to execute payment transactions was found (Gardner, Citation2020; Jindal & Sharma, Citation2020; Samantha, Citation2020) in comparison with previous studies that claim a more distributed satisfaction with internet banking. Furthermore, the perceived security of the internet banking system seemed to be highlighted by banks through social media campaigns which might have helped to reduce a negative perception in this regard (Naeem & Ozuem, Citation2021). However, neither of these findings differentiates online banking adoption by socio-demographic features, such as urbanicity.

To explain the factors affecting consumers’ adoption of internet banking and the influence of the use of this technology, researchers have proposed a variety of theoretical models. This work taps into the technology acceptance model (TAM) introduced by Davis (Citation1989) to provide a solid theoretical basis for the study of new-technology’s adoption, such as online banking (Zhang et al., Citation2018). The TAM considers perceived usefulness and perceived ease of use as the main determinants of technology acceptance behaviours. These two essential beliefs are linked to users’ attitudes, intentions, and use behaviour. Nevertheless, only a few studies have focussed on online banking in Spain (e.g. Liébana-Cabanillas et al., Citation2016; Özbay et al., Citation2011), where the banking sector has had to reinvent itself since the economic crisis in 2007 to reduce costs while not lowering the quality of their services. Although the rapid growth and diffusion of internet technologies have helped the finance industry in this work, questions remain unanswered about online banking dynamics.

Few studies have analyzed the effect of socio-demographic factors in new-technology adoption, dismissing the moderation role they have played to explain technology use. Prior studies have supported the differing performance of electronic banking technologies adoption according to the role of technology, social, channel, personal factors, and similar others (Alalwan et al., Citation2017; Blut et al., Citation2016; Chawla & Joshi, Citation2018; Giovanis et al., Citation2019). Mainly, there is evidence that new remote banking solutions, such as mobile banking, are differently accessed according to the socio-demographic characteristics of users (Blut et al., Citation2016; Malaquias & Hwang, Citation2019). In Spain, the self-governing territories with the fewest internet users are overwhelmingly rural, even though the majority of citizens have a cellphone (98%) or a computer (79.5%) (National Observatory of Telecommunications & Information Society, 2019). As seen in , online banking use percentage decreases with population size and is dramatically different regarding age groups where older people have less use of this service.

Table 1. Online banking use by population size.

The present study contributes to theoretically and empirically enhance the understanding of the adoption of online banking technologies in Spanish towns and cities. To the authors’ knowledge, this comparison has not been previously addressed. Therefore, based on a dataset from the Survey of the Spanish Sociological Research Centre (Sociological Research Centre, Citation2019), this study’s sample is made up of 2,481 individuals. To assess the socio-demographical differences, the sample was divided into two groups: people living in towns and people living in cities (or those not living in towns).

Following on from the above, the following research questions are stated:

What factors influence citizens’ tendency to use online banking?

Does the digitalisation of banking influence different towns’ and cities’ use of online banking?

Has online banking been implemented equally in Spanish towns and cities?

Overall, addressing these concerns may enable not just an understanding of the current implementation of online banking services, but also to assess them in terms of their social responsibility. Bank managers, policymakers, and other stakeholders might find in these results an applicable source to increase customers’ perception of usefulness, ease of use, and/or security to influence their willingness to use their services in rural and/or urban contexts’.

The remainder of the paper is structured as follows. The next section elaborates on the proposed research framework stemming from TAM to explain the uptake of online banking services. In section 3, the research model and hypotheses are presented. Sections 4 and 5 correspond to the empirical research and discussion of results. The final section extracts the main contributions, limitations, implications, and future lines of research.

2. Theoretical foundation

This section presents the relevant theoretical background based on the literature reviewed. It analyses the importance and nature of online banking and deepens TAM through the beliefs, namely perceived usefulness (PU), perceived ease of use (PEOU), and use behaviour (UB) constructs. Besides, the perceived security (PS) construct is developed as it plays an essential role in banking technologies.

2.1. Online banking

Internet banking, or online banking, supports the efficiency and scope of financial services using technology in the banking industry (Aldás‐Manzano et al., Citation2009). It is one of the electronic banking services along with telephone banking, mobile banking, and ATMs. Like other digital services, online banking delivers cutting-edge functionalities for regular services that result in benefits for customers and banking institutions.

Online banking use delivers advantages over that of the traditional setting, such examples being: i) access to account information anywhere and at any time; ii) extensive local and international competition; iii) high profitability and savings; iv) the avoidance of time spent in queues in bank offices; v) convenience; vi) affordable delivery channels (Eckhardt et al., Citation2009; Haider et al., Citation2019); and vii) inclusion of people living in rural areas through access to financial products (Xue et al., Citation2011). It also ends up being beneficial for banking institutions through low operating costs, synchronised and updated consumers datasets, more automatised processes, and so forth (Ege Oruç & Tatar, Citation2017).

Four fields attempt to study and explain online banking, namely information technology, finance, marketing, and service management. Online banking adoption has been mainly explained by social science theories, with the leading theoretical model employed being TAM (Hanafizadeh et al., Citation2014). Moreover, there is a call to broaden theories underlying online behaviour, taking into consideration different contexts such as those in less-developed regions and comparative effects of socio-demographic variables as they are found to impact online banking (Hanafizadeh et al., Citation2014). For these reasons, this study aims to explore the state of online banking in Spanish cities and towns.

2.2. Technology acceptance model

This study seeks to provide an in-deep analysis of the adoption of internet banking in cities and towns. To achieve this, it draws on the technology acceptance model (TAM) (Davis, Citation1989) that is used to study the behavioural intentions of individuals to use technology (Davis, Citation1986) such as banking services by online means.

TAM provides a frame to understand consumer willingness to adopt information technology and can be improved according to the analysis of a specific technological solution (Zhang et al., Citation2018). Some scholars have adapted the model to incorporate new variables for the model’s betterment upon the adoption of a technological system (Dash et al., Citation2011; Hanafizadeh et al., Citation2014). New versions of the model present external factors that influence customers in accepting online banking services (Rawashdeh, Citation2015; Wu et al., Citation2016). The model encompasses perceived ease of use and perceived usefulness as attitude determinants that influence the intention to use that predicts the UB of a specific technology (Davis, Citation1986, Citation1989).

Several investigations have studied TAM’s performance in diverse contexts within developed and developing countries around the world. In previous years, studies on internet banking were conducted in Taiwan (Lee, Citation2009; Yen & Wu, Citation2016), India (Hossain et al., Citation2020), Bangladesh (Kumar Sharma & Madhumohan Govindaluri, Citation2014), Iran (Yaghoubi & Bahmani, Citation2010), Pakistan (Haider et al., Citation2019), Jordan (Rawashdeh, Citation2015) and UK (McKechnie et al., Citation2006) among others. Nevertheless, a few studies have focussed on Spanish online banking use through TAM. Only a handful of such previous investigations are apparent: one which aimed to analyze product involvement, perceived risk, and trust in internet banking use (Aldás‐Manzano et al., Citation2009), while a more recent study aimed to explore the determining factors for users’ acceptance of mobile banking applications for Santander bank users (Muñoz-Leiva et al., Citation2017). None of these studies had considered the differing effects that TAM’s variables may have in different contexts, namely cities and towns.

To specify the online banking performance acceptance model, this study considers TAM and includes the PS variable in the theoretical structure proposed as Aldás‐Manzano et al. (Citation2009) suggested in a similar study for the Spanish case. To elaborate on the model beliefs and interactions, the following sections are presented.

2.2.1. Perceived usefulness (PU)

Although global growth and technological advances have been impressive over the years, there are still many areas with limited internet access. Internet access enables the possibility to use online banking (Sathye, Citation1999). Users with internet access have a greater understanding of technology (Gefen, Citation2003). They can perceive more usefulness of technology than consumers without much access (Karahanna et al., Citation1999). Thus, the use of the internet will allow users to have a better understanding of technology and how to operate with it (Ye & Potter, Citation2011). Without an internet connection, online banking transactions are not possible, which means a determinant for users to benefit from it (Al-Somali et al., Citation2008).

Almogbil (Citation2005) explained the positive relationship between the speed of internet access and the use behaviour of internet banking services. Moreover, this author found that the more hours of internet used per week, the more familiar and safer the user will feel to carry out bank transactions. Davis (Citation1993) shows that PU of internet and new technologies enables us to know how the adoption would be and how it would improve its performance. Individual PU shows the potential intention to use new and innovative banking technologies (Pikkarainen et al., Citation2004). Later, Yang and Lee (Citation2010) found that PU supports the adoption of digital banking. Taking into account that both variables have been well studied in the field of finance and online banking (Bing Tan et al., Citation2012; Suki, Citation2010), this work recognises the important relationship between the PU and the UB of bank transactions.

2.2.2. Perceived ease of use (PEOU)

PEOU was defined as ‘the degree to which the prospective users expect the target system to be free of effort’ (Davis, Citation1989). It has a positive and significant relationship with behavioural intention towards a new information system (Davis, Citation1989; Liébana-Cabanillas et al., Citation2014; Yee-Loong Chong et al., Citation2015), and with UB. The more familiar and concerned consumers are with science, technology, and the internet, the easier it will be for them to conduct online transactions. Familiarity, previous experience, and knowledge about the internet and new technologies can help diminish uncertainty in online transactions (Gefen, Citation2003).

Because PEOU of technology leads to the significant use of e-banking, banks are encouraged to design an easy-to-use internet bank platform so that customers with little technological knowledge and experience perceive that they are easy-to-handle. Bank should care about the difficulties that citizens encounter on commercial websites and, consequently, enhance their online service to increase their trust (Grabner‐Kräuter & Faullant, Citation2008). Besides, if it is not perceived as useful, customers may not use the platform or application even when they find it easy-to-use (Banu et al., Citation2019).

2.2.3. Use behaviour (UB)

UB refers to individual consumers’ actions in benefitting from a product or service and is also understood as its adoption by the consumer. TAM supports that the use of technology is the final consequence of beliefs (Oyeleye et al., Citation2015), such as PU, PEOU, and in this study, PS. This work refers to the UB of online banking. Scholars have found support for a significant association between intention to use and the actual adoption of e-banking (Aldás‐Manzano et al., Citation2009; Hanafizadeh et al., Citation2014; Walker & Johnson, Citation2006). This investigation approaches internet banking acceptance by modelling the influence of determinants or beliefs on UB.

Although it is common to consider usage intention as a mediator or predictor of UB, previous studies support the direct influence of PEOU and PU, as well as other complementary determinants, on actual usage (Eriksson et al., Citation2008; Pallister et al., Citation2007). While actual behaviour is the observable response in certain situations (Ajzen, Citation1991), the intention is an indication of a person’s readiness to perform the given behaviour (Ajzen, Citation1991). This paper considers online banking acceptance as actual behaviour because of the characteristics of the data analyzed.

The information obtained from this study enables the focus on online banking use as a reflection of the beliefs that shape user attitude. In this study, PU, PEOU, and PS are beliefs that determine UB. Taken into consideration, adequate internet access, easy-to-use platforms, and few security risks are likely to foster online banking use amongst Spanish citizens. However, it is expected that this will be different between the inhabitants of cities and those in towns. For these reasons, the first hypotheses assert the interplay among traditional TAM variables in online banking:

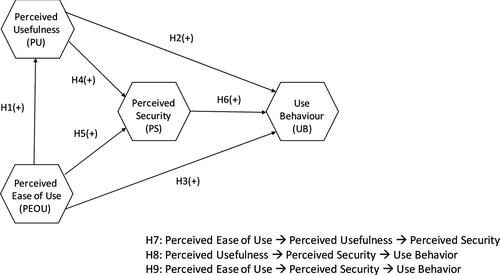

H1. Perceived ease of use is positively related to perceived usefulness.

H2. Perceived usefulness is positively related to use behaviour.

H3. Perceived ease of use is positively related to use behaviour.

2.2.4. Perceived security (PS)

Banks are not responsible for customer behaviour regarding online banking services, nor can they control it. This is the reason why consumers must make sure to navigate through safe and secure online banking platforms. However, it is a priority for banking institutions to make consumers feel secure and provide efficient processes to safeguard their private personal information (Rifon et al., Citation2005). Consumers need a reliable environment to decide whether to adopt online banking services. Without an adequate PS level, the UB of internet banking will be at risk (Lu et al., Citation2006; Masrek et al., Citation2018; Pikkarainen et al., Citation2004) as concerns about safety and security of platforms may be raised taking into account the increase of cyber-attacks or cyber-crimes.

The PS construct comprises three dimensions: i) safety, ii) reliability and iii) privacy (Nui Polatoglu & Ekin, Citation2001). These aspects of security assure a perception of confidentiality and integrity of bank accounts (Banu et al., Citation2019). Hence, the level of security plays a remarkable role in online services, particularly in online banking. However, little is known about the security awareness and security behaviours of final users of financial technologies (Davinson & Sillence, Citation2014).

For this reason, this study includes in the model the PS variable as a mediator as did prior studies on Spanish online banking (Aldás‐Manzano et al., Citation2009). This analysis will also provide information about cities and towns, to target preventive measures against online fraud, identity cloning, and other cybersecurity threats that are perceived in both regions. This variable suggests additional hypotheses for this study:

H4. Perceived usefulness is positively related to perceived security.

H5. Perceived ease of use is positively related to perceived security.

H6. Perceived security is positively related to use behaviour.

H7. Perceived usefulness mediates the relation between perceived ease of use and perceived security.

H8. Perceived security mediates the relation between perceived usefulness and use behaviour.

H9. Perceived security mediates the relation between perceived ease of use and use behaviour.

Drawing upon these theoretical foundations, this study researches the determinants of citizens’ attitudes towards internet banking acceptance in Spain using the Technology Acceptance Model. The research model proposed is presented in .

Figure 1. Hypothesised research model.

Source: Author.

3. Methodology

3.1. Data collection and sample

The empirical analysis of the hypotheses is conducted based on a sample of 2,481 people from 256 municipalities obtained from a database of the Sociological Research Centre (CIS, using its Spanish acronym) of 2018 (Sociological Research Centre, Citation2019). This Spanish Centre is an Autonomous Organism whose primary purpose is the scientific study of Spanish society, mainly through sociometric instruments. (Sociological Research Centre, Citation2020).

The database came from a CIS survey that assessed inhabitants based on population size of their habitat. Seven categories were defined: less than or equal to 2,000 inhabitants; from 2,001 to 10,000; from 10,001 to 50,000; from 50,001 to 100,000; from 100,001 to 400,000; from 400,001 to 1,000,000, and more than 1,000,000 inhabitants. For this study, two divisions were considered: people living in towns (less than 10,000 individuals) and people living in cities (the rest), reaching 552 and 1,929 individuals, respectively. The analysis focussed on the identification of significant differences between both groups. In , the main characteristics of the survey are presented.

Table 2. Survey features.

3.2. Measurement instrument

The inclusion of variables from the CIS’s survey was guided by the literature review. Variables matched the constructs used in TAM and the PS mediator variable. The research instrument encompassed nine variables (five of them control variables) and 14 items. Variables PEOU and PS were measured using a four-point Likert scale ranging from 1 None to 4 Much, variable UB is dichotomic, and PU was measured through days of internet use (3 or 4 days per week, 1 or 2 days per week, once a month, less frequently or never).

3.3. Data analysis

This study applied Partial Least Squares Structural Equations Modelling (PLS-SEM) to test the hypothesised research model empirically. This methodology allows the assessment of the reliability and validity of the measuring items (i.e. indicators), constructs (i.e. latent variables), and the complex relationships between them (Barroso et al., Citation2010; Hairet al., Citation2016; Citation2017). SmartPLS 3.2.9 software was used to test the validity and statistical significance of the measurement model, structural model, and the Importance-Performance Map Analysis (Ringle et al., Citation2015).

4. Results

The interpretation of the PLS model comprises two phases: measurement model (outer model) analysis and structural model (inner model) analysis. Additionally, the Importance – Performance Map (IPMA) Analysis was carried out to map the impact of the indicators and constructs on the dependent variable.

4.1. Measurement model assessment

The estimation of the measurement model is satisfactory. shows that outer loadings are higher than 0.707. This means that all indicators are suitable (Hair, Hult, et al., Citation2014). Furthermore, the construct reliability requirement is adequate because Cronbach’s alpha, rho_A, and composite reliability values are higher than 0.7 for all the reflective constructs. The convergent validity criterion was met as the average variance extracted (AVE) values are greater than 0.5.

Table 3. Individual item reliability, construct reliability, and convergent validity.

presents the discriminant validity according to the heterotrait-monotrait (HTMT) criterion which is met by this study as the values obtained are under the suggested threshold of 0.85 points (Kline, Citation2015).

Table 4. Discriminant validity.

4.2. Structural model assessment

Structural model analysis used the bootstrapping technique (5000 re-samples) to generate standard errors, t-statistics, p-values, and 95% bias-corrected confidence intervals (BCCI) (Hair, Sarstedt, et al., Citation2014). These indicators help to understand the statistical significance of the hypothesised relationships in the research model. The coefficient of determination (R2) was also obtained as it is the main criterion for measuring the explained variance of the model under study.

and encompass the main parameters that are obtained for the structural models for both towns () and cities (). reveals that nearly all the direct relationships hypothesised appear to be statistically significant. There is no empirical support for H5, although this relationship is significant when it is mediated by PU (H9). The control variables – namely gender, age, and economic situation – do not show a significant effect on the town inhabitants’ sample. shows the same pattern for the city inhabitants’ sample. Hence, there is not a statistically significant positive direct link between PEOU and PS (H5). However, the links among the variables PEOU, PS, and UB are positive and significant in both samples. Education level acts as a non-significant moderator of the model for both groups.

Table 5. Structural model results for towns.

Table 6. Structural model results for cities.

The nonparametric confidence set multi-group analysis (MGA) approach was employed to compare the sample-specific bootstrap confidence intervals (). Sarstedt et al. (Citation2011) point out that this method is a solution to the possible defects of previous methods that seek similar objectives. Specifically, this analysis constructs the bootstrap-based 95 percent BCCI for the two groups (towns and cities) and proves whether the estimated parameter for a path relationship of group 1 falls within the corresponding confidence interval of group 2 or vice versa. In this study, 95% BCCI of the group of town inhabitants is used, and the analysis assesses if the path coefficient of the group of city inhabitants is within this range. If this happens, it is because there are no significant differences between the sample-specific path coefficients. In the same way, if such superimposition is not perceived, one can accept that the sample-specific path coefficients are significantly different (Sarstedt et al., Citation2011).

Table 7. Nonparametric confidence set approach multi-group analysis (MGA).

4.3. Importance-performance map analysis

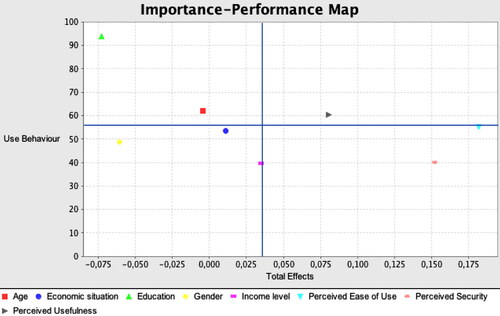

This study carries out a complementary technique to delve into the empirical outcomes obtained, called the Importance-Performance Map Analysis (IPMA) technique or priority map analysis or importance-performance matrix (Ringle & Sarstedt, Citation2016). Using the average latent variable scores, this analysis allows us to know the relevance of the most critical antecedent constructs while determining a particular target construct.

shows the representation of the variables in the IPMA diagram. The Y-axis represents the antecedent construct’s performance and the X-axis represents the importance of the antecedent constructs while determining the target constructs. In this case, UB is the target construct. The two supplementary lines divide the importance-performance map into four quadrants (Ringle & Sarstedt, Citation2016), one horizontal line (performance) and another vertical line (importance) representing the average values of both dimensions. In this way, we can assess values above and below the average. Although initially there are no established labels for quadrants, the following labels are proposed:

Figure 2. IPMA: Constructs’ standardised effects.

Source: Author.

Quadrant 1: values above the average in both the importance and performance dimension (upper-right quadrant).

Quadrant 2: values above the average in the importance dimension but which are currently below the average in the performance dimension (lower-right quadrant).

Quadrant 3: values below the average in both the importance dimension and the performance dimension (lower-left quadrant).

Quadrant 4: values above the average in the performance dimension and below the average in the importance dimension (upper-left quadrant).

presents the IPMA results for the two groups. In the case of the town inhabitants’ sample, variables PU and PEOU (skimming the line) are in quadrant 1 (upper-right) while the variable PS is in quadrant 2. Control variables are in quadrants 3 and 4. Concretely, variables gender, income level, and economic situation have low performance and importance. Regarding the cities diagram, PU and PEOU have the greatest importance and performance, that is, they are key differentiation factors in achieving the objective. The variable PEOU clearly lies within the quadrant. On the other hand, the PS requires immediate improvement since it is the factor with the least performance and the most important. As in the previous case, the control variables are also found in quadrants 3 and 4. However, the variable age brushes the line. Therefore, there are no great differences in the IPMA graphic representation for cities and towns.

5. Discussion and conclusions

This study discusses the potential factors that influence towns’ and cities’ orientation to use online banking services and aims to identify the differences between its implementation in both regions. The main theoretical contribution lies in the comparison of two samples (towns and cities) according to socio-demographic traits. To the authors’ knowledge, the extant research lacks empirical studies that apply the Technology Acceptance Model to Spanish online banking; it remains necessary nowadays to compare and understand the difference between these two contexts.

Building on previous literature, this study tested a research model with four variables, namely PEOU, PU, PS, and UB, and aimed to clarify the direct and mediated links amongst them. To address this gap, the well-known TAM developed by Davis (Citation1989) served as the theoretical foundation to detect how these main factors impact the use of internet banking services in Spanish towns and cities.

Through empirical methods, the evidence found with our sample reveals that both the direct and indirect effects are positive and statistically significant for all hypotheses except for H5 (PEOU → PS). However, a higher level of interaction (H9: PEOU → PS → UB) containing this last relationship and an ultimate effect on UB reached a positive and significant effect. These results find support with prior research that also employed TAM. For instance, Yen and Wu (Citation2016), in their study of mobile financial services, found that the link between PEOU and PU is non-significant (regarding gender as moderator) as in this study’s results. Besides, MGA yielded no significant differences between the two compared groups (towns and cities). In this analysis, it is noticeable that the variable PEOU affects PU and UB differently, although minimally.

Based on the surveys by the the National Institute of Statistics (Citation2019), the results lead to the assertion that implementation of e-banking, such as the use of online banking services, is increasing considerably in towns and cities. Thus, we could answer the questions asked in the introduction: Does banking digitalisation influence online banking use in both towns and cities? Has online banking been implemented equally in Spanish towns and cities? According to the present analysis, it seems that there are no great differences between the use of online banking services in cities and towns. One possible explanation could be the efforts by public and private institutions to provide online banking services to customers across diverse Spanish areas.

This study has several important managerial and practical implications for banking companies, governmental entities, and telecommunication companies. Although internet and online banking services are increasing rapidly, financial institutions must still implement measures to engage their clients. For example, promoting online services, namely internet or mobile banking, through social networks (Muñoz-Leiva et al., Citation2017); developing more intuitive and straightforward websites and banking applications; or training through workshops or courses in the use of new technologies in rural areas which are more affected by depopulation and ageing. In this way, they may gain market share while strengthening their relationship with clients (Prodanova et al., Citation2015).

Most importantly, it is necessary to act on cyber-risks that could jeopardise the security and private information of clients, therefore affecting their perception of security. Risk prevention measures should be on the agenda as it has been shown in this study that PS significantly mediates online banking use behaviour. For these reasons, bank managers should focus on strengthening the introduction of new quality and safety technologies among clients who may suffer greater financial exclusion, which later on reduces costs in a market of low profitability for the banking business.

On the other hand, policies on telecommunications should guarantee access to (high-speed) internet in all Spanish territories. To this end, politicians must prioritise the keys presented in the OECD report entitled ‘Bridging the rural digital divide’. According to this report, among the keys to closing the existent digital gap between urban and rural territories, it is suggested to control the broadband quality, reduce monthly fees as costs associated with facilities, create municipal and school networks, establish a minimum speed, increase service reliability, and increase the digital literacy of the population (OECD, Citation2018). Therefore, boosting digitisation and innovation requires investment and effort from the private and public sectors due to its consequential effect on other economic sectors.

Notwithstanding the contributions of this study, this work has various limitations that represent research opportunities. Firstly, this study has been performed with secondary data from a particular geographical context (Spain). Though data are of high quality, these results should not be generalised. Secondly, the set of items to measure the constructs and design of the questionnaire are limited. A survey enabled to include a population around the world could control for intercultural aspects but at the same time could assess the differing online banking use in both cities and towns. Future research in this area could design a measurement instrument based on reliable scales with enough validity evidence. Thirdly, the individual perception of the participants was overlocked while taking a representative value for the sample. Future investigations are called to design case studies to complement these results which could later improve the participation of the government, financial entities, and telecommunication companies. Fourthly, it might be interesting to investigate the degree of digital adaptation of different generational groups (e.g. baby boomers, millennials, and digital natives) to online banking. Fifthly, a variable to measure the number of cyber-attacks on respondents could be explored and related to the degree of security or PS. Finally, it is advisable to compare the current results to the implementation of online banking in cities and towns in the mid- or post-Covid-19 era. This extraordinary situation has probably reduced the elderly population in villages and increased use of online banking applications in both urban and rural contexts.

Disclosure statement

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

References

- Ajzen, I. (1991). The theory of planned behavior. Organizational Behavior and Human Decision Processes, 50(2), 179–211. https://doi.org/10.1016/0749-5978(91)90020-T

- Alalwan, A. A., Dwivedi, Y. K., & Rana, N. P. (2017). Factors influencing adoption of mobile banking by Jordanian bank customers: Extending UTAUT2 with trust. International Journal of Information Management, 37(3), 99–110. https://doi.org/10.1016/j.ijinfomgt.2017.01.002

- Aldás‐Manzano, J., Lassala‐Navarré, C., Ruiz‐Mafé, C., & Sanz‐Blas, S. (2009). Key drivers of internet banking services use. Online Information Review, 33(4), 672–695. https://doi.org/10.1108/14684520910985675

- Almogbil, A. M. A. (2005). Security, perceptions, and practices. Challenges facing adoption of online banking in Saudi Arabia [ProQuest Dissertations and Theses]. The George Washington University.

- Al-Somali, S. A., Gholami, R., & Clegg, B. (2008). Internet banking acceptance in the context of developing countries: an extension of the technology acceptance model. European Conference on Management of Technology, 12(9), 1–16.

- Al-Somali, S. A., Gholami, R., & Clegg, B. (2009). An investigation into the acceptance of online banking in Saudi Arabia. Technovation, 29(2), 130–141. https://doi.org/10.1016/j.technovation.2008.07.004

- Banu, A. M., Mohamed, N. S., & Parayitam, S. (2019). Online banking and customer satisfaction: Evidence from India. Asia-Pacific Journal of Management Research and Innovation, 15(1–2), 68–80. https://doi.org/10.1177/2319510X19849730

- Barroso, C., Carrión, G. C., & Roldán, J. L. (2010). Applying maximum likelihood and PLS on different sample sizes: Studies on SERVQUAL model and employee behavior model. In Handbook of Partial Least Squares (pp. 427–447). Springer.

- Bing Tan, P. J., Robert Potamites, P., & Wens’Chi, L. (2012). Applying the TAM to understand the factors affecting use of online banking in the Pescadores. ARPN Journal of Science and Technology, 2(11), 1022–1028. https://cutt.ly/4jTU9WH

- Blut, M., Wang, C., & Schoefer, K. (2016). Factors influencing the acceptance of self-service technologies. Journal of Service Research, 19(4), 396–416. https://doi.org/10.1177/1094670516662352

- Chawla, D., & Joshi, H. (2018). The moderating effect of demographic variables on mobile banking adoption: An empirical investigation. Global Business Review, 19(3_suppl), S90–S113. https://doi.org/10.1177/0972150918757883

- Crosman, P. (2020). Digital banking is surging during the pandemic. Will it last. American Banker, 185(81), 1.

- Dash, M., Mohanty, A. K., Pattnaik, S., Mohapatra, R. C., & Sahoo, D. S. (2011). Using the TAM model to explain how attitudes determine adoption of internet banking. European Journal of Economics, Finance and Administrative Sciences, 36(1), 50–59.

- Davinson, N., & Sillence, E. (2014). Using the health belief model to explore users’ perceptions of ‘being safe and secure’ in the world of technology mediated financial transactions. International Journal of Human-Computer Studies, 72(2), 154–168. https://doi.org/10.1016/j.ijhcs.2013.10.003

- Davis, F. D. (1989). Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS Quarterly, 13(3), 319. https://doi.org/10.2307/249008

- Davis, F. D. (1993). User acceptance of information technology: System characteristics, user perceptions and behavioral impacts. International Journal of Man-Machine Studies, 38(3), 475–487. https://doi.org/10.1006/imms.1993.1022

- Davis, F. (1986). A technology acceptance model for empirically testing new end-user information systems: Theory and results [Doctoral Dissertation]. Massachusetts Institute of Technology. https://doi.org/10.1016/S0378-7206(01)00143-4

- Eckhardt, A., Laumer, S., & Weitzel, T. (2009). Who influences whom? Analyzing workplace referents’ social influence on it adoption and non-adoption. Journal of Information Technology, 24(1), 11–24. https://doi.org/10.1057/jit.2008.31

- Ege Oruç, Ö., & Tatar, Ç. (2017). An investigation of factors that affect internet banking usage based on structural equation modeling. Computers in Human Behavior, 66, 232–235. https://doi.org/10.1016/j.chb.2016.09.059

- Eriksson, K., Kerem, K., & Nilsson, D. (2008). The adoption of commercial innovations in the former Central and Eastern European markets. International Journal of Bank Marketing, 26(3), 154–169. https://doi.org/10.1108/02652320810864634

- Gardner, B. (2020). Dirty banknotes may be spreading the coronavirus, WHO suggests. Daily Telegraph, 8p.

- Gefen, D. (2003). TAM or just plain habit. Journal of Organizational and End User Computing, 15(3), 1–13. https://doi.org/10.4018/joeuc.2003070101

- Giovanis, A., Assimakopoulos, C., & Sarmaniotis, C. (2019). Adoption of mobile self-service retail banking technologies. International Journal of Retail & Distribution Management, 47(9), 894–914. https://doi.org/10.1108/IJRDM-05-2018-0089

- Grabner‐Kräuter, S., & Faullant, R. (2008). Consumer acceptance of internet banking: the influence of internet trust. International Journal of Bank Marketing, 26(7), 483–504. https://doi.org/10.1108/02652320810913855

- Haider, Z., Rahim, A., & Aslam, F. (2019). Antecedents of online banking adoption in Pakistan: An empirical study. International Research Journal of Arts and Humanities, 47(47), 197–214. https://sujo-old.usindh.edu.pk/index.php/IRJAH/article/view/5135/3232

- Hair, J., Jr., Hult, G. T., Ringle, C., & Sarstedt, M. (2014). A primer on partial least squares structural equation modeling (PLS-SEM). SAGE.

- Hair, J., Jr., Hult, G. T., Ringle, C., & Sarstedt, M. (2016). A primer on partial least squares structural equation modeling (PLS-SEM). SAGE.

- Hair, J., Jr., Sarstedt, M., Hopkins, L., & G. Kuppelwieser, V. (2014). Partial least squares structural equation modeling (PLS-SEM). European Business Review, 26(2), 106–121. https://doi.org/10.1108/EBR-10-2013-0128

- Hair, J., Hollingsworth, C. L., Randolph, A. B., & Chong, A. Y. L. (2017). An updated and expanded assessment of PLS-SEM in information systems research. Industrial Management & Data Systems, 117(3), 442–458. https://doi.org/10.1108/IMDS-04-2016-0130

- Hanafizadeh, P., Keating, B. W., & Khedmatgozar, H. R. (2014). A systematic review of Internet banking adoption. Telematics and Informatics, 31(3), 492–510. https://doi.org/10.1016/j.tele.2013.04.003

- Hossain, S. A., Bao, Y., Hasan, N., & Islam, F. (2020). Perception and prediction of intention to use online banking systems. International Journal of Research in Business and Social Science, 9, 112–116.

- Jindal, M., & Sharma, V. L. (2020). Usability of online banking in India during COVID-19 pandemic. International Journal of Engineering and Management Research, 10(6), 69–72.

- Karahanna, E., Straub, D. W., & Chervany, N. L. (1999). Information technology adoption across time: A cross-sectional comparison of pre-adoption and post-adoption beliefs. MIS Quarterly, 23(2), 183. https://doi.org/10.2307/249751

- Kline, R. B. (2015). Principles and practice of structural equation modelling. The Guilford Press.

- Kumar Sharma, S., & Madhumohan Govindaluri, S. (2014). Internet banking adoption in India. Journal of Indian Business Research, 6(2), 155–169. https://doi.org/10.1108/JIBR-02-2013-0013

- Laukkanen, T. (2007). Internet vs mobile banking: Comparing customer value perceptions. Business Process Management Journal, 13(6), 788–797. https://doi.org/10.1108/14637150710834550

- Lee, M.-C. (2009). Factors influencing the adoption of internet banking: An integration of TAM and TPB with perceived risk and perceived benefit. Electronic Commerce Research and Applications, 8(3), 130–141. https://doi.org/10.1016/j.elerap.2008.11.006

- Liébana-Cabanillas, F., Muñoz-Leiva, F., Sánchez-Fernández, J., & Viedma-del Jesús, M. I. (2016). The moderating effect of user experience on satisfaction with electronic banking: empirical evidence from the Spanish case. Information Systems and e-Business Management, 14(1), 141–165. https://doi.org/10.1007/s10257-015-0277-4

- Liébana-Cabanillas, F., Sánchez-Fernández, J., & Muñoz-Leiva, F. (2014). The moderating effect of experience in the adoption of mobile payment tools in Virtual Social Networks: The m-Payment Acceptance Model in Virtual Social Networks (MPAM-VSN). International Journal of Information Management, 34(2), 151–166. https://doi.org/10.1016/j.ijinfomgt.2013.12.006

- Lu, C., Lai, K., & Cheng, T. C. E. (2006). Adoption of internet services in liner shipping: An empirical study of shippers in Taiwan. Transport Reviews, 26(2), 189–206. https://doi.org/10.1080/01441640500246713

- Malaquias, R. F., & Hwang, Y. (2019). Mobile banking use: A comparative study with Brazilian and U.S. participants. International Journal of Information Management, 44, 132–140. https://doi.org/10.1016/j.ijinfomgt.2018.10.004

- Masrek, M. N., Halim, M. S. A., Khan, A., & Ramli, I. (2018). The impact of perceived credibility and perceived quality on trust and satisfaction in mobile banking context. Asian Economic and Financial Review, 8(7), 1013–1025. https://ideas.repec.org/a/asi/aeafrj/2018p1013-1025.html https://doi.org/10.18488/journal.aefr.2018.87.1013.1025

- McKechnie, S., Winklhofer, H., & Ennew, C. (2006). Applying the technology acceptance model to the online retailing of financial services. International Journal of Retail & Distribution Management, 34(4/5), 388–410. https://doi.org/10.1108/09590550610660297

- Montazemi, A. R., & Qahri-Saremi, H. (2015). Factors affecting adoption of online banking: A meta-analytic structural equation modeling study. Information & Management, 52(2), 210–226. https://doi.org/10.1016/j.im.2014.11.002

- Muñoz-Leiva, F., Climent-Climent, S., & Liébana-Cabanillas, F. (2017). Determinants of intention to use the mobile banking apps: An extension of the classic TAM model. Spanish Journal of Marketing - ESIC, 21(1), 25–38. https://doi.org/10.1016/j.sjme.2016.12.001

- Naeem, M., & Ozuem, W. (2021). The role of social media in internet banking transition during COVID-19 pandemic: Using multiple methods and sources in qualitative research. Journal of Retailing and Consumer Services, 60, 102483. https://doi.org/10.1016/j.jretconser.2021.102483

- National Institute of Statistics. (2019). Survey on equipment and use of information and communications technology in households. Year 2019. https://www.ine.es/prensa/tich_2019.pdf

- National Observatory of Telecommunications and Information Society. (2019). Report on the information society and telecommunications and the ICT and content sector in Spain by autonomous communities (Spain). https://www.ontsi.red.es/sites/ontsi/files/2019-10/InformeEspaña.pdf

- Nui Polatoglu, V., & Ekin, S. (2001). An empirical investigation of the Turkish consumers’ acceptance of internet banking services. International Journal of Bank Marketing, 19(4), 156–165. https://doi.org/10.1108/02652320110392527

- OECD. (2018). Bridging the rural digital divide. OECD Digital Economy Papers 265. https://doi.org/10.1787/852bd3b9-en

- Oyeleye, O., Sanni, M., & Shittu, T. (2015). An investigation of the effects of customer’s educational attainment on their adoption of e-banking in Nigeria. The Journal of Internet Banking and Commerce, 20(3), 133. https://doi.org/10.4172/1204-5357.1000133

- Özbay, R. D., Dinçer, H., & Hacioglu, Ü. (2011). Internet based innovation strategy for the banks in the era of 2008 global financial crisis. International Journal of Business and Social Science, 2(22).

- Pallister, J. G., Wang, H. C., & Foxall, G. R. (2007). An application of the style/involvement model to financial services. Technovation, 27(1–2), 78–88. https://doi.org/10.1016/j.technovation.2005.10.001

- Pikkarainen, T., Pikkarainen, K., Karjaluoto, H., & Pahnila, S. (2004). Consumer acceptance of online banking: An extension of the technology acceptance model. Internet Research, 14(3), 224–235. https://doi.org/10.1108/10662240410542652

- Prodanova, J., San-Martín, S., & Jiménez, N. (2015). The present and the future of m-banking according to spanish bank customers. Universia Business Review, pp. 94–117.

- Rawashdeh, A. (2015). Factors affecting adoption of internet banking in Jordan. International Journal of Bank Marketing, 33(4), 510–529. https://doi.org/10.1108/IJBM-03-2014-0043

- Rifon, N. J., LaRose, R., & Choi, S. M. (2005). Your privacy is sealed: Effects of web privacy seals on trust and personal disclosures. Journal of consumer affairs, 39(2), 339–362. https://doi.org/10.1111/j.1745-6606.2005.00018.x

- Ringle, C. M., & Sarstedt, M. (2016). Gain more insight from your PLS-SEM results. Industrial Management & Data Systems, 116(9), 1865–1886. https://doi.org/10.1108/IMDS-10-2015-0449

- Ringle, C. M., Wende, S., & Becker, J.-M. (2015). SmartPLS 3. SmartPLS GmbH.

- Samantha, M. K. (2020). Dirty money: The case against using cash during the coronavirus outbreak. CNN. Retrieved May 16, 2020, https://edition.cnn.com/2020/03/07/tech/mobile-payments-coronavirus/index.html

- Sarstedt, M., Henseler, J., & Ringle, C. M. (2011). Multigroup analysis in partial least squares (PLS) path modeling: Alternative methods and empirical results. In M. Sarstedt, M. Schwalger, & C. R. Taylor (Eds.), Advances in international marketing (pp. 195–218). Emerald Group Publishing Limited. https://doi.org/10.1108/S1474-7979(2011)0000022012

- Sathye, M. (1999). Adoption of Internet banking by Australian consumers: An empirical investigation. International Journal of Bank Marketing, 17(7), 324–334. https://doi.org/10.1108/02652329910305689

- Sociological Research Centre. (2019). Report of activities 2018. http://www.cis.es/cis/export/sites/default/-Archivos/Memorias/MEMORIA_CIS_2018.pdf

- Sociological Research Centre. (2020). Report of activities 2019. http://www.cis.es/cis/export/sites/default/-Archivos/Memorias/MEMORIA_CIS_2019.pdf

- Suki, N. M. (2010). An empirical study of factors affecting the Internet banking adoption among Malaysian consumers. Journal of Internet Banking and Commerce, 15(2), 1–11. https://cutt.ly/LjTIcRZ

- Walker, R. H., & Johnson, L. W. (2006). Why consumers use and do not use technology‐enabled services. Journal of Services Marketing, 20(2), 125–135. https://doi.org/10.1108/08876040610657057

- White, H., & Nteli, F. (2004). Internet banking in the UK: Why are there not more customers? Journal of Financial Services Marketing, 9(1), 49–56. https://doi.org/10.1057/palgrave.fsm.4770140

- Wu, Y. W., Wen, M. H., Chen, C. M., & Hsu, I. T. (2016). An integrated BIM and cost estimating blended learning model - Acceptance differences between experts and novice. EURASIA Journal of Mathematics, Science and Technology Education, 12(5), 1347–1363. https://doi.org/10.12973/eurasia.2016.1517a

- Xue, M., Hitt, L. M., & Chen, P. (2011). Determinants and outcomes of internet banking adoption. Management Science, 57(2), 291–307. https://doi.org/10.1287/mnsc.1100.1187

- Yaghoubi, N.-M., & Bahmani, E. (2010). Factors affecting the adoption of online banking: An integration of technology acceptance model and theory of planned behavior. Pakistan Journal of Social Sciences, 7(3), 231–236. https://doi.org/10.3923/pjssci.2010.231.236

- Yang, K., & Lee, H. (2010). Gender differences in using mobile data services: Utilitarian and hedonic value approaches. Journal of Research in Interactive Marketing, 4(2), 142–156. https://doi.org/10.1108/17505931011051678

- Ye, C., & Potter, R. (2011). The role of habit in post-adoption switching of personal information technologies: An empirical investigation. Communications of the Association for Information Systems, 28, 35. https://doi.org/10.17705/1CAIS.02835

- Yee-Loong Chong, A., Liu, M. J., Luo, J., & Keng-Boon, O. (2015). Predicting RFID adoption in healthcare supply chain from the perspectives of users. International Journal of Production Economics, 159, 66–75. https://doi.org/10.1016/j.ijpe.2014.09.034

- Yen, Y.-S., & Wu, F.-S. (2016). Predicting the adoption of mobile financial services: The impacts of perceived mobility and personal habit. Computers in Human Behavior, 65, 31–42. https://doi.org/10.1016/j.chb.2016.08.017

- Zhang, T., Lu, C., & Kizildag, M. (2018). Banking “on-the-go”: Examining consumers’ adoption of mobile banking services. International Journal of Quality and Service Sciences, 10(3), 279–295. https://doi.org/10.1108/IJQSS-07-2017-0067