?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The novel Covid-19 virus has changed the dynamics of ‘flight to safety’ investment for various economies. Thus, the hedging ability of the stocks must be revisited in the scenario of this pandemic. For this purpose, specifically understanding the importance of a semi-strong form of an efficient market hypothesis is important. This was to observe the speed at which the markets react to the news announcement, and how rapidly they absorb new information to regain thier position in the market. Hence, this study conducts an event study analysis on Pakistan’s emerging market to detect the financial and non-financial stock price reactions towards the lockdown announcement, following the spread of Covid-19 in Pakistan. The daily data on the KSE-100 index for thirty different industries, comprising of ninety firms, spanning from December 12, 2019, till June 7, 2020, was collected and analyzed. The abnormal returns were recorded to be at around 21 [−10. +10] and 41 days [−20, +20] event window, around the day of the lockdown announcement. These abnormal returns were obtained through the market model regression. The data collected implied that most of the industries were stable and behaved well before the event day, while the affected sectors recovered fairly quickly. Therefore, it has been affirmed that Pakistan’s equity portfolios are informationally efficient, and can benefit the investors during a pandemic.

JEL CODES:

1. Introduction

Pandemics arise and change the dynamics of the people; Coronavirus (Covid-19) is also among these pandemics that transform the lifestyles of a common man and the decision-making criteria of policymakers (Su, Dai, et al., Citation2021; Umar, Ji, Kirikkaleli, & Xu, Citation2020). Due to the outbreak of Covid-19, the year 2020 will be remembered in history. It is a respiratory disease for which treatment is still unavailable (Liu et al., Citation2020). (Mirza et al., Citation2020) declare that pandemics are originated naturally, possess weak venues to access the potency of price and reaction scenarios of different mutual funds. Covid-19 brought countless challenges across the globe. It has affected the lives of the common man and shakes the foundations of various countries' economic and financial systems (Su, Song, et al., Citation2021). According to the data obtained by John Hopkin's university resource center (https://coronavirus.jhu.edu/map.html) as of March 16, 2021, a total of 120,453,308 active cases with 2,663,741 causalities amid Covid-19 were recorded across the world. These circumstances are indicating the recession of the global economy. In June 2020, The World Economic Outlook forecasted the global economic growth would drop by 4.9 percent 2020. The worldwide trade was also affected in 2020 and decreased by 32 percent compared to the post-Covid-19 year (World Trade Organization).

There has been emerging literature on the influence of Covid-19 concerning the financial performance of different economies. The inclusive impression of the Covid-19 has been explained comprehensively by (Gao et al., Citation2021; Mirza et al., Citation2020; Su, Sun, et al., Citation2021; Yarovaya et al., Citation2020). In the early study of (Rizvi et al., Citation2020), the three phases of Covid-19 have been examined to assess the performance of mutual funds of the EU through various investment styles. The study observes the variation in investment behaviour across all the phases (Su, Sun, et al., Citation2021). Similarly, the study by (Yarovaya et al., Citation2020) asserts the diversified impact of Covid-19 to explore the nexus among human capital efficiency and performance of mutual funds for the most affected European countries included Spain, Italy, France, Germany, and Belgium, while (Mirza et al., Citation2020) examined this influence for Latin Americana mutual funds. Similarly, in the context of the individual firm analysis, the solvency of the non-financial firms of EU member states during the pandemic crisis has been studied by (Mirza et al., Citation2020)for numerous stress circumstances. It has been documented by the above studies that they focused on most of the developed economies along with the high mortality rate caused by Covid-19. This forces us to derive the motivation of this research to analyze the hedge and safe haven ability of financial and non-financial stocks of emerging economies like Pakistan as investors are in constant need of diversified portfolios (Umar et al., Citation2021).

According to the United Nations, Pakistan is the fifth largest populated country globally, and its population covers 2.8% of the world's population. The World Health Organization was expected that the virus would spread rapidly, and it became a catastrophe for populated countries(Su, Dai, et al. Citation2021). Thus the protection of a huge population needs wise strategies to tackle the pandemic (Abid et al., Citation2020). Fortunately, the first confirmed case of Covid-19 in Pakistan was reported on February 26, 2020, in Karachi city, and a total of 645,356 confirmed cases are reported to this research, with 14,091 deaths (Su, Dai, et al., Citation2021). Hence, the number of cases and recovery rate is far better than other countries globally, such as the USA, Italy, France, Spain, etc. The statistics reported by Asian Development Bank show that the GDP of Pakistan suffers by 1.57% and unemployment of 946,000 citizens. Likewise, in other countries globally, Pakistan was also expected to affect badly by the emergence of Covid-19, especially when the Government of Pakistan started preparing Lockdown. The global market crash, deceleration in oil prices, and increasing unemployment are the major influence of the Covid-19 (Su, Dai, et al., Citation2021). Pakistan was confronted with a tough time in early 2020 as the country's health infrastructure is very poor. World Health Organization declared the news of Covid-19 outbreak around the globe, and suddenly public health emergency on January 30, 2020, Government of Pakistan started planning to handle the upcoming pandemic situation in the country.

Thus keeping in view the pandemic situation, multiple questions have been addressed in the present study. Firstly it seems to be very important to observe that how volatile a market like Pakistan reacts toward the news of Lockdown? Alternatively, to test the semi-strong form of efficient market hypothesis in Pakistan, the impact has been observed to all firms listed in financial and non-financial sectors under the umbrella of the Pakistan stock exchange (PSX) (Umar et al., Citation2021). Thirdly can investors trust the equity portfolios belong to the financial and non-financial sectors of Pakistan? That is. Can stocks hedge against Lockdown of Covid-19 and protects investors from loss. The fruitful answers will make two-fold contributions to the developing literature on Covid-19. First, it will contribute to the existing literature of Covid-19 in the scenario of Pakistan as this is the first study that covers both financial and non-financial industries of Pakistan as most of the studies are done for the US market (Goodell & Huynh, Citation2020; Sharif et al., Citation2020) and EU states (Mirza et al., Citation2020; Rizvi et al., Citation2020). Second, the event study analysis is employed for each industry, and conclusions will be made after considering the impact of Covid-19 on the individual industry of both sectors. The adequacy measures of the market model have also been accessed through various statistical diagnostic tests. The current study signifies and will be a valuable addition in enriching the literature of Covid-19 in the field of finance as it is the first study in the context of an emerging economy that took all the firms for analysis.

The rest of the paper is organized as follows. Section 2 describes a review of related literature, and section 3 explains the Methodology, and section 4 discusses the results, while section 5 concludes.

2. Literature review

Nowadays, voluminous literature is evolving around the globe related to the influence of Covid-19 on different economies. Some of the important contributions in this context are cited below. (Salisu & Akanni, Citation2020) constructed the global fear index (GFI) specified to the Covid-19 pandemic. They analyzed that the prediction of the stock return index could be made using this global fear index (GFI), having all the necessary parameters like deaths, recoveries, and reported cases (Umar et al., Citation2021). The OECD and BRICS nations were used to build the global fear index (GFI). It was concluded that at this hour of a pandemic, the global fear index (GFI) was a better predictor of panic in the stock market than the Index that is currently being used.

(Lyócsa et al., Citation2020) between fear of the virus and the stock market. The hypothesis was made that the higher the search volume related to pandemics, the more fear exists in the world population resulting in randomness in respective stock markets. The Heterogeneous Autoregressive (HAR) model of (Corsi, Citation2009) was deployed to fulfil the required goal. A strong correlation was found between price variation and the volume of google searches. The research concluded that numerous stock markets worldwide had lost a huge chunk of their value due to small investor fears about the pandemic. (Hauzenberger et al., Citation2020) used Bayesian Smooth-Transition Vector Autoregression (ST-VAR) to deduce the effect of conventional and non-conventional policies of the European central bank during the Covid-19 situation. Their results deduced that the quantitative easing measure had a higher effect in this uncertain time compared to the conventional monetary policy adopted by the European central bank. The study analyzed the effect of the Euro Area (EA) financial market data on the date of announcement of conventional and non-conventional policies implemented by the Central bank to overcome this situation. The high variation in the financial market was noted when the policies were passed (Su, Song, et al., Citation2021; Su et al., Citation2020). Due to the pandemic, shocks were observed in much short-term policy and multiple key financial quantities of Euro Area (EA).

(Conlon & McGee, Citation2020) highlighted the time-tested haven properties that are associated with Bitcoin. It is concluded that in the current scenario of the pandemic, a downward spiral of Bitcoin is observed along with the S&P 500 index at the time of crisis. The Methodology used for the analysis is downside risk measurement (Umar et al., Citation2021). Two-moment value is used to deduce the downside risk or the level of the tail. It has been observed from the analysis that there would be an increase in downside risk if the investor has invested in Bitcoin and the USA market. The study reveals that Bitcoin's maximum one-day loss was 66.49% compared to the S&P 500 index with 12.77%. (Shen et al., Citation2020) studied the performance of Chinese corporations in this Covid-19 situation. The research concluded that there was an impact on these industries regarding reduced total revenue, and investment scales also took a hit. A negative return rate was observed due to a decline in operations, production, and sales. The analysis indicates that the catering and accommodation industry was highly affected by the pandemic, with a net profit margin being −0.02. The strict quarantine measures declined production as well as consumption of products. Due to the decreasing sales revenue, the negative impact was faced by the corporations in China.

(Zubair et al., Citation2020) They investigated the finances of private firms in the Netherlands during the financial crisis. The authors found significant reductions in investment in small and medium-sized firms as compared to large firms. It was analyzed that there was a reduction in the investment of about 1.3% of total assets. Internal finance had much more effect on the private firm's investments than the firms' external finance during the pandemic time period. The standard investment model was used for these deductions (Umar, Ji, Kirikkaleli, Shahbaz, et al., Citation2020). Moreover, the study asserts that private Small and mid-size enterprise's (SMEs) future investments could be deduced by banks financing policies rather than the internal finance of the firm.

(Baig et al., Citation2021) analyzed multiple variables of the pandemic that affect the volatility and liquidity of the USA equity markets. They suggest that illiquidity and volatility increase as the number of deaths and patients of Covid-19 rises in the USA. Furthermore, it was also detected that Lockdown in the USA also harmed the stability and liquidity of the market while public fear also had a significant role in the instability of the market. (Primiceri & Tambalotti, Citation2020) analyzed the USA's macroeconomic variables, including a fall in employment rate and consumption. The result indicates that there has been a decline in the employment rate even after the virus was in a state of retreat (Su, Dai, et al., Citation2021). It is indicated that there would be more than a 20 percent decline in the employment rate before coming to a steady state in 2023. Vector Autoregression (VAR) is used to accomplish the goal of the study. Related to consumption, the result shows that as of July 2020, it would raise, but pre-Covid-19 days would not be accomplished. According to the authors, if the pandemic problem is solved faster, then there would be a speedy recovery expected in the economic system of the USA. The data is acquired assuming the virus would cease to exist until 2020, or the next wave would be faced in the fall or eliminated by the fall. All of these assumptions were made to deduce the effect of the virus for the next 3 years (Sun et al., Citation2021).

(Iyke, Citation2020) analyzed the reaction of gas and oil producers to the pandemic in the USA. Different results were acquired from the study as the pandemic was the reason for 27% of return volatility and 28% of returns. The estimates of the EGARCH (1,1) model were found qualitatively consistent when Covid-19 indicators were used. A total of 90 oil and gas producers were taken, and only 7 recorded positive returns, while the latter indicated a negative return in a pandemic. (Liu et al., Citation2020) used Time-Varying Parameter Vector Autoregression (TVP-VAR) model to analyze the interaction of Covid-19, stock market, and crude oil market in the USA (Su, Huang, et al., Citation2021). The result indicates that there is no correlation between the stock market and the crude oil market. It was inferred in the study that the pandemic has a positive effect on both stock returns and crude oil returns. Furthermore, it was suggested that these markets do not need a political bailout to strive in these pandemic conditions (Su et al., Citation2020). Authors observed impulse response among crude oil returns, stock market returns, and Covid-19, proving that their relationship is time-varying. According to the results, the basic economic theory cannot be applied as there is an overall positive impact of the virus on these markets.

(Narayan, Citation2020) investigated the influence of global oil price news and the Covid-19 pandemic on oil prices. It was observed that when the number of worldwide infected individuals reached 84,479, it has a maximum effect on oil prices. The oil news had a negligible effect on the price of oil. It has been observed by employing the threshold regression model that when the threshold is oil price volatility, both oil news and cases influenced the prices, and in this scenario, the dominating variable is negative oil price news (Su, Huang, et al., Citation2021).

(Gil-Alana & Monge, Citation2020) contributed to examine the effect of Covid-19 on crude oil prices by utilizing the long memory techniques. Fractional integration techniques were applied to the data, and the result suggested that the hypothesis was accurate if the sample ended in 20-01-2020. When the data of the pandemic phase was considered, the order of integration was 0.84, which implies that there is a mean-reverting phenomenon in the oil price series. Thus, it is indicating that oil price shocks are temporary but would have a long-lasting effect (Su, Huang, et al., Citation2021). (S. R. Baker et al., Citation2020) use a text-based method to determine the effect of the entire pandemics from the 1900s until now on the USA's stock market. These included pandemics like the Spanish Flu, influenza pandemics, etc., that Killed many individuals in the USA. The study determined that Covid-19 had such a massive impact on stocks while the last pandemic did not affect much.

To find the effect of social distancing and the government's intervention in Covid-19, (Farboodi et al., Citation2020) constructed a model to compare external targets with data like fatalities, social activity, and Reproduction number R (t). It was deduced that the Government social distance policy did not have that much effect as the Reproduction equilibrium was above 1 before and after the government's policy. The study further realized that the policy did reduce the cost of the Covid-19 from $12,700 to $8,100 per person. Thus, large welfare gain was achieved by the government's policy. (Hassan et al., Citation2020) analyzed the USA's role in how different firms' sentiment, exposure, and risk are affected by the pandemic of Covid-19. It was found that, unlike other pandemics, Covid-19 affected all the firms (Su, Dai, et al., Citation2021; Umar, Ji, Kirikkaleli, & Xu, Citation2020). It created uncertainty, and the firm's business outlook went on a downward spiral. It was highlighted that many Tech-based firms found a way to get benefits from this pandemic while the transportation sector suffered losses. It was also deduced that, as in other pandemic cases, shock from demand was observed, while in Covid-19, both demand and supply observed shocks(Su, Dai, et al., Citation2021; Su, Huang, et al., Citation2021).

(Ling et al., Citation2020) examined the transmission of shocks from the asset markets to capital markets. The impact on commercial real estate (CRE) was observed with the increase in cases of Covid-19 geographically (GeoCovid). The result showed that there is a negative relationship between GeoCovid and abnormal returns. At the same time, a positive correlation was seen between health care and technology sectors with GeoCovid. The study also concluded that lifting policies like social distancing did not affect the stock's performance. (Papanikolaou & Schmidt, Citation2020) Investigates worldwide the effect of Covid-19 on the supply side of workers and firms and the ability of workers to do their work remotely. It was evident that the firms in which the majority of the workers could not work remotely experienced a decline in revenue growth, their stock market took a hit, and a decline in employment was observed. When it comes to individual employment, low-paid workers and women with small children were highly affected by the pandemic.

(Phan & Narayan, Citation2020) inspect the effect of Covid-19 on stock prices of 25 economies and test the hypothesis that unpredicted information can cause havoc in the market, and as the news becomes more acknowledged by the individuals, the market becomes more stable. They examined the adverse response of different countries to this pandemic in terms of their policies adopted and actions taken (Su, Dai, et al., Citation2021; Umar, Ji, Kirikkaleli, & Xu, Citation2020). They investigated 25 countries that were more affected by the pandemic. To analyze the pattern, time-series data was used to determine the pattern between stock prices and government policies. They concluded that there was a downward spiral in the stock market of most of these countries in the early period, but the market correction was observed in almost half of the market when most of the countries reached 100 deaths and 100,000 infections. (Al-Awadhi et al., Citation2020) explored the effect of the pandemic on the Chinese stock market. Panel data methodology is chosen to determine the effect of the market. The Shanghai Stock Exchange and Hang Seng Index data and positive cases were used for this analysis. The time frame was spanning from January 10, 2020, to March 16, 2020. It was found that the Chinese stock holds a negative impact when the number of infected people and casualties increases in China (Umar et al., Citation2021).

Focusing on the time before and after the Lockdown in Covid-19, (Alam et al., Citation2020) analyzed the situation of the Indian stock market. To determine the effect, Event study methodology is applied. The data used consists of 3831 companies enlisted in the Bombay Stock Exchange (BSE). The timestamp for this data consists of 35 days, 20 days before the event, and 15 days after. T1 is taken as the time when the event took place. The average Abnormal Returns (AAR) of the data during the lockdown period is remarkably positive compared to AAR before the Lockdown took place, as there was pain among the investors. The study shows that the market performed in positively during the Lockdown and gives positive Abnormal Returns. (Polemis & Soursou, Citation2020) studied the relationship between the Greek energy firms and the Covid-19 pandemic. For this purpose, they took 11 listed Greek energy companies as a sample. The time taken is 10 days pre-lockdown and 10 days post-lockdown in Greek held on (23/3/2020). The market model approach is used to examine the abnormal returns of energy firms (Umar et al., Citation2021). The deduction is made by these firms' 'closing prices' from the Athens Stock Exchange (ASE). The results reveal that there would not be long-term divergence, and the market would try to return to its usual equilibrium. The study concluded that there was a downward spiral in terms of negative abnormal returns before the announcement was made and during the event window.

The above literature highlights the importance of studying the influence of Covid-19 on several economies. It has been observed that many of the studies have been done for developed countries. Thus this study contributes to the emerging country as new investment avenues can be opened.

3. Methodology

Since the seminal work of ( H. K. Baker & Gallagher, Citation1980; S. R. Baker et al., Citation2020; Dolley, Citation1933; Myers & Bakay, Citation1948 ), event study analysis gained popularity in the literature of economic and finance. Nowadays, the event study methodology used mainly followed the approach of (Brown & Warner, Citation1980; Fama et al., Citation1969) in the scenario of firm-specific, economic, and non-economic shocks, political happenings, global financial crisis, and more recently, a pandemic of Covid-19, etc. Particularly firm-specific events are earning announcements (Ball & Brown, Citation1968; Fama, Citation1991; Iqbal, Citation2012; MacKinlay, Citation1997), Political aspect of event study in terms of nuclear detonation has been highlighted by (Javed & Ahmed, Citation1999), non-economic shocks such as effect on Australian stock market has been explored by (Berman et al., Citation2000) as Sydney will going to host Olympic Games in the year 2000, the announcement of epidemics taken into consideration by (Chen et al., Citation2007; Donadelli et al., Citation2017). Specifically, for Covid-19 (Alam et al., Citation2020; Pandey & Kumari, Citation2021; Polemis & Soursou, Citation2020), etc., are note-worthy. More recently, the European investment funds price reaction against Covid-19 has been explored by (Mirza et al., Citation2020) through event study analysis under the framework of GARCH.

3.1. Event window

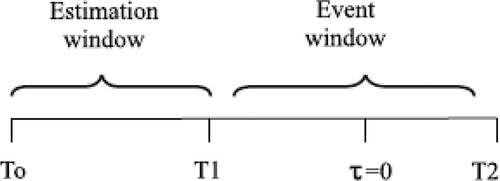

The selection of time period in event study analysis is of important concern. This study followed the timeline proposed by (Polemis & Soursou, Citation2020) for Greek energy firms consisting of ten, twenty, and fifty days event window, while due to homogenous impact, two timelines will be discussed. In Pakistan, news related to lockdown was circulated on March 18, 2020; thus, we took the news date as an event day, i.e., Various time windows have been taken to access the real and long-term impact of Covid-19 on financial and non-financial firms of Pakistan. Thus we use a time window of before and after 10 days [-10. +10] and the second is before and after 20 days [-20, +20] .In this context, the estimation period varies according to the selected window period.

depicts the timeline of Event study in which Event window and Estimation window has been explained. The whole sample spanning from till

divided into event and estimation window, respectively. The estimation and event window must be non-overlapping. The event window cannot be used to estimate the market model. The data frequency of this study ranges from December 12, 2019, till June 7, 2020, indicating

is December 12, 2019,

is January 6, 2020, and

June 4, 2020. For 21 days of the event window, the data ranges from March 4, 2020, to April 2, 2020. For the 41 days window, data is spanning from February 19, 2020, to April 16, 2020.

Figure 1. Timeline of event study.

Source: Authors Estimation.

3.2. Market model

The main purpose of event study analysis is to observe the abnormal changes in the prices/returns of stocks after any specific event (Umar et al., Citation2021). The regression-based models used to estimate abnormal returns are the average adjusted return rate model, the market index adjusted return rate model, and the market model. Out of the three, the market model is widely used (Huang et al., Citation2020) due to its good predictive property (Brenner, Citation1979), and its efficacy towards efficient market hypothesis (Polemis & Soursou, Citation2020) makes this model more beneficial. Therefore this study employs the following market model from the estimation window to estimate the abnormal returns for the event window;

(1)

(1)

Where the dependent variable represents the continuously compounded market returns, i.e., KSE-100 index, an explanatory variable

are the continuously compounded returns of

firm at time t belongs to the respective sector. The error term is the zero mean and homoscedastic residual term while

and

are intercept and slope of the model, respectively. The error term of the model (1) imitates the price response of the company owing to the event under consideration and follows the standard regression assumptions. The market model regression is only employed in the estimation window, and their estimates will utilize to obtain the abnormal returns;

(2)

(2)

The following hypothesis will be tested to observe the abnormal reaction of firms concerning the event;

There are significant positive abnormal returns Abnormal returns around the event date, i.e., Lockdown announcement date, and it is significantly greater than zero.

There are significant negative abnormal returns Abnormal returns around the event date, i.e., Lockdown announcement data, and it is significantly less than zero.

The abnormal returns are then averaged across the company;

(3)

(3)

The average abnormal returns will then use to calculate Cumulative abnormal returns for each firm c as;

(4)

(4)

3.3. Diagnostic tests of market model regression

The diagnostic and stability tests have been applied to assess the specification and adequacy of the market model estimated for the estimation window. Following are the tests utilized in this study;

3.4. Jarque-Bera (J-B) test

The Jarque-Bera test is used to test whether the residuals of the market model follow a normal distribution or not. This study reports the average test statistic and p-value for each sector and all sectors. The percentage of firms that rejected the test's null hypothesis individually has also been reported in the study. The following hypothesis has been tested for the J-B test;

Residuals of market model follow Normal distribution

Residuals of market model do not follow Normal distribution

The Test Statistic used for the J-B Test is calibrated as follows;

K is the number of estimated parameters in the market model. In our case, it is 2, S is the skewness, and k is the kurtosis.

The small p-value leading leads the test towards rejection of the null hypothesis.

3.5. White's heteroskedasticity (1980) test

The White test belongs to the family of heteroskedasticity tests, and White developed it in 1980. It is used to observe that whether the errors follow common variance or not. The test statistic is obtained by estimating the auxiliary regression of the market model consisting of square terms of the independent variable. The study reports the average test statistic and p-value for each firm and all industries. Following is the hypothesis that needs to be tested in the White test;

Residuals of market model possess common variance (No Heteroskedasticity)

Residuals of market model do not possess common variance (Heteroskedasticity of some unknown general form)

The test statistics can be written as;

Where k is the number of variables in auxiliary regression, in this case, k = 2

3.6. Bruche Godfrey (BG) LM test

The full name of this test is Bruche Godfrey (BG) Lagrange Multiplier Test and is used to test the serial correlation in the errors of the market model. The test statistic is obtained by estimating the auxiliary regression of lag order p for the market model consisting of square terms of the independent variable. The study reports the average test statistic and p-value for each firm and all industries, including the percentage of rejection for the null hypothesis. Following is the hypothesis needs to be tested i

Residuals of market model possess no serial correlation up to lag p

Residuals of market model possess serial correlation up to lag p

The test statistics can be written as;

Where k is the degrees of freedom, i.e., lag p, this study used the lag order of 2.

3.7. Ramsey RESET test

The RESET test is used concerning specification issues, i.e., omitted variable or incorrect functional form of the market model. It stands for Regression Specification Error Test, and it was developed by (Ramsey, Citation1969). The study reports the average test statistic and p-value for each firm and all industries, including the percentage of rejection for the null hypothesis. Following is the hypothesis that needs to be tested;

Coefficients on the powers of fitted values are all zero

Coefficients on the powers of fitted values are all not zero

The test statistic of the RESET test is -a log-likelihood ratio.

4. Results and discussion

displays the results of estimates of abnormal returns computed for each firm and then aggregated for each industry. Keeping in view the pandemic situation, it has been observed that the response of financial and non-financial sectors is almost similar towards the announcement of Lockdown in Pakistan on average. The influence on the firms behaves differently concerning the length of pandemic and announcement of Lockdown. As in the [-10,+10] event window, on average, the financial sector suffered −7.4% cumulative average abnormal returns on event day while the financial sector loses −7.3%. The market's reaction started two days before the announcement and produced negative abnormal returns, whereas, at +7 day, the market got stable and continued to progress till +10 days. These results are consistent with (Waheed et al., Citation2020) as they showed that the Pakistan market behaves differently in Covid-19 due to the smart strategies implemented by the Government. Overall, both sectors maintain their position in terms of returns which is dissimilar to the results obtained by (Al-Awadhi et al., Citation2020)for the Chinese market. It has also been noted that the financial sector holds negative returns before the fourth day of the announcement, and it continued after one day of the announcement; meanwhile, the non-financial sector possessed a negative attitude before two days of the announcement, and just after day it becomes positive. Inclusively the abnormal returns are mutually exclusive for both sectors as significant positive effects have been seen for several days than negative significance. In early March 2020, compensation was provided by the IMF regarding loan payments and the sufficient relief package of $1.4 Billion that stabilize the economic situation.

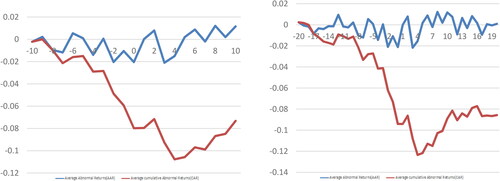

The graph has been plotted with the timeline to see the clearer scenario of Average abnormal Returns and Cumulative Average abnormal returns. The left panel of presents 21 days window, and the right panel has been drawn for 41 days window. The curve pattern is somehow similar for both timelines as the magnitude of Covid-19 is not affected the returns. It has been evident from the figure that various CAAR is negative after the announcement of Lockdown. The pattern gradually declines towards the negative returns while these returns are statistically insignificant in terms of influence ().

Figure 2. AAR and CAAR for lockdown announcements (Non-financial sector).

Source: Authors Estimation.

Table 1. Average Abnormal Returns (AAR) and Cumulative Average Abnormal Returns (CAAR) of financial and non-financial sector for [−10, +10] (March 2, 2020-April 2, 2020).

Furthermore, on average AAR seems to be positive throughout the time line except on the event day and few of the next days.

portrayed the results of abnormal returns and their significance at a 5% level for financial and non-financial sectors. These abnormal returns have been computed for 41 days window. On event day, the cumulative average abnormal return is −9.7% and 9.6% for non-financial and financial companies, respectively, while the return is insignificant. In the long horizon, significant positive effects are more than the negative sign. As indicated by (Xu, Citation2020), the cost of capital increases due to the shrinkage of investors in uncertain situations; thus, Pakistan took bold decisions to save the investors, especially associated with small and construction industries. The benefits provided by Government during the Lockdown such as reduction in electricity and gas bills to small industries, Relief packages for daily wages labors, tax relief to different SME's, raised the status of the construction sector into the industry, and remotely distributed food among the suburban, etc. is reflecting through the positive response of stocks for both sectors. These findings are also in line with the market efficiency as deviation from the long-run equilibrium resolves quickly, and the market is informationally efficient.

Table 2. Average Abnormal Returns (AAR) and Cumulative Average Abnormal Returns (CAAR) of financial and non-financial sector for [−20, +20] (February 19, 2020–April 16, 2020).

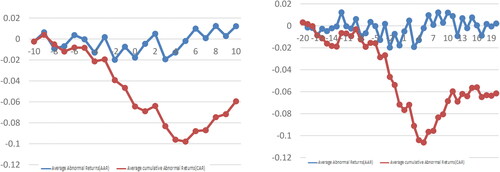

is depicting the AAR and CAAR for financial sectors. The left panel is for the [-10, +10], and the right panel presents [-20, +20] timelines. Since several Abnormal Average returns possessed negative signs, but the effect is negligible, most of them are insignificant. Moreover, the behaviour is looking similar in both time windows. The reaction of the financial sector toward the announcement date is similar to the non-financial sector as various incentives have also been provided to the financial sector during the Lockdown, such as lowering the markup rate for active taxpayers from 4% to 3%, easy business loan facility announced for small businessman and instructed banks and DFI's to suspend their dividend declaration for first quarter till the second. Thus smart strategies implemented by the Government of Pakistan that have also been praised worldwide are sparkling in the retrieved results of this study.

Figure 3. AAR and CAAR for lockdown announcements (financial sector).

Source: Authors Estimation.

The market model adequacy was then accessed through various diagnostic measures. reports the aggregated test statistic and p-values for individual firms and all industries. The percentage of rejection of null hypothesis for each test and each firm has been computed and also displayed in . Overall the residuals of the market model follow a normal distribution as most of the industries have 0% rejection of null hypothesis in the J-B test. The problem of serial correlation (BG-LM Serial Correlation) and heteroscedasticity (White heteroskedasticity test) is also not evident in the model, while the model is also specified correctly for most industries RESET test.

Table 3. Diagnostic test on market model regression (non-financial sector).

5. Conclusion and policy implication

The study investigated the influence of the announcement of Lockdown due to Covid-19 on the emerging nation of Pakistan. Covid-19 has been accessed for various developed countries, and negative influence has been found, but emerging economies like Pakistan respond differently and achieve good returns in the market. The financial and non-financial firms listed in the Pakistan Stock Exchange (PSX) have been taken to observe the announcement's impact. The abnormal returns were computed for each firm and aggregated for each industry by utilizing the market model regression.

On average, cumulative abnormal returns possessed negative patterns before and after the Lockdown date announcement, while the significance of abnormal returns for both the timelines shows a positive sign for both the sectors that support the efficient market hypothesis. Overall the reaction of both the sectors is satisfactory around the announcement date as the emerging market is more liquid than developed markets. The results are not generalized for other countries as the smart strategies implemented by Pakistan are unique from other countries.

The present study results cannot be generalized as it has only been done for a single country. Since the pandemic response behaves differently and varies from country to country, the consequences of the crisis are also not uniform. However, the current research results are essential for investors as diversified portfolios are always the source of attraction for stockholders. In the pandemic, the investment opportunity shines in Pakistan as the economy's recovery is quick. The construction industry is flourishing in pandemic due to the smart strategies of government while Banks and other financial institutions are also growing exponentially. The research can be further extended for other emerging countries and the application of more sophisticated statistical methodologies to facilitate investors around the globe.

Disclosure statement

No potential conflict of interest was reported by the authors.

Correction Statement

This article has been republished with minor changes. These changes do not impact the academic content of the article.

Additional information

Funding

References

- Abid, K., Bari, Y. A., Younas, M., Tahir Javaid, S., & Imran, A. (2020). <? Covid19?> Progress of COVID-19 Epidemic in Pakistan. Asia-Pacific Journal of Public Health, 32(4), 154–156. https://doi.org/10.1177/1010539520927259

- Alam, M. N., Alam, M. S., & Chavali, K. (2020). Stock market response during COVID-19 lockdown period in India: An event study. The Journal of Asian Finance, Economics and Business, 7(7), 131–137. https://doi.org/10.13106/jafeb.2020.vol7.no7.131

- Al-Awadhi, A. M., Alsaifi, K., Al-Awadhi, A., & Alhammadi, S. (2020). Death and contagious infectious diseases: Impact of the COVID-19 virus on stock market returns. Journal of Behavioral and Experimental Finance, 27, 100326. https://doi.org/10.1016/j.jbef.2020.100326

- Baig, A. S., Butt, H. A., Haroon, O., & Rizvi, S. A. R. (2021). Deaths, panic, lockdowns and US equity markets: The case of COVID-19 pandemic. Finance Research Letters, 38, 101701. https://doi.org/10.1016/j.frl.2020.101701

- Baker, S. R., Bloom, N., Davis, S. J., Kost, K., Sammon, M., & Viratyosin, T. (2020). The unprecedented stock market reaction to COVID-19. The Review of Asset Pricing Studies, 10(4), 742–758. https://doi.org/10.1093/rapstu/raaa008

- Baker, H. K., & Gallagher, P. L. (1980). Management’s view of stock splits. Financial Management, 9(2), 73–77. https://doi.org/10.2307/3665171

- Ball, R., & Brown, P. (1968). An empirical evaluation of accounting income numbers. Journal of Accounting Research, 6(2), 159–178. https://doi.org/10.2307/2490232

- Berman, G., Brooks, R., & Davidson, S. (2000). The Sydney Olympic Games announcement and Australian stock market reaction. Applied Economics Letters, 7(12), 781–784. https://doi.org/10.1080/135048500444796

- Brenner, M. (1979). The sensitivity of the efficient market hypothesis to alternative specifications of the market model. The Journal of Finance, 34(4), 915–929. https://doi.org/10.1111/j.1540-6261.1979.tb03444.x

- Brown, S. J., & Warner, J. B. (1980). Measuring security price performance. Journal of Financial Economics, 8(3), 205–258. https://doi.org/10.1016/0304-405X(80)90002-1

- Chen, M.-H., Jang, S. S., & Kim, W. G. (2007). The impact of the SARS outbreak on Taiwanese hotel stock performance: An event-study approach. International Journal of Hospitality Management, 26(1), 200–212. https://doi.org/10.1016/j.ijhm.2005.11.004

- Conlon, T., & McGee, R. (2020). Safe haven or risky hazard? Bitcoin during the COVID-19 bear market. Finance Research Letters, 35, 101607. https://doi.org/10.1016/j.frl.2020.101607

- Corsi, F. (2009). A simple approximate long-memory model of realized volatility. Journal of Financial Econometrics, 7(2), 174–196. https://doi.org/10.1093/jjfinec/nbp001

- Dolley, J. C. (1933). Characteristics and procedure of common stock split-ups. Harvard Business Review, 11(3), 316–326.

- Donadelli, M., Kizys, R., & Riedel, M. (2017). Dangerous infectious diseases: Bad news for Main Street, good news for Wall Street? Journal of Financial Markets, 35, 84–103. https://doi.org/10.1016/j.finmar.2016.12.003

- Fama, E. F. (1991). Time, salary, and incentive payoffs in labor contracts. Journal of Labor Economics, 9(1), 25–44. https://doi.org/10.1086/298257

- Fama, E. F., Fisher, L., Jensen, M. C., & Roll, R. (1969). The adjustment of stock prices to new information. International Economic Review, 10(1), 1–21. https://doi.org/10.2307/2525569

- Farboodi, M., Jarosch, G., & Shimer, R. (2020). Internal and external effects of social distancing in a pandemic. National Bureau of Economic Research.

- Gao, X., Ren, Y., & Umar, M. (2021). To what extent does COVID-19 drive stock market volatility? A comparison between the U.S. and China. Economic Research-Ekonomska Istraživanja, 1–21. https://doi.org/10.1080/1331677X.2021.1906730

- Gil-Alana, L. A., & Monge, M. (2020). Crude oil prices and COVID-19: Persistence of the shock. Energy Research Letters, 1(1), 13200.

- Goodell, J. W., & Huynh, T. L. D. (2020). Did Congress trade ahead? Considering the reaction of US industries to COVID-19. Finance Research Letters, 36, 101578. https://doi.org/10.1016/j.frl.2020.101578

- Hassan, T. A., Hollander, S., Van Lent, L., Schwedeler, M., & Tahoun, A. (2020). Firm-level exposure to epidemic diseases: Covid-19, SARS, and H1N1. National Bureau of Economic Research.

- Hauzenberger, N., Pfarrhofer, M., & Stelzer, A. (2020). On the effectiveness of the European Central Bank’s conventional and unconventional policies under uncertainty. ArXiv Preprint ArXiv:2011.14424.

- Huang, S.-Z., Chau, K. Y., Chien, F., & Shen, H. (2020). The Impact of startups’ dual learning on their green innovation capability: The effects of business executives’ environmental awareness and environmental regulations. Sustainability, 12(16), 6526. https://doi.org/10.3390/su12166526

- Iqbal, J. (2012). Stock market in Pakistan: An overview. Journal of Emerging Market Finance, 11(1), 61–91. https://doi.org/10.1177/097265271101100103

- Iyke, B. N. (2020). COVID-19: The reaction of US oil and gas producers to the pandemic. Energy Research Letters, 1(2), 13912.

- Javed, A. Y., & Ahmed, A. (1999). The response of Karachi stock exchange to nuclear detonation. The Pakistan Development Review, 38(4II), 777–786. https://doi.org/10.30541/v38i4IIpp.777-786

- Ling, D. C., Wang, C., & Zhou, T. (2020). A first look at the impact of COVID-19 on commercial real estate prices: Asset-level evidence. The Review of Asset Pricing Studies, 10(4), 669–704. https://doi.org/10.1093/rapstu/raaa014

- Liu, L., Wang, E.-Z., & Lee, C.-C. (2020). Impact of the COVID-19 pandemic on the crude oil and stock markets in the US: A time-varying analysis. Energy Research Letters, 1(1), 13154.

- Lyócsa, Š., Baumöhl, E., Výrost, T., & Molnár, P. (2020). Fear of the coronavirus and the stock markets. Finance Research Letters, 36, 101735. https://doi.org/10.1016/j.frl.2020.101735

- MacKinlay, A. C. (1997). Event studies in economics and finance. Journal of Economic Literature, 35(1), 13–39.

- Mirza, N., Hasnaoui, J. A., Naqvi, B., & Rizvi, S. K. A. (2020). The impact of human capital efficiency on Latin American mutual funds during Covid-19 outbreak. Swiss Journal of Economics and Statistics, 156(1), 1–7. https://doi.org/10.1186/s41937-020-00066-6

- Myers, J. H., & Bakay, A. J. (1948). Influence of stock split-ups on market price. Harvard Business Review, 26(2), 251–255.

- Narayan, P. K. (2020). Oil price news and COVID-19—Is there any connection? Energy Research Letters, 1(1), 13176.

- Pandey, D. K., & Kumari, V. (2021). Event study on the reaction of the developed and emerging stock markets to the 2019-nCoV outbreak. International Review of Economics & Finance, 71, 467–483. https://doi.org/10.1016/j.iref.2020.09.014

- Papanikolaou, D., & Schmidt, L. D. (2020). Working remotely and the supply-side impact of COVID-19. National Bureau of Economic Research.

- Phan, D. H. B., & Narayan, P. K. (2020). Country responses and the reaction of the stock market to COVID-19—A preliminary exposition. Emerging Markets Finance and Trade, 56(10), 2138–2150. https://doi.org/10.1080/1540496X.2020.1784719

- Polemis, M., & Soursou, S. (2020). Assessing the impact of the COVID-19 pandemic on the Greek energy firms: An event study analysis. Energy Research Letters, 1(3), 17238.

- Primiceri, G. E., & Tambalotti, A. (2020). Macroeconomic Forecasting in the Time of COVID-19. Manuscript, Northwestern University.

- Ramsey, J. B. (1969). Tests for specification errors in classical linear least‐squares regression analysis. Journal of the Royal Statistical Society: Series B (Methodological), 31(2), 350–371.

- Rizvi, S. K. A., Mirza, N., Naqvi, B., & Rahat, B. (2020). Covid-19 and asset management in EU: A preliminary assessment of performance and investment styles. Journal of Asset Management, 21(4), 281–291. https://doi.org/10.1057/s41260-020-00172-3

- Salisu, A. A., & Akanni, L. O. (2020). Constructing a global fear index for the COVID-19 pandemic. Emerging Markets Finance and Trade, 56(10), 2310–2331. https://doi.org/10.1080/1540496X.2020.1785424

- Sharif, A., Aloui, C., & Yarovaya, L. (2020). COVID-19 pandemic, oil prices, stock market, geopolitical risk and policy uncertainty nexus in the US economy: Fresh evidence from the wavelet-based approach. International Review of Financial Analysis, 70, 101496. https://doi.org/10.1016/j.irfa.2020.101496

- Shen, H., Fu, M., Pan, H., Yu, Z., & Chen, Y. (2020). The impact of the COVID-19 pandemic on firm performance. Emerging Markets Finance and Trade, 56(10), 2213–2230. https://doi.org/10.1080/1540496X.2020.1785863

- Su, C.-W., Dai, K., Ullah, S., & Andlib, Z. (2021). COVID-19 pandemic and unemployment dynamics in European economies. Economic Research-Ekonomska Istraživanja, 1–13. https://doi.org/10.1080/1331677X.2021.1912627

- Su, C.-W., Huang, S.-W., Qin, M., & Umar, M. (2021). Does crude oil price stimulate economic policy uncertainty in BRICS? Pacific-Basin Finance Journal, 66, 101519. https://doi.org/10.1016/j.pacfin.2021.101519

- Sun, T.-T., Tao, R., Su, C.-W., & Umar, M. (2021). How Do Economic Fluctuations Affect the Mortality of Infectious Diseases? Front Public Health, 9, 678213 https://doi.org/10.3389/fpubh.2021.678213

- Su, C.-W., Qin, M., Tao, R., & Umar, M. (2020). Financial implications of fourth industrial revolution: Can bitcoin improve prospects of energy investment? Technological Forecasting and Social Change, 158, 120178 https://doi.org/10.1016/j.techfore.2020.120178

- Su, C.-W., Song, Y., & Umar, M. (2021). Financial aspects of marine economic growth: From the perspective of coastal provinces and regions in China. Ocean & Coastal Management, 204, 105550. https://doi.org/10.1016/j.ocecoaman.2021.105550

- Su, C.-W., Sun, T., Ahmad, S., & Mirza, N. (2021). Does institutional quality and remittances inflow crowd-in private investment to avoid Dutch Disease? A case for emerging seven (E7) economies. Resources Policy, 72, 102111. https://doi.org/10.1016/j.resourpol.2021.102111

- Umar, M., Ji, X., Kirikkaleli, D., Shahbaz, M., & Zhou, X. (2020). Environmental cost of natural resources utilization and economic growth: Can China shift some burden through globalization for sustainable development? Sustainable Development, 28(6), 1678–1688. https://doi.org/10.1002/sd.2116

- Umar, M., Ji, X., Kirikkaleli, D., & Xu, Q. (2020). COP21 Roadmap: Do innovation, financial development, and transportation infrastructure matter for environmental sustainability in China? J Environ Manage, 271, 111026 https://doi.org/10.1016/j.jenvman.2020.111026

- Umar, M., Mirza, N., Rizvi, S. K. A., & Furqan, M. (2021). Asymmetric volatility structure of equity returns: Evidence from an emerging market. The Quarterly Review of Economics and Finance, https://doi.org/10.1016/j.qref.2021.04.016

- Waheed, R., Sarwar, S., Sarwar, S., & Khan, M. K. (2020). The impact of COVID‐19 on Karachi stock exchange: Quantile‐on‐quantile approach using secondary and predicted data. Journal of Public Affairs, 20(4), e2290.

- Xu, Z. (2020). Economic policy uncertainty, cost of capital, and corporate innovation. Journal of Banking & Finance, 111, 105698. https://doi.org/10.1016/j.jbankfin.2019.105698

- Yarovaya, L., Brzeszczynski, J., Goodell, J. W., Lucey, B. M., & Lau, C. K. (2020). Rethinking Financial Contagion: Information Transmission Mechanism during the COVID-19 pandemic. Available at SSRN 3602973.

- Zubair, S., Kabir, R., & Huang, X. (2020). Does the financial crisis change the effect of financing on investment? Evidence from private SMEs. Journal of Business Research, 110, 456–463. https://doi.org/10.1016/j.jbusres.2020.01.063