?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The current study aims to explore the role of environmental taxes and regulations for the renewable energy consumption, focusing on reporting policy suggestions to overcome climate change issues and achieve environmental sustainability. The main objective of this paper is to examine the relation between renewable energy, environmental taxes, environmental technologies, and environmental regulations in 29 OECD countries during 1996–2018. More precisely, we inspect the impact of the environmental regulations and environmental technologies on the renewable energy consumption. The authors employ CIPS and CADF unit root tests, panel Westerlund co-integration test, FMOLS, and Quantile regression methods for the econometric analysis. The econometric analysis suggests that the environmental regulations impede the renewable energy consumption in OECD economies. The study suggests that environmental policy initiatives should focus on implementing environmental strategies to inspire cohesiveness between environmental regulations and the development of environmental technologies in order to promote the renewables industry in the developed countries.

1. Introduction

Global climate change has presented some unprecedented challenges such as extreme weather conditions, extinction of species, and scarcity of food to humanity. After the industrial revolution, large amounts of polluting gases, producing the so called greenhouse effect, were released into the atmosphere. It is assumed that is affected by various factors of economic activity (Lapinskienė et al., Citation2017). Researchers proved that not only country and regional socioeconomic development and energy consumption are highly affected by the environmental issues, but also the entire environmental tax system is impacted by different socioeconomic factors (Vasylieva et al., Citation2020); there is a tight interdependence among them.

In order to overcome these environmental and climate challenges, the Paris Climate Agreement (COP21) was signed by 195 countries to limit global temperature rise below 2 °C (Ahmad et al., Citation2019; Azam et al., Citation2021). It is necessary to understand the determinants of the environmental degradation to formulate effective environmental policies (Farooq et al., Citation2019; Khoshnevis Yazdi & Dariani, Citation2019; Wu et al., Citation2019). Furthermore, to overcome these challenges, one of the most debatable issues is the introduction of environmental taxesFootnote1 and environment-related technologies and their subsequent impact on renewable energy demand, which is increasingly becoming popular as it is a less carbon-intensive and sustainable energy source. The OECD countries currently account for 63% of world GDP (measured in constant 2010 US dollars) and are responsible for 80% of the world trade; consequently, the member countries collaborate at regional, national, and local levels (Gygli et al., Citation2019). Therefore, it is no surprise that 12 of the top 20 carbon emitters belong to OECD, where the USA, Japan, and South Korea are responsible for 15%, 3%, and 2.2% of global carbon emission, respectively (Shahzad, Citation2020). OECD's per capita energy use (4145.046 kilograms of oil equivalent) and per capita generation of CO2 emissions (9.534 metric tons) are much higher compared to world's average per capita energy use (1920.58) and per capita generation of CO2 emissions (4.970) (Shahzad, Citation2020). Against this backdrop of the environmental degradation, the OECD countries have paid a significant attention in promoting the environmental research and development. Indeed, the USA, Japan, and Germany are ranked first, third, and fourth with 581, 193, and 123 US$billion funding towards green R&D investments in 2019 alone (Petrović & Lobanov, Citation2020). As renewable energy negatively impacts on the environmental pollution while relying on the environmental scientific innovation, this analysis aiming to explore the association between the renewable energy, environmental taxes, environmental patents, and expenditures could be of great interest, especially for the case of the industrial economies such as OECD.

Due to the acceptance of renewable energy in preventing the environmental degradation, OECD economies have implemented several policy initiatives to promote energy efficiency and renewable energy by increasing the share of renewable energy consumption into the energy mix. A special attention has been given to introducing biofuels in order to improve the renewable energy consumption; also, some policy initiatives as tax credits were introduced to increase investments in energy-efficient technologies. These policy changes have brought significant results, as the share of renewable energy consumption in the energy mix has almost doubled, and it is expected to increase further. Additionally, OECD members Germany, Sweden, Finland, France, and the UK, among others, have set aggressive goals to promote further renewable energy consumption (Erdogan et al., Citation2020). Currently, the energy mix of the OECD group consists of petroleum (35.4%), natural gas (25.4%), solid fossil fuel (19%), nuclear energy (10.2%), and renewable energy (10%) (Ozcan et al., Citation2020).

As for the association between the environmental regulations and renewable energy consumption, the existing literature can be divided into two major themes. The first opinion is that environmental regulations promote renewable energy consumption, as the environmental regulations influence businesses and the general public to adopt renewable energy as an energy source (Bae & Yu, Citation2018; Hille et al., Citation2020). The second point of view is that environmental regulation impedes renewable energy consumption (Hájek et al., Citation2019). One possible explanation is that the introduction of the market-based instruments to support the environmental regulations is critical in creating a positive association between the renewable energy and technological innovation.

Furthermore, the high intellectual property rights costs and restriction of technological transmission also impede the renewable energy use (Cheng et al., Citation2019). Most researchers agree that the economic literature about renewable energy has to overcome these inconsistent findings. One possible explanation is that different researchers have used different proxies for environmental regulations (Shahzad et al., Citation2020; Shahzad, Doğan et al., Citation2021). Another justification is that the existing literature has failed to consider the detailed classification of the environmental regulations on the renewable energy consumption; hence, they have provided some general conclusions and not specific policy recommendations. Several studies have suggested that different proxies of the environmental regulations tend to influence differently (Montero, Citation2002; Ren et al., Citation2018; Requate & Unold, Citation2003). Hence, it is essential to investigate the environmental regulation proxies and their collective effect on creating demand for the renewable energy consumption. Besides, it is also critical to investigate how different environmental regulations impact on the economic growth in OECD economies. The environmental management policy system in OECD is categorized as regional, where the domestic governments are the primary conductors to design and implement environmental regulations (Lei et al., Citation2017). So, the economic and financial behavior will affect the implementation of such protocols, i.e., lower marketization could force domestic governments to intervene to protect the economic growth targets (Khan et al., Citation2019). Therefore, the economic and market conditions significantly influence the impact of the environmental regulations.

The main objective of our research is to analyze the association between the environmental tax and renewable energy consumption in OECD economies; also, we go further with the discussion towards the role of innovation in the environmental technologies area, environmental stringency index,Footnote2 and environmental expendituresFootnote3 in promoting clean energy sources. Existing literature has proven that the renewable energy is critical in mitigating climate change as an alternative solution against the existing energy policies, which are heavily dependent on the fossil fuels. Furthermore, the existing economic models pose some serious environmental and health issues and are also the biggest contributors to GHG emissions. Transition to the renewable energy sources will make a significant progress towards the environmental goals set under Paris Climate Agreement, but the failure to introduce policy mechanisms in OECD countries in order to promote the renewable energy will seriously impede SDGs (SDG-13: Climate Action; SDG-11: Sustainable Cities and Communities; SDG-7: Affordable and clean energy). Keeping in mind the above-mentioned discussion, the current study makes the following research contributions: Firstly, in order to overcome the issue of the lack of studies concerning the role of environmental regulations towards a sustainable energy system, the current study attempts to investigate how the environmental regulations and policies affect green energy sources as the development of the sustainable energy system allows the economic development without environmental degradation. Secondly, the present research covers the research gap by studying several environmental and economic indicators (environmental taxes, economic growth, industrialization, environmental technologies, environmental policy stringency index, environmental expenditures, and financial development), which allows us to draw some new empirical findings and policy recommendations regarding the renewable energy consumption and environmental sustainability.

2. Environmental taxes and energy use in OECD

The environmental regulation (Shahzad, Radulescu et al., Citation2021) has played an essential role in reducing fossil fuel reliance in OECD economies as OECD countries sought an optimal method to reduce GHG emissions. The existing literature such as Grossman and Krueger (Citation1995) suggests that effective environmental regulations are a significant factor in promoting the clean energy production. Some academic researchers believe that the energy use is the manifestation of the industrial production process, which requires additional restrictions in the form of the environmental reforms. To overcome the dilemma of the economic development and environmental protection, the environmental regulation is considered an adequate tool in realizing the social welfare (Shahzad et al., Citation2020; Shahzad, Fareed et al., Citation2021; Wang & Zhang, Citation2015). However, imperfect environmental regulation, i.e., alternate energy source subsidies, policy implementation lags, and strict carbon emission tax, promote green paradox by encouraging businesses to increase extraction levels, hence leading to higher GHG emissions (Wahab et al., Citation2021; Van der Werf & Di Maria, Citation2012). The existing literature suggests that environmental regulations and environmental technologies have a different impact on the carbon emissions in different countries (Bogusz & Howlett, Citation2008; Hu et al., Citation2020; Kalkuhl et al., Citation2012; Voigt et al., Citation2014). Hence, figuring out some effective environmental regulations in the developed economies such as OECD are important for achieving GHG reduction levels prescribed under various climate agreements, i.e., Kyoto protocol, Paris climate agreement.

The introduction of the environmental regulation can be categorized into three types. The first is a single indicator, a proxy to cover environmental regulation, under Pollution Abatement and Control Expenditures (Grover, Citation2017; Rubashkina et al., Citation2015), and evaluates the environmental expenditure and investments to control the environmental pollution at the sectoral level. However, the country-level data for OECD countries under PACE is not available. The second category includes the multi-indicators to analyze the differential impact of the environmental regulations. Several studies have used such indicators to evaluate the impact of the environmental regulations on different environmental pollutants. Bartik (Citation1988) evaluated the introduction of pollutant regulations and state water protection policies. Some researchers such as Xie et al. (Citation2017) researched the market and non-market financial mechanisms to distinguish some various environmental regulations and concluded that market-based environmental instruments increase opportunity cost to control the environmental damage and GHG emissions, while non-market environmental regulations enforce the existing environmental policies.

Compared to the aforementioned environmental approaches, OECD countries have developed a composite index, the Environmental Policy Stringency (EPS) index, which consists of market and non-market environmental instruments with equal weights. Additionally, market-based environmental instruments include emission trading schemes, DRS, feed-in tariffs, and environmental taxes, while R&D subsidies and environmental standards form the non-market instruments. Also, every aspect consists of specific indicators; 15 policy instruments are used in scoring stringent environmental policies, where scores are allocated from 0 to 6, with 6 being the most stringent environmental policies. The implication of multi-dimensional environmental policies has contributed to EPS being the first tangible policy mechanism to evaluate environmental stringency and introduce further policy reforms (Albrizio et al., Citation2017; Ben Jebli et al., Citation2020; Shahzad, Citation2020).

3. Literature review

Current industrial processes heavily depend on the fossil fuels because the economic growth is directly associated with a continuous energy demand. In this regard, the renewable energy sources have emerged as an alternative to the conventional energy sources, as we are moving in a direction where a hybrid energy system is an effective approach to overcome the environmental degradation issues (Mez, Citation2020). Bearing in mind the current standing of the renewable energy, we investigate the existing literature regarding the environmental innovations and regulations.

Environmental taxes are pricing instruments implemented to reshape the energy consumption patterns and create a “win-win” for both the environment and economic growth (Bi et al., Citation2019; Quirion & Giraudet, Citation2008; Rausch & Reilly, Citation2012). Ding et al. (Citation2019) studied the long-term scope of the environmental tax scenarios and suggested that the introduction of the environmental taxes and environmental technologies reduces carbon emissions by 28% in the highly polluted economies. Carrera et al. (Citation2015) and Lu et al. (Citation2010) used the computable general equilibrium (CGE) approach to analyze the environmental policies and adopted a balanced approach towards the economic development and environmental reforms to reveal that the carbon taxes have positive impacts on the environment and economy. Shi et al. (Citation2019) studied the environmental tax as an energy policy instrument, reducing carbon emissions and enhancing the energy efficiency. By using a dynamic general equilibrium, the researchers revealed that the exact impact of environmental taxes depends upon the nature of the economic sectors.

Villoria-Saez et al. (Citation2016) reviewed the emission trading schemes and GHG legislation in six major economies to reveal that emission trading schemes contribute to a 1.58% annual reduction in the carbon emissions. Rapanos and Polemis (Citation2005) claimed that environmental taxes lower the carbon emissions in Greece, and further suggested that a better environmental outcome would be possible if different tax rates are chosen for various economic sectors, especially in the EU countries. Mardones and Baeza (Citation2018) pointed out that only the highest level of environmental tax can help lower CO2 emissions in most of the South American countries. Allan et al. (Citation2014) concluded that with the help of a tax of £50 per ton of carbon dioxide, the GHG emissions in Scotland would be reduced by almost 37%. Roman et al. (Citation2017) applied the social accounting matrix to illustrate that the introduction of US$5 of carbon tax per ton reduces the GHG emissions by 1800 grams. While having mentioned all the positive impacts of CO2 on GDP, there are still cases illustrating the relapsing effects, which ultimately leads to negative growth (Abdullah & Morley, Citation2014; Xie, Dai, & Dong, Citation2018; Xie, Dai, et al., Citation2018).

Probst and Sauter (Citation2015) investigated the GHG emissions and suggested that the improper implementation of the environmental policies could increase the CO2 emissions. By implementing the strategy of various taxes on the emissions of CO2 at different levels, in the short run, this can contribute to an economic slowdown in the domestic economy (Tian et al., Citation2017). Lee et al. (Citation2012) used the macroeconomic theoretical approach to conclude that environmental tax reforms only showed a mild reduction in the carbon dioxide emission levels in Japan. Yi and Li (Citation2018) suggested that environmental taxes do not necessarily reduce carbon emissions in the long run, as the final outcomes depend on the environmental pollution and the policy mechanism chosen in order to implement these taxes. Recent studies (Bashir et al., Citation2021; Dong et al., Citation2019; Lin & Li, Citation2011) concluded that the carbon taxes and policies possess some varied impacts in different countries or different areas within the same region.

Tang et al. (Citation2017) used the CGE model to study the environmental taxes and concluded that not only environmental taxes reduce environmental pollutants, but they are also positively associated with the economic activities in the ‘green industry’. According to Carrera et al. (Citation2015), the policies that are implementing carbon taxes are attempts to find better, suitable, and well-balanced layouts between the economic development and carbon emissions to protect the environment. Guo et al. (Citation2014) applied the CGE model to study the effects of the carbon taxes on the Chinese economy and environment. The empirical estimates showed that the implementation of environmental taxes would significantly reduce the carbon emissions caused by the fossil fuels. Still, it can also be negatively-related to the economic growth. However, CTR is another alternative tool that has been used in many other research projects for different industries, which leads to a possible partial deal for various sectors and provinces of the same country or even for the regional level to the country level. Under this situation, few researchers have shifted their attention from the country to the provincial level. Weng et al. (Citation2018) carefully studied the impact of the macroeconomic and welfare elements on CO2 in Guangxi Province in China to specify that different CO2 intensity targets in different areas would improve the environmental quality in Guangxi province; furthermore, it will have a positive correlation with the social welfare, and economic contribution. Effective tax policy for lowering the CO2 emissions can only be established, which is pretty constant for reducing the carbon emissions from national to provincial levels to balance the economic development and environmental protection. In a similar study, Zhou et al. (Citation2018) established a CGE model to report that CO2 tax has a significant impact on different economic sectors, especially in the transport sector. The revenues from CO2 taxes are generally used to subsidize the households and different enterprises by lowering the existing taxes.

Kemp (Citation2000) found out that the environmental regulations are one of the major factors among many others as they influence CO2 emissions, and the policies implemented after the carbon taxes can affect the outcomes of the environmental innovations. The environmental regulations also hold the key to reduce the discharge of pollutants in OECD and the Latin American countries. Hashmi and Alam (Citation2019) emphasized the need to promote the green innovation by implementing the carbon taxes, which is a key indicator in the reduction of the GHG emissions. Therefore, these empirical findings for the OECD countries allowed the researchers to conclude that patents are environmentally friendly as one percent increase in the environmental innovation reduces CO2 emissions by 1.7 percent.

O’Ryan and Sánchez (Citation2008) estimated how much the environmental regulation instruments can bring the net benefits in Chile. The findings indicate that the CO2 concentrations can be lowered by adopting the tradable permit system. O’Ryan and Bravo (Citation2001) found that the economic benefits of the firms are based on implementing the optimal level of regulations related to the environment and availability of the cleaner fuels industrial scale. Some scholars have suggested that some industrial indicators can be considered in order to enhance economic growth. However, within this spectrum, the tradable permits create a system scenario at an individual source level. This would help reduce CO2 emissions at a relatively lower cost. It also enhances the industrial sources when the objectives for reducing the pollutants are of the highest-level requirements. Regarding the aspect of the sustainable environment, Halkos and Papageorgiou (Citation2018) concluded that not only CO2 taxation reduces the GHG emissions, but it can also be implemented to offset the fiscal deficit in the developing economies.

On a different aspect, it was found that the substantial charges for pollution and higher taxes on the CO2 emissions are setting some effectual patterns for the use of the available resources, achieving a sustainable environment, and encouraging economic growth. The CO2 externalities mainly originate from the economic activities, from the energy intensive industries. These pollutant emissions can be decreased by imposing higher taxes on higher pollutants. Hence, the environmental taxes and regulations are the main instruments to ensure the environmental reforms and to achieve the desired outcomes (Shahzad, Radulescu et al., Citation2021; Wang et al., Citation2019). Shuai et al. (Citation2018) used the STIRPAT framework to assess the impact of the environmental policies on the economic outcomes. They found that different dimensions can be considered for the regional environmental degradation that can be influenced by the pollutant charges of various industrial, energy, and economic sectors. Moreover, the implementation of the environmental taxation can promote further developments in the renewable energy sector (Danish & Ulucak, Citation2020; Niu et al., Citation2018; Shahzad, Citation2020). Acemoglu et al. (Citation2016) investigated the relationship between the environmental regulations and GHG emissions in the emerging economies to conclude that the environmental regulations significantly reduce CO2 emission in the developed economies to bring further growth in the renewable energy sector, which contributes to a clean environment and ultimately lead to the sustainable development goals for the economies.

4. Materials and methods

4.1. Data Specification

This research relies on secondary published data in the attempt to analyze the impact of the environmental regulations and policies over the renewable energy consumption by analyzing the empirical datasets from 1996 to 2018 for 29 OECD economies. The dependent variable is the renewable energy consumption (% of total energy consumption). The independent variables include the environmental taxes that are taken as constant 2010 US dollars from the OECD database. GDP covers the economic growth in the domestic economy (per capita, constant 2010 US$), Industrialization accounts for the added-value of the industrial sectors as constant 2010 US$, environmental technologies is taken as a share of all the technologies, environmental policy synergy index (stringency of environmental policy), environmental expenditures (millions USD, 2010 PPP prices) and financial development indexFootnote4 (development of the financial markets and financial institutions). The inclusion of control ensures no biasness in the empirical modeling. The general regression framework of the current study is as follows:

(1)

(1)

(2)

(2)

(3)

(3)

In the EquationEquations 1–3, represents cross-sections for OECD countries,

represents time, i.e., 1996-2018. The variable details and data source information are provided in and .

Table 1. Data and Variables specification.

Table 2. Descriptive statistics.

4.2. Estimation strategy

We begin the empirical analysis by checking the cross-sectional dependence as it can produce inconsistent and biased empirical findings (Phillips & Sul, Citation2003). Recent economic progress has ensured that different economic regions rely on each other for bilateral trade, political and economic channels, which can contribute to CD among datasets. To overcome this issue, we utilize the empirical test proposed by Pesaran (Citation2004). The following equation is used to test cross-sectional dependence within our dataset

(5)

(5)

where the number of countries is represented by N, time by T, and estimation of the cross-sectional correlation of country

and

is represented by

The null hypothesis advocates for the absence of cross-sectional dependence, whereas the alternative hypothesis supports the presence of cross-sectional dependence.

4.2.1. Panel unit root testing

After confirmation of the CD, we have performed the unit root tests. The economists generally affirm that the second-generation unit root tests are ideal for solving the issue of the cross-sectional dependence as they can overcome the issue of low power to accommodate CD. Furthermore, the second-generation unit root tests assume no CD in the dataset. For this purpose, we chose cross-sectional Im-Pesaran-Shin (CIPS), and cross-sectional augmented Dickey-Fuller (CADF) as these statistical tests consider heterogeneity and cross-sectional across the dataset.

4.2.2. Westerlund (2007) cointegration test

In comparison to the existing empirical literature, we rely on a useful statistical approach suggested by Westerlund (Citation2007) to deal with cross-sectional dependence and heterogenous slope effectively. This approach provides reliable long-run cointegration results. Westerlund (Citation2007) mainly relies on four statistics, two for each panel and group statistics, where panel statistics hypothesizes that null of at least one cross-section is cointegrated, while the group statistics proposes null hypothesis for the whole group. and

represent panel statistics while

and

denote group statistics.

4.2.3. Panel quantile regression

Koenker and Bassett (Citation1978) developed the quantile regression approach, which computes a set of regression functions, each referring to a different quantile of the conditional distribution. The significant distinction between OLS and quantile regression is that OLS approximates the regression coefficients as a consequence where the regression line runs through the average of the data set. However, on the contrary, quantile regression lines rely on different quantiles of the data distributions. For higher quantiles, most of the data set lies below the quantile regression line or vice versa. This enables us to examine the association between the dependent and independent variables over the whole data distribution. The quantile regression is a widely used empirical approach in economics (McDonald et al., Citation2016; Xu & Lin, Citation2016; Zhu et al., Citation2016). The quantile regression model is estimated as follows:

(6)

(6)

(7)

(7)

where the vector of the explanatory variables is represented by x, explained variables is represented by ye; error term by μ, whose distribution of conditional quantile is equal to zero. The dependent variable’s

th quantile is

),

is regression estimator of

th quantile and is following formula’s solution:

(8)

(8)

Different parameters will be estimated when θ is equal to different values. In order to efficiently examine the complex relationship between environmental taxes and energy consumption (energy intensity), we have selected several quantiles (i.e., 25th, 50th, & 75th quantiles). The application of the bootstrap method has ensured the estimation of the confidence interval for the quantile regression parameters. Traditional regression provides analysis based on the sample subset, but unlike the traditional regression, the quantile regression utilizes the whole data to provide analytics for different quantile parameters (Cade & Noon, Citation2003).

4.2.4. FMOLS and OLS fixed effects

We have further examined the long-run analysis through the econometric tools such as FMOLS and OLS with fixed effects. These econometric techniques are reliable in solving the issues of endogeneity and serial correlation. The FMOLS technique relies on a non-parametric method to control the issues of autocorrelation and endogeneity, whereas the fixed effects OLS approach controls time-invariant unobserved individual characteristics that can be correlated with the observed independent variables.

5. Empirical results and discussion

The empirical findings of CD and second-generation unit root tests are presented in , which supports the existence of cross-section within our dataset; hence, we ignore the null hypothesis. After confirming CD in our data, we have investigated the integrated level of the variables through CIPS and CAF unit root tests, which have indicated that besides GDP, all variables have unit root problems at level, but data series becomes stationary at first difference.

Table 3. Results of cross-sectional and unit-root tests.

The findings of CD and second-generation unit root tests contribute to the implementation of Westerlund (Citation2007) co-integration test, which helps to identify the co-integration if some cross-independence issues exist in the dataset; summary findings are presented in . The outcome with renewable energy (RE) as the response variable suggests that all variables are cointegrated since the hypothesis of no cointegration is rejected at 1% level of significance using the robust p-values. The empirical estimates based on robust p-values provide a strong evidence of co-integration amongst the dataset. Hence, we can conclude that the analyzed variables possess a long-term association.

Table 4. Results of the panel Westerlund co-integration test.

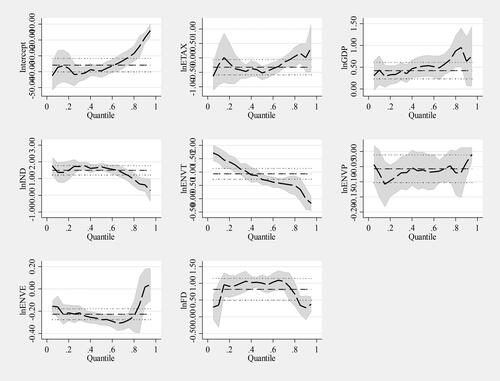

The empirical findings of the quantile regression in the extended form to examine the effect of the environmental taxes on the energy consumption and energy intensity are presented in (). Our findings indicate that the environmental taxes are significant at all quantiles in all three models and present negative associations. These findings indicate that the introduction of the environmental taxation to transform OECD countries into some energy-efficient economies will require further policy adjustments. For the environmental taxes to become effective, the imposed increase in these taxes should be spread over a longer time so that the enterprises can adapt and maintain their economic competitiveness. The economic growth is significant and has a positive association in all of the econometric models. This signifies that the economic growth has a significant effect on the renewable energy consumption. Therefore, the effective and efficient policies should prioritize the clean energy sources in the OECD economic block. The industrialization is positive and significant in all three econometric models, which supports the fact that the renewable energy fosters the sustainable industrialization to drive further developments in the industrial sector and to form the economic competitiveness.

Figure 1. Estimates of coefficients from quantile regressions for variables.

Source: Authors.

Table 5. Results of quantile regression for three models.

The financial development is also revealed to be significant and positive, except lower quantile in Model −1. These results indicate that a balanced approach to the financial development and energy reforms has ensured the effective integration of the clean energy sources in preventing the environmental degradation. The environmental technologies have a positive and significant association with the renewable energy consumption in the OECD countries as the renewable energy consumption relies upon continuous technological improvements, in order to improve especially the production efficiency function. Lastly, the environmental patents and environmental expenditures are significant, but they present a negative association at the lower, middle, and higher quantiles in Model 2 and Model 3, respectively. This can be attributed to the fact that the recent environmental regulations in the OECD countries have not been effective in mitigating the GHG emissions and climate change as the OECD economies should facilitate environmental policies to accelerate the diffusion of the environmental expenditures and patents.

illustrates the long-run estimates for the FMOLS (fully modified ordinary least squares) and OLS fixed effects methods. For Model-1, Model-2, and Model-3, the coefficient for the environmental taxes is negative and significant, suggesting that the introduction of the environmental taxes carries a negative effect on the renewable energy consumption across the OECD countries. These findings further imply that in order to control the overall energy consumption and energy intensity, the OECD countries need to employ some strict regulations and introduce further institutional reforms, which will support the increase of the share of the clean energy sources in the energy mix. Hájek et al. (Citation2019) analyzed the role of the environmental taxes and emission trading schemes in the European countries. They concluded that, in the short-run, the environmental taxes do not promote the renewable energy, though the influence of the economic instruments, i.e., environmental taxes, becomes apparent only in the long run. Lapinskienė et al. (Citation2017) also proved in their study for the European countries a positive relation between the environmental tax and GHG emissions, highlighting that the environmental tax doesn’t support the increase of the renewable energy consumption. Next, the coefficient of GDP carries a positive association with the renewable energy, which implies that the renewable energy is promoted within the economic growth framework. Al-Mulali et al. (Citation2013) examined the association of the renewable energy and GDP in high-income, middle-income, and lower-middle-income countries. They suggested that the GDP growth and renewable energy have a feedback relationship in Uzbekistan and Zambia. Apergis et al. (Citation2010) and Tugcu et al. (Citation2012) supported similar findings. We have also found that the association of the industrialization and renewable energy consumption is positive in the FMOLS approach, but negative under the OLS findings. Liu et al. (Citation2016) investigated the impact of the industrialization in South Korea and China to conclude that a rapid industrialization requires fossil fuels, which deteriorates the environment and limits the progress in the renewable energy consumption. Though, Hussain et al. (Citation2021), Bhattacharya et al. (Citation2017), and Bulut and Muratoglu (Citation2018) indicated that the industrialization has a positive association with the renewable energy consumption in the medium and long run.

Table 6. Results from conventional long-run estimators.

The observed association of the financial development and renewable energy consumption is negative, which means that the financial development does not contribute to the increase of the renewable energy consumption. Jalil and Feridun (Citation2011) reported similar findings and suggested that higher financial developments lead to a rapid industrial growth, which in turn increases the reliance of the respective economy on the traditional fossil fuel, hence creating a negative impact over the use of the renewable energy sources. In a more recent study, Sarkodie and Strezov (Citation2019) suggested that the financial development contributes to the environmental degradation by promoting the FDI inflows in the developing economies while also increase the reliance on the traditional energy sources. Next, the coefficient value for the environmental technologies shows a positive and significant impact on the renewable energy consumption. Costantini et al. (Citation2015) researched the renewable energy consumption for 36 industrial countries to indicate that the environmental technologies have a bidirectional causal association with the renewable energy consumption. Likewise, Kim et al. (Citation2017) investigated the association of the environmental technologies system in 16 OECD countries from 1991 to 2007 to articulate that the environmental technologies promote the cleaner energy sources as a substitute for the fossil fuels. Finally, the estimates for the environmental patents and environmental expenditures display a negative association in the respective empirical model. These findings are counter-intuitive, as the development of the environmental technologies and environmental expenditures should promote renewable energy use. A possible explanation is that the current environmental regulations require further policy changes to address the environmental issues in the industrial economies such as OECD. Schleich et al. (Citation2017) analyzed the impact of the policy instruments and environmental patents in OECD economies and suggested that the policy instruments curtailed the patenting activities leading to a negative impact on the renewable energy consumption. Similarly, Cheng et al. (Citation2019) and Böhringer et al. (Citation2017) analyzed the renewable energy patents for BRICS and Germany, respectively. Their initial findings supported the existence of the innovation hypothesis; however, they also concluded that the adoption of the environmental policies after the year 2000 led to a negative impact on the renewable energy consumption. Similarly, Wolde-Ghiorgis (Citation2002) suggested that lowering the environmental expenditure from 1% to 0.1% resulted in a negative impact on the renewable energy consumption in the African economies.

6. Conclusion and practical implications

Recent environmental protection efforts have determined the policymakers to introduce some sustainable policies to combine the economic growth with a lower environmental impact. This study examines the possible impact of seven determinant variables (namely environmental taxes, economic growth, industrialization, environmental technologies, environmental patents, environmental expenditures, and financial development) in impeding the renewable energy consumption, which has been overlooked in the previous studies. In order to gauge the potential impact between the renewable energy consumption and its determinants, FMOLS, OLS with fixed effects, and panel quantile regressions extended in different quantiles (25th, 50th, 75th) have been applied in the presence of asymmetries to examine the long run results and implications. The economic growth and industrialization promote the renewable energy consumption as the OECD economies move away from the fossil fuels in order to promote the sustainable growth models. Similarly, the environmental technologies positively impact on the renewable energy consumption as the advanced technologies contribute to limit the environmental pollutants’ emissions. However, some of our findings are inconsistent with existing studies focused on the industrial economies: (1) Environmental taxes are crucial in promoting the green energy in the industrial economies (Fan et al., Citation2019), but these findings are contrary to our estimates about the environmental taxes. This is the reason for which we suggest that the market-based instruments should support the environmental regulations to increase the renewable energy consumption in the OECD economies. (2) Environmental expenditures and environmental patents are negatively associated with the renewable energy consumption; these findings contradict the existing literature (Yang et al., Citation2019; Youssef, Citation2020). To overcome this, easing the restrictions on the technological transmission and lowering the intellectual property rights costs can positively link the environmental patents, environmental expenditure, and renewable energy.

Our empirical findings provide some vital suggestions for the OECD policymakers. First, the negative association between the environmental taxes and the renewable energy shows that the OECD countries should establish a green financial system to promote the renewable energy, as renewable energy projects are capital intensive, which is why there is a need for such reforms in the financial sector in order to promote green finance, where cleaner energy sources must be prioritized for the credit availability. Some additional reforms in the fiscal policies, i.e., tax cut policies, scientific subsidies policies, can play a significant role in eliminating the high cost and low benefits of the renewable energy consumption. Second, the cost reduction and technological progress are also significant challenges concerning climate change. More policy initiatives are required to overcome the technical problems, i.e., from research about relevant technical approaches to typical demonstration applications. Third, the OECD countries need to accelerate the system reform by focusing on the price marketization. Eventually, the market rules rather than policy subsidies must be allowed to accelerate the sustainable development of the renewable energy consumption. Fourth, the OECD countries should simplify the complex bureaucratic procedures towards securing the environmental patents and licenses as the high cost of RE innovations need close attention. Lastly, the OECD economies need a fundamental transformation in respect to the energy and economic structure as the environmental policies introduced during the transition from the non-renewable to renewable substitutions must avoid the market disruption of non-renewables, or, in other words, the government interventions result in higher carbon prices. Hence, a gradual implementation of the environmental reforms and policies for creating a more efficient financial sector and for developing the environmental technologies are some efficient methods to promote the renewable energy consumption.

The present research also highlights a few shortcomings that future research contributions can address. As the integration of the renewable energy into the energy mix depends on several indicators within and across the OECD economies, it is of great significance to establish the long-term environmental policies to overcome the regulatory, costs, capacity, and infrastructure barriers. Another critical point is to address the bureaucratic and institutional frameworks that affect the environmental and energy policies, as the energy structure, environmental legislation, and economic development are influenced by these indicators. Lastly, further research can also address the issues such as crowding out between the energy and non-energy environmental patents to analyze the environmental policy frameworks.

Competing interests

The authors declare that they have no known competing financial interests or personal relationships that could have appeared to influence the work reported in this paper.

Ethics approval and consent to participate

Not applicable.

Availability of data and materials

The datasets used during the current study are available from the corresponding or first author on reasonable request.

Correction Statement

This article has been republished with minor changes. These changes do not impact the academic content of the article.

Additional information

Funding

Notes

1 Environmental taxes are the pricing instruments which are implemented to encourage the broad-based actions to reduce the environmental damage.

2 The degree to which environmental policies put an explicit or implicit price on polluting or environmentally harmful behavior.

3 Capital expenditures related to characteristics activities and facilities specified in the classifications of the environmental protection activities.

4 Financial development is developed by I.M.F. which includes 9 indices that summarizes efficiency, depth and access towards financial markets and financial institutions.

References

- Abdullah, S., & Morley, B. (2014). Environmental taxes and economic growth: Evidence from panel causality tests. Energy Economics, 42, 27–33. https://doi.org/10.1016/j.eneco.2013.11.013

- Acemoglu, D., Akcigit, U., Hanley, D., & Kerr, W. (2016). Transition to clean technology. Journal of Political Economy, 124(1), 52–104. https://doi.org/10.1086/684511

- Ahmad, M., Ul Haq, Z., Khan, Z., Khattak, S. I., Ur Rahman, Z., & Khan, S. (2019). Does the inflow of remittances cause environmental degradation? Empirical evidence from China. Economic Research-Ekonomska Istraživanja, 32(1), 2099–2121. https://doi.org/10.1080/1331677X.2019.1642783

- Albrizio, S., Kozluk, T., & Zipperer, V. (2017). Environmental policies and productivity growth: Evidence across industries and firms. Journal of Environmental Economics and Management, 81, 209–226. https://doi.org/10.1016/j.jeem.2016.06.002

- Allan, G., Lecca, P., McGregor, P., & Swales, K. (2014). The economic and environmental impact of a carbon tax for Scotland: A computable general equilibrium analysis. Ecological Economics, 100, 40–50. https://doi.org/10.1016/j.ecolecon.2014.01.012

- Al-Mulali, U., Fereidouni, H. G., Lee, J. Y., & Sab, C. N. B. C. (2013). Examining the bi-directional long run relationship between renewable energy consumption and GDP growth. Renewable and Sustainable Energy Reviews, 22, 209–222. https://doi.org/10.1016/j.rser.2013.02.005

- Apergis, N., Payne, J. E., Menyah, K., & Wolde-Rufael, Y. (2010). On the causal dynamics between emissions, nuclear energy, renewable energy, and economic growth. Ecological Economics, 69(11), 2255–2260. https://doi.org/10.1016/j.ecolecon.2010.06.014

- Azam, A., Rafiq, M., Shafique, M., & Yuan, J. (2021). Renewable electricity generation and economic growth nexus in developing countries: An ARDL approach. Economic Research-Ekonomska Istraživanja, 34(1), 2423–2446. https://doi.org/10.1080/1331677X.2020.1865180

- Bae, H., & Yu, S. (2018). Information and coercive regulation: The impact of fuel mix information disclosure on states’ adoption of renewable energy policy. Energy Policy, 117, 151–159. https://doi.org/10.1016/j.enpol.2018.03.010

- Bartik, T. J. (1988). The effects of environmental regulation on business location in the United States. Growth and Change, 19(3), 22–44. https://doi.org/10.1111/j.1468-2257.1988.tb00473.x

- Bashir, M. F., Ma, B., Shahbaz, M., Shahzad, U., & Vo, X. V. (2021). Unveiling the heterogeneous impacts of environmental taxes on energy consumption and energy intensity: Empirical evidence from OECD countries. Energy, 226, 120366. https://doi.org/10.1016/j.energy.2021.120366

- Ben Jebli, M., Farhani, S., & Guesmi, K. (2020). Renewable energy, CO2 emissions and value added: Empirical evidence from countries with different income levels. Structural Change and Economic Dynamics, 53, 402–410. https://doi.org/10.1016/j.strueco.2019.12.009

- Bhattacharya, M., Churchill, S. A., & Paramati, S. R. (2017). The dynamic impact of renewable energy and institutions on economic output and CO2 emissions across regions. Renewable Energy, 111, 157–167. https://doi.org/10.1016/j.renene.2017.03.102

- Bi, H., Xiao, H., & Sun, K. (2019). The impact of carbon market and carbon tax on green growth pathway in China: A dynamic CGE model approach. Emerging Markets Finance and Trade, 55(6), 1312–1325. https://doi.org/10.1080/1540496X.2018.1505609

- Bogusz, C., Howlett, C. (2008). Policy options for reducing CO2 emissions. Congressional Budget Office, no. 2930, Washington. https://www.cbo.gov/sites/default/files/110th-congress-2007-2008/reports/02-12-carbon.pdf

- Böhringer, C., Cuntz, A., Harhoff, D., & Asane-Otoo, E. (2017). The impact of the German feed-in tariff scheme on innovation: Evidence based on patent filings in renewable energy technologies. Energy Economics, 67, 545–553. https://doi.org/10.1016/j.eneco.2017.09.001

- Bulut, U., & Muratoglu, G. (2018). Renewable energy in Turkey: Great potential, low but increasing utilization, and an empirical analysis on renewable energy-growth nexus. Energy Policy, 123, 240–250. https://doi.org/10.1016/j.enpol.2018.08.057

- Cade, B. S., & Noon, B. R. (2003). A gentle introduction to quantile regression for ecologists. Frontiers in Ecology and the Environment, 1(8), 412–420. https://doi.org/10.1890/1540-9295(2003)001[0412:AGITQR2.0.CO;2]

- Carrera, L., Standardi, G., Bosello, F., & Mysiak, J. (2015). Assessing direct and indirect economic impacts of a flood event through the integration of spatial and computable general equilibrium modelling. Environmental Modelling & Software, 63(11), 109–122. https://doi.org/10.1016/j.envsoft.2014.09.016

- Cheng, C., Ren, X., Wang, Z., & Yan, C. (2019). Heterogeneous impacts of renewable energy and environmental patents on CO2 emission – Evidence from the BRIICS. Science of the Total Environment, 668, 1328–1338. https://doi.org/10.1016/j.scitotenv.2019.02.063

- Costantini, V., Crespi, F., Martini, C., & Pennacchio, L. (2015). Demand-pull and technology-push public support for eco-innovation: The case of the biofuels sector. Research Policy, 44(3), 577–595. https://doi.org/10.1016/j.respol.2014.12.011

- Danish, & Ulucak, R. (2020). How do environmental technologies affect green growth? Evidence from BRICS Economies. Science of the Total Environment, 10, 1365041–1365047. https://doi.org/10.1016/j.scitotenv.2020.136504

- Ding, S., Zhang, M., & Song, Y. (2019). Exploring China's carbon emissions peak for different carbon tax scenarios. Energy Policy, 129, 1245–1252. https://doi.org/10.1016/j.enpol.2019.03.037

- Dong, K., Dong, X., & Dong, C. (2019). Determinants of the global and regional CO2 emissions: What causes what and where? Applied Economics, 51(46), 5031–5044. https://doi.org/10.1080/00036846.2019.1606410

- Erdogan, S., Okumus, I., & Guzel, A. E. (2020). Revisiting the Environmental Kuznets Curve hypothesis in OECD countries: The role of renewable, non-renewable energy, and oil prices. Environmental Science and Pollution Research International, 27(19), 23655–23663. https://doi.org/10.1007/s11356-020-08520-x

- Fan, X., Li, X., & Yin, J. (2019). Impact of environmental tax on green development: A nonlinear dynamical system analysis. PLoS One, 14(9), e0221264. https://doi.org/10.1371/journal.pone.0221264

- Farooq, M. U., Shahzad, U., Sarwar, S., & Zai Jun, L. (2019). The impact of carbon emission and forest activities on health outcomes: Empirical evidence from China. Environmental Science and Pollution Research International, 26(13), 12894–12906. https://doi.org/10.1007/s11356-019-04779-x

- Grossman, G. M., & Krueger, A. B. (1995). Economic growth and the environment. The Quarterly Journal of Economics, 110(2), 353–377. https://doi.org/10.2307/2118443

- Grover, D. (2017). Declining pollution abatement R&D in the United States: Theory and evidence. Industrial and Corporate Change, 26(5), 845–863.

- Guo, Z., Zheng, Y., & Zhang, X. (2014). Analysis of the energy-environment-economy system in China based on the dynamic CGE model. Journal Systems Engineering, 29, 581–591.

- Gygli, S., Haelg, F., Potrafke, N., & Sturm, J. E. (2019). The KOF Globalization index–revisited. The Review of International Organizations, 14(3), 543–574. https://doi.org/10.1007/s11558-019-09344-2

- Hájek, M., Zimmermannová, J., Helman, K., & Rozenský, L. (2019). Analysis of carbon tax efficiency in energy industries of selected EU countries. Energy Policy, 134, 110955. https://doi.org/10.1016/j.enpol.2019.110955

- Halkos, G. E., & Papageorgiou, G. J. (2018). Pollution, environmental taxes and public debt: A game theory setup. Economic Analysis and Policy, 58, 111–120. https://doi.org/10.1016/j.eap.2018.01.004

- Hashmi, R., & Alam, K. (2019). Dynamic relationship among environmental regulation, innovation, CO2 emissions, population, and economic growth in OECD countries: A panel investigation. Journal of Cleaner Production, 231, 1100–1109. https://doi.org/10.1016/j.jclepro.2019.05.325

- Hille, E., Althammer, W., & Diederich, H. (2020). Environmental regulation and innovation in renewable energy technologies: Does the policy instrument matter? Technological Forecasting and Social Change, 153, 119921. https://doi.org/10.1016/j.techfore.2020.119921

- Hu, J., Huang, Q., & Chen, X. (2020). Environmental regulation, innovation quality and firms’ competitivity – Quasi-natural experiment based on China’s carbon emissions trading pilot. Economic Research-Ekonomska Istraživanja, 33(1), 3307–3333. https://doi.org/10.1080/1331677X.2020.1771745

- Hussain, M., Bashir, M. F., & Shahzad, U. (2021). Do foreign direct investments help to bolster economic growth? New insights from Asian and Middle East economies. World Journal of Entrepreneurship, Management and Sustainable Development, 17(1), 62–84.

- Jalil, A., & Feridun, M. (2011). The impact of growth, energy and financial development on the environment in China: A cointegration analysis. Energy Economics, 33(2), 284–291. https://doi.org/10.1016/j.eneco.2010.10.003

- Kalkuhl, M., Edenhofer, O., & Lessmann, K. (2012). Learning or lock-in: Optimal technology policies to support mitigation. Resource and Energy Economics, 34(1), 1–23. https://doi.org/10.1016/j.reseneeco.2011.08.001

- Kemp, R. (2000). Technology and environmental policy: Innovation effects of past policies and suggestions for improvement, innovation and the environment (pp. 35–36). OECD Publications.

- Khan, Z., Sisi, Z., & Siqun, Y. (2019). Environmental regulations an option: Asymmetry effect of environmental regulations on carbon emissions using non-linear ARDL. Energy Sources, Part A: Recovery, Utilization, and Environmental Effects, 41(2), 137–155.

- Khoshnevis Yazdi, S., & Dariani, A. G. (2019). CO2 emissions, urbanisation and economic growth: Evidence from Asian countries. Economic Research-Ekonomska Istraživanja, 32(1), 510–530. https://doi.org/10.1080/1331677X.2018.1556107

- Kim, K., Heo, E., & Kim, Y. (2017). Dynamic policy impacts on a technological-change system of renewable energy: An empirical analysis. Environmental and Resource Economics, 66(2), 205–236. https://doi.org/10.1007/s10640-015-9946-5

- Koenker, R., & Bassett, G. (1978). Regression quantiles. Econometrica, 46(1), 33–50. https://doi.org/10.2307/1913643

- Lapinskienė, G., Peleckis, K., & Nedelko, Z. (2017). Testing environmental Kuznets curve hypothesis: The role of enterprise’s sustainability and other factors on GHG in European countries. Journal of Business Economics and Management, 18(1), 54–67. https://doi.org/10.3846/16111699.2016.1249401

- Lee, S., Pollitt, H., & Ueta, K. (2012). An assessment of Japanese carbon tax reform using the E3MG econometric model. TheScientificWorldJournal, 2012, 835917–835919. https://doi.org/10.1100/2012/835917

- Lei, P., Tian, X., Huang, Q., & He, D. (2017). Firm size, government capacity, and regional environmental regulation: Theoretical analysis and empirical evidence from. Journal of Cleaner Production, 164, 524–533. https://doi.org/10.1016/j.jclepro.2017.06.166

- Lin, B., & Li, X. (2011). The effect of carbon tax on per capita CO2 emissions. Energy Policy, 39(9), 5137–5146. https://doi.org/10.1016/j.enpol.2011.05.050

- Liu, Y., Huang, J., & Zikhali, P. (2016). The bittersweet fruits of industrialization in rural China: The cost of environment and the benefit from off-farm employment. China Economic Review, 38, 1–10. https://doi.org/10.1016/j.chieco.2015.11.006

- Lu, C., Tong, Q., & Liu, X. (2010). The impacts of carbon tax and complementary policies on Chinese economy. Energy Policy, 38 (11), 7278–7285. https://doi.org/10.1016/j.enpol.2010.07.055

- Mardones, C., & Baeza, N. (2018). Economic and environmental effects of a CO2 tax in Latin American countries. Energy Policy, 114, 262–273. https://doi.org/10.1016/j.enpol.2017.12.001

- McDonald, S. M., Ortaglia, A., Bottai, M., & Supino, C. (2016). Differential association of cardiorespiratory fitness and central adiposity among US adolescents and adults: A quantile regression approach. Preventive Medicine, 88, 1–7. https://doi.org/10.1016/j.ypmed.2016.03.014

- Mez, L. (2020). 40 years promoting renewable energy in Germany. In L. Mez, L. Okamura, & H. Weidner (Eds.), The ecological modernization capacity of Japan and Germany. Energiepolitik und Klimaschutz. Energy policy and climate protection (pp. 119–136). Springer VS.

- Montero, J. P. (2002). Permits, standards, and technology innovation. Journal of Environmental Economics and Management, 44(1), 23–44. https://doi.org/10.1006/jeem.2001.1194

- Niu, T., Yao, X., Shao, S., Li, D., & Wang, W. (2018). Environmental tax shocks and carbon emissions: An estimated DSGE model. Structural Change and Economic Dynamics, 47, 9–17. https://doi.org/10.1016/j.strueco.2018.06.005

- O’Ryan, R., & Bravo, R. (2001). Permisos transables frente a la introducción de un combustible limpio: Estudio de caso para PM-10 y NOx en Santiago, Chile. Estudio de Economía, 28(2), 267–291.

- O’Ryan, R., & Sánchez, J. M. (2008). Comparison of net benefits of incentive-based and command and control environmental regulations: The case of Santiago. The World Bank Economic Review, 22(2), 249–269. https://doi.org/10.1093/wber/lhm013

- Ozcan, B., Tzeremes, P. G., & Tzeremes, N. G. (2020). Energy consumption, economic growth and environmental degradation in OECD countries. Economic Modelling, 84, 203–213. https://doi.org/10.1016/j.econmod.2019.04.010

- Pesaran, H. (2004). General diagnostic tests for cross-sectional dependence in panels [Cambridge Working Papers in Economics, 435]. University of Cambridge.

- Petrović, P., & Lobanov, M. M. (2020). The impact of R&D expenditures on CO2 emissions: Evidence from sixteen OECD countries. Journal of Cleaner Production, 248, 119187. https://doi.org/10.1016/j.jclepro.2019.119187

- Phillips, P. C., & Sul, D. (2003). Dynamic panel estimation and homogeneity testing under cross section dependence. The Econometrics Journal, 6(1), 217–259. https://doi.org/10.1111/1368-423X.00108

- Probst, M., & Sauter, C. (2015). CO2 emissions and greenhouse gas policy stringency – An empirical assessment [IRENE Working Paper, 1–38].

- Quirion, P., & Giraudet, L. G. (2008). Efficiency and distributional impacts of tradable white certificates compared to taxes, subsidies and regulations. Revue D'économie Politique, 118(6), 885–914. https://doi.org/10.3917/redp.186.0885

- Rapanos, V. T., & Polemis, M. L. (2005). Energy demand and environmental taxes: The case of Greece. Energy Policy, 33(14), 1781–1788. https://doi.org/10.1016/j.enpol.2004.02.013

- Rausch, S., & Reilly, J. (2012). Carbon tax revenue and the budget deficit: A win-win-win solution? [Report No. 228]. MIT Joint Program on the Science and Policy of Global Change, MIT.

- Ren, S., Li, X., Yuan, B., Li, D., & Chen, X. (2018). The effects of three types of environmental regulation on eco-efficiency: A cross-region analysis in China. Journal of Cleaner Production, 173, 245–255. https://doi.org/10.1016/j.jclepro.2016.08.113

- Requate, T., & Unold, W. (2003). Environmental policy incentives to adopt advanced abatement technology: Will the true ranking please stand up? European Economic Review, 47(1), 125–146. https://doi.org/10.1016/S0014-2921(02)00188-5

- Roman, R., Cansino, J., & Ordóñez, M. (2017). An assessment of the effects of the new chilean carbon tax. In Óscar Dejuán, Manfred Lenzen, & María-Ángeles Cadarso (eds.), Environmental and economic impacts of decarbonization input-output studies on the consequences of the 2015 Paris agreements (pp. 370–395). Routledge (Francis & Taylor Group).

- Rubashkina, Y., Galeotti, M., & Verdolini, E. (2015). Environmental regulation and competitiveness: Empirical evidence on the Porter Hypothesis from European manufacturing sectors. Energy Policy, 83, 288–300. https://doi.org/10.1016/j.enpol.2015.02.014

- Sarkodie, S. A., & Strezov, V. (2019). Effect of foreign direct investments, economic development and energy consumption on greenhouse gas emissions in developing countries. The Science of the Total Environment, 646, 862–871. https://doi.org/10.1016/j.scitotenv.2018.07.365

- Schleich, J., Walz, R., & Ragwitz, M. (2017). Effects of policies on patenting in wind-power technologies. Energy Policy, 108, 684–695. https://doi.org/10.1016/j.enpol.2017.06.043

- Shahzad, U. (2020). Environmental taxes, energy consumption, and environmental quality: Theoretical survey with policy implications. Environmental Science and Pollution Research International, 27(20), 24848–24862. https://doi.org/10.1007/s11356-020-08349-4

- Shahzad, U., Doğan, B., Sinha, A., & Fareed, Z. (2021). Does export product diversification help to reduce energy demand: Exploring the contextual evidences from the newly industrialized countries. Energy, 214, 118881. https://doi.org/10.1016/j.energy.2020.118881

- Shahzad, U., Fareed, Z., Shahzad, F., & Shahzad, K. (2021). Investigating the nexus between economic complexity, energy consumption and ecological footprint for the United States: New insights from quantile methods. Journal of Cleaner Production, 279, 123806. https://doi.org/10.1016/j.jclepro.2020.123806

- Shahzad, U., Ferraz, D., Doğan, B., & Aparecida do Nascimento Rebelatto, D. (2020). Export product diversification and CO2 emissions: Contextual evidences from developing and developed economies. Journal of Cleaner Production, 276, 124146. https://doi.org/10.1016/j.jclepro.2020.124146

- Shahzad, U., Radulescu, M., Rahim, S., Isik, C., Yousaf, Z., & Ionescu, S. A. (2021). Do environment-related policy instruments and technologies facilitate renewable energy generation? Energies, 14(3), 690. https://doi.org/10.3390/en14030690

- Shi, H., Qiao, Y., Shao, X., & Wang, P. (2019). The effect of pollutant charges on economic and environmental performances: Evidence from Shandong Province in China. Journal of Cleaner Production, 232, 250–256. https://doi.org/10.1016/j.jclepro.2019.05.272

- Shi, Q. S., Ren, H., Cai, W. C., & Gao, J. (2019). How to set the proper level of carbon tax in the context of Chinese construction sector? A CGE analysis. Journal of Cleaner Production, 240, 117955. https://doi.org/10.1016/j.jclepro.2019.117955

- Shuai, C., Chen, X., Wu, Y., Tan, Y., Zhang, Y., & Shen, L. (2018). Identifying the key impact factors of carbon emission in China: Results from a largely expanded pool of potential impact factors. Journal of Cleaner Production, 175, 612–623. https://doi.org/10.1016/j.jclepro.2017.12.097

- Tang, L., Shi, J., Yu, L., & Qin, B. (2017). Economic and environmental influences of coal resource tax in China: A dynamic computable general equilibrium approach. Resources, Conservation and Recycling, 117(A), 34–44. https://doi.org/10.1016/j.resconrec.2015.08.016

- Tian, X., Dai, H., Geng, Y., Huang, Z., Masui, T., & Fujita, T. (2017). The effects of carbon reduction on sectoral competitiveness in China: A case of Shanghai. Applied Energy, 197, 270–278. https://doi.org/10.1016/j.apenergy.2017.04.026

- Tugcu, C. T., Ozturk, I., & Aslan, A. (2012). Renewable and non-renewable energy consumption and economic growth relationship revisited: Evidence from G7 countries. Energy Economics, 34(6), 1942–1950. https://doi.org/10.1016/j.eneco.2012.08.021

- Van der Werf, E., & Di Maria, C. (2012). Imperfect environmental policy and polluting emissions: The green paradox and beyond. International Review of Environmental and Resource Economics, 6(2), 153–194. https://doi.org/10.1561/101.00000050

- Vasylieva, T., Machová, V., Vysochyna, A., Podgórska, J., & Samusevych, Y. (2020). Setting up architecture for environmental tax system under certain socioeconomic conditions. Journal of International Studies, 13(4), 273–285. https://doi.org/10.14254/2071-8330.2020/13-4/19

- Villoria-Saez, P., Tam, V. W., del Río Merino, M., Arrebola, C. V., & Wang, X. (2016). Effectiveness of greenhouse-gas emission trading schemes implementation: A review on legislations. Journal of Cleaner Production, 127, 49–58. https://doi.org/10.1016/j.jclepro.2016.03.148

- Voigt, S., De Cian, E., Schymura, M., & Verdolini, E. (2014). Energy intensity developments in 40 major economies: Structural change or technology improvement? Energy Economics, 41, 47–62. https://doi.org/10.1016/j.eneco.2013.10.015

- Wahab, S., Zhang, X., Safi, A., Wahab, Z., & Amin, M. (2021). Does energy productivity and technological innovation limit trade-adjusted carbon emissions? Economic Research-Ekonomska Istraživanja, 34, 1–16. https://doi.org/10.1080/1331677X.2020.1860111

- Wang, J., Wang, K., Shi, X., & Wei, Y. M. (2019). Spatial heterogeneity and driving forces of environmental productivity growth in China: Would it help to switch pollutant discharge fees to environmental taxes? Journal of Cleaner Production, 223, 36–44. https://doi.org/10.1016/j.jclepro.2019.03.045

- Wang, Y. F., & Zhang, S. Q. (2015). The dynamic effect of fiscal impulse to social welfare and macroeconomics: Analysis based on DSGE model. Journal of Central University of Finance & Economics, 4(3), 11–19.

- Weng, Z., Dai, H., Ma, Z., Yang, X., & Peng, W. (2018). A general equilibrium assessment of economic impacts of provincial unbalanced carbon intensity targets in China. Resources, Conservation and Recycling, 133, 157–168. https://doi.org/10.1016/j.resconrec.2018.01.032

- Westerlund, J. (2007). Testing for error correction in panel data. Oxford Bulletin of Economics and Statistics, 69(6), 709–748. https://doi.org/10.1111/j.1468-0084.2007.00477.x

- Wolde-Ghiorgis, W. (2002). Renewable energy for rural development in Ethiopia: The case for new energy policies and institutional reform. Energy Policy, 30(11-12), 1095–1105. https://doi.org/10.1016/S0301-4215(02)00061-7

- Wu, Y., Tam, V. W., Shuai, C., Shen, L., Zhang, Y., & Liao, S. (2019). Decoupling China's economic growth from carbon emissions: Empirical studies from 30 Chinese provinces (2001-2015). The Science of the Total Environment, 656, 576–588. https://doi.org/10.1016/j.scitotenv.2018.11.384

- Xie, J., Dai, H., Xie, Y., & Hong, L. (2018). Effect of carbon tax on the industrial competitiveness of Chongqing. Energy for Sustainable Development, 47, 114–123. https://doi.org/10.1016/j.esd.2018.09.003

- Xie, R. H., Yuan, Y. J., & Huang, J. J. (2017). Different types of environmental regulations and heterogeneous influence on “green” productivity: Evidence from China. Ecological Economics, 132, 104–112. https://doi.org/10.1016/j.ecolecon.2016.10.019

- Xie, Y., Dai, H., & Dong, H. (2018). Impacts of SO2 taxations and renewable energy development on CO2, NOx and SO2 emissions in Jing-Jin-Ji region. Journal of Cleaner Production, 171, 1386–1395. https://doi.org/10.1016/j.jclepro.2017.10.057

- Xu, B., & Lin, B. (2016). A quantile regression analysis of China's provincial CO2 emissions: Where does the difference lie? Energy Policy, 98, 328–342. https://doi.org/10.1016/j.enpol.2016.09.003

- Yang, F., Cheng, Y., & Yao, X. (2019). Influencing factors of energy technical innovation in China: Evidence from fossil energy and renewable energy. Journal of Cleaner Production, 232, 57–66. https://doi.org/10.1016/j.jclepro.2019.05.270

- Yi, Y. Y., & Li, J. X. (2018). Cost-sharing contracts for energy saving and emissions reduction of a supply chain under the conditions of government subsidies and a carbon tax. Sustainability, 10, 895.

- Youssef, S. B. (2020). Non-resident and resident patents, renewable and fossil energy, pollution, and economic growth in the USA. Environmental Science and Pollution Research, 27, 40795–40810.

- Zhou, Y., Fang, W., Li, M., & Liu, W. (2018). Exploring the impacts of a low-carbon policy instrument: A case of carbon tax on transportation in China. Resources, Conservation and Recycling, 139, 307–314. https://doi.org/10.1016/j.resconrec.2018.08.015

- Zhu, H., Duan, L., Guo, Y., & Yu, K. (2016). The effects of FDI, economic growth and energy consumption on carbon emissions in ASEAN-5: Evidence from panel quantile regression. Economic Modelling, 58, 237–248. https://doi.org/10.1016/j.econmod.2016.05.003