?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This paper develops a game-theoretic model that analyzes how a grocery store responds to the entry of a Walmart Supercenter using its store-format choice. By adopting a set of realistic assumptions, such as the cost advantage of Walmart and differentiated services of grocery stores, we find that the distance to a Walmart Supercenter is a key moderating factor in the store-format choice of grocery stores. Grocery stores would prefer to sell non-food items, but when sufficiently close to Walmart Supercenters they would specialise in food items, as consumers find it less costly to engage in two-stop shopping, making the gain from non-food items smaller. So an asymmetric equilibrium becomes feasible, wherein grocery stores carrying increasingly more non-food products and a new grocery store concept like Whole Foods and Wild Oats emphasising high-quality, organic foods can coexist. Our results yield important managerial implications. Under the specialisation strategy, the quality of its differentiated services should be sufficiently high, at least two to four times the disutility of two-stop shopping. Under the expansion strategy, grocery stores should engage in loss leadership, pricing non-food items below cost to lure large-basket consumers while earning higher margins from food items to compensate for the loss.

1. Introduction

The advent of the Supercenter format in 1988 has brought a drastic change to U.S. food retailing, catapulting Walmart to the top spot in grocery selling over Kroger and Safeway by 2000. One of the most prominent and recent changes in this industry is format blurring: A grocery store carries increasingly more product categories, with an emphasis on non-food items, to compete directly with a Walmart Supercenter.Footnote1 Seeming to contrast this trend is a new store concept, such as Whole Foods and Wild Oats, focussed on providing ‘highest quality natural and organic foods’ at premium prices to a niche market.Footnote2 There is no apparent answer to which of these strategies is optimal, and while prior studies of Walmart have examined its effects on various aspects of the U.S. economy, the effect of the Supercenter format on the store-format choice of grocery stores is not yet well understood. This paper develops a theoretical model to derive the optimal strategy of a grocery store for its store-format choice in response to the entry of a Walmart Supercenter and identifies the conditions under which one of the two strategies becomes optimal over the other.

Our research questions are as follows: Under what conditions does a grocery store specialise in food items or expand to non-food items (‘format blurring’)? Specifically, how does the distance to a Walmart Supercenter affect the store-format choice of a grocery store? We aim to ascertain if a grocery store, faced with competition from a Walmart Supercenter, responds by fundamentally changing its store format from a traditional grocer to a hybrid of a grocery store and a discount store. This decision would be moderated by a host of factors, such as any (dis)advantage in costs or services that a grocery store has over a Walmart Supercenter. Related to this question is: Does the store format choice affect the pricing strategies of a grocery store? Specifically, how does a grocery store set the prices of food and non-food items under the two different strategies of specialisation and expansion? Our aim here is to provide a possible mechanism behind the pricing strategy of both a grocery store underlying its store-format choice.

To address our research questions, we develop a game-theoretic model wherein a grocery store and a Walmart Supercenter located at the two ends of a linear city compete for the share of consumers using prices and (in the case of a grocery store) store-format choice. A Walmart Supercenter sells both food and non-food items, while a grocery store decides whether to specialise in food items or to expand to non-food items. Our model embodies a set of realistic assumptions: The marginal costs for both food and non-food items are lower for a Walmart Supercenter than for a grocery store. But a grocery store offers a unique set of differentiated services tailored to the needs of local consumers, such as fresh produce and meats, ethnic food selection, or an increased emphasis on deli, which a Walmart Supercenter cannot duplicate. Consumers can buy food items at one store and non-food items at the other, but they incur transportation costs based on the distance travelled for the entire shopping trip. So one-stop shopping becomes an important factor in our analysis, as consumers try to economise on time and costs spent on their shopping trips.

Our analysis shows that the distance from a Walmart Supercenter plays an important role in the store-format choice of a grocery store: Although a grocery store finds it optimal to expand to non-food items in most cases, it specialises in food items if sufficiently close to a Walmart Supercenter. The rationale behind this strategy is the following: Under the expansion strategy, a grocery store with a cost disadvantage adopts a loss-leader strategy by selling non-food items below costs, but it generates higher sales and profits for food items than under the specialisation strategy. As the two stores become sufficiently close, consumers find two-stop shopping less costly and start shopping food items at a grocery store but non-food items at a Walmart Supercenter, which reduces the gain from adopting non-food items for a grocery store. Even when a grocery store is sufficiently close to a Walmart Supercenter, the quality of differentiated services (the advantage of a grocery store) must be sufficiently high for the specialisation strategy to become a viable option. Specifically, the utility from differentiated services must be at least two to four times larger than the disutility from two-stop shopping for consumers. As an aside, there is only one possible equilibrium outcome under the expansion strategy: A Walmart Supercenter charges lower prices for both food and non-food items than a grocery store, which is consistent with actual prices of these two store types observed in the real world.

The rest of this paper is organised as follows. The next section discusses the theoretical background to our work, followed by the outline of our theoretical model in Section 3, where a grocery store, facing competition from a Walmart Supercenter, decides whether to specialise in food items or expand to non-food items. Section 4 identifies the conditions under which the grocery store adopts the specialisation (or expansion) strategy, where the analysis of the key model parameters, such as the distance between the two stores and differentiated services of the grocery store, results in strong managerial implications. Section 5 concludes, followed by the Appendix which shows the derivation of equilibrium prices and demands in Section 4.

2. Theoretical background

Our theoretical model builds on the earlier works of Lal and Matutes (Citation1989), Zhu et al. (Citation2011), and Rhodes and Zhou (Citation2019). These papers study the retail strategy, using product ranges and prices, of multiproduct firms and the equilibrium market structure. Central to modelling the competition between multiproduct firms is the idea of ‘one-stop shopping’, the ability to buy multiple products in a single shopping trip, which reduces search and transportation costs for consumers. We extend them by analysing the case where grocery stores can opt to choose between selling only food items (specialisation) and selling both food and non-food items (expansion) upon the entry of a Walmart Supercenter and deriving the conditions under which these strategies are optimal.

There is a growing body of literature on the retail strategy of multiproduct firms. Zhou (Citation2014) examines the relationship between consumer search costs and the prices of multiproduct firms, finding that multiproduct search can make product prices decrease with search costs. Rhodes (Citation2015) studies how a retailer’s product range affects its product, pricing and advertising decisions, while Shelegia (Citation2012) studies how the prices of two goods by multiproduct firms are correlated depending on whether they are complements or substitutes. Hagiu et al. (Citation2020) examine the conditions under which a multiproduct firm can offer a platform to its rival by inviting them to sell products or services on top of its core product. Hosting a platform can make the rival complement the multiproduct firm rather than competing with it. Similar to our study, Zhu et al. (Citation2011) consider how the entry of a low-cost discounter influences the pricing strategy of incumbent stores, finding that incumbents’ prices may go up for the products not sold by the new entrant.

There is also research on multiproduct firms and the equilibrium market structure (Armstrong & Vickers, Citation2010; Brandão et al., Citation2014; Lal & Matutes, Citation1989; Rhodes & Zhou, Citation2019). Armstrong and Vickers (Citation2010) study the effect of nonlinear pricing and bundling on consumer welfare and firm profit, while Lal and Matutes (Citation1989) model the competition between multiproduct firms with heterogeneous consumers. Both Armstrong and Vickers (Citation2010) and Lal and Matutes (Citation1989) assume that the market structure is exogenously symmetric, so all the firms end up with the same product range. Brandão et al. (Citation2014) incorporate two-stop shopping, extending Lal and Matutes (Citation1989), to study the competition between department stores and shopping malls, finding that the market structure of two shopping malls is expected to emerge in equilibrium. In contrast, Rhodes and Zhou (Citation2019) show how consumer search frictions can yield an asymmetric market structure, where large multiproduct firms and small firms with narrow product ranges can coexist.

We depart from these papers in the following aspects. In our model, the incumbents and the new entrant are asymmetric: The new entrant can procure goods more cheaply than the incumbents, whereas the incumbents offer differentiated services not provided by the new entrant. This setting mirrors the competition between grocery stores and Walmart Supercenters realistically, enabling us to provide a plausible explanation of the market structure found in the U.S. supermarket industry. While Zhu et al. (Citation2011) set the location of incumbents exogenously at the ends of a linear city, only considering the pricing strategy, we model the location of grocery stores to be endogenously determined, taking into account both pricing and product range decisions. Furthermore, our model, like Rhodes and Zhou, allows for the asymmetric equilibrium market structure, where some grocery stores adopt the specialisation strategy and others the expansion strategy. Finally, unlike other papers, we consider heterogeneous consumers who differ in both reservation price and transportation costs.

Our paper is also related to those papers that study Walmart’s effects on the U.S economy. These papers are mostly empirical, dealing with various Walmart-related topics, such as manufacturers’ channel coordination strategies in the presence of a dominant retailer (Chen, Citation2003; Cui et al., Citation2008; Dukes et al., Citation2006; Geylani et al., Citation2007; Raju & Zhang, Citation2005; Su & Mukhopadhyay, Citation2012); economies of density in Walmart’s store network (Holmes, Citation2011; Jia, Citation2008); competition between mass merchandisers (Ellickson et al., Citation2013; Zhu et al., Citation2009; Zhu & Singh, Citation2009); Walmart’s effects on consumer goods prices, including groceries (Basker, Citation2005; Basker & Noel,(Citation2009); Walmart’s effects on sales and employment of incumbent supermarkets (Ellickson & Grieco, Citation2013; Seenivasan & Talukdar, Citation2016; Singh et al., Citation2006); and Walmart’s effects on consumers’ store visits and per-visit spending (Hwang & Park, Citation2016). Our paper is more closely related to those papers that study the strategic responses of incumbent supermarkets due to Walmart’s entry, notably Ailawadi et al. (Citation2010) and Zhu et al. (Citation2011). We add to these papers by showing how cost advantages and differentiated services affect the adoption of non-food items by grocery stores and why grocery stores use the loss-leader pricing strategy on non-food items.

3. Model

Consider a population of consumers distributed uniformly along the interval [0,]. At one end of this city is a Walmart Supercenter (W) and at the other end a grocery store (G). Without loss of generality, store W is located at

and store G is at

Store W sells both food and non-food products, indexed by F and NF, at prices pW,F and pW,NF, respectively, while store G has two options of selling only food items (specialisation) and selling both food and non-food items (expansion) at prices pG,F and pG,NF, respectively.

Store W incurs a constant marginal cost cW, and store G incurs cG, for selling food and non-food items; the marginal cost of selling food items is assumed to be equal to that of selling non-food items (cW = cW,F = cW,NF and cG = cG,F = cG,NF), so that we can focus on the cost difference between stores W and G. Store W has a cost advantage over store G, and hence cW is assumed to be smaller than cG. This assumption is realistic in that Walmart maintains lower costs than supermarket chains such as Kroger, Albertsons, and Safeway (Singh et al., Citation2006). Without loss of generality, we set cW = 0 and cG > 0 and denote the cost difference by c = cG cW = cG

0 = cG.

Store G offers differentiated service for its food items, DS, which cannot be duplicated by store W. Here DS can be interpreted as the difference in service quality between stores G and W. For example, store G has a set of unique services that store W cannot match, such as fresh produce and meats, an increased emphasis on deli, and an improved focus on understanding local needs such as ethnic or organic foods (Chen & Rey, Citation2012; Singh et al., Citation2006). It is assumed that this service enhances the perceived value of shopping food items at store G, with the associated benefits of DS.

We assume a unit demand for both food and non-food items: Given pW,F, pW,NF, pG,F, pG,NF, and DS, every consumer buys at most one unit of foods and at most one unit of non-foods. There are two segments of consumers in the market: segment S (segment with a ‘small’ basket) that buys only food items and segment L (segment with a ‘large’ basket) that buys both food and non-food items. We use to denote the proportion of segment L in the population. This assumption is used to represent the difference in purchase frequencies of food and non-food items. On average, consumers buy food items more frequently than non-food items (Zhu et al., Citation2011). We simplify our analysis somewhat by assuming that consumers value both food and non-food items at V and that this value is high enough for the market to be fully covered.

Consumers incur the transportation cost for travelling to stores G and W. For mathematical simplicity, this cost is assumed to be linear in distance travelled, and the transportation cost per unit distance is assumed to be the same for all consumers and normalised to one. Consumers can save on the transportation cost by shopping for both food and non-food items at one store, which makes ‘one-stop shopping’ an important factor in the store choices.

Given pW,F, pW,NF, pG,F, pG,NF, and DS, the surplus at location x from consuming foods and non-foods at stores G and W can be expressed as follows:

Consumers in segment S who buy only food items choose store W if (or store G otherwise), whether store G sells only food items or sells both food and non-food items. So

is the location at which consumers in segment S are indifferent between stores G and W (

).

On the other hand, whether store G sells non-food items or not affects the store choice of consumers in segment L who buy both food and non-food items. If store G decides to sell only food items (‘the specialisation strategy’), consumers in segment L compare the surpluses from the following two options: buying food items at store G but non-food items at store W versus buying both food and non-food items at store W. So consumers in segment L will buy both food and non-food items at store W if or else they will buy food items at store G and non-food items at store W. So

is the location at which consumers in segment L are indifferent between the two shopping options if store G sells only food items. Of course, everybody in segment L buys non-food items at store W in this case.

Under the specialisation strategy, we can derive the demand functions as:

(1)

(1)

simply by referring to the definitions of

and

above.

If store G decides to sell both food and non-food items (‘the expansion strategy’), deriving the demand functions becomes more complex. As in Lal and Matutes (Citation1989), we consider three combinations of pW,F, pW,NF, pG,F and pG,NF: (1) pW,F < pG,F and pW,NF < pG,NF (or pG,F < pW,F and pG,NF < pW,NF), (2) pW,F < pG,F and pW,NF > pG,NF, and (3) pW,F > pG,F and pW,NF < pG,NF.

If one store offers lower prices for everything (pW,F < pG,F and pW,NF < pG,NF, or pG,F < pW,F and pG,NF < pW,NF), consumers in segment L will engage in one-stop shopping: That is, some consumers in segment L will buy everything at store G, while others will do the same at store W. Specifically, consumers in segment L at location x will buy everything at store W if or else they will buy everything at store G. So

is the location at which consumers in segment L are indifferent between buying everything at either store G or store W.

The demand functions for pW,F < pG,F and pW,NF < pG,NF, or pG,F < pW,F and pG,NF < pW,NF, can be derived as:

(2)

(2)

If store W sells food items at lower prices but non-food items at higher prices than store G, or pW,F < pG,F and pW,NF > pG,NF, consumers in segment L at location x will buy both food and non-food items at store W if the following condition holds:

or else they will buy food items at store W and non-food items store G, and

is the location at which they are indifferent between the two options. On the other hand, consumers in segment L at location x will buy both food and non-food items at store G if the following condition holds:

or else they will buy food items at store W and non-food items at store G, and

is the location at which they are indifferent between the two options. So if

consumers in segment L at

will buy both food and non-food items at store W, and those at

will buy both food and non-food items at store G, and those at

will buy food items at store W and non-food items at store G.

The demand functions for pW,F < pG,F, pW,NF > pG,NF and can be derived as:

(3)

(3)

If the two-stop shopping will not occur, so the demand functions will be the same as

and

Finally, we consider the case where store G sells food items at lower prices but non-food items at higher prices than store W, or pW,F > pG,F and pW,NF < pG,NF. Let be the location at which consumers in segment L are indifferent between the two options of buying both food and non-food items at store W and of buying food items at store G and non-food items at store W. And let

be the location at which consumers in segment L are indifferent between the two options of buying both food and non-food items at store G and of buying food items at store G and non-food items at store W.

Then the demand functions for pW,F > pG,F, pW,NF < pG,NF and can be derived as:

(4)

(4)

4. Analysis

Store G may or may not adopt non-food items, resulting in two scenarios: one under the specialisation strategy and the other under the expansion strategy. In both games, stores G and W simultaneously set food and non-food prices to maximise their respective profits. In what follows, we derive equilibrium outcomes for both games using backward induction. By comparing equilibrium outcomes between the two scenarios, we identify the conditions under which store G chooses to specialise in food items or expands to non-food items.

4.1. Specialisation strategy

Suppose that store G sells only food items. Given the demand functions

and

in EquationEquation (1)

(1)

(1) , stores W and G maximise their respective profits:

Solving the first-order conditions for and

yields the equilibrium prices for food itemsFootnote3:

(5)

(5)

Substituting and

with

and

in demand (

) and profit (

) functions, we obtain the equilibrium demands for food-items

(6)

(6)

and the equilibrium profits

(7)

(7)

where

To ensure that prices and demands for both segments S and L are positive, we require that the following inequalities hold:

and

Note that store G’s equilibrium strategies do not rely on store W’s monopoly pricing for non-food items.

The association between prices and demands, and parameters α, c, and DS are intuitive. For instance, DS affects positively but

negatively. In other words, higher quality of differentiated services gives store G the leverage to charge higher prices on its superior food items, and store W must charge lower prices on its inferior food items. In addition, the supply-side factor c (the cost difference between stores G and W) and the demand-side factor DS (the perceived value of differentiated services) are counterbalancing forces in shaping

and

As stores G and W get farther apart (or as d gets larger), the two stores become more geographically differentiated, so they can raise prices

and

resulting in less intense price competition.

4.2. Expansion strategy

Suppose now that store G sells both food and non-food items. Given the demand functions

and

for k = 2, 3, 4 in EquationEquations (2)–(4), stores W and G maximise their respective profits:

We first consider the case where one store offers lower prices for both food and non-food items: pW,F < pG,F and pW,NF < pG,NF, or pG,F < pW,F and pG,NF < pW,NF. Given consumer demands

and

solving the first-order conditions gives us equilibrium prices

(8)

(8)

equilibrium demands

(9)

(9)

and equilibrium profits

(10)

(10)

To ensure that equilibrium prices and demands are positive, we require that the following inequalities hold: and

In equilibrium store W charges lower prices for both food and non-food items than store G does: and

This finding is hardly surprising, as the costs for both food and non-food items are lower for store W than for store G. At the same time, store G has differentiated services that store W cannot duplicate, which in turn enables store G to charge the higher price for its food items than store W does. So DS enables store G to charge higher prices for its food items than for its non-food items despite our assumption that the costs for both food and non-food items are the same: cW = cW,F = cW,NF and cG = cG,F = cG,NF. Surprisingly, store G engages in loss leadership by selling its non-food items below cost:

using non-food items strictly to lure consumers in segment L into the store while earning higher margins from food items to compensate for the loss.Footnote4 Finally, store W earns higher profits than store G, or

if and only if

so the magnitudes of

and

determines whether store G or W becomes more profitable.

Result 1.

If Store G follows an expansion strategy, Store W charges lower prices for both food and non-food items than store G does: and

Result 2.

If Store G follows an expansion strategy, it charges higher prices for food items than for non-food items, or and sells non-food items below costs:

We now consider the case where store W sells food items at lower prices but non-food items at higher prices than store G: pW,F < pG,F and pW,NF > pG,NF. Given consumer demands

and

we can solve the first-order conditions for equilibrium prices:

Recall from Section 3 that

and

must satisfy

However, it is easily shown that

so

and

cannot constitute an equilibrium.

Finally, we consider the case where store W sells non-food items at lower prices but food items at higher prices than store G: pW,NF < pG,NF and pF,N > pG,F. Given consumer demands

and

we can solve the first-order conditions for equilibrium prices:

Here is necessary to ensure that

Recall from Section 3 that

must be true for

The two inequalities again contradict each other, so

and

do not constitute an equilibrium.

4.3. Optimal strategy for a grocery store

We now turn our attention to the optimal strategy of store G for choosing its store format in competing with store W. Since our main interest lies in the two strategic options of store G—namely, specialisation and expansion strategies—our analysis focuses on the market condition under which both strategies are feasible. For parameter values satisfying

comparing equilibrium prices in EquationEquations (5)

(5)

(5) and Equation(8)

(8)

(8) and demands in EquationEquations (6)

(6)

(6) and Equation(9)

(9)

(9) for the two strategic options of store G allows us to ascertain the change in store G’s profits when switching its store format.

Result 3.

We find that whereas

if and only if

Result 3 says that store G always enjoys higher prices and margins for its food items when it sells non-food items than it does not. This is because, under the expansion strategy, store G does not need to lower its price on food items so much as to compensate for the large-purchase consumer’s disutility from two-stop shopping. It also says that store G enjoys the higher demand for food items when selling non-food items under the expansion strategy, if and only if the cost of two-stop shopping, as represented by the distance travelled (d), is larger than the perceived difference in service quality between stores G and W (DS).

To identify the conditions under which store G sells only food items (or sells both food and non-food items), we compare the equilibrium profits between the specialisation and expansion strategies. Given and

in EquationEquations (7)

(7)

(7) and Equation(10)

(10)

(10) , store G prefers to sell only food items if and only if

or else it prefers to sell both food and non-food items.

Our analysis shows that if and only if

So store G chooses to sell only food items when it is close enough to store W, or store G chooses to sell both food and non-food items (or ), when it is sufficiently far away from store W (or

).

Result 4.

Store G adopts the specialisation strategy if its distance to store W is smaller than the threshold or else it adopts the expansion strategy.

The reasoning behind Result 4 is as follows: As stores G and W get closer, consumers in segment L find it less costly to engage in two-stop shopping, making store G’s gain in profits from carrying non-food items smaller. The cost disadvantage (c) further reduces the incentive for store G to carry non-food items (which are sold at loss). Consequently, as the distance between the two stores gets smaller, the expansion strategy becomes less attractive to store G, and below the threshold value of d*, the specialisation strategy is always preferred.

shows the comparison of store G’s profits between the specialisation and expansion strategies, where Region A is where the specialisation strategy is chosen over the expansion strategy. The size of Region A is relatively small (even for varying parameter values), which implies that it is often more profitable for store G to expand to non-food items.

Figure 1. Comparison of store G’s profits between the specialisation and expansion strategies (c = 0.5, α = 0.5). A: B:

C: Non-feasible areas, Dashed line:

Source: Authors.

![Figure 1. Comparison of store G’s profits between the specialisation and expansion strategies (c = 0.5, α = 0.5). A: ΠG1*−ΠG2*>0, B: ΠG1*−ΠG2*<0, C: Non-feasible areas, Dashed line: DS=[c(1+α)].Source: Authors.](/cms/asset/673a23df-30df-44e4-9c48-296a2c5166e4/rero_a_1962384_f0001_b.jpg)

We have access to limited information on the actual store-format choices of grocery stores in a Southern state for the year 2006. Out of roughly one hundred and fifty stores, about twelve percent of them sold only food items, consistent with a small size of Region A in . For grocery stores that adopted the specialisation strategy (i.e., grocery stores without any non-food departments), the average distance to the nearest Walmart Supercenter is about 4.4 miles, whereas for grocery stores that adopted the expansion strategy it was about 6.3 miles, the difference of nearly 2 miles. So as Proposition 1 predicts, a grocery store closer to a Walmart Supercenter tends to adopt the specialisation strategy than the one farther apart. Although our data are too limited in information to allow a full-scale, rigorous empirical analysis, these summary statistics are still supportive of our key hypothesis.

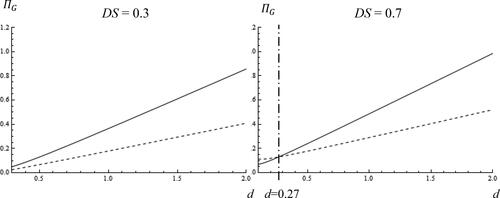

shows how changes along with the distance between stores G and W. If

the difference in store G’s profits of selling both food and non-food items over selling only food items is increasing in the distance from store W, or

Note that when DS is too small (for example, DS = 0.3), the expansion strategy is the dominant strategy as it always yields higher profits than the specialisation strategy. Store G is always better off adopting non-food items, as (without sufficient support of differentiated service) the gain in higher store traffics from carrying non-food items is bigger than the loss from selling non-food items. So the quality of differentiated service must be fairly high (specifically,

)Footnote5 for the specialisation strategy to even be feasible.

Figure 2. Store G’s profits for different levels of service (c = 0.5, α = 0.5). Dashed line = Straight line =

Source: Authors.

Result 5.

Store G obtains larger profits under the specialisation strategy relative to the expansion strategy only if the quality of differentiated services is sufficiently high, i.e., Or else, the expansion strategy is the more profitable option for store G.

Results 4 and 5 show that if the quality of differentiated service is sufficiently high (), the distance between stores G and W must be less than a certain cutoff value (

), for store G to choose the specialisation strategy. But how high should be the level of DS to compensate for the disutility of consumers in segment L from two-stop shopping so that store G can sell only food items?

Let us look at an example where the distance between stores G and W is set at d = 0.27 in , where c = 0.5 and α = 0.5. In this case, for store G to adopt the specialisation strategy, the minimum level of DS is 0.7. In other words, the utility from differentiated services must be at least 2.6 (DS/d = 0.7/0.27) times the disutility from travelling for two-stop shopping, or else store G is better off adopting the expansion strategy.

To investigate this question more thoroughly, we compute DS/d* for different values of parameters and c, where d* in Region A is represented by a bold curve on the top of Region A in . For each combination of the two parameter values, a set of DS/d* is generated by computing DS/d* numerically for all values of DS obtained by the grid search with an interval of 0.025 within the feasible range of DS in Region A. presents the summary statistics for the data sets of DS/d*, which is the minimum value of DS/d in the entire Region A. The utility from differentiated services, on average, must be at least 2 to 4 times larger than the disutility from travelling the distance between two stores, as the means of DS/d* ranges from 2.18 to 4.01 in this table. So, even if store G is located sufficiently close to store W such that the specialisation strategy is feasible, store G must be capable of offering a high enough quality of differentiated services for the specialisation strategy to be a viable option.

Table 1. Examination of [DS/d*] for different parameter values.

Result 6.

For the specialisation strategy to be a viable option for store G, the utility from differentiated services (DS) must be at least 2 to 4 times larger than the disutility from two-stop-shopping for consumers in segment L.

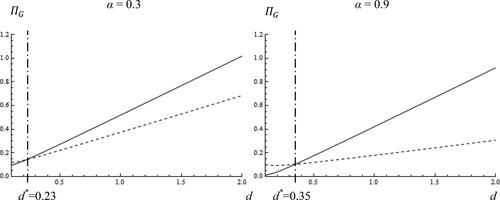

also shows that the value of DS/d* decreases as the proportion of segment L () in the market increases. Our numerical analysis shows that

In , if

increases from 0.3 to 0.9, d* increases from 0.23 to 0.35 for c = 0.5 and DS = 0.7 and, as a result, DS/d* decreases from 3.1 to 2.02. An increase in

has two profit effects: Under the specialisation strategy, two-stop shopping becomes a more prominent factor in the L-segment consumer’s store choice at a higher level of

while under the expansion strategy, a higher level of

implies that store G must cater to more L-segment consumers who are more costly to serve. Recall that non-food items, for example, are being sold at loss. Our derivation that

is simply saying that the latter profit effect is larger than the former.

Figure 3. Store G’s profits for different α values (c = 0.5, DS = 0.7).

Source: Authors.

shows that DS/d* does not vary much with c—the incremental cost of store G over store W—or that the level of differentiated services required for store G to adopt the specialisation strategy is independent of the size of its cost disadvantage. Store G must offer a higher level of services to compensate for the disutility of two-stop shopping.

Our main results are robust to different values of c and α, although a change in parameter values gives rise to the variation in shapes of the regions A, B, and C, as seen in . For example, the area of Region A gets smaller, as the cost disadvantage drops from c = 0.9 to c = 0.1, implying that as the cost disadvantage disappears, it becomes more likely for store G to adopt the expansion strategy. In this sense, DS and c are two sides of the same coin: Below a certain threshold of c, store G always adopts the expansion strategy, similar to our claim in Result 5.

Figure 4. Store G’s profits for different values of c and α. A: B:

C: Non-feasible areas, Dashed line:

Source: Authors.

![Figure 4. Store G’s profits for different values of c and α. A: ΠG1*−ΠG2*>0, B: ΠG1*−ΠG2*<0, C: Non-feasible areas, Dashed line: DS=[c(1+α)].Source: Authors.](/cms/asset/85aa0184-9875-4ea6-abc3-2f871d5c6a76/rero_a_1962384_f0004_b.jpg)

5. Conclusion

This paper has studied the role of the Supercenter format in the store-format choice of grocery stores. Our interest lies in solving an apparent paradox: There is a phenomenon of ‘format blurring’ wherein grocery stores emulate the Supercenter format by adopting ever more product categories, especially non-food items. At the same time, the new store concept, such as Whole Foods and Wild Oats, competes with the Supercenter format by providing high-quality, organic food items. When do these strategies become optimal for a grocery store competing with a Walmart Supercenter? To this end, we have developed a game-theoretic model that accommodates the cost advantage of a Walmart Supercenter, the differentiated services of a grocery store, and the one-stop shopping by customers. Our analysis yields the conditions under which a grocery store specialises in food items or expands to non-food items.

Our analysis has produced the following results. In most cases, grocery stores would emulate the Supercenter format by expanding to non-food items, and under this expansion scenario, our analytical derivation shows that a grocery store engages in loss leadership by selling non-food items below costs to increase store traffic but sells food items at higher margins. The key insight here is that non-food items are used only to lure consumers into grocery stores. Nevertheless, some grocery stores would adopt the specialisation strategy by selling food items only especially when they are sufficiently close to a Walmart Supercenter. Our insight into this finding is as follows. Travel costs of two-stop shopping for shoppers would diminish as the two stores get close by, so grocery stores can generate enough store traffic without adding non-food items on their shelf space. But even when sufficiently close to a Walmart Supercenter, our analytical derivation shows that a grocery store must provide high-quality differentiated services on its food items to be profitable.

Our paper has several managerial implications. First, let us consider a grocery store that opts to specialise in food items and forgo non-food items. Our theoretical derivation shows that the quality of its differentiated services must be sufficiently high. Differentiated services cannot simply compensate for the travel costs of consumers from two-way shopping. Rather, the utility from differentiated services must be at least two to four times larger than the disutility of two-stop shopping. Going back to our discussion on differentiation services, the grocery store opting to specialise in food items should raise the utility from differentiated services by delivering fresh produce and meats, providing a wide variety of ethnic foods, and increasing its emphasis on deli, to the degree that a Walmart Supercenter cannot duplicate. Second, let us now consider a grocery store that opts to expand to non-food items. Our theoretical derivation shows that it should engage in loss leadership by selling its non-food items below cost, thus using non-food items to lure large-basket consumers into the store and charging higher margins for its food items to compensate for the loss.

Our analysis is a contribution to the literature on the retail strategy of multiproduct firms and the resultant market structure. Papers in this area have studied how consumer search costs affect the pricing strategy of multiproduct firms (Zhou, Citation2014) and how the product range of a multiproduct firm affects its pricing strategy (Rhodes, Citation2015; Shelegia, Citation2012). Similar to our analysis, Zhu et al. (Citation2011) consider how the entry of a low-cost discounter affects the pricing strategy of incumbent stores, although they do consider the decision to adopt non-food items by incumbent stores. Other papers study the equilibrium market structure with multiproduct firms (Armstrong & Vickers, Citation2010; Lal & Matutes, Citation1989; Rhodes & Zhou, Citation2019). Of particular interest to us is Rhodes and Zhou (Citation2019), as they show the existence of an asymmetric market structure, where large multiproduct firms and small firms with narrow product ranges coexist. Our analysis differs from the earlier efforts in the following ways. First and foremost, our theoretical model embodies the real-world scenario with the setup of a low-cost entrant, a Walmart Supercenter, and the incumbents with differentiated services, grocery stores. Furthermore, the locations of incumbents are endogenously determined, and consumers are assumed to be heterogeneous in reservation price as well as transportation costs in our model. Consequently, our analytical results offer a plausible explanation in line with the real-world phenomena, such as the loss-leading pricing of non-food items by grocery stores and the co-existence of grocery stores that carry increasingly more non-food products and a new grocery store concept like Whole Foods and Wild Oats that focuses on high-quality, organic foods.

We close out this section by pointing out the limitations of our study. First and foremost, our model is a simplified version of the real retail environment. Admittedly, a more complicated and realistic model may add other dimensions—for example, product variety of a store—in the analysis. Such a model, incorporating, say, the difference in the number of SKUs between a grocery store and a Walmart Supercenter, may produce even more interesting and useful insights for store managers. Secondly, the other important dimension, service quality, may become a choice variable for the firm. By treating it as exogenously given, our model abstracts from this decision to pursue a niche strategy of specialising in quality foods and related services. Relaxing these and other assumptions of our model, such as changing the unit-demand assumption to reflect the heterogeneity of basket sizes across consumers, are left for future research.

Disclosure statement

No potential conflict of interest was reported by the authors.

Notes

1 RETAIL USA: What's In Store 2016? Todd Hale, Senior Vice President, Consumer & Shopper Insights, Nielsen

3 See the Appendix for the derivation of equilibrium solutions for this and other cases.

4 Similar to this finding, Chen and Rey (Citation2012) show that large retailers use loss leading on products of smaller rivals to discriminate multi-stop shoppers from one-stop shoppers.

5 This condition () is obtained from the intersection of d* and one of the boundary constraints (

).

References

- Ailawadi, K. L., Zhang, J., Krishna, A., & Kruger, M. W. (2010). When Wal-Mart enters: How incumbent retailers react and how this affects their sales outcomes. Journal of Marketing Research, 47(4), 577–593. https://doi.org/10.1509/jmkr.47.4.577

- Armstrong, M., & Vickers, J. (2010). Competitive non-linear pricing and bundling. Review of Economic Studies, 77(1), 30–60. https://doi.org/10.1111/j.1467-937X.2009.00562.x

- Basker, E. (2005). Selling a cheaper mousetrap: Wal-Mart’s effect on retail prices. Journal of Urban Economics, 58(2), 203–229. https://doi.org/10.1016/j.jue.2005.03.005

- Basker, E., & Noel, M. (2009). The evolving food chain: Competitive effects of Wal-Mart’s entry into the supermarket industry. Journal of Economics & Management Strategy, 18(4), 977–1009. https://doi.org/10.1111/j.1530-9134.2009.00235.x

- Brandão, A., Correia-da-Silva, J., & Pinho, J. (2014). Spatial competition between shopping centers. Journal of Mathematical Economics, 50, 234–250. https://doi.org/10.1016/j.jmateco.2013.09.002

- Chen, Z. (2003). Dominant retailers and the countervailing-power hypothesis. The RAND Journal of Economics, 34(4), 612–625. https://doi.org/10.2307/1593779

- Chen, Z., & Rey, P. (2012). Loss leading as an exploitative practice. American Economic Review, 102(7), 3462–3482. https://doi.org/10.1257/aer.102.7.3462

- Cui, T. H., Raju, J. S., & Zhang, Z. J. (2008). A price discrimination model of trade promotions. Marketing Science, 27(5), 779–795. https://doi.org/10.1287/mksc.1070.0314

- Dukes, A., Gal-Or, E., & Srinivasan, K. (2006). Channel bargaining with retailer asymmetry. Journal of Marketing Research, 43(1), 84–97. https://doi.org/10.1509/jmkr.43.1.84

- Ellickson, P. B., & Grieco, P. L. E. (2013). Wal-Mart and the geography of grocery retailing. Journal of Urban Economics, 75, 1–14. https://doi.org/10.1016/j.jue.2012.09.005

- Ellickson, P. B., Houghton, S., & Timmins, C. (2013). Estimating network economies in retail chains: A revealed preference approach. The Rand Journal of Economics, 44(2), 169–193. https://doi.org/10.1111/1756-2171.12016

- Geylani, T., Dukes, A. J., & Srinivasan, K. (2007). Strategic manufacturer response to a dominant retailer. Marketing Science, 26(2), 164–178. https://doi.org/10.1287/mksc.1060.0239

- Hagiu, A., Jullien, B., & Wright, J. (2020). Creating platforms by hosting rivals. Management Science, 66(7), 3234–3248. https://doi.org/10.1287/mnsc.2019.3356

- Holmes, T. J. (2011). The diffusion of Wal-Mart and economies of density. Econometrica, 79(1), 253–302.

- Hwang, M., & Park, S. (2016). The impact of Walmart Supercenter conversion on consumer shopping behavior. Management Science, 62(3), 817–828. https://doi.org/10.1287/mnsc.2014.2143

- Jia, P. (2008). What happens when Wal-Mart comes to town: An empirical analysis of the discount retailing industry. Econometrica, 76, 1263–1316.

- Lal, R., & Matutes, C. (1989). Price competition in multimarket duopolies. The RAND Journal of Economics, 20(4), 516–537. https://doi.org/10.2307/2555731

- Raju, J., & Zhang, J. (2005). Channel coordination in the presence of a dominant retailer. Marketing Science, 24(2), 254–162. https://doi.org/10.1287/mksc.1040.0081

- Rhodes, A. (2015). Multiproduct retailing. The Review of Economic Studies, 82(1), 360–390. https://doi.org/10.1093/restud/rdu032

- Rhodes, A., & Zhou, J. (2019). Consumer search and retail market structure. Management Science, 65(6), 2607–2623. https://doi.org/10.1287/mnsc.2018.3058

- Seenivasan, S., & Talukdar, D. (2016). Competitive effects of Wal-Mart Supercenter entry: Moderating roles of category and brand characteristics. Journal of Retailing, 92(2), 218–225. https://doi.org/10.1016/j.jretai.2015.09.003

- Shelegia, S. (2012). Multiproduct pricing in oligopoly. International Journal of Industrial Organization, 30(2), 231–242. https://doi.org/10.1016/j.ijindorg.2011.10.001

- Singh, V. P., Hansen, K. T., & Blattberg, R. C. (2006). Market entry and consumer behavior: An investigation of a Wal-Mart Supercenter. Marketing Science, 25(5), 457–476. https://doi.org/10.1287/mksc.1050.0176

- Su, X., & Mukhopadhyay, S. K. (2012). Controlling power retailer’s gray activities through contract design. Production and Operations Management, 21(1), 145–160. https://doi.org/10.1111/j.1937-5956.2011.01245.x

- Zhou, J. (2014). Multiproduct search and the joint search effect. American Economic Review, 104(9), 2918–2939. https://doi.org/10.1257/aer.104.9.2918

- Zhu, T., & Singh, V. (2009). Spatial competition with endogenous location choices: An application to discount retailing. Quantitative Marketing and Economics, 7(1), 1–35. https://doi.org/10.1007/s11129-008-9048-6

- Zhu, T., Singh, V., & Dukes, A. (2011). Local competition, entry, and agglomeration. Quantitative Marketing and Economics, 9(2), 129–154. https://doi.org/10.1007/s11129-011-9097-0

- Zhu, T., Singh, V., & Manuszak, M. D. (2009). Market structure and competition in the retail discount industry. Journal of Marketing Research, 46(4), 453–466. https://doi.org/10.1509/jmkr.46.4.453

Appendix

Derivation of equilibria under the specialisation strategy

Given the demand functions in EquationEquation (1)(1)

(1) , store W and G have the following profit maximisation problems:

Solving the first-order conditions of stores W and G

results in the equilibrium prices

The second-order conditions and

are satisfied here.

Only store W sells non-food items and consumer valuation V is sufficiently high for the market to be fully covered, so we have So store W raises

until

to maximise its profits, given the constraints for non-negativity of the consumer surpluses for segment L and the boundary constraints for non-negativity of prices and demands shown in section 4.1. It is then straightforward to derive the equilibrium demands and profits as in EquationEquations (6)

(6)

(6) and Equation(7)

(7)

(7) .

Derivation of equilibria under the expansion strategy

Among three different scenarios (k = 2, 3, 4), equilibrium outcomes are obtained only for k = 2, where pW,F < pG,F and pW,NF < pG,NF (or pG,F < pW,F and pG,NF < pW,NF). Given the demand functions

and

in EquationEquations (2)

(2)

(2) , store W and G have the following profit maximisation problems:

Solving the first-order conditions of stores W and G

results in the equilibrium prices

The second-order conditions are satisfied, as the Hessian matrix

is negative definite for any value of

and

where j = G, W.

Substituting

and

with

and

in the demand functions

and

as well as the profit functions

and

it is straightforward to derive the equilibrium demands and profits as in EquationEquations (9)

(9)

(9) and Equation(10)

(10)

(10) .

Let us now consider the two other cases (k = 3, 4), both of which do not constitute an equilibrium. Given the demand functions

and

in EquationEquations (3)

(3)

(3) , the first-order conditions of the profit functions

and

with respect to prices are:

Lastly, given the demand functions

and

in EquationEquations (4)

(4)

(4) , the first-order conditions of the profit functions

and

with respect to prices are:

We can solve for prices using the above first-order conditions for each case, but those solutions do not constitute an equilibrium as shown in Section 4.2.