?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

In the past 30 years, Jiangsu Province in China has achieved great feats regarding its export trade; however, its export trade growth rate has not only been showing a recent downward trend but also great fluctuations. Hence, the competitiveness of Jiangsu Province’s export products seems to have weakened. Through an empirical analysis, we demonstrate the relationship between financial development and export trade in Jiangsu Province, showing that the influence of financial development on the growth and the structure of provincial export trade is relatively weak. Thus, we believe that provincial financial development lacks coordination with export trade, requiring further efforts from actors at coordinating both. This paper puts forward relevant suggestions that may facilitate stakeholders to promote the steady development, transformation, and improvement of Jiangsu Province’s export trade.

1. Introduction

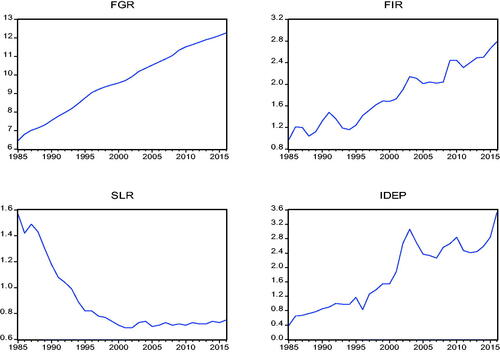

Jiangsu Province’s financial industry has developed rapidly during the past decades and is characterised by diversity, high efficiency, and internationality. Additionally, in China, financial institutions generally have high benefits and have been at the forefront of national financial reforms and innovation. Jiangsu Province, in particular, has achieved great feats regarding financial development. In 1985, the total provincial deposit and loan was 63.418 billion yuan; by 2016, it had reached 1210.658 billion yuan (: the FGR considers the sum of deposits and loans, and then considers the logarithm); hence, it showed an increasing trend. Moreover, the financial interrelations ratio (FIR), calculated as the ratio between total financial assets and the gross domestic product (GDP), increased from 0.97 in 1985 to 2.79 in 2016. Nonetheless, the loan-to-deposit ratio (SLR) declined from 1.57 in 1985 to 0.82 in 1995. Further, upon China’s implementation of the new Commercial Bank Law, which strictly controlled the SLR at 0.75, the SLR of Jiangsu Province became relatively stabilised. Additionally, since 1985, the provincial insurance depth index (IDEP), calculated as the ratio between insurance premium income and the GDP, has shown a relatively stable growth trend.

Figure 1. Variation trend of Jiangsu Province’s financial development indicators from 1985–2016.

Source: Jiangsu Province Bureau of statistics (http://tj.jiangsu.gov.cn/index.html) and the China Banking and Insurance Regulatory Commission. (http://www.cbirc.gov.cn/).

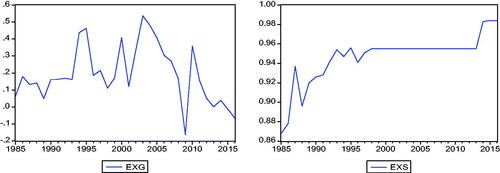

Hence, as an economically developed coastal region, Jiangsu Province’s export trade, being the main mechanism of its economic growth, occupies an extremely important share in its total economic output. Since China’s reform and opening up, Jiangsu Province has also achieved important export trade goals, as follows: The export value of foreign trade increased from US$1.586 billion in 1985 to US$324.42 billion in 2016, an increase of 204.6 times (all data cited are taken from the Jiangsu Province Statistical Yearbook). However, recently, the annual export trade growth rate (EXG) of Jiangsu Province has shown large fluctuations, indicating that its competitiveness in export trade is weakened; the EXG reached 53.69% in 2003, but went on to decline to its lowest rate (−16.3%) in 2009. This demonstrates that the international financial crisis of 2008 severely affected the provincial export trade. The rebound, in 2010, was again followed by a steady decline in the EXG. The ratio between the exports of manufactured goods and total exports increased rapidly from 1985 to 1995; afterwards, it remained stable, and started to increase slightly only since 2016 ().

Figure 2. Trend of annual export trade growth rate and export rate structure from 1985–2016.

Source: Jiangsu Province Bureau of statistics (http://tj.jiangsu.gov.cn/index.html) and the China Banking and Insurance Regulatory Commission. (http://www.cbirc.gov.cn/).

Currently, China’s financial system is facing major changes; the degree of marketisation is accelerating and new forms of financial development are emerging, providing strong support for economic development. Therefore, to ensure the stable growth of Jiangsu Province’s export trade, research should focus on the role of institutional factors, on the comparative advantages of the financial system, and on the provision of financial support to this region—all while ensuring that the province makes full use of various governmental resource endowments.

The remainder of this paper is structured as follows: Section 2 includes a literature review. In Section 3, we use the Gelin–Berthou model to analyse the general impact of financial development on export trade. In Section 4, we use data from Jiangsu Province to analyse the impact of provincial financial development on provincial export trade. Finally, we describe potentially relevant measures based on the results of the empirical analysis and the current condition of Jiangsu Province’s financial development.

2. Literature review

2.1. Influence of financial development on international trade

The traditional neoclassical economic growth theory does not consider funding to be important for economic growth, suggesting that the financial system is not essential for it. In this theory, economic growth occurs majorly due to technological advancements generated by factor accumulation and innovation (Ginevičius et al., Citation2019). Using a resource-based framework, Camisón-Haba et al. (Citation2019) found that companies can become technology-based and/or highly innovative firms when they are able to accumulate a high endowment of knowledge and technological capabilities. The accumulation of knowledge and technology, nonetheless, requires financial support. With the deepening of research on finance, Svilokos et al. (Citation2019) suggested that the role of the financial sector is very important for determining industrialisation level. Worldwide, national policymakers and banking sectors have been endeavouring to raise financial inclusion levels and stimulate sustainable economic growth (Nizam et al., Citation2020).

Moreover, new trade theories posit that not only factor endowment, technology, and economies of scale (i.e., concepts emphasised by traditional trade theories) but also institutional factors can have an impact on export trade. Thus, they demonstrate that the financial system indeed has a great impact on export trade and economists should pay attention to it. Kletzer and Bardhan (Citation1987) believed that even if technology and factor endowment were similar between two countries, owing to the imperfect credit market world, these countries would differ in the formation of comparative costs and trade patterns. Specifically, organisations are required to cover the costs of entering the international market before they can profit from export trade. Under sovereign risk, countries with low financial development face higher equilibrium interest rates, which encourage the national firms to avoid the specialised production of complex products because such products require more working capital, sale costs, and trade finance. Therefore, compared with countries with low financial development, those with high financial development have an advantage in the production of manufactured goods.

By generating comparative advantage, we can infer that the manufactured goods industry of high financially developed countries has a higher external financing dependence, thus benefitting more from the reduction of financing costs brought by financial development (Yao & Shi, Citation2013). Moreover, Manova (Citation2013), using local equilibrium analysis, proposed that for ensuring the export of enterprises, there is a need to overcome fixed costs, a variable that is dependent on national financial development level. Particularly, overcoming fixed costs may be done by the internal financing of export enterprises and bank loans. Therefore, the threshold for enterprises to export is dependent on industry characteristics and their own tangible assets: if enterprises have less fixed assets, or if the external financing needs of the industry in which the enterprises are located are higher, then the threshold for companies to export will also be higher.

To solve this financing problem, companies may need to rely on external financial support. Indeed, Manova (Citation2013) demonstrated that credit constraints are an important determinant of export trade patterns. Ma and Xie (Citation2019) also theorised that the financial development of a destination country is as important as that of the originating country in shaping bilateral trade patterns; this serves for both the extensive margin and the intensive margin of export trade. Furthermore, Monteiro et al. (Citation2019) investigated how intangible resources (financial, informational, and relational resources), dynamic capabilities, and entrepreneurial orientation impacted export trade performance. The intangible resources exerted a positive and direct influence on the development of dynamic capabilities, which in turn affected export performance. Therefore, even under the same conditions of labour resources, natural endowments, and economies of scale, a country’s financial development can still constitute comparative advantages.

2.2. Empirical test of the influence of financial development on international trade

Beck (Citation2002, Citation2003) conducted an in-depth study on external financing dependence based on the theory proposed by Kletzer and Bardhan (Citation1987). Based on empirical findings, these studies posited that countries with high financial development could meet the external financing needs of trading enterprises and promote economies of scale, resulting in a large export trade. Moreover, Liu and Zhang (Citation2016) empirically found that financial development is an important factor influencing trade structure and comparative advantage. Further, Qi and Wang (Citation2016) underpinned that financial development has a different impact on the net technical complexity of exports in different industries, as well as that the financial development level of industries with high external financial dependence had a significant effect on the improvement of the net technical complexity of exports. From the perspective of external financing dependence, Geng and Hao (Citation2017) empirically tested the relationship between the purchasing of intermediate products by the United States of America from a country and the trading country financial development level. They showed that when multinational companies choose the location of an international production network, they distribute complex production links in countries with high financial development; this serves to improve the efficiency of enterprise resource allocation at the micro-level.

In the context of China, Manova et al. (Citation2015) proposed that credit constraints currently restrict export trade and affect the business model of multinational companies. Specifically, foreign-funded enterprises and joint ventures were shown to have better export behaviour in this financially vulnerable sector than private enterprises; this is primarily owing to the possibility of obtaining financial support from their parent company, easing credit constraints. Additionally, Xu et al. (Citation2019) showed that financial development has a significant and robust impact on export duration by easing the financing constraints of organisations. Liu and Yang (Citation2020) went on to examine the exit and entry of export organisations by export quality, aiming to define the role of financial development in export market share. Through a regression analysis, they showed that there is an inverse U-shaped relationship between financial development and export quality. Financial development also played a vital role in the strategic competition of enterprises regarding the choice of export quality and the lower price of products for different export quality firms. Finally, it indirectly affected export market share.

2.3. Impact of financial development on provincial export trade

China has an uneven provincial economic development, evoking significant variations for the export trade of different provinces. Accordingly, whether inter-provincial financial development influences export trade has gained scholarly attention. Zhao (Citation2007) and Gao (Citation2010), for example, empirically analysed financial development and export trade relations in Hubei and Jiangsu Provinces and showed that financial development had a positive effect on export trade. In another empirical study, Jiao and Zhang (Citation2012) explored the relationship between financial development and export trade in Zhejiang Province using the following variables: FIR, credit transfer rate, the dependence of foreign trade, and the foreign trade commodity structure index. They noticed that a long-term relationship existed between Zhejiang Province’s export trade scale and financial development efficiency; they concluded that financial development had important effects on the sustainable development of export trade. Hence, their study depicts the importance of financial development to export trade growth.

Jiang and Cha (Citation2013) also conducted an empirical study in Shanghai to investigate the impact of financial development on export growth, describing that the scale effect of Shanghai’s financial development on export growth was insignificant. Instead, financial development played a major role in promoting export structure optimisation; specifically, it promoted the export of capital- and technology-intensive mechanical and electrical products, which are highly dependent on external financing, providing evidence of how financial development has a great impact on industries with a high degree of external financing dependence. Meanwhile, Ji and Cheng (Citation2015), while examining the impact of Beijing’s financial development on export trade, observed that the relationship between financial development and export trade structure did not pass the Granger causality test; specifically, Beijing’s financial development did not seem to support the optimisation of the export trade structure.

As pointed out in this literature review, China’s provincial economic development is extremely uneven. Accordingly, we see value in discussing whether these aforementioned conclusions are suitable for the economic status quo of Jiangsu Province. Therefore, this study aims to investigate the impact of financial development on the export trade of Jiangsu Province. Our research data may be helpful for stakeholders aiming to assess the financial development difficulties that affect the provincial export trade; specifically, we hope that this research will facilitate well-informed decisions for corresponding countermeasures.

3. Theoretical model

According to Berthou’s (Citation2010) theoretical model, we assumed that the consumption utility function of country j was:

(1)

(1)

where

is the consumption of manufactured goods; and

is the consumption of primary products. The consumption of manufactured goods, meanwhile, can be described as follows:

(2)

(2)

where

is the diversified product consumption set produced by industry k in country j; meanwhile,

is the consumption quantity of each diversified commodity in country j. Moreover,

is the difference index of the products in industry k, and

is the elasticity of substitution.

Thereafter, if we assume that the production of technology and of primary products has same scale return implications, can be freely traded, and can be used as the currency exchange standard, it allows us to standardise the wages in countries i and j to Meanwhile, diversified product can be defined as the industrial finished product, and it has the characteristic of increasing returns to scale. Then, its production cost is

where

is the labour cost of producing the commodity;

is the fixed cost of exporting from country i to country j, expressed as the quantity of labour

The ‘iceberg cost’ is then

and the CIF of the export of country i to country j is expressed by the variable cost

Then, the total cost of exporting goods from country i to country j comprises variable and constant costs, as follows:

(3)

(3)

Then, if the export productivity has heterogeneity and randomness, and conforms to Pareto distribution

then:

(4)

(4)

where

is the organisation heterogeneity within an industry; in it, the higher the value, the lower the heterogeneity.

Moreover, the international market is a monopolistic and competitive market. This denotes that the equilibrium price of each product exported from country i to country j is a constant markup over the marginal cost, as follows:

(5)

(5)

Thereafter, the demand for manufactured goods in country j is:

(6)

(6)

Furthermore, is the price index in country j, where

and

are the total number of exporting organisations in countries i and j, respectively; and G(a) is the distribution of exporting companies, as follows:

(7)

(7)

Then, we set financial transaction costs, as described:

(8)

(8)

where

refers to financial development efficiency; if

= 0, it demonstrates complete financial markets, in that companies can obtain external financial assets for

here, Ω is the dependency of outside financing for the enterprise.

EquationEquations (5)(5)

(5) and Equation(7)

(7)

(7) were used to represent the company’s net profit. Then, when the productivity of the company exceeds the critical point of productivity, expressed by

it is implied that the company can obtain profits from its participation in export trade:

(9)

(9)

(10)

(10)

Where the total amount of export trade can be summarised as:

(11)

(11)

Thereafter, EquationEquations (5)(5)

(5) and Equation(6)

(6)

(6) can be substituted into EquationEquation (11)

(11)

(11) , to obtain:

(12)

(12)

Here, G(a) is expressed as export productivity, and total exports are expressed as:

(13)

(13)

At this point, EquationEquation (10)(10)

(10) is substituted into EquationEquation (13)

(13)

(13) to constitute the total export trade function, including financial transaction costs and with

as a constant:

(14)

(14)

(15)

(15)

(16)

(16)

We observed here that financial development plays a positive role in export trade, especially in industries with a high demand for external financing.

4. Empirical test

4.1. Data sources

We collected data from the Jiangsu Province Statistical Yearbook and China Insurance Yearbook, specifically for the year interval of 1985–2016. From 1985 to 1997, there was no direct recorded data on manufactured goods; hence, we assumed that the total amount of product exports from the light industry and heavy industry represent the sum of all manufactured goods exports during this period. We calculated and organised the raw data using Excel. Our empirical economic analysis was conducted using the Eviews software.

4.2. Variables of interest

4.2.1. Financial development variables

The financial scale and financial efficiency indicators were selected to reflect financial development. The financial development scale (FGR and FIR) is high and indicates that the scale of financial development is enlarging; the financial development efficiency index is the SLR.

According to Goldsmith (Citation1969), financial development is reflected through an increase in the ratio between total financial assets and GDP; in other words, an increase in the FIR. Since the sum of the deposits and loans accounted for a large proportion of Jiangsu Province’s total financial assets, we adopted this value to represent the total financial assets. The SLR represented the efficiency of the conversion of deposits into loans. In traditional capital formation equations, we assume that the SLR will always be 1; that is, all deposits are converted into loans. However, this index is always less than 1. In this study, the higher the SLR, the higher the efficiency of the financial system.

Financial development manifests itself not only by the expansion of bank scale but also of non-bank financial institutions. Therefore, financial development should consider not only the development of traditional banks but also of other financial intermediaries. As an important part of the financial institutions in Jiangsu Province, insurance companies have recently shown a rapid development trend. Hence, to examine provincial financial development, we included insurance companies as financial intermediaries; hence, we considered financial development efficiency would be described by an increase in the IDEP.

Furthermore, we used total foreign direct investment (FDI; we took a logarithmic approach for this variable) and the exchange rate (RFE; the exchange rate of RMB against US dollars) as control variables.

4.2.2. Export trade indicators

To measure the export trade development level, we used the export trade growth rate and export trade structure variables. Growth rate was expressed by the EXG, and the structure was expressed by the ratio between export of manufactured goods and total exports (EXS).

4.3. Empirical test and analysis

4.3.1. Descriptive statistics of interest variables

Our results show that the EXG of Jiangsu Province’s export trade had a mean of 21.5%, with the highest EXG being 53.7% and the lowest EXG being −16.3%. Therefore, Jiangsu Province’s export trade maintained a high EXG from 1985–2016. Despite this maintenance, it was affected by the 2008 global financial crisis, reaching the lowest EXG point in 2009; it still increased in 2009 and 2010, showing a downward trend in the following years (i.e., 2011–2016). Hence, upon being affected by the international environment, Jiangsu Province’s EXG started to fluctuate greatly, indicating that the provincial export commodities lacked competitiveness in the international market and that these commodities also faced greater risks.

Regarding EXS, its mean was 95.4%, with the maximum being 98.8%, the minimum being 86.8%, and the median being 95.87%. Therefore, from 1985–2016, the EXS in Jiangsu Province was stable. During this period, the FIR, IDEP, FGR, and other financial development indicators also showed a steady growth trend ().

Table 1. Descriptive statistical analysis of each variable of interest.

4.3.2. Correlation analysis

The EXG was positively correlated with RFE, IDEP, and FDI, indicating that these variables had a positive impact on EXG. The SLR, FGR, and FIR were negatively correlated with EXG. Meanwhile, the EXS was positively correlated with FGR, FIR, IDEP, RFE, and FDI, and negatively correlated with SLR. This finding concurs with prior literature (Zhang et al., Citation2013). Specifically, we showed that China’s trade openness is relatively high, whereas financial openness is relatively low; hence, stakeholders promoting export trade opening in this province of China seem to be non-concordant with those that promote financial support regarding export trade. This is possibly due to most organisations that promote exports in Jiangsu Province being small and medium-sized enterprises; it is common for companies of this size to encounter hinderances when obtaining financial support from banks and other financial institutions. This fact may be limiting the impact of financial development on export trade ().

Table 2. Correlation analysis among the variables of interest.

4.3.3. Analysis of the main causes for the relationship between interest variables

According to our analysis, SLR, IDEP, and FIR showed multicollinearity effects. To solve this problem, we conducted principal component analysis on these three indexes, constructing a comprehensive index that reflected the efficiency of financial development. The results of this analysis are shown in .

Table 3. Results of the principal component analysis for SLR, IDEP, and FIR.

Among the three components, only the eigenvalue of the first component was greater than 1, and the variance contribution rate was 87.54%. Hence, we chose only one principal component. In Jiangsu Province, the financial development efficiency was reflected not only in the improvement of the operating efficiency of financial institutions but also in the diversification of financial intermediaries. Moreover, the asset scale of the insurance industry was similar to that of the banking industry, and the IDEP also demonstrated the provincial financial development efficiency. The SLR, FIR, and IDEP were highly correlated. Based on this, we used the principal component method to construct a comprehensive measure index of financial development efficiency, which allowed us to comprehensively examine this variable. The coefficients of the FIR, IDEP, and SLR components were calculated, following which we constructed the comprehensive test index ().

Table 4. Augmented Dickey–Fuller unit root test results.

After its construction, to avoid the false regression of non-stationary time series, we used the augmented Dickey–Fuller method to test data stability.

4.3.4. Co-integration test and granger causality test

To demonstrate the long-term stable relationship between variables, we conducted a co-integration test on them. The results show that EXG had a co-integration relationship with the financial efficiency comprehensive index, FGR, LNFDI, and RFE. Meanwhile, EXS showed a co-integration relationship with the financial efficiency comprehensive index, FGR, LNFDI, and RFE.

To investigate the short-term relationship between variables, we performed the Granger causality test. It refers to the Granger noncausal understanding, which is based on the past understanding of a variable X and the past understanding of another variable Y. Particularly, when predicting X, if the predicted result by adding the past value of Y is more accurate than the one using the past value of X, then Y can be said to be the Granger cause of X. Therefore, Granger causality can be generally understood more as a predictive or leading relationship than a causal one (Lv, Citation2013). To explore whether financial development caused short-term changes in the total EXG and EXS, we conducted Granger causality tests on the variables in the two groups. First-order variables are stationary; according to the principle of the Granger test, all variables must be of the same order to be tested. Therefore, we converted all variables into first-order variables ( and ).

Table 5. Results of the Granger test for export trade growth rate and independent variables.

Table 6. Results of the Granger test for export trade structure and independent variables.

4.3.5. Regression analysis

To explore the influence of financial development on Jiangsu Province’s export trade, we conducted a regression analysis using the comprehensive measure index of financial development, FGR, and the control variables of FDI and RFE.

4.3.5.1. Regression of the financial efficiency comprehensive index, FGR, LNFDI, and RFE to EXG

As shown in , the fitting degree was 0.528, which was low; this indicates that financial development had a weak impact on export trade. The financial efficiency comprehensive index and RFE passed the significance test at the 1% level; hence, both had a certain influence on EXG. Although FDI had a positive effect on EXG, it was very weak; hence, our results conform to the current status of the impact of financial development in Jiangsu Province on export trade, which we described in the Introduction. Specifically, most export traders in the province are small and medium-sized enterprises, denoting that they receive less financial support.

Table 7. Regression results for the influence of financial development on the export trade of Jiangsu Province.

4.3.5.2. Regression of the Financial Efficiency Comprehensive Index, FGR, LNFDI, and RFE to EXS

As shown in , the fitting degree was 0.782, which was high; nonetheless, the financial efficiency comprehensive index and LNFDI passed the significance test at the 1% level. The residuals also passed the tests of autocorrelation, normality, and heteroscedasticity.

Table 8. Regression results of the effect of financial development on the export trade structure of Jiangsu Province.

EXS = 0.5900*FIR + 0.5971*IDEP - 0.5433*SLR - 0.0036 * FGR

+ 0.0120 + LNFDI - 0.0007 + RFE + 0.8306 (1)

Then, Formula (1) was substituted into Formula (2) to get:

EXS = 0.0002 * FE-0.0036 * FGR + 0.0120 * LNFDI -0.0007 * RFE + 0.8306 (2)

4.3.5.3. Concluding Analysis

Financial development showed no significant impact on the growth of Jiangsu Province’s export trade. According to the correlation analysis, although the correlation between the RFE and EXG was the highest, its value was still small (i.e., only 0.5), indicating that this influence is weak. Moreover, the correlation between EXG and financial development scale, FIR, and IDEP were even smaller than that between EXG and RFE. Meanwhile, the correlation between FDI and EXG was also not obvious, with a correlation coefficient of 0.1037. Additionally, the correlation between the SLR and EXG was even negative. Therefore, the growth of Jiangsu Province’s export trade needs to be discussed from other perspectives, such as factor endowment, international economic growth, and institutional factors.

We also showed that financial development had a significant impact on Jiangsu Province’s EXS. According to the correlation analysis, the correlation coefficient between IDPE and EXS was 0.72, depicting a high correlation; in the regression analysis, IDPE showed the largest coefficient as well, indicating that the financial structure of insurance companies can play a major role in promoting EXS. Moreover, FGR, FIR, FDI, and RFE were highly correlated with EXS, showing a high influence on the structure of Jiangsu Province’s export trade. In the regression analysis, FIR and FDI showed positive coefficients, hence demonstrating their positive impact on export trade structure.

Especially, the FDI showing this positive effect demonstrates how FDI can evoke a good learning effect in Jiangsu Province’s industry. Through such financing, the related industries and enterprises at the province-level may absorb advanced technology and achieve technological upgrading of their export products. Meanwhile, the coefficient of FGR to export trade in the regression was negative; this demonstrates that the expansion of the financial scale in the region is not conducive to the improvement of Jiangsu Province’s EXS. Additionally, the SLR regression coefficient was negative, indicating that financial institution efficiency may have a negative effect on EXS. Finally, the RFE coefficient was also negative, indicating that adjusting Jiangsu Province’s EXS through exchange rate policies will not evoke significant impacts. Summarising, stakeholders in improving the provincial EXS should focus on encouraging foreign trade enterprises and on their investment potential to strengthen technological innovation at the provincial level.

5. Policy suggestions

Our analysis outlines that Jiangsu Province should, within the framework of existing national laws and regulations, make full use of various financial means to optimise its export trade structure and ensure its sustainable development.

First, it should utilise existing financial resources to increase EXG. Our empirical results demonstrated that the influence of financial development on EXG is weak, denoting that provincial stakeholders should discuss how to promote the growth of export trade from other perspectives. These include increasing the introduction of foreign capital, reducing institutional costs, increasing human capital, among others.

Second, Jiangsu Province should make full use of various financial policies in China to optimise its EXS and improve the technical content of the export products. According to our empirical analysis, financial development had a significant impact on Jiangsu Province’s EXS. Therefore, based on our understanding that improving the operational efficiency of financial intermediaries may enhance EXS, provincial stakeholders should vigorously develop non-bank financial institutions (e.g., insurance companies, equity funds, and fund companies), create multi-level financial markets, and increase the supply of financial products and services.

Through these financial policies and measures, on the one hand, export organisations in the region may be provided with convenient financing services; on the other, export organisations may be enabled to make use of various financial instruments, effectively helping them to strengthen risk management and reduce financial constraints. Particularly, we see the need for solving the mismatch between the main bodies promoting foreign trade (i.e., support organisations) and those supporting financial development (i.e., financial institutions); doing so may ensure that private enterprises promoting trade opening can receive loan support from the formal financial sector. This notion concurs with prior research (Zhang et al., Citation2013).

Finally, FDI should be reasonably guided and promoted. According to the empirical analysis, FDI had a significant positive effect on EXS, namely, foreign direct investment can optimise the EXS in the studied region. Therefore, stakeholders should focus not only in FDI quantity but also its quality. Through financial development, we believe that the region will attract FDI for human capital, research and development-intensive and technology-intensive industries, and moderately reduce the total amount of foreign investment in labour- and resource-intensive industries. We hope that these measures serve to accelerate the transformation and upgrading of export trade in Jiangsu Province.

Disclosure statement

No potential conflict of interest was reported by the authors.

References

- Beck, T. (2002). Financial development and international trade: Is there a link? Journal of International Economics, 57(1), 107–131. https://doi.org/10.1016/S0022-1996(01)00131-3

- Beck, T. (2003). Financial dependence and international trade. Review of International Economics, 11(2), 296–316. https://doi.org/10.1111/1467-9396.00384

- Berthou, A. (2010). The distorted effected of financial development on international trade flows. CEPII WorkingPaper, 9, 296–316.

- Camisón-Haba, S., Clemente-Almendros, J. A., & Gonzalez-Cruz, T. (2019). How technology-based firms become also highly innovation firms? The role of knowledge, technological and managerial capabilities, and entrepreneurs’ background. Journal of Innovation & Knowledge, 4(3), 162–170. https://doi.org/10.1016/j.jik.2018.12.001

- Gao, C. (2010). An empirical analysis of Hubei’s financial development and foreign trade relations. Cooperative Economics and Technology, 404, 66–68.

- Geng, W., & Hao, B. (2017). Financial development and the offshore level of intermediate goods: Empirical analysis based on the external financing dependence of manufacturing industry. World Economy Studies, 10, 123–134.

- Ginevičius, R., Dudzevičiūtė, G., Schieg, M., & Peleckis, K. (2019). The inter-linkages between financial and economic development in the European Union Countries. Economic Research-Ekonomska Istraživanja, 32(1), 3315–3332. https://doi.org/10.1080/1331677X.2019.1663436

- Goldsmith, R. W. (1969). Financial structure and development. Yale University Press.

- Ji, Y., & Cheng, B. (2015). The influence of financial development on international Trade. International Economic Cooperation, 5, 83–89.

- Jiang, H., & Cha, W. (2013). Research on the influence mechanism and effect of Shanghai financial development on export growth. East China Economic Management, 27(10), 11–15.

- Jiao, B., & Zhang, S. (2012). Empirical research on financial development and foreign trade relations in Zhejiang Province. Price Monthly, 2, 50–55.

- Kletzer, K., & Bardhan, P. (1987). Credit markets and patterns of international trade. Journal of Development Economics, 27(1–2), 57–70. https://doi.org/10.1016/0304-3878(87)90006-X

- Liu, F., & Yang, Y. (2020). The role of financial development in exporters market share. Journal of Harbin University of Commerce, 170(01), 19–33.

- Liu, Z., & Zhang, J. (2016). The empirical analysis on the relationship between financial level and trade structure. Economic Theory and Business Management, 1, 71–83.

- Lv, G. (2013). A research on model selection and related strategies of Granger causality test. Statistics & Information Tribune, 28(03), 3–9.

- Ma, X., & Xie, W. (2019). Destination country financial development and margin of international trade. Economics Letters, 177, 99–104. https://doi.org/10.1016/j.econlet.2019.02.006

- Manova, K. (2013). Credit constraints, heterogeneous firms, and international trade. The Review of Economic Studies, 80(2), 711–744. https://doi.org/10.1093/restud/rds036

- Manova, K., Wei, S. J., & Zhang, Z. (2015). Firm exports and multinational activity under credit constraints. Review of Economics and Statistics, 97(3), 574–588. https://doi.org/10.1162/REST_a_00480

- Monteiro, A. P., Soares, A. M., & Rua, O. L. (2019). Linking intangible resources and entrepreneurial orientation to export performance: The mediating effect of dynamic capabilities. Journal of Innovation & Knowledge, 4(3), 179–187. https://doi.org/10.1016/j.jik.2019.04.001

- Nizam, R., Karim, Z. A., Rahman, A. A., & Sarmidi, T. (2020). Financial inclusiveness and economic growth: New evidence using a threshold regression analysis. Economic Research-Ekonomska Istraživanja, 33(1), 1465–1484. https://doi.org/10.1080/1331677X.2020.1748508

- Qi, J., & Wang, X. (2016). The effects of financial development on net technical sophistication of export: Based on empirical analysis of external financial dependence. World Economy Studies, 2, 123–134.

- Svilokos, T., Vojinić, P., & Tolić, M. S. (2019). The role of the financial sector in the process of industrialization in Central and Eastern European countries. Economic Research-Ekonomska Istraživanja, 32(1), 384–402. https://doi.org/10.1080/1331677X.2018.1523739

- Xu, H., Li, J., & Wang, H. (2019). Research on financial development affecting enterprise export duration. Journal of Shandong University of Finance and Economics, 31(3), 48–61.

- Yao, Y. J., & Shi, W. (2013). Financial development and international trade: Empirical evidence from the Yangtze River Delta. Regional Finance Research, 2, 9–14.

- Zhang, C., Zhu, Y., & Lu, Z. (2013). The inhibitory effect of openness on financial development in China. Financial Research, 6, 16–30.

- Zhao, J. (2007). Empirical analysis of financial development and foreign trade relations. China Management Informatization, 11, 59–63.