?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Uncertainty is an economically important risk factor in the banking sector. Using a sample of Chinese listed commercial banks over the period 2005 − 2018, this research conducted pooled OLS and found evidence that economic uncertainty significantly increases bank risk and lowers profitability. Furthermore, we constructed a partial equilibrium model to explain how risk governance alters the risk-increasing effect and profit-decreasing effect of economic uncertainty on bank risk and profitability. Consistent with theory, empirical results suggested the effects of economic uncertainty on bank risk and performance tend to be considerably weaker when there exists a strong risk governance mechanism. These findings stand when subjected to several endogeneity and robustness checks. Risk governance plays a key role in weakening the detrimental consequences of economic uncertainty on banks and promoting a sustainable growth of the banking sector. A financial regulator entity should require banks to establish a sound risk governance system in order to mitigate financial systemic risk and safeguard overall financial stability.

1. Introduction

Uncertainty has been an increasing concern of economists, policymakers, and financial institutions since the 2008 global financial crisis. They hold the belief that uncertainty was the main cause of the crisis and led to economic downturn. Currently, the COVID-19 pandemic is triggering a massive spike in uncertainty. Although there has been a growing literature investigating the effect of economic uncertainty, most focus on the real economy, such as economic growth (Balcilar et al., Citation2016; Barrero et al., Citation2017; Bloom, Citation2009), corporate capital investment (Gulen & Ion, Citation2015; Kahle & Stulz, Citation2013), and business financial decisions (Bonaime et al., Citation2018; Çolak et al., Citation2017). Few have explored the relationship between economic uncertainty and the performance and risk of Chinese commercial banks. These banks have to cope with economic uncertainty until they successfully achieve supply-side structural reforms for gradual development under the New Normal Era.

The risk-increasing effects of economic uncertainty on bank risk profile and business performance have been well documented (Wu et al., Citation2020). Higher economic uncertainty drives up the default probability of firms and transmits higher risk to commercial banks. In addition, increased economic uncertainty hinders the ability to accurately forecast the returns of investment projects, therefore diminishing banks’ earnings (Peng et al., Citation2018). Conversely, economic uncertainty may incentivize banks to “search for yield” by investing in ‘‘high-risk, high-return” projects (Dell’Ariccia et al., Citation2014), an action that is likely to increase bank risk-taking and business performance.

Beyond examining the overall impacts of economic uncertainty on bank risk and performance, this research also aimed to uncover a meaningful way to moderate these impacts. Al-Thaqeb and Algharabali (Citation2019) pointed out that the best way to deal with uncertainty is to raise awareness. For banks, strengthening risk awareness of all employees is vital as the Basel Committee on Banking Supervision (Basel Committee on Banking Supervision (BCBS),), Citation2015), the Financial Stability Board (Financial Stability Board, Citation2017) and other regulators began to require banks to establish stricter risk governance mechanisms. Risk governance emerged following the 2008 financial crisis due to exposure of the failure of traditional corporate governance in financial institutions (Beltratti & Stulz, Citation2012). Banks have explored efficient risk governance practices in the past few years in order to avoid bankruptcy amid high uncertainty. Case in point is the qualitative organization of the bank risk management process to ensure stability and security for the banking system as a whole (Kazbekova et al., Citation2020). Under the current bank system scenario, three Chinese commercial banks, Baoshang Bank, Bank of Jinzhou, and Hengfeng Bank were disposed by the China Banking and Insurance Regulatory Commission (CBIRC) in 2019, due to governance malpractices which triggered risk exposure. Moreover, bank governance has just been introduced in the Commercial Bank Law (Revised Draft) announced by the People’s Bank of China in 2020. This led to an increasing attention being paid to risk governance. Therefore, we explored whether risk governance played the intended role of preventing Chinese banks from suffering economic uncertainty. As opposed to the extant literature that directly examines the relationship between risk governance and bank risk and performance (e.g., Aljughaiman & Salama, Citation2019; Nahar et al., Citation2016), we concentrated on the moderating role of risk governance to see whether economic uncertainty is less influential when risk governance exerts a strong influence.

This research aims to confirm the negative impacts of economic uncertainty on bank risk and performance, which is a topic currently only evidenced by very limited research. It also extends the investigation by exploring whether risk governance mechanisms alter the direction of these impacts. On the one hand, it benefits commercial banks to enhance risk governance practices to avoid uncertainty-induced fragility. On the other hand, it assists financial regulators to implement an efficient set of policy instruments on risk governance to weaken the detrimental consequences of economic uncertainty on banking stability.

The partial equilibrium model developed here allows us firstly to provide a theoretical explanation of the moderating role of bank risk governance mechanisms, and secondly to empirically verify the hypothesis that the negative effects of economic uncertainty on bank risk and performance are moderated by the level of risk governance. We provided evidence that banks should strengthen their risk governance mechanisms to reduce risk exposure, survive uncertainty and achieve better performance.

This study complements the existing literature by focusing not only on the impact that economic uncertainty per se had on bank risk, but also by considering the effect of risk governance to highlight the moderating effect of such interaction. Along those lines, bank risk governance compensates for uncertainty as it has the perfect risk management framework and requires an experienced and professional chief risk officer (CRO) to identify, measure, and control financial risk. To the best of our knowledge, these effects have not been previously investigated. The contribution of this paper to the literature is twofold. First, it adds to the rising literature on the bank risk channel of economic uncertainty. Unlike most studies emphasizing the negative impact of economic uncertainty on bank lending or credit growth, this research focuses on the underexplored effects on bank risk and profitability. Second, we extend the inquiry on the role of risk governance in the relationship between economic uncertainty and bank risk-taking and performance through a theoretical model and empirical tests. This study is the first to shed light on the stabilizing effect of risk governance on bank risk and performance amid uncertainty. Our findings suggest that economic uncertainty is both a risk-increasing and performance-worsening force in commercial banks, supplementing the discussion in Wu et al. (Citation2020).

The rest of paper is structured as follows. Section 2 reviews the related literature. Section 3 proposes the hypotheses through theoretical analysis. Section 4 introduces variables and empirical methodology. Section 5 reports the empirical results and robustness checks. Section 6 concludes.

2. Literature review

Since the book The Age of Uncertainty authored by John Kenneth Galbraith was published in 1977, many significant events have signalled that uncertainty is a relevant issue in the financial system. Besides general economic uncertainty, some works pay attention on several specific types of uncertainty, such as economic policy uncertainty (EPU), a topic deeply explored by a number of researchers since it was developed by Baker et al. in 2016, including political uncertainty (Francis et al., Citation2014), regulatory uncertainty (Gissler et al., Citation2016) as well as contesting monetary policy scenarios (Dou et al., Citation2021).

Many studies have examined the impact of EPU on real economic outcomes, suggesting uncertainty as one of the main forces leading to the depth and length of an economic slump (e.g., Azzimonti, Citation2018; Bachmann et al., Citation2013; Baker et al., Citation2016; Bernanke, Citation1983; Bloom et al., Citation2007). Al-Thaqeb and Algharabali (Citation2019) documented that macroeconomic changes would negatively affect the earnings of firms, especially during adverse events (Bonsall et al., Citation2013). Thus, we learned that economic uncertainty makes the economic activity fall and affects a balanced growth of the real economy. A growing body of literature has examined the effect of EPU on financial outcomes, such as stock returns, bond prices (Gilchrist et al., Citation2014), oil prices (Balcilar et al., Citation2017) and the bitcoin market (Wang et al., Citation2020). In the banking literature, Chi and Li (Citation2017), Karadima & Louri, Citation2021) both found a positive effect of EPU on non-performing loans. Iqbal et al. (Citation2020) noted the impact of EPU on bank performance as significant and negative. Moreover, bank values lower with high uncertainty because uncertainty decreases bank loan growth (He & Niu, Citation2018). In addition, the association between EPU and credit growth (Bordo et al., Citation2016), banks’ loan pricing (Ashraf & Shen, Citation2019) and loan loss provisions (Ng et al., Citation2020), as well as bank stability (Phan et al., Citation2021) have been widely investigated.

Nevertheless, few studies have examined how economic uncertainty affects bank risk-taking and performance. Economic uncertainty plays a vital role in risk management (Kelly et al., Citation2016). Wu et al. (Citation2020) found evidence that bank risk increases as economic uncertainty increases. Furthermore, their empirical results support that an uncertainty-bank risk nexus is more attributable to “search-for-yield” strategies and bank herding behaviors. However, they did not demonstrate whether bank performance is associated with economic uncertainty. Therefore, further investigation is needed.

Acemoglu et al. (Citation2016) proposed that corporate governance can lessen uncertainty and thereby lead to better returns. Commercial banks are special firms that professionally operate and manage risk. It is therefore assumed that bank risk governance can help reduce the effect of uncertainty on performance and risk-taking. While there is abundant literature on the relationship between risk governance and bank risk and performance, none explores the role of risk governance under economic uncertainty. Therefore, we concentrated on the moderating role of risk governance. In theory, if risk governance plays a substantive monitoring role for bank risk management, it is very likely to affect the risk and performance of banks (Lundqvist, Citation2015). If banks only symbolically establish a risk governance framework to meet the requirement of the regulator, it is hard to guarantee a significant relationship between risk governance and their business performance (Ames et al., Citation2018; Hines & Peters, Citation2015). Empirical tests that measure risk governance are limited but have become popular after Ellul and Yerramilli (Citation2013) and Magee et al. (Citation2019) assembled the risk governance index, which is calculated with several risk governance characteristics. In doing so, Ellul and Yerramilli (Citation2013) confirmed that an independent and robust risk governance mechanism can significantly reduce banks’ risk-taking and improve their business performance. Lingel and Sheedy (Citation2012) also pointed out that a higher level of risk governance led to lower risk and risk governance can serve as an important channel to improve bank performance. Ames et al. (Citation2018) found a positive impact of risk governance on ratings and long-term profitability.

However, fewer works have underscored the negative effects of risk governance. For instance, Erkens et al. (Citation2012) proposed that strengthening risk regulation during turbulent times would overly stifle businesses and suppressed profits during periods of economic slowdown. Magee et al. (Citation2019) found that risk governance did not have the effect of reducing risk, instead, it would increase the risk.

Other studies have addressed the mediating role of risk governance. Leone et al. (Citation2018) reached a conclusion similar to Aebi et al. (Citation2012) in the sense that risk governance characteristics make the original corporate governance variables lose their significance and also describing the mediating role of risk governance. Battaglia and Gallo (Citation2015) selected 36 listed banks in P.R. China and India for similar verification, proving that the intermediary role of risk governance still existed in emerging markets. Our research is intended to explore the moderating role of risk governance on the linkage between economic uncertainty and bank risk and performance, which is not included in previous studies, both enriching the literature on economic uncertainty and bank risk governance.

3. Theoretical analysis and hypothesis

There are three forces that may theoretically account for the “economic uncertainty-bank performance and risk-taking” association. First, from the perspective of adverse economic shock channels, the recessionary effect of uncertainty on aggregate demand will worsen corporate profitability, decrease collateral values, and increases the default probability, which is likely to deteriorate banks’ risk profile (Wu et al., Citation2020). Therefore, we postulate that economic uncertainty affects banks risk by increasing the default risk of borrowers. It will increase the non-performing loan ratio and contribute to bank risk, potentially inflicting higher fragility to banks.

Second, economic uncertainty may also encourage banks’ incentive to take a higher risk to “search for yield”. On one hand, increased uncertainty will induce a lower risk-free rate, and firms would delay their investments in period of uncertainty. Both tend to lower the interest rate of bank lending (Hartzmark, Citation2016). On the other hand, banks need to pay much more on funding as they are exposed to large adverse shocks due to higher uncertainty (Valencia, Citation2017). Therefore, the interest rate spread is greatly narrowed, which means economic uncertainty negatively affects the bank’s profitability. However, the profit pressure from shareholders will drive banks to allocate their assets toward “high-risk, high-return” projects (Dell’Ariccia et al., Citation2014). Hence, bank risk would likely increase with the increased uncertainty.

Third, economic uncertainty exacerbates the information asymmetry faced by banks since an increased uncertainty makes it more difficult to accurately forecast the future returns of invested projects. From the perspective of risk identification channels, economic uncertainty acts as noise signals in banks’ decision-making (Peng et al., Citation2018). Under such circumstances, homogeneous lending behaviors will occur in banks credit decisions. However, “herding behaviors” may lead to higher risk in the banking sector, even bank crisis or systemic financial risk.

As a result, we propose,

Hypothesis 1: Economic uncertainty worsens the earnings of commercial banks.

Hypothesis 2: Economic uncertainty has a negative impact on bank risk.

Sound risk governance is a topic that is attracting increasing attention from regulators and financial institutions following the 2008 global financial crisis. We intend to clarify how risk governance plays a role in preventing banks from suffering economic uncertainty. As hinted by Aastveit et al. (Citation2017) and Gu and Yu (Citation2019), we constructed a partial equilibrium model to theoretically illustrate the moderating effect of risk governance in the relationship between economic uncertainty and bank risk-taking and performance, including the following assumptions:

Entrepreneurs apply for credit loan from commercial banks to invest in projects. We set c as the homogeneous investment amount for each project.

is the risk parameter of project i. The larger the

There are 3 periods. The bank decides to allocate the capital to project i or invest in a risk-free asset in period 0. The risk-free asset yields a gross interest rate

The bank gets nonnegative profits from the loan project if h materializes in period 1 as

The distance between

Economic state is not predictable in period 0 due to the uncertainty. In period 1, uncertainty about y is realized, and the bank may choose whether to invest the project after observing this level. We assume the resale price of capital does not exceed y after y is realized and the interest will not be reinvested.

According to Bernanke (Citation1983), economic uncertainty negatively affects the corporate investment. We assume the credit loan c is a function of economic certainty μ, and

Then we consider, the net present value for the bank investing in the project in period 0 is

(2)

(2)

while the net present value from postponing the investment decision until period 1 is

(3)

(3)

This can be seen as the role of risk governance since delaying the decision, the investor gets the option to invest in the risk-free asset rather than an unprofitable project. Consequently, for banks with an efficient risk governance mechanism, there will be investment in period 0 subject to

(4)

(4)

Substitute (2) and (3) to (4) to obtain

(5)

(5)

We define the right formula to be The above critical condition indicates that the bank will invest the credit loan project if and only if

is the upper risk limit the bank can tolerate when making an investment decision. In other words, it is the maximum of bank’s risk tolerance, which is one of the most important elements in risk governance framework.

(6)

(6)

According to (1), we obtain,

(7)

(7)

Therefore,

(8)

(8)

We substitute (8) into (6),

(9)

(9)

Assumptions (4) and (7) tell us and

hence,

This shows that under risk governance, within the circumstance of maximizing bank performance, the higher the economic uncertainty, the lower the bank’s risk appetite, which helps reduce the bank’s risk-taking behaviors.

The role of risk governance can also be explained by the co-evolution theory used in management which examines the nature of the linkage of firms and their environment. For banks, risk governance is a constantly evolving variable since change usually happens within the real sector or financial market over time. For example, risk governance act like an enzyme or catalyst when banks conduct a good development strategy or construct a wonderful organizational structure, speeding up to a superior business performance. Moreover, it also reduces the harmful effect to banks caused by worse macroeconomy.

Hence, we propose,

Hypothesis 3: Risk governance moderates the negative effect of economic uncertainty on bank performance.

Hypothesis 4: Risk governance reduces the bank risk-taking behaviors in uncertain economy.

4. Variables and empirical methodology

4.1. Variables

4.1.1. Explanatory variable

4.1.1.1. Economic uncertainty

Referring to Talavera et al. (Citation2012), we adopt conditional variance generated from GARCH (1,1) to measure economic uncertainty. The GARCH model is set as follows,

(10)

(10)

(11)

(11)

Where is the conditional variance, the proxy of economic uncertainty. We used monthly indicators of industrial value-added to be estimated in GARCH to capture more information as GDP is a quarterly disclosure indicator. We firstly performed the variable stationarity test, and then used the first-order autoregression to obtain the monthly conditional variance, to finally calculate the annual average to be the value of economic uncertainty.

4.1.1.2. Risk governance

There are currently two main ways to proxy the risk governance variable. One is to create dummy variables, where either the bank has a designated CRO or it sets up a risk committee (Aljughaiman & Salama, Citation2019). The other way is to use multiple risk governance characteristic indicators to construct a risk governance index. Considering that a risk governance index enables to capture more important risk governance information, we chose the latter in our empirical analysis. Ellul and Yerramilli (Citation2013) used 5 CRO-related indicators and 3 risk committee-related indicators to construct RGI. On this basis, and referring to Vaidun Vidyadhar and Hovey (Citation2013), Dupire and Slagmulder (Citation2019), Lingel and Sheedy (Citation2012), Sheedy and Griffin (Citation2018), we selected 10 publicly available risk governance characteristic indicators to construct a risk governance index (rgi), including the following factors:

whether to set up a chief risk officer (CRO),

whether the CRO’s salary rank among the top five of all executives (TOP5),

the proportion of risk committee members to board members (RCM),

the proportion of independent directors in the risk committee (RCI),

the frequency of risk committee meetings (FRC),

the size of the board of directors (BS),

the frequency of board meetings (FBM),

the proportion of independent directors in the board of directors (IND),

whether the board of directors has set up a risk management framework (BRF),

whether the board of directors has set a risk appetite for different types of risks (RAR).

Following Ellul and Yerramilli (Citation2013), we performed principal components analysis (PCA) on the above 10 risk governance indicators year by year to determine the weight of each indicator, thereby calculating the risk governance index.

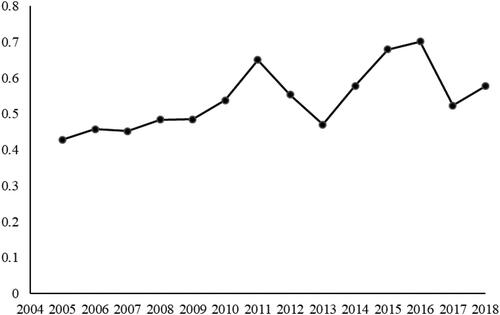

To obtain a more intuitive understanding of the trend of overall risk governance levels in the Chinese commercial banks, we calculated the average of risk governance index for the sample banks from 2005 to 2018, as shown in . Despite slight fluctuations, the overall risk governance level basically shows an upward trend.

Figure 1. Average of risk governance index from 2005 to 2018.

Source: based on the econometric results obtained.

4.1.2. Explained variable

4.1.2.1. Bank risk

Laeven and Levine (Citation2009) suggested taking the natural logarithm of the z-score as the proxy for bank risk-taking, so we have where roe and eta are the 3-year moving average of a bank’s return on equity and equity to assets, respectively. On the other hand, sdroe is the standard deviation of roe and z-score is inversely related with bank risk. The higher the z-score the smaller the bank risk.

4.1.2.2. Bank performance

As suggested by Nahar et al. (Citation2016), we used the accounting-based performance, measured by roa, as the proxy of bank performance. We calculated roa as the net income divided by the average of total assets in the two most recent years.

4.1.3. Control variables

We controlled 3 categories of potential factors which are expected to affect risk-taking behaviors and business performance. Bank characteristics variables included total asset (size), measured by the natural logarithm of total assets, loan-to-deposit ratio (ltd), equity-to-asset ratio (eta), and loan loss reserves ratio (llr). Macroeconomic conditions variables included real GDP growth (rgdp), M2/GDP (m2gdp) and the 90-days Shanghai Interbank Offered Rate (shibor). Bank regulations variables included capital adequacy ratio (car) and tier capital adequacy ratio (tier).

We presented the definition of our main variables and their main descriptive statistics in . We noted that more than half of the sample banks had risk lower than the average since the median value of z-score is larger than the mean. It also reinforces the high profitability and progressive growth in the Chinese banking system as the high level of roa show. Economic uncertainty experienced a relatively huge volatility in the sample years.

Table 1. Variable definitions and descriptive statistics.

The information on risk governance was obtained from banks’ annual reports, and other data were retrieved from Wind, Bankscope and CSMAR databases for the period 2005-2018. We collected unbalanced panel data for 44 publicly listed banks in P.R. China. After excluding samples with 3 years of discontinuous data, the final sample used in the empirical analysis had 32 listed commercial banks (including 15 A-share banks, 10 A + H-share banks, and 7 H-share banks). In addition, 1% winsorization was processed to eliminate the influence of outliers.

4.2. Regression model

Our baseline econometric model is specified as follows,

(12)

(12)

(13)

(13)

Where represents the risk of bank i in period t, and we use the z-score as proxy. Meanwhile,

represents control variables,

indicates the time effect of the bank, respectively, and

is the error term. Similarly,

represents the business performance, and we use roa as proxy.

Considering the moderating role of risk governance on economic uncertainty, the cross-product of rgi and eu is introduced in Equationeq. (12)(12)

(12) and Equation(13)

(13)

(13) , then the model is constructed as:

(14)

(14)

(15)

(15)

Where represents risk governance bank i in period t, and

is the cross-product of rgi and eu for bank i in period t.

5. Empirical results and discussion

5.1. Pairwise correlations

We first carried out the Pearson correlation test for all the variables before estimation. presents the correlations between each pair of variables. Univariate results offer preliminary confirmation of our hypothesis that economic uncertainty(eu) is negatively associated with bank risk indicator, z-score, and negatively associated with bank performance indicator, roa. This implies banks experience more risk and worse performance amid higher uncertainty. shows the absence of strong correlations between the variables, and the risk of multicollinearity is low.

Table 2. Pairwise correlations.

Table 2. Pairwise correlations (continued).

5.2. Baseline results

Similar to Nahar et al. (Citation2016), we used pooled OLS to estimate the regressive equations. The results are summarized in . Columns (1) and (2) show the effect of economic uncertainty on bank profitability and bank risk, respectively. The estimated coefficient of eu to roa is significantly negative, which is interpreted as a decrease of bank profitability with higher economic uncertainty. Besides, the negative coefficient of eu to z-score indicates that bank risk increases with higher economic uncertainty, consistent with the findings of Wu et al. (Citation2020). Commercial banks are likely to be involved in “herding behaviours” when facing economic uncertainty due to the lack of forward identification by risk framework. What is more telling is that banks may “search for yield” to achieve the profit goal by investing in high-risk projects. However, the estimated results indicate these behaviours turned out to not obtain the intended returns but rather yielded more risk. The empirical results support hypotheses 1 and 2 that economic uncertainty is an economically important risk factor for banks performance.

Table 3. Estimation results by pooled OLS.

5.3. The moderate effect of risk governance

In order to further examine the role of risk governance, the results show rgi_eu has a positive coefficient to roa and z-score, opposite to the sign of coefficient of eu, which means the moderating effect of risk governance on the relationship between economic uncertainty and bank risk and performance does exist. Banks with good risk governance act more conservatively when economic uncertainty is high. Such stabilizing impact from risk governance greatly benefits the bank performance when handling economic uncertainty. This may occur because board of directors, risk committee members, or CROs would become more risk-averse during the periods of uncertainty. As pointed out by Bloom (Citation2009), Panousi and Papanikolaou (Citation2012), risk governance internally reduces management’s appetite for risk-taking.

At the same time, considering intrinsic differences in governance structures and business models between A-share listed banks (listed in mainland China) and H-share listed banks (listed in Hong Kong), we divided the sample into two sub-samples, A-share banks and H-share plus A + H shares, to investigate whether there is a different effect of risk governance on the association between economic uncertainty and bank risk and performance. These results are shown in columns (5)-(8) of . The coefficients of rgi_eu to roa and z-score in the two sub-samples are both positive, indicating that risk governance helps reduce risk-taking behaviour and improve bank performance. However, the coefficient in A-share sample was not significant. The moderate effect of risk governance was more pronounced for H and A + H shares. This is consistent with the stricter governance requirements and regulations prevailing in Hong Kong.

5.4. Robustness tests and the endogeneity issue

5.4.1. Alternative indicators of bank risk and performance

We conducted robustness tests based on alternative indicators of bank risk and performance. We used roe as a proxy for bank performance. The results are shown in columns (1) and (2) in . The coefficient of eu to roe is significantly negative and rgi_eu is positive to roe. Considering the work of Karadima and Louri (Citation2021) on the association between economic uncertainty and non-performing loans (npl), we selected npl as an alternative proxy of bank risk. The results shown in columns (3) and (4), confirmed that eu is still significantly positive to npl and rgi_eu have a negative coefficient to npl. We therefore conclude that economic uncertainty decreases bank profitability and increases risk, albeit risk governance reduces this effect by playing a moderating role.

Table 4. Robustness checks: alternative indicators.

5.4.2. Alternative indicators of economic uncertainty

To further validate our findings, we used epu, constructed by Baker et al. (Citation2016) as a proxy of economic uncertainty. These results are shown in columns (5) and (6) of . The coefficients of epu to roa and z-score are both significantly negative while rgi_eu is positively related to roa and z-score, which strongly validates the findings obtained here.

5.4.3. Alternative econometric methodologies

In addition to using the pooled OLS method, we applied the Hausman test on the regression model and rejected the null hypothesis. On this basis, the fixed-effects model is used for re-estimation. The results are shown in the columns (1) - (4) in . Following Aljughaiman and Salama (Citation2019), the dynamic panel system generalized moment estimation method (system GMM) is used to avoid heteroscedasticity and autocorrelation in OLS and fixed effect estimations. The system GMM can not only control the endogenous correlation between the first-order lag term of the explained variable and the error term, but it also controls a potential endogenous correlation between the explanatory variable and the control variable and the error term (Blundell & +Bond, Citation1998). The regression model is constructed as follows:

(16)

(16)

(17)

(17)

Table 5. Robustness checks: alternative econometric methodologies.

Where, and

is the first-order lag term of

and

According to Blundell and Bond (Citation1998) and Guidara et al. (Citation2013), the first-order difference of the independent variables, the lagged value and the first-order difference of the dependent variables are commonly chosen as efficient instrument variables. Thus, we selected the lagged values and first-order difference of the z-score, roa and the first-order difference of eu, rgi as instrumental variables in the system GMM estimation. Furthermore, we also used the Chinese political cycle (pc) and macroprudential policy indicator (mpi) as exogenous instrumental variables. We set pc to be a dummy, pc = 1, if it is the year holding the National Congress of the Communist Party of P.R. China, otherwise, pc = 0. Lastly, mpi is the natural algorithm of the total times of macroprudential tools implemented in a year. We collected the data of mpi from Lim et al. (Citation2011) and updated them to 2018 as found in the website of the People’s Bank of China. Columns (5)- (8) in show the results estimated by system GMM. The statistics of the AR(2) test and the Sargan test confirm the selected instrumental variables were valid. The estimated results by fixed effects model and system GMM both reinforced that economic uncertainty deteriorate bank’s profitability and increase risk. However, risk governance does help to lessen such harmful effects. The conclusions drawn from the previous analysis are indeed robust.

6. Conclusions

The significance of economic uncertainty is higher than ever amid the current COVID-19 pandemic. This research investigated whether greater economic uncertainty contributes to higher bank risk and weaker business performance. The results generated by pooled OLS presented negative coefficients of economic uncertainty to bank risk, z-score, and profitability, roa, which confirmed our hypotheses that economic uncertainty exerts its impact on commercial banks by increasing risks and decreasing returns.

We extended our study by considering whether risk governance has a moderating role in reducing the risk-increasing and performance-worsening effect of economic uncertainty on banks. We constructed a partial equilibrium model to explain how a risk governance mechanism influences banks’ decision under uncertain conditions. We also used the pooled OLS method to empirically test it and found that economic uncertainty has a positive impact on bank risks and a negative impact on bank profitability, but these impacts are partially ameliorated by higher risk governance. Our findings shed light on the prominent role of risk governance in weakening the detrimental consequences of economic uncertainty on banks and promoting the development of the banking sector. Al-Thaqeb and Algharabali (Citation2019) questioned the possibility of eradicating economic uncertainty using risk management techniques. Risk governance should be an alternative answer for seeking a reduction of the negative impact of economic uncertainty on bank risk and business performance.

This paper offers important managerial implications for both commercial banks and financial regulators. Strengthening risk governance is greatly beneficial for banks’ decisions during periods of uncertainty, avoiding the uncertainty-induced fragility and achieving sustainable growth. For regulators, it is essential to require banks to establish a strong risk governance system in order to dampen their risk-taking incentives, reduce the herding behaviours, and then mitigate financial systemic risk and safeguard financial stability.

Few studies have examined how economic uncertainty affects bank risk-taking and performance, and none has reported on the moderating role of bank risk governance. Our research fills this gap and enriches the literature on economic uncertainty and bank risk governance. Nevertheless, there are some inherent limitations. Measuring risk culture presented some challenges that prevented us from including some risk culture indicators when constructing the risk governance index. These unsolved issues need further consideration as risk culture is an important element in the overall risk governance framework.

Author contributions

Xing Zhang provides the methodology and the first draft. Fengchao Li collects the data and conducts the empirical analyses. Yingying Xu makes valuable suggestions throughout. Jaime Ortiz conceptualizes the idea and edits the paper.

Disclosure statement

No potential conflict of interest was reported by the authors.

Correction Statement

This article has been republished with minor changes. These changes do not impact the academic content of the article.

Additional information

Funding

References

- Aastveit, K. A., Natvik, G. J., & Sola, S. (2017). Economic uncertainty and the influence of monetary policy. Journal of International Money and Finance, 76, 50–67. https://doi.org/10.1016/j.jimonfin.2017.05.003

- Acemoglu, D., Johnson, S., Kermani, A., Kwak, J., & Mitton, T. (2016). The value of connections in turbulent times: Evidence from the United States. Journal of Financial Economics, 121(2), 368–391. https://doi.org/10.1016/j.jfineco.2015.10.001

- Aebi, V., Sabato, G., & Schmid, M. (2012). Risk management, corporate governance, and bank performance in the financial crisis. Journal of Banking & Finance, 36(12), 3213–3226. https://doi.org/10.1016/j.jbankfin.2011.10.020

- Aljughaiman, A. A., & Salama, A. (2019). Do banks effectively manage their risks? The role of risk governance in the MENA region. Journal of Accounting and Public Policy, 38(5), 106680. https://doi.org/10.1016/j.jaccpubpol.2019.106680

- Al-Thaqeb, S. A., & Algharabali, B. G. (2019). Economic policy uncertainty: A literature review. The Journal of Economic Asymmetries, 20, e00133. https://doi.org/10.1016/j.jeca.2019.e00133

- Ames, D. A., Hines, C. S., & Sankara, J. (2018). Board risk committees: Insurer financial strength ratings and performance. Journal of Accounting and Public Policy, 37(2), 130–145. https://doi.org/10.1016/j.jaccpubpol.2018.02.003

- Ashraf, B. N., & Shen, Y. (2019). Economic policy uncertainty and banks’ loan pricing. Journal of Financial Stability, 44, 100695. https://doi.org/10.1016/j.jfs.2019.100695

- Azzimonti, M. (2018). Partisan conflict and private investment. Journal of Monetary Economics, 93, 114–131. https://doi.org/10.1016/j.jmoneco.2017.10.007

- Bachmann, R., Elstner, S., & Sims, E. R. (2013). Uncertainty and economic activity: Evidence from business survey data. American Economic Journal: Macroeconomics, 5(2), 217–249. https://doi.org/10.1257/mac.5.2.217

- Baker, S. R., Bloom, N., & Davis, S. J. (2016). Measuring economic policy uncertainty. The Quarterly Journal of Economics, 131(4), 1593–1636. https://doi.org/10.1093/qje/qjw024

- Balcilar, M., Bouri, E., Gupta, R., & Roubaud, D. (2017). Can volume predict Bitcoin returns and volatility? A quantiles-based approach. Economic Modelling, 64, 74–81. https://doi.org/10.1016/j.econmod.2017.03.019

- Balcilar, M., Gupta, R., & Segnon, M. (2016). The role of economic policy uncertainty in predicting US recessions: A mixed-frequency Markov-switching vector autoregressive approach. Economics, 10(1), 1–20. https://doi.org/10.5018/economics-ejournal.ja.2016-27

- Barrero, J. M., Bloom, N., & Wright, I. (2017). Short and long run uncertainty. NBER Working Paper. No.23676. https://doi.org/10.3386/w23676.

- Basel Committee on Banking Supervision (BCBS). 2015. Corporate governance principles for banks. Available online: https://www.bis.org/bcbs/publ/d328.pdf (accessed on 8th Jul. 2015).

- Battaglia, F., & Gallo, A. (2015). Risk governance and Asian bank performance: An empirical investigation over the financial crisis. Emerging Markets Review, 25, 53–68. https://doi.org/10.1016/j.ememar.2015.04.004

- Beltratti, A., & Stulz, R. M. (2012). The credit crisis around the globe: Why did some banks perform better. Journal of Financial Economics, 105(1), 1–17. https://doi.org/10.1016/j.jfineco.2011.12.005

- Bernanke, B. S. (1983). Irreversibility, uncertainty, and cyclical investment. The Quarterly Journal of Economics, 98(1), 85–106. https://doi.org/10.2307/1885568

- Bloom, N. (2009). The impact of uncertainty shocks. Econometrica, 77(3), 623–685. https://doi.org/10.3982/ECTA6248

- Bloom, N., Bond, S., & Van Reenen, J. (2007). Uncertainty and investment dynamics. Review of Economic Studies, 74(2), 391–415. https://doi.org/10.1111/j.1467-937X.2007.00426.x

- Blundell, R., & Bond, S. (1998). Initial conditions and moment restrictions in dynamic panel data models. Journal of Econometrics, 87(1), 115–143. http://doi.org/10.3390/jrfm10030015. https://doi.org/10.1016/S0304-4076(98)00009-8

- Bonaime, A., Gulen, H., & Ion, M. (2018). Does policy uncertainty affect mergers and acquisitions? Journal of Financial Economics, 129(3), 531–558. https://doi.org/10.1016/j.jfineco.2018.05.007

- Bonsall, I. V., S. B., Bozanic, Z., & Fischer, P. E. (2013). What do management earnings forecasts convey about the macroeconomy? Journal of Accounting Research, 51(2), 225–266. https://doi.org/10.1111/1475-679X.12007

- Bordo, M. D., Duca, J. V., & Koch, C. (2016). Economic policy uncertainty and the credit channel: Aggregate and bank level US evidence over several decades. Journal of Financial Stability, 26, 90–106. https://doi.org/10.1016/j.jfs.2016.07.002

- Chi, Q., & Li, W. (2017). Economic policy uncertainty, credit risks and banks’ lending decisions: Evidence from Chinese commercial banks. China Journal of Accounting Research, 10(1), 33–50. https://doi.org/10.1016/j.cjar.2016.12.001

- Çolak, G., Durnev, A., & Qian, Y. (2017). Political uncertainty and IPO activity: Evidence from US gubernatorial elections. Journal of Financial and Quantitative Analysis, 52(6), 2523–2564. https://doi.org/10.1017/S0022109017000862

- Dell’Ariccia, G., Igan, D., Laeven, L., & Tong, H. (2014). Credit booms and macrofinancial stability. Economic Policy, 31(86), 299–355. https://www.elibrary.imf.org/view/IMF071/20264-9781475543407/20264-9781475543407/ch11.xml?language=en&redirect=true.

- Dou, Z., Wang, J., Zhang, C., & Luo, W. (2021). The nonlinear time-varying effects of quantitative and price-based monetary policy instruments on banking systemic risks. Transformations in Business & Economics, 20(1), 280–297.

- Dupire, M., & Slagmulder, R. (2019). Risk governance of financial institutions: The effect of ownership structure and board independence. Finance Research Letters, 28, 227–237. https://doi.org/10.1016/j.frl.2018.05.001

- Ellul, A., & Yerramilli, V. (2013). Stronger risk controls, lower risk: Evidence from US bank holding companies. The Journal of Finance, 68(5), 1757–1803. https://doi.org/10.1111/jofi.12057

- Erkens, D. H., Hung, M., & Matos, P. (2012). Corporate governance in the 2007–2008 financial crisis: Evidence from financial institutions worldwide. Journal of Corporate Finance, 18(2), 389–411. https://doi.org/10.1016/j.jcorpfin.2012.01.005

- Financial Stability Board. (2017). Thematic review on risk governance. Retrieved April 28, 2017, from https://www.fsb.org/wp-content/uploads/Thematic-Review-on-Corporate-Governance.pdf.

- Francis, B. B., Hasan, I., & Zhu, Y. (2014). Political uncertainty and bank loan contracting. Journal of Empirical Finance, 29, 281–286. https://doi.org/10.1016/j.jempfin.2014.08.004

- Gilchrist, S., Sim, J. W., & Zakrajšek, E. (2014). Uncertainty, financial frictions, and investment dynamics. NBER Working Paper, (w20038). 1–58. https://doi.org/10.3386/w20038.

- Gissler, S., Oldfather, J., & Ruffino, D. (2016). Lending on hold: Regulatory uncertainty and bank lending standards. Journal of Monetary Economics, 81, 89–101. https://doi.org/10.1016/j.jmoneco.2016.03.011

- Gu, H., & Yu, J. (2019). China’s economic policy uncertainty and bank’s risk-taking. Journal of World Economy, 42, 148–171. (in Chinese).

- Guidara, A., Lai, V. S., Soumaré, I., & Tchana, F. T. (2013). Banks’ capital buffer, risk and performance in the Canadian banking system: Impact of business cycles and regulatory changes. Journal of Banking & Finance, 37(9), 3373–3387. https://doi.org/10.1016/j.jbankfin.2013.05.012

- Gulen, H., & Ion, M. (2015). Policy uncertainty and corporate investment. Review of Financial Studies, 29(3), hhv050–564. https://doi.org/10.1093/rfs/hhv050

- Hartzmark, S. M. (2016). Economic uncertainty and interest rates. Review of Asset Pricing Studies, 6(2), 179–220. https://doi.org/10.1093/rapstu/raw004

- He, Z., & Niu, J. (2018). The effect of economic policy uncertainty on bank valuations. Applied Economics Letters, 25(5), 345–347. https://doi.org/10.1080/13504851.2017.1321832

- Hines, C. S., & Peters, G. F. (2015). Voluntary risk management committee formation: Determinants and short-term outcomes. Journal of Accounting and Public Policy, 34(3), 267–290. https://doi.org/10.1016/j.jaccpubpol.2015.02.001

- Iqbal, U., Gan, C., & Nadeem, M. (2020). Economic policy uncertainty and firm performance. Applied Economics Letters, 27(10), 765–770. https://doi.org/10.1080/13504851.2019.1645272

- Kahle, K. M., & Stulz, R. M. (2013). Access to capital, investment, and the financial crisis. Journal of Financial Economics, 110(2), 280–299. https://doi.org/10.1016/j.jfineco.2013.02.014

- Karadima, M., & Louri, H. (2021). Economic policy uncertainty and non-performing loans: The moderating role of bank concentration. Finance Research Letters, 38, 101458. https://doi.org/10.1016/j.frl.2020.101458

- Kazbekova, K., Adambekova, A., Baimukhanova, S., Kenges, G., & Bokhaev, D. (2020). Bank risk management in the conditions of financial system instability. Entrepreneurship and Sustainability Issues, 7(4), 3269–3285. https://doi.org/10.9770/jesi.2020.7.4(46)

- Kelly, B., Pástor, Ľ., & Veronesi, P. (2016). The price of political uncertainty: Theory and evidence from the option market. The Journal of Finance, 71(5), 2417–2480. https://doi.org/10.1111/jofi.12406

- Laeven, L., & Levine, R. (2009). Bank governance, regulation and risk taking. Journal of Financial Economics, 93(2), 259–275. https://doi.org/10.1016/j.jfineco.2008.09.003

- Leone, P., Gallucci, C., & Santulli, R. (2018). How does corporate governance affect bank performance? The mediating role of risk governance. International Journal of Business and Management, 13(10), 212. https://doi.org/10.5539/ijbm.v13n10p212

- Lim, C. H., Costa, A., Columba, F., Kongsamut, P., Otani, A., Saiyid, M., … Wu, X. (2011). Macroprudential policy: what instruments and how to use them? Lessons from country experiences. IMF Working Papers, 1–85.

- Lingel, A., & Sheedy, E. A. (2012). The influence of risk governance on risk outcomes-international evidence. SSRN Papers, https://doi.org/10.2139/ssrn.2187116

- Lundqvist, S. A. (2015). Why firms implement risk governance–Stepping beyond traditional risk management to enterprise risk management. Journal of Accounting and Public Policy, 34(5), 441–466. https://doi.org/10.1016/j.jaccpubpol.2015.05.002

- Magee, S., Schilling, C., & Sheedy, E. (2019). Risk governance in the insurance sector—determinants and consequences in an international sample. Journal of Risk and Insurance, 86(2), 381–413. https://doi.org/10.1111/jori.12218

- Nahar, S., Jubb, C., & Azim, M. I. (2016). Risk governance and performance: a developing country perspective. Managerial Auditing Journal, 31(3), 250–268. https://doi.org/10.1108/MAJ-02-2015-1158

- Ng, J., Saffar, W., & Zhang, J. J. (2020). Policy uncertainty and loan loss provisions in the banking industry. Review of Accounting Studies, 25(2), 726–752. https://doi.org/10.1007/s11142-019-09530-y

- Panousi, V., & Papanikolaou, D. (2012). Investment, idiosyncratic risk, and ownership. The Journal of Finance, 67(3), 1113–1148. https://doi.org/10.1111/j.1540-6261.2012.01743.x

- Peng, Y. C., Han, X., & Li, J. J. (2018). Economic policy uncertainty and corporate financialization. China Industrial Economics, 1, 137–155. (in Chinese). https://doi.org/10.19581/j.cnki.ciejournal.20180115.010.

- Phan, D. H. B., Iyke, B. N., Sharma, S. S., & Affandi, Y. (2021). Economic policy uncertainty and financial stability–Is there a relation? Economic Modelling, 94, 1018–1029. https://doi.org/10.1016/j.econmod.2020.02.042

- Sheedy, E., & Griffin, B. (2018). Risk governance, structures, culture, and behavior: A view from the inside. Corporate Governance: An International Review, 26(1), 4–22. https://doi.org/10.1111/corg.12200

- Talavera, O., Tsapin, A., & Zholud, O. (2012). Macroeconomic uncertainty and bank lending: the case of Ukraine. Economic Systems, 36(2), 279–293. https://doi.org/10.1016/j.ecosys.2011.06.005

- Vaidun Vidyadhar, S., & Hovey, M. T. (2013). A risk governance index. SSRN Papers, 1–24. https://doi.org/10.2139/ssrn.1918309.

- Valencia, F. (2017). Aggregate uncertainty and the supply of credit. Journal of Banking & Finance, 81, 150–165. https://doi.org/10.1016/j.jbankfin.2017.05.001

- Wang, P., Li, X., Shen, D., & Zhang, W. (2020). How does economic policy uncertainty affect the bitcoin market? Research in International Business and Finance, 53, 101234. https://doi.org/10.1016/j.ribaf.2020.101234

- Wu, J., Yao, Y., Chen, M., & Jeon, B. N. (2020). Economic uncertainty and bank risk: Evidence from emerging economies. Journal of International Financial Markets, Institutions and Money, 68, 101242. https://doi.org/10.1016/j.intfin.2020.101242