?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Sustainable Development Goals (SDGs) highlight the importance of poverty reduction, and call for policy implementation that leads to the socio-economic development of impoverished people. However, there is a lack of knowledge about assessing individual-level socio-economic development, and how financial inclusion through microfinance can contribute to it. Therefore, the role of commercially operated Microfinance Banks (MFBs) is also considered to be controversial in the literature. This study assesses the overall socio-economic development by considering different sustainable livelihoods, multidimensional poverty, living standards, and social development measures. Thus, the Multidimensional Poverty Index (MPI), and Living Standard Index (LSI) have been estimated to gauge poverty and improvements in living standards. Data comprising 503 customers of MFBs, and 500 control respondents, has been gathered through a survey to signify this impact for two years. This paper substantiates that the microfinance obtained from MFBs contributes positively towards sustainable livelihoods, multidimensional poverty reduction, and living standards. However, microfinance does not contribute to social development. Impoverished people, mainly women living in urban areas, reap more benefits from microfinance, than their rural counterparts. Overall, financial inclusion shall be a gateway to achieve the SDGs in the long run through the socio-economic development of an impoverished segment of the society.

1. Introduction

The Millennium Development Goals (MDGs) and Sustainable Development Goals (SDGs), designed by the United Nations (UN), comprises of targets to be attained for socio-economic and environmental development (Ji et al., Citation2021; Sachs, Citation2012; Umar et al., Citation2021). In this regard, equitable and inclusive growth is the real agenda of development, also known as sustainable development. It must be noted that Macro-economic growth is only one aspect of development. True development is triggered by the people‘s accessibility to sustainable livelihood (Mok, Citation2000), and the individual level socio-economic development, which will ensure the accomplishment of other development goals (Montgomery & Weiss, Citation2011). Therefore, poverty reduction, by at`taining sustainable livelihood, is a pivotal socio-economic policy and also a challenging target for developing countries (Mazumder & Lu, Citation2015). Poverty is a multidimensional phenomenon (Liu, Citation2021, and Žiković, 2020) in its implications and effects, which influences the socio-economic status of impoverished people, that too in multiple dimensions (Mirza et al., Citation2020; Strielkowski et al., Citation2020).

The capabilities and resources (physical assets, monetary, or social capital) required for living, and fulfilling ones consumption needs are called livelihood. These will be called sustainable livelihoods especially if these are enough to bear the economic shocks that are experienced by individuals and corporations alike (Solesbury, Citation2003). Therefore, the stable access to necessities of life is known as sustainable livelihood that outrides the conventional definition of poverty reduction. The growth in income and expenditure (related to routine consumption, infrastructure, and schooling of children) are considered as the outcomes of sustainable livelihoods (Solesbury, Citation2003), which could ultimately improve the living standards and the quality of life considerably (Mazumder & Lu, Citation2015). Financial inclusion, through microfinance, is an important phenomenon to attain individual-level socio-economic development by reducing poverty (Bruton et al., Citation2015; Das, Citation2019; Lopatta & Tchikov, Citation2017; Noreen et al., Citation2011; M. Uddin et al., Citation2020; Umar et al., Citation2021) and improving the livelihoods of individuals (Montgomery & Weiss, Citation2011; Solesbury, Citation2003).

However, there are two major concerns embedded within it. The first one of these is the precise assessment of individual-level socio-economic development (Nadeem et al., Citation2021 and Saydaliyev et al., Citation2020). The second is the impact of financial inclusion, through microfinance, on this individual-level socio-economic development, which will be addressed in this study. Estimating poverty, poverty reduction and individuals’ socio-economic development is a controversial area of study in the impact assessment literature (Naqvi et al., Citation2021; Valead et al., Citation2018). That is to mention that, researchers normally miscue some important dimensions that are associated with this discipline.

This study will provide a novel empirical lens that can be used to magnify the importance of microfinance in the individual-level socio-economic development that may be translated into macro-economic development. Rather than merely focussing on the income and expenditures based unidimensional measures of poverty, this study focuses on a more dynamic approach of gauging the individual-level socio-economic development of impoverished people. Along with the measures related to sustainable livelihood (such as improvement in income, clothing, medication, education, cooking fuel, drinking water, and infrastructural development), social development, living standard, and multidimensional poverty are dimensions that have been incorporated to encompass the overall socio-economic development.

In this study, the Multidimensional Poverty Index (MPI) has been estimated to measure the poverty levels, and the decrease in its score reflects poverty reduction. After alleviating poverty, and fulfilling the basic consumption needs, the next priority to be addressed is the betterment in living standards. Therefore, this study has introduced a novel measure of living standards (Living Standard Index-LSI), covering nine dimensions related to its betterment. This could help shed light on the holistic understanding of socio-economic development of individuals.

In short, this study has contributed to the literature with five novelties put into place. First, the focus is on individual-level overall economic development; therefore, along with multiple livelihood measures, the MPI has also been incorporated to estimate the economic development of impoverished people. Second, social development of impoverished people has also been incorporated into the analysis. Third, the LSI has been developed in order to analyze the improvement in the living standards of impoverished people. Forth, multiple empirical investigations (logistic regression, multiple regression, and Propensity Score Matching – PSM) have been carried out in order to make concrete and precise impact assessments. Fifth, in light of the above findings, this study expounds on the contribution of financial inclusion towards attaining SDGs, particularly in developing countries such as Pakistan.

Our findings indicate a positive impact of financial inclusion on the socio-economic development of impoverished people. To our knowledge, this is the first study of its kind to consider, as well as focus on the role of Microfinance Banks (MFBs) as an industry, and assess the impact of financial inclusion through MFBs on socio-economic development, which is important empirical evidence against the argument of mission drift. Our findings also provide a roadmap to the policymakers for the socio-economic development of the impoverished segment of society, and eventually for the accomplishment of SDGs.

2. Literature review and hypotheses development

According to the United Nations (UN), poverty is one of the biggest tribulations that have plagued the society. Impoverished people‘s lack of economic resources, and their inability to generate external financing, further augment their vulnerability to poverty (Samat et al., Citation2018). Irrespective of the utilisation of funds (building a house, establishing or strengthening the business, debt servicing, or fighting against their economic recession), external financing typically reduces these individuals’ vulnerability to poverty (Noreen et al., Citation2011), and could get them out of this vicious cycle as well (Bruton et al., Citation2015; Hermes & Lensink, Citation2007; Lopatta & Tchikov, Citation2017; M. Uddin et al., Citation2020).

However, the poor have been neglected by the formal financial institutions. Therefore, Microfinance Institutions (MFIs) have been designed and supported by development agencies worldwide, so as to provide financial services to these un-bankable customers (Noreen et al., Citation2011; Umar et al., Citation2021). Moreover, MFIs played a significant role in building a non-dependent financial system for the poor (Hermes & Lensink, Citation2007), which has increased micro-entrepreneurship (Khanam et al., Citation2018; Lopatta & Tchikov, Citation2017), improved their income (T. A. Chowdhury & Mukhopadhaya, Citation2012), enhanced their overall well-being (Mazumder & Lu, Citation2015), improved their socio-economic status, and ensured dignity. Worldwide, the regulatory authorities and the central banks also regulate MFIs, formally known as Microfinance Banks (MFBs). MFBs are the means of providing a variety of financial services to the poor, based on market-driven and commercial approaches.

Microfinance also enables the poor to attain economic self-sufficiency and sustainability, which helps to alleviate their ailing conditions (Audu & Achegbulu, Citation2011; Bruton et al., Citation2015; Das, Citation2019; Lopatta & Tchikov, Citation2017; Samat et al., Citation2018), improves living standards, prioritises the education of children (Holvoet, Citation2004; Noreen et al., Citation2011), ensures prosperity (F. Hossain & Knight, Citation2008) fosters peace, promotes harmony, nurtures economic growth (Ocasio, Citation2012), and aids in the overall rural development (Agbaeze & Onwuka, Citation2014). Along with the exposure to microfinance, the borrower‘s educationalso contributes towards poverty alleviation (M. S. Awan et al., Citation2011). Eventually, microfinance contributes positively towards the overall well-being of the poor. It does so by improving the rate of literacy, aiding to gain better earnings, helping in getting better access to healthcare services, helping access healthier food and safe drinking water, improving the infrastructure of the accommodations, gaining valuable assets, and improving the net worth of individuals (Atmadja et al., Citation2016).

Microfinance has significantly contributed towards bringing a positive and upward change in the lives of impoverished people in Ghana (Valead et al., Citation2018), Nigeria (Agbaeze & Onwuka, Citation2014; Audu & Achegbulu, Citation2011), Solomon Islands and Vanuatu (Feeny & McDonald, Citation2016), Malaysia (Al-Shami et al., Citation2018; Samat et al., Citation2018), India (Das, Citation2019), Sri-Lanka (Kumari et al., Citation2019), Bangladesh (Mazumder & Lu, Citation2015; Sheel et al., Citation2018) and Pakistan (Niaz & Iqbal, Citation2019). In Pakistan specifically, scholars (Akram & Hussain, Citation2011; Durrani et al., Citation2011) mentioned that the income levels had experienced an increase and poverty had been reduced among the users of microfinancing. In addition to this, according to Niaz and Iqbal (Citation2019), social status, empowerment, and income levels have also shown an upward and improved trend among the women of Pakistan, whereas the level of poverty has also reduced significantly (Jamil et al., Citation2021). Some other studies in the extant literature (Augsburg et al., Citation2015; Banerjee et al., Citation1998; Rajbanshi et al., Citation2015)concluded that there is only a marginal impact, or no impact of microfinance on the economic well-being of the impoverished people. These diverse opinions in the impact assessment studies exist because of the different outcome measures and assessment methodologies (Holvoet, Citation2004; Weiss & Montgomery, Citation2005), making this impact a controversial phenomenon to look into (Noreen et al., Citation2011). Sustainable livelihood as an outcome is the recommended measure of poverty reduction (Solesbury, Citation2003), therefore, adopted as one of the proxies of socio-economic development. Our measurement methodologies and the econometric model address the limitations of the previous studies with a robust impact assessment framework. Based on this discussion, we hypothesised the following:

Hypothesis-1 (H1): Financial inclusion through microfinance significantly influences the sustainable livelihood of impoverished people.

Studies in literature (Akram & Hussain, Citation2011; Durrani et al., Citation2011; Jamal, Citation2008; Montgomery & Weiss, Citation2011; Noreen et al., Citation2011; Shirazi & Khan, Citation2009) have thus far only considered unidimensional measures of poverty, and described that microfinance has a positive impact on the livelihood, poverty, and housing arrangements of people. However, the methodology of estimating the betterment in livelihood, housing, and poverty reduction has its due limitations. There is mixed evidence about the impact of microfinance in the literature, primarily due to the difference in poverty measures and assessment tools that are used by the researchers (Rajbanshi et al., Citation2015), which makes those inferences even more controversial. They have taken improvement in income as a proxy of poverty reduction and quality of life. Nevertheless, multidimensional poverty measures are appropriate, and must be preferred over other measures (Feeny & McDonald, Citation2016). Internationally, scholars (A. R. Chowdhury et al., Citation1986; Feeny & McDonald, Citation2016; Sheel et al., Citation2018; Valead et al., Citation2018) have tried to estimate multidimensional poverty, but the measures they have often resorted to have limited scope, especially in estimating poverty reduction.

Arguably, economic development is evident in the improvement of infrastructure, household assets, availability of clean drinking water, sanitation, and electricity (He & Collins, Citation2021). This study therefore incorporates the multidimensional poverty index (MPI), and proposes a living standard index (LSI) as a more dynamic proxy of poverty reduction, and growth in living standards, respectively. In Pakistan specifically, the evidence related to the impact of microfinance on multidimensional poverty and living standards is limited. It drives us to derive to the following hypotheses:

Hypothesis-2 (H2): Financial inclusion through microfinance significantly influences multidimensional poverty.

Hypothesis-3 (H3): Financial inclusion through microfinance significantly influences the living standards of impoverished people.

Poverty adversely affects the social status and recognition of individuals and families on the whole. Because of the lack of resources and a relatively difficult life, these people often seek financial help from individuals around them. Due to this, their self-respect and self-esteem are often compromised, which ultimately results in a wretched social status and a lack of self-worth. Improvement in social status is a critical agenda, as this could potentially be a driving force for economic progression (Cristea et al., Citation2020). Soft factors such as self-esteem and self-respect compel individuals to work harder, smarter and abandon the listless approach and attitude towards their socio-economic conditions (Emler, Citation2001). Access to financial resources shall then result in better social status (Durrani et al., Citation2011; Tariq et al., Citation2015). Therefore, it can be hypothesised that:

Hypothesis-4 (H4): Financial inclusion through microfinance significantly influences the social status of impoverished people.

The provision of microfinance through NGOs is considered to be more effective, with the ability to reduce poverty (R. Amin & Becker, Citation1998; Audu & Achegbulu, Citation2011; A. R. Chowdhury et al., Citation1986). MFBs are usually to be blamed for being commercial, less focussed on the development of impoverished people (Montgomery & Weiss, Citation2011), and more focussed on their profitability, rather than the socio-economic well-being of impoverished people (Lopatta et al., Citation2017). However, the commercially operated MFBs may also aid in socio-economic development primarily because MFBs are more focussed on viable lending, and ensure that there is a productive use of funds (Blanco-Oliver & Irimia-Diéguez, Citation2021). This discussion raises an important question: Are commercially operated MFBs productively able to contribute towards this goal of socio-economic development of impoverished people? This compels us to develop the hypothesis given below:

Hypothesis-5 (H5): Microfinance through commercially operated MFBs significantly influences the socio-economic development of impoverished people.

Sustainable socio-economic growth in the lives of impoverished people has paramount significance in developing countries (UNDP, 2016). Among the seventeen SDGs, the top seven goals of any nation (no poverty, hunger alleviation, good health and well-being, quality education, gender equality, clean water and sanitation, and decent working conditions and economic growth) are mainly associated with the development of the impoverished segment of the society (Sachs, Citation2012). Sustainable growth in their livelihoods shall improve the socio-economic status, particularly in poorer countries (Asadullah & Savoia, Citation2018; Mazumder & Lu, Citation2015), while also accomplishing these development goals alongside (Montgomery & Weiss, Citation2011). Financial inclusion is also considered to be a rather critical and effective catalyst for accomplishing these goals (Bank, Citation2017). As poverty eradication is the gateway of economic development (Ocasio, Citation2012) and equity in any society, other development goals could be achieved by eradicating poverty as well (Samat et al., Citation2018). The tendency of the state to adopt these development goals and implement relevant policies is another contributing factor towards significantly alleviating poverty. Only inclusive growth shall result in real, sustainable development, and for this, financial inclusion plays a pivotal role (T. A. Wilson, Citation2012). Based on these arguments, it is hypothesised that:

Hypothesis-6 (H6): Financial inclusion through microfinance significantly contributes towards the accomplishment of SDGs.

3. Data and methods

3.1. Data

For this study, individual-level primary data of 1,003 respondents was gathered through semi-structured interviews. The semi-structured interviews were preferred over a questionnaire, as our target population was uneducated or barely educated. The interviewer elaborated upon (where necessary), clarified the questions and doubts, and ensured the accuracy of the data gathered. However, a questionnaire was developed to administer these interviews. The dimensions of the variables were extracted from different studies that were consulted for this purpose. For the dimensions related to poverty and livelihoods, the basic inspiration was the UNDP‘s Human Development Index (HDI), and MPI of OPHI. Certain dimensions were also extracted from the questionnaire used by Noreen (Citation2011) as well. For good reasons, we opted for individual-level primary data. The macroeconomic data had many other influencing factors, such as the fiscal-monitory mix, and the economic development at large. Furthermore, the performance of large-scale industries overrode the macroeconomic indicators.

The respondents comprised of two groups: customers of MFBs, who had borrowed from MFBs (called treatment group), and non-borrowers with similar demographics (called the control group). The individuals, who had taken loans in 2016, were interviewed in 2018, allowing a reasonable time to witness their socio-economic development. For this very reason, the current customers, who had taken the loans fairly recently for the first time, were not taken into consideration. Then, the Stratified Random Sampling and Snowball Sampling techniques were applied in order to ensure the uniformity of the treatment and control groups‘ demographics, and the socio-economic conditions. Every chosen district was considered as a separate stratum. Initially, the respondents were selected from each stratum randomly, with the help of the MFBs‘ database, and with the help of the treatment group members. Furthermore, the respondents were contacted for inclusion in the control group. In this way, the chance of endogeneity, and the selection bias had been eliminated significantly.

The formula of Yamane (1967) has thus been used to determine the sample size.

where; n = sample size, z = 1.96 (the value of z, at a 95% confidence interval), P = the proportion of variability, N = population size, and e = margin of error (at a 95% confidence interval, the margin of error is 0.05).

A total of 1,485,165 borrowers received the loan, of which 550,263 were the customers of MFBs (PMR, 2018). The formula put together recommends a sample size of 457 respondents for the treatment group. We planned for 500 respondents from the treatment group, and 500 from the control group in order for the results to be more representative and accurate. Furthermore, in order to have a reasonable sample from each stratum, the sampling target was increased, and we conducted 1,184 interviews in total, out of which 181 responses were declined due to response errors and unhealthy responses.

Our unit of analysis is an individual. The dataset obtained through a field survey contains the respondents‘ demographic variables and measures related to livelihood, living standards, and multidimensional poverty. The current information, and the information before taking the loan had been gathered at the time of the interview. From this information, the change in the socio-economic conditions has been estimated, so as to encompass the growth. This data was classified, quantified, tabulated, and empirically tested by using the SPSS and STATA software.

3.2. Variable Definition

The overall Socio-economic development of an individual is assessed through multiple proxies (explained in ). Sustainable livelihood, social development, growth in living standards, and multidimensional poverty reduction are incorporated in order to conceptualize the overall socio-economic development of impoverished people. In this regard, and describe these outcome variables and the explanatory variables, along with their measurements, respectively.

Figure 1. Conceptualization of socio-economic development.

Source: Author Estimations.

Table 2. Description and measurement of outcome variables.

Table 3. Description of independent/treatment variables.

3.2.1. Sustainable livelihoods

Sustainable livelihoods ensure the income growth that supports the expenditure on the necessities of life, and the basic infrastructural development called the outcome of livelihoods (Solesbury, Citation2003). An increase in the per-capita household income ensures the provision of the basic necessities of life. If this growth persists, this will reflect in capital expenditures that are related to infrastructural development, which reflects one‘s accessibility to a sustainable livelihood. Therefore, growth of accessibility to the medical facility, per-capita expenditure on clothes, cooking fuel used, accessibility to clean drinking water, children‘s education, ownership status of the house, roof material used in the house, overall condition of the house, and the household assets are incorporated as proxies of sustainable livelihood. The growth in these variables is measured through dichotomous variables; therefore, Binary Logistic Regression Model and the PSM analysis have been incorporated for statistical inferences.

During the pilot study, it was revealed that there are four types of housing structures. These include slum houses, mud houses, houses with T-iron roofs, and concrete roof houses. Moreover, these housing structures are the individuals’ own, rented, or inherited houses (living with a joint family system). However, it is tricky to calculate the growth in the case of an inherited house. The marginal improvement in the infrastructure, such as building a personal bathroom, improvements in the kitchen, improvements in the floor, improvements in the roof, installation of personal water boring, and expenditures on the renovation of the inherited portion of the house are also to be incorporated.

3.2.2. Living Standard

Unlike the measures used by M. A. Hossain and Asada (Citation1984), as cited in Khanam et al. (Citation2018), this study has incorporated multiple dimensions (particularly related to capital expenditures), reflecting the improvement in the living standards. It includes the improvement in the ownership status of the house, roof material used in the construction, overall condition of the house, floor material used, household assets owned, cooking fuel used, access to safe drinking water, availability of electricity, availability of a personal bathroom, and a working sanitary system of the house. If there is a growth in the said dimensions, it will be allocated ‘1’, and if not, then ‘0’.

The factor analysis method has been used to find commonalities, and excludes the irrelevant factors (which have comparatively very high or low variability). The Extraction Method and the Varimax Rotation have been applied to get rigorous outcomes. Moreover, LSI has been developed with the help of the Principal Component Analysis (PCA), in order to combine the relevant elements of the living standards. The score of LSI reflects the average growth in the living standard of the respondents.

3.2.3. Multidimensional poverty

Multidimensional poverty is a more dynamic measure of poverty, and usually defines the economic status of impoverished people (Das, Citation2019; Feeny & McDonald, Citation2016). In this study, MPI has been developed by following the guidelines of OPHI. It incorporates dimensions related to education, health, and housing collectively, in order to gauge the poverty level. presents the methodology used to construct the MPI. The score of MPI indicates the average level of deprivation faced by an individual. The score of MPI varies from ‘0’ to ‘1’, where ‘1’ reflects the complete deprivation in all factors, and ‘0’ reflects no deprivation. The 0.33 score achieved is the threshold point (poverty line). If someone has a 0.33 score or higher, then they are poor at a multidimensional level, otherwise they are not poor. In this study, the scores of the current MPI ‘MPINow’ (reflecting the poverty level in 2018), and older MPI ‘MPIBef’ (reflecting the poverty level in 2016) of every respondent have been estimated. Furthermore, in order to estimate the change in this multidimensional poverty over time, ‘MPIDiff’ has been calculated by taking the difference of ‘MPINow’ and ‘MPIBef’. It is also noteworthy that ‘MPIDiff’ is used in further statistical analysis as a proxy of change in the multidimensional level of poverty.

Table 1. Construction of Multidimensional Poverty Index (MPI).

3.2.4. Social development

The accessibility to economic resources shall improve the social status, which is also called social development. In this study, the data related to perceived social status has been collected through a survey, and a dichotomous variable has been used as a proxy of social development. If the perceived social status improves over time, then Yes =‘1’, otherwise is would be No =‘0’.

The above stated table reflects the outcome variables (see ) which are likely to be affected by financial inclusion, other demographics, and socio-economic factors (called explanatory variables).

3.2.5. Explanatory/independent variables

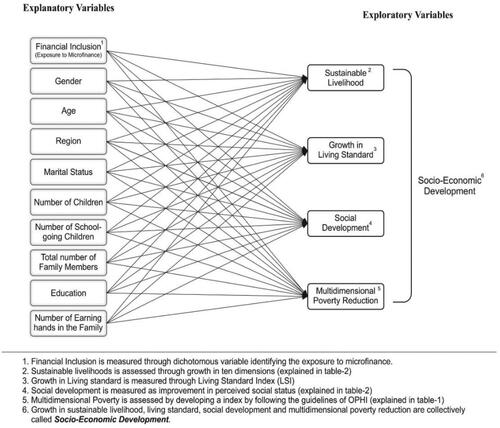

As the paper‘s focus is the socio-economic development of individuals, an individual-level measure of financial inclusion has also been incorporated in our analysis. The accessibility to financial products and services, in order to meet their financing needs is called financial inclusion (Bank, Citation2017), and is measured as one‘s exposure to microfinance (LoanMFI). The dichotomous variables (‘1′ represents the borrower, and ‘0′ represents the non-borrowers) have been incorporated in this study. Moreover, the socio-economic status and its development are not independent of the demographic and other socio-economic factors. Therefore, along with ‘LoanMFI‘, other demographic factors such as the gender (Gen), age (Age), region (Region), marital status (MS), number of children (NChild), number of school-going children (NSChild), the total number of family members (Tfmem), level of education (Edu), and the number of earning hands in the family (EarnH) have also been incorporated as the covariates. In this context, the detailed description and measurement of all the explanatory variables have been presented in .

3.3. Methodology and model specification

describes the conceptual framework that posits the empirical investigation carried out in this study. In order to investigate the impact of financial inclusion, on the socio-economic development, a simple to complex approach has been followed. Along with the descriptive analysis and the univariate analysis, we have also applied the logistic regression method, in order to analyze the impact on sustainable livelihood and social development. Furthermore, a regression analysis is carried out in order to analyze the impact of financial inclusion on the living standards and multidimensional poverty.

Figure 2. Conceptual framework of the study.

Source: Author Estimations.

3.3.1. Univariate analysis

In order to observe the difference in the two groups (borrowers and non-borrowers), the cross-tabulation technique, and the independent-sample t-test were carried out.

3.3.2. Regression analysis

In this study, eleven logistic regression models have been carried out in order to analyze the impact of financial inclusion on sustainable livelihood and social development. Moreover, multiple linear regression analysis have been carried out as well, so as to analyze the impact of microfinance on the multidimensional poverty, and the living standards of the respondents. Following is the functional form of the regression models used in this study:

(I)

(I)

where Zi is the set of dependent variables (see ). Then, βi is the vector of coefficients of the independent variables. Also, Xi is the vector of the independent variables of the ith respondent (see ).

3.3.3. Propensity score matching (PSM)

The treatment (exposure to microfinance) is not random in nature, and the provision of microfinance is dependent on the choice of the lenders (MFBs) and borrowers (the households). Furthermore, the chance of getting microfinance is based on some predefined criteria that may lead to a problem of selection bias in the sample. In order to avoid this problem, and check the robustness of the results, the PSM analysis has been used to assess the impact of financial inclusion (the treatment). In the PSM analysis, the impact of the treatment is estimated rigorously by comparing the outcomes of the treated group, and the control group based on some common characteristics. This method helps draw a comparison by obtaining a summary variable called the propensity score (PS), which is the probability of being treated, based on the treated conditions (observable characteristics). Moreover, the explanatory variables (see ) are used as observable characteristics to estimate the PS. The observations from the treatment and control groups with similar (or closest) PS have also been matched to form a counterfactual setting (Bryson et al., Citation2002; Pan & Bai, Citation2015; Thavaneswaran, n.d.).

All the outcome variables have been tested for the treatment variable‘ financial inclusion‘ (LoanMFI). The results of both the ‘Psmatch‘ and ‘Psmatch2‘ had been obtained for rigorous analysis. The Average Treatment Effect on the Treated (ATT) was obtained by using the Nearest Neighbor (NN), Kernel, Radius Caliper, and Stratification methods. In addition to this, (Becker & Ichino, Citation2002) advised that the results of all the methods were estimated and presented to check the robustness, but the Kernel method results were preferred and discussed. The bootstrap procedure has been used for the Kernel matching method, in order to obtain more robust coefficients and respective standard errors. Therefore, the ATT () for financial inclusion can thus be given as:

(A)

(A)

where, Xi represents the set of outcome variables, X1 represents the measures related to the treatment group, and X0 represents the measures related to the control group.

4. Empirical results and discussion

4.1. Descriptive Analysis

presents the descriptive statistics of the treatment and control groups. Out of the total, 503 respondents (50.1%) have not taken loans from MFBs (control group), and 500 respondents (49.9%) have taken loans from MFBs (treatment group). As some MFBs focus on females only, therefore, the majority of the sample (66.8%) comprises of female respondents. out of these 328 individuals (49.0%) requested and gained access to microfinance. Out of the total number of males (333), 172 (51.7%) belonged to the treatment group. The sample is almost evenly distributed in the urban (51.4%), and rural (48.6%) populations. It seems that MFBs prefer younger people, as the majority of the respondents (68.7%) are below the age of 40 years. This is because they can work harder, and also reap the benefits of the loans and repay them promptly. Furthermore, 90.7% of the respondents were either single or married, whereas only 9.3% of respondents were widows/widowers or divorced.

Table 4. Two-way stratified random data of treatment group and control group.

Moving on, 596 (59.4%) respondents reported that their incomes had not improved in the last two years, out of which 417 (70.0%) belonged to the control group, and 179 (30.0%) belonged to the treatment group. The rest of the 407 (40.6%) respondents stated that their income had improved, out of which 321 (78.9%) had taken loans from MFBs. In this way, 64.2% of the treatment group reported that their income had increased over time, which reflects the positive impact of financial inclusion on an income level. More importantly, the statistics of ‘MPInow‘ reflected that 707 (70.5%) respondents were no longer multidimensional poor, whereas only 296 (29.5%) respondents were still below the poverty line. From the results of ‘MPIDiff‘, it has been observed that the multidimensional poverty of 64.3% of the respondents has been reduced over time, out of which 350 belonged to the treatment group. At the same time, the multidimensional poverty of 244 respondents was unchanged. Results postulate that there has been a marginal reduction in multidimensional poverty, primarily due to financial inclusion.

Moving on, 499 respondents mentioned that their social status improved over time, and 227 (45.4%) of these belonged to the treatment group. 54.1% of the treatment group explained that their social status did not improve over time. This indicated that at large, the social status of the treatment group had not improved, reflecting that social development is not influenced by financial inclusion.

4.2. Propensity score

presents the result of the Probit model, a measure that determines the probability of receiving microfinancing options and its determinants. The overall model was observed to be significant, thus reflecting that gender, age, region, marital status, number of school-going children, can duly explain the probability of receiving microfinance. It is also observed that Females are more likely to receive microfinance. Moreover, respondents of higher age groups, and those who belong to the rural areas are less likely to receive any microfinance. Applicants having marital status as single are less likely to receive microfinance. The higher the number of school-going children in a family, the higher the probability of receiving a loan. These socio-economic indicators (having significant results) show the relevance to the selection criteria. From this Probit model, the PS for each respondent is estimated, and is used to estimate the effect (ATT) of financial inclusion on the different dimensions of socio-economic development.

Table 5. Estimation of propensity scores (probit model) – determinants of the probability of receiving microfinance.

4.3. Impact on the sustainable livelihood

According to the analysis of the t-statistics (see ), a significant difference in the per capita household income growth of the borrowers and non-borrowers has been observed. It theorises that the growth in the income level of the borrowers is marginally higher. Furthermore, the borrowers (treatment group) also witnessed growth in the ownership status of the house, roof material of the house, overall condition of the house, number of school-going children, accessibility to safe drinking water, ability to bear medical expenditure, and clothing expenditures, as compared to their control group counterparts.

Table 6. Results of t-statistics for exposure to microfinance as a grouping variable.

Furthermore, logistic regression analysis is carried out to assess the impact of microfinance on the sustainable livelihoods of impoverished people. The results (see ) suggest that at large, sustainable livelihoods are likely to improve due to financial inclusion.

Table 7. Impact of microfinance on the sustainable livelihoods.

The concept of Purchasing power parity is the basic yardstick to estimate poverty, and the per capita household income growth positively influences it. It is the fundamental indicator of poverty reduction, as well as a reflection of sustainable livelihoods. Therefore, it is considered to be the first indication, and a pivotal step towards socio-economic development. The absolute poverty level varies across the countries (Mazumder & Lu, Citation2015). Therefore, the focuses on absolute poverty measures restrict the scope of this study. The logistic model with ‘chngincom‘ as a dependent variable has thus taken the following functional form:

(1)

(1)

The results suggest that the increase in income is a likely reality for those who have received microfinancing (OR = 8.91). Therefore inferring that financial inclusion increases the chance of improvement in the income level. This income growth eventually improves the ability to bear day-to-day expenditures, and capital expenditures, respectively.

In order to analyze it further, a logistic regression analyses were carried out for the other proxies of sustainable livelihoods. The results (presented in ) showed that the accessibility to safe drinking water, the ability to meet medical expenditures, expenditures on clothing, and the number of children going to school are likely to improve due to financial inclusion. Moreover, according to the findings, more often than not, children are immediately available labour for the family‘s earning adults, and serving in the family business hinders their academic progression as well (Shimamura & Lastarria-Cornhiel, Citation2010). On the contrary, we have inferred that financial inclusion is likely to influence children‘s education positively. Whereas, the cooking fuel used in the kitchen is not likely to improve due to financial inclusion. Cooking fuel, in fact, is associated with the lifestyle and the living standard; therefore, it is hard to experience an improvement in it in the short run.

Accessibility to safe drinking water is of paramount importance, which reduces the vulnerability to many diseases. People use water from a pond, extracted from a tube-well/boring, tap water, and boiled water. During the survey, mixed evidence was been found regarding the availability of safe drinking water among the borrowers and non-borrowers. However, the t-test and logistic regression results suggested that the treatment group witnessed a marginal improvement in this accessibility.

In rural areas, one‘s accessibility to medical facilities is a serious dilemma. This is primarily because of the unavailability of medical facilities, affordability (if the medical facility is available), and the willingness to have the medical facilities to meet these needs. During the survey, it was observed that these people were more focussed on the guidance provided by peers/fakirs/taweez (witch doctors/quacks/amulets), etc., and this mindset, being ingrained in since generations, is one that is hard to alter. In general, the survey and the analysis inferred that if an individual is willing to avail a medical facility, their accessibility is likely to improve due to financial inclusion. Borrowers are better able to gain benefit from proper medical practitioners or specialists. Furthermore, the better quality of the environment and drinking water reduces the need for medical facilities. Overall, it is inferred that accessibility to the necessities of life is likely to improve due to financial inclusion, thus reflecting economic development.

As far as the expenditures of capital nature are concerned, we can prioritise them after the day-to-day expenditures. The chances of betterment in the ownership status of the house, roof material used in the house, and the overall condition of the house tend to improve with the exposure to microfinance. At the same time, household assets are not likely to grow with the exposure to microfinance. This means that overall, financial inclusion is likely to positively influence infrastructural development, which marginally improves the living standards of people. The results also corroborate the findings of (Mazumder & Lu, Citation2015; M. M. Uddin, Citation2017). Furthermore, results also indicate that respondents who belonged to urban areas are likely to have better access to infrastructure and condition of their houses, as compared to the same in rural areas.

In general, the results of the logistic regression models infer that out of ten, eight are likely to improve because of financial inclusion. Furthermore, the chances of a positive improvement in the ownership status of the house, the number of school-going children, cooking fuel used, access to safe drinking water, and expenditure on clothing tends to be higher in women. The personal education of the respondents does not impact sustainable livelihoods. Unlike the ideas put forth by (Imai et al., Citation2012), no difference has been found in the rural and urban areas. Whereas, the clothing expenditures, and the condition of the house are likely to deteriorate in rural areas, which corroborates the findings (Valead et al., Citation2018). As described by Nizam et al. (Citation2020), our findings support the argument pertaining to the lack of outreach, and the mission drift theory.

In order to make more rigorous inferences about sustainable livelihood, and also confirm the results of the logistic regression analysis, the PSM analysis has also been carried out. Results of all the methods explored (see ) are quite similar, and therefore posit that financial inclusion positively influences sustainable livelihoods. It is worthy of taking note that the users of microfinancing options have witnessed a significant improvement in their income levels (Khan et al., Citation2014; Samat et al., Citation2018; Valead et al., Citation2018), ownership status of the house, roof material used in a house, overall condition of the house (Noreen et al., Citation2011), number of school-going children (Holvoet, Citation2004; Noreen et al., Citation2011), and access to clean drinking water (as described by (Mazumder & Lu, Citation2015)). Whereas, there seems to be no significant difference (among borrowers and non-borrowers) in their household assets (as described by (Noreen et al., Citation2011) and the cooking fuel used. This lack of evidence regarding the positive impact on the consumption and lifestyle is aligned with the results reported by other scholars (Attanasio et al., Citation2015), (Augsburg et al., Citation2015), and (S. Amin et al., Citation2003). Hence, we can affirm that the study induces (Tariq et al., Citation2015) that exposure to microfinance improves the economic condition of impoverished people.

Table 8. PSM estimates for the impact of microfinance on sustainable livelihoods.

Conclusively, for those who have exposure to microfinance, their income level is most likely to improve, and on average, their poverty level is also likely to reduce due to microfinance, thus reflecting an improvement in the sustainable livelihood that they may achieve. Therefore, as described by (Mazumder & Lu, Citation2015; M. M. Uddin, Citation2017), people’s ability to spend on clothing, medical facility, and clean drinking water is also likely to improve. Clean drinking water shall prevent them from diseases, and it would positively affect their overall quality of life as well. However, the overall sustainable livelihoods tend to deteriorate in rural areas. Furthermore, the expenditure related to the infrastructural development of the house is also likely to improve; and these results are aligned with the findings of (Niaz & Iqbal, Citation2019). This analysis signals a positive contribution of microfinancing towards the living standards of impoverished people. To have more concrete inferences about the impact on living standards, the LSI has been developed by incorporating important dimensions that are related to the living standards.

4.4. Impact on living standard (LSI)

The results of the t-statistics (see ) postulate that the borrowers‘ growth in living standards (LSI) is at a higher level. This indicates that due to financial inclusion, the living standards have marginally improved. The multiple linear regressions and the PSM analysis have thus been carried out for concrete inferences about the impact of financial inclusion, on the growth of living standards.

The regression analysis results (presented in ) have indicated that on average, the living standards have witnessed a marginal growth over time, and the exposure to microfinance further has augmented this growth in the living standards. As (Mazumder & Lu, Citation2015) have described, those who have exposure to microfinancing can better invest in infrastructural development. The living standard deteriorates with the increase in age, in rural areas, and with a higher number of school-going children, in the social setup. For instance, in a country like Pakistan, with the increase in age the responsibilities towards the family tend to increase. This causes a shift in priorities and, therefore, less investment towards the improvement in living standards. In addition to this, a higher number of school-going children indicates higher expenditures on schooling, therefore observing lesser investment towards the living standards. Respondents who belonged to urban areas have a better living standard than those in the rural areas, primarily due to the fact that the exposure and availability of facilities in the urban areas are better. Whereas the people of rural areas are not entirely interested in improving their living standards, as they are somewhat content in their mud houses, and basic level of utensils. No association of education and living standards has been observed, unlike (Mazumder & Lu, Citation2015), who witnessed an inverse association of education and living standards.

In order to check the robustness of these results, the PSM analysis has also been carried out. The results (as presented in ) confirm that the growth in the living standard of borrowers is slightly higher than the same for non-borrowers (ATT = 0.277, p = 0.00). Therefore, it can be concluded that impoverished people who are exposed to microfinance have managed to improve their living standards over time.

Table 10. PSM estimates - impact assessment on multidimensional poverty and living standard.

It is noteworthy that one important social factor was revealed during the survey: that impoverished borrowers invest in the infrastructure of the inherited houses (or land). In most cases, those living in joint family systems build their room (mostly built of wooden roof or T-iron) in a portion of the common land in order to start their life, apart from the joint family. Those who had exposure to microfinance could easily afford this infrastructural development, without disturbing their entrepreneurial activities. It has also been revealed that in some cases, the loan taken for entrepreneurial activities was invested in such infrastructural developments.

4.5. Impact on multidimensional poverty

As endorsed by scholars (Das, Citation2019; Feeny and Mcdonald, Citation2016), MPI is estimated (see ) in order to assess the multidimensional poverty of the respondents. The impact of microfinance, on the current multidimensional poverty, and the change in multidimensional poverty has been assessed with the help of the univariate and multivariate analysis. The ‘MPINow‘ and ‘MPIDiff‘ have also been used as proxies of the current multidimensional poverty level, and the change in multidimensional poverty, respectively.

The descriptive statistics (see ) pertaining to the study indicate that borrowers tend to be comparatively less poor. Furthermore, the reduction in the multidimensional poverty is higher in the borrowers than non-borrowers. In addition to this, the results of the t-statistics (see ) suggested that the multidimensional poverty level of the treatment group (borrowers) is significantly different as compared to that of the control group (non-borrowers), thus reflecting that borrowers are less poor than the non-borrowers. Furthermore, out of the total, the poverty level of 645 respondents had been reduced, out of which 350 (54.3%) belonged to the treatment group (they are 70% of the total borrowers). Whereas, only 21.8% (109) and 8.2% (41) of the borrowers had the same poverty level, or their poverty increased, respectively. This indicated that the borrowers have a marginally better tendency for poverty reduction.

The result of the regression analysis (see ) indicates that, on average, all the respondents were below the poverty line (α = 0.353), as the threshold level (poverty line) was worked out to be ‘0.33′. At the same time, poverty was at 0.023 units lower in the borrowers than the non-borrowers. These findings happen to be consistent with the extant literature written on the discipline (Das, Citation2019; Feeny & McDonald, Citation2016; Niaz & Iqbal, Citation2019). It also indicates that those who have exposure to microfinance are less poor in multidimensional terms. Furthermore, respondents having a higher level of education are less poor in multidimensional terms. This endorses the results of (U. Awan et al., Citation2019). The number of school-going children is negatively associated with the multidimensional poor, which happens to be a good sign. At the same time, more number of children tends to enhance the level of multidimensional poverty. This is primarily because of the higher level of day-to-day expenditures that augment their poverty level.

Table 9. Multiple Linear Regression – Impact assessment on Multidimensional Poverty and Living Standard.

For the changes experienced in multidimensional poverty ‘MPIDiff,‘ the regression analysis postulates that in general, the multidimensional poverty is reduced in all the respondents (α = −0.077). Moreover, the exposure to microfinance ‘LoanMFI‘ further reduces multidimensional poverty by 0.023 units. It indicates that the multidimensional poverty of borrowers has reduced by 0.10 units (‘-0.077‘ + ‘-0.023‘). Furthermore, this poverty reduction factor is higher in women as compared to men, therefore endorsing the results reported by the scholars (Niaz & Iqbal, Citation2019), (Valead et al., Citation2018), (Miled & Rejeb, Citation2015). This is primarily because females are more focussed and dedicated towards making their situation better. They also invest the maximum possible time in their entrepreneurial activities. Moreover, marital status, number of children, and the number of school-going children are the source of poverty reduction for them. However, personal education does not support multidimensional poverty reduction. Rather, multidimensional poverty increases with the increase in the level of education, thus confirming the logistic regression analysis results. It indicates that persons with lesser, or even no education are comparatively better able to fight against poverty. This is because the nature and environment of the businesses (at the cottage industry level) are not entirely respected in the society. An uneducated person, or a person with a lower level of education starts working even in adverse working conditions. At the same time, an educated person is conscious of the level and environment of the work, which hinders their economic growth (poverty reduction as well) in the short run. The results of the regression analysis (for ‘MPINow‘ and ‘MPIDiff‘) reflect that educated individuals are comparatively less poor, but their poverty does not reduce during the period they spend during their time studying. Another possible reason is the short period of the analysis, as the survey assesses the change over a two year time span only. Therefore, keeping the other findings in view, it can be concluded that the focus on the quality of operations somewhat delays the development process, but will not harm economic development in the longer run.

In order to assess the robustness of the results, the PSM analysis has also been carried out for ‘MPINow‘ and ‘MPIDiff‘. The PSM estimates (see ) the inference that the borrowers are less poor than the non-borrowers (ATT= −0.027, p = 0.00). Furthermore, the results (ATT=-0.024, p = 0.00) also posit that multidimensional poverty has significantly reduced in the borrowers over time. Conforming to the regression analysis results, it can also be assumed and inferred that access to microfinance causes a marginal reduction in the multidimensional poverty. Overall, the results of the regression and PSM confirm that financial inclusion, through microfinance, has a favorable impact on multidimensional poverty, and multidimensional poverty reduction. These results also support the logistic regression results, thus confirming that microfinance has a significant impact on the economic development of impoverished people.

4.6. Impact on social development

Poverty tends to deteriorate the social status and recognition. In this regard, it has been hypothesised that the accessibility to economic resources improves the social status of individuals, and this is called social development. Following this context, the descriptive analysis (see ) indicates that in comparative terms, a high number of borrowers (54.6%) reported that their social status did not improve over time. At the same time, 54.1% of the non-borrowers responded that their social status had improved over time. Similarly, the results of the t-statistics (see ) suggest that social development is marginally higher in the non-borrowers.

The logistic regression analysis results (see ) also show that the improvement in the social status is less likely to be possible for the borrowers. In order to check the robustness, the PSM analysis has also been carried out, and the results (see ) conform to the results of the logistic regression. From the results, it has been inferred that, in general, the respondents exposed to microfinance did not witness an improvement in their social status. This essentially means the exposure to microfinance is not likely to influence social development, and these results are contradictory to the results reported by the scholars such as (Niaz & Iqbal, Citation2019), (Tariq et al., Citation2015), and (Durrani et al., Citation2011).

The negative impact on the perceived social status is a bewildering phenomenon. It reflects that borrowers have not witnessed an improvement in their social status, whereas their economic status has been improved. In this regard, it is contradictory to both the underline theory and the literature, as it depicts that social development is inversely associated with financial inclusion. This is primarily because borrowers face financial tightness in the short run, due to the increased financial liability, which would eventually be adjusted in the medium-run, or the long run. Therefore, keeping in view the other empirical findings of this study, it can be inferred that this perceived deterioration in the social status is for the short-run only, and will improve after some time.

Whereas, the deterioration in social status with the change in marital status is quite logical in certain socio-cultural settings, such as those in Pakistan, where divorced individuals or widowers have a lesser degree of social acceptability. Therefore, the social development of a widower is less likely to be favorable as compared to a single or married person. However, the perceived social status of the impoverished people belonging to the rural areas has improved over time. This reflects a positive contribution of microfinance towards the rural poor, which positively signals outreach, and counters the mission drift theory.

Overall, the empirical analysis reveals that exposure to microfinance contributes significantly to the economic development of impoverished people. Due to the exposure to microfinance, sustainable livelihoods, infrastructural development, and living standards have also improved, whereas multidimensional poverty has reduced. As discussed by Montgomery and Weiss (Citation2011), this study confirms the positive impact of microfinance provided by commercially operated MFBs, on the economic development of impoverished people.

As the dimensions of socio-economic development under inquiry are associated with SDGs, clear evidence has been found, affirming that the exposure to microfinance will help attain SDGs, by improving the socio-economic condition of the impoverished segment of society.

5. Conclusion

The impact of financial inclusion on the socio-economic development of impoverished people, and the accomplishment of SDGs has been thoroughly investigated in this study. Ten dimensions related to sustainable livelihood, and one dimension of social development have been examined through logistic regression method and the PSM analysis. Furthermore, two indices, namely living standard (LSI) and multidimensional poverty (MPI) were estimated, so as to assess economic development. The Regression analysis and PSM have been used to observe the impact of financial inclusion.

This paper substantiates that financial inclusion significantly contributes towards the economic development of impoverished people. Also, it is noteworthy that financial inclusion improves the income levels of the borrowers, and consequently the spending on clothing, education of children, and medication. An increase in this income ignites economic development by supporting day-to-day expenditures and infrastructural development. In addition to this, the improvements in roof material, overall condition of the facility, accessibility to clean drinking water, and ownership status of the house is positively influenced by the financial inclusion. This positive impact of financial inclusion is greater on borrowers who are women.

As discussed, poverty is a multidimensional phenomenon, and therefore, the estimation of MPI and its investigation about the impact of financial inclusion on it has been carried out. The results also inferred that exposure to microfinance helps fight against (multidimensional) poverty, and also reduces it marginally over time. Along with the type of roof, floor, and overall infrastructure of the house, the availability of a working restroom, household assets, electricity, proper sanitation, cooking fuel used, and the availability of clean drinking water are key ingredients of one’s decent living standard. Therefore, LSI has been developed by incorporating all these dimensions. The empirical investigation signifies that there is a positive impact of financial inclusion on the living standard of these impoverished people. Overall, these results confirm the significant contribution of financial inclusion in the economic development of impoverished people.

Furthermore, the potential for this improvement in economic conditions is more prevalent in urban areas than the rural ones. This has raised a serious question regarding the outreach of the MFBs, and the utilisation of funds in rural areas. However, no evidence has been found about the positive impact of microfinance on social development. This is rather disappointing, as it undervalues the scope of MFBs, and the benefits of microfinance. However, the betterment achieved in the sustainable livelihoods and multidimensional poverty reduction indicate that the financial liability generated through microfinance causes temporary financial distress, due to which the perceived social status does deteriorates. Nevertheless, this is expected to be a temporary phenomenon, and this stress would end with the tenure of the loan.

Financial inclusion shall be a gateway for achieving the SDGs in the long run, as the seven goals (no poverty, zero hunger, good health & well-being, quality education, gender equality, clean water & sanitation, and decent work & economic growth) are directly linked with the economic conditions of the individuals, and this study infers that these could be attained through financial inclusion. This study also corroborates that the incidence of poverty in women is reduced significantly due to financial inclusion, thus leading towards gender equality. This study conforms to the findings of the scholars, such as (Atmadja et al., Citation2016; Lopatta et al., Citation2017; Montgomery & Weiss, Citation2011; Samat et al., Citation2018), and describes that microfinance helps in attaining the development goals.

6. Policy implication

This study has produced profound evidence regarding the positive contribution of MFBs towards the economic development of impoverished people. However, this success only is not sufficient because of the limited outreach. Due to a tough and autocratic approach of MFBs, people are reluctant to avail microfinancing, which could be another reason for social distress (Samat et al., Citation2018). We therefore endorse the argument of (E. Wilson et al., Citation2020), there must be structured reforms at the corporate and government level. In order to promote financial inclusion with better outreach. It is also recommended that MFBs must relax their lending procedures, loan tenure, and collection processes. They must therefore increase their loan tenure and reduce the interest rate so that these economically distressed segments of the society may not feel an immense amount of social distress. For this to happen, governments must launch a special package for MFBs, and lend them at zero interest rate, or at least on subsidised rates, with a condition to increase the outreach. Such a strategy shall be far better than the government‘s cash-dole out, income support, and rural development programs. If MFBs lend at economical interest rates to the impoverished people, and they use these funds efficiently, poverty will experience a significant reduction. The consistent and persistent efforts to promote financial inclusion in this impoverished segment of the society shall lead to economic development and prosperity, as targeted in SDGs by the UN.

Furthermore, Pakistan Microfinance Network (PMN) explained that MFBs operating in Pakistan only serve the transitory poor and above. Extremely poor and chronically poor people have been neglected by MFBs (Hina et al., Citation2012). Moreover, careful policy intervention shall strengthen the true and effective microfinance outreach. Nonetheless, the current lending schemes shall continue to augment the socio-economic development, despite its apparent shortfalls. Also, the MFBs must ensure the effective and efficient provision of funds to moderate poor, and their socio-economic development shall contribute towards the poverty reduction of chronic and extreme poor classes. Evidently, this process will be relatively slower, and socio-economic development could be delayed, but this is a sustainable and risk averse model for commercial MFBs. The extreme and chronic poor also lack education, skills, and aptitude that impedes their efforts for their socio-economic development. If MFBs provide funds to them, it can harm the survival and growth of MFBs as well.

The recent adoption of information technology, as tool of operation by the MFBs of Pakistan, is a positive development. But regrettably, it is being used only as a money transfer mechanism. It has been observed that most of the telecommunication companies have (wholly or partly owned) MFBs as their subsidiaries. They are purely focussed on improving their funds‘ transfer business, rather than working for poverty alleviation, ultimately hindering the social performance of MFBs. MFBs must use this technological advancement in loaning and collection processes, in order to reduce their cost of operations. This will certainly result into sustainable outreach. This misplacement of objectives needs to be rectified by the regulators through a more effective oversight of such MFBs.

7. Limitations and future research direction

This study addresses the contribution of microfinance towards sustainable livelihood and multidimensional poverty. However, this contribution is not independent of the macroeconomic environment. Macro-economic indicators, such as discount points (cost of capital), monitory-fiscal mix, ease of doing business, cost of energy, overall economic condition, GDP growth, exchange rates, government policies, etc., directly affect the entrepreneurial activity at all levels. Due to methodological limitations, these macroeconomic indicators could not be incorporated in this study. Therefore, such macro-economic indicators must also be incorporated in the future empirical investigations. Most of the impoverished people start up their micro-enterprises. This contributions of microfinance towards enterprise, and entrepreneurial development must also be considered in the future studies.

References

- Agbaeze, E. K., & Onwuka, I. O. (2014). Microfinance banks and rural development: The Nigeria experience. International Journal of Rural Management, 10(2), 147–171. https://doi.org/10.1177/0973005214546597

- Akram, M., & Hussain, I. (2011). The role of microfinance in uplifting income level: A study of District Okara-Pakistan. Interdisciplinary Journal of Contemporary Research in Business, 2(11), 83–94.

- Al-Shami, S. S. A., Razali, R. M., & Rashid, N. (2018). The effect of microcredit on women empowerment in welfare and decisions making in Malaysia. Social Indicators Research, 137(3), 1073–1090. https://doi.org/10.1007/s11205-017-1632-2

- Amin, R., & Becker, S. (1998). NGO-promoted microcredit programs and women’s empowerment in rural Bangladesh: Quantitative and qualitative evidence. The Journal of Developing Areas, 32(2), 221–236.

- Amin, S., Rai, A. S., & Topa, G. (2003). Does microcredit reach the poor and vulnerable? Evidence from northern Bangladesh. Journal of Development Economics, 70(1), 59–82. https://doi.org/10.1016/S0304-3878(02)00087-1

- Asadullah, M. N., & Savoia, A. (2018). Poverty reduction during 1990–2013: Did millennium development goals adoption and state capacity matter? World Development, 105, 70–82. https://doi.org/10.1016/j.worlddev.2017.12.010

- Atmadja, A. S., Su, J.-J., & Sharma, P. (2016). Examining the impact of microfinance on microenterprise performance (implications for women-owned microenterprises in Indonesia). International Journal of Social Economics, 43(10), 962–981. https://doi.org/10.1108/IJSE-08-2014-0158

- Attanasio, O., Augsburg, B., De Haas, R., Fitzsimons, E., & Harmgart, H. (2015). The impacts of microfinance: Evidence from joint-liability lending in Mongolia. American Economic Journal: Applied Economics, 7(1), 90–122.

- Audu, M. L., & Achegbulu, J. O. (2011). Microfinance and poverty reduction: The Nigerian experience. International Business and Management, 3(1), 220–227.

- Augsburg, B., De Haas, R., Harmgart, H., & Meghir, C. (2015). The impacts of microcredit: Evidence from Bosnia and Herzegovina. American Economic Journal: Applied Economics, 7(1), 183–203.

- Awan, M. S., Malik, N., Sarwar, H., & Waqas, M. (2011). Impact of education on poverty reduction.

- Awan, U., Sroufe, R., & Kraslawski, A. (2019). Creativity enables sustainable development: Supplier engagement as a boundary condition for the positive effect on green innovation. Journal of Cleaner Production, 226, 172–185. https://doi.org/10.1016/j.jclepro.2019.03.308

- Banerjee, A., Dolado, J., & Mestre, R. (1998). Error‐correction mechanism tests for cointegration in a single‐equation framework. Journal of Time Series Analysis, 19(3), 267–283. https://doi.org/10.1111/1467-9892.00091

- Bank, (2017). W. World development report 2018: Learning to realize education’s promise. The World Bank.

- Becker, S. O., & Ichino, A. (2002). Estimation of average treatment effects based on propensity scores. The Stata Journal: Promoting Communications on Statistics and Stata, 2(4), 358–377. https://doi.org/10.1177/1536867X0200200403

- Blanco-Oliver, A., & Irimia-Diéguez, A. (2021). Impact of outreach on financial performance of microfinance institutions: A moderated mediation model of productivity, loan portfolio quality, and profit status. Review of Managerial Science, 15(3), 633–636. https://doi.org/10.1007/s11846-019-00353-4

- Bruton, G., Khavul, S., Siegel, D., & Wright, M. (2015). New financial alternatives in seeding entrepreneurship: Microfinance, crowdfunding, and peer–to–peer innovations. SAGE Publications Sage CA.

- Bryson, A., Dorsett, R., & Purdon, S. (2002). The use of propensity score matching in the evaluation of active labour market policies.

- Chowdhury, A. R., Fackler, J. S., & McMillin, W. D. (1986). Monetary policy, fiscal policy, and investment spending: An empirical analysis. Southern Economic Journal, 52(3), 794–806. https://doi.org/10.2307/1059275

- Chowdhury, T. A., & Mukhopadhaya, P. (2012). Assessment of multidimensional poverty and effectiveness of microfinance-driven government and NGO projects in the rural Bangladesh. The Journal of Socio-Economics, 41(5), 500–512. https://doi.org/10.1016/j.socec.2012.04.016

- Cristea, M., Noja, G. G., Dănăcică, D. E., & Ştefea, P. (2020). Population ageing, labour productivity and economic welfare in the European Union. Economic Research-Ekonomska Istraživanja, 33(1), 1354–1376. https://doi.org/10.1080/1331677X.2020.1748507

- Das, T. (2019). Does credit access lead to expansion of income and multidimensional poverty? A study of rural Assam. International Journal of Social Economics, 46(2), 252–270. https://doi.org/10.1108/IJSE-12-2017-0592

- Durrani, M. K. K., Usman, A., Malik, M. I., & Shafiq, A. (2011). Role of micro finance in reducing poverty: A look at social and economic factors. International Journal of Business and Social Science, 2(21). https://doi.org/10.7176/JESD/10-5-04

- Emler, N. (2001). Self esteem: The costs and causes of low self worth. York Publishing Services.

- Feeny, S., & McDonald, L. (2016). Vulnerability to multidimensional poverty: Findings from households in Melanesia. The Journal of Development Studies, 52(3), 447–464. https://doi.org/10.1080/00220388.2015.1075974

- He, Y., & Collins, A. R. (2021). Optimal dynamic electricity consumption function estimation: An institutional experimental evidence from Guangzhou, China (1949-2016). Economic Research-Ekonomska Istraživanja, 0(0), 1–25. https://doi.org/10.1080/1331677X.2021.1875864

- Hermes, N., & Lensink, R. (2007). The empirics of microfinance: What do we know? The Economic Journal, 117(517), F1–F10. https://doi.org/10.1111/j.1468-0297.2007.02013.x

- Hina, H., Lightfoot, G., & Harvie, D. (2012). Microfinance: Sustainable Entrepreneurship and the Funding Gap.

- Holvoet, N. (2004). Impact of microfinance programs on children’s education: Do the gender of the borrower and the delivery model matter? Journal of Microfinance/ESR Review, 6(2), 3.

- Hossain, M. A., & Asada, K. (1984). Inactivation of ascorbate peroxidase in spinach chloroplasts on dark addition of hydrogen peroxide: Its protection by ascorbate. Plant and Cell Physiology, 25(7), 1285–1295.

- Hossain, F., & Knight, T. (2008). Can micro-credit improve the livelihoods of the poor and disadvantaged?*: Empirical observations from Bangladesh. International Development Planning Review, 30(2), 155–175. https://doi.org/10.3828/idpr.30.2.4

- Imai, K. S., Gaiha, R., Thapa, G., & Annim, S. K. (2012). Microfinance and poverty—A macro perspective. World Development, 40(8), 1675–1689. https://doi.org/10.1016/j.worlddev.2012.04.013

- Jamal, H. (2008). Exploring the impact of Microfinance in Pakistan. Social Policy and Development Centre.

- Jamil, B., Yaping, S., Ud Din, N., & Nazneen, S. (2021). Do effective public governance and gender (in)equality matter for poverty? Economic Research-Ekonomska Istraživanja, 0(0), 1–17. https://doi.org/10.1080/1331677X.2021.1889391

- Ji, X., Zhang, Y., Mirza, N., Umar, M., & Rizvi, S. K. A. (2021). The impact of carbon neutrality on the investment performance: Evidence from the equity mutual funds in BRICS. Journal of Environmental Management, 297, 113228 https://doi.org/10.1016/j.jenvman.2021.113228

- Khan, A. J., Azim, P., & Syed, S. H. (2014). The impact of exchange rate volatility on trade: A panel study on Pakistan’s trading partners. The Lahore Journal of Economics, 19(1), 31–66. https://doi.org/10.35536/lje.2014.v19.i1.a2

- Khanam, D., Mohiuddin, M., Hoque, A., & Weber, O. (2018). Financing micro-entrepreneurs for poverty alleviation: A performance analysis of microfinance services offered by BRAC, ASA, and Proshika from Bangladesh. Journal of Global Entrepreneurship Research, 8(1), 1–17. https://doi.org/10.1186/s40497-018-0114-6

- Kumari, J. P., Azam, S. F., & Khalidah, S. (2019). The effect of microfinance services on poverty reduction: Analysis of empirical evidence in Sri Lankan perspectives. European Journal of Economic and Financial Research, 3(5). http://dx.doi.org/10.46827/ejefr.v0i0.654

- Liu, Y. (2021). Does urban spatial structure affect labour income? – Research based on 97 cities in China. Economic Research-Ekonomska Istraživanja, 34(1), 545–569. https://doi.org/10.1080/1331677X.2020.1798265

- Lopatta, K., & Tchikov, M. (2017). The causal relationship of microfinance and economic development: Evidence from transnational data. International Journal of Financial Research, 8(3), 162–171. https://doi.org/10.5430/ijfr.v8n3p162

- Lopatta, K., Tchikov, M., Jaeschke, R., & Lodhia, S. (2017). Sustainable development and microfinance: The effect of outreach and profitability on microfinance institutions’ development mission. Sustainable Development, 25(5), 386–399. https://doi.org/10.1002/sd.1663

- Mazumder, M. S. U., & Lu, W. (2015). What impact does microfinance have on rural livelihood? A comparison of governmental and non-governmental microfinance programs in Bangladesh. World Development, 68, 336–354. https://doi.org/10.1016/j.worlddev.2014.12.002

- Miled, K. B. H., & Rejeb, J.-E B. (2015). Microfinance and poverty reduction: A review and synthesis of empirical evidence. Procedia - Social and Behavioral Sciences, 195, 705–712. https://doi.org/10.1016/j.sbspro.2015.06.339

- Mirza, N., Hasnaoui, J. A., Naqvi, B., & Rizvi, S. K. A. (2020). The impact of human capital efficiency on Latin American mutual funds during Covid-19 outbreak. Swiss Journal of Economics and Statistics, 156(1), 1–7. https://doi.org/10.1186/s41937-020-00066-6

- Mok, K. (2000). Economic Growth and People’s Livelihood. In K. Mok, (Ed.), Social and Political Development in Post-Reform China. (pp. 19–38). https://doi.org/10.1057/9780230286436_2

- Montgomery, H., & Weiss, J. (2011). Can commercially-oriented microfinance help meet the millennium development goals? Evidence from Pakistan. World Development, 39(1), 87–109. https://doi.org/10.1016/j.worlddev.2010.09.001

- Nadeem, M., Jun, Y., Niazi, M., Tian, Y., & Subhan, S. (2021). Paths of economic development: A global evidence for the mediating role of institutions for participation in global value chains. Economic Research-Ekonomska Istraživanja, 34(1), 687–708. https://doi.org/10.1080/1331677X.2020.1804426

- Naqvi, B., Mirza, N., Rizvi, S. K. A., Porada-Rochoń, M., & Itani, R. (2021). Is there a green fund premium? Evidence from twenty seven emerging markets. Global Finance Journal, 50, 100656. https://doi.org/10.1016/j.gfj.2021.100656

- Niaz, M. U., & Iqbal, M. (2019). Effect of Microfinance on Women Empowerment: A Case Study of Pakistan. Paradigms, 13(1), 52–59.

- Nizam, R., Karim, Z. A., Rahman, A. A., & Sarmidi, T. (2020). Financial inclusiveness and economic growth: New evidence using a threshold regression analysis. Economic Research-Ekonomska Istraživanja, 33(1), 1465–1484. https://doi.org/10.1080/1331677X.2020.1748508

- Noreen, U. (2011). Impact of microfinance on poverty. Lap Lambert Academic Publ.

- Noreen, U., Imran, R., Zaheer, A., & Saif, M. I. (2011). Impact of microfinance on poverty: A case of Pakistan. World Applied Sciences Journal, 12(6), 877–883.

- Ocasio, V. M. (2012). Essays on the role of microfinance institutions in financial deepening, economic growth and development. Colorado State University.

- Pan, W., & Bai, H. (2015). Propensity score analysis: Fundamentals and developments. Guilford Publications.

- Rajbanshi, R., Huang, M., & Wydick, B. (2015). Measuring microfinance: Assessing the conflict between practitioners and researchers with evidence from Nepal. World Development, 68, 30–47. https://doi.org/10.1016/j.worlddev.2014.11.011

- Sachs, J. D. (2012). From millennium development goals to sustainable development goals. The Lancet, 379(9832), 2206–2211. https://doi.org/10.1016/S0140-6736(12)60685-0