?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Having analysed the history of acquisitions by public Chinese companies over the period of 1996–2020, we document no persistent statistically significant short-term market reaction upon deal completion. Short-term cumulative abnormal returns are non-different from zero regardless of whether the acquisition is the first or one of many on acquirers’ record, whether it is domestic or cross-border or whether it is vertical or horizontal as well as regardless of industry and declared purpose of acquisition. In the overwhelming majority of cases, acquirers’ prior acquisition experience plays no role in shaping short-term post-acquisition returns. Lower returns are associated with serial acquirers especially if the series of acquisitions occurs within the same industry. Likewise, significantly lower cumulative returns are observed if the acquiree is a state-owned entity. Overall, the markets appear to attach no abnormal returns to firms’ inorganic growth regardless of its span across geographies, industries and time.

Keywords:

1. Introduction

Empirical literature concerning the impact of inorganic growth on shareholder wealth creation contains a plethora of ambiguous and frequently contradictory conclusions. The majority of studies (e.g., Cai & Sevilir, Citation2012; Ishii & Xuan, Citation2014; Renneboog & Vansteenkiste, Citation2019) focus on short-term market response to deal completion and conclude that M&A transactions fail to deliver consistent abnormal shareholder returns (Malmendier et al., Citation2018).

While value creating effects of M&As are well-investigated on the empirical material from mature markets, it remains undercovered on emerging markets (Borodin et al., Citation2020; Langenstein et al., Citation2018; Zhang & Haico, Citation2010). The M&A activities of Chinese companies have intensified significantly over the past decade fueled by rapid economic expansion, encouraged by the regulatory framework favouring international expansion and home-market consolidation in pursuit of higher productivity. The resulting surge in acquisitions deserves an in-depth study in terms of ensuing effects for shareholders. The present paper attempts to fill this gap by undertaking a comprehensive review of all acquisitions undertaken by public Chinese companies over the period of 1996–2020 and quantifying their short-term effect on shareholder returns.

Prior studies on mature markets suggest that investors tend to assign a short-term valuation premium to firms that decide to undertake a strategy of inorganic growth by engaging in acquisitions (Dandapani et al., Citation2020). Investors expect acquirers to benefit from consolidation-driven operational improvements, expansion of product portfolio, amelioration of supply chains, synergies, penetration of new markets and increase of market share, appropriation and integration of acquirees’ innovative technologies/knowhow (Haleblian et al., Citation2009). By attracting investors’ interest, such expectations may cause a short-term stock price surge allowing investors to earn superior abnormal returns around transaction completion. The long-term shareholder wealth effects of M&As are, however, contingent upon the effectiveness of post-transaction integration efforts. Therefore, it seems consistent that the shareholder effect of transaction announcements has been shown to gradually wear off for firms undertaking multiple sequential acquisitions (Golubov et al., Citation2015).

The general premise underpinning the theoretical explanations of short-term stock outperformance surrounding deal completion is that initiation of inorganic growth reveals material non-public information about the acquirers’ prospective performance, strategic plans and managerial capabilities. It signals the firms’ preparedness to enter a new stage of their development (Dandapani et al., Citation2020). Depending on whether investors perceive these signals as credible and the acquirers’ growth strategy as feasible, an appropriate stock response ensues (Duppati et al., Citation2015).

In order to verify the short-term shareholder wealth effects of acquisitions, we compiled a comprehensive dataset encompassing 2650 transactions undertaken by 1803 Chinese public companies during 1996–2020. Having quantified and analysed short-term stock price dynamics surrounding deal completion, we found no significant persistently observable abnormal returns accompanying these events regardless of transactions’ geographical or temporal span as well as regardless of types of targets and acquirer–acquiree industry relatedness. Neither acquirers’ prior acquisition experience, nor the timing of the transactions appears to alter these findings. Likewise, acquirer–acquiree complementarity and industry links play no role in shaping short-term post-transaction returns.

Investors appear to assign no short-term premium to firms’ inorganic growth strategy even if it involves international expansion or takeover of acquirees’ technologies/strategic assets. We observe no difference in short-term cumulative abnormal returns (CARs) following the completion of domestic and foreign acquisitions, thereby finding no confirmation for market premium for firms’ internationalisation efforts (Dandapani et al., Citation2020). Lack of such premium may originate both from the resistance that Chinese firms encounter when undertaking international expansion (Zhu & Zhu, Citation2016) and from integration difficulties resulting from cultural and geographical distance between Chinese acquirers and foreign-domiciled acquirees.

At the same time, in line with prior studies (e.g., Aktas et al., Citation2016; Kolasinski & Li, Citation2013), we find that serial acquirers record significantly lower CARs than one-off acquirers. Interestingly, we find no significant differences in marginal effect of each subsequent acquisition for serial acquirers when analysed in isolation from the remainder of the sample (equally insignificant CARs are observed in response to the second, third and fourth subsequent acquisitions). Lower returns are observed among older firms, suggesting that investors may perceive acquisitions as a signal that acquirers exhausted their organic growth potential and are, therefore, forced to resort to inorganic expansion to maintain dynamics.

We advance several possible explanations for the discovered statistical patterns. It is possible that the lack of significant market reaction to acquisition completions may be engendered by information leakages (Ma & Pagan, Citation2009). Another potential explanation may be related to investors’ relatively cold response to M&A deals stemming from their skepticism with regards to the potential value creation through inorganic growth. As a substantial portion of acquisitions do not induce any significant operational performance improvements in acquirers (Buckley et al., Citation2014), investors may regard transactions primarily through the prism of industry consolidation, which exercises an additive rather than cumulative effect on the combined entities’ value creating potential. Finally, absence of a systematic response to deal completion may simply stem from the strength of noise observed on the highly volatile Chinese public capital markets. Even the studies that identify persistent abnormal acquirer returns following deal completion document a relatively modest magnitude of this effect (Offenberg et al., Citation2014), which borders statistical significance. Unlike mature markets, which tend to exhibit gradual growth correlated with general business cycles and investor sentiment, the Chinese market is more likely to experiences subperiods of sharp volatility spikes, exuberant rallies and protracted periods of price stagnation. The price effects of acquisitions may, therefore, become indistinguishable from the impact of other random noise factors.

Unlike prior empirical studies focusing on short-term market response to deal completion (e.g., Li et al., Citation2018; Qian & Zhu, Citation2017), we cross-check the studied effects across a number of observation windows of different lengths (1, 3, 7 and 30 days following deal completion announcement). At the same time, it is the first study to undertake a comprehensive review of the population of acquisitions undertaken by Chinese public acquirers over more than two decades (the bulk of which occurred during the 2010s) during which both their domestic and international acquisition activities experienced a dynamic growth fueled by efficiency-seeking consolidation, economic expansion and softer macroeconomic policies. The institutional specificity of the Chinese capital market, regulatory settings and internationalisation strategies of Chinese companies warrant an in-depth inquiry into the short-term shareholder wealth effects of rapidly growing M&A deals. We dedicate particular attention to the analysis of marginal acquisition effects within series of transactions completed by the same acquirer in order to disentangle the possible impact of prior experience on short-term market response.

2. Literature review

Empirical studies analysing the short-term effects of M&A transactions on shareholder returns fail to reach unambiguous conclusions pointing to the multitude of factors that play a role in shaping investors’ perception of the deal (Netter et al., Citation2011). Short-term event studies remain the method of first choice due to methodological difficulties related to the selection of appropriate long-term return benchmarks and isolation of transaction-specific effects from the long-term dynamics of stock prices and operational performance indicators (Bessembinder et al., Citation2019). The prevailing viewpoint is that abnormal shareholder returns are the best gauge of deals’ success as it directly relates to shareholder value.

While the shareholders of target companies are reported to earn positive abnormal returns originating from acquirers’ bidding efforts and superior negotiating power (Alexandridis et al., Citation2017), the returns accruing to acquirers’ shareholders are documented to be much more modest and impersistent (Maksimovic et al., Citation2011). Cross-transaction returns differentials are explained by a number of factors of organisational, institutional, managerial and cultural origins, which preclude generalisation and encourage further empirical studies on the subject matter.

Several competing hypotheses have been advanced and developed in the empirical literature in an attempt to explain relatively poor or impersistent short-term post-acquisition stock performance of acquirers. To start with, markets may already discount deal-specific information at the moment of transaction finalisation due to information leaks, insider dealing and prior rumors (Baruch et al., Citation2017). Another explanation for meager returns is underpinned by investors’ proclivity to extrapolate acquirers’ fundamentals when assessing the deals’ value crating potential (Rau & Vermaelen, Citation1998). As expected synergies fail to materialise in the short run and valuation ratios slide down regressing to the mean, a stock price adjustments cause acquirer’s returns to shrink. Identification of the sources of short-term abnormal returns remains a methodological challenge as investors’ perceptions, method of transaction settlement and negotiation frictions have been shown to exercise a sizable impact on deal outcomes.

In line with the key research objectives of the present study, we focus on the prior empirical studies that enquired into short-term effects of initial domestic and cross-border acquisitions, acquirers’ prior acquisition experience and target typology on acquirers’ returns.

To start with, the markets are generally recognised to price acquirers’ initial inorganic growth efforts with a valuation premium. First acquisitions are frequently reported to earn positive short-term abnormal returns (Antoniou et al., Citation2007). Investors appear to perceive the completion of the first transaction as evidence of acquirers’ future growth options and strategic vision directed towards consolidating market power. Similarly, positive short-term abnormal returns are documented to accompany first cross-border acquisitions (Dandapani et al., Citation2020). Shareholders appear to regard these transactions as a signal of acquirers’ long-term intention to enter the international arena, penetrate new markets and compete globally, all of which is priced in as a long-term real option to expand the scale of acquirers’ operations. While signalling the availability of attractive growth opportunities, cross-border acquisitions may carry a number of integration-related risks (Uysal et al., Citation2008) as geographical and cultural proximity have been shown to be positively associated with post-acquisition outcomes in terms of shareholder value.

Despite a positive reaction to the first acquisitions, investors appear to be less responsive to subsequent transactions undertaken by the same company. Multiple studies (e.g., Billett & Qian, Citation2008; Kose et al., Citation2011) document diminishing returns accruing to acquirers’ shareholders following serial acquisitions with the magnitude of the associative link seemingly unaffected by the learning curve. The possible explanations for the relative underperformance of serial acquirers appear to mostly derive from theories of managerial hubris and overconfidence. Overconfident executives, especially those with a record of managing prior takeovers, may exhibit a higher proclivity to express unjustified optimism with regards to the outcomes of pending acquisitions (Malmendier & Tate, Citation2008).

As firms grow larger and engage in consecutive rounds of inorganic growth, managerial opportunism and agency conflicts may exacerbate prompting the deployment of corporate resources towards economically unjustified acquisitions. CEOs’ overconfidence may cause an overvaluation of prospective synergies and underestimation of integration costs, all of which may contribute to deteriorating post-transaction operational performance (Klasa & Stegemoller, Citation2007). Due to high relative frequency of acquisitions undertaken by serial acquirers on developed markets, integration problems are likelier to accumulate putting a downward pressure on medium-term bottom lines. The pool of potential targets is also gradually being exhausted causing serial bidders to engage into lower-quality deals.

Lower returns accompanying serial acquisitions may stem from managerial proclivity to extrapolate past post-acquisition returns to pending transactions during the bidding process. A positive market reaction to the first transaction may encourage executives to place higher bids while negotiating subsequent deals (Aktas et al., Citation2011). One may therefore reasonably expect lower prior acquisition returns to be associated with better outcomes for follow-up transactions, which contradicts the majority of empirical studies documenting diminishing cross-transaction returns. Ultimately, the short- and long-term acquisition outcomes may be contingent upon executives’ expertise in selecting the right targets. A successful prior acquisition experience appears to be a reliable predictor of subsequent acquisition outcomes pointing to the presence of persistent skills-based learning effect (Kengelbach et al., 2012; Qian & Zhu, Citation2017). Finally, heterogeneity of acquisition results may be explained by cross-acquirer differences in endowment with organisational capital defined as a set of business practices, human resources and analytical expertise necessary to facilitate post-transaction integration (Li et al., Citation2018). However, even after controlling for these factors, serial acquirers are reported to produce lower short- and long-term returns than one-time takeovers.

The rivalry between the learning and overconfidence hypotheses, which have divergent predictions with respect to the performance of serial acquirers, remains unresolved despite the majority of studies pointing to the validity of the latter.

One of the most important factors deciding on the outcomes of acquisitions is acquirer–acquiree industry relatedness. Conventional wisdom postulates that horizontal acquisitions should generate superior results as post-acquisition integration is facilitated by similarity in resource endowment, technological processes, managerial practices and organisational capital.

The empirical literature remains ambiguous with regards to the impact of acquirer–acquiree industry relatedness on post-deal shareholder returns. On one hand, Hoberg and Phillips (Citation2010) document a positive impact of firm complementarity on acquisition performance: similarity of product portfolios offered by participating entities is evidenced to be positively associated with post-transaction sales dynamics and overall business profitability. Complementarity of human and organisational capital defined as similarity of employees’ skillset and business profiles may also play a role by allowing for greater post-deal cost optimisation as well as positive knowledge spillover effects (Lee et al., Citation2018). While the majority of empirical studies find asset complementarity and industry relatedness to be beneficial, some report the opposite or indeterminate effect. Martynova et al. (Citation2007) document no difference in the dynamics of operational performance across vertical and horizontal acquisitions. In some cases, divergence in acquirers’ and acquirees’ business profiles may play to the benefit of the combined entity by allowing for re-deployment of resources and knowhow to the less efficient and less specialised targets (Fresard et al., Citation2017).

The present study attempts to establish the short-term shareholder effects of acquisition completion depending on the geographical, intertemporal and industry scope of transactions as well as to elucidate the intermediating role of acquirers’ prior experience on transaction outcomes. As such, it represents a comprehensive multidimensional follow-up study covering a major emerging market. The strategic goals and scope of acquisitions undertaken by Chinese companies have undergone substantial changes over the past two decades. Having been mostly focused on the provision of access to natural resources during the first wave, the takeovers are now primarily aimed at securing technological superiority through acquisition of targets’ technologies and knowhow (Zhou et al., Citation2014). Gradual consolidation on the domestic market in turn is expected to positively contribute to the efficiency of manufacturing processes by slashing duplicate expenses, increasing economies of scale and securing better access to external financing. The principal difficulties encountered by Chinese acquirers along the way originate from lack of acquisition experience, institutional barriers, regulatory pressure and targets’ defensiveness. By inquiring into the short-term wealth effects of acquisitions, we intend to verify whether positive or negative anticipated acquisition outcomes predominate in the perceptions of investors.

3. Dataset and research design

For the purposes of the present empirical study, we compiled an extensive database of acquisitions completed by Chinese public companies over the period between 1994 and 2020. The total population of transactions was filtered of all deals, which were announced, but which were not subsequently completed. Second, we limited the sample only to transactions with deal value of more than USD 1 million. Third, we eliminated all acquirers belonging to the financials and utilities industries from the sample. The deal metadata were assembled from Thomson Reuters M&A database. The data on price dynamics, which were used to calculate post-transaction stock returns, were downloaded from Thomson Reuters datastream. Firm-level financials, which are included as control variables across econometric model specifications, were compiled from Bloomberg database. The final research sample created after applying the aforementioned filters includes 3297 unique acquisitions completed by 1805 public acquirers. At the same time, due to the missing price data, control variables or closure/delisting, some of the observations were dropped at the stage of econometric analysis reducing the total sample size to 2650 unique transactions.

Each of the tested econometric models contains a set of firm-level control variables. The macroeconomic data on GDP growth in targets’ country were obtained from the World Bank.

The variables used in our empirical analysis are defined in . The descriptive statistics are presented in . Nominal variables are scaled with appropriate deflators or logarithmised to normalise their distributions. Winsorisation at 1% and 99% levels allows us to eliminate the distortionary impact of outliers on econometric results.

Table 1. Definitions of the key variables.

Table 2. Descriptive statistics.

The initial analysis of descriptive statistics reveals several features of the acquisitions undertaken by Chinese companies. Precisely, 83% of the analysed transactions resulted in a purchase of controlling interest (>50%) in the acquirees’ business. The average ownership share acquired is 60.2%. Cross-industry/vertical/conglomerate acquisitions predominate over horizontal acquisitions with the latter constituting ca. 37% of the analysed transactions. Most deals – ca. 52% – target private companies. In 5.5% of cases, target companies are join ventures.

The average age of a public Chinese company at the moment of undertaking its first acquisition is 15.56 years, which is almost three times higher than the average age at which U.S. firms undertake their first inorganic growth effort (Dandapani et al., Citation2020). Overall, Chinese companies take longer to mature and are less expansive in their acquisitions than their peers from mature markets. At the moment of undertaking a given acquisition, an average sampled acquirer has completed 0.89 prior acquisitions with the absolute majority of them involving domestically domiciled targets. It is extremely rare to see a company, which starts its acquisition record with a foreign target. Only 4.9% of sampled acquirers initiated their inorganic growth with an international acquisition.

Serial acquisitions remain relatively rare on the Chinese market as compared to mature markets. Overall, 21.8% of the analysed public companies undertook a second acquisition; 9.5% completed a third deal; ca. 4.6% have four acquisitions on record; 2.2% completed five or more transactions. On average, subsequent transactions occur with an interval of 2.22 years (standard deviation of 2.73 years).

Overall, the intensity and scale of acquisition processes on the Chinese market remain well below those exhibited by mature markets. At the same time, industry consolidation processes have been gaining strength over the past decade prompting a dynamic growth in acquisitions. International acquisitions have also been on a steady rise precipitated by Chinese firms’ plans to gain access to superior technologies and knowhow of their peers from developed markets. On the whole, 23% of acquisitions involve targets operating in high-technology sectors. Cross-border transactions undertaken by Chinese companies mostly involve targets from developed countries – U.S.A., Germany, Austria, Singapore, Japan, Italy, France and Australia. Some of the transactions are clearly motivated by acquirers’ desire to gain access to raw materials or gain better control of international supply chains. International acquisitions efforts of Chinese companies are frequently impeded by regulatory pushback and negative public coverage, which may put a long-term constraint on acquirers’ cross-border expansion. The uncertainty frequently surrounding such transactions may explain the ambiguous market reaction to the completion of such deals.

To quantify the short-term shareholder wealth effects of acquisition completion, we rely on the most commonly used event-study metric – CAR. This indicator estimates the total/additive abnormal return, which may be earned by shareholders during the observation window spanning a period commencing before the event in question and ending a certain period of time following the event.

The methodology used for estimating CAR is similar to that used by Dandapani et al. (Citation2020).

(1)

(1)

where

is the abnormal return of the ith stock on date j;

is the simple raw return of the ith stock on date j;

is the expected return of the ith stock on date j estimated from market model derived by regressing returns of the ith stock on benchmark index returns over a period of 250 trading days prior to transaction completion date. We use two different benchmark indices to estimate market models for each stock: Shanghai Composite and Shenzhen Composite Indices depending on the primary location of listing of the company. One of the important shortcomings of many empirical studies is the reliance on a unique benchmark index serving as a proxy for performance of the entire stock market in a given jurisdiction. By choosing the appropriate benchmark index for each sampled firm, we alleviate this concern. CARs are then estimated for each acquirer within the event window starting one day prior to transaction completion date and ending t days after transaction completion date:

(2)

(2)

We use several observation windows ranging from [–1;+1] to [–1;+30] days around acquisition completion date. This approach allows us to cross-check our empirical findings and to avoid the common criticism of cherry-picking short-term event windows. The descriptive statistics for CARs are presented in .

Having estimated CARs for the analysed transactions, we run a set of multivariate cross-section regressions attempting to establish deal characteristics that may be associated with non-zero CARs. The regressands are CARs estimated on different observation windows. The baseline econometric models include the following regressors: (1) acquirer’s size, (2) acquirer’s operating profit margin, (3) acquirer’s intangible assets, (4) acquirer’s cash reserves, (5) acquirer’s tangible investments, (6) acquirer’s level of debt, (7) deal size, (8) ownership stake purchased, (9) deal attitude, (10) binary variable encoding deals involving acquirers and targets from high-tech industries, (11) binary variable encoding government-owned targets, (12) binary variable encoding privately owned targets, (13) binary variable encoding joint ventures, (14) binary variable encoding deals aimed at overtaking acquiree’s technologies and knowhow, (15) acquirer’s age, (16) binary variable encoding deals involving a transfer of the controlling equity stake (>50%) and (17) GDP growth.

In addition, the tested econometric models include a set of experimental variables encoding acquirers’ prior experience, acquirer–acquiree industry relatedness and geographical scope (Dicu et al., Citation2019) of transactions. These variables are the focus of the present study. All econometric models include industry and year fixed effects to control for sample heterogeneity as well as time-invariant explanatory factors. All reported models are documented to have satisfactory econometric properties, which allow for appropriate statistical inference.

In addition to multivariate regression analysis, we run a set of univariate tests (t-test for the difference of mean returns and Wilcoxon rank-sum (Mann–Whitney) test for the difference in distributions) to verify whether statistically significant differences in CARs are observed between the first and subsequent acquisitions.

4. Empirical findings

The results for baseline regression models are reported in . We document no difference between CAR recorded at acquirers’ first acquisition (regardless of whether it is domestic or cross-border) and the remainder of sampled transactions. Negative associative link is found between acquirers’ age at transaction completion and CARs across all observation windows. Somewhat lower returns are reported for transactions involving government-owned targets (the respective coefficients for one- and seven-day CARs are significant at 10% level). Among the control variables, only acquirers’ contemporaneous operating profit margin is found to exhibit positive associative link with transaction-related CARs. The types of targets (private vs public), deal attitude, deal size and ownership share being acquired are documented to exhibit no relationship with acquirers’ CARs. Transactions involving targets from high-technology industries, which have been conventionally perceived as more attractive in terms of potential synergies and knowledge spillovers, do not generate superior CARs. Overall, we demonstrate that markets do not put a statistically significant premium in the form of positive CAR on the acquirers’ initial acquisition experience.

Table 3. Baseline regression models: market reaction to firms’ first acquisitions (regardless of whether the first acquisition is foreign or domestic).

We further investigate whether market reactions measured by CARs are heterogenous depending on the geographical scope of acquisitions. In , we summarise the relevant econometric findings. Neither the first domestic, nor the first foreign acquisitions of Chinese public companies are evidenced to elicit CARs different from the sample means. The respective regression coefficients remain persistently insignificant across all event windows. Serial acquisitions (transactions completed by firms having more than two prior acquisitions on record) are also found to generate CARs insignificantly different from those of the entire sample under analysis. These findings are corroborated with univariate statistical tests comparing CARs surrounding the first and subsequent acquisitions undertaken by the studied companies. The respective results are reported in . We run two-sample t-tests and two-sample Wilcoxon rank-sum (Mann–Whitney) tests comparing subsample CARs. We find no statistically significant difference in mean or median CARs for the subsample of first acquisitions as compared to subsequent deals completed by a given acquirer. Statistically significant difference is documented in seven-day CARs with first acquisitions generating somewhat lower CARs than subsequent ones; however, this result is not persistent across the remaining event windows. The distributions of CARs for first and subsequent acquisitions (presented in ) are found to have similar characteristics with means being non-different from zero, which points to a lack of market premia attributable to inorganic growth.

Figure 1. Frequency distributions of cumulative abnormal returns contingent on whether acquisition is the first on record for a given company.

The charts represent frequency distributions of CAR td estimated on the even window of [–1;t] days where t varies from 1 to 30 days. Univariate t-test and Wilcoxon rank-sum (Mann–Whitney) test results for respective CARs are reported in .

Source: own elaboration.

![Figure 1. Frequency distributions of cumulative abnormal returns contingent on whether acquisition is the first on record for a given company.The charts represent frequency distributions of CAR td estimated on the even window of [–1;t] days where t varies from 1 to 30 days. Univariate t-test and Wilcoxon rank-sum (Mann–Whitney) test results for respective CARs are reported in Table 5.Source: own elaboration.](/cms/asset/aa76a0df-345e-4301-a1b7-3eceaa788eba/rero_a_1997621_f0001_c.jpg)

Table 4. Market reaction upon completion of the firms’ first and subsequent foreign/domestic acquisitions.

Table 5. Univariate tests for the difference in distributions of CARs [–1;t] for subsamples of first and subsequent acquisitions for a given acquirer.

The analysis of the impact of acquirers’ prior experience on transaction-driven CARs is summarised in . The number of transactions completed by a given acquirer prior to the analysed deal is shown to have a weak negative associative link with short-term one-day and three-day CARs: an additional prior transaction is associated with a reduction of short-term CARs by ca. 0.3%. Whether the acquirers’ prior experience is cross-border or domestic is found to have no repercussions for short-term shareholder response to deal completion. Overall, we demonstrate that acquirers’ prior acquisition experience plays no role in intermediating the market’s response to acquisition completion. The learning hypothesis stating that acquirers may get better at selecting acquisition targets as they gain more experience finds no support in our empirical findings.

Table 6. Market reaction following deal completion contingent upon acquirers’ prior acquisition experience.

Despite a discovered weak negative link between the number of acquirers’ prior completed transactions and transaction-related CARs, we find no statistically significant differences between mean CARs accompanying first, second, third, fourth and fifth consecutive transactions for any given serial acquirer. The results of two-sample t-tests are reported in : pairwise mean CARs are found to be equal across all transaction subsamples. The graphical representation of subsample means and medians is shown in . We fail to identify any diminishing returns accruing to acquirers’ shareholders along with subsequent acquisitions. Whenever corroborating the presence of such effect, prior empirical studies attributed it to the gradual exhaustion of acquisition opportunities available to serial acquirers causing them to buy less attractive targets. Our findings suggest that investors remain indifferent with regards to both initial acquisitions as well as subsequent transactions without discriminating between them in terms of short-term returns.

Figure 2. Mean (subplot A) and median (subplot B) CARs for the first/second/third/fourth/fifth acquisitions for a given acquirer.

The charts represent mean (subplot A) and median (subplot B) CARs td estimated on the even window of [–1;t] days where t varies from 1 to 30 days. Univariate tests for differences in mean and median CARs are reported in .

Source: own elaboration.

![Figure 2. Mean (subplot A) and median (subplot B) CARs for the first/second/third/fourth/fifth acquisitions for a given acquirer.The charts represent mean (subplot A) and median (subplot B) CARs td estimated on the even window of [–1;t] days where t varies from 1 to 30 days. Univariate tests for differences in mean and median CARs are reported in Table 7.Source: own elaboration.](/cms/asset/646ee265-e459-40d1-b4b5-d7359d1d78c3/rero_a_1997621_f0002_c.jpg)

Table 7. Univariate tests for the difference in mean CARs [–1;t] for subsamples of fist/second/third/fourth/fifth acquisitions for a given acquirer.

Our econometric analysis reveals lack of difference in CARs generated around both the first domestic and the first cross-border acquisitions. Whether acquirers initiate their inorganic expansion with a domestic or an internationally domiciled target, the CARs around the transaction remain non-different from the mean for the entire analysed sample. The relevant econometric results are reported in . Univariate tests relying on kernel density estimation plots () confirm these findings. CAR distributions for first domestic and first cross-border acquisitions are similar with mean CARs being non-different from zero. Investors appear to assign no abnormal value to the events related to acquirers’ expansion both on the international and domestic markets. These results are at odds with some novel empirical findings for mature markets (e.g., Dandapani et al., Citation2020), which document a premium investors attach to acquirers’ efforts to enter global markets through cross-border acquisitions.

Figure 3. Kernel density estimation plots of cumulative abnormal acquirer returns following the first foreign and first domestic acquisition.

The charts represent kernel density estimate plots of CAR td bootstrapped on the even window of [–1;t] days where t varies from 1 to 30 days.

Source: own elaboration.

![Figure 3. Kernel density estimation plots of cumulative abnormal acquirer returns following the first foreign and first domestic acquisition.The charts represent kernel density estimate plots of CAR td bootstrapped on the even window of [–1;t] days where t varies from 1 to 30 days.Source: own elaboration.](/cms/asset/6b4beae0-3266-4770-b6ea-bb5c2351108b/rero_a_1997621_f0003_c.jpg)

Table 8. Market reaction following firms’ first foreign/domestic acquisitions.

The pace at which acquirers undertake subsequent acquisitions is found to play no role in shaping short-term shareholder returns (). The time elapsed neither since the first transaction nor since prior acquisitions (in case of serial acquirers) is found to be associated with superior/inferior CARs. Even though serial acquirers undertake subsequent transactions in relatively short intervals (2.22 years on average with substantial intra-sample heterogeneity), faster expansion seems to have no impact on investors’ short-term response.

Acquirer–acquiree industry relatedness has been reported to have an impact on short-term acquirers’ shareholder returns (Megginson et al., Citation2004). Resource complementarity, lower information asymmetry and the perceived relative ease of post-acquisition integration could all improve the transactions’ perception by investors. We test whether acquisitions involving acquirers and targets from the same industry – labelled horizontal – perform better in terms of short-term CARs than vertical/conglomerate acquisitions spanning different industries. The results of our quantitative analysis are reported in . To start with, we find that horizontal acquisitions generate significantly lower in 7-day and 30-day CARs. However, no differences in one-day and three-day CARs have been found. The geographical span of the transaction (whether target is domestic or foreign; see for a detailed geographical distribution of targets) is evidenced to exercise no impact on short-term CARs. Lower 30-day CARs are documented to accompany initial foreign horizontal acquisitions, but we refrain from generalising this result.

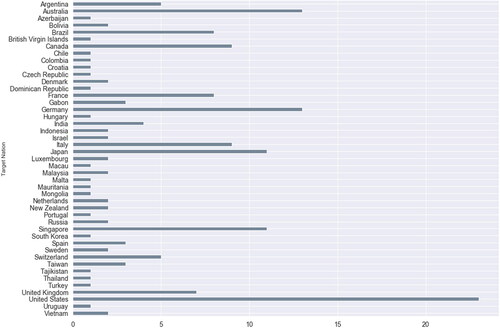

Figure 4. Geographical distribution of cross-border acquisitions completed by listed Chinese acquirers during 1996–2020.

Source: own elaboration.

Table 9. Market reaction to horizontal and conglomerate acquisitions depending on acquirers’ prior acquisition experience.

The negative link between the number of prior acquisitions and short-term returns is found to be somewhat more pronounced in case of horizontal acquisitions (see for graphical depiction of marginal effects of consecutive acquisitions on CARs). While this finding may speak in favour of hypothesis postulating diminishing returns from acquisitions stemming from gradual reduction of the number of attractive acquisition targets, we perceive our evidence as inconclusive on this matter.

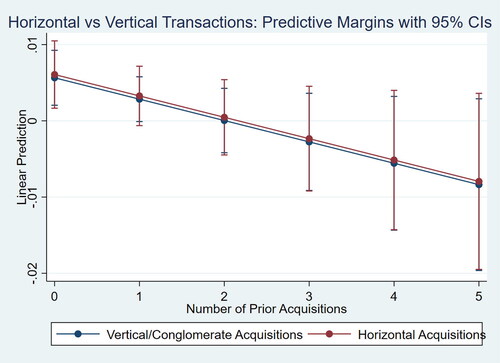

Figure 5. Marginal effect of acquirers’ prior acquisition experience on post-acquisition (CAR 3d) cumulative abnormal returns with 95% confidence interval.

The chart represents marginal effect of acquirers’ prior acquisition experience (measured as a number of acquisition completed prior to the analysed transaction by the same acquirer). Marginal effects are derived from partial cross-sectional regression coefficients reported in .

Source: own elaboration.

Panel B in corroborates our prior findings regarding the lack of intermediating role of acquirers’ prior acquisition experience in shaping short-term shareholder returns. Types of targets, industry relatedness, ownership structure and deal size are found to remain insignificant in explaining transaction-related CARs.

5. Conclusions

Similar to the majority of prior empirical studies, the present inquiry suggests that acquisitions fail to deliver persistent statistically significant positive CARs. Despite a wide heterogeneity of investors’ reactions to deal completion across the studied sample of public Chinese acquirers, the overall performance of completed deals during the period of 1994–2020 in terms of short-term CARs is non-different from zero. Neither the geographical scope of acquisitions, i.e., whether the target is domiciled in China or overseas, nor the acquirer–acquiree industry relatedness, nor acquirers’ prior experience have been shown to alter this pattern.

Unlike on mature markets (Dandapani et al., Citation2020), investors on the Chinese market appear to attach no premium to the public companies’ inorganic expansion strategies with neither initial nor follow-up deals resulting in superior shareholder returns.

We find no short-term underperformance of same-industry acquisitions in terms of CARs compared to vertical and conglomerate acquisitions. Industry relatedness is found to play no role in intermediating the relationships between acquirers’ experience, geographical diversification and short-term returns.

We document indistinguishable short-term CARs surrounding both the first and subsequent acquisitions undertaken by serial acquirers. In contrast, serial acquirers overall (public companies undertaking three or more acquisitions regardless of the frequency of deal completion) are found to earn relatively lower CARs especially in case of horizontal acquisitions.

Acquirers’ experience with prior acquisitions is found to have no explanatory power in the study of short-term CARs. Shareholder returns are documented to vary independently from the frequency of completed transactions, length of intervals between transactions, the industry and geographical scope of serial transactions.

While our results agree with prior empirical studies by showing a lack of persistent short-term abnormal returns attributable to the completion of acquisitions (Ma & Pagan, Citation2009), the question of why investors’ reaction remains indifferent with regards to firms’ inorganic expansion is left to be answered. Several possible explanations emerge. One posits that information leakage, which was found to permeate emerging stock markets, may cause investors to discount deal-related information in asset prices before transaction finalisation. The second possibility is that investors approach acquisitions as a long-term endeavor with uncertain outcomes therefore attacking no short-term premium to deal finalisation. Finally, a lack of significant positive CARs could simply be an idiosyncratic feature of the Chinese public capital market. With certain controls in place limiting the inflow of capital, the Chinese market has nevertheless behaved in a rollercoaster manner over the past two decades experiencing both subperiods of remarkable growth and rapid declines. Intermittent roaring growth of asset prices has frequently been followed by drastic corrections, which may be partially responsible for the short-term shareholder effects described in the present study.

Follow-up studies should focus on the reasons standing behind the observable lack of significant market reaction to the M&A deals completed by Chinese companies. The possible explanations meriting in-depth empirical investigation include capital market frictions, information asymmetry between firms’ executives and shareholders, insufficient market liquidity and excessive volatility on public capital markets. Investors’ reactions may also be contingent upon the declared goals of M&A deals; therefore, further studies may elucidate the nexus between the expected transaction outcomes and stock price response.

Disclosure statement

No potential conflict of interest was reported by the authors.

References

- Aktas, N., De Bodt, E., Bollaert, H., & Roll, R. (2016). CEO narcissism and the takeover process: From private initiation to deal completion. Journal of Financial and Quantitative Analysis, 51(1), 113–137. https://doi.org/10.1017/S0022109016000065

- Aktas, N., De Bodt, E., & Roll, R. (2011). Serial acquirer bidding: An empirical test of the learning hypothesis. Journal of Corporate Finance, 17(1), 18–32. https://doi.org/10.1016/j.jcorpfin.2010.07.002

- Alexandridis, G., Antypas, N., & Travlos, N. (2017). Value creation from M&As: New evidence. Journal of Corporate Finance, 45, 632–650. https://doi.org/10.1016/j.jcorpfin.2017.05.010

- Antoniou, A., Petmezas, D., & Zhao, H. (2007). Bidder gains and losses of firms involved in many acquisitions. Journal of Business Finance & Accounting, 34(7–8), 1221–1244. https://doi.org/10.1111/j.1468-5957.2007.02012.x

- Baruch, S., Panayides, M., & Venkataraman, K. (2017). Informed trading and price discovery before corporate events. Journal of Financial Economics, 125(3), 561–588. https://doi.org/10.1016/j.jfineco.2017.05.008

- Bessembinder, H., Cooper, M., & Zhang, F. (2019). Characteristic-based benchmark returns and corporate events. The Review of Financial Studies, 32(1), 75–125. https://doi.org/10.1093/rfs/hhy037

- Billett, M., & Qian, Y. (2008). Are overconfident CEOs born or made? Evidence of self-attribution bias from frequent acquirers. Management Science, 54(6), 1037–1051. https://doi.org/10.1287/mnsc.1070.0830

- Borodin, A., Sayabek, Z. S., Islyam, G., & Panaedova, G. (2020). Impact of mergers and acquisitions on companies’ financial performance. Journal of International Studies, 13(2), 34–47. https://doi.org/10.14254/2071-8330.2020/13-2/3

- Buckley, P., Elia, S., & Kafouros, M. (2014). Acquisitions by emerging market multinationals: Implications for firm performance. Journal of World Business, 49(4), 611–632. https://doi.org/10.1016/j.jwb.2013.12.013

- Cai, Y., & Sevilir, M. (2012). Board connections and M&A transactions. Journal of Financial Economics, 103(2), 327–349. https://doi.org/10.1016/j.jfineco.2011.05.017

- Dandapani, K., Hibbert, A., & Lawrence, E. (2020). The shareholder’s response to a firm’s first international acquisition. Journal of Banking & Finance, 118, 105852. https://doi.org/10.1016/j.jbankfin.2020.105852

- Dicu, R., Toma, C., Aevoae, G., & Mardiros, G. (2019). The influence of deal value’s determinants in mergers and acquisitions with community dimension: Some empirical evidence from the European Union. Transformations in Business Economics, 18, 510–529.

- Duppati, G., Abidin, S., & Hu, J. (2015). Do mergers and acquisitions in China create value to acquiring firms? Corporate Ownership and Control, 12(4), 117–140. https://doi.org/10.22495/cocv12i4p9

- Fresard, L., Hege, U., & Phillips, G. (2017). Extending industry specialization through cross-border acquisitions. The Review of Financial Studies, 30(5), 1539–1582. https://doi.org/10.1093/rfs/hhx008

- Golubov, A., Yawson, A., & Zhang, H. (2015). Extraordinary acquirers. Journal of Financial Economics, 116(2), 314–330. https://doi.org/10.1016/j.jfineco.2015.02.005

- Haleblian, J., Devers, C., McNamara, G., Carpenter, M., & Davison, R. (2009). Taking stock of what we know about mergers and acquisitions: A review and research agenda. Journal of Management, 35(3), 469–502. https://doi.org/10.1177/0149206308330554

- Hoberg, G., & Phillips, G. (2010). Product market synergies and competition in mergers and acquisitions: A text-based analysis. Review of Financial Studies, 23(10), 3773–3811. https://doi.org/10.1093/rfs/hhq053

- Ishii, J., & Xuan, Y. (2014). Acquirer-target social ties and merger outcomes. Journal of Financial Economics, 112(3), 344–363. https://doi.org/10.1016/j.jfineco.2014.02.007

- Kengelbach, J., Klemmer, D., & Schwetzler, B. (2012). An anatomy of serial acquirers, M&A learning, and the role of post-merger integration. SSRN Working Paper. Retrieved from http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1946261

- Klasa, S., & Stegemoller, M. (2007). Takeover activity as a response to time-varying changes in investment opportunity sets: Evidence from takeover sequences. Financial Management, 36(2), 1–25. https://doi.org/10.1111/j.1755-053X.2007.tb00085.x

- Kolasinski, A., & Li, X. (2013). Can strong boards and trading their own firm’s stock help CEOs make better decisions? Evidence from acquisitions by overconfident CEOs. Journal of Financial and Quantitative Analysis, 48(4), 1173–1206. https://doi.org/10.1017/S0022109013000392

- Kose, J., Liu, Y., & Taffler, R. (2011, 22 June). It takes two to tango: Overpayment and value destruction in M&A deals [Paper presentation]. 20th European Financial Management Association (EFMA), Braga, Portugal.

- Langenstein, T., Vojtková, A., Užík, M., & Ruepp, A. (2018). Cross-border acquisitions in Central and Eastern Europe with focus on Russia versus Germany deals: An empirical analysis. E + M Ekonomie a Management, 21(4), 207–225. https://doi.org/10.15240/tul/001/2018-4-014

- Lee, K., Mauer, D., & Xu, E. (2018). Human capital relatedness and mergers and acquisitions. Journal of Financial Economics, 129(1), 111–135. https://doi.org/10.1016/j.jfineco.2018.03.008

- Li, L., Qiu, R., & Shen, R. (2018). Organizational capital and mergers and acquisitions. Journal of Financial and Quantitative Analysis, 53(4), 1871–1909. https://doi.org/10.1017/S0022109018000145

- Ma, J., & Pagan, J. (2009). Abnormal returns to mergers and acquisitions in ten Asian stock markets. International Journal of Business, 14(3), 235–250.

- Maksimovic, V., Phillips, G., & Prabhala, N. (2011). Post-merger restructuring and the boundaries of the firm. Journal of Financial Economics, 102(2), 317–343. https://doi.org/10.1016/j.jfineco.2011.05.013

- Malmendier, U., Moretti, E., & Peters, F. (2018). Winning by losing: Evidence on the long-run effects of mergers. The Review of Financial Studies, 31(8), 3212–3264. https://doi.org/10.1093/rfs/hhy009

- Malmendier, U., & Tate, G. (2008). Who makes acquisitions? CEO overconfidence and the market’s reaction. Journal of Financial Economics, 88(1), 20–43.

- Martynova, M., Oosting, S., & Renneboog, L. (2007). The long-term operating performance of European mergers and acquisitions. In G. Gregoriou & L. Renneboog (Eds.), International mergers and acquisitions activity since 1990: Recent research and quantitative analysis (pp. 79–116). Elsevier.

- Megginson, W., Morgan, A., & Nail, L. (2004). The determinants of positive long-term performance in strategic mergers Corporate focus cash. Journal of Banking & Finance, 28(3), 523–552. https://doi.org/10.1016/S0378-4266(02)00412-0

- Netter, J., Stegemoller, M., & Wintoki, M. (2011). Implications of data screens on merger and acquisition analysis: A large sample study of mergers and acquisitions from 1992 to 2009. Review of Financial Studies, 24(7), 2316–2357. https://doi.org/10.1093/rfs/hhr010

- Offenberg, D., Straska, M., & Waller, H. (2014). Who gains from buying bad bidders? Journal of Financial and Quantitative Analysis, 49(2), 513–540. https://doi.org/10.1017/S0022109014000167

- Qian, J., & Zhu, J. (2017). Return to invested capital and the performance of mergers and acquisitions. Management Science, 64(10), 4471–4695.

- Rau, P., & Vermaelen, T. (1998). Glamour, value and the post-acquisition performance of acquiring firms. Journal of Financial Economics, 49, 223–253.

- Renneboog, L., & Vansteenkiste, C. (2019). Failure and success in mergers and acquisitions. Journal of Corporate Finance, 58(C), 650–699. https://doi.org/10.1016/j.jcorpfin.2019.07.010

- Uysal, V., Kedia, S., & Panchapagesan, V. (2008). Geography and acquirer returns. Journal of Financial Intermediation, 17(2), 256–275. https://doi.org/10.1016/j.jfi.2007.12.001

- Zhang, J., & Haico, E. (2010). Why half of China’s oversea acquisitions could not be completed. Journal of Current Chinese Affairs, 39(2), 101–131. https://doi.org/10.1177/186810261003900204

- Zhou, C., Witteloostuijn, A., & Zhang, J. (2014). The internationalization of Chinese industries: Overseas acquisition activity in Chinese mining and manufacturing industries. Asian Business & Management, 13(2), 89–116. https://doi.org/10.1057/abm.2014.1

- Zhu, H., & Zhu, Q. (2016). Mergers and acquisitions by Chinese firms: A review and comparison with other mergers and acquisitions research in the leading journals. Asia Pacific Journal of Management, 33(4), 1107–1149. https://doi.org/10.1007/s10490-016-9465-0