?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

One of the strategic objectives of China is to increase renewable energy consumption by reducing non-renewable energy consumption. This motivates us to carefully investigate the asymmetric effects of financial deepening on renewable and non-renewable energy consumption for China, using annual data from 1990 to 2019. The results show that in China, a positive shock in bank deposits and broad money has a significant increasing effect on renewable energy consumption, while a negative shock in bank deposits and broad money has also a significant increasing effect on renewable energy consumption in the long-run. Moreover, positive change in bank deposits and broad money has an inverse impact on non-renewable energy consumption, while negative change has stimulating non-renewable energy consumption in long run. Thus, government and policymaker's policies aimed at promoting financial deepening in China must be persistent and sustainable to foster renewable energy consumption.

1. Introduction

Two major concerns for the international community, over the last few decades, are rising energy consumption and environmental degradation. According to International Energy Agency (IEA) carbon emissions have increased manifold due to an enormous increase in the consumption of fossil fuels (IEA, Citation2017). On one side, the massive growth in economic activities has consumed a large chunk of non-renewable energy sources (e.g., coal, oil, and gas), whereas, on the other side, it has seriously damaged the ecosystem. Hence, energy security and environmental sustainability have become two major challenges for the world’s leaders and have become the hottest topic on all international forums (Ullah et al., Citation2020; Usman et al., Citation2021a). The role of emerging economies in achieving both these targets has become crucial due to their massive reliance on non-renewable energy sources for their economic growth (Qin & Ozturk, Citation2021).

Along with the rapid growth and huge energy demand, the environmental challenges are facing by China to replace the non-renewable energy consumption with alternative renewable energy consumption sources. As these alternative renewable energy consumption sources would meet the growing energy demand as well as increase environmental quality. To achieve the sustainable development goals (SDGs) 13, one of the basic targets is to provide clean and affordable energy sources by encouraging the share of renewable energy consumption in the energy mix, which enhanced green job, facilitate green GDP, and improved the quality of life (Azam et al., Citation2021a). The common features of renewable energy consumption sources such as solar, hydropower, wind, tides, biomass, biofuels, and geothermal are considered natural, clean, and environmentally friendly.

China has emerged from a poor nation, in the 1970s, to the world’s second-largest economy in the 21st century. China’s economic growth is largely based on the consumption of non-renewable energy sources and its energy consumption has increased from 397.1 million tons to 3.1 billion tons oil equivalent during the period 1978 to 2017. In terms of average, this increase is equal to 5.4% per annum, whereas, the world’s average during this period hovered around 2.8% per annum (BP Statistical Review of World Energy, Citation2018). For almost 17 years China’s average energy consumption remained higher than the world’s average, which is strong enough evidence to prove China’s impressive growth alongside its unwelcoming role in environmental degradation. Precisely, China has become the world’s largest energy consumer as well as the highest emitters of greenhouse gas emissions (Zhao et al., Citation2021).

Presently, China’s energy resource bequest is comprised of coal (58%), oil (20%), gas (8%), hydro (8%), nuclear (2%), and renewable resources (5%) (Center, 2020). China started to open up its economy in 1978, from that time onwards China has achieved a massive growth rate and its average growth rate, during 1978–2017, remained at 9.6% per annum (WDI, Citation2018). However, its consumption of non-renewable energy during the same period has increased enormously. Among the sources of non-renewable energy, coal is considered the main contributor to the economic growth of China (Sadorsky, Citation2009) and the main reason behind the energy price unpredictability, carbon productions, and environmental degradation (Azam et al., Citation2021b; Destek & Aslan, Citation2017; Koçak & Şarkgüneşi, Citation2017). It is important to consider that the Chinese economy is still growing at an enormous pace with substantial potential to develop more, hence, the demand for per capita energy consumption will further increase. In the perspective of this development, policy-makers in China must see the alternative sources of energy that can, in the future, fulfill the growing need of China’s energy demand.

Without a doubt, energy, whether renewable or non-renewable, is served as a crucial input in the production function of the firm and vital for the overall growth of a country. However, due to the environmental cost attached to the use of energy, maintaining a balance between renewable and non-renewable energies is very crucial from the standpoint of sustainable development. Therefore, finding the determinants of renewable and non-renewable energy sources have always remained an important theme for energy-economist. A large number of studies are available that have shed light on the relationship between energy and economic growth (Azam et al., Citation2021c; Citation2021d; Khan et al., Citation2020; Ozturk & Salah Uddin, Citation2012; Skare et al., Citation2020; Wandji, Citation2013), but very few have included financial deepening as a determinant of energy.

Financial deepening simply means the volume of the financial sector in the economy. In other words, the total number of banks, other financial organizations, and financial marketplaces in the economy. In empirical literature financial deepening is calculated as a ratio of private credit to GDP (World Bank). Financial deepening can increase energy consumption through business, income, and customer effects (Ozturk, Citation2010; Sadorsky, Citation2010), whereas, it can conserve energy by investing more in sophisticated production methods. To attain energy safety without conceding the environment, it is essential to build a financial sector that implants resources towards ecological sustainability. Financial depth can affect environmental quality through many channels. It promotes economic growth, which leads to a rise in the development and consumption of clean energy sources (Assi et al., Citation2020; Azam et al., Citation2021e). Moreover, financial development induces the producers to invest heavily in the new, more energy-efficient technologies resulting in increased output alongside less reliance on fossil fuels. It can be suggested that depressing borrowing expenses, promoting savings, increasing confidence between debtors and investors, lending more to the projects of renewable energy, and financing R&D programs in the energy sector will inspire organizations and people to create innovations and register patents to discover novel sources of clean energy (Assi et al., Citation2020; Usman et al., Citation2021b). In this situation, it is imperative to scrutinize how positive and negative shocks regarding financial depth can influence energy demand in China.

Due to China’s massive economic growth, rise in its energy demand, and its role in polluting the environment China has become an ideal country to see from the perspective of energy security and environmental sustainability. This study fills the gap by incorporating financial deepening as the main variable in the energy demand function of China. The novelty of this study is further strengthened by including the asymmetry assumptions in the model, which allow us to split our main variable i.e., financial deepening into its positive and negative parts. As a result, we will get separate estimates for positive and negative shocks, on the basis of which we can make a decision about the presence of asymmetric effects in our time series. If both the negative and positive shocks significantly differ in terms of sign and magnitude this confirms the presence of asymmetry. For empirical estimation, we have taken recourse to linear and non-linear ARDL techniques. Besides, time series analysis is better than panel data because it does not suffer from the issue of aggregate bias.

The structure of the study is as follows. A literature review on the energy-finance nexus is presented in the next section. The second section is booked for the data estimation technique. In section third, results are discussed in detail and the conclusion based on our results is provided n section four.

Literature review

The past studies summarized three influential channels through which financial development enhance consumption of energy (Sadorsky, Citation2011). First, the direct impact of financial development indicates that it enable consumers to borrow money easily for the purchase of automobiles, air conditioners, air tickets, and so on, consequently result in increasing consumption of energy. Secondly, financial development directly influence business sector as in a well-operative financial structure, enterprises get easy access to finance such as equity and debt financing, that enables enterprise to invest in their current and capital assets for enhancing their business. This increases demand of energy for production. Third influence is the wealth effect which shows that any upsurge in stock market accomplishments could increase business and consumer confidence, increase non-renewable energy consumption, and enhance economic activities. However, the influence of financial development on non-renewable consumption of energy is not positive always. The technical influence specifies that financial development appeal FDI and enable firms to find finance easily for investment in efficient and advanced technologies, and consequently reduce non-renewable consumption of energy (Shahbaz et al., Citation2017). From these three theoretical influences, it is confirmed that financial development has fundamental effect on non-renewable energy consumption but the direction of impact is not clear.

In a bulk of studies literature have examined the association between financial development and non-renewable energy consumption. Few studies reported positive impact of financial development on non-renewable energy consumption (Charfeddine & Kahia, Citation2019; Kahouli, Citation2017; Sadorsky, Citation2011), whereas other studies show that financial development has negative influence on non-renewable energy consumption (Ouyang & Li, Citation2018). But these studies ignored the impact of country instability on financial development and non-renewable energy consumption. More explicitly, there might be asymmetric impact of financial development on non-renewable energy consumption due to diversification in instabilities among countries, which is less explored by existing literature. Furthermore, environmental, political, financial, and economic uncertainties influence the purchasing powers of consumers, producers, and firms that effect the individuals’ decisions regarding non-renewable energy consumption and energy demand. It specifies that financial development and volatility of energy prices result in changing non-renewable energy consumption (Jarrett et al., Citation2019). Under well-operative financial system, output of firms increase deliberately, which increase economic development of economies by mean of enhancing the investment and capital efficiency and by reducing credit constraints that ultimately result in increasing non-renewable energy consumption (Boutabba, Citation2014). However, the well-functioning financial system could also reduce non-renewable energy consumption. Through financial support the economies with stable political, financial, and economic environments could inspire firms to invest in technological production and could appeal FDI to bring modern technological innovations (Chishti et al., Citation2020). Consequently, non-renewable energy consumption reduces and energy efficiency improves. Accordingly, the financial development have asymmetric influence on non-renewable energy consumption under diversified country risk environment.

A lot of previous studies have focused on the association between conventional energy consumption and financial development. Government investments are not sufficient to fulfill the requirements of renewable energy, hence financial sector encourages the conversion of energy sector. A well-functioning financial system indorses large scale finance for the industries related to renewable energy at minor costs, which subsequently result in increasing investment and boosts the energy demand (Usman et al., Citation2021a). The strong financial structure support firms to alleviate the liquidity risk and increased the credit mandatory for mounting efficiency-based energy technologies. Furthermore, financial development smooths the funds redistribution from out-dated low energy production to development of renewable energy. The effect of long-run investment on consumption of renewable energy and positive projections for viable development justify the association between financial development and renewable energy consumption (Azam et al., Citation2021d).

Irrespective of the divergent opinions on economic and financial impact, the level of financial sector expansion can be a substantial aspect in consumption of renewable energy. Renewable energy production is no doubt very expensive. These projects involve higher starting costs, regular investments in R&D, and long-run repayments of debt (Ullah et al., Citation2021). A well-organized financial structure may channels financial support to renewable energy production and consumption industries in an effective manner. Conversely, the less organized financial system may stop new renewable energy projects to emerge even though there is demand for those projects. Unfortunately, the available literature on the nexus of renewable energy and financial sector development is very limited. The pioneer study on this issue is done by Brunnschweiler (Citation2010) which confirmed the positive impact of financial sector development on renewable energy production for panel of non-OECD economies. For China, Lin et al. (Citation2016) explored the most effective determinants of renewable electricity consumption and concluded that consumption of renewable electricity is positively linked with financial consumption. Shahbaz et al. (Citation2021) examined the causal association between financial developments, trade, real GDP, and renewable energy consumption and reported unidirectional causality transmitting from renewable energy consumption to financial development. For a panel of 12 Commonwealth states, Rasoulinezhad and Saboori (Citation2018) investigated the causal association between economic growth and energy consumption (renewable and non-renewable) by incorporating the roles of financial development and trade intensity. The study reports that unidirectional causality runs from financial development to renewable energy. For 19 Asian economies, Ali et al. (Citation2018) examined the linkage between total reserves, renewable energy, trade sanitation, tourism, and financial development. The study reports that renewable energy and financial development have bidirectional association for high, middle, and low income Asian economies.

2. Model, methods, and data

Following the literature (Qin & Ozturk, Citation2021; Sadorsky, Citation2010), we have constructed two energy demand functions one for non-renewable or traditional energy and the other for renewable and clean energy that could help us in detecting the determinants of both forms of energies. According to economic theory (Sadorsky, Citation2010), the level of financial development can influence renewable energy consumption through direct effect, wealth effect, and business effect. The models are as follows:

(1)

(1)

(2)

(2)

Where NRE, represents non-renewable energy and RE, represents renewable energy. The dependent variables in both the models are the same viz. financial deepening (FD), remittances (REM), income (GDP), and trade openness (Trade). EquationEquations (1)(1)

(1) and Equation(2)

(2)

(2) are the long-run models and only provide long-run estimates. To get the short-run estimates as well, we need to convert these equations into the form of error-correction specification as suggested by Pesaran et al. (Citation2001).

(3)

(3)

(4)

(4)

EquationEquations (3)(3)

(3) and Equation(4)

(4)

(4) are known as the ARDL model, which offer both the short-run and long-run estimates, where short-run results are signified by the estimates of first-differenced variables and the long-run results are represented by the estimates of

normalized

To confirm that our results are not absurd we turn our attention to two tests of co-integration F-test or t-test. Once co-integration is established with any of the tests we can say that our long-run variables are converging. The ARDL technique is a better option while performing the time series analysis because we don’t need to worry about the integrating properties of the variables and a combination of I(0) and I(1) variables can be included in the model. Hence, checking the stationarity of the variables through unit root testing is not a mandatory condition. Furthermore, this model proves efficient even if the sample size is small.

To convert linear analysis into nonlinear one, which is our main purpose, we will use the partial sum technique and split the FD variable into two variables i.e., positive and negative. The mathematical equation of the partial sum procedure is as follows:

The positive shocks in the series are symbolized by and the series of negative shocks are symbolized by

In the next step, these positive and negative shocks are to be replaced in the place of original variables in EquationEqs. (3)

(3)

(3) and Equation(4)

(4)

(4) and the consequential equation will look like as shown below:

(7)

(7)

(8)

(8)

Now EquationEqs. (7)(7)

(7) and (8) have become NARDL models proposed by Shin et al. (Citation2014). This is not a new model rather an extension of the linear ARDL model, hence, the technique of estimation remains the same, as well as the same critical values of the F-test, are applicable for both models. Furthermore, the diagnostic tests for both models are the same, apart from some asymmetric tests which are to be performed in the non-linear model. Among them, first in the line is adjustment asymmetry which is established if the lag-length (k) attached to

and

is unalike. Next, we add the estimates attached to positive shocks and compare this number to the addition of the estimates of negative shocks through Wald test. If we successfully reject the null hypothesis (∑

= ∑

) of short-run Wald test this is a sign of short-run adjustment asymmetry. Lastly, to confirm the long-run asymmetric effects between the positive and negative shocks we must reject the null hypothesis (

) of long-run Wald test. The question of causality between financial deepening, renewable energy, and non-renewable energy consumption in China is also addressed in this study. We check causality in a non-linear framework by conducting the panel causality test of Hatemi-J (Citation2012).

China has made more significant progress in financial resources and has more share of energy consumption in the world. For this reason, we collect yearly data from 1990 to 2019 for China. The dependent variables of the study are renewable energy and non-renewable energy consumption that both measured in quad BTU. Financial deepening is hard to quantify properly, we use two command proxies. One is the Bank deposits to GDP (%) and the other is broad money (M2) as a percent of GDP. These both proxies are suggested by McKinnon (Citation1973), Shaw (Citation1973), and Darrat (Citation1999) in economies growth literature. The data on renewable energy and non-renewable energy consumption is sourced from the Energy Information Administration (EIA), while data on financial deepening are obtained from the International Monetary Fund (IMF). The control variable data on Remittances, GDP growth, Trade openness are attained from the World Development Indicators (WDI). The detailed variable definitions are given in .

Table 1. Variable definitions.

3. Results and discussion

To check whether the impact of financial deepening on renewable and non-renewable energy consumption in China is asymmetric or not we apply the NARDL technique. Though the unit root test is not mandatory for the application of the ARDL model but for our own satisfaction we have applied two types of unit root tests i.e., unit root without breakpoint and unit root with breakpoint the results of which are provided in . Both types of tests confirm that none of our variables is I(2), hence, we can proceed further. Once we decide to proceed with the ARDL technique, the next thing we need to decide is the number of lags to be included. As the data used in the analysis is annual, therefore, we apply a maximum of two lags and to select the optimum number of lags Akaike Information Criterion (AIC) is used.

Table 2. Unit root testing.

Table 3 provides the results of short and long-run estimates of renewable and non-renewable energy models. In addition, the results of co-integration tests viz. bounds F-test and ECMt-1 and other diagnostic tests are also presented in . First of all, we want to confirm the validity of the long-run results which depend on the co-integration tests. From the estimates of the F-test and ECMt-1 we confirm that long-run results are co-integrated. These findings suggest that there is a valid long-run relationship between RE, BD, BM, GDP, TRADE, REM and NRE, BD, BM, GDP, TRADE, REM.

Table 3. NARDL estimates of renewable and non-renewable energy consumption.

The long-run estimates convey, that the estimates linked to BD_POS and BM_POS are positively significant in the RE model suggesting that a 1% increase in bank deposits and broad money increase the RE consumption in China by 0.249% and 7.150% respectively. Some previous findings by Sadorsky (Citation2010), Eren et al. (Citation2019), and Anton and Nucu (Citation2020) also supported our findings. Out finding shows that financial development can facilitate the reallocation of funds from traditional energy to renewable energy development. According to Lei et al. (Citation2021), the level of financial development can influence renewable energy consumption through three different channels: the direct effect, the wealth effect, and the business effect. The financial sector provides resources and boosts green investment in energy-consuming products and renewable technologies. Financial development shows an important role in increasing renewable energy consumption, therefore reducing non-renewable energy consumption among the old EU members (Anton & Nucu, Citation2020).

Positive shocks in BD & BM mean that ratio of bank deposits to GDP and broad money as a percentage of GDP increase suggesting an improvement in financial deepening. Due to increased financial depth in the economy, services related to banks and other financial institutions are accessible to more and more people. Investment loans will be easily available that encourage the investors to start new businesses, as a result, the process of wealth creation will be started which promotes overall economic activities in the country. Once the economy of the country takes off it pushes the per capita income and living standard of the people up. Consequently, people start consuming more luxury items such as cars, air conditioners, and heaters, microwaves, refrigerators, LEDs, mobiles, washing machines etc. Hence, energy consumption in the economy increases manifold due to business, wealth, and consumer effects (Ozturk, Citation2010; Sadorsky, Citation2010). Financial deepening on one side promotes economic growth but, on the other side, encourages the expansion of the projects of renewable energy sources and their usage. Moreover, providing resources and funds, on a priority basis, to the people and organizations who are involved in the R&D projects in the clean energy sector, promotes both the production and consumption of renewable energy (Assi et al., Citation2020).

In an emerging economy like China where the energy mix is heavily dominated by non-renewable energy sources, financial depth can help promote the use of renewable energy consumption. The major shift in the mindset of Chinese officials, with regards to environmental degradation, was observed during China’s 11th five-year plan, over the period 2006–2010, when they imposed strict penalties on the violators of environment laws and forcefully shutdown many ventures based on breaching environment-related rules and regulations (Wang, 2013). Under such circumstances, financial deepening can be used as an effective tool to promote investment in renewable energy projects. On the other side, the estimated coefficients BD_NEG & BM_NEG in the renewable energy model are significantly negative conferring that a 1% fall in both the measures of financial depth in China increases the consumption of renewable energy by 1.501% due to bank deposits and 1.177% due to broad money. This result shows the renewable energy has become an indispensable commodity and its demand has become inelastic that despite the fall in financial depth in the Chinese economy its consumption is increasing. This could be because China is an emerging economy and growing at a great pace, hence, there are many factors like urbanization, industrialization, tourism, trade etc. that all contribute to the rising demand of energy consumption and shrinkage of one or two sectors might not affect the overall renewable energy consumption. By observing these findings, we can say that the long-run asymmetric effects between BD_POS (BM_POS) and BD_NEG (BM_NEG) on renewable energy consumption in China are established and this notion is further fortified by the significant estimate attached to Wald-LR.

Now we will see the role of both the measures of financial deepening on the consumption of traditional sources of energy. From the estimates we see, NRE consumption decreases by 0.011% and 1.071% as a result of a 1% increase in bank deposits and broad money, respectively. Topcu and Payne (Citation2017) and Destek et al. (Citation2018) observed similar types of findings for different regions and countries. Conversely, a 1% fall in bank deposit and broad money increases the NRE consumption by 0.045% and 4.311%, correspondingly. These findings confer that banks and financial institutions in China are heading towards pro-environment behavior and are providing funds and loans to the firms and individuals who are developing newer technologies that are more energy-efficient and helpful in conserving energy. Moreover, the financial institutions might be investing in the programs of eco-innovations and renewable energy innovations that would not only promote economic growth but lessen the dependence on fossil fuels. Here again, the estimated statistic of Wald-LR is significant confirming the long-run asymmetric effects.

Among the control variables, the first one is GDP per capita, which confirms that a 1% surge in economic growth increases the renewable and non-renewable energy consumption by 0.462% and 0.031% respectively supporting the growth effect for the Chinese economy. However, a 1% increase in trade openness reduces renewable energy consumption by 0.085%, whereas, increases non-renewable energy consumption by 0.006%. Sadorsky (Citation2010) and Dedeoğlu and Kaya (Citation2013) all supported that trade pushes the energy demand because of growth and consumption effects. Likewise, a 1% increase in remittances decreases RE consumption by 1.058% and improves NRE consumption by 0.343%.

In the short run, the estimated coefficients of both the measures of financial deepening have provided mixed results i.e., positive at some lags and negative at others. The adjustment asymmetry between positive and negative effects of both the measures can’t be observed because the lag length attached to positive and negative shocks are the same for both measures in both models. The short-run impact asymmetry is confirmed for both the measures in only RE model, as the Wald-SR estimates are only significant in RE model. All other short-run estimates also provided mixed results.

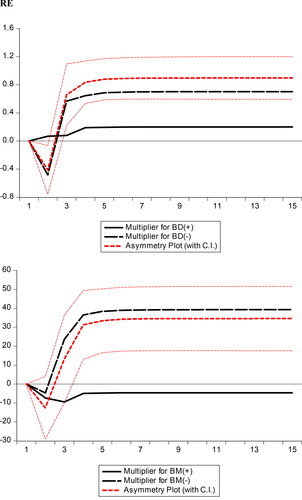

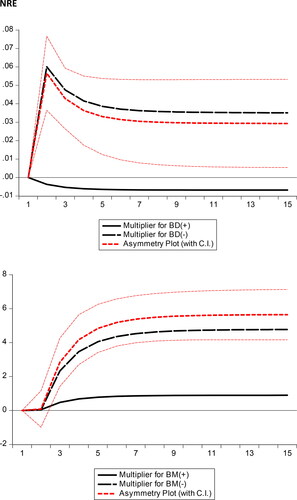

Some other diagnostic tests are also illustrated in . To detect first-order serial correlation we apply Langrage Multiplier (LM) test which confirms that our residuals are not serially correlated. Then, Ramsey RESET test documents that we have correctly specified the model, Breusch-Pagan-Godfrey (BPG) test confirm that our errors are homoscedastic. Lastly, CUSUM & CUSUMSQ proves that all our models are parametrically stable. and provide us with the detail of multiplier graphs, which are drawn on the basis of the NARDL method. The graph illustrates the asymmetric combination of the dynamic multipliers as a result of the rise and fall in the financial deepening.

Figure 1. Dynamic multiplier of RE.

Source: Authors’ Calculations.

Figure 2. Dynamic multiplier of NRE.

Source: Authors’ Calculations.

The estimates of asymmetric causal analysis are provided in . According to the estimates, uni-directional causality is running from BM_NEG → RE, NRE→BD_NEG, BM_POS→NRE. However, evidence of bi-directional causality is found between BD_NEG↔RE and BD_POS↔NRE confirming the feedback effect.

Table 4. Asymmetric causality.

4. Conclusion and policy implications

This contribution investigates the dynamic impact of financial deepening on renewable energy and non-renewable energy consumption in China, using the non-linear ARDL approach from 1990 to 2019. In the study, financial deepening is measured by bank deposits to the percent of GDP and broad money to the percent of GDP. The results indicate that positive and negative shocks in bank deposits have a positive impact on renewable energy consumption. While, in the case of broad money, the results show that positive and negative shocks in broad money exert a positive influence on renewable energy consumption in long-run. However, positive shocks in bank deposits and broad money have a negative impact on non-renewable energy consumption, while negative shocks in bank deposits and broad money exert a positive influence on non-renewable energy consumption in long run. On the other hand, the negative shocks in broad money and bank deposits have a positive effect on renewable and non-renewable energy consumption in the short-run. The short-run outcomes of the study infer that positive and negative shocks in broad money have a positive and significant effect on renewable energy consumption, while negative shocks in broad money has a negative effect on renewable energy consumption.

The study has some important policy recommendations for China. Authorities and policymakers should prioritize the allocation of financial resources for clean energy and technology innovations. Further, authorities should also redesign their renewable energy policies to improve more environmental quality as it helps them to adapt more green and energy-efficient technologies in their production of goods and services. These revised energy and finance policies may further assist China to maximize green growth and meet its targets of climate change. China's energy sector can be benefitted from financial deepening by increasing renewable energy consumption. Thus, government and policymaker's policies aimed at promoting financial deepening in China must be persistent and sustainable to foster renewable energy consumption. Policies that foster macroeconomic stability, and therefore improve green growth and environmental quality, would also have a significant effect on financial sector development in the long run. The government of China should direct the financial institutions to make an investment in the renewable and non-renewable energy consumption sector by providing credits at a lower cost for acquiring energy-efficient technologies. In this way, the Chinese government can enhance productivity, sustainable growth, and quality of the environment.

The joint link between government and academia can bridge the gap in consuming efficient renewable energy consumption with less CO2 emission and high green economic growth. Government should finance to encourage the use of green and clean energy consumption in the COVID-19 pandemic. China should take preemptive measures to protect the financial sector deepening against COVID-19 shocks. The central banks of China with the help of federal governments should protect the financial institutions, particularly, the banks against COVID-19. The unavailability of other proxies data is one of the limitations of this study. Future research can replace other proxies of financial deepening with bank deposits and broad money for new insight. Future studies may aim to focus on panel-specific analysis to draw more clear policy recommendations for a longer period for the globe. Similar analysis can be conduct by authors for emerging economies. The future study should investigate the asymmetric determinants of renewable and non-renewable energy consumption at the provincial and national levels in China.

References

- Ali, Q., Khan, M. T. I., & Khan, M. N. I. (2018). Dynamics between financial development, tourism, sanitation, renewable energy, trade and total reserves in 19 Asia cooperation dialogue members. Journal of Cleaner Production, 179, 114–131. https://doi.org/10.1016/j.jclepro.2018.01.066

- Anton, S. G., & Nucu, A. E. A. (2020). The effect of financial development on renewable energy consumption. A panel data approach. Renewable Energy., 147, 330–338. https://doi.org/10.1016/j.renene.2019.09.005

- Assi, A. F., Isiksal, A. Z., & Tursoy, T. (2020). Highlighting the connection between financial development and consumption of energy in countries with the highest economic freedom. Energy Policy, 147, 111897. https://doi.org/10.1016/j.enpol.2020.111897

- Azam, A., Rafiq, M., Shafique, M., Ateeq, M., & Yuan, J. (2021a). Investigating the impact of renewable electricity consumption on sustainable economic development: A panel ARDL approach. International Journal of Green Energy, 18(11), 1185–1192. https://doi.org/10.1080/15435075.2021.1897825

- Azam, A., Rafiq, M., Shafique, M., & Yuan, J. (2021b). An empirical analysis of the non-linear effects of natural gas, nuclear energy, renewable energy and ICT-Trade in leading CO2 emitter countries: Policy towards CO2 mitigation and economic sustainability. Journal of Environmental Management, 286, 112232. https://doi.org/10.1016/j.jenvman.2021.112232

- Azam, A., Rafiq, M., Shafique, M., & Yuan, J. (2021c). Renewable electricity generation and economic growth nexus in developing countries: An ARDL approach. Economic Research-Ekonomska Istraživanja, 34(1), 2423–2446. https://doi.org/10.1080/1331677X.2020.1865180

- Azam, A., Rafiq, M., Shafique, M., Zhang, H., Ateeq, M., & Yuan, J. (2021d). Analyzing the relationship between economic growth and electricity consumption from renewable and non-renewable sources: Fresh evidence from newly industrialized countries. Sustainable Energy Technologies and Assessments, 44, 100991. https://doi.org/10.1016/j.seta.2021.100991

- Azam, A., Rafiq, M., Shafique, M., Zhang, H., & Yuan, J. (2021e). Analyzing the effect of natural gas, nuclear energy and renewable energy on GDP and carbon emissions: A multi-variate panel data analysis. Energy, 219, 119592. https://doi.org/10.1016/j.energy.2020.119592

- Boutabba, M. A. (2014). The impact of financial development, income, energy and trade on carbon emissions: Evidence from the Indian economy. Economic Modelling, 40, 33–41. https://doi.org/10.1016/j.econmod.2014.03.005

- BP Statistical Review of World Energy (2018). BP Statistical Review of World Energy 2018: Two steps forward, one step back. Retrieved June 2018, from https://www.bp.com/content/dam/bp/business-sites/en/global/corporate/pdfs/energy-economics/statistical-review/bp-stats-review-2018-full-report.pdf

- Brunnschweiler, C. N. (2010). Finance for renewable energy: An empirical analysis of developing and transition economies. Environment and Development Economics, 15(3), 241–274. https://doi.org/10.1017/S1355770X1000001X

- Center, B. (2020). Annual Energy Outlook 2020. Energy Information Administration, DC.

- Charfeddine, L., & Kahia, M. (2019). Impact of renewable energy consumption and financial development on CO2 emissions and economic growth in the MENA region: A panel vector autoregressive (PVAR) analysis. Renewable Energy, 139, 198–213. https://doi.org/10.1016/j.renene.2019.01.010

- Chishti, M. Z., Ullah, S., Ozturk, I., & Usman, A. (2020). Examining the asymmetric effects of globalization and tourism on pollution emissions in South Asia. Environmental Science and Pollution Research International, 27(22), 27721–27731. https://doi.org/10.1007/s11356-020-09057-9

- Darrat, A. F. (1999). Are financial deepening and economic growth causally related? Another look at the evidence. International Economic Journal, 13(3), 19–35. https://doi.org/10.1080/10168739900000002

- Dedeoğlu, D., & Kaya, H. (2013). Energy use, exports, imports and GDP: New evidence from the OECD countries. Energy Policy, 57, 469–476. https://doi.org/10.1016/j.enpol.2013.02.016

- Destek, M. A., & Aslan, A. (2017). Renewable and non-renewable energy consumption and economic growth in emerging economies: Evidence from bootstrap panel causality. Renewable Energy, 111, 757–763. https://doi.org/10.1016/j.renene.2017.05.008

- Destek, M. A., Ulucak, R., & Dogan, E. (2018). Analyzing the environmental Kuznets curve for the EU countries: The role of ecological footprint. Environmental Science and Pollution Research International, 25(29), 29387–29396.

- Eren, B. M., Taspinar, N., & Gokmenoglu, K. K. (2019). The impact of financial development and economic growth on renewable energy consumption: Empirical analysis of India. Science of the Total Environment, 663, 189–197. https://doi.org/10.1016/j.scitotenv.2019.01.323

- Hatemi-J, A. (2012). Asymmetric causality tests with an application. Empirical Economics, 43(1), 447–456. https://doi.org/10.1007/s00181-011-0484-x

- International Energy Agency. (2017). Energy technology perspectives 2017: Catalysing energy technology transformations. OECD.

- Jarrett, U., Mohaddes, K., & Mohtadi, H. (2019). Oil price volatility, financial institutions and economic growth. Energy Policy, 126, 131–144. https://doi.org/10.1016/j.enpol.2018.10.068

- Kahouli, B. (2017). The short and long run causality relationship among economic growth, energy consumption and financial development: Evidence from South Mediterranean Countries (SMCs). Energy Economics, 68, 19–30. https://doi.org/10.1016/j.eneco.2017.09.013

- Khan, S. A. R., Zhang, Y., Kumar, A., Zavadskas, E., & Streimikiene, D. (2020). Measuring the impact of renewable energy, public health expenditure, logistics, and environmental performance on sustainable economic growth. Sustainable Development, 28(4), 833–843. https://doi.org/10.1002/sd.2034

- Koçak, E., & Şarkgüneşi, A. (2017). The renewable energy and economic growth nexus in Black Sea and Balkan countries. Energy Policy, 100, 51–57. https://doi.org/10.1016/j.enpol.2016.10.007

- Lei, W., Liu, L., Hafeez, M., & Sohail, S. (2021). Do economic policy uncertainty and financial development influence the renewable energy consumption levels in China? Environmental Science and Pollution Research, 1–10. https://doi.org/10.1007/s11356-021-16194-2

- Lin, B., Omoju, O. E., & Okonkwo, J. U. (2016). Factors influencing renewable electricity consumption in China. Renewable and Sustainable Energy Reviews, 55, 687–696. https://doi.org/10.1016/j.rser.2015.11.003

- McKinnon, R. I. (1973). Money and Capital in Economic Development. The Brookings Institution.

- Ouyang, Y., & Li, P. (2018). On the nexus of financial development, economic growth, and energy consumption in China: New perspective from a GMM panel VAR approach. Energy Economics, 71, 238–252.

- Ozturk, I. (2010). A literature survey on energy–growth nexus. Energy Policy, 38(1), 340–349. https://doi.org/10.1016/j.enpol.2009.09.024

- Ozturk, I., & Salah Uddin, G. (2012). Causality among carbon emissions, energy consumption and growth in India. Economic Research-Ekonomska Istraživanja, 25(3), 752–775. https://doi.org/10.1080/1331677X.2012.11517532

- Pesaran, M. H., Shin, Y., & Smith, R. J. (2001). Bounds testing approaches to the analysis of level relationships. Journal of Applied Econometrics, 16(3), 289–326. https://doi.org/10.1002/jae.616

- Qin, Z., & Ozturk, I. (2021). Renewable and non-renewable energy consumption in BRICS: Assessing the dynamic linkage between foreign capital inflows and energy consumption. Energies, 14(10), 2974. https://doi.org/10.3390/en14102974

- Rasoulinezhad, E., & Saboori, B. (2018). Panel estimation for renewable and non-renewable energy consumption, economic growth, CO2 emissions, the composite trade intensity, and financial openness of the commonwealth of independent states. Environmental Science and Pollution Research, 25(18), 17354–17370. https://doi.org/10.1007/s11356-018-1827-3

- Sadorsky, P. (2009). Renewable energy consumption and income in emerging economies. Energy Policy, 37(10), 4021–4028. https://doi.org/10.1016/j.enpol.2009.05.003

- Sadorsky, P. (2010). The impact of financial development on energy consumption in emerging economics. Energy Policy, 38, 2528–2535.

- Sadorsky, P. (2011). Financial development and energy consumption in Central and Eastern European frontier economies. Energy Policy, 39(2), 999–1006. https://doi.org/10.1016/j.enpol.2010.11.034

- Shahbaz, M., Sinha, A., Raghutla, C., & Vo, X. V. (2021). Decomposing scale and technique effects of financial development and foreign direct investment on renewable energy consumption. Energy, 238, 121758.

- Shahbaz, M., Van Hoang, T. H., Mahalik, M. K., & Roubaud, D. (2017). Energy consumption, financial development and economic growth in India: New evidence from a nonlinear and asymmetric analysis. Energy Economics, 63, 199–212. https://doi.org/10.1016/j.eneco.2017.01.023

- Shaw, E. S. (1973). Financial deepening in economic development. Oxford University Press.

- Shin, Y., Yu, B., & Greenwood-Nimmo, M. (2014). Modelling asymmetric cointegration and dynamic multipliers in a nonlinear ARDL framework. In Festschrift in honor of Peter Schmidt. (pp. 281–314). Springer.

- Skare, M., Tomic, D., & Stjepanovic, S. (2020). Energy consumption and green GDP in Europe: A panel cointegration analysis 2008–2016. Acta Montanistica Slovaca, 25(1), 46–56.

- Topcu, M., & Payne, J. E. (2017). The financial development–energy consumption nexus revisited. Energy Sources, Part B: Economics, Planning, and Policy, 12(9), 822–830. https://doi.org/10.1080/15567249.2017.1300959

- Ullah, S., Ozturk, I., Majeed, M. T., & Ahmad, W. (2021). Do technological innovations have symmetric or asymmetric effects on environmental quality? Evidence from Pakistan. Journal of Cleaner Production, 316, 128239. https://doi.org/10.1016/j.jclepro.2021.128239

- Ullah, S., Ozturk, I., Usman, A., Majeed, M. T., & Akhtar, P. (2020). On the asymmetric effects of premature deindustrialization on CO2 emissions: Evidence from Pakistan. Environmental Science and Pollution Research International, 27(12), 13692–13702.

- Usman, A., Ozturk, I., Hassan, A., Zafar, S. M., & Ullah, S. (2021a). The effect of ICT on energy consumption and economic growth in South Asian economies: An empirical analysis. Telematics and Informatics, 58, 101537. https://doi.org/10.1016/j.tele.2020.101537

- Usman, A., Ozturk, I., Ullah, S., & Hassan, A. (2021b). Does ICT have symmetric or asymmetric effects on CO2 emissions? Evidence from selected Asian economies. Technology in Society, 67, 101692. https://doi.org/10.1016/j.techsoc.2021.101692

- Wandji, Y. D. F. (2013). Energy consumption and economic growth: Evidence from Cameroon. Energy Policy, 61, 1295–1304.

- WDI. (2018). World Development Indicators (WDI), World Bank Data. Retrieved from https://data.worldbank.org/indicator

- Zhao, W., Zhong, R., Sohail, S., Majeed, M. T., & Ullah, S. (2021). Geopolitical risks, energy consumption, and CO2 emissions in BRICS: An asymmetric analysis. Environmental Science and Pollution Research, 28(29), 39668–39679. https://doi.org/10.1007/s11356-021-13505-5