?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Employing Chinese customs data and the Peking University Digital Financial Inclusion Index of China, this paper studies the impact of China's digital finance development on the upgrading of export at the city level and further explores the heterogeneity across cities and the mechanisms through which digital finance influences export upgrading. Benchmark results suggest that digital inclusive finance can significantly promote the upgrading of export. The heterogeneity analysis shows that cities with a smaller size, lower wage, higher human capital level, and better location advantage experience greater facilitating effects of digital inclusive finance on promoting export upgrading. It suggests that, compared with ‘icing on the cake’, the digital inclusive finance plays a better role in ‘offering fuel in snowy weather’, whereas full exertion of the inclusiveness of digital finance requires higher human capital and location advantage. Further mechanism analysis shows that innovation effect and market effect are the main channels where digital inclusive finance promotes the upgrading of a city’s export.

1. Introduction

After the outbreak of the global financial crisis in 2008, the global trade dropped dramatically by 12%, which pushed the attention about the impact of financial development on export to a new height. Finance development is conducive to reducing the transaction costs of both supply and demand sides and improving the efficiency of capital use (Levine, Citation2005). Based on the model of international trade with heterogeneous firms, the development of a financial market can ease the financing constraints and improve firms’ productivity, promoting the export activities of the whole economy (Chaney, Citation2016). However, due to the poor ability to resist risks and the lack of business records, small and medium-sized enterprises often experience financial exclusion in international trade. According to the World Bank Group's World Development Report, by 2013, only 34% of enterprises in the world could borrow from a formal financial system, and this proportion is only 51% in developed countries. Similarly, at the individual level, more than 2.05 billion adults in the world have no access to formal financial services, accounting for about half of the total number of adults in the world at that time, among which 88% come from developing countries (World Bank, Citation2013). These facts show that traditional finance can also restrict the development of trade activities due to its exclusion.

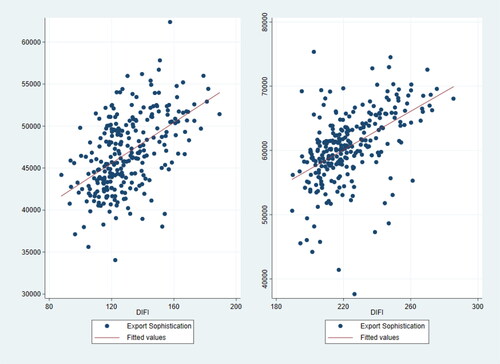

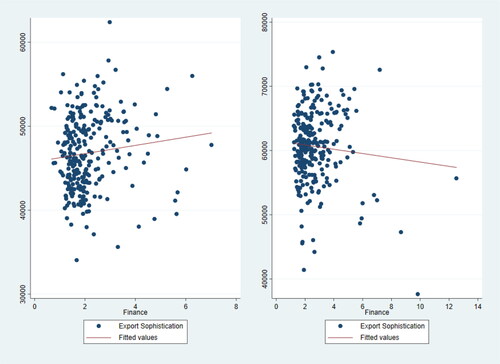

However, digital finance can weaken the exclusiveness of traditional finance and reduce the asymmetry in investment and borrowing exclusion levels in traditional financial markets (Zhong & Jiang, Citation2021) to promote the transformation and upgrading of export. Taking China as an example, thanks to the rapid development of information technology like 5G, big data, and cloud computing, China's digital economy (especially digital finance) has experienced rapid development in the past few years (Zhang et al., Citation2019). The widespread use of mobile payment applications, such as Alipay and WeChat payments, has improved the efficiency of capital use of individuals and small and medium-sized enterprises. Meanwhile, digital inclusive finance provides financial services at affordable costs for small businesses and other individuals who could not obtain financial resources from elsewhere (Wang et al., Citation2020), thus promoting the operation efficiency of the whole social and economic activities. By matching Chinese customs data with the Peking University Digital Financial Inclusion Index of China from 2013 to 2017, we can find that digital inclusive finance plays a significant role in promoting export sophistication at the city level (). In contrast, the role of traditional finance in promoting a city’s export sophistication is fairly limited and even gradually turns negative in recent years (). In addition, we also find that the impact of digital inclusive finance on export sophistication shows strong city heterogeneity. To better understand these phenomena and the causes, it is necessary to analyse the influence mechanisms of digital inclusive finance on a city’s export upgrading.

Figure 1. Digital Financial Inclusion Index and city’s export sophistication in 2013 (left) and 2017 (right).

Source: The Authors.

Figure 2. Traditional finance development and city’s export sophistication in 2013 (left) and 2017 (right).

Source: The Authors.

Under the above background, this paper matches Chinese customs data with the Peking University Digital Financial Inclusion Index of China from 2013 to 2017 at the city level to examine the impact of digital inclusive finance on the upgrading of a city’s export. First, this paper empirically verifies the promotion effect of digital inclusive finance on upgrading a city’s export. Second, the heterogeneity analysis suggests that digital inclusive finance can significantly promote the upgrading of export in cities with a smaller size, lower wage, higher human capital level, and better location advantage, rather than their counterparts. The results indicate that human capital and location advantage are necessary to bring the inclusiveness of digital inclusive finance into full play in improving export sophistication in less developed cities. Then, mechanism analysis shows that innovation and market effects are important channels through which digital inclusive finance promotes the upgrading of a city’s export.

The remainder of the paper is organised as follows: Section 2 summarises related literature and theory. Section 3 theoretically analyses possible impacts and mechanisms of digital finance on export sophistication, then comes up with hypotheses. Section 4 constructs empirical models and quantifies all the variables. Section 5 estimates the benchmark model and reports the estimation results. Section 6 mainly conducts heterogeneity analysis and mechanism analysis and discusses the results. Section 7 concludes the paper.

2. Literature review

With the adjustment of international trade strategies, the focus of research on export has shifted from export scale to export quality. Hausmann and Rodrik (Citation2003) first put forward the concept of sophistication to measure the technical content of a country's export. On this basis, Rodrik (Citation2006) points out that the export sophistication can be regarded as the productivity of a country’s exports and develops an indicator that measures the productivity level associated with a country’s export basket. The concept and measurement of export sophistication lay a foundation for quantitative research in this field, so some scholars empirically investigate the factors affecting export sophistication. Some scholars admit the role of economic growth and economic scale in improving export sophistication (Hausmann et al., Citation2007; Rodrik, Citation2006; Weldemicael, Citation2014), while others explore the role of factor inputs and find that human capital (Hausmann et al., Citation2007; Hüseyni, Citation2019; Wang et al., Citation2010), knowledge and intelligence (Odilova, Citation2018), foreign direct investment (Baliamoune-Lutz, Citation2019; Görg & Greenaway, Citation2004; Harding & Javorcik, Citation2009; Xu & Lu, Citation2009), and outward foreign direct investment (Rehman & Ding, Citation2020) are conducive to increasing export sophistication. From the perspective of trade mode, some scholars have also verified that the import of intermediate inputs (Bas & Strauss-Kahn, Citation2014) and processing exports (Assche & Gangnes, Citation2010; Branstetter & Lardy, Citation2006; Schott, Citation2008) can impact export sophistication. Additionally, national policy and institutional environment can also affect export sophistication, such as trade liberalisation policy (Nguyen, Citation2016), institutional quality (Berkowitz et al., Citation2006; Cabral & Veiga, Citation2010) and intellectual property rights protection (Chen & Puttitanun, Citation2005).

In addition to the aforementioned factors, financial development also plays an irreplaceable role in improving export quality. At the macro level, based on the framework of the Heckscher-Ohlin-Samuelson (HOS) model, Kletzer and Bardhan (Citation1987) find that different countries have comparative advantages in different industries because of various financial development levels, thus forming discrepant international trade modes. Also based on the HOS framework, Ju and Wei (Citation2011) conclude that factor endowment matters for economies with a high-quality financial sector, while the quality of the financial system is an independent source of comparative advantage for economies with a low-quality financial sector. At the micro enterprise level, Chor and Manova (Citation2012), Feenstra et al. (Citation2014), Manova (Citation2013) and Chaney (Citation2016) introduce the financing constraints into the export theory with heterogeneous firms put forward by Melitz (Citation2003) to discuss export behaviour under imperfect financial market competition. They find that the low efficiency of the financial system and the lag of financial development significantly affect enterprises’ export behaviour.

Under the support of relevant theories, the existing research has empirically analysed the impact of financial development on trade. Hur et al. (Citation2006) find that economies with higher levels of financial development have higher export shares and trade balance in industries with more intangible assets. Becker et al. (Citation2013) argue that a developed financial system can therefore facilitate exports, because financial development is associated with more exports in industries in which fixed costs are high as well as to importers that require high costs. Using matched customs and firm-level bank credit data from Peru, Paravisini et al. (Citation2015) find that credit shocks affect the intensive margin of exports, and credit shortages reduce exports through raising the variable cost of production rather than the cost of financing sunk entry investments. Leibovici (Citation2018) finds that financial friction reduces trade share by distorting the production decisions of exporters relative to non-exporters and distorting the decision to export. Susanto and Rosson (Citation2011) point out that financial development has positive impacts on exports and the impacts differ significantly across regions. Yu and Hu (Citation2015) find that improvement of financial development plays a decisive role in upgrading both domestic and total sophistication of China's manufactured exports. By building an endogenous technological progress model with intermediate product expansion, Fang et al. (Citation2015) find that financial development can promote export technical sophistication in China. Although most studies confirm the positive role of financial development in exports and export sophistication, Tang (Citation2016) finds that higher stock market and bank development have a negative rather than positive effect on exports.

Returning to China's realistic context, we must recognise that China's emerging financial market is imperfect and incomplete with many market impediments, such as transaction costs, taxes, and information asymmetry (Chan et al., Citation2007). Additionally, traditional financial institutions tend to serve economically developed areas and exclude the least-developed cities (Zhong & Jiang, Citation2021), both leading to and exacerbating financial exclusion. But, to some extent, the imperfection and long-term insufficient supply of traditional financial services is an important prerequisite for the leapfrog development of digital finance, which brings increased competition and efficiency to the traditional financial sector by mobile terminals and the internet (Lorente & Schmukler, Citation2018). Furthermore, with the deep integration between internet technology and finance, digital finance can help decrease information asymmetry, reduce transaction costs, improve availability of financial services, and optimise resource allocation in the financial market (Li et al., Citation2020).

Existing research on digital finance focuses on its impacts on the economy (Anand & Chhikara, Citation2013; Sarma & Paris, Citation2011) and the traditional financial market (Berger, Citation2003; Lorente & Schmukler, Citation2018). In addition, some research indicates that big data-based risk evaluation can help save transaction cost and decrease the degree of information asymmetry, thus helping small- and micro-businesses secure financing (Moenninghoff & Wieandt, Citation2013). Stojcic et al. (Citation2019) point out that for countries and regions to catch up with modern manufacturing characterised by automation and data exchange, an important requirement is the development of the digital infrastructure. Beck et al. (Citation2018) show significant quantitative implications of payment technology innovation for entrepreneurial growth and macroeconomic development by reducing financial transaction costs and alleviating the information asymmetry. Drawing from harmonised firm-level data for 16 industrialised and emerging economies, Aghion et al. (Citation2007) find that access to finance matters most for the entry of small firms and in sectors that are more dependent upon external finance. Mahdiraji et al. (Citation2019) find that the digital banking strategy can more effectively distinguish customers’ needs to offer services proportionate to their manner than the traditional banking operation mode.

Although the existing literature directly studying the impact of digital finance on export sophistication is rare, some scholars have confirmed that the internet has positive effects on export performance (Freund & Weinhold, Citation2004; Lin, Citation2015; Mallick, Citation2014; Ricci & Trionfetti, Citation2012). Information and communication technology (ICT) is an innovation responsible for the upswing of the world economy and the start of the fifth Kondratieff cycle in the 1970s (Yushkova, Citation2014). Digital technology can reduce information and search costs in international trade (Anderson & Van Wincoop, Citation2004; Goldfarb & Tucker, Citation2019; Lendle et al., Citation2016; Nath & Liu, Citation2017) and reduce trade barriers by reducing trade costs to promote the development of trade (Choi, Citation2010). Moreover, the use of the internet helps improve the probability of enterprises participating in trade (Clarke, Citation2008; Ricci & Trionfetti, Citation2012; Yadav, Citation2014). Besides that, some scholars find the heterogeneity in this issue. Freund and Weinhold (Citation2002) show that the impact of the internet on trade is greater in underdeveloped countries than in developed countries. Similarly, Clarke (Citation2008) believes that the internet mainly promotes the export of enterprises in low- and middle-income countries.

To sum up, the existing research provides support theoretically and empirically for this study, but there is still room for us to make a marginal contribution. First, there are sufficient theoretical and empirical studies about the influence of finance on trade. Most studies focus on traditional finance and pay more attention to the total amount of trade or trade mode while rarely exploring the impact of digital finance on export sophistication. On this basis, we start with digital inclusive finance, which brings more inclusive growth and studies its impact on upgrading a city’s export, to supplement the existing literature. Second, we focus on the city level, which can support us in verifying the inclusiveness of digital finance across cities, whether the less developed cities benefit more from the inclusive growth brought by digital finance in improving export sophistication. Finally, we discuss whether innovation and market effects are the two channels through which digital inclusive finance affects export sophistication. By doing so, we attempt to supplement the existing research on the analysis of the mechanisms of digital inclusive finance affecting export.

3. Theoretical analysis

3.1. Digital inclusive finance and a city’s export upgrading

Digital inclusive finance alleviates the financing constraints faced by enterprises through a wider coverage of financial services. According to the export theory of heterogeneous enterprises (Melitz, Citation2003), digital inclusive finance improves the production efficiency of enterprises to promotes export. On the one hand, if firms face liquidity constraints when accessing foreign markets, it prevents some firms from exporting because they cannot access financial markets and cover entry costs into foreign markets (Chaney, Citation2016). Therefore, the development of digital inclusive finance improves enterprises’ participation in export through offering more convenient and effective financial support for enterprises facing financing constraints, which makes up for variable costs, thereby promoting export. On the other hand, due to the low ability to resist risks and the lack of business records, it often takes a long period for small and medium-sized enterprises to borrow through the formal traditional financial channels. More seriously, these enterprises are more likely to face the fracture of the capital chain and higher time costs in the process of export. The digitalisation of finance may provide new technologies that have the potential to improve access to finance for firms and afford new possibilities for investors (Buchak et al., Citation2018) to provide liquidity and enhance the risk resistance ability for small and medium-sized enterprises. Therefore, the development of digital inclusive finance expands the number of enterprises participating in export and increases the types of export products and export modes, promoting export scale as well as export sophistication.

On this basis, this paper puts forward our first hypothesis:

H1: The development of digital inclusive finance is conducive to the upgrading of a city’s export upgrading.

3.2. Inclusiveness of the impact of digital inclusive finance on a city’s export upgrading

There exists city heterogeneity in the impact of digital inclusive finance on the upgrading of a city’s export. Severe information asymmetry and high marginal costs are key factors leading to exclusion from traditional finance (Zhong & Jiang, Citation2021). In the least developed cities, individuals generally have little savings and few investments, but scarce collateral and credit certificates limit their access to bank credit (Fungáčová & Weill, Citation2015). Whereas, by reducing transaction costs, reducing the asymmetry between the two sides of the transaction, and improving the efficiency of financial services, digital inclusive finance provides less developed cities with previously unreachable opportunities, helping these cities achieve faster and more comprehensive economic growth. On the one hand, with the development of internet technology, digital inclusive finance has broadened the scope, mode, type, and efficiency of financial services. Therefore, the threshold to participate in digital finance is relatively low, which makes digital finance a long-tailed market (Liao et al., Citation2020). On the other hand, the low threshold and low cost of digital inclusive finance improve the satisfaction of financial service requirements in less developed cities. Based on the above analysis, the inclusiveness of digital finance makes the effect on the export upgrading of less developed cities stronger than their counterparts. In other words, digital inclusive finance is better in ‘offering fuel in snowy weather’ than ‘icing on the cake’. However, driven by technology, digital inclusive finance has a certain ‘pickiness’. The popularisation and application of technology require certain knowledge stock. Especially in the early development of digital finance, insufficient knowledge stock will lead to the mismatch between the demand side and the supply side of financial products because the knowledge threshold or the development of digital inclusive finance face human capital constraints. Similarly, export activities require location advantages, such as ports, and insufficient locations will also restrict the full play of digital inclusive finance in improving city's export sophistication.

Based on the above analysis, this paper puts forward following two hypotheses:

H2: The inclusiveness of digital finance makes less developed cities benefit more in export upgrading.

H3: The full play of inclusiveness of digital finance requires the support of human capital level and export-related location advantage.

3.3. The impact of digital inclusive finance on a city’s export upgrading: the innovation effect

Digital finance combines digital technology and financial services in the form of internet finance, mobile finance, fin-tech, and other forms (Li et al., Citation2020). Promoting innovation effectively requires well-functioning financial markets that play critical roles in reducing financing costs, allocating scarce resources, evaluating innovative projects, managing risk, and monitoring managers (Hsu et al., Citation2014). Meanwhile, the widespread of information technology can facilitate knowledge diffusion among businesses to boost their innovation performance (Paunov & Rollo, Citation2016). Therefore, compared with traditional finance, digital inclusive finance has more advantages in promoting innovation. From the perspective of alleviating financing constraints, digital inclusive finance has the advantages of fast financing and low cost for enterprises and individuals, thus it is conducive to promoting the development of innovation activities through breaking the financing constraints. Meanwhile, higher lending levels will also promote enterprises to make more innovative investments (Chen et al., Citation2015). Besides, small and medium-sized enterprises are more active in innovation activities, but they face more financing constraints (Ryan et al., 2014). The development of digital finance provides strong support for those enterprises to carry out innovation. Consequently, digital inclusive finance promotes the overall innovation performance by driving innovation activities at a micro-level. From the perspective of using the internet and information technology, the knowledge sharing effect and spillover effect enables enterprises to receive more and farther information, the learning inducing effect accelerates the accumulation of human capital, and the application expansion can effectively change enterprises’ behaviour and industry’s organisational structure to promote innovation. Through innovation, firms can enter new geographical markets with novel and better products, therefore making exports more successful (Golovko & Valentini, Citation2011).

To sum up, this paper puts forward a fourth hypothesis:

H4: Digital inclusive finance promotes the upgrading of a city’s export by producing an innovation effect.

3.4. The impact of digital inclusive finance on a city’s export upgrading: the market effect

The development of digital finance extends the boundary of trade by incorporating more participants and improving resource accessibility. In terms of the former, digital finance has great potential to broaden access to financial services by lowering costs, reducing information asymmetries and enabling more transparency (Gabor & Brooks, Citation2017), as well as improving efficiency (Li et al., Citation2020). Then, digital finance makes it possible to match the financial demand side with the supply side, where the parties may be geographically disparate (Pierrakis & Collins, Citation2013). Meanwhile, digital finance makes financing more versatile and accessible for individuals and small business owners. As for improving resource accessibility, funds and information are two major market resources. The utilisation of internet technology enriches marketing information and expands transaction channels, resulting in improved resource accessibility (Yang & Lim, Citation2015). Above all, the development of digital finance expands the boundary of cross-regional transactions and improves market accessibility, thus producing a market effect. Furthermore, the improvement of market accessibility strengthens the regional industrial agglomeration, then increases the total factor productivity of enterprises (Holl, Citation2016), and finally improves the overall export, optimising export structure.

From the above analysis, this paper puts forward a fifth hypothesis:

H5: Digital inclusive finance promotes the upgrading of a city’s export through the market effect.

4. Empirical model, variables, and data

4.1. Empirical model

To further quantify the impact of digital inclusive finance on a city’s export upgrading, we build the following econometric model:

(1)

(1)

where

represents the city, and

is the time.

means the fixed effect of the city, or the controlling of unobserved factors that do not change with time in a particular city.

is the time fixed effect that does not change with the individual characteristics of the city.

is a random error term that obeys the standard normal distribution.

is the core explained variable of this paper. Referring to the existing research on China's export structure and competitiveness (Xu & Lu, Citation2009; Jarreau & Poncet, Citation2012), we employ the natural logarithm of the sophistication index to measure the upgrading of a city’s export.

the development of digital inclusive finance, is the core explanatory variable of this paper, measured by the natural logarithm of the Peking University Digital Financial Inclusion Index of China at the city level.

are the other control variables that affect the city's export upgrading.

4.2. Variables

4.2.1. Explained variable

The explained variable of this paper is to measure the upgrading of a city’s export. From the perspective of the supply side, the upgrading of export technology is often accompanied by the upgrading of export. Therefore, export sophistication measures the upgrading of a city’s export. Referring to the measurement method proposed by Hausmann et al. (Citation2007), according to the export data by HS 6-digit product, this paper first calculates the export sophistication of each product, which is the weighted average of the per capita GDPs of countries exporting a given product. It then calculates the export sophistication at the city level, which is a weighted average of the export sophistication in the city’s overall export basket. The specific calculation process is as follows:

(2)

(2)

where

is export sophistication of product

in year

is the value-share of the commodity in the country’s overall export basket.

represents the per-capita

of country

On the basis of EquationEquation (2)(2)

(2) , combined with export product structure of each city, the export sophistication associated with city

is defined by:

(3)

(3)

where

is export sophistication of city

in year

is the export scale of product

of city

in year

4.2.2. Explanatory variables

The core explanatory variable of this paper is the digital inclusive finance index at the city level. We use the city-level data of the Peking University Digital Financial Inclusion Index of China, produced by a research team from the Institute of Digital Finance at Peking University and the Ant Financial Services Group. This index involves three dimensions, including coverage breadth, usage depth, and digitisation level, and it uses 33 indicators, such as Alipay's number per 10,000 people. This index can depict the development trend of digital inclusive finance across cities in China.

4.2.3. Control variables

Based on the existing research, this paper selects the following control variables that may affect the city's export upgrading. The degree of city’s openness () is measured by the natural logarithm of the proportion of the actual use of foreign investment in the city's

(Schott, Citation2008). The development of traditional finance (

) is measured by the natural logarithm of the proportion of the balance of deposits and loans of financial institutions at the end of the year in the whole city's

By controlling the development of traditional finance, we can distinguish the effects of digital inclusive finance from traditional finance on the upgrading of a city’s export. Industrial structure (

) is a crucial factor affecting China's export (Mazumdar, Citation1996), and the manufacturing industry contains more export enterprises, so we use the proportion of the secondary industry in the city's

to measure the city's industrial structure. In terms of total factor productivity (

), referring to Battese and Coelli (Citation1995), we use the SFA method to calculate the natural logarithm of total factor productivity to measure the efficiency of a city’s economic development. Considering the positive impact of the agglomeration of a city’s population on trade (Koenig et al., Citation2010), we use the natural logarithm of the city's average population at the end of the year to measure the city's population size (

). Given the fact that the expansion of fiscal expenditure may affect the trade balance (Costinot, Citation2009), we use the ratio of the city's public expenditure to the city's

to measure the scale of government expenditure (

).

4.3. Data

The sample period covers 2013 to 2017. The city-level digital inclusive finance index is from the Peking University Digital Financial Inclusion Index of China. The trade data used in constructing export sophistication is from Chinese customs data. The rest of the control variables are mainly from the China City Statistical Yearbook, and the statistical calibre is prefecture-level cities. Due to missing data in some cities, we filter out 272 prefecture-level cities. The descriptive statistics of the main variables are in .

Table 1. Descriptive statistics of main variables.

5. Empirical tests and results

5.1. Benchmark results

Based on the above empirical model, this paper focuses on the impact of digital inclusive finance on export upgrading at the city level. We start with fixed effect regression and use the clustering standard error at the city level (Bertrand et al., Citation2004) to deal with the potential serial correlation and heteroscedasticity. Then, we replace the explanatory variable with the sub-dimension of digital inclusive finance or the natural logarithm of digitisation degree () to investigate its impact on the upgrading of a city’s export. In addition, the development of digital inclusive finance presents spatial agglomeration and still relies on entity economy and traditional finance. Therefore, we remove first-tier cities, such as Beijing, Shanghai, Shenzhen, and Guangzhou, and cities with a high degree of internet finance development, such as Hangzhou, from the sample to alleviate the possible overestimation of the development of digital inclusive finance.

shows the results of the fixed effect regression. Column (1) is the regression result of the influence of digital inclusive finance () on the upgrading of a city’s export. The coefficient of digital inclusive finance is significantly positive, meaning that the city’s export will upgrade with the development of digital inclusive finance promoting the export sophistication. As shown in column (2), the rise in digitisation degree also promotes the upgrading of a city’s export. The regression results in columns (3) and (4) show that after removing the cities with a high spatial agglomeration of digital inclusive finance, the digital inclusive finance promotion still plays a positive role in promoting the upgrading of a city’s export. Therefore, H1 is verified.

Table 2. Benchmark regression results.

In addition, we also follow the influence of traditional finance () on the upgrading of a city’s export. As shown in , the corresponding coefficients are all negative and significant, indicating that the development of traditional finance has an inhibitory effect on the upgrading of cites’ export, which is consistent with the results shown in . This may be because the development of traditional finance has not completely eased the financing constraints of private enterprises or small and medium-sized enterprises, thus restricting the development of exports (Ciani & Bartoli, Citation2013). In contrast, through integrating digital technology with financial services, digital inclusive finance improves the availability of financial services, enhances enterprise productivity, and promotes export upgrading. This further highlights the benefits of digital development for export development. Besides, government expenditure (

) represents the government's intervention in the upgrading of a city’s export. Its significantly negative coefficient indicates it is more difficult for cities to upgrade their export under government intervention. This result is consistent with the research conclusions of Levchenko (Citation2007) and Auty (Citation2009), which point out that the superior regional development conditions may induce the government to stretch out a ‘predatory hand’ and distort the spontaneous process of the market. This would then hinder the formation of export comparative advantage in the export sophisticate sector. This suggests that the government should find a reasonable position rather than excessive intervening in the process of a city’s export upgrading.

5.2. Endogenetic treatment

Considering that there may be endogenous problems in the development of city’s digital inclusive finance, cities with higher export sophistication may improve their digital inclusive finance. We use the instrumental variable method to solve the potential reverse causality problem.

In terms of the choice of instrumental variables, we refer to existing research and choose the number of fixed-line telephones per 100 people in 1984. The reason for choosing this instrumental variable is that the development of digital inclusive finance mainly benefits from the continuous upgrading of internet technology. Specifically, as for the development of internet technology in China, the first step is to access the internet through the fixed-line telephone network, then gradually develop to optical fibre broadband and wireless mobile phones. It can be inferred that the popularity of the fixed-line telephone in history has laid the foundation for the development of internet technology. Therefore, the number of fixed-line telephones in cities in history meets the requirements of the relevance of instrumental variables. Whereas, with the rapid development of the internet and mobile communication technology, the influence of the fixed-line telephone on export is gradually disappearing. After controlling the influence of other factors, choosing the number of fixed-line telephones in history as the instrumental variable also meets the exclusivity requirements. In addition, this study uses panel data, while the number of fixed-line telephones in history is cross-sectional data. Therefore, we refer to the setting method of Nunn and Qian (Citation2014) to interact the number of fixed-line telephones with the lagged of the number of internet access users per capita of the whole city and the lagged of the number of mobile phone users per capita of the whole city, respectively. The above two variables are logarithmic, and the time trend of historical data correlation matches with the sample. The first stage exclusive F statistic tests the strong correlation between instrumental variables and endogenous variables. shows the regression results of instrumental variables.

Table 3. Estimation results of instrumental variables.

Columns (1) and (3) in are the results of panel instrumental variables of the whole sample and the sample excluding the five cities with high degrees of inclusive finance agglomeration. The results show that the p-value of the Hansen J statistic is greater than 0.25, indicating that the instrumental variables meet the requirements of exogenous. The coefficients of the two instrumental variables are significantly positive in the first stage of regression, which meets the requirements of the correlation between instrumental variables and endogenous variables. The F-test statistic is significantly positive in the first stage, indicating that there is no weak instrumental variable problem. Besides, the coefficient of digital inclusive finance is significantly positive, which shows that it has a strong role in promoting the upgrading of a city’s export, and it also shows the robustness of the benchmark results. Furthermore, to prove the exogenous of the selected instrumental variables is valid, we conduct an IV-GMM test, and columns (2) and (4) of show the estimation results. The p-value of the Hansen J statistic verifies the exogenous of instrumental variables, and the coefficient of digital inclusive finance is still significantly positive, which again indicates the robustness of the benchmark results.

5.3. Robustness test

To further test the robustness of the results of this study, we conduct robustness checks from the following aspects.

First, the explained variable is replaced by the ratio of dependence on export, which is measured by the ratio of the city's export to the city's Since cities with higher demand for export upgrading often have a higher ratio of dependence on export, we can choose it as the alternative variable. As shown in column (1) of , the coefficient of digital inclusive finance is significantly positive, indicating that this variable has a significant positive relationship with export dependence, suggesting the robustness of the benchmark results.

Table 4. Regression results of robustness test.

Second, we calculate the residual of the model (1), and we delete the samples whose absolute value of residual is greater than 2.5 times of the standard deviation to re-estimate the results to eliminate the influence of outliers. Results in column (2) show that the removal of the sample outlier does not significantly affect the coefficient and significance of digital inclusive finance, which can still explain the significant impact on the upgrading of a city’s export.

Then, we re-estimate the results after removing the provincial capital cities from the whole sample. This is mainly because the provincial capital cities have high primacy and concentrate more resources (including financial resources), so we need to exclude this influence. As shown in column (3), the coefficient of digital inclusive finance is still significantly positive.

Finally, the random effect replaces the fixed effect, and column (4) shows the results. After replacing the empirical method, our conclusion still holds.

In general, although the coefficient and significance of some explanatory variables are slightly different, the robustness checks still support the conclusion that digital finance significantly improves export sophistication. In short, the overall results show strong robustness.

6. Expansibility analysis

6.1. Heterogeneity analysis: what kind of cities benefit from ‘inclusiveness’?

The above results show that the development of digital inclusive finance promotes the upgrading of the city's export. Then, as for different cities, what kind of cities can take better advantage of the development of digital inclusive finance to promote the upgrading of their export? This is the issue we are interested in and attempt to verify. As a matter of fact, the connotation of digital inclusive finance is to improve the inclusiveness of financial services through digital means and provide more convenient financial services to the whole society, especially the less developed areas, at a lower cost to give play to its inclusiveness. Therefore, to deepen the understanding of the relationship between digital inclusive finance and city’s export upgrading, we further investigate what kind of cities benefit more.

For this purpose, referring to the heterogeneity analysis in existing studies (Bombardini et al., Citation2017; Nunn & Qian, Citation2011; Nunn & Wantchekon, Citation2011), we discuss what kind of cities benefit more from the development of digital finance in improving export sophistication through dividing the analysis into subsamples. The reason we choose subsample estimation over analysis with interaction effects is that the former assumes systematic differences across subsamples rather than the interaction between core variables and grouped variables. Therefore, subsample analysis is more in line with our purpose of discussing city heterogeneity.

6.1.1. Heterogeneity of city size

According to existing literature and empirical facts, larger cities have greater agglomeration, which is more conducive to the development of a city’s export (Duranton & Puga, Citation2004; Wagner & Zahler, Citation2015). As shown in the China Statistical Yearbook, in 2020, the import and export of megacities such as Beijing and Shanghai are among the highest in China. In contrast, small and medium-sized cities are short in resources to promote the upgrading and transformation of export, so they need more efficient and lower-cost financial instruments, which the emergence of digital inclusive finance can tackle effectively.

However, small and medium-sized cities lag behind big cities in infrastructure, finance, human capital, and traditional financial development, thus they need inclusive finance to supplement the defects of export development. While digital inclusive finance reduces information costs and provides convenient conditions for promoting export upgrading. Based on this, classified by population in 2017, we list the top 25% of the sample cities as big cities and the remaining 75% as small and medium-sized cities. According to this classification, we investigate the impact of digital inclusive finance on the upgrading of export in cities of different size. Columns (1) and (2) of list the corresponding results, which show that the coefficient of digital inclusive finance in small and medium-sized cities is significantly positive, while it is insignificant in large cities. This illustrates that, compared with large cities, the export upgrading of small and medium-sized cities benefits more from the development of digital inclusive finance. This is mainly because the development of digital inclusive finance improves the opportunities for small and medium-sized cities to enjoy financial services by reducing the threshold and transaction costs, thereby promoting the transformation and upgrading of export in small and medium-sized cities. The results also confirm the inclusive nature of digital inclusive finance in China.

Table 5. Estimation results of city’s heterogeneity analysis.

6.1.2. Heterogeneity of a city’s wage level

The increase in wage level is due largely to the development of export (Grossman & Helpman, Citation2005), so the cities with larger export tend to have higher wages. However, with the continuous improvement of export, the wage gap may continue to expand (Han et al., Citation2012). In this regard, we need to investigate the impact of digital inclusive finance on the upgrading of export in cities with different wage levels and test whether digital finance presents inclusiveness and narrows the export gap across cities. We divide the average wage of on-the-job workers at the city level into three equal groups. The first equal group is cities with high wages, and the other two equal groups are cities with low and medium wages. Columns (3) and (4) of list the corresponding estimation results, showing that the coefficient of low and medium wage cities is 0.1232 and significant, while the coefficient of high wage cities is insignificant.

The results suggest that the development of digital inclusive finance has significantly promoted the upgrading of export in low and medium-wage cities but has no such effect in high-wage cities. From the above analysis, we can infer that the development of digital inclusive finance can alleviate the financing constraints of low and medium-wage cities, promote the upgrading of export, and narrow the gap of export development among cities of different sizes. The results further verify the inclusiveness of digital inclusive finance in China.

Through the above analysis of city heterogeneity, the hypothesis of H2 has been confirmed.

6.1.3. Heterogeneity of a city’s human Capital level

Digital financial services have certain requirements for users' digital technology and financial knowledge. The improvement of the level of human capital can effectively improve the cognitive level and learning ability, reduce the exclusion of financial services, enhance the participation of digital inclusive finance, and then promote the transformation and upgrading of the city's export. On the contrary, the relatively low level of human capital will lead to the underuse of digital inclusive finance, and then impede the full play of the role of digital inclusive finance in promoting the upgrading of a city’s export. Therefore, we use the number of college students per 10,000 people to measure the level of a city’s human capital. We divide these into three equal groups, where the first equal group is cities with high levels of human capital and the other are cities with low and medium levels of human capital. Columns (5) and (6) of list the corresponding estimation results, which shows that the coefficient of cities with high human capital level is 0.1899 and significant, while the coefficient of the counterpart is positive but insignificant. The results indicate that the development of digital inclusive finance in cities with high human capital levels has significantly promoted the upgrading of export, while we cannot detect similar effects in cities with low and medium human capital levels. Therefore, we can infer that the improvement of human capital level is helpful to give full play to the role of digital inclusive finance in promoting the upgrading of a city’s export.

6.1.4. Heterogeneity of location advantage

The development of export needs the support of good location advantage. There is no doubt that convenient port conditions can effectively promote the development and upgrading of export. On the contrary, cities without relevant advantages cannot fully enjoy the dividend of digital inclusive finance in promoting the upgrading of export. On this basis, we use and divide the spherical distance between the city and the nearest port into three equal groups. The cities in the first group are closer to the port, defined as port cities. While the cities in the remaining two groups are farther from the port, defined as non-port cities. Columns (7) and (8) of show the corresponding estimation results. The coefficient of port cities is 0.1867 and is significantly positive, showing that digital inclusive finance plays an obvious role in promoting the upgrading of export in port cities, but we observe no similar effect in non-port cities. These results show that export-related location advantage and digital inclusive finance play a complementary role in promoting the upgrading of export.

Through the above two heterogeneity analysis, hypothesis H3 is confirmed.

Given the results of the heterogeneity analysis, we can deduce that digital inclusive finance in China possesses inclusiveness. The upgrading of export in less developed cities can obtain greater benefits from the development of digital inclusive finance. However, the full play of the role of digital inclusive finance in promoting the upgrading of export requires a higher level of human capital and better export-related location advantage.

6.2. Mechanism analysis: innovation and market effects

The benchmark results show that the development of digital inclusive finance can significantly promote the upgrading of a city’s export, but the mechanism has not been verified. As explained in the theoretical analysis in this paper, the development of digital inclusive finance drives a city’s innovation and market effects, which promotes the upgrading of the city's export. In order to verify the above two mechanisms, this paper follows Baron and Kenny (Citation1986) to test the existence of innovation effect and market effect. We divide the specific empirical strategies into three steps. The first step is to test the role of digital inclusive finance in promoting the upgrading of a city’s export, which we verify above. The second step is to check the impact of digital inclusive finance on innovation effect and market effect. If the corresponding coefficient is significantly positive, we can infer that the development of digital inclusive finance has produced the above two effects. The third step is examining the impact of digital inclusive finance and the above two effects on the city's export upgrading. If the coefficients of the above two effects are significantly positive, we can deduct that they are important mechanisms for digital inclusive finance to affect the city’s export upgrading. The specific empirical models are as follows.

(4)

(4)

(5)

(5)

(6)

(6)

Among them, EquationEquation (4)(4)

(4) is the same as EquationEquation (1)

(1)

(1) , which is the first step of mechanism analysis.

in EquationEquations (5)

(5)

(5) and Equation(6)

(6)

(6) is the mediating variable. Significantly positive

in EquationEquation (5)

(5)

(5) shows that digital inclusive finance has significant impact on mediating variables, and significantly positive

in EquationEquation (6)

(6)

(6) shows that the mediating variable plays a mechanism role in the promotion of a city’s export by digital inclusive finance. Meanwhile, if the coefficient

in EquationEquation (6)

(6)

(6) is significant, the mediating variable only plays a partial mediating effect, whereas, if the coefficient is not significant, the mediating variable plays a complete mediating effect.

6.2.1. Innovation effect

By reducing transaction costs and providing wider coverage of financial services, digital inclusive finance provides support for technological innovation, which is conducive to the transformation and upgrading of export. Therefore, we investigate how the innovation effect acts as a mediating mechanism to promote the impact of digital inclusive finance on the upgrading of a city’s export. The logarithm of city’s patent application quantity per 10,000 people () is the mediating variable of a city’s innovation effect, and shows the estimation results. The coefficient of digital inclusive finance in column (1) is significantly positive, indicating that digital inclusive finance promotes a city’s innovation. Meanwhile, the coefficient of innovation effect in column (2) is significantly positive, indicating that the innovation effect plays a positive role in the process of digital inclusive finance promoting a city’s export upgrading. The coefficient of digital inclusive finance is significantly positive and less than that in the benchmark results, which indicates that the innovation effect plays a partial mediating effect in promoting a city’s export upgrading. Besides, the Sobel test result is significant, which further verifies that innovation has a certain mediating effect. Specifically, 28.16% of the effect of digital inclusive finance on a city’s export upgrading is through the improvement of innovation.

Table 6. Mechanism results of innovation effect.

To check the robustness of the mechanism analysis, we use the previous instrumental variable model. The significance of the coefficients in columns (3) and (4) are the same as the fixed effect results, which confirms the robustness of the mechanism of innovation effect. On this basis, it has proved hypothesis H4 that digital inclusive finance promotes the upgrading of a city’s export through innovation effect.

Furthermore, referring to existing methods used to study mediation mechanisms (Preacher & Hayes, Citation2008; Preacher et al., Citation2007; Tofighi & MacKinnon, Citation2011), we use the nonparametric percentile bootstrap method to analyse the mechanism of in EquationEquations (5)

(5)

(5) and Equation(6)

(6)

(6) , because the specific performance of the mediation mechanism is the significant interaction

Specifically, we get 100, 200, 500, and 1,000 bootstrap samples for EquationEquations (5)

(5)

(5) and Equation(6)

(6)

(6) , then record the parameters

and

and generate

The descriptive statistics of

are shown in .

Table 7. Bootstrap sampling mechanism results of innovation effect ().

As shown in the sampling results under different repetition times, the mechanism variable of innovation effects is significantly positive, whether they be direct or indirect effects. We can regard the data between the 5% quantile and 95% quantile as a 90% confidence interval. As shown in , 0 is not included in the 90% confidence interval, which further proves the mechanism role of innovation effects in improving export sophistication by digital inclusive finance.

6.2.2. Market effect

The development of digital inclusive finance reduces the probability of information asymmetry and transaction cost and also improves resource accessibility. This promotes circulation among markets and stimulates market potential. Meanwhile, the market effect brought by the stimulation of market potential promotes the productivity of enterprises and further promotes export (Melitz, Citation2003). Therefore, we test how market effect plays a mediating role in the process of digital inclusive finance promoting a city’s export upgrading. We refer to the research of Head and Mayer (Citation2011) to construct the market potential index as the proxy variable of a city’s market effect.

(7)

(7)

(8)

(8)

where

is the market potential index.

is the GDP of city

in year

and

is the

of city

in year

is the distance from city

to city

and

is the internal distance of city

is the land area of city

administrative region. We use the logarithm of the city’s market potential index (

) to measure the city’s market effect. shows the specific regression results.

Table 8. Mechanism test of market effect.

The coefficient of digital inclusive finance in column (1) is significantly positive, indicating that the development of digital inclusive finance has brought an obvious market effect to cities. Meanwhile, the coefficient of market effect in column (2) is also significantly positive, indicating that the market effect has played a mediating role in promoting the city's export by digital inclusive finance. However, the coefficient of digital inclusive finance in column (2) is insignificant, suggesting that the market effect plays a complete mediating mechanism role. Furthermore, the statistical significance of the Sobel test also confirms that the market effect has some certain mediating role. Specifically, 48.73% of the effect of digital inclusive finance on a city’s export upgrading is from the improvement of the market effect. Then, we use the instrumental variable model to verify the robustness of the mediating mechanism. Through the results in columns (3) and (4), we can see that the significance of the coefficient is the same as that of the fixed effect, which indicates that the mechanism of the market effect is robust. On this basis, hypothesis H5 has been proved that digital inclusive finance promotes the upgrading of a city’s export through market effect.

Furthermore, referring to the nonparametric percentile bootstrap method mentioned above, this paper analyses the mechanism of the market effect. lists the descriptive statistics of As shown from the sampling results under different repetition times, the mechanism variable of market effect is significantly positive, whether the effects are direct or indirect. Similarly, we can regard the data between the 5% quantile and 95% quantile as 90% confidence interval, and 0 is not included in this interval, further suggesting the mechanism role of the market effect in improving export sophistication by digital inclusive finance.

Table 9. Bootstrap sampling mechanism results of market effect ().

7. Conclusion

Based on the Chinese customs data and the Peking University Digital Financial Inclusion Index of China from 2013 to 2017, this paper verifies the impact of digital inclusive finance on the upgrading of a city’s export and further explores the heterogeneity across cities and the mechanisms through which digital finance influences export upgrading.

This paper finds that the development of digital finance rather than traditional finance significantly promotes the upgrading of a city’s export, and the conclusion still holds after dealing with the endogenous problem and a series of robustness tests. Therefore, the popularisation of digital finance provides new development opportunities for the promotion of a city’s export competitiveness. Furthermore, to test the inclusiveness of digital finance in improving export sophistication, this paper studies the heterogeneity of the impact of digital inclusive finance on the upgrading of export across cities. This study finds that digital inclusive finance plays a stronger role in promoting the upgrading of export in cities with smaller sizes and lower wages, indicating that digital finance has brought inclusive growth to the promotion of export competitiveness in less developed cities, that is ‘offering fuel in snowy weather’. However, digital inclusive finance has a certain ‘pickiness’ in promoting the upgrading of a city’s export. Specifically, the promotion effect is sharper in cities with high levels of human capital and port cities. This shows that although digital finance brings inclusive growth, it needs the coordination of knowledge reserve and location advantage to better promote export upgrading of less developed cities. Finally, through mechanism analysis, we confirm that digital finance can promote the upgrading of a city’s export through innovation and market effects. Digital finance can promote enterprise innovation by alleviating the financing constraints and accelerating the process of knowledge spillover, learning, and application. Through stimulating productivity and promoting competitiveness due to cost reduction, innovation is often regarded as one of the most important components of export sophistication (Atasoy, Citation2020). By reducing the degree of information asymmetry, killing geographical distance, and improving the availability of resources, digital finance can improve the participation rate of export enterprises and expand the scope of the market, further promoting the upgrading of a city’s export.

Based on the above conclusions, we put forward the following suggestions to improve China's export sophistication. First, considering the important role of digital finance in promoting the upgrading of a city’s export, it is necessary to continue strengthening digital finance development. In recent years, China has implemented many policies aimed at accelerating the construction of new infrastructures, such as the 5G network and data centre, which has laid a solid foundation for the rapid development of digital finance. However, in this process, we should note the importance of guiding digital finance to give full play to its inclusive nature.

Specifically, in the construction of new infrastructure related to digital finance, the government can give certain policy preference to small and medium-sized cities and rural areas with less developed economies and poor resource acquisition ability to narrow the ‘digital divide’ across regions. This is not only conducive to giving full play to the inclusiveness of digital finance, but it also helps narrow China's huge regional gap and urban-rural gap in the long run.

Second, while promoting the development of digital finance, it is necessary to improve the level of human capital, especially in less developed regions. Certain knowledge reserves, especially those related to digital information technology and financial knowledge, help to understand and use digital financial services to better enjoy the dividend of digital finance in promoting the upgrading of a city’s export. Therefore, the popularisation of relevant digital finance knowledge should be promoted simultaneously and harmoniously with relevant infrastructure construction. Furthermore, it is necessary to strengthen the connection between inland cities (especially small and medium-sized cities) and port cities to benefit the location advantages of port cities to cities with weak development foundations. China has always attached great importance to the construction of municipal public engineering facilities such as transportation, posts and telecommunications, and logistics. China's railway and logistics have developed rapidly and are well-known globally, but we should not underestimate the gap between developed and less developed cities. Next, the Chinese government should further improve the infrastructure construction in less developed regions and integrate small cities and rural areas into the national public transport and logistics network.

Finally, the government can encourage and protect innovation through the measures such as optimising the institutional environment and protecting intellectual property rights.

Additionally, by reducing the degree of information asymmetry and improving the liquidity of resources and factors, the widespread use of digital technology can break down the obstacles caused by market segmentation and further open up the influence channel of digital finance to promote the upgrading of a city’s export. China's digital finance development is at the forefront of the world. If China can grasp the emerging trend of a digital economy and make it better serve the export, it will undoubtedly play a positive role in promoting China’s export quality to a higher level, strengthening the high-quality development of China's economy.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

References

- Aghion, P., Fally, T., & Scarpetta, S. (2007). Credit constraints as a barrier to the entry and post-entry growth of firms. Economic Policy, 22(52), 732–779. https://doi.org/10.1111/j.1468-0327.2007.00190.x

- Anand, S., & Chhikara, K. S. (2013). A theoretical and quantitative analysis of financial. inclusion and economic growth. Management and Labour Studies, 38(1–2), 103–133. https://doi.org/10.1002/jid.1698

- Anderson, J. E., & Van Wincoop, E. (2004). Trade costs. Journal of Economic. literature, 42(3), 691–751. https://doi.org/10.1257/0022051042177649

- Assche, A. V., & Gangnes, B. (2010). Electronics production upgrading: Is China exceptional?. Applied Economics Letters, 17(5), 477–482. https://doi.org/10.1080/13504850701765101

- Atasoy, B. S. (2020). The determinants of export sophistication: Does digitalization matter?. International Journal of Finance & Economics. https://doi.org/10.1002/ijfe.2058

- Auty, R. (2009, September). The political economy of hydrocarbon revenue cycling in Trinidad and Tobago. In May, paper prepared for workshop on Myths and Realities of Commodity Dependence: Policy Challenges and Opportunities for Latin America and the Caribbean, World Bank.

- Baliamoune-Lutz, M. (2019). Trade sophistication in developing countries: Does export destination matter?. Journal of Policy Modeling, 41(1), 39–51. https://doi.org/10.1016/j.jpolmod.2018.09.003

- Baron, R. M., & Kenny, D. A. (1986). The moderator–mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. Journal of Personality and Social Psychology, 51(6), 1173–1182. [Database] https://doi.org/10.1037/0022-3514.51.6.1173

- Bas, M., & Strauss-Kahn, V. (2014). Does importing more inputs raise exports? Firm-level evidence from France. Review of World Economics, 150(2), 241–275. https://doi.org/10.1007/s10290-013-0175-0

- Battese, G. E., & Coelli, T. J. (1995). A model for technical inefficiency effects in a stochastic frontier production function for panel data. Empirical Economics, 20(2), 325–332. https://doi.org/10.1007/BF01205442

- Beck, T., Pamuk, H., Ramrattan, R., & Uras, B. R. (2018). Payment instruments, finance and development. Journal of Development Economics, 133, 162–186. https://doi.org/10.1016/j.jdeveco.2018.01.005

- Becker, B., Chen, J., & Greenberg, D. (2013). Financial development, fixed costs, and international trade. The Review of Corporate Finance Studies, 2(1), 1–28. https://doi.org/10.1093/rcfs/cfs005

- Berger, A. N. (2003). The economic effects of technological progress: evidence from the banking industry. Journal of Money, credit and Banking, 141–176.

- Berkowitz, D., Moenius, J., & Pistor, K. (2006). Trade, law, and product complexity. The Review of Economics and Statistics, 88(2), 363–373. https://doi.org/10.1162/rest.88.2.363

- Bertrand, M., Duflo, E., & Mullainathan, S. (2004). How much should we trust differences-in-differences estimates? The Quarterly Journal of Economics, 119(1), 249–275. https://doi.org/10.1162/003355304772839588

- Bin, X., & Jiangyong, L. U. (2009). Foreign direct investment, processing trade, and the sophistication of China's exports. China Economic Review, 20(3), 425–439.

- Bombardini, M., Li, B., & Wang, R. (2017). Import competition and innovation: Evidence from China. Researchpaper: http://www7.econ.hitu.ac.jp/cces/trade_conference_2017/paper/matilde_bombardini

- Branstetter, L. G., & Lardy, N. R. (2006). China’s embrace of globalization. NBER Working Paper.

- Buchak, G., Matvos, G., Piskorski, T., & Seru, A. (2018). Fintech, regulatory arbitrage, and the rise of shadow banks. Journal of Financial Economics, 130(3), 453-483. https://doi.org/10.1016/j.jfineco.2018.03.011

- Cabral, M. H., & Veiga, P. (2010). Determinants of export diversification and sophistication in Sub-Saharan Africa.

- Chan, K. C., Fung, H. G., & Thapa, S. (2007). China financial research: A review and synthesis. International Review of Economics & Finance, 16(3), 416–428. https://doi.org/10.1016/j.iref.2005.09.004

- Chaney, T. (2016). Liquidity constrained exporters. Journal of Economic Dynamics and Control, 72, 141–154. https://doi.org/10.1016/j.jedc.2016.03.010

- Chen, Y. H., Nie, P. Y., & Wen, X. W. (2015). Analysis of innovation based on financial structure. Economic Research-Ekonomska Istraživanja, 28(1), 631–640. https://doi.org/10.1080/1331677X.2015.1087327

- Chen, Y., & Puttitanun, T. (2005). Intellectual property rights and innovation in developing countries. Journal of Development Economics, 78(2), 474–493. https://doi.org/10.1016/j.jdeveco.2004.11.005

- Choi, C. (2010). The effect of the Internet on service trade. Economics Letters, 109(2), 102–104. https://doi.org/10.1016/j.econlet.2010.08.005

- Chor, D., & Manova, K. (2012). Off the cliff and back? Credit conditions and international trade during the global financial crisis. Journal of International Economics, 87(1), 117–133. https://doi.org/10.1016/j.jinteco.2011.04.001

- Ciani, A., & Bartoli, F. (2013). Export quality upgrading and credit constraints. In Annual Conference of European Trade Study Group (ETSG), 15 October).

- Clarke, G. R. (2008). Has the internet increased exports for firms from low and middle-income countries?. Information Economics and Policy, 20(1), 16–37. https://doi.org/10.1016/j.infoecopol.2007.06.006

- Costinot, A. (2009). On the origins of comparative advantage. Journal of International Economics, 77(2), 255–264. https://doi.org/10.1016/j.jinteco.2009.01.007

- Duranton, G., & Puga, D. (2004). Micro-foundations of urban agglomeration economies. In J. Scott Bentley (Ed.), Handbook of regional and urban economics (Vol. 4, pp. 2063–2117). Elsevier.

- Fang, Y., Gu, G., & Li, H. (2015). The impact of financial development on the upgrading of China’s export technical sophistication. International Economics and Economic Policy, 12(2), 257–280. https://doi.org/10.1007/s10368-014-0277-8

- Feenstra, R. C., Li, Z., & Yu, M. (2014). Exports and credit constraints under incomplete information: Theory and evidence from China. Review of Economics and Statistics, 96(4), 729–744. https://doi.org/10.1162/REST_a_00405

- Freund, C. L., & Weinhold, D. (2002). The Internet and international trade in services. American Economic Review, 92(2), 236–240.

- Freund, C. L., & Weinhold, D. (2004). The effect of the Internet on international trade. Journal of International Economics, 62(1), 171–189. https://doi.org/10.1016/S0022-1996(03)00059-X

- Fungáčová, Z., & Weill, L. (2015). Understanding financial inclusion in China. China Economic Review, 34, 196–206. https://doi.org/10.1016/j.chieco.2014.12.004

- Gabor, D., & Brooks, S. (2017). The digital revolution in financial inclusion: international development in the fintech era. New Political Economy, 22(4), 423–436.

- Goldfarb, A., & Tucker, C. (2019). Digital economics. Journal of Economic Literature, 57(1), 3–43. https://doi.org/10.1257/jel.20171452

- Golovko, E., & Valentini, G. (2011). Exploring the complementarity between innovation and export for SMEs’ growth. Journal of International Business Studies, 42(3), 362–380.

- Görg, H., & Greenaway, D. (2004). Much ado about nothing? Do domestic firms really benefit from foreign direct investment?. The World Bank Research Observer, 19(2), 171–197. https://doi.org/10.1093/wbro/lkh019

- Grossman, G. M., & Helpman, E. (2005). Outsourcing in a global economy. Review of Economic Studies, 72(1), 135–159. https://doi.org/10.1111/0034-6527.00327

- Harding, T., & Smarzynska Javorcik, B. (2009). A Touch of Sophistication: FDI and Unit values of exports.

- Han, J., Liu, R., & Zhang, J. (2012). Globalization and wage inequality: Evidence from urban China. Journal of International Economics, 87(2), 288–297. https://doi.org/10.1016/j.jinteco.2011.12.006

- Hausmann, R., Hwang, J., & Rodrik, D. (2007). What you export matters. Journal of Economic Growth, 12(1), 1–25. https://doi.org/10.1007/s10887-006-9009-4

- Hausmann, R., & Rodrik, D. (2003). Economic development as self-discovery. Journal of Development Economics, 72(2), 603–633. https://doi.org/10.1016/S0304-3878(03)00124-X

- Head, K., & Mayer, T. (2011). Gravity, market potential and economic development. Journal of Economic Geography, 11(2), 281–294. https://doi.org/10.1093/jeg/lbq037

- Holl, A. (2016). Highways and productivity in manufacturing firms. Journal of Urban Economics, 93, 131–151. https://doi.org/10.1016/j.jue.2016.04.002

- Hsu, P. H., Tian, X., & Xu, Y. (2014). Financial development and innovation: Cross-country evidence. Journal of Financial Economics, 112(1), 116–135. https://doi.org/10.1016/j.jfineco.2013.12.002

- Hur, J., Raj, M., & Riyanto, Y. E. (2006). Finance and trade: A cross-country empirical analysis on the impact of financial development and asset tangibility on international trade. World Development, 34(10), 1728–1741. https://doi.org/10.1016/j.worlddev.2006.02.003

- Hüseyni, İ. (2019). Determinants of export sophistication: An investigation for selected developed and developing countries using second-generation panel data analyses. Ekonomický časopis, 67(05), 481–503.

- Jarreau, J., & Poncet, S. (2012). Export sophistication and economic growth: Evidence from China. Journal of Development Economics, 97(2), 281–292. https://doi.org/10.1016/j.jdeveco.2011.04.001

- Ju, J., & Wei, S. J. (2011). When is quality of financial system a source of comparative advantage? Journal of International Economics, 84(2), 178–187. https://doi.org/10.1016/j.jinteco.2011.03.004

- Kletzer, K., & Bardhan, P. (1987). Credit markets and patterns of international trade. Journal of Development Economics, 27(1-2), 57–70. https://doi.org/10.1016/0304-3878(87)90006-X

- Koenig, P., Mayneris, F., & Poncet, S. (2010). Local export spillovers in France. European Economic Review, 54(4), 622–641. https://doi.org/10.1016/j.euroecorev.2009.12.001

- Leibovici, F. (2018). Financial development and international trade [FRB St. Louis Working Paper 2018–15].

- Lendle, A., Olarreaga, M., Schropp, S., & Vézina, P. L. (2016). There goes gravity: eBay and the death of distance. The Economic Journal, 126(591), 406–441. https://doi.org/10.1111/ecoj.12286

- Levchenko, A. A. (2007). Institutional quality and international trade. The Review of Economic Studies, 74(3), 791–819. https://doi.org/10.1111/j.1467-937X.2007.00435.x

- Levine, R. (2005). Finance and growth: theory and evidence. Handbook of Economic Growth, 1, 865–934.

- Li, J., Wu, Y., & Xiao, J. J. (2020). The impact of digital finance on household consumption: Evidence from China. Economic Modelling, 86, 317–326. https://doi.org/10.1016/j.econmod.2019.09.027

- Liao, G., Yao, D., & Hu, Z. (2020). The spatial effect of the efficiency of regional financial resource allocation from the perspective of internet finance: evidence from Chinese provinces. Emerging Markets Finance and Trade, 56(6), 1211–1223. https://doi.org/10.1080/1540496X.2018.1564658

- Lin, F. (2015). Estimating the effect of the Internet on international trade. The Journal of International Trade & Economic Development, 24(3), 409–428. https://doi.org/10.1080/09638199.2014.881906

- Lorente, J. C., & Schmukler, S. L. (2018). The Fintech Revolution: A threat to global banking? [World Bank Research and Policy Briefs, 125038].

- Mahdiraji, H. A., Kazimieras Zavadskas, E., Kazeminia, A., & Abbasi Kamardi, A. (2019). Marketing strategies evaluation based on big data analysis: A CLUSTERING-MCDM approach. Economic Research-Ekonomska Istraživanja, 32(1), 2882–2892. https://doi.org/10.1080/1331677X.2019.1658534

- Mallick, H. (2014). Role of technological infrastructures in exports: evidence from a cross-country analysis. International Review of Applied Economics, 28(5), 669–694. https://doi.org/10.1080/02692171.2014.907244

- Manova, K. (2013). Credit constraints, heterogeneous firms, and international trade. The Review of Economic Studies, 80(2), 711–744. https://doi.org/10.1093/restud/rds036

- Mazumdar, J. (1996). Do static gains from trade lead to medium-run growth? Journal of Political Economy, 104(6), 1328–1337. https://doi.org/10.1086/262062

- Melitz, M. J. (2003). The impact of trade on intra-industry reallocations and aggregate industry productivity. Econometrica, 71(6), 1695–1725. https://doi.org/10.1111/1468-0262.00467

- Moenninghoff, S. C., & Wieandt, A. (2013). The future of peer-to-peer finance. Schmalenbachs Zeitschrift für betriebswirtschaftliche Forschung, 65(5), 466–487.

- Nath, H. K., & Liu, L. (2017). Information and communications technology (ICT) and services trade. Information Economics and Policy, 41, 81–87. https://doi.org/10.1016/j.infoecopol.2017.06.003

- Nguyen, D. X. (2016). Trade liberalization and export sophistication in Vietnam. The Journal of International Trade & Economic Development, 25(8), 1071–1089. https://doi.org/10.1080/09638199.2016.1179778

- Nunn, N., & Qian, N. (2011). The potato's contribution to population and urbanization: Evidence from a historical experiment. The Quarterly Journal of Economics, 126(2), 593–650.

- Nunn, N., & Qian, N. (2014). US food aid and civil conflict. American Economic Review, 104(6), 1630–1666. https://doi.org/10.1257/aer.104.6.1630

- Nunn, N., & Wantchekon, L. (2011). The slave trade and the origins of mistrust in Africa. American Economic Review, 101(7), 3221–3252. https://doi.org/10.1257/aer.101.7.3221

- Odilova, S. (2018). Intelligence and export sophistication: a cross-country test. Mankind Quarterly, 58(3).

- Paravisini, D., Rappoport, V., Schnabl, P., & Wolfenzon, D. (2015). Dissecting the effect of credit supply on trade: Evidence from matched credit-export data. The Review of Economic Studies, 82(1), 333–359. https://doi.org/10.1093/restud/rdu028

- Paunov, C., & Rollo, V. (2016). Has the internet fostered inclusive innovation in the developing world?. World Development, 78, 587–609. https://doi.org/10.1016/j.worlddev.2015.10.029

- Pierrakis, Y., & Collins, L. (2013). Crowdfunding: A new innovative model of providing funding to projects and businesses. Available at SSRN 2395226. https://doi.org/10.2139/ssrn.2395226

- Preacher, K. J., & Hayes, A. F. (2008). Asymptotic and resampling strategies for assessing and comparing indirect effects in multiple mediator models. Behavior Research Methods, 40(3), 879–891.

- Preacher, K. J., Rucker, D. D., & Hayes, A. F. (2007). Addressing moderated mediation hypotheses: Theory, methods, and prescriptions. Multivariate Behavioral Research, 42(1), 185–227.

- Rehman, F. U., & Ding, Y. (2020). The nexus between outward foreign direct investment and export sophistication: new evidence from China. Applied Economics Letters, 27(5), 357–365. https://doi.org/10.1080/13504851.2019.1616056

- Ricci, L. A., & Trionfetti, F. (2012). Productivity, networks, and export performance: Evidence from a cross-country firm dataset. Review of International Economics, 20(3), 552–562. https://doi.org/10.1111/j.1467-9396.2012.01038.x

- Rodrik, D. (2006). What’s so special about China’s exports?. China & World Economy, 14(5), 1–19. https://doi.org/10.1111/j.1749-124X.2006.00038.x

- Ryan, R. M., O’Toole, C. M., & McCann, F. (2014). Does bank market power affect SME financing constraints?. Journal of Banking & Finance, 49, 495–505. https://doi.org/10.1016/j.jbankfin.2013.12.024

- Sarma, M., & Pais, J. (2011). Financial inclusion and development. Journal of International Development, 23(5), 613–628. https://doi.org/10.1002/jid.1698

- Schott, P. K. (2008). The relative sophistication of Chinese exports. Economic Policy, 23(53), 6–49.