?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study investigates the impact of four legal origins (i.e., English, French, German, and Scandinavian) of a sample of countries on the rate of surplus value and rule of law. It also examines how these factors affect the size of credit provided by banks and economic performance. We found that the rate of surplus value and rule of law affect both the size of bank credit and economic performance. Simultaneously, the rate of surplus value and the rule of law are correlated. Furthermore, the marginal effects of the rate of surplus value and the rule of law on economic performance differ by legal origin.

1. Introduction

The discussion of ‘varieties of capitalism’ reached the mainstream of political economy in the 2000s. Research on the varieties of capitalism focuses on the roles of companies, employers, and financial markets in classifying the state of capitalism in each country. Similar to Albert (Citation1993) and Hall and Soskice (Citation2001), and using the ‘régulation approach’, Amable (Citation2003) and Boyer (Citation2015) focus on the institutions of each country and the institutional complementarity and path dependency that occur between those institutions. They find that different capitalisms coexist depending on the institutional interrelationships in each country.

According to Acemoglu and Robinson (Citation2012), economic institutions determine whether a country will prosper, though politics and political institutions still determine the types of economic institutions a country has. The rule of law created by economic institutions via property rights creates economic incentives. Hence, the argument is that institutional deprivation leads to stagnation and poverty because economic growth is linked to economic and political institutions. Marxian economics also offers an institutional analysis of exploitation. However, the factors that lead to the diversity of capitalism in each country’s institutions have not been analysed thus far from the Marxian economics perspective.

Our analysis is based on the régulation approach, emphasising institutional complementarity, wage-labour relations, and financial markets. It focuses on economic institutions and institutional deprivation, highlighted in Acemoglu and Robinson (Citation2012). From an empirical perspective, we use the rate of surplus value and the rule of law variables to identify their relevance to economic performance. In this process, we also consider the origins of the four types of law.

The rate of surplus value is a concept discussed in Marxian economics, defined as the value of surplus labour divided by the value of socially necessary labour.Footnote1 The surplus labour is the value that workers produce through their labour minus the value of their socially necessary labour, the latter of which is the labour necessary for the worker to earn a living. Therefore, the rate of surplus value is also known as the exploitation rate.Footnote2

According to Silkenat et al. (Citation2014), the rule of law is rooted in the concept of removing the arbitrary will of the person in authority as much as possible. This is justified by the ethical principles of normative individualism.Footnote3 In other words, the concept is that even the king cannot transcend the law and is equal under the law.

In this study, we assume that the rate of surplus value and the strength of the rule of law depends on the origins of the legal traditions of each country. La Porta et al. (Citation1998, Citation2000, Citation2002) propose four main legal origins: English, French, German, and Scandinavian.Footnote4 Additionally, institutions within a country can differ widely depending on the type of legal origin (La Porta et al., Citation1998, Citation2000, Citation2002). These studies suggest that the legal origins of each country influence institutions related to investor and creditor protection, and these institutional differences influence the subsequent development of financial markets and ownership structures.

We consider that legal origins affect the rate of surplus value through the laws and endogenous institutions of labour, simultaneously affecting the intensity of the rule of law. Using a sample of 82 countries from 2004 to 2017 with data available, we test the hypothesis that legal origins affect the rate of surplus value and the intensity of the rule of law. Additionally, we test whether the rate of surplus value and the intensity of the rule of law influence economic performance.

First, we test the relevance of the rate of surplus value or rule of law to legal origins in a regression model with a dummy variable. Subsequently, we estimate how the rate of surplus value and the rule of law affect the size of credit provided by banks. We believe that the former can affect the size of credit provided by banks through corporate retained earnings and financing, and the latter can affect the size of credit provided by banks through the strength of property rights and jurisdiction affecting the financial system.

Second, we assess the relationship between economic performance and the rate of surplus value and between economic performance and the rule of law. We then use the dummy variable of legal origins and the rate of surplus value or legal origins and the rule of law as interaction terms. Regression analysis using the interaction term allows us to identify which legal origin leads to a high rate of surplus value and the strength of the rule of law, as well as the effect of high value and strength on GDP per capita.

2. Analytical framework

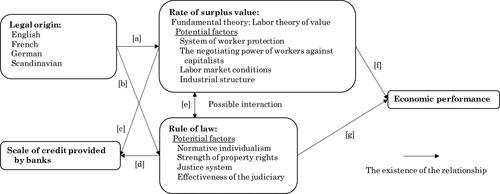

This section describes the framework of this study presented in . La Porta et al. (Citation1998, Citation2000, Citation2002) and La Porta et al. (Citation2008, Citation2013) show that the differences in legal origins generate further differences with respect to property rights, judicial systems, financial market institutions, commercial law and labour law.

Figure 1. Conceptual framework. Note: The scale of credit provided by banks is relevant to economic performance, but this is beyond the scope of this study and are thus excluded. Arrows indicate the destination of the influence. Source: Prepared by the author.

shows that legal origins affect the rate of surplus value. The concept of the rate of surplus value is grounded in the labour value theory of Marxian economics.Footnote5 We classify capital into two categories: invariant capital (e.g., equipment) and variable capital, which represents workers—the idea being that variable capital is the source of new value. We assume that a potential factor reducing the rate of surplus value is the environment surrounding workers. For instance, a system of worker protection and higher bargaining power over capitalists would reduce the rate of surplus value. Naturally, labour market conditions such as unemployment would also affect the rate of surplus value. From another perspective, we also believe that differences in industry structures affect the rate of surplus value as industries differ in terms of their labour intensiveness. If legal origins affect the system of worker protection and the bargaining power of workers over capitalists, then it is quite possible that differences in legal origins also affect the rate of surplus value.

shows that legal origins affect the rule of law. According to Zweigert and Kötz (Citation1998), the difference between whether the national courts relies upon laws following a common law or civil law principle depends on the legal origin. The rule of law is a fundamental principle of Anglo-American law in a common law-based country, where the concept of ‘law’ implies an autonomous and spontaneous norm. In a civil law country, it is called the ‘legal state’ (Rechtsstaat). During the great class conflict in Germany in the 1800s, the adoption of Roman law (Pandekten jurisprudence) aimed to implement the rule of the state by law and in accordance with the law. In France, the Napoleonic Code, enacted in the early 1800s, was the original source of the later French Civil Code.

According to Silkenat et al. (Citation2014), the rule of law and legal state have similarities and differences. These concepts share a common function in that they eliminate the dominance of arbitrary state power and binding authority via law. The rule of law formally restrains state power through autonomous and spontaneous norms. Conversely, the legal state implements a substantive rule of law that establishes objective laws and regulations, guarantees various behavioural activities, mitigates class conflict, and guarantees rights and freedoms. However, in the legal state, the state follows its own laws as enacted, and therefore, unfavourable laws can also become laws.

The rule of law index published by the Worldwide Governance Indicators reflects the degree of authorities’ compliance with social norms. In particular, it quantifies the quality of contract enforcement, property rights, police and courts and appropriate responses to crime and violence. It considers the substance of the legal environment of the rule of law and the legal state.

shows that the rate of surplus value affects the scale of credit provided by banks. A high surplus value rate simply indicates that the capitalist’s share is high. In Marxian economics, ‘capitalist’ refers to a class of people, but now business corporations serve this role. The remaining revenue after deducting the investment amount and expenses is the profit, which the company distributes to shareholders as dividends and retains the remainder. According to the pecking order hypothesis, if firms have more retained earnings when they invest, they are more likely to prioritise the use of retained earnings over bank loans.Footnote6 Thus, the rate of surplus value may affect the size of credit provided by banks.

shows that the rule of law affects the scale of credit provided by banks. The rule of law affects property rights, creditor protection, and the justice system through the ethical principle of normative individualism. According to the World Bank (Citation2017), the rule of law is a necessary element for achieving stability and equitable development. That is, if the rule of law is strong, then trust in ownership, creditor protection, and a well-structured judicial system may facilitate the supply of funds from banks. Thus, the influence of the rule of law is far reaching. Hence, as in , the rule of law may have an indirect effect on the rate of surplus value through a system of worker protection.Footnote7

shows that the rate of surplus value affects economic performance. At the rate of surplus value, work that exceeds the socially necessary level is surplus labour. Focusing on value creation for society in general, socially necessary labour indicates an equivalent exchange of labour value and wages. Therefore, socially necessary labour alone does not create additional value for companies, considering the net investment in companies. That is, under the labour value theory, surplus labour enhances economic performance via new corporate investment.Footnote8

shows the relationship between the rule of law and economic performance. According to Silkenat et al. (Citation2014), the rule of law is the strongest currently than it has ever been and this is the key to sustainable political and economic development in society. Although the rule of law personifies an abstract concept of normative individualism, it is an important concept linked to human rights, democracy building, constitutionalism and good governance. The World Bank (Citation2017) shows that the rule of law is positively associated with GDP per capita and the relationship is robust, though the mechanisms of the positive association were not stated. However, if well-structured rule of law is related to a well-structured property rights and justice system, well-structured financial market institutions and labour laws, as Silkenat et al. (Citation2014) suggest, then we consider that the strength of the rule of law can achieve high economic performance through institutional coordination.

3. Data and models

3.1. Data

In this section, we explain the data and models used in this study. lists the sample countries and their legal origins. We used the legal origins classification in La Porta et al. (Citation2008). summarises the definitions of the variables and data sources. We use the ILO’s Sustainable Development Goals indicators (2020), International Monetary Fund’s World Economic Outlook Database (2020), World Bank’s World Development Indicators (2020b), and Worldwide Governance Indicators (2020a). We refer to the Organisation for Economic Co-operation and Development (OECD) website (2020) to check whether the country was an OECD member. In addition, we use annual data from 2004 to 2017. If data for a year were unavailable and the previous year’s data existed, then we used the data for the previous period used for only one period. If data for the previous year were unavailable, then we used the data for one year later. If both the data from the previous and subsequent years were unavailable, then we regarded the present year’s data as missing.

Table 1. Target countries and legal origins.

Table 2. Definitions of variables.

The variable Surplus is the rate of surplus value, calculated by subtracting labour costs from GDP and dividing the result by labour costs.Footnote9 Varley (Citation1938), Amsden (Citation1981), Cuneo (Citation1984), and Lynch et al. (Citation1994) define the rate of surplus value as a monetary measurement as follows. They calculate the value added in manufacturing minus the worker’s wages and divide that value by the worker’s wages. We base the rate of surplus value on the monetary measurement method in these studies. In addition, we do not use the added value of manufacturing, but GDP, which is a simple method for estimating all industries.

The Rule of law variable is an indicator of the rule of law, with values ranging from −2.5 to 2.5. A higher value indicates a higher intensity of the rule of law. We use the natural logarithm of GDP per capita, denoted GDP/Capita, to measure a country’s economic performance. GDP per capita is valued in US dollars and adjusted for purchasing power parity. Legal origins has four dummy variables: English, French, German, and Scandinavian. For example, if the dummy variable is English, then countries with English legal origins have a value of 1, and the remaining countries have a value of 0. OECD is a dummy variable set to 1 if the target country is a member of the OECD. Bank is a variable that indicates the scale of credit provided by banks. This variable uses the natural logarithm of the amount of credit provided by banks divided by GDP. Unemployment is the unemployment rate, Growth is the annual growth rate of GDP, and Industry refers to the added value of manufacturing divided by GDP. The manufacturing sector includes mining, construction, power, water and gas.

presents the descriptive statistics for each variable. reports the results of the unit root tests for the dependent and main variables. We performed two types of tests on the panel data; the results confirm that these variables are stationarity.

Table 3. Descriptive statistics.

Table 4. Unit root tests of the main variables.

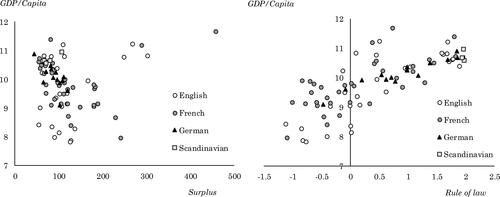

shows the relationship between GDP/Capita and Surplus and between GDP/Capita and Rule of law. In GDP/Capita, while the English and French legal origins are widely distributed, German legal origins tend to have an upper value. Furthermore, the rule of law is close to the highest level in countries with a Scandinavian legal origin.Footnote10

Figure 2. Relationship between GDP/Capita and rate of surplus value and between GDP/Capita and rule of law. Note: GDP/Capita is the natural logarithm. For the classification of legal origins, refer to La Porta et al. (Citation2008). The figure uses the arithmetic mean from 2004 to 2017 for each country. The number of observations was 82. Source: Compiled by the author.

3.2. Models

In this section, we first build a model to investigate whether the difference in legal origins leads to differences in the rate of surplus value. Simultaneously, we estimate the relationship between the amount of credit provided by banks and the rate of surplus value. The estimated regression models are

(1)

(1)

In EquationEq. (1)

(1)

(1) , Surplus refers to the rate of surplus value, and legal origin removes only the base category legal origin and adds a dummy variable for the other legal origins. Bank refers to the credit scale provided by banks.Footnote11 We use GDP/Capita, Unemployment, Growth, and Industry as Control variable 1.Footnote12 We also incorporate Year as a year dummy, where i is the country, t is the period, and ε is the error term.

Second, we build a model to investigate whether differences in legal origins affect the strength of the rule of law. Simultaneously, we estimate the relevance of the rule of law to the scale of credit provided by banks. The estimated regression models are

(2)

(2)

Here, Rule of law is an indicator of the rule of law, and Legal origins are dummy variables that indicate legal origins. Bank is the size of credit provided by banks, as in EquationEq. (1)

(1)

(1) . Control variable 2 uses GDP/Capita and Growth and adds Year, a year dummy.Footnote13 In this equation, i is the country, t is the period, and e is the error term. In EquationEqs. (1)

(1)

(1) and Equation(2)

(2)

(2) , the legal origins are dummy variables that do not change during the target period. We cannot estimate the legal origins in a fixed-effects model that completely removes the effect of time-invariant covariates. Hence, we use a pooled regression or random-effects model to estimate the models, including legal origins. In addition, the Breusch-Pagan test determines whether the model is a pooled regression model or a random-effects model. To remove endogeneity between Surplus and Rule of Law, we also estimate the model using the generalised method of moments (GMM) approach.

Finally, we investigate the impact of the rate of surplus value and the rule of law on economic performance. We analyse in detail the economic performance of countries according to their legal origin and that have high surplus value rates or high rule-of-law intensity. We conduct the analysis using the interaction term of legal origin and the rate of surplus value or the interaction term of legal origin and the variable indicating the rule of law. The estimated regression model is

(3)

(3)

In EquationEq. (3)

(3)

(3) , GDP/Capita is the natural logarithm of GDP per capita, representing economic performance. Surplus is the rate of surplus value, Legal origins is a dummy variable indicating legal origins, and Surplus × Legal origins is the interaction term of the rate of surplus value and legal origins. Rule of law indicates the intensity of the rule of law, and the Rule of law × Legal origins is the interaction term between the rule of law and legal origins. As control variables, we add OECD, Unemployment, Growth, and Year.Footnote14 Here, i is the country, t is the period and e is the error term. As this model also includes the legal origins dummy, we estimate it using a pooled regression model or random-effects model based on the outcome of the Breusch-Pagan test.

The coefficients estimated in EquationEq. (3)(3)

(3) can indicate the marginal effects for each legal origin. Comparing these marginal effects enables us to measure the effect of the rate of surplus value and the rule of law on the economic performance of countries with each type of legal origin. The results are discussed in detail in the next section.

4. Estimation results and discussion

presents the results of the estimation of EquationEq. (1)(1)

(1) . In the model using the English legal origin as the base category for the dummy variables, although the coefficient for French is not significant in both the random-effects and GMM models, the coefficients for German and Scandinavian are negative and significant. The coefficients for German and Scandinavian are negative and significant in both models with French legal origin as the base category. The Scandinavian coefficient is not significant in the random-effects model with German legal origin as the base category. However, in the GMM, the coefficient for Scandinavian is positive and significant. In any case, the rate of surplus value is higher in English and French legal origins, while German and Scandinavian legal origins tend to have lower rates of surplus value. Moreover, in the random-effects model, the coefficient for the relationship between Surplus and Bank is negative at the 1% level. However, the coefficient of Bank is not significant in the GMM. In contrast, after removing the variables of the legal origin and estimating with a fixed-effects model, the coefficient of Bank is negative and significant.

Table 5. Estimation results (EquationEq. (1)(1)

(1) ).

presents the estimated results of EquationEq. (2)(2)

(2) with the Rule of law as the dependent variable. In the model with English legal origin as the base category, the coefficient of French is negative and significant at the 1% level. In the same model, the coefficient for German is not significant, but in the GMM model, the coefficient for German is significant. The coefficient for Scandinavian is positive and significant at the 1% level. In the model with French legal origin as the base category, the coefficient for German is positive and significant at the 1% level. Similarly, the coefficient for Scandinavian is positive and significant at the 1% level. In the model with German legal origin as the base category, the Scandinavian coefficient is positive and significant at the 1% level. The overidentifying restrictions test rejects the model estimated by the GMM and the reliability of the model is weak. However, we find no results contradicting those of the random-effects model. That is, the intensity of the rule of law is the strongest in countries with a Scandinavian legal origin, followed by those with German and English legal origins. Countries with a French legal origin tends to exhibit a weak rule of law. Moreover, the coefficient for the association between the Rule of law and Bank is positive at the 1% level.

Table 6. Estimation results (EquationEq. (2)(2)

(2) ).

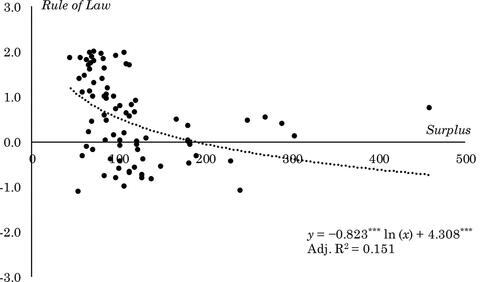

The estimation results in and also demonstrate a specific association between the rate of surplus value and the rule of law. This is because the rate of surplus value is higher, while the intensity of the rule of law is lower for English and French legal origins. Therefore, we created a scatter plot in with the Rule of law as the vertical axis and Surplus as the horizontal axis. In the scatterplot, when Surplus is the natural logarithm of the horizontal axis, we observe a decreasing function. Hence, the strength of the rule of law could reduce the increase in the rate of surplus value. The normative individualism notion of the rule of law may restrain corporate ‘exploitation’. Countries with French and English legal origins include many former colonies. Therefore, the state of corporate ‘exploitation’ from the past may have continued to the present due to path dependency.

Figure 3. Relationship between rule of law and rate of surplus value. Note: The rate of surplus value is the natural logarithm. The estimation uses the least squares method, and the figure uses the arithmetic mean from 2004 to 2017 for each country. The number of observations was 82. Source: Compiled by the author.

The size of the credit provided by banks may be positively related to both the rate of surplus value and the strength of the rule of law. In countries with a high rate of surplus value, firms may have more retained earnings and may decline funding from banks, as such funds have a higher cost of capital than retained earnings. Meanwhile, countries with a stronger rule of law may have creditor protection via property rights, and the size of credit provided by banks may be larger. In addition, the low rate of surplus value in countries with the rule of law in place indirectly implies that firms may depend on banks rather than retained earnings for funding.

presents the estimated results of EquationEq. (3)(3)

(3) . The Breusch-Pagan test favoured a random-effects model. Considering that we aim to estimate the marginal effects of the interaction term, we put the coefficients of the intersection term into perspective. The coefficient for Surplus × French was not significant in the model with English legal origin as the base category. In the same model, the coefficient for Surplus × German was negative and significant at the 1% level, but the coefficient for Surplus × Scandinavian was not significant. The coefficient for Rule of law × French was not significant, that for the Rule of law × German was not significant, and that for Rule of law × Scandinavian was negative and significant at the 5% level.

Table 7. Estimation results (EquationEq. (3)(3)

(3) ).

Next, we discuss the French legal origin as the base category. The coefficient for Surplus × German was negative and significant at the 1% level, whereas that for Surplus × Scandinavian was not significant. Although the coefficient for Rule of law × German was not significant, the coefficient for Rule of law × Scandinavian was negative and significant at the 5% level.

Finally, we discuss the model with German legal origin as the base category. The coefficient for Surplus × Scandinavian was positive and significant at the 1% level, for Rule of law × Scandinavian was negative and significant at the 5% level, and those for Surplus and Rule of law in were positive and significant at the 1% level for all models.

shows the marginal effects of the interaction term (the interaction term between the rate of surplus value and legal origins) that affect the dependent variable, GDP/Capita. The marginal effect of the rate of surplus value on GDP/Capita was negative and low for countries of German legal origin. Thus, an increase in the rate of surplus value has a negative effect on economic performance in countries that adopted German legal origin.

Table 8. Marginal effects of the interaction term on GDP/Capita (Surplus).

Similarly, shows the marginal effects of the interaction term (the interaction term between the rule of law and legal origins) that affect the dependent variable GDP/Capita. The marginal effect is positive in legal origins other than the Scandinavian legal origin. The rule of law has a positive effect on economic performance in countries with English, French, and German legal origins.

Table 9. Marginal effects of the interaction term on GDP/Capita (Rule of law).

In , we split the sample by legal origin to check for robustness and we use a GMM model that excludes the interaction term from EquationEq. (3)(3)

(3) and that removes the simultaneous determinacy of Surplus and Rule of Law and the endogeneity of the variables. The estimation by GMM was almost rejected in the overidentification restrictions test, so the model has low reliability. However, these results are consistent with the results in . That is, in countries with German legal origins, the coefficient for Surplus was negative and significant at the 1% level. Meanwhile, in countries with Scandinavian legal origins, the coefficient for Rule of law was not significant.

Table 10. GMM Model with the sample separated by legal origin.

These models suggest that the marginal effects of the rate of surplus value and the rule of law on economic performance depend on the legal origins. In other words, policies that raise the rate of surplus value in countries with German legal origins can reduce economic performance. In contrast as illustrates, the rule of law in countries with Scandinavian legal origins is high. An increase in the rate of surplus value is associated with an increase in economic performance. Indeed, the more the value of the workers' output exceeds the value of their labour, the higher the workers’ economic performance will be. However, the marginal effects of each legal origin are different, and the German legal origin has a negative impact.

5. Conclusions and implications

This study investigates how the rate of surplus value and the rule of law relate to economic performance, based on a régulation approach that emphasises institutional complementarity, wage-labour relations, and financial markets. In addition, we study the tendency for each of the four legal origin using dummy variables. We found that the rate of surplus value is high for French and English legal origins and relatively low for German and Scandinavian legal origins.

The strength of the rule of law is the highest under Scandinavian legal origins, followed by German and English legal origins. However, the strength of the rule of law is the lowest under French legal origins.

Legal origins influence both the rate of surplus value and the rule of law. Hence, we see a negative relationship between the rate of surplus value and the rule of law. That is, the strength of the rule of law shows the potential to reduce the increase in the rate of surplus value. The normative individualist notion of the rule of law may restrain corporate ‘exploitation’. In addition, the set of countries with French and English legal origins that showed a high rate of surplus value include many former colonies. The current situation of ‘exploitation’ of variable capital by corporates from the past may continue into the present via path dependency. As Acemoglu and Robinson (Citation2012) demonstrate, the rule of law, which limits the tyranny of politicians, weakens the tendency towards institutional deprivation.

Subsequently, we analysed the relationship between the rate of surplus value and the size of credit provided by banks. The former is smaller in countries with a high rate of surplus value. This phenomenon can be explained by the fact that, in countries with a high rate of surplus value, there is a larger share of added value within firms that have more retained earnings. According to the pecking order hypothesis, firms direct funds with a small capital cost for investment. In other words, countries with a high rate of surplus value have more retained earnings and are likely to invest their earnings. Consequently, firms are less likely to receive funding from banks.

Simultaneously, the size of credit provided by banks is larger in countries with a higher rule of law. We believe that the reason for this positive relevance is that the concept of the rule of law is linked to the judicial system, property rights, the institution of creditor protection, and the system of access to information, to facilitate the supply of funds to banks. In summary, the size of credit provided by banks may depend on the individual financial institution.

We investigated how the rate of surplus value and the rule of law affect economic performance, as measured by GDP per capita. In this case, we considered the impact of legal origins in each country. The model estimates for economic performance were higher in countries with German legal origins with a lower rate of surplus value. In countries that do not have German legal origins, an increase in the rate of surplus value is associated with an increase in economic performance.

The rule of law is associated with higher economic performance in countries besides those with Scandinavian legal origins, where the rule of law has always been strong. In short, the marginal effects of the rate of surplus value and the rule of law on economic performance depend on legal origins. Therefore, while the legal origin and its institutional complementarity with the rule of law are essential, the question of subsequent capital investment and profit-sharing of the firms’ larger share of surplus value will be an important focus of future debate.

The implications of this study are as follows. As each country’s situation differs according to its legal origins, policies should consider and apply the legal origins and legal environment, as well as endogenous institutions in each country. That is, blindly applying best practices from other countries to one’s own country may create not only institutional discrepancies and reduce economic performance but also discrepancies in the environment surrounding workers.

This study has several limitations. For instance, it is unclear which legal doctrine at each legal origin affects the rate of surplus value and the rule of law. That is, due to the absence of a detailed theoretical model, we were able to conduct an empirical analysis within only a larger macroscopic framework. Therefore, future research must establish a detailed theoretical model.

Acknowledgments

I express my deepest gratitude to Professor Keiji Abe, Takasaki City University of Economics, for the comments provided at the conference of the Japan Financial Management Association. I thank the two anonymous reviewers for their useful comments. I would also like to thank Editage (www.editage.com) for English language editing. Special thanks to Makiko and Akari, my family, who supported me throughout.

Disclosure statement

There are no relevant financial or non-financial competing interests to declare.

Data availability

This study uses publicly available data from the OECD, ILO, World Bank, and IMF.

Notes

1 According to Chavance (Citation2007), the school of régulation retains the tradition of Marxian economics in its emphasis on commodity producers' market relations and the relationship between capital and labour. However, the régulation approach is very different from Marxian economics; it rejects the tendential decline of profit and does not regard the institutional stages of continuous capital accumulation as inevitable. The régulation approach emphasises institutional ‘coordination’ (institutional complementarity) and the wage-labour relationship. On the other hand, mainstream economics essentially emphasises both labour and capital investment in the production relationship. Therefore, it is not easy to analyse the distributional relationship between firms and workers purely in terms of the labour share or profit rate. To analyse the wage-labour relationship in this study, we use the rate of surplus value, which represents the percentage of workers and the share of companies. We believe that this fusion of the various schools of thought will offer new perspectives in this area of study.

2 The exploitation rate here simply indicates the ratio of the share between the employer and the employee. It does not include negative implications.

3 The rule of law prioritises a system of precedent where the courts produce precedents from unwritten rules and customs, whereas the legal state (Rechtsstaat) prioritises congressional statutes. However, Silkenat et al. (Citation2014) discuss the intrinsic link between the rule of law and the legal state to the protection of human dignity and democracy.

4 English legal origins are classified as common law, while French, German and Scandinavian legal origins are classified as civil law (continental law). The French legal origin, based on civil law, originates from the Napoleonic Code, whereas the German legal origin has its roots in Roman law. Although the Scandinavian legal origin is generally described as Scandinavian civil law, its form does not belong to either the Anglo-American or continental legal tradition. While based on civil law, it also lacks a case law system. Zweigert and Kötz (Citation1998) recognise the uniqueness of the Scandinavian legal origin.

5 David Ricardo provided the origin of the theory of labour. Additionally, Acemoglu and Robinson (Citation2012) stated that the institutional structure of political deprivation and exploitation influences economic institutions. Therefore, we can also consider the rate of surplus value as a surrogate variable for depriving institutions.

6 Myers and Majluf (Citation1984) proposed the pecking order hypothesis based on the empirical observation that firms finance using the source with the lowest cost of capital. Firms first use retained earnings, which have low transaction costs, and then finance the shortfall by debt such as bank loans and then by issuing bonds, which have higher capital costs. The last method is to issue shares, which has the highest issuance costs.

7 In this regard, it is not clear whether endogenous institutions, as expressed in the rate of surplus value, affect the legal environment or whether the legal environment, based on the rule of law, affects the rate of surplus value.

8 However, although we do not address it here, we feel that the issue of distribution in the value of surplus labour is a concern because a high rate of surplus value implies a high rate of exploitation on the part of firms in the modern era.

9 The original definition of the rate of surplus value is the value obtained by dividing surplus labour by socially necessary labour. However, the unit of socially necessary labour is time, and, therefore, it is unobservable. Although ‘value’ and ‘price’ have different definitions, we use observable labour costs as a surrogate for socially necessary labour. Thus, we define this surrogate variable for the rate of surplus value, measured in terms of price rather than value, as a monetary measure.

10 The regression analysis estimated in the following model controls for the differences in income levels and different stages of economic growth in each country.

11 If the ratio of surplus value is high, the capitalist’s share will be higher. If that money goes to the firm’s retained earnings, the firm’s demand for financing will be less. Thus, the rate of surplus value and the scale of credit provided by banks may be negatively related.

12 As explained in Section 2, we add to the regression model to control for factors that are thought to affect the labour market. The variable of economic performance, GDP/Capita, and the variable of unemployment rate, Unemployment, are considered to directly affect the labour environment. Further, the variable of economic growth rate, Growth, which indicates the stage of development of the economy and the variable of Industry, which indicates the industrial structure, are economic factors affecting the labour environment.

13 We include GDP/Capita and Growth in the regression model to remove other factors that affect the rule of law. High economic performance may lead to the development of normative individualism and high strength of the rule of law. Conversely, a well-formed rule of law may lead to high economic performance. In addition, the strength of the rule of law is likely to be higher at higher stages of economic development.

14 In Eqs. (1) and (2), we add GDP/Capita to the regression model as a control variable for economic performance to control for the characteristics of developed countries. However, as the dependent variable in Eq. (3) is GDP/Capita, we add the OECD dummy variable as a secondary control for the characteristics of developed countries.

References

- Acemoglu, D., & Robinson, J. A. (2012). Why nations fail: The origins of power, prosperity, and poverty. Crown Publishing.

- Albert, M. (1993). Capitalism vs. capitalism: How America’s obsession with individual achievement and short-term profit has led it to the brink of collapse. Four Walls Eight Windows.

- Amable, B. (2003). The diversity of modern capitalism. Oxford University Press.

- Amsden, A. H. (1981). An international comparison of the rate of surplus value in manufacturing industry. Cambridge Journal of Economics, 5(3), 229–249. https://doi.org/10.1093/oxfordjournals.cje.a035483

- Boyer, R. (2015). Économie politique des capitalisms: Théorie de la régulation des crises. [Political economy of capitalisms: Theory of regulation and crises]. La Découverte.

- Chavance, B. (2007). L'économie institutionnelle. [Institutional Economics]. La Découverte.

- Cuneo, C. J. (1984). Reconfirming Karl Marx’s rate of surplus value. Canadian Review of Sociology/Revue Canadienne de Sociologie, 21(1), 98–104. https://doi.org/10.1111/j.1755-618X.1984.tb01286.x

- Hall, P. A., & Soskice, D. (2001). Varieties of capitalism: Institutional foundation of comparative advantage. Oxford University Press.

- International Labour Organization (ILO). (2020). Labour statistics for the sustainable development goals (SDGs). https://ilostat.ilo.org/topics/sdg/

- International Monetary Fund (IMF). (2020, April). World economic outlook database. https://www.imf.org/en/Publications/WEO/weo-database/2020/April

- La Porta, R. L., Lopez-de-Silanes, F., & Shleifer, A. (2008). The economic consequences of legal origins. Journal of Economic Literature, 46(2), 285–332. https://doi.org/10.1257/jel.46.2.285

- La Porta, R. L., Lopez-de-Silanes, F., & Shleifer, A. (2013). Law and finance after a decade of research. In G. M. Constantinides, M. Harris, & R. M. Stulz (Eds.), Handbook of the economics of finance (pp. 425–491). Elsevier.

- La Porta, R. L., Lopez-de-Silanes, F., Shleifer, A., & Vishny, R. (1998). Law and finance. Journal of Political Economy, 106(6), 1113–1155. https://doi.org/10.1086/250042

- La Porta, R. L., Lopez-de-Silanes, F., Shleifer, A., & Vishny, R. (2000). Investor protection and corporate governance. Journal of Financial Economics, 58(1–2), 3–27. https://doi.org/10.1016/S0304-405X(00)00065-9

- La Porta, R. L., Lopez-de-Silanes, F., Shleifer, A., & Vishny, R. (2002). Investor protection and corporate valuation. The Journal of Finance, 57(3), 1147–1170. https://doi.org/10.1111/1540-6261.00457

- Lynch, M. J., Groves, W. B., & Lizotte, A. (1994). The rate of surplus value and crime. A theoretical and empirical examination of Marxian economic theory and criminology. Crime, Law and Social Change, 21(1), 15–48. https://doi.org/10.1007/BF01307806

- Myers, S. C., & Majluf, N. S. (1984). Corporate financing and investment decisions when firms have information that investors do not have. Journal of Financial Economics, 13(2), 187–221. https://doi.org/10.1016/0304-405X(84)90023-0

- OECD. (2020). Member countries. http://www.oecd.org/about/members-and-partners/

- Silkenat, J. R., Hickey, J. E., & Barenboĭm, P. (Eds.). (2014). The legal doctrines of the rule of law and the legal state (Rechtsstaat) (Vol. 38, pp. 3–90). Springer.

- Varley, D. (1938). On the computation of the rate of surplus value. Science & Society, 2(3), 393–396.

- World Bank. (2017). World development report: Governance and law. World Bank Group.

- World Bank. (2020a). The Worldwide Governance Indicators (WGI) Project. http://info.worldbank.org/governance/wgi/

- World Bank. (2020b). World Development Indicators. https://data.worldbank.org/indicator.

- Zweigert, K., & Kötz, H. (1998). An introduction to comparative law (3rd ed.). Oxford University Press.