?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Corporate social responsibility (CSR) reports are important carriers of enterprises non-financial information disclosure, which are inextricably related to the production efficiency and performance of enterprises. The objective of this paper is discovering the causal effect of the CSR mandatory disclosure policy and the total factor productivity (TFP) of enterprises. This paper uses the sharp regression discontinuity design based on the micro data of the enterprises to study the impact by taking China's mandatory disclosure policy in 2008 as a quasi-natural experiment. This paper makes some contribution to the impact of mandatory CSR disclosure on enterprise TFP and the mechanism and heterogeneity of this impact. The research draws the following conclusions: First, the CSR mandatory disclosure can significantly improve the TFP of enterprises on the whole, and this effect has the characteristics of long-term and dynamic decline. Second, the mechanism of mandatory disclosure of CSR on TFP is through the mediating effect of R&D and innovation expenditures. Third, the heterogeneity of the impact of CSR mandatory disclosure on TFP is reflected in two aspects: industry and equity nature differences. These conclusions are strongly correlated with the contingent decision-making behaviour of enterprises and give some ideas to the policy makers.

1. Introduction

CSR reports are important carriers of enterprises non-financial information disclosure, and their impact on the behavior of enterprises has aroused a lot of discussion. Enterprises compile CSR reports by summarizing their concept, strategy, ways and methods to fulfill their social responsibility, as well as information like the direct and indirect impact, achievements and shortcomings caused by their business activities. Any information disclosure may have impacts on the production and operation of enterprises (Jinglin et al., Citation2021; Mayorova, Citation2019; Sedláček & Popelková, Citation2020). Many scholars have studied the impact of CSR on the economic benefits of enterprises, including the market value, stock price and debts (Xu, Albitar, & Li et al., Citation2020; Ji et al., Citation2019; Okafor et al., Citation2021). The core goal of almost all enterprises is to improve productivity, and the TFP, which is closely related to the information disclosed in CSR report (Uras, Citation2014), has a comprehensive function of measuring the technology upgrading, management mode improvement, product quality improvement and structure upgrading of enterprises. Therefore, it is necessary to study the impact of CSR report disclosure on the total factor productivity of enterprises.

As a developing country, China is transforming from high-speed development to high-quality development and has implemented a series of environmental policies, with particular emphasis on the popularization of environmental awareness and the implementation of environmental protection measures (Sial et al., Citation2018). Due to different development stages, China did not make mandatory requirements on CSR disclosure in 2007, that is, it implemented voluntary disclosure. Accordingly, before 2007, less than 3% of China's listed companies disclosed CSR reports. In order to reduce the opportunities of hidden environmental pollution by enterprises, as well as to decrease the cost of government regulation, Shanghai Stock Exchange (SSE) issued the SSE Environmental Disclosure Guideline of Listed Companies in May 2008, stipulating that SSE listed enterprises must report environmental information in the form of temporary public announcement, serious polluting enterprises recognized by the environmental protection department must disclose certain scopes of information. It also clarifies the procedural requirements on environmental information disclosure. On December 31, 2008, the Shanghai Stock Exchange issued the “Notice on Doing a Good Job in the 2008 Annual Report of Listed Companies”, requiring three types of companies, namely sample companies of the "SSE Corporate Governance Sector", companies issuing overseas listed foreign shares and financial companies, to disclose their social responsibility reports, and encouraging other qualified companies to voluntarily disclose their social responsibility reports and social contribution value per share.

This paper focuses on the impact of CSR mandatory disclosure on corporate TFP with the purpose of observing if the policy is effective and what enterprises will do to achieve the standard of policy and therefore is addressed to the policy makers. The specific marginal contributions are as follows: First, we use regression discontinuity design to evaluate the impact of CSR mandatory disclosure on corporate TFP. This empirical study shows that CSR mandatory disclosure can significantly improve the TFP of enterprises as a whole, which has the characteristics of long-term and dynamic decline. From the analysis of corporate behaviour characteristics, the CSR mandatory disclosure increases the cost of enterprises in R&D expenditure, but on the other hand improves the technical level and reputation of enterprises, thus promoting the growth of TFP. Based on this, through CSR mandatory disclosure, enterprises can achieve a certain degree of coordination between social responsibility and economic effect. The TFP dynamic decline feature reveals that the promotion of TFP has a certain limit, so CSR mandatory disclosure can reduce the output gap of enterprises. Second, the impact mechanism of CSR mandatory disclosure on TFP is through the intermediary effect of R&D innovation expenditure. The mandatory disclosure of CSR will bring some costs to enterprises, but it can not only enhance the reputation of enterprises, but also realize their economic effects in the medium and long term by achieving their sustainable development strategies through R&D and innovation expenditure. Therefore, the path of CSR mandatory disclosure to improve TFP is realized through R&D innovation expenditure. Third, the heterogeneity of the impact of CSR mandatory disclosure on TFP is reflected in the differences of industry and ownership nature, and this heterogeneity reveals the contingent decision-making behaviour of enterprises. Enterprises have different decision-making motivations due to their own attributes. Industrial enterprises are more sensitive to the impact of CSR, especially environmental responsibility, and their R&D and innovation expenditure have more significant effects on their environment and profits, so the mandatory disclosure of CSR has a stronger impact on the TFP of industrial enterprises. For Chinese enterprises, the goal and purpose of state-owned enterprises is to achieve the coordination of economic interests and social responsibility. Therefore, the mandatory disclosure of CSR can enhance the TFP of state-owned enterprises more obviously.

The rest of this paper is arranged as follows: The second part the review of literature. The third part is the research methodology, which describes the basic hypothesis, model setting of regression discontinuity design, data and core variable measurement. The forth part is the empirical analysis. Through parameter estimation, we get the impact of CSR mandatory disclosure on corporate TFP and its mechanism. The fifth part is the robustness test. In this paper, the robustness of the empirical results is tested from perspectives like the bandwidth, the discontinuity and algorithm selection. The sixth part is the heterogeneity analysis of the impact of CSR mandatory disclosure on TFP. The seventh part is the discussion about the results obtained. The eighth part draws the basic conclusion and provide further research recommendations.

2. Review of the literature

With the deepening of the concept of sustainable development, a lot of countries begin to pay more attention to the release of environmental information and green policies (Utomo et al., Citation2020), and the academia also pays increasing attention to the impact of green policies on corporate performance. Xu and Li (Citation2020) and Yuming et al. (Citation2020) have found that green credit policy significantly improves the financing convenience of green listed companies, and Simin et al. (Citation2021) further discovers that green credit has welfare effects on the society. Anzolin and Lebdioui (Citation2021) believe that green industrial policy has three dimensions: the consumption-centered dimension, the firm-level sustainability dimension, and the production innovation-driven dimension. This obviously has a positive effect on the green development of enterprises. Chen et al. (Citation2020) alternatively think that green industrial policies with dual objectives are effective ways to encourage the development of heavy polluting enterprises in a more balanced and sustainable manner. Both types of above-mentioned policies have been proven to be effective in pollution control, but they have not been linked to the other behaviours such as economic performance of enterprises.

Since CSR has attracted great attention, a large number of scholars have studied the role of CSR reports from various aspects. On the macro level, CSR has a positive impact on both inclusive finance and financial stability (Muhammad et al., Citation2021; Tuzcuoglu, Citation2020), and it can improve social welfare (Miller, Eden, & Li et al., Citation2020; Zhang, Cao, Zhang, Liu, & Li et al., Citation2020). In terms of business operation, Chen et al. (Citation2021) have proved that CSR can improve the profit of manufacturers for the real economy, and meanwhile, Manzoor et al. (Citation2019) and Muhammad et al. (Citation2021) believe it can improve the financial performance. In terms of investment and financing, Ubeda-Garcia et al. (Citation2021) have proved that CSR can improve the financing performance of enterprises by improving productivity and Bousselmi et al. (Citation2019) point that it can significantly improve the efficiency of enterprises' foreign investment. As for the enterprise value, CSR reports reveal a number of important non-financial information, so they reduce the chances for enterprises to shelter evil people and practices (Nguyen, Citation2020). Depending on whether enterprises adopt environmental regulations or not, and what kind of risk they face, CSR reports would have different effects on firm value (Li et al., Citation2020; Lu et al., Citation2021). In general, CSR reports have positive effects on all aspects of enterprises, but whether these positive effects can be turned into improvement of total factor productivity is remained to be studied.

According to the research methods, the above-mentioned literature can be divided into two categories: one is the evaluation literature based on double difference model. This kind of research well avoids the problem of endogeneity. Bamezai (Citation1995) points out that the setting is very scientific, and the basic principle is easy to understand, but the application is very flexible, so the requirement for data quality is high, based on a series of assumptions. The second category is based on sample grouping to observe the applicability and mechanism of the research object. The grouping methods are mainly as follows: the nature of equity (Zhang & Vigne, Citation2021), the size of enterprises (Yuming et al., Citation2020), the nature of pollution (Xu & Li, Citation2020), and so on. Compared with general policy evaluation method, this paper adopts the sharp regression discontinuity design, which has the following advantages: first, all the samples are accurately included, avoiding the error caused by missing data; second, it can effectively use the realistic constraints to analyze the causal relationship between variables.

3. Research methodology

3.1. Research hypotheses

The first objective of this research is to observe the relationship between the policy implementation of CSR mandatory disclosure and the TFP of enterprises. CSR mandatory disclosure can promote the full disclosure of enterprise information, thus effectively realize the coordination of stakeholders (Clarkson, Citation1995), promoting the TFP. Theoretically, from the perspective of labour factors, such as caring for employees, training and organizing employees to do volunteer service, can enhance the cohesion of employees, reserve the company's talents, cultivate employees' sense of responsibility, and ultimately improve the human value of the company; from the perspective of capital and technical factors, the adoption of new technology and the development of environmentally friendly products are the driving forces to maintain continuous innovation of products and technologies(Hong et al., Citation2020); from the perspective of output, through initiatives such as fostering emerging markets and cause marketing, enterprises can expand the market scale and improve profits and performance. Based on the above analysis, the following hypothesis is proposed:

H1: The CSR mandatory disclosure can significantly improve enterprise TFP.

The second objective of this research is to discover the mechanism of how CSR mandatory disclosure cause impact on the TFP of enterprises. After mandatory disclosure of CSR reports, in order to meet relevant disclosure requirements, enterprises will make adjustment decisions based on their own pursuit of economic benefits, so as to achieve the balance of interests of stakeholders. The green R&D and innovation expenditures of enterprises can on the one hand fulfill their environmental responsibilities, on the other hand promote the technological improvement of enterprises and realize their sustainable development strategy. Therefore, enterprises tend to invest in green R&D and innovation to fulfill CSR, so as to achieve the balance of interests of all stakeholders as well as meet the requirements of CSR mandatory disclosure. In this context, this paper puts forward the following hypothesis:

H2: The CSR mandatory disclosure enhances enterprise TFP through the mediating effect of R&D and innovation input.

The third objective of this research is to discover the heterogeneity of the impact we observed at the first step. Faced with the CSR mandatory disclosure policy, enterprises will make decisions based on their own attributes, external characteristics and profit optimization. Therefore, the impact of CSR mandatory disclosure on enterprise TFP is heterogeneous. Enterprises in different industries have different costs and benefits in fulfilling their CSR. For example, industrial enterprises have relatively large input costs, but they can generate relatively long-term benefits after the investment of green technology innovation. Therefore, it is beneficial for industrial enterprises to consider the implementation of CSR strategically. Enterprises in the service industry has a relatively low technology intensity and the cost of CSR fulfilment is relatively low, so the significant degree of TFP enhancement in the process of CSR fulfilment is relatively low. At the same time, the behaviour pattern of enterprises will also be affected by the nature of equity. Different nature of enterprise equity results in different stakeholders as well as different interest demands of all parties. For example, shareholders of state-owned enterprises emphasize more on strategic development and CSR, and mandatory disclosure of CSR has a more significant impact on their TFP. However, non-state-owned enterprises focus more on the maximization of economic benefits, so that to some extent, shareholders will make contingent decisions on all dimensions of CSR mandatory disclosure to maximize their economic value. Based on this, this paper puts forward the following hypothesis:

H3: Heterogeneity exists in the impact of CSR mandatory disclosure on enterprise TFP due to industry and equity differences.

3.2. Model specification

Regression discontinuity (RD) is second only to random experiment, which can effectively use real constraints to analyze the causal relationship between variables (Hahn et al., Citation2001). In this paper, every enterprise has a score of TFP, and the CSR mandatory disclosure policy implemented by Shanghai Stock Exchange in 2008 which can be regarded as a quasi-natural experiment will generate discontinuity to the enterprise TFP. Samples selected in this paper are companies that strictly responded to the policy but did not disclose CSR reports before 2008. The discontinuous change can be used to learn about the local causal effect of the policy, because enterprises with scores barely below the cutoff before 2008 can be used as counterfactuals for enterprises with scores barely above it after 2008. Therefore, this paper uses the sharp regression discontinuity models (1) and (2) to test hypothesis 1:

(1)

(1)

(2)

(2)

In functions (1) and (2), TFP refers to the total factor productivity of company i; Year represents the year; c indicates that discontinuity begins in 2008 when mandatory disclosure policy is implemented; PLi is the processing variable: when company i is affected by the policy and discloses CSR report, it takes 1, otherwise it takes 0. Size represents the size of the company; CLD is the logarithm of capital-labour density, FA refers to the fixed asset ratio; Age is the age of the company; Lever is the capital structure; yr is the fixed variable of the year, and id is the fixed variable of the industry.

3.3. Data

3.3.1. Samples

This paper selects Chinese A-share listed companies that were forced to disclose their CSR in 2008 as the initial research samples. In order to implement the regression discontinuity design and take into account the availability of data, this paper only considers the data of the samples affected by the policy 4 years before and after the policy implementation, that is, the annual data of sample listed companies from 2004 to 2012. Besides, due to the performance loss of enterprises, their TFP and operation will change significantly, so that their decision-making behaviourss when facing the policy implementation cannot fully reflect those of normal operation. Therefore, this paper follows the standard practice and excludes the enterprises that have been ST/ST* during the research period from January 2004 to December 2012.

In addition, the target of CSR compulsory disclosure policy includes financial enterprises. Besides their own CSR performance, financial enterprises also involve the support for green projects of non-financial enterprises, which to a certain extent reflects the correlation between the society as a whole. Therefore, the samples of financial enterprises are included in this paper. The time period of the annual data in this paper starts from 2004, thus companies listed after January 1, 2004 are excluded. After the above sample processing, the sample size of this empirical study is 239. Since the policy was issued on December 31, 2008, the CSR disclosure of the company in 2008 was subject to the policy disclosure, while the total factor productivity of the enterprise in 2008 was not affected by the policy; on the other hand, some companies may feel the policy direction and have made corresponding changes in advance, so the data in 2008 are not stable, and 1912 annual data are obtained after elimination. The financial data and social responsibility data of this paper are from the CSMAR database and the China Research Data Service Platform (CNRDS).

3.3.2. Control variables

For the control variables, referring to Feng et al. (Citation2020), this paper mainly considers the internal characteristics of enterprises: (1) The enterprise scale, expressed by the logarithm of total assets. Small companies usually have less motivation for reform and less advantages in technological innovation, while large companies have more advantages in technological innovation and productivity improvement (Cowen et al., 1987; Cormier et al., Citation2005) thus causing impact on the explained variable. (2) The capital labour density, which is expressed by the ratio of the net value of fixed assets to the total number of employees. In the same industry, productivity factors (such as capital and labour) and their weights have a great impact on productivity changes. (3) The fixed assets ratio, which is the ratio of net fixed assets to total assets. The smaller the ratio is, the more liquid the company is, which is a good sign of company operation. (4) The company age. In this paper, the age of a company is expressed by the difference between the study year and the year the company was founded. According to enterprise life cycle theory, the characteristics such as productivity of enterprises are different when they are under different life stages. (5) The capital structure, namely the leverage ratio. The higher the debt ratio is, the greater the debt risk the enterprise bears, which may limit the productivity of the enterprise to a certain extent (Gray, Javad, Power, & Sinclair, 2001).

3.3.3. Measurement of the explained variables

Referring to Luasa et al. (Citation2018), this paper uses the Bootstrap-DEA model based on the Global Malmquist (GM) index proposed by Pastor and Lovell (Citation2005). The Data envelopment analysis was proposed by Charnes et al. (Citation1978) to evaluate the relative efficiency of a group of decision-making units with multiple inputs and outputs. Each company is regarded as an investment-decision-making unit (Demirtaş & Keçeci, Citation2020), with total assets and labour as input indicators, main business income and earnings per share as expected output, based on which, we use the Bootstrap method proposed by Kneip et al. (Citation2008) to sample several times and get the final TFP. The input-output indicators are shown as .

3.3.4. Descriptive statistics

In order to connect the distribution characteristics of variables as a whole, descriptive statistics are made for each variable according to the distribution before policy implementation (before treatment) and after policy implementation (after treatment). With 2008 as the processing discontinuity, before processing, the data of companies are from 2004 to 2007, and after processing, the data of companies are from 2009 to 2012. Considering the differences of variables of different industries and different equity rights, descriptive statistics are also made for the corresponding groups, so the sub-samples include enterprises of industry, construction industry, service industry, state-owned and non-state-owned. According to the sample division, the number of industrial enterprises is about twice that of the other two enterprises, and the number of state-owned enterprises (SOEs) is about three times that of non-state-owned enterprises (non-SOEs). The descriptive statistics of related variables before and after treatment are shown in .

Table 2. Descriptive statistics of variable.

As can be seen from the descriptive statistics in , TFP changes significantly before and after the implementation of the CSR mandatory disclosure policy, and heterogeneity is observed in enterprises of different industries and equity rights. From the perspective of TFP, on the whole, the mean TFP of enterprises before 2008 is 1.002, and after 2008, it is 1.027, significantly increased by 0.025. In terms of different industries, the mean TFP of industrial enterprises significantly increased by 0.02, that of construction enterprises decreased by 0.02, and that service enterprises increased by 0.03. In terms of the nature of equity rights, the mean TFP of state-owned enterprises significantly increased by 0.02, while that of non-state-owned enterprises increased by 0.04. These indicate that TFP has changed significantly after the implementation of CSR mandatory disclosure. As for other control variables, from the horizontal perspective of company size and fixed asset ratio, the mean values of all kinds of enterprises are similar. The capital labour density of construction industry is the highest, but that of state-owned enterprises is the lowest. At the same time, the age of construction industry companies is also the smallest, and the leverage ratio of capital structure is the highest. Therefore, there is no significant change of control variables after CSR mandatory disclosure.

4. Empirical analysis of the impact of mandatory disclosure on TFP

4.1. Analysis of regression results

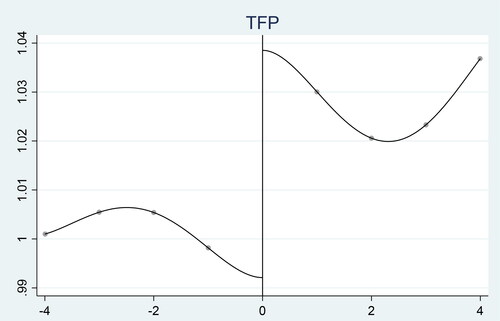

There are differences between RD estimation and benchmark regression in dealing with natural experiments. On the one hand, RD estimation does not require endogenous variables; on the other hand, RD design is closer to randomized controlled experiment (Lee & Lemieux, Citation2010). Before RD estimation, we need to examine whether mandatory CSR will cause significant changes in TFP. First, the years of variables are standardized, that is, the policy implementation year 2008 is subtracted from each year to investigate whether the TFP of enterprises has discontinuous changes at the breakpoint (Calonico et al., Citation2015). The results are shown in .

Figure 1. Regression discontinuity estimation.

Source: Authors.

As can be seen from , before and after the implementation of the CSR mandatory disclosure policy, the TFP of enterprises has changed significantly, showing a jump fluctuation. TFP of enterprises had an upward jump in 2008, from 0.99 to 1.04. The trend of TFP after 2008 was significantly higher than that before 2008, indicating that the CSR mandatory disclosure policy is an important factor leading to the change of TFP of enterprises, which proved that the RD method is suitable for the study. In the regression, local polynomials need to be set. In this paper, by setting an appropriate local polynomial and then carrying out parameter estimation, we obtain the specific baseline regression estimation and RD estimation results, as shown in .

Table 3. Sharp RD estimation using local polynomial.

As can be seen from , the impact results obtained by different methods are opposite, but there is no difference in significance. Column (1) is the result obtained by using baseline regression; Column (2) is the parameter estimation result obtained by RD. Column (1) shows that the coefficient of PL is significant under the condition of 5%, but it is −0.0774, indicating a negative influence. Column (2) shows The RD estimation result, which is significant under the condition of 1% and is 0.0403, indicating a positive effect. By comparing the two methods, it is found that the estimation results by using the baseline regression parameters are not significant, indicating that the information provided by the data captured by the model is insufficient. The RD estimation results are significant, so RD regression can capture most of the information provided by relevant data. Therefore, RD regression model should be selected. From the parameter estimation results of RD regression model, it can be seen that the CSR mandatory disclosure policy has a significant promoting effect on TFP of enterprises. After the implementation of the policy in 2008, the total factor productivity of enterprises has been significantly improved.

4.2. Mechanism analysis

Mandatory disclosure of CSR has a significant positive effect on TFP, but the mechanism may have multi-path characteristics. According to the analysis of various dimensions of CSR and the stakeholder theory, enterprises can improve their reputation by performing employee protection(Fang et al., Citation2021;Hooghiemstra, 2000), and then obtain corporate brand effect, so as to enhance their goodwill value; enterprises can improve the role of technological innovation in the whole process by investing in green technological innovation (Su & Yu, Citation2019), which can on the one hand promote the sustainable development of enterprises, on the other hand, fulfill their CSR. Through a number of experimental comparison and theoretical analysis of research hypotheses, this paper finds that mandatory disclosure of CSR improves TFP through the path of R&D innovation expenditure. Based on this, this paper uses the mediating effect to test the impact of R&D expenditure ratio on TFP. The basic form of the model is as follows:

(3)

(3)

(4)

(4)

(5)

(5)

In formula (3) ∼ (5), RDSR represents the R&D expenditure ratio of an enterprise, which is measured by the ratio of R&D expenditure to main business income. In this paper, the regression coefficients are tested step by step. The meaning and the calculation method of other variables are consistent with the RD model. β1 measures the impact of mandatory disclosure policy on the TFP; β2 measures the impact of mandatory disclosure policy on RDSR; β3 measures the direct impact of mandatory disclosure policy on the TFP of enterprises, and β4 measures the impact of R&D expenditure ratio on the TFP. The results of parameter estimation are shown in .

Table 4. RDSR mediating effect test results.

It can be seen from that the impact mechanism of mandatory disclosure of CSR on TFP is realized through the mediating effect of R&D and innovation expenditure. Column (1) verifies the direct impact of CSR mandatory disclosure on enterprise TFP; Column (2) verifies the impact of CSR mandatory disclosure on the R&D expenditure ratio of enterprises. The regression coefficient is 0.00613 and significantly positive, which means that CSR mandatory disclosure does lead to an increase in the R&D expenditure ratio; In the third column, the impact coefficients of CSR mandatory disclosure on TFP and R&D expenditure ratio are significantly positive, which means that the R&D expenditure of enterprises partially plays a mediating effect in the impact of CSR mandatory disclosure on TFP. The empirical results indicate that the impact of CSR mandatory disclosure on enterprise TFP is realized to some extent by increasing the R&D investment. Meanwhile, Sobel test is used to verify that the mediating effect is robust.

According to the empirical results, we can find that, due to the implementation of mandatory disclosure of CSR, enterprises increase R&D and innovation expenditure in order to fulfill their environmental responsibilities; at the same time, the investment in green technology innovation increases, which can promote the technological improvement of enterprises, realize the sustainable development strategy of enterprises, and improve the TFP of enterprises as a whole.

5. Robustness test

5.1. Validity test of RDD

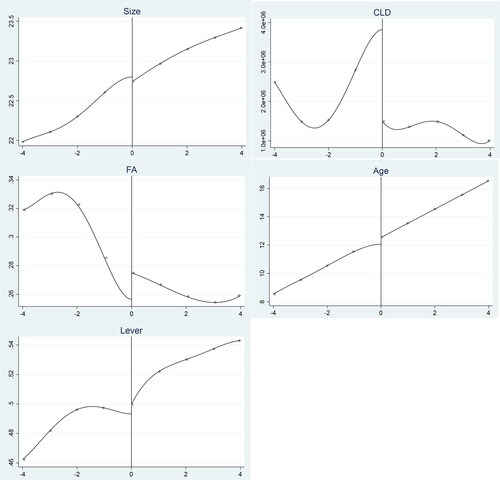

In order to ensure the robustness of the above research conclusions, mandatory disclosure of CSR is taken as a quasi-natural experiment in the design process. In the robustness test, the validity of RDD should be tested first, and the following aspects needs to be paid attention to: First, the driving variables of RDD are not artificially manipulated. Since the processing variable in this paper is the year variable and the driving variable is the mandatory disclosure policy of CSR, the year exists objectively and cannot be manipulated artificially, so the requirement that the driving variable itself is not manipulated artificially is satisfied. Second, in order to avoid capturing the discontinuity effect of control variables, it is necessary to investigate whether other control variables change continuously at the breakpoint. can help verify whether the control variable is smooth at the breakpoint.

Figure 2. Discontinuity effect of control variable.

Source: Authors.

shows that there are differences in the significance of whether there are discontinuity effects in the control variables. The size, the age and the capital structure of the enterprise obviously do not jump and rise smoothly, but the ratio of capital labour density and fixed assets seem to jump. Therefore, it is necessary to make a strict statistical test on whether there is a discontinuity effect in these two indicators. The results of the discontinuity effect test are shown in .

Table 5. Discontinuity effect of the control variables.

shows that in the implementation of CSR mandatory disclosure, each control variable has no significant jump at the breakpoint under the regression, which meets the premise requirements of the RDD smoothness hypothesis.

5.2. RDD placebo test

In order to eliminate the possibility that the conclusion above only reflects the difference of enterprise TFP in time, this part mainly changes the year of the discontinuity, that is, the two years 2007 and 2009 are respectively taken as the implementation timepoint of mandatory disclosure, so as to test whether there is any error in the impact of CSR mandatory disclosure, and the data of 2008 are added in this part. The specific results are shown in .

Table 6. Test results after changing the discontinuity years.

It can be seen from that there is no significant jump in TFP after changing the discontinuity time, indicating that the aforementioned conclusion is robust in the placebo test. In , column (1) shows the results of changing the discontinuity year to 2007, and column (2) shows the results of changing the discontinuity year to 2009. The TFP of enterprises did not jump significantly in 2007 nor 2009. It indicates that the change of enterprise TFP didn’t occur in 2007 or 2009, but in 2008 when the mandatory disclosure of CSR policy was released.

5.3. Robust test of different bandwidths

The accuracy of RDD is affected by the model setting, of which the bandwidth is the key (Arai & Ichimura, Citation2018). In this part, the nonparametric estimation method is used to verify the results after changing the bandwidth, and the triangular kernel estimation and rectangular kernel estimation results are reported at the same time. Since three times of the optimal bandwidth is close to the time period of four years tested in this paper, changing the bandwidth to 1.5, 3 and 6 times of the optimal bandwidth corresponds to 0.5, 1 and 2 times of the bandwidth in this paper. The estimated results are shown in .

Table 7. Test results of different bandwidths.

The results in show that the above empirical conclusions are also robust by changing the bandwidth. In , column (1) is the estimation result of triangular kernel, and (2) is the estimation result of rectangular kernel. There are four blocks in total. The number after lwald is the percentage of optimal bandwidth. The triangular kernel estimation is similar to the rectangular kernel estimation. The implementation of the policy starts to have a strong effect from one year to one and a half years, which is significant under the condition of 1%, and the coefficient gradually increases before 3.5 years, but gradually decreases after 3.5 years; it becomes significant under the condition of 5% after 6 years, which indicates that the mandatory disclosure policy can still have a significant impact on the TFP of enterprises until 6 years later.

6. Heterogeneity analysis of the impact of CSR mandatory disclosure on TFP

6.1. Industry heterogeneity

This part verifies Hypothesis 3 by examining the heterogeneity of the impact of CSR mandatory disclosure on enterprise TFP in different industries. According to the classification of industrial production process and referring to the existing literature, all industries are divided into four categories: agriculture, industry, construction, and service. Since there are no agricultural enterprises in the sample, the samples in this paper are divided into three categories. is the reclassification standard according to the subdivided industry standards. The final classification results show 161 samples of industrial enterprises, 5 samples of construction enterprises and 73 samples of service enterprises.

Table 8. Industry classification results.

Models (1) and (2) are used again to estimate the parameters of each sub-sample obtained according to the differences in the production process. The parameter estimation results are shown in .

Table 9. Industry heterogeneity analysis.

As can be seen from , the impact of CSR mandatory disclosure on enterprise TFP is heterogeneous among different industries. Column (1), (2) and (3) in are the RD estimation results of industrial, construction and service enterprises respectively. The regression result of TFP of industrial enterprises is significant at 1%, while the sample size of construction industry is too small, while that of service industry is not significant at all.

6.2. Equity rights heterogeneity

The difference in the nature of equity rights leads to the difference in corporate stakeholders and discretionary choices. Therefore, this paper continues to discuss the impact of CSR mandatory disclosure on TFP in view of the difference in ownership. According to the white paper on China's Corporate Social Responsibility Research Report (2012) issued by the corporate social responsibility research centre of the Economics Department of the Chinese Academy of Social Sciences, there are clear differences between state-owned enterprises and non-state-owned enterprises in their CSR development index and difficulty amplification. This part tests the impact of CSR mandatory disclosure on enterprise TFP with different equity rights to verify Hypothesis 3. In 2008, there are 188 state-owned enterprises and 51 non-state-owned enterprises. The results of RD regression are shown in .

Table 10. Equity rights heterogeneity analysis.

As can be seen from , the impact of CSR mandatory disclosure on enterprise TFP is heterogeneous among enterprises with different equity rights. Column (1) and (2) in are the RD parameter estimation results of state-owned enterprises and non-state-owned enterprises respectively. We can see that state-owned enterprises are significant at 1%, while non-state-owned enterprises are not significant. There are clear differences between the stakeholders of state-owned enterprises and non-state-owned enterprises.

7. Discussion

This study used RDD to analyze and interpret the impact of CSR mandatory disclosure on corporate TFP based on 1912 annual micro data. In what follows, we discuss our key findings of the research.

First of all, the policy of CSR mandatory disclosure has a significant effect on enterprises' TFP as a whole. It can be seen that CSR mandatory disclosure can promote the full disclosure of enterprise information, thus effectively realize the coordination of stakeholders. Although this policy increases the cost of the enterprise in some aspects, the technology and reputation of the enterprise are also improved correspondingly, which promote the growth of the enterprise TFP. In the subsequent test of changing the bandwidth, we also observed that the effect of the policy has the characteristics of long-term and dynamic decline. It began to produce a strong effect in about 1.4 years, reached the highest effect in 3 or 4 years, and then the effect decreased, but it still had a strong effect until 6 years later. Enterprises will gradually develop a habit of disclosing its non-financial information as they are always forced to achieve the standard. Moreover, importance will be attached to not only the behaviour of disclosure but also the quality of the report in the later time. Therefore, the policy can keep a strong effect in a longer period.

Secondly, mandatory disclosure of CSR enables enterprises to achieve TFP improvement by increasing R&D and innovation expenditure to a certain extent. In order to fulfill their social responsibility, enterprises turn to the green R&D and innovation expenditures. With more green products, enterprises can on the one hand fulfill their environmental responsibilities, on the other hand promote the technological improvement, thus enhancing their reputation and realizing their sustainable development strategy. Therefore, enterprises can achieve medium- and long-term economic benefits.

Thirdly, the impacts of implementing mandatory disclosure policy on different enterprises are heterogeneous. First, the policy has a significant impact on industrial enterprises, but no significant impact on other industries. Compared with other industries, the pollution problems of industrial enterprises are more serious. They have to make bigger changes to meet the standard, so the information disclosed in their CSR reports has a greater impact on their input and output. On the other hand, industrial enterprises are also the main target of the policy, just as what shows in the mandatory list, in which industrial enterprises accounts for a big part. From this perspective, we can tell that the policy does make a difference. Second, the policy has a better effect on SOEs than non-SOEs. One of the stakeholders of state-owned enterprises is the state (investor), while the investors of non-state-owned enterprises are from the private sector. As an investor, the country’s effect on capital is not only economic oriented (Matei, Citation2020), but also reflects the will of the country and relevant strategies for sustainable development. Therefore, the initial goal of state-owned enterprise investors is different to a certain extent. At the same time, the motivation of state-owned enterprises to implement national strategies is stronger than that of non-state-owned enterprises to some extent. Therefore, when mandatory disclosure of CSR is made, state-owned enterprises will have a stronger ability to implement relevant policies, and the effect will be reflected in advance or even to a deeper degree.

8. Conclusions

After dealing with the environmental governance of enterprises, China attaches importance to the role of corporate social responsibility reports. Combined with the discussion in part 7, this paper draws the following conclusions: First, the CSR mandatory disclosure can significantly improve the TFP of enterprises on the whole, and this effect has the characteristics of long-term and dynamic decline. Second, the mechanism of mandatory disclosure of CSR on TFP is through the mediating effect of R&D and innovation expenditures. Third, the heterogeneity of the impact of CSR mandatory disclosure on TFP is reflected in two aspects: industry and equity nature differences. The study also has some shortcomings and there are some suggestions for future research:

It should be noted that the sharp RDD method used in this paper can ensure that all samples are included in the study, but at the same time, the conclusion is drawn only for enterprises that strictly follow the policy. However, it takes time for the policy to affect all enterprises, and more studies are needed to evaluate the comprehensive effect of the policy. Meanwhile, corporate social responsibility reports measure various performance of enterprises from multiple dimensions including shareholder, employee, stakeholder’s right, environment and social responsibility, and more detailed and accurate analysis from each of the above five dimensions is worth studying. On the other hand, it is also recommended that more factors of TFP and their mechanism to be discovered not only from the perspective of CSR. Moreover, in response to the appeal of environment protection, green total factor productivity (GTFP) might be a meaningful topic.

Disclosure statement

No potential conflict of interest was reported by the authors.

Table 1. Input-output indicators of TFP measurement.

References

- Anzolin, G., & Lebdioui, A. (2021). Three dimensions of green industrial policy in the context of climate change and sustainable development. The European Journal of Development Research, 33(2), 371–405. https://doi.org/10.1057/s41287-021-00365-5

- Arai, Y., & Ichimura, H. (2018). Simultaneous selection of optimal bandwidths for the sharp regression discontinuity estimator. Quantitative Economics, 9(1), 441–482. https://doi.org/10.3982/QE590

- Bamezai, A. (1995). Application of difference-in-difference techniques to the evaluation of drought-tainted water conservation programs. Evaluation Review, 19(5), 559–582. https://doi.org/10.1177/0193841X9501900505

- Bousselmi, H. e W., Caridad, L., & Villamandos, N. C. (2019). Structural models in corporate social responsibility: Attraction of investment in Tunisia. Sustainability, 11(18). https://doi.org/10.3390/su11185009

- Calonico, S., Cattaneo, M. D., & Titiunik, R. (2015). Optimal data-driven regression discontinuity plots. Journal of the American Statistical Association, 110(512), 1753–1769. https://doi.org/10.1080/01621459.2015.1017578

- Charnes, A., Cooper, W. W., & Rhodes, E. (1978). Measuring the efficiency of decision making units. European Journal of Operational Research, 2(6), 429–444. https://doi.org/10.1016/0377-2217(78)90138-8

- Chen, L., Zhou, R., Chang, Y., & Zhou, Y. (2020). Does green industrial policy promote the sustainable growth of polluting firms? Evidences from China. Science of the Total Environment, 764. https://doi.org/10.1016/j.scitotenv.2020.142927

- Chen, T.-S., Huang, Y.-F., Weng, M.-W., & Do, M.-H. (2021). Two-Stage Production System Pondering upon Corporate Social Responsibility in Food Supply Chain: A Case Study. Applied Sciences, 11(3). https://doi.org/10.3390/app11031088

- Clarkson, M. B. E. (1995). Stakeholder framework for analyzing and evaluating corporate social performance. Academy of Management Review, 20(1), 92–117.

- Cormier, D., Magnan, M., & Velthoven, B. V. (2005). Environmental disclosure quality in large German companies: Economic incentives, public pressures or institutional conditions?: European Accounting Review. European Accounting Review, 14(1), 3–39. https://doi.org/10.1080/0963818042000339617

- Cowen, S. S., Ferreri, L. B., & Parker, L. D. (1987). The impact of corporate characteristics on social responsibility disclosure: A typology and frequency-based analysis. Accounting, Organizations and Society, 12(2), 111–122. https://doi.org/10.1016/0361-3682(87)90001-8

- Demirtaş, Y. E., & Keçeci, N. F. (2020). The efficiency of private pension companies using dynamic data envelopment analysis. Quantitative Finance and Economics, 4(2), 204–219.

- Fang, M., Fan, P., Nepal, S., & Chang, C. P. (2021). Dual-mediation paths linking corporate social responsibility to employee’s job performance: A multilevel approach. Frontiers in Psychology, 11. https://doi.org/10.3389/fpsyg.2020.612565

- Feng, Y., Chen, S., & Failler, P. (2020). Productivity effect evaluation on market-type environmental regulation: A case study of SO2 emission trading pilot in China. International Journal of Environmental Research and Public Health, 17(21). https://doi.org/10.3390/ijerph17218027

- Gray, R., Javad, M., Power, D. M., & Sinclai, C. D. (2001). Social and environmental disclosure and corporate characteristics: A research note and extension. Journal of Business Finance & Accounting, 28, 3–4.

- Hahn, J., Todd, P., & Klaauw, W. V. d. (2001). Identification and estimation of treatment effects with a regression-discontinuity design. Econometrica, 69(1), 201–209. https://doi.org/10.1111/1468-0262.00183

- Hong, M., Drakeford, B., & Zhang, K. (2020). The impact of mandatory CSR disclosure on green innovation: evidence from China. Green Finance, 2(3), 302–322. https://doi.org/10.3934/GF.2020017

- Hooghiemstra, R. (2000). Corporate communication and impression management–new perspectives why companies engage in corporate social reporting. Journal of Business Ethics, 27(1/2), 55–68. https://doi.org/10.1023/A:1006400707757

- Ji, Y., Xu, W., & Zhao, Q. (2019). The real effects of stock prices: learning, disclosure and corporate social responsibility. Accounting & Finance, 59, 2133–2156. https://doi.org/10.1111/acfi.12494

- Jinglin, J., Vikram, N., & Chong, X. S. (2021). Stock-market disruptions and corporate disclosure policies. Journal of Corporate Finance, 66. https://doi.org/10.1016/j.jcorpfin.2020.101762

- Kneip, A., Simar, L., & Wilson, P. W. (2008). Asymptotics and consistent bootstraps for DEA estimators in nonparametric frontier models. Econometric Theory, 24(6), 1663–1697. https://doi.org/10.1017/S0266466608080651

- Lee, D. S., & Lemieux, T. (2010). Regression discontinuity designs in economics. Journal of Economic Literature, 48(2), 281–355. https://doi.org/10.1257/jel.48.2.281

- Li, Z., Liao, G., & Albitar, K. (2020). Does corporate environmental responsibility engagement affect firm value? The mediating role of corporate innovation. Business Strategy and the Environment, 29(3), 1045–1055. https://doi.org/10.1002/bse.2416

- Lu, H., Oh, W. Y., Kleffner, A., & Chang Y. K. (2021). How do investors value corporate social responsibility? Market valuation and the firm specific contexts. Journal of Business Research, 125. https://doi.org/10.1016/J.JBUSRES.2020.11.063

- Luasa, S. N., Dineen, D., & Zieba, M. (2018). Technical and scale efficiency in public and private Irish nursing homes – a bootstrap DEA approach. Health Care Management Science, 21(3), 326–347. https://doi.org/10.1007/s10729-016-9389-8

- Manzoor, M. S., Rehman, R. U., Usman, M. I., & Ahmad, M. I. (2019). How corporate governance and csr disclosure affect firm performance? E + M Ekonomie a Management, 22(3), 20–35. https://doi.org/10.15240/tul/001/2019-3-002

- Matei, I. (2020). Is financial development good for economic growth? Empirical insights from emerging European countries. Quantitative Finance and Economics, 4(4), 653–678. https://doi.org/10.3934/QFE.2020030

- Mayorova, E. (2019). Corporate social responsibility disclosure: Evidence from the European retail sector. Entrepreneurship and Sustainability Issues, 7(2), 891–905. https://doi.org/10.9770/jesi.2019.7.2(7)

- Miller, S. R., Eden, L., & Li, D. (2020). CSR reputation and firm performance: A dynamic approach. Journal of Business Ethics, 163(3), 619–636. https://doi.org/10.1007/s10551-018-4057-1

- Muhammad, R., Muhammad, A., & Muhammad, A. (2021). How does corporate social responsibility affect financial performance, financial stability, and financial inclusion in the banking sector? Evidence from Pakistan. Research in International Business and Finance, 55.

- Nguyen, T. T. D. (2020). An empirical study on the impact of sustainability reporting on firm value. Journal of Competitiveness, 12(3), 119–135. https://doi.org/10.7441/joc.2020.03.07

- Okafor, A., Adeleye, B. N., & Adusei, M. (2021). Corporate social responsibility and financial performance: Evidence from U.S tech firms. Journal of Cleaner Production, 292. https://doi.org/10.1016/j.jclepro.2021.126078

- Pastor, J. T., & Lovell, C. A. K. (2005). A global Malmquist productivity index. Economics Letters, 88(2), 266–271. https://doi.org/10.1016/j.econlet.2005.02.013

- Sedláček, J., & Popelková, V. (2020). Non-financial information and their reporting—evidence of small and medium-sized enterprises and large corporations on the Czech capital market. National Accounting Review, 2(2), 204–206. https://doi.org/10.3934/NAR.2020012

- Sial, M. S., Zheng, C., Khuong, N. V., Khan, T., & Usman, M. (2018). Does firm performance influence corporate social responsibility reporting of chinese listed companies? Sustainability, 10(7), 2217. https://doi.org/10.3390/su10072217

- Simin, A., Bo, L., Dongping, S., & Xue, C. (2021). Green credit financing versus trade credit financing in a supply chain with carbon emission limits. European Journal of Operational Research, 292(1), 125–142. https://doi.org/10.1016/j.ejor.2020.10.025

- Su, Y., & Yu, Y. (2019). Effects of technological innovation network embeddedness on the sustainable development capability of new energy enterprises. Sustainability, 11(20). https://doi.org/10.3390/su11205814

- Tuzcuoglu, T. (2020). The impact of financial fragility on firm performance: an analysis of bist companies. Quantitative Finance and Economics, 4(2), 310–342.

- Ubeda-Garcia, M., Claver-Cortes, E., Marco-Lajara, B., & Zaragoza-Saez, P. (2021). Corporate social responsibility and firm performance in the hotel industry. The mediating role of green human resource management and environmental outcomes. Journal of Business Research, 123, 57–69. https://doi.org/10.1016/j.jbusres.2020.09.055

- Uras, B. R. (2014). Corporate financial structure, misallocation and total factor productivity. Journal of Banking and Finance, 39, 177–191. https://doi.org/10.1016/j.jbankfin.2013.11.011

- Utomo, M. N., Rahayu, S., Kaujan, K., & Irwandi, S. A. (2020). Environmental performance, environmental disclosure, and firm value: empirical study of non-financial companies at Indonesia Stock Exchange. Green Finance, 2(1), 100–113. https://doi.org/10.3934/GF.2020006

- Xu, M., Albitar, K., & Li, Z. (2020). Does corporate financialization affect EVA? Early evidence from China. Green Finance, 2(4), 392–408. https://doi.org/10.3934/GF.2020021

- Xu, X., & Li, J. (2020). Asymmetric impacts of the policy and development of green credit on the debt financing cost and maturity of different types of enterprises in China. Journal of Cleaner Production, 264, 121574. https://doi.org/10.1016/j.jclepro.2020.121574

- Yuming, Z., Chao, X., & David, T. (2020). Redistribution of China's green credit policy among environment-friendly manufacturing firms of various sizes: Do banks value small and medium-sized enterprises? International Journal of Environmental Research and Public Health, 18(1).

- Zhang, Q., Cao, M., Zhang, F., Liu, J., & Li, X. (2020). Effects of corporate social responsibility on customer satisfaction and organizational attractiveness: A signaling perspective. Business Ethics: A European Review, 29(1), 20–34. https://doi.org/10.1111/beer.12243

- Zhang, D. Y., & Vigne, S. A. (2021). The causal effect on firm performance of China’s financing–pollution emission reduction policy: Firm-level evidence. Journal of Environmental Management, 279. https://doi.org/10.1016/j.jenvman.2020.111609