?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Corporate Social Responsibility (CSR) is considered as an important business agenda in the current age. Based on the data of A-share listed companies from 2010 to 2020, this study used a fixed-effect model, heterogeneity analysis and intermediary effect test to investigate the relationship between parent-subsidiary geographical distance and CSR. Our study findings revealed that the parent-subsidiary companies’ geographic distance has a negative effect on CSR. Results of our study further indicated that the effect was more stronger for non-state-owned enterprises and the firms in the eastern region. Findings of our study also reported that the enterprise internal control had an obvious mediating effect in the association among parent-subsidiary companies’ geographic distance and CSR. The government needs to reinforce legal construction, actively guide enterprises to perform CSR through incentive measures, and implement special supervision on enterprises with a large number of subsidiaries. This study not only enriches the literature on the factors influencing corporate social responsibility but also provides a theoretical perspective and important ideas for the effective implementation of regional diversification and the improvement of CSR levels in practice.

1. Introduction

Recently, CSR has attracted a lot of attention, to explore the determinants of CSR, several studies have focused on the factors such as corporate financial characteristics (Fiedler et al., Citation2021; Muhammad et al., Citation2019), executive characteristics (Faraudello et al., Citation2020; Fernandez-Feijoo et al., Citation2012; Luo & Moon, Citation2021; McCarthy et al., Citation2017; Okafor & Ujah, Citation2020; Rao & Tilt, Citation2016; Rosnan et al., Citation2013), corporate governance (Chijoke-Mgbame et al., Citation2019; Garas & ElMassah, Citation2018; Ozturk, Citation2011; Ruangviset et al., Citation2014; Tang et al., Citation2020; Zaman et al., Citation2020), ownership (Bárcena-Ruiz & Sagasta, Citation2021; Guo & Zheng, Citation2021), external environment or institutional factors (Cahan et al., Citation2015; Chen et al., Citation2019; El Ghoul et al., Citation2019; Ioannou & Serafeim, Citation2012; Ozturk, Citation2016). However, there are few literature analyzing CSR from the perspective of corporate geographic factors. Shi et al. (Citation2017) considered American listed companies as samples and, based on the background of regional diversification, found that geographic dispersion is a factor that negatively affects CSR; in other words, geographically discrete firms manage to have less CSR scores.

From a macro perspective, CSR as a social appeal, will be significantly affected by the external environment and institutional factors, such as public opinion environment, media attention, and marketization process (Cahan et al., Citation2015; Chen et al., Citation2019; El Ghoul et al., Citation2019; Zyglidopoulos et al., Citation2012). Other studies have shown that the political connection between the enterprise and the government will promote the fulfillment of CSR (Huang & Zhao, Citation2016; Ji et al.,Citation2020; Nguyen et al., Citation2021; Su & He, Citation2010). Industry associations can significantly improve corporate social responsibility performance. That is, compared with firms that have not participated in industry associations, firms that have participated in industry associations have a significantly higher investment in social responsibilities such as treating employees, protecting the environment, and charitable donations. From a personal perspective, the personal characteristics of corporate executives, such as gender (Faraudello et al., Citation2020; Fernandez-Feijoo et al., Citation2012; Manner, Citation2010), ethics (Huimin & Ryan, Citation2011; Ríos-Manríquez et al., Citation2021; Rosnan et al., Citation2013), and self-confidence (McCarthy et al., Citation2017) also affect CSR. In addition, based on the upper echelons perspective, some scholars found that top management team (TMT) heterogeneity (social capital heterogeneity, tenure heterogeneity, educational specialty heterogeneity, and age heterogeneity) also had a significant impact on CSR (Chen et al.,Citation2019; Hafsi & Turgut, Citation2013; Rao & Tilt, Citation2016; Ratri et al., Citation2021).

Geographical diversification is the expansion of enterprises in different geographical sub-markets through horizontal or vertical integration, which is an important strategic means for business development, and as well as is an interesting research topic in theoretical circles. The influence of geographic diversification on corporate decision-making, corporate stock returns, funding costs, credit supply, risk implications, earnings management and corporate value has been the focus of scholars in the past decade (Boubaker et al., Citation2019; Davide & Joana, Citation2021; Fahad & Wang, Citation2018; Levine et al., Citation2021; Mammen et al.,Citation2021; Ozturk, Citation2017; Shi et al., Citation2015). A direct manifestation of geographic diversification is the increase of subsidiaries in different locations. The number and distribution of subsidiaries have broadened the space geography distance between them and their parent companies, aggravating the geographic dispersion of the enterprise, which has a significant impact on information asymmetry and agency costs (Cashman et al., Citation2019; El Ghoul et al., Citation2013), and is bound to affect corporate decisions, corporate risk and corporate governance (Fahad & Wang, Citation2020; Fitania & Firmansyah, Citation2020; Mammen et al.,Citation2021). Based on this, some researchers have done work on the effect of parent-subsidiary companies’ geographic distance on the company’s value, corporate governance, internal control, corporate investment behavior, corporate efficiency, and audit quality in the context of geographic diversification. However, the issue of how the parent-subsidiary companies’ geographic distance affects CSR is ignored.

As an important way to improve market share and market competitiveness at home and abroad, geographic diversification is becoming increasingly popular among enterprises. Given the broad implementation of geographic diversification, it has gradually become the focus of scholars in the theoretical field. Some domestic and foreign studies began to emphasize the importance of geographic diversification and discussed the influence of geographic diversification on company’s risk (Mammen et al., Citation2021), corporate profitability (Shi et al., Citation2015; Subramaniam & Wasiuzzaman, Citation2019), firm performance (Song & Kang, Citation2019) and so on in the context of geographic diversification. For example, Mammen et al. (Citation2021) found that total geographic diversification increases enterprise risk. Subramaniam and Wasiuzzaman (Citation2019) found that geographical diversification had a positive impact on the profitability of small and medium-sized enterprises by using the data of Malaysian listed companies from 2010 to 2013. Song and Kang (Citation2019) used data of 258 U.S. accommodation enterprises from 1990 to 2015 and found that geographical diversification has a positive and significant impact on corporate performance. Shi et al. (Citation2015) studied the impact of geographic dispersion on the earnings management for some of the listed companies in the United States from 1994 to 2011 and found that geographically dispersed companies have lesser accrual-based management and advanced actual earnings management system compared to geographically focused enterprises.

Based on the research status of these two aspects, an abundance of studies clearly exists on the influencing factors of CSR and regional diversification and its consequences. However, there are few studies on regional diversification or geographic factors of enterprises and CSR. Based on the geographic diversification background, they measured the geographic dispersion according to the number of states in which these companies operate, and found that geographic dispersion has an apparent negative influence over CSR, while ignoring the influence of parent-subsidiary companies’ geographic distances. Hence, based on the geographic diversification background of China’s actual situation, this study discusses the impact of parent-subsidiary companies’ geographic distance on Chinese CSR from the viewpoint of the individual heterogeneity of parent-subsidiary enterprises, which will supplement the existing literature and has certain theoretical value.

Based on the above, this study selects data on Chinese A-share listed companies from 2010 to 2020. Firstly, we assess the direct relationship between the parent-subsidiary companies’ geographic distance and CSR. Secondly, we split sample data to compare and analyze the effect of parent-subsidiary companies’ geographical distance on CSR. Specifically, according to the nature of property rights of Chinese enterprises and the regions where the enterprises are located, we divide the sample into state-owned enterprises and non-state-owned enterprises, enterprises in the eastern region, and enterprises in the midwestern regions. In China, there are large differences in the development goals, positioning and governance models of enterprises with different property rights, which will directly affect the firm’s management and strategic decisions. Existing literature studies have proved that non-state-owned enterprises’ awareness and performance of social responsibility still have a big disparity with state-owned Chinese companies, and have taken more social obligations (Huang & Zhao, Citation2016). Therefore, when discussing the impact of parent-subsidiary companies’ geographic distance on CSR, it is necessary to consider the property rights of the enterprise. In addition, China has a vast territory, and the economic development level and marketization process in different regions are very different. Enterprises tend to be more cautious in their decision-making, and many factors such as regional economic development level and institutional environment need to be considered comprehensively. The development strategies and decision-making of enterprises in different regions are also different. Therefore, it is essential to reflect the effect of regional differences. Finally, few studies have shown that in the process where the parent-subsidiary companies’ geographic distance affects corporate value and audit quality, corporate internal control often has an intermediary role. Therefore, the study also considers internal control factors and explores whether the parent-subsidiary companies’ geographic distance has an indirect impact on CSR?

There are three main contributions to this research. Firstly, we prove that in the context of geographic diversification, the parent-subsidiary companies’ geographic distance can significantly affect CSR. Notably, the research by Shi et al. (Citation2017) has proved that in the context of geographic diversification, the geographic dispersion of enterprises is a negative factor affecting CSR. But their research was based on the states numbers where the company functions, without taking into account the factors of geographic distance. This is the difference between our study and theirs. In addition, the existing research typically studied the affecting elements of CSR from the overall viewpoint of listed companies, such as enterprise characteristics (Finegold et al., Citation2010; Nguyen et al., Citation2021), corporate culture (Soschinski et al., Citation2021). It defaults to the assumption that the parent and subsidiary are homogeneous in space geography, thus ignoring the influence of the parent’s and subsidiary’s individual heterogeneity as an enterprise component. We creatively explore the impact of geographical distance of subsidiaries on CSR. Secondly, we prove that under different corporate property rights and regional, the parent-subsidiary companies’ geographic distance has different impacts on CSR. That is, the impact is particularly obvious in non-state-owned companies and enterprises of the eastern region. These conclusions enrich the study on state-owned enterprises and regional differences of enterprises. Finally, based on the relationship between parent-subsidiary companies’ geographical distance and CSR, we find that internal control has an intermediary effect, which makes up for the deficiency of current research.

The research will focus on understanding the specific impact of the parent-subsidiary companies’ geographical distance on CSR', and whether this impact will be different due to property rights and regions of enterprises. In addition, researchers will also explore the affects path to parent-subsidiary companies’ geographical distance on CSR and what role internal control will play in it.

2. Theoretical analysis and research hypotheses

2.1. The direct impact of parent-subsidiary companies’ geographic distance on CSR

Previous studies found that geographical location has different effects on corporate social responsibility. Non-local long-term institutional ownership has a negative impact on CSR, but local long-term institutional ownership has a positive impact on CSR (Chang et al., Citation2021). This study simply divides the geographical characteristics of enterprises into local institutional ownership and non-local institutional ownership, ignoring the geographical distance between enterprises and ownership institutions. Boeprasert (Citation2012) showed that firms whose headquarters are farther away from big cities have higher social responsibility scores (Boeprasert, Citation2012), but this finding does not take into account the geographic dispersion of firms. A firm that has its’ headquarters far from a big city is not necessarily geographically centralized. In other words, firms headquartered far from big cities may be geographically dispersed given the implementation of a regional diversification strategy, thus further affecting the implementation of CSR. We attempt to comprehend the association between parent-subsidiary companies’ geographic distance and CSR from the following two aspects.

Alternatively, from the outlook of information asymmetry and agency cost effect, geographic diversification increases the number of subsidiaries in different places, which enlarges the space geographic distance among forms the geographic dispersion of enterprises and parent and subsidiary companies. However, it also intensifies the information asymmetry and agency problem between subsidiary and parent companies. The problem of information asymmetry caused by distance is more obvious (Ayari, Citation2010; Cashman et al., Citation2019). Further parent-subsidiary companies’ geographic distance results in greater information asymmetry and, thus, easier inducement of opportunistic behavior by management. At the same time, Von Zedtwitz and Gassmann (Citation2002) believe that distance affects the frequency and quality of communication, increases transaction costs, and aggravates the principal-agent problem. The increasing distance of parent-subsidiary companies’ extends the agency chain of listed companies and increases the complexity of the agency structure and costs, which facilitates the opportunistic behavior of enterprise management authorities. In this information age with a developed network, although network media and electronic communication equipment shorten the space-time interval of human society, it has not really solved the information asymmetry and agency problems. The influence of geographic distance on the information asymmetry and agency problems is still significant. To seize on its own best interests, management often neglects to protect the interests of all stakeholders, thus reducing the enthusiasm of fulfilling CSR.

From the viewpoint of idle resources theory, fulfilling social responsibility as a strategic decision of an enterprise may be restricted by idle resources. In general, these resources can not only respond to the changes in enterprise internal and external environment pressure, guaranteeing normal operation and survival of enterprises (Buchholtz et al., Citation1999). They can also help enterprises actively maintain relationships with various stakeholders, such as consumers, employees, and the government, and pay more attention to environmental protection (Waddock & Graves, Citation1997). In contrast, even if enterprises are willing to maintain their good corporate citizenship image by actively abiding by social laws and regulations, serving the public, protecting the environment, and donating, they must consider their actual number of existing resources. However, the increase in the variances between parent and subsidiaries apparently increases the difficulty of enterprise groups’ managing and controlling companies and management costs, resulting in a certain degree of internal resource consumption. Therefore, companies are more inclined to maintain their financial flexibility and use spare resources (especially financial resources) to maintain the enterprises’ investments and daily operations alleviate external financing constraints, and cope with cost increases-all of which are more practical activities than the fulfilling of social responsibility requirements. Therefore, enterprises do not pay much attention to CSR, and the resources invested in CSR are greatly reduced. In the light of following analysis, this manuscript proposes the following hypotheses.

H1: Parent-subsidiary companies’ geographic distance is negatively correlated with CSR.

2.1.1. Differences in property rights

In China, the difference in the nature of property rights will directly affect the business management and strategic decision-making of enterprises, including the fulfillment of CSR. Therefore, when discussing the impact of the parent-subsidiary companies’ geographic distance on CSR, it is necessary to consider the property rights of the enterprise.

In comparison to non-state-owned listed enterprises, the parent-subsidiary companies’ geographic distance has no obvious influence on CSR of state-owned companies, which is caused by the nature and objectives of state-owned companies. The actual holder of the state-owned enterprise is the government, and under the government’s intervention, the business objectives of the state-owned enterprise are distorted. The goal of state-owned enterprises is not to maximize the value of enterprises (Fan et al., Citation2014), but also to bear the national policy burden, such as maintaining social stability, increasing social employment rates, protecting and improving environmental quality, and stabilizing taxes. Therefore, on the one hand, when the parent-subsidiary companies’ dispersion leads to information asymmetry, cost increase and equivalent resource consumption, the state-owned enterprises will not care too much, and the parent-subsidiary companies’ geographic distance has no obvious influence on the state-owned enterprises. Alternatively, the fulfillment of social responsibility of state-owned companies is greatly restricted by policy factors (Jia & Liu, Citation2014), which makes state-owned enterprises have good social responsibility performance, thus weakening the negative effect of parent-subsidiary companies’ geographic distance on CSR.

Non-state-owned enterprises do not have non-economic goals due to private ownership of property rights. Instead, they focus more on the survival and development of the enterprise itself. Its main goal is to pursue value-added on the basis of legal compliance. Therefore, non-state-owned companies will consider the negative effects of parent-subsidiary dispersion on their economic profits, and will retain or invest more financial resources to maintain normal production and operation, rather than fulfilling CSR. In addition, in comparison to state-owned enterprises, due to the lack of social obligation policies and institutional constraints, non-state-owned enterprises have a strong arbitrariness in performing their social responsibilities and lack clear social responsibility goals. Therefore, the parent-subsidiary companies’ geographic distance has a more obvious impact in order to fulfill social responsibilities of non-state-owned enterprises. As per this analysis, this article suggests the second hypothesis:

H1a: In comparison to state-owned enterprises, the parent-subsidiary companies’ geographic distance has a more obvious impact on CSR of enterprises not owned by the government.

2.1.2. Differences in regions

Enterprises are deeply affected by local macro environment such as politics, economy and culture. China has a huge territory, and because of historical and geographical factors, there are great differences between the eastern coastal plains and the midwestern mountainous areas in economic development level, local government governance ability and degree of opening to the outside world. Hence, it is necessary for scholars to analyze the differences between eastern enterprises and central and midwestern enterprises. Sotorrío and Sánchez (Citation2008) showed that different regions of enterprises will affect the level of CSR.

As we know, not only economy, the degree of marketization and government governance in various regions of China are different, which will affect CSR. Kim and Kim (Citation2014) and Lee et al. (Citation2013) found that CSR practice of enterprises are closely related to the economic level. Besides, as the frontier of China’s opening to the outside world, the eastern region has advantages in marketization which means less government intervention, thus CSR of eastern enterprises depends on their internal factors. The marketization of the midwestern regions is weak, and enterprises need to rely on the support of various policies and measures of the government. They are deeply affected by the government, which weakens the impact of geographical distance on CSR to a certain extent.

Research shows that the primary factor affecting the diversified strategic decisions of Chinese listed companies is the process of regional marketization. The greater the government intervention, the lower the degree of diversification; the more intense the industry competition, the more companies tend to diversify (Li & Liu, Citation2007). There are large imbalances in the level of economic development in various parts of China, there are large differences in the marketization process in different regions, as well as the degree of government intervention in enterprises and industry competition are also different. Due to the earlier reform and opening up in the eastern part of China, the marketization process is faster. The enterprise has rich experience in advanced management, more flexible management mechanisms, and a stronger sense of market competition (Li & Olorunniwo, Citation2008). In addition, the economy in the eastern region of China is more developed. The formation of the ‘Yangtze River Delta Economic Belt (YRDEB)’, the ‘Pearl River Delta Economic Belt (PRDEB)’ and the ‘Beijing-Tianjin-Tangshan Economic Belt (BTTEB)’ has created a good external economic environment in the eastern region of China, providing more and better investment development opportunities. Therefore, listed companies are more inclined to expand the market scale by implementing a diversified strategy and setting up a large number of off-site subsidiaries. Relatively speaking, midwestern regions in China are relatively backward, and the government is ‘stronger’. The autonomy of enterprise development is relatively weak, and its development strategy is more susceptible to the influence of government policies, resulting in a weaker geographic diversification than enterprises in developed regions in the east (Wang & Shen, Citation2012). Therefore, the geographic distance dispersion of parent-subsidiary company in the eastern region is more common than that in the midwestern regions, and information asymmetry and agency problems as well as resource internal consumption may be more serious. As per the above analysis, this study intends Hypothesis 1b:

H1b: Compared with the midwestern regions, the parent-subsidiary companies’ geographic distance has a more obvious impact on CSR of enterprises in the eastern region.

2.2. The indirect impact of the parent-subsidiary enterprises and geographic distance on CSR

The indirect impact of the parent-subsidiary companies’ geographic distance on corporate social responsibility is mainly reflected in the intermediary effect of variables. Here we will analyze that whether or not the internal control of the company has an intermediary effect.

Under the modern enterprise system, internal control, as one of the most important mechanisms of the corporate governance, has a very important self-regulation and restriction function in the production and operation activities. Studies have shown that high-quality internal controls can significantly promote the implementation of CSR (Yang, Citation2019), mainly through the management and supervision of and restrictions on CSR. On the one hand, it can promote the rationalization and standardization of the implementation of corporate social responsibility by formulating decision-making mechanisms, processing procedures, and periodic evaluation systems for implementing corporate social responsibility (Wang & Shen, Citation2012). On the other hand, it can implement effective management and control of effectively avoid corporate social responsibility risks by timely monitoring and correcting behaviors that harm public interests, evade or even fail to fulfill social responsibility. In summary, effective internal control showed a positive impact over the CSR. On the contrary, low-quality internal control has non-favorable impact over the improvement of CSR. Therefore, Hypothesis H2 is proposed:

H2: Internal control has significant and positive correlation to CSR.

Research indicates that the eminence of internal control of companies is affected by the geographic differences between the parent and the subsidiary companies. The further the parent-subsidiary companies’ geographic distance is, the lower the quality of internal control will be (Li, Citation2015). This is mainly because the dispersion of parent and subsidiary companies affects the five elements of internal control, namely control environment, risk assessment, internal supervision, control activities, and information and communication. Specifically, the implementation of geographic diversification makes the parent and subsidiary companies in different institutional environments, resulting in the overall control environment of the enterprise is uneven. Given the increase in remote subsidiaries and the increase in parent-subsidiary companies’ geographic distance, the overall organizational structure of companies has become increasingly large and complex, and the internal and external risks facing the company will increase accordingly. At the same time, the more dispersed the distance, the weaker the management and internal supervision of parent and subsidiary companies, which even leads to the formality of internal supervision, thus reducing the implementation of related control activities, and may result in such control activities being unable to maintain the company’s risk within an acceptable range. In addition, the expansion of parent-subsidiary companies’ geographic differences makes it impossible to guarantee the authenticity and timeliness of majority of transmission of information between parent and subsidiaries, hence reducing the efficiency of information and communication. It is difficult for an enterprise to find defects in the internal control of the parent or subsidiary company, or fail to propose an effective rectification plan for internal control defects, thereby affecting the effective operation of internal control systems. Therefore, we conclude that the dispersion of the parent-subsidiary company leads to the reduction of the internal control quality of the enterprise group, which weakens its supervision and restriction on corporate social responsibility and further leads to the reduction of the level of CSR. Therefore, this article proposes Hypothesis H3:

H3: Internal control has a mediating effect on the negative relationship between parent-subsidiary companies’ geographic distance and CSR.

3. Methodology

3.1. Sample and data

This study used data on Chinese A-share listed firms from 2010 to 2020 as the preliminary sample and collected 25225 raw data.Footnote1 In the process of data selection and information processing, firstly, in view of the particularity of the listed companies in the financial and insurance industry and those listed by ST (ST*), such samples are excluded. Then, samples without subsidiaries or undisclosed subsidiaries, as well as samples with missing CSR score and relevant financial indicators were excluded, leaving 22725 valid observed values.

The CSR data required in this paper come from HeXun,Footnote2 which is scored based on CSR reports and annual reports. On December 29, 2009, the China securities regulatory commission (CSRC)Footnote3 issued a document that clearly stated that all listed companies need to progress the awareness of social accountability, actively assume social accountability, and disclose their social accountability reports along with their annual reports. Therefore, from 2010 at the beginning, listed companies began to implement and disclose corporate social responsibility reports. The HeXun corporate social responsibility score data were also initiated in 2010, which is why this study used 2010 as the starting point for the sample years.

The data of internal control selected from the internal control index provided by Shenzhen DIB Risk Management Consulting Company; other financial information and relevant data is obtained from the Guotaian database (CSMAR). In the process of data processing, this article mainly uses the two statistical analysis software EXCEL 2010 and STATA 15.0.

3.2. Dependent variable

The dependent variable selected in this study is CSR. This study uses the responsibility score based on proficient evaluation system of HeXun Online-based CSR report to measure CSR. The index can comprehensively reflect the performance of all listed companies in the area of CSR and is available and authoritative. The higher the CSR score indicates better CSR performance on behalf of individual listed companies.

3.3. Independent variables

This paper uses parent-subsidiary companies’ geographic distance (GeoDis) as the core explanatory variable. In addition, the natural logarithm of the average geographic differences between the parent and the subsidiary companies is adopted to measure it. First, sort out the registered locations of the parent companies and each of their subsidiary, take the prefecture-level city as the basis for calculating the distance, and use the computer running code to calculate the spherical surface distance between the city where exists the location of parent company and the city where exists the location of each subsidiary. Then, the average geographic distance of the parent company compared to each listed company and all of its subsidiaries is obtained by using the arithmetic average method, and the natural logarithm of the average distance is taken as the measurement index of the geographic distance between the parent companies and their subsequent subsidiaries. A larger GeoDis value indicates farther parent-subsidiary companies’ space geography distance. It should be noted that the external economic environments of Hong Kong, Macao, Taiwan, and other countries may differ from that of Inland China. During the calculation process, the subsidiaries of listed firms in Hong Kong, Macao, Taiwan, and other countries are not considered.

3.4. Mediator variables

In this paper, internal control (IC) is a mediation variable. Internal control is a measure, method, and procedure that enables various businesses within the enterprise to interact and restrict each other. It is difficult to measure directly. Most scholars use the internal control index provided by Shenzhen DIB Risk Management Consulting Company to analyze the qualities of internal control measurement of listed enterprises, such as Li et al. (Citation2019). According to the completion of internal control objectives, it builds an internal control system based on five criteria of internal control (risk, environment, control activities, communication and supervision) to measure the internal control level of the superior company, and adjusts measurement results based on the number of defects in internal control. It can better reflect the internal control level of listed companies, which has been generally recognized by researchers, and has certain representativeness and authority. By taking into account the data availability, this paper draws on the approach using the DIB internal control index as a measure of internal control. Based on evaluation outcomes, the range for internal control index value for all listed companies is between [0,1000]. Considering the unity of dimensions, the treatment of this index is generally recognized by Chinese scholars. Some scholars divided the internal control index by 1000 while other used the natural logarithm to measure the internal control index. Our study is designed on practice of Li et al. by taking natural logarithm into account as a measure of quality of the internal control index (Li et al., Citation2019).

3.5. Control variables

Considering the influence of individual differences, this paper chooses company size (Size), company age (Age), solvency (Lev), profitability (Roe), operating capacity (Tat), ownership concentration (LarHol) and chairman’s part-time status (CeoDu) as control variables. In addition, considering the fixed effect of year and industry, the year dummy variable (Year) and industry dummy variable (Ind) are also included. The specific definition of control variables is defined in .

Table 1. Variable definitions.

3.6. Empirical model

This study uses the panel data of Chinese listed companies from 2010 to 2020. Under the background of panel data regression, the simplest way to explain the differences of individual or time behavior is the fixed effect model (Nerlove & Balestra, Citation1992). Fixed effect regression has certain information advantages because it can weaken the endogenous problems caused by omitted variables that do not change with time. Compared with other statistical methods such as multiple linear regression, fixed effect model can control all individual characteristics that do not change with time, so it can effectively avoid ‘omitted variable bias’ at the individual level.

Neumark and Wascher (Citation1992) first applied the two-way fixed effects model to the study of minimum wage, fixing the two factors of region and time. According to the data characteristics and Quan’ research (Quan et al., Citation2015), this paper uses the two-way fixed effect model of year and industry. To test the model and hypotheses, the following empirical models are constructed, respectively:

(1)

(1)

(2)

(2)

(3)

(3)

Subscripts i and t indicate the enterprise and year respectively. CSR is a dependent variable which indicates an enterprise CSR performance, GeoDis is a test variable that represents the parent-subsidiary companies’ geographic distance of the listed firm. IC is the mediator variable and represents internal control of the enterprise. Size, Age, Lev, Roe, Tat, LarHol and CeoDu are control variables as specifically defined in ; β is the parameter to be estimated, β1-β9 represent the regression coefficients of their respective variables. Year is the year fixed effect, Ind is the industry fixed consequence and ε is the randomized error term.

4. Empirical evaluation and results analysis

4.1. Descriptive statistical evaluation

indicates the distribution of samples and key variables (CSR) during 2010–2020. We can see that the sample size for 2010–2020 is on the rise, mainly because our sample selection is based on available CSR score data of listed firms. Since 2010, an increasing number of listed firms have begun to disclose CSR reports, increasing the availability of CSR score data.

Table 2. Distribution of 22725 samples and CSR from 2010 to 2020.

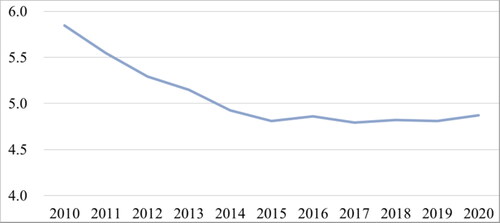

From 2010 to 2020, the CSR score was not stable, but it showed a downward trend overall. As shown in .

Figure 1. Line chart of the average score of CSR in 2010–2020.

Source: Authors compilation.

shows the descriptive information for given variables in the sample. Among them, the maximum value of CSR is 30, whereas the minimum value is −15, and the standard deviation is 4.322, indicating that the CSR level in China in the study sample is relatively low and there is a big difference between the specified companies. The highest value of GeoDis is 9.856, the lowest value is 0.042, while the average value is 8.3, which is close to the maximum. This indicates that the geographic distance between subsidiaries and subsidiaries of listed companies in the sample is relatively far and geographic dispersion is relatively common, which may be caused by the implementation of geographic diversification strategy by listed companies. The average value generated by IC is 6.473 and the highest value is 6.886, that shows the internal control qualities of Chinese listed companies are relatively good. The descriptive statistics of other control variables, respectively, reflect the financial status and corporate governance level of the sample companies.

Table 3. Descriptive statistics.

4.2. Multivariate analysis

Based on the hypotheses and the model, this study selected a fixed-effect model to examine and analyze the impact of parent-subsidiary companies’ geographic distance on CSR. Additionally, for reducing the heteroscedasticity within the groups and avoiding underestimated standard error, thereby generating misleading inferences, we cluster the standard errors at the firm level during regression, and obtained some effective research results.

4.2.1. Parent-subsidiary companies’ space geography distance and CSR

Without considering grouping and mediating effect, regression analysis was first conducted on the direct effect of the parent-subsidiary companies’ geographic distance on CSR in the full sample, and control variables were gradually increased. After the algorithm automatically dropped a singleton observation, the outcomes are depicted in .

Table 4. Parent-subsidiary companies’ geographic distances and CSR.

Column (1) in is the univariate regression results of parent-subsidiary companies’ geographic distance and corporate social responsibility without control variables. The results show that GeoDis has a negative correlation with CSR at the 1% significance level (p < 0.01, coefficient = −0.170). Columns (2) and (3) are the regression results after adding corporate financial characteristics and corporate governance variables. The results in both columns show that GeoDis and CSR are significantly negatively correlated at the 1% significance level, with coefficient values of −0.172 and −0.173, respectively. This result shows that a farther parent-subsidiary companies’ space geography distance of listed companies results in a more dispersed enterprise, a lower CSR score, which verifies hypothesis H1. The main reason for this result may be that the implementation of a geographic diversification strategy has resulted in the separation of parent and subsidiary companies in space geography, aggravating the information asymmetry and agency problems in enterprise groups, and fostering opportunistic behavior. Geographic dispersion causes the operating and management costs of enterprise groups to inevitably increase, resulting in a certain amount of internal resource consumption. Enterprises often reduce their investment in CSR to retain more idle resources (especially financial resources) to manage the increase in costs.

In addition, most of the control variables showed a significant relationship to CSR. Among the variables of corporate financial characteristics, size, age and profitability have a significant positive correlation with CSR at the levels of 1%, and operating capacity has significant positive correlated with CSR at the levels of 5%. This is because the amount of financial resources of enterprises determines their willingness and degree to participate in social responsibility practice, and enterprises with sufficient resources are more willing to fulfill social responsibility (Waddock & Graves, Citation1997). Similarly, when performing social responsibility, enterprises need to put forward higher requirements for operating capacity. The change of operating capacity will directly affect the implementation ability of enterprises. The improvement of operating capacity will not only contribute to the sustainable operation of enterprises, but also help enterprises better boost their social responsibility. Therefore, firms with larger assets, higher profitability, stronger operation ability, longer listing time have rich available resources, which provides a good foundation for the enterprise to fulfill its social responsibility.

4.2.2. Heterogeneity analysis

In order to test the difference in the influence of parent-subsidiary companies’ geographic distance on CSR under different samples, we conducted a heterogeneity test to verify Hypotheses H1a and H1b.

Firstly, according to the property right nature of the enterprises, the samples of the companies were divided into two groups i.e., enterprises owned by state and enterprises not owned by state for group testing. The regression results in show that for state-owned enterprises sample group, GeoDis is significantly negatively correlated with CSR at the level of 10%. For non-state-owned enterprises sample group, coefficient of GeoDis is −0.283 and significant at the level of 1%. These situations show that, in comparison to state-owned enterprises, there is negative impact of geographical distance between parent and subsidiary companies on CSR is more significant in non-state-owned enterprises. Therefore, hypothesis H1a is verified.

Table 5. Parent-subsidiary companies’ geographic distances, property nature and CSR.

Then, according to the city where the headquarters of the listed company is located, the company’s sample is divided into the eastern, central and the western regions for group testing. The eastern region consists of 11 provinces i.e., Beijing, Hebei, Shandong, Tianjin, Shanghai, Zhejiang, Liaoning, Jiangsu, Guangdong, Hainan and Fujian. The regression analysis is shown in . In the eastern region sample group, the coefficient of GeoDis is −0.187, which is significant at levels of 1%; while in the midwestern region sample group, the coefficient of GeoDis is only significant negatively at levels of 5%, while the coefficient is 0.127.This shows that compared with the eastern region, enterprises located in the midwestern regions have weakness in both significance and impact coefficient, and the negative impact of geographical distance between the parent-subsidiary companies’ geographic distance on CSR is more obvious in the eastern region. Therefore, hypothesis H1b is verified.

Table 6. Parent-subsidiary companies’ geographic distances, regional differences and CSR.

4.2.3. Mediating effect test of internal control

To verify whether the internal control truly plays an intermediary role in relation to parent-subsidiary companies’ geographic distance and CSR, we learn from the practices of some scholars, such as (Jia & Liu, Citation2014; Li & Zheng, Citation2018), using the three-step method when testing the mediation effect, regression model (2) and model (3). The regression results are shown in .

Table 7. Test results of intermediary effect.

The column (1) shows that IC and CSR are significantly positive at a level of 5% (p < 0.05, coefficient = 0.443), indicating that internal control has a endorsing effect on CSR. The Hypothesis H2 is verified. On this basis, we add variable internal control (IC) to model (1) to verify Hypothesis H3. Regardless of whether or not the regression coefficients of GeoDis are significant, the internal control has a mediating effect as long as the IC coefficient is significant. Column (2) of shows that the coefficient of the IC variable has significance at the 5% confidence level and positively correlated with CSR, whereas the coefficient of GeoDis has negative significance at 1% level. This indicates that internal control plays an intermediary role in the negative relationship between the parent-subsidiary companies’ geographic distance and CSR, which verifies Hypothesis H3. This is because, to some extent, the dispersion of parent-subsidiary companies in geographic distance hinders the effective operation of the internal control mechanism of enterprises, thus weakening the supervision and guarantee role of internal control on CSR.

4.2.4. Robustness test

To ensure the robustness of the main regression results, we carried out the robustness test by excluding the samples belonging to the municipality directly under the central government. On the one hand, when we calculate the parent-subsidiary companies’ geographic distance, it is mainly based on the prefecture-level city where each company is located, not the provincial city. The four municipalities (Beijing, Shanghai, Tianjin and Chongqing) are in the same class as the provinces, so the geographic distance calculated for the companies located in the municipalities may be biased. On the other hand, compared with the cities in other provinces, the municipal regions under direct control of central government have more developed economy, so there are naturally more companies registered and established in the municipal regions under direct control of central government. As a result, many enterprises headquartered in the municipal regions are part of the research sample.

To avoid the impact of this part of the sample on the entire regression result, we will remove it and then perform regression test again. As shown in , the parent-subsidiary companies’ geographic distance and CSR are significantly negative at the level of 1%, which is not substantially different from the previous regression results. Therefore, the main outcomes of proposed study are relatively robust.

Table 8. Robustness test: delete four municipalities.

5. Conclusions

5.1. Conclusions and discussions

CSR is a research hotspot of enterprise management. Although the existing studies are fruitful on CSR (Fiedler et al., Citation2021; Luo & Moon, Citation2021; Muhammad et al., Citation2019; Tang et al., Citation2020; Zaman et al., Citation2020), but most of these studies default that the parent companies and subsidiary companies are a whole and rarely analyze the impact of subsidiaries on CSR. There is even less literature on CSR from geographical perspective. Shi et al. (Citation2017) found that geographical dispersion has a negative impact on CSR, but his research is limited to the number of states where the company operates that data are too vague to represent geography. The research on the relationship between geographical distance of parent-subsidiary companies and CSR is still insufficient. This study uses the data of Chinese A-share listed companies from 2010 to 2020 to investigate the impact mechanism of geographical distance between parent and subsidiary companies on corporate social responsibility and the intermediary effect of internal control. Conclusions and discussions of our research are as follows:

Firstly, the results show that parent-subsidiary companies’ geographic distance is negatively related to CSR. Perhaps due to the limitation of subsidiary data, there is a lack of existing research on the relationship between parent-subsidiary companies’ geographical distance and CSR. This study matches multiple databases to collect samples and data of subsidiaries of Chinese A-share listed enterprises, which proves that geographical distance of parent-subsidiary companies has a negative impact on CSR. Geographical distance will lead to the increase of agency cost and information asymmetry (Cashman et al., Citation2019; El Ghoul et al., Citation2013), which provides space for the opportunism of subsidiaries, and the decision to maximize the interests of subsidiaries may hinder the CSR of the parent company. This paper breaks through the research status of treating parent companies and subsidiary companies as a whole, and studies the impact of geography on CSR according to the geographical characteristics of paren-subsidiary companies. We adopted the actual geographical distance of parent-subsidiary companies, which is an upgrade and improvement of Shi et al.s’ (2017) research.

Second, further analysis shows that the negative impact of parent-subsidiary companies’ geographical distance on CSR is more noticeable for non-state-owned enterprises and eastern enterprises in China. It can be said that state-owned enterprises preserve CSR out of ‘nature’ (Wang et al., Citation2019), the decisive influence of the government weakens the affection of geographical distance on state-owned enterprises’ CSR. The degree of marketization in eastern China is higher, thus main factors impacting CSR are the enterprises themselves, which lead the negative affection of geographical distance is fully reflected. However, the Midwest regions are on the contrary. These conclusions have vital contributions to the study of the social role of state-owned enterprises and the regional differences of Chinese enterprises.

Thirdly, internal control plays an intermediary role. The geographical distance of parent-subsidiary companies is negatively correlated with internal control, and internal control is positively correlated with CSR. Geographical distance increases the difficulty for the parent company to obtain the information of subsidiaries, reduces the parent company’s supervision over subsidiaries, weakens the enterprise’s internal control, and finally has an adverse impact on CSR. These conclusions reveal the influence path of parent-subsidiary companies’ geographical distance on CSR, and also enlightens enterprise managers to improve CSR by strengthening the control of subsidiaries.

5.2. Policy suggestions

For enterprises. First of all, enterprises manager should reasonably implement the diversification strategy, avoid blindly seeking expansion in other places, reasonably distribute subsidiaries companies. The geographical distance of parent-subsidiary companies beyond the limit will increase the enterprise cost, reduce the execution efficiency, and is not conducive to CSR. Second, in the process of cross regional operation, listed companies should strengthen the management control and information communication of their subsidiaries, so as to reduce the information asymmetry and internal control failure caused by regional expansion. Facing the challenge of geographical diversification, enterprises should further improve digital information technology and adopt information means to resist the negative impact of parent-subsidiary companies’ geographical distance on CSR. Parent companies should make full use of Internet, reinforce the connection with subsidiary companies, ensure the timeliness of information, and realize a high integration under geographical dispersion. Third, when implementing a diversification strategy, enterprises should pay more attention to the construction of internal control. These enterprises should upgrade their internal control system, ensure the effectiveness of internal control and enfeeble the adverse effect of geographical distance on CSR. Fourth, enterprises should reinforce the awareness of CSR, take CSR as an crucial content of corporate culture construction, and integrate CSR into corporate strategy and decision-making.

Many enterprises regard CSR as an additional burden and adopt an evasive attitude towards social responsibility. Therefore, the government should guide enterprises to promote CSR through effective measures. First, it is necessary to improve the relevant legal system, accelerate the legalization of CSR, advance the legal and regulatory system related to CSR, strengthen supervision of government, and take administrative or legal means to punish enterprises that violate laws and regulations. Second, the government should integrate enterprise interests and social interests. For enterprises that actively fulfill their social responsibilities and participate in public welfare activities, the government can effectively unify enterprise interests and social interests through government procurement, tax preference, financing support and other incentive measures. Third, the government should arrange special supervision on the enterprises that have a great deal of subsidiaries in different regions because of regional diversification strategy. Government can conductor these enterprise managers to enhance internal control and strengthen the supervision of subsidiaries, so as to tremendously accelerate CSR.

However, our study still has a few limitations. First, in view of the available of firm data, the sample for this study only includes A-share listed companies in China and has yet to examine the contents of growth enterprises market board- and small and medium board-listed companies. Second, this research only investigates the effect of geographic distance on CSR, but does not include institutional distance and cultural distance. Therefore, in future research, we will further expand the research sample, and focus on exploring the impact of institutional distance and cultural distance between parent and subsidiary companies on corporate social responsibility.

Disclosure statement

The authors declare no conflict of interest.

Additional information

Funding

Notes

1 Shenzhen DIB risk management consulting company provides Chinese listed companies internal control data, after excluding the value of 0 and data missing samples, there are 25,225 data from 2010 to 2020. The calculation method of internal index equal to 0 is inconsistent with that of other indexes, so the value of 0 is excluded.

2 Hexun Information Network (http://www.hexun.com) is an independent financial portal in China. It provides financial information and global financial market information for all participants in the capital markets, especially investors. It has a certain authority. Since 2010, Hexun.com has professionally ranked the CSR for Chinese listed enterprises from their annual financial reports and listed companies’ independent social responsibility reports and published the outcomes of the ratings publicly. The evaluation system calculates measurements using five responsibility aspects: employee responsibility, customer-supplier and consumer rights responsibility, shareholder responsibility, social responsibility, and environmental responsibility. By assigning values to different indicators, the social responsibility index and various sub-indices are calculated.

3 The full name of CSRC is the China Securities Regulatory Commission. It is a ministerial level institution directly under the State Council. In accordance with laws, regulations and the authorization of the State Council, it uniformly supervises and manages the national securities and futures market, maintains the order of the securities and futures market and ensures its legal operation.

References

- Ayari, N. (2010). Geographic distance and R&D activities of subsidiaries located in Spain. Region et Developpement, 32, 203–224.

- Bárcena-Ruiz, J. C., & Sagasta, A. (2021). Cross-ownership and corporate social responsibility. The Manchester School, 89(4), 367–384. https://doi.org/10.1111/manc.12363

- Boeprasert, A. (2012). Does geographical proximity affect corporate social responsibility? Evidence from US market. International Business Research, 5(9), 138. https://doi.org/10.5539/ibr.v5n9p138

- Boubaker, S., Chkir, I., Chourou, L., & Saadi, S. (2019). Does geographic location matter to stock return predictability? Journal of Forecasting, 38(4), 311–326. https://doi.org/10.1002/for.2556

- Buchholtz, A. K., Amason, A. C., & Rutherford, M. A. (1999). Beyond resources: The mediating effect of top management discretion and values on corporate philanthropy. Business & Society, 38(2), 167–187. https://doi.org/10.1177/000765039903800203

- Cahan, S. F., Chen, C., Chen, L., & Nguyen, N. H. (2015). Corporate social responsibility and media coverage. Journal of Banking & Finance, 59, 409–422. https://doi.org/10.1016/j.jbankfin.2015.07.004

- Cashman, D., Harrison, M., Seiler, J., & Sheng, H. (2019). The impact of geographic and cultural dispersion on information opacity. The Journal of Real Estate Finance and Economics, 59(2), 143–166. https://doi.org/10.1007/s11146-017-9607-2

- Chang, K., Kabongo, J., & Li, Y. (2021). Geographic proximity, long-term institutional ownership, and corporate social responsibility. Review of Quantitative Finance and Accounting, 56(1), 297–328. https://doi.org/10.1007/s11156-020-00895-9

- Chen, C., Wan, S., & Zhu, L. (2019). SOE executive compensation and corporate social responsibility – The moderating effect of organizational slack and the market process. China Soft Science, 06, 129–137.

- Chen, W., Zhou, G., & Zhu, X. (2019). CEO tenure and corporate social responsibility performance. Journal of Business Research, 95, 292–302. https://doi.org/10.1016/j.jbusres.2018.08.018

- Chijoke-Mgbame, M., Mgbame, O., Akintoye, S., & Ohalehi, P. (2019). The role of corporate governance on CSR disclosure and firm performance in a voluntary environment. Corporate Governance: The International Journal of Business in Society, 20(2), 294–306. https://doi.org/10.1108/CG-06-2019-0184

- Davide, C., & Joana, A. (2021). Geographic diversification and credit supply in times of trouble: Evidence from microlending. Journal of Business Research, 132, 848–859. https://doi.org/10.1016/j.jbusres.2020.10.071

- El Ghoul, S., Guedhami, O., Nash, R., & Patel, A. (2019). New evidence on the role of the media in corporate social responsibility. Journal of Business Ethics, 154(4), 1051–1079. https://doi.org/10.1007/s10551-016-3354-9

- El Ghoul, S., Guedhami, O., Ni, Y., Pittman, J., & Saadi, S. (2013). Does information asymmetry matter to equity pricing? Evidence from firms’ geographic location. Contemporary Accounting Research, 30(1), 140–181. https://doi.org/10.1111/j.1911-3846.2011.01147.x

- Fahad, S., & Wang, J. (2018). Farmers’ risk perception, vulnerability, and adaptation to climate change in rural Pakistan. Land Use Policy, 79, 301–309. https://doi.org/10.1016/j.landusepol.2018.08.018

- Fahad, S., & Wang, J. (2020). Climate change, vulnerability, and its impacts in rural Pakistan: a review. Environmental Science and Pollution Research International, 27(2), 1334–1338. https://doi.org/10.1007/s11356-019-06878-1

- Fan, J. P., Wong, T. J., & Zhang, T. (2014). Politically connected CEOs, corporate governance, and the post‐IPO performance of China's partially privatized firms. Journal of Applied Corporate Finance, 26(3), 85–95. https://doi.org/10.1111/jacf.12084

- Faraudello, A., Seddio, P., & Songini, L. (2020). The why and how of corporate social responsibility in family business: a literature review. International Journal of Transitions and Innovation Systems, 6(4), 1. https://doi.org/10.1504/IJTIS.2020.10033282

- Fernandez-Feijoo, B., Romero, S., & Ruiz, S. (2012). Does board gender composition affect corporate social responsibility reporting. International Journal of Business and Social Science, 3, 31–38.

- Fiedler, I., Kairouz, S., & Reynolds, J. (2021). Corporate social responsibility vs. financial interests: the case of responsible gambling programs. Journal of Public Health, 29(4), 993–1000. https://doi.org/10.1007/s10389-020-01219-w

- Finegold, D., Klossek, A., Nippa, M., & Winkler, A. L. (2010). Explaining firm approaches to corporate social responsibility: institutional environment and firm size. European Journal of International Management, 4(3), 213–233.

- Fitania, D. N., & Firmansyah, A. (2020). The effect of geographic diversification, competition level, and corporate governance on risk disclosure. International Journal of Scientific & Technology Research, 9(3), 366–372.

- Garas, S., & ElMassah, S. (2018). Corporate governance and corporate social responsibility disclosures: The case of GCC countries. Critical Perspectives on International Business, 14(1), 2–26. https://ssrn.com/abstract=3140229 https://doi.org/10.1108/cpoib-10-2016-0042

- Guo, M., & Zheng, C. (2021). Foreign ownership and corporate social responsibility: Evidence from China. Sustainability, 13(2), 508. https://doi.org/10.3390/su13020508

- Hafsi, T., & Turgut, G. (2013). Boardroom diversity and its effect on social performance: Conceptualization and empirical evidence. Journal of Business Ethics, 112(3), 463–479. https://doi.org/10.1007/s10551-012-1272-z

- Huang, H., & Zhao, Z. (2016). The influence of political connection on corporate social responsibility – Evidence from listed private companies in China. International Journal of Corporate Social Responsibility, 1(1), 1–19. https://doi.org/10.1186/s40991-016-0007-3

- Huimin, G., & Ryan, C. (2011). Ethics and corporate social responsibility – An analysis of the views of Chinese hotel managers. International Journal of Hospitality Management, 30(4), 875–885. https://doi.org/10.1016/j.ijhm.2011.01.008

- Ioannou, I., & Serafeim, G. (2012). What drives corporate social performance? The role of nation-level institutions. Journal of International Business Studies, 43(9), 834–864. https://doi.org/10.1057/jibs.2012.26

- Ji, H., Miao, Z., & Zhou, Y. (2020). Corporate social responsibility and collaborative innovation: The role of government support. Journal of Cleaner Production, 260(6), 121028. https://doi.org/10.1016/j.jclepro.2020.121028

- Jia, X., & Liu, Y. (2014). External environment, internal resource and corporate social responsibility. Nankai Business Review, 17, 13–18.

- Kim, M., & Kim, Y. (2014). Corporate social responsibility and shareholder value of restaurant firms. International Journal of Hospitality Management, 40, 120–129. https://doi.org/10.1016/j.ijhm.2014.03.006

- Lee, S., Singal, M., & Kang, K. H. (2013). The corporate social responsibility–financial performance link in the U.S. restaurant industry: Do economic conditions matter? International Journal of Hospitality Management, 32, 2–10. https://doi.org/10.1016/j.ijhm.2012.03.007

- Levine, R., Lin, C., & Xie, W. (2021). Geographic diversification and banks' funding costs. Management Science, 67(5), 2657–2678. https://doi.org/10.1287/mnsc.2020.3582

- Li, B. (2015). Parent-subsidiary companies distance, internal control quality and corporate value. Economy and Management, 37(4), 95–105.

- Li, Q., & Liu, S. M. (2007). A motive study of listed companies diversification. Journal of South China Normal University (Social Science Edition), 5, 49–56.

- Li, X., & Olorunniwo, F. (2008). An exploration of reverse logistics practices in three companies. Supply Chain Management: An International Journal, 13(5), 381–386. https://doi.org/10.1108/13598540810894979

- Li, L., Wang, Z., & Kan, L. (2019). Internal control and corporate social responsibility performance: Mediating effect test based on agency cost. Nanjing Audit University, 16, 28–36.

- Li, B., & Zheng, W. (2018). Parent-subsidiary companies' distance, risk-taking and firm efficiency. Business Management Journal, 40(04), 50–68.

- Luo, J., & Moon, J. (2021). Airline chief executive officer and corporate social responsibility. Sustainability, 13(15), 8599. https://doi.org/10.3390/su13158599

- Mammen, J., Alessandri, T. M., & Weiss, M. (2021). The risk implications of diversification: Integrating the effects of product and geographic diversification. Long Range Planning, 54(1), 101942. https://doi.org/10.1016/j.lrp.2019.101942

- Manner, M. (2010). The impact of CEO characteristics on corporate social performance. Journal of Business Ethics, 93(S1), 53–72. https://doi.org/10.1007/s10551-010-0626-7

- McCarthy, S., Oliver, B., & Song, S. (2017). Corporate social responsibility and CEO confidence. Journal of Banking & Finance, 75, 280–291. https://doi.org/10.1016/j.jbankfin.2016.11.024

- Muhammad, A. N., Jun, L., Ramiz, U. R., Muhammad, I. A., & Rizwan, A. (2019). Moderating role of financial ratios in corporate social responsibility disclosure and firm value. Plos One, 14(4), e0215430. https://doi.org/10.1371/journal.pone.0215430

- Nerlove, M., & Balestra, P. (1992). Formulation and estimation of econometric models for panel data. The econometrics of panel data. Advanced Studies in Theoretical and Applied Econometrics, 28, 3–18. https://doi.org/10.1007/978-94-009-0375-3_1

- Neumark, D., & Wascher, W. (1992). Employment effects of minimum and subminimum wages: Panel data on state minimum wage laws. Industrial and Labor Relations Review, 46(1), 55–81. https://doi.org/10.2307/2524738

- Nguyen, T. H., Vu, Q. T., Nguyen, D. M., & Le, H. L. (2021). Factors influencing corporate social responsibility disclosure and its impact on financial performance: The case of Vietnam. Sustainability, 13(15), 8197. https://doi.org/10.3390/su13158197

- Okafor, E., & Ujah, U. (2020). Executive compensation and corporate social responsibility: Does a golden parachute matter? International Journal of Managerial Finance, 16(5), 575–598. https://doi.org/10.1108/IJMF-12-2018-0379

- Ozturk, I. (2011). The macroeconomic effects of IMF programs in MENA countries. African Journal of Business Management, 5(11), 4379–4387.

- Ozturk, I. (2016). The relationships among tourism development, energy demand and growth factors in developed and developing countries. International Journal of Sustainable Development & World Ecology, 23(2), 122–131. https://doi.org/10.1080/13504509.2015.1092000

- Ozturk, I. (2017). The dynamic relationship between agricultural sustainability and food energy-water poverty in a panel of selected Sub-Saharan African countries. Energy Policy, 107, 289–299. https://doi.org/10.1016/j.enpol.2017.04.048

- Quan, X., Wu, S., & Yin, H. (2015). Corporate social responsibility and stock price crash risk: Self-interest tool or value strategy? Economic Research Journal, 50(11), 49–64.

- Rao, K., & Tilt, C. (2016). Board diversity and CSR reporting: An Australian study. Meditari Accountancy Research, 24(2), 182–210. https://doi.org/10.1108/MEDAR-08-2015-0052

- Ratri, C., Harymawan, I., & Kamarudin, A. (2021). Busyness, tenure, meeting frequency of the CEOs, and corporate social responsibility disclosure. Sustainability, 13(10), 5567. https://doi.org/10.3390/su13105567

- Ríos-Manríquez, M., Ferrer-Ríos, M. G., & Sánchez-Fernández, M. D. (2021). Structural model of corporate social responsibility. An empirical study on Mexican SMEs. Plos One, 16(2), e0246384–22. https://doi.org/10.1371/journal.pone.0246384

- Rosnan, H., Saihani, S. B., & Yusof, N. M. (2013). Attitudes towards corporate social responsibility among budding business leaders. Procedia – Social and Behavioral Sciences, 107, 52–58. https://doi.org/10.1016/j.sbspro.2013.12.398

- Ruangviset, J., Jiraporn, P., & Kim, J. (2014). How does corporate governance influence corporate social responsibility? Procedia – Social and Behavioral Sciences, 143, 1055–1057. https://doi.org/10.1016/j.sbspro.2014.07.554

- Shi, G., Sun, J., & Luo, R. (2015). Geographic dispersion and earnings management. Journal of Accounting and Public Policy, 34(5), 490–508. https://doi.org/10.1016/j.jaccpubpol.2015.05.003

- Shi, G., Sun, J., Zhang, L., & Jin, Y. (2017). Corporate social responsibility and geographic dispersion. Journal of Accounting and Public Policy, 36(6), 417–428. https://doi.org/10.1016/j.jaccpubpol.2017.09.001

- Song, J., & Kang, H. (2019). The moderating effect of CEO duality on the relationship between geographic diversification and firm performance in the US lodging industry. International Journal of Contemporary Hospitality Management, 31(3), 1488–1501. https://doi.org/10.1108/IJCHM-12-2017-0848

- Soschinski, K., Giordani, M., Klann, C., & Brizolla, M. (2021). Influence of national culture on corporate social responsibility. CrossCultural Management Journal, 1, 71-88.

- Sotorrío, L. L., & Sánchez, J. L. F. (2008). Corporate social responsibility of the most highly reputed European and North American firms. Journal of Business Ethics, 82(2), 379–390. https://doi.org/10.1007/s10551-008-9901-2

- Su, J., & He, J. (2010). Does giving lead to getting? Evidence from Chinese private enterprises. Journal of Business Ethics, 93(1), 73–90. https://doi.org/10.1007/s10551-009-0183-0

- Subramaniam, V., & Wasiuzzaman, S. (2019). Geographical diversification, firm size and profitability in Malaysia: A quantile regression approach. Heliyon, 5(10), e02664. https://doi.org/10.1016/j.heliyon.2019.e02664

- Tang, P., Yang, S., & Yang, S. (2020). How to design corporate governance structures to enhance corporate social responsibility in China's mining state-owned enterprises? Resources Policy, 66, 101619. https://doi.org/10.1016/j.resourpol.2020.101619

- Von Zedtwitz, M., & Gassmann, O. (2002). Market versus technology drive in R&D internationalization: Four different patterns of managing research and development. Research Policy, 31(4), 569–588. https://doi.org/10.1016/S0048-7333(01)00125-1

- Waddock, S. A., & Graves, S. B. (1997). The corporate social performance–financial performance link. Strategic Management Journal, 18(4), 303–319. https://doi.org/10.1002/(SICI)1097-0266(199704)18:4<303::AID-SMJ869>3.0.CO;2-G

- Wang, J. (2012). Corporate social responsibility and internal control: Interactive relationship and optimization path research. Communication of Finance and Accounting, 9, 13–15.

- Wang, J., & Shen, X. (2012). Corporate social responsibility and internal control: interactive relationship and optimization path research. Communication of Finance & Accounting, 9, 13–15. https://doi.org/10.16144/j.cnki.issn1002-8072.2012.09.025

- Wang, F., Sun, J., & Liu, Y. S. (2019). Institutional pressure, ultimate ownership, and corporate carbon reduction engagement: Evidence from China. Journal of Business Research, 104, 14–26. https://doi.org/10.1016/j.jbusres.2019.07.003

- Yang, J. (2019). Internal control, double agency costs and corporate social responsibility. Open Journal of Social Sciences, 07(09), 155–167. https://doi.org/10.4236/jss.2019.79012

- Zaman, R., Jain, T., Samara, G., & Dima, J. (2020). Corporate governance meets corporate social responsibility: Mapping the interface. Business & Society, 000765032097341. https://doi.org/10.1177/0007650320973415

- Zyglidopoulos, S. C., Georgiadis, A. P., Carroll, C. E., & Siegel, D. S. (2012). Does media attention drive corporate social responsibility? Journal of Business Research, 65(11), 1622–1627. https://doi.org/10.1016/j.jbusres.2011.10.021