?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

A green and sustainable business environment has gained the attention of recent researchers and policymakers due to environmental and social issues globally. Therefore, the present research investigates the impact of corporate social responsibilities (CSR), green investment, green credit, and assets return on the stock return of the Chinese export industry. This study has taken the ten top export companies from China using the database of the Shanghai stock exchange. This study collected data from financial statements and stock exchange databases from 2009 to 2020. This study has used panel data analysis techniques such as robust standard error and fixed effect model (FEM) to examine the relations among the variables. The results revealed that CSR, green investment, green credit, and return on assets have a significant and positive association with the stock return of selected industries. These results imply that CSR instigates higher financial performance in the export industry; thus, improving CSR and sustainable financing promote socio-economic and societal development.

1. Introduction

The augmentation of business sustainability has become a pressing need for companies to attain an exceptional place in society and market both at the national or international level, especially when people are getting aware of social and requirements (Chien et al., Citation2021; He et al., Citation2021). Business sustainability occurs when a company carries on its operations without disturbing the balance or damaging the quality of society and the environment. A sustainable business undertakes its activities in the best interest of society and the environment (Baloch et al., Citation2021; Caldera et al., Citation2018). An environmentally and socially conscious firm focuses more than simply on profits; it also analyses the effects of its activities on society and the environment (Khan et al., Citation2021; Wang et al., Citation2021). A business like this can be considered sustainable since it contributes to the social and environmental safety of the community in which it operates, hence contributing to creating an environment in which the business can flourish (Razzaq et al., Citation2021b; Xuefeng et al., Citation2021). There is serious competition in the market, where customers want the required products and want social safety and environmental protection from companies. People like to do business with companies that put a high priority on quality. People prefer to do business with companies concerned about the general public's social and environmental requirements, as well as regulatory bodies (Sun et al., Citation2021; Zhuang et al., Citation2021).

The triple bottom line concept, coined by John Elkington, described sustainability to determine the business's long-term sustainability. This model comprises three components society, environment, and profits (An et al., Citation2021; Tseng et al., Citation2019). A sustainable company earns profits demonstrating responsibility towards the community and protecting environmental resources (Cosenz et al., Citation2020; Ling et al., Citation2021). The current study aims to analyze the interrelationship between the stock return, CSR strategy, green credit, and green investment in China. The study researches the underlying factors and sustainable business in the top ten export companies listed in the stock exchange of China. The Chinese growth rate is estimated to be 8.5 percent by 2021, and the country's gross domestic product will be $16.64 trillion in 2021. Total exports of the country will be $2.59 trillion in 2020. The primary industries of China are mining, oil processing, steel, aluminum, coal, machine building, textiles, petroleum, chemicals, and automobiles, financial services, and railcars, etc. (Ngai et al., Citation2018). China is one of the most exporting countries around the globe, but currently, the Chinese exports industry survives; that's why this study examines the top ten exporting companies (Ding et al., Citation2019). Some statistics related to the exports and imports of the Chinese economy are given in .

Figure 1. Exports and imports of China.

Source: General Administration of Customs of the P.R. China.

When a business achieves and maintains social, environmental, ad financial performance, it can create and enhance sustainability. Business sustainability, which combines consistent social, environmental, and economic performance and helps drive a sustainable position in the market, can be derived through some significant elements (Freudenreich et al., Citation2020; Sharif et al., Citation2020). Researchers have paid great attention to drivers of business sustainability to provide a guideline to the businesses on how they can enhance business sustainability (Ding et al., Citation2021). This study aims to check the relationship between the three factors: CSR strategy, green credit, and green investment on stock return. An in-depth analysis of the like CSR strategy, green credit, and green investment and their role in achieving business sustainability is intended to be made. This research is an extension to the studies which have already discussed green credit and green investment as a whole in the form of green finance while addressing the predictors of sustainable business as the study of Ngai et al. (Citation2018) has described the influences of green finance, including green securities, green credit, and green investment collectively as the predictor of business sustainability. But our study tries to describe the influences of green credit and green investment on stock return. In the existing literature, either the research has been conducted on CSR as a predictor of sustainable business (stock return), while green credit and green investment as contributors to sustainable business (stock return) (Shahzad et al., Citation2020b; Citation2021b). The study of Bellucci et al. (Citation2020) has addressed the impacts of CSR on sustainable business but shown the need to pay attention to the influence of green credit and green investment on stock return. Likewise, the study of Risi (Citation2020) has explored the relationship of green credit and green investment with sustainable business. Still, it shows the lack of association between CSR and sustainable business. Thus, the cumulative measurement of sustainable business through CSR, green credit, and green investment dramatically contributes to the literature on business sustainability. The analysis of the nexus between CSR implementation, green credit, and green investment and business in the economy of China is also an addition to the literature.

This study is structured into different portions. After the introduction, the second portion of the study is a literature review that deals with the authors' arguments presented in the past studies about the influences of CSR strategy, availability of green credit, and undertaking of green investment on stock return which enhance the performance of the sustainable business. The third section describes how the authors collected the quantitative data for further analysis. Then, in the fourth portion of the study, results are developed from analyzing the influences of CSR strategy, availability of green credit, and green investment on sustainable business (stock return). In the last portion, through appropriate discussion, the study results are approved by the previously conducted studies, implications, conclusions, and limitations of the study are described.

2. Literature review

Business sustainability refers to a company's activities to operate its functions and operations in a way that they do not put harmful effects on the environment or the health of its customers while also improving social relations with stakeholders (Li et al., Citation2021). According to Bocken et al. (Citation2019) highly sustainable firm maintains its policies, strategies, and operations to maximize revenues while protecting the natural environment, thereby benefiting all stakeholders. Business sustainability maintains the firms' position in the market by retaining its capacity to compete against rival businesses (Shahzad et al., Citation2021a). Some business approaches and financial policies are formulated and executed considering the environmental concerns of government regulatory authorities, the general public, and customers. CSR is the business self-regulatory approach that aims to contribute to social and ecological goals while performing business activities (Shahzad et al., Citation2020b). The effective execution of CSR minimizes the negative social and environmental impacts of business activities (De Stefano et al., Citation2018; Sun et al., Citation2021). Besides, the green integration in the financial policies like green credit, green securities, and green investment is also a powerful tool to remove the negative industrial or manufacturing impacts from the environment. That is why CSR and green finance enhances business sustainability. The effects of CSR, green credit, and green investment on business sustainability have a dominant place in the literature. The study presents its concepts with the help of the arguments of past authors.

The research was conducted by Bajic and Yurtoglu (Citation2018) to investigate the interrelationship between CSR, firms' value, and market share. Research design examines observational data with the help of panel data methods along with ordinary least squares methods, firm-fixed effect, and firm-random effect. The data has been acquired from thirty-five countries over 2003–2016. This study analyzes the firms' value and market capturing from the three aspects of CSR's environmental, social, and corporate governance. The study demonstrates that the firms have competitive advantages like more active human resources, good quality resources, a good relationship with the stakeholders, and more productivity (Razzaq et al., Citation2021a; Shahzad et al., Citation2020a). These competitive advantages help the firm to capture the market. A research study was conducted by Sanclemente-Téllez (Citation2017) to seek the relationship between CSR concept and marketing with the presentation of the classification of several theoretical perspectives based on which these two predictors are interrelated. This study states that when organizations apply CSR, they have intact relations with the stakeholder (suppliers, employees, and customers), which help respond to market shifts, corporate agency requirements, and customers' desires. Thus, appropriately, the study shows that CSR has a positive relation to market capture. In a scholarly article, Zahari et al. (Citation2020) test the role of CSR, financial-based brand equity, and marketing performance of the firms for the economy of Malaysia. The study selected the top 100 brands in Malaysia and used the CSR checklist instrument to test the extent of CSR practice. The study's findings posit that the effective implementation of CSR practices leads to social and environmental performance and financial performance, improving brand equity and making it possible to have high market capturing (Ding et al., Citation2020). Through a study, the authors Cazeri et al. (Citation2018) assess the association between CSR practices and management systems for the economy of Brazil, aiming at sustainability in firms. A mixed approach (qualitative and quantitative) was used to collect data through the electronic distribution of questionnaires to 148 experts. The study posits that CSR implementation improves the organizational management system, resulting in business effectiveness, raising competitive advantages, and driving high business sustainability.

A literary article was presented by He et al. (Citation2019), to examine green credit, renewable energy resources, sustainable business, and sustainable economy and their mutual impacts. The study chose renewable energy firms (the enterprises that deal in or employ renewable energy resources) of China's A-share market as the sample for collecting data for 2004–2015. LLC test, AD fisher test, PP fisher test, and co-integration test were applied for analyzing the data and extracting results about the nature of the relationship among green credit, renewable energy resources, sustainable business, and sustainable economy. Their results indicate that green credit encourages the production and usage of renewable energy resources, enhancing sustainability in business development and economic growth (Irfan et al., Citation2021; Sharif et al., Citation2019). Empirical research was made by Wang et al. (Citation2019) in China to show the significance of green credit policy from the environmental and economic points of view. A panel data for the period of 2008–2016 from 320 companies in badly polluting industries listed in the Shanghai stock exchange. The fixed effects regression model was applied to examine the influence of green credit policy on environmental quality and business sustainability. According to the study results, the use of green credit protects the environment for the general public and improves the work environment quality for the labor force.

Consequently, there is a large amount of productivity and marketing, which enhances business sustainability. The study of Hu et al. (Citation2020) was conducted to explore the impacts of green credit on industrial structure and sustainable business development on an individual level. An empirical research design was applied, and data from eastern, central, and western China were collected from 2006 to 2016. The fixed-effects model was constructed to extract the association between green credit, industrial structure, and sustainable business development. The results reveal that green credit has brought a positive change in the industrial structure. Many industries are going towards environmentally friendly improvement in business operations, which creates sustainability in business development. The study presented by Ng (Citation2018) examines green finance development and its significance in sustainable business enhancement. Multiple case-study approaches were applied for data collection. Three cases of sizeable listed enterprises in Hong Kong Global Financial Centre of China (GFCC), a regional green finance hub, were taken to extract results. The study implies that green credit has a positive influence on business sustainability.

The literary investigation by Guo et al. (Citation2020) tests the green investment in different sorts of technology used in economic activities and their influence on sustainable business development. During the investigation in Paris, 2453 green technologies were chosen as examples. These technologies are divided into five categories: environment quality, energy consumption, resource consumption, ecological safety, life health, and 30 secondary and 87 tertiary categories. The study posits that the investment in green technologies that do not negatively impact the environment while being operated improves the environment quality, gives more production with the same resources, adds value to the products and services, and saves resources for future use (Shahzad et al., Citation2021b). This improves environmental, social, and financial performance at the same time. The study was conducted by Shen et al. (Citation2021) to test the association of green investment, natural resource rent, energy consumption, and financial progress with carbon emission and sustainable business enhancement. A cross-sectional panel data were acquired from enterprises in Chinese 30 provinces for the time 1995–2017. Augmented autoregressive distributive lags (ARDL) methodology was applied to analyze the association between the aforementioned factors and carbon emission. The study represents that the investment in business activities to bring green improvement reduces the emission of harmful gases like carbon dioxide, damaging living beings' environmental quality and health. This initiative improves business performance and enhances business sustainability. Zhang et al. (Citation2020) check how the manufacturers tend to make green investments in competitive marketing as a common retailer. The data to infer the role of green investment in enhancing business sustainability were acquired from manufacturing enterprises through questionnaires. The study implies that the investment in ecological friendly resources like environmentally friendly technology employed in all organizational areas like operations, production, and marketing, develops agility in all processes, improves quality products, and enhances customers' confidence. Thus, green investment leads to sustainability in the business. Wang et al. (Citation2020), investigate the influences of green investment, carbon emission, environmental protection, and business sustainability. Time series data from 1998 to 2017 were acquired from Chinese enterprises to analyze the influences of green investment, carbon emission, environmental protection, and business sustainability. This study applied the autoregressive distributed lag model (ARDL) technique for co-integration. The green investment reduces the emission of carbon into the air and contributes to business sustainability by protecting natural resources for future use.

3. Methodology

This article investigates the impact of CSR and green investment, green credit on stock return in Chinese business environments. This study has taken the ten top exporting companies from each country using the Shanghai stock exchange database. This study has collected the data from selected companies' financial statements and stock exchange databases from 2009 to 2020. This study has used panel data analysis techniques such as robust standard error and FEM to examine the relations among the variables. The estimation equation of the understudy variables is given as under:

(1)

(1)

where SR represents Stock Return, i mean Company, t for time period, CSR shows Corporate Social Responsibility, GC means Green Credit, GI represents Green Investment, ROA means Return on Assets. This study has taken the stock return as the measurement of the sustainable business enhancement and calculated by the log of changes in the stock return. In addition, the study has taken three predictors: CSR measured as the ratio of CSR expenses and total expenses, green credit measured as the ratio of green credit and total credit, and green investment measured as the ratio of green investment and total investment. Finally, the present study also used the return on assets as the control variable and measured as the ratio of net income and total assets. These measurements are shown in .

Table 1. Measurements of variables.

The study has examined the descriptive statistics showing the constructs' standard deviation, mean values, and minimum and maximum values. In addition, this article has also shown the correlation matrix that shows the nexus among the constructs. Moreover, this research also executed the variance inflation factor (VIF) to check the multicollinearity assumption. The VIF equations are as follow:

(2)

(2)

(3)

(3)

(4)

(4)

The current article has used the Hausman test to check the appropriate model among fixed and random models. If the probability value shows less than 0.05, then the FEM is appropriate and vice versa. The current article executed the FEM, and the equation is given as under:

(5)

(5)

The subscript (i) in the above equation represented the individual company and made the different companies according to their characteristics. In addition, FEM refers to a regression model in which the ‘group means are fixed’ instead of a random-effects model in which the group means are a random sample from a population. FEM equation by using understudy variables as under:

(6)

(6)

Finally, the relation among the variables has also been examined by using the robust standard error because it adjusts the model's heterogeneity issues that generally exist. The equation for robust standard error with understudy variables is as under:

(7)

(7)

4. Results of the study

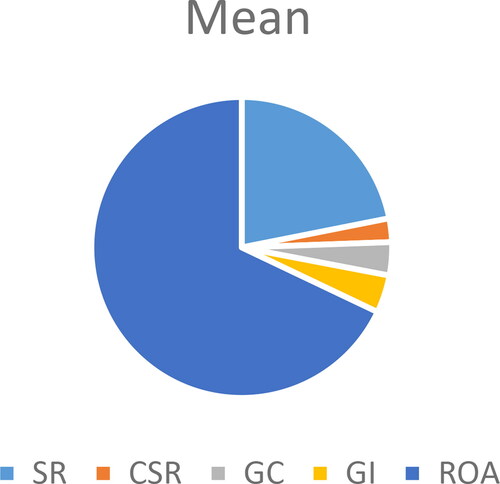

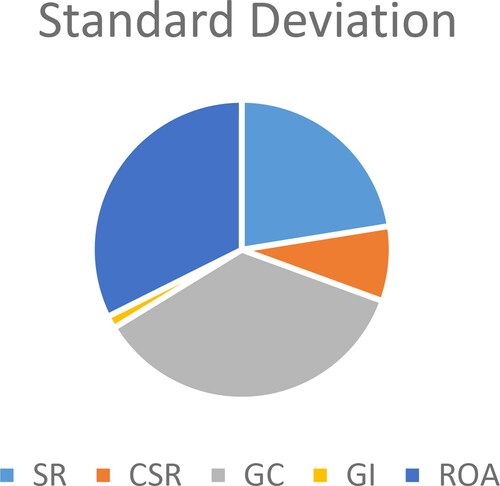

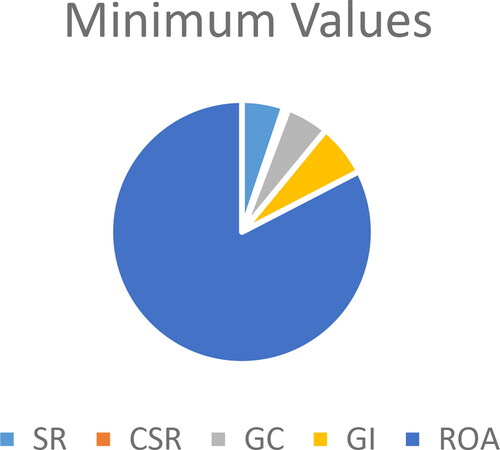

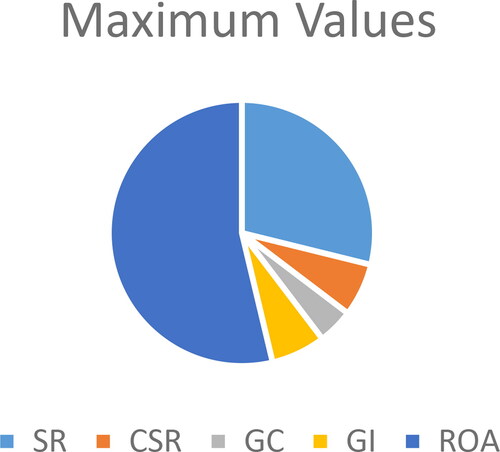

The study results section includes the descriptive statistics, correlation matrix, VIF, Hausman test and FEM, and robust standard error. Firstly, the study has examined the descriptive statistics showing the standard deviation, mean values, and minimum and maximum values of the constructs. The mean value of SR is 1.620, while CSR is 0.188. In addition, the average value of GC is 0.264, while the average value of GI is 0.301 and the average value of ROA is 5.028. These values are mentioned in and .

Figure 2. Mean values.

Source: Author’s calculation.

Figure 3. Standard deviations.

Source: Author’s calculation.

Figure 4. Minimum values.

Source: Author’s calculation.

Figure 5. Maximum values.

Source: Author’s calculation.

Table 2. Descriptive statistics.

In addition, this article has also shown the correlation matrix that shows the nexus among the constructs. The results indicated that the CSR, GC, GI, and ROA positively associated with the companies' SR that show significant business sustainability enhancement. These values are mentioned in .

Table 3. Correlation matrix.

Moreover, this research also executed the VIF to check the assumption of multicollinearity of the variables. The results revealed that VIF values are lower than five that show no issue of multicollinearity, and these outcomes are shown in .

Table 4. Variance inflation factor.

The current article has used the Hausman test to check the appropriate model among fixed and random models. If the probability value shows less than 0.05, then the FEM is appropriate and vice versa. The results indicated that the probability value is less than 0.05, which means FEM is appropriate. show the results of the Hausman test given below:

Table 5. Hausman specification test.

Firstly, FEM has been operated to check the nexus among the constructs. The results revealed that CSR, green investment, and green credit have a significant and positive association with stock return in the Chinese business environment. In addition, 45.6 percent of variations in sustainable business (stock return) are due to CSR, green credit, green investment, and ROA because the R square value is 0.456. These values are mentioned in .

Table 6. Fixed effect model.

Finally, a robust standard error has been operated to check the nexus among the constructs. The results revealed that CSR and green investment, and green credit have a significant and positive association with stock return in the Chinese business environment. These values are shown in .

Table 7. Robust standard error.

5. Discussions and key implications

5.1. Discussion

It's been indicated by the previous study that the implementation of CSR has a positive association with stock return. The study implies that business organizations focus on profits and social welfare (health protection, economic benefits, and quality environment). This improves the companies' reputation in the eye of society and assists gain broad marketing for the products and services. These results align with Ashrafi et al. (Citation2020) previous study, which has been written to check CSR benefits in a business organization. This study implies that companies that effectively indicate CSR carries the business processes successfully develop positive relations with stakeholders like customers, suppliers, investors, and employees. These relationships help get business effectiveness and the expansion of the business. Thus, the efficient implementation of CSR brings enhancement in the business sustainability. These results are also in line with the previous study of Deer and Zarestky (Citation2017), which suggests that CSR is the policies and practices designed and implemented to achieve the business goals, considering the government regulatory authorities' environmental requirements, customers, and the general public. CSR implementation motivates the business management to provide a pollution-free environment by employing renewable energy resources, eco-friendly raw materials, and processes that may cause minimum waste. In an eco-friendly environment, the employees can have good health and work more efficiently, sustaining the firm's economic activities. The previous study of Farooq et al. (Citation2020) also approves these results. This study tests the role of CSR in getting highly sustainable business. The study highlights that the policy of CSR keeps a check on the business decisions and operations so that the business activities may not leave any negative impact on the atmosphere, natural resources, and the health of living beings. In this way, the natural resources will be saved for the future generation, and an active workforce will be available, which can carry economic activities without any distraction. Hence, CSR ensures business sustainability. The study results have also indicated that green credit is linked with sustainable business enhancement in a positive manner.

The study demonstrates that the issuance of green credit to social organizations or business enterprises to start green programs to ensure high environmental quality leads the businesses towards sustainable performance. These results are supported by the previous research study of Chatzitheodorou et al. (Citation2021), which intends to show how the issuance of green credits guarantees sustainable business development. The study implies that the firms that gain green credits from financial institutions can have sustainable business development. The mention of green credits in the organizational prospects develops confidence in the general public and maintains this confidence in the customers. Thus, the availability of green credit allows having sustainable business development. These results are also in line with Maltais and Nykvist (Citation2020) results, who believe that the business organizations that have the facility of green credit can easily turn their policies into practice, the policies whose objective is to gain business effectiveness and competitive advantages. The availability of green credit enables the organization to keep the atmosphere safe from toxic substances like chemicals or harmful gases. This ensures the availability of good quality natural resources and skilled human resources for the organization, saving sustainable business performance. These results are also in line with the past study of Huybrechs et al. (Citation2019), which shows that the economy where the financial institutions have the policy to provide the credits to invest in ecological friendly programs like the procurement of green material and technology, and the adoption of environmentally friendly techniques to be used to produce the products and services. The use of green materials, technology, and processes enhance the brand image and the company's reputation in the general public's mind. The study results have also represented that green investment has a positive link with sustainable business. These results are in line with the past study of Caldera et al. (Citation2018), which implies that the tendency of the business organizations to invest eco-friendly resources and techniques helps to keep consistency in the undertaking of economic activities as the ecological friendly resources (technology, tools, and energy resources). Techniques help reduce the emission of toxic gas, abominable chemicals, and harmful wastes, which can obstruct business operations. The past study approves these results of Cui et al. (Citation2019), which states that the willingness and ability of the business organization to spend money to employ ecological friendly technology, infrastructure, and logistics improves the quality of products and services and creates agility in the business operation, which ensures the sustainable profitability.

5.2. Research implications

This literary research is a remarkable addition to the business literature. This study represents the relationship of three main factors: CSR strategy, green credit, and green investment on business sustainability (stock return). This study gives a detailed description of national and international CSR strategy, the issuance of green credit, and the act of green investment. It checks their role in attaining the augmentation in business sustainability. Many studies have been written about business sustainability and the ways which can accelerate business sustainability. Many of these studies have discussed the nexus between CSR and business sustainability enhancement. Although CSR practices were considered an extra financial burden, in the real situation, the CSR of Chinese firms helps enhance environmental sustainability and firm performance in the long run. Further, the latest studies have acknowledged the integration of the green financial policies (regarding credit and investment) for business and financial institution's performance and sustainability. Further, the initiation of green bonds in China as a source of green financing also has a strong instinct for eco-performance. This study provides a strong base for firm sustainability by adopting green investment, green credit, CSR for stock return in a novel way that simultaneously influences business sustainability.

The study has great practical significance in an emerging economy as it guides the economists and top management on how to increase business sustainability through the green channel of investments. This study findings provide the guidelines to the regulators while developing the policies related to sustainable business performance concerning environmental and social issues in their investment plans and strategies. By highlighting key channels to enhance green and sustainable business performance; such as (1) banks to grant green credit on easy condition and through the convenient process, (2) the tendency of business organizations to make the green investment, and (3) effectively implement CSR, this study outspread its scope and implications by Chinese export firms. Green sources of financing and logistics are very helpful for conserving environmental deterioration and protection resources for the future generation.

6. Conclusion

Sustainability in business performance is the necessity of organizations to achieve and maintain a high position in the marketplace. Thus, there was a need to investigate the ways which can enhance business sustainability. The current research was conducted to explore the role of CSR implementation, green credit, and green investment on business sustainability enhancement. The study had chosen the context of several Chinese business companies for the practical analysis of the nexus between CSR implementation, green credit, green investment, and business sustainability enhancement. The empirical analysis in Chinese companies helps find results about CSR implementation, green credit, and green investment on the business sustainability enhancement. The study results indicated that the integration of companies under CSR within a particular industry keeps a check on the economic activities they undertake so that the interests of general people or customers towards society or the environment cannot be harmed. The CSR secures the natural resources and environment for future use. Hence, CSR sustains business development. The results showed that the issuance of green credits encourages the commercial units to employ environmentally friendly resources and techniques that do not harm the natural environment. This results in business effectiveness and creates consistency in business processes. Thus, green credit leads to sustainable business performance. Likewise, the results made it clear that the investment in green projects assures long-term sustainability. It helps protect the natural resources and natural environment for present and future use.

The current study has a certain number of limitations. These limitations boost the researchers and practitioners to make further analyses while replicating or extending to this study. The first limitation of the study is that this study analyzes only three predictors of stock return, such as CSR implementation, green credit, and green investment. Many other elements can also affect stock returns. But the study gives no heed to the factors except CSR implementation, green credit, and green investment. The limitation can be removed if the studies that extend this study include more predictors of sustainable business performance and stock return. This study has taken only five years of data from 2016 to 2020 and suggested that future studies should add more periods in their studies. The current study results are based on the empirical analysis of CSR implementation, green credit, and green investment and their impact on stock return in two developing countries. Though the results of this study have proper validity in developing countries, they may not have equal validity in developed economies. For general conception, underlying factors should be analyzed in both developing and developed economies.

Disclosure statement

No potential conflict of interest was reported by the authors.

Correction Statement

This article has been republished with minor changes. These changes do not impact the academic content of the article.

References

- An, H., Razzaq, A., Nawaz, A., Noman, S. M., & Khan, S. A. R. (2021). Nexus between green logistic operations and triple bottom line: Evidence from infrastructure-led Chinese outward foreign direct investment in Belt and Road host countries. Environmental Science and Pollution Research, 1–24.

- Ashrafi, M., Magnan, G. M., Adams, M., & Walker, T. R. (2020). Understanding the conceptual evolutionary path and theoretical underpinnings of corporate social responsibility and corporate sustainability. Sustainability, 12(3), 760–786. https://doi.org/10.3390/su12030760

- Bajic, S., & Yurtoglu, B. (2018). Which aspects of CSR predict firm market value? Journal of Capital Markets Studies, 2(1), 50–69. https://doi.org/10.1108/JCMS-10-2017-0002

- Baloch, Z. A., Tan, Q., Kamran, H. W., Nawaz, M. A., Albashar, G., & Hameed, J. (2021). A multi-perspective assessment approach of renewable energy production: Policy perspective analysis. Environment, Development and Sustainability, 1–29. https://doi.org/10.1007/s10668-021-01524-8

- Bellucci, M., Bini, L., & Giunta, F. (2020). Implementing environmental sustainability engagement into business: Sustainability management, innovation, and sustainable business models Innovation strategies in environmental science (pp. 107–143). Elsevier.

- Bocken, N., Boons, F., & Baldassarre, B. J. J. (2019). Sustainable business model experimentation by understanding ecologies of business models. Journal of Cleaner Production, 208, 1498–1512. https://doi.org/10.1016/j.jclepro.2018.10.159

- Caldera, H., Desha, C., & Dawes, L. (2018). Exploring the characteristics of sustainable business practice in small and medium-sized enterprises: Experiences from the Australian manufacturing industry. Journal of Cleaner Production, 177, 338–349. https://doi.org/10.1016/j.jclepro.2017.12.265

- Cazeri, G. T., Anholon, R., da Silva, D., Ordoñez, R. E. C., Quelhas, O. L. G., Leal Filho, W., & de Santa-Eulalia, L. A. (2018). An assessment of the integration between corporate social responsibility practices and management systems in Brazil aiming at sustainability in enterprises. Journal of Cleaner Production, 182, 746–754. https://doi.org/10.1016/j.jclepro.2018.02.023

- Chatzitheodorou, K., Tsalis, T. A., Tsagarakis, K. P., Evangelos, G., & Ioannis, N. (2021). A new practical methodology for the banking sector to assess corporate sustainability risks with an application in the energy sector. Sustainable Production and Consumption, 27, 1473–1487. https://doi.org/10.1016/j.spc.2021.03.005

- Chien, F., Anwar, A., Hsu, C. C., Sharif, A., Razzaq, A., & Sinha, A. (2021). The role of information and communication technology in encountering environmental degradation: Proposing an SDG framework for the BRICS countries. Technology in Society, 65, 101587. https://doi.org/10.1016/j.techsoc.2021.101587

- Cosenz, F., Rodrigues, V. P., & Rosati, F. (2020). Dynamic business modeling for sustainability: Exploring a system dynamics perspective to develop sustainable business models. Business Strategy and the Environment, 29(2), 651–664. https://doi.org/10.1002/bse.2395

- Cui, L., Chan, H. K., Zhou, Y., Dai, J., & Lim, J. J. (2019). Exploring critical factors of green business failure based on Grey-Decision Making Trial and Evaluation Laboratory (DEMATEL). Journal of Business Research, 98, 450–461. https://doi.org/10.1016/j.jbusres.2018.03.031

- De Stefano, F., Bagdadli, S., & Camuffo, A. (2018). The HR role in corporate social responsibility and sustainability: A boundary‐shifting literature review. Human Resource Management, 57(2), 549–566. https://doi.org/10.1002/hrm.21870

- Deer, S., & Zarestky, J. (2017). Balancing profit and people: Corporate social responsibility in business education. Journal of Management Education, 41(5), 727–749. https://doi.org/10.1177/1052562917719918

- Ding, X., Appolloni, A., & Shahzad, M. (2021). Environmental administrative penalty, corporate environmental disclosures and the cost of debt. Journal of Cleaner Production, 129919. https://doi.org/10.1016/j.jclepro.2021.129919

- Ding, X., Qu, Y., & Shahzad, M. (2019). The impact of environmental administrative penalties on the disclosure of environmental information. Sustainability ( Sustainability), 11(20), 5820. https://doi.org/10.3390/su11205820

- Ding, X., Qu, Y., & Shahzad, M. (2020). Stock market' s reaction to self-disclosure of environmental administrative penalties: An empirical study in China. Polish Journal of Environmental Studies, 29(6), 4029–4039. https://doi.org/10.15244/pjoes/118584

- Farooq, Q., Liu, X., Fu, P., & Hao, Y. (2020). Volunteering sustainability: An advancement in corporate social responsibility conceptualization. Corporate Social Responsibility and Environmental Management, 27(6), 2450–2464. https://doi.org/10.1002/csr.1893

- Freudenreich, B., Lüdeke-Freund, F., & Schaltegger, S. (2020). A stakeholder theory perspective on business models: Value creation for sustainability. Journal of Business Ethics, 166(1), 3–18. https://doi.org/10.1007/s10551-019-04112-z

- Guo, R., Lv, S., Liao, T., Xi, F., Zhang, J., Zuo, X., Cao, X., Feng, Z., & Zhang, Y. (2020). Classifying green technologies for sustainable innovation and investment. Resources, Conservation and Recycling, 153, 104580. https://doi.org/10.1016/j.resconrec.2019.104580

- He, L., Zhang, L., Zhong, Z., Wang, D., & Wang, F. (2019). Green credit, renewable energy investment and green economy development: Empirical analysis based on 150 listed companies of China. Journal of Cleaner Production, 208, 363–372. https://doi.org/10.1016/j.jclepro.2018.10.119

- He, X., Mishra, S., Aman, A., Shahbaz, M., Razzaq, A., & Sharif, A. (2021). The linkage between clean energy stocks and the fluctuations in oil price and financial stress in the US and Europe? Evidence from QARDL approach. Resources Policy, 72, 102021. https://doi.org/10.1016/j.resourpol.2021.102021

- Hu, Y., Jiang, H., & Zhong, Z. (2020). Impact of green credit on industrial structure in China: Theoretical mechanism and empirical analysis. Environmental Science and Pollution Research, 8, 1–14. https://doi.org/10.1007/s11356-020-07717-4

- Huybrechs, F., Bastiaensen, J., & Van Hecken, G. (2019). Exploring the potential contribution of green microfinance in transformations to sustainability. Current Opinion in Environmental Sustainability, 41, 85–92. https://doi.org/10.1016/j.cosust.2019.11.001

- Irfan, M., Razzaq, A., Suksatan, W., Sharif, A., Elavarasan, R. M., Yang, C., Hao, Y., & Rauf, A. (2021). Asymmetric impact of temperature on COVID-19 spread in India: Evidence from quantile-on-quantile regression approach. Journal of Thermal Biology, 103101.

- Khan, S. A. R., Razzaq, A., Yu, Z., & Miller, S. (2021). Industry 4.0 and circular economy practices: A new era business strategies for environmental sustainability. Business Strategy and the Environment, https://doi.org/10.1002/bse.2853

- Li, W., Chien, F., Hsu, C.-C., Zhang, Y., Nawaz, M. A., Iqbal, S., & Mohsin, M. (2021). Nexus between energy poverty and energy efficiency: Estimating the long-run dynamics. Resources Policy, 72, 102063. https://doi.org/10.1016/j.resourpol.2021.102063

- Ling, G., Razzaq, A., Guo, Y., Fatima, T., & Shahzad, F. (2021). Asymmetric and time-varying linkages between carbon emissions, globalization, natural resources and financial development in China. Environment, Development and Sustainability, 1–29.

- Maltais, A., & Nykvist, B. (2020). Understanding the role of green bonds in advancing sustainability. Journal of Sustainable Finance & Investment, 1–20. https://doi.org/10.1080/20430795.2020.1724864

- Ng, A. W. (2018). From sustainability accounting to a green financing system: Institutional legitimacy and market heterogeneity in a global financial centre. Journal of Cleaner Production, 195, 585–592. https://doi.org/10.1016/j.jclepro.2018.05.250

- Ngai, E., Law, C. C., Lo, C. W., Poon, J., & Peng, S. (2018). Business sustainability and corporate social responsibility: Case studies of three gas operators in China. International Journal of Production Research, 56(1–2), 660–676. https://doi.org/10.1080/00207543.2017.1387303

- Razzaq, A., Ajaz, T., Li, J. C., Irfan, M., & Suksatan, W. (2021a). Investigating the asymmetric linkages between infrastructure development, green innovation, and consumption-based material footprint: Novel empirical estimations from highly resource-consuming economies. Resources Policy, 74, 102302. https://doi.org/10.1016/j.resourpol.2021.102302

- Razzaq, A., Sharif, A., Najmi, A., Tseng, M. L., & Lim, M. K. (2021b). Dynamic and causality interrelationships from municipal solid waste recycling to economic growth, carbon emissions and energy efficiency using a novel bootstrapping autoregressive distributed lag. Resources, Conservation and Recycling, 166, 105372. https://doi.org/10.1016/j.resconrec.2020.105372

- Risi, D. (2020). Time and business sustainability: Socially responsible investing in Swiss banks and insurance companies. Business & Society, 59(7), 1410–1440. https://doi.org/10.1177/0007650318777721

- Sanclemente-Téllez, J. C. (2017). Marketing and corporate social responsibility (CSR). Moving between broadening the concept of marketing and social factors as a marketing strategy. Spanish Journal of Marketing – Esic, 21, 4–25. https://doi.org/10.1016/j.sjme.2017.05.001

- Shahzad, F., Yannan, D., Kamran, H. W., Suksatan, W., Nik Hashim, N. A. A., & Razzaq, A. (2021b). Outbreak of epidemic diseases and stock returns: An event study of emerging economy. Economic Research-Ekonomska Istraživanja, 1–20. https://doi.org/10.1080/1331677X.2021.1941179

- Shahzad, M., Qu, Y., Javed, S., Zafar, A., & Rehman, S. (2020a). Relation of environment sustainability to CSR and green innovation: A case of Pakistani manufacturing industry. Journal of Cleaner Production, 253, 119938. https://doi.org/10.1016/j.jclepro.2019.119938

- Shahzad, M., Qu, Y., Rehman, S., Zafar, A., Ding, X., & Abbas, J. (2020b). Impact of knowledge absorptive capacity on corporate sustainability with mediating role of CSR: Analysis from the Asian context. Journal of Environmental Planning and Management, 63(2), 148–174. https://doi.org/10.1080/09640568.2019.1575799

- Shahzad, M., Qu, Y., Zafar, A. U., & Appolloni, A. (2021a). Does the interaction between the knowledge management process and sustainable development practices boost corporate green innovation? Business Strategy and the Environment, 1–17. https://doi.org/10.1002/bse.2865

- Sharif, A., Baris-Tuzemen, O., Uzuner, G., Ozturk, I., & Sinha, A. (2020). Revisiting the role of renewable and non-renewable energy consumption on Turkey’s ecological footprint: Evidence from Quantile ARDL approach. Sustainable Cities and Society, 57, 102138. https://doi.org/10.1016/j.scs.2020.102138

- Sharif, A., Raza, S. A., Ozturk, I., & Afshan, S. (2019). The dynamic relationship of renewable and nonrenewable energy consumption with carbon emission: A global study with the application of heterogeneous panel estimations. Renewable Energy., 133, 685–691. https://doi.org/10.1016/j.renene.2018.10.052

- Shen, Y., Su, Z.-W., Malik, M. Y., Umar, M., Khan, Z., & Khan, M. (2021). Does green investment, financial development and natural resources rent limit carbon emissions? A provincial panel analysis of China. Science of the Total Environment, 755, 142538. https://doi.org/10.1016/j.scitotenv.2020.142538

- Sun, Y., Duru, O. A., Razzaq, A., & Dinca, M. S. (2021). The asymmetric effect eco-innovation and tourism towards carbon neutrality target in Turkey. Journal of Environmental Management, 299, 113653.

- Tseng, M.-L., Chang, C.-H., Wu, K.-J., Lin, C.-W R., Kalnaovkul, B., & Tan, R. R. (2019). Sustainable agritourism in Thailand: Modeling business performance and environmental sustainability under uncertainty. Sustainability, 11(15), 40–56. https://doi.org/10.3390/su11154087

- Wang, F., Yang, S., Reisner, A., & Liu, N. (2019). Does green credit policy work in China? The correlation between green credit and corporate environmental information disclosure quality. Sustainability, 11(3), 733–753. https://doi.org/10.3390/su11030733

- Wang, L., Luo, G. L., Sharif, A., & Dinca, G. (2021). Asymmetric dynamics and quantile dependency of the resource curse in the USA. Resources Policy, 72, 102104. https://doi.org/10.1016/j.resourpol.2021.102104

- Wang, L., Su, C.-W., Ali, S., & Chang, H.-L. (2020). How China is fostering sustainable growth: The interplay of green investment and production-based emission. Environmental Science and Pollution Research International, 27(31), 39607–39618. https://doi.org/10.1007/s11356-020-09933-4

- Xuefeng, Z., Razzaq, A., Gokmenoglu, K. K., & Rehman, F. U. (2021). Time varying interdependency between COVID-19, tourism market, oil prices, and sustainable climate in United States: Evidence from advance wavelet coherence approach. Economic Research-Ekonomska Istraživanja, 1–23. https://doi.org/10.1080/1331677X.2021.1992642

- Zahari, A. R., Esa, E., Rajadurai, J., Azizan, N. A., & Muhamad, T. P. F. (2020). The effect of corporate social responsibility practices on brand equity: An examination of Malaysia's top 100 brands. The Journal of Asian Finance, Economics and Business, 7(2), 271–280. https://doi.org/10.13106/jafeb.2020.vol7.no2.271

- Zhang, X., Jin, Y., & Shen, C. (2020). Manufacturers' green investment in a competitive market with a common retailer. Journal of Cleaner Production, 276, 123–142. https://doi.org/10.1016/j.jclepro.2020.123164

- Zhuang, Y., Yang, S., Razzaq, A., & Khan, Z. (2021). Environmental impact of infrastructure-led Chinese outward FDI, tourism development and technology innovation: A regional country analysis. Journal of Environmental Planning and Management, 1–33.