?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Socio-economic and environment-friendly initiatives are imperative to ensure sustainable development. And corporate social responsibility (CSR) emerged as a solution to create a balance in society through sustainable business performance. However, organizations need plentiful resources to comply with the philosophies of sustainability and CSR. Therefore, the current study explores the role of green financing that covers the social, environmental, and economic aspects of green financing for achieving, excelling and enhancing CSR in the banking sector. Through the employment of survey methodology and the application of Partial Least Square-Structural Equation Modelling (PLS-SEM), the data confirms the contributing role of green finance and its respective dimensions (Environmental, Economics, and Social) in enhancing the multiple facets of CSR. Based on these findings, it is recommended that the banking sector should allocate additional financial resources to promote CSR attributes.

1. Introduction

Corporate Social Responsibility (CSR) emerges as the phenomenon that customers strictly regard and consider while purchasing any product and service in recent times (Castro-González et al., Citation2019). Moreover, the service industries are one of the prominent strategies in relationship building across the world (Jeon et al., Citation2020). As the world is witnessing immense competition in the market, retaining existing customers and attracting new potential clients has become extremely crucial (Raza et al., Citation2020). Furthermore, in the context of the banking sector, there is standardization and unanimous in terms of product offering because of being strictly governed by the rules of the central or state bank of the government, in which the banks cannot offer the product on their own (Shah & Khan, Citation2019). Therefore, banks used CSR as the strategy for relationship building and market differentiation through which customers are retained and enhanced market value (Raza et al., 2021; Shah & Khan, Citation2019).

Since CSR is being emerged as a promotional and marketing solution that helps the bank promote and market themselves, their product, it assists in developing relationships that last for a longer period (Khan et al., Citation2015; Shah & Khan, Citation2019). Because of the incorporation of multiple aspects within the philosophies of CSR, its conceptualization which is kept specific to a particular context remains challenging for scholars and researchers (Uhlig et al., Citation2020). Therefore, Pérez and DEL Bosque (Citation2014) proposed a multi-facet construct that incorporates the multiple related and relevant stakeholders of the society, including customers, suppliers, and all of the areas that are covered under the umbrella of business sustainability (Pérez & DEL Bosque, Citation2014) which incorporates the three dimensions including customers, suppliers and environment (Raza et al., 2021).

In addition to this, for excelling towards CSR, there is a need to have sufficient resources as well by which at least the financial requirements of the contribution or investments are taken care of (Zheng et al., Citation2021; Raza et al., 2021). Especially in the situation of environmental uncertainties, when organizations are producing at the cost of the environment, the management of welfare responsibilities need to be made with an objective to preserve the environment so that not only an additional burden on the ecology is made, but the existing are accordingly countered (Najmi et al., Citation2021a; Ozturk et al., Citation2021; Zheng et al., Citation2021). Therefore, in such a scenario, a need for investments or financing emerged that are made according to the principles of green or sustainability (Zheng et al., Citation2021).

The term “Green Finance”, which is also used in the academics, literature, and researches as “Green Investments,” has multiple facets and is still being evolved (Dörry & Schulz, Citation2018; Liu et al., Citation2020; Razzaq, Ajaz et al., Citation2021; Sun et al., Citation2021). Nevertheless, the ultimate objective of Green Finance is to arrange the financial and monetary resources and events through which sustainable development is achieved at the least possible adverse cost to the ecology and habitat (Zhou et al., Citation2020). In addition to this, it is also being regarded as the phenomena in which there is an integration of monetary principles while following the nurturing as well as preservation of the environment and economic aspects, through enabling the events and projects which are used to enhance the level of sustainability (Zheng et al., Citation2021). Such initiation of projects or events can include but are not limited to financing in renewable energy projects (Sharif et al., Citation2019, Citation2020), waste management, natural preservation and conservation, controlling for climatic change, and so on (Razzaq, Wang et al., Citation2021; Zheng et al., Citation2021; Zhuang et al., Citation2021).

On the other hand, the banking industry being the initiator of financial resources are needed to comply with the principles of sustainability, whereas their product offerings should also have an element that is not just channelized their financial resources to the green investments but also provides consumers with the reasonable and affordable financing to the projects that are made for increasing the sustainability in the society while having the incorporation of economic, environmental and social aspects (Raza et al., 2021; Zheng et al., Citation2021). Therefore, based on the discussion, the current study explores the role of green financing that covers the social, environmental, and economic aspects for achieving, excelling and enhancing the CSR goals in the banking sector. The rest of the research has been organized as; the next section covers the literature support for the research objective, followed by the operationalization of the study, statistical estimation, and lastly, the study is concluded, and recommendations are proposed.

2. Literature review

2.1. Green finance's economic dimension and the CSR-goals

The economic dimension revolves around the principles and processes of enhancing profitability, economies of scale, production, and the financial implications that follow the philosophies of sustainability and environmental well-being (Wang et al., Citation2021; Zhang et al., Citation2021; Zheng et al., Citation2021). Precisely in the banking sector, since the operations of the industry itself revolve around economic and financial activities; therefore, this dimension is regarded as the most crucial and important (Zheng et al., Citation2021). It has been reported that when banking institutions offer green financing by which the protection and safeguarding of the environment are ensured, including financing for solar energy, renewable energy, waste management, and other initiatives that boost the development towards clean and green technology and development (Xuefeng et al., Citation2021), then such product offerings tend to improve the image of the banks in the market while making it competitive which also lead to improving the economic performance of the banks (Akter et al., Citation2018).

Over the period, CSR has become a practice that is imperative for organizations to be followed, as it helps them in attaining excellence in their operational performance, competitive advantage while improving the company's value in the customers' perceptions (Currás-Pérez et al., Citation2018; Farooq & Salam, Citation2020; Nyuur et al., Citation2019). Despite the fact that through CSR, companies can improve their financial and operational performance (Ali et al., Citation2020; Farooq & Salam, Citation2020); it is also had a rebound effect where improved financial positions of the companies lead them to contribute higher in the CSR. In contrast, an external verification in terms of the companies' acknowledgement and acceptance of CSR boosts them to invest more (Ding et al., Citation2022; Gal & Akisik, Citation2020). On the other hand, Pérez et al. (Citation2013) and Pérez and DEL Bosque (Citation2016) stated that five sub-dimensions of CSR are connected or linked with the organizations as stakeholders. These include employees, customers, society and community, shareholders, and ethical and legal compliance (Ding et al., Citation2019; Pérez & DEL Bosque, Citation2014; Shahzad et al., Citation2020).

Though it is reported that banking professionals are found to be least aware while having minimal understanding and knowledge of green financing (Raihan, Citation2019), however when the economic aspects of the banks are sound, they lead them to invest in projects like improving the salaries of the employees, providing maximum satisfaction to the customers, participating in the social and cultural events of the society, contributing and assisting the underprivileged people of the society, whereas while having sophisticated profits ratio, banks also increase their compliance to the government policies, levies, taxes and ensure the legal and ethical compliance across all of the operations (Raza et al., 2021; Zheng et al., Citation2021). Since the study is following the sub-dimensions highlighted by Pérez and DEL Bosque (Citation2016) and Pérez and del Bosque (Citation2017), therefore it has been proposed that:

H1: Green Finance's Economic Dimension is significantly related to CSR towards Employees

H2: Green Finance's Economic Dimension is significantly related to CSR towards Customers

H3: Green Finance's Economic Dimension is significantly related to CSR towards Community

H4:Green Finance's Economic Dimension is significantly related to CSR towards Shareholders

H5: Green Finance's Economic Dimension is significantly related to CSR towards Legal and Ethical issues

2.2. Green finance's environment dimension and the CSR-goals

Another important element of Green Finance in terms of its gist, essence, and similarities in terms of the philosophies of environmental sustainability is the Environment Dimension (An et al., Citation2021; Zheng et al., Citation2021). By the help, this, the environmental challenges like global warming, irregular and volatilities in the environment and climatic conditions (Najmi et al., Citation2019), elimination of greenhouse gases (Czerny & Letmathe, Citation2017) especially carbon emissions and footprints (Sadiq et al., 2021), waste management (Najmi et al., Citation2021b) and responsible consumption (Najmi et al., Citation2021a) of the societies are encouraged and strategized. An organization willing to integrate green philosophies into its operations is more likely to perform better in finance, operations, and, most importantly, in terms of business sustainability (Ahmed et al., Citation2018; Najmi et al., Citation2020). Since the essence of environmental sustainability is related to CSR, the company's green financing is assumed to invest the CSR (Raza et al., 2021; Zheng et al., Citation2021). As already discussed, in the current study, Pérez et al. (Citation2013) and Pérez and DEL Bosque (Citation2016) were followed, who stated precisely in the banking sector that there are five sub-dimensions of the CSR that are connected or linked with the organizations as stakeholders. These include employees, customers, society and community, shareholders, and ethical and legal compliance (Pérez & DEL Bosque, Citation2014). Therefore it has been proposed that:

H6: Green Finance's Environment Dimension is significantly related to CSR towards Employees

H7: Green Finance's Environment Dimension is significantly related to CSR towards Customers

H8: Green Finance's Environment Dimension is significantly related to CSR towards Community

H9: Green Finance's Environment Dimension is significantly related to CSR towards Shareholders

H10: Green Finance's Environment Dimension is significantly related to CSR towards Legal and Ethical issues

2.3. Green finance's social dimension and the CSR-goals

The social dimension covers the aspects of green financing through which the contribution towards employees welfare, stakeholder rights and obligations, customer satisfaction, and society's well-being (Ding et al., Citation2020; Curran & Hamilton, Citation2017). Through this dimension, an organization can boost their market credibility, brand image, perceived value, and development of trust, which can further lead to operational and financial excellence (Zheng et al., Citation2021). While linking it with CSR, it is assumed to be most related based on the shared essence and philosophies (Raza et al., 2021). For instance, these dimensions cover that employees are being paid equally without discrimination, customers are delightfully satisfied, stakeholders are being taken care of, society is being contributed, and legal compliances are ensured, all of these are also shared by the CSR (Pérez & DEL Bosque, Citation2014; Popovic et al., Citation2013). Therefore, it is assumed that companies, prsecisely banks, are assumed to enhance the level of green financing for covering the social aspects which eventually assist them in achieving the CSR goals (Raza et al., 2021; Zheng et al., Citation2021). As already discussed, in the current study, Pérez et al. (Citation2013) and Pérez and DEL Bosque (Citation2016) were followed, who stated precisely in the banking sector that there are five sub-dimensions the CSR that are connected or linked with the organizations as stakeholders. These include employees, customers, society and community, shareholders, and ethical and legal compliance (Pérez & DEL Bosque, Citation2014). Therefore it has been proposed that:

H11: Green Finance's Social Dimension is significantly related to CSR towards Employees

H12: Green Finance's Social Dimension is significantly related to CSR towards Customers

H13: Green Finance's Social Dimension is significantly related to CSR towards Community

H14: Green Finance's Social Dimension is significantly related to CSR towards Shareholders

H15: Green Finance's Social Dimension is significantly related to CSR towards Legal and Ethical issues

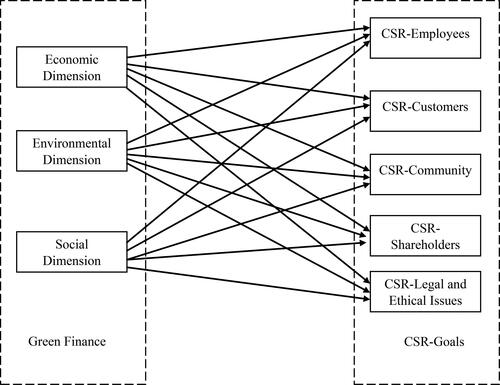

2.4. Conceptual framework

Based on the hypotheses discussed in the previous sections, the proposed conceptual framework is shown in .

Figure 1. Conceptual framework.

3. Methodology

In order to evaluate the research objectives and proposed hypotheses discussed in the previous section, the present adopted the quantitative research by employing the survey research design. In this research design, the data is collected from the potential respondents through the development of a self-administered survey questionnaire that needs to be prepared with careful consideration as it is the tool through which the data is collected for the application of possible statistical analysis. In designing and executing the methodology for the current study, the guidelines proposed by Cooper et al. (Citation2006) are followed.

Moreover, since the development of the questionnaire is a crucial stage, hence in order to increase the possibility of the data's internal consistency and validity, the adapted measurements were used to gauge the responses of the respondents against the studied phenomena. Furthermore, the questionnaire was divided into two sections. In the first section, the measurements of the focused phenomena were listed, whereas, in the second section, questions seeking the respondents' demographic information were listed. For section 1 of the questionnaire, all of the questions were scaled on the Likert scale of the 5 points, in which “1 is for Strongly Disagree, 2 is for Disagree, 3 is for Neither Disagree nor Agree, 4 is for Agree, and 5 is for Strongly Agree”. The sources from where the measurements were adapted are listed in .

Table 1. Source of measures.

Before addressing the questionnaire to the respondents for the purpose of data collection, its “Face and content validity” was ensured by the experts. For this purpose, five experts were approached who validated the questionnaire in terms of its relatedness to the studied phenomena and the language of the items so that respondents do not find any difficulty while responding to the questionnaire. The experts suggested the replacement of certain jargon, which may not be easy to comprehend for respondents. Hence these words were replaced by relatively simpler words. After this stage, a pilot study was conducted on a low sample size to have an idea of whether the questionnaire is collecting and reflecting reliable data or not. The pilot study results were found robust and reliable, which gives the direction to continue with the questionnaire for ample data collection.

3.1. Common method variance

”Common Method Variance” (CMV) is the un-wanted biases that are majorly captured while a research study is being executed. Since it is an unwanted variance, it requires careful ascertainment and must be controlled before applying any statistical techniques; otherwise, the generated outcome can be vague and dubious. In the research, especially involving the quantitative methodology, its significance of ascertainment was highlighted by Podsakoff et al. (Citation2003), who urge to control it in behavioral researches. There are several methods by which it can be controlled, whereas it ascertainment can also be made. Podsakoff et al. (Citation2012) proposed several procedural and statistical remedies by which its magnitude can be countered. The procedural remedies can be employed before and during the data collection phase, whereas the statistical remedies are employed to ascertain the level of CMV once the data is collected.

Considering the procedural remedies, Podsakoff et al. (Citation2012) have mentioned a number of strategies by which the level of CMV can be countered. Among them, the most important is making the statements of the measuring items easy to comprehend and understand. This remedy was ensured at the face and content validity stage by the experts who suggested the removal of jargon and complex words. On the other hand, statistically, the assessment of CMV was ensured by using Harman (1967) 's Single Factor test. According to this test, the higher generation of the variation by a single variable indicates CMV. Therefore, following the procedure Najmi and Ahmed (Citation2018) discussed, the outcome confirms the absence of CMV. In addition to this, the CMV can also be assessed by the value of correlation between two variables. The value exceeding 0.9 indicates CMV (Najmi et al., Citation2021a), which is not the case in this research as the values listed in are far beyond the threshold above.

4. Estimations and results

After the data collection process, the first step that needs to be followed is data screening. In this step, the data were evaluated in terms of values that are possibly out of range, having the attributes of being the outliers as per the overall distribution of the data and missing values. The process of data screening performed leads to the absence of all of the issues above. Therefore, the final data upon which the application of further statistical is made comprised of 357 respondents. The demographic profiles of the respondents are listed in .

Table 2. Descriptive statistics.

4.1. Partial least square- structural equation modeling

After the description of the demographic profiles of the respondents, the application of “Partial Least Square- Structural Equation Modeling” (PLS-SEM) was made. The software used in the application of PLS-SEM is the Smart-PLS, which was developed by Ringle et al. (Citation2015) and has emerged as the leading software for the application of PLS-SEM in recent times. The application of PLS-SEM is made because of the several advantages that are being associated with it. Some of the benefits that make PLS-SEM superior compared with the conventional regression and SEM-based techniques include its immunity to predicting even if the data is not normal, models are complex, and possess low or weak statistical power (Hair et al., Citation2019). In addition to this, in PLS-SEM, the assessment of significance is done by following the methodological framework of Bootstrapping in which multiple sub-samples are created from the existing sample, and then after performing the required number of iterations, the subsequent significance is estimated (Hair Jr et al., Citation2016). Hence, following the guidelines by Hair Jr et al. (Citation2016), the application of PLS-SEM is a two-staged process that involves assessment of the measurement model (MM) and the structural model (SM). These applications and the related discussions are made in the subsequent sections.

4.1.1. Measurement model

The assessment of MM is made to evaluate the internal consistency, reliability, and validity among the studied latent variables. In MM, there is an assessment of two further criteria: the assessment of Convergent Validity and Discriminant Validity. These criteria are further evaluated through the help of multiple tests and measures, which are discussed below.

Convergent validity reflects inter-connectedness among the measuring items belonging to the same construct (Mehmood & Najmi, Citation2017). In this research, the assessment of convergent validity is made through four criteria. Firstly through the factor loading, which should exceed the value of 0.7; secondly, through Cronbach's Alpha which should also exceed the value of 0.7; thirdly, Composite Reliability which should also exceed the value of 0.7 and is superior to the Cronbach's Alpha and lastly, by “Average Variance Extracted” (AVE) which should exceed the value of 0.5. The threshold mentioned for all of the aforementioned criteria is discussed by Hair Jr et al. (Citation2016). The assessment of MM is listed in .

Table 3. Measurement model results.

On the other hand, Discriminant Validity reflects dis-connectedness among the measuring items belonging to the one construct with the measuring items belonging to another construct (Mehmood & Najmi, Citation2017). In this research, the assessment of Discriminant validity is made through three criteria. Firstly through the comparison of factor loadings with the cross-loadings. According to this criterion, the factor loadings of a measuring item should be highly loaded into its respective construct. The value loaded into other constructs must exceed the difference of 0.1 (Gefen & Straub, Citation2005). The values listed in show that the meeting of the cross-loading criterion.

Table 4. Results of loadings and cross loadings.

Secondly, the assessment is made through the criterion proposed by Fornell and Larcker (1981). According to this, the values of the correlations among the constructs should be below the square root of the AVE. is the depiction of the Fornell-Larcker criterion. In this table, the diagonal values represent the square root of AVE, whereas the values other than that reflect the correlations among the construct. It is visible that the diagonal values exceed the off-diagonal values.

Table 5. Discriminant validity Fornell-Larcker criterion.

Lastly, the assessment of Discriminant validity is made through the criterion, which is relatively more recent compared with the others and proposed by Henseler et al. (Citation2015). This criterion has been termed as “Heterotrait-Monotrait Ratio of Correlations” (HTMT). Henseler et al. (Citation2015) proposed the threshold of the HTMT values as below 0.85, which is accordingly met in the current study ().

Table 6. Results of HTMT ratio of correlations.

4.1.2. Structural model

This step involves the assessment of the quality of estimation power, which includes assessing “predictive relevance” through “coefficient of determination” R-square and “cross-validated redundancy” Q-square of the criterion constructs assessed by Q-Square. Though Cohen (Citation1988) proposed a threshold of R-square as values exceeding 0.26 and considered as substantial, however, it is highly dependent on the nature of the relationship between predictors and criterion, whereas the more number of predictors explaining criterion, the more will be the value of R-Square. On the other hand, Hair Jr et al. (Citation2016) considered a value above 0 as acceptable for Q-Square. The assessment of “coefficient of determination” and “cross-validated redundancy” are listed in .

Table 7. Predictive power of construct.

4.1.3. Hypotheses testing

For examining the proposed hypotheses, two things need to be considered. The first thing is the value of the beta coefficient, which reflects the change in the criterion variable being caused by the predictor variable. In contrast, the second thing that needs to be considered is the p-value that reflects the statistical significance of the studied relationships. Initially, the study's objective is to explore the potential contribution made by green financing in excelling CSR. Therefore, multiple dimensions of green finance and CSR were identified through the literature, which is assessed statistically.

Firstly, the three dimensions of green finance were explored on the CSR towards employees. Focusing on the relationship between the economic dimension and CSR towards employees, the economic dimension is reported to be a contributing factor as it has been found to have a positive and significant relationship It means that the one per cent improvement in the economic dimension of green finance could improve CSR towards employees by 11.3%. In other words, when there is an additional investment of resources into green finance that covers the economic aspects, it will improve the CSR towards employees (Raza et al., 2021; Zheng et al., Citation2021). Similarly, focusing on the relationship between environment dimension and CSR towards employees, the environmental dimension is also reported to be a contributing factor as it has been found to have a positive and significant relationship

It means that the one per cent improvement in the environmental dimension of green finance could improve CSR towards employees by 24.6%. In other words, when there is an additional investment of resources into green finance that covers the environmental aspects, it will improve the CSR towards employees (Raza et al., 2021; Zheng et al., Citation2021).

On the other hand, focusing on the relationship between the social dimension and CSR towards employees, the social dimension is also reported to be a contributing factor as it has been found to have a positive and significant relationship It means that the one per cent improvement in the social dimension of green finance could improve CSR towards employees by 21.7%. In other words, when there is an additional investment of resources into green finance that covers the social aspects, it will improve the CSR towards employees (Raza et al., 2021; Zheng et al., Citation2021). Such improvements can be in the form of improving the salaries up to the fair level; providing equal opportunities to everyone irrespective of their gender, caste, and race; assisting with training and development for environment conservation so that skills of the employees are being developed which will eventually benefit the organizations precisely in the case of Banks and so on. The assessment and the outcome of the hypotheses are listed in .

Table 8. Results of path coefficients.

Secondly, the three dimensions of green finance were explored on the CSR towards customers. Focusing on the relationship between the economic dimension and CSR towards customers, the economic dimension is reported to be a contributing factor as it has been found to have a positive and significant relationship It means that the one per cent improvement in the economic dimension of green finance could improve the CSR towards customers by 24.2%. In other words, when there is an additional investment of resources into green finance that covers the economic aspects, it will improve the CSR towards customers (Raza et al., 2021; Zheng et al., Citation2021). Similarly, focusing on the relationship between the environment dimension and CSR towards customers, the environmental dimension is also reported to be a contributing factor as it has been found to have a positive and significant relationship

It means that the one per cent improvement in the environmental dimension of green finance could lead to improve the CSR towards customers by 11.8%. In other words, when there is an additional investment of resources into green finance that covers the environmental aspects, it will improve the CSR towards customers (Raza et al., 2021; Zheng et al., Citation2021).

On the other hand, focusing on the relationship between the social dimension and CSR towards customers, the social dimension is also a contributing factor as it has a positive and significant relationship It means that the one per cent improvement in the social dimension of green finance could improve CSR towards customers by 23.5%. In other words, when there is an additional investment of resources into green finance that covers the social aspects, it will improve the CSR towards customers (Raza et al., 2021; Zheng et al., Citation2021). Such improvements can be in the form of improving customer satisfaction by offering products following their requirements, efficient resolution of complaints, improving transparency while communicating with them, providing services to them in an environment-friendly manner, and so on. The assessment and the outcome of the hypotheses are listed in .

Thirdly, the three dimensions of green finance were explored on the CSR towards the community. Focusing on the relationship between the economic dimension and CSR towards community, the economic dimension is a contributing factor as it has a positive and significant relationship It means that the one per cent improvement in the economic dimension of green finance could improve the CSR towards the community by 18.2%. In other words, when there is an additional investment of resources into green finance that covers the economic aspects, it will improve the CSR towards the community (Raza et al., 2021; Zheng et al., Citation2021). Similarly, focusing on the relationship between environment dimension and CSR towards community, the environmental dimension is also a contributing factor. It has been found to have ave positive and significant relationship

It means that the one per cent improvement in the environmental dimension of green finance could improve the CSR towards the community by 12%. In other words, an additional investment of resources into green finance that covers the environment will improve the CSR towards the community (Raza et al., 2021; Zheng et al., Citation2021).

Moreover, focusing on the relationship between the social dimension and CSR towards community, the social dimension is also a contributing factor. It has been found to have ave positive and significant relationship It means that the one per cent improvement in the social dimension of green finance could improve the CSR towards the community by 17.6%. In other words, an additional investment of resources into green finance that covers the social aspects will improve the CSR towards the community (Raza et al., 2021; Zheng et al., Citation2021). Such improvements can be in the form of contributing and returning back to the society, which can be through assisting the people underprivileged, investing in the cultural events and social gathering through which norms and values are derived and sustained, donating and participating in the initiatives through which the environment and natural habitat are being protected and conserved, etc. The assessment and the outcome of the hypotheses are listed in .

Fourthly, the three dimensions of green finance were explored on the CSR towards shareholders. Focusing on the relationship between the economic dimension and CSR towards shareholders, the economic dimension is a contributing factor as it has ave positive and significant relationship It means that the one per cent improvement in the economic dimension of green finance could improve the CSR towards shareholders by 11.9%. In other words, when there is an additional investment of resources into green finance that covers the economic aspects, it will improve the CSR towards shareholders (Raza et al., 2021; Zheng et al., Citation2021). Similarly, focusing on the relationship between environment dimension and CSR towards shareholders, the environmental dimension is also a contributing factor as it has been found to have a positive and significant relationship

It means that the one per cent improvement in the environmental dimension of green finance could improve the CSR towards shareholders by 19.2%. In other words, an additional investment of resources into green finance that covers the environment will improve the CSR towards shareholders (Raza et al., 2021; Zheng et al., Citation2021). On the other hand, focusing on the relationship between the social dimension and CSR towards shareholders, the social dimension is also reported to be a contributing factor as it has been found to have a positive and significant relationship

It means that the one per cent improvement in the social dimension of green finance could improve CSR towards shareholders by 15%. In other words, when there is an additional investment of resources into green finance that covers the social aspects, it will improve the CSR towards shareholders (Raza et al., 2021; Zheng et al., Citation2021). Such improvements can be made in the form of channelizing the investment in the best possible way that it protects the bank's profitability which eventually safeguards the shareholders whereas improving the transparency in the operations so that shareholders are regularly being updated, safeguard their rights and benefits, and investing in the environmental initiatives while creating the balance between environment and economic aspects, etc. The assessment and the outcome of the hypotheses are listed in .

Lastly, the three dimensions of green finance were explored on the CSR towards legal and ethical aspects. Focusing the relationship between the economic dimension and CSR towards legal and ethical aspects, the economic dimension is a contributing factor as it has a positive and significant relationship It means that the one per cent improvement in the economic dimension of green finance could improve the CSR towards legal and ethical aspects by 22.9%. In other words, when there is an additional investment of resources into green finance that covers the economic aspects, it will improve the CSR towards shareholders (Raza et al., 2021; Zheng et al., Citation2021). Similarly, focusing on the relationship between environment dimension and CSR towards legal and ethical aspects, the environmental dimension is also reported to be a contributing factor as it has been found to have a positive and significant relationship

It means that the one per cent improvement in the environmental dimension of green finance could improve the CSR towards legal and ethical aspects by 17.4%. In other words, an additional investment of resources into green finance that covers the environment will improve the CSR towards legal and ethical aspects (Raza et al., 2021; Zheng et al., Citation2021).

On the other hand, focusing on the relationship between the social dimension and CSR towards legal and ethical aspects, the social dimension is also a contributing factor as it has been found to have a positive and significant relationship It means that the one per cent improvement in the social dimension of green finance could improve the CSR towards legal and ethical aspects by 9%. In other words, when there is an additional investment of resources into green finance that covers the social aspects, it will improve the CSR towards legal and ethical aspects (Raza et al., 2021; Zheng et al., Citation2021). Such improvements can be in the form of complying with the rules and regulations, paying taxes and levies timely, avoiding environmental violations, protecting the rights and obligations of all stakeholders, including customers, shareholders, suppliers, society, etc. The assessment and the outcome of the hypotheses are listed in .

5. Conclusion and recommendations

The present study seeks to answer the questions regarding the contributing role of green finance and its three dimensions in achieving the CSR goals in the banking sector. For said purpose, the quantitative research approach was selected. The data was collected from the consumers of banking services, and their responses were consolidated and statistically analyzed through PLS-SEM. The results revealed the contributing and excelling role of all three dimensions of green financing in all CSR-sub dimensions.

Based on the findings, it is recommended that companies in general and the banking sector, in particular, allocate further financial resources in CSR so that all of the stakeholders of society are being taken care of. Moreover, since green financing emerged and was empirically reported as the potential solution for attaining sustainability, then there is a need to have legal guidelines for governing it. In addition to this, from the signalling point of view, the CSR and green financing could initiate further motivation and trends to the other organization operating in the industry; therefore, regular disclosure in the financial reports and marketing of CSR related activities need to be done and ensured so that the other organizations can also be encouraged to do the same. Lastly, for consumers, banks need to offer more financial-friendly products to the initiatives being made in clean and green technology, environmentally friendly projects, etc.

Based on the limitations, it has been proposed that the same framework needs to be explored in the context of other industries so that the relevancy and legitimacy of the framework are validated. Secondly, exploring nonlinear relationships among the studied phenomena can also contribute to the literature. Thirdly in-depth data analysis needs to be done by incorporating machine learning-based artificial intelligence-oriented techniques. Lastly, expanding the current framework by integrating marketing could also significantly link customer satisfaction, brand image, equity, etc.

Acknowledgement

The authors acknowledge the financial supports from the Philosophy & Social Science Fund of Tianjin City, China (TJYJ21-003).

Disclosure statement

No potential conflict of interest was reported by the authors.

References

- Ahmed, W., Ahmed, W., & Najmi, A. (2018). Developing and analyzing framework for understanding the effects of GSCM on green and economic performance. Management of Environmental Quality: An International Journal, 29(4), 740–758. https://doi.org/10.1108/MEQ-11-2017-0140

- Akter, N., Siddik, A. B., & Mondal, S. A. (2018). Sustainability reporting on green financing: A study of listed private sustainability reporting on green financing: A study of listed private commercial banks in Bangladesh. J. Bus. Technol, 12, 14–27.

- Ali, H. Y., Danish, R. Q., & Asrar-Ul-Haq, M. (2020). How corporate social responsibility boosts firm financial performance: The mediating role of corporate image and customer satisfaction. Corporate Social Responsibility and Environmental Management, 27(1), 166–177. https://doi.org/10.1002/csr.1781

- An, H., Razzaq, A., Nawaz, A., Noman, S. M., & Khan, S. A. R. (2021). Nexus between green logistic operations and triple bottom line: Evidence from infrastructure-led Chinese outward foreign direct investment in Belt and Road host countries. Environmental Science and Pollution Research International, 28(37), 51022–51045.

- Castro-González, S., Bande, B., Fernández-Ferrín, P., & Kimura, T. (2019). Corporate social responsibility and consumer advocacy behaviors: The importance of emotions and moral virtues. Journal of Cleaner Production, 231, 846–855. https://doi.org/10.1016/j.jclepro.2019.05.238

- Cohen, J. (1988). Statistical power analysis for the behavioral sciences (2nd ed.). Academic Press.

- Cooper, D. R., Schindler, P. S., & Sun, J. (2006). Business research methods (Vol. 9, pp. 1–744). Mcgraw-hill.

- Curran, W., & Hamilton, T. (2017). Just green enough: Urban development and environmental gentrification (1st ed.). Routledge.

- Currás-Pérez, R., Dolz-Dolz, C., Miquel-Romero, M. J., & Sánchez-García, I. (2018). How social, environmental, and economic CSR affects consumer-perceived value: Does perceived consumer effectiveness make a difference? Corporate Social Responsibility and Environmental Management, 25(5), 733–747. https://doi.org/10.1002/csr.1490

- Czerny, A., & Letmathe, P. (2017). Eco‐efficiency: GHG reduction related environmental and economic performance. The case of the companies participating in the EU Emissions Trading Scheme. Business Strategy and the Environment, 26(6), 791–806. https://doi.org/10.1002/bse.1951

- Ding, X., Qu, Y., & Shahzad, M. (2019). The impact of environmental administrative penalties on the disclosure of environmental information. Sustainability, 11(20), 5820. https://doi.org/10.3390/su11205820

- Ding, X., Appolloni, A., & Shahzad, M. (2022). Environmental administrative penalty, corporate environmental disclosures and the cost of debt. Journal of Cleaner Production, 332, 129919. https://doi.org/10.1016/j.jclepro.2021.129919

- Ding, X., Qu, Y., & Shahzad, M. (2020). Stock market’s reaction to self-disclosure of environmental administrative penalties: An empirical study in China. Polish Journal of Environmental Studies, 29(6), 4011–4029. https://doi.org/10.15244/pjoes/118584

- Dörry, S., & Schulz, C. (2018). Green financing, interrupted. Potential directions for sustainable finance in Luxembourg. Local Environment, 23(7), 717–733. https://doi.org/10.1080/13549839.2018.1428792

- Farooq, M. S., & Salam, M. (2020). Nexus between CSR and DSIW: A PLS-SEM approach. International Journal of Hospitality Management, 86, 102437. https://doi.org/10.1016/j.ijhm.2019.102437

- Fornell, C., & Larcker, D. F. (1981). Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research, 18(1), 39–50. https://doi.org/10.1177/002224378101800104

- Gal, G., & Akisik, O. (2020). The impact of internal control, external assurance, and integrated reports on market value. Corporate Social Responsibility and Environmental Management, 27(3), 1227–1240. https://doi.org/10.1002/csr.1878

- Gefen, D., & Straub, D. (2005). A practical guide to factorial validity using PLS-Graph: Tutorial and annotated example. Communications of the Association for Information Systems, 16(1), 91–105. https://doi.org/10.17705/1CAIS.01605

- Hair Jr, J. F., Hult, G. T. M., Ringle, C., & Sarstedt, M. (2016). A primer on partial least squares structural equation modeling (PLS-SEM). Sage Publications.

- Hair, J. F., Risher, J. J., Sarstedt, M., & Ringle, C. M. (2019). When to use and how to report the results of PLS-SEM. European Business Review, 31(1), 2–24. https://doi.org/10.1108/EBR-11-2018-0203

- Harman, H. H. (1967). Modem factor analysis. University of Chicago.

- Henseler, J., Ringle, C. M., & Sarstedt, M. (2015). A new criterion for assessing discriminant validity in variance-based structural equation modeling. Journal of the Academy of Marketing Science, 43(1), 115–135. https://doi.org/10.1007/s11747-014-0403-8

- Jeon, M. M., Lee, S., & Jeong, M. (2020). Perceived corporate social responsibility and customers' behaviors in the ridesharing service industry. International Journal of Hospitality Management, 84, 102341. https://doi.org/10.1016/j.ijhm.2019.102341

- Khan, Z., Ferguson, D., & Pérez, A. (2015). Customer responses to CSR in the Pakistani banking industry. International Journal of Bank Marketing, 33(4), 471–493. https://doi.org/10.1108/IJBM-07-2014-0097

- Liu, N., Liu, C., Xia, Y., Ren, Y., & Liang, J. (2020). Examining the coordination between green finance and green economy aiming for sustainable development: A case study of China. Sustainability, 12(9), 3717. https://doi.org/10.3390/su12093717

- Mehmood, S. M., & Najmi, A. (2017). Understanding the impact of service convenience on customer satisfaction in home delivery: Evidence from Pakistan. International Journal of Electronic Customer Relationship Management, 11(1), 23–43. https://doi.org/10.1504/IJECRM.2017.086752

- Najmi, A., & Ahmed, W. (2018). Assessing channel quality to measure customers' outcome in online purchasing. International Journal of Electronic Customer Relationship Management, 11(2), 179–201. https://doi.org/10.1504/IJECRM.2018.090210

- Najmi, A., Kanapathy, K., & Aziz, A. A. (2019). Prioritizing factors influencing consumers' reversing intention of e-waste using analytic hierarchy process. International Journal of Electronic Customer Relationship Management, 12(1), 58–74. https://doi.org/10.1504/IJECRM.2019.098981

- Najmi, A., Kanapathy, K., & Aziz, A. A. (2021a). Exploring consumer participation in environment management: Findings from two‐staged structural equation modelling‐artificial neural network approach. Corporate Social Responsibility and Environmental Management, 28(1), 184–195. https://doi.org/10.1002/csr.2041

- Najmi, A., Kanapathy, K., & Aziz, A. A. (2021b). Understanding consumer participation in managing ICT waste: Findings from two-staged structural equation modeling-artificial neural network approach. Environmental Science and Pollution Research International, 28(12), 14782–14796. https://doi.org/10.1007/s11356-020-11675-2

- Najmi, A., Maqbool, H., Ahmed, W., & Rehman, S. A. U. (2020). The influence of greening the suppliers on environmental and economic performance. International Journal of Business Performance and Supply Chain Modelling, 11(1), 69–90. https://doi.org/10.1504/IJBPSCM.2020.108888

- Nwobu, O. A., Owolabi, A. A., & Iyoha, F. O. (2017). Sustainability reporting in financial institutions: A study of the Nigerian banking sector. Journal of Internet Banking and Commerce, 22(S8), 1–15.

- Nyuur, R. B., Ofori, D. F., & Amponsah, M. M. (2019). Corporate social responsibility and competitive advantage: A developing country perspective. Thunderbird International Business Review, 61(4), 551–564. https://doi.org/10.1002/tie.22065

- Ozturk, I., Aslan, A., & Altinoz, B. (2021). Investigating the nexus between CO2 emissions, economic growth, energy consumption and pilgrimage tourism in Saudi Arabia. Economic Research-Ekonomska Istraživanja, 1–16. https://doi.org/10.1080/1331677X.2021.1985577

- Pérez, A., & DEL Bosque, I. R. (2014). Customer CSR expectations in the banking industry. International Journal of Bank Marketing, 32(3), 223–244. https://doi.org/10.1108/IJBM-09-2013-0095

- Pérez, A., & DEL Bosque, I. R. (2016). The stakeholder management theory of CSR. International Journal of Bank Marketing, 34(5), 731–751. https://doi.org/10.1108/IJBM-04-2015-0052

- Pérez, A., & del Bosque, I. R. (2017). Personal traits and customer responses to CSR perceptions in the banking sector. International Journal of Bank Marketing, 35(1), 128–146. https://doi.org/10.1108/IJBM-02-2016-0023

- Pérez, A., Martínez, P., & DEL Bosque, I. R. (2013). The development of a stakeholder-based scale for measuring corporate social responsibility in the banking industry. Service Business, 7(3), 459–481. https://doi.org/10.1007/s11628-012-0171-9

- Podsakoff, P. M., MacKenzie, S. B., & Podsakoff, N. P. (2012). Sources of method bias in social science research and recommendations on how to control it. Annual Review of Psychology, 63, 539–569.

- Podsakoff, P. M., MacKenzie, S. B., Lee, J. Y., & Podsakoff, N. P. (2003). Common method biases in behavioral research: A critical review of the literature and recommended remedies. The Journal of Applied Psychology, 88(5), 879–903.

- Popovic, T., Kraslawski, A., & Avramenko, Y. (2013). Applicability of sustainability indicators to wastewater treatment processes. In A. Kraslawski & I. Turunen (Eds.), 23rd European Symposium on Computer Aided Process Engineering (Vol. 32, pp. 931–936). Elsevier.

- Raihan, M. Z. (2019). Sustainable finance for growth and development of banking industry in Bangladesh: An equity perspective. MIST International Journal of Science and Technology, 7(1), 41–51.

- Razzaq, A., Ajaz, T., Li, J. C., Irfan, M., & Suksatan, W. (2021). Investigating the asymmetric linkages between infrastructure development, green innovation, and consumption-based material footprint: Novel empirical estimations from highly resource-consuming economies. Resources Policy, 74, 102302. https://doi.org/10.1016/j.resourpol.2021.102302

- Razzaq, A., Wang, Y., Chupradit, S., Suksatan, W., & Shahzad, F. (2021). Asymmetric inter-linkages between green technology innovation and consumption-based carbon emissions in BRICS countries using quantile-on-quantile framework. Technology in Society, 66, 101656. https://doi.org/10.1016/j.techsoc.2021.101656

- Raza, A., Rather, R. A., Iqbal, M. K., & Bhutta, U. S. (2020). An assessment of corporate social responsibility on customer company identification and loyalty in banking industry: A PLS-SEM analysis. Management Research Review, 43(11), 1337–1370. https://doi.org/10.1108/MRR-08-2019-0341

- Raza, A., Saeed, A., Iqbal, M. K., Saeed, U., Sadiq, I., & Faraz, N. A. (2020). Linking corporate social responsibility to customer loyalty through co-creation and customer company identification. Sustainability, 12(6), 2525. https://doi.org/10.3390/su12062525

- Ringle, C. M., Wende, S., & Becker, J. M. (2015). SmartPLS 3. SmartPLS GmbH. http://www.smartpls.com.

- Sun, Y., Duru, O. A., Razzaq, A., & Dinca, M. S. (2021). The asymmetric effect eco-innovation and tourism towards carbon neutrality target in Turkey. Journal of Environmental Management, 299, 113653DOIhttps://doi.org/10.1016/j.jenvman.2021.113653

- Sharif, A., Raza, S. A., Ozturk, I., & Afshan, S. (2019). The dynamic relationship of renewable and nonrenewable energy consumption with carbon emission: A global study with the application of heterogeneous panel estimations. Renewable Energy., 133, 685–691. https://doi.org/10.1016/j.renene.2018.10.052

- Sharif, A., Baris-Tuzemen, O., Uzuner, G., Ozturk, I., & Sinha, A. (2020). Revisiting the role of renewable and non-renewable energy consumption on Turkey’s ecological footprint: Evidence from Quantile ARDL approach. Sustainable Cities and Society, 57, 102138. https://doi.org/10.1016/j.scs.2020.102138

- Sadiq, M., Nonthapot, S., Mohamad, S., Chee Keong, O., Ehsanullah, S., & Iqbal, N. (2021). Does green finance matter for sustainable entrepreneurship and environmental corporate social responsibility during COVID-19? China Finance Review International https://doi.org/10.1108/CFRI-02-2021-0038

- Shah, S. S. A., & Khan, Z. (2019). Corporate social responsibility: A pathway to sustainable competitive advantage? International Journal of Bank Marketing, 38(1), 159–174. https://doi.org/10.1108/IJBM-01-2019-0037

- Shahzad, M., Qu, Y., Rehman, S., Zafar, A., Ding, X., & Abbas, J. (2020). Impact of knowledge absorptive capacity on corporate sustainability with mediating role of CSR: Analysis from the Asian context. Journal of Environmental Planning and Management, 63(2), 148–174. https://doi.org/10.1080/09640568.2019.1575799

- Shahzad, M., Qu, Y., Javed, S., Zafar, A., & Rehman, S. (2020). Relation of environment sustainability to CSR and green innovation: A case of Pakistani manufacturing industry. Journal of Cleaner Production, 253, 119938. https://doi.org/10.1016/j.jclepro.2019.119938

- Uhlig, M. R. H., Mainardes, E. W., & Nossa, V. (2020). Corporate social responsibility and consumer's relationship intention. Corporate Social Responsibility and Environmental Management, 27(1), 313–324. https://doi.org/10.1002/csr.1807

- Wang, L., Luo, G. L., Sharif, A., & Dinca, G. (2021). Asymmetric dynamics and quantile dependency of the resource curse in the USA. Resources Policy, 72, 102104. https://doi.org/10.1016/j.resourpol.2021.102104

- Xuefeng, Z., Razzaq, A., Gokmenoglu, K. K., & Rehman, F. U. (2021). Time varying interdependency between COVID-19, tourism market, oil prices, and sustainable climate in United States: Evidence from advance wavelet coherence approach. Economic Research-Ekonomska Istraživanja, 1–23. https://doi.org/10.1080/1331677X.2021.1992642

- Zhang, H., Razzaq, A., Pelit, I., & Irmak, E. (2021). Does freight and passenger transportation industries are sustainable in BRICS countries? Evidence from advance panel estimations. Economic Research-Ekonomska Istraživanja, 1–21. https://doi.org/10.1080/1331677X.2021.2002708

- Zhuang, Y., Yang, S., Razzaq, A., & Khan, Z. (2021). Environmental impact of infrastructure-led Chinese outward FDI, tourism development and technology innovation: A regional country analysis. Journal of Environmental Planning and Management, 1–33. https://doi.org/10.1080/09640568.2021.1989672

- Zheng, G. W., Siddik, A. B., Masukujjaman, M., & Fatema, N. (2021). Factors Affecting the Sustainability Performance of Financial Institutions in Bangladesh: The Role of Green Finance. Sustainability, 13(18), 10165. https://doi.org/10.3390/su131810165

- Zheng, G. W., Siddik, A. B., Masukujjaman, M., Fatema, N., & Alam, S. S. (2021). Green finance development in Bangladesh: The Role of Private Commercial Banks (PCBs). Sustainability, 13(2), 795. https://doi.org/10.3390/su13020795

- Zhou, X., Tang, X., & Zhang, R. (2020). Impact of green finance on economic development and environmental quality: A study based on provincial panel data from China. Environmental Science and Pollution Research, 27(16), 19915–19932. https://doi.org/10.1007/s11356-020-08383-2