?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Given recent environmental reforms and the focus on the problem of climate change, it is necessary to evaluate whether green growth and environmental taxes can reduce CO2 emissions for countries. Even though a number of studies have analysed the ways to reduce environmental pollution, the literature lacks enough evidence for the role of green growth and environmental taxes in determining the level of carbon emissions. Therefore, the objective of the empirical analysis is to estimate the impacts on CO2 emissions of green growth and environmental taxes by including sustainable indicators for a group of 25 environmentally friendly countries from 1994 to 2018 by applying advanced panel data analysis models. By applying the novel quantile regressions on the largest amount of available data from 1994 to 2018, this article shows that the coefficients of green growth, environmental taxes, renewable energy and energy efficiency are negative at lower, medium and higher quantiles. According to the results of the quantile regression, environmental taxes, renewable energy and energy efficiency are key factors in decreasing CO2 emissions. Overall, renewable energy should be given greater priority through research supports, subsidies and government incentives while environmental taxes should be more implemented to discourage activities that promote pollution.

1. Introduction

Over the last few decades, one of the most serious global problems, other than unemployment, poverty, inequality, financial crisis and others, is now environmental pollution. To prevent global warming, countries have agreed that they need to lower greenhouse gas (GHG) emissions. On the other hand, they would like to increase the consumption of renewable energy and improve energy efficiency. All these goals are regulated by the Rio Declaration on Environment and Development (United Nations, Citation1992), the Kyoto Protocol (1997) and the Paris Agreement (United Nations, Citation2015). The European Union (EU) has also set ambitious targets to tackle climate change and promote a cleaner environment. This refers to the decrease in GHG emissions by 55% by 2030 (European Commission, 2021). Many countries made new commitments during the UN climate conference in Glasgow (2021) known as COP26. However, the most important question is how to achieve these targets. According to the World Energy Outlook (IEA, Citation2021), even if all the announced pledges were fully implemented on time, the world would be heading for a warming by 2.1 °C by the end of the century, missing the Paris Agreement targets and hugely increasing climate risks. Since 1990, global GHG emissions have increased 1.5-fold, mainly due to higher economic growth and greater fossil fuel consumption in developing countries (OECD, Citation2021). However, according to the Environmental Performance Index (EPI, Citation2020), there are different ranks in terms of environmental health and ecosystem vitality among the 180 countries surveyed. The highest-scoring countries have the best policies and programs to protect the environment, especially natural resources, and decrease GHG emission. The top five countries in 2020 were Denmark, Luxembourg, Switzerland, the United Kingdom and France. Their high scores make them leaders in environmental health, meaning that they are the most environmentally friendly countries. The best example is Denmark, which has cut its GHG emissions by more than half. This has been achieved through increased investment in wind energy and biomass, people using more bicycles than cars and the adoption of district heating and cooling systems. Its aim is to become the first carbon neutral capital city by 2025. According to the EPI (Citation2020), the countries that have had the greatest success in mitigating climate change need to make additional efforts to decarbonize their electricity sector. Therefore, GHG emissions must be sustainably reduced, and the EPI (Citation2020) makes it clear that no country is undertaking decarbonization fast enough.

To mitigate the problem of climate change, governments have various environmental instruments and regulations, consisting of carbon pricing, energy-efficient technologies, environmental subsidies and environmental taxes to reduce pollution. In line with economic theory, the role of taxes is to achieve the economic and environmental objectives of the government program. The aim of environmental taxes is to price environmental damage or negative externalities to steer production and consumption decisions in a more environmentally friendly direction (European Parliament, Citation2020). Environmental taxes can potentially address all the aspects of environmental and conservation problems. These include incentives for citizens and businesses to make greener choices with the aim of mitigating climate damage and pollution, and revenue raising to fund government environmental programs. Hence, environmental taxes are a combination of several of the UN Sustainable Development Goals (SDGs).

The British economist Arthur C. Pigou (Pigou, Citation1920), pioneer of environmental taxation, studied the use of taxes in environmental policy, where he stated that environmental taxes were the most important instrument for lowering CO2 emissions. Later, Baumol and Oates (Citation1971) suggested that the tax rate should be a function of the environmental target to be achieved. For example, the higher the GHG emissions, the higher the tax rate. Like any tax, an environmental tax has advantages and disadvantages. The advantages include environmental effectiveness, transparency and the ability to raise revenue. In the OECD area, environment-related taxes raised 793 billion USD in 2019, accounting for the majority of environment-related tax revenues (OECD, Citation2021). However, the share of environment-related tax revenues continues to decline and amounted to 5.2% of total tax revenues in 2019, down from 6.1% in the early 2000s. On the other hand, the drawbacks are unintended behavioral responses and compatibility with firms’ decision-making. According to Freire-González (Citation2018), an effective economic instrument to incentivize greener production and consumer behavior is the environmental tax. Moreover, Maxim and Zander (Citation2019) found that environmental taxes are the main driver of green tax reforms. The result of green tax reforms is a green economy and green growth or environmentally sustainable economic growth. This means that the processes and practices used are sustainable and reduce or minimize damage to ecosystems and the environment.

In light of the aforementioned explanations and arguments, the main motivation for this article is to present whether increasing green growth and environmental taxes makes statistical and economic sense to explain the reduction in CO2 emissions in 25 environmentally friendly countries. These countries were selected because they are leaders in environmental conservation and have the best policies and programs to protect the environment. The second reason was to overcome the lack of studies on the role of green growth and environmental taxes and to provide some new empirical evidence and policy recommendations. Therefore, the aim of this empirical analysis is to estimate the impact of green growth and environmental taxes on CO2 emissions with the inclusion of sustainability indicators for a group of 25 environmentally friendly countries over the period from 1994 to 2018 by applying advanced panel data analysis models. It is noteworthy that this is the largest amount of available data condition upon the fact that the data on environmental taxes are not available prior to the above. The contributions of this article are threefolds. First, this research for the first time conducts an empirical analysis on the nexus of carbon emissions, green growth, and environmental taxes for environmentally friendly countries. Second, renewable energy and energy efficiency as sustainable development indicators are reported for the aforementioned country group. Third, it develops the thin body of literature on quantile regression analysis by using a novel methodology. The structure of the article is as follows. Following the introduction, the most relevant literature on environmental taxes and green growth are presented. The data and model are described within the third section. The fourth section presents the methodology and empirical results obtained. In the last section, the conclusion and policy recommendations are provided.

2. Literature review

A lot of studies have investigated the different sides of CO2 variables from macroeconomic and environment aspects, where they differ in the significance and the level of relationship with other socioeconomic variables. Hence, there are no alliances in the existing literature on the influence of environmental taxes and green growth on CO2 emissions. It was therefore attempted to outline the literature on the factors of CO2 emissions by focusing on environmental taxes, green growth, renewable energy consumption and energy intensity. One of the roles of environmental taxes is to prevent pollution, but also to improve environmental quality without compromising economic growth. Most empirical studies have confirmed that higher environmental taxation has a positive effect on the environment (Bosquet, Citation2000; Morley Citation2012). Moreover, environmental taxes and regulations are the most important tools to ensure environmental reforms (Shahzad et al. Citation2021; Wang et al., Citation2019). Ding et al. (Citation2019) found that environmental taxes and technologies reduce carbon emissions by 28% in heavily polluted economies. Similarly, Miller and Vela (Citation2013) found that, in 50 world countries over the period 1995–2010, higher environmental tax revenues led to greater reductions in CO2 emissions. Sterner (Citation2007) investigated the impact of fuel taxes in Europe in the long term, claiming that carbon emissions are reduced by more than half through the implementation of high fuel taxes, which generate the positive impact of fuel taxes. Moreover, Sundar et al. (Citation2016) showed that CO2 concentration decreases with the increase in environmental taxes. Similar results were found by Hashmi and Alam (Citation2019) for 29 OECD countries, He et al. (Citation2019a) for OECD countries and Chinese provinces and Mardones and Baeza (Citation2018) for South American countries. Rapanos and Polemis (Citation2005), using Greece as an example, found that using various tax rates for different sectors of the economy lead to a better environmental outcome. By investigating the EU countries and Norway in the period 1995–2006, Morley (Citation2012) confirmed a negative linkage between environmental taxes and pollution. Based on all the aforementioned, there is a general opinion that the influence of environmental taxes on CO2 emissions is negative. According to authors like Niu et al. (Citation2018) and Shahzad (Citation2020), the introduction of environmental taxes promotes renewable energy development. This type of development is possible with the use of environmentally friendly sources. These sources are very well known as renewable energy resources. Moreover, they play an important role in the reduction of CO2 emissions (Cheng et al., Citation2019). To combat environmental problems and promote a decrease in CO2 emissions, the efficient use of renewable energy is crucial. A wealth of literature indicates that renewable energy is a key element to minimize reliance on non-renewable energy sources while reducing emissions (Bhattacharya et al., Citation2016; Ulucak & Khan, Citation2020). Although there are various studies confirming that clean energy performs an important purpose in fostering economic growth (Alper & Oguz, Citation2016; Fatur Šikić, Citation2020; Inglesi-Lotz, Citation2016), the literature examining the purpose of green growth in low-carbon emissions is limited. The connection to clean energy production with the aim to improve efficiency in the use of energy (Ji et al., Citation2021) is found in long-term sustainability. According to Borozan (Citation2018), the efficiency of energy taxes can be strengthened through a combination of changes in energy prices and policies that produce a change in electricity consumption patterns.

Bashir et al. (Citation2021) studied the linkage between renewable energy, environmental taxes, technologies and regulations on a sample of 29 OECD countries over the period 1996–2018. They indicated that environmental taxes stimulated the industry to reduce energy consumption and invest in green equipment, while improving energy efficiency. They also indicated that OECD countries need to substantiate a green finance system to promote renewable energy, as these projects are capital intensive. To achieve this, governments need to provide more green finance and investment (Taghizadeh-Hesary & Yoshino, Citation2020; Zhang et al., Citation2019). In addition, green investment stimulates the development of green energy infrastructures, enhances energy and resource efficiency and also protects ecosystems. The solution can be found in implementing more renewable energy in the energy mix (Dogan & Seker, Citation2016). Other solution can be found in enhancing environmental innovations which affects firms’ productivity (Aldieri et al., Citation2020). Moreover, Wolde-Rufael and Mulat-Weldemeskel (Citation2021) examined the effectiveness of environmental taxes and renewable energy in mitigating CO2 emissions, in Latin American and Caribbean countries. The results of their research showed that the outcome of environmental taxes and renewable energy on CO2 emissions is heterogeneous. Hao et al. (Citation2021) investigated the effects of green growth, environmental taxes, human capital and renewable energy consumption on the CO2 emissions of G7 countries. Their results show that green growth, environmental taxes, human capital and renewable energy consumption lower CO2 emissions. Moreover, they concluded that the possibility of green growth will move the industry to use more renewable energy sources. Hence, green growth is an important road map to achieve sustainable development.

Chien et al. (Citation2021) investigated the linkage between green growth and carbon neutrality targets in a case of the USA. Their results showed a significant and negative influence of green growth and environmental taxes on determining CO2 emissions for the US economy. As environmental quality is low in terms of higher CO2 emissions, the recommendation is to put more of an accent on green growth, environmental taxes and renewable energy sources. In addition, their recommendation for improvement is to evolve efficient policies for the environment and to enforce these policies effectively. However, Uzuner et al. (Citation2020) examined the asymmetric long-term cointegration relationship between variables such as the impact of tourism, globalization and economic growth on CO2 emissions. They concluded that any environmental policy to reduce CO2 emissions by decreasing tourism in Turkey would only be effective in the short run, as positive and negative shocks in tourism would have a positive effect on CO2 emissions in the long run. Based on the discussion aforementioned, the literature still lacks sufficient evidence for the part of green growth and environmental taxes in determining the level of carbon emissions. Therefore, keeping in mind the aforementioned studies, our main hypothesis is that environmental taxes, renewable energy and energy efficiency are key determinants in decreasing CO2 emissions in environmentally friendly countries defined by EPI.

3. Model and data

This article relies on the well-known theoretical EKC model (Grossman and Krueger, Citation1995). This model states that pollution rises with income in the early stages of economic growth, but later on, an increase in income leads to environmental improvement (Grossman and Krueger, Citation1991). Furthermore, conventional economic growth is replaced by green growth, and environmental tax, renewable energy and energy intensity are included as control variables following the recent green-environment literature (Chien et al., Citation2021; Hao et al., Citation2021; Khan et al., Citation2021):

(1)

(1)

where CO2 stands for production-based CO2 emissions in millions of tons; GG is green growth measured by the pollution-adjusted economic growth; ETAX denotes environment-related taxes as a share of total tax revenue; REN is the renewable energy supply measured by the share of renewable energy in the total energy supply; EI stands for energy intensity/energy efficiency, which is measured by tons of oil equivalent per person. The annual data from 1994 to 2018 are taken from the OECD database (https://stats.oecd.org/). At this juncture, it is worth noting that this article uses the largest time period, because environmental tax data are not available before 1994 and many indicators are not available after 2018 as of December 2021. The data have been in level and converted into a natural logarithm. The 25 most environmentally friendly countries have been selected according to the 2020 EPI (https://epi.yale.edu/).

4. Methods and empirical results

To examine the stationarity of the variables, the Breitung panel unit root test (Breitung, Citation2000; Breitung & Das, Citation2005) and augmented Dickey–Fuller (CADF) panel unit root test (Pesaran, Citation2007) have been applied. To avoid the problem of independence of cross-sections and slope homogeneity in the models, the second generation of the CADF test has been applied. The results are presented in .

Table 1. The results of the panel unit root test.

At a 1% significance level, all the variables are stationary at first difference, according to the results of the Breitung and CADF panel unit root tests. This means that the mean and variance of the variables used in both models vary over time. To decide whether or not the variables move together in the long run, the Pedroni panel cointegration test (Pedroni, Citation1999) and the Westerlund panel cointegration test (Westerlund, Citation2005) have been applied. The Pedroni test accounts for heterogeneity in covariates across countries. The Westerlund cointegration test is important because it can be applied to models that suffer from slope heterogeneity. In addition, the test deals with cross-sectional dependence. The results are presented in .

Table 2. The results of the panel cointegration test.

The empirical results based on both cointegration methods provide strong evidence of cointegration amongst the dataset. Thus, it can be concluded that the carbon emissions and independent variables move together in the long run in the case of the 25 environmentally friendly countries for the analysed period, implying that the variables analysed have a stable long-run association. To explore the performance of green growth and environmental taxes on CO2 emissions with a view to renewable energy and energy intensity as control variables, this article applies the standard ordinary least squares (OLS) method and the quantile regression method by Koenker (Citation2004). Estimating a large number of parameters in a non-linear model can lead to estimates that are severely biased, as originally pointed out by Neyman and Scott (Citation1948) and Hahn and Newey (Citation2004) in the case of panel models. At the same time, estimating a large number of parameters can be computationally demanding in situations when n is large. However, the fixed effects approach by Koenker (Citation2004) takes advantage of modern developments in sparse matrix algebra and solves a relatively simple linear programming problem that performs well in large panel applications. Quantile regression can better justify the conditional distribution by examining the relationships between the variables at the upper and lower levels. In addition, quantile regression does not require strict assumptions regarding normality, homoscedasticity and the absence of outliers (Johnston & DiNardo Citation1997). This type of regression extends the classical least squares estimation of the conditional mean, because it portrays the cause of a regressor to change at different points of the conditional distribution.

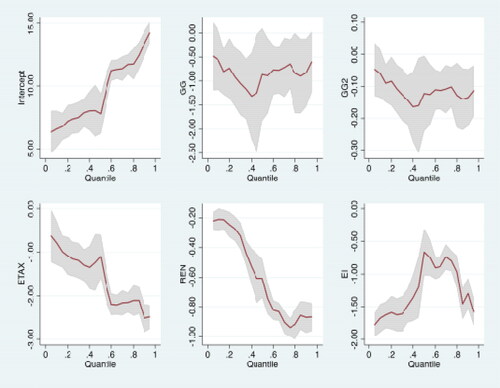

Primarily, the OLS results show that all the variables have a strong significant negative impact on CO2 emissions. Hence, as noted, the OLS results are not robust, since they only calculate the conditional mean. Therefore, the panel quantile method is performed and estimated in seven quantiles. Moreover, these seven quantiles have been divided into five groups. These are the lower, middle lower, middle, middle upper and upper quantiles. The quantile results presented in indicate that the influences of covariates on CO2 emissions are heterogeneous.

Table 3. Koenker (Citation2004)’s quantile results.

We start by showing the OLS estimates as a sort of benchmark, which are then contrasted with the results of the quantile regression. The OLS regression results showed that green growth, square green growth, environmental taxes, renewable energy and energy intensity are key determinants affecting CO2 emissions in the 25 environmentally friendly countries. From the observed results, it can be concluded that all the variables have a negative influence on CO2 emissions. From the observations presented in , the OLS coefficients are –1.21 for environmental tax and –1.23 for green growth. In other words, by increasing environmental taxes or green growth by 1%, CO2 emissions are expected to decrease by 1.21% and 1.23%, respectively. According to the results of the quantile regression, environmental taxes, renewable energy and energy intensity are key factors in decreasing CO2 emissions in all of the quantiles. Moreover, the results showed that the impact of green growth on CO2 emissions was negatively significant at the 0.25th, 0.75th and 0.90th quantiles at the 5% and 10% levels, respectively. This suggests that higher green growth in the economy of the 25 environmentally friendly countries tends to have a negative impact on CO2 emissions, thus reducing pollution in the long-run estimation. Hao et al. (Citation2021) provided similar results for the G7 countries.

The results of the quantile regression imply that environmental taxes are significant in all of the quantiles and have a negative impact on CO2 emissions. This is evidence that the introduction of an environmental tax to transform the 25 environmentally friendly countries into low-carbon economies leads to good results, but it will require further policy adjustments. It is interesting to note that the impact of environmental taxes on CO2 emissions is small in low quantiles (–0.62 at the 0.05th quantile) and increases to –2.48 in the 0.95th quantile. This implies that the higher the environmental taxes, the larger the decrease in CO2 emissions. These results coincide with Ding et al. (Citation2019) for heavily polluted countries, Miller and Vela (Citation2013) for 50 world countries, Hashmi and Alam (Citation2019) for 29 OECD countries, He et al. (Citation2019a) for OECD countries and Chinese provinces, Mardones and Baeza (Citation2018) for South American countries and Morley (Citation2012) for the EU countries and Norway. In all of the quantiles, renewable energy consumption is significant and negatively related to CO2 emissions. Various studies have examined the purpose of renewable energy sources in reducing CO2 emissions. For example, Yao et al. (Citation2019) empirically demonstrated that a 10% increase in the renewable energy consumption would lead to a 1.6% reduction in CO2 emissions. Similarly, Kahia et al. (Citation2019) found that higher renewable energy consumption lowers CO2 emissions in a case of Middle Eastern and North African countries. Moreover, Wolde-Rufael and Mulat-Weldemeskel (Citation2021) found that the outcome of environmental taxes and renewable energy on CO2 emissions is statistically significant in countries with higher emissions and merely insignificant in countries with minor emissions. Energy intensity also proves to be significant and negative in all of the quantiles. These results show that continuous improvement in energy intensity/efficiency reduces CO2 emissions in the 25 environmentally friendly countries.

As a robustness check, the quantile regression estimator for panel data with non-additive fixed effects proposed by Powell (Citation2016) has been applied. The preference of this method compared to existing quantile estimators with additive FEs (αi) is that parameters can vary based on an unspecified fixed effect function and an observation-specific disturbance term, while allowing for individual-specific heterogeneity. The empirical results from the quantile regressions of Powell (Citation2016) are presented in .

Table 4. Powell (Citation2016)’s quantile results.

Clearly, the signs of the estimates by Koenker (Citation2004) and Powell (Citation2016) are very similar. The magnitudes of the Powell quantile regression are larger than the coefficients of the Koenker quantile regression. Compared to the Koenker results, the Powell method suggests that green growth and green growth squared are more significant in reducing CO2 emissions in the 25 environmentally friendly countries. This provides evidence that higher green growth in the economy tends to have a negative impact on CO2 emissions, thus degrading pollution in the long run. By causing that, it is an important road map for executing sustainable development. As such, it has the potential to manage economic development and environmental sustainability. Therefore, green growth has the potential to fulfill these objectives, since it is important for the future of environmentally friendly countries. The negative values for the coefficients of green growth and green growth square illustrate the concave-shaped relationship between green growth and environmental degradation. In the early stages, green growth leads to fewer CO2 emissions, while in the later stages, the extent of green growth decreases. These results can guide the environmentally friendly countries to develop appropriate policies for sustainable CO2 emissions. The efforts of environmentally friendly countries to reduce CO2 emissions are praiseworthy. However, the absolute contribution of environmentally friendly countries to CO2 emissions is still high. By adopting the green growth strategy, increasing environmental taxes and renewable energy consumption while improving energy efficiency, environmentally friendly countries can reduce their CO2 emissions.

The negative values of the coefficients for energy intensity illustrate the inverted U-shaped relationship between energy intensity and environmental degradation, meaning that as energy intensity increases, CO2 emissions initially increase until they begin to decrease at a certain point. checks and confirms the outcomes in and .

Figure 1. Results from quantile regression.

Source: Authors.

5. Conclusions and policy implications

Although, the governments of environmentally friendly countries have a wide range of instruments and environmental regulations, they are still struggling regarding how to effectively reduce pollution. Therefore, there are a lot of examinations in the literature that have analyzed the factors of environmental pollution, as well as estimation techniques. In line with economic theory, to solve environmental problems, governments can intermediate through two main policy instruments. These instruments are financial and legal in nature. The financial instruments include environmental taxes, user fees, emissions trading and others, whereas legal instruments include the regulation of waste disposal, environmental standards, pollution prohibitions and others. In addition, these instruments will promote growth and development. The aim of this article is to analyze the impacts on carbon emissions of green growth and environmental taxes alongside renewable energy and energy efficiency as sustainable indicators for the group of 25 environmentally friendly countries for the period 1994–2018.

By applying the quantile regression method, green growth, green growth squared, environmental taxes, renewable energy consumption and energy intensity were found to perform an important purpose in reducing CO2 emissions in the 25 environmentally friendly countries. Our empirical results showed that CO2 emissions have a negative relationship on green growth and environmental taxes, demonstrating the continuous improvement of the environmental quality in the 25 environmentally friendly economies. In addition, the empirical results provide important policy implications. The recommendation for policymakers is to initiate efficient energy policies in a timely manner to alleviate environmental problems by embracing low-carbon energy sources. Therefore, renewable energy should be given greater priority. Environmental taxes can discourage activities that promote CO2 emissions. Putting a price on carbon encourages a shift in production and consumption decisions toward low-carbon options. To avoid these taxes, investors need to launch environmentally friendly projects, which will cause environmental effectiveness and economic efficiency. However, the overall progress on carbon pricing remains modest. Following all the aforementioned, awareness of global environmental protection is inspiring policy-makers to follow sustainable economic practices with the dual goal of combining growth and a reduced environmental impact. This can be achieved by promoting green growth, environmental taxes, renewable energy sources and energy efficiency. In addition, the recommendation for the policymakers of the 25 environmentally friendly countries is to develop efficient policies to improve the quality of the environment and also effectively enforce these policies in the country. An important step is also to convince relevant authorities to take the necessary steps to achieve green growth development. The limitation of this article is a specific group of environmentally friendly countries for a limited period of time, due to the restrictions of publicly available data. Moreover, there are weaknesses of the empirical analysis. First, the sample used in the analysis refers to a group of environmentally friendly countries. Hence, the results cannot be specified for each specific country. Second, there are significant socioeconomic and institutional differences among the group of 25 environmentally friendly countries, reflected in differences in environmental taxes, renewable energy consumption, energy intensity and CO2 emissions. These are not considered in this empirical analysis, but should be carefully analyzed in further research. Also, the results should be taken into account in formulating the energy policy mix for the group of 25 environmentally friendly countries. Further research should investigate whether the relationship between green growth, environmental taxes and CO2 emissions would be different if each type of environmental tax (energy tax, transport tax and pollution tax) were considered in a multivariate framework. Third, it would be interesting to analyze the impact of environmental taxes on CO2 emissions from industrial sector. Besides all, the recommendation for further research is to examine longer time periods to include more countries and to estimate the results separately.

Disclosure statement

The authors report there are no competing interests to declare.

Data availability statement

The data are available upon request.

Additional information

Funding

References

- Aldieri, L., Makkonen, T., & Vinci, C. P. (2020). Environmental knowledge spillovers and productivity: A patent analysis for large international firms in the energy, water and land resources fields. Resources Policy, 69, 101877–101877. https://doi.org/10.1016/j.resourpol.2020.101877

- Alper, A., & Oguz, O. (2016). The role of renewable energy consumption in economic growth: Evidence from asymmetric causality. Renewable and Sustainable Energy Reviews, 60, 953–959. https://doi.org/10.1016/j.rser.2016.01.123

- Bhattacharya, M., Paramati, S. R., Ozturk, I., & Bhattacharya, S. (2016). The effect of renewable energy consumption on economic growth: Evidence from top 38 countries. Applied Energy, 162, 733–741. https://doi.org/10.1016/j.apenergy.2015.10.104

- Bashir, F. M., Ma, B., Bashir, M. A., Radulescu, M., & Shahzad, U. (2021). Investigating the role of environmental taxes and regulations for renewable energy consumption: Evidence from developed economies. Economic Research-Ekonomska Istraživanja, 34, 1–23. https://doi.org/10.1080/1331677X.2021.1962383.

- Baumol, W. J., & Oates, W. E. (1971). The use of standards and prices for protection of the environment. In P. Bohm & A. V. Kneese (Eds.), The economics of environment (pp. 53–65). Palgrave Macmillan.

- Borozan, D. (2018). Efficiency of energy taxes and the validity of the residential electricity environmental Kuznets curve in the European Union. Sustainability, 10(7), 2464. https://doi.org/10.3390/su10072464

- Bosquet, B. (2000). Environmental tax reform: Does it work? A survey of the empirical evidence. Ecological Economics, 34(1), 19–32. https://doi.org/10.1016/S0921-8009(00)00173-7

- Breitung, J. (2000). The local power of some unit root tests for panel data. In B.H. Baltagi (Ed.), Advances in econometrics: Nonstationary panels, panel cointegration, and dynamic panels (Vol. 15, pp. 161–178). JAI Press.

- Breitung, J., & Das, S. (2005). Panel unit root tests under cross-sectional dependence. Statistica Neerlandica, 59(4), 414–433. https://doi.org/10.1111/j.1467-9574.2005.00299.x

- Cheng, C., Ren, X., Wang, Z., & Yan, C. (2019). Heterogeneous impacts of renewable energy and environmental patents on CO2 emission – Evidence from the BRIICS . The Science of the Total Environment, 668, 1328–1338. https://doi.org/10.1016/j.scitotenv.2019.02.063

- Chien, F., Sadiq, M., Nawaz, M. A., Hussain, M. S., Tran, T. D., & Le Thanh, T. (2021). A step toward reducing air pollution in top Asian economies: The role of green energy, eco-innovation, and environmental taxes. Journal of Environmental Management, 297, 113420. https://doi.org/10.1016/j.jenvman.2021.113420

- Ding, S., Zhang, M., & Song, Y. (2019). Exploring China’s carbon emissions peak for different carbon tax scenarios. Energy Policy, 129, 1245–1252. https://doi.org/10.1016/j.enpol.2019.03.037

- Dogan, E., & Seker, F. (2016). Determinants of CO2 emissions in the European Union: The role of renewable and non-renewable energy. Renewable Energy., 94, 429–439. https://doi.org/10.1016/j.renene.2016.03.078

- Environmental Performance Index (EPI). (2020). Yale Center for Environmental Law and Policy. Retrieved January 9, 2022, from https://epi.yale.edu/.

- European Commission. (2021). Fit for 55': Delivering the EU's 2030 climate Target on the way to climate neutrality (COM/2021/550 Final). European Commission.

- European Parliament. (2020). Understanding environmental taxation. https://www.europarl.europa.eu/RegData/etudes/BRIE/2020/646124/EPRS_BRI(2020)646124_EN.pdf

- Fatur Šikić, T. (2020). The impact of energy consumption on economic growth in developed and post-transition countries of European Union. Zbornik Radova Ekonomski Fakultet u Rijeci, 38(2), 475–497. https://doi.org/10.18045/zbefri.2020.2.475

- Freire-González, J. (2018). Environmental taxation and the double dividend hypothesis in CGE modelling literature: A critical review. Journal of Policy Modeling, 40(1), 194–223. https://doi.org/10.1016/j.jpolmod.2017.11.002

- Grossman, G. M., & Krueger, A. B. (1995). Economic growth and the environment. The Quarterly Journal of Economics, 110(2), 353–377. https://doi.org/10.2307/2118443

- Grossman, G. M., & Krueger, A. B. (1991). Environmental impacts of a North American free trade agreement. Working paper No. 3914. National Bureau of Economic Research.

- Hahn, J., & Newey, W. (2004). Jackknife and analytical bias reduction for nonlinear panel models. Econometrica, 72(4), 1295–1319. https://doi.org/10.1111/j.1468-0262.2004.00533.x

- Hao, L. N., Umar, M., Khan, Z., & Ali, W. (2021). Green growth and low carbon emission in G7 countries: how critical the network of environmental taxes, renewable energy and human capital is? Science of the Total Environment, 752, 141853. https://doi.org/10.1016/j.scitotenv.2020.141853

- Hashmi, R., & Alam, K. (2019). Dynamic relationship among environmental regulation, innovation, CO2 emissions, population, and economic growth in OECD countries: A panel investigation. Journal of Cleaner Production, 231, 1100–1109.

- He, P., Ning, J., Yu, Z., Xiong, H., Shen, H., & Jin, H. (2019). Can environmental tax policy really help to reduce pollutant emissions? An empirical study of a panel ARDL model based on OECD countries and China. Sustainability, 11(16), 4384.

- Inglesi-Lotz, R. (2016). The impact of renewable energy consumption to economic growth: A panel data application. Energy Economics, 53, 58–63. https://doi.org/10.1016/j.eneco.2015.01.003

- International Energy Agency (IEA). (2021). World energy outlook. www.iea.org/weo

- Ji, X., Umar, M., Ali, S., Ali, W., Tang, K., & Khan, Z. (2021). Does fiscal decentralization and eco-innovation promote sustainable environment? A case study of selected fiscally decentralized countries. Sustainable Development, 29(1), 79–88. https://doi.org/10.1002/sd.2132

- Johnston, J., & DiNardo, J. (1997). Econometrics methods (4th ed). McGraw-Hill.

- Kahia, M., Ben Jebli, M., & Belloumi, M. (2019). Analysis of the impact of renewable energy consumption and economic growth on carbon dioxide emissions in 12 MENA countries. Clean Technologies and Environmental Policy, 21(4), 871–885. https://doi.org/10.1007/s10098-019-01676-2

- Khan, S. A. R., Ponce, P., & Yu, Z. (2021). Technological innovation and environmental taxes toward a carbon-free economy: An empirical study in the context of COP-21. Journal of Environmental Management, 298, 113418. https://doi.org/10.1016/j.jenvman.2021.113418

- Koenker, R. (2004). Quantile regression for longitudinal data. Journal of Multivariate Analysis, 91(1), 74–89. https://doi.org/10.1016/j.jmva.2004.05.006

- Mardones, C., & Baeza, N. (2018). Economic and environmental effects of a CO2 tax in Latin American countries. Energy Policy, 114, 262–273. https://doi.org/10.1016/j.enpol.2017.12.001

- Maxim, M., & Zander, K. (2019). Can a green tax reform entail employment double dividend in European and non-European countries? A survey of the empirical evidence. International Journal of Energy Economics and Policy, 9(3), 218–228. https://doi.org/10.32479/ijeep.7578

- Miller, S. J., & Vela, M. A. (2013). Are environmentally related taxes effective? (Inter-American Development Bank Working Series No. IDB-WP-467). https://doi.org/10.2139/ssrn.2367708

- Morley, B. (2012). Empirical evidence on the effectiveness of environmental taxes. Applied Economics Letters, 19(18), 1817–1820. https://doi.org/10.1080/13504851.2011.650324

- Neyman, J., & Scott, E. L. (1948). Consistent estimates based on partially consistent observations. Econometrica, 16(1), 1–32. https://doi.org/10.2307/1914288

- Niu, T., Yao, X., Shao, S., Li, D., & Wang, W. (2018). Environmental tax shocks and carbon emissions: An estimated DSGE model. Structural Change and Economic Dynamics, 47, 9–17. https://doi.org/10.1016/j.strueco.2018.06.005

- OECD. (2021). Environment at a glance: Climate change, environment at a glance: Indicators. https://www.oecd.org/environment/environment-at-a-glance-indicators-ac4b8b89-en.htm

- Pedroni, P. (1999). Critical values for cointegration tests in heterogeneous panels with multiple regressors. Oxford Bulletin of Economics and Statistics, 61(Suppl 1), 653–670. https://doi.org/10.1111/1468-0084.61.s1.14

- Pesaran, M. H. (2007). A simple panel unit root test in the presence of cross-section dependence. Journal of Applied Econometrics, 22(2), 265–312. https://doi.org/10.1002/jae.951

- Pigou, A. C. (1920). The economics of welfare. Macmillan and Co.

- Powell, D. (2016). Quantile regression with nonadditive fixed effects. https://ideas.repec.org/c/boc/bocode/s458157.html

- Rapanos, V. T., & Polemis, M. L. (2005). Energy demand and environmental taxes: The case of Greece. Energy Policy, 33(14), 1781–1788. https://doi.org/10.1016/j.enpol.2004.02.013

- Shahzad, U. (2020). Environmental taxes, energy consumption, and environmental quality: Theoretical survey with policy implications. Environmental Science and Pollution Research International, 27(20), 24848–24862. https://doi.org/10.1007/s11356-020-08349-4

- Shahzad, U., Radulescu, M., Rahim, S., Isik, C., Yousaf, Z., & Ionescu, S. A. (2021). Do environment-related policy instruments and technologies facilitate renewable energy generation? Energies, 14(3), 690. https://doi.org/10.3390/en14030690

- Sterner, T. (2007). Fuel taxes: An important instrument for climate policy. Energy Policy, 35(6), 3194–3202. https://doi.org/10.1016/j.enpol.2006.10.025

- Sundar, S., Mishra, A. K., & Naresh, R. (2016). Effect of environmental tax on carbon dioxide emission: A mathematical model. American Journal of Applied Mathematics and Statistics, 4(1), 16–23. https://doi.org/10.12691/ajams-4-1-3

- Taghizadeh-Hesary, F., & Yoshino, N. (2020). Sustainable solutions for green financing and investment in renewable energy projects. Energies, 13(4), 788. https://doi.org/10.3390/en13040788

- Ulucak, R., & Khan, S. U.-D. (2020). Determinants of the ecological footprint: Role of renewable energy, natural resources, and urbanization. Sustainable Cities and Society, 54, 101996. https://doi.org/10.1016/j.scs.2019.101996.

- United Nations. (1992). Report of the United Nations conference on environment and development (A/CONF.151/26), Vol. I. United Nations

- United Nations. (1997). Report of the conference of the parties on its third session, held at Kyoto from 1 To 11 December 1997, FCCC/CP/1997/7/Add.1. United Nations

- United Nations. (2015). Adoption of the Paris agreement (Decision 1/CP.21. Article 2.1(a)). United Nations.

- Uzuner, G., Akadiri, S. S., & Lasisi, T. T. (2020). The asymmetric relationship between globalization, tourism, CO2 emissions, and economic growth in Turkey: implications for environmental policy making. Environmental Science and Pollution Research International, 27(26), 32742–32753. https://doi.org/10.1007/s11356-020-09190-5

- Wang, J., Wang, K., Shi, X., & Wei, Y. M. (2019). Spatial heterogeneity and driving forces of environmental productivity growth in China: Would it help to switch pollutant discharge fees to environmental taxes? Journal of Cleaner Production, 223, 36–44. https://doi.org/10.1016/j.jclepro.2019.03.045

- Westerlund, J. (2005). New simple tests for panel cointegration. Econometric Reviews, 24(3), 297–316. https://doi.org/10.1080/07474930500243019

- Wolde-Rufael, Y., & Mulat-Weldemeskel, E. (2021). The moderating role of environmental tax and renewable energy in CO2 emissions in Latin America and Caribbean countries: evidence from Method of Moments Quantile Regression. Environmental Challenges, 6, 100412. https://doi.org/10.1016/j.envc.2021.100412

- Yao, S., Zhang, S., & Zhang, X. (2019). Renewable energy, carbon emission and economic growth: A revised environmental Kuznets Curve perspective. Journal of Cleaner Production, 235, 1338–1352 https://doi.org/10.1016/j.jclepro.2019.07.069

- Zhang, D., Zhang, Z., & Managi, S. (2019). A bibliometric analysis on green finance: current status, development, and future directions. Finance Research Letters, 29, 425–430. https://doi.org/10.1016/j.frl.2019.02.003