Abstract

In order to test the key factors affecting users' continuance intention of mobile banking Apps, this study combined the Technology acceptance model (TAM) with the perceptual sinteraction model, and further added human-system interaction and perceived privacy security that was not explored in these models before. Data were collected from 349 users who had experience with mobile banking to test the model and were analyzed with a structural equation model. The present study showed that various interactive characteristics of mobile banking (human-human interaction, human-information interaction, human-system interaction) had significant positive impacts on users' perceptions of using mobile banking (perceived usefulness, perceived ease of use, perceived privacy security). Users' perceptions of using mobile banking had significantly positive impacts on users' satisfaction with mobile banking, and user satisfaction had a significant impact on users' continuance intention. Users’ income level had a significantly negative impact on their continuance intention. In order to further enhance users’ continuance intention for mobile banking, designers and managers of mobile banking are suggested to pay special attention to the interactive characteristics of mobile banking and the impact on users' perceptions of mobile banking, so as to improve customer satisfaction and continuous intention.

1. Introduction

With the rapid development of information technology and the continuous expansion of the banking market, mobile banking, one of the key innovations in mobile communications, has gradually become an essential part of people's daily lives (Jebarajakirthy & Shankar, Citation2021; Sharma, Citation2019). Mobile banking refers to the banking services provided in online banking platforms with mobile terminals such as mobile phones and PDAs (Payne et al., Citation2018). Mobile banking allows consumers to access their bank accounts and process a series of financial and non-financial transactions at any time and any place (Sharma, Citation2019; Zhou, Citation2020). It has also enriched the connotation of banking services, enabling banks to provide customers with traditional and innovative services in a convenient, efficient, and relatively safe way. As mobile terminals are portable, they also become successful and influential successors to ATM, Internet banking, and POS for banks to conduct business. As a result, it has attracted increasing attention from international bankers (Kiljan et al.,Citation2017). (Kiljan et al.,Citation2017). Digital banking is attracting more and more consumers. According to Juniper Research, the number of global digital banking customers will exceed 3.6 billion in 2024, up 54% from 2.4 billion in 2020 (Ti, Citation2021). In terms of related industries, Deloitte (Citation2019) conducted a global digital banking survey on e-banking behaviour and usage in 17 countries worldwide. it showed that 73% of the customers use online banking at least once a month, while 59% of customers use mobile banking (Deloitte, Citation2019). As a result, mobile banking is new and has received increasing attention as an innovative delivery channel of financial services throughout the world (Mater et al., Citation2021).

The past decade has witnessed a vast number of researches focusing on people's motivation of using mobile banking and its effects. Previous literature mainly investigates these topics from three aspects: (1) use intention, (2) customer satisfaction, and (3) cultural differences.

First, in terms of intention to use, most studies have explored different predictors of users' intention to use mobile banking and usage behaviour based on (TAM) theory, such as factors that promote usage intention (e.g. perceived usefulness, perceived ease of use, compatibility, convenience, subjective norms, perceived behavioural control, perceived benefits, trust, social influence, attitudes) and factors that inhibit usage intention (e.g. privacy concerns, security risks, financial risks, uncertainty, unavailability, costs) (Jebarajakirthy & Shankar, Citation2021). Yu and Fang (Citation2009) proposed six dimensions to measure customers’ perception of mobile banking services, including security services, interactivity, relative advantages, ease of use, interface creativity, and customer service. These dimensions were supported by exploratory and confirmatory factor analysis. Luo et al. (Citation2010) showed that trust beliefs and risks significantly affected customers' willingness to adopt mobile banking. Sharma (Citation2019) collected data from 225 mobile banking users, used innovative two-stage methods to analyze the data, and found that trust and autonomous motivation are the two main predictors of the acceptance of mobile banking. Jebarajakirthy and Shankar (Citation2021) found that factors such as use aim, value, risk, tradition, and image would all affect customers' intention to adopt mobile banking (Jebarajakirthy & Shankar, Citation2021). Zhou (Citation2020) used the elaboration likelihood model (ELM) as the theoretical basis and found that the central clues (i.e., information quality and service quality) and peripheral clues (i.e., system quality, reputation, and structural assurance) both had impacts on mobile banking using behaviours.

Ho et al. (Citation2020) collected data from adults with mobile phones and bank accounts in Taiwan (N = 164; via paper-based questionnaire) and Vietnam (N = 213; via online survey) and found that both self-efficacy and convenience had an indirect effect on their intention to adopt mobile banking; specifically, three factors - compatibility, perceived usefulness and perceived risk - influenced their attitudes towards mobile banking, with compatibility having the largest effect, perceived risk having the smallest effect and perceived usefulness having an indirect effect on intention through attitude.

Second, in terms of customer satisfaction, research showed that there are still problems with consumer satisfaction related to the benefits of mobile banking services, especially in developing countries (Al-Otaibi et al., Citation2018; Manser et al., Citation2021; Sampaio et al.,Citation2017) pointed out that many customers complained about application-related problems or service failures, increasing the number of complaints about the use of mobile banking applications. Therefore, the authors collected data from 383 participants from Brazil, India, and the United States, who were bank customers having experiences with service failures in specific mobile banking applications. Analysing the data through confirmatory factors and structural equation modelling to explore the benefits of using mobile banking and satisfaction with mobile banking use. This study explores service failure and perceived fairness in further depth and examines the moderating role of perceived fairness and uncertainty avoidance orientations. The results showed that the benefits of mobile banking were positively related to customer satisfaction. Customers usually complained about service errors caused by technical problems, which directly affected customer satisfaction. Generally, there are three types of complaints about mobile banking applications: Security, ease of use, and convenience (Maxham & Netemeyer, Citation2002). As banks directly benefit from customers’ satisfaction with mobile banking services, such as trust, loyalty, and positive word of mouth (WOM), banks should be aware of such complaints and analyze the failure in providing satisfactory service in all departments. In addition, Geebren et al. (Citation2021) pointed out that consumer satisfaction has been widely accepted as a critical factor of continuous use and success in the literature about information systems, e-commerce, and mobile banking.

Third, concerning cultural differences, Sampaio et al. (Citation2017) investigated customers in Brazil, India, and the United States and found that cultural differences in uncertainty avoidance orientation would affect the trading environment between banks and customers. Ho et al. (Citation2020) focused on consumers in Taiwan and Vietnam to investigate predictors of the adoption of mobile banking. At the same time, they discussed the differences in the intention of Taiwanese and Vietnamese in adopting mobile banking. They found that differences in cultural customs, values, social trust and development levels in different countries would affect mobile banking adoption practices. The willingness to adopt mobile banking was directly affected by the perceived behavioural control in the two countries. In addition to classic cultural dimensions such as individualism/collectivism (Ho et al., Citation2020), this study also found that the relative degree of innovation across countries had a significant impact on the adoption rate of mobile banking.

To summarize, previous studies discussing customers’ intention and satisfaction with using mobile banking are largely based on the technology acceptance model (TAM) theory. Perceived usefulness and perceived ease of use are also widely used in the research of mobile banking. Various research has shown that there were direct and indirect associations between perceived usefulness (perceived ease of use) and behavioural intentions (Hampshire, Citation2017; Jebarajakirthy & Shankar, Citation2021; King & He, Citation2006; Marangunić & Granić, Citation2015; Veríssimo, Citation2016). However, given that mobile banking allows customers to complete financial and non-financial transactions electronically (Payne et al., Citation2018), security issues are restricting factors for mobile banking development while regarding guaranteed security as one of the advantages of mobile banking applications (KPMG., Citation2020). In previous literature, few scholars have studied perceived privacy security as a predictive factor for the continuous use of mobile banking. Therefore, the present study explores the influence of customers’ sense of security on their acceptance of mobile banking. At the same time, most of the previous literature focused on analysing the antecedents (such as perceived usefulness and perceived ease of use) of their motives of using mobile banking but ignored the antecedents of these predictors. As far as we know, only a limited number of studies applied the perceived interactivity theory to study the predictors of the perceptual behaviour of users using mobile banking. Mobile banking was born in the human-computer interaction environment. Therefore, the human-computer interaction environment is needed to determine the antecedents of consumers' continuance intention of mobile banking. As continuance intention is considered a powerful indicator of a successful information system (including mobile banking) (Lin et al., Citation2020), the present study focuses on analyzing how various interactive environmental factors of mobile banking (human-human interaction, human-information interaction, human-system interaction) affect the user's perceived behaviour of using mobile banking. These perceived behaviours further affect their satisfaction and continuance intention of mobile banking. Including perceived interactivity as a prerequisite factor of the Extended Technology Acceptance Model (TAM) can provide implications for users' continuance intention of mobile banking and provide suggestions for mobile banking development agencies.

In addition, previous studies about the adoption of information technology usually include demographic characteristics and socioeconomic variables as important variables, such as age, gender, income, and education. Thusi and Maduku (Citation2020) pointed out that age had moderating effects on the associations between various technological acceptance relationships. Some scholars pointed out gender role differences (i.e., male versus female) may be a psychological manifestation of biological gender differences (i.e., male versus female). In terms of income, Hanafizadeh et al. (Citation2014) believe that income level played an important role in adopting and using mobile banking services. As for education, Jebarajakirthy and Shankar (Citation2021) pointed out that education also affects the adoption intention of mobile banking. Given the relationship between the demographic factors and the acceptance of mobile banking found in previous research, it is necessary that the present study included customers’ age, gender, income, and education as covariates in the analysis of mobile banking using behaviour.

To summarize, we aim to study the predictor of users’ acceptance of mobile banking and whether perceived interactivity can improve the interactive design of mobile banking, and we tend to extend the technology acceptance model (TAM) to the mobile banking environment. The following research questions are proposed: (1) Does the user's perceived interactivity of mobile banking (human-human interaction, human-information interaction, and human-system interaction) impact their perceptions (perceived usefulness, perceived ease of use, and perceived privacy security)? (2) Does individual perceived behaviour influence satisfaction and the continuance intention of mobile banking? (3) Make differences in age, gender, income, and education affect users' continuance intention of mobile banking?

This study is organized as follows: First, we review the existing literature on technology acceptance theory and perceived interactivity theory to propose our conceptual model, research, and hypotheses. Then research methodology and data analysis are described. Finally, we discuss the implications of research findings for theory and practice.

2. Theoretical background

2.1. Technology acceptance model (TAM)

The Technology Acceptance Model (TAM) was initially developed by Davis (Davis, Citation1989; Davis et al., Citation1989). It is an information system theory that explains computer using behaviours and has been proven to be a reliable model for predicting users’ acceptance of information technology (Cheng, Citation2011; Gu et al., Citation2010; Lin & Chang, Citation2018; Riad et al., Citation2013). According to TAM, perceived usefulness and ease of use are the two main determinants of whether an individual adopts new technologies (Aggelidis & Chatzoglou, Citation2009; Handayani et al., Citation2017; Ifinedo, Citation2016; Lin & Chang, Citation2018; Mher et al., Citation2017). Perceived usefulness is also called performance expectation, which refers to users' belief that particular information technology or system can improve their job performance (Davis, Citation1989; Davis et al., Citation1989). Perceived ease of use, also known as effort expectation, refers to the degree of users believing little effort is involved in using particular information technology or system (Davis, Citation1989).

Although both perceived usefulness and perceived ease of use have proven to be significant predictors of information technology acceptance, some studies suggested the influence of perceived ease of use on use intention becomes weaker when users develop high familiarity and adaptability towards the technology (Karahanna et al., Citation1999; Lin et al., Citation2020). Moreover. Bhattacherjee and Barfar (Citation2011) believed that perceived ease of use did not significantly affect the continuance intention of information technology. Perceived usefulness and perceived ease of use – are identified as influential factors in influencing consumers to adopt mobile technology for facilitating banking services (Farah et al., Citation2018; Shankar et al., Citation2020; Zhang et al., Citation2018). Recognizing the reality of exchanging information in the online environment, customers become increasingly concerned every time their private information is given out in information exchange (Zhang et al.,Citation2018). As a result, technology safety concerns, including reliability and privacy factors, play an essential role in motivating consumers to embrace mobile banking (Albort-Morant et al., Citation2021; Zhang et al.,Citation2018). The significant advantage of mobile banking is that financial transactions can be conducted anytime and anywhere. Security is a serious concern when conducting financial transactions through electronic channels (Singh & Srivastava, Citation2018). Therefore, this could be one of the significant barriers to the adoption of mobile banking, as personal or monetary information could be exposed and used for fraudulent activities (Liébana-Cabanillas et al., Citation2017; Singh & Srivastava, Citation2018). security is defined as “a threat which creates circumstances, condition, or event with the potential to cause economic hardship to data or network resources in the form of destruction, disclosure, modification of data, denial of service and/or fraud, waste, and abuse” (Singh & Srivastava, Citation2018). In order to better study the factors influencing mobile banking acceptance and use intention, we have extended the TAM model and added variables related to perceived privacy security. Perceived privacy security refers to the customer's assessment and perception of the risks of privacy leaking and security problems in electronic payment systems (Ding et al., Citation2019; Liébana-Cabanillas et al., Citation2017; Linck et al., Citation2006).

2.2. Perceived interactivity

The theory of perceived interactivity was first proposed by Hoffman and Novak (Citation1996). The connotation of perceived interactivity may differ in different technological use situations (Hsu et al., Citation2015). Previous studies generally defined perceptual interactivity from the following four different perspectives: (1) a feature of technology, (2) a process of information exchange, (3) a user’s perception after using technology or experiencing a process, and (4) a combination of the abovementioned concepts (Hsu et al., Citation2015; McMillan & Hwang, Citation2002; Zhao & Lu, Citation2012). In measuring the level of interactivity, how users perceive or experience technical features is more important than providing these features (Lee, Citation2000). Therefore, in this study, we define perceptual interactivity from a perception-based perspective as “the extent to which the users regard their experience as a simulation of interpersonal communication and how they feel in front of others in real society” (Thorson & Rodgers, Citation2006; Zhao & Lu, Citation2012).

Perceived interactivity is a multi-dimensional concept (Lin & Chang, Citation2018; Zhao & Lu, Citation2012). Hoffman and Novak (Citation1996) proposed a two-dimensions structure of perceptual interactivity, namely technical interactivity, and social interactivity. On top of the idea of technical and social interactivity, combined with the technological context related to mobile banking, perceived interactivity can be further divided into three different dimensions: human-human interaction, human-information interaction, and human-system interaction (Hoffman & Novak, Citation1996; Hsu et al., Citation2015; Ko et al., Citation2005; Lin & Chang, Citation2018). Human-human interaction refers to the degree to which users send and receive information through information technology functions and communicate and respond with others (Hsu et al., Citation2015; Lin & Chang, Citation2018); Lu et al., Citation2010). Human-information interaction refers to the process of participants publishing and receiving information through information technology (e.g., browsing and sharing information) (Lu et al., Citation2010). The motivation to use mobile banking per se is seeking the interaction between people and machines (Lee & Lee, Citation2019). From a technical point of view, interactivity is the foundation of interpersonal communication practices or information exchange between senders, receivers, and their interfaces, indicating that a good network interactivity design can promote network-based communication (Qiao, Citation2019; Sundar et al., Citation2016). Mobile banking is a widespread emerging phenomenon. With a good understanding of the perceived interactivity of mobile banking and its impact on continuance intention, the design of information technology interactivity on different topics can be adjusted, improve user interaction and online interpersonal communication (Lee & Lee, Citation2019). The theory of perceived interactivity was mainly applied in the research of information technology and mobile information technology. In contrast, it was rarely applied to analyze the antecedents and consequences of continuance intention of mobile banking. Therefore, this study uses the perceived interactivity theory to study the predictor of the continuance intention of mobile banking to narrow the gaps in the field of research. As one of the important information technologies, mobile banking is defined in this study as follows from the three abovementioned dimensions: (1) Human-human interaction is defined as users’ feelings or emotional responses when communicating with online customer service through the mobile banking App; (2) Human-information interaction is defined as the process of information interaction between people and various financial services provided by mobile banks (Lin & Chang, Citation2018; Zhao & Lu, Citation2012). High levels of interaction between people and information also improved the efficiency of finding targets (Hsu et al., Citation2015). This interaction is considered an important dimension of perceptions of their bank use (Bettman et al., Citation1998). (3) Human-system (human-machine) interaction is defined as the users’ feeling or emotional response to the system environment and content when using the mobile banking app in real-time. It emphasizes the user's feelings about using the mobile banking App system (Hoffman & Novak, Citation1996).

3. Research models and hypotheses

3.1. Environment and personal perception

Studies have pointed out that the information technology environment based on Internet services has higher requirements for interactivity compared to media. The degree of interactivity perceived by users is considered to be one of the most important factors affecting user experience and is also a function to realize the core value of information technology (Lin & Chang, Citation2018; Lu et al., Citation2010; Sicilia et al., Citation2005). Research findings showed that interactivity enhances user participation, and the perception of interactivity greatly affects user satisfaction, which further affects their continuance intention of information technology. The Internet provides users with higher interactivity than traditional forms of media (Lin & Chang, Citation2018). Lu et al. (Citation2010) also pointed out that the interactivity in the network environment included human-human interaction, human-information interaction, and human-system interaction. At the same time, users have diversified demands for the use of the Internet, which has led to different forms of Internet applications and different levels of satisfaction, pleasant experience, and participation (Lin & Chang, Citation2018). All factors that affect mobile banking applications, such as usefulness, ease of use, and security, are affected by users’ perceptions (Ho et al., Citation2020). It is pointed out in related literature that there is a positive relationship between the environmental cues brought about by different interactions and the users’ cognitive response (e.g., perceived usefulness, perceived convenience, perceived ease of use, and perceived privacy security), leading the users to intentionally adopt and use mobile banking services (Jebarajakirthy & Shankar, Citation2021).

3.1.1. Human-human interaction and personal perceptions

The essence of mobile banking is a platform for users to interact with people in a virtual environment (Hsu et al., Citation2015). That is to say, human-human interaction refers to bilateral communication, which is the interpersonal interaction in which users can communicate and interact through the website for transactions, information exchange, and dialogue (Lin & Chang, Citation2018). Mobile banking can be considered as an interactive mechanism by which users could exchange information with bank customer service staff (Hsu et al., Citation2015). Lee and Lee (Citation2019) investigated 367 users using mobile information technology and found that human-human interaction has a positive impact on perceived usefulness and ease of use, and has a negative impact on perceived risk. Lu et al. (Citation2010) and Hsu et al. (Citation2015) also found the same results. They believed that human-human interaction can promote users' loyalty to information technology. Users would be motivated when their needs for interpersonal communication are met, which in turn would affect their use intentions. Therefore, the following hypotheses were developed.

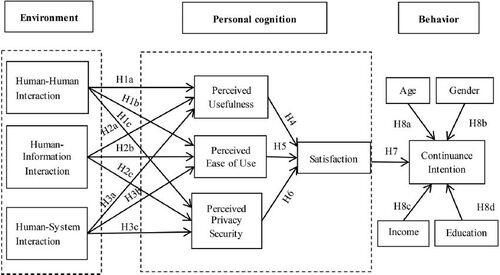

Hypothesis 1a: Human-human interaction has a positive impact on the users’ perceived usefulness of mobile banking Apps.

Hypothesis 1b: Human-human interaction has a positive impact on the users’ perceived ease of use of mobile banking Apps.

Hypothesis 1c: Human-human interaction has a positive impact on the users' perception of the security of mobile banking Apps.

3.1.2. Human-information interaction and personal perception

Human-information interaction refers to participants’ interactions with messages (browsing and sharing messages) through the functions of mobile banking APP (Hsu et al., Citation2015). In general, a high level of human-information interaction can improve the effectiveness of information searching and feedback. This kind of interactivity has been considered an important dimension of interaction (Hsu et al., Citation2015). In other words, Users can realize human-information interaction by using functions such as selection, search, editing, and modification, which also helps them to achieve fast and effective searching and browsing the information (Lin & Chang, Citation2018; Lu et al., Citation2010). Lee and Lee (Citation2019) studied online social media users and found that the human-information interaction had a positive impact on users' perceived usefulness, ease of use, and security of information technology. This is also supported by Lin and Chang (Citation2018), Sampaio et al. (Citation2017), and Lu et al. (Citation2010). They also pointed out that a higher level of human-information interaction would lead to an increase in users’ positive attitudes towards the website. Therefore, we propose the following hypotheses:

Hypothesis 2a: Human-information interaction has a positive impact on the users' perceived usefulness of mobile banking Apps.

Hypothesis 2b: Human-information interaction has a positive impact on the users' perceived ease of use of mobile banking Apps.

Hypothesis 2c: Human-information interaction has a positive impact on the users' perceived security of mobile banking Apps.

3.1.3. Human-system interaction and personal perception

Human-system interaction refers to the degree to which users think they can easily enjoy information by interacting with mobile banking APP platform functions (Lu et al., Citation2010). From the results of the literature review and expert survey, the more users interact with the system, the more users perceive the usefulness of mobile banking app. Its reason is human-system interaction provides users with the ability to modify the form or content of the intermediary environment (Lu et al., Citation2010). Hsu et al. (Citation2015) pointed out that the more frequently users interact with the system, the more familiar users are with the system environment of mobile banking APP, and the more obvious users perceive the ease of use of mobile banking APP. The increase of human-system interaction will enhance users' perception of mobile banking privacy security because human-system interaction will enhance customers' sense of experience and trust in mobile banking. When users build trust in the system platform, they will feel that transactions in the system are safe (Manser et al., Citation2021; Zhou, Citation2020). Lu et al. (Citation2010) also found that human-system interaction can meet the different needs of users and have a positive impact on users' perceived usefulness, ease of use, and security. High-quality information systems with usefulness, ease of use, and security are expected to bring higher user satisfaction and utilization rate (DeLone & McLean, Citation2003; Lee & Lee, Citation2019). Other scholars have also pointed out that human-system interaction has a positive impact on users' personal perceptions (Lee & Lee, Citation2019; Lin & Chang, Citation2018). Therefore, we proposed:

Hypothesis 3a: Human-system interaction has a positive impact on the users' perception of the usefulness of mobile banking Apps.

Hypothesis 3b: Human-system interaction has a positive impact on the users' perception of the ease of use of mobile banking Apps.

Hypothesis 3c: Human-system interaction has a positive impact on the users' perception of the security of mobile banking Apps.

3.2. Personal perception and satisfaction

Perceived usefulness is a fundamental component of technology adoption in the banking industry and is acknowledged as having a strong, positive effect on the use of innovation (Alonso-Dos-Santos et al., Citation2020; Zhang et al., 2018). The predominant belief is that users will be satisfied and adopt a technology if they perceive it to be useful (Zhang et al., 2018). In recent years, mobile banking has been regarded as one of the most effective banking transaction methods because of its unique advantages compared to those of traditional offline banking services (Zhang et al., 2018). Through mobile banking, customers can enjoy faster transaction speed, avoidance of wait time, 24/7 personalized service, higher information transparency, convenience, and no location constraints (Sampaio et al., Citation2017; Veríssimo, Citation2016). Customers will feel satisfied and willing to use mobile banking when they perceive that it is useful and advantageous for their efficiency at work. They also perceive mobile banking as useful when they see their colleagues, friends, or family members use it and give positive recommendations. On the other hand, if people perceive that a system does not help them perform personal activities, they will be dissatisfied and it is unlikely that it will be received favorably (Alonso-Dos-Santos et al., Citation2020). In the banking industry, many studies have included the construct of perceived usefulness as an influential factor of satisfaction and technology adoption (Hanafizadeh et al., Citation2014; Jebarajakirthy & Shankar, Citation2021). Research indicates that perceived usefulness is considered to be one of the advantages of mobile banking Apps, as well as one of the factors fostering users’ adoption and use of mobile banking (Sampaio et al., Citation2017; Shankar et al., Citation2020; Veríssimo, Citation2016). Perceived usefulness influences customers’ mobile banking acceptance and satisfaction toward mobile financial services, and it also had a direct and positive impact on their behavior and satisfaction (Hanafizadeh et al., Citation2014; Sampaio et al., Citation2017; Veríssimo, Citation2016; Zhang et al., 2018). Therefore, the following hypotheses are developed:

Hypothesis 4: The perceived usefulness of mobile banking has a positive impact on customer satisfaction.

Perceived ease of use is another advantage of mobile banking Apps, ease of use has become one of the main advantages associated with customers’ satisfaction (Sampaio et al.,Citation2017). Perceived ease of use refers to an individual’s assessment of the amount of effort needed to perform a task using new technology (Zhang et al., 2018). Although Davis (Citation1989) put more emphasis on the relationship between perceived usefulness and attitudes than between perceived ease of use and attitudes, he posited that users will not adopt a new technology unless it is easy to use. Mobile technology is believed to enhance convenience for bank customers, and its ease of use is key in customer satisfaction (Hanafizadeh et al., Citation2014). Mobile banking technology should be simple and easy for the customer to understand in order to enhance satisfaction and acceptance (Alonso-Dos-Santos et al., Citation2020; Sampaio et al., Citation2017; Singh & Srivastava, Citation2018). In mobile banking, many factors can increase complexity, such as navigation problems, a small screen size, and transaction issues. If the mobile banking service is easy to learn and use, it positively influences the customer’s satisfaction (Singh & Srivastava, Citation2018). In the banking industry, the relationship between perceived ease of use and satisfaction toward new technologies has been validated in many studies (Jebarajakirthy & Shankar, Citation2021; Lin, Citation2014). Particularly, several studies (Hanafizadeh et al., Citation2014; Zhang et al., Citation2018) found empirical support for the effect of perceived ease of use on customers’ mobile banking satisfaction. According to Alonso-Dos-Santos et al. (Citation2020), perceived ease of use affects a person’s attitude (i. e. satisfaction) toward the use of technology. Perceived ease of use in the identification of information and the transactions carried out should lead to a favorable and convincing individual experience. Previous research indicates that perceived ease of use positively influences customers’ satisfaction to use mobile apps and their loyalty toward mobile apps (Zhang et al., 2018). Riquelme and Rios (Citation2010) insisted that PEU influences customers’ satisfaction and adoption of mobile banking. In addition, Veríssimo (Citation2016) investigated adult customers of the Bank of Portugal and found that their perceived ease of use of mobile banking has a positive impact on customer satisfaction. This is also supported by Hanafizadeh et al. (Citation2014) and Zhang et al. (2018). Therefore, the following hypothesis is proposed:

Hypothesis 5: The perceived ease of use of mobile banking has a positive impact on customer satisfaction.

Mobile banking also involves greater uncertainty and risk to the customer (Singh & Srivastava, Citation2018). Some scholars pointed out that one of the main risks of mobile banking is the increase in information security threats. High risks of using mobile banking would reduce customers’ willingness to use this technology (Veríssimo, Citation2016). Security is a major factor valued by customers who conduct financial transactions through the Internet (Sampaio et al. (Citation2017)). Customers believe that a secure electronic platform is sufficient to avoid leaking sensitive personal and business information related to the transaction (Jebarajakirthy et al., Citation2020). Jebarajakirthy and Shankar (Citation2021) investigated Indian users and found that perceived risk is the main obstacle for customers to use mobile banking Apps. In the mobile/wireless environment, security can be categorized as mobile payment-enabling application security, network security, and device security (Singh & Srivastava, Citation2018). Singh and Srivastava (Citation2018) noted that that security challenges and privacy issues are significant concerns for customers using mobile banking. Consumers prefer safe transaction channels and channels that protect consumers from sharing information. Compared with consumers with lower perceived security risks, consumers with higher perceived security risks had lower perceived value about using banking services on mobile banking platforms. As such, customers’ perception of safety had a positive effect on satisfaction (Jebarajakirthy et al., Citation2020; Sampaio et al., Citation2017; Shankar et al., Citation2020). The following hypothesis is therefore developed:

Hypothesis 6: Perceived privacy security of mobile banking has a positive impact on customer satisfaction.

3.3. User satisfaction and continuance intention

Satisfaction refers to the individuals’ evaluation and psychological state produced by their overall experience of a product or service (Sampaio et al., Citation2017; Zhao & Lu, Citation2012). Satisfaction is an antecedent to the repurchase of services on virtual platforms. It has been empirically shown that continuing to carry out financial transactions via mobile banking is determined by satisfaction with previous experiences (Alonso-Dos-Santos et al., Citation2020). In this case, user satisfaction is extremely important for banks in evaluating operational performance (Sampaio et al., Citation2017). Lin et al. (Citation2020) explained that continuous use is the long-term use of information technology by individual users after accepting information technology. Users’ continuance intention of information technology is based on their previous experience of using information technology and their expectations for the upcoming benefits of continuously using information technology (Bhattacherjee & Barfar, Citation2011); in other words, to satisfy customers, it is necessary to know their expectations well to offer a service that meets their needs(Alonso-Dos-Santos et al., Citation2020). Customer satisfaction is considered a key factor when measuring the success of the use of mobile banking (Alonso-Dos-Santos et al., Citation2020; Lin & Wang, Citation2006; Shankar et al., Citation2020). If a user revalues his or her user experience of an information system positively, it is likely that his or her willingness to use such information system again will increase. Lin et al. (Citation2017) used the Technology Acceptance Model (TAM) to investigate and analyze information technology users, and believed that users with high satisfaction with the information system also had a high willingness to continue using the system; when they are satisfied, they tend to use the information system more frequently (Kwon, Citation2006; Lin et al., Citation2017; Zhao & Lu, Citation2012). Therefore, we develop the following hypothesis:

Hypothesis 7: Customer satisfaction with mobile banking has a positive impact on continuance intention.

3.4. Age, gender, income, education, and continuance intention

Studies have pointed out that consumers’ willingness to adopt information technology was affected by their demographic information (Chou et al., Citation2009; Kim & Real, Citation2016; Lin, Citation2014; Thackeray et al., Citation2013). On the contrary, Dospinescu et al. (Citation2021) pointed out that clients with different socio-demographic variables (excluding the separation between Millennials and Generation Z generations) are not different in terms of the level of perception of satisfaction offered by the use of FinTech services. Shankar et al. (Citation2020) found that customers’ age, gender, income, and education level might affect their intention of adopting information technology. First of all, in terms of age, some scholars have found that young people and the elderly were more willing to use mobile banking than people of other ages (Goh & Sun, Citation2014). Hanafizadeh et al. (Citation2014) further pointed out that compared with other users, young users (25-34 years old) were particularly interested in mobile banking and tended to adopt and use mobile banking services, believing that mobile banking is more suitable for their lifestyle. In terms of gender differences, Goh and Sun (2014) focused on college students' views on bank text messages and found that only 34.4% of women used mobile banking, compared with 70% of the men being investigated. As for income, consumers with higher income levels were more likely to use digital services such as mobile banking than consumers with lower income since they do not want to spend time in physical banks for transactions (Clemes et al., Citation2014; Hsu et al., Citation2015; Veríssimo, Citation2016); It is interesting that some researchers believed that users in low-income countries rarely owned computers, whereas more people had mobile phones, so customers in low-income countries may be more likely to choose mobile services (Hanafizadeh et al., Citation2014). Finally, in terms of education level, Hanafizadeh et al. (2014)] and other scholars pointed out that education level plays an important role in the acceptance of mobile banking services. Citizens with higher education have more opportunities to use mobile devices with new technologies, and they are more confident to be users of mobile information technology. On the contrary, users with lower levels of education may have insufficient knowledge in making full use of mobile technology. Users with higher education levels are therefore more inclined to use mobile information technology (Hsu et al., 2015; Lee et al., Citation2020). Therefore, it is interesting to look at the differences in the acceptance of mobile banking based on customers’ demographic statistics (age, gender, income, and education level) (Jebarajakirthy & Shankar, Citation2021). This will help researchers and practitioners understand the characteristics of the users. The influences of the covariates on the continuance intention of mobile banking are hypothesized as below:

Hypothesis 8a: Age has a significant impact on the continuance intention of mobile banking.

Hypothesis 8b: Gender has a significant impact on the continuance intention of mobile banking.

Hypothesis 8c: Revenue has a significant impact on the continuance intention of mobile banking.

Hypothesis 8d: Education has a significant impact on the continuance intention of mobile banking.

Based on the theoretical background proposed above, we proposed a research model to investigate the factors influencing the Continuance Intention of mobile banking. The research model is shown in .

Figure 1. Research model.

Data Source: This Paper.

4. Methodology

A quantitative approach using a survey questionnaire was adopted for the data collection. The target respondents of this study were individuals who already used or had used mobile banking.

4.1. Instruments

This study uses an approach of cross-sectional sampling for data collection. All items are measured using a 5-point Likert scale, ranging from 1 (strongly agree), 2 (agree), 3 (neutral), 4 (disagree), to 5 (strongly disagree). In order to ensure the validity of the measurement, the items measuring the construct are mainly developed from previous studies, and some items have been slightly adjusted to be suited to the context of the mobile banking App. Before conducting the survey, two experts’ information management and financial management and three mobile banking App users were invited to review the items. Specifically, the items' logical consistency, comprehensibility, and sequence were evaluated, and the relevance of the items to mobile banking Apps was evaluated. Based on their suggestions, some minor changes were made to the questionnaire. A pilot test of the questionnaire was after that conducted among 42 participants. Based on their opinions and suggestions, the questionnaire was further revised. The questionnaire includes two parts. The first part collects the participants' basic demographic and socioeconomic information, including their gender, age, income, and education level. The second part collects data related to the research variables (see Appendix A). The questionnaire contains eight primary constructs measured by 28 items. Human-human interaction is measured by three items, adapted from Hsu et al. (Citation2015) and Lin et al. (Citation2017). The four items measuring human-information interaction were adapted from Hsu et al. (Citation2015) and Lee and Lee (Citation2019). The three items assessing human-system interaction are adapted from Yang and Lai (Citation2011) and Lu et al. (Citation2010). Perceived usefulness was measured by four items, adapted from Sampaio et al. (Citation2017) and Davis (Citation1989). Perceived ease of use is measured using five items adapted from Sharma (Citation2019) and Davis et al. (Citation1989). Perceived privacy security is measured by three items adapted from Jebarajakirthy and Shankar (Citation2021) and Sharma (Citation2019) and others. Three items adapted from Hsu et al. (Citation2015) and Tandon et al. (Citation2016) are used to measure satisfaction. The three items used to measure continuance intention are adapted from Hsu et al. (Citation2015) and Sharma (Citation2019).

4.2. Participants and procedure

The empirical data were collected through an online questionnaire in January 2021. A survey was performed using the online questionnaire tool in SO JUMP, a platform providing functions equivalent to Amazon Mechanical Turk. The authors contacted participants in mainland Chinese through the ‘Circle of Friends’ in WeChat. Those who received the questionnaire were asked to send it to their friends on WeChat. A total of 377 participants finished the questionnaire, 28 of whom had not used mobile banking apps. To prepare the data for subsequent analysis, the database was first cleaned. We firstly used frequency analysis to check the existence of non-responses (missing). This methodology enables the identification of questions that were not well understood by respondents. After removing invalid questionnaires, 349 valid surveys were used in the analysis, with the effective rate amounting to 92.57%. In the final sample, 150 (42.93%) were male, and 199 (57.02%) were female. Most of the participants were from the age group of 31-40 years old (N = 156, 44.7%), and others were from the age group of 41-50 years old (N = 110, 31.52%). In terms of their monthly income, 37.25% (N = 130) of the participants had a monthly income of more than US$1543, and 35.82% (N = 125) had a monthly income of US$771-1542. In addition, 79.08% (N = 276) of the participants had a university or college degree, and 12.03% (N = 42) had a postgraduate degree. Appendix B shows the demographic and socioeconomic characteristics of the participants in this study.

In the present study, structural equation modelling was applied to examine relations between latent variables simultaneously.

5. Data analysis and results

The SmartPLS 3 and SPSS version 22 software were used for statistical analyses. The SmartPLS software was used because it supported partial least square (PLS) structural equation modelling (SEM) techniques in predicting key target constructs and exploring or extending an existing structural theory (Hair et al., Citation2011). Hair et al. (2011) suggested that a minimum sample size of 100–150 was needed to perform SEM techniques. The total sample size in this study met the requirement for SEM with maximum likelihood estimation.

Data analysis was performed using the two-step approach suggested by Sampaio et al. (Citation2017): estimating a measurement model and then examining structural relationships among latent constructs. The primary purpose of the two-step approach was to assess the reliability and validity of the measures before applying them to the entire model.

5.1. Measurement model evaluation

The measurement model was evaluated through reliability and validity analysis. presents the Cronbach α of the measurement model, the reliability of the combination, and the Average Variance Extracted (AVE). Results showed that all Cronbach α values were higher than 0.7, indicating acceptable reliability of the construct. The factor loading, AVE, and CR (Composite Reliability) were used to test the convergence validity (Hanafizadeh et al., Citation2014). All factor loadings were higher than 0.7 except that HSI1 was reverse. All AVE values were higher than 0.5, and all CR values were higher than 0.7 except that HSI1 was reverse. Therefore, the scale has high convergent validity.

Table 1. Measurement model statistics.

The validity of the discrimination was tested by the heterotrait-monotrait (HTMT) ratio of correlations and comparing the square root of AVE and the correlation coefficient between the variables. shows the results of comparing the square root of AVE and the correlation coefficient between the variables. The correlation coefficients of all variables were smaller than the square root of AVE, indicating that the discriminant validity defined by Fornell and Larcker (Citation1981) is good. The value of the heterotrait-monotrait ratio of correlations is recommended to be smaller than 0.90 (Henseler et al., Citation2015). shows the results of the heterotrait-monotrait ratio of correlations. The heterotrait-monotrait ratio of correlations is smaller than 0.9 for all but one indicator. In general, the questionnaire in this study has high reliability and validity.

Table 2. Construct correlations and square roots of average variance extracted.

Table 3. HTMT test results.

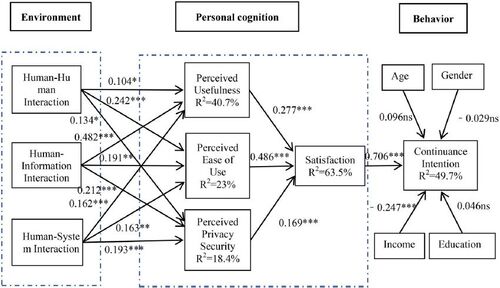

The R-square value was used to measure the goodness of fit (Bentler & Bonett, Citation1980). R-square value was 40.7% for perceived usefulness, 23% for perceived ease of use, 18.4% for perceived privacy security, 63.5% for satisfaction, and 49.7% for continuance intention. An R-square value below 10% indicated a poor fit of the model to the data (Correia et al., Citation2014). All R-square values of the research model in the current study are higher than 10% (see ).

Figure 2. Results of structural equation modeling analysis of the hypothesized model.

Note: *p<0.05; **p<0.01; ***p<0.001; ns, non-significant.

Data Source: This Paper.

5.2. Structural equation modeling

shows the standardized path coefficients, and displays the results of testing the research hypotheses (ns: not significant, *p < 0.05, **p < 0.01, ***p < 0.001). As expected, human-human interaction had a significantly positive impact on perceived usefulness (β = 0.104, t = 1.977, p = 0.049), perceived ease of use (β = 0.242, t = 4.027, p < 0.001), and perceived privacy security (β = 0.134, t = 2.160, p = 0.031), which supported H1a, H1b and H1c. Human-information interaction had a significantly positive impact on perceived usefulness (β = 0.482, t = 8.979, p < 0.001), perceived ease of use (β = 0.191, t = 3.125, p = 0.002), and perceived privacy security (β = 0.212, t = 3.376, p < 0.001), supporting H2a, H2b, and H2c. Human-system interaction had a significantly positive impact on perceived usefulness(β = 0.162, t = 3.456, p < 0.001), perceived ease of use(β = 0.163, t = 3.058, p = 0.002), and perceived privacy security (β = 0.193, t = 3.508, p < 0.001), and these results supported H3a, H3b and H3c. Perceived usefulness (β = 0.277; t = 6.433, p < 0.001), perceived ease of use (β = 0.486; t = 11.035, p < 0.001), and perceived privacy security (β = 0.169; t = 4.406, p < 0.001) all had a significantly positive impact on satisfaction, which supported H4, H5 and H 6. Satisfaction had a significantly positive effect on continuance intention (β = 0.706, t = 18.556, p < 0.001), which supported H7. Regarding the relationship between demographic characteristics and continuance intention, age did not have a significant effect on continuance intention (β = 0.096, t = 1.61, p = 0.108), so that H8a is rejected; gender did not have a significant effect on continuance intention (β=-0.029, t=-513, p = 0.608), and H8b is therefore rejected; income level had a negative correlation with continuance intention (β=-0.247, t=-3.938, p < 0.001), which supported H8a; education level did not have a significant effect on continuance intention (β = 0.046, t = 0.818, p = 0.414), which rejected H8c. Human-human interaction, human-information interaction, human-system interaction, perceived usefulness, perceived ease of use, perceived privacy security, and satisfaction all have significant positive effects on continuous intention, among which satisfaction has the most significant impact on continuous intention, followed by perceived usefulness and perceived ease of use.

Table 4. Results of study hypotheses testing.

6. Discussion

This study integrates perceived interactivity and the expanded theoretical model of TAM to study the key predictors of users' continuance intention of mobile banking Apps. Specifically, the main factors affecting users' continuance intention of mobile banking Apps are interactions (human-human interaction, human-information interaction, human-system interaction) and personal cognition (perceived usefulness, perceived ease of use, perceived privacy security, and perceived satisfaction). The relationships between these variables have also been analyzed and supported by perceived interactivity theory and technology acceptance theory. The results showed that perceived interactivity and personal cognition play an important role in users' willingness to continue using mobile banking Apps.

First of all, the present study confirmed that the human-human interaction, human-information system, and human-system interaction had positive impacts on users’ personal perceptions of using mobile banking Apps (including perceived usefulness, perceived ease of use, and perceived privacy and security). In terms of human-human interaction, it is important to provide users with easy access to the bank’s human customer service through the mobile banking app, so that customers can communicate with the staff and can express their various needs and demands. That is, the two-way interpersonal communication through the mobile banking App would improve the users’ understanding of the mobile banking App, and their perceptions of usefulness, ease of use, and privacy. In terms of human-information interaction, the mobile banking App is advised to actively provide useful information to customers in a timely manner, allowing users to efficiently use the mobile banking App to search for relevant and interesting financial information (i.e., when people are interacting with information). In this case, users’ perceived usefulness, ease of use, and privacy security of mobile banking Apps would be improved. In terms of human-system interaction, when users frequently use mobile banking Apps and rely heavily on mobile banking Apps, users will have a strong sense of belonging. Human-system interaction would help improve users’ perceived usefulness, ease of use, and privacy security of mobile banking Apps. Therefore, perceived interactivity is a powerful predictor of individual behaviors. This result is also supported by the study of Lee and Lee (Citation2019). That is to say, higher levels of user interaction would improve the users’ satisfaction with the bank. The present study provided additional empirical evidence that in the mobile banking environment, the interactive design of mobile banking Apps can affect users’ perception of mobile banking App interactivity. Users experiencing a high degree of perceived interactivity in using mobile banking Apps would perceive mobile banking Apps as more useful, easier to use, and safer, as they already had high abilities and ambitions to use them.

Secondly, in this study, cognitive factors including perceived usefulness perceived ease of use, and perceived privacy security all had a significantly positive correlation with user satisfaction of mobile banking App. This finding is consistent with the study of Sampaio et al. (Citation2017), who reported that customers are paying increasing attention to the benefits of using mobile banking Apps, the usefulness, ease of use, and security brought by mobile banking Apps. Such benefits are positively related to customers’ satisfaction. 10 Using mobile banking helps customers to complete various financial tasks and transactions easily and quickly at any time, anywhere, which saves users time and costs. Compared with perceived usefulness and safety, perceived ease of use is the strongest predictor of satisfaction. The results showed that while mobile banking users expect useful and safe mobile banking services, they also prefer simple and convenient operations. This means that an easier functional design of the mobile banking App system can help people to understand, learn and use these systems, and thereafter increase customers’ satisfaction with the system. The present study provided additional empirical evidence users perceiving the mobile banking App as useful, easy to use, safe would feel satisfied, leading to their continuance intention of the Apps.

Third, this study confirmed that customers satisfaction with using mobile banking Apps had positive effects on customers’ intentions and behaviors to continue using the Apps, which is consistent with findings from previous research (Lin et al., Citation2017; Lu et al., Citation2010). They also pointed out that customers’ satisfaction had a positive effect on the intention and behavior of the continuance intention of information technology. Only customers who are highly satisfied with the information technology showed stronger and more frequent intention to use the Apps.

Finally, regarding the role of demographic characteristics, in this study, our results showed that age, gender, and education level did not have significant influences on customers' intentions and behaviors of continuance intention mobile banking Apps, while income level had a significantly negative effect on customers' use of mobile banking Apps. Previous studies have also investigated the influence of demographic characteristics on using behaviors of mobile banking App. In terms of age, Hanafizadeh et al. (Citation2014) found that young people were more interested in mobile banking because they were the earliest adopters of new information technology products or systems (Hanafizadeh et al., Citation2014). According to the results of the present study, users were mostly from the age group of 21 to 50-year-old. This age group rarely has a "digital divided" situation. This might be one of the plausible reasons that we found different results from previous studies. In terms of gender, a study by Goh and Sun (2014) pointed out that men considered usefulness as an important factor in using software, while women regarded ease of use as the main factor in making a decision; both men and women regarded risk factors as important, and the relative advantage appeared to be more important for men. Riquelme and Rios (Citation2010) also pointed out that women were more concerned about security issues than men for mobile banking, while men were more concerned about effectiveness. Kertzman et al. (Citation2018) found that men usually focused on the possible risk in risk decision-making, while women paid more attention to future consequences. In case of perceiving future loss, women would feel higher risks than men do, leading to differences in self-perception and acceptance behavior. The results of this study showed that gender did not have a significant effect on the use of mobile banking, which is different from previous studies. A plausible reason is that mobile banking Apps are already popular among citizens in China, and digital currency is the main transaction currency. Therefore, we did not find significant gender differences in the present study. In terms of income level, this study confirmed that income had a significantly negative association with the continuance intention of mobile banking Apps. That is to say, users from low-income groups were more inclined to use mobile banking Apps than high-income groups, which is consistent with results from Hanafizadeh et al. (Citation2014) and Hanafizadeh et al. (Citation2014). In terms of education level, Jebarajakirthy and Shankar (Citation2021) included education level as an independent variable but did not find a significant influence of education level on the adoption of mobile banking. This study also further confirmed the results. In this research, we have obtained a deeper understanding of Chinese citizens’ continuance intention of mobile banking. Based on the previous discussion, some important implications are provided for future theories and practices.

7. Implications

7.1. Theoretical implications

The present study has made several theoretical contributions to the mobile banking literature. First of all, although many previous studies have used technology acceptance models to assess users’ satisfaction with mobile banking usage and explore the influencing factors of using intention of mobile banking, few studies have combined perceptual interaction theory with technology acceptance models to examine the determinants of continuous use of mobile banking. As far as we know, this study is one of the first studies to examine the link between interactive characteristics and personal cognition. In this way, this study has enriched the related literature.

Secondly, most of the previous studies mainly focused on perceived usefulness, perceived ease of use, perceived trust, and perceived risk as to the predictors of users’ satisfaction and continuance intention of mobile banking, whereas the effect of perceived privacy security on users’ satisfaction and continuance intention was rarely discussed. Therefore, according to the characteristics of mobile banking APP, this study further included perceived privacy security in the TAM and explored the influence of this factor on users’ satisfaction and continuance intention, which may enrich the theoretical framework for promoting acceptance and use of the technology.

Third, while prior literature has tested the influences of human-human interaction and human-information interaction on continuance intention, there might be other interactive factors that may affect users’ perceptions of an application as well. In the mobile-banking context, the application of perceived interactivity theory is still in its infancy and a comprehensive framework is needed. In this study, we, therefore, introduced a new construct, namely, human-system interaction into this theoretical framework. Our study showed there were substantial associations between human-system interaction and satisfaction and continuance intention of mobile banking, and between the three types of interactions as well.

Finally, the present study also investigated the influence of demographic characteristics (i.e., age, gender, income, and education level) on the use of mobile banking Apps, and found that age, gender, and education level did not have a significant effect on continuance intention. However, income level had a significantly negative association with continuance intention. These are the main theoretical contributions of this study.

7.2. Managerial implications

From a practical perspective, our results also provide implications for mobile banking App designers and managers aiming to improve their service quality and promote competitiveness. The results showed that users’ satisfaction with mobile banking had the most essential and salient influence on their continued use of mobile banking. This suggested that banks are supposed to continuously and systematically analyze the factors that affect customer satisfaction in mobile banking usage. According to Stafford et al. (Citation2004), satisfaction on using the Internet includes three different types: process satisfaction, content satisfaction, and social satisfaction. Content satisfaction refers to satisfaction towards the information carried by the Internet; process satisfaction points to satisfaction with the actual use of the internet, and social satisfaction concerns whether customers find it satisfactory to use the Internet as a social environment. When users use information technology to interact with social systems, human-human interaction and human-system interaction will increase process satisfaction and social satisfaction. Human-information interaction would affect content satisfaction (Hsu et al., Citation2015). Therefore, we provided some suggestions as follows.

First, banks should focus on understanding customers’ behavior and accordingly design high-quality mobile banking apps that provide users with satisfactory perceived interactions. Mobile banking APP designers are encouraged to enhance and optimize the design of interactive environments for mobile banking apps. Banks should equip staff in customer services with strong communication skills and proficient teaching skills to guide and help customers with mobile banking problems. The design of mobile banking software is suggested to be rich yet concise so that customers would perceive most of the information and content as applicable. At the same time, the designed system interface (e.g., open navigation) should be clear and easy to understand to make the operation process and mobile banking services easily accessible to customers. In other words, people from any education level can easily use mobile banking services without feeling confused or inconvenient. This would also considerably save customers’ transaction time and costs. These practices would help strengthen the two-way relationship between human-human interactions, human-information interactions, and human-system interactions. Meanwhile, these measures are also beneficial for enhancing customers’ perceived usefulness, ease of use, and perceived safety and would thus improve user loyalty and effectively attract potential users.

Secondly, we found that perceived privacy security had a significant association with users’ satisfaction. This suggests device manufacturers and service providers should enhance the security of mobile devices to further encourage customers’ active use. To enhance customer satisfaction, efforts are required to build relevant policies, regulations, and legal frameworks. Business practitioners are also advised to improve their data transmission services and ensure privacy protection for users. Periodic analyses of managerial and technical procedures are also necessary to protect transaction data and user information.

Finally, mobile banking service providers may consider applying different strategies for users with different income levels to improve user satisfaction and their continuance of mobile banking. As we did not find significant associations between users’ age, gender, education level, and continuance intention, banks may emphasize making different strategies for customers with different gender, ages, and education levels. In addition, more banks must start implementing mobile banking services and encourage their customers to use them.

8. Limitations

This study has two significant limitations. First of all, the surveyed participants are mainly recruited from the "Circle of Friends" of WeChat in mainland China, and our results may not be generalized to other countries/regions. For example, the demographic characteristics, customers’ perceptions, and psychological responses may be influenced by the unique cultural characteristics of China. Future research may consider conducting cross-cultural comparisons between different countries. Second, there might be potential sample selection bias. In other words, our results based on a sample of WeChat users may not be generalized to a larger population.

9. Conclusion

Mobile banking App is one of the innovative applications of mobile technology. Therefore, it is necessary to analyze and examine the important factors that influence customers' willingness to use the technology. Understanding the predictors of mobile banking can provide mobile banking service providers and researchers with some insights about improving user satisfaction and continuance intention. This study used a research model that combines perceived interactivity and technology acceptance theory and showed that the interactivity and personal cognition of mobile banking Apps would have positive effects on customer satisfaction, which in turn would have a positive influence on customers' continuance intention of mobile banking Apps. Customers' income may influence users’ continuance intention, while customers’ age, gender, and education level may not. Based on the results of this study, we suggest that the design and management of mobile banking Apps enrich the functions available in the system, and create a good user experience based on “interaction” between the App and the user (Lin et al., Citation2020), to promote their use of mobile banking.

Ethical considerations

This study complies with the Declaration of Helsinki guidelines on human research. This research proposal was approved by the Academic Ethics Committee of Taizhou University (No. 2021001). All those who participated in the online survey gave informed consent by filling in an online form designed by the author. In this informed consent, it is stated that they can refuse their participation in this study at any time if they want to. All the survey data are stored on a password-protected computer.

Acknowledgments

The authors sincerely appreciate the contributions of Prof. Weilun Huang to this research. Without his support, it would not have been possible to complete this study.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

References

- Aggelidis, V. P., & Chatzoglou, P. D. (2009). Using a modified technology acceptance model in hospitals. International Journal of Medical Informatics, 78(2), 115–126. https://doi.org/10.1016/j.ijmedinf.2008.06.006

- Albort-Morant, G., Sanchís-Pedregosa, C., & Paredes Paredes, J. R. (2021). Online banking adoption in Spanish cities and towns. Finding differences through TAM application. Economic Research-Ekonomska Istrazivanja, 9, 1–19.

- Alonso-Dos-Santos, M., Soto-Fuentes, Y., & Valderrama-Palma, V. A. (2020). Determinants of mobile banking users’ loyalty. Journal of Promotion Management, 26(5), 615–633. https://doi.org/10.1080/10496491.2020.1729312

- Al-Otaibi, S., Aljohani, N. R., Hoque, M. R., & Alotaibi, F. S. (2018). The satisfaction of Saudi customers toward mobile banking in Saudi Arabia and the United Kingdom. Journal of Global Information Management, 26(1), 85–103.

- Bentler, P. M., & Bonett, D. G. (1980). Significance tests and goodness of fit in the analysis of covariance structures. Psychological Bulletin, 88(3), 588–606. https://doi.org/10.1037/0033-2909.88.3.588

- Bettman, J., Luce, M. F., & Payne, J. W. (1998). Constructive consumer choice processes. Journal of Consumer Research, 25(3), 187–217. https://doi.org/10.1086/209535

- Bhattacherjee, A., & Barfar, A. (2011). Information technology continuance research: Current state and future directions. Asia Pacific Journal of Information Systems, 21, 1–18.

- Cheng, Y. M. (2011). Antecedents and consequences of e-learning acceptance. Information Systems Journal, 21(3), 269–299. https://doi.org/10.1111/j.1365-2575.2010.00356.x

- Chou, W. Y., Hunt, Y. M., Beckjord, E. B., Moser, R. P., & Hesse, B. W. (2009). Social media use in the United States: Implications for health communication. Journal of Medical Internet Research, 11(4), e48. https://doi.org/10.2196/jmir.1249

- Clemes, M. D., Gan, C., & Zhang, J. (2014). An empirical analysis of online shopping adoption in Beijing. China. Journal of Retailing and Consumer Services, 21(3), 364–371. https://doi.org/10.1016/j.jretconser.2013.08.003

- Correia, Loureiro, S. M., Kaufmann, H. R., & Rabino, S. (2014). Intentions to use and recommend to others: An empirical study of online banking practices in Portugal and Austria. Online Information Review, 38(2), 186–208.

- Davis, F. D. (1989). Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS Quarterly: Management Information Systems, 13(3), 319–339. https://doi.org/10.2307/249008

- Davis, F. D., Bagozzi, R., & Warshaw, P. (1989). User acceptance of computer technology: A comparison of two theoretical models. Management Science, 35(8), 982–1003. https://doi.org/10.1287/mnsc.35.8.982

- Deloitte. (2019). The value of online banking channels in a mobile-centric world. https://www2.deloitte.com/us/en/insights/industry/financial-services/online-banking-usage-in-mobile-centric-world.html

- DeLone, W. H., & McLean, E. R. (2003). The DeLone and McLean model of information systems success: A ten-year update. Journal of Management Information Systems, 19(4), 9–30.

- Ding, Z., Saide, S., Siti Astuti, E., Muwardi, D., Najamuddin, N., Jannati, M., & Herzavina, H. (2019). An adoption of acceptance model for the multi-purpose system in university library. Economic Research-Ekonomska Istraživanja, 32(1), 2393–2403. https://doi.org/10.1080/1331677X.2019.1635898

- Dospinescu, O., Dospinescu, N., & Agheorghiesei, D. T. (2021). Fintech services and factors determining the expected benefits of users: Evidence in Romania for millennials and generation. E + M Ekonomie a Management, 24(2), 101–118. https://doi.org/10.15240/tul/001/2021-2-007

- Farah, M. F., Hasni, M. J. S., & Abbas, A. K. (2018). Mobile-banking adoption: Empirical evidence from the banking sector in Pakistan. International Journal of Bank Marketing, 36(7), 1386–1413. https://doi.org/10.1108/IJBM-10-2017-0215

- Fornell, C., & Larcker, D. F. (1981). Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research, 18(1), 39–50. https://doi.org/10.1177/002224378101800104

- Geebren, A., Jabbar, A., & Luo, M. (2021). Examining the role of consumer satisfaction within mobile eco-systems: Evidence from mobile banking services. Computers in Human Behavior, 114(9), 106584. https://doi.org/10.1016/j.chb.2020.106584

- Goh, T. T., & Sun, S. (2014). Exploring gender differences in Islamic mobile banking Acceptance. Electronic Commerce Research, 14(4), 435–458. https://doi.org/10.1007/s10660-014-9150-7

- Gu, J. C., Fan, L., Suh, Y. H., & Lee, S. C. (2010). Comparing utilitarian and hedonic usefulness to user intention in multipurpose information systems. Cyberpsychology, Behavior and Social Networking, 13(3), 287–297. https://doi.org/10.1089/cyber.2009.0167

- Hair, J. F., Ringle, C. M., & Sarstedt, M. (2011). PLS-SEM: Indeed a silver bullet. Journal of Marketing Theory and Practice, 19(2), 139–151. https://doi.org/10.2753/MTP1069-6679190202

- Hampshire, C. (2017). A mixed-methods empirical exploration of UK consumer perceptions of trust, risk, and usefulness of mobile payments. International Journal of Bank Marketing, 35(3), 354–369. https://doi.org/10.1108/IJBM-08-2016-0105

- Hanafizadeh, P., Behboudi, M., Koshksaray, A. A., & Tabar, M. J. S. (2014). Mobile-banking adoption by Iranian bank clients. Telematics and Informatics, 31(1), 62–78. https://doi.org/10.1016/j.tele.2012.11.001

- Handayani, P. W., Hidayanto, A. N., Pinem, A. A., Hapsari, I. C., Sandhyaduhita, P. I., & Budi, I. (2017). Acceptance model of a hospital information system. International Journal of Medical Informatics, 99, 11–28. https://doi.org/10.1016/j.ijmedinf.2016.12.004

- Henseler, J., Ringle, C. M., & Sarstedt, M. (2015). A new criterion for assessing discriminant validity in variance-based structural equation modeling. Journal of the Academy of Marketing Science, 43(1), 115–135. https://doi.org/10.1007/s11747-014-0403-8

- Ho, J. C., Wu, C. G., Lee, C. S., & Pham, T. T. T. (2020). Factors affecting the behavioral intention to adopt mobile banking: An international comparison. Technology in Society, 63(1), 101360–101369. https://doi.org/10.1016/j.techsoc.2020.101360

- Hoffman, D. L., & Novak, T. P. (1996). Marketing in hypermedia computer-mediated environments conceptual foundations: Conceptual foundations. Journal of Marketing, 60(3), 50–68. https://doi.org/10.1177/002224299606000304

- Hsu, M. H., Chang, C. M., Lin, H. C., & Lin, Y. W. (2015). Determinants of continued usage toward social media: The perspectives of uses and gratifications theory and perceived interactivity. Information Research, 20(2), 671–686.

- Hsu, M. H., Tien, S. W., Lin, H. C., & Chang, C. M. (2015). Understanding the roles of cultural differences and socio-economic status in social media continuance intention. Information Technology & People, 28(1), 224–241. https://doi.org/10.1108/ITP-01-2014-0007

- Ifinedo, P. (2016). The moderating effects of demographic and individual characteristics on nurses’ acceptance of information systems: A Canadian study. International Journal of Medical Informatics, 87, 27–35. https://doi.org/10.1016/j.ijmedinf.2015.12.012

- Jebarajakirthy, C., & Shankar, A. (2021). Impact of online convenience on mobile banking adoption intention: A moderated mediation approach. Journal of Retailing and Consumer Services, 58(23), 102312–102323. https://doi.org/10.1016/j.jretconser.2020.102323

- Jebarajakirthy, C., Yadav, R., & Shankar, A. (2020). Insights for luxury retailers to reach customers globally. Marketing Intelligence & Planning, 38(7), 797–811.

- Karahanna, E., Straub, D. W., & Chervany, N. L. (1999). Information technology adoption across time: A cross-sectional comparison of pre-adoption and post-adoption belief. MIS Quarterly, 23(2), 183–213. https://doi.org/10.2307/249751

- Kertzman, S., Fluhr, A., Vainder, M., Weizman, A., & Dannon, P. N. (2018). The role of gender in association between inhibition capacities and risky decision making. Psychology Research and Behavior Management, 11, 503–510.

- Kiljan, S., Simoens, K., Cock, D. D., Eekelen, M. V., & Vranken, H. (2017). A survey of authentication and communications security in online banking. ACM Computing Surveys, 49(4), 1–35. https://doi.org/10.1145/3002170

- Kim, S., & Real, K. (2016). A profile of inactive information seekers on influenza prevention: A survey of health care workers in Central Kentucky. Health Information and Libraries Journal, 33(3), 222–238.

- King, W. R., & He, J. (2006). A meta-analysis of the technology acceptance model. Information & Management, 43(6), 740–755. https://doi.org/10.1016/j.im.2006.05.003

- Ko, H., Cho, C. H., & Roberts, M. S. (2005). Internet uses and gratifications: A structural equation model of interactive advertising. Journal of Advertising, 34(2), 57–70. https://doi.org/10.1080/00913367.2005.10639191

- KPMG. (2020). Mobile banking. Publications/Documents/PDF/mobile-banking-report-2015.pdf, http://www.kpmg.com/UK/en/IssuesAndInsights/Articles

- Kwon, N. (2006). User satisfaction with referrals at a collaborative virtual reference service. Information Research, 11(2), 246.

- Lee, M., Kang, D., Yoon, J., Shim, S., Kim, I. R., Oh, D., Shin, S. Y., Hesse, B. W., & Cho, J. (2020). The difference in knowledge and attitudes of using mobile health applications between actual users and non-user among adults aged 50 and older. Plos One, 15(10), 14.

- Lee, J. H., & Lee, C. F. (2019). Extension of TAM by perceived interactivity to understand usage behaviors on ACG social media sites. Sustainability, 11, 1–19.

- Lee, J. S. (2000). Interactivity: A new approach. In Association of Education in Journalism and Mass Communication Conference, Phoenix, AZ.

- Liébana-Cabanillas, F., Ramos de Luna, I., & Montoro-Ríos, F. (2017). Intention to use new mobile payment systems: A comparative analysis of SMS and NFC payments. Economic Research-Ekonomska Istraživanja, 30(1), 892–910. https://doi.org/10.1080/1331677X.2017.1305784