?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This paper examined the firm-specific abnormal returns of transportation and travel services sectors from the USA, UK, France, China, India, Mexico, Turkey, and Thailand in response to Coronavirus Disease 2019 (COVID-19) using event study methodology. Our results revealed that investors in developed countries provide significant long term abnormal returns for the first 101 days. Furthermore, no significant cumulative average abnormal returns (CAAR) were found in response to the COVID-19 outbreak, travel restrictions, lockdown, stimulus package, and historical decline in oil prices except in the case of the USA. It is concluded that with the gradual increase in new cases and deaths, abnormal returns are also adjusted, making the effects of these events insignificant at the time of their occurrence. Results also showed that firms in developing countries recognized significant negative abnormal returns in response to the second wave of COVID-19. These results are useful for investors in devising investment strategies relevant to contextual settings.

1. Introduction

In the current era of globalization, the connected global resources, easy access to worldwide destinations, and increased mobility increase the likelihood of spreading contagious diseases such as Severe Acute Respiratory Syndrome Coronavirus-1 (SARS-COV-1) (Hung, Citation2003 and Likhacheva, Citation2006), Middle East Respiratory Syndrome (MERS) (Wong et al., Citation2015), Ebola Hemorrhagic Fever (Ebola) (Adebanji et al., Citation2017) and Coronavirus Disease 2019 (COVID-19) (Huang et al., Citation2020). COVID-19 originated from Wuhan, China, in January 2020 and has spread worldwide to become a pandemic. Despite implementing travel bans and quarantine policies, the COVID-19 quickly spread worldwide with a total number of 225.19 million infections and more than 4.6 million deaths at the time of writing. Although COVID-19 affected different industries and working behaviour, the impact on the stock market is seen more prominent (Al-awadhi et al., Citation2020; Ashraf, Citation2020; Baker et al., Citation2020; Farooq et al., Citation2021; Liu, Manzoor et al., Citation2020; Mazur et al., Citation2021; Naik et al., Citation2021; Phuong, Citation2021).

Literature shows that unexpected catastrophic events such as COVID-19 affect stock markets to document high abnormal returns (Carpentier & Suret, Citation2015; Maneenop & Kotcharin, Citation2020; Singh & Neog, Citation2020). Such a relationship shows a robust effect in industries whose operations are directly interrupted by the undesirable event. For instance, during COVID-19, travel restrictions, lockdown, and quarantine policies reduced the national and international mobility that negatively affected the airlines and other allied transportation industries. These companies may provide negative stock returns in response to such adverse operational outcomes. Moreover, the COVID-19 changed people's sentiments and behaviour, which also affected the stock market and the abnormal returns. Behavioural theorists postulate that the abnormal returns are the function of investors' psychological and behavioural factors (Ryu et al., Citation2017). For instance, Lee et al. (Citation2002) contended that investor optimism positively affects price volatility, while pessimistic behaviours act conversely. Since COVID-19 created uncertainty and pessimistic behaviour, one can expect more abnormal returns for the airline and transportation sector.

Investors are always keen to know the nature and intensity of such adverse stock market reactions before devising their investment strategy (Hossain et al., Citation2021). Moreover, policymakers also require the knowledge of such adverse shocks to devise pertinent regulations. Therefore, the primary purpose of this research is to explore the abnormal returns of one of the most affected sectors, i.e., transportation, during COVID-19. However, due to the COVID-19 outbreak, significant events such as travel restrictions, lockdown, oil price crisis and stimulus packages also happened. The stated events affected the business operations of almost every industry and particularly the airline and transportation sector. Hence, this study further explores the abnormal returns of the transportation sector during these events. Mainly, event study methodology is used to calculate the abnormal returns before and after the events of COVID-19 cases, deaths, lockdown, travel restrictions and historical oil price crisis.

Furthermore, the impact of COVID-19 depends on the nature of the financial markets and the macroeconomic environment. For instance, the adverse outcomes of a pandemic can be severe for developing countries where stocks are more volatile and exposed to systematic risks. For instance, Thampanya et al. (Citation2020) contended that investors’ behavioural response to the stock market during the financial crisis is more significant in developing countries. However, investors in developed countries act more rational and respond accordingly. This makes it imperative to investigate the comparative effects of COVID-19 on the financial markets of developed and developing countries. This research is also interesting to investigate such comparative effects of COVID-19.

Thus, the current study revolves around three objectives. First, the impact of the COVID-19 outbreak on abnormal stock returns of the transportation sector is studied. Second, the abnormal returns are explored during major allied events, including travel restrictions, lockdown, oil price crisis and stimulus packages. Third, a comparative analysis of transportation is made for developed and developing countries to provide policy implications. Although some of the studies have explored the impact of COVID-19 on the overall stock markets (Aharon et al., Citation2021; Al-awadhi et al., Citation2020; Ashraf, Citation2020; Baker et al., Citation2020; Farooq et al., Citation2021; Liu, Manzoor et al., Citation2020; Liu, Wang, et al., Citation2020), however, the cross-country, sector-specific and event-based studies are limited particularly in case of the transportation sector. Therefore, the outcome of this research would have strong implications, particularly for investors and policymakers in constructing investment strategies and regulatory frameworks.

The subsequent part of the study consists of four sections. The next chapter will explore the literature related to the impact of pandemics (particularly the COVID-19) on stock performances. The third section explains the tools and techniques used to achieve the research objectives. The fourth section presents the results, while in the last section, a conclusion with limitations and future research recommendations are provided.

2. Literature review

Traditional financial theories believe that the firm-specific fundamental factors are the determinants of stock prices. For instance, the three-factor model assumes that market exposure, size, and book-to-market ratio are the determinants of cross-sectional returns (Fama & French, Citation1992). However, behavioural theories argue that stock prices are the function of investors' psychological and behavioural changes (Ryu et al., Citation2017). Emergencies, catastrophes, and pandemics are among the factors that cause such changes in investor sentiments to provide abnormal results. For instance, Lamb (Citation1995) discussed the impact of 1992 Hurricane Andrew on South Florida and Louisiana stock markets. Takao et al. (Citation2013) investigated the impact of the Great East Japan Earthquake 2011 on stock performances. Similarly, Loh (Citation2006) studied the impact of SARS-COVID-I on stock returns of the aviation industry. These studies found that catastrophic and pandemic events affect the stock markets negatively.

Similar results are found in the case of ongoing COVID-19 that affected the financial markets from all over the world (Liu, Wang et al., Citation2020). COVID-19 affected almost every industry, but the impact on airlines, transportation, and the hospitality sector is more significant due to lockdown and travel restrictions. Lockdown and travel restrictions reduced the operational activities of the airlines and transportation sector. Such negative performances can result in reduced stock returns of the airline and transportation sector. Farooq et al. (Citation2021) explained such negative stock performances with a pessimistic theory where investors respond depressingly to the expected negative cash flows. Furthermore, the pandemics like COVID-19 affect investor sentiments negatively. Such negative sentiments could also result in negative stock performances. This research aims to explore such a relationship between COVID-19 and stock performances of the transportation sector. However, before moving forward, it is imperative to explore the previous literature on the relationship between infectious diseases (such as COVID-19) and stock returns of airlines and the transportation sector. Following search query was used to find the targeted literature from Scopus database.

TITLE-ABS-KEY((transportation OR airline* OR "air services" OR "travel services") AND ("stock market*" OR "stock return*" OR "abnormal return*" OR "stock price*") AND (COVID OR corona OR coronavirus OR "corona virus" OR catastrophe* OR "infectious disease" OR pandemic OR epidemic)) AND (LIMIT-TO (SRCTYPE, "j")) AND (LIMIT-TO (DOCTYPE, "ar"))

The above query was designed to explore the research articles investigating three concepts, i.e., stock market reactions, COVID-19, and the transportation sector. The search query is further filtered by focusing only on journal articles. As a result, the above query provided 26 research documents. After reading the title and abstract of each article, only 18 relevant research articles were found. These studies can be segregated into three types. The first type of studies investigated the impact of COVID-19 on stock performances of different industries, including the airline and transportation sectors. For instance, He et al. (Citation2020) found that COVID-19 adversely affected transportation, mining, electricity & heating, and environment industries in China, particularly in the short run. They used event methodology and calculated abnormal returns for the event window of t-30 to t30. Alam et al. (Citation2021) studied the impact of COVID-19 on stock returns from multiple sectors listed on the Australian Stock Exchange. Their results showed that stock performances of the transportation sector declined during a 10-day window of their event study analysis. Atems and Yimga (Citation2021) quantified the impact of the COVID-19 shock on the United State’s airline industry stock prices. They documented the negative influence of the COVID-19 shock on stock prices, which persisted beyond the day of shock. Carter et al. (Citation2022) studied the factors employed by the market participants to price the negative information into airline, hotel, and tourism firms stocks. They concluded that large firms with higher market-to-book and cash reserves ratios were less affected whereas firms with more leverage were severely affected by the COVID-19.

Liu, Manzoor et al. (Citation2020) explored the short-term effects of COVID-19 on China's stock market. They found that Chinese and Asian stock markets declined after the outbreak of COVID-19. Furthermore, transportation, lodging, and catering sectors documented negative abnormal returns for their event window of t0 to t10. Sherif (Citation2020) investigated the stock returns of sharia-compliant firms from different industries and found that the transportation sector performed worst comparatively. Sayed and Eledum (Citation2021) explored the short term effect of seven COVID-19 related events on the stock returns of the Saudi financial market. They found that the transportation sector is among the most affected sector in this respect. Herwany et al. (Citation2021) showed the effect of COVID-19 on the stock performances of the different sectors from the Indonesian Stock Exchange. Their results showed that the transportation sector documented abnormal returns but less than the financial service, trade and services sectors. Singh and Shaik (Citation2021) explored the short term effect of different WHO announcements regarding COVID-19 on the stock performances of nine different indices (world, developed and developing) from all over the world. They found that the effect of COVID-19 varies across the indices from developed and developing countries. In short, the first type of studies investigated the industry-specific stock performances, including the airlines and transportation sector from different countries.

The second type of studies explored the adverse effects of COVID-19, specifically for the airlines and transportation sectors. For instance, Maneenop and Kotcharin (Citation2020) investigated 52 airlines’ abnormal returns from eight countries using the event study methodology. They selected the event window of t-5 to t5. Their study focused on three announcement dates of the first COVID case in Thailand, the outbreak in Italy, and the assertion of COVID as a global pandemic. Their results revealed that the effect of the declaration of COVID as a pandemic was adverse. They contended that the investors in the transportation sector from western countries responded aggressively to COVID-19 compared to the rest of the world.

Liew (Citation2020) found that the lockdown during COVID-19 affected the stock performances of three leading travel corporations. Similarly, Amuthan (Citation2020) explored that the stock returns of five major Indian airlines decreased during the COVID-19 lockdown. Kökény et al. (Citation2022) studied the impact of COVID-19 on stock performances of major European airlines in the contingency of business model. Lin and Falk (Citation2021) studied the stock returns and volatility of the travel and leisure sector for three Nordic countries during the COVID-19 outbreak. Their results revealed that the idiosyncratic risk of international transportation firms significantly increased after the COVID-19. In short, the second type of studies focuses on the abnormal returns due to COVID-19 for the transportation sector specifically.

The third type of studies tried to develop a prediction model of stock returns and volatility. For instance, Jabeen et al. (Citation2021) developed a prediction model of stock returns using positive and negative sentiments regarding COVID-19. Deb (Citation2021) used Twitter data and Google trends to predict the stock volatility of three major airlines. Despite this, a couple of studies also investigated the spillover effect of the transportation sector (Qiao & Yan, Citation2020). In conclusion, the above-stated literature confirms that COVID-19 negatively affected the stock performances of the transportation sector. However, most of these studies focus on the number of cases and deaths due to COVID-19. Prior studies have paid less attention to other allied events such as stimulus packages (Harjoto et al., Citation2021; Narayan et al., Citation2021), lockdown (Anh & Gan, Citation2021; Huo & Qiu, Citation2020), travel restrictions (Narayan et al., Citation2021), and historical oil price crisis (Prabheesh et al., Citation2020; Zhang et al., Citation2021).

Furthermore, the cross-country comparison between developed and developing countries is missing in prior studies to suggest contextual policy implications. For instance, the stock markets of developing countries are more volatile and more exposed to behavioural changes. If it is true, then the effect of COVID-19 could be more adverse for developing countries than developed countries. Another vital facet can be to assess the short term and long-term early response to the ongoing pandemic.

This research considers these critical perspectives missing in earlier literature and compares the effects of five events related to COVID-19 on the stock market performances of 268 listed firms from the transportation sector and travel services from four developed and developing four countries for a larger event window of 101 days. The outcome of this research will have strong practical implications for a specific context that could help in devising responsive strategies in the expected second wave of COVID or similar circumstances.

3. Methodology

This research selected a sample of 268 transportation and travel service firms from eight different countries, including the USA, UK, France (FR), Mexico (ME), China (CH), Thailand (TH), Turkey (TU), and India (IN). The first four countries belong to developed countries, while the other four are developing economies. presents the distribution of the selected sample from each country. These countries are selected based on four criteria.

Table 1. Demographics of sample countries.

First, we selected the top countries where the tourism sector contributed significantly to their GDP. In the second stage, we segregated these firms into developed and developing countries. In the third stage, we ranked these countries based on the number of COVID-19 cases and deaths for both categories. At the fourth stage, the top four countries (from each category) are selected for which the stock market data of at least six firms are available in Yahoo Finance. It is because we extracted all the stock market data from Yahoo Finance. Although, there are some other countries where the tourism sector significantly contributes and are affected by the high number of COVID-19 cases, such as Italy and Spain. However, we could not include such firms due to the data limitation. At last, the top four developing and developed countries are selected for further analysis.

This research deployed the event study methodology using seven announcements, including the first COVID-19 case, day of highest new cases, day of highest deaths, stimulus package announcement, lockdown, travel restrictions, and oil price crisis. The dates of first six events were collected from the IMF Policy Tracker database, and the oil price crisis data were taken from the International Energy Agency database. The abnormal returns are calculated for 101 days from January 01, 2020, to May 31, 2020. The estimation window for model development consists of 250 days before January 01, 2020. We have used one estimation window for each country to avoid estimation and prediction bias. By using one estimation window, we will be able to analyze the unbiased abnormality of each country due to the pandemic. Furthermore, the reason for selecting 101 days window is the occurrence of five events (including Lockdown, Travel restriction, stimulus packages and historical oil price crisis) during this period.

The announcement dates of each event are provided in . The first event is the announcement of the first COVID-19 case reported in a country. It is argued that such an announcement can significantly create abnormal returns in the short term. Investors may not feel the urgency to respond to the probability of risk, particularly in developed countries. This research further explored the impact of the COVID-19 outbreak (based on the highest new cases and deaths).

Table 2. Announcement dates of each event.

provides the highest and daily average COVID cases and deaths in each country for the sample period from the data taken from the COVID-19 pandemic dataset (Ritchie et al., Citation2020). For instance, the highest cases reported on April 26, 2020, are 38504 in the USA. There were 12515 average daily new cases in the first five months and 760 average daily deaths in the US. Particularly, on April 17, 2020, a total of 6409 people died in the USA in a single day. The announcement of such topmost new cases and deaths could significantly affect investors’ behaviour to create more abnormal stock returns.

Table 3. Reported number of COVID cases and deaths.

Another noteworthy event was the historical crisis of oil prices. On April 20, 2020, the American benchmark prices for oil, West Texas intermediate (WTI), dropped as low as minus $-37.63 per barrel. The decrease in oil prices may be positive news for the transportation and travel service sector. However, during COVID, the transportation sector could not benefit from low oil prices as lockdown and travel restrictions limited human mobility. Similarly, many countries offered stimulus packages for the business to survive during infectious diseases. Such news can have positive effects if the stakeholders trust the government, or it can be devastating news describing the adversity of the problem. At last, two other announcement dates of lockdown and travel restrictions are also critical events for the transportation sector. Abnormal returns in response to these events are also analyzed using the t-1 to t7 window, where t0 is the event date. However, for the first COVID case event, abnormal returns are analyzed until May 31, 2020.

Daily market data of all the firms are extracted from Yahoo Finance using R-package "batchgetsymbols" (Perlin & Maintainer, 2018). This package extracts the publicly available stock price data from Yahoo Finance in a tidy format that can be used for event study analysis. Previously various studies have used this method of scrapping the stock market data from Yahoo Finance (Dima et al., Citation2021; Ganesh & Iyer, Citation2021; Tomio, Citation2020). After fetching the prices, the single-factor market model of GARCH (1,1) errors was applied using the R-package "EventStudy" as proposed by Schimmer et al. (Citation2014). The expected return and conditional variance

of GARCH model is as follow;

Eq. 1

Eq. 1

Eq. 2

Eq. 2

Equation 2 is the variance model of GARCH (1, 1), where ω is the intercept coefficient, σt2 is the conditional variance, and residuals constructed from mean filtration is indicated with ε. The above stated mean-variance formulas measure abnormal returns of stock concerning specific events (Chang et al., Citation2018). Abnormal returns are calculated with the following equation 3

Eq. 3

Eq. 3

ERit is the expected returns extracted from equation (1) applied to the estimation window, and Rit is the actual returns of the event window. Average abnormal returns are further calculated to find the sectoral abnormality in the market using the following equation.

Eq. 4

Eq. 4

The significance of the AAR is analysed using the following t test;

Eq. 5

Eq. 5

Where

This research also calculated Cumulative average abnormal returns (CAAR) to check the event window's overall performance and significance. CAAR values are calculated between two periods using the following formula.

Eq. 6

Eq. 6

Where

4. Results

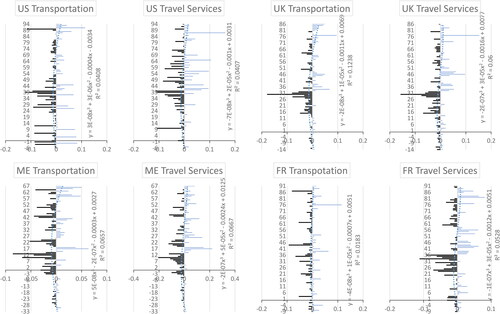

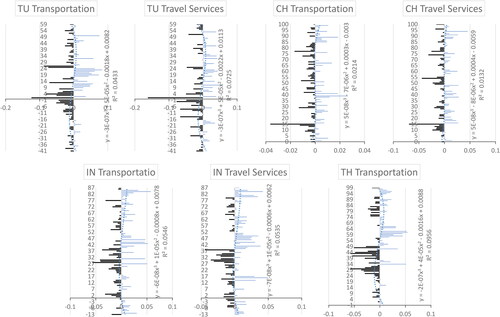

and provide the AARs of 101 days for both transportation and travel service sectors from developed and developing countries, respectively. These figures explore how COVID 19 has affected the stock returns in a timeline of 101 days. The horizontal line on each graph shows the event date of the first COVID case announcement. Red lines on each graph's left side represent the negative abnormal returns, while the blue lines on the right side are positive abnormal returns. Each graph's trend line represents the three-order polynomial regression that indicates the overall movement of abnormal returns of the market using the following equation

Eq. 7

Eq. 7

Figure 1. Average abnormal return (AAR) and polynomial regression of major event Window for developed countries.

Source: Authors calculation.

Figure 2. Average abnormal return (AAR) and polynomial regression of major event Window for developing countries.

Source: Authors calculation.

and show that the R-squares of all the figures are less than 0.15 indicating the low predictability of the stock returns. We also tested the polynomial model from 2nd to 6th order and found the same bad fitness for developing and developed countries. This indicates that the GARCH single factor model fails to predict stock returns and verifies the existence of abnormal returns during the selected period.

shows that the trend line of abnormal returns in most cases is quadratic for developed countries. Initially, firms documented negative abnormal returns, while almost after the 40th to 50th day of the first COVID cases, these abnormal returns started moving to positive abnormal returns. At the end of the window period, abnormal returns of both sectors from developed countries remain positive. Conversely, Turkey (TU) and Thailand (TH) show polynomial trends where abnormal returns were negative initially and become positive preceding to becoming negative again, as shown in .

Notably, the first COVID case was reported in Turkey after two months of the pandemic. There is a spillover effect of other market performance on Turkey's tourism market before the first COVID case. AARs started to become negative as there was set back in the rest of the world that affected the mobility and tourism sector worldwide. There was a recovery time that shifted average abnormal returns to positive, but it turned negative after some time. The transportation sector of Thailand also documented high negative abnormal returns in the starting period that became positive for time but again moved back to negative abnormal returns. Since no company record was found for Thailand travel services, the transportation sector results are provided only. These results indicate that developing countries react more negatively to the second phase of the pandemic than developed countries. However, in the case of Indonesia, abnormal returns are found quadratic as abnormal returns turn positive after the initial negative phase.

presents the CAAR and ABHAR of 101 days from January 10, 2020, to May 31, 2020. In the table, bold values represent significant statistics based on nonparametric tests. Results show that no developing country documented significant CAAR for both transportation and travel services sectors. Similar results are found in the case of ABHAR, where only the transportation sector of Thailand documented significant ABHAR.

Table 4. CAAR and ABHAR during January 10, 2020, to May 31, 2020.

also shows that 33 firms out of 79 showed positive CAAR while the rest of the 46 firms recognized negative CAAR. These statistics show that COVID-19 did not affect developing countries severely in the long run. It is possible that the high volatility risk of developing countries created positive abnormal returns opportunities. Consequently, positive abnormal returns may intersect the effects of negative abnormal returns to provide insignificant results.

Conversely, all the developed countries except France showed significant negative CAAR for 101 days. The average CAAR of all the developed countries is −0.3671, much greater than the average CAAR of developed countries (-0.0532). Results revealed that 158 out of 191 firms from developed countries recognized negative CAAR compared to only 33 firms with positive CAAR. It concludes that COVID-19 affected the transportation and travel sector of developed countries more severely. Mainly, COVID-19 affected the transportation sector of the USA, Mexico and the UK. From 108 transportation firms in the US, only 19 firms have positive CAAR, while the other 88 firms documented negative CAAR. One of the reasons for such negative consequences can be rational investors. Since developed markets are less volatile, and participants respond more rationally as compared to developing countries. Therefore, it is might possible that investors are seeing COVID-19 rationally and evaluating its long-term negative consequences. Hence, it is concluded that COVID-19 affected developed countries' transportation and travel service sectors in the long run.

Furthermore, abnormal returns of seven selected events (as mentioned in ) are analyzed at the window of t-3 to t7. analyses the abnormal returns after the first COVID case announcement. In the table, bold values are significant abnormal returns based on the generalized sign Z test. Results indicated no potential impact of the announcement of the first COVID case on the tourism sector as all the CAAR values are not significant. Investors did not react immediately to the event. In Turkey's case, negative abnormal returns of −12.4% and −16.1% are evidenced for transportation and travel services, respectively, but these numbers are not significant. These results are consistent with Kim and Gu (Citation2004), who found no significant effect of the first COVID case during t0 to t+5.

Table 5. Major events and CAAR of transportation sector.

However, considering the peak of new cases, only the USA transportation sector documented significant negative CAAR as shown in . Similar results are found in the case of peak deaths. However, no significant negative CAAR or AAR was evidenced in France after the peak new cases or death. This indicates that the event of the highest cases and deaths are not important for these markets. It is possible that the market already has reacted to the increasing number of cases and deaths before reaching the maximum level. It is because new cases and deaths reached to its peak gradually and adjusted abnormal returns accordingly. Hence, it is concluded that investors do not respond aggressively to COVID related events (both positive and negative) in a shorter period. shows that all other events (i.e. oil price, package, lockdown and restrictions) did not affect the CAAR but in the USA. The previous argument of already adjustment can be applied over here. Since, the COVID-19 cases and deaths increased gradually, therefore it is probable that the market has already adjusted the negative performances and further resisted to provide more abnormal returns in response to these events. In short, it can be concluded that COVID-19 affected stock returns of developed countries in the long run for the first 101 days while the highest deaths and cases in a single day, lockdown, travel restrictions and oil price crisis did not provide short term abnormal returns.

5. Conclusions

The current study analyses the stock abnormality of the transportation and travel service sectors in response to COVID-19. It is argued that abnormal returns during COVID-19 can be different for firms in developed and developing countries. It is because the stock markets of developing countries are more volatile, while investors in developed countries are rational. Therefore, this research selected 268 firms from four developed countries (USA, UK, Mexico, and France) and four developing countries (Turkey, India, Thailand, and China). The sample countries are selected due to the significant contribution of the tourism sector to their GDP. Results revealed that the first COVID case in Turkey was reported late. However, before the first case, firms in Turkey reported negative abnormal returns due to the spillover effect from other developed countries. On average, COVID-19 affected the transportation and travel service of developed countries more severely compared to developing countries till May 31, 2020. In developing countries, investors got both benefits and losses due to high volatility. As a result, insignificant CAAR was found in developing countries during the event window of 101 days.

It is also found that abnormal returns in developing countries follow the polynomial pattern and document negatively again to the second wave of COVID-19. Conversely, investors in developed countries react rationally and respond to COVID-19 in the long run. Initially, the abnormal returns of developed countries were negative, and after 40 days, these abnormal returns were positive. The negative abnormal returns can be due to expected negative cash flow as contended by 2. Farooq et al. (Citation2021) argued that when negative cash flows are expected due to pandemics, investors respond pessimistically and lead to more abnormal returns. Therefore, it is concluded that investors in developed countries are responding rationally. The reason of their rationality can be the less asymmetric information and technical efficiencies of the stock market operations. Furthermore, abnormal returns are analyzed in response to seven events, including COVID first date, highest death case, highest new cases, the decline in oil prices, lockdown, travel restrictions, and stimulus packages. Results revealed no significant CAAR in response to these events for all countries except the USA. It is conjectured that a gradual increase in new cases and deaths during the ongoing pandemic gradually contributed to abnormal returns. Consequently, abnormal returns are not recognized aggressively in response to such events.

5.1. Limitations and future research recommendations

This study used the stock market data from Yahoo Finance. Due to the data limitation, this study could not analyze important countries such as Italy and Spain. Furthermore, the analysis covered only the transportation sector and travel services. Similar analysis of tourism operators can provide valuable insights. The scope of this research is also confined to the first 100 days after the COVID-19 first case announcement. Further analysis is required to explore the third, fourth, and fifth waves of COVID-19. Hence, future studies are recommended to explore abnormal returns for other important countries and industries considering the third and fourth waves. The upcoming studies also contribute to this contemporary literature in the following ways. First, the upcoming studies compared the impact of different variants of COVID-19 such as SARS-CoV-2, Delta, and Omicron on the stock markets and investor’s behaviour in the different regions of the world. Second, the researchers should employ the various robust models of forecasting abnormal returns as our study is limited to the five-factor model. The third exciting area is to analyze the abnormality of stock retruns in periods of the COVID-19 new cases outbursts. Fourth, the future studies should exmine the impact of COVID-19 on abnormal returns of various types of stock e.g., Islamic stocks vs. conventional stocks. Finally, the other promising area is adding the country-specific anomalies such as natural culture, business cycle, micro and/or macroeconomic indicators, healthcare facilities, and health-consciousness among the general public in the analysis while exploring the impact of the COVID-19 on stock markets.

Disclosure statement

No potential conflict of interest was reported by the authors.

References

- Adebanji, A., Oluwole, O. I., Ogunnaike, O. O., & Ibidunni, A. S. (2017). Globalization and Ebola disease: Implications for business activities in Nigeria. African Journal of Business Management, 11(3), 47–56. https://doi.org/10.5897/AJBM2016.8133

- Aharon, D. Y., Jacobi, A., Cohen, E., Tzur, J., & Qadan, M. (2021). COVID-19, government measures and hospitality industry performance. PloS One, 16(8), e0255819. https://doi.org/10.1371/journal.pone.0255819

- Alam, M. M., Wei, H., & Wahid, A. N. M. (2021). COVID-19 outbreak and sectoral performance of the Australian stock market: An event study analysis. Australian Economic Papers, 60(3), 137–482. https://doi.org/10.1111/1467-8454.12215

- Al-awadhi, A. M., Alsaifi, K., Al-awadhi, A., & Alhammadi, S. (2020). Death and contagious infectious diseases: Impact of the COVID-19 virus on stock market returns. Journal of Behavioral and Experimental Finance, 27, 100325–100326. https://doi.org/10.1016/j.jbef.2020.100326

- Amuthan, R. (2020). COVID-19 impacts on stock return outlooks of stock exchange listed aviation transport companies in India. Journal of Critical Reviews, 7(17), 1155–1160. https://doi.org/10.31838/jcr.07.17.146

- Anh, D. L. T., & Gan, C. (2021). The impact of the COVID-19 lockdown on stock market performance: Evidence from Vietnam. Journal of Economic Studies, 48(4), 836–851. https://doi.org/10.1108/JES-06-2020-0312

- Ashraf, B. N. (2020). Stock markets' reaction to COVID-19: Cases or fatalities? Research in International Business and Finance, 54, 101246–101249. https://doi.org/10.1016/j.ribaf.2020.101249

- Atems, B., & Yimga, J. (2021). Quantifying the impact of the COVID-19 pandemic on US airline stock prices. Journal of Air Transport Management, 97, 102141. https://doi.org/10.1016/j.jairtraman.2021.102141

- Baker, S. R., Bloom, N., Davis, S. J., Kost, K. J., Sammon, M. C., Bloom, N., Viratyosin, T., & Bloom, N. (2020). The unprecedented stock market impact of COVID-19. No. w26945. National Bureau of Economic Research. https://doi.org/10.3386/w26945

- Carpentier, C., & Suret, J. M. (2015). Stock market and deterrence effect: A mid-run analysis of major environmental and non-environmental accidents. Journal of Environmental Economics and Management, 71, 1–18. https://doi.org/10.1016/j.jeem.2015.01.001

- Carter, D., Mazumder, S., Simkins, B., & Sisneros, E. (2022). The stock price reaction of the COVID-19 pandemic on the airline, hotel, and tourism industries. Finance Research Letters, 44, 102047. https://doi.org/10.1016/j.frl.2021.102047

- Chang, C.-L., Hsu, S.-H., & McAleer, M. (2018). An event study analysis of political events, disasters, and accidents for Chinese tourists to Taiwan. Sustainability, 10(11), 4307–4377. https://doi.org/10.3390/su10114307

- Cowan, A. R. (1992). Nonparametric event study tests. Review of Quantitative Finance and Accounting, 2(4), 343–358. https://doi.org/10.1007/BF00939016

- Deb, S. (2021). Analyzing airlines stock price volatility during COVID-19 pandemic through internet search data. International Journal of Finance and Economics, https://doi.org/10.1002/ijfe.2490

- Dima, B., Dima, Ş. M., & Ioan, R. (2021). Remarks on the behaviour of financial market efficiency during the COVID-19 pandemic. The case of VIX. Finance Research Letters, 43, 101967. https://doi.org/10.1016/j.frl.2021.101967

- Fama, E. F., & French, K. R. (1992). The cross-section of expected stock returns. The Journal of Finance, 47(2), 427–465. https://doi.org/10.2307/2329112

- Farooq, U., Nasir, A., Bilal, & Quddoos, M. U. (2021). The impact of COVID-19 pandemic on abnormal returns of insurance firms: A cross-country evidence. Applied Economics, 53(31), 3658–3678. https://doi.org/10.1080/00036846.2021.1884839

- Ganesh, A., & Iyer, S. (2021). Impact of firm-initiated tweets on stock return and trading volume. Journal of Behavioral Finance, 1–12. https://doi.org/10.1080/15427560.2021.1949717

- Harjoto, M. A., Rossi, F., & Paglia, J. K. (2021). COVID-19: Stock market reactions to the shock and the stimulus. Applied Economics Letters, 28(10), 795–797. https://doi.org/10.1080/13504851.2020.1781767

- He, P., Sun, Y., Zhang, Y., & Li, T. (2020). COVID–19’s impact on stock prices across different sectors—An event study based on the Chinese stock market. Emerging Markets Finance and Trade, 56(10), 2198–2212. https://doi.org/10.1080/1540496X.2020.1785865

- Herwany, A., Febrian, E., Anwar, M., & Gunardi, A. (2021). The influence of the COVID-19 pandemic on stock market returns in Indonesia stock exchange. Journal of Asian Finance, Economics and Business, 8(3), 39–47.https://doi.org/10.13106/jafeb.2021.vol8.no3.0039

- Hossain, S., Gavurová, B., Yuan, X., Hasan, M., & Oláh, J. (2021). The impact of intraday momentum on stock returns: Evidence from S&P500 and CSI300. E & M Ekonomie A Management, 24(4), 124–141.

- Huang, J., Wang, H., Fan, M., Zhuo, A., Sun, Y., & Li, Y. (2020). Understanding the impact of the COVID-19 pandemic on transportation-related behaviors with human mobility data. In Proceedings of the ACM SIGKDD International Conference on Knowledge Discovery and Data Mining (pp. 3443–3450). https://doi.org/10.1145/3394486.3412856

- Hung, L. S. (2003). The SARS epidemic in Hong Kong: What lessons have we learned? Journal of the Royal Society of Medicine, 96(8), 374–378. https://doi.org/10.1258/jrsm.96.8.374

- Huo, X., & Qiu, Z. (2020). How does China’s stock market react to the announcement of the COVID-19 pandemic lockdown? Economic and Political Studies, 8(4), 436–461. https://doi.org/10.1080/20954816.2020.1780695

- Jabeen, A., Afzal, S., Maqsood, M., Mehmood, I., Yasmin, S., Niaz, M. T., & Nam, Y. (2021). An LSTM based forecasting for major stock sectors using COVID sentiment. Computers, Materials and Continua, 67(1), 1–21. https://doi.org/10.32604/cmc.2021.014598

- Kim, H., & Gu, Z. (2004). Impact of the 9/11 terrorist attacks on the return and risk of airline stocks. Tourism and Hospitality Research, 5(2), 150–163. https://doi.org/10.1057/palgrave.thr.6040013

- Kökény, L., Kenesei, Z., & Neszveda, G. (2022). Impact of COVID-19 on different business models of European airlines. Current Issues in Tourism, 25(3), 458–474. https://doi.org/10.1080/13683500.2021.1960284

- Lamb, R. P. (1995). An exposure-based analysis of property-liability insurer stock values around Hurricane Andrew. The Journal of Risk and Insurance, 62(1), 111. https://doi.org/10.2307/253695

- Lee, W. Y., Jiang, C. X., & Indro, D. C. (2002). Stock market volatility, excess returns, and the role of investor sentiment. Journal of Banking & Finance, 26(12), 2277–2299. https://doi.org/10.1016/S0378-4266(01)00202-3

- Liew, S. (2020). The effect of novel coronavirus pandemic on tourism share prices. Journal of Tourism Futures, https://doi.org/10.1108/JTF-03-2020-0045

- Likhacheva, A. (2006). SARS revisited. Ethics Journal of the American Medical Association, 8(4), 219–222.https://doi.org/10.1001/virtualmentor.2010.12.8.medu1-1008

- Lin, X., & Falk, M. T. (2021). Nordic stock market performance of the travel and leisure industry during the first wave of Covid-19 pandemic. Tourism Economics, 135481662199093. https://doi.org/10.1177/1354816621990937

- Liu, H., Manzoor, A., Wang, C., Zhang, L., & Manzoor, Z. (2020). The COVID-19 outbreak and affected countries stock markets response. International Journal of Environmental Research and Public Health, 17(8), 2800. https://doi.org/10.3390/ijerph17082800

- Liu, H. Y., Wang, Y., He, D., & Wang, C. (2020). Short term response of Chinese stock markets to the outbreak of COVID-19. Applied Economics, 52(53), 5859–5872. https://doi.org/10.1080/00036846.2020.1776837

- Loh, E. (2006). The impact of SARS on the performance and risk profile of airline stocks. International Journal of Transport Economics, 33(3), 401–422.https://doi.org/10.1400/55242

- Maneenop, S., & Kotcharin, S. (2020). The impacts of COVID-19 on the global airline industry: An event study approach. Journal of Air Transport Management, 89(August), 101920. https://doi.org/10.1016/j.jairtraman.2020.101920

- Mazur, M., Dang, M., & Vega, M. (2021). COVID-19 and the March 2020 stock market crash. Evidence from S&P1500. Finance Research Letters, 38, 101690. https://doi.org/10.1016/j.frl.2020.101690

- Naik, P. K., Shaikh, I., & Huynh, T. L. D. (2021). Institutional investment activities and stock market volatility amid COVID-19 in India. Economic Research-Ekonomska Istraživanja, 1–19. https://doi.org/10.1080/1331677X.2021.1982399

- Narayan, P. K., Phan, D. H. B., & Liu, G. (2021). COVID-19 lockdowns, stimulus packages, travel bans, and stock returns. Finance Research Letters, 38, 101732. https://doi.org/10.1016/j.frl.2020.101732

- Perlin, M., & Maintainer. (2018). Package “BatchGetSymbols” title downloads and organizes financial data for multiple tickers (2.6.1). R package version. ftp://cran.r-project.org/pub/R/web/packages/BatchGetSymbols/BatchGetSymbols.pdf

- Phuong, L. C. M. (2021). How Covid-19 affects the share price of Vietnam's pharmaceutical industry: Event study method. Entrepreneurship and Sustainability Issues, 8(4), 250–261. https://doi.org/10.9770/jesi.2021.8.4(14)

- Prabheesh, K. P., Padhan, R., & Garg, B. (2020). COVID-19 and the oil price–stock market nexus: Evidence from net oil-importing countries. Energy Research Letters, 1(2), 13745. https://doi.org/10.46557/001c.13745

- Qiao, F., & Yan, Y. (2020). A demand-oriented industry-specific volatility spillover network analysis of china’s stock market around the outbreak of COVID-19. Asian Economic and Financial Review, 10(11), 1321–1341. https://doi.org/10.18488/journal.aefr.2020.1011.1321.1341

- Ritchie, H., Mathieu, E., Rodés-Guirao, L., Appel, C., Giattino, C., Ortiz-Ospina, E., Hasell, J., Macdonald, B., Beltekian, D., & Roser, M. (2020). Coronavirus pandemic (COVID-19). https://ourworldindata.org/coronavirus

- Ryu, D., Kim, H., & Yang, H. (2017). Investor sentiment, trading behavior and stock returns. Applied Economics Letters, 24(12), 826–830. https://doi.org/10.1080/13504851.2016.1231890

- Sayed, O. A., & Eledum, H. (2021). The short-run response of Saudi Arabia stock market to the outbreak of COVID-19 pandemic: An event-study methodology. International Journal of Finance and Economics,https://doi.org/10.1002/ijfe.2539

- Schimmer, M., Levchenko, A., & Müller, S. (2014). EventStudyTools (Research Apps). http://www.eventstudytools.com

- Sherif, M. (2020). The impact of Coronavirus (COVID-19) outbreak on faith-based investments: An original analysis. Journal of Behavioral and Experimental Finance, 28, 100403. https://doi.org/10.1016/j.jbef.2020.100403

- Singh, M. K., & Neog, Y. (2020). Contagion effect of COVID-19 outbreak: Another recipe for disaster on Indian economy. Journal of Public Affairs, 20(4), 1–8. https://doi.org/10.1002/pa.2171

- Singh, G., & Shaik, M. (2021). The short-term impact of covid-19 on global stock market indices. Contemporary Economics, 15(1), 1–18. https://doi.org/10.5709/ce.1897-9254.432

- Takao, A., Yoshizawa, T., Hsu, S., & Yamasaki, T. (2013). The effect of the great east Japan earthquake on the stock prices of non-life insurance companies. The Geneva Papers on Risk and Insurance - Issues and Practice, 38(3), 449–468. https://doi.org/10.1057/gpp.2012.34

- Thampanya, N., Wu, J., Nasir, M. A., & Liu, J. (2020). Fundamental and behavioural determinants of stock return volatility in ASEAN-5 countries. Journal of International Financial Markets, Institutions and Money, 65, 101193. https://doi.org/10.1016/j.intfin.2020.101193

- Tomio, B. (2020). Carry trade in developing and developed countries: A Granger causality analysis with the Toda-Yamamoto appr. Economics Bulletin, 40(3), 2154–2164.

- Wong, G., Liu, W., Liu, Y., Zhou, B., Bi, Y., & Gao, G. F. (2015). MERS, SARS, and Ebola: The role of super-spreaders in infectious disease. Cell Host & Microbe, 18(4), 398–401. https://doi.org/10.1186/s40854-021-00277-7

- Zhang, F., Narayan, P. K., & Devpura, N. (2021). Has COVID-19 changed the stock return-oil price predictability pattern? Financial Innovation, 7(1), 1–10. https://doi.org/10.1016/j.chom.2015.09.013 https://doi.org/10.1186/s40854-021-00277-7