?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Using the institutional theoretical perspective, this study seeks to unearth the antecedents of the mixed results in the extant literature regarding the association between corporate green investment (CGI) and profitability. The study utilized a novel dataset comprising environmental research data from Chinese A-share listed companies for the period 2010–2019. The findings indicate that CGI enhances profitability and that the positive association is reinforced by the promulgation of Environmental Protection Law 2015. Regional development also augments CGI’s positive effect on firms’ profitability. Nevertheless, no significant association is observed between firm profitability and CGI among firms operating within environmentally sensitive sectors. Our findings imply that apart from regulatory forces, normative and cognitive pressures are also key instruments that may be employed by governments to motivate firms to embrace greener and more sustainable practices.

1. Introduction

Since the signing of the Kyoto Protocol in 2005, various governments have recognized the value of enterprises aimed at reducing carbon emissions and improving environmental performance (Shen et al., Citation2020). It is now evident that businesses are responsible for a considerable proportion of environmental pollution worldwide. From the perspective of institutional development, the regulations issued by different governments aim to enhance the ecological environment whereby firms are also considered liable for preventing and controlling environmental pollution, as they are the primary users of resources. In practice, these regulations urge businesses to participate in environmental protection efforts and invest in projects that serve as a micro-foundation for long-term sustainable growth (Xu & Yan, Citation2020). However, firms that engage in environmental protection initiatives may face greater operating costs and lower profitability. Thus, the goal of these firms is to develop environmental strategies that minimize environmental pollution while facilitating improved economic performance (Lee et al., Citation2015).

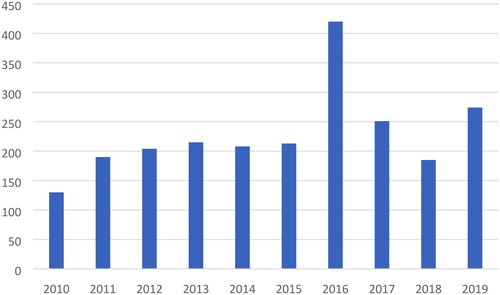

A growing body of research concerning the economic benefits of corporate environmental investment has emerged. However, the extant literature does not provide a clear direction or type (negative, positive, etc.) of association between environmental protection investment and firm performance. For example, some studies have observed a positive correlation between CGI and financial performance (Nakamura, Citation2011; Singal, Citation2014), while others claimed a negative or non-significant relationship between them (de Souza Cunha & Samanez, Citation2013; Lee et al., Citation2015; Su, Citation2019; Zhang & Shuang, Citation2021). At the same time, several studies have demonstrated a non-linear association between them (Pekovic et al., Citation2018). These contradictory results can be explained by these studies’ lack of any theoretical underpinning to explain the relationship, methodological issues, and contextual factors, such as the regulatory environment under which firms operate (Wong et al., Citation2018). In terms of contextual factors, governmental actions have the potential to enhance or impede overall sustainable economic growth. The regulations introduced by governments have a major impact on firms’ behavior with respect to environmental responsibility, particularly when it comes to investing in environmental initiatives (Huang & Lei, Citation2021). In this scenario, it remains unclear how firms deal with the institutional pressures they experience and how they maintain environmental legitimacy while sustaining profitability. To fill the above research gap, the current study is designed to understand the impact of the institutional environment on the association between CGI and profitability. For empirical analysis, we used in this study the updated green investment data pertaining to Chinese listed companies for the period 2010–2019 (). The Chinese institutional setting is selected because of the considerable institutional involvement in the promotion of green investments and the rapid rise in Chinese firms’ investments, as depicted in .

Figure 1. Yearly number of listed companies made green investment in China made by Chinese listed companies.

Source: Authors calculation based on the data obtained from CSMAR.

This study contributes to the extant literature in several ways. First, we add to the debate concerning the economic benefits of investing in corporate green management practices (Stevanović et al., Citation2019; Wong et al., Citation2018), specifically investments in environmental protection initiatives (Lundgren & Zhou, Citation2017; Nakamura, Citation2011; Shabbir & Wisdom, Citation2020; Su, Citation2019). In particular, our research provides evidence for CGI’s positive influence on Chinese firms’ profitability. Second, our study identifies environmental policy, regional development, and environmental industry affiliation as institutional factors that influence the relationship between CGI and profitability. It functions as a link between institutional growth and corporate environmental management. Third, the present study employs the novel longitudinal green investment dataset (for the period 2010–2019) pertaining to Chinese companies obtained from the country’s largest database. In comparison to earlier investigations conducted in similar contexts (Chen & Feng, 2019; Chen & Ma, 2021; Su, 2019), the availability of up-to-date longitudinal data allows us to capture the cross-sectional industry effects in our analysis. Finally, the current study contributes to institutional theory by arguing that, apart from regulatory forces, normative and cognitive pressures are also key instruments that governments may employ to motivate firms to embrace greener and more sustainable practices.

The rest of the paper is organized into sections. Section 2 explains this work’s theoretical foundations, reviews relevant literature, and generates the hypotheses. Section 3 describes the research methodology, while Section 4 analyzes the empirical findings. Section 5 concludes the study with a discussion of the significant results and presents the findings’ implications and future research prospects.

2. Theory, literature, and hypothesis

2.1. Theoretical perspective

Dimaggio and Powell (Citation2013) influential study on the convergence of firms’ behaviors due to institutional pressures in various organizational fields is widely cited in the extant literature on firm behavior and business strategy. Institutional theory concerns stakeholders’ attitudes and expectations toward a firm’s environmental performance under different internal and external contingency factors (Yang et al., Citation2018). This theory suggests that the coercive, normative, and mimetic pressures from formal and informal institutions shape and constrain the strategies and decisions adopted by firms stemming from concerns for legitimacy (Grewal & Dharwadkar, Citation2002; Matten & Moon, Citation2008).

Chiu and Sharfman (Citation2011) suggested that a firm’s environmentally and socially responsible behavior stems from its legitimacy-seeking drive under external pressures elicited by stakeholders and society. Through these actions, firms disseminate signals indicating that they are proactively engaged in environmentally responsible activities in an attempt to garner legitimacy (Frondel et al., Citation2008). Due to CGI the negative environmental impacts of firm’s operations is minimized, thus increasing a firm’s reputation and competitive advantage. In turn, this can help increase firm value and improve its financial performance.

Under institutional theory, coercive pressures are induced by regulatory forces, such as policies, laws, and rules formulated by the authorized entities. In a recent study, Naveed et al. (Citation2021) reported these pressures as the key drivers of environmental management practices. These tools use enabling incentives or impeding sanctions to channel firms’ actions toward the desired behaviors. Therefore, firms are inherently motivated to comply with laws and policies devised by the authorities (Qian et al., Citation2010) not only as a means of garnering legitimacy, but also to avoid penalties and to establish a relationship with them (Huang & Sternquist, Citation2007).

The normative pressures also induce environmentally responsible behaviors from the perspective of a firm’s legitimacy urge. The external environment reportedly elicits differential legitimacy drives in various regions based on the mix of cognitive forces and enabling/impeding conditions (Marquis et al., Citation2007). Such differences generate various levels of normative pressures that potentially guide a firm’s behavior in terms of environmental responsibility (Campbell, Citation2007; Kolk & Levy, Citation2001; Matten & Moon, Citation2008).

Mimetic pressures under institutional theory are enticed by the professional and internalized norms of appropriate actions in an organizational field (Fini & Toschi, Citation2016). Industry setting is one such organizational field, which can be attributed to the differentiated adoption of environmentally responsible behaviors (Cormier et al., Citation2005; Jackson & Apostolakou, Citation2010). In their study, Clarkson et al. (Citation2008) proposed the preferential adoption of environmentally responsible behaviors through different entities based on stakeholders’ the legitimacy urge, which is shaped by the environmental impacts of a firm. In view of the above discussion, institutional theory, complemented by the legitimacy view, constitutes the current study’s theoretical underpinning.

2.2. CGI and profitability

Recent corporate finance research has empirically underlined the imperative of financial risk management and investment efficiency via market performance, especially in volatile economic and social settings (Mirza et al., Citation2020, Citation2022; Rizvi et al., Citation2020; Yarovaya et al., Citation2021). Furthermore, some research has been published on the efficiency and performance of corporate socially and environmentally responsible investment funds in financial markets over the long and short term (Ferrat et al., Citation2022; Ielasi et al., Citation2018; Lobato et al., Citation2021). However, despite four decades of research on the financial performance of corporate green practices, no single theoretical perspective can explain the inconsistent results (for a review, see Stevanović et al., Citation2019). Studies that proposed a negative relationship between green and financial performance (Hatakeda et al., Citation2012; Wagner, Citation2010) are guided by the traditional perspective. They argue that, in response to environmental issues, businesses must incur additional expenses and financial constraints, thus reducing productivity and firm value (Lundgren & Zhou, Citation2017). However, supporters of the positive financial outcomes of corporate environmental activities (Clarkson et al., Citation2011; Li et al., Citation2017; Wong et al., Citation2018) believe that firms may increase their profitability by being the first to implement green policies that can enhance corporate competitiveness (Porter & Van Der Linde, Citation1995). Some have even claimed a non-linear relationship between corporate environmental performance and financial outcomes (Boakye et al., Citation2021; Zhang et al., Citation2020).

These contradictory findings can be explained by the differences in study contexts (Molina‐Azorín et al., Citation2009), the sizes of the firms under observation (Boakye et al., Citation2021), the empirical methodologies used for analysis (Horváthová, Citation2010), the extent of environmental performance (Trumpp & Guenther, Citation2017), and the directions of association and time horizons (Hang et al., Citation2019). Lee et al. (Citation2015) asserted that an in-depth conceptual characterization of corporate environmental performance is required. Environmental performance is not a unidimensional construct but includes various aspects that are expected to behave differently in varying contexts, with diverse financial implications. This situation prompts the study of various aspects of corporate environmental performance in both theoretical and quantitative research (Hang et al., Citation2019).

Given that a growing body of literature has investigated the impacts of CGI, a key research question that has been addressed is whether it pays to invest in green initiatives. First, several studies have reported the positive influence of CGI on firm profitability (Shabbir & Wisdom, Citation2020; Singal, Citation2014; Su, Citation2019; Zhang & Shuang, Citation2021). Nakamura (Citation2011) used a longitudinal dataset of small and medium-sized Japanese corporations to investigate the impact of green investments on firm performance. The findings revealed positive financial performance arising from environmental protection efforts in the long run. The results suggest that a time lag exists between green investment and financial outcomes. However, several researchers have claimed that investments in environmental initiatives can hinder profitability (de Souza Cunha & Samanez, Citation2013; Lee et al., Citation2015; Sueyoshi & Goto, Citation2009). In contrast to both strands, Pekovic et al. (Citation2018) observed a non-linear relationship between CGI and corporate economic performance, arguing that profit generation from investments in green projects tends to decrease as the point of optimization, which surpasses expectation, is reached quickly. A firm must then identify the type of appropriate green investment with regard to various stakeholders, because the process of generating profits is complicated by increased environmental costs. At this point, the right magnitude of green investment can determine the decline or improvement of corporate profits. The presence of inconsistent findings suggests that no universal route exists that allows firms to sustain profitability while investing in green projects. Thus, firms should identify and develop green strategies in accordance with their stakeholders’ demands.

At present, many global corporations are embracing various green strategies in response to global calls to mitigate the impacts of climate change on society (Reid & Toffel, Citation2009; Todaro et al., Citation2021). Multiple factors determine the adoption of green strategies, including volume of business, industry affiliation, and a firm’s environmental proactivity, among others (Lee, Citation2012; Radu et al., Citation2020; Weinhofer & Hoffmann, Citation2010). However, the financial implications of sustainable green strategies remain the subject of debate (see, e.g. Damert et al., Citation2017; Lee, Citation2012). Proactive companies have been shown to invest in different sustainable green initiatives. In particular, Orsato (Citation2006) argued that green investment is a strategic decision: managers must proactively identify and invest in projects that benefit society while optimizing company financial returns in the long run. Orsato (Citation2006) further theorized that companies should make sustainable investments based on their strategic skillsets. For example, for some businesses, effective resource usage may pay off as green investment, while for others, the acquisition of environmental certifications and the development of green products may be a source of increasing competitive advantage. Based on the above arguments and discussion, we hypothesize the following.

H1: CGI is positively associated with profitability.

2.3. Roles of institutional factors

Institutional factors have a significant impact on the operations of Chinese corporations – a typical phenomenon in emerging and transition economies. Therefore, we investigated the moderating roles of environmental policy, regional development, and industry membership in the relationship between CGI and profitability.

2.3.1. Environmental policy

To address climate change, the Chinese government has implemented several environmental regulations under the auspices of China’s State Environmental Protection Administration (CSEPA), Measures for Disclosure of Environmental Information (MDEI) (Situ & Tilt, Citation2018), and the Shanghai Stock Exchange (SSE) (Li et al., Citation2018). This new legislation, the strictest environmental administrative regulation in China, has bolstered corporate accountability for pollution control and enhanced the severity of legal penalties for environmental breaches (Huang & Lei, Citation2021).

The theoretical literature on the effect of environmental policy has served as a forum of debates since the introduction of the Porter hypothesis. This hypothesis states that appropriately strict environmental legislations may bring about dynamic innovation, improve efficiency, and eventually increase productivity (Porter & Van Der Linde, Citation1995). However, empirical studies on the relationship between environmental regulations and green investment have only been conducted at the provincial (Hu & Wang, Citation2020; Ren et al., Citation2020) and industrial levels (Jingyan & Lisha, Citation2010; Leiter et al., Citation2011). Few studies have investigated the microfirm-level effects of corporate environmental regulations on green investment. For instance, You et al. (Citation2019) used a sample of Chinese manufacturing companies and found that environmental regulations positively influenced the extent of corporate eco-investments. Their findings also indicated that domestic administration, one of the key stakeholders, exerted significant pressure and restrictions on company economic performance and encouraged businesses to undertake green investments in a bid to meet regulatory compliance. Jin-Fang et al. (Citation2020) found that environmental policy positively moderated the relationship between corporate innovation and green investment. However, Huang and Lei (Citation2021) observed an inverted U-shaped relationship between environmental regulations and green investments in China. Their findings provide support for the Chinese government’s encouragement for green improvements and the role of environmental policies.

However, a trade-off exists between the cost of green investment and that of non-compliance in the context of mandatory regulations. This trade-off includes fewer intensive regulations, thus enabling firms to easily meet the cost of compliance and induce high investments in green technologies. However, when the intensity of regulations is high, the cost of compliance also increases, and firms can only respond passively because it would be difficult for them to satisfy the requirements. Consequently, to reap economic benefits, firms prefer to pay the cost of non-compliance penalties instead (Huang & Lei, Citation2021).

Although the enforcement of mandatory environmental regulations requires firms to comply with policies concerning emissions reduction and other environmental indicators (L. Huang & Lei, Citation2021), firms can also develop their environmental capabilities to deal with such regulatory changes. These capabilities are dependent on the institutional environment in which the firm operates (Madsen, Citation2009). Firms’ capabilities are dynamic, as they often introduce new and eco-friendly production processes while making more investments in green technologies. Doing so not only allows firms to align their operations with mandatory regulations, but also improves their corporate reputations, thereby enhancing their profitability (Gangi et al., Citation2020). Based on the above discussion, we hypothesize the following:

H2a: The enactment of the Environmental Protection Law of China (2015) significantly impacts the positive association between CGI and profitability.

2.3.2. Regional development

The regional context, such as whether the government is centralized or decentralized, is determined by the socioeconomic structure of the country in question, as well as by the civil ethos and the progress of well-being institutes (Albareda et al., Citation2007). Local institutions often promote an environment that enhances regional competitiveness. Regions can foster competitiveness through several measures, one of which is the creation of policies pertaining to corporate social and environmental responsibility. The creation of regional policies for social and environmental activities will assist companies in conducting social responsibility plans and improving their competitiveness, ultimately contributing to the region’s competitiveness (Apospori, Citation2018). Moreover, the appropriateness and efficiency of local authorities’ social and environmental policies may differ according to regional context.

Based on the institutional theoretical framework (Dimaggio, Citation1983), Marquis et al. (Citation2007) emphasized the relevance of legitimacy in various regions as a source of institutional pressure, which substantiates the profitability gaps in corporate green initiatives. In China’s case, the importance of social and environmental issues varies among regions, leading to the emergence of distinct institutional contexts in which environmental policies must be implemented. Wong et al. (Citation2018) noted that corporate green practices differ across Chinese provincial regions. They argued that firms generate more financial returns from green practices in regions where their policies are aligned with the domestic institutional environment. This is not just helpful for firms that aim to establish good relationships with local institutions, but also allows the former to acquire resources or other benefits that will generate positive financial returns. Similarly, Gao et al. (Citation2019) indicated that companies are likelier to have lower earnings if they do not link their social responsibility initiatives with the degree of regional development. They contend that stakeholders in industrialized regions have higher expectations of corporate social responsibility. Consequently, companies in developed regions must devise differential strategies to meet stakeholders’ demands.

Nevertheless, governments design environmental regulations to incentivize and assist businesses in executing eco-friendly projects, given that the execution of such policies is deemed crucial. As in East China, eco-friendly policies are strictly monitored by the regional government under a penalty and reward system (Wong et al., Citation2018). For instance, governments may give preferred tax policies and priority treatment, or they may use local infrastructure as an incentive to encourage firms to participate in green projects (Wang et al., Citation2008). Institutional theory holds that a conducive atmosphere for compliance promotes a method of oversight that aids businesses in adhering to environmental standards (Campbell, Citation2007). Under such a regulatory environment, firms are encouraged to become eco-innovative to achieve competitive advantage (Porter & Van Der Linde, Citation1995). This enables companies to maintain rapport with public authorities for legitimacy-seeking and invest in green products and processes to gain profits, which can ultimately improve environmental quality. By contrast, firms acquire legitimacy by merely fulfilling their environmental responsibilities, especially in a regulatory environment wherein corporate pro-green efforts are not encouraged and in which the rewards system is lax or non-existent.

Given China’s regional sustainability, a substantial regional environmental performance disparity exists (Yu & Choi, Citation2015). Based on the discussion above, we conclude that regional development in China effectively shapes the institutional settings of different regions whereby businesses are often subject to different regulatory environments, and environmental preservation measures cannot always reap financial advantages. We also anticipate that firms from developed regions are likely to generate greater profits from ERI than those from underdeveloped regions. Therefore, we hypothesize the following:

H2b: Regional development significantly impacts the positive association between CGI and profitability.

2.3.3. Environmental industry

Industry setting is an important organizational field that influences the extent to which firms will engage in green behavior. This is because the stakeholders and the public have different expectations regarding green investments from firms associated with various industries. In this regard, Bansal and Roth (Citation2000) reported a strong positive relationship between the characteristics of industry setting and variant expectations of stakeholders relating to green behavior. Studies focused on this dimension operationalize the phenomenon through the bifurcation of industries into more and less polluting industries. Given that firms with greater polluting potential and environmental impact have higher environmental sensitivity, they are overtly expected to have greater social and environmental responsibility (Reverte, Citation2009). The logic behind the stated proposition is derived from legitimacy theory, which argues that environmentally sensitive industries are liable for endangering environmental health, leaving them vulnerable to the extra pressure to obtain social and environmental accreditations to operate. The existing literature reports that firms from industries with greater greener impact, such as the oil and gas, mining, and chemical sectors, are more liable for socially responsible and green behaviors (Jenkins & Yakovleva, Citation2006; Ness & Mirza, Citation1991). Given the above discussion, we hypothesize the following:

H2c: Environmental industry affiliation significantly impacts the positive association between CGI and profitability.

3. Methodology

3.1. Data

The study sample comprises China’s A-share listed firms for the period 2010–2019. The data pertaining to all variables of the study were sourced from the China Stock Market and Accounting Research (CSMAR) database. The longitudinal data on environmental investment were recently updated in CSMAR under the environmental research database. This database includes various datasets relating to financial and non-financial variables. Other researchers have also used CSMAR as a primary source of data for their investigations (Li et al., Citation2020; Su, Citation2019). To obtain the final sample for the research, we merged data pertaining to different variables and excluded missing values. Finally, we obtained an unbalanced sample of 2290 firm-year observations for our empirical analysis.

3.2. Variables

3.2.1. Firm profitability

The dependent variable of the study was determined to capture a firm’s internal financial performance on the balance sheet. It is measured as the ratio of a firm’s annual return to its total assets (Lee et al., Citation2015).

3.2.2. CGI

Following Zeng et al. (Citation2020), we measured this variable as the ratio of a firm’s green investment to its total assets at the end of each year. This variable conceptualizes a firm’s tendency to invest in green initiatives. However, in operational terms, the scale of green investment represents firms’ level of commitment to reducing the impacts of environmental degradation.

3.2.3. Environmental policy

China introduced its Environmental Protection Law at the end of 2014, and it came into effect in 2015. It is among the most stringent environmental policies that have been regulated to reduce the negative impacts of business and industrial operations on the external environment. This law requires listed firms to publicly disclose their environmental protection activities, including their green performance. Since its implementation, it has strengthened corporate responsibility for controlling pollution and has improved the severity of legal consequences for environmental violations. Hence, to understand the impacts of stringent environmental policy on firms’ green investment and profitability, we measured environmental policy as a dummy variable. This is represented as the value of 1 if the year of observation is equal to or greater than 2015 and 0 otherwise (Huang & Lei, Citation2021).

3.2.4. Regional development

Following earlier studies (Gao et al., Citation2019; Wei et al., Citation2017), we used provincial GDP per capita to assess the level of development in each region of China. To operationalize the variable, we created a dummy for regional development by using the median value among the averages. It has a value of 1 if the GDP amount of the region is greater than the median GDP and 0 otherwise. Thus, we divided regions into the two categories of ‘high’ and ‘low’ levels of development. This bifurcation supports our investigation of the differential impacts of high- and low-development regions on the association between firm CGI and profitability.

3.2.5. Environmental industry

To identify distinct industrial classifications in China, we used a two-digit industry code from the China Securities and Regulatory Commission (CSRC, 2012). We constructed a dummy variable equal to 1 based on the purpose of the examination (i.e. whether a company falls within the category of polluting industries, such as metallic, nonmetallic, energy, other manufacturing, etc., and 0 otherwise.

3.2.6. Control variables

We employed firm characteristics and corporate governance factors as control variables in the current work following previous studies (Lee et al., Citation2015; Nakamura, Citation2011; Pekovic et al., Citation2018; Sueyoshi & Goto, Citation2009; Zhang & Shuang, Citation2021). First, we used environmental performance (ENVP) to control for the influence of business environmental action on profitability (i.e. return on assets, ROA). In terms of other firm variables, we controlled for firm size (SIZE), age (AGE), leverage (LEVG), and fixed asset (FAR). SIZE and LEVG enable businesses to acquire more resources and maximize them to generate more profits. Furthermore, AGE enables firms to run their operations with a defined strategy and plan, allowing them to improve their financial performance. Finally, FAR calculates company growth based on the effective utilization of noncurrent assets. In general, the greater the FAR, the larger a firm’s sales, hence, the higher the profits.

In terms of the corporate governance framework, research suggests that board size (BSIZE) and institutional ownership (INSHR) have a positive impact on ROA, while board independence (BIND) and company performance have a mixed relationship (Merendino & Melville, Citation2019; Rashid, Citation2018, Citation2020). Thus, we used BSIZE, BIND, and INSHR as controls for the effects of corporate governance on ROA. Finally, we included industry and year dummies to account for cross-sectional variations across industrial sectors over time.

3.3. Empirical models

We used the least squares dummy variable (LSDV) panel regression technique to empirically evaluate the impacts of CGI on firm profitability (ROA) while adjusting for industry- and year-fixed effects. The LSDV includes indicator variables for each panel unit (e.g. industry and year dummies in our model). It cannot produce estimates for predictors that do not vary within panel units, because the latter are collinear with the indicator variables. In this work, we selected LSDV over the fixed effects (FE) model, because it only controls for the cross-sectional variations among panel but not time variations of group characteristics. To control the effect of extreme values, we winsorized all continuous variables at 1%. The base model is shown below.

(1)

(1)

In the above research model, profitability is the dependent variable, CGI is the main independent variable, and all others are control variables (see for variable definitions). Further, to examine the effect of environmental policy (POLICY), regional development (RGDP), and environmental industry affiliation (INDENV) on the association between CGI and profitability, we include interaction terms and run the following regression models:

(2)

(2)

(3)

(3)

(4)

(4)

Table 1. Definitions of all the variables of the study.

4. Empirical results

4.1. Descriptive results

presents the descriptive statistics of the explanatory and dependent variables employed in this study. For our sample firms, the profitability (ROA) ratio is 4.3%, on average, with a maximum value of 19.5%. This is because the sample composition is based on larger, medium, and small-sized firms (SIZE). The mean green investment ratio (CGI) shows that each firm invests 0.5%, with significant variations in the rate of investment. Similarly, there is a sizable gap between firms with respect to their ENVP. These differences prevail in emerging market firms, whereby each firm must deal with external pressures based on the available resources. Furthermore, the sample includes a mixture of young and old firms (AGE) with reasonable financial leverage (LEVG).

Table 2. Descriptive statistics.

reports the results of the pairwise correlation between the independent and dependent variables. As anticipated, CGI and ENVP show a positive correlation with ROA. However, we find no significant correlations between the explanatory variables.

Table 3. Pairwise correlation matrix.

4.2. Main results

presents the results of the main effect and moderation effects. Model (1) reports that CGI is positively associated with ROA in China thereby indicating that investments in greener initiatives generate positive financial returns for Chinese companies. These results are consistent with earlier studies (Nakamura, Citation2011; Singal, Citation2014; Su, Citation2019) but contradict the findings of Shabbir and Wisdom (Citation2020) and Lee et al. (Citation2015).

Table 4. Regression results based on LSDV.

To investigate the moderating impacts of China’s Environmental Protection Law 2015 (POLICY), regional development (RGDP), and polluting industries (ENVIND) on the association between CGI and ROA, we included interactions in Models 2–4. Model 2 demonstrates that CGI*POLICY has a significant positive effect on the relationship between CGI and ROA This suggests that environmental laws in China are not sufficiently strict to impede corporate profits while safeguarding the external environment. Similarly, we find a significantly positive moderating effect of CGI*RGDP on CGI-profitability association

The results reveal that regional development has a significant positive impact on the ERI–ROA relationship, which is in line with the findings of Wong et al. (Citation2018) and Gao et al. (Citation2019). However, regarding the effect of a firm’s affiliation with environmentally polluting sectors, we do not find any significant impact. Taken together, these findings suggest that environmentally sensitive industries are under tremendous regulatory pressure and that businesses must fulfil their environmental responsibilities to achieve credibility for the sake of legitimacy.

also presents the results of the control variables. ENVP shows a positive relationship with ROA, representing corporate environmental efforts that generate profits for Chinese corporations. Among the firm characteristics, FAR and SIZE show a positive relationship with ROA, while AGE and LEVG are negatively associated with firm profitability. Moreover, the corporate governance variables do not have any significant positive effect on ROA, except INSHR.

4.3. Robustness

To ensure the sensitivity of our findings, we used a second proxy of firm profitability (measured as return on equity (ROE)). We also reran all regressions of the main and moderating effects models. The results are shown in .

Table 5. Robust regression results based on LSDV.

As shown in , the main effect’s findings are similar to earlier findings, thus representing a significant positive relationship between firm profitability and CGI. As anticipated, the results relating to POLICY demonstrate that environmental regulation positively enhances CGI–profitability relationship. Similarly, results concerning the effect of regional development suggest that firms operating in developed areas of China generate positive financial returns from their greener efforts. Finally, our results demonstrate that firms in environmentally sensitive industries do not find it profitable to invest in green initiatives. In general, all the study’s results hold in . However, higher coefficients of CGI are found in all models, thus suggesting that ERI is more strongly associated with ROE than ROA. The results pertaining to the control variables remain the same across all models. Hence, our results remain robust to the use of another proxy for financial profitability in our analysis.

4.4. Endogeneity

Endogeneity can be induced by reverse causality, simultaneity, omitted variables, and company-specific heterogeneities (Semykina & Wooldridge, Citation2010). The endogeneity shown in our main findings () may be attributed to the reverse causality and omitted variable bias. As we propose that green investments produce positive corporate returns, it is also possible to theorize that profitable firms are more inclined toward environmental efforts, because they possess larger financial resources. Thus, endogeneity may affect the generalizability of the current study’s findings. We employed two-stage least squares (2SLS) with an instrumental variable approach (Baum et al., Citation2007) to resolve the problem of endogeneity in our study, which may be due to the reverse causation and omitted variables. Previous studies have identified ENVP as the endogenous variable and the ‘industry mean of ENVP’ as the instrumental variable (Al-Hadi et al., Citation2019; Shahab et al., Citation2018). It has been argued that the level of a firm’s social and environmental performance differs across industries due to variations in product nature, monitoring, and social standards (Mammilla & Siegel, Citation2001).

presents the results of the analysis that used 2SLS as a technique to control for endogeneity. We found that no results are dissimilar to the study’s main findings (). In particular, the empirical results indicate that green investments yield positive returns for Chinese listed companies. Moreover, this relationship is reinforced by the implementation of China’s Environmental Protection Law 2015, and firms from developed Chinese provinces and less polluted industrial sectors do generate profits from their greener efforts.

Table 6. Regression results based on 2sls.

presents the results of the tests depicting the attributes of the instrument variable used in the analysis. To demonstrate a powerful instrument, the ‘Kleibergen–Paap rk LM statistic’ should be significant, and the value of the ‘Cragg–Donald Wald F statistic’ should be larger than 10. Under the ‘Stock-Yogo weak ID test critical values’, the ‘Kleibergen-Paap rk Wald F statistic’ should be greater than the 10% maximum IV size for weak identification tests. All endogeneity tests that we applied fulfilled the criteria and confirmed that the instrument used was strong enough to control for reverse causality and omitted variable bias. Overall, these findings indicate that the problem of endogeneity is effectively addressed by the present study’s analysis.

5. Discussion and conclusions

CGI has emerged as a significant challenge to the economy and efforts to achieve sustainable development. However, the impact of CGI on firm profitability remains unclear due to the positive externalities of investment in environmental protection initiatives and the public goods features of environmental governance (Chen & Ma, 2021). To open up the black box of companies’ CGI, the current study employed a novel panel dataset of Chinese listed companies for the period 2010–2019 to investigate the effect of ERI on firm profitability. Our findings demonstrate that CGI promotes firms’ profitability. Furthermore, the results of the cross-sectional variations present the significance of environmental policy for improving the CGI–profitability relationship. This indicates that on the regulatory level, China’s environmental laws are not negatively strict in terms of limiting firms’ profits while addressing environmental concerns.

In addition, regional development also contributes to corporate environmental investment behaviors and facilitates profitability. The results further reveal that regional development has a significant positive impact on the relationship between green investment and firm profitability. These findings are in line with the proposition of Wong et al. (Citation2018) regarding the general impact of regional development on firm outcomes. However, the CGI–profitability association does not prevail for firms that operate within environmentally sensitive industrial sectors. This finding confirms the earlier finding of Gao et al. (Citation2019) in the field of CGI: environmentally sensitive industries are under tremendous regulatory pressure and are required to fulfil their environmental responsibilities to achieve credibility for the sake of legitimacy. Therefore, their profitability is not impacted by CGI.

5.1. Policy implications

The policy implications of the empirical findings are as follows. First, the study considers the earlier suggestion of Lee et al. (Citation2015) to craft strategies that help improve firms’ environmental measures with less negative economic impact. This study reveals that the implementation of China’s Environmental Protection Law 2015 has not hampered corporate economic returns, except for environmentally polluting firms. These findings imply that the government should carefully manage and increase charges and penalties for all enterprises, in general, and for environmentally sensitive firms, in particular. These should be designed in such a way that the positive track of the environmental regulations’ effects on corporate profitability is maintained. Second, the cross-regional differences in economic development in China lead to inconsistent institutional growth (Gao et al., Citation2019). It is inevitable for ‘greener and cleaner’ China that the central government ensures balanced regional GDP growth. Focusing on the underdeveloped regions, the Chinese government should provide resources and ensure the implementation of environmental regulations in such localities (Campbell, Citation2007). Given that underdeveloped regions are already combating other economic challenges, these regions usually sacrifice their resources and environmental status in favor of economic development. Furthermore, such regions are unable to create a corporate-friendly environment in which firms can effectively execute their green strategies to obtain a competitive advantage. Therefore, institutional incentives should be employed to encourage local governments in China to promote firms’ active green governance in an endogenous manner (Wong et al., Citation2018).

5.2. Managerial implications

To address the environmental challenges, firms must invest their financial and non-financial resources. Firms that are proactive in addressing environmental concerns frequently encounter budget restrictions; nevertheless, this presents opportunities that – if managed effectively – can contribute to greater financial performance. As this study has demonstrated, green investment enhances firm profitability. The actual advantages of investing in greener initiatives may not be evident, because managers lack the tools to assess outcomes and frequently overlook valuable business possibilities due to a lack of information. The availability of a realistic instrument to assess the costs and advantages of environmental-financial performance can assist managerial executives in developing strategies and making long-term sustainable financial decisions (Lee et al., Citation2015). At the same time, managers from environmentally polluting firms should redesign their green strategy. In particular, by using Porter’s framework, firms should transform their reactive strategies into proactive environmental decision making. Ultimately, the successful transformation of green strategies will enable firms to obtain a competitive advantage.

The regions across China differ in terms of institutional contexts, business norms, regulatory frameworks, and stakeholders. Managers should be cognizant of variations in local institutional contexts, because obtaining resources and assistance from local authorities is a strategic task, particularly in developing regions. Thus, to ensure an effective green strategy, managers must fully examine the local institutional context as well as the local government’s intentions with respect to green governance.

5.3. Limitations and future research

Apart from contributing to the extant literature, the present study has some limitations and suggestions for future research. First, given that we employed CGI as an element of corporate green management performance, future studies should consider multiple green management dimensions and compare their effects on firm profitability. Second, the study was conducted in an emerging market context; other researchers may conduct similar investigations in developed countries that have different institutional and business environments. Third, future investigations may identify other contingency factors affecting the CGI–profitability relationship. In particular, it would be useful to perform an industry-by-industry study to determine how different sectors’ demands and resources may be combined to derive financial benefits from green management.

Disclosure statement

No potential conflict of interest was reported by the authors.

References

- Al-Hadi, A., Chatterjee, B., Yaftian, A., Taylor, G., & Monzur Hasan, M. (2019). Corporate social responsibility performance, financial distress and firm life cycle: Evidence from Australia. Accounting & Finance, 59(2), 961–989.

- Albareda, L., Lozano, J. M., & Ysa, T. (2007). Public policies on corporate social responsibility: The role of governments in Europe. Journal of Business Ethics, 74(4), 391–407. https://doi.org/10.1007/s10551-007-9514-1

- Apospori, E. (2018). Regional CSR policies and SMEs’ CSR actions: Mind the gap – The case of the tourism SMEs in Crete. Sustainability, 10(7), 2197. https://doi.org/10.3390/su10072197

- Bansal, P., & Roth, K. (2000). Why companies go green: A model of ecological responsiveness. Academy of Management Journal, 43(4), 717–736.

- Baum, C. F., Schaffer, M. E., & Stillman, S. (2007). Enhanced routines for instrumental variables/generalized method of moments estimation and testing. The Stata Journal: Promoting Communications on Statistics and Stata, 7(4), 465–506. https://doi.org/10.1177/1536867X0800700402

- Boakye, D. J., Tingbani, I., Ahinful, G. S., & Nsor-Ambala, R. (2021). The relationship between environmental management performance and financial performance of firms listed in the Alternative Investment Market (AIM) in the UK. Journal of Cleaner Production, 278, 124034. https://doi.org/10.1016/j.jclepro.2020.124034

- Campbell, J. L. (2007). Why would corporations behave in socially responsible ways? An institutional theory of corporate social responsibility. Academy of Management Review, 32(3), 946–967. https://doi.org/10.5465/amr.2007.25275684

- Chen, Y., & Feng, J. (2019). Do corporate green investments improve environmental performance? Evidence from the perspective of efficiency. China Journal of Accounting Studies, 7(1), 62–92. https://doi.org/10.1080/21697213.2019.1625578

- Chen, Y., & Ma, Y. (2021). Does green investment improve energy firm performance? Energy Policy, 153, 112252. https://doi.org/10.1016/j.enpol.2021.112252

- Chiu, S.-C., & Sharfman, M. (2011). Legitimacy, visibility, and the antecedents of corporate social performance: An investigation of the instrumental perspective. Journal of Management, 37(6), 1558–1585. https://doi.org/10.1177/0149206309347958

- Clarkson, P. M., Li, Y., Richardson, G. D., & Vasvari, F. P. (2008). Revisiting the relation between environmental performance and environmental disclosure: An empirical analysis. Accounting, Organizations and Society, 33(4-5), 303–327. https://doi.org/10.1016/j.aos.2007.05.003

- Clarkson, P. M., Li, Y., Richardson, G. D., & Vasvari, F. P. (2011). Does it really pay to be green? Determinants and consequences of proactive environmental strategies. Journal of Accounting and Public Policy, 30(2), 122–144. https://doi.org/10.1016/j.jaccpubpol.2010.09.013

- Cormier, D., Magnan, M., & Van Velthoven, B. (2005). Environmental disclosure quality in large German companies: Economic incentives, public pressures or institutional conditions? European Accounting Review, 14(1), 3–39. https://doi.org/10.1080/0963818042000339617

- Damert, M., Paul, A., & Baumgartner, R. J. (2017). Exploring the determinants and long-term performance outcomes of corporate carbon strategies. Journal of Cleaner Production, 160, 123–138. https://doi.org/10.1016/j.jclepro.2017.03.206

- de Souza Cunha, F. A. F., & Samanez, C. P. (2013). Performance analysis of sustainable investments in the Brazilian stock market: A study about the corporate sustainability index (ISE). Journal of Business Ethics, 117(1), 19–36. https://doi.org/10.1007/s10551-012-1484-2

- Dimaggio, P. (1983). State expansions and organizational fields. In R. E. Hall & R. H. Quinn (Eds.), Organizational theory and public policy, 147–161. Beverly Hills: Sage.

- Dimaggio, P., & Powell, W. W. (2013). The economics of social institutions: Institutional isomorphism and collective rationality in organizational fields. In J. Davis & A. Christoforou (Eds.), The Economics of social institutions. Edward Elgar Publishers.

- Ferrat, Y., Daty, F., & Burlacu, R. (2022). Short-and long-term effects of responsible investment growth on equity returns. The Journal of Risk Finance, 23(1), 1–13. https://doi.org/10.1108/JRF-07-2021-0107

- Fini, R., & Toschi, L. (2016). Academic logic and corporate entrepreneurial intentions: A study of the interaction between cognitive and institutional factors in new firms. International Small Business Journal: Researching Entrepreneurship, 34(5), 637–659. https://doi.org/10.1177/0266242615575760

- Frondel, M., Horbach, J., & Rennings, K. (2008). What triggers environmental management and innovation? Empirical evidence for Germany. Ecological Economics, 66(1), 153–160. https://doi.org/10.1016/j.ecolecon.2007.08.016

- Gangi, F., Daniele, L. M., & Varrone, N. (2020). How do corporate environmental policy and corporate reputation affect risk‐adjusted financial performance? Business Strategy and the Environment, 29(5), 1975–1991. https://doi.org/10.1002/bse.2482

- Gao, Y., Yang, H., & Hafsi, T. (2019). Corporate giving and corporate financial performance: The S-curve relationship. Asia Pacific Journal of Management, 36(3), 687–713. https://doi.org/10.1007/s10490-019-09668-y

- Grewal, R., & Dharwadkar, R. (2002). The role of the institutional environment in marketing channels. Journal of Marketing, 66(3), 82–97. https://doi.org/10.1509/jmkg.66.3.82.18504

- Hang, M., Geyer‐Klingeberg, J., & Rathgeber, A. W. (2019). It is merely a matter of time: A meta‐analysis of the causality between environmental performance and financial performance. Business Strategy and the Environment, 28(2), 257–273. https://doi.org/10.1002/bse.2215

- Hatakeda, T., Kokubu, K., Kajiwara, T., & Nishitani, K. (2012). Factors influencing corporate environmental protection activities for greenhouse gas emission reductions: The relationship between environmental and financial performance. Environmental and Resource Economics, 53(4), 455–481. https://doi.org/10.1007/s10640-012-9571-5

- Horváthová, E. (2010). Does environmental performance affect financial performance? A meta-analysis. Ecological Economics, 70(1), 52–59. https://doi.org/10.1016/j.ecolecon.2010.04.004

- Hu, W., & Wang, D. (2020). How does environmental regulation influence China’s carbon productivity? An empirical analysis based on the spatial spillover effect. Journal of Cleaner Production, 257, 120484. https://doi.org/10.1016/j.jclepro.2020.120484

- Huang, L., & Lei, Z. (2021). How environmental regulation affect corporate green investment: Evidence from China. Journal of Cleaner Production, 279, 123560. https://doi.org/10.1016/j.jclepro.2020.123560

- Huang, Y., & Sternquist, B. (2007). Retailers’ foreign market entry decisions: An institutional perspective. International Business Review, 16(5), 613–629. https://doi.org/10.1016/j.ibusrev.2007.06.005

- Ielasi, F., Rossolini, M., & Limberti, S. (2018). Sustainability-themed mutual funds: An empirical examination of risk and performance. The Journal of Risk Finance, 19(3), 247–261. https://doi.org/10.1108/JRF-12-2016-0159

- Jackson, G., & Apostolakou, A. (2010). Corporate social responsibility in Western Europe: An institutional mirror or substitute? Journal of Business Ethics, 94(3), 371–394. https://doi.org/10.1007/s10551-009-0269-8

- Jenkins, H., & Yakovleva, N. (2006). Corporate social responsibility in the mining industry: Exploring trends in social and environmental disclosure. Journal of Cleaner Production, 14(3-4), 271–284. https://doi.org/10.1016/j.jclepro.2004.10.004

- Jin-Fang, T., Chao, P., Rui, X., Xiao-Tong, Y., Chen, W., Xu-Zhao, J., & Yu-Li, S. (2020). Corporate innovation and environmental investment: The moderating role of institutional environment. Advances in Climate Change Research, 11, 85–91.

- Jingyan, F., & Lisha, L. (2010). A case study on the environmental regulation, the factor endowment and the international competitiveness in industries. Management World, 10, 87–98.

- Kolk, A., & Levy, D. (2001). Winds of change: Corporate strategy, climate change and oil multinationals. European Management Journal, 19(5), 501–509. https://doi.org/10.1016/S0263-2373(01)00064-0

- Lee, K.-H., Min, B., & Yook, K.-H. (2015). The impacts of carbon (CO2) emissions and environmental research and development (R&D) investment on firm performance. International Journal of Production Economics, 167, 1–11. https://doi.org/10.1016/j.ijpe.2015.05.018

- Lee, S. (2012). Corporate carbon strategies in responding to climate change. Business Strategy and the Environment, 21(1), 33–48. https://doi.org/10.1002/bse.711

- Leiter, A. M., Parolini, A., & Winner, H. (2011). Environmental regulation and investment: Evidence from European industry data. Ecological Economics, 70(4), 759–770. https://doi.org/10.1016/j.ecolecon.2010.11.013

- Li, D., Cao, C., Zhang, L., Chen, X., Ren, S., & Zhao, Y. (2017). Effects of corporate environmental responsibility on financial performance: The moderating role of government regulation and organizational slack. Journal of Cleaner Production, 166, 1323–1334. https://doi.org/10.1016/j.jclepro.2017.08.129

- Li, D., Huang, M., Ren, S., Chen, X., & Ning, L. (2018). Environmental legitimacy, green innovation, and corporate carbon disclosure: Evidence from CDP China 100. Journal of Business Ethics, 150(4), 1089–1104. https://doi.org/10.1007/s10551-016-3187-6

- Li, Z., Liao, G., & Albitar, K. (2020). Does corporate environmental responsibility engagement affect firm value? The mediating role of corporate innovation. Business Strategy and the Environment, 29(3), 1045–1055. https://doi.org/10.1002/bse.2416

- Lobato, M., Rodríguez, J., & Romero, H. (2021). A volatility-match approach to measure performance: The case of socially responsible exchange traded funds (ETFs). The Journal of Risk Finance, 22(1), 34–43. https://doi.org/10.1108/JRF-04-2020-0066

- Lundgren, T., & Zhou, W. (2017). Firm performance and the role of environmental management. Journal of Environmental Management, 203(Pt 1), 330–341.

- Madsen, P. M. (2009). Does corporate investment drive a “race to the bottom” in environmental protection? A reexamination of the effect of environmental regulation on investment. Academy of Management Journal, 52(6), 1297–1318. https://doi.org/10.5465/amj.2009.47085173

- Mammilla & Siegel, D. (2001). Corporate social responsibility: A theory of firm perspective. Academy of Management Review, 26(1), 117–127.

- Marquis, C., Glynn, M. A., & Davis, G. F. (2007). Community isomorphism and corporate social action. Academy of Management Review, 32(3), 925–945. https://doi.org/10.5465/amr.2007.25275683

- Matten, D., & Moon, J. (2008). “Implicit” and “explicit” CSR: A conceptual framework for a comparative understanding of corporate social responsibility. Academy of Management Review, 33(2), 404–424. https://doi.org/10.5465/amr.2008.31193458

- Merendino, A., & Melville, R. (2019). The board of directors and firm performance: Empirical evidence from listed companies. Corporate Governance: The International Journal of Business in Society, 19(3), 508–551. https://doi.org/10.1108/CG-06-2018-0211

- Mirza, N., Naqvi, B., Rahat, B., & Rizvi, S. K. A. (2020). Price reaction, volatility timing and funds’ performance during Covid-19. Finance Research Letters, 36, 101657.

- Mirza, N., Rizvi, S. K. A., Saba, I., Naqvi, B., & Yarovaya, L. (2022). The resilience of Islamic equity funds during COVID-19: Evidence from risk adjusted performance, investment styles and volatility timing. International Review of Economics & Finance, 77, 276–295. https://doi.org/10.1016/j.iref.2021.09.019

- Molina‐Azorín, J. F., Claver‐Cortés, E., López‐Gamero, M. D., & Tarí, J. J. (2009). Green management and financial performance: A literature review. Management Decision, 47(7), 1080–1100. https://doi.org/10.1108/00251740910978313

- Nakamura, E. (2011). Does environmental investment really contribute to firm performance? An empirical analysis using Japanese firms. Eurasian Business Review, 1(2), 91–111.

- Naveed, K., Voinea, C. L., Ali, Z., Rauf, F., & Fratostiteanu, C. (2021). Board gender diversity and corporate social performance in different industry groups: Evidence from China. Sustainability, 13(6), 3142. https://doi.org/10.3390/su13063142

- Ness, K. E., & Mirza, A. M. (1991). Corporate social disclosure: A note on a test of agency theory. The British Accounting Review, 23(3), 211–217. https://doi.org/10.1016/0890-8389(91)90081-C

- Orsato, R. J. (2006). Competitive environmental strategies: When does it pay to be green? California Management Review, 48(2), 127–143. https://doi.org/10.2307/41166341

- Pekovic, S., Grolleau, G., & Mzoughi, N. (2018). Environmental investments: Too much of a good thing? International Journal of Production Economics, 197, 297–302. https://doi.org/10.1016/j.ijpe.2018.01.012

- Porter, M. E., & Van Der Linde, C. (1995). Green and competitive: Ending the stalemate. Harvard Business Review, Septembre-Octobre.

- Qian, G., Khoury, T. A., Peng, M. W., & Qian, Z. (2010). The performance implications of intra‐and inter‐regional geographic diversification. Strategic Management Journal, 31(9), 1018–1030.

- Radu, C., Caron, M.-A., & Arroyo, P. (2020). Integration of carbon and environmental strategies within corporate disclosures. Journal of Cleaner Production, 244, 118681. https://doi.org/10.1016/j.jclepro.2019.118681

- Rashid, A. (2018). Board independence and firm performance: Evidence from Bangladesh. Future Business Journal, 4(1), 34–49. https://doi.org/10.1016/j.fbj.2017.11.003

- Rashid, M. M. (2020). Ownership structure and firm performance: The mediating role of board characteristics. Corporate Governance: The International Journal of Business in Society, 20(4), 719–737. https://doi.org/10.1108/CG-02-2019-0056

- Reid, E. M., & Toffel, M. W. (2009). Responding to public and private politics: Corporate disclosure of climate change strategies. Strategic Management Journal, 30(11), 1157–1178. https://doi.org/10.1002/smj.796

- Ren, S., Hu, Y., Zheng, J., & Wang, Y. (2020). Emissions trading and firm innovation: Evidence from a natural experiment in China. Technological Forecasting and Social Change, 155, 119989. https://doi.org/10.1016/j.techfore.2020.119989

- Reverte, C. (2009). Determinants of corporate social responsibility disclosure ratings by Spanish listed firms. Journal of Business Ethics, 88(2), 351–366. https://doi.org/10.1007/s10551-008-9968-9

- Rizvi, S. K. A., Mirza, N., Naqvi, B., & Rahat, B. (2020). Covid-19 and asset management in EU: A preliminary assessment of performance and investment styles. Journal of Asset Management, 21(4), 281–291. https://doi.org/10.1057/s41260-020-00172-3

- Semykina, A., & Wooldridge, J. M. (2010). Estimating panel data models in the presence of endogeneity and selection. Journal of Econometrics, 157(2), 375–380. https://doi.org/10.1016/j.jeconom.2010.03.039

- Shabbir, M. S., & Wisdom, O. (2020). The relationship between corporate social responsibility, environmental investments and financial performance: Evidence from manufacturing companies. Environmental Science and Pollution Research, 27(32), 1–12.

- Shahab, Y., Ntim, C. G., Chengang, Y., Ullah, F., & Fosu, S. (2018). Environmental policy, environmental performance, and financial distress in China: Do top management team characteristics matter? Business Strategy and the Environment, 27(8), 1635–1652. https://doi.org/10.1002/bse.2229

- Shen, Y., Su, Z.-W., Huang, G., Khalid, F., Farooq, M. B., & Akram, R. (2020). Firm market value relevance of carbon reduction targets, external carbon assurance and carbon communication. Carbon Management, 11(6), 549–563. https://doi.org/10.1080/17583004.2020.1833370

- Singal, M. (2014). The link between firm financial performance and investment in sustainability initiatives. Cornell Hospitality Quarterly, 55(1), 19–30. https://doi.org/10.1177/1938965513505700

- Situ, H., & Tilt, C. (2018). Mandatory? Voluntary? A discussion of corporate environmental disclosure requirements in China. Social and Environmental Accountability Journal, 38(2), 131–144. https://doi.org/10.1080/0969160X.2018.1469423

- Stevanović, S., Jovanović, O., & Hanić, A. (2019). Environmental and financial performance: Review of selected studies. Economic Analysis, 52(2), 113–127.

- Su, X. (2019). Can green investment win the favor of investors in China? Evidence from the return performance of green investment stocks. Emerging Markets Finance and Trade, 57(11), 1–19.

- Sueyoshi, T., & Goto, M. (2009). Can environmental investment and expenditure enhance financial performance of US electric utility firms under the clean air act amendment of 1990? Energy Policy, 37(11), 4819–4826. https://doi.org/10.1016/j.enpol.2009.06.038

- Todaro, N. M., Testa, F., Daddi, T., & Iraldo, F. (2021). The influence of managers’ awareness of climate change, perceived climate risk exposure and risk tolerance on the adoption of corporate responses to climate change. Business Strategy and the Environment, 30(2), 1232–1248. https://doi.org/10.1002/bse.2681

- Trumpp, C., & Guenther, T. (2017). Too little or too much? Exploring U‐shaped relationships between corporate environmental performance and corporate financial performance. Business Strategy and the Environment, 26(1), 49–68. https://doi.org/10.1002/bse.1900

- Wagner, M. (2010). The role of corporate sustainability performance for economic performance: A firm-level analysis of moderation effects. Ecological Economics, 69(7), 1553–1560. https://doi.org/10.1016/j.ecolecon.2010.02.017

- Wang, H., Choi, J., & Li, J. (2008). Too little or too much? Untangling the relationship between corporate philanthropy and firm financial performance. Organization Science, 19(1), 143–159. https://doi.org/10.1287/orsc.1070.0271

- Wei, F., Ding, B., & Kong, Y. (2017). Female directors and corporate social responsibility: Evidence from the environmental investment of Chinese listed companies. Sustainability, 9(12), 2292. https://doi.org/10.3390/su9122292

- Weinhofer, G., & Hoffmann, V. H. (2010). Mitigating climate change–how do corporate strategies differ? Business Strategy and the Environment, 19(2), 77–89.

- Wong, C. W. Y., Miao, X., Cui, S., & Tang, Y. (2018). Impact of corporate environmental responsibility on operating income: Moderating role of regional disparities in China. Journal of Business Ethics, 149(2), 363–382. https://doi.org/10.1007/s10551-016-3092-z

- Xu, X., & Yan, Y. (2020). Effect of political connection on corporate environmental investment: Evidence from Chinese private firms. Applied Economics Letters, 27(18), 1515–1521. https://doi.org/10.1080/13504851.2019.1693692

- Yang, X., Wang, Y., Hu, D., & Gao, Y. (2018). How industry peers improve your sustainable development? The role of listed firms in environmental strategies. Business Strategy and the Environment, 27(8), 1313–1333. https://doi.org/10.1002/bse.2181

- Yarovaya, L., Mirza, N., Abaidi, J., & Hasnaoui, A. (2021). Human capital efficiency and equity funds’ performance during the COVID-19 pandemic. International Review of Economics & Finance, 71, 584–591. https://doi.org/10.1016/j.iref.2020.09.017

- You, D., Zhang, Y., & Yuan, B. (2019). Environmental regulation and firm eco-innovation: Evidence of moderating effects of fiscal decentralization and political competition from listed Chinese industrial companies. Journal of Cleaner Production, 207, 1072–1083. https://doi.org/10.1016/j.jclepro.2018.10.106

- Yu, Y., & Choi, Y. (2015). Measuring environmental performance under regional heterogeneity in China: A metafrontier efficiency analysis. Computational Economics, 46(3), 375–388. https://doi.org/10.1007/s10614-014-9464-5

- Zeng, C., Zhang, L., & Li, J. (2020). The impact of top management’s environmental responsibility audit on corporate environmental investment: Evidence from China. Sustainability Accounting, Management and Policy Journal, 11(7), 1271–1291. https://doi.org/10.1108/SAMPJ-09-2018-0263

- Zhang, J., & Shuang, Z. I. (2021). Socially responsible investment and firm value: The role of institutions. Finance Research Letters, 41, 101806. https://doi.org/10.1016/j.frl.2020.101806

- Zhang, Y., Wei, J., Zhu, Y., & George-Ufot, G. (2020). Untangling the relationship between corporate environmental performance and corporate financial performance: The double-edged moderating effects of environmental uncertainty. Journal of Cleaner Production, 263, 121584. https://doi.org/10.1016/j.jclepro.2020.121584