Abstract

Accounting ethics emerged as a significant socio-economic issue due to the recent frauds that eroded the public trust in financial statements and in accountants who prepare them. Therefore, ethical behaviour in business must be indorsed. This article examines the effect of affective professional commitment of accountants on their perception of importance of accounting ethics principles application with the mediation of the Code of Ethics for Professional Accountants by ISEBA. As in other vocations, some professional accountants have an innate sense of morality but the others should be advised to consult the Code of Ethics. This explains the direct and indirect (with the Code of Ethics as the mediator) relationship between affective professional commitment and the accounting ethics principles application. According to our findings, accountants with higher levels of affective professional commitment are more likely to perceive the importance of accounting ethics principles. Application of the five fundamental accounting ethics principles (integrity, objectivity, professional competence and due care, confidentiality and professional behaviour) should be promoted while consulting the Code of Ethics should be supported in order to decrease unethical behaviour of the professional accountants.

Subject classification codes:

1. Introduction

1.1. Objective

Human behaviour is based on moral intuition. Distinguishing right from wrong and understanding why something is right or wrong is the root of ethical judgement. As Smith et al. (Citation2009) acknowledged, ‘Ethics provides the boundaries by which people relate to the world, including how they do business, treat other people and care for the environment’. According to Pusti (Citation2017) ethics, as a normative science, scrutinizes the values and beliefs as the guides for people’s actions. Virtues represent socially appropriate traits and values like honesty, compassion, generosity and responsibility. These traits and values become normally deep-seated through deliberate and repetitive practice, and therefore are the predispositions for ethical behaviour (Arthur et al., Citation2021). Conversely, unethical behaviour is perceived as harmful to others and morally unacceptable to a wider community or even illegal (Biong et al., Citation2010). Arthur et al. (Citation2021) argued that contemporary organisations that are more focused on specific goals (like greater profit margin) tend to overlook the dimensions of character of the employees. Deterioration of business ethics is noted in many studies (e.g. Carmeli & Sheaffer, Citation2009; Higgs-Kleyn & Kapelianis, Citation1999; Huehn, Citation2008; Valentine & Fleischman, Citation2008). Relativizing ethical issues and trivialization of unethical behaviour became usual in business practice. Armstrong et al. (Citation2004, p. 366) defined banality of wrongdoing as ‘the ever-present environment within an organization that is not ethical or moral’. Their research confirmed that a banal wrongdoing environment is related to increased ethical violations or unethical practices. Recent studies widely explored the impact of ethical climate (e.g. Elçi & Alpkan, Citation2009; McManus & Subramaniam, Citation2014; Okpara & Wynn, Citation2008; Shafer, Citation2009; Shafer et al., Citation2013). Erben and Güneşer (Citation2008) reported positive effect of ethical climate on organisational commitment. Domino et al. (Citation2015) revealed that ethical climate affects accountants’ ethical behaviour. Cullen et al. (Citation2003) pointed out the importance of ethical climate in organisations noting that ethical climate of benevolence has a positive relationship with organizational commitment while egoistic climate is negatively related to commitment. Chen et al. (Citation2019) referring to the social cognitive theory acknowledged that people are products of their environment but at the same time, they are also creators of that environment. Ethical behaviour (of management as well as employees) is important in boosting collective efficacy. Many scholars argued that the code of ethics should be applied to enhance ethical behaviour (Davidson & Stevens, Citation2013; Fu et al., Citation2011; Higgs-Kleyn & Kapelianis, Citation1999; Valentine et al., Citation2002).

Since the professional accountants had their fair share in the recent financial scandals (Alzola, Citation2017; Fassin & Drover, Citation2017; Lail et al., Citation2017; Payne et al., Citation2019) their professional ethics emerged as a wider social issue. Marques and Azevedo-Pereira (Citation2009) stated that accountants are highly exposed to ethical dilemmas. Therefore, professional accountants often face difficulties in their attempt to attain complete professional independence. Barrainkua and Espinosa-Pike (Citation2020) acknowledged that professionalism could be jeopardised when accountants work in bureaucratic contexts that emphasize profit at the expense of their professional values. Facing various ethical dilemmas in accounting practice could be influenced by professional commitment of accountants.

This article seeks to explore the relationship between professional commitment and ethical principles of accountants. Committed professionals are of great value to the society (Smith & Hall, Citation2008) especially if their line of work is directly related to the public interest. Employees with high professional commitment identify strongly with the professional goals and show strong willingness to sustain membership in the chosen profession. They are also willing to exert substantial effort in their profession (Singh & Gupta, Citation2015, p. 1195). According to Arthur et al. (Citation2021) judgements informed by good character are necessary for effective and purposeful professional practice because of their capacity to perceive wider good (and ability to detect the opposite). Thus, the aim of this article is to determine whether affective professional commitment affects perception of importance of accounting ethics principles. In addition, the mediating role of understanding the accounting ethics code is investigated in this context.

1.2. Professional commitment of accountants

Organisational commitment is widely explored theme while professional commitment is scarcely examined (Goulet & Singh, Citation2002; Singh & Gupta, Citation2015) particularly when the studies on accounting professional are concerned (Loscher et al., Citation2020). Loscher et al. (Citation2020) pointed out that organisational commitment is conceptually distinct from professional commitment because they are based on different values. Organisations impose managerial control over work promoting efficiency while profession gives emphasis to the role of autonomy and independence. Škare et al. (Citation2013) acknowledged that employee commitment is correlated to the perceived training effectiveness, job satisfaction and motivation, which consequently has an indirect impact on productivity. Professional commitment can be defined as psychological attachment to (also identification with) one’s profession (Bagraim, Citation2003; Hall et al., Citation2005; Smith & Hall, Citation2008). Meyer et al. (Citation1993) distinguished three components, also known as dimensions, of occupational (professional) commitment. Bagraim (Citation2003, p. 6) named these three components as affective professional commitment, continuance professional commitment and normative professional commitment. Affective professional commitment refers to the identification with one’s profession as well as involvement in, and emotional attachment to that profession. According to Hall et al. (Citation2005, p. 90) affective professional commitment is the extent to which an individual ‘wants to stay’ in the profession. Continuance professional commitment relates to the extent to which an employee ‘has to stay’ in the profession (Smith & Hall, Citation2008) because of the costs and losses associated with leaving the chosen profession (Bagraim, Citation2003). Employees with strong continuance professional commitment are reluctant to change profession since they have already invested much (e.g. to gain skills and knowledge). Normative professional commitment is grounded on a sense of obligation to the profession. People with strong normative professional commitment feel that they ‘ought to stay’ in their profession (Hall et al., Citation2005). All mentioned dimensions of professional commitment have implications on a decision whether to stay with or to leave the current profession.

Although there is limited number of studies on professional commitment of accountants, the majority of them were focused on the affective commitment (Hall et al., Citation2005). Given that most of studies used Professional Commitment Questionnaire, Smith and Hall (Citation2008) assessed that research instrument (its scale) and found very high positive correlation with affective professional commitment scale (when accountants are considered).

Employed persons dedicate much of their time to their chosen profession or line of work so their belief in what they do and their willingness to maintain the membership in that occupation might be of great importance to them. Understanding the psychological bond between accountants and accounting as their profession was in research focus of Loscher et al. (Citation2020) who found out that accountants are strongly committed towards their profession. Gendron et al. (Citation2009) documented that accountants show higher level of professional commitment comparing to their organisational commitment. Loscher et al. (Citation2020) identified six latent profiles based on organizational and professional commitment ranging from weakly committed to fully committed. They revealed that there are significant differences between the values of conscientiousness, confidentiality and own-responsibility, as well as efficiency in these six profiles. Smith and Hall (Citation2008, p. 87) proposed four factors affecting the development of accountants’ professional commitment: tertiary training, professional accounting qualifications, organisational culture and professional membership requirements and services. They concluded that profession has a strong effect on individual behaviour namely through the code of ethics, continual education and licensing. Caron and Fortin (Citation2014) noticed that accountants scored higher in professional commitment comparing to organisational commitment. Sejjaaka and Kaawaase (Citation2014) reported that professionalism and rewards are weak predictors of accountants’ organisational commitment. Shafer et al. (Citation2016) found a strong positive relationship between tax accountants’ belief in the importance of corporate ethics and social responsibility and their level of professional commitment. Barrainkua and Espinosa-Pike (Citation2020) acknowledged positive correlation between professional commitment of accountants and their perceived ethical environment and public interest. Ethics and professionalism of accountants play important role in building sound corporate governance (Bonaci et al., Citation2013, p. 31). To sum up, the latest studies, that are linking professional commitment and ethics of accountants, are noting that it is an important socioeconomic issue.

1.3. Accounting ethics code

Business ethics emerged as an important issue worldwide. A collective lack of application of ethical standards has led to countless conflicts, tensions and even scandals (Fassin & Drover, Citation2017). Accounting frauds have considerably damaged the functionality of the global economic system (Lail et al., Citation2017). Recent financial crisis demonstrated the failure of professional gatekeepers (e.g. accountants, auditors, corporate lawyers and securities analysts) to detect and disrupt corporate misconduct (Alzola, Citation2017). Therefore, the public trust and investor confidence in financial statements and audit reports have eroded (Cardona et al., Citation2020). A gradual deterioration of accountants’ ethics is the result of the social context that instigates growing greed over the professional objectivity (Gendron et al., Citation2006). Thus, the mechanisms that prevent unethical behaviour of the professional accountants should be applied (Maniora, Citation2017; Vladu et al., Citation2017). To mitigate ethical dilemmas and misconduct of accountants many scholars advised the application of the Code of Ethics for Professional Accountants published by the International Ethics Standard Board for Accountants (Clements et al., Citation2009; Ishaque, Citation2021; Nerandzic et al., Citation2012; Rogošić & Bakotić, Citation2019; Spalding & Oddo, Citation2011; Žager et al., Citation2019). This Code of Ethics, among other things, can serve to the professional accountants (auditors included) to confirm their public interest responsibility as well as their status (Nerandzic et al., Citation2012, p. 291). The Code of Ethics for Professional Accountants (IESBA, Citation2018) promotes five fundamental principles:

integrity (as an essence of trust, based on consistency, necessary in building effective and long-lasting business relationships),

objectivity (uncompromised professional or business judgments freed from bias, conflict of interest or inappropriate influence of others),

professional competence and due care (attaining and maintaining accounting skills and knowledge at the level necessary for delivering competent professional service based on relevant legislation and recent technical and professional standards while acting diligently and in accordance with applicable technical and professional standards),

confidentiality (being discreet when handling information learned from the professional and business relationships), and

professional behaviour (complying with relevant laws and regulations and avoiding any conduct that might discredit the profession).

The empirical research of Žager et al. (Citation2019) revealed that these ethical principles are perceived as an outcome of upbringing and family values but can also be taught. Accounting professionals can receive ethics related training from three different sources: tertiary education programs, the profession and the organizations they are employed (Higgs-Kleyn & Kapelianis, Citation1999). Due to the changes in social context that have eroded ethics of the professional accountants, many scholars argue that ethics education should be integrated in the accounting education curricula (e.g. Christensen et al., Citation2018; Dellaportas, Citation2006; Tweedie et al., Citation2013; Williams & Elson, Citation2010). The threats to compliance with the aforementioned core principles are also clarified in this Code of Ethics so they could be identified, evaluated and properly addressed (IESBA, Citation2018). To reduce the threats to an acceptable level, accountant should apply safeguards that are described in the Code of Ethics. Ishaque (Citation2021) noted that the Code of Ethics has the risk management framework and Velayutham (Citation2003) compared it with the quality assurance protocol. Although slightly criticised, the Code of Ethics is globally accepted and used as a framework for various national accounting ethics guides. Even the Code of Professional Conduct established by the American Institute of Certified Public Accountants (AICPA) has begun to promote ethical principles accordingly (Spalding & Lawrie, Citation2019). Smith et al. (Citation2009) explored the components of the accounting ethics codes in Canada, Egypt and Japan. They found strong similarities among the observed codes in these three countries especially when the key principles are considered. Bayou et al. (Citation2011, p. 120) noted that the US Institute of Management Accountants’ (IMA) promotes four standards of conduct: competence, confidentiality, integrity and credibility that are based on its fundamental ethical principles of honesty, fairness, objectivity and responsibility. Vladu et al. (Citation2017, p. 634) stated that truthfulness is essential in accounting ethics and stated that harsh penalties for violating the code of ethics should be promoted in order to decrease opportunistic behaviour. Previous studies supported application of accounting ethics code (Bonaci et al., Citation2013; Clements et al., Citation2009; Huterski et al., Citation2020; Ishaque, Citation2021; Nerandzic et al., Citation2012; Odar et al., Citation2017; Rogošić & Bakotić, Citation2019; Smith et al., Citation2009; Spalding & Oddo, Citation2011; Žager et al., Citation2019) because of the guidelines it provides and awareness it enhances leading to more appropriate professional conduct.

1.4. Hypotheses development

So far, accounting ethics has been explored from various aspects. Prior studies have revealed the relationship between accounting ethics and organisational commitment (e.g. Cullen et al., Citation2003; Cullinan et al., Citation2008). The relationship between professional commitment and ethics was rarely investigated (Elias, Citation2008) but the latest studies on accountants’ professional commitment have broaden the horizon and put it in a wider perspective. Jeffrey et al. (Citation1996) as well as Lord and DeZoort (Citation2001) studied auditors’ professional commitment and its effect on ethical reasoning. Clayton and van Staden (Citation2015) revealed that the high levels of organizational and/or professional commitment of professional accountants were found to mitigate inappropriate social influence pressure on ethical decision making. Research results of Shafer et al. (Citation2016, p. 125) indicated that higher levels of professional commitment are good predispositions of greater moral fortitude in remaining professional standards when tax accountants face a client pressure to commit unethical and fraudulent activities. Barrainkua and Espinosa-Pike (Citation2020, p. 669) pointed out that providing the fair presentation of financial statements could be accomplished if accountants believe that their role is to serve the public interest and meet society’s expectations. Those accountants might be more resistant to organisational pressures to disobey professional standards. Since good character makes good professional with developed technical competencies adjoined with excellence of character required for ethical and systematic deliberation (Arthur et al., Citation2021) it is reasonable to assume:

H1: Affective professional commitment of accountants is positively associated with their understanding of the Code of Ethics.

According to Alzola (Citation2017) there are four major reasons justifying gatekeeping duties that every accountant should be aware of. These arguments for gatekeeping duties are: non-complicity (i.e., accountants and auditors should avoid assisting and supporting corporate fraud), ability (i.e., professional accountants have the knowledge and skills to prevent misconduct), social efficiency (i.e., proper monitoring in accounting is the most efficient way to reduce deterrence costs) and contracts (i.e., professional accountants have contractual and fair play duties to protect the public interest). Alzola (Citation2017, p. 718) also acknowledged that ‘the contents and strength of gatekeeping duties depend on their moral justification’. A prior study (Greenfield et al., Citation2008) revealed that accountants and managers with higher levels of professional commitment seem less likely to engage in earnings management behaviour and less likely to behave opportunistically. Conversance with the Code of Ethics and understanding the effects of compliant professional behaviour of accountants might be crucial for their awareness how important is to apply accounting ethics principles in practice. As already stated, many authors promoted the application of accounting ethics code since it provides a sound framework for acceptable professional behaviour. Actually, the application of the Code of Ethics is the first step in implementation of compliance and ethics programme (Ishaque, Citation2021). Since awareness of accounting ethics issues can enable ethical professional conduct, the mediating role of conversance with the Code of Ethics could be crucial. Based on this discussion, we test the following two hypotheses:

H2: Better understanding of the Code of Ethics is positively associated to the perceived importance of application of accounting ethics principles.

H3: The Code of Ethics mediates the effect of affective professional commitment on the perceived importance of accounting ethics principles application.

2. Methods

The online questionnaire used as a research instrument was addressed to e-mails of 1228 professional accountants in business. To test our hypotheses, we drew on measures of affective professional commitment as an independent variable, understanding the Code of Ethics as a mediating variable and accounting ethics principles as the dependent variable. Responses for all the items () were made on a five-point Likert scale (1 = “I strongly disagree”, 5 = “I strongly agree”). We measured affective professional commitment using the questionnaire of Meyer et al. (Citation1993), which was also deployed in recent studies (e.g., Gendron et al., Citation2009; Shafer et al., Citation2016; Smith & Hall, Citation2008). We measured the Code of Ethics for Professional Accountants' conversance and its effects to estimate accountants' understanding of its practical implications. Six items that measure the perceived importance of applying accounting ethics principles are formulated from the definitions of those fundamental principles: integrity, objectivity, professional competence and due care (observed separately in this study), confidentiality and professional behaviour. Variables and their constructs (items) are listed in .

Table 1. A list of items and their abbreviations used in the model.

Covariance-based structural equation modelling (SEM) through AMOS 23.0 was applied to test the hypotheses. This multivariate statistical technique allows simultaneous analysis of the entire system of variables to determine the extent to which it is consistent with the data (Tabachnick & Fidell, Citation2013). It is used to analyse structural relationships, so it was suitable for modelling the relationship between the variables of affective professional commitment, the Code of Ethics, and the accounting ethics principles and simultaneously analysing the interactions between them. SEM analysis followed the two-step approach: testing of a measurement model and structural model. First, the measurement model determined the structure's unidimensionality, reliability and validity. After assessing the measurement model, the structural model was utilized to analyse the hypothetical relationships between latent variables. The total number of responses analysed was 322, with 21.1% males and 78.9% female respondents. Over 90% of respondents are older than 30 years, and 51.55% of them have more than 10 years of experience in the organization in which they currently work.

3. Results

3.1. Exploratory factor analyses

Exploratory factor analysis (EFA) was performed to identify the structure of the factors. The Kaiser–Meyer–Olkin measure confirmed the adequacy of sampling for analysis, KMO = 0.890. The Bartlett Test of Sphericity resulted in an approximated chi-square of 4538.04 with 171 degrees of freedom (p < .001). These results indicate that the data used in this study were appropriate for EFA.

Principal component analysis with varimax rotation was performed with the 19 items to identify the underlying dimensions of the constructs. Factor analysis produced three – a factors solution with eigenvalues greater than 1.0 and suppressing all factor coefficients less than 0.5. Accordingly, one item (CE1) was removed from the analysis because of its weak (0.299), non-clean loading and low communalities. Hair et al. (Citation2009) suggested that the value of communalities below 0.5 should be removed. Consequently, two items (AEP5 and PC1) were dropped, continuing the analysis with 16 items. shows the most interpretable form of the factor analysis that was performed with the remaining 16 items and three factors that explained 74.92% of the total variance.

Table 2. Rotated factor loadings.

The appropriateness of the instrument reliability was tested before the measurement model. Using Cronbach's alpha coefficient, reliability analysis was run on each scale. The Cronbach’s alphas for the 16-item three-factors in the present study were 0.832 for accounting ethics principles (AEP), 0.947 for code of ethics (CE) and 0.946 for affective professional commitment (PC), and 0.881 for the total scale. Reliability analysis showed that all variables have adequate Cronbach's alpha coefficient.

3.2. Measurement model

The confirmatory factor analysis (CFA) was performed for the measurement model following EFA to determine whether the hypothesized measurement model fitted the data set. As recommended by Jackson et al. (Citation2009), we examined the assessment of univariate and multivariate normality before CFA. The univariate normality was examined by conducting normality tests using Kolmogorov–Smirnov and Shapiro–Wilk significance tests through SPSS Statistics 23 software. The multivariate normality was tested using AMOS Graphic 23.0 software by calculating Mardia's coefficient. The results showed that data violated the univariate and multivariate normality assumptions. Whereas maximum likelihood estimation (MLE) rests on the assumption of multivariate normality, researchers are commonly faced with samples clearly from non-normal populations (Micceri, Citation1989). The bootstrapping approach has received growing attention recently since researchers began to encounter violations of the assumption of normality (Cheung & Lau, Citation2008). Accordingly, a bootstrap approach was applied in this study.

One method for managing nonnormality in SEM uses the Bollen–Stine p-value to assess the overall model fit. When estimating standard errors using the bootstrap, the resampling scheme for the bootstrap does not depend on any assumption regarding the distributional form of the population (Nevitt & Hancock, Citation2001). A Bollen–Stine was run on 2000 bootstrap samples, and AMOS detected that the Bollen–Stine bootstrap p-value was .081. Using a conventional significance level of .05, we conclude that the model fits the data well.

An assessment of the assumed model shows a Chi-square of 147.970 with df 98. Unidimensionality, validity and reliability assessment of a latent construct assessment was done. CFA showed that the unidimensionality requirement is achieved, and all items have acceptable factor loadings for the particular latent construct. Additionally, composite reliability (CR), average variance extracted (AVE) and Cronbach's alpha values () indicate the presence of convergent validity and reliability.

Table 3. Convergent validity and reliability measurements for variables.

Criteria for construct validity and the overall model fit were examined. A Chi-square p-value was .001, and it should be nonsignificant to indicate the fit model. However, Chi-square is sensitive to sample size and violation of multivariate normality, so Chi-square goodness of fit should not be the only method used to conclude data-model fit (Bollen & Long, Citation1993). Therefore, we consider a variety of fit indicators. The goodness-of-fit indices of the 16-item model were adequate and reflected a good fit ().

Table 4. Overall model fit summary.

The measurement model yielded highly acceptable indices in all respects. Therefore, the goodness-of-fit indicators support the three factors 16-item hypothesized measurement model.

The requirement for discriminant validity was also assessed, and not too high correlations among latent variables suggested the presence of discriminant validity. The discriminant validity index summary () showed a diagonal value (square root of AVE) is higher than the values in its row and column (correlation between latent variables) and the discriminant validity for all three constructs was achieved.

Table 5. Discriminant validity analysis for variables.

After analysing the measurement model, it was concluded that the assumptions of one-dimensionality, validity and reliability were met and that the model fits the data well. According to these results, there was sufficient evidence to proceed with the investigation of the hypothetical dependencies based on path analysis in the structural model.

3.3. Structural equation modelling

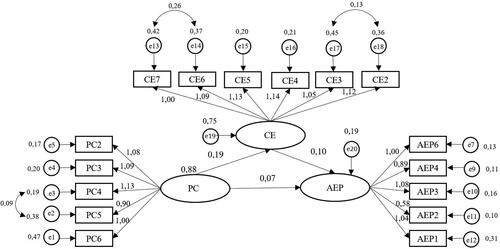

The proposed hypotheses of the research were tested through covariance-based structural equation modelling (using AMOS 23.0). The Structural (SEM) model () was identified by three interrelated latent constructs (affective professional commitment, Code of Ethics and accounting ethics principles).

Figure 1. Structural model: unstandardized solution.

Source: Authors.

Before interpreting the structural model of relationships, fit tests of the created SEM model were calculated. Since the Chi-square statistic showed that the model did not fit the data well, Chi-square of 147,970 with 98 degrees of freedom (p < .001), the other fit indicators were examined. Goodness of fit indicators indicate that the structural model satisfactorily fit the data (GFI: 0.947; RMSEA: 0.040; AGFI: 0.927; CFI: 0.988; TLI: 0.985; NFI: 0.966; Chisq/df: 1.510) and indicated a sufficient basis for testing the proposed hypotheses.

As hypothesized, affective professional commitment (β = 0.186, p < .001) had a significant and positive impact on the understanding of the effects of the Code of Ethics, and the Code of Ethics (β = 0.103, p = .001) had a significant and positive impact on the perceived importance of accounting ethics principles application ().

Table 6. Structural equation model results.

According to the results in and , the first two hypotheses were supported. Therefore, this study verifies that affective professional commitment is a positive driver for using the Code of Ethics and understanding its positive effects. The understanding of the Code of Ethics is a positive driver for applying the accounting ethics principles.

In addition, we investigated the mediating role of the Code of Ethics between affective professional commitment and accounting ethics principles. The mediating effect was tested using the bootstrapping approach with 2000 bootstrap samples. The maximum likelihood (ML) bootstrap with 95% bias-corrected confidence intervals was obtained.

Initially, the relationship between the affective professional commitment and accounting ethics principles without the Code of Ethics (mediator) was tested. The results indicated that the relationship between affective professional commitment and accounting ethics principles was significant (p = .005). In a further phase, the indirect effect of the affective professional commitment through the Code of Ethics to accounting ethics principles was tested, and the results indicated a significant indirect effect (p = .001) and showed mediation between the affective professional commitment and accounting ethics principles (). The direct effect between the affective professional commitment and accounting ethics principles with a mediator (the code of ethics) was tested to determine whether this mediation was full or partial. The results showed that the direct relationship was also statistically significant (p = .040), which indicates that the relationship between the professional commitment and accounting ethics principles was partially mediated by the Code of Ethics ().

Table 7. Indirect and direct effect of professional commitment on accounting ethical principles.

Based on bootstrapping, the indirect procedure provides a 95% confidence interval for the value of the indirect effect from affective professional commitment to accounting ethics principles via the Code of Ethics. The lower bound of this confidence interval is 0.006; the upper bound is 0.047, and since the confidence interval did not contain zero, the third hypothesis was supported. The results indicate that the Code of Ethics mediates the effect of affective professional commitment on the perceived importance of accounting ethics principles application.

4. Discussion

4.1. Explanation of the findings

Like in some other countries (Odar et al., Citation2017), no requirements related to professional qualification of accountants in business are prescribed by Croatian legislation. Accountants in Croatia are not required to have any professional certificate or license. Therefore, there are no restrictions nor requirements needed for providing accounting services in business. Accountants in Croatia can use the Code of Ethics for Professional Accountants by ISEBA for ethical guidance. This Code of Ethics is translated into Croatian and available online but prescribed only to auditors (professional accountants in public practice) by the chamber although it is also addressed to professional accountants in business (thus, employed in commerce, industry or service, public sector, non-profit organisations and regulatory or professional bodies). Our results indicate that the accountants’ self-assessment regarding the conversance with the Code of Ethics is irrelevant (CE1) so this item was removed from analysis. Conversely, all the observed effects of understanding the Code of Ethics were significant. This Code of Ethics highly promotes the application of five fundamental accounting ethics principles. According to our results, only the confidentiality (AEP5) was excluded from the model (although it is the most applicable principle judging from the mean value of 4.89).

Due to the weak loading, importance of being an accountant for self-image (PC1) was excluded from our model. Interestingly, the identical item was dropped from the model of Smith and Hall (Citation2008) because of to the same reason (loading below 0.5).

To sum up, our findings indicate that affective professional commitment of accountants in business is positively associated with perceived importance of application of accounting ethics principles in practice. Empirical results show that it is reasonable to expect that professional accountants in business act according to the accounting ethics principles even more if they are decidedly involved in the accounting profession. As Smith and Hall (Citation2008, p. 87) pointed out, ‘affective professional commitment will develop when an accountant becomes involved in, recognizes the value relevance of, and/or derives his/her identity from, the accounting profession’. The awareness of the implications of the Code of Ethics also contributes to better application of the accounting ethics principles. Smith et al. (Citation2009) acknowledged that just reminding of some ethical guidelines like Ten Commandments leads to lesser degree of unethical behaviour. Therefore, the role of the Code of Ethics is to enhance the awareness of the importance of accounting ethics principles and their application in everyday work.

Although the professional accountants in business may not know the Code of Ethics in detail, they are quite aware that understanding it and using its guidelines could have effect on: decrease of fraud and corruption; decrease of pressure occurrence (intimidation or other threat to compliance), decrease of attachment bias, decrease of conflict of interest, increase of financial statements credibility, increase of the respect for information privity.

Prior research (Smith & Hall, Citation2008, p. 87) revealed that accountants with high affective professional commitment ‘experience enhanced identification and commitment to the goals, objectives and standards of the profession’. Our empirical results confirm that professional accountants in business with higher levels of affective professional commitment are more likely to perceive the importance of accounting ethics principles. This finding is in line with the conclusion of Greenfield et al. (Citation2008) who pointed out that more professionally committed accountants are less prone to behave opportunistically. In addition, our results correspond to those of Elias (Citation2008) who confirmed that higher levels of professional commitment and higher perception of the importance of financial reporting were found in those who are more likely to perceive questionable actions as unethical and less likely to engage in such actions.

As Byza et al. (Citation2019) stated, ‘values are individuals’ moral compasses that guide people’s decisions and interactions in their social and work environment’. Hence, this positive relationship between professional commitment and accounting ethics principles perception could be justified from psychological perspective. Our findings can be summarized as Jeffrey et al. (Citation1996) pointed out, ‘higher professional commitment is associated with a higher level of moral reasoning’.

4.2. Concluding remarks

While some people have an innate sense of morality, the others should be guided and constantly reminded. Therefore, the role of the Code of Ethics was assumed (and confirmed) to be significant in application of the accounting ethics principles. Recognizing the positive effects that awareness of the guidelines of the Code of Ethics have on upgrading the perception of accounting ethics principles application was in the focus of our study. The results presented in this study provide some suggestions for the improvement of the accounting ethics principles application. Improvements in accounting ethics principles application may be facilitated by addressing both the affective professional commitment of accountants and the Code of Ethics implementation as the latter has both direct and indirect associations with accounting ethics principles implementation.

The effect of affective professional commitment on the perceived importance of accounting ethics principles application was explored. Professional accountants in business agree that it is reasonable to expect that an accountant should behave according to the accounting ethics principles (integrity, objectivity, professional competence and due care, confidentiality and professional behaviour) more so if they report high level of affective professional commitment (identification with, involvement in and emotional attachment to the accounting profession).

Although this article extends the literature on accounting ethics, it has several limitations. First, the analysis is based on a quantitative research method; we used a set of cross-sectional data. This limitation constrains our confidence in how consistent and long-lasting effects of affective professional commitment and the effects of the Code of Ethics understanding on the perceived importance of accounting ethics principles might be. Future studies could perform a longitudinal analysis and use the time series methods. Second, like in all survey research the subjectivity of respondents cannot be fully controlled so biases may occur. Finally, some additional relevant factors such as other concepts of professional commitment could be considered for inclusion into the research to make it more comprehensive.

Accounting ethics emerged as an important socio-economic issue due to the recent accounting scandals with enormous consequences. Focusing on improvement, both affective professional commitment and the Code of Ethics implementation may enable greater accounting ethics principles application.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

References

- Alzola, M. (2017). Beware of the watchdog: Rethinking the normative justification of gatekeeper liability. Journal of Business Ethics, 140(4), 705–721. https://doi.org/10.1007/s10551-017-3460-3

- Armstrong, R. W., Williams, R. J., & Barrett, J. D. (2004). The impact of banality, risky shift and escalating commitment on ethical decision making. Journal of Business Ethics, 53(4), 365–370. https://doi.org/10.1023/B:BUSI.0000043491.10007.9a

- Arthur, J., Earl, S. R., Thompson, A. P., & Ward, J. W. (2021). The value of character-based judgement in the professional domain. Journal of Business Ethics, 169(2), 293–308.

- Bagraim, J. J. (2003). The dimensionality of professional commitment. SA Journal of Industrial Psychology, 29(2), 6–9. https://doi.org/10.4102/sajip.v29i2.104

- Barrainkua, I., & Espinosa-Pike, M. (2020). Antecedents of organisational professional conflict faced by professional accountants in different work settings. Revista Brasileira de Gestão de Negócios, 22(3), 686–704.

- Bayou, M. E., Reinstein, A., & Williams, P. F. (2011). To tell the truth: A discussion of issues concerning truth and ethics in accounting. Accounting, Organizations and Society, 36(2), 109–124. https://doi.org/10.1016/j.aos.2011.02.001

- Biong, H., Nygaard, A., & Silkoset, R. (2010). The influence of retail management’s use of social power on corporate ethical values, employee commitment, and performance. Journal of Business Ethics, 97(3), 341–363. https://doi.org/10.1007/s10551-010-0523-0

- Bollen, K. A., & Long, J. S. (1993). Testing structural equation models. Sage.

- Bonaci, C. G., Strouhal, J., Müllerová, L., & Roubickova, J. (2013). Corporate governance debate on professional ethics in accounting profession. Central European Business Review, 2(3), 30–35. https://doi.org/10.18267/j.cebr.52

- Byza, O. A., Dörr, S. L., Schuh, S. C., & Maier, G. W. (2019). When leaders and followers match: The impact of objective value congruence, value extremity, and empowerment on employee commitment and job satisfaction. Journal of Business Ethics, 158(4), 1097–1112.

- Cardona, R. J., Rezaee, Z., Rivera-Ortiz, W., & Vega-Vilca, J. C. (2020). Regulatory enforcement of accounting ethics in Puerto Rico. Journal of Business Ethics, 167(1), 63–76. https://doi.org/10.1007/s10551-019-04137-4

- Carmeli, A., & Sheaffer, Z. (2009). How leadership characteristics affect organizational decline and downsizing. Journal of Business Ethics, 86(3), 363–378. https://doi.org/10.1007/s10551-008-9852-7

- Caron, M.-A., & Fortin, A. (2014). Accountants’ construction of CSR competencies and commitment. Sustainability Accounting, Management and Policy Journal, 5(2), 172–196. https://doi.org/10.1108/SAMPJ-03-2013-0013

- Chen, Y., Zhou, X., & Klyver, K. (2019). Collective efficacy: Linking paternalistic leadership to organizational commitment. Journal of Business Ethics, 159(2), 587–603. https://doi.org/10.1007/s10551-018-3847-9

- Cheung, G. W., & Lau, R. S. (2008). Testing mediation and suppression effects of latent variables: Bootstrapping with structural equation models. Organizational Research Methods, 11(2), 296–325. https://doi.org/10.1177/1094428107300343

- Christensen, A., Cote, J., & Latham, C. K. (2018). Developing ethical confidence: The impact of action-oriented ethics instruction in an accounting curriculum. Journal of Business Ethics, 153(4), 1157–1175. https://doi.org/10.1007/s10551-016-3411-4

- Clayton, B. M., & van Staden, C. J. (2015). The impact of social influence pressure on the ethical decision making of professional accountants: Australian and New Zealand evidence. Australian Accounting Review, 25(4), 372–388. https://doi.org/10.1111/auar.12077

- Clements, C. E., Neill, J. D., & Stovall, O. S. (2009). The impact of cultural differences on the convergence of international accounting codes of ethics. Journal of Business Ethics, 87(3), 383–391.

- Cullen, J. B., Parboteeah, K. P., & Victor, B. (2003). The effects of ethical climates on organizational commitment: A two-study analysis. Journal of Business Ethics, 46(2), 127–141. https://doi.org/10.1023/A:1025089819456

- Cullinan, C., Bline, D., Farrar, R., & Lowe, D. (2008). Organization-harm vs. organization-gain ethical issues: An exploratory examination of the effects of organizational commitment. Journal of Business Ethics, 80(2), 225–235. https://doi.org/10.1007/s10551-007-9414-4

- Davidson, B. I., & Stevens, D. E. (2013). Can a code of ethics improve manager behavior and investor confidence? An experimental study. The Accounting Review, 88(1), 51–74. https://doi.org/10.2308/accr-50272

- Dellaportas, S. (2006). Making a difference with a discrete course on accounting ethics. Journal of Business Ethics, 65(4), 391–404. https://doi.org/10.1007/s10551-006-0020-7

- Domino, M. A., Wingreen, S. C., & Blanton, J. E. (2015). Social cognitive theory: The antecedents and effects of ethical climate fit on organizational attitudes of corporate accounting professionals – A reflection of client narcissism and fraud attitude risk. Journal of Business Ethics, 131(2), 453–467. https://doi.org/10.1007/s10551-014-2210-z

- Elçi, M., & Alpkan, L. (2009). The impact of perceived organizational ethical climate on work satisfaction. Journal of Business Ethics, 84(3), 297–311. https://doi.org/10.1007/s10551-008-9709-0

- Elias, R. (2008). Auditing students’ professional commitment and anticipatory socialization and their relationship to whistleblowing. Managerial Auditing Journal, 23(3), 283–294. https://doi.org/10.1108/02686900810857721

- Erben, G. S., & Güneşer, A. B. (2008). The relationship between paternalistic leadership and organizational commitment: Investigating the role of climate regarding ethics. Journal of Business Ethics, 82(4), 955–968. https://doi.org/10.1007/s10551-007-9605-z

- Fassin, Y., & Drover, W. (2017). Ethics in entrepreneurial finance: Exploring problems in venture partner entry and exit. Journal of Business Ethics, 140(4), 649–672. https://doi.org/10.1007/s10551-015-2873-0

- Fu, W., Deshpande, S. P., & Zhao, X. (2011). The impact of ethical behavior and facets of job satisfaction on organizational commitment of Chinese employees. Journal of Business Ethics, 104(4), 537–543. https://doi.org/10.1007/s10551-011-0928-4

- Gendron, Y., Suddaby, R., & Lam, H. (2006). An examination of the ethical commitment of professional accountants to auditor independence. Journal of Business Ethics, 64(2), 169–193. https://doi.org/10.1007/s10551-005-3095-7

- Gendron, Y., Suddaby, R., & Qu, S. Q. (2009). Professional–organisational commitment: A study of Canadian professional accountants. Australian Accounting Review, 19(3), 231–248. https://doi.org/10.1111/j.1835-2561.2009.00060.x

- Goulet, L. R., & Singh, P. (2002). Career commitment: A re-examination and an extension. Journal of Vocational Behavior, 61(1), 73–91. https://doi.org/10.1006/jvbe.2001.1844

- Greenfield, A. C., Norman, C. S., & Wier, B. (2008). The effect of ethical orientation and professional commitment on earnings management behavior. Journal of Business Ethics, 83(3), 419–434. https://doi.org/10.1007/s10551-007-9629-4

- Hair, J. F., Black, W. C., Babin, B. J., & Anderson, R. E. (2009). Multivariate data analysis (7th ed.). Pearson Prentice Hall.

- Hall, M., Smith, D., & Langfield‐Smith, K. (2005). Accountants' commitment to their profession: Multiple dimensions of professional commitment and opportunities for future research. Behavioral Research in Accounting, 17(1), 89–109. https://doi.org/10.2308/bria.2005.17.1.89

- Higgs-Kleyn, N., & Kapelianis, D. (1999). The role of professional codes in regarding ethical conduct. Journal of Business Ethics, 19(4), 363–374. https://doi.org/10.1023/A:1005899517191

- Huehn, M. P. (2008). Unenlightened economism: The antecedents of bad corporate governance and ethical decline. Journal of Business Ethics, 81(4), 823–835. https://doi.org/10.1007/s10551-007-9550-x

- Huterski, R., Voss, G., & Huterska, A. (2020). Professional ethics in accounting as assessed by managers of economic units. European Research Studies, 23, 720–731.

- IESBA. (2018). International Ethics Standards Board for Accountants (IESBA), International Code of Ethics for Professional Accountants.

- Ishaque, M. (2021). Managing conflict of interests in professional accounting firms: A research synthesis. Journal of Business Ethics, 169(3), 537–555. https://doi.org/10.1007/s10551-019-04284-8

- Jackson, D. L., Gillaspy, J. A. Jr., & Purc-Stephenson, R. (2009). Reporting practices in confirmatory factor analysis: An overview and some recommendations. Psychological Methods, 14(1), 6–23.

- Jeffrey, C., Weatherholt, N., & Lo, S. (1996). Ethical development, professional commitment, and rule observance attitudes: A study of auditors in Taiwan. The International Journal of Accounting, 31(3), 365–379. https://doi.org/10.1016/S0020-7063(96)90025-4

- Lail, B., MacGregor, J., Marcum, J., & Stuebs, M. (2017). Virtuous professionalism in accountants to avoid fraud and to restore financial reporting. Journal of Business Ethics, 140(4), 687–704. https://doi.org/10.1007/s10551-015-2875-y

- Lord, A. T., & DeZoort, F. T. (2001). The impact of commitment and moral reasoning on auditors’ responses to social influence pressure. Accounting, Organizations and Society, 26(3), 215–235. https://doi.org/10.1016/S0361-3682(00)00022-2

- Loscher, G., Ruhle, S., & Kaiser, S. (2020). Commitment profiles of accountants: A person-centered study of the commitment towards profession and organization. Behavioral Research in Accounting, 32(1), 51–68. https://doi.org/10.2308/bria-52476

- Maniora, J. (2017). Is integrated reporting really the superior mechanism for the integration of ethics into the core business model? An empirical analysis. Journal of Business Ethics, 140(4), 755–786. https://doi.org/10.1007/s10551-015-2874-z

- Marques, P. A., & Azevedo-Pereira, J. (2009). Ethical ideology and ethical judgments in the Portuguese accounting profession. Journal of Business Ethics, 86(2), 227–242. https://doi.org/10.1007/s10551-008-9845-6

- McManus, L., & Subramaniam, N. (2014). Organisational and professional commitment of early career accountants: Do mentoring and organisational ethical climate matter? Accounting & Finance, 54(4), 1231–1261. https://doi.org/10.1111/acfi.12029

- Meyer, J. P., Allen, N. J., & Smith, C. A. (1993). Commitment to organizations and occupations: Extension and test of a three-component conceptualization. Journal of Applied Psychology, 78(4), 538–551. https://doi.org/10.1037/0021-9010.78.4.538

- Micceri, T. (1989). The unicorn, the normal curve, and other improbable creatures. Psychological Bulletin, 105(1), 156–166. https://doi.org/10.1037/0033-2909.105.1.156

- Nerandzic, B., Perovic, V., & Zivkov, E. (2012). Personality and moral character traits and acknowledging the principles of management ethics, auditing and accounting ethics. Economic Research-Ekonomska Istraživanja, 25(suppl. 1), 288–312. https://doi.org/10.1080/1331677X.2012.11517566

- Nevitt, J., & Hancock, G. R. (2001). Performance of bootstrapping approaches to model test statistics and parameter standard error estimation in structural equation modeling. Structural Equation Modeling, 8(3), 353–377. https://doi.org/10.1207/S15328007SEM0803_2

- Odar, M., Jerman, M., Jamnik, A., & Kavčič, S. (2017). Accountants’ ethical perceptions from several perspectives: Evidence from Slovenia. Economic Research-Ekonomska Istraživanja, 30(1), 1785–1803. https://doi.org/10.1080/1331677X.2017.1392885

- Okpara, J. O., & Wynn, P. (2008). The impact of ethical climate on job satisfaction, and commitment in Nigeria: Implications for management development. Journal of Management Development, 27(9), 935–950. https://doi.org/10.1108/02621710810901282

- Payne, D. M., Corey, C., Raiborn, C., & Zingoni, M. (2019). An applied code of ethics model for decision-making in the accounting profession. Management Research Review, 43(9), 1117–1134. https://doi.org/10.1108/MRR-10-2018-0380

- Pusti, A. (2017). Comparison of perception of ethics among the accounting professionals, accounting educators and accounting students. International Journal of Business Ethics in Developing Economies, 6(1), 41–49.

- Rogošić, A., & Bakotić, D. (2019). Job satisfaction of accountants and their professional ethics. Ekonomski Vjesnik, 32(1), 165–177.

- Sejjaaka, S. K., & Kaawaase, T. K. (2014). Professionalism, rewards, job satisfaction and organizational commitment amongst accounting professionals in Uganda. Journal of Accounting in Emerging Economies, 4(2), 134–157.

- Shafer, W. E. (2009). Ethical climate, organizational‐professional conflict and organizational commitment. Accounting, Auditing & Accountability Journal, 22(7), 1087–1110. https://doi.org/10.1108/09513570910987385

- Shafer, W. E., Poon, M. C., & Tjosvold, D. (2013). An investigation of ethical climate in a Singaporean accounting firm. Accounting, Auditing & Accountability Journal, 26(2), 312–343. https://doi.org/10.1108/09513571311303747

- Shafer, W. E., Simmons, R. S., & Yip, R. W. Y. (2016). Social responsibility, professional commitment and tax fraud. Accounting, Auditing & Accountability Journal, 29(1), 111–134. https://doi.org/10.1108/AAAJ-03-2014-1620

- Singh, A., & Gupta, B. (2015). Job involvement, organizational commitment, professional commitment, and team commitment: A study of generational diversity. Benchmarking: An International Journal, 22(6), 1192–1211. https://doi.org/10.1108/BIJ-01-2014-0007

- Škare, M., Kostelić, K., & Justić Jozičić, K. (2013). Sustainability of employee productivity as a presumption of sustainable business. Economic Research-Ekonomska Istraživanja, 26(suppl. 1), 311–330. https://doi.org/10.1080/1331677X.2013.11517654

- Smith, D., & Hall, M. (2008). An empirical examination of three-component model of professional commitment among public accountants. Behavioral Research in Accounting, 20(1), 75–92. https://doi.org/10.2308/bria.2008.20.1.75

- Smith, M., Charoensukmongk, P. P., Elkassabgi, A., & Lee, K. H. H. (2009). Aspects of accounting codes of ethics in Canada, Egypt, and Japan. Internal Auditing, 24(6), 26–34.

- Spalding, A. D., & Lawrie, G. R. (2019). A critical examination of the AICPA’s new “conceptual framework” ethics protocol. Journal of Business Ethics, 41(4), 349–360.

- Spalding, A. D. Jr., & Oddo, A. (2011). It’s time for principles-based accounting ethics. Journal of Business Ethics, 99(S1), 49–59. https://doi.org/10.1007/s10551-011-1166-5

- Tabachnick, B. G., & Fidell, L. S. (2013). Using multivariate statistics. Pearson.

- Tweedie, D., Dyball, M. C., Hazelton, J., & Wright, S. (2013). Teaching global ethical standards: A case and strategy for broadening the accounting ethics curriculum. Journal of Business Ethics, 115(1), 1–15. https://doi.org/10.1007/s10551-012-1364-9

- Valentine, S., & Fleischman, G. (2008). Professional ethical standards, corporate social responsibility, and the perceived role of ethics and social responsibility. Journal of Business Ethics, 82(3), 657–666. https://doi.org/10.1007/s10551-007-9584-0

- Valentine, S., Godkin, L., & Lucero, M. (2002). Ethical context, organizational commitment, and person-organization fit. Journal of Business Ethics, 41(4), 349–360. https://doi.org/10.1023/A:1021203017316

- Velayutham, S. (2003). The accounting profession’s code of ethics: Is it a code of ethics or a code of quality assurance? Critical Perspectives on Accounting, 14(4), 483–503. https://doi.org/10.1016/S1045-2354(02)00138-7

- Vladu, A. B., Amat, O., & Cuzdriorean, D. D. (2017). Truthfulness in accounting: How to discriminate accounting manipulators from non-manipulators. Journal of Business Ethics, 140(4), 633–648. https://doi.org/10.1007/s10551-016-3048-3

- Williams, J., & Elson, R. J. (2010). The challenges and opportunities of incorporating accounting ethics into the accounting curriculum. Journal of Legal, Ethical and Regulatory Issues, 13(1), 105–115.

- Žager, K., Dečman, N., & Novak, A. (2019). Importance of ethics in the education of accountants. Ekonomski Vjesnik, 32(2), 463–476.