?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Sustainable development has gained the attention of researchers worldwide and is becoming an important topic, especially in relation to corporate governance principles. This study investigates the influence of corporate governance on sustainable development in a sample of 185 countries over 2005–2020 using a panel linear regression model. Separate analyses are also conducted on subsamples of high- and low-income countries. Our findings highlight the positive influence of corporate governance, as measured by board efficacy, the strength of audits and reports, and digitalisation, on sustainable development, as measured by the Human Development Index, Human Capital Index, and Environmental Performance Index. Moreover, we find a higher positive and marginal effect of the influence of corporate governance on sustainable development for low-income countries than for high-income countries. The robustness checks performed using variables related to the happiness index, women in top management positions, and technology adoption verify our results. Our findings are important for managers and policymakers to consolidate sustainable development through the incentive brought about by high-quality corporate governance.

1. Introduction

The well-being of a company should be a common interest of all engaged parties. Although researchers have long emphasised the importance of corporate governance principles (Nedelchev, Citation2013), Howell and Sorour (Citation2016) raised the importance of implementing good practices to ensure organizational well-being. Hashanah and Mazlina (Citation2005) also underlined the corporate governance elements that directly hamper the healthy development of society. Thus, implementing good corporate governance principles ensures the positive and therefore sustainable development of the business.

Various studies have analyzed the relationships between corporate governance and corporate social responsibility (CSR) (Achim et al., Citation2017; Crane & Matten, Citation2007; Kolk & Pinkse, Citation2010) as well as between CSR and sustainable development (Kahraman Akdogu, Citation2017; Truant et al., Citation2017). However, few studies (e.g., De Luca, Citation2020; Dienes et al., Citation2016) have investigated the direct relationship between corporate governance and sustainable development. To bridge this gap in the literature, we analyze the impact of corporate governance on social and environmental performance as well as compare the influence of corporate governance in high- and low-income countries. We use a sample of 185 countries over 2005–2020 and panel linear regressions. To validate our main results, we also check their robustness using variables such as the happiness index, women in top management positions, and technology adoption. The results show that the level of sustainable development increases when the use of corporate governance best practices increases. Moreover, we find that corporate governance has a higher impact on the low-income countries than in the high-income countries than

The novelty of this study brought to the literature consists in the fact that it covers a gap in literature and it comes with important evidences of the role of corporate governance on boosting the sustainable development of the society. The increase of the quality of corporate governance realised through the increase in efficiency of board, audit quality, participating female in ownership and top management and the increase of digitalisation, are important channels for improving the performances of the companies and for creating sustainable development for the society. These findings have many policy implications for all the participant at the business environment.

The structure of the reminder of this paper is as follows. In Section 2, we review the literature on the relationships between corporate governance and CSR as well as between CSR and sustainable development. Section 3 presents the methodology and describes the data. Section 4 summarises our results from the empirical tests. Section 5 discusses the findings in relation to the literature. The last section concludes, including limitations, policy implications, and avenues for future research.

2. Literature review

2.1. Corporate governance and CSR

Sustainable development is a matter of great importance for modern society and is gaining increasing research attention. In the wake of major accounting scandals such as Enron, Tyco, and Worldcom, corporate governance is promoting CSR to restore investor confidence in the financial system through the transparent presentation of financial statements and deployment of corporate governance practices. Thus, starting to this point, the well-being of a company has became an important objective of stakeholders through the adoption of corporate governance principles. At the same time, the issues of a sustainable economy and social responsibility have cleared the path for a new role for companies in society. More specifically, strategic choices and performance have had to be reconsidered (Salvioni & Gennari, Citation2019). In this view, Mirza et al. (Citation2020) also underlined the importance of business achievements in a pandemic context, finding that a hybrid approach can help companies adapt to everchanging times. Regarding the concept of corporate governance, the study of Waddock and Graves (Citation1997) argued that corporate governance aims to balance economic and social goals as well as individual and community goals. The same idea is supported by Kendall (1999), who argued that good corporate governance supports the interests of those engaged with CSR policy. Aguilera et al. (Citation2007) argued that companies that have implemented good governance procedures (transparency and social responsibility) have a greater inclination to implement CSR practices. Jamali et al. (Citation2008) found that most managers see corporate governance as a necessary pillar of CSR. In addition, Kong (Citation2013) showed that companies’ CSR activities significantly affect corporate governance and may, to some extent, replace the governance role of minority shareholders.

Clearly, corporate governance and CSR are related concepts (Achim et al., Citation2017; Crane & Matten, Citation2007; Kolk & Pinkse, Citation2010). However, Flammer (Citation2015) stated that their relationship is extremely complex. Zingales et al. (Citation2016) showed that management practices and CSR strategies depend on corporate governance factors, with the board of directors and shareholding structure heavily influencing strategic decision-making and risk-taking in CSR activities, which may affect CSR policies to cover unethical behaviour and misconduct. As CSR is a suitable indicator of the implementation of a business’s sustainable behaviour, companies might apply CSR policies because they think it is the responsible thing to do or to raise performance (Ullah et al., Citation2019).

In the same vein, various studies (e.g., Crane & Matten, Citation2007; Spitzeck, Citation2009; Welford, Citation2007) have demonstrated a close link between corporate governance and the business ethics adopted by a company. Promoting both managers and their subordinates to behave ethically has a decisive impact on the end results of the entire organisation. To understand what is right and wrong in business behaviour, Crane and Matten (Citation2007) referred to morality, which is reflected by individual and social values and community beliefs.

Regarding drivers of CSR behaviour, Fahad and Mubarak (Citation2020) found that CSR disclosure can be improved by board independence and CEO duality. Habbash (Citation2016) underlined that firm size, family ownership, government ownership, and firm age affect the quality of CSR reporting. Coffie et al. (Citation2018) demonstrated that using larger/smaller boards and establishing CSR committees improve CSR disclosure. Similarly, Welford (Citation2007) and Spitzeck (Citation2009) showed that good CSR policies are related to qualitative corporate governance reporting. In other words, if CSR is integrated into the corporate governance structure, companies have an incentive to act responsibly. After investigating various definitions of corporate governance, Kolk and Pinkse (Citation2010) concluded that this concept is largely related to the concepts of CSR. They found that more than half of the 250 companies in their sample allocate a dedicated section to corporate governance in their CSR reports. Similarly, Chan et al. (Citation2014) concluded that businesses that present a CSR policy provide qualitative corporate governance reporting.

2.2. CSR and sustainable development

The topic of sustainable development arose in 1970 with the publication of the first report of the Club of Rome entitled ‘The Limits of Growth.’ The best-known definition of this concept is mentioned in the report of the World Commission on Environment and Development (United Nations, Citation1987), which defines sustainable development as ‘development that meets the needs of the present generation, without compromising the ability of future generations to meet their own needs.’ In the context of sustainable development (Achim et al., Citation2017), CSR refers to the orientation and attitude of an organization to voluntarily integrate into its strategy and social and environmental concerns while ensuring the economic success of the business. At the macroeconomic level, sustainable development includes economic, social, and environmental pillars, which should be equally integrated into the process of enhancing development. Hence, applying CSR principles positively impacts sustainable development (Kahraman Akdogu, Citation2017).

Husser et al. (Citation2012) concluded that majorities of French companies excepting the companies that have to deal with the pollution aspects are concerned on CSR disclosure rather than sustainable development. Thus, the study reveals a short- term orientation of the French companies rather than a long-term one. Kahraman Akdogu (Citation2017) stated that CSR appeared as a ‘reaction for sustainable development’, therefore businesses can contribute to sustainable development by promoting CSR activities. Environmental, social, and governance (ESG) performance, as provided in a sustainability report, measures a firm’s accountability to both external and internal stakeholders (Calabrese et al., Citation2017). Truant et al. (Citation2017) tested the complex relationship between sustainability reporting and the disclosure of ethical, social, and environmental risk, finding a negative relationship between sustainability reporting and environmental risk and that social risk can damage a company’s reputation. Fatemi et al. (Citation2018) demonstrated that the association between a company’s ESG activities and its evaluation is moderated by its disclosures of those activities. Therefore, CSR reporting contributes to ESG disclosures, creating benefits for information users. Adams (Citation2017) and Gardberg and Fombrun (Citation2006) argued that CSR reports lead to greater transparency by outlining the links between financial performance and ESG. At the same time, high ESG performance creates competitive advantage for a firm.

The reporting of non-financial data consists of descriptions, opinions, and facts that cannot be expressed in monetary units (Gernon and Gary, Gernon & Gary, Citation2000) and may be prospective or retrospective in nature. With the implementation of the 2014/95 Directive, listed EU companies are now obliged to provide non-financial reporting (Salvioni & Bosetti, Citation2014). However, the European Union wants to implement these reports for non-listed companies as well because all companies should be socially responsible regardless of their size. However, despite being an important tool in CSR management, non-financial reporting requirements for small and medium-sized businesses have not yet been developed (Baumann-Pauly et al., Baumann-Pauly et al., Citation2013).

Few studies have investigated the relationship between corporate governance and sustainable development. Dienes et al. (Citation2016) identified that the structure of property, size of the company, and visibility of the media are the most important factors in the disclosure of sustainability reports. Similarly, De Luca (Citation2020) found that several factors represent the basis of sustainable development, namely, the structure and size of corporate governance, institutional factors, the objective of companies’ activities, and their profitability (De Luca, Citation2020).

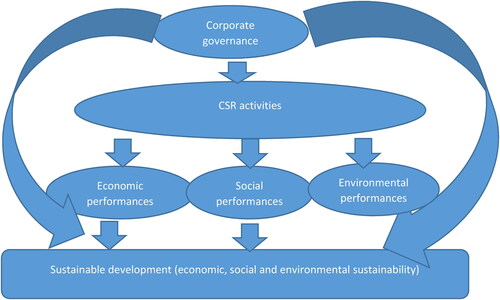

Based on the foregoing, we investigate whether a high level of corporate governance in a firm increases its level of sustainable development. We also examine the extent to which the corporate governance–sustainable development relationship depends on a country’s development level. In other words, does it differ between high- and low-income countries? presents the research framework.

Figure 1. The causal relationships between corporate governance and sustainable development.

Source: own projection

3. Methodology and data

3.1. Measuring the variables

3.1.1. Dependent variable: Sustainable development

Sustainable development, the dependent variable, is measured using the following three indicators.

The Human Development Index (HDI) is a composite index for evaluating the development of a country, not just its economic growth. It is a summary measure of the average achievement in three key dimensions of human development: life expectancy, education, and per capita income (UNDP (2022)/Human Development Reports, Citation2022). Other studies have used the HDI as a proxy indicator of sustainable development (Absalyamova et al., Citation2016; Murshed & Mredula, Citation2018).

The Human Capital Index (HCI) measures human capital using three pillars: survival, as measured by under-5 mortality rates; expected years of quality-adjusted schooling, which combines information on the quantity and quality of education; and the health environment. Human capital is an important determinant of environmental performance (Kim & Go, Citation2020).

The Environmental Performance Index (EPI) describes how close countries are to meeting their environmental policy goals. The EPI offers a scorecard that highlights leaders and laggards in environmental performance, provides insights into best practices, and guides countries that aspire to be leaders in sustainability (Yale University, Citation2022). It is used in many studies as a proxy for environmental performance (Emerson et al., Citation2012; Esty et al., Citation2008; Gallego-Alvarez et al., Citation2014; Kim & Go, Citation2020).

3.1.2. Independent variable: corporate governance

We use two important variables to measure corporate governance (Achim & Borlea, Citation2020): Efficacy of corporate board (BE) and Strength of audits and reports (SAR). Both indicators are calculated and reported in the Global Competitiveness Report (2021), which is a tool for measuring national competitiveness for economies globally provided annually by the World Economic Forum. They are scored between 1 (the weakest) and 7 (the strongest), thus reflecting the efficiency of corporate governance in national economies.

In addition, in the era of the digital economy, high-quality corporate governance requires a high level of digitisation. The digitisation of the activities of companies above the traditional methods of operations and organizational bureaucracy is a key factor to their success. According to Fréminville (Citation2020), digitalisation affects interested parties through ‘e-reputation, price volatility, dematerialisation of operations, protection of board information, disintermediation, and emergence of new players.’ Digital corporate governance empowers company boards to make better strategic decisions (Tricor Group, Citation2020). Thus, a high level of digitisation can be considered as a good proxy for corporate governance. Following Achim et al. (Citation2021), we measure the level of digitisation as the number of individuals using the Internet (Internet) as a percentage of the total population.

3.1.3. Control variables

In the literature, the following factors are found to be determinants of sustainable development: public governance, urbanisation, unemployment, and culture. First, the efficiency of a country’s public governance influences its level of development (Absalyamova et al., Citation2016; Forson et al., Citation2017; Hoinaru et al., Citation2020). More precisely, a higher level of corruption in public institutions erodes the development of the economy. Hoinaru et al. (Citation2020) highlighted the destructive role of corruption on the economic and sustainable development of states. Similarly, Forson et al. (Citation2017) found that corruption poses a long-term threat to the sustainable development of economies in sub-Saharan Africa. Absalyamova et al. (Citation2016) found a negative effect of corruption on sustainable development, with a 1% increase in corruption in the socioeconomic systems of a state leading to a decrease of more than 1% in the value of the human capital sustainable development index of that state. According to the World Governance Indicators provided by the World Bank (2021), the quality of governance can be expressed using six dimensions: voice and accountability (VA), political stability and absence of violence (PS), government effectiveness (GE), regulatory quality (RQ), rule of law (RL), and control of corruption (CC).

Second, studies (e.g., Rogers et al., Citation2012; Satterthwaite, Citation2008; Zeng et al., Citation2016) find that urbanisation is crucial to regional and global sustainability and that all the richest nations are highly urbanised, while all the poorest nations are predominantly rural. In addition, the level of urbanisation provides strong developmental advantages such as lowering the unit costs of providing piped water, drains, health care, and education, but also some strong environmental advantages, including reducing energy use, cutting waste, controlling pollution, and lowering greenhouse gas emissions (Satterthwaite, Citation2008).

Third, regarding culture as a determinant of sustainable development, cultural heritage, cultural and creative industries, sustainable cultural tourism, and cultural infrastructure can serve as strategic tools for creating benefits, especially in developing countries, given their often rich cultural heritages and substantial labour forces. Since January 2012, culture has been included in 70% of the United Nations Development Assistance Frameworks (UNESCO, Citation2012). The role of culture in achieving sustainable development is also included in the UN 2030 Agenda for Sustainable Development (United Nations, Citation2015). Related to this, the Committee on Culture of UCLG (2018) document highlights the relevance of culture, emphasising that cultural services are basic services and that equal access to them should be guaranteed for all, including the poor and vulnerable. In addition, cultural expressions, services, goods, and heritage sites can contribute to inclusive and sustainable economic development. In the same view, the study of Gallego-Álvarez and Pucheta-Martínez (Citation2021) started their research from the institutional theory whereby firms domiciled in the same institutional context will behave in a similar manner related to innovation practices and ways of creating benefits. They find the cultural dimensions of power distance, masculinity, uncertainty avoidance, and long-term orientation are positively associated with innovation, while individualism has a negative effect, and indulgence has no effect whatsoever.

In our paper, culture relies on the multidimensional cultural model of Hofstede (Hofstede Centre, Citation2022) summing up the following: Power distance (PD), Individualism versus collectivism (IDV), Masculinity versus Femininity (MAS), Uncertainty avoidance (UAI), Long-term orientation (LTO) and the latest added dimension, Indulgence versus restraint (IND).

Finally, high rates of unemployment and underemployment, particularly among young men in small island developing states, are often associated with anti-social behaviour, including crime and drug use, which threatens political stability and sustainable development (United Nations, Citation2014). In addition, reducing youth unemployment rates and empowering vulnerable groups such as women, young people, and people with disabilities are stated as major targets in the 2030 Agenda. Picatoste and Rodriguez-Crespo (Citation2020) underlined decreasing youth unemployment as a way to achieve sustainable development, as the probability of youth unemployment is three times greater than that of adults. Table A in Appendix A summarises these variables.

3.2. Model

Our data cover a sample of 185 countries over 2005–2020. Despite striving to maximise the number of observations, they still comprise an unbalanced panel structure. We estimate panel linear regression models in which sustainable development is determined as a function of the corporate governance proxies and control variables. We use the pooled OLS method for the panel data and the forward estimation technique to build from a simple linear regression model to multiple regressions (see EquationEquation (1)(1)

(1) ). The resulting models are estimated as fixed effects models (FEMs) and random effects models (REMs). The Hausman test probability indicates the optimal technique (bolded and included in the results tables).

The general form of our model is

(1)

(1)

where

Sustainable developmentit is the dependent variable for country i in year t;

Corporate governanceit is the independent variable for country i in year t;

Controls(j)it represents the jth control variable for country i in year t;

β0 is the intercept;

β1 is the regression coefficient that indicates the extent to which the independent variable (Corporate governance) is associated with the dependent variable (Sustainable development) if β1 is found to be statistically significant;

β2(j) is the regression coefficient for the jth variable in the vector of control variables;j denotes the ranges of the vector of control variables (public governance, urbanisation, unemployment, and culture);

εit is the residual or prediction error for country i in year t.

presents the descriptive statistics. Further, we classify the 185 sample countries by their level of economic development into high- and low-income countries. This classification is based on data provided by the World Bank (2020), which classifies countries as high-income, upper-middle-income, lower-middle-income, and low-income countries. We thus divide our sample into 128 low-income countries (comprising low- and middle-income economies) and 57 high-income countries. Table B in Appendix B lists the two subsamples.

Table 1. Summary statistics.

that shows the average HDI for high-income countries is higher than that of low-income countries by 0.20 units, or about 33%. For the HCI and EPI, the relative changes are even higher, at about 47% and 54%, respectively, for high-income countries compared with low-income countries. Similarly, corporate governance quality in high-income countries is significantly higher than that in low-income countries. Specifically, the indexes of BE and SAR are 14% and 30% higher, respectively, for developed countries than for developing ones. The difference for digitalisation is even larger. More precisely, about 70.4% of the population in high-income countries use the Internet on average compared with about 24.2% in low-income countries (2.9 times higher).

For the control variables, we note significantly higher values for high-income countries than for low-income ones. The average level of public governance in high-income countries is above 1 unit, while the values are negative for all six dimensions for low-income countries. The values of the cultural components are significantly different for the two groups of countries. In addition, the percentage of urbanisation in high-income countries is 60% higher than that in low-income countries, while the level of unemployment is about 14% lower.

4. Results

4.1. Baseline results

presents the estimation of the impact of the various corporate governance proxies on sustainable development, proxied by HDI. Models (1)–(5) determine the impact exerted by BE on HDI, models (6)–(9) determine the impact of SAR on HDI, and models (10)–(14) determine the impact exerted by Internet on HDI. All the signs of the corporate governance proxies are positive, indicating a direct relationship; the values of these coefficients indicate the change in the dependent value caused by a one-unit change in the independent variables.

Table 2. Regression results for sustainable development measured by HDI as a function of corporate governance measured by CB, SAR, Internet and other control variables.

First, according to the estimated coefficient of model (1), for a one-unit increase in BE, HDI is higher on average by 0.0634. The predictive accuracy of this model is given by a coefficient of determination (R2) of 0.0962, representing the amount of variance in HDI explained by BE. The significance of the overall model increases as more variables are added: PS as a governance indicator (in model (2)); PD, IDV, UAI, and LTO as cultural dimensions (in model (3), with a negative impact for PD and a positive impact for IDV, UAI, and LTO); and unemployment in model (4) (the OLS model). Model (5) estimates the FEM, as pointed out by the Hausman test, but the cultural variables are omitted owing to multicollinearity. The positive and significant coefficients are maintained for BE and PS; therefore, the higher corporate governance and political stability, the higher is HDI. The negative relationship between HDI and unemployment is also revalidated in model (5).

Model (6) shows that when SAR increases by one unit, HDI is higher on average by 0.0769, significant at the 1% level. This positive impact is maintained in models (7) and (8), which include the positive influence of RQ on HDI (models (7) and (8), also kept in model (9)) and the direct impact of urbanisation on HDI (the cultural dimensions are not significant in model (8)).

Digitalisation, measured by Internet, as a novel corporate governance proxy, exerts a positive impact on HDI in models (10)–(14), and its coefficients are significant at the 1% level, although more variables are added (multiple regression modelling in models (11)–(13) for the OLS regression and model (14) for the FEM). In model (10), for a one-unit increase in Internet, HDI is higher on average by 0.004. GE exerts a positive impact (models (11)–(14)), while IDV and UAI have a positive impact on HDI (models (12) and (13)). Urbanisation, as previously proven, has a direct impact on HDI (models (13) and (14)).

presents the estimations of the impact exerted by the various corporate governance proxies on HCI as a sustainable development indicator. When significant, all three corporate governance proxies (BE in models (1)–(6), SAR in models (7)–(11), and Internet in models (12)–(16)) have a direct relationship with HCI, boosting its level. The interpretations of the simple linear regressions in models (1), (7), and (12) are as follows: for a one-unit increase in BE, HCI is higher on average by 0.0815 (model (1)); for a one-unit increase in SAR, HCI is higher on average by 0.0805 (model (7)); and for a one-unit increase in Internet, HCI is higher on average by 0.0042 (model (12)); moreover, all the coefficients are significant at the 1% level. PS (as an indicator of public governance) has a positive impact on HCI (models (2)–(5) and models (8)–(10)). Similarly, GE (another proxy for public governance) positively influences HCI (models (13)–(16)), while no other government proxy is validated for a multiple regression model of HCI when Internet is considered to be the main exogenous variable. Of the cultural dimensions, PD exerts a negative impact on HCI (models (3)–(5) and models (9) and (10)), while UAI and LTO have a positive impact on HCI (models (3)–(5) and models (9) and (10)). IND has a negative impact on HCI (models (14) and (15)). Urbanisation has a direct influence on HCI (models (4)–(6) and models (10) and (11)), while unemployment has an indirect relationship with HCI (models (5) and (6) as well as models (15) and (16)).

Table 3. Regression results for sustainable development measured by HCI as a function of corporate governance measured by CB, SAR, Internet and other control variables.

presents the estimation of the impact of the various corporate governance proxies on environmental sustainability (EPI). Models (1)–(4) determine the impact exerted by BE on EPI, models (5)–(9) determine the impact of SAR on EPI, and models (10)–(13) determine the impact of Internet on EPI. All the signs of the coefficients of these three corporate governance proxies are positive when significant, indicating a direct relationship: the better corporate governance, the higher is environmental performance through various mechanisms.

Table 4. Regression results for sustainable development measured by EPI as a function of corporate governance measured by CB, SAR, Internet and other control variables.

Starting with model (1), when BE increases by one unit, EPI is higher on average by 9.3194 units. The adjusted R2 of 0.1866 proves the significance of the overall model, which increases to 0.5159 in model (3) as VA and all the cultural dimensions are added into the multiple regression model. The positive and significant coefficients of BE and VA are maintained in model (4) as well; when the estimation technique is changed to the FEM, the cultural influences are omitted because of multicollinearity.

Model (5) shows that when SAR increases by one unit, EPI is higher on average by 9.2235 units. This positive impact of SAR on EPI is maintained in models (6)–(8), which include the positive influence of RQ on EPI and the impact of urbanisation on EPI (positive in models (7)–(9)) and that of unemployment (positive in model (8) and negative in model (9)).

Internet exerts a direct influence on EPI. Throughout models (10)–(13), its coefficients are positive and significant at the 1% level, although more variables are added (multiple regression modelling in models (11)–(13) with GE and the cultural indicators). In model (10), for a one-unit increase in Internet, EPI is higher on average by 0.4267. GE exerts a positive and significant impact (models (11) and (12)). Moreover, IDV, MAS, and UAI have a positive impact on EPI, while LTO and IND have a negative impact (model (12)), all significant at the 1% level.

For the subsample estimations, we consider the same three proxies of corporate governance (BE, SAR, and Internet), but reduce the number of estimated models for each proxy to three: a simple regression model (models (1), (4), and (7); see 4a and ), a multiple regression model built on the forward estimation technique to generate the complex model (models (2), (5), and (8); see 4a and ), and finally the FEM/REM estimation of that complex model (models (3), (6), and (9); see 4a and ).

, and 4a include the estimation of the sustainable development indicators as a function of corporate governance proxies plus the supplementary explanatory variables of public governance, culture, urbanisation, and unemployment. As shown in , BE, SAR, and Internet exert a positive impact on HDI in high-income countries. These coefficients are lower than those for the similar regression for the full sample (see ), suggesting that the impact of BE is lower for high-income countries than for the full sample. Thus, corporate governance seems to be a better tool for boosting social performance in low-income countries.

Table 2a. Regression results for sustainable development measured by HDI as a function of corporate governance measured by CB, SAR, Internet and other control variables, for high income countries (HI).

shows the estimated impact of BE (models (1)–(3)), SAR (models (4)–(6)), and Internet (models (7)–(9)) on HDI as proxies of social development. In addition to their positive impact, these models validate PS, VA, and GE as HDI determinants, with a direct impact when significant. Of the cultural variables, PD exerts a negative impact on HDI (models (2) and (3) as well as models (8) and (9)), as does LTO and IND (model (8)). On the contrary, some cultural variables exert a positive impact on HDI: IND (models (8) and (9)) as well as MAS and UAI (model (8)). Urbanisation and unemployment are not significant in the multiple regression models.

presents the estimated impact of BE (models (1)–(3)), SAR (models (4)–(6)), and Internet (models (7)–(9)) on HCI for the subsample of high-income countries. Besides the positive impact of corporate governance proxies (with the exception of model (6)), these models also validate GE and PS as HCI determinants, with a positive impact when significant (models (2), (3), and (5) for PS and model (8) for GE). Of the cultural variables, PD exerts a negative impact on HCI (models (2) and (3)), IDV exerts a positive impact on HCI (model (5)), and LTO has a positive influence on HCI (model (2)). Urbanisation is validated as an explanatory variable of HCI in model (8), with an indirect influence, while the estimated sign of the coefficient of unemployment is positive in the OLS multiple regression in model (8) and negative in the FEM (model (9)).

Table 3a. Regression results for sustainable development measured by HCI as a function of corporate governance measured by CB, SAR, Internet and other control variables, for high income countries.

estimates BE (models (1)–(3)), SAR (models (4)–(6)), and Internet (models (7)–(9)) as the determinants of EPI for the subsample of high-income countries. Their impact is positive and usually robust to the estimation technique (OLS versus FEM/REM). Of the public governance proxies, GE (models (8) and (9)) and VA (models (2) and (5)) are validated. The cultural variables that remain significant are PD with a negative impact (model (2)); IDV with a positive impact in models (5) and (8); MAS with a positive impact in models (2), (5), and (8); UAI with a negative impact in model (5); LTO with a positive impact in models (2) and (5), but a negative impact in model (8); and IND with a negative impact in model (8). Unemployment has a positive impact on EPI (models (2) and (5)), which becomes negative when the FEM technique is used to estimate the complex model (model (6)).

Table 4a. Regression results for sustainable development measured by EPI as a function of corporate governance measured by CB, SAR, Internet and other control variables, for high income countries.

b, 3 b, and 4 b show the regression results for sustainable development measured by HDI, HCI, and EPI as a function of corporate governance measured by BE, SAR, Internet, and the other control variables for the group of low-income countries. shows the estimated impact of BE (models (1)–(3)), SAR (models (4)–(6)), and Internet (models (7)–(9)) on HDI; estimates their impact on HCI; and evaluates the corporate governance determinants of EPI for the subsample of 128 low-income countries.

Table 2b. Regression results for sustainable development measured by HDI as a function of corporate governance measured by CB, SAR, Internet and other controls variables, for low income countries.

Table 3b. Regression results for sustainable development measured by HCI as a function of corporate governance measured by CB, SAR, Internet and other control variables, for low income countries.

Table 4b. Regression results for sustainable development measured by EPI as a function of corporate governance measured by CB, SAR, Internet and other control variables, for the low income countries.

In , when significant, BE, SAR, and Internet are positively correlated with HDI. Of the public governance quality indicators, VA (model (2)), RQ (models (5) and (6)), and GE (models (8) and (9)) are found to be determinants of HDI. Of the cultural variables, in contrast to high-income countries, IDV exerts a positive impact on HDI (models (2), (3), and (8)); UAI also has a positive influence on HDI (models (2), (3), and (8)), as does LTO (model (2)). Urbanisation is directly related to HDI (models (5) and (6) as well as models (8) and (9)), while the coefficient of unemployment is negative and significant in model (8).

shows the estimated impact of BE, SAR, and Internet on HCI for the subsample of low-income countries. The corporate governance proxies have a positive impact on HCI. These models also validate PS as an HCI determinant, with a positive impact (models (2) and (3) as well as models (8) and (9)), while none of the six governance proxies are validated in models (5) and (6). Of the cultural variables, PD exerts a positive impact on HCI (models (2) and (5)), as do UAI (models (2), (3), (5), (8), and (9)) and LTO (models (2) and (5)). IND has a negative impact in model (8). Urbanisation is not validated as an explanatory variable of HCI, while unemployment has a negative impact on HCI (models (2) and (3), (5) and (6), and (8) and (9)).

estimates the impact of BE (models (1)–(3)), SAR (models (4)–(6)), and Internet (models (7)–(9)) on EPI for the subsample of low-income countries. Their impact is positive, and most of the coefficients are significant at the 1% level. Of the governance proxies, RQ (models (2) and (3) as well as models (5) and (6)) and PS (models (8) and (9)) provide the highest explanatory power, whereas the positive impact of RQ is not robust to the estimation technique. The positive impact of PD, as opposed to in high-income countries, is present in models (2) and (5). MAS and UAI both have a positive impact in models (2), (5), and (8), while the impact of IND is negative (models (2) and (8)). Unemployment has a positive impact on EPI (models (2), (3), and (5)).

4.2. Robustness checks

To check the robustness of our main results, we perform a battery of robustness tests. First, we use another proxy for our dependent variable of sustainable development, namely, the happiness index (Happy); the results are in . Second, we use three other proxies for our main independent variable of corporate governance, namely, women in top management positions (FM) and female ownership (FO), and measure digitalisation by technology adoption (TA), with the results shown in . Table A in Appendix A describes the variables. Our robustness checks mostly support the strength of our main results. Specifically, we find that an improved level of corporate governance, expressed as greater gender diversity, leads to a higher level of sustainable development. In addition, as the level of technology adoption increases, the level of sustainable development rises.

Table 5. Regression results for sustainable development measured by Happy as a function of corporate governance measured by CB, SAR, Internet and other control variables.

Table 6. Regression results for sustainable development measured by HDI, HCI and EPI as a function of corporate governance measured by FO, FM and TA and other control variables.

5. Discussions

Our research examines whether higher corporate governance increases sustainable development using a variety of proxy indicators. For the full sample, about 9.6% of the variation in HDI is explained by board efficacy, whereas 25.3% is explained by the quality of audits and reports. By contrast, board efficacy and the quality of audits and reports explain relatively more of the variation in HCI (20.6% and 31.7%, respectively). EPI is also positively and significantly impacted by board efficacy and the quality of audits and reports (18.66% and 31.89%, respectively). Among the three main proxies of corporate governance (BE, SAR, and Internet), Internet has the largest impact on sustainable development, in line with the results of Dienes et al. (Citation2016) and De Luca (Citation2020), who found a positive impact of corporate governance on sustainable development. More precisely, they show that some elements of corporate governance quality, such as the structure of property and structure and size of corporate governance, along with other economic and institutional factors, represent the foundation for sustainable development.

The results differ when analyzing the two subgroups of countries classified according to their level of development,. We estimate higher regression coefficients of BE, SAR, and Internet for the regressions of sustainable development conducted in low-income countries than in high-income countries. Thus, the intensity of the way in which high-quality corporate governance impacts sustainable development is higher in low-income countries than in high-income countries. A one-unit increase in corporate governance determines higher increases in the level of sustainable development in low-income countries than in high-income countries. In other words, the marginal effects of corporate governance on sustainable development are higher in low-income countries.

Regarding the control variables, public governance exerts a significant positive influence on sustainable development in all countries irrespective of their development level, meaning that increasing the quality of public governance provides higher-quality public services in the form of health care, education, and security services. These results are in line with those of Hoinaru et al. (Citation2020), Absalyamova et al. (Citation2016), and Forson et al. (Citation2017), who also found that high-quality public governance influences societal development, in terms of both the economic and the sustainable dimensions.

Our findings also indicate that culture influences sustainable development, in line with earlier studies (UNESCO, Citation2012). We find that lower power distance, higher individualism, higher masculinity, higher uncertainty avoidance, higher long-term orientation, and lower restraint increase sustainable development. The estimated coefficients of Hofstede’s cultural dimensions are typically higher in low-income countries than in high-income countries, suggesting that culture exerts a greater influence on sustainable development in low-income countries. In addition, the influence of power distance on sustainable development differs between the two groups of countries, with positive (negative) coefficients for low-income (high-income) countries. High power distance, which generally characterises low-income countries (see ), means that there is greater acceptance that the less powerful members of society must accept and expect power to be distributed unequally. This high degree of accepting inequality could be a channel for obtaining high short-term benefits in the form of bribes for contracting or avoiding paying taxes. Thus, higher power distance increases sustainable development in low-income countries. Indeed, previous studies support the ‘grease the wheels’ theory by documenting a positive effect of corruption and the shadow economy on the economic and sustainable development of countries (Hoinaru et al., Citation2020; Zaman & Goschin, Citation2015), especially low-income countries.

Urbanisation has a positive influence on sustainable development. This result is in line with the studies of Satterthwaite (Citation2008), Rogers et al. (Citation2012), and Zeng et al. (Citation2016), who found that urbanisation is crucial to regional and global sustainability. Indeed, our results also concur with those of the United Nations (Citation2014) and Picatoste and Rodriguez-Crespo (Citation2020), who showed that unemployment, especially among young men, is a major threat to sustainable development. Similarly, we find that higher unemployment decreases sustainable development in the low-income subsample, while mixed results are obtained for the full sample.

6. Conclusions

This study investigated the influence of corporate governance on sustainable development using a panel linear regression model applied to a sample of 185 countries over 2005–2020. Separate analyses were also conducted for high- and low-income countries. Our findings highlight the positive influence of corporate governance on sustainable development measured by the HDI, HCI, and EPI. In addition, we find a higher positive and marginal effect of the influence of corporate governance on sustainable development for low-income countries than for high-income countries.

Further, we find that high-quality public governance, a high level of urbanisation, and low unemployment increase sustainable development. Culture impacts the sustainable development of a society markedly for both high- and low-income countries, but this effect is particularly high in the latter. The robustness checks performed using the supplementary variables of the happiness index, women in top management positions, and technology adoption verify our results.

Our results have both theoretical and practical implications. Theoretically, our finding of a direct relationship between corporate governance and sustainable development may create new research directions. The practical implications of the findings include showing that the quality of corporate governance directly affects sustainable development, which could help policymakers better manage this relationship. Thus, adopting more best practices in corporate governance raises the sustainable development in a society. Managers and policymakers should be interested in the continuous supervision and boosting of this relationship. Corporate governance practices may therefore be used as leverage to boost sustainable development, which is desirable. The continuous development of corporate governance proxies such as those tested in our large sample increases human development and raises environmental performance.

The limitations of this study may include the ways of measuring the level of corporate governance using macroeconomic proxies. Future studies should adopt a microeconomic view by analyzing this relationship in a sample of companies from different countries. Furthermore, a multivariate data analysis approach could be adopted, including using lagged variables and interaction terms.

Additional information

Funding

References

- Absalyamova, S., Absalyamov, T., Khusnullova, A., & Mukhametgalieva, C. (2016). The impact of corruption on the sustainable development of human capital [Paper presentation]. Journal of Physics: Conference Series, Volume 738, 5th International Conference on Mathematical Modeling in Physical Sciences, Athens, Greece. (IC-MSquare 2016) 23–26, May 2016

- Achim, M. V., Borea, N. S., & Miron, G. M. (2017). Corporate governance, corporate social responsibility and business performances. A global perspective. Economica, 2(100), 1–9.

- Achim, M. V., & Borlea, N. S. (2020). Economic and financial crime. Corruption, shadow economy, and money laundering. Switzerland AG: Springer Nature. https://doi.org/10.1007/978-3-030-51780-9

- Achim, M. V., Borlea, S. N., & Văidean, V. L. (2021). Does technology matter for combating economic and financial crime? A panel data study. Technological and Economic Development of Economy, 27(1), 223–261. https://doi.org/10.3846/tede.2021.13977

- Adams, C. (2017). Understanding integrated reporting: The concise guide to integrated thinking and the future of corporate reporting. Routledge. https://doi.org/10.4324/9781351275002

- Aguilera, R., Rupp, D. & Ganapathi, J. (2007) Putting the S back in corporate social responsibility: A multilevel theory of social change in organizations. Academy of Management Review, 32, 836–863.

- Baumann-Pauly, D., Wickert, C., Spence, L. J., & Scherer, A. G. (2013). Organizing corporate social responsibility in small and large firms: Size matters. Journal of Business Ethics, 115(4), 693–705. https://link.springer.com/article/10.1007%2Fs10551-013-1827-7. https://doi.org/10.1007/s10551-013-1827-7

- Calabrese, A., Costa, R., Ghiron, N. L., & Menichini, T. (2017). Materiality analysis in sustainability reporting: a method for making it work in practice. European Journal of Sustainable Development, 6(3), 439–439. https://doi.org/10.14207/ejsd.2017.v6n3p439

- Chan, M. C., Watson, J., & Woodliff, D. (2014). Corporate Governance Quality and CSR Disclosures. Journal of Business Ethics, 125(1), 59–73. https://doi.org/10.1007/s10551-013-1887-8[Mismatch] AQ6]

- Coffie, W., Aboagye-Otchere, F., & Musah, A. (2018). Corporate social responsibility disclosures (CSRD), corporate governance and the degree of multinational activities: Evidence from a developing economy. Journal of Accounting in Emerging Economies, 8(1), 106–123. https://doi.org/10.1108/JAEE-01-2017-0004

- Crane, A., & Matten, D. (2007). Business Ethics: Managing corporate citizenship and sustainability in the age of globalization. Oxford University Press.

- De Luca, F. (2020). Mandatory and discretional non-financial disclosure after the European Directive 2014/95/EU: An empirical analysis of Italian listed companies' behavior. Emerald Publishing Limited, Bingley. https://doi.org/10.1108/9781839825040

- Dienes, D., Sassen, R., & Fischer, J. (2016). What are the drivers of sustainability reporting? A systematic review. Sustainability Accounting, Management and Policy Journal, 7(2), 154–189. https://doi.org/10.1108/SAMPJ-08-2014-0050

- Emerson, J. W., Hsu, A., Levy, M. A., de Sherbinin, A., Mara, V., Esty, D. C., & Jaiteh, M. (2012). Environmental performance index and pilot trend environmental performance index. Yale Center for Environmental Law and Policy. http://epi.yale.edu.

- Esty, D., Levy, M. A., Kim, C. H., de Sherbinin, A., Srebotnjak, T., & Mara, V. (2008). Environmental performance index. Yale Center for Environmental Law and Policy.

- Fahad, P., & Mubarak, R. P. (2020). Impact of corporate governance on CSR disclosure. International Journal of Disclosure and Governance, 17(2), 155–167. https://doi.org/10.1057/s41310-020-00082-1.

- Fatemi, A., Glaum, M., & Kaiser, S. (2018). ESG performance and firm value: The moderating role of disclosure. Global Finance Journal, 38, 45–64. https://doi.org/10.1016/j.gfj.2017.03.001

- Forson, J. A., Buracom, P., Chen, G., & Baah-Ennumh, T. Y. (2017). Genuine wealth per capita as a measure of sustainability and the negative impact of corruption on sustainable growth in Sub-Sahara Africa. South Africa Journal of Economics, 85(2), 178–195. https://doi.org/10.1111/saje.12152

- Flammer, C. (2015). Does corporate social responsibility lead to superior financial performance? A regression discontinuity approach. Management Science, 61(11), 2549–2824. https://doi.org/10.1287/mnsc.2014.2038

- Fréminville, M. d. (2020). Corporate governance and digital responsibility. In M. de Fréminville, Cybersecurity and decision makers: Data security and digital trust (pp. 39–68). John Wiley & Sons. https://doi.org/10.1002/9781119720362ch2

- Gallego-Álvarez, I., & Pucheta-Martínez, M. C. (2021). Hofstede’s cultural dimensions and R&D intensity as an innovation strategy: a view from different institutional contexts. Eurasian Business Review, 11(2), 191–220. https://doi.org/10.1007/s40821-020-00168-4

- Gallego-Alvarez, I., Vicente-Galindo, M., Galindo-Villardón, M., & Rodríguez-Rosa, M. (2014). Environmental performance in countries worldwide: Determinant factors and multivariate analysis. Sustainability, 6(11)2014, 7807–7832. 10.3390/su6117807

- Gardberg, N. A., & Fombrun, C. J. (2006). Corporate citizenship: Creating intangible assets across institutional environments. Academy of Management Review, 31(2), 329–346. https://doi.org/10.5465/amr.2006.20208684

- Gernon, H., & Gary, K. M. (2000). Accounting: An international perspective. MBEraw-Hill.

- Habbash, M. (2016). Corporate governance and corporate social responsibility disclosure: Evidence from Saudi Arabia. Social Responsibility Journal, 12(4), 740–754. 10.1108/SRJ-07-2015-0088

- Hashanah, I., & Mazlina, M. (2005). PN9/2001: Case of public reprimands. Presented at FEP Seminar, 2005

- Hofstede Centre (2022). Available at http://geert-hofstede.com.

- Hoinaru, R., Buda, D., Borlea, S. N., Văidean, V. L., & Achim, M. V. (2020). The impact of corruption and shadow economy on the economic and sustainable development. Do They “Sand the Wheels” or “Grease the Wheels”? Sustainability, 12(2), 481. https://doi.org/10.3390/su12020481

- Howell, K. E., & Sorour, M. K. (2016). Corporate governance in Africa: assessing implementation and ethical perspectives. Palgrave Macmillan, London.

- Husser, J., Andre, J.-M., Barbat, G., & Lespinet-N, V. (2012). CSR and sustainable development: are the concepts compatible? Management of Environmental Quality. An International Journal, 23(6)2012 pp., 658–672.

- Jamali, D., Safieddine, A. M., & Rabbath, M. (2008). Corporate Governance and Corporate Social Responsibility Synergies and Interrelationships. Journal Compilation, 16(5), 443–459.

- Kim, D., & Go, S. (2020). Human Capital and Environmental Sustainability. Sustainability, 12(11), 4736. https://doi.org/10.3390/su12114736

- Kahraman Akdogu, S. (2017). The Link Between CSR and Sustainable Development in a Global Economy. In S. Vertigans &S. Idowu (Eds.), Corporate social responsibility. CSR, sustainability, ethics & governance. Springer. https://doi.org/10.1007/978-3-319-35083-7_13

- Kolk, A., & Pinkse, J. (2010). The integration of corporate governance in corporate social responsibility disclosure. Corporate Social Responsibility and Environmental Management, 17(1), 15–26.

- Kong, D. (2013). Does corporate social responsibility affect the participation of minority shareholders in corporate governance? Journal of Business Economics and Management, 14(Supplement_1), S168–S187. , https://doi.org/10.3846/16111699.2012.711365

- Mirza, N., Rahat, B., Naqvi, B., & Rizvi, S. K. A. (2020). Impact of Covid-19 on corporate solvency and possible policy responses in the EU. The Quarterly Review of Economics and Finance,https://doi.org/10.1016/j.qref.2020.09.002

- Murshed, M., & Mredula, F. A. (2018). Impacts of corruption on sustainable development: a simultaneous equations model estimation approach. Journal of Accounting, Finance and Economics, 8(1), 109–133.

- Nedelchev, M. (2013). Good practices in corporate governance: one-size-fits-all vs. Comply-or-explain. International Journal of Business Administration, 4(6), 75–81. https://doi.org/10.5430/ijba.v4n6p75

- Picatoste, X., & Rodriguez-Crespo, E. (2020). Decreasing youth unemployment as a way to achieve sustainable development. In W. Leal Filho, A. M. Azul, L. Brandli, A. Lange Salvia, & T. Wall (Eds.), Decent work and economic growth. Encyclopedia of the UN sustainable development goals. Springer.

- Rogers, D. S., Duraiappah, A. K., Antons, D. C., Munoz, P., Bai, X., Fragkias, M., & Gutscher, H. (2012). A vision for human well-being: transition to social sustainability. Current Opinion in Environmental Sustainability, 4(1), 61–73. https://doi.org/10.1016/j.cosust.2012.01.013

- Salvioni, D. M., & Bosetti, L. (2014). Sustainable Development and Corporate Communication in Global Markets. Symphonya. Emerging Issues in Management, (1), 32–51. https://doi.org/10.4468/2014.1.03salvioni.bosetti

- Salvioni, D. M., & Gennari, F. (2019). Stakeholder Perspective of Corporate Governance and CSR Committees. Symphonya. Emerging Issues in Management, (1), 28–39. https://doi.org/10.4468/2019.1.03salvioni.gennari

- Satterthwaite, D. (2008). Urbanization and sustainable development. Available at https://www.un.org/en/development/desa/population/pdf/commission/2008/keynote/satterthwaite-text.pdf.

- Spitzeck, H. (2009). The development of governance structures for corporate responsibility. Corporate Governance: The International Journal of Business in Society, 9(4), 495–505. https://doi.org/10.1108/14720700910985034

- Tricor Group. (2020). Available at https://www.tricorglobal.com/blog/digital-corporate-governance-a-strategic-step-towards-building-forward-thinking-organizations. Accessed on December 26 2021.

- Truant, E., Corazza, L., & Scagnelli, S. D. (2017). Sustainability and risk disclosure: An exploratory study on sustainability reports. Sustainability, 9(4), 636. https://doi.org/10.3390/su9040636

- Ullah, M., Muttakin, M., & Khan, A. (2019). Corporate governance and corporate social responsibility disclosures in insurance companies. International Journal of Accounting & Information Management, 27(2), 284–300. 10.1108/IJAIM-10-2017-0120

- UNDP (2022)/Human Development Reports. (2022). UNDP (2022)/Human Development Reports. Available online: http://hdr.undp.org

- UNESCO. (2012). Culture: a driver and an enabler of sustainable development Thematic Think Piece UNESCO. Available at: https://www.un.org/millenniumgoals/pdf/Think%20Pieces/2_culture.pdf. Accessed on January 17th 2022.

- United Nations. (1987). World commission on environment and development. our common future (pp. 27). Oxford University Press. Human Development Reports. http://hdr.undp.org.

- United Nations. (2014). Sustainable development through decent jobs for youth, 29 July 2014

- United Nations. (2015). The UN 2030 Agenda for Sustainable Development, 21 October 2015.

- Waddock, S. A., & Graves, S. B. (1997). The corporate social performance-financial performance link. Strategic Management Journal, 18, 303–319.

- Welford, R. (2007). Corporate governance and corporate social responsibility: Issues for Asia. Corporate Social Responsibility and Environmental Management, 14(1), 42–51. https://doi.org/10.1002/csr.139

- Yale University. (2022). Environmental performance index. https://epi.envirocenter.yale.edu

- Zaman, G., & Goschin, Z. (2015). Shadow economy and economic growth in Romania. Cons and pros. Procedia Economics and Finance, 22, 80–87. https://doi.org/10.1016/S2212-5671(15)00229-4

- Zeng, C., Deng, X., Dong, J., & Hu, P. (2016). Urbanization and sustainability: Comparison of the processes in “BIC” countries. Sustainability, 8(4), 400. https://doi.org/10.3390/su8040400

- Zingales, L., Guiso, L., & Sapienza, P. (2016). The values of corporate culture. Journal of Financial Economics, 117(1), 60–76.