?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study is aimed to investigate the effects of the trade policy uncertainty (T.P.U.) on the trade flow of 113 emerging economies and low-income developing countries to 143 destination countries. It further investigates the effects of T.P.U. based on income heterogeneity. Moreover, it considers the effects of T.P.U. on trade flow between developing countries’ pair and non-manufacture trade. The two-step Heckman sample selection model is applied to run the structural gravity model of trade using three-year intervals for the period 2004–2019. The analysis is repeated using the Poisson pseudo-maximum likelihood (P.P.M.L.) model for the robustness test. The results imply that the extensive and intensive margin of trade flow of emerging economies and low-income developing countries are adversely affected by the T.P.U. of destination countries. However, the T.P.U. of origin has an adverse effect on the extensive margin of trade. It also negatively affects the trade flow between developing-developing pairs. We also conduct a counterfactual simulation analysis to convert the effect of T.P.U. on trade flow to distance equivalent. To sum up, the findings of this study imply that T.P.U. is a more important barrier to trade for emerging economies and low-income developing countries. Policy implications are forwarded based on the findings.

1. Introduction

Trade policy uncertainty (T.P.U.) is pervasive in the world trade system, and the potential for trade wars seems to happen. Trade negotiations for a new approach to trade policy have become the focus of increased attention among politicians, investors, and market participants (Caldara et al., Citation2019). The global economy has faced several policy uncertainties in the last two decades. For example, the U.S. trade protection and withdrawal from the Trans-Pacific Partnership (T.P.P.), tariff hikes on U.S. steel and aluminum imports, the new trade agreement renegotiations of U.S. (Robinson & Thierfelder, Citation2019), economic depression and financial crises, Brexit, European regulation and trade, and the reduction of and blocking new appointments of Appellate Body of the World Trade Organization (W.T.O.) (Bekkers, Citation2019), global trade disputes and escalating U.S.–China trade tensions (Yang & Nie, Citation2020) have occurred in the last two decades.

Several studies have revealed that policy uncertainty significantly affects economic activities and has an adverse or positive effect on all economic systems. The studies have been conducted mainly concerning the effects of policy uncertainties on economic activities (Caldara et al., Citation2019), inflation (Jones & Olson, Citation2013), oil prices (Hoque et al., Citation2019), the stock market (Hua et al., Citation2020), and investment (Rashid et al., Citation2021; Ebeke & Siminitz, Citation2018; Yan & Shi, Citation2021).

The change of T.P.U. and the subsequent magnitude of those changes on countries’ trade performance are uncertain. Thus, the relationship between T.P.U. and trade performance is unclear and inconclusive. Some studies propose that the relationship between T.P.U. and trade is robustly negative, implying that T.P.U. has an adverse effect on countries’ trade performance (Dixit & Pindyck, Citation1994; Handley, Citation2014; Handley & Limão, Citation2015; Scheffel, Citation2016; Krol, Citation2018; Crowley et al., Citation2018; Greenland et al., Citation2019; Novy & Taylor, Citation2020). The risk of a trade policy reversal acts as a fixed cost to enter the export market and negatively impacts the extensive margin of trade (Handley, Citation2014). Likewise, Crowley et al. (Citation2018) and Handley and Limão (Citation2015) indicate that investment decision and entry into international trade and export markets is reduced when T.P.U. is high. Thus, the effects of unexpected changes in T.P.U. are adverse on investment and trade performances (Caldara et al., Citation2019).

On the other hand, some scholars argue that uncertainty may encourage investment and promote countries’ trade performance. For example, based on the growth option theory, Bar-Ilan and Strange (Citation1996) indicated that uncertainty is positively associated with investment and investment decisions and thus encourages trade flows and the probability of entering foreign trade. Likewise, Abel (Citation1983) and Hartman (Citation1972) argue that risk-averse firms have the flexibility to change production in line with elevated uncertainty and take more risk and increase investment to compensate for the loss caused by increased uncertainty which may, in turn, promote the intensive and extensive margins of trade.

Furthermore, policy uncertainty will also affect the extensive margin trade. Handley and Limão (Citation2015) revealed that with sunk costs of trade in which firms make entry and trade decisions, policy uncertainty limits firms’ entry into foreign trade. Moreover, it may adversely affect trade by impacting the future expectations of the firms. Thus, they adjust their trade plans and reduce trade-related investments affecting the probability to trade.

Even though some studies have investigated the relationship between T.P.U. and the trade performance of countries, they mainly focused on developed countries and a few emerging markets (Greenland et al., Citation2019; Handley, Citation2014; Crowley et al., Citation2018; Handley & Limão, Citation2015). The empirical studies regarding the effects of T.P.U. on the trade flow of emerging economies and low-income developing countries are scarce though the average level of uncertainty is higher in developing economies than in advanced economies (Ahir et al., Citation2020).

Therefore, this article aims to investigate the effects of the T.P.U. on the trade flow of 113 emerging economies and low-income developing countries by applying the two-step Heckman sample selection procedure of the structural gravity specification utilising three-year intervals data for the periods 2004–2019. The exercise is repeated by classifying countries based on income heterogeneity. Besides, further analysis is conducted to investigate the effects of T.P.U. on non-manufacture export and developing-to-developing country pairs.

This study fills the gaps in the existing literature on the impact of T.P.U. on trade flow in several ways. First, this study is the first in its kind to investigate the effects of T.P.U. on the trade flow of emerging economies and low-income developing countries, which is relatively an under-researched area. Second, it has also repeated the analysis based on income heterogeneity. Third, this study includes the effects of T.P.U. of destination countries because the trade flow of the origin country cannot only be affected by T.P.U. of itself but it can also be affected by the T.P.U. of the destination countries. Fourth, this study investigates the effects of T.P.U. on the non-manufacture trade of countries. Fifth, we employ the two-step Heckman model to control sample selection bias and examine the intensive and extensive margin of trade. Sixth, for robustness analysis, the Poisson pseudo-maximum likelihood (P.P.M.L.) estimator is used to solve zero-valued observations and heteroscedasticity concerns. Finally, we conduct a counterfactual simulation analysis to convert the effect of T.P.U. on trade flow to illustrative distance equivalent.

The remaining sections of this study are organised as follows. Section two presents the literature review. Section three discusses the data and methodology of the study. Section four provides the results and findings of the study. Section five provides a robustness check or sensitivity analysis. Section six presents discussions and policy implications.

2. Literature review

Regarding the theoretical literature, there are several strands of studies that investigate the relationship between the T.P.U. on trade flow (Abel, Citation1983; Hartman, Citation1972; Bernanke, Citation1983; Dixit & Pindyck, Citation1994; Bar-Ilan & Strange, Citation1996; Handley, Citation2014; Wang et al., Citation2014; Handley & Limão, Citation2017; Tam, Citation2018). However, they have generated contradictory predictions about the relationship. Thus, the theoretical basis of the relationship between T.P.U. and trade flow shows an unresolved puzzle in the relationship.

On the one hand, the changes in trade policies can impact trade negatively, implying that high T.P.U. has an adverse effect on trade performance. For example, the real option value theory indicates that policy uncertainty creates a real option value of waiting (Bernanke, Citation1983), i.e., if the export value is not less than the value of the holding option, the exporting firm executes the option and begins to export (Dixit & Pindyck, Citation1994). Conversely, when the policy uncertainty is high, the value of the option to invest in the future increases, delaying the decision to invest.

This theory was also supported by Wang et al. (Citation2014), Krol (Citation2018) and Novy and Taylor (Citation2020), that provide evidence that exporting firms cut investments in existing markets while delaying new markets when there are high policy uncertainties. Therefore, for prospective firms, uncertainty about future prices and consumer demand can serve as a barrier to entry and limit the extensive margins of trade.

Consistent with real options theory, the theoretical framework developed by Handley (Citation2014) and Handley and Limão (Citation2015) suggests that an increase in policy uncertainties encourages firms to postpone entry to the market to avoid paying sunk entry costs. Therefore, according to these theories, policy uncertainty can be considered as one of the major factors that affect economic activity and trade adversely (Scheffel, Citation2016).

On the other hand, some theoretical literature argues that there is a positive relationship between policy uncertainty and trade. For example, the classical theory of Qi-Hartman-Abel claims that policy uncertainty positively contributes to the trade performance of countries because risk-averse firms will take more risk and increase investment to compensate for the loss due to high uncertainty (Hartman, Citation1972), which will positively contribute to trade. Furthermore, the growth option theory provides evidence that policy uncertainty is positively associated with investment (Bar-Ilan & Strange, Citation1996), positively affecting trade. This theory is consistent with the Qi-Hartman-Abel theory that suggests risk-averse firms take more risk and increase investment to compensate for the loss due to high uncertainty (Abel, Citation1983).

Therefore, based on these theoretical bases, some empirical studies have examined the effects of T.P.U. on trade performance, even though they were limited to a few developed countries. For example, Jaaskela and Mathews (Citation2015) imply that the effect of uncertainty on investment affects global trade and explains the recent slowdown in global trade. Moreover, Handley (Citation2014) and Handley and Limão (Citation2015) show that uncertainty severely affects firms exporting behavior. Their findings predict that when market entry costs are sunk, T.P.U. will create a real option value of waiting to enter export markets until the uncertainty is resolved. Similarly, Handley and Limão (Citation2017) demonstrate that the decline in T.P.U. in Sino-U.S. trade has increased the willingness of Chinese firms to enter the export market. Likewise, Imbruno (Citation2019) provided evidence that lower T.P.U. allows access to import more high-quality foreign goods. Also, Lindé and Pescatori (Citation2019) argue that trade wars can lead to permanently lower trade volumes.

Furthermore, Alberto et al. (Citation2018) investigate the effects of T.P.U. on the extensive and intensive margins of trade, and their results show that T.P.U. is an important barrier to exports. Besides, Greenland et al. (Citation2019) indicate that increases in policy uncertainty decrease both trade values and the extensive margin. Additionally, Crowley et al. (Citation2018) show that firms are less likely to enter new markets and more likely to exit the existing markets when policy uncertainty is high. Regarding the effects of T.P.U. on investment, Caldara et al. (Citation2019) reveal that increases in T.P.U. reduce business investment. Likewise, Ebeke and Siminitz (Citation2018) show a negative relationship between the T.P.U. and investment. Finally, a study by Liao et al. (Citation2021) implies that perceived macroeconomic uncertainty has a significant negative impact on trade flow.

In general, the impacts of policy uncertainty on the economic performance of countries are a prime focus in the empirical and theoretical literature and policy frameworks. Despite the contradictory theoretical predictions of the relationship between T.P.U. and trade flow, empirical studies have indicated a negative relationship between policy uncertainty and trade flows (Handley & Limão, Citation2017; Tam, Citation2018; Handley & Limão, Citation2017; Lindé & Pescatori, Citation2019; Greenland et al., Citation2019; Crowley et al., Citation2018; Caldara et al., Citation2019; Alberto et al., Citation2018). However, limited empirical studies have been conducted on the impacts of T.P.U. on the trade performance of emerging and low-income developing economies. The studies conducted so far are limited to developed countries even though the average level of uncertainty is higher in developing economies than in advanced economies (see in Appendix B).

3. Methodology and data

3.1. Method of analysis

The structural gravity model is applied using the Heckman (Citation1979) two-step sample selection procedure to accommodate zero-valued observations and sample selection bias. Theoretically, this model includes two equations: one focusing on selection into the sample (extensive margin) and the outcome (intensive margin). Thus, it permits a two-stage decision process via estimating determinants of the extensive margin simultaneously with estimating the intensive margin, avoiding any bias involved because of sample selection and omission of the extensive margin (Helpman et al., Citation2008). Thus, the following outcome equation characterises the volume of trade conditioned on trade taking place.

(1)

(1)

Where X' is vectors of independent variables, i is the origin, j is the destination, and t is time. Finally, γ is the normally distributed error term, β is the primary parameter vector.

The outcome model in EquationEquation (1)(1)

(1) can be modified as follows to retain the Inverse Mills ratio (

):

(2)

(2)

Where tradeijt is the size of pre-existing trade, Xijt explanatory variables influencing the size of existing trade and β and γijt indicate parameters and stochastic terms, respectively.

Therefore, based on the above theoretical foundation of the intensive margin of two-step Heckman (Citation1979), the outcome equation of our study is developed in EquationEquation (3)(3)

(3) .

(3)

(3)

Tradeijt denotes bilateral trade flow between i and j countries. Cijt represents control variables such as the logarithm form of the real G.D.P. per capita of origin and destination countries, the logarithm form of the population size of the origin and destination countries, and W.T.O. membership, the distance between capital of i and j countries, colonial relationship, contiguity, common language, and regional trade agreement (R.T.A.). TPUtt represents T.P.U. of the origin, TPUjt is T.P.U. of the destination, and MRTijt is the inverse Mills ratio, δit is exporter-time fixed effects and δjt importer-time fixed effects and γijt shows the stochastic term.

The outcome equation in EquationEquation (2)(2)

(2) will be observed based on the extensive margin, which can be stated as follows:

(4)

(4)

(5)

(5)

Where Selection* is unobserved trade, z’ is vectors of predictor variables, i is the origin, j is the destination, and t is time. Besides, κ is normally distributed error terms, β is the primary parameter vector of interest.

Actual trade will exist if the selection propensity (Selection) in EquationEquation (5)(5)

(5) exceeds zero. That is Selection* > 0 when i export to j and Selection* = 0 when it does not. Therefore, the extensive margin of this study in EquationEquation (6)

(6)

(6) is used to control the T.P.U. of the origin and destination countries based on the theoretical gravity specifications defined in EquationEquations (4)

(4)

(4) and Equation(5)

(5)

(5) . Therefore, the extensive margin of this study shows that Tradeijt defined in EquationEquation (3)

(3)

(3) is observed when the following condition is satisfied:

(6)

(6)

Where businessit denotes business entry cost and δit and δit are exporter-time fixed effects and importer-time fixed effects, respectively. µijt is the stochastic term.

Business entry cost is used as an exclusion restriction in EquationEquation (6)(6)

(6) following the works of Helpman et al. (Citation2008) and Yushi and Borojo (Citation2019). It is excluded from the outcome EquationEquation (3)

(3)

(3) and included in the selection EquationEquation (6)

(6)

(6) as it affects fixed trade costs but does not affect variable trade costs. Therefore, it satisfies the exclusion restriction. Based on this theoretical foundation, we applied Principal component analysis to develop an index of entry cost using cost to start the business per G.D.P., procedure, and time to start a business in origin countries. The eigenvalue of the first component is greater than one and has a variance of 1.88, explaining 63% of the total variance. Hence we include the first component of the business entry indicator in our analysis (see ).

Table 2. The effects of T.P.U. on trade flow based on income heterogeneity.

3.2. Data

Data for this study is utilised from different sources. The T.P.U. index has been retrieved from the Economics Intelligence Unit (E.I.U.) reports for 143 countries. The index captures the quarterly average frequency of uncertainty related to trade policy developed by Ahir et al. (Citation2018) and reported in the E.I.U. report. A high index means greater levels of T.P.U. and vice versa. Moreover, annual data for T.P.U. is computed taking averages of quarterly data for T.P.U. following the works of Saleem et al. (Citation2018). Trade flow data was derived from the U.N. Comtrade database. The trends of T.P.U. and trade performance of countries are indicated in in Appendix B. The origin and destination countries’ real per capita G.D.P. and population were gathered from World Development Indicators (W.D.I.) databases. Business entry indicators were taken from World Bank doing business database. Bilateral distance, R.T.A., W.T.O. membership, contiguity, colonial relationship, and common language between origin and destination countries were derived from the C.E.P.I.I. database. The list of sample countries included in this study (113 emerging and low-income developing countries and 143 destination countries) is reported in Appendix A. Also, summary statistics of the variables is reported in .

Table 1. The impacts of T.P.U. on trade (baseline).

The adjustment of trade flow in response to policy changes will not be visible immediately. Thus, estimation applied to data pooled over consecutive years is criticised because independent and dependent variables cannot fully adjust in a single year’s time (Cheng & Wall, Citation2005). In other words, the estimations performed with panel samples pooled over consecutive years produce suspicious results of the trade cost elasticity parameters (Anderson & Yotov, Citation2016; Yotov et al., Citation2016; Borojo et al., Citation2021). Therefore, it is recommended to use panel data with intervals instead of data pooled over consecutive years. Therefore, we used three-year intervals except for the last interval (2004, 2007, 2011, 2014, 2017 and 2019), following the recommendations of Anderson and Yotov (Citation2016) and Borojo et al. (Citation2021).

4. Results and findings

4.1. The impacts of trade policy uncertainty on the trade flow of emerging and low-income developing economies

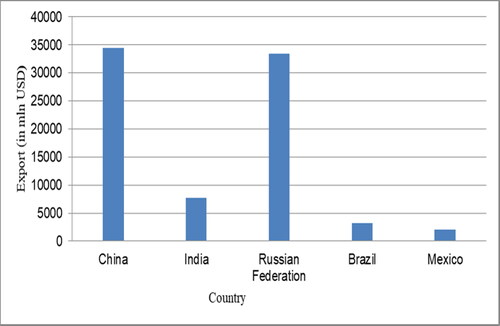

reports the impacts of T.P.U. on extensive and intensive margins of trade. In Column (I) whole sample of emerging economies and low-income developing countries is considered. The exercise is repeated in Column (II), excluding China and Russia from the sample because they are among the top exporters from emerging economies ( in Appendix C). China is among the top exporters of manufactured goods globally (World Trade Organization, Citation2019) and, to some extent Russia. Besides, China possessed comparative advantages in manufactured and processed products (Maryam et al., Citation2018). Likewise, China has done exceptionally well in the last two decades among all emerging economies in agricultural exports. Its agricultural export constituted 35% of the emerging market exports (Chaturvedi, Citation2019).

The coefficients of the Inverse Mills ratio are negative and significant in all specifications, signifying that O.L.S. would produce downwardly biased estimates, and the selection problem is apparent in the models. The coefficients of the standard gravity variables are in line with the trade theories and empirical studies. The effects of the population size of origin and destination countries on the intensive and extensive margins of trade are significantly positive. The impacts of real G.D.P. per capita of the origin and destination countries are robustly positive, implying that the economic size of exporting and partner countries’ economies considerably determines the countries’ export performance.

Besides, the effect of the physical distance between the origin and their trade partners on the extensive and intensive margin of trade is statistically significant and negative, revealing that physical distance discourages the countries’ export performance. Besides, contiguity has a robustly positive effect on intensive and extensive trade margins, implying that countries with a common boundary trade more than countries with no common boundary.

Also, the impacts of colonial relationships on trade volume are significantly positive, implying that countries with colonial relationships trade more than countries with no colonial relationship. Similarly, the coefficient of a common language has a significantly positive effect on intensive and extensive margins of trade, implying that countries speaking common language trade. Also, the W.T.O. membership of origin and destination countries has a significant positive effect on the intensive and extensive margins of trade. Finally, R.T.A.s have a robustly positive effect on trade volume and probability of trade in all specifications.

Regarding our variables of interest, our results offer strong support for the notion that the trade partner countries’ T.P.U. has a significant negative effect on the volume of trade of exporting countries. Similarly, its effect on the extensive margin of trade of exporting countries is significantly negative. These results are consistent with theories and existing empirical studies that show adverse effects of T.P.U. on export and firms’ entry into foreign markets because of T.P.U. shocks in one country may spill over to others and affect their trade performance through the global value chain and trade linkages (Tam, Citation2018; Handley, Citation2014; Handley & Limão, Citation2017; Imbruno, Citation2019). Therefore, these findings are logical because global trade integration has significantly increased firms’ exposure to foreign T.P.U. and diffused uncertainty across borders.

Furthermore, origin countries’ T.P.U. has a significant detrimental effect on trade flows at a 10% significance level for the whole sample. Moreover, it has negative impacts on extensive trade margins, indicating that it adversely affects the probability of trade. These results are congruent because the role of future conditions is essential when firms decide on costly irreversible investments such as producing a new good, adopting technology, or selling in a new market (Handley & Limão, Citation2015).

4.2. The impacts of trade policy uncertainty on trade based on income heterogeneity

Based on the I.M.F. income classification, we have separately investigated the effects of T.P.U., categorising countries into emerging and low-income developing economies. Low-income developing countries’ trade mainly concentrates on a few natural resources and agricultural commodities with limited diversification (World Bank, Citation2015). Trading with limited diversification may force them to suffer external shocks, including policy changes from the destination countries. For example, tariff uncertainty faced by low-income countries is still high and creates costly policy uncertainty for the countries. Furthermore, tariff peaks and escalation policies also affect market access and export diversification of low-income developing countries. Additionally, changes in domestic regulatory policies and non-tariff restrictions can affect the trade performance of developing countries (World Bank, Citation2015). Therefore, based on this evidence, the exercise is repeated to investigate the effects of T.P.U. on emerging economies and low-income developing countries separately.

The standard gravity variables have expected impacts on the trade performance of both emerging economies and low-income developing countries. The effects of the T.P.U. of destination countries on the extensive and intensive margins of trade performance are negative and statistically significant for both emerging economies and low-income developing countries (). However, unlike the whole sample, the effect of T.P.U. of origin countries on the extensive trade margin is robustly negative for low-income developing economies.

4.3. The impacts of trade policy uncertainty on non-manufactured exports

Merchandise trade can also be divided into broad categories, such as natural resources, agriculture, and manufacturing (United Nations, Citation2021). The highest annual percentage change was recorded for agricultural products compared to manufactured goods, and fuels and mining products exports from 2010 to 2018 (World Trade Organization, Citation2019). Moreover, agriculture share in global trade has expanded persistently in the last two decades (Chaturvedi, Citation2019). However, the sector has been subjected to more uncoordinated policy interventions than any other sector (Anderson, Citation2016). More specifically, agricultural export has experienced several policy changes and uncertainties. For example, the failure of the Doha Round represents a failure of international cooperation in trade and development (Bouët & Laborde, Citation2008). The loss of demand for U.S. agricultural exports due to tariff imposition on U.S. imports of steel and aluminum from certain countries and other imported products from China, the response of China with retaliatory tariffs on U.S. exports, particularly agricultural products. Moreover, the misguided trade policies that attempted to address domestic concerns in 2007–2008, 2010–2011, and 2012–2013 subject to a high global agricultural commodity price through beggar-thy-neighbor policies that increased price volatility.

Even though many developing countries are striving to diversify their exports, natural resources and agriculture export still remain a large share of many developing countries’ exports ( in Appendix B). Specifically, commodity dependence is more common for raw material suppliers in Africa and Latin American countries, and energy export concentration is more common for Middle East countries. However, among developing countries, a few emerging economies have diversified their export. Therefore, it is worthwhile to extend our analysis to investigate the effects of T.P.U. on natural resources and agriculture trade (non-manufactured trade).

The results imply that the T.P.U. of destination countries has a statistically significant adverse effect on the trade performance of non-manufactured commodities of developing countries. Besides, T.P.U. of origin countries has a negative and statistically significant effect on the extensive margin of trade flow ().

Table 3. The effects of T.P.U. on non-manufacture trade.

4.4. Developing-developing country pair

South–South trade, where most developing countries exist, represented an estimated 52% of total developing economies’ exports in 2018 (World Trade Organization, Citation2019). Besides, a report by the W.T.O. (2019) indicates that trade between developing countries constituted an average of 50.64% of the total export from 2008 to 2018, implying that developing economies’ exports to other developing economies surpassed their exports to developed countries. Moreover, intra-regional trade among developing countries in South–South trade was more resilient. It outperformed North–South trade in the last five years due to regional integration strategies in the form of regional value chains and regional trade agreements. However, extra-regional South–South trade has been the most volatile for developing countries (United Nations, Citation2019). Therefore, as the trade relationship between developing countries is increasing, it is worthwhile to investigate the effects of T.P.U. on the trade flow of developing countries to developing countries.

The results are consistent with the baseline results. The effects of T.P.U. of destination countries have an economically significant negative effect on extensive margins of trade. Unlike the baseline results, T.P.U. of origin countries has a significant negative effect on both extensive and intensive margin of trade ().

Table 4. The effects of T.P.U. on trade flow (developing-developing pair).

5. Robustness analysis

An alternative method commonly used in gravity model specification is the P.P.M.L. model. It is a convenient strategy to solve zero-valued trade flow observations and heteroscedasticity is to estimate the gravity model in multiplicative form instead of the logarithmic form (Santos Silva & Tenreyro, Citation2006). If the gravity specification contains the correct set of explanatory variables, the P.P.M.L. method consistently estimates the original non-linear model. Thus, we apply the P.P.M.L. estimator to estimate the gravity specification of the impacts of T.P.U. on trade performance for robustness and sensitivity analysis using the following outcome equation.

(7)

(7)

The dependent variable (trade flow) is included in levels instead of logarithms in the model specification. However, the estimates of the independent variables, which are taken in the logarithmic form, can be interpreted as elasticities.

The findings are consistent with the findings reported in . The standard gravity estimates have expected signs and significance except for minor differences in magnitude and significance. The effects of T.P.U. of destination are robustly negative, reinforcing the baseline results. Besides, the coefficients of T.P.U. of origin are significant at a 10% significance level for the whole sample and emerging economies and a 1% level of significance for low-income developing countries ().

Table 5. The impacts of T.P.U. on trade flow (P.P.M.L.).

6. Counterfactual analysis

Calculating demonstrative distance equivalent is worthwhile to show how the structural gravity estimates can be converted into trade volume effects. The simulation shows that the percent improvement would be gained by improving T.P.U. to the average performer using estimates for the whole sample, emerging economies, and low-income developing countries ( and ). We used estimates for distance and T.P.U. from and and the average value of the distance from in Supplementary Materials. Moreover, detailed discussions of the calculation of counterfactual analysis are reported in the supplementary material available online. The results imply that the gain from improvement in T.P.U. is more robust for emerging economies compared to low-income developing countries. ()

Table 6. Simulation results.

7. Discussions and policy implications

This study’s findings show that the high T.P.U. in trade partner countries adversely affects the trade volume of exporting countries (see ). The negative impacts of T.P.U. of trade destination countries reveal that higher T.P.U. in a destination country increases business exposure to risks, adversely affecting the trade performance of its trade partner countries. Moreover, T.P.U. on destination countries has negative effects on the extensive margin of trade for exporting countries. The impacts of T.P.U. of destination countries remain qualitatively unchanged regardless of whether the origin country is an emerging or low-income developing and whether it focuses on non-manufacture trading. Additionally, it has an adverse effect on the extensive margin of trade between developing countries. These results are consistent with theories and existing empirical studies because of T.P.U. shocks in one country can have a spillover effect and significantly affect the trade performance of exporting countries through the trade linkage and value chain (Tam, Citation2018; Jia et al., Citation2020). Thus, the impacts of destination countries’ T.P.U. should get due attention because sunk and opportunity costs related to trade may force firms to prefer countries with a lower level of T.P.U. These findings are reasonable because global integration has considerably increased firms’ exposure to foreign policy uncertainty and transmitted uncertainty across borders.

Furthermore, the findings indicate that the origin countries’ T.P.U. affects the extensive trade margin for low-income developing economies. Besides, it has an adverse effect on the extensive margin of non-manufacture export of emerging economies and low-income developing countries. However, its effect is negative and statistically significant on the extensive and intensive margin of trade between developing countries pair. The results are congruent with the theoretical predictions of the effect of uncertainty on export performance. The findings are in line with the findings of (Greenland et al., Citation2019; Wang et al., Citation2014; Crowley et al., Citation2018).

Regarding the effects of T.P.U. on extensive margins of trade, the results can be justified because exporting firms lower investments in existing markets while delaying investments in new markets, affecting the extensive margin of export under high T.P.U. (Wang et al., Citation2014). This justification is congruent with the theoretical notions of the relationship between policy uncertainty and international trade. For instance, by increasing the risk associated with irreversible investments (Bernanke, Citation1983), policy uncertainty creates a real option value of waiting and conservatism. As a result, firms delay market entry amid heightening policy uncertainty to avoid high sunk entry costs (Greenland et al., Citation2019). Therefore, the findings of this study are in line with the option theory of investment that provides a significant part to policy uncertainty as a determinant of investment spending and predicts that when political, economic, and policy uncertainty is high, firms delay the decision to invest and enter into trade. Moreover, the study’s findings are in line with the theoretical framework of Handley (Citation2014) and Handley and Limão (Citation2015), which imply that an increase in uncertainties forces firms to delay entry to the market to avoid paying sunk entry costs.

The counterfactual simulation analysis used to calculate the illustrative variable (physical distance) indicates that the uncertainty substantially impacts the countries’ export performance. The results allow one to simulate the gains from controlling the T.P.U. to the average performing country to a distance-reduction equivalent. It implies that developing policy options to control the policy uncertainty to the average decreases the average distance by 5.39%, 6.53%, and 2.32% for the whole sample, emerging economies, and low-income developing countries, respectively.

From a policy implications angle, policymakers should take more decisive and target action to control high T.P.U. to promote the intensive and extensive margins of emerging economies and low-income developing countries’ trade. Besides, policymakers should make their policy actions predictable, provide forward guidance on the stance of policy and supervise implementations of policies to reduce T.P.U. Thus, transparency of regulations and policy actions needs to be increased from trade destination countries. Moreover, countries, especially advanced economies, should settle disputes and reduce trade tensions among themselves and with developing countries. Also, any policy alternatives to reduce T.P.U. should be critically evaluated because the actions taken into account will be distorted and create additional uncertainties. Multilateral and regional trade agreements should strive to correct trade policy externalities in developing countries on top of managing the level of trade barriers.

Besides, low-income developing countries’ exports are concentrated on non-manufactured commodities and have lower export supply elasticity. Additionally, they have relatively lower export and destination diversification. Therefore, this study calls for collective action to promote export diversification and reduce policy uncertainties for their trade. To sum up, the findings of this study are sound from both policy implications and empirical contributions.

Acknowledgments

We would like to thank the editor and referees for their detailed evaluation and constructive suggestions, which significantly improved the manuscript. All remaining errors are ours.

Disclosure statement

The authors declare no conflict of interest.

Data availability statement

The data used in this study are available from the corresponding author whenever requested.

Additional information

Funding

References

- Abel, A. B. (1983). Optimal investment under uncertainty. American Economic Review, 73(1), 228–233. https://www.jstor.org/stable/1803942

- Ahir, H., Bloom, N., & Furceri, D. (2018). The world uncertainty index. https://www.policyuncertainty.com/wui_quarterly.html

- Ahir, H., Bloom, N., & Furceri, D. (2020). 60 years of uncertainty. International Monetary Fund, 57(1), 58–60.

- Alberto, A., Roberta, P., & Nadia, R. (2018). The heterogeneous effects of trade policy uncertainty: How much do trade commitments boost trade? (World Bank Policy Research Working Paper No. 8567). World Bank, Washington DC.

- Anderson, J. E., & Yotov, Y. V. (2016). Terms of trade and global efficiency effects of free trade agreements, 1990-2002. Journal of International Economics, 99(C), 279–298. https://doi.org/10.1016/j.jinteco.2015.10.006

- Anderson, K. (2016). Agricultural trade, policy reforms, and global food security. In Palgrave Studies in Agricultural Economics and Food Policy (pp. 207–224). Palgrave Macmillan. https://doi.org/10.1057/978-1-137-46925-0_9

- Bar-Ilan, A., & Strange, W. C. (1996). Investment lags. American Economic Review, 86(3), 610–622. https://www.jstor.org/stable/2118214

- Bekkers, E. (2019). Challenges to the trade system: The potential impact of changes in future trade policy. Journal of Policy Modeling, 41(3), 489–506. https://doi.org/10.1016/j.jpolmod.2019.03.016

- Bernanke, B. S. (1983). Irreversibility, uncertainty, and cyclical investment. The Quarterly Journal of Economics, 98(1), 85–106. https://doi.org/10.2307/1885568

- Borojo, D. G., Yushi, J., & Miao, M. (2021). The impacts of economic policy uncertainty on trade flow. Emerging Markets Finance and Trade, 58(8), 2258–2272. https://doi.org/10.1080/1540496X.2021.1971075

- Bouët, A., & Laborde, D. (2008). The potential cost of a failed Doha Round (I.F.P.R.I. Issue Brief No. 56).

- Caldara, D., Iacoviello, M., Molligo, P., Prestipino, A., & Raffo, A. (2019). The economic effects of trade policy uncertainty. Journal of Monetary Economics, 109, 38–59. https://doi.org/10.1016/j.jmoneco.2019.11.002

- Chaturvedi, S. (2019). Trade, production, and emerging economies: Rising trends in agriculture and manufacturing. Turkish Policy Quarterly, 17(4), 101–113.

- Cheng, I.-H., & Wall, H. J. (2005). Controlling for heterogeneity in gravity models of trade and integration. Federal Reserve Bank of St.Louis Review, 87(1), 49–63.

- Crowley, M., Meng, N., & Song, H. (2018). Tariff scares: Trade policy uncertainty and foreign market entry by Chinese firms. Journal of International Economics, 114, 96–115. https://doi.org/10.1016/j.jinteco.2018.05.003

- Dixit, A. K., & Pindyck, R. S. (1994). Investment under uncertainty. Princeton University Press.

- Ebeke, C., & Siminitz, J. (2018). Trade uncertainty and investment in the Euro Area (I.M.F. Working Paper No. W.P./18/281).

- Greenland, A., Ion, M., & Lopresti, J. (2019). Exports, investment and policy uncertainty. Canadian Journal of Economics/Revue Canadienne D'économique, 52(3), 1248–1288. https://doi.org/10.1111/caje.12400

- Handley, K. (2014). Exporting under trade policy uncertainty: Theory and evidence. Journal of International Economics, 94(1), 50–66. https://doi.org/10.1016/j.jinteco.2014.05.005

- Handley, K., & Limão, N. (2015). Trade and investment under policy uncertainty: Theory and firm evidence. American Economic Journal: Economic Policy, 7(4), 189–222. https://doi.org/10.1257/pol.20140068

- Handley, K., & Limão, N. (2017). Policy uncertainty, trade, and welfare: Theory and evidence for china and the United States. American Economic Review, 107(9), 2731–2783. https://doi.org/10.1257/aer.20141419

- Hartman, R. (1972). The effects of price and cost uncertainty on investment. Journal of Economic Theory, 5(2), 258–266. https://doi.org/10.1016/0022-0531(72)90105-6

- Heckman, J. J. (1979). Sample selection bias as a specification error. Econometrica, 47(1), 153–161. https://doi.org/10.2307/1912352

- Helpman, E., Melitz, M., & Rubinstein, Y. (2008). Estimating trade flows: Trading partners and trading volumes. The Quarterly Journal of Economics, CXXIII, 123(2), 441–487. https://doi.org/10.1162/qjec.2008.123.2.441

- Hoque, M. E., Wah, L. S., & Zaidi, M. A. S. (2019). Oil price shocks, global economic policy uncertainty, geopolitical risk, and stock price in Malaysia: Factor augmented V.A.R. approach. Economic Research-Ekonomska Istraživanja, 32(1), 3700–3732. https://doi.org/10.1080/1331677X.2019.1675078

- Hua, R., Zhao, P., Yu, H., & Fang, L. (2020). Impact of US uncertainty on Chinese stock market volatility. Emerging Markets Finance and Trade, 56(3), 576–592. https://doi.org/10.1080/1540496X.2018.1519413

- Imbruno, M. (2019). Importing under trade policy uncertainty: Evidence from China. Journal of Comparative Economics, 47(4), 806–826. https://doi.org/10.1016/j.jce.2019.06.004

- Jaaskela, J., & Mathews, N. (2015). Explaining the slowdown in global trade. R.B.A. Bulletin. Reserve Bank of Australia, 39–46.

- Jia, F., Huang, X., Xu, X., & Sun, H. (2020). The effects of economic policy uncertainty on export: A gravity model approach. Prague Economic Papers, 29(5), 600–622. https://doi.org/10.18267/j.pep.754

- Jones, P. M., & Olson, E. (2013). The time-varying correlation between uncertainty, output, and inflation: Evidence from a DCC-GARCH model. Economics Letters, 118(1), 33–37. https://doi.org/10.1016/j.econlet.2012.09.012

- Krol, R. (2018). Does uncertainty over economic policy harm trade, foreign investment, and prosperity? Mercatus Center at George Mason University. https://doi.org/10.2139/ssrn.3169563

- Liao, J., Luo, L., Xu, X., & Wang, A. (2021). Perceived macroeconomic uncertainty and export: Evidence from cross-country data. Economic Research-Ekonomska Istraživanja, 35(1), 213–229. https://doi.org/10.1080/1331677X.2021.1890176

- Lindé, J., & Pescatori, A. (2019). The macroeconomic effects of trade tariffs: Revisiting the lerner symmetry result. Journal of International Money and Finance, 95, 52–69. https://doi.org/10.1016/j.jimonfin.2019.01.019

- Maryam, J., Banday, U. J., & Mittal, A. (2018). Trade intensity and revealed comparative advantage: An analysis of Intra-BRICS trade. International Journal of Emerging Markets, 13(5), 1182–1195. https://doi.org/10.1108/IJoEM-09-2017-0365

- Novy, D., & Taylor, A. M. (2020). Trade and uncertainty. The Review of Economics and Statistics, 102(4), 749–765. https://doi.org/10.1162/rest_a_00885

- Rashid, A., Nasimi, A. N., & Nasimi, R. N. (2021). The uncertainty-investment relationship: Scrutinizing the role of firm size. International Journal of Emerging Markets, ahead-of-print. https://doi.org/10.1108/IJOEM-09-2019-0698

- Robinson, S., & Thierfelder, K. (2019). Global adjustment to U.S. disengagement from the world trading system. Journal of Policy Modeling, 41(3), 522–536. https://doi.org/10.1016/j.jpolmod.2019.03.019

- Saleem, H., Jiandong, W., & Khan, M. B. (2018). The impact of economic policy uncertainty on the innovation in China: Empirical evidence from autoregressive distributed lag bounds tests. Cogent Economics & Finance, 6(1), 1514929. https://doi.org/10.1080/23322039.2018.1514929

- Santos Silva, J. M. C., & Tenreyro, S. (2006). The log of gravity. The Review of Economics and Statistics, 88(4), 641–658. https://doi.org/10.1162/rest.88.4.641

- Scheffel, E. M. (2016). Accounting for the political uncertainty factor. Journal of Applied Econometrics, 31(6), 1048–1064. https://doi.org/10.1002/jae.2455

- Tam, P. S. (2018). Global trade flows and economic policy uncertainty. Applied Economics, 50(34–35), 3718–3734. https://doi.org/10.1080/00036846.2018.1436151

- United Nations. (2019). Key statistics and trends in international trade, international trade rebounds. https://digitallibrary.un.org/record/3813137?ln=en

- United Nations. (2021). Key statistics and trade trends under the COVID-19 pandemic: In International Trade 2020. https://doi.org/10.18356/9789210056502

- Wang, Y., Chen, C. R., & Huang, Y. S. (2014). Economic policy uncertainty and corporate investment: Evidence from China. Pacific-Basin Finance Journal, 26(2014), 227–243. https://doi.org/10.1016/j.pacfin.2013.12.008

- World Bank (2015). Low-income developing countries and G-20 trade and investment policy: Trade and competitiveness global practice. (World Bank Report No. 99933).

- World Trade Organization. (2019). World trade statistical review. https://www.wto.org/english/res_e/statis_e/wts2019_e/wts2019_e.pdf

- Yan, M., & Shi, K. (2021). The impact of high-frequency economic policy uncertainty on China’s macroeconomy: Evidence from mixed-frequency V.A.R. Economic Research-Ekonomska Istraživanja, 34(1), 3201–3224. https://doi.org/10.1080/1331677X.2020.1870519

- Yang, Y., & Nie, P. (2020). Optimal trade policies under product differentiations. Journal of Business Economics and Management, 21(1), 241–254. https://doi.org/10.3846/jbem.2020.11923

- Yotov, Y. V., Piermartini, R., Monteiro, J.-A., & Larch, M. (2016). An advanced guide to trade policy analysis: The Structural Gravity Model. World Trade Organization. http://vi.unctad.org/tpa.

- Yushi, J., & Borojo, D. G. (2019). The impacts of institutional quality and infrastructure on overall and intra-Africa trade. Economics: The Open- Access, Open-Assessment E-Journal, 13 (10), 1–34. https://doi.org/10.5018/economics-ejournal.ja.2019-10

Appendix A.

List of countries

Destination countries: Afghanistan, Albania, Algeria, Angola, Argentina, Armenia, Australia, Austria, Azerbaijan, Bangladesh, Belarus, Belgium, Benin, Bolivia, Bosnia and Herzegovina, Botswana, Brazil, Bulgaria, Burkina Faso, Burundi, Cambodia, Cameroon, Canada, Central African Republic, Chad, Chile, China, Colombia, D.R. Congo, Republic Congo, Costa Rica, Côte d'Ivoire, Croatia, Czech Republic, Denmark, Dominican Republic, Ecuador, Egypt, El Salvador, Eritrea, Ethiopia, Finland, France, Gabon, The Gambia, Georgia, Germany, Ghana, Greece, Guatemala, Guinea, Guinea-Bissau, Haiti, Honduras, Hong Kong, Hungary, India, Indonesia, Iran, Iraq, Ireland, Israel, Italy, Jamaica, Japan, Jordan, Kazakhstan, Kenya, Korea, Kuwait, Kyrgyz Republic, Lao P.D.R., Latvia, Lebanon, Lesotho, Liberia, Libya, Lithuania, F.Y.R. Macedonia, Madagascar, Malawi, Malaysia, Mali, Mauritania, Mexico, Moldova, Mongolia, Morocco, Mozambique, Myanmar, Namibia, Nepal, Netherlands, New Zealand, Nicaragua, Niger, Nigeria, Norway, Oman, Pakistan, Panama, Papua New Guinea, Paraguay, Peru, Philippines, Poland, Portugal, Qatar, Romania, Russia, Rwanda, Saudi Arabia, Senegal, Sierra Leone, Singapore, Slovak Republic, Slovenia, South Africa, Spain, Sri Lanka, Sudan, Sweden, Switzerland, Taiwan Province of China, Tajikistan, Tanzania, Thailand, Togo, Tunisia, Turkey, Turkmenistan, Uganda, Ukraine, United Arab Emirates, United Kingdom, United States, Uruguay, Uzbekistan, Venezuela, Vietnam, Yemen, Zambia and Zimbabwe

Origin emerging: Albania, Algeria, Angola, Argentina, Armenia, Azerbaijan, Belarus, Bosnia and Herzegovina, Botswana, Brazil, Bulgaria, Chile, China, Colombia, Costa Rica, Croatia, Dominican Republic, Ecuador, Egypt, El Salvador, Gabon, Georgia, Guatemala, Hungary, India, Indonesia, Islamic Republic of Iran, Iraq, Jamaica, Jordan, Kazakhstan, Kuwait, Lebanon, Libya, Lithuania, F.Y.R. Macedonia, Malaysia, Mexico, Morocco, Namibia, Oman, Pakistan, Panama, Paraguay, Peru, Philippines, Poland, Qatar, Romania, Russia, Saudi Arabia, South Africa, Sri Lanka, Thailand, Tunisia, Turkey, Turkmenistan, Ukraine, United Arab Emirates, Uruguay and Venezuela.

Origin low-income developing: Afghanistan, Bangladesh, Benin, Bolivia, Burkina Faso, Burundi, Cambodia, Cameroon, Central African Republic, Chad, the Democratic Republic of the Congo, Republic of Congo, Côte d'Ivoire, Eritrea, Ethiopia, The Gambia, Ghana, Guinea, Guinea-Bissau, Haiti, Honduras, Kenya, Kyrgyz Republic, Lao P.D.R., Lesotho, Liberia, Madagascar, Malawi, Mali, Mauritania, Moldova, Mongolia, Mozambique, Myanmar, Nepal, Nicaragua, Niger, Nigeria, Papua New Guinea, Rwanda, Senegal, Sierra Leone, Sudan, Tajikistan, Tanzania, Togo, Uganda, Uzbekistan, Vietnam, Yemen, Zambia and Zimbabwe

Appendix B

Figure B1. The average export of top exporters among emerging economies (2001–2019).

Source: Authors' calculations from U.N. Comtrade database.

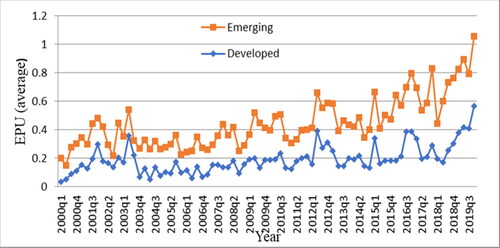

Figure B2. T.P.U. of developed and developing countries.

Source: Authors' calculations based on E.P.U index by Ahir et al. (Citation2018).

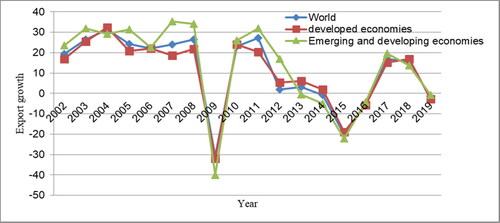

Figure B3. T.P.U. and trade performance. a. T.P.U. change. b. Export growth.

Source: Authors' calculations based on E.P.U index by Ahir et al. (Citation2018).

Figure B4. Trade performance of low-income countries.

Source: Authors' calculations from U.N. Comtrade database.