?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The study aims to analyze the economic determinants of national carbon emissions in a large cross-section of 119 countries. The study followed the ‘theory of sustainable development’ to assess the national sustainable developmental agenda. The study employed cross-sectional, robust least squares, and Markov switching regression for parameter estimates. The findings indicate that information disclosure, the cost of business start-up procedures, sustainable fuel imports, and renewable energy decrease emissions stock. In contrast, ease of doing business and logistics operations increase it. According to the ex-ante analysis, information disclosure, the cost of business start-up procedures, and environmentally friendly logistical operations would likely reduce emissions stock. Ease of doing business and lower renewable fuel expenditures will almost certainly increase emissions stock in the majority of subsequent years. Over time, information disclosure is expected to significantly impact carbon emissions, followed by renewable energy consumption, doing business, and logistical operations. Sustainable economic policies worldwide make it possible for green technology and environmentally friendly manufacturing to be put into place.

1. Introduction

Economic activities require more energy to run economic projects, causing environmental degradation. The substantial use of fossil fuel burning in logistics activities to demonstrate carbon footprints, and the actual transfer of commodities from one location to another, causes a burdensome environmental quality (Uyar et al., Citation2020, Sasmoko et al., Citation2021, Bose et al., Citation2021). It is imperative to switch economic activities from nonrenewable to renewable fuels (Khan et al. Citation2020, Karaman et al. Citation2020, and Anser et al. Citation2020a). Sustained economic growth is dependent on several factors, including the disclosure of financial information and business ownership, the legal framework for a congenial working environment, sustainable logistical operations, and a reduction in the cost of starting up new enterprises (Khan et al., Citation2021, Saeed et al. Citation2021). Green innovation and environmentally friendly production are highly needed for the sustainable growth of nations (Awan et al., Citation2021; Cheng et al., Citation2021, Awan & Sroufe, Citation2022). The study seeks to answer the following research question, i.e., what is the effect of six national-level economic determinants (i.e., corporate information transparency, cost of business startup procedures, ease of doing business, logistics performance, fuel imports, renewable energy consumption) on national carbon emissions. This question is critical to understanding the need to optimize sustainable economic policies to mitigate carbon emissions through different sustainable instruments, including carbon pricing, incentive-based regulations, and eco-innovation processes (Baloch et al., Citation2021, Ahmad et al. Citation2021). The stated question is further linked to the national logistics profile, which views fossil fuel burning as a negative factor for the environment when moving commodities from one place to another. The need to transition from nonrenewable to renewable fuels in logistics operations contributes to achieving sustainable growth results (Golroudbary et al., Citation2019, Aldakhil et al., Citation2018, Awan, Citation2019). Importing nonrenewable energy obstructs the country's green growth plan, eventually harming its economic output.

The following earlier studies have developed the link between different economic determinants and national level carbon emissions rise, i.e., Kraus et al. (Citation2020) analyzed data from 297 manufacturing enterprises in Malaysia's economy to determine the country's green business activities. The findings indicate that green strategies and innovative processes may assist in enhancing environmental standards and enhancing the company profile's eco-friendliness and efficiency. Abbas (Citation2020) suggested that total quality management (TQM) procedures are feasible components of green business processes since they assist organizations in achieving sustainable outcomes. Additionally, corporate responsibility initiatives significantly improve green practices in Pakistan via the mediation of TQM. The need to strengthen organizational strategy competencies to react to corporate environmental issues would aid in the transition to a green developmental agenda. Úbeda-García et al. (Citation2021) examine the links between business responsibility and corporate performance regarding environmental quality criteria using a panel of Spanish hotel companies. The findings verified the favorable correlation between business responsibility and performance via green human resource management strategies and corporate environmental standards. The need to equip human resources with green practices facilitated sustainable corporate outcomes through human capital. Han et al. (Citation2022) surveyed 211 workers from various Chinese firms to determine the impact of institutional success on corporate green investment plans and discovered a significant correlation. The competitiveness of government-led organizations enables new investment options that benefit ecological conservation and business resources. Chang et al. (Citation2020) stated that an organizational green vision is a potential element in enhancing green business activities, eventually promoting sustainable product creation. Li et al. (Citation2020a) stressed the need to enhance business credit ratings to get the green certification. The issuing of green bonds and certificates generated a positive signal from stakeholders to invest in eco-friendly goods, lowering the cost of acquiring environmental certifications and allowing for more effective environmental governance. Yu et al. (Citation2020) gathered significant data from Malaysian fast-moving consumer goods (FMCG) companies to examine green business activities related to eco-friendly manufacturing, green buying behavior, and green awareness campaigns. The findings indicate that organizational reputation is critical for developing a green corporate image associated with sustainable business activities such as green recycling efforts, green purchasing practices, and environmental assistance programs. A green business image is critical to achieving long-term benefits from enhanced business initiatives. Zhou et al. (Citation2021) analyzed data from Chinese publicly traded banks between 2008 and 2018 to determine the effect of green credit in mediating corporate efforts and banks' financial performance. The findings indicate that, in the short run, commercial responsibility has a detrimental effect on banks' financial operations. However, the findings are reversed in the long term, confirming the positive correlation between the two variables in the context of green credit. The requirement to generate green financing enables organizations to effectively manage their green commercial responsibility efforts by confronting financial choices connected to ecological standards. Li & Wang (Citation2021) suggest that organizational competitiveness helps invest in sustainable commerce activities by expanding green manufacturing and innovation processes. Government funding may be necessary to get businesses to follow safety rules and change their corporate identities through green innovation processes.

There are few macro-level studies on sustainable logistics operations, which are critical for achieving long-term economic growth. For instance, Li et al. (Citation2021a) stated that carbon emissions caused by technology and logistics obstruct business sustainability efforts, resulting in adverse economic consequences. According to Anser et al. (Citation2020a), green energy resources should be employed in logistics operations to enhance performance metrics and increase export capabilities and competitiveness. Sasmoko et al. (Citation2021) found that through greening business efforts globally, the healthcare supply chain process played a critical part in lowering pandemic-associated mortality rates and resulting in more positive results. Magazzino et al. (Citation2021) found a sparse number of economic factors as significant predictors of logistics performance, including technology innovation, human capital generation, and trade liberalization policies. These variables contribute to the country's economic development by expanding logistical activities at the expense of carbon emissions. As a result, it is essential to develop a sustainable logistics strategy to mitigate the harmful cost of carbon emissions on a global scale. Li et al. (Citation2021b) discovered that green logistics improve economic activity and environmental quality in a wide variety of regions of the globalized globe. By being used in logistical operations, green fuels would aid in achieving the sustainability goal. According to Rehman et al. (Citation2021), a green information system serves as the foundation for a sustainable supply chain process that benefits both the firm's competitiveness and environmental stewardship. The environmental disclosure index assists organizations in developing competencies that pave the path for green innovation processes. Using data from Asia, Yu et al. (Citation2021) examined the links between a region's green supply chain management, energy consumption, and environmental deterioration. The findings indicate that using green energy sources helps offset the adverse effects of carbon emissions while promoting sustainable practices in a region. The following hypotheses need to be evaluated in light of the literature review, i.e.,

H1: Corporate information transparency is negatively related to national carbon emissions.

H2: The cost of business start up procedures is negatively related to national carbon emissions.

H3: The ease of doing business is negatively related to national carbon emissions.

H4: Logistics performance is negatively related to national carbon emissions.

H5: Fuel imports are positively related to national carbon emissions.

H6: Renewable energy consumption is negatively related to national carbon emissions.

Based on the critical discussion, the following study goals have been set up in response to the stated research hypotheses:

To investigate the effect of national-level economic determinants on emissions stock.

To examine the role of fuel imports in the environmental sustainability agenda, and

To assess the impact of renewable energy demand on the nation's green developmental agenda.

Different regression estimators were used in various countries to look at the set goals and make policy recommendations on the research issues.

2. The study's theoretical basis and contribution

The study mainly focused on the ‘theory of sustainable development’, which includes economic, social, and environmental sustainability that amalgamate to achieve an environmental sustainability outcome. Economic actions should be environmentally friendly and complemented by a diverse range of pro-sustainability goals (Awan et al., Citation2021, Bhutto et al., Citation2021). The information disclosure index is a critical component of economic growth since it enables policymakers to see economic performance over time (Absar et al., Citation2021, Awawdeh et al., Citation2021, Garanina & Aray, Citation2021). The environmental disclosure index will continue to serve as a foundation for the nation's pro-sustainability behavior, demonstrating responsible material production and consumption (Jawaad & Zafar Citation2020, Etse et al. Citation2022). The start-up expenses of new enterprises have impacted the natural environment, which may be addressed via the ease of a tax subsidy program that assists in allocating an acceptable amount of money for environmentally friendly manufacturing (Fauziah et al. Citation2020, Muralidharan Citation2021). Strict environmental regulations compel economic businesses to develop sanitary goods (Li et al. Citation2020b, Baah et al. Citation2020). The business logistics profile assists in evaluating the transfer of physical items from one location to another within a specific period. An efficient customs clearance process means businesses will have a global and competitive image (Kozenkova et al., Citation2021).

The theory of sustainable development argues that economies should not stay focused on their financial statements while pursuing social and environmental sustainability to get a competitive edge on production. The stated theory focuses on three distinct but closely related factors without which economic, social, and environmental sustainability cannot be attained. According to the stated concept, economies may achieve economic sustainability by lowering operating costs via cleaner manufacturing technologies. Valuing social sustainability enables the economy to engage people in community development programs and provide education, health, and well-being. Finally, environmental sustainability emphasizes ecological resources by reducing carbon emissions via ecologically friendly technologies, responsible production and consumption, and conservation. Eco-friendly manufacturing enables businesses to achieve long-term profitability and contribute to economic development projects.

Specifically, the research makes a significant new addition by evaluating a broad range of alternative and plausible economic determinants in connection to emissions per capita across a diverse range of nations that have been relatively understudied in the previous literature. For instance, the information disclosure index, the cost of doing business, the cost of business start-up procedures, and the logistics performance index were all used in the study, which primarily covered financial aspects of the economy that influenced the country's per capita emissions stock. Furthermore, the utilization of fuel imports in the context of a sustainable development agenda communicated to policymakers the need to shift their energy base away from nonrenewable fuel imports and toward renewable energy sources, which aids in achieving clean and green development. Finally, green energy sources continue to play an essential role in improving environmental quality; as a result, the stated variable has been included to the modeling framework in order to keep the countries' goals for using it to contribute to globally shared prosperity.

3. Data and methodology

The study used emissions per capita (denoted by EPC, CO2 metric tonnes per capita) as a dependent variable. In contrast, the business extent of disclosure index (abbreviated BED) (0 = less disclosure to 10 = more disclosure), the cost of business startup procedures (abbreviated CBSP) (percent of GNI per capita), the ease of doing business score (abbreviated EDB) (0 = lowest performance to 100 = best performance), and the logistics performance index (abbreviated LPI) (1 = low to 5 = high) served as regressors of the study. Emissions reduction is dependent on company compliance with environmental regulations; however, firms' carbon structures vary depending on their productive capacity and output level (Cadez et al., Citation2019, Cadez and Guilding, Citation2017). Emissions trading is an efficient method of reducing carbon emissions (Cadez and Czerny Citation2016). As a result, the feasibility of carbon emission reduction is critical for long-term company performance, which ultimately results in sustainable national outcomes. The study used two control variables: fuel imports (denoted by FIMP) (percentage of merchandise imports) and renewable energy consumption (denoted by REC) (percentage of total final energy consumption). The World Bank's (Citation2021) database is used for data collection. The study does an empirical estimate using a cross-section of 119 nations. The BEDI, CBSP, and EDB variables were gathered in 2019, while the other variables, including LPI, EPC, FIMP, and REC, were collected in the most recent year available, 2018. The appendix's contains a list of the nations included in the study.

The study used the information disclosure index, the cost of business start-up procedures, corporate logistics, and ease of doing business as critical components of economic development, thus keeping the country's objective of attaining green development in mind. Previous studies, including Anser et al. (Citation2021a) and Sasmoko et al. (Citation2021), used several economic determinants related to carbon emissions; hence, the same variables were used for ready reference. The following equation is used to illustrate empirically, i.e.,

(1)

(1)

Where EPC shows carbon emissions per capita, BEDI shows the business extent to discourse index, CBSP shows the cost of business start-up procedures, EDB shows the ease of doing business, LPI shows logistics performance index, FIMP shows fuel imports, REC shows renewable energy consumption, and ε shows error term.

According to EquationEq. (1)(1)

(1) , economic determinants are expected to have a differential influence on carbon emissions. It is considered that BEDI and CBSP have a positive impact on the natural environment, but EDB and LPI have a negative impact. Getting fuel from other countries is expected to cause more carbon dioxide emissions, which could be reduced by switching to renewable fuels like wind and solar.

3.1. Econometric analysis framework

The study used the empirical procedures outlined below to look at EquationEq. (1)(1)

(1) :

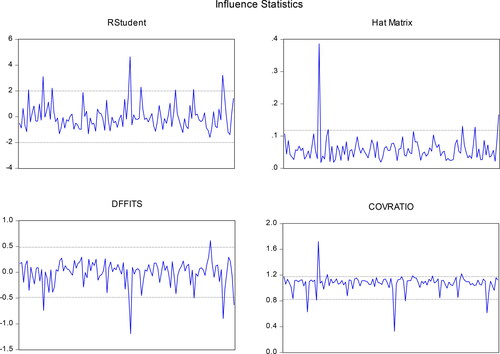

Step 1: create influence statistics

The initial stage is to discover structural breaks in the entire model, represented by EquationEq. (1)(1)

(1) . To find likely model outliers, the study used four influential statistics: R-student, Hat Matrix, DFFITS, and COVRATIO. Statistics from the system's internal and external factors would help us move forward in dealing with outliers from both sides of the system.

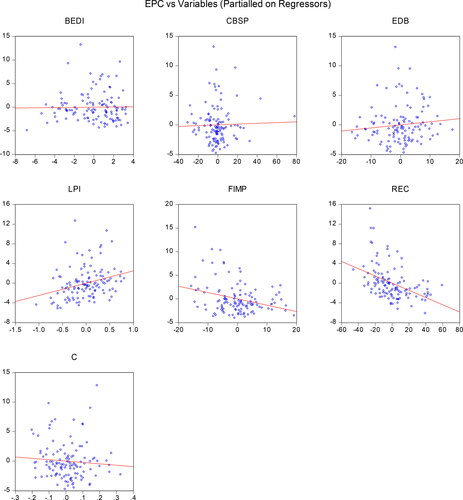

Step 2: create leverage plots

Following the identification of potential outliers in the supplied model, the study creates ‘leverage plots’ for each variable in the system. The leverage plots aid in assessing structural breakdowns in the response variable and potential causes that influence it over time. Leverage plots show how far dependent and independent variables differ from their mean value. The higher the variance of the variables from their mean values, the larger the residuals, making the parameter estimations biased and inconsistent.

Step 3: robust least squares regression

Because of the high leverage in the variables plot, the conventional linear regression model is susceptible to structural breaks, which may increase the magnitude of the residuals. The traditional OLS cannot deal with potential outliers and produce biassed parameter estimates that lack the blue property of coefficient estimates. The robust least squares regression (RLS) is an improved version of the traditional OLS regression that can handle outliers in the system equation while still providing unbiased parameter estimates. There are three types of RLS estimators, each with its own set of characteristics, i.e.,

M (like a maximum likelihood estimator) – Estimator

S (S stands for ‘scale statistic’) – Estimator, and

MM- Estimator.

Huber (Citation1973) introduced an RLS-M estimator with a unique feature for dealing with any outliers in the outcome variable to limit the residuals' size. Leverage plots would help determine if the endogenous variable included any structural discontinuities in the data period across time. The M-estimator type of RLS regression may be used based on the leverage plots. Rousseeuw and Yohai (Citation1984) extended the RLS estimator to become an S-type estimator. The S-estimator determines how much the exogenous variables differ from their actual mean values, showing system outliers. As a result, using the leverage plots, one may easily find the regressors' outliers to reduce the candidate variables' leverage. Finally, Yohai (Citation1987) created the MM-estimator by first computing an S-type estimator and then linking it to the M-type estimator to construct the MM-estimator. The MM-type estimator aids in removing outliers from the overall model and ensures that the parameters have the BLUE characteristic.

Step 4: sensitivity analysis

In addition to the RLS estimator, the study used two other statistical tests to validate the coefficient estimates: cross-sectional regression and the Markov Switching Regime −1 estimator. Both tests have previously been employed in various cross-sectional regressions to get unbiased and consistent results (Anser et al., Citation2021b). Both tests were used in the study to look at the variables differently.

Step 5: innovation accounting matrix (IAM)

The IAM technique comprises two methods: impulse response function (IRF) and variance decomposition analysis (VDA). Both techniques are compliant with the VAR standard. Over time, the IRF and VDA estimations showed inter-temporal links between the variables examined. The IRF estimates showed that the variables should be directed toward the dependent variable in the forecasting framework. Positive shocks indicate that both variables influence each other in the same manner over time. On the other hand, the adverse shocks suggest that the variables contrarily impact each other. As a result, policy formulations would be simple to construct over a more extended period. Similarly, the VDA estimates indicated the extent of the candidate factors' influence on the response variable across time. A 1% shock in the system variables is likely to cause a significant quantity of variance error shocks on the response variable, which aids in understanding the system's most influential factor over a time horizon. The VDA decomposition is shown in EquationEq. (2)(2)

(2) , i.e.,

(2)

(2)

The mean square error term is set for the designated predictors that represent in EquationEq. (3)(3)

(3) , i.e.,

(3)

(3)

Where, MSE shows mean square error.

4. Results

The descriptive statistics for the candidate variables are shown in . The average carbon emissions per capita value is 4.733 metric tonnes, with a high of 21.622 (Kuwait) and a low of 0.052 (Burundi). The standard deviation is 4.597, and the distribution is positively skewed (i.e., 1.501) with a high kurtosis value (i.e., 5.132). BEDI and EDB had 7 out of 10 and 69.765 out of 100, respectively. Out of 119 nations, 9 received the maximum index score for information transparency in a sample country, while 18 received a score of more than 80 for ease of doing business. The average cost of business start-up procedures are 12.409% of GNP, with a standard deviation of 18.413%. The LPI has a median value of 2.810 out of five index values, with a maximum value of 4.200 and the lowest value of 1.950. Fuel imports and renewable energy demand account for 14.432% of total imports and 29.786% of total global energy consumption.

Table 1. Descriptive statistics.

The correlation matrix is shown in . Except for registering a new firm, the data reveals that the other economic factors, such as the information transparency index, logistics profile, and ease of doing business, are positively correlated with carbon emissions. CBSP, on the other hand, was adversely linked to carbon emissions. Consequently, economic activities are inconsistent with the country's vision of accomplishing green development goals, which must be ecologically controlled to enhance the developmental performance of the economies. Carbon emissions are adversely associated with fuel imports and renewable energy sources. It suggests that increasing expenditure on green energy sources and reducing reliance on fuel imports are beneficial to creating eco-friendly outputs that achieve cleaner production. The provided analysis helps determine the degree and direction of the relationship between the variables in response to the influence of carbon emissions. The regression analysis would suggest that making economic policies green and clean across countries is desirable.

Table 2. Correlation matrix.

Prior to performing robust least squares regression, the study determined the number of potential outliers in the supplied model. illustrates four distinct ‘influence statistics,’ including R-student, Hat Matrix, DFFITS, and COVRATIO. Five outliers were discovered in the R-student. Outliers are concentrated in Brunei Darussalam, Canada, Kuwait, Luxembourg, and UAE. The Hat Matrix identifies four outliers in a given model. The following cross-sectional nations primarily exhibit unique values in their respective variable series, resulting in structural model breaks: Central African Republic, Sierra Leone, Switzerland, and Zimbabwe. While DFFITS identifies five potential outliers among cross-sectional nations, COVRATIO identifies four possible outliers. It turns out that the model has many outliers that affect the regression estimates, so it is best to use the RLS estimator to deal with any outliers in the data set provided.

Figure 1. Influence statistics.

Source: Authors’ estimate.

After finding structural breakdowns in a particular model, the study sought to determine if outliers were concentrated in the outcome variable or the regressors. The study illustrates leverage plots in to aid in determining the outlier's existence in the variables utilized in the investigation. The illustration demonstrates that economic factors primarily have a higher degree of dispersion in their series, deviating from their mean value and possessing a high degree of leverage in the data series. By contrast, the outcome variable, emissions per capita, has a smooth pattern but lacks leverage in its series. So, we can say that the high leverage plots are more visible when there are more exogenous components in the model. This means that we can use the RLS S-type estimator to deal with regressor outliers.

Figure 2. Leverage plots.

Note: EPC shows carbon emissions per capita, BEDI shows the business extent to discourse index, CBSP shows the cost of business start-up procedures, EDB shows the ease of doing business, LPI shows logistics performance index, FIMP shows fuel imports, and REC shows renewable energy consumption.

Source: Author’s estimation.

H1: Corporate information transparency is negatively related to national carbon emissions.

H2: Cost of business start up procedures is negatively related to national carbon emissions.

H3: Ease of doing business is negatively related to national carbon emissions.

Three distinct regression estimators are shown in to verify the parameter estimations. The findings indicate that corporate information transparency, the cost of business start-up procedures, sustainable fuel imports, and renewable energy significantly reduce emissions stock. The information transparency index places a premium on the percentage share of lowering carbon emissions, followed by sustainable fuel imports, renewable energy demand, and the cost of business start-up procedures. A 1% increase in the information disclosure index results in a 1.25% reduction in the Markov switching regime-I. Additionally, the results indicate that the ease of doing business and corporate logistics profiles contribute to increased carbon emissions due to inadequate environmental regulations, validating the pollution haven hypothesis. Using non-renewable fuels in logistics operations substantiates logistics-induced carbon emissions across countries. As a result, we may investigate the impact of fuel imports on future inter-temporal forecasting estimates to gain a more critical perspective. Renewable energy has a negative effect on carbon emissions, so putting green energy to use in the economy is a vital part of a green development strategy.

Table 3. Cross-sectional regression estimates.

The findings are consistent with the critical research listed below and further examined in the discussion section. Galant and Cadez (Citation2017) asserted that the greater the financial success of the economy, the greater the tendency toward social-oriented projects, and the greater the likelihood of receiving long-term benefits. Feng et al. (Citation2021) emphasized the need to adopt ‘go-for-green’ economic policies that balance economic profits with long-term sustainability outcomes, which aids in advancing nations' long-term sustainable growth. As mentioned by Zhang et al. (Citation2022), progress in the green and climate bond markets aids in the development of a popular marketing strategy that invests in environmentally friendly initiatives to reap economic benefits. Li et al. (Citation2021c) endorsed that green investment contributes to the advancement of the stock market's performance, ultimately leading to a rise in stock returns. Several alternative and plausible factors have been proposed by Nguyen and Ngo (Citation2021) to improve economic performance in order to achieve sustainable development goals, including technological advancement in cleaner production, improvement in the supply chain process, and sustainable logistics activities that contribute to long-term payoffs.

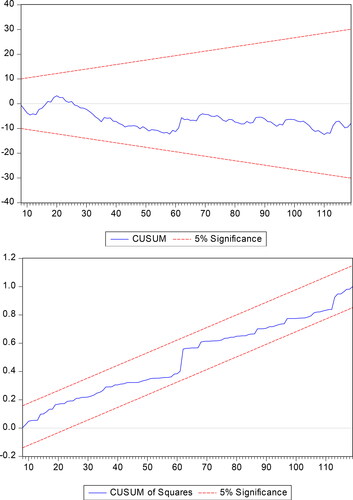

The CUSUM and CUSUM square estimates in indicate that the supplied model is stable at the 5% significance level. As a result, the model is functionally balanced and trustworthy.

Figure 3. CUSUM and CUSUM square estimates.

Source: Author’s estimates.

illustrates the IRF's intertemporal estimates of carbon emissions. The findings indicate that the information transparency index, the cost of business start-up procedures, and logistical activities are all likely to have a negative effect on carbon emissions stock in many subsequent years. On the other hand, the ease of doing business, fuel imports, and green energy sources would almost certainly result in a rise in carbon stocks in many subsequent years. Environmental disclosure indexes and sustainable logistics operations would benefit future economic activities to enhance environmental quality. In contrast, the ease with which government rules are implemented, the increased reliance on non-renewable fuels, and the inefficient utilization of green energy sources negatively affect environmental quality, obstructing the global green development goal. Economies would need to use cleaner manufacturing methods and renewable energy sources to move toward long-term economic activities on a global level.

Table 4. Impulse response estimates of EPC.

illustrates the results of the VDA analysis of carbon emissions, which revealed that the ease of doing business would most likely have a higher impact on carbon emissions stock in the year 2031, with a variance error shock of 1.933% in that year. Green energy sources are projected to play a significant role in increasing economic initiatives, which significantly impact carbon emissions stock and have a variance error shock of 1.674% over time. The information transparency index was shown to have the most significant impact on carbon emissions stock over the next ten years, with a percentage shift of 1.462% in favour of a friendly working environment. According to the results, the cost of business start-up procedures on carbon emissions stock would be the least affected, with a variation shock of 1.248% over time.

Table 5. Variance decomposition analysis of EPC.

5. Discussion

The regression analysis findings presented here are consistent with those obtained in previous investigations. For instance, Karim et al. (Citation2021) suggested that global warming is a critical concern impeding the implementation of economic operations throughout the globe. To effectively quantify the amount of carbon emissions disclosure, the vulnerability of carbon emissions must be communicated to the various parties involved. Internal governance may play a critical role in decarbonization. Li et al. (Citation2021c) concluded that cleaner technologies are beneficial in reducing the negative carbon effect of business logistics operations, which is beneficial in ensuring green supply chain practices throughout the globe. Anser et al. (Citation2020b) discovered that the intelligent manufacturing process plays a critical role in enhancing supply chain management, allowing for the adoption of fuel-efficient technology and reducing carbon emissions. When it comes to mitigating carbon emissions, Razzaq et al. (Citation2021) provided valuable insights into the positive direction of green technological advancement. This information aids in reaching definitive conclusions about the level of country-based consumption of carbon emissions, which in turn leads to a more diverse impact on the overall economy. Doğan et al. (Citation2021) stressed the need to expand the use of green energy sources in the conventional energy mix to minimize carbon emissions in manufacturing, which would aid in achieving the sustainable development goal in many nations across the world. According to Koondhar et al. (Citation2021), green energy sources would positively impact environmental quality through the channels of financial development and cleaner technologies. It necessitated the development of a more developed capital market and the development of fuel-efficient, cleaner technologies to achieve green sectoral growth across the country. Saeed et al. (Citation2021) concluded that an economy's social responsibility and carbon mitigation strategies are realistic in terms of enhancing the good governance that has effectively adopted sustainable business practices throughout the globe. Sadiq et al. (Citation2022) emphasized the need to strengthen SME firms that generate new ideas and technologies throughout the manufacturing process to advance the country's sustainable development strategy. The corporate structure must fulfill the interests of its stakeholders and politicians to generate environmentally friendly goods, which will aid in the achievement of long-term commercial objectives. In their study, Garzón-Jiménez & Zorio-Grima (Citation2021) suggest that businesses' environmental disclosures ensure actions to maintain environmental quality via their pro-environmentally friendly manufacturing behavior, eventually lowering their cost of equity. As a result, these companies are more likely to be fined than the higher polluters, who have a higher equity cost of capital. Even worse, the certification of environmental sustainability reports does not promote a fair and transparent procedure. Meanwhile, it helps eliminate asymmetries in disclosure reports, which helps lower the equity cost of capital and carbon emissions. Ali et al. (Citation2020) say that the green procurement process, sustainable logistics operations, environmentally friendly manufacturing, and business process design are the most critical green enablers that help improve the environment worldwide.

6. Conclusions and policy implications

Globalization has emphasized the need to enhance economic activities that are environmentally friendly to support the country's greener goal. The study's objective is to assess the impact of different national-level economic determinants on emissions per capita by limiting fuel imports and increasing demand for renewable energy across 119 nations. The study used three regression estimators to produce unbiased and consistent parameter estimates. The findings indicate that corporate information disclosure, the cost of business start-up procedures, sustainable fuel imports, and demand for renewable energy all contribute to reducing emissions stock. In comparison, the ease of implementing environmental policies and logistics operations increases emissions stock across nations. According to the IRF's estimates, the information disclosure index, the cost of business start-up procedures, and green logistics operations would likely reduce emissions stock over the next decade. In contrast, the ease of environmental regulations, fuel imports, and low adoption of green energy sources would almost certainly increase emissions stock in the majority of the following years. According to the VDA estimates, the ease of doing business would likely have a greater impact on carbon emissions stock over time. The study made the following policy suggestions under the country's green development plan, i.e.,

Economies should strengthen their environmental disclosure information systems by implementing practical measures for eco-friendly production using green innovation technologies and green manufacturing processes. The business sector must successfully oversee economic operations while also managing ecological infrastructure via a more environmentally friendly manufacturing method. By giving information on economic policies for environmental protection, the economy needs to achieve two objectives: first, it would enjoy competitive gain over rivals, and second, it would maximize the long-term benefits of its investments.

It is also possible that the density of newly registered enterprises will grow over time due to perfect competition, resulting in greater environmental harm due to increased carbon footprints. Stricter environmental regulations would almost certainly boost economic businesses and lower the number of polluting companies throughout the globe. The command-and-control system should be well-established so that polluting businesses can be found and banned while encouraging environmentally-friendly manufacturing practices.

The national logistics infrastructure should operate according to greening principles, which necessitates a larger quantity of money for its restructuring to transfer business operations from nonrenewable to renewable fuels. It is highly desired to have sustainable logistics operations to create sustainable economic results.

The importation of nonrenewable fuels has a more considerable negative effect on the concept of sustainability than the exportation of renewable fuels. The burning of fossil fuels can harm the natural ecosystem while raising the global average temperature, resulting in disastrous periods of global warming. An energy tax would be a viable policy choice for controlling nonrenewable fuels and assisting in searching for new avenues of plentiful natural resources to develop cleaner energy fuels for healthy living, and

Using green energy sources in economic activities would provide a solid foundation for environmentally friendly manufacturing, maximizing payoffs via green innovation processes. Emissions-cap trading and carbon offsets could help cut carbon emissions by making green energy more efficient.

In order to achieve a Pareto-efficient outcome, the Polluters-Paying Principle should be applied. This will allow the economy to develop an efficient taxation policy, improve its environmental information systems, and streamline its regulatory processes toward a green developmental agenda. The study evaluated the economic determinants of national carbon emissions. The study can be extended by using the same model in firm-specific contexts to get more insights into internal and external determinants of corporate activities. Furthermore, the study can be extended to assess the given model at some country-specific or regional level to get more insights into green corporate activities. Finally, corporate governance factors can be added to firm-level data to see how companies act in the environment.

Disclosure statement

No potential conflict of interest was reported by the authors.

References

- Abbas, J. (2020). Impact of total quality management on corporate green performance through the mediating role of corporate social responsibility. Journal of Cleaner Production, 242, 118458. https://doi.org/10.1016/j.jclepro.2019.118458

- Absar, M. M. N., Dhar, B. K., Mahmood, M., & Emran, M. (2021). Sustainability disclosures in emerging economies: Evidence from human capital disclosures on listed banks’ websites in Bangladesh. Business and Society Review, 126(3), 363–378. https://doi.org/10.1111/basr.12242

- Ahmad, M., Işık, C., Jabeen, G., Ali, T., Ozturk, I., & Atchike, D. W. (2021). Heterogeneous links among urban concentration, non-renewable energy use intensity, economic development, and environmental emissions across regional development levels. The Science of the Total Environment, 765, 144527.

- Aldakhil, A. M., Nassani, A. A., Awan, U., Abro, M. M. Q., & Zaman, K. (2018). Determinants of green logistics in BRICS countries: An integrated supply chain model for green business. Journal of Cleaner Production, 195, 861–868. https://doi.org/10.1016/j.jclepro.2018.05.248

- Ali, S. S., Kaur, R., Ersöz, F., Altaf, B., Basu, A., & Weber, G. W. (2020). Measuring carbon performance for sustainable green supply chain practices: A developing country scenario. Central European Journal of Operations Research, 28(4), 1389–1416. https://doi.org/10.1007/s10100-020-00673-x

- Anser, M. K., Yousaf, S. U., Hyder, S., Nassani, A. A., Zaman, K., & Abro, M. M. Q. (2021a). Socio-economic and corporate factors and COVID-19 pandemic: A wake-up call. Environmental Science and Pollution Research International, 28(44), 63215–63226. https://doi.org/10.1007/s11356-021-15275-6

- Anser, M. K., Godil, D. I., Khan, M. A., Nassani, A. A., Askar, S. E., Zaman, K., Salamun, H., Indrianti, Y., & Abro, M. M. Q. (2021b). Nonlinearity in the relationship between COVID-19 cases and carbon damages: Controlling financial development, green energy, and R&D expenditures for shared prosperity. Environmental Science and Pollution Research, 29(4), 5648–5660. https://doi.org/10.1007/s11356-021-15978-w.

- Anser, M. K., Yousaf, Z., & Zaman, K. (2020a). Green technology acceptance model and green logistics operations: ‘To see which way the wind is blowing’. Frontiers in Sustainability, 1, 3. https://doi.org/10.3389/frsus.2020.00003

- Anser, M. K., Khan, M. A., Awan, U., Batool, R., Zaman, K., Imran, M., Indrianti, Y., Khan, A., Bakar, Z. A. (2020b). The role of technological innovation in a dynamic model of the environmental supply chain curve: Evidence from a panel of 102 countries. Processes, 8(9), 1033. https://doi.org/10.3390/pr8091033

- Awan, U. (2019). Impact of social supply chain practices on social sustainability performance in manufacturing firms. International Journal of Innovation and Sustainable Development, 13(2), 198–219. https://doi.org/10.1504/IJISD.2019.098996

- Awan, U., & Sroufe, R. (2022). Sustainability in the circular economy: Insights and dynamics of designing circular business models. Applied Sciences, 12(3), 1521. https://doi.org/10.3390/app12031521

- Awan, U., Arnold, M. G., & Gölgeci, I. (2021). Enhancing green product and process innovation: Towards an integrative framework of knowledge acquisition and environmental investment. Business Strategy and the Environment, 30(2), 1283–1295. https://doi.org/10.1002/bse.2684

- Awawdeh, A. E., Ananzeh, M., El-khateeb, A. I., & Aljumah, A. (2021). Role of green financing and corporate social responsibility (CSR) in technological innovation and corporate environmental performance: A COVID-19 perspective. China Finance Review International, 12(2), 297–316. https://doi.org/10.1108/CFRI-03-2021-0048

- Baah, C., Jin, Z., & Tang, L. (2020). Organizational and regulatory stakeholder pressures friends or foes to green logistics practices and financial performance: Investigating corporate reputation as a missing link. Journal of Cleaner Production, 247, 119125. https://doi.org/10.1016/j.jclepro.2019.119125

- Baloch, M. A., Ozturk, I., Bekun, F. V., & Khan, D. (2021). Modeling the dynamic linkage between financial development, energy innovation, and environmental quality: Does globalization matter? Business Strategy and the Environment, 30(1), 176–184. https://doi.org/10.1002/bse.2615

- Bhutto, T. A., Farooq, R., Talwar, S., Awan, U., & Dhir, A. (2021). Green inclusive leadership and green creativity in the tourism and hospitality sector: Serial mediation of green psychological climate and work engagement. Journal of Sustainable Tourism, 29(10), 1716–1737. https://doi.org/10.1080/09669582.2020.1867864

- Bose, S., Minnick, K., & Shams, S. (2021). Does carbon risk matter for corporate acquisition decisions? Journal of Corporate Finance, 70, 102058. https://doi.org/10.1016/j.jcorpfin.2021.102058

- Cadez, S., & Czerny, A. (2016). Climate change mitigation strategies in carbon-intensive firms. Journal of Cleaner Production, 112, 4132–4143. https://doi.org/10.1016/j.jclepro.2015.07.099

- Cadez, S., & Guilding, C. (2017). Examining distinct carbon cost structures and climate change abatement strategies in CO2 polluting firms. Accounting, Auditing & Accountability Journal, 30(5), 1041–1064. https://doi.org/10.1108/AAAJ-03-2015-2009

- Cadez, S., Czerny, A., & Letmathe, P. (2019). Stakeholder pressures and corporate climate change mitigation strategies. Business Strategy and the Environment, 28(1), 1–14. https://doi.org/10.1002/bse.2070

- Chang, T. W., Yeh, Y. L., & Li, H. X. (2020). How to shape an organization’s sustainable green management performance: The mediation effect of environmental corporate social responsibility. Sustainability, 12(21), 9198. https://doi.org/10.3390/su12219198

- Cheng, Y., Awan, U., Ahmad, S., & Tan, Z. (2021). How do technological innovation and fiscal decentralization affect the environment? A story of the fourth industrial revolution and sustainable growth. Technological Forecasting and Social Change, 162, 120398.

- Doğan, B., Driha, O. M., Balsalobre Lorente, D., & Shahzad, U. (2021). The mitigating effects of economic complexity and renewable energy on carbon emissions in developed countries. Sustainable Development, 29(1), 1–12. https://doi.org/10.1002/sd.2125

- Etse, D., McMurray, A., & Muenjohn, N. (2022). The effect of regulation on sustainable procurement: Organisational leadership and culture as mediators. Journal of Business Ethics, 177(2), 305–325. https://doi.org/10.1007/s10551-021-04752-0

- Fauziah, D. A., Sukoharsono, E. G., & Saraswati, E. (2020). Corporate social responsibility disclosure towards firm value: Innovation as mediation. International Journal of Research in Business and Social Science (2147- 4478), 9(7), 75–83. https://doi.org/10.20525/ijrbs.v9i7.967

- Feng, Y., Akram, R., Hieu, V. M., & Tien, N. H. (2021). The impact of corporate social responsibility on the sustainable financial performance of Italian firms: Mediating role of firm reputation. Economic Research-Ekonomska Istraživanja, 1–19. https://doi.org/10.1080/1331677X.2021.2017318

- Galant, A., & Cadez, S. (2017). Corporate social responsibility and financial performance relationship: A review of measurement approaches. Economic Research-Ekonomska Istraživanja, 30(1), 676–693. https://doi.org/10.1080/1331677X.2017.1313122

- Garanina, T., & Aray, Y. (2021). Enhancing CSR disclosure through foreign ownership, foreign board members, and cross-listing: Does it work in Russian context? Emerging Markets Review, 46, 100754. https://doi.org/10.1016/j.ememar.2020.100754

- Garzón-Jiménez, R., & Zorio-Grima, A. (2021). Effects of carbon emissions, environmental disclosures and CSR assurance on cost of equity in emerging markets. Sustainability, 13(2), 696. https://doi.org/10.3390/su13020696

- Golroudbary, S. R., Zahraee, S. M., Awan, U., & Kraslawski, A. (2019). Sustainable operations management in logistics using simulations and modelling: A framework for decision making in delivery management. Procedia Manufacturing, 30, 627–634. https://doi.org/10.1016/j.promfg.2019.02.088

- Han, S. R., Li, P., Xiang, J. J., Luo, X. H., & Chen, C. Y. (2022). Does the institutional environment influence corporate social responsibility? Consideration of green investment of enterprises—evidence from China. Environmental Science and Pollution Research, 29, 12722–12739. https://doi.org/10.1007/s11356-020-09559-6.

- Huber, P. J. (1973). Robust regression: Asymptotics, conjectures and Monte Carlo. The Annals of Statistics, 1(5), 799–821. https://doi.org/10.1214/aos/1176342503

- Jawaad, M., & Zafar, S. (2020). Improving sustainable development and firm performance in emerging economies by implementing green supply chain activities. Sustainable Development, 28(1), 25–38. https://doi.org/10.1002/sd.1962

- Karaman, A. S., Kilic, M., & Uyar, A. (2020). Green logistics performance and sustainability reporting practices of the logistics sector: The moderating effect of corporate governance. Journal of Cleaner Production, 258, 120718. https://doi.org/10.1016/j.jclepro.2020.120718

- Karim, A. E., Albitar, K., & Elmarzouky, M. (2021). A novel measure of corporate carbon emission disclosure, the effect of capital expenditures and corporate governance. Journal of Environmental Management, 290, 112581.

- Khan, R., Awan, U., Zaman, K., Nassani, A. A., Haffar, M., & Abro, M. M. Q. (2021). Assessing hybrid solar-wind potential for industrial decarbonization strategies: Global shift to green development. Energies, 14(22), 7620. https://doi.org/10.3390/en14227620

- Khan, S. A. R., Zhang, Y., Kumar, A., Zavadskas, E., & Streimikiene, D. (2020). Measuring the impact of renewable energy, public health expenditure, logistics, and environmental performance on sustainable economic growth. Sustainable Development, 28(4), 833–843. https://doi.org/10.1002/sd.2034

- Koondhar, M. A., Shahbaz, M., Ozturk, I., Randhawa, A. A., & Kong, R. (2021). Revisiting the relationship between carbon emission, renewable energy consumption, forestry, and agricultural financial development for. Environmental Science and Pollution Research, 28(33), 45459–45473. https://doi.org/10.1007/s11356-021-13606-1

- Kozenkova, T. A., Abalakina, T. V., Suleymanov, Z. E., Bank, S. V., Sokolnikova, O. B. (2021). Customs and logistics activity in geopolitical and economic changes: Problems, strategies, and risks. In Bogoviz A. V., Suglobov A. E., Maloletko A. N., Kaurova O. V., Lobova S. V. (eds.) Frontier information technology and systems research in cooperative economics. Studies in systems, decision and control, vol 316. Springer. https://doi.org/10.1007/978-3-030-57831-2_118

- Kraus, S., Rehman, S. U., & García, F. J. S. (2020). Corporate social responsibility and environmental performance: The mediating role of environmental strategy and green innovation. Technological Forecasting and Social Change, 160, 120262. https://doi.org/10.1016/j.techfore.2020.120262

- Li, D., & Wang, L. F. (2021). Does environmental corporate social responsibility (ECSR) promote green product and process innovation? Managerial and Decision Economics. https://doi.org/10.1002/mde.3464

- Li, Z., Tang, Y., Wu, J., Zhang, J., & Lv, Q. (2020a). The interest costs of green bonds: Credit ratings, corporate social responsibility, and certification. Emerging Markets Finance and Trade, 56(12), 2679–2692. https://doi.org/10.1080/1540496X.2018.1548350

- Li, D., Tang, F., & Zhang, L. (2020b). Differential effects of voluntary environmental programs and mandatory regulations on corporate green innovation. Natural Hazards, 103(3), 3437–3456. https://doi.org/10.1007/s11069-020-04137-y

- Li, J., Anser, M. K., Tabash, M. I., Nassani, A. A., Haffar, M., & Zaman, K. (2021a). Technology-and logistics-induced carbon emissions obstructing the Green supply chain management agenda: Evidence from 101 countries. International Journal of Logistics Research and Applications, 1–25. https://doi.org/10.1080/13675567.2021.1985094

- Li, X., Sohail, S., Majeed, M. T., & Ahmad, W. (2021b). Green logistics, economic growth, and environmental quality: Evidence from one belt and road initiative economies. Environmental Science and Pollution Research International, 28(24), 30664–30674. https://doi.org/10.1007/s11356-021-12839-4

- Li, Z., Wei, S. Y., Chunyan, L., N. Aldoseri, M. M., Qadus, A., & Hishan, S. S. (2021c). The impact of CSR and green investment on stock return of Chinese export industry. Economic Research-Ekonomska Istraživanja, 1–17. https://doi.org/10.1080/1331677X.2021.2019599

- Magazzino, C., Alola, A. A., & Schneider, N. (2021). The trilemma of innovation, logistics performance, and environmental quality in 25 topmost logistics countries: A quantile regression evidence. Journal of Cleaner Production, 322, 129050. https://doi.org/10.1016/j.jclepro.2021.129050

- Muralidharan, K. (2021). Lean, green, and clean quality assessment models. In Sustainable development and quality of life. Springer. https://doi.org/10.1007/978-981-16-1835-2_5

- Nguyen, T. D., & Ngo, T. Q. (2021). The role of technological advancement, supply chain, environmental, social, and governance responsibilities on the sustainable development goals of SMEs in Vietnam. Economic Research-Ekonomska Istraživanja, 1–23. https://doi.org/10.1080/1331677X.2021.2015611

- Razzaq, A., Wang, Y., Chupradit, S., Suksatan, W., & Shahzad, F. (2021). Asymmetric inter-linkages between green technology innovation and consumption-based carbon emissions in BRICS countries using quantile-on-quantile framework. Technology in Society, 66, 101656. https://doi.org/10.1016/j.techsoc.2021.101656

- Rehman, A., Ma, H., Chishti, M. Z., Ozturk, I., Irfan, M., & Ahmad, M. (2021). Asymmetric investigation to track the effect of urbanization, energy utilization, fossil fuel energy and CO2 emission on economic efficiency in China: Another outlook. Environmental Science and Pollution Research, 28(14), 17319–17330. https://doi.org/10.1007/s11356-020-12186-w

- Rousseeuw, P. J., & Yohai, V. J. (1984). Robust regression by means of S-estimators. In Franke, J., Härdle, W., & Martin, D. (eds.), Robust and nonlinear time series, lecture notes in statistics No. 26. Springer-Verlag.

- Sadiq, M., Nonthapot, S., Mohamad, S., Ehsanullah, S., & Iqbal, N. (2022). Does green finance matter for sustainable entrepreneurship and environmental corporate social responsibility during COVID-19? China Finance Review International, 12(2), 317–333. https://doi.org/10.1108/CFRI-02-2021-0038

- Saeed, A., Noreen, U., Azam, A., & Tahir, M. S. (2021). Does CSR governance improve social sustainability and reduce the carbon footprint: International evidence from the energy sector. Sustainability, 13(7), 3596. https://doi.org/10.3390/su13073596

- Sasmoko, M. S. L., Aziz, A. R. A., Bandar, N. F. A., Embong, R., Jabor, M. K., Anis, S. N. M., & Zaman, K. (2021). Health-care preventive measures, logistics challenges and corporate social responsibility during the COVID-19 pandemic: Break the ice. Foresight. https://doi.org/10.1108/FS-05-2021-0098

- Úbeda-García, M., Claver-Cortés, E., Marco-Lajara, B., & Zaragoza-Sáez, P. (2021). Corporate social responsibility and firm performance in the hotel industry. The mediating role of green human resource management and environmental outcomes. Journal of Business Research, 123, 57–69. https://doi.org/10.1016/j.jbusres.2020.09.055

- Uyar, A., Karaman, A. S., & Kilic, M. (2020). Is corporate social responsibility reporting a tool of signaling or greenwashing? Evidence from the worldwide logistics sector. Journal of Cleaner Production, 253, 119997. https://doi.org/10.1016/j.jclepro.2020.119997

- World Bank (2021). World development indicators. World Bank.

- Yohai, V. J. (1987). High breakdown-point and high efficiency robust estimates for regression. The Annals of Statistics, 15(2), 642–656. https://doi.org/10.1214/aos/1176350366

- Yu, Y., Zhu, W., & Tian, Y. (2021). Green supply chain management, environmental degradation, and energy: Evidence from Asian countries. Discrete Dynamics in Nature and Society, 2021, 1–14. https://doi.org/10.1155/2021/5179964

- Yu, Z., Khan, S. A. R., & Liu, Y. (2020). Exploring the role of corporate social responsibility practices in enterprises. Journal of Advanced Manufacturing Systems, 19(03), 449–461. https://doi.org/10.1142/S0219686720500225

- Zhang, M., The Cong, P., Sanyal, S., Suksatan, W., Maneengam, A., & Murtaza, N. (2022). Insights into rising environmental concern: Prompt corporate social responsibility to mediate green marketing perspective. Economic Research-Ekonomska Istraživanja, 1–17. https://doi.org/10.1080/1331677X.2021.2021966

- Zhou, G., Sun, Y., Luo, S., & Liao, J. (2021). Corporate social responsibility and bank financial performance in China: The moderating role of green credit. Energy Economics, 97, 105190. https://doi.org/10.1016/j.eneco.2021.105190

Appendix A

Table A1. List of countries.