?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The purpose of this article is to analyse the impact of partisan conflict on bank credit, and take the global financial crisis as the time node to analyse the variability of this impact before and after the financial crisis. This article examines the impacts of partisan conflict on the bank credit by employing the US data covering the past 40 years and captures the variability in the effects of partisan conflict based on the rolling sample and time-varying parameter VAR analysis. The full sample results reveal that one standard deviation partisan conflict shock will shrink the bank credit growth rate to nonfinancial sectors, and the negative effects of partisan conflict on bank credit are more substantial after the global financial crisis. The rolling sample and time-varying parameter VAR analysis further confirm that the impacts of partisan conflict shock have varied substantially over time, where bank credit still negatively reacts to the impacts of partisan conflict in recent periods. Additionally, we estimate two extended models and support the intermediate role of economic policy uncertainty in transmitting the partisan conflict and the substitution effect of cross-border bank lending on domestic bank credit. Finally, our major results are unchanged by performing a series of robustness checks. The conclusion of this article is that partisan conflict has a significant impact on bank credit and shows obvious variability, which is more significant after the global financial crisis.

1. Introduction

Political polarization is not a new phenomenon in American politics. In economic theory, this kind of polarization is an exogenous shock in the real business cycle (RBC) model to understand the fluctuations in economic variables in addition to the traditional productivity shock (Azzimonti and Talbert, Citation2014). The shifts in political ideology or political disagreements indicate partisan conflictFootnote1, which has been emphasized by recent literature (Jiang and Shi, Citation2018; Azzimonti, Citation2018, Citation2019) that the growing partisan conflict will generate complex effects on economic activities. Following a seminal work by Azzimonti (Citation2014) constructs a novel textual data from the coverage frequency of newspaper, subsequent studies quantitatively examine the potential economic and financial impacts of partisan conflict shock from distinct aspects, such as private investment, bilateral trade (Jiang and Shi, Citation2018), foreign direct investment, investors’ behaviours, and international spillovers of US partisan conflict to euro area (Cheng et al., Citation2016). In this article, we study how partisan conflict affects bank credit in a structural vector autoregression (SVAR) framework and capture the variability in the effects of partisan conflict shock through the rolling sample and time-varying parameter vector autoregression model. Our empirical model is especially suitable for addressing the following unresolved research issues.

First, why we should care about the responses of bank credit to partisan conflict? In theory, the investment activity will be subjected to a strong cash flow constraint when the bank credit, as an external source of investment, declines significantly in the face of higher partisan conflict (Ivashina and Scharfstein, Citation2010; Cingano et al., Citation2016). In empirics, although the negative effects of partisan conflict on investment have been confirmed empirically, the issue that how partisan conflict affects bank credit fails to be investigated thoroughly. Azzimonti (Citation2014) concludes that the decrease in investment in response to partisan conflict is persistent, and investment only recovers after eight quarters (around two years). Azzimonti (Citation2018) further decomposes the investment into three components: fixed residential and non-residential investment and inventory changes. The overall impacts of partisan conflict shock on three components of investment are negative, regardless of the existence of the Global Financial Crisis (2007-2009). Azzimonti (Citation2021) provides a signal channel in understanding how partisan conflict influences investment decisions through the institutional environment and tax reforms. Based on a Bayesian learning model, Azzimonti (Citation2021) shows that an increase in the partisan conflict index reduces expected returns and induces lower investment, even though there is no change in macroeconomic fundamentals.

The purpose of this article is to establish a correlation channel between partisan conflict and bank credit, and interpret the impact of political differentiation on the economic and financial fields by analyzing the impact of partisan conflict on bank credit. Therefore, this article sets the following research hypotheses: first, partisan conflict has a negative impact on bank credit. Second, the impact of partisan conflict on bank credit is variable.

2. Literature Survey

The research of this article involves the interweaving of partisan conflict, GDP, bank credit and other issues. The research results of the relationship between them are of reference significance to our work.

Batrancea (Citation2020) took 10 countries in central and Eastern Europe as the research object and confirmed that net savings had an impact on GDP growth in these countries. Similar research work has been carried out in India, Brazil, Romania and other countries. Non-performing loans, carbon dioxide emissions, bank credit and inflation have become the influencing factors of GDP growth (Batrancea, Citation2020). In addition, official corruption (Batrancea, Citation2018) and citizens’ tax attitude (Batrancea, Citation2012, 2015, 2019, Citation2021) will also have an impact on GDP growth. At the same time, Batrancea (2009, Citation2013) also pointed out that many crises facing the global banking system will affect the development of the world economy. He further studied the characteristics, causes and solutions of the banking system crisis.

A bulk of existing studies uncovers that partisan conflict will affect the firms’ decisions and cross-border capital flows, including cash holdings at the aggregate and firm levels, asset price, and foreign direct investment in response to higher partisan conflict, few attempts to critically evaluate the responses of bank credit to partisan conflict. Hankins et al. (Citation2016) use a sign restrictions approach to identify structural shocks to partisan conflict and uncover that corporate managers actively react to political disagreement, which further results in a higher cash-to-total assets ratio. Furthermore, Cheng et al. (Citation2018) distinguishes political uncertainty proxied by partisan conflict from policy uncertainty shock and demonstrate that partisan conflict will drive corporate to hold more cash and delay investment to any business decisions for satisfying the precautionary motive. Gupta et al. (Citation2018) unveil that a larger partisan conflict tends to predict lower stock market volatility because the risk of policy change declines with a divided government. Gupta et al. (Citation2019) considers a quartile SVAR model conditional on an increase in partisan conflict and studies the impact of fiscal policy on asset price as well as the reverse channel. Their empirical results show that partisan conflict does not significantly affect the relationships between the fiscal surplus to GDP and housing and equity return but partisan conflict affects the actual implementation of fiscal policy actions. Azzimonti (Citation2019) supports the view that partisan conflict does deter FDI inflows to the US. Therefore, the financial outcomes of partisan conflict have been discussed extensively; however, the impact of partisan conflict on bank credit is still a research gap.

Based on the extant empirical evidence, the propagation channel from partisan conflict to bank credit has been established implicitly but is never explicitly examined through a rigorous empirical framework. Azzimonti and Talbert (Citation2014) document that intensified partisan conflict is associated with high volatility of fiscal policy and further increases economic policy uncertainty. Bordo et al. (Citation2016) link the economic policy uncertainty and bank loan through the lens of aggregate and bank-level autoregression model of real bank loan growth and conclude that economic policy uncertainty has a significant negative effect on bank credit growth. Therefore, existing literature has already established an indirect channel from partisan conflict to bank lending behaviours through the role of economic policy uncertainty. In this study, we will perform a formal analysis to link the nexus between partisan conflict and bank credit to provide more empirical evidence for this relationship.

Throughout the study, we systematically examine the impacts of partisan conflict on the bank credit in the US in a unified structural framework and split the full sample into two parts: pre- and post-global financial crisis (2007-2009, GFC) to explore whether the bank credit in responses to partisan conflict changes due to the outbreak of the GFC. Besides, we attempt to capture the time-varying impacts of partisan conflict on the bank credit through the rolling sample analysis. It is worth noting that the rolling sample VAR model is more tractable than the time-varying parameter VAR model (TVP-VAR) to some extent because we do not need to impose strict assumptions for a prior parameter space. Consistent with Choi (Citation2017), to complement the results of the rolling sample VAR model, we still estimate the main findings utilizing a TVP-VAR model with stochastic volatility developed by Primiceri (Citation2005) and Nakajima (Citation2011), which enables us to capture possible changes in the underlying structure of the economy in a flexible and robust manner. Furthermore, we consider the intermediate role of economic policy uncertainty in transmitting the partisan conflict shock and the substitutability of cross-border bank lending to domestic bank credit for comprehensive the underlying mechanism and opposite force from partisan conflict to the dynamics of bank credit.

A number of salient facts emerge from our analysis. The full sample analysis shows that one standard deviation partisan conflict shock will shrink the bank credit growth rate to nonfinancial sectors around 0.06% in the peak. By further decomposing the sample into two components, we find that the negative impacts of partisan conflict on bank credit are more substantial after the global financial crisis. Besides, in the post-GFC periods, partisan conflict accounts for more movements in bank credit compared to the pre-GFC periods. The rolling sample and time-varying parameter VAR analysis further confirm that the impacts of partisan conflict shock have varied substantially over time, where bank credit still negatively reacts to the impacts of partisan conflict in recent periods. We also conduct two extended models incorporating the indirect channel and substitute effects on bank credit and conclude that two extended models support the intermediate role of economic policy uncertainty and the substitutability of cross-border bank lending. Finally, our empirical results are unchanged by performing a series of robustness checks.

Our article has three major contributions. First, our article fills the research gap related to the bank credit in response to an unexpected increase in partisan conflict. More importantly, we uncover the heterogeneous impacts of partisan conflict in pre- and post-GFC and time-varying effects of partisan conflict on bank credit. Second, bank credit as a non-negligible external financing channel complements the research on understanding the dynamic behaviours of private investment (Azzimonti, Citation2014; Citation2018; Citation2021). Third, this article formally establishes the direct channel from partisan conflict to bank credit, which is ignored by previous literature (Azzimonti and Talbert, Citation2014; Bordo et al., Citation2016).

This article is organized along the following lines. Section 2 presents and discusses the empirical strategy incorporating the SVAR model, rolling the sample VAR model, and time-varying parameter VAR model. Section 3 explains the variable selection and data source. Section 4 investigates the main empirical results with the help of impulse responses and variance decompositions from various VAR models. The last section concludes this article.

3. Theoretical Framework and Empirical Method

3.1. Theoretical framework

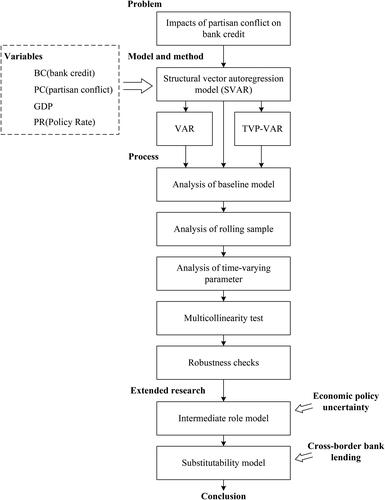

The purpose of this article is to analyse the impact of partisan conflict on bank credit and the variability of this impact. In order to complete this work, this article uses structural vector autoregressive model (SVAR) as the research tool, collects sample data with variables such as bank credit, party conflict, GDP and policy interest rate, successively completes baseline model analysis, rolling sample analysis, time-varying parameter analysis, multicollinearity test and robustness check, and then draws the final conclusion through extended research, The whole theoretical framework of this article is shown in .

Figure 1. Theoretical framework.

Source: authors.

The vector autoregressive model (VAR) only describes the statistical description of the dynamic relationship between multiple variables. Although we mentioned in the impulse response analysis that the order of each variable in the establishment of the VAR model may have a great impact on the impulse response analysis. However, we have never clearly described the meaning of economic structure between endogenous variables involved in VAR model system.

There is no clear structural relationship between economic variables, which is a deficiency of VAR model, especially unconstrained VAR model.

The emergence of structural vector autoregressive model (SVAR) solves this problem to a certain extent. The so-called structural vector autoregressive model, as its name indicates, can capture the instantaneous structural relationship between various variables in the model system.

3.2. Structural Vector Autoregression (SVAR) Model

Following Bordo et al. (Citation2016), Azzimonti (Citation2018) and Cheng et al. (Citation2018), the structural vector autoregression is specified as follows:

(1)

(1)

where

in our baseline model. PC is the partisan conflict index expressed in log transformation, PR is the central bank policy rate, GDP is the real GDP growth rate, BC is the growth rate of bank credit to the private nonfinancial sector.

is the coefficient matrix and

is a vector of structural shocks. We also consider two extended models in our subsequent analysis. In the first extended model, we include economic policy uncertainty (EPU) index, then

Also, we consider the second extended model with the substitutability of cross-border bank lending (CBL), so we have

The optimal lag order

is 4 to capture the potential seasonality in our model. We impose a choice of the Cholesky order and set

in our baseline model. This kind of Cholesky order assumes that partisan conflict is independent of other variables but bank credit will be affected by the other three variables with contemporaneous and lagged effects. Assuming that

is a lower triangular matrix,

The reduced-form representation is expressed as follows:

(2)

(2)

where

and

so the matrix

maps the structural shocks

into the reduced-form residuals

and

where

is the standard deviation of each of the identified structural shocks. Follow the reduced-form VAR model, the baseline specification for the bank credit is:

(3)

(3)

3.3. Rolling Sample VARs

For the rolling sample VAR model, we follow the empirical specification prosed by Choi (Citation2017) and estimate the VAR model with the initial sample (10 years = 40 quartersFootnote2). The subsequent VARs add one observation value at a time and drop an initial observation to keep the constant window length. The sample length in our article is from 1981Q1 to 2018Q4, therefore, the sequences of rolling sample VARs is specified as follows:

(4)

(4)

Choi (Citation2017) points out two advantages of the VAR model with rolling samples. This approach not only allows the estimation of dynamic trends of unknown parameters in a simple way but avoids strong assumptions in terms of intensive parameters specified as the TVP-VAR model. For the SVAR model, we can plot the two dimensions (horizons and responses) and for the rolling sample model, it is possible for us to draw the three dimensions (time, horizons, and responses) to visualize the time-varying patterns of impulse responses.

3.4. Time-varying parameter VAR (TVP-VAR)

We utilize the TVP-VAR model with stochastic volatility proposed by Primiceri (Citation2005) and Nakajima (Citation2011) to confirm the pattern of variability in the responses of the bank credit to partisan conflict using the rolling sample VARs. The model is considered as follows:

(5)

(5)

where

is the lower triangular matrix and

is the diagonal matrix. By rewriting the model (5), then we have:

(6)

(6)

Here, where the symbol

represents the Kronecker product. Because all parameters have a time subscript, thus the coefficients

and the parameters

and

are all time varying. Let

be the vector of non-zero and non-one elements of matrix

(stacked by row) and

be the vector of elements of matrix

The dynamics of the model’s time-varying parameters are specified as follows:

where

All the innovations in the TVP-VAR model are assumed to be jointed normally distributed by imposing an assumption on the variance-covariance matrix:

where

is an

identity matrix, while Q, S, and T are positive definite matrices. Refer to Primiceri (Citation2005) and Nakajima (Citation2011), we further assume that the shocks to the innovations of the time-varying parameters are uncorrelated among the parameters

and

which improves the efficiency of the sampling algorithm. The Markov chain Monte Carlo method is employed for the estimation of the TVP-VAR models with stochastic volatility as described in Primiceri (Citation2005) and Nakajima (Citation2011). In the later estimation, we draw 10000 samples to compute the posterior estimates after abandoning the initial 1000 samples as a burn-in period for convergence.

4. Data Sources and Variables

The US partisan conflict index (PC) is maintained and provided by the Federal Reserve Bank of Philadelphia based on the research of Azzimonti (Citation2014). This index belongs to the textual data constructed from the coverage frequency of major newspapers published in the US. According to the definition of partisan conflict mentioned above, this index reflects the degree of political disagreement and political uncertainty among U.S. politicians at the federal level. Azzimonti (Citation2014) points out that the search procedure captures disagreement not only about economic policy (e.g., related to budgetary decisions, tax rates, deficit levels, welfare programs, etc.), but also about private-sector regulation (e.g., financial and immigration reform), national defense issues (e.g., wars, terrorism), and other dimensions that divide policymakers’ views (e.g., same-sex marriage, gun control, abortion rights, among others). It is worth noting that partisan conflict (political uncertainty) and economic policy uncertainty are fundamentally different but exist the potential transmission channel from the former to the latter (Azzimonti, Citation2018).

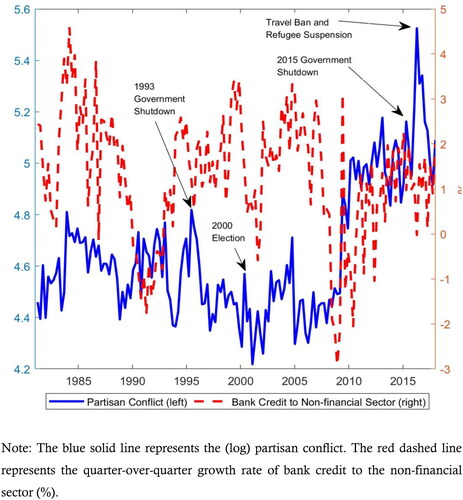

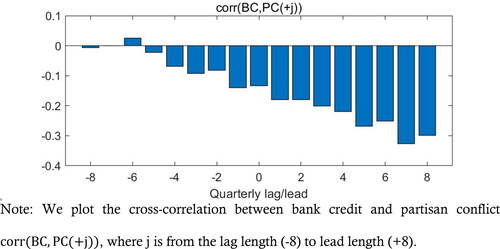

Bank credit to the private nonfinancial sector is collected from the database of Bank for International Settlements (BIS). The cross-border bank lending is collected from locational banking statistics updated by the BIS. We calculate the quarter-over-quarter growth rate of bank credit and cross-border bank lending in our empirical analysis. plots the time trends of the growth rate of bank credit to nonfinancial sectors and partisan conflict. We label four significant political events that potentially cause higher partisan conflict, including the 1995 and 2003 federal government shutdown, 2000 election, as well as the travel ban and refugee suspension enforced by Trump government in 2017. For the partisan conflict, we discover a marked structural jump in the partisan conflict. It is evident that higher partisan conflict tends to lower the bank credit growth rate and the correlation coefficient is −0.1355. exhibits the dynamic correlations between partisan conflict and bank credit growth rate. Refer to the business cycle literature, we find significant negative correlations between bank credit growth rate and lags of the partisan conflict index, with a stable correlation of 0.3 after four quarters.

Figure 2. Evolution of bank credit to nonfinancial sectors and partisan conflict.

Source: authors.

Figure 3. Dynamic correlations between partisan conflict and bank credit.

Source: authors.

The central bank policy rate is also collected from the BIS. We should notice that the US effective fed funds rate is a proxy of the central bank policy rate before 1985 and the mid-point of the Federal Reserve target rate becomes the proxy of the central bank policy rate after 1985. In the robustness checks, we replace the central bank policy rate by the bank prime loan rate (lending rate) collected from Federal Reserve Economic Data, which is the rate posted by a majority of the top 25 (by assets in domestic offices) insured U.S.-chartered commercial banks. Prime is one of several base rates used by banks to price short-term business loans.

We also have the real GDP growth rate from the Federal Reserve Economic Data and economic policy uncertainty index from https://www.policyuncertainty.com/ updated on the basis of Baker et al. (Citation2016)’s approach. The definition, source, and extra note of all variables are summarized in .

Table 1. Sources and definition of variables.

The sample period is from 1981Q1 to 2018Q4 for all variables excluding cross-border bank lending, which spans from 1995Q4 to 2018Q4. In the rolling VAR model, the first sample period is 1981Q1-1990Q4 and the subsequent VARs add one observation each time and drop an initial observation to keep the window size remains fixed (40 quarters). For the second extended model with cross-border bank lending, the first sample period is 1995Q4-2005Q3. The summary statistics for all variables in our model are reported in .

Table 2. Summary statistics.

5. Empirical Results and Analysis

In this section, we first discuss the results of the baseline model, rolling sample and time-varying parameter vector autoregression models, and then investigate two extended models. Finally, we perform a battery of robustness checks to show that the empirical results do not depend on the particular model specification or variable selection.

5.1. Results of the Baseline Model

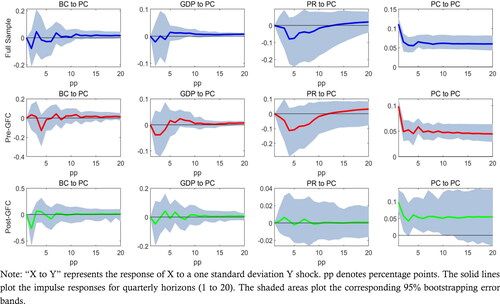

To analyse how bank credit reacts to partisan conflict shock, we estimate the SVAR(4) model as described in the empirical strategy and then calculate the impulse responses. The estimated responses to a one standard deviation positive shock to partisan conflict (PC) are exhibited in . Follow the empirical specification as Wang (Citation2014), we also divide the full sample into two subsamples: pre- and post-GFC. To eliminate the potential biasedness caused by the government regulations during the great recession periods, we remove the great recession periods from 2007Q4 to 2009Q2. Therefore, the pre-GFC periods are from 1981Q1 to 2007Q3 and the post-GFC periods are from 2009Q3 to 2018Q4. It is evident that the magnitude of the PC shock is around 0.06 (the value at time 0) in . We consider the impulse responses up to 20 quarters and plot the estimates along with the 95% error bands.

Figure 4. Impulse responses: partisan conflict shock.

Source: authors.

In the full sample analysis, one standard deviation partisan conflict shock will shrink the bank credit growth rate to nonfinancial sectors around 0.06% in the peak. Although the partisan conflict will lift up the bank credit growth rate temporarily in the third period, the overall impacts of partisan conflict on bank credit are negative.

To understand the contribution of the partisan conflict shock in the empirical model, we also perform a variance decomposition of the variables contained in the VAR system at different horizons. reports the forecast error variance decomposition for the baseline model at three prediction horizons quarters. We only compare the empirical results at the prediction horizon

In the full sample analysis, the partisan conflict seems only explain around 1% movements in bank credit and central bank policy rate and 0.5% fluctuations in GDP. However, when we turn to consider the subsample analysis, it is obvious that the contribution of partisan conflict to bank credit and GDP substantially increases. Specifically, in the post-GFC periods, the partisan conflict shock accounts for more than 10% fluctuations in bank credit and 4% fluctuations in GDP. Therefore, the importance of partial conflict in shaping the bank decisions and aggregate macroeconomy at business cycle frequencies increases after the global financial crisis.

Table 3. Forecast error variance decomposition.

5.2. Results of Rolling Sample VARs

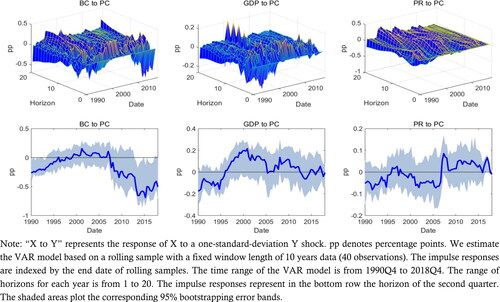

To further capture the time-varying impacts of partisan conflict on bank credit and shed light on this effect, we rely on the rolling sample VARs. To visualize the time-varying patterns of impulse responses, we plot the three dimensions to illustrate the complete picture.

Following our empirical specification, we estimate the VAR model based on a rolling sample with a fixed window length of 10 years data (40 observations). visualizes the dynamic responses that are indexed by the end date of rolling samples. The time range of the VAR model is from 1990Q4 to 2018Q4. The range of horizons for each year is from 1 to 20. In the bottom row, the impulse responses as a snapshot represent the horizon of the second quarter. The shaded areas plot the corresponding 95% bootstrapping error bands.

Figure 5. Impulse responses from rolling sample VARs.

Source: authors.

The three dimensions of impulse response intuitively present the dynamic impacts of partisan conflict on bank credit, GDP, and policy rate. For the bank credit growth rate, we can divide the sequences of responses into three periods: before 1999, between 1999 and 2007, after 2007. In the first and third subperiods (before 1999 and after 2007), partisan conflict shrinks the bank credit growth rate and this contractionary effect becomes more significant after 2007. Between 1999 and 2007, the partisan conflict fails to generate a marked negative effect on the bank credit growth rate, which to some extent reflects the economic prosperity and optimistic investor motivation before the GFC. Furthermore, the time-varying responses of GDP and central bank policy rate can be clearly divided into two subsamples. It is worth noting that the empirical results obtained from the rolling sample VARs are consistent with the subsample analysis in the pre- and post-GFC periods.

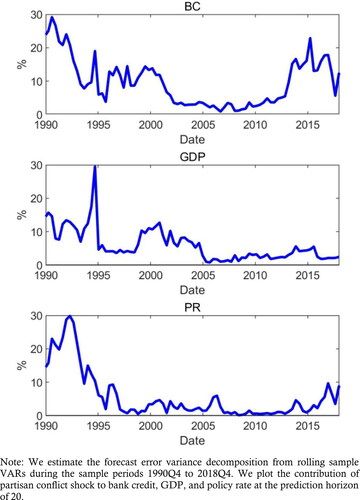

presents the forecast error variance decomposition from the rolling sample VARs during the sample periods 1990Q4 to 2018Q4. From the top to the bottom, we plot the contribution of partisan conflict shock to bank credit, GDP, and policy rate at the prediction horizon of 20. Here, we only focus on how partisan conflict contributes to the movements in bank credit. It is clear that the importance of partisan conflict shock in explaining bank credit is greater before 2000 and after 2014. Contrary to the periods of significant impacts, during the sample periods between 2000 and 2014, partisan conflict shock only accounts for less than 2% fluctuations in bank credit. We should notice that this dynamic pattern is ignored in , no matter the full sample analysis or the subsample analysis. By combining with the impulse responses based on rolling sample analysis, we can conclude that partisan conflict will explain more bank credit during the periods when the responses to partisan conflict shock are negative.

Figure 6. Forecast error variance decomposition from rolling sample VARs.

Source: authors.

5.3. Results of TVP-VAR

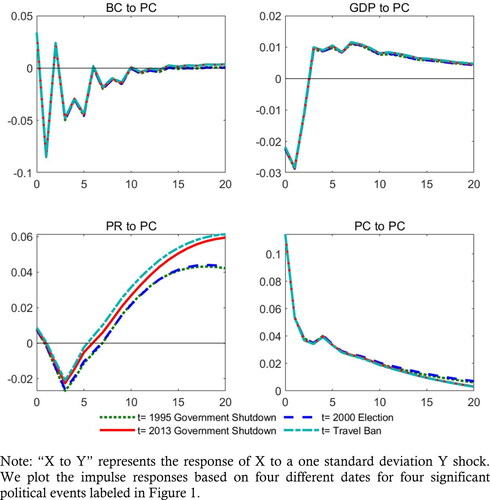

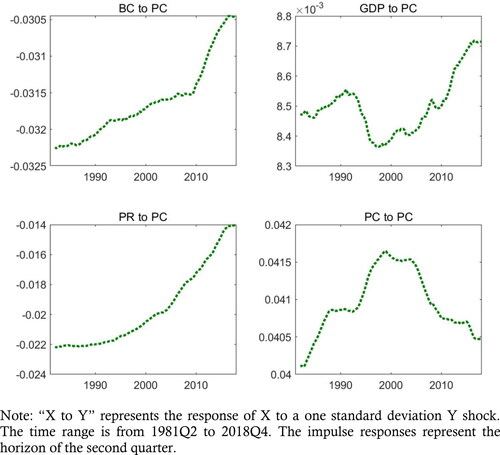

In this section, we estimate a TVP-VAR model with stochastic volatility to examine whether the results using a more tightly parameterized model corroborate the evidence from the nonparametric rolling sample VARs. To focus on the time-varying responses of the bank credit to partisan conflict shock, we consider the responses at different horizons by fixing an initial shock size from the particular political events and the responses over time by fixing the predication horizons at the second quarter. Although we cannot directly compare the results from the TVP-VAR model with those from the sample-split (Choi, Citation2017), the sign and the relative magnitude of the responses in and are largely consistent with the evidence from the full sample analysis in and rolling sample analysis in .

Figure 7. Impulse responses from TVP-VAR: four different dates.

Source: authors.

Figure 8. Impulse response from TVP-VAR: horizon fixed.

Source: authors.

shows the reactions of bank credit, GDP, and policy rate by giving an increase in partisan conflict shock at four different times. In particular, we consider the 1995 and 2013 federal government shutdown, 2000 presidential election, and 2017 travel bank and refugee suspension. First, although we choose different political events that occur in different times, the impulse responses at different horizons exhibit a similar trend. Specifically, an increase in partisan conflict shock decreases the overall growth rate of bank credit during the sample periods and causes the maximum reduction in the bank credit growth rate by around 0.09% percentage point. For other major variables in our model, the partisan conflict shock acts as a negative shock deteriorates the GDP growth rate and lowers the effective fed funds rate.

presents the posterior mean responses in the three macroeconomic variables at the 2-quarter horizon. The changing responses in the macroeconomic variables obtained using the TVP-VAR model show a similar trend to the rolling sample VARs, albeit with more gradual changes. This finding is mainly due to the random walk assumption in the TVP-VAR model that characterizes the process for time-varying parameters (Primiceri, Citation2005; Nakajima, Citation2011; Choi, Citation2017). Consistent with the pattern in the rolling sample VARs, bank credit tends to decrease in response to partisan conflict shocks in the earlier periods, while the bank credit increases in response to higher partisan conflict during the periods 2000-20107 in the rolling sample VARs. On the whole, both approaches imply a consistent pattern of the variation in the impacts of partisan conflict shocks over time in the US economy. In addition, the variability in the GDP response is also in line with the evidence from rolling sample VARs. An exception is the central bank policy rate, the negative effect on the policy rate of partisan conflict shock clearly has decreased over time in the TVP-VAR estimation framework but the central bank policy rate will be elevated in recent periods based on the empirical evidence from the rolling sample VAR model.

5.4. Multicollinearity Test

Due to the design of the regression model and data, there is likely to be a certain degree of linear relationship between the explanatory variables of the model. The problem of multicollinearity between related variables is likely to lead to the failure of the regression model of empirical analysis and the inaccuracy of the final result. Specifically, a slight change in the observed value of a sample, an increase or decrease in the number of explanatory variables may change the estimated value of the parameters of the model, which will have a serious impact, so it cannot correctly reflect the impact of the explanatory variables on the explained variables. Therefore, the collinearity test was carried out on the samples, and the results are shown in .

Table 4. Multicollinearity test results.

It can be seen from the test results that the characteristic root of each variable does not have a value close to 0 in dimension 3 or 4, and there is no item with condition index greater than 30. Therefore, the test passes, and the correlation of variables is low, indicating that the fitting degree of regression model is high.

5.5. Robustness Checks

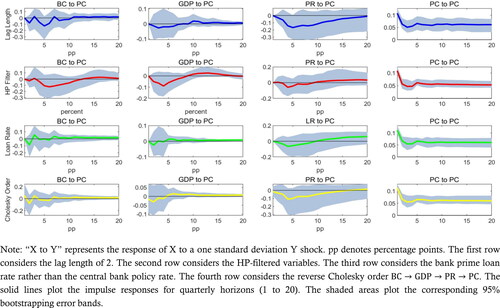

In this section, we perform a series of robustness checks based on the baseline model to confirm our empirical results more rigorously. Specifically, the first robustness uses a different lag length of 2 rather than 4 in the baseline model. The second robustness considers the HP-filtered bank credit and GDP variables rather than the quarter-over-quarter growth rate. The third robustness chooses a different proxy variable of the bank prime loan rate rather than the central bank policy rate. The last robustness considers the reverse Cholesky order Similar to the preceding analysis, the solid lines plot the impulse responses for quarterly horizons (1 to 20). The shaded areas plot the corresponding 95% bootstrapping error bands. displays the complete results of robustness checks. Obviously, our empirical results are insensitive to different variable selections, model specifications, and variable transformations. Although the magnitudes of impulse responses are distinct, the directions of responses keep consistent. Hence, our conclusions in the baseline model are mostly robust under various scenarios.

6. Discussion

6.1. Comparison of Baseline Model Analysis Results with Others

In the analysis results of the baseline model, the conclusion of this article is that the impact of party conflict on bank credit is negative as a whole, but there will be incentive effect in some stages.

Theoretically, higher political disagreement will deteriorate the bank credit activity due to two reasons. First, higher political disagreement indicates more uncertain political ideology (Cheng et al., Citation2018) and results in the efficacy of government policy (Gupta et al., Citation2019), therefore, private investment will inevitably decrease in the face of higher partisan conflict, which means the demand of bank credit declines. Second, the lending incentives of the commercial banks also lower during the higher partisan conflict periods, which imply less supply of bank credit.

We are also interested in knowing the effects of partisan conflict on other endogenous variables. The real GDP growth rate declines in response to a higher partisan conflict, which keeps consistent with Azzimonti (Citation2014; Citation2018) and Cheng et al. (Citation2016). This decrease is persistent, with the real GDP growth rate recovering after five quarters. The central bank also cuts the policy rate in response to a higher partisan conflict as Cheng et al. (Citation2016; Citation2018) and this decrease is more persistent compared to the real GDP growth rate and bank credit growth rate, with policy rate only recovering after 12 quarters (close to three years).

When we turn to discuss the impacts of partisan conflict before and after the global financial crisis, the response dynamics to the partisan conflict are more nuanced. First, the real GDP growth rate will be lower, no matter in pre- or post-GFC, which keeps in line with the full sample analysis. Second, different from the post-GFC periods, the bank credit growth rate in the initial periods will be positive in response to a higher partisan conflict before the GFC periods and then turns negative after three quarters. On the contrary, the lagged responses of bank credit to partisan conflict do not exist in the post-GFC periods. Third, the partisan conflict will generate opposite impacts on the central bank policy rate before and after the GFC periods. In the pre-GFC periods, the policy rate tends to decline in the face of higher partisan conflict as the full sample analysis, but the policy rate is more likely to increase after the GFC. Way (Citation2000) concludes that the effects of partisan government and central bank organization are mutually contingent. The pattern of results anticipated by partisan theory only arises where central banks are under political control, whereas when central banks are independent, left governments are disadvantaged and right governments privileged in their ability to achieve their partisan goals. We can expect that after the GFC, the fed reserve maintains its dependence and raises the interest rate to achieve its policy target and is less influenced by partisan conflict. Therefore, compared to Cheng et al. (Citation2016; Citation2018), our empirical results exhibit richer patterns on the reaction of the central bank policy rate.

6.2. Extended Model I: the intermediate role of economic policy uncertainty

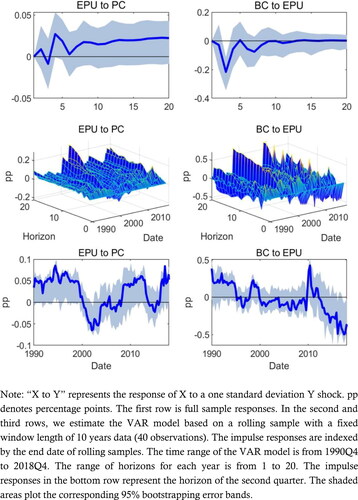

An underlying mechanism that partisan conflict deteriorates bank credit and economic activity because it increases economic policy uncertainty (Baker et al., Citation2016; Azzimonti, Citation2018; Citation2019). Azzimonti (Citation2018) conclude that firms exposed to government spending are expected to have lower investment rates when partisan conflict is high (but moderate) through the uncertainty channel. Cheng et al. (Citation2018) also distinguish the political conflict from policy uncertainty and uncover new empirical facts related to the distinct impacts of two types of uncertainty. In addition, the negative impacts of economic policy uncertainty have been discussed extensively and summarized in recent literature. Bordo et al. (Citation2016) empirically confirm that economic policy uncertainty has a substantial negative effect on bank credit growth. Therefore, it is reasonable to conjecture that the economic policy uncertainty plays an intermediate role in propagating the partisan conflict shock. To examine this hypothesis, we incorporate the economic policy uncertainty index developed by Baker et al. (Citation2016) in our first extended model. In the VAR model, which implies that only partisan conflict will directly enter the economic policy uncertainty equation rather than other endogenous variables.

plots the impulse responses including the full sample VAR model and rolling sample VAR model. Here, we only plot the responses of EPU to one standard deviation PC shock and the responses of BC to one standard deviation EPU shock. In the full sample analysis (the first row), we discover that higher partisan conflict will cause higher economic policy uncertainty as suggested by Baker et al. (Citation2016). The three dimensions present more complete picture and dynamic responses from 1990Q4 to 2018Q4. The economic policy uncertainty will generate a negative impact on bank credit since 1997, although there will be a temporary positive impact during the global financial crisis periods. In the meanwhile, the partisan conflict will have more complex impacts on the economic policy uncertainty during our sample periods. To conclude, the economic policy uncertainty as an intermediate transmitting the partisan conflict shock will have a nonlinear pattern, which is usually ignored in the existing study like Bordo et al. (Citation2016).

Figure 9. Impulse responses: the role of economic policy uncertainty.

Source: authors.

6.3. Extended Model II: the substitutability of cross-border bank lending

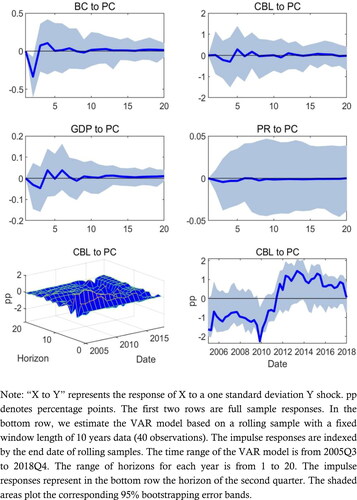

Partisan conflict in the US not only has domestic impacts but also has spillover effects (Cheng et al., Citation2016; Jiang and Shi, Citation2018). In this section, we consider the substitutability of cross-border bank lending on domestic bank credit to examine whether the spillover effects of partisan conflict are important to alter the response of domestic bank credit. In the second extended model, we incorporate the cross-border bank lending, then Under this specification, cross-border lending will affect the bank credit rather than the reverse channel.

also shows the impulse responses including the full sample VAR model and rolling sample VAR model. According to the full sample analysis, the partisan conflict will have slight positive effects in the initial few periods and then generate negative effects after the third period. The three dimensions impulse responses exhibit the time trend of impulse responses since 2005Q3. Before 2011, cross-border lending declines in response to higher partisan conflict but substantially increases in response to partisan conflict. Compared to the responses of domestic bank credit to partisan conflict shock, it is straightforward to conclude that domestic bank credit and cross-border bank lending are substitutes, so the regimes of the high growth rate of bank credit correspond to the regimes of the low growth rate of cross-border bank lending and vice versa. The substitutability effects of other financial markets on bank credit are also supported by current literature, for example, Choi (Citation2019) considers the public debt market as another substitute for domestic bank lending. Therefore, the substitutability of cross-border bank lending to domestic bank credit is a crucial channel to understand the impacts of partisan conflict shock.

Figure 10. Impulse responses: the role of cross-border bank lending.

Source: authors.

Figure 11. Robustness checks.

Source: authors.

7. Conclusion

This study comprehensively examines the impacts of partisan conflict on the bank credit in the US in a structural vector autoregression model and captures the variability in the effects of partisan conflict. The full sample analysis shows that one standard deviation partisan conflict shock will shrink the bank credit growth rate to nonfinancial sectors around 0.06% in the peak. By further decomposing the sample into two components, we find that the negative impacts of partisan conflict on bank credit are more substantial after the global financial crisis, which keeps consistent with the rolling sample and time-varying parameter analysis. Besides, in the post-GFC periods, partisan conflict accounts for more movements in bank credit compared to the pre-GFC periods. We also conduct two extended models incorporating the indirect channel and substitute effects on bank credit and conclude that two extended models support the intermediate role of economic policy uncertainty and the substitutability of cross-border bank lending. Finally, our empirical results are unchanged by performing a series of robustness checks.

Our article is the first attempt to build a direct relationship between partisan conflict and domestic bank credit. Although the theoretical analysis is beyond our scope and we leave it for future research, we still have intriguing policy implications based on our empirical analysis. Bordo et al. (Citation2016) emphasize that high economic policy uncertainty may have slowed the U.S. economic recovery from the Great Recession by restraining overall credit growth through the bank lending channel. Therefore, our empirical results add a new channel of partisan conflict to understand why the growth rate of bank lending shrinks in some specific periods. In addition, the partisan conflict might affect the behaviours of the central bank in implementing the monetary policy, which undermines the independence of the central bank. Therefore, how to lower the negative effects of partisan conflict might improve the efficacy of monetary policy.

By comparing the research results with others and further expanding the research, we find two key problems: first, the impact of party conflict on bank credit shows a negative effect on the whole, but shows a reverse incentive effect in some stages. Second, the impact of partisan policy conflict on banks. This provides the feasibility for the reasonable solution of practical problems. On the one hand, we hope that political sharing, cooperation and win-win will bring a stable development environment to the financial industry. On the other hand, when political differences are inevitable and party conflicts are bound to occur, we can consider appropriate responses to ensure the stability of bank credit. First, from the emergence of party conflict to the middle of development, reduce bank credit business to reduce unnecessary losses. Secondly, when the party conflict develops to the middle and late stage, make full use of the variability of the impact of party conflict, seize its reverse incentive cycle and do a good job in bank credit. Thirdly, during the period of party conflict, distinguish various relevant policies, do not touch the financial scope involved in uncertain policies, and formulate reasonable bank credit business development strategies for determining policies.

Finally, the regional heterogeneity of partisan conflict on bank credit is another interesting extension in the next study. In particular, we can consider measures of local and state partisan conflict that would help researchers measure the response of bank credit behaviours to nonfinancial sectors within and across states.

Disclosure statement

No potential conflict of interest was declared by the authors.

Additional information

Funding

Notes

1 For the definition of partisan conflict, refer to Azzimonti (Citation2018), partisan conflict generates from the interaction between two parties with different purposes in the political field. Policymakers’ ideological disputes (polarization) are undoubtedly important determinants of political disagreement.

2 The basic results are unchanged when we use a larger window length (80 quarters).

References

- Azzimonti, M. (2014). Partisan conflict. Federal Reserve Bank of Philadelphia Working Paper, 14–19.

- Azzimonti, M. (2018). Partisan conflict and private investment. Journal of Monetary Economics, 93, 114–131. https://doi.org/10.1016/j.jmoneco.2017.10.007

- Azzimonti, M. (2019). Does partisan conflict deter FDI inflows to the US? Journal of International Economics, 120, 162–178. https://doi.org/10.1016/j.jinteco.2019.06.001

- Azzimonti, M. (2021). Partisan conflict, news, and investors' expectations. Journal of Money, Credit and Banking, 53(5), 971–1003.

- Azzimonti, M., & Talbert, M. (2014). Polarized business cycles. Journal of Monetary Economics, 67, 47–61. https://doi.org/10.1016/j.jmoneco.2014.07.001

- Baker, S. R., Bloom, N., & Davis, S. J. (2016). Measuring economic policy uncertainty. The Quarterly Journal of Economics, 131(4), 1593–1636. https://doi.org/10.1093/qje/qjw024

- Batrancea, L., Rathnaswamy Malar, M., Batrancea, I., Nichita, A., Rus, M. I., Tulai, H., Fatacean, G., Masca, E. S., & Morar, I. D. (2020). Adjusted net savings of CEE and Baltic Nations in the context of sustainable economic growth: A panel data analysis. Journal of Risk and Financial Management, 13, 234.

- Batrancea, I., Rathnaswamy Malar, M., Batrancea, L., Nichita, A., Gaban, L., Fatacean, G., Tulai, H., Bircea, I., & Rus, M. I. (2020). A panel data analysis on sustainable economic growth in India, Brazil. And Romania, Journal of Risk and Financial Management, 13(8), 170.

- Batrancea, L., Nichita, A., Batrancea, I., & Gaban, L. (2018). The strength of the relationship between shadow economy and corruption: Evidence from a worldwide country-sample. Social Indicators Research, 138(3), 1119–1143. https://doi.org/10.1007/s11205-017-1696-z

- Batrancea, L. M., Nichita, R. A., Batrancea, I., & Moldovan, B. A. (2012). Tax compliance models: From economic to behavioral approaches. Transylvanian Review of Administrative Sciences, 8(36), 13–26.

- Batrancea, L. (2021). An econometric approach regarding the impact of fiscal pressure on equilibrium: Evidence from electricity, gas and oil companies listed on the New York stock exchange. Mathematics, 9(6), 630. https://doi.org/10.3390/math9060630

- Batrancea, I., Moscviciov, A., Sabau, C., & Batrancea, L. M. (2013). Banking crisis: Causes. Characteristics and Solutions, Proceedings of the DIEM 2013 “Scientific Conference on Innovative Approaches to the Contemporary Economic Problems” (pp.1–15) [ISSN: 978-953-7153-30-4].

- Batrancea, L., & Batrancea, I. (2009). The world financial crisis-roots, evolution and consequences. In Alma Mater (Ed.), The financial and economic crisis: causes, effects and solutions. Cluj-Napoca.

- Bordo, M. D., Duca, J. V., & Koch, C. (2016). Economic policy uncertainty and the credit channel: Aggregate and bank level US evidence over several decades. Journal of Financial Stability, 26, 90–106. https://doi.org/10.1016/j.jfs.2016.07.002

- Cheng, C. H. J., Chiu, C. W. J., Hankins, W. B., & Stone, A. L. (2018). Partisan conflict, policy uncertainty and aggregate corporate cash holdings. Journal of Macroeconomics, 58, 78–90. https://doi.org/10.1016/j.jmacro.2018.08.010

- Cheng, C. H. J., Hankins, W. B., & Chiu, C. W. J. (2016). Does US partisan conflict matter for the Euro area? Economics Letters, 138, 64–67. https://doi.org/10.1016/j.econlet.2015.11.030

- Choi, S. (2017). Variability in the effects of uncertainty shocks: New stylized facts from OECD countries. Journal of Macroeconomics, 53, 127–144. https://doi.org/10.1016/j.jmacro.2017.06.006

- Choi, S. (2019). Changes in the effects of bank lending shocks and development of public debt markets [Finance Research Letters].

- Gupta, R., Lau, C. K. M., Miller, S. M., & Wohar, M. E. (2019). US fiscal policy and asset prices: The role of partisan conflict. International Review of Finance, 19(4), 851–862. https://doi.org/10.1111/irfi.12188

- Gupta, R., Pierdzioch, C., Selmi, R., & Wohar, M. E. (2018). Does partisan conflict predict a reduction in US stock market (realized) volatility? Evidence from a quantile-on-quantile regression model. The North American Journal of Economics and Finance, 43, 87–96. https://doi.org/10.1016/j.najef.2017.10.006

- Hankins, W., Cheng, C. H. J., Chiu, C. W. J., & Stone, A. L. (2016). Does partisan conflict impact the cash holdings of firms? A sign restrictions approach. Working Paper. Bank of England.

- Jiang, X., & Shi, Y. (2018). Does US partisan conflict affect US-China? International review of economics and finance.

- Nakajima, J. (2011). Time-varying parameter VAR model with stochastic volatility: An overview of methodology and empirical applications. Monetary and Economic Studies, 29, 107–142.

- Primiceri, G. E. (2005). Time varying structural vector autoregressions and monetary policy. The Review of Economic Studies, 72(3), 821–852. https://doi.org/10.1111/j.1467-937X.2005.00353.x

- Wang, L. (2014). Who moves East Asian stock markets? The role of the 2007–2009 global financial crisis. Journal of International Financial Markets, Institutions and Money, 28, 182–203. https://doi.org/10.1016/j.intfin.2013.11.003

- Way, C. (2000). Central banks, partisan politics, and macroeconomic outcomes. Comparative Political Studies, 33(2), 196–224. https://doi.org/10.1177/0010414000033002002

- Cingano, F., Manaresi, F., & Sette, E. (2016). Does credit crunch investment down? New evidence on the real effects of the bank-lending channel. Review of Financial Studies, 29(10), 2737–2773. https://doi.org/10.1093/rfs/hhw040

- Ivashina, V., & Scharfstein, D. (2010). Bank lending during the financial crisis of 2008. Journal of Financial Economics, 97(3), 319–338. https://doi.org/10.1016/j.jfineco.2009.12.001