Abstract

Sustainable business performance is a rapidly growing field of research that encompasses both academia and business. The purpose of this study is to identify current and emerging research trends and provide a comprehensive map of the knowledge structure in the field of sustainable business performance, consistent with recent developments in bibliometric research. Therefore, this article offers a comprehensive bibliometric analysis based on the performance analysis and science mapping of the academic literature related to sustainable business performance published between 1996 and 2021 in 807 publications on the Web of Science. By using two powerful bibliometric visual software tools, VosViewer and CiteSpace, and by applying various bibliometric analyses such as co-citation analysis, co-authorship analysis, bibliographic coupling, co-occurrence of keywords analysis, burst detection analysis, and timeline view analysis, this paper presents the fundamental characteristics of the body of knowledge in this research field, while identifying the most influential publications, institutions, source titles, countries, and authors, and the evolution of keywords these years. The paper concludes with a discussion of the most popular research topics and identification of emerging research pattern areas that should be on the future research agenda for researchers interested in sustainable business performance.

1. Introduction

In the actual socio-economic context, business companies face real challenges; thus, it is imperative to identify new ways or more effective methods to become competitive and increase their value under the pressure of effective coordination of financial, environmental, and social requirements to provide sustainable business performance. Considering the growing interest in this promising field of research on sustainable business performance, its contents must be reviewed. Although there are some significant review papers in the area, with some different emphases (e.g., Geissdoerfer et al., Citation2018a, Shakeel et al., Citation2020 – sustainable business model innovation, Geissdoerfer et al., Citation2020 – circular business models, Bocken et al., Citation2014 - sustainable business model archetypes), no prior evidence of a comprehensive literature review related to the broad field of sustainable business performance using bibliometric analysis has been found. This study aims to map the field of sustainable business performance by providing data on the intellectual structure of knowledge and allowing the most influential articles, institutions, source titles, countries and authors. The findings of this bibliometric analysis can provide a solid basis for positioning actual contributions in this field and detecting emerging trends and guidelines for future research.

According to some researchers (Wang et al., Citation2021, Citation2021, Citation2022) to comprehensively understand the broad field of a certain research field, bibliometric analysis is one of the most suitable approaches to reveal the key topics and emerging research directions visually and is an effective way to present the evolution and relationships of items of a topic or a journal by analysing the relevant literature. As other researchers recently remarked (Wang et al., Citation2021, Citation2021, Citation2022: Xu et al., Citation2021b), bibliometric analysis is one of the mature and effective statistical methods based on quantitative analysis that have the great potential to reveal researchers a comprehensive overview of a certain domain of research from a holistic perspective. The great advantage of bibliometric analysis is that it can highlight the internal structure, current status, and development trends of a particular research field (Wang et al., Citation2021; Xu et al., Citation2021b). Therefore, the results of a well-conducted bibliometric analysis could shed light on future research guidelines that could advance further profound development of the research field under investigation (Wang et al., Citation2022).

Thus, the aim of this study is to provide a comprehensive overview of existing publications through an extensive bibliometric analysis of the field of sustainable business performance research, based on a sample of 807 articles from the Web of Science for the period 1996–2021, and using two bibliometric software tools, VosViewer and CiteSpace. This study addresses the following research questions employing the corresponding bibliometric methods.

RQ1: What are the most influential journals, authors, countries, and research papers in the field?

RQ2: What are the key emerging research trends related to sustainable business performance that could open directions to unexplored avenues of research in this field?

RQ3: What is the intellectual structure of knowledge related to sustainable business performance?

RQ4: What are the most-researched topics that have been studied with the greatest frequency and are currently attracting the most attention?

In summary, the contributions of this study to sustainable business performance research are indicated in at least four ways: (1) A comprehensive assessment of the literature related to sustainable business performance research during the last quarter of the century and fundamental statistical indicators are presented from the perspective of the number of publications and citations over time, most influential authors, articles, institutions, countries, and highly cited publications are presented. (2) Using certain techniques for science mapping (such as co-citation analysis, co-occurrence analysis, bibliographic coupling, and co-authorship analysis) combined with enrichment bibliometric techniques (such as networks and clustering visualisation), a comprehensive visual image of the intellectual structure of knowledge related to sustainable business performance can be obtained. (3) A relevant keyword perspective in this research field (through burst detection analysis and timeline view analysis), which is relevant to identify emerging research trends and potentially transformative changes. (4) A synthesis of guidelines for future research agendas on this topic is provided.

The originality of this paper lies in the fact that it helps to understand the evolution of research in the field of sustainable business performance from the perspective of bibliometric analysis and provokes researchers to proceed to explorations from multiple aspects in this field. Despite the importance of the topic, to the authors' knowledge, there is no prior evidence of a comprehensive bibliometric review related to the broad field of sustainable business performance to date. Compared with most of the literature reviews in this field, using a combination of two bibliometric software (VosViewer and CiteSpace), this study provides a more comprehensive holistic view of sustainable business performance, while emerging research trends are identified and a synthesis of essential guidelines for future work still to be done in this field is provided.

The remainder of this paper is organised as follows. Section 2 discusses in detail the methodology used in this study, including the database and search protocol and a description of the bibliometric methods used. Section 3 presents the results of the bibliometric analysis in detail, including the performance analysis, science mapping analysis, emerging trends for future research, a discussion of the most popular research topics, and guidelines for future research agendas. Finally, Section 4 provides concluding remarks.

2. Methods and materials

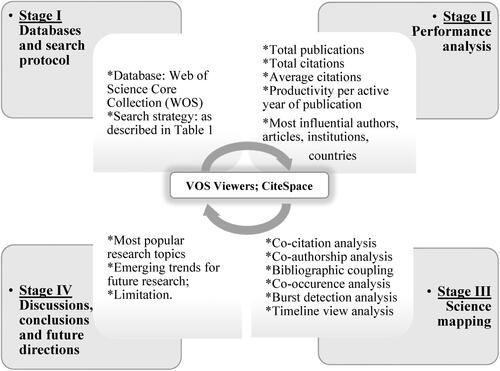

The main purpose of this study is to provide a comprehensive bibliometric analysis of the existing literature on sustainable business performance. For that purpose and consistent with recent research trends (Alshater et al., Citation2021; Anuar et al., Citation2022; Donthu et al., Citation2021; Wang et al., Citation2021, Citation2022; Dabic et al., Citation2020), the development of this bibliometric analysis is based on the research framework illustrated in .

Figure 1. Research framework of the methodology.

Source: created by the author.

2.1. Database and search protocol

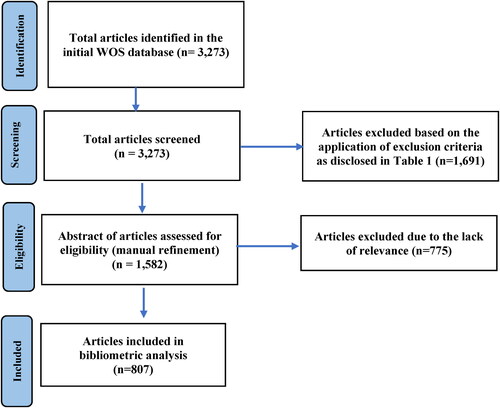

To provide a comprehensive map of the knowledge structure in the field of sustainable business performance, consistent with recent developments in bibliometric research (Alshater et al., Citation2021; Anuar et al., Citation2022; Dabic et al., Citation2020) we adopted a database search that followed one of the most well-known systematic review protocols. Therefore, data extraction for bibliometric analysis was performed using the Preferred Reporting Items for Systematic Reviews and Meta-Analyses (PRISMA) protocol as recently revised by Page et al. (Citation2021). The first version of this protocol was published in 2009 (PRISMA 2009) as a reporting guideline designed to increase transparency and a more rigorous approach to developing systematic reviews and meta-analyses to facilitate readers' understanding of why the review was conducted, the methodological steps followed by the authors, and what they found. Page et al. (Citation2021) argued that recent advances in systematic review methodology and terminology require an update of this guideline. Therefore, PRISMA 2020, as presented by Page et al. (Citation2021), includes new reporting guidelines to reflect advances in the methods for identifying, selecting, evaluating, and synthesising studies. As other authors have recently remarked (Streimikis & Saraji, Citation2022), the PRISMA protocol provides some clear advantages, such as a detailed, rigorous and well-described checklist that helps academics and researchers improve the way they conduct bibliometric analysis, systematic review reporting, and meta-analyses. The PRISMA flowchart used in this study is shown in .

Figure 2. PRISMA flowchart for systematic review.

Source: Created by the author and adapted from Page et al. (Citation2021).

The main objective of this review is to investigate current and emerging research trends in the field of sustainable business performance, while identifying future research directions. According to the first step of the PRISMA protocol, one of the most comprehensive sources of peer-reviewed research literature, the Web of Science Core Collection (WOS), was selected. The Web of Science database was chosen because it produces the highest quality publications and is a reliable source for indexing highly ranked journals (Caputo et al., Citation2021; Raghuram et al., Citation2019). The search began on 5 October 2021 and ended on 2 November 2021. As other researchers have remarked (Alshater et al., Citation2021) the reliability of bibliometric studies is significantly affected by the accuracy of the search criteria used to collect data. Therefore, we consider a list of all possible expressions associated with sustainable business performance, such as ‘sustainable business performance’, ‘sustainable business value’, ‘sustainable performance’, ‘sustainable business’.

Thus, these selected keywords must be present in the titles, abstracts, or keywords of the articles to ensure the comprehensive nature of this search. The application of the first search criterion yielded 3,273 documents published until the end of October 2021. Subsequently, several exclusion criteria were applied. As a result of this online selection, the sample included only articles and reviews written in English related to the fields of business, management, economics, sustainable green science technology, and public administration. This step excludes a set of related articles published in out-of-area journals. The results of this stage included 1,582 articles. In the next stage, following the procedures of Alshater et al. (Citation2021) Caputo et al. (Citation2021), and Khan et al. (Citation2020), subjective refinement was carried out to confirm the eligibility of the articles, namely whether all extracted documents are related to business and economics. The second stage yielded 807 articles, of which 775 were excluded for relevance. More precisely, this manual refinement supposes inclusion in the sample only for articles in which sustainable business performance is discussed within the broader field of business and economics, and in a non-tangential mode. provides a detailed overview of the search procedure used in this study. At the end of the search procedure, the final sample of articles was exported in plain text and comma-separated values (CSV) file formats as required for the software used for the bibliometric analysis. The first article on sustainable business in the final sample was published in the Long-Range Planning Journal in 1996 (Jose, Citation1996). Therefore, all the articles collected were from 1996 to 2021, which means that a quarter century has passed since this topic has aroused the interest of researchers. Since then, Jose (Citation1996) has argued for the stringent necessity of adopting sustainable business policies that should include an environmentally friendly strategy due to the deterioration of the earth’s environment.

Table 1. Description of the search procedure.

2.2. Bibliometric analysis

As a recent scientometric discipline, bibliometric analysis involves the application of statistical methods to evaluate scientific activities in the field of research (Broadus, Citation1987). This analysis allows the summarisation of large amounts of scientific data to describe and identify the state of the intellectual structure and emerging trends of a certain research topic (Donthu et al., Citation2021). Therefore, the bibliometric field has gained increasing popularity in business and economic research in recent years (Khan et al., Citation2020; Alshater et al., Citation2021; Donthu et al., Citation2021; Wang et al., Citation2021, Citation2021, Citation2022). Most recently, Donthu et al. (Citation2021) highlighted that the popularity of bibliometric analysis is justified for the following reasons: first, the availability and rapid technical evolution of various bibliometric software and scientific databases, such as Web of Science, Scopus, Dimensions, and others; second, the utility of bibliometric analysis is provided by the opportunity to handle a large sample of scientific data; and third, emerging trends in a certain research field can be more easily detected. For these reasons, bibliometric analysis is expected to have a significant impact on current research, especially on further research. To date, there is no widely accepted guide for bibliometric analysis in business and economic research. Donthu et al. (Citation2021) attempted to fill this gap by offering through their paper a step-by-step guideline for conducting in an appropriately manner bibliometric analyses in economics and business academics.

Bibliometric analysis requires the application of two main techniques: performance analysis and science mapping (Aria & Cuccurullo, Citation2017; Donthu et al., Citation2021). Based on this, this study presents a bibliometric analysis built on these two parts to provide a comprehensive understanding of the developments and map of knowledge structure in the field of sustainable business performance.

Performance analysis is based on activity indicators (Mingers & Leydesdorff, Citation2015) which provide an overview of the data regarding the productivity and impact of research using a wide range of indicators (Donthu et al., Citation2021; Caputo et al., Citation2021; Wang et al., Citation2021, Citation2022), including the number of publications counted by a unit of analysis (year, authorship, country, affiliation, etc.), productivity per active year of publication, number of citations, average number of citations, highly cited publications, most relevant publications, and most relevant source titles.

The second part of the bibliometric analysis is science mapping analysis, which investigates the intellectual interactions and relationships between research constituents (Donthu et al., Citation2021; Baker et al., Citation2021), allowing identification of the structural and dynamic organisation of knowledge for the investigated research field or topic (Iwami et al., Citation2020). According to Donthu et al. (Citation2021) and Caputo et al. (Citation2021), science mapping techniques include the following indicators.

Co-citation analysis includes the evaluation of references cited by scientific publications included in the selected dataset and the analysis of the relationships among cited publications to better understand the development of foundational themes in a certain research field.

Co-authorship analysis examines the intellectual collaboration between researchers and research institutions based on the number of publications jointly authored. This form of analysis has become increasingly important because research networks among scholars can lead to improvements in the research field, with greater clarity and richer insights.

Bibliographic coupling investigates the connections between publications to understand the significance of documents in a dataset in terms of their network position according to periodic or present developments of themes in a research field that could arise.

The co-occurrence of keywords provides a form of content analysis which provides the number of publications in which both keywords occur together in the title, abstract, or list of keywords. This form of analysis relies on the premise that, when keywords occur in a publication, the concepts related to those keywords should be closely related. In addition, this form of analysis allows the identification of thematic clusters.

All these techniques combined with enrichment techniques, such as network metrics, are essential for adequately presenting the intellectual structure of the investigated research field (Donthu et al., Citation2021; Baker et al., Citation2021: Raghuram et al., Citation2019). More precisely, network analysis can significantly enrich the discussion of research trends in certain research fields or topics.

In terms of the bibliometric tool used for the bibliometric analysis presented in this article, according to the recent practices of latest studies in bibliometrics published in the field of business and economics (Anuar et al., Citation2022; Caputo et al., Citation2021; Wang et al., Citation2021, Citation2021, Citation2022; Ferreira, Citation2018), we adopted the software program VOSViewer (Van Eck & Waltman, Citation2010), which allows three types of scientific maps such as network visualization, overlay visualisation, and density visualisation. Furthermore, to identify emerging research trends and potentially transformative changes in the field of sustainable business performance, we adopted another popular bibliometric software tool, CiteSpace, which allows academics to better understand the status and dynamics of a certain body of knowledge (Chen et al., Citation2014).

As other researchers remarked (Xu et al., Citation2021a, Citation2021b), when selecting a bibliometric tool, the researcher must consider its applicability and operability. According to Donthu et al. (Citation2021), each bibliometric software has its advantages and disadvantages; therefore, in many situations, the best choice would be to use a combination of bibliometric software to most valorise the advantages but also to counteract the disadvantages of each software (Donthu et al., Citation2021, Citation2020; Xu et al., Citation2021a, Citation2021b). We decided to use VosViewer because of its advantages. First, VosViewer is relatively easy to use, the user does not have to own programming skills, and setting the parameters of bibliometric analysis is not difficult (Xu et al., Citation2021a). Second, this software allows one to work with large datasets in a very pragmatic way and has superior mapping capabilities with much easier interpretations (Donthu et al., Citation2020, Citation2021). Third, based on various adopted metrics, this software is a very useful mapping tool that allows the presentation of the relationships and cooperation of subjects more clearly (Xu et al., Citation2021a, Citation2021b). Then we decided to use CiteSpace because it is another powerful bibliometric tool (Xu et al., Citation2021a, Citation2021b) because of its advantages compared to other bibliometric software. First, this software allows researchers to generate burst detection analysis, which is a valuable indicator of the most active research topics at various levels of granularity (Chen et al., Citation2014). Second, the timeline view analysis provided by CiteSpace software allows identification of development and emerging research trends in the field of research under inquiry (Wang et al., Citation2021). Third, this excellent bibliometric software improves scholars' ability to detect and understand the dynamics of a certain research field (Xu et al., Citation2021b; Wang et al., Citation2021).

3. Results and discussions

According to the methodology described in the above section, this section presents the results of a comprehensive bibliometric analysis of scientific publications related to sustainable business performance. The results are disclosed according to the unit of analysis under investigation, such as articles, authors, journals, and identification of conceptual research themes in this field. The final purpose of this bibliometric analysis is to present a comprehensive picture of past, current, and emerging trends in sustainable business performance research.

3.1. Performance analysis

As presented in , this study is based on 807 articles on sustainable business performance related to business, economics and management disciplines published in 234 journals. Next, through the presentation of several bibliometric indicators, this performance analysis provides an overview of the development and distribution of sustainable business performance from the following statistical perspectives: the number of publications related to sustainable business performance, number of citations, most active institutions contributing to publications related to sustainable business performance, most active sources for publications related to sustainable business performance, most active countries contributing to publications related to sustainable business performance and highly cited publications in this field.

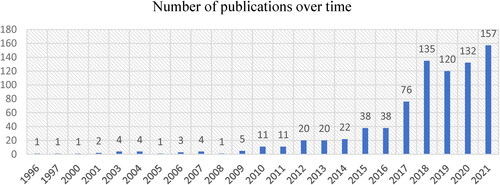

3.1.1. Evolution over time of the number of publications related to sustainable business performance

The data set consists of 807 publications from 1996 to 2021, and the evolution of the number of publications over time is shown in . Despite the extended period (25 years) in which these articles were published, academic interest in this field of research has begun to grow significantly in the last five years (2017–2021). The trend in the number of publications continues to increase, while for 2021, the highest number of publications can be seen; however, this year was not completely included in the sample (up to November 2021). This finding strongly supports the idea that this field of research related to sustainable business performance will become of increasing interest to researchers, especially in the context of the various challenges faced by many countries to ensure the harmonisation of financial, environmental, and social objectives in the carrying out of business activities to create and maximize real value.

Figure 3. Evolution over time of the number of publications related to sustainable business performance.

Source: created by the author.

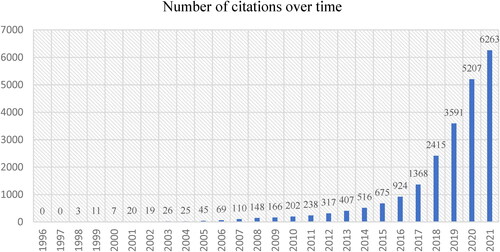

3.1.2. Evolution over time of the number of citations

The same increasing trend is observed in the evolution of the number of citations, as shown in . The significant increase in the number of citations received by publications related to sustainable business performance, particularly in the last five years, demonstrates the growing popularity and influence of this topic on academics. Furthermore, it can be noted that the highest number of citations so far was registered in 2021 (6.263 citations). The highest number of citations (214) was registered in 2021 for the study conducted by Bocken et al. (Citation2014), who proposed a categorisation of sustainable business model archetypes in eight archetypes developed so that they could be the starting point for broadening and unifying the research agenda regarding sustainable business models. Furthermore, a significant number of citations were recorded in 2021 for other relevant papers, such as Murray et al. (Citation2017) (210 citations), Boons and Lüdeke-Freund (Citation2013) (131 citations), and Lewandowski (Citation2016) (130 citations).

Figure 4. Evolution over time of the number of citations.

Source: created by the author.

3.1.3. Most active institutions contributed to publications related to sustainable business performance

shows the top 15 most active institutions that contributed to this research field related to sustainable business performance. To obtain a comprehensive picture of these institutions and their relevance in this field, presents significant information on the total number of citations, the average citations per item, and the H-index recorded for the publications of each institution’s publications. According to the Web of Science website, the H-index indicates the productivity of the authors based on their publication records and citation records. The value of the H-index is equal to the number of papers (n) on a list with at least n citations. The H-index indicates the number of papers (n) published by an institution with at least (n) citations.

Table 2. Top-15 most active institutions contributed to publications related to sustainable business performance.

An interesting phenomenon may be observed when analysing the data presented in . If the first two institutions (University of Cambridge and Delft University of Technology) ranked first and second, since the number of publications is also in the same position as the number of citations and the H-index for the following positions, this assumption is no longer certified in all cases. For instance, one may note the case of Bucharest University of Economic Studies (ranked third), which, even if it had 16 publications in this field, had received only 173 citations thus far, with an H-index of 7, meaning that this institution has seven publications related to sustainable business performance cited at least seven times. The following positions, University Sains Malaysia (15 publications) and Lund University (13 publications) recorded a higher number of citations for their publications.

3.1.4. Most active source titles for publications related to sustainable business performance

lists the 15 most productive source titles in this research field classified according to the number of articles. To provide a complete picture of these journals and their relevance in this field, presents information on the total number of citations, average citations per item, and the impact factor recorded for each journal. Even if on the first position as the number of publications in this field is the Sustainability journal (196 publications), the most influential and highly cited journal is the Journal of Cleaner Production (ranked second), but with the greatest number of citations (8.738) for 144 publications, meaning an average citation per item of 60,68. As shown in , the journals with the highest impact factor attracted the most citations for their publications related to this field of research.

Table 3. Top-15 most active source titles for publications related to sustainable business performance.

3.1.5. Countries contributed to the publications related to sustainable business performance

lists the top 15 most productive countries in this research field classified according to the number of articles. Following the same procedure as in the previous sections, to provide a comprehensive picture of the role and relevance of these countries in this field, presents information about the total number of citations and the average citations per item. The most influential countries that contributed to the development and global dissemination of publications in the field of sustainable business performance are the United Kingdom (94 articles cited 5.569 times), United States of America (90 articles cited 4.841 times), and China (75 articles cited 1.254 times).

Table 4. Top-15 Countries contributed to publications related to sustainable business performance.

3.1.6. Highly cited publications

lists the 15 authors and publications most cited in this field of research related to sustainable business performance ranked according to the number of total citations received. The number of citations received by a publication reflects one of the most reliable measures of the quality and relevancy of this publication. According to the data disclosed in , the most influential article was published by Bocken et al. (Citation2014) with the highest number of citations (1.146) and the average number of citations per year (143,25). In fact, according to Section 3.1.2 presented above, the same publication also received the highest number of citations only in 2021 (214 citations). These most cited studies in this research field focused mainly on sustainable business models and their innovation through a triple bottom approach while ensuring the harmonisation of financial, environmental, and social interests of various stakeholders (Bocken et al., Citation2014; Boons & Lüdeke-Freund, Citation2013; Boons et al., Citation2013; Stubbs & Cocklin, Citation2008; Evans et al., Citation2017, Geissdoerfer et al., Citation2018a), Sustainable Value Added as an approach for measuring corporate performance (Figge & Hahn, Citation2004), Sustainable Balanced Scorecard (SBSC) conceptual framework (Hubbard, Citation2009), the triple layered business model a tool for exploring sustainability-oriented business model innovation (Joyce & Paquin, Citation2016), links between information technology (IT), information systems and firm performance (Powell & Dent-Micallef, Citation1997; Rai et al., Citation2006; Watson et al., Citation2010), and the concept of circular economy, as one of the most recent attempt to conceptualize the integration of economic activity and environmental wellbeing in a sustainable way of obtaining business performance (Murray et al., Citation2017; Lewandowski, Citation2016; Geissdoerfer et al., Citation2018b).

Table 5. Top-15 Highly cited publications related to sustainable business performance.

3.2. Science mapping analysis

The main purpose of the science mapping analysis is to summarise the bibliometric structure and intellectual structure of the selected research field (Donthu et al., Citation2021; Caputo et al., Citation2021), by using certain techniques for science mapping (such as co-citation analysis, co-occurrence analysis, bibliographic coupling, co-authorship analysis) combined with enrichment bibliometric techniques (such as networks and clustering visualisation).

3.2.1. Co-citation analysis

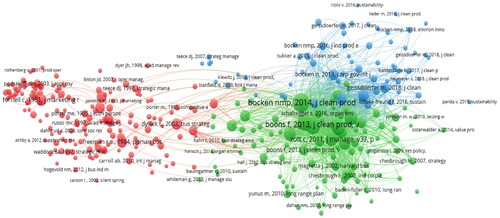

As noted above, co-citation analysis includes the evaluation of the references cited by the scientific publications included in the selected dataset and the analysis of the relationships among cited publications to better understand the development of foundational themes in a certain research field. In other words, as highlighted by Ferreira (Citation2018), co-citation analysis allows for the identification of publications that are co-cited by several other articles, which means that these cited publications are somehow meaningfully related. For our sample of 807 articles, 41.549 cited references were identified, and a minimum threshold of 10 citations of a cited reference was considered, which contained 329 cited references that met the threshold. To foster an understanding of the co-citation analysis of articles, illustrates the network diagram, allowing visualisation of the co-citation network of researchers in the field of sustainable business performance. shows the top ten references cited in our 807 selected articles with the highest link strength, citations, and number of links in the field of sustainable performance research field. According to the , there are three major clusters of cited references, where the largest cluster (red) has 164 cited references, the second cluster (green) has 99 cited references, and the last cluster (blue) has 66 cited references. It is interesting to note that of the top 10 cited references disclosed in , almost all references (except Joyce A, 2016, J Clean Prod, V135, P1474, Doi 10.1016/J.Jclepro.2016.06.067) are included in the green cluster of cited references shown in . In fact, the cited references included in the green cluster focused mainly on sustainable business models, sustainable innovation, and business model innovation.

Figure 5. The co-citation network diagram of cited references.

Source: created by the author based on the VOSviewer analysis.

Table 6. Top 10 cited references in the selected sample.

3.2.2. Co-authorship analysis

Co-authorship analysis examines the intellectual collaboration between researchers and research institutions based on the number of publications jointly authored. This type of analysis is widely used to understand and assess patterns of scientific collaboration in certain research fields. For our sample of 807 articles, a total of 2.133 authors were identified and a minimum threshold of three publications per author was considered; the resulting set contained 54 authors who met the threshold. To provide a better understanding of the co-authorship analysis, presents the top ten authors classified based on the total link strength of the co-authorship.

Table 7. Top 10 most collaborative authors in the selected sample in the field of sustainable business performance.

Analysing the activity of most collaborative authors from the selected sample of 807 articles, it can be noted that the first three authors from co-authored together with other authors, a group of seven articles that provide valuable contributions in this field of research, such as:

Testing the triple bottom line construct for to implement sustainable business practices in companies and their business networks (Svensson et al., Citation2016a; Padin et al., Citation2016; Høgevold et al., Citation2015)

Developing and testing a stakeholder construct to increase the efficiency of companies in achieving business sustainability goals within their business networks, marketplaces, and society. They proposed five stakeholder dimensions related to business sustainability in a cross-industry sample of organizations, including the focal company, downstream stakeholders, social stakeholders, market stakeholders and upstream stakeholders (Svensson et al., Citation2016b; Ferro et al., Citation2017).

Promoting the development of more rigorous sustainable business practices should consider the organizational challenges of sustainable business models, while incorporating the evolution of economic effects, social boundaries, and necessary environmental actions (Høgevold et al., Citation2014).

3.2.3. Bibliographic coupling

As noted above, bibliometric coupling investigates the connections between publications to understand the significance of documents in a dataset in terms of their network position. According to Caputo et al. (Citation2021), bibliographic coupling occurs when two documents cite a common third document, suggesting that they potentially debate a common topic. Thus, bibliographic coupling allows for the analysis of connections between publications, providing insights into the significance of publications in the selected dataset in terms of their networking positioning.

In terms of the bibliographic coupling analysis of journals, considering a minimum threshold of two documents per journal, the resulting set contained 76 journals that met the threshold. presents the top ten journals in terms of link strength. It should be noted that the Journal of Cleaner Production and Sustainability is far from other journals that are the most influential journals in this research field.

Table 8. Top 10 journals in terms of bibliographic coupling link strength.

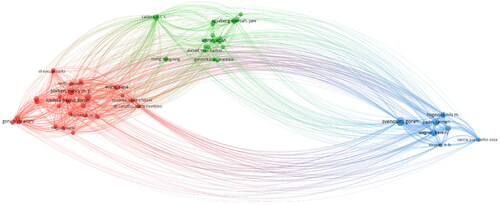

Continuing with the bibliographic coupling from the authors’ perspective and considering a minimum threshold of three articles per author, the resulting set contained 54 authors who met the threshold. presents the authors with the highest classified bibliographic coupling link strengths, based on the total link strength of the bibliographic coupling. According to Caputo et al. (Citation2021), the highest strength of bibliographic coupling links means that these authors have a higher centrality in the network of citations and are intensively included in conversations. Degree of centrality refers to the number of relational ties an author has in a research network (Donthu et al., Citation2021). When comparing the data disclosed in with those in , it is interesting to note that the five most collaborative authors in this field of research are also those with the highest centrality in the citation network; therefore, they have the strongest link from the perspective of bibliographic coupling. illustrates the network diagram, which allows for visualisation of the bibliographic coupling network of authors in the field of sustainable business performance. In addition, it can be noted that seven of the top ten authors formed a single cluster.

Figure 6. The bibliographic coupling network diagram of the authors.

Source: created by the author based on the VOSviewer analysis.

Table 9. Top 10 authors in terms of bibliographic coupling link strength.

Proceeding to the bibliographic coupling of the 807 articles in the selected data set and considering a minimum threshold of five citations per document, 475 of the 807 articles met the threshold. presents the top 10 papers with the highest index of bibliographic coupling among these studies; eight of these 10 papers were published in the most recent period 2018-2020.

Table 10. Top 10 papers in terms of bibliographic coupling link strength.

3.2.4. Co-occurrence analysis of keywords

As mentioned above, the major purpose of keyword co-occurrence analysis is to provide a form of content analysis which allows the identification of connections between keywords from a selected sample of publications. According to Fakhar Manesh et al. (Citation2021), the significance of this analysis lies in the opportunity to identify thematic areas grouped into thematic clusters so that the main theoretical or foundational topics of the research field can be depicted.

To perform this keyword analysis, another tool was used in this study, namely the Keywords Plus tool from the Web of Science. If author keywords are terms set by the authors as representatives of the content of their papers, Keywords Plus provided by WOS are generated using an automatic computer algorithm, with the words and phrases that appear commonly together in the titles of an article's references. Zhang et al. (Citation2016) argued that using both Keyword Plus and author keyword terms, the analysis of the knowledge structure of a certain research field may be more comprehensive.

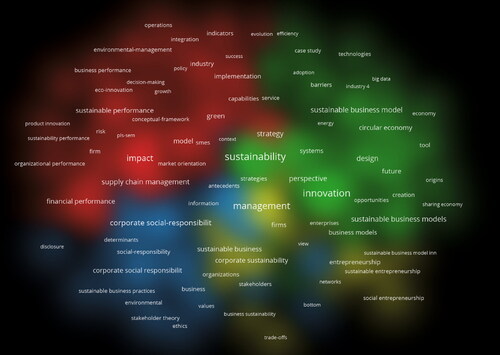

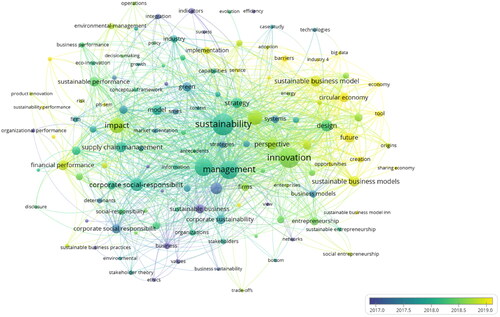

Taking into account the minimum threshold for the occurrence of keywords, 130 keywords were identified from a total of 3255 keywords. Therefore, the five keywords that occurred most frequently were sustainability (208 occurences), innovation (186 occurences), management (155 occurences), performance (145 occurences), and impact (112 occurences). To foster an understanding of the co-occurrence of keywords, shows the cluster density visualisation of high-frequency keywords, which is enriched visualisation because the density of keywords is displayed separately for each cluster of keywords. Another useful diagram is the overlay visualisation, which allows the identification of the temporal distribution of keywords in each cluster (see ). In overlay visualisation, keywords are coloured according to a score that is computed based on the average year of occurrence of a keyword. Thus, colours vary from blue (the oldest year) to green to yellow (most recent years). Analysing overlay visualisation, one can note that the field of studies on sustainable business performance has evolved from a previous focus on topics such as sustainable development, ethics, and indicators (oldest years) to more integrated and challenging concepts such as sustainable business models, circular economy, sharing economy, environmental management, sustainable business model innovation (most recent years) and most recent technological developments (Industry 4.0, Big Data), which will bring more challenges to this research field.

Figure 7. The co-occurrence of keywords density diagram using cluster density.

Source: created by the author based on the VOSviewer analysis.

Figure 8. The co-occurrence of keywords overlay diagram.

Source: created by the author based on the VOSviewer analysis.

3.3. Emerging trends for future research

It is important to identify emerging trends and potential transformative changes to understand the dynamics of the body of knowledge related to sustainable business performance. For this purpose, another useful tool for mapping scientific literature, CiteSpace, is used. The CiteSpace tool is based on a Java application for analysing and visualising the co-citation network and has the primary goal of providing an analysis of emerging trends in a certain research field (Chen, Citation2006; Chen et al., Citation2014). To foster an understanding of the origins, current, and development trends of the sustainable business performance field, in the following sections, a burst detection and timeline view analysis were processed using the CiteSpace tool.

3.3.1. Burst detection analysis

According to the developers of the CiteSpace tool (Chen et al., Citation2010; Chen et al., Citation2014), the burstness of subject categories, keywords, terms and cited references is a valuable indicator of the most active research topics at various levels of granularity. The burstness of the frequency of keywords over time provides significant indications of the specific period within which the number of citations for a keyword or term suddenly increases (Chen et al., Citation2010; Chen et al., Citation2014). Therefore, the CiteSpace burst detection function was used to examine current and emerging trends in the field of research related to sustainable business performance.

The results presented in highlight the top nine keywords in citation bursts over time, classified according to burst strength. Nine keywords related to research in the field of sustainable business performance received the most attention between 1996 and 2021. The blue lines in indicate the observed time intervals, whereas the duration of the burstness period of the keyword is indicated by a red line segment. According to the data shown in , the keyword with the first burst of citation is ‘sustainable development’ (3,57), and its burst period lasted 5 consecutive years (2009–2013). Then, it is followed by ‘climate change’ (2010–2012), ‘sustainable business’ (2010–2016), and ‘sustainable business practices’ (2010–2017). This is understandable because, starting in this period, global trends have begun to pay increasing attention to the impact of climate change on sustainable business practices. Next, more attention has been focused on the effects of ‘corporate social responsibility’ (2014–2016) and ‘social responsibility’ (2015–2017) on corporate business performance.

Table 11. Top 9 keywords on citation burst over time.

Furthermore, more recently, the burst pattern of keywords indicates that research themes related to ‘supply chain management’ (2017–2019) and ‘environmental issues’ (2017–2019) have gained the upper hand. Finally, the most recent keyword is ‘environmental performance’ with a burst period from 2018 to the present, highlighting the popularity of this subject in the most recent debates on sustainable business performance. The attention paid to environmental performance has flourished in recent years, especially in the context of stringent requirements to ensure not only the simple consideration of environmental aspects but also the achievement of an adequate level of key environmental performance indicators.

In summary, a conclusion can be drawn that research on these research themes has generated and will continue to generate significant contributions in the field of research related to sustainable business performance.

3.3.2. Timeline view analysis

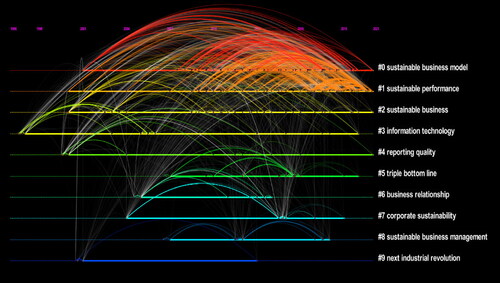

Next, using CiteSpace and proceeding to the analysis of the keyword timeline view, presents a timeline view of the different clusters of high-frequency keywords. Following this analysis, ten major clusters with core labels were generated. The horizontal line shows the clusters along the timeline, and the label of each cluster is shown at the end of the cluster timeline (Yin et al., Citation2020). According to the CiteSpace software developer (Chen et al., Citation2014), the clusters were numbered in descending order of cluster size, starting from the largest cluster #0, the second largest cluster #1, and so on. The colour of each line corresponds to the time slice in which the occurrence of these keywords is observed. Furthermore, the large number of connected curves indicates a symbiotic relationship between the terms, indicating the advent of emerging research trends in this field of research (Wang et al., Citation2021).

Figure 9. Timeline view of the co-occurrence network of keywords in different clusters.

Source: created by the author based on the CiteSpace analysis.

The largest area (Cluster #0) with high-frequency keywords in the selected sample is ‘sustainable business model’, followed by ‘sustainable performance’, ‘sustainable business’, ‘information technology’, ‘reporting quality’, ‘triple bottom line’, ‘business relationship’, ‘corporate sustainability’, ‘sustainable business management’, and ‘next industrial revolution’. As one can see, most of the clusters are concentrated from the beginning of the 21st century onward, except for Cluster #3 ‘information technology’ whose duration with high-frequency keywords started before 1998. It can be noted that the longest duration belongs to the Cluster #0 (sustainable business model), Cluster #1(sustainable performance), Cluster #2 (sustainable business), and Cluster #4 (reporting quality). Interestingly, the same clusters remained active after a 20-year period. Cluster #5 (triple bottom line), although it is a relatively recent research theme in this field (starting in 2007), seems no longer of interest in the last 2 years. It can be seen that for several clusters such as Cluster #6 ‘business relationship’ (2004–2013), Cluster #7 ‘corporate sustainability’ (2004–2019), Cluster #8 ‘sustainable business management’ (2007–2018), Cluster #9 ‘next industrial revolution’ (2001–2013), even if they had a relatively long duration of high frequency keywords, they appear to carry little to the present.

3.4. Most popular research topics – content analysis

Sustainable business performance is a complex and challenging topic which has attracted increasing academic interest in recent years. The research field related to sustainable business performance is not new, but it has experienced exponential development and special interest from researchers in recent years. Green innovations, environmental performance, and corporate social responsibility have defined many of the recent academic agendas in the context of the growing need to ensure a sustainable future. Based on the results of the extensive analysis of keyword co-occurrence and keyword clusters based on burst detection and timeline view analysis, four hot mainstream topics that need more academic attention in the current and future research agendas were summarised.

3.4.1. Sustainable business models

‘Sustainable business models’ is the first and largest research mainstream within most of the keywords are linked. Within this major mainstream, a growing body of literature has received considerable attention from academics and practitioners. However, many research gaps in this mainstream stream still need to be addressed. According to Bocken et al. (Citation2014), sustainable business models incorporate a triple bottom approach while considering a wide range of stakeholder interests, including environmental and social issues. Sustainability, as a key driver to obtain competitive advantage, must be integrated into a corporate strategy based on the implementation of sustainable business models so that business actions align with the social, environmental and economic requirements of the context in which a company operates.

The first sub-stream relates to business model innovation. Despite extensive literature on this topic, it remains ambiguous (Shakeel et al., Citation2020). According to Geissdoerfer et al. (Citation2016), innovation in business models is a key driver of the strategic use of sustainability in organisations. Some of the first notable developments on this topic of ‘business model innovation’ were made by some authors such as Chesbrough (Citation2010), Upward and Jones (Citation2016) and Joyce and Paquin (Citation2016). Geissdoerfer et al. (Citation2016) described business model innovation as a ‘process of transformation from one business model to another within incumbent companies or after mergers and acquisitions, or the creation of entirely new business models in start-up’. The ability of a company to continuously adapt and innovate its business models can determine its resilience to various changes in its context while providing a valuable sustainable competitive advantage (Geissdoerfer et al., Citation2018a). Business model innovation implies the diversification or transformation of existing business models to other business models to gain a competitive advantage in a fluctuating business environment (Shakeel et al., Citation2020). Geissdoerfer et al. (Citation2018a) suggest that this transformation can impact a company’s structure in terms of its value proposition, value creation and delivery, value capture elements, and value networks. Shakeel et al. (Citation2020) highlight the main challenges faced by business model innovations. Therefore, if the main challenges are given by the target and scope of innovation, we must not forget that the innovation of existing business models and ways of doing business should provide not only financial value but also other types of benefit, such as customer values, value chain, value for organisational structure and infrastructure, and social and environmental value for a wide range of stakeholders (Shakeel et al., Citation2020; Bocken et al., Citation2014).

The second sub-stream is related to sustainable business models. Academic interest in sustainable business models has grown significantly since the first decade of the 21st century. Stubbs and Cocklin (Citation2008) provided some notable contributions in this field, highlighting that sustainable business models should be ideal for a sustainable organisation. Through their study, Stubbs and Cocklin (Citation2008) achieved a significant goal in the conceptualization of a sustainable business model, starting from the premise that organization sustainability will be ensured only if neoclassical business models are metamorphosed considering both social and environmental priorities, especially in the context of the perspective of ecological modernization of sustainability. Based on two case studies of entities considered leaders in operationalizing sustainability, Stubbs and Cocklin (Citation2008) focused on the characteristics and components of a sustainable business model and concluded that when adopting a sustainable business model, an organisation ‘must develop internal structural and cultural capabilities to achieve firm-level sustainability and collaborate with key stakeholders to achieve sustainability for the system of that an organization is part.’ Although there is a widely accepted consensus that transformations in business models are fundamental to achieving innovations for the purpose of sustainability, little is known about the successful adoption of sustainable business models (Evans et al., Citation2017). Evans et al. (Citation2017) also provided a relevant contribution to the theoretical foundation of this emerging field of sustainable business models, proposing a unified theoretical perspective with five propositions (integrating sustainability into a sustainable value flow among multiple stakeholders, mutual value creation, and value networks) to understand the innovation of business models that should lead to better organizational economic, environmental, and social performance. Geissdoerfer et al. (Citation2018a) argued that the concept of sustainable business models has evolved and that this concept is now increasingly approached as a source of competitive advantage. The same authors proposed a new enhanced conceptual approach arguing that sustainable business models represent business models that ‘incorporate proactive multi-stakeholder management, the creation of monetary and non-monetary value for a broad range of stakeholders, and hold a long-term perspective’ (Geissdoerfer et al., Citation2018a). Furthermore, value capture is described as the value provided for a stakeholder that can be transformed into value useful for the organisation. Shakeel et al. (Citation2020) noted the diversity in the conceptualization of sustainable business models in the literature. However, the research agenda on this topic has quickly moved toward embedding innovation into its sustainability agenda. Thus, a new concept has emerged, namely, sustainable business model innovation.

The third sub-stream is related to the circular business models. To explain the various mechanisms for delivering sustainability, Bocken et al. (Citation2014) provide a deeper analysis and categorisation of sustainable business model archetypes such as frugal business models associated with the bottom of the pyramid, product service systems, or circular business models. According to Bocken et al. (Citation2016), the circular approach assumes the identification of economically viable solutions to continuously reuse products and materials using renewable resources, where possible. Circular business models have been proposed as a business model strategy in the context of circular economic thinking, and this new paradigm begins with the recognition of limitations in planetary resources and energy use (Bocken et al., Citation2016). Thus, a circular economy requires the identification of new concepts and tools to describe and construct this new paradigm. Linder and Williander (Citation2017) defined the circular business model as one in which ‘the conceptual logic for value creation is based on utilizing economic value retained in products after use in the production of new offerings’. Later, Geissdoerfer et al. (Citation2018a) argued that circular business models are not only designed to provide sustainable value, employing a long-term and pro-active perspective, but also these models should be designed to ‘close, slow, intensify, dematerialise, and narrow resource loops’. Proceeding to a systematic review of the literature in the field of circular economy practices in agriculture, Barros et al. (Citation2020) concluded that further research needs to consider the development of new circular business models that are expected to facilitate the business management of materials and energy that circulate inside and outside the organization. The lack of clarity regarding its theoretical conceptualisation and position in the economic and operations literature is also highlighted by Geissdoerfer et al. (Citation2020) through a systematic literature review. Recently, Donner and Vries (Citation2021) proposed the innovation of circular business models by considering a circular bio-economy approach through the valorisation of agricultural waste for new products. In this regard, eight European circular business case studies integrated the conversion of agricultural waste and by-products into value-added products into their business models, with particular attention paid to their business models and organizational and technological innovations. Donner and Vries (Citation2021) concluded that business models for a circular bio-economy require new business configurations instead of linear innovation business strategies that are still dominant, while new combined organisational and technological innovations are needed for the most efficient employment of agricultural waste and by-products.

Finally, the fourth sub-stream is related to sustainable business model innovation, as one of the emerging topics in this field, as also, other authors admitted (Geissdoerfer et al., Citation2016). This concept is based on the idea that sustainability cannot be fully embraced without innovation (Shakeel et al., Citation2020). According to Roome and Louche (Citation2016), business model innovation is the process through which companies transform their existing business models for sustainable development. Geissdoerfer et al. (Citation2016) proposed two key elements that should be embedded in sustainable business model innovation: the creation of economic, societal and environmental value, and collaboration with a wider range of stakeholders. Geissdoerfer et al. (Citation2018a) considered sustainable business model innovation as a sustainable development process that includes positive or reduced negative impacts on the environment, society and long-term prosperity for multiple stakeholders. They concluded that there are four types of sustainable business model innovation: sustainable start-ups, sustainable business model transformation, sustainable business model diversification, and sustainable business model acquisition.

3.4.2. Sustainable performance

‘Sustainable performance’ is the second mainstream within the research field related to sustainable business performance, which needs more academic attention in the current and future research agenda. This topic has been intensively debated by academics in recent years, especially in terms of green innovation and environmental performance, which should help companies gain competitive advantage and sustainable performance.

The first relevant sub-stream, which requires further attention, is related to environmental performance. Zhu et al. (Citation2007) defined environmental performance as the effectiveness of a company in reducing carbon emissions, wastewater, solid waste, consumption of hazardous/harmful/toxic materials, frequency of environmental accidents, and taking all necessary actions to improve the environmental situation of a company’s environmental situation. Relevant contributions to this field have recently been published. For instance, Shahab et al. (Citation2020) conducted one of the first studies to examine the sustainability and environmental performance of Chinese companies using comprehensive longitudinal data. Therefore, these authors examined the impact of the attributes of the chief executive officer (CEO) on sustainable performance, environmental performance, and environmental reporting. Their findings support the conclusion that CEOs with research background, financial expertise, and foreign exposure tend to engage more in activities that improve sustainable performance, environmental performance, and environmental reporting, and are positively linked with increased sustainable environmental performance and reporting. Suganthi (Citation2020) examined the relationship between the implementation of corporate social responsibility initiatives and environmental performance and identified a positive relationship. Therefore, these authors confirmed the results of Sidhoum and Serra (Citation2017), who argued that environmentally friendly technologies will improve financial health and help develop a better environmental system, leading to better economic performance. Yusoff et al. (Citation2020) conducted the first empirical study examining the relationship between green human resource management practices and environmental performance in the hotel industry. Based on a study of 206 hotels, their findings argue that green recruitment and selection, green training and development, and green compensation are significantly related to environmental performance. Yasir et al. (Citation2020) empirically examined the effect of environmental orientation on environmental performance while considering the mediating role of green business strategies using data collected from managers of 126 manufacturing industries in Pakistan. They argued that organizations should pay more attention to the requirements of stakeholders with respect to environmental protection. Therefore, environmental orientation is necessary to formulate green business strategies and identify pertinent solutions to improve environmental performance. Nutsugah et al. (Citation2021) argued that the benefits of environmental performance to companies and their transformation into gains have not been sufficiently clarified in the literature. In this vein, these authors examined the influence of a company’s environmental performance on its overall firm performance and the mediating role of integrated marketing communication, using data from 194 firms. They found a negative and significant influence of environmental performance on firm performance, explained by companies’ reluctance towards environmental protection, but the introduction of integrated marketing communication changed this relationship into a positive one.

The second relevant sub-stream is green innovation. As some authors have admitted (Zailani et al., Citation2015), the topic of green innovation has received increasing academic interest due to the growing concern of governments, citizens, and international communities regarding the degradation of natural resources and environmental pollution, while improving green innovation for corporate sustainability is a recent debate around the world (Shahzad et al., Citation2020). Using data from 153 companies in the Malaysian automotive supply chain industry, Zailani et al. (Citation2015) concluded that environmental regulations, market demand and internal firm initiatives have a positive effect on green innovation initiatives, while green innovation has a positive effect on the three categories of sustainable performance (i.e., environmental, social, and economic). The positive effect of green innovation on sustainable performance was also confirmed by Tantayanubutr and Panjakajornsak (Citation2017), who examined this impact in the Thai food industry using green supply chain integration and corporate social responsibility as key influencing variables. Awan et al. (Citation2019) provided an interesting approach to this topic, promoting the idea that the impact of green innovation on environmental, social, and economic performance could be boosted by creative thinking. Advancing the idea of the importance of creative thinking as a driving green innovation tool for improving sustainable business performance, Awan et al. (Citation2019) suggested that creative thinking could enable companies to focus more on strong cooperative links that facilitate inter-firm resource exchange and influence green innovation. Shahzad et al. (Citation2020) emphasised the importance of the knowledge management process for green innovation and the impact of green innovation on the three categories of sustainable performance (i.e., environmental, social, and economic), which represents one of the recent relevant contributions regarding the examination of the multidimensional relationship among knowledge management, green innovation, organizational agility, and corporate sustainable performance. Recently, relevant contributions in what regards the determinant factors for the adoption of green innovation, while providing strong arguments in what regards the relevance of green innovation in promoting sustainable business performance were obtained by Asadi et al. (Citation2020) and Khan, P.A. et al. (Citation2021). However, green innovation and its driving factors remain an emerging topic that requires further research.

3.4.3. Innovative technologies and industry 4.0

‘Innovative technologies and Industry 4.0′ is also one of the recent topics that has attracted the attention of researchers interested in the field of sustainable business performance research. Even if there are some notable contributions regarding potential linkages between information technology and corporate sustainable performance from the 20th century (Powell & Dent-Micallef, Citation1997), most of the significant contributions in this area were disseminated in the last three years of the analysed period, especially in terms of the adoption of innovative technologies that should enhance sustainable business performance.

The first relevant sub-stream, which requires further attention, is related to blockchain technology. Blockchain is an innovative technology that expands business horizons and has all the necessary properties to ensure the transparency and validity of sustainable business practices (Nayak & Dhaigude, Citation2019). Tiscini et al. (Citation2020) provided relevant contributions in terms of the contribution of blockchain technology to sustainable business models in the agri-food industry, arguing that blockchain technology has significant potential to ensure technological innovation in sustainable business models. In the same vein, recently, Mercuri et al. (Citation2021) applying the CAOS (‘Characteristic, Ambience, Organization, Start-up’) model to a start-up operating company in the agri-food sector, provided findings that supported the conclusion that blockchain technology can enhance sustainable business performance by achieving the traceability, security, and non-manipulability of information. Khanfar et al. (Citation2021) addressed the potential of blockchain technology to address the challenges in developing sustainable business practices in the manufacturing industry. These authors argue that the sustainable business performance of manufacturers can be increased by blockchain technology, while its properties ensure transparency, traceability, real-time information sharing, and security of data capabilities. One of the most recent and relevant contributions on this topic was provided by Sislian and Jaegler (Citation2022), who examined the use of blockchain technology and enterprise resource planning (ERP) modules. These authors argue that using them together could significantly improve sustainable business performance and make them better prepared to face the challenges of an uncertain future.

The second significant sub-stream is related to Big Data analytics and its impact on sustainable business development. Academic efforts to explain the impact of Big Data analytics on the sustainable business performance goal of the organization are quite recent, and this topic has become very popular in academia as well as in industry (Raut et al., Citation2019). Jeble et al. (Citation2018) made some of the first notable contributions to this area. Using the resource-based logic view and contingency theory, these authors developed a theoretical model to explain the impact of Big Data and predictive analytics on the organization's goal of sustainable business development goal. Nimmagadda et al. (Citation2018) highlighted the challenges provoked by the integration of emerging technologies, such as Big Data, to improve sustainable business performance. Using spatial-temporal attribute dimensions in the context of the oil and gas industry, these authors argue that the integration of Big Data framework leads businesses to become more sustainable, productive, and valuable to multiple chains of an industry. Singh and El-Kassar (Citation2019) proposed another conceptual model based on the theory of dynamic capabilities, considering internal processes that constitute sustainable capabilities, and provided empirical arguments to support the integration of green supply chain management, green human resource management practices, and Big Data analytics to improve corporate sustainability business performance. Raut et al. (Citation2019) analysed the predictors of sustainable business performance through big data analytics in the context of developing countries and using data from manufacturing companies that had implemented sustainable business practices. They argued that management and leadership style, state and central government policy are the two most important predictors of Big Data analytics and sustainability business practices. More recently, Sivarajah et al. (Citation2020) examined the ability of Big Data and social media analytics within a participatory web environment to enable business-to-business organisations to become more efficient and sustainable through marketing-related business activities and strategic operations. Through qualitative research arising from interviews with managers, they provided relevant arguments that led to a better understanding of the utility of participatory Web tools to achieve sustainable business performance.

The third sub-stream is represented by a consistent group of researchers that discussed the impact of Industry 4.0, on sustainable business performance in various contexts. As Tirabeni et al. (Citation2019) argued, this new Industry 4.0 paradigm has been mainly addressed by academic literature, mostly from a technological perspective, while approaches to this concept from economic, ethical, social and sustainable perspectives have only recently aroused the interest of researchers. It is worth noting the point of view of the authors (Tirabeni et al., Citation2019), according to which even if some researchers put the equal sign between Industry 4.0 and the Fourth Industrial Revolution, they are still different. Thus, if the Fourth Industrial Revolution is a concept that explains significant technological developments over the years, the concept of Industry 4.0 is specifically focused on manufacturing in the actual context, and one major difference between these two concepts is related to the scope. The idea of contributions and opportunities provided by this new paradigm of Industry 4.0 in terms of sustainable development was also highlighted by Garcia-Muiña et al. (Citation2020). These authors analysed the impact of investments in Industry 4.0 on sustainable business practices in the case of an Italian ceramic tile producer based on a triple layer business model canvas. Despite the limitations of this study, resulting from the use of individual case studies, the authors provide a basis for future research on the design of operational innovation of sustainable business models in various manufacturing areas. The challenges of implementing Industry 4.0, based on various operational and financial constraints, especially in the case of SMEs, were highlighted by Kumar et al. (Citation2020) based on the DEMATEL approach and sensitivity analysis to examine the degree of influence and interrelationships among challenges. More recently, Gupta et al. (Citation2021) provided a framework resulting from a mix of quantitative and qualitative research methods based on the concepts of circular economy, sustainable cleaner production, and Industry 4.0 standards to assess the sustainability business performance of manufacturing companies. Gupta et al. (Citation2021) argued that circular economy practices, followed by cleaner production practices, and Industry 4.0, are the most important factors in promoting sustainability performance in manufacturing contexts. Most recently, Khan I.S. et al. (Citation2021) highlighted the major contributions of Industry 4.0, technologies, and their implications for sustainable development based on a systematic mapping review. They argued that the circular economy and sustainable business models focused on the adoption and implementation of Industry 4.0 are one of the most recent emerging research topics.

3.4.4. Sustainability reporting quality

‘Sustainability reporting quality’ is the fourth mainstream but is as important as the first three discussed above. This topic has gained significant attention in recent years, particularly in the context of its increasing importance in achieving sustainable business performance goals. It is worth mentioning that recently, the attention paid to sustainability reporting quality was also argued by the establishment of a new organisation, namely, the Value Reporting Foundation, established in June 2021, as the merged entity of the International Integrated Reporting Council (IIRC) and the Sustainability Accounting Standards Board (SASB). The main purpose of this organization is to provide a comprehensive corporate reporting framework with guidelines and standards to drive global sustainability performance reporting.

Beyond making claims about the sustainability practices of organizations, they should also be able to disclose their sustainability efforts (Zrnic et al., Citation2020). As Amran et al. (Citation2014) noted, the quality of sustainability reporting represents the affirmative commitment of many corporations to the implementation of sustainable business practices. If sustainability reporting was first established on a voluntary basis, it has recently become a legal obligation for some type of organisation, arguing in this regard the importance of sustainable performance globally (Zrnic et al., Citation2020).

Under pressure to ensure adequate quality of sustainability reporting, the concept of materiality assessment with respect to information that matters and reduces the amount of unnecessary information is becoming increasingly important. Therefore, companies must provide transparency and accountability when conducting comprehensive materiality assessments. According to Puroila and Mäkelä (Citation2019), the concept of materiality assessment is a central element in filtering the relevant information that should be incorporated in corporate sustainability reporting. The latest version of various sustainability reporting guidelines and standards (Integrated Reporting Framework-IR Framework, Global Reporting Initiative-GRI, and Standards for disclosure of sustainability information to investors-SASB) give due importance to this concept in defining the contents of sustainability reporting disclosure.

Following a systematic review of the literature on sustainability reporting, Zrnic et al. (Citation2020) concluded that there are eight emerging issues related to this topic: assurance, boards, communication, framework, impact, indicators, materiality and practices. Furthermore, the same author argued for the need to develop an effective method to establish materiality assessment, as stakeholders and managers play an important role in shaping materiality disclosures in sustainability reporting. Similarly, Jorgensen et al. (Citation2022) highlighted the increasing importance of materiality in sustainability performance measurement and reporting, which is diverse in the approaches used in practice for materiality assessment in sustainability reporting. Starting from the main approaches of materiality in two of the most widely used sustainability reporting standards (based on the Global Reporting Initiative definition and the Sustainability Accounting Standards Board definition), Jorgensen et al. (Citation2022) argued that different approaches to materiality in practice may draw unjustified conclusions in sustainability reports, emphasising the perceived shortcomings in the availability and quality of information from the perspectives of various stakeholders with various information needs. Therefore, as Jorgensen et al. (Citation2022) stated, more clarity is required in the establishment and communication of materiality in sustainability reports to benefit sustainability report users.

3.5. Future research agenda

The bibliometric analysis developed in this study contributes to the consolidation of emerging research pattern areas in the literature on sustainable business performance and suggests a future research agenda. presents a helpful synthesis of important future research directions that researchers interested in emerging topics in research related to sustainable business performance. Despite the increasing awareness of business and academic research toward sustainable business performance, there are several research gaps within this field that need to be addressed further.

Table 12. Future research directions.

4. Conclusions and limitations

As other researchers have stated (Ferreira, Citation2018), having a map of the conceptual framework for a certain research field can be of great interest in providing a holistic view of the research field, allowing the understanding of relationships between most analysed topics and, thus, highlighting essential research work still to be done. The bibliometric analysis developed from various perspectives within this study on journals, articles, and authors provides comprehensive and relevant insights that allow the identification of fundamental characteristics and systematisation of the body of knowledge of this hot research field on sustainable business performance. Based on the results of the bibliometric analysis, the most popular topics, challenges and directions for future research were discussed, confirming that the research field of sustainable business performance is vital and of increasing interest to both academia and business.