?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study proposes a framework to analyze the strategic value of integration, when separation of ownership and control is considered. According to this framework, we investigate the optimal integration strategy in different control distribution and discuss how external market influences the best strategic choice. Beside theoretical analysis, we also provide evidence from Chinese listed firms to validate our research. The key results of our study show that first, unintegrated strategy works best, if the level of control-ownership disparity is extremely high. Second, in general, vertical strategy is more appropriate for substitute markets, while horizontal strategy may bring more benefits in a highly complementary market. Third, the impact of integration strategy on a firm’s performance is negatively moderated by control-ownership disparity. However, this moderate effect may be weakened by market structure. Our results provide a new and comprehensive perspective for understanding the inconsistent results from previous studies. Moreover, the analysis in this study also highlights a firm’s strategic decision and market regulation policy.

1. Introduction

Integration Strategy has been playing an increasingly important role in international business, and it is gradually transforming into a significant approach that firms adopt to expand and obtain knowhow (Häkkinen et al., Citation2004). Most of previous studies addressing integration strategies have focused on two alternatives, full vertical and horizontal integrations, without considering the partial ownership agreements and control distribution. However, typically, a firm acquires less than 100% of shares in its target firm and its ownership and control is separated, when strategic integration is implemented (Allen & Phillips, Citation2000; Fiocco, Citation2016). In general, the strategy of partial integration and inconsistent control distribution is much more common than that of full integrations (Gilo & Spiegel, Citation2011). Despite the practical relevance of this phenomenon, there are few studies devoted, thus far, to partial integration with inconsistent control distribution. The purpose of our study is to investigate the optimal integration strategy for a firm and how market environment and structure influence the optimal strategy, considering separation of ownership and control. To address this problem, drawing on Milliou and Petrakis (Citation2019) and Douven et al. (Citation2014), we propose a framework with two firm hierarchies, wherein a firm can either integrate backward or horizontally (Douven et al., Citation2014; Milliou & Petrakis, Citation2019). In the benchmark case of no integration, we employ the Stackelberg model to describe the interactions among the firms and show that higher homogeneity of final products tends to enhance market power of upstream firms. Considering separation of ownership and control, we then compare vertical integration with horizontal integration by equilibrium analysis. Based on equilibrium analysis, we argue that the optimal integration strategies primarily depend on market structure, if the integration strategy is implemented without control. In addition, when the integration of firms occurs with centralized control, it complicates the situation. In this case, the optimal integration strategies depend on market structure and will be significantly affected by the ownership structure of integration firms. Subsequently, the impact of market environment and market structure on integration strategies is investigated, respectively. Through the comparative static analysis, the important conclusions of this study are inferred. First, integration strategies outperform no integration in most cases, except for a few rare instances. Second, there is a U-shaped relationship between market environment and firm’s performance. Third, the market environment cannot affect optimal integration strategy when the integration firm’s control is decentralized. Finally, compared with horizontal integration strategy, vertical integration strategy performs better in most cases, except when the market approaches perfect complement. In addition, to validate the framework proposed in this study, we also provide empirical evidence from Chinese listed firms to examine the hypothesis derived from the key conclusions.

The findings of this study contribute to literatures regarding integration strategies. According to previous studies, some firms may primarily pursue profits improvement, market share increasement, or service enhancement by the rapid expansion via integration strategy (Saeedi et al., Citation2017; Xing et al., Citation2017), whereas for others, the motivation for integration is to gain greater control and build a conglomerate (Sorensen, Citation2000; Werle, Citation2019). In general, most of the firms intend to achieve synergies and economics of scale through integration strategies (Schäfer & Steger, Citation2014). According to the previous studies, numerous scholars have focused on the performance differential between integrated and non-integrated firms and shown that the integration strategy leads to efficiency (Chipty, Citation2001; Crawford et al., Citation2018; Droge et al., Citation2012). Hortacsu and Syverson (Citation2007) and Forbes and Lederman (Citation2010), who conduct a case study and an empirical study respectively, find that the integration strategies significantly improve the firm efficiency and increase shareholder wealth (Forbes & Lederman, Citation2010; Hortacsu & Syverson, Citation2007). Similarly, David et al. (Citation2013) who study the integration of U.S. health industry. They argue that integrated organizations exhibit less task misallocation and produce better health outcomes in comparison to unintegrated entities (David et al., Citation2013). Atalay et al. (Citation2014) also infer similar conclusions, by systematically documenting the differences between integrated and non-integrated U.S. manufacturing plants (Atalay et al., Citation2014). Although benefits are clear and emphasized when integration strategy is implemented, literatures on integration strategies have provided inconsistent results and reported many cases of failure (Lin et al., Citation2020; Spoor & Chu, Citation2018). Li et al. (Citation2017) analyze two different cross-industry datasets of firms in developing countries and find a negative impact of integration on firms’ performance (Li et al., Citation2017). They argue that the integration strategies enable inefficient rent-seeking by an insider, particularly in developing country settings—characterized by poor corporate governance and legal protections—and consequently induce the decline in firms’ performance. In this study, we provide an alternative perspective to interpret these inconsistent results on integration strategies by considering the external market and separation of ownership and control in integration process.

A large body of literatures have discussed the impact of vertical and horizontal integration. Herger and McCorriston (Citation2016) explore cross-border integration strategies by using data on cross-border acquisition (Herger & McCorriston, Citation2016). They distinguish between the two strategies and argue that vertical integration relates to endowment seeking motives while horizontal integration rests on a firm’s desire to access to another market. Perez-Saiz (Citation2015) and Moresi and Schwartz (Citation2017) investigate the positive externalities of integration strategy (Moresi & Schwartz, Citation2017; Perez-Saiz, Citation2015). They find that integration strategies may be often accompanied by transfer of intangible assets and can expand the industrial output. The conventional wisdom in these literatures is that vertical integration can eliminate double marginalization, which results in higher sale price, lower demand, lower consumer surplus, and smaller profit, and improves the firm’s performance (Boom & Buehler, Citation2020; Jeuland & Shugan, Citation1983; Vallespir & Kleinhans, Citation2001). Another widely accepted belief is that horizontal integration reduces competition and brings greater market power for integration firms (Nickell, Citation1996). Although this type of integration—to a certain extent—achieves economy of scale for firms, it may also reduce innovation. As a result, the value of social welfare is often uncertain (Huang, Citation2016). In addition, our study is also related to the literature on separation of ownership and control. Since the two competing hypotheses on managerial ownership, ‘convergence of interest hypothesis’ and ‘managerial entrenchment hypothesis’, have been put forward by Jensen and Meckling (Citation1976), the agency problem—which is derived from control-ownership disparity—has become a hot issue for scholars (Jensen & Meckling, Citation1976). Previous studies provide evidence for the practical separation of ownership and control and show that a small number of founding shareholders are effectively controlling a business group through integration strategies and pyramidal ownership chain, particularly in developing countries (Claessens et al., Citation2002; Leuz et al., Citation2003; Porta et al., Citation1999). In the Chinese context, although Jiang and Kim (Citation2015) argue that a series of reforms and regulations implemented by the government may reduce the negative effects of control-ownership disparity, many studies continue to suggest that integration strategies may exacerbate the agency problem between controlling and minority shareholders (Jiang & Kim, Citation2015; Liu et al., Citation2015). To the best of our knowledge, relatively little theoretical research has investigated the integration strategies by considering separation of ownership and control. The seminal articles of Colangelo (Citation1995) and McGuire and Staelin (Citation1983) provide a formal foundation for the equilibrium analysis of vertical and horizontal integrations (Colangelo, Citation1995; McGuire & Staelin, Citation1983). More recently, a framework that describes the partial integration strategies is proposed by Fiocco (Citation2016). The chief contribution of our study is to unveil the optimal integration strategy by considering separation of ownership and control. The results of this study provide novel insights into impact of market environment and structure on integration strategies and can thus be considered to complement and expand on the previous works.

The rest of the paper is organized as follows. Section 2 proposes the framework of our mathematical model, and discusses the benchmark case of a no-integrated firm. Section 3 provides an equilibrium analysis of different integration strategies by considering the separation of ownership and control. Section 4 investigates how market environment and structure affect integration strategy. Finally, Sec. 5 provides empirical evidence from Chinese listed firms to support the main conclusions derived from Secs. 3 and 4. Conclusions and discussions are presented in Sec. 6.

2. The model

Drawing on Colangelo (Citation1995), McGuire and Staelin (Citation1983), and Kim et al. (Citation2019), we consider a two-tier market consisting of an upstream monopolist and two symmetrically downstream firms

and

(Colangelo, Citation1995; Kim et al., Citation2019; McGuire & Staelin, Citation1983). The downstream firms produce differentiated goods, by using—in a one-to-one proportion—an essential input produced by

and face demand for their final goods. In order to describe the market structure, the demand function for firm

with

is assumed by

in our study, with

where

and

represent

’s selling quantities and market prices respectively (Douven et al., Citation2014; Milliou & Petrakis, Citation2019). The intercept

represents the market potential. The parameter

represents market structure of final goods, which indicates the degree of competition intensity induced by consumer preferences (Colangelo, Citation1995). Specifically,

measures the degree of product complementarity. As

approaches −1, the products of

and

become perfect complements. And

measures the degree of product substitutability. As

approaches 1, the products become perfect substitutes, which implies high competition intensity (Bhaskaran & Ramachandran, Citation2011; Tyagi, Citation1999). Where

the products of downstream firms are independent of each other. We assume that when the upstream firm

produces the input at cost

no vertical restraint is available, and no further cost, other than input price, is incurred by downstream firms. This framework can also be considered as an extension and modification of the model by Sim et al. (Citation2019) and Bonanno and Vickers (Citation1988), which has been widely used to investigate the industry structure in the literature (Bonanno & Vickers, Citation1988; Sim et al., Citation2019).

To better appreciate how strategic decisions of integration follows from the presence of vertical and horizontal integration’s value, we first consider the benchmark case in which the three firms (

and

) are separated. A Stackelberg framework is proposed to describe the interaction of upstream monopolist and the two downstream firms (Robson, Citation1990). In the benchmark situation, the upstream firm

at first, sets the prices of intermediate goods, or wholesale prices

with

for downstream firm

by considering

’s response of final goods price. Then, each downstream firm

with

decides its final goods price

to achieve profit maximization. The solution concept we adopt is Pure Strategy Nash Equilibrium (Nash, Citation1951). Proceeding backwards, we first compute the price for final goods of the two downstream firms for a given input price. Afterwards, we derive the prices of intermediate goods. Finally, we obtain the equilibrium profit of each firm. It is worth noting that the order quantity of the downstream firm and its final good price are corresponding one after the other. Therefore, the order quantity

and the price

are determined simultaneously by firm

In the benchmark case, the problem of downstream firm with

may be written as follows.

(1)

(1)

And, the upstream firm’s maximization problem is as follows.

(2)

(2)

Lemma 1.

In the separation case, the equilibrium profits of upstream firm and downstream firm

, with

, are

and

, respectively, as shown as (3) and (4).

(3)

(3)

(4)

(4)

Proof.

Substituting into the objective function in (1), and differentiating this objective function with respect to

yields the first-order conditions (FOCs):

=0 and

=0. Solving the FOCs yields

(5)

(5)

With

and

Then, by substituting (5) into the objective function in (2), and differentiating this objective function with respect yields the FOCs of

After some algebraic manipulation, the FOCs produce the following input price equations.

(6)

(6)

Finally, substituting (6) and (5) into

with

and

we can obtain (3) and (4).

In the benchmark case, we obtain

and

which indicate the equal footing for the upstream monopolist, regardless of the product diversity degree of

and

In addition, denoting

to measure the profit sharing among upstream and downstream firms in separation case, we can obtain

Proposition 1.

Market structure significantly affects profit distribution along the supply chain. In the separation case, higher homogeneity of final products tends to induce higher profit distribution ratio of upstream firm, specifically,

if the final products are perfect complements, the proportion of the upstream firm’s profit to supply chain profit is

if the final products are perfect substitutes, the proportion of upstream firm’s profit to supply chain profit is 1, namely the upstream firm takes all the supply chain profit.

Proof.

Substituting (3) and (4) into yields

(7)

(7)

Taking the derivative of in (7) with respect to

yields

(8)

(8)

The equality (8) illustrates that the profit distribution ratio of the upstream firm increases with the degree of product substitutability, namely the homogeneity of final products. In special case, according to (7), when

and

when

3. Equilibrium analysis of integration strategy

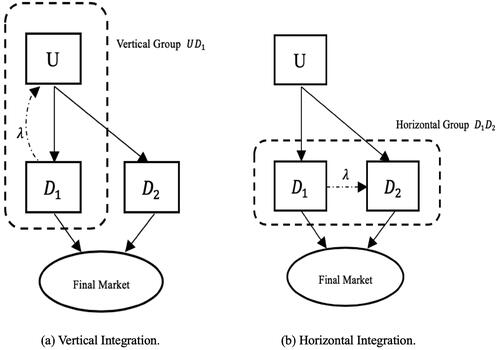

To better appreciate and compare the strategic value of vertical and horizontal integration, we focus on the integration strategy of firm and assume that there is no further cost of integration, without fundamentally changing insights afforded by our model. As shown in , firm

has two alternative integration strategies. The vertical integration strategy can be implemented by firm

In this case, firm

integrates backward and we assume the ownership stake

is acquired by

in

Alternatively, firm

can choose horizontal integration wherein it acquires

per cent of shares in its horizontally related firm

Figure 1. Vertical and horizontal integration.

Source: own research.

Drawing on Fama and Jensen (Citation1983) and Jeter et al. (Citation2018), we consider the separation of ownership and control in both vertical and horizontal circumstances (Fama & Jensen, Citation1983; Jeter et al., Citation2018). Without control, firm receives cash bonuses and cannot influence the decision making of its integrated firms (

in vertical case or

in horizontal case).However, if firm

has control over its integrated firm, besides obtaining cash dividends, firm

can intervene in the decisions of its integrated firm and consequently, maximize its profit. It worth noting that the equilibrium analysis in this section is based on the supply chain system, rather than either stage of supply chain process.

3.1. Integration without control

If control is excluded when firm implements integration strategy, the decision sequence remains the same as the benchmark case. First, the upstream firm

first offers a wholesale price

for the downstream firm

), where the wholesale price

is set to maximize the upstream firm

’s profit. If the wholesale price contract is made, the downstream firm

determines selling order quantity

and market clearing price

simultaneously. Finally, the selling period starts and the profits of upstream and downstream firms are determined.

Without control, the maximization problem of downstream firm and upstream firm

remain unchanged as (1) and (2), regardless of vertical or horizontal integration, namely

and

where the superscript represents vertical (

) or horizontal (

) integration without control, and the subscript represents firm

and firm

However, in case of vertical integration, the problem of downstream firm

may be written as follows.

(9)

(9)

Lemma 2.

In case of vertical integration without control, the equilibrium profits of upstream firm and downstream firm

, with

, are shown as (10)–(12).

(10)

(10)

(11)

(11)

(12)

(12)

where

(13)

(13)

(14)

(14)

Proof.

Proceeding along the same lines as in the Proof of lemma 1, we can obtain Lemma 2.

And, in case of horizontal integration, the problem of downstream firm may be written as (15).

(15)

(15)

Lemma 3.

In case of horizontal integration without control, the equilibrium profits of upstream firm and downstream firm

, with

, are shown as (16)–(18).

(16)

(16)

(17)

(17)

(18)

(18)

Proof.

Proceeding along the same lines as in the Proof of lemma 1, we can obtain Lemma 3.

Either vertical or horizontal integration changes profits composition of firm In addition to the profits from firm

the last terms of (9) and (15) depict the profits from the firm that was integrated by firm

We use superscripts

and

to denote no integration, vertical integration without control, and horizontal integration without control, respectively. We can obtain Proposition 2 in equilibrium.

Proposition 2.

Comparing the equilibrium order quantity and wholesale price of integration case with benchmark.

For order quantity, it holds that:

if

, namely the final market is a complement, then

if

For wholesale price, it holds that:

if

if

Proof.

The solution concept we adopt is the Perfect Bayesian Equilibrium (PBE) (Fudenberg & Tirole, Citation1991), and by proceeding backwards, first, we compute the order quantity and price of final goods for a given wholesale price. Afterwards, we derive the equilibrium wholesale price. The PBEs of benchmark and integration case without control are shown in .

Table 1. PBEs of benchmark and integration case without control.

We prove in part (i) of Proposition 2, and the proofs of other three parts are similar. Denoting

and

we obtain (19)–(21) in the light of .

(19)

(19)

(20)

(20)

(21)

(21)

If given

and the fact that

with

as continuous functions with respect to

and

it yields that

and

By using

we can obtain

and

Combining this with

and

Therefore, if

it holds that

in boundary.

In addition, combining and

in case of

we find four meaningful stationary points:

(-

(

and (

As the stationary points

(-

(

are boundary points that we have discussed, we consider the internal stationary point (

At this stationary point, as shown in (22), we find that the Hessian Matrix of function

is a positive definite quadratic form.

(22)

(22)

where

Therefore, the stationary point ( is a local minimum point of function

Since

=0, we obtain

within defined space. Similarly, we can find

and

within defined space. Combining

and

we consequently find

Since the downstream firms are decentralized to maximize their individual profits without control, the Herfindahl-Hirschman Index (HHI) of final market remains unchanged (Calkins, Citation1983). Proposition 2 indicates that the market structure is important for the equilibrium decisions of all firms. Since

and

hold, horizontal integration improves market demand (

) in a complementary market, while it decreases market demand (

) in a substitute case, compared with the benchmark case. For vertical integration, complementary market induces greater market share for firm

and less market share for

respectively, and the opposite happens in the substitute market’s circumstance. Besides, compared with the benchmark case, the wholesale price for both downstream firms are increased by vertical integration in complementary market (

with

). In substitute market, it is more favorable for firm

to adopt horizontal integration strategy without control. This may be induced by considering upstream profit of firm

in vertical integration. It worth noting that according to , the order quantity and market price for both downstream firms are the same in the horizontal case. Accordingly, the different profits of downstream firms depend only on the differentiated price strategy provided by upstream firms.

In general, given the ownership stake acquired by

with the absence of control, vertical integration makes profits of firm

sensitive to that of firm

and consequently puts firm

at a disadvantaged position, compared with non-integrated rival

On the other hand, horizontal integration, to some extent, gives more bargaining power to downstream firms for renegotiating with upstream firm and results in market expansion. Further, the Proposition 3 explains how the degree of integration (ownership stake acquired by

) influences the strategic selection of firm

in the absence of control.

Proposition 3.

In the absence of control, integration strategy always gains a better performance than no integration circumstance. In addition, there are two thresholds of market structure and

that make the following arguments hold.

if

if

if

the vertical strategy outperforms the horizontal strategy for firm

the horizontal strategy outperforms the vertical strategy for firm

Proof.

Denoting with

as a function of

we have that

is a constant and

Proceeding along the same lines, as in the proof of Proposition 2, since

and

we can obtain

and

This shows that firm

always prefers the integration strategy.

Suppose due to Fourier-Budan Theorem and Descartes’ Rule, we can derive that there is a real root in the interval

if and only if

and there is no real root in the interval

if and only if

or

(Bensimhoun, Citation2016; Melkman, Citation1974). When

we denote the real root of function

in

as

The

and

are shown as (23) and (24).

(23)

(23)

(24)

(24)

where

In addition, and for every

small enough, inequality

holds. Combining with the facts that

if

and

if

Proposition 3 is proved. ■

The Proposition 3 illustrates the dependence of integration strategy on shareholding and market structure in uncontrolled circumstance. First, integration strategy not only opens new profit sources for firm but also makes firm

in the advantage position in the competition with its rival. Because of this, integration strategy, whether vertical or horizontal, is always preferred by firm

compared with no integration strategy. Second, it is worth noting that

This says that the vertical integration is always adopted when the final market is substitute. In a complementary market, integration strategy depends on the degrees of market complementarity. At last, a stronger market complementarity leads horizontal strategy adopted by firm

while the ownership stake has become the determinant for strategic alternatives in an independent final market. Generally, vertical integration strategy promotes two effects: revenue and control. It helps firm

in getting a part of the revenue from firm

by holding some shares of firm

Consequently,

’s profits increase (revenue effect) and since the integrated firm

is not controlled by

vertical integration does not weaken double marginalization. Instead, it puts firm

at a disadvantaged position when negotiating with firm

For this reason, vertical strategy may decrease the profit of firm

(control effect).

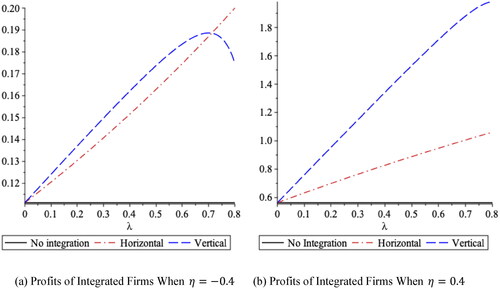

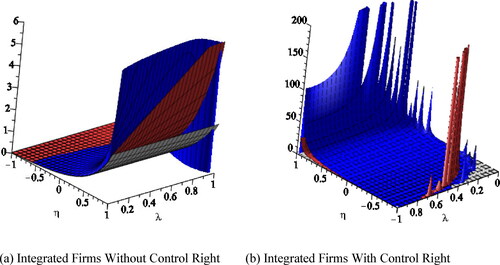

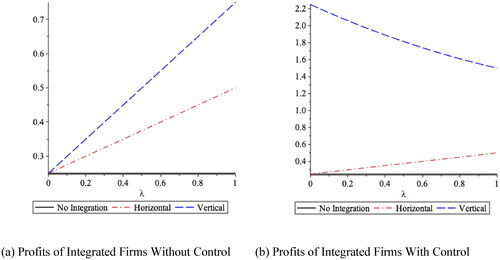

When we assign the parameters with the values: shows the profits of uncontrolled integration firms

and the benchmark

in case of

and

respectively. It worth mention that figure shape maintains unchanged when

and

takes positive and negative values respectively. The essential reason behind Proposition 3 may be due to the tradeoff between these two effects. In case of the substitute market, there is keen competition between the two downstream firms. Consequently, upstream firm

takes the major profit of the supply chain and the revenue effect is enhanced. On the contrary, the complementary market endows downstream firms greater bargaining power to negotiate the contract terms with upstream firm. In this case, the control effect is determinant. In addition, when the products in final market are independent, the stock holding quantity is important, and higher per cent of shareholding makes the revenue effect significant.

Figure 2. Profits of integrated firms without control.

Source: own research.

3.2. Integration with control

If integration strategy of firm enables the control, we denote the vertical integration group as

and the horizontal integration group as

(shown in ). In case of vertical integration, firstly, the wholesale price

for firm

), selling order quantity

and market clearing price

are simultaneously decided by the vertical group

to maximize the profit of its parent firm (ultimate controlling owner of group

). After the wholesale price contract is offered to firm

by group

firm

determines its selling order quantity

and market clearing price

Finally, the selling period stars and the profits of group

and firm

are determined. In case of horizontal integration, the decision sequence can be described as follows: First, the upstream firm

sets a wholesale price

for firm

) to maximize its profit. Then, the horizontal group

determines its selling order quantity

) and market clearing price

), simultaneously, to maximize the profit of

’s parent firm (ultimate controlling owner of group

). Finally, the selling period starts and the profits of firm

and group

are determined.

Considering control for integrated firm, the offered for firm

can be seen as internal settlement price of group

in vertical integration. Therefore, we can derive the Lemma 4 below.

Lemma 4.

In case of vertical integration with control, the equilibrium internal settlement price of group is zero, namely

Proof.

In case of vertical integration with control, the problem of group ’s ultimate controlling owner can be written as

(25)

(25)

Differentiating the objective function of (25) with respect to yields

To maximize

is offered by group

Comparing the problem (25) and (9), it is found that control right brings more discretion to vertical integration group. In case of centralized decision making, the parent firm of vertical integration group can not only determine its own order quantity and market price, but also design contract of upstream firm offered to its rival. We keep the optimal problem of firm unchanged, and Lemma 5 can be obtained.

Lemma 5.

In case of vertical integration with control, the equilibrium profits of integration group and its rival

are shown as (26) and (27).

(26)

(26)

(27)

(27)

Proof.

Proceeding along the same lines, as in the Proof of lemma 1, we can obtain Lemma 5.

In the circumstance of horizontal integration, we suppose the downstream firms and

forms a group

In this integration group, the ownership stake

of subsidiary

is acquired by its parent firm

and the ultimate control of this group is reserved by parent firm

In this case, the problem of firm

the ultimate controlling owner of group

can be written as (28).

(28)

(28)

Lemma 6.

In case of horizontal integration with control, the equilibrium profits of the upstream firm and the integration group

are shown as (29) and (30).

(29)

(29)

(30)

(30)

Proof.

Proceeding along the same lines, as in the Proof of lemma 1, we can obtain Lemma 6.

Generally, if the ultimate control is reserved by parent firm, we solve problems (25) and (28), by proceeding backwards. The PBEs of benchmark and integration cases with control are shown in .

Table 2. PBEs of benchmark and integration case with control.

illustrates the solutions of decision variables and profits in equilibrium. In analogy with the solutions in , when control transfers from subsidiary to integration firm, vertical integration avoids double marginalization, because and price discriminates against the non-integrated rival because

At this point, the control effect disappears and only revenue effect remains in vertical integration. In horizontal integration, the internalization of cross-price effect on demand by this integration increases the market power of group

If we measure the profits of entities in group

separately, we find that firm

is losing money due to

and

If we consider the centralized decision making of downstream firms, the group

created by horizontal integration, is monopolizing the final market. Proposition 4 explains how the degree of integration (ownership stake acquired by

) influences the strategic selection, if the decision making of integration group is centralized by firm

Proposition 4.

When the ultimate control is reserved by integration firm:

In case of complementary market (

if , then no integration outperforms either integration strategy for firm

if , then the vertical strategy outperforms either horizontal strategy, or there is no integration for firm

if , then the horizontal strategy outperforms either vertical strategy or there is no integration for firm

In case of substitute market (

if , no integration performs best when

, and vertical strategy performs best when

for firm

if, no integration performs best when

, horizontal strategy performs best when

, and vertical strategy performs best when

, for firm

In case of independent market (

Proof.

Denoting with

and

as a function of

we obtain that the

is a constant and both

and

are hyperbolas. According to and , combining with

the asymptote of

and

are (31) and (32), respectively.

(31)

(31)

(32)

(32)

First, we prove the conclusion that if

if

and

if and only if

Taking the derivative of

with respect to

yields

Due to the condition of

we get that the

is positive (

). Moreover, we can easily prove

if

and

if

In case of

that was induced by

and

hold, simultaneously. Combing with the condition that

if

and

the conclusions above are proved.

Then, the properties of curves of and

can be obtained due to their hyperbolas:

and

if

and

if

and

always hold in

if

Besides we get

and

Furthermore, for hyperbola

there is a minimum at its right branch due to the first order condition of

with respect to

This minimum of

is obtained as:

(33)

(33)

where

It can be easily show that if

and

if

In case of since

and

the hyperbola

has only one intersection at its left branch, with the straight line

We denote the abscissa of this interaction as

Comparing

and

we get

Combing with

we can get that the curve

and

has two intersections. We denote the abscissa of these two intersections as

and

and part (i) of Proposition 4 is proved. However, in case of

combing

and

it easily shows that the hyperbola

has only one intersection at its right branch, with the straight line

We denote the abscissa of this interaction as

Combing

and

the hyperbola

and

have intersections in

Hence, part (ii) of Proposition 4 is proved.

Finally, in case of =0, the profits function of

and

can be obtained as:

(34)

(34)

(35)

(35)

(36)

(36)

According to (34)–(36), we get in

Hence, part (iii) of Proposition 4 is proved.

The Proposition 3 is proved.

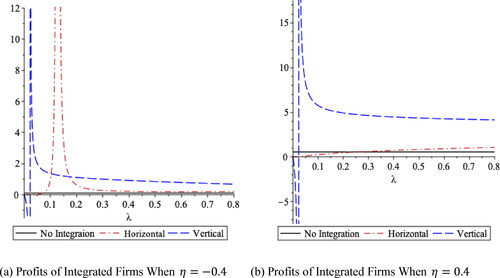

describes the profits of integration firms

and the benchmark

in case of

and

respectively. It worth mention that the shape of curves in remains unchanged if

takes positive and negative values respectively. According to , the benefits gained of integration are significantly affected by the proportion of acquired stakes. Contrary to intuition, with an increasing shareholding ratio, the profits of integration firms do not continuously rise, and the relationship between firm value and the ratio of its controlled shareholdings is not monotonous. For horizontal and vertical integrations, there are optimal ratios to takeover for inducing the maximize profits. Besides, the optimal ratio in horizontal case is always higher than it is in vertical integration, regardless of whether the market is complementary or substituting. also intuitively explains Proposition 4. The control right can bring excess return for integration firm, only if the proportion of acquisition stakes exceeds a certain level. When the market complements, horizontal integration has a better performance for integrated firms in case of minority stakes, and the vertical outperforms horizontal integration in case of majority equity. Contrarily, in the substitute market, the vertical integration strategy always outperforms the horizontal integration strategy. Compared with the complementary market, the downstream firms face more competition in a substitute environment. In this case, vertical integration strategy can significantly improve the firm’s competitiveness and help it to gain a cost advantage over its rival.

Figure 3. Profits of integrated firms with control.

Source: own research.

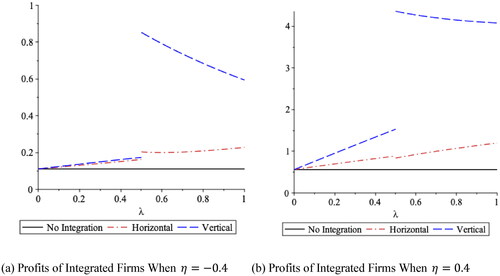

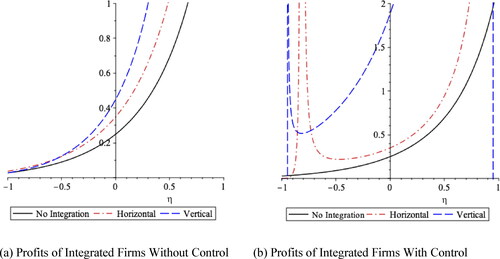

It is noteworthy that we separate the control right of integration firms from its ownership structure, in our equilibrium analysis. Although separation of corporate ownership and control is widely discussed in previous studies, the stock right continues to be accompanied by voting right, in most cases (Kim & An, Citation2018; Maximiano et al., Citation2013). The absolute holding big shareholder dominates various resources of the firm in general circumstances. Considering the consistent situation between ownership structure and control right, we suppose that the integrated firm can control its subsidiary, only if it owns more than 50% of the subsidiary’s stock. When the integrated firm is limited to 50% stakes in the firm being pursued, it cannot control its subsidiary after integration strategy, and the subsidiary may make its decisions independently. We fixed the value of parameters as: and

In the circumstance that the corporate ownership and control is consistent, illustrates the profits of vertical and horizontal integration firms, in case of

and

respectively.

Figure 4. Profits of integrated firms in consistent circumstance between ownership and control.

Source: own research.

In , we assume that the integration firm controls its subsidiary, only if it holds more than half of its subsidiary’s stakes. In , the market structure parameter takes values of −0.4 and 0.4 as examples. However, the main shape of figure may not change if the takes other positive and negative values. According to , regardless of whether the market structure is complementary or substitute, vertical strategy is always better than horizontal strategy, and the horizontal strategy is always better than no integration strategy for integration firms. This may be induced by two determinants. First, the benefits from upstream and downstream markets can be gained by the integration firm in vertical strategy, while in horizontal strategy, the integration firm can only get the benefits from the downstream market. Second, compared with horizontal strategy, vertical strategy gives more competitive advantage to integration firm through merging the upstream firm. In addition, since the substitutability of final products moderates these two determinants positively, also shows that substitute market is more valuable than complementary market, for either horizontal or vertical strategy. Finally, we argue that these conclusions from are derived by the assumption that the threshold of shareholdings for control right is 50%. If the threshold is less than 50%, the conclusion that vertical strategy performs best in all cases cannot be maintained.

4. Impacts of market environment and structure

The propositions 3 and 4, which we discussed in Sec. 3, have provided us the strategic decisions in equilibrium by static comparison. This static analysis treated the strategic value as a function of ownership structure and fixed the parameter of market environment and market structure as exogenous given. However, the strategic value of vertical or horizontal integration is affected by internal ownership structure and external market environment and structure. Thus, we study how the market environment and structure affect the integration strategy in this section.

4.1. Impact of market environment

Drawing on Yang et al. (Citation2015), we consider the raw material cost and the potential demand of market

in our framework, as the proxies for market environment (Yang et al., Citation2015). A relatively lower raw materials cost and higher potential market demand—which are affected by macroeconomic policy (Gupta & Gerchak, Citation2002), economic cycles (Derouiche et al., Citation2018), or characteristics of specific industry (Uysal, Citation2011), et al—represent a better market environment, while a worse or more competitive market may induce increase in cost and decrease in demand.

To study the impacts of market environment wherein ownership structure and control is separated in integration firm, we compare the different strategic values corresponding to fluctuating raw material costs and potential market demand. If we consider the equilibrium strategic values, namely the equilibrium profits with

as the functions of either

or

it is clear that

with

are all quadratic functions with respect to either

or

and represent three upward parabolas with the same symmetric axis (

in functions of

and

in functions of

). Since the coefficient of quadric entries of

cannot be bigger than that of

and

simultaneously, this indicates that the strategy choice only depends on the size of the opening mouth of parabolas

and

and consequently, is independent of the market environment, when integration strategy is implemented without control. Comparing the opening mouth of parabolas

and

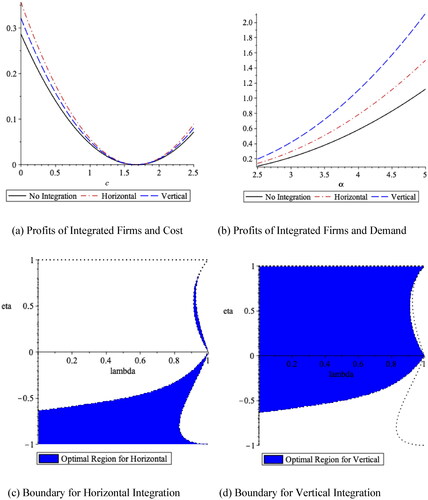

illustrates the profits of integration firm in different market environments and the boundary conditions for an optimal integration strategy. Firstly, implementation of integration strategy is appropriate for a specific firm. Either vertical or horizontal strategy can bring more benefits for firms compared with strategy of no integration. Secondly, if the distribution of control in subsidiaries is decentralized after integration, neither raw material cost nor market potential demand can affect the strategy choice. The optimal strategy only depends on market and ownership structures. Thirdly, in case of substitute market, vertical integration obtains more benefits, in most cases, and horizontal strategy performs best, only if shareholding of integration firm to its subsidiary reaches approximately 100%. In the complementary market, horizontal strategy induces more benefits in case of strong complementary, while vertical strategy can perform better in case of weak complementary.

Figure 5. Impacts of market environment without control.

Source: own research.

In addition, we study the impacts of market environment wherein the integration firm completely controls the subsidiary. When the integration strategy is implemented with the concentration of control, shows the profits of the integration firm in different market environments. It is obvious that there is a U-shaped relationship between firm’s performance and market environment, provided that ownership structure and control is separated in integration firm. Denoting the symmetric axis of parabolas

and

as

and

respectively, we can obtain that the

based on . Comparing the size of opening mouth of the three parabolas and positions of their symmetric axis, illustrates the boundary conditions for an optimal integration strategy. According to , first, the integration strategy is not always superior. When the market approaches perfect substitute and integration firm has a minority stake in its subsidiary, the integration strategy may induce a decrease in the firm’s value. Second, the strategies of no integration and horizontal integration cannot be the best choice when the market is complementary. Third, even in the substitute market, vertical integration strategy performs best in a vast majority of cases. Moreover, the strategies of no integration and horizontal integration perform better than that of vertical integration, only in case of minority stakes. At last, the integration decision process is complex and the explicit solution of indifference region for horizontal, vertical, and no integration cannot be found from function

and

Thus, to investigate the indifference region for different strategies, numerical analysis is conducted and shows the indifference curves for vertical, horizontal, and no integration.

Figure 6. Impacts of market environment with control.

Source: own research.

Besides, in the complementary market, the vertical integration strategy performs best, if the complementarity of market is lower. Moreover, when the market approaches perfect complement, the performance of different strategies is uncertain. For example, in the highly complementary market, if the integration firm only holds a minority stake in its subsidiary, there are two threshold costs, and the vertical integration strategy performs best, if

and no integration strategy performs best, if

4.2. Impact of market structure

The equilibrium profits

and

with

can be considered as the functions of two variables, ownership structure

and market structure

Since the explicit expression of

and

cannot be derived from the function of equilibrium profits, a numerical analysis is conducted to investigate how the ownership and market structure impact the strategy choice. To be consistent with previous static analysis, we set

and

without affecting the main analytical results. According to numerical simulation, provides us with the 3D images to explain how the strategic value of vertical and horizontal integrations, namely the profits of such firms, is affected by ownership and market structure.

Figure 7. Profits of vertical and horizontal integrated firms.

Source: own research.

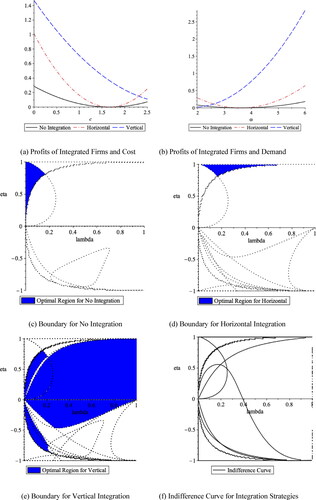

In , the blue and red surfaces represent profit of vertical and horizontal integration firms, respectively. The grey surface represents the benchmark that the profit of firm without integration. As shown in , regardless of whether the ownership and control are separated in the integration firm, vertical integration strategy outperforms horizontal and no integration strategies, with a few exceptions. If the integration strategy is implemented without control right, horizontal strategy performs best, only if the market structure approaches perfect complement or the integration firm has nearly 100% shares of its subsidiary. This is because the market’s complementarity and subsidiary’s equity portion that are acquired by integration firm moderate the advantage creation of horizontal integration, positively. However, when the integration firm is centralized, the space wherein horizontal performs best includes complementary market and minority stakes (approximate 30% to 40%). In case of majority stakes, the strategy of horizontal integration outperforms that of vertical and no integration, only if the market is nearly perfect substitute. This conclusion derived from is—to a certain extent—supported by Gupta and Gerchak (Citation2002). They argue that in a perfect substitute market, integrating with horizontal rivals creates advantages, such as improving market power, which may be not possible with its vertical firms (Gupta & Gerchak, Citation2002). Furthermore, to study the impacts of market structure on strategic value, we extract the cross-section projection of from the 3D images in . The cross-section projection, which illustrates how the profits of integrated firms change with market structure is shown as .

Figure 8. Profits of integrated firms and market structure.

Source: own research.

shows the impacts of market structure on the value of different integration strategies. When the control right is maintained in the subsidiary after integration, the strategy of vertical integration outperforms that of horizontal and no integration, except for a small interval of market structure However, the impacts of market structure may become complex, when the control right is transferred to integrated firms. In this case, the optimal strategic choice depends on the ownership structure, when the market is nearly a perfect complement, or substitute. Besides, in most areas of market structure

the strategy of vertical integration outperforms that of horizontal and no integration, except for a specific complement interval (for example the approximate complement interval is

if

as shown in ), wherein the horizontal strategy performs best.

At last, the profits of integrated firms in an independent market () is illustrated by . Significantly, the vertical integration is always the optimal strategy choice, when the market of final products is independent. It still worth noting that the conclusions derived from are general. Although specific regions or curves shown in coordinate plane may vary in detail, their shapes are the same in principle.

Figure 9. Profits of integrated firms in case of independent market.

Source: own research.

5. Empirical analysis: evidence from China

According to the equilibrium analysis above, several hypotheses can be derived from our framework. First, the integration firms may perform better compared with no integration firms, in most cases. Second, the sensitivity of integration strategy to firm’s performance tends to increase with the market substitutability. Third, the impact of integration strategy on performance would be negatively moderated by a separation of ownership and control. Fourth, this moderated effect of separation of ownership and control would be weakened with the horizontal case in a complementary market, and with the vertical case in a substitute market. At last, there is a U-shaped relationship between the performance of integration firms and market environment. In this section, we provide evidence from Chinese listed firms to support the hypotheses.

5.1. Data, sample, and variables

Our data were collected from the Wind database,Footnote1 CSMAR database,Footnote2 and feasibility report of merger and acquisition proposed online.Footnote3 In the initial sample, we include all merger and acquisition deals first announced by acquirers in Chinese market, between January 1, 2010 and December 31, 2018, where the acquiring firms were publicly listed on the Chinese stock market. To obtain our final sample, following ‘Listed Company Professional Classification Directions’ issued by China Security Regulatory Commission (CSRC), we discard financial firms since the specifics of their financial resources compared with other industries (Derouiche et al., Citation2018). Besides, drawing on Uysal (Citation2011) and Flannery and Rangan (Citation2006), we also exclude the utility firms, such as QIAOYIN Co. Ltd., Interchina Water Treatment Co. Ltd., etc., and the firms with insufficient information (Flannery & Rangan, Citation2006; Uysal, Citation2011). The final sample consists of observations, covering 1764 firms, wherein approximately 23% of our initial samples, over the period from 2010 to 2018.

Through manually collecting and collating data in a feasibility report of mergers and acquisitions, first, we create two dummy variables: vertical integration (VER) and horizontal integration (HOR). The variable (VER) takes the value of one, if either acquiring and target firms belong to a same industry according to ‘Listed Company Professional Classification Directions’ issued by CSRC, or the markets faced by acquiring and target firms are highly relevant. And the value is zero otherwise. The variable (HOR) takes the value of one, if the acquiring and target firms belong to different industries according to ‘Listed Company Professional Classification Directions’ issued by CSRC, or else the value is zero. Then, the NERI index of marketization of China’s provinces (NNM) that the acquiring companies subordinate to, which is the most popular instrument to measure market environment in the Chinese context is used as a proxy for the market environment faced by integration firms (Fan et al., Citation2011, Citation2019; Ma & Liu, Citation2016). Finally, in order to describe the market structures as close as modeled by our framework, we propose two measures to act as proxies for market structures: Market Substitutability (MS) and Market Complementarity (MC) following Nevo (Citation2001) and Palmatier et al. (Citation2007), which we define as follows (Nevo, Citation2001; Palmatier et al., Citation2007).

Market substitutability (MS) is defined as the extent to which a close substitute exists for a specific product. Consistent with prior studies, MS in this paper is calculated as total sales of listed companies in the same industry divided by total operating costs of listed companies in the same industry, where industry is given by ‘Listed Company Professional Classification Directions’ issued by CSRC (Liu et al., Citation2018). A larger value of MS indicates a higher degree of substitutability.

Market complementarity (MC), following Palmatier et al. (Citation2007), is measured by questionnaire survey through sojump.com (the largest online survey website in China) and graduate students from Southwestern University of Finance and Economics in China (Palmatier et al., Citation2007). The respondents rated the firm-level performance in terms of products and marketing which represent the complementarity of market. The response set for these items was in a 10-point scale ranging from 1, lowest complementarity, to 10, highest complementarity. We collect the data of MC through a self-administrated questionnaire, following the procedure adopted by Ray et al. (Ray et al., Citation2004). At last, we have received 402 useable survey responses, thereby producing a response rate of 67%.

According to Li et al. (Citation2020), we estimate the level of firm’s control-ownership disparity (COD) based on CSMAR, in which it identifies a single ultimate controlling shareholder and consequently provides a measure of level of firm’s control ownership disparity for each firm (Li et al., Citation2020). Consistent with most of previous studies, control is determined as by voting right while ownership refers to rights for cash flow (Cumming et al., Citation2019; Villalonga, Citation2019). If the shares of a firm are taken by owners directly, control rights and ownership are equal. The diverging of control and ownership only occurs in case of pyramid or cross-holding schemes. For example, imagine a chain of ownership in which firm M (or a person) plays the role of ultimate owner of firm T and owns 90% shares of firm S which in turn owns 25% of firm K which in turn wholly owns firm T. The cash flow rights for firm M in firm T are calculated as 0.9*0.25*1 = 22.5%. If all ownership shares in this case carry equal voting rights, the control rights of ultimate owner, firm M, in firm T is 25%. Therefore, in this case, we can further compute control-ownership disparity (COD) for firm T as 25%-22.5%=2.5%.

Further, the conventional event studies are chosen to help us to estimate the performance of integration firms from two aspects: short-term marketing performance and long-term strategic performance for integration.

Short-term marketing performance is estimated by four-day cumulative abnormal returns (CARs), after merger and acquisition announcement. According to previous studies, the four-day CARs is usually used to measure the consequence of merger and acquisition (El-Khatib et al., Citation2015; Tao et al., Citation2019). In this study, for each merger and acquisition announcement, first, we estimate the abnormal returns of stocks for integration firms, i.e., acquirers during a four-day

Long-term strategic performance for integration is measured by two-year lagged industry adjusted Tobin’s q which is used to measure the long-term performance by many scholars (Callahan et al., Citation2003; Esqueda et al., Citation2019; Lin et al., Citation2018). Specifically, we first compute the Tobin’s q as follow.

where represents the market value of equity,

represents preferred stock,

represents debt that equal to long-term debt plus short-term liabilities minus short-term assets, and

is the total assets. All these data can be found in the balance sheet at the end of second year after the merger and acquisition are announced.

The two-year lagged Tobin’s q is then adjusted for industry effects by subtracting the average Tobin’s q for the industry.

In addition, a series of control variables are used in our study, in accordance with most of the previous literatures pertaining to firm performances, in the Chinese context (Brandt et al., Citation2017; Kuo et al., Citation2014). The firm size (SIZE) is a natural log of a firm’s total assets. Firm growth is controlled by book-to-market value ratio (BM). Leverage ratio (LEV) and free cash flow (FREECASH) are proxies for firm’s financial risk. The integration strategy is controlled via two variables: merger and acquisition deal size (RELSIZE) and the indicator of whether a target firm is public listed prior to announcement date (PUBLIC). Besides, return on assets (ROA), which is defined as a ratio of net profit to the lagged total asset is used as the benchmark of the firm’s performance. Furthermore, a dummy variable (PROPERTY)—with the value of one, if the integration firm is state-owned, otherwise zero—is also introduced as a control variable. To reduce the effect of errors caused by outliers, we winsorize all the variables at 1% and 99% levels.

5.2. Empirical results

To empirically investigate the relation between firm’s performance and its integration strategy, we conduct a multivariate regression analysis with the four-day CAR, CAR(0,+3), and two-year lagged industry adjusted Tobin’s q as the dependent variables respectively. Key independent variables include integration strategies (VER and HOR), control-ownership disparity (COD), market structures (MS and MC), and market environment (HNM). represents the results of regression analysis, after controlling for year fixed effects.

Table 3. Regression results of firm’s short-term (long-term) performance.

reports the regression results of the influence of integration strategy on firms’ short-term and long-term performance. The numbers reported out of the brackets and in the brackets in are the regression coefficient of regression model with dependent variable of four-day CAR, CAR(0,+3), and two-year lagged industry adjusted Tobin’s q respectively. According to the results, the first column, model 1, reports the results of the impact of integration strategies on the firm’s performance. Consistent with conclusions from the most previous literatures, we find that the firms, which implemented integration strategy, are more likely to perform better as the VER and HOR are positively and significantly associated with both and two-year logged industry adjusted Tobin’s q (Ogada et al., Citation2016; Zhang et al., Citation2018). Nevertheless, the contribution of horizontal integration on firms’ long-term strategic performance is not as significant as it in short-term aspect. Intuitively, it illustrates that the diversification discount is more apparent over long periods. Generally, the model 1 indicates that the integration firms may have better performance compared with no integration firms.

Model 2 and model 3 shown in report the results of estimating the effect of market structure on the integration strategy’s sensitivity. We use market substitutability (MS) and market complementarity (MC) as proxies for market structure in model 2 and 3 respectively, and find that the coefficient that measures the effect of market substitutability on sensitivity of integration strategy is positive and significant at 10% level. Besides, from model 2 and model 3, the key points of note include: First, the impact of both market substitutability and market complementarity on firm’s performance are significantly positive no matter or two-year lagged industry adjusted Tobin’s q is chosen to proxy the firm’s performance. This may illustrate that heterogeneous market promotes firms’ performance. Second, if we focus on short-term performance, effect of market complementarity on integration-performance sensitivity is not significant. It shows the sensitivity of integration strategy to firm’s performance tends to increase with the market substitutability, and cannot be moderated by market complementarity. Comparing the coefficients of two interaction terms in model 2, the interaction terms of model 3 is not feasible in short-term performance, suggesting only a higher degree of market substitutability can bring more benefits through the integration strategy and a higher degree of market complementarity may not contribute to the integration-performance sensitivity. However, we find sensitivity of horizontal integration rather than vertical integration to firm’s performance is significantly positive associated with market complementarity when considering firm’s long-term performance. This phenomenon illustrates that both complementary market and substitute market may moderate the effect of integration strategy on firm’s performance in long term. At last, although the interaction term of vertical integration and market complementary in model 3 is not feasible, the negative coefficient still partly explained the phenomenon of diversification discount.

Model 4 examines the impact of control-ownership disparity on firm’s performance and the effect of control-ownership disparity on the sensitivity of integration strategy. Consistent with most of previous studies, coefficient of COD is negative and statistically significant in our regression model, indicating that control-ownership disparity had a negative effect on the firm’s performance (Monsen et al., Citation1968). Following previous literatures, this may probably be induced by critical agency problem (Shaikh et al., Citation2019; Wang & Chou, Citation2018). Besides, in terms of economic significance, model 4 shows coefficients in circumstance of firm’s short-term performance on interaction terms between integration strategy and firm’s performance, that are −0.014 in vertical case and −0.020 in horizontal case, respectively. And those in circumstance of firm’s long-term performance on interaction terms between integration strategy and firm’s performance, that are −0.010 in vertical case and −0.017 in horizontal case, respectively. It proves that control-ownership disparity can moderate the impact of integration strategy on performance negatively, regardless of whether the integration strategy is vertical or horizontal and whether we use or two-year lagged industry adjusted Tobin’s q to measure the firm’s performance. However, this moderate effect of control-ownership disparity is more effective in the horizontal circumstance compared with vertical one. Column 5 and 6, the models 5 and 6, investigate the moderate effects of market structure based on model 4. It is clear that the primary conclusion derived from our mathematical framework that the moderated effect of control-ownership disparity would be weakened with horizontal integration in a complementary market and vertical integration in a substitute market is supported by our empirical evidence. Finally, in model 7, we examine the impact of market environment on the firm’s performance. In model 7, we use the NERI index of marketization of China’s provinces (NHM) as the proxy of market environment and find that the coefficient of market environment is negative, while that of its square is positive, in terms of economic significance. In general, model 7 illustrates the U-shaped relationship between the market environment and firm’s performance and, in a manner, not only supports the conclusions derived from our framework, but also confirms the inference of literature from a specific perspective (Yuan et al., Citation2020).

5.3. Robutness test

For a robustness check, different event windows i.e., (0,+5), (0,+9), are used for estimating CAR firstly, and it finds that the sign of main independent variables and its interaction terms remain unchanged and significant in all models shown in . Then, robustness tests are conducted for variables of market environment. As the Herfindahl-Hirschman Index (HHI) is generally considered as the best measurement for external environment, which greatly affect firms’ performance, we use the HHI as the proxy for market environment and observe the same results (Ni et al., Citation2017; Owen et al., Citation2007). In addition, considering four-day CAR as the proxy for firm’s performance, we also divide the samples into two groups based on the level of firm’s control-ownership disparity, following Lee and Chun (Lee & Chun, Citation2014); these findings are shown in . The results are unchanged and even stronger, compared with the conclusions derived from .

Table 4. Robustness check for different levels of control-ownership disparity.

Since DID (difference-in-difference) model can control the systematic differences between treatment and control groups and isolate the changes in outcomes over time between the samples that were or were not influenced by integration strategy, it is powerful to avert endogenous problems that typically arises (Meyer, Citation1995; Mohsin et al., Citation2021). As a result, in this study, DID approach is also employed in robustness tests for both substitute and complementary market sample group considering two-year lagged industry adjusted Tobin’s q as the proxy for firm’s performance at last.

After pairing samples that ever never announced merger and acquisition in our sample periods based on principle of industry and firm’s size, 3096 observations are finally obtained by us. The proposed DID model can be then defined as follow.

(40)

(40)

(41)

(41)

where

represents the two-year lagged industry adjusted Tobin’s q.

is a dummy variable for control-ownership disparity. If the level of control-ownership disparity is high,

otherwise,

and

are the dummy variables to represent whether the firm implement vertical or horizontal integration respectively.

is the vector of control variables including firm size (SIZE), firm growth (BM), leverage ratio (LEV), free cash flow (FREECASH), merger and acquisition deal size (RELSIZE), target firm’s type (PUBLIC), return on assets (ROA), and a dummy variable for firm’s property (PROPERTY). The

and

are the intercepts, and

and

are the random term (or disturbance) of DID model. reports the results of robustness test through DID method. According to , the main results derived from both mathematical framework and empirical evidence of our study are verified by DID robustness tests that first integration strategies generally improve firm’s performance. Then, consistent with results from , the influence of integration strategies on firm’s performance is significantly negative moderated by control-ownership disparity. At last, it also verifies that this moderated effect for vertical integration is weakened in substitute market, while it for horizontal integration is weakened in complementary market.

Table 5. Robustness check based on DID approach.

6. Conclusions and Discussions

Integration strategies have become an inseparable part of firms’ development. Although partial acquisition and control-ownership disparity is typically practiced, most of the previous theoretical and empirical literatures pertaining to integration strategies have ignored the ownership structure and control distribution in integration. In this study, by considering separation of ownership and control, a framework is proposed to provide the optimal integration strategies for a firm and investigate how market environment and market structure influence the optimal strategies.

Based on the equilibrium analysis of our framework, the main conclusions of our study are inferred. Firstly, the profits distribution in supply chain is dependent on the market structure. In addition, substitute market is more beneficial for upstream firms than complementary market. Secondly, whether it is vertical or horizontal, integration strategies are profitable for firms, except for some rare cases. Specifically, unintegrated firms outperform integration firms, only if holding minority stakes in subsidiaries can bring absolute control for subsidiaries. Thirdly, when the integration group is decentralized, market structure is determinant for different integration strategies, while the integration strategy depends more on ownership structure, when integration firms can absolutely control its subsidiaries. In general, compared with horizontal integration, vertical integration performs better, in most cases. Horizontal integration overperforms vertical integration in a market with high degree of complementarity. Finally, we find a U-shaped relationship between the firm’s performance and market environment, and argue that the market environment cannot affect the integration strategy when the target firm cannot be controlled by acquirer after integration. In addition, empirical analysis conducted by us provides Chinese evidence for the impact of integration strategy on firms’ performance. This empirical evidence tests hypothesis derived from our main conclusions and consequently validates the framework proposed in this study, to a certain extent.

Our findings make important theoretical contributions to the literature. This study is among the first to investigate the integration strategies, by considering the separation of ownership and control. Compared with the previous studies, the framework proposed in this study is more comprehensive and can be considered as an extension of existent mathematical models. This framework is not limited to strategies’ comparison and decision optimization for a specific integration firm; it can also be easily extended to diverse complex circumstances. The results of our framework and the empirical evidence derived from equilibrium analysis also contribute to the literature. They support the previous studies, to a certain extent, and provide an alternative perspective to explain the strategy choice for integration. In addition, some useful implications can be derived from our study for integrated business groups and the market regulatory authorities. We provide reference guides for integration groups on how to choose the integration strategy and develop an internal ownership and control structure based on market environment and market structure to maximize its benefits. Furthermore, our study is also relevant for market regulatory authorities as it sheds light on protecting market competition and preventing monopolization by limiting excessive expansion of business groups.

One limitation of our study is that we assume a linear relationship between market demand and the sales price of the final product. Although this assumption simplified the model, it limits the generalizability of our results. In our future study, uncertainty of market demand would be introduced in the framework to capture more real-world characteristics. In addition, although the internal ownership structure of integration firms is described in our framework. We omit the cost of equity acquisition. Considering the different costs in implementing vertical and horizontal integration strategy may provide us with more interesting and meaningful conclusions. Further, the symmetric and complete information between acquiring and target firms is assumed in our study. However, in practice, the game between acquiring and target firms typically plays an important role in the integration strategy. In our follow up studies, consequently, we may extend our framework to capture the dynamic interactions between acquiring and target firms in integration strategy. Finally, the evidence from Chinese listed firms is provided to examine the primary conclusions derived from our model. However, due to the limited data availability, this examination may not support our framework and equilibrium analysis directly. Although empirical evidence provided in Sec. 5 supports the important results that are derived from our framework and equilibrium analysis, and can be seemed as indirect validation for our framework, a future study is still warranted to provide more direct empirical evidence.

Acknowledgments

We would like to thank the editors and referees for their detailed evaluation and constructive suggestions, which significantly improved the manuscript.

Disclosure statement

The authors declare no conflict of interest.

Additional information

Funding

Notes

References

- Allen, J. W., & Phillips, G. M. (2000). Corporate equity ownership, strategic alliances, and product market relationships. The Journal of Finance, 55(6), 2791–2815. https://doi.org/10.1111/0022-1082.00307

- Atalay, E., Hortacsu, A., & Syverson, C. (2014). Vertical integration and input flows. American Economic Review, 104(4), 1120–1148. https://doi.org/10.1257/aer.104.4.1120

- Bensimhoun, M. (2016). Historical account and ultra-simple proofs of Descartes's rule of signs, De Gua, Fourier, and Budan's rule. Mathematics, 1, 1–35.

- Bhaskaran, S. R., & Ramachandran, K. (2011). Managing technology selection and development risk in competitive environments. Production and Operations Management, 20(4), 541–555. https://doi.org/10.1111/j.1937-5956.2010.01165.x

- Bonanno, G., & Vickers, J. (1988). Vertical separation. The Journal of Industrial Economics, 36(3), 257–265. https://doi.org/10.2307/2098466

- Boom, A., & Buehler, S. (2020). Vertical structure and the risk of rent extraction in the electricity industry. Journal of Economics & Management Strategy, 29(1), 210–237. https://doi.org/10.1111/jems.12327

- Brandt, L., Van Biesebroeck, J., Wang, L. H., & Zhang, Y. F. (2017). WTO accession and performance of Chinese manufacturing firms. American Economic Review, 107(9), 2784–2820. https://doi.org/10.1257/aer.20121266

- Calkins, S. (1983). The new merger guidelines and the Herfindahl-Hirschman Index. California Law Review, 71(2), 402–429. https://doi.org/10.2307/3480160

- Callahan, W. T., Millar, J. A., & Schulman, C. (2003). An analysis of the effect of management participation in director selection on the long-term performance of the firm. Journal of Corporate Finance, 9(2), 169–181. https://doi.org/10.1016/S0929-1199(02)00004-4

- Chipty, T. (2001). Vertical integration, market foreclosure, and consumer welfare in the cable television industry. American Economic Review, 91(3), 428–453. https://doi.org/10.1257/aer.91.3.428

- Claessens, S., Djankov, S., Fan, J. P. H., & Lang, L. H. P. (2002). Disentangling the incentive and entrenchment effects of large shareholdings. The Journal of Finance, 57(6), 2741–2771. https://doi.org/10.1111/1540-6261.00511

- Colangelo, G. (1995). Vertical vs horizontal integration - preemptive merging. The Journal of Industrial Economics, 43(3), 323–337. https://doi.org/10.2307/2950583

- Crawford, G. S., Lee, R. S., Whinston, M. D., & Yurukoglu, A. (2018). The welfare effects of vertical integration in multichannel television markets. Econometrica, 86(3), 891–954. https://doi.org/10.3982/ECTA14031

- Cumming, D., Meoli, M., & Vismara, S. (2019). Investors' choices between cash and voting rights: Evidence from dual-class equity crowdfunding. Research Policy, 48(8), 103740. https://doi.org/10.1016/j.respol.2019.01.014

- David, G., Rawley, E., & Polsky, D. (2013). Integration and task allocation: Evidence from patient care. Journal of Economics & Management Strategy, 22(3), 617–639. https://doi.org/10.1111/jems.12023

- Derouiche, I., Hassan, M., & Amdouni, S. (2018). Ownership structure and investment-cash flow sensitivity. Journal of Management & Governance, 22(1), 31–54. https://doi.org/10.1007/s10997-017-9380-x

- Douven, R., Halbersma, R., Katona, K., & Shestalova, V. (2014). Multiperiod production and ordering policies for a retailer-led supply chain through option contract. Journal of Economics & Management Strategy, 23(2), 344–368. https://doi.org/10.1111/jems.12056

- Droge, C., Vickery, S. K., & Jacobs, M. A. (2012). Does supply chain integration mediate the relationships between product/process strategy and service performance? An empirical study. International Journal of Production Economics, 137(2), 250–262. https://doi.org/10.1016/j.ijpe.2012.02.005

- El-Khatib, R., Fogel, K., & Jandik, T. (2015). CEO network centrality and merger performance. Journal of Financial Economics, 116(2), 349–382. https://doi.org/10.1016/j.jfineco.2015.01.001

- Esqueda, O. A., Ngo, T., & Susnjara, J. (2019). The effect of government contracts on corporate valuation. Journal of Banking & Finance, 106, 305–322. https://doi.org/10.1016/j.jbankfin.2019.07.003

- Fama, E. F., & Jensen, M. C. (1983). Separation of ownership and control. The Journal of Law and Economics, 26(2), 301–325. https://doi.org/10.1086/467037

- Fan, G., Ma, G., & Wang, X. (2019). Institution reform and economic growth of China: 40-years progress toward marketization. Acta Oeconomica, 69(s1), 7–20. https://doi.org/10.1556/032.2019.69.s1.2

- Fan, G., Wang, X., & Zhu, H. (2011). NERI index of marketization of china’s provinces. Economic Science Press.

- Fiocco, R. (2016). The strategic value of partial vertical integration. European Economic Review, 89, 284–302. https://doi.org/10.1016/j.euroecorev.2016.07.006

- Flannery, M. J., & Rangan, K. P. (2006). Partial adjustment toward target capital structures. Journal of Financial Economics, 79(3), 469–506. https://doi.org/10.1016/j.jfineco.2005.03.004

- Forbes, S. J., & Lederman, M. (2010). Does vertical integration affect firm performance? Evidence from the airline industry. The RAND Journal of Economics, 41(4), 765–790. https://doi.org/10.1111/j.1756-2171.2010.00120.x