?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Recently, sustainability practices have become a global requirement to attain the high-performance goals of the organizations and capture the focus of regulators and recent researchers. Therefore, the present article aim is to investigate the board diversity (percentage of women directors, percentage of non-executive directors and board member nationality) and firm size (logarithm of total assets) on the sustainability practices (expenditures on environmental sustainability) of the top ten registered firms in China. The researchers have adopted the secondary source of data collection and extracted the data from the financial statements of the adopted firms from 2005 to 2019. Additionally, the researchers used a fixed-effect model (FEM) and a robust standard error model to investigate the relationship between the two concepts. There were positive correlations between firm size (logarithmic total assets) and board diversity (percentage of women directors, percentage of non-executive directors, and board member nationality) and China's top ten registered firms' sustainability practises (expenditures on environmental sustainability). This research provides help to the policymakers while formulating strategies and policies related to the adoption of sustainability practices.

1. Introduction

The board of directors of a corporation is responsible for ‘supervising management's activities and decisions’. They are a corporation's most powerful decision-making entity Qureshi et al. (Citation2020). Their responsibilities range from making critical financial and strategic choices, such as authorizing capital structure changes/mergers and acquisitions, to the tough duty of selecting the company's top executive leadership Méndez et al. (Citation2021). As better governance is the ultimate aim of any organization with a view to achieving the term of sustainability. The decision by the management of the firm floats its impact to every aspect of the firm as decision-making is a crucial step. The decision of any organization management decides the future of that firm. The highest authority or body of any firm is the firm Board Aksoy et al. (Citation2020) and Martínez‐Ferrero et al. (Citation2021). The performance of any organization's board is vital for the better performance of the organization. These directors saw themselves as representing the company as a whole, and their actions as representing corporate governance. A board's gender diversity, size, and other criteria all have a role in corporate governance. Board diversity and board size will be examined as part of this study's emphasis on sustainability. Any organization's ultimate goal is to be long-term in its performance, since this is a sign that the company is heading in the correct way Gil-Cordero et al. (Citation2021). The word ‘Corporate Governance’ is highly regarded in the literature of business. Several studies have already emphasised its significance (Dixon et al., 2017; Eton et al., Citation2021; Udeh et al., Citation2017).

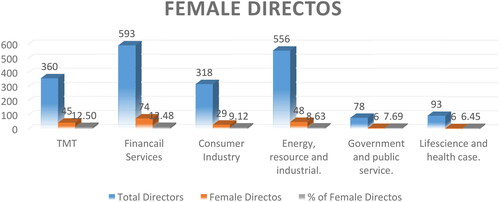

Technological and innovation developments have created several chances for registered firms in China to preserve their environmental policies. Board diversity and company size are key factors that influence viable methods to maintain expenditures as well as the environment of sustainable practices Ezzat and Fayed (Citation2020). Board diversity of public firms is a growing concern among regulators, corporations, and research institutes as an essential component of corporate governance, involving professional Lee and Brahmasrene (Citation2020) experience, education, gender, and age, among other factors (Bektur & Arzova, Citation2020; Rehman et al., Citation2020). Gender diversity, among these characteristics, mostly refers to an increase in the ratio of women on corporate boards. As corporate governance plays a vital role in firm sustainability. The diversity of Chines industry boards is given in .

Figure 1. Number of female directors in China.

Source: ourselves.

In addition, Ismail and Latiff (Citation2019), investigated the relationship between board diversity and corporate sustainability practices in Malaysian-listed firms. The data collected from 38 listed companies by covering the tenure of 2010 to 2016 and proposed that board diversity is positively associated with corporate sustainability practices. Further, proposed that board diversity is the determinant for corporate sustainability practices. Olaleye et al. (Citation2021), investigated the relationship between board diversity and firm performance in China. The data was collected from 806 non-financial Chinese employees by covering the period from 2009 to 2017. Data were analyzed by applying Tobit regression two-step system GMM. The results of the studies proposed that board diversity enhances firm performance in China. The findings also suggested that a diverse board might improve the knowledge, abilities, and competence of its members, which is linked to the company's improved success (Arato & Kano, Citation2021). From an Asian viewpoint, Alabdullah et al. (Citation2019) did a research on board size, CSR, and corporate governance in relation to Asian companies. Partial Least Square-PLS was used to analyse data from 91 publicly traded corporations. Board size and corporate social responsibility disclosure were shown to have a favourable correlation in a study on corporate governance. In Colombia, researchers Orozco et al. (Citation2018) examined the link between board size and firm performance. A total of 84 businesses from the years 2008 to 2012 were used to compile the information. According to the findings, board size has a bearing on a company's success (Callagher & Cullis, Citation2021).

There are various gaps in the literature that will be addressed in this research, like as Malaysian researchers evaluated the association between board diversity and sustainable practises, whereas this study will extend the model to Chinese-registered businesses with adjustments (i.e., adding company size element). A study conducted by MacMillan et al. (Citation2004) explored the link between corporate governance and the board of directors and called for an assessment of corporate governance factors like directors in terms of their backgrounds, etc. The significance of the present study is 1) will highlight the importance of corporate governance concept for registered firms as better corporate governance leads to encourage the positive behavior of board, improvise the top-level decision making, reduction in company cost of capital, internal control assurance, enablement of strategic planning etc., 2) will also help the Chinese registered firms professionals to have better understanding and decision making regarding future of the firm (Aliedan, Citation2022; Elrayah, Citation2022; Harimbawa et al., Citation2022; Que et al., Citation2022; Salas-Rueda & Alvarado-Zamorano, Citation2022).

The structure of the present study is composed of several phases, the first phase is about the introduction, and after an introduction, the second phase of the study deals with evidence regarding board diversity, the board size, and sustainability practices in light of past studies. The third phase of the study throws light on the methodology applied to collect the data about the board diversity, board size, and sustainability practices and analyze its validity. The fourth phase compares the study results with the findings of other authors about the same subject and thus, approves these results. The paper ends with proper study implications, conclusions, and future recommendations (Fahrurrozi, Citation2022; Hereth, Citation2022; Hlongwane & Daw, Citation2022; Makhitha, Citation2022).

2. Literature review

Technological and innovation advancements have opened various opportunities to sustain the environmental practices of registered organizations in China. Board diversity and firm size are important measures that induce feasible measures to sustain the expenditures as well as the environment of sustainable practices. Yang et al. (Citation2019), investigated the relationship between corporate social responsibility and the characteristics of female directors. It is upon the qualification and educational criteria specified for the board of directors which are being placed for the applicability of sustainable practices and controlling expenses. Various factors have been taken to analyze the relationship and influence among these factors by applying various statistical approaches Paltanavičiūtė (Citation2022). Results indicate a statistically significant influence of the percentage of women directors who are positive toward the control of expenditures on the environment and sustainable practices. Alazzani et al. (Citation2019) and Hernández-Lara and Gonzales-Bustos (Citation2020) analyzed the debate about family businesses and innovation which is processed by the role of female directors. Non-family, family and innovative firms are mainly focused to ascertain the positive or negative role of women directors. Numerous statistical and theoretical methodologies have been utilised to examine different aspects of the representation of women on corporate boards and the diversity of the board as a whole. According to the findings, having a higher percentage of female directors in charge of environmental sustainability spending is beneficial. According to several environmental sustainability parameters, Ellwood and Garcia-Lacalle (Citation2018) looked at the function of women directors in companies. Quality of service and return are generally dependent on the female director's personality. The proportion of female directors and the amount of money spent on environmental sustainability are taken into account. Various ratios and statistical methodologies are used to examine how these variables are connected. The findings indicate a strong and favourable link between these factors and a variety of social outcomes (Saeidi et al., Citation2021).

Female directors’ certainty in the current practicing environment has positively contributed significant role to enable efficacious controls in registered firms of China. Oradi and E-Vahdati (Citation2021), assessed the relationship between women directors and their role to control the weaknesses prevailing in internal controls. While examining the role of women directors, the environmental sustainable expenditures are analyzed with the elements of internal control. By applying various sensitivity tests, the relationship between them is significant. Results show the prominent impact of women directors not only in sustaining the expenditures on the environment but also on internal controls. Broietti et al. (Citation2018), aimed to assess the influence upon the spending on environmental sustainability among the municipalities of Brazil. A variety of determinants exist in the environmental expenditures which usually assert the measures influential upon them. Using the panel data model and different variables pertaining to the diversity of the board and female directors, the results endorsed significant relations. Results indicate a rise in the percentage of women directors who are positively contributing toward the expenditures on environmental sustainability. Baker et al. (Citation2018) and Qureshi et al. (Citation2020) examined the evolution of board diversity factors and its evolution toward the controls of environmental management. The extent of female directors is an eminent measure that could be considered as an evolution toward the spending on environmental management. By using fond of variables and measures, different statistical and theoretical approaches have been used. Studies indicate significant and positive efforts that help to control the expenditures on environmental sustainability (Genc, Citation2021).

Managing the organization is a complex requirement and executive, as well as non-executive directors, are important and in dire need of the current organizations of China. Cullinan et al. (Citation2019), assessed the relationship between corporate social responsibility, environmental sustainability, board characteristics, and non-executive directors. Various factors are taken into consideration to assert the role as well as the relationship. Using various strategic and theoretical approaches, the independent factors are viewed upon the expenditures on environmentally sustainable practices. Results depicted a clear view about the dominance of non-executive directors which play efficiently without any influence to control the expenditures on environmental sustainability (Paraschiv et al., Citation2021). Papenfuß et al. (Citation2018), examined the functioning of non-executive directors and their role in the placement of corporate governance in organizations(Yousaf et al., Citation2021). Controls and sustainability practises factor heavily into the evaluation of these corporate governance procedures. In several cases, econometric methodologies have verified board diversity and non-executive director responsibilities. Non-executive directors have a considerable and concentrated influence in the expenditures for sustainable environmental practises, according to the report. There is a need for non-executive directors to play an important role in ensuring the long-term viability of environmental sustainability Ascherl et al. (Citation2019) The non-executive directors' sustainability practises are mostly evaluated as the performance measurement. Financial and statistical tools are used to examine the board's diversity concurrently. The findings of the research show that board diversity has a substantial impact on environmental sustainability spending restrictions.

Non-executive directors have attained much importance in the current Chinese markets due to their accomplishment of tasks without any influence. Huang and Boateng (Citation2017), examined the impact of leadership and executive stakeholders and their compensation which could be enlightened to forecast the expenditures on sustainable practices. The wide association is also certainly due to the facilitation of management for holding structural powers to maintain the environment. Some statistical and econometric approaches have been used upon the asymmetry of information regarding non-executive leadership. Findings indicated a significant and prominent impact of non-executive directors on the expenditures of environmentally sustainable practices. Saleem et al. (Citation2021), identified various factors that influence the expenditures of healthcare institutions' environmental sustainability. These factors are best related to the improvements of budgeting that is compelled to be a concern with the expenditures on environmental sustainability and management (Bhatti et al., Citation2022; Huo et al., Citation2022; Macheridis, Citation2022; Peternel & Grešš, Citation2021). Using numerous dimensions of directors and their specifications, ARDL bound test and Bayer-Hanck co-integration tests are applied. The study shows a positive contribution of income, services, and infrastructure over the degradation in expenses that are linked with environmental sustainability. Khan et al. (Citation2020), analyzed the bifurcation of budgets that are usually used in the sustainability of environments in the organizations. Renewable energy consumption, income, health expenditure, and foreign direct investment are the elected factors that are positive contributions toward environmental pollution. Generalized methods of the moment are used in this study with the assistance of least square methods to explore the relationship among the factors. The study shows the positive impacts of non-executive directors and diversified boards on environmental sustainability expenditures (Al-masaeed et al., Citation2021; Diep & Hieu, Citation2021; Handoyo et al., Citation2021; Jeffrey, Citation2021; Mattayaphutron et al., Citation2021; Saifan et al., Citation2021; Zhu et al., Citation2021).

Current organizations are facing different constraints to maintain the expenditures over environmental sustainability. Sustainability practices have become a global requirement to attain the high-performance goals of the organizations and capture the focus of regulators and recent researchers. Because of this, registered organisations in China may face additional difficulties due to cultural and national differences. (Ford & Ihrke, Citation2016) analysed the environmental sustainability practises of urban and non-urban boards. The nationality element supports the public performance as a contributing component. The performance of environmental sustainability has seen a significant increase using different data and theoretical frameworks. Expenditures on environmental sustainability measures are affected by the nationality of board members, according to research. A range of essential board member and board structure features were investigated by Fahrner and Harris (Citation2021) to determine their importance for environmental sustainability. Nationality holders' actions and judgments are reflected in the cultures of the companies in which they work. The probit model is used to demonstrate the link between board characteristics, board structures, and board membership. Results show that board member nationality has a significant influence on environmental sustainability expenditures. Hershatter and Epstein (Citation2010) investigated the link between board member retention and recruiting that is effective for environmental sustainability. While asserting the impact of board member nationality, non-profit board of directors and volunteering board directors are taken. Statistical approaches of analyzing the relationship and impacts provided certain results. Board member nationality maintains the governance at organizational levels through local and international reasoning to manage the expenditures on environmental sustainability.

The Independent functioning of board directors has considerably raised the elimination of problems related to the expenditures of sustainable practices in China. These practices are mostly occur due to conflict of culture and nationality and somehow overcome due to these factors. Cui et al. (Citation2020), analyzed the reasoning of the board director’s nationality that serves in the organization for the development and uplifting independently (Al-Shammari, Citation2021; Jermsittiparsert, Citation2021; Josaiman et al., Citation2021; Mamghaderi et al., Citation2021). The nationality of the director is the most important mode where the groups of the board of directors are unable to conflict. To ascertain the reasoning among board members' nationality, strategic and theoretical approaches have been applied. The study reveals a positive indication of board members' nationality acts independently to control the expenditures on environmental sustainability. Ganda (Citation2021), investigated the impacts of health expenditures on the sustainability of energy emissions in organizations. There is an involvement of board members in the organizations which play a significant role in the control and rise in expenditures that pertain to environmental sustainability. Grander causality, vector error correction, and least square tests are performed to examine the relationship among these factors. Results state the positive influence of board members' nationality over the organizations due to hierarchical and diversified implementations on the sustainable environment. Tamayo-Torres et al. (Citation2019), examined the relationship between supply chain management and the value of organizations in different environments of the market. The nationality of board members is an eminent one that asserts the influence of governance practices in the organizations. By applying various ratios and statistical approaches, the results indicated a positive relationship between the selected variables. Governance by the board member nationality is directly linked that significantly poses its impact on the expenditures of environmental sustainability (Jin, Citation2021; Khoma & Vdovychyn, Citation2021; Lipińska, Citation2021).

The changing world has placed many innovative measures for the firms to manage and control uncertain elements related to environmental sustainability. These elements comprise various structures that relate to firm size and board size in China. Both these elements are simultaneously functioning in the organizations to induce prominent controls for expenditures that occurred on the environmental sustainability practices. Li et al. (Citation2020), examined the effects of firm size on the commercialization of knowledge and product which is embedded in environmental sustainability. Firm size contributes through various modes in the sustainable practices to maintain the expenditures. Using the DAE model, firm size is significantly correlated with environmental sustainability. Findings also show the efficacy and significance of firm efficiency due to its firm size for managing the expenditures on environmental sustainability. Coetzee et al. (Citation2019), analyzed the commercial and professional logic of firm size practices in the internal and changing environment of an organization. Various events are focused on the firm size in order to induce managing controls. For this purpose, a qualitative approach has been conducted for asserting various threats to environmental sustainability. Findings reveal positive impacts of firm size on the expenditures on environmentally sustainable practices. Ocampo (Citation2018), explored the analytical process of a firm size that applies various decisions into the integration of sustainability. It is conducted through various statistical means comprising numerous linguistic variables that prevail in the firm size. Results indicated the feasible firm size is efficacious toward the maintainability of a sustainable environment. It is further helpful for the effective firm size to induce controls that are flexible to control the expenditures over the environmental sustainability.

Most of the organizations are dependent on their hierarchy that leads to a rise in their costs of sustainable practices in China. If the size of the company and the size of the board of directors best result in the reduction of expenditures on sustainable practises, these practises might be much better. According to Türegün (Citation2018), there is a connection between board member qualities, business size, and borrowing costs that affect financial management. Ordinary least squares techniques are used to determine the independence of company size on environmental sustainability, which affirms the significant impact of firm size. Furthermore, the size and cost of the board are also influenced by the firm's size since the most effective cost-cutting measures may be readily occupied by larger enterprises. Businesses were studied by Coles et al. (Citation2017), in order to determine the relative importance of cost aspects and environmental resources. Generally speaking, the environmental and economic success of businesses is characterised by an optimistic outlook. However, the vector analysis business model identifies several important aspects influencing the long-term viability of environmental spending. The findings show that the size of a company has a significant impact on environmental sustainability expenses. In their recent study, Halkos and Paizanos (Citation2017) looked at the link between government expenditure and environmental quality. The importance of business size on environmental sustainability expenditures is shown via a variety of ways. Different econometric methodologies have been used to prove the marginal impacts of different company size parameters. Expenditures on environmental sustainability were positively influenced by the size of the company and its related elements.

3. Research methods

The article investigates the board diversity and firm size on the sustainability practices of the top ten registered firms in China. The researchers have adopted the secondary source of data collection and extracted the data from the financial statements of the adopted firms from 2005 to 2019. The researchers also executed the robust standard error along with a fixed-effect model to examine the nexus between the constructs. The equation for this article is given below:

(1)

(1)

Where;

EES = Expenditures on Environmental Sustainabilityi = Firmst = Time Period

PWD = Percentage of Women Directors

PNED = Percentage of Non-executive Directors

BMN = Board Member Nationality

FS = Firm Size

The researchers have taken the sustainability practices as the dependent variable and measured as the percentage of expenditures on environmental sustainability to total expenditures. In addition, the researchers also used two predictors, such as board diversity measured as the percentage of women directors to total directors, percentage of non-executive directors to total directors and board member nationality, while the firm size is measured as the logarithm of total assets. shows the variables and measurements.

Table 1. Measurements of variables.

The researchers have investigated the descriptive statistics that show the observation, mean and standard deviation. In addition, it also shows the minimum and maximum values of all the constructs. Moreover, the researchers also executed the correlation matrix that shows the relationships among the variables. It only shows the direction but ignores the significance of the nexus among variables. In addition, the researchers also run the variance inflation factor (VIF) to check the multicollinearity. If results show less than five values, then no issue of multicollinearity in the model. The equations for VIF are mentioned below:

(2)

(2)

(3)

(3)

(4)

(4)

The researchers also used the Hausman test to find a suitable model for checking relationships among random and fixed models. If the probability value is less than 0.05, then the fixed model is appropriate and vice versa. Thus, the researchers have executed the FEM model, and the equation for this model is given below:

(5)

(5)

‘The individual company’ was represented by subscript I in this equation, and the various companies were ‘based on their characteristics’. Due to a lower than 0.5% Hausman probability, the FEM is required. The model's equation is shown below, along with the current research variables.

(6)

(6)

Finally, the researchers have run the robust standard error to explore the links among the variables. The robust standard error is an effective statistical tool that adjusts the ‘model's heterogeneity issues’ that generally exist. The equation for robust standard error equation is mentioned as under with present study variables:

(7)

(7)

4. Research findings

The researchers have investigated the descriptive statistics that show the observation, mean and standard deviation. In addition, it also shows the minimum and maximum values of all the constructs. The figures highlighted that a total of 150 (15 years x 10 firms) observations are used by the researchers while the average value of EES is 0.292, and the mean value of PWD is 0.180. Moreover, the average value of PNED is 0.737, while the mean value of BMN is 0.178, and the average value of FS is 13.837. shows the descriptive statistics of the constructs.

Table 2. Descriptive statistics.

Researchers also created a correlation matrix to demonstrate how the factors are related. The nexus between variables is solely shown as a directional indicator. EES is positively associated with PWD, PNED, BMN and FS as seen in the figures. Shown in , the correlation matrix.

Table 3. Correlation matrix.

In addition, the researchers also run the VIF to check the multicollinearity. If results show less than five values, then no issue of multicollinearity in the model. The results indicated that the values of VIF are lower than five that shows no multicollinearity exists. shows the VIF results.

Table 4. Variance inflation factor.

The researchers also used the Hausman test to find a suitable model for checking relationships among random and fixed models. If the probability value is less than 0.05, then the fixed model is appropriate and vice versa. The results revealed that probability values, if lower than 0.05 that shows FEM is appropriate. shows the Hausman test results.

Table 5. Hausman test.

Firstly, FEM is used to investigate the links between the constructs. The results indicated that board diversity (percentage of women directors, percentage of non-executive directors and board member nationality) and firm size (logarithm of total assets) have a positive impact on the sustainability practices (expenditures on environmental sustainability) of the top ten registered firms in China. In addition, R square (0.526) indicated that 52.6 per cent of variations in EES are due to all the predictors used by the researchers. shows the FEM results.

Table 6. Fixed effect model.

Finally, the robust standard error is employed to analyse the relationships between the constructs. More women directors, non-executive directors and board member nationality were shown to have a beneficial influence on environmental sustainability practises (expenditures on environmental sustainability) in China's top 10 registered companies, according to the findings of the study. presents the findings with the most accurate standard error.

Table 7. Robust standard error.

5. Discussion and implications

The study results have indicated that the percentage of women directors on board has a positive association with the expenditures environmental sustainability which determine the number of sustainable practices undertaken within the organization. These results are in line with the previous study of Lu and Herremans (Citation2019), which analyzes the impact of board diversity on sustainable development within the organization. This study analyzes that if the board comprises more women directors than the male ones, it can deal with the issues or risks more effectively. Women have the soft corner in their hearts, and they can understand the emotions and needs of the customers, employees, general public, and other stakeholders. So, they prefer to spend some extra money if needed to mitigate the negative environmental impacts of business activities to save the health of stakeholders and promote their welfare. These results are also supported by the past study of Cordeiro et al. (Citation2020), which states that having more female directors helps in an effective financial management, governance, and diligence for better decision making to tackle the risks involved. The board comprising of women directors prefer to make the investment in sustainable practices like waste management, effectively carrying on sanitation system, and applying ecological friendly material or technology. Thus, the organizations having women directors show high sustainable performance.

According to the findings of the research, the proportion of non-executive directors is positively associated with the amount of money spent on environmental sustainability, which in turn influences whether or not the company adopts sustainable practises. Non-executive directors, according to Homroy and Slechten (Citation2019), are not responsible for participating in the regular functions of business; rather, they represent the interests of stakeholders, such as shareholders, customers, the general public, or government authorities, and work to protect their rights. When it comes to legislation or corporate planning, executive directors take environmental considerations into account. Non-executive directors, on the other hand, enable the company to spend money on initiatives aimed at reducing the negative environmental repercussions of business activities. (García Martín & Herrero, Citation2020) previously found that non-executive directors have no vested interest in the company's success and conduct business in a non-disruptive manner that does not interfere with stakeholders' rights. In order to offer a safe working environment for their workers and increase the quality of the company's natural resources, these directors develop environmental policies and initiatives. Consequently, non-executive directors encourage the company's management to enhance its environmental performance.(Méndez et al., Citation2021).

The study results have also shown that board member nationality has a positive association with the expenditures on environmental sustainability, which represents the sustainable practices of the firm. These results are supported by the previous study of Zaid et al. (Citation2020), which states that the fact that the directors have the nationality of the country or, in other words, they belong to the same country, affects the environmental performance of the firm. The directors having the nationality of the country, have an emotional attachment with the country and do their best for the welfare of the country people. So, when they make policies or business planning, they focus on the quality of the environment by allowing investment in practices that could prevent the emission of pollutants. These results are also supported by the previous study of Beji et al. (Citation2021), which shows that when the board of directors have the nationality of the country, it becomes possible for them to make arrangement for the funds at the time of need. The ability of the directors to make the investment in ecological friendly programs like the procurement of renewable energy resources, environmentally friendly technology, and techniques to handle the harmful wastes determine the sustainability of the firms’ performance, maintaining a good quality work environment and availability of good quality resources for future use.

It has also been revealed by the study results that firm size has a positive association with the expenditures environmental sustainability which determine the sustainable practices undertaken within the organization. These results are supported by the previous study of Andriana and Anisykurlillah (Citation2019), which states that the total assets of the business firm determine its financial strength to carry the business activities according to the requirements of the customers and regulatory authorities. The business firms which have more assets than their liabilities are able to make the investment in the ecological friendly technology which uses minimum energy resources or material to manufacture products and do not release any harmful wastes or gases, which could adversely affect the environmental quality and natural resources. Thus, the large firm size enhances the sustainable performance of the firm. These results agree with the study of Deswanto and Siregar (Citation2018), which shows that firms having a large number of assets like cash or bank balance easily implement the policies or strategies designed for sustainable business progress. The firm assets are used to apply information and communication technology which assists the firm to have information about the ecological friendly resources and techniques. In this way, they are able to high sustainable performance.

Both theoretical and empirical implications have been made by the current study. This study has a tremendous theoretical significance because of its remarkable contribution to the literature on business sustainability. This study analyzes the influences of board diversity indicators such as percentage of women directors, percentage of non-executive directors, board member nationality, and firm size on expenditures on environmental sustainability, which help determine sustainability practices executed within the firm. In the existing literature, the researchers have only discussed the board of directors as a factor without the diversity of the percentage of women directors, percentage of non-executive directors, and board member nationality while analyzing expenditures on environmental sustainability or sustainable practices. More research are needed to examine how different board composition, non-executive director gender ratios, nationality of board members, and business size affect environmental sustainability and sustainable practises spending. As a result of our research, we're able to better understand the importance of board diversity metrics including gender parity, non-executive director representation, country of origin, and size in relation to the environment. The present research offers a great deal of practical value. Policymakers may use the findings of this study to assist them develop strategies and policies to encourage the adoption of sustainable practises. For economists in developing countries like China, this paper is essential reading since it lays forth a theoretical framework for ensuring that sustainable practises are implemented and are successful. In light of the high number of women directors, the high percentages of non-executive directors, board member nationality, and company size, the research recommends that corporate management make expenditures on environmental sustainability.

6. Conclusion and limitations

The current study aimed to ensure how the diverse formation of the board, such as women directors, non-executive directors, and board member nationality, and firm size play an influential role in the implementation of sustainability practices allowing the expenditures on environmental sustainability. The study analyzed the management and performance of registered firms in China to check whether the effective diversity in the formation of the board like percentage of women directors, percentage of non-executive directors, board member nationality could be useful in leading the organization towards sustainable performance and firm size on expenditures on environmental sustainability. The study implied that diverse boards and directors play a diverse role in decision making and problem handling. The results indicated that when the board of directors is comprised of female members, it can more effectively carry business functions so that sustainable performance can be attained because women show more care for the health and well-being of the stakeholders and allow expenditures on environmental sustainability. As the non-executive directors have no personal interest, they form the policies indifferently to protect the environmental quality and well-being of the general people and the board members who have countries national have particular concern towards its environment and people’s welfare and have the ability to do something in this regard; thus, they allow sustainable practices within the organization. The study results showed that as firm size determine the financial strength, the businesses with large firm size can make the investment on ecological friendly programs which enhances sustainability in the environmental performance of the firm.

Though the study has greatly contributed to the economy based literature, the upcoming authors are still recommended to make further improvements. This study examines the influences of only two factors board diversity with women directors, non-executive directors, and board member nationality, and firm size play on the implementation of sustainability practices allowing the expenditures on environmental sustainability. Many other significant factors like economic conditions, green finance, and energy efficiency could also determine sustainable practices. The current study pays no special attention to these significant factors. As a result, the scope of the study is limited. Researchers and practitioners are recommended to focus on these factors as well along with board diversity and firms to address the sustainable practices. The empirical data to present the study concepts have been collected from the economy of China. China is a developing country with a large population, specific geographical and economic conditions. Thus, this may not be considered equally for other economies. So, the scholars must address influences of board diversity in the form of women directors, non-executive directors, and board member nationality, and firm size on the implementation of sustainability practices and the expenditures on environmental sustainability in a significant number of countries as well.

Disclosure statement

No potential conflict of interest was reported by the authors.

References

- Aksoy, M., Yilmaz, M. K., Tatoglu, E., & Basar, M. (2020). Antecedents of corporate sustainability performance in Turkey: The effects of ownership structure and board attributes on non-financial companies. Journal of Cleaner Production, 276(1), 124284–124132. https://doi.org/10.1016/j.jclepro.2020.124284

- Alabdullah, T. T. Y., Ahmed, E. R., & Muneerali, M. (2019). Effect of board size and duality on corporate social responsibility: What has improved in corporate governance in Asia? Journal of Accounting Science, 3(2), 121–135. https://doi.org/10.21070/jas.v3i2.2810

- Alazzani, A., Wan-Hussin, W. N., & Jones, M. (2019). Muslim CEO, women on boards and corporate responsibility reporting: Some evidence from Malaysia. Journal of Islamic Accounting and Business Research, 10(2), 274–296. https://doi.org/10.1108/JIABR-01-2017-0002

- Aliedan, M. (2022). The Geopolitics of International Trade in Saudi Arabia: Saudi Vision 2030. Cuadernos de Economía, 45(127), 11–19.

- Al-masaeed, S., Alsoud, A. R., Ab Yajid, M. S., Tham, J., Abdeljaber, O., & Khatibi, A. (2021). How the relationship between Information Technology, Entrepreneurship, and International Trade lead to the International Relations? Croatian International Relations Review, 27(87), 32–62.

- Al-Shammari, M. M. (2021). A strategic framework for designing knowledge-based customer-centric organizations. International Journal of eBusiness and eGovernment Studies, 13(2), 1–16.

- Andriana, A. E., & Anisykurlillah, I. (2019). The effects of environmental performance, profit margin, firm size, and environmental disclosure on economic performance. Accounting Analysis Journal, 8(2), 143–150. https://doi.org/10.15294/aaj.v8i2.28659

- Arato, S., & Kano, S. (2021). Platform technology management of biotechnology companies in Japan. Journal of Commercial Biotechnology, 26(3), 45–51. https://doi.org/10.5912/jcb1016

- Ascherl, C., Schrand, L., Schaefers, W., & Dermisi, S. (2019). The determinants of executive compensation in US REITs: Performance vs. corporate governance factors. Journal of Property Research, 36(4), 313–342. https://doi.org/10.1080/09599916.2019.1653955

- Baker, C. R., Cohanier, B., & Gibassier, D. (2018). Environmental management controls at Michelin – How do they link to sustainability? Social and Environmental Accountability Journal, 38(1), 75–96. https://doi.org/10.1080/0969160X.2018.1438300

- Beji, R., Yousfi, O., Loukil, N., & Omri, A. (2021). Board diversity and corporate social responsibility: Empirical evidence from France. Journal of Business Ethics, 173(1), 133–155. https://doi.org/10.1007/s10551-020-04522-4

- Bektur, Ç., & Arzova, S. B. (2020). The effect of women managers in the board of directors of companies on the integrated reporting: Example of Istanbul Stock Exchange (ISE) Sustainability Index. Journal of Sustainable Finance & Investment, 11(1), 1–17. https://doi.org/10.1080/20430795.2020.1796417

- Bhatti, D. M. A., Alyahya, D. M., Juhari, D. A. S., & Alshiha, D. A. A. (2022). Green HRM practices and employee satisfaction in the hotelindustry of Saudi Arabia. International Journal of Operations and Quantitative Management, 28(1), 100–120. https://doi.org/10.46970/2022.28.1.6

- Broietti, C., Flach, L., Rover, S., & Salvador de Souza, J. A. (2018). Public expenditure and the environmental management of Brazilian municipalities: A panel data model. International Journal of Sustainable Development & World Ecology, 25(7), 630–641. https://doi.org/10.1080/13504509.2018.1485599

- Callagher, L., & Cullis, C. (2021). Innovations arising from post-COVID-19 in Bioentrepreneurship Education. Journal of Commercial Biotechnology, 26(3), 25–34. https://doi.org/10.5912/jcb1014

- Coetzee, C., Barac, K., & Seligmann, J. (2019). Institutional logics and sustainability of selected small and medium-sized audit firms. South African Journal of Accounting Research, 33(3), 163–186. https://doi.org/10.1080/10291954.2019.1655189

- Coles, T., Warren, N., Borden, D. S., & Dinan, C. (2017). Business models among SMTEs: Identifying attitudes to environmental costs and their implications for sustainable tourism. Journal of Sustainable Tourism, 25(4), 471–488. https://doi.org/10.1080/09669582.2016.1221414

- Cordeiro, J. J., Profumo, G., & Tutore, I. (2020). Board gender diversity and corporate environmental performance: The moderating role of family and dual‐class majority ownership structures. Business Strategy and the Environment, 29(3), 1127–1144. https://doi.org/10.1002/bse.2421

- Cui, X., Peng, X., Jia, J., & Wu, D. (2020). Does board independence affect environmental disclosures by multinational corporations? Moderating effects of national culture. Applied Economics, 52(52), 5687–5705. https://doi.org/10.1080/00036846.2020.1770681

- Cullinan, C. P., Mahoney, L., & Roush, P. B. (2019). Directors & corporate social responsibility: Joint consideration of director gender and the director’s role. Social and Environmental Accountability Journal, 39(2), 100–123. https://doi.org/10.1080/0969160X.2019.1586556

- Deswanto, R. B., & Siregar, S. V. (2018). The associations between environmental disclosures with financial performance, environmental performance, and firm value. Social Responsibility Journal, 14(1), 180–193. https://doi.org/10.1108/SRJ-01-2017-0005

- Diep, L. T. N., & Hieu, V. M. (2021). Examining quality of English language learning of university students in Vietnam: The moderating role of competition factor. Eurasian Journal of Educational Research, 95, 55–79. https://doi.org/10.14689/ejer.2021.95.4

- Dixon, R., Guariglia, A., & Vijayakumaran, R. (2017). Managerial ownership, corporate governance and firms' exporting decisions: Evidence from Chinese listed companies. The European Journal of Finance, 23(7–9), 802–840. https://doi.org/10.1080/1351847X.2015.1025990

- Ellwood, S., & Garcia-Lacalle, J. (2018). New development: Women with altitude—Exploring the influence of female presence and leadership on boards of directors. Public Money & Management, 38(1), 73–78. https://doi.org/10.1080/09540962.2017.1323430

- Elrayah, M. (2022). Improving teaching professionals' satisfaction through the development of self-efficacy, engagement, and stress control: A cross-sectional study. Educational Sciences: Theory & Practice, 22(1), 1–12.

- Eton, M., Mwosi, F., Sunday, A., & Poro, S. G. (2021). Corporate governance and firms financial performance amongst private business enterprises in Uganda, a perspective from Lira City. African Journal of Business Management, 15(9), 219–231.

- Ezzat, A. M., & Fayed, M. E. (2020). Central bank independence and democracy: Does transparency matter? Contemporary Economics, 14(2), 90–112. https://doi.org/10.5709/ce.1897-9254.334

- Fahrner, M., & Harris, S. (2021). Trust within sport NGB boards: Association with board structure and board member characteristics. European Sport Management Quarterly, 21(4), 524–543. https://doi.org/10.1080/16184742.2020.1757735

- Fahrurrozi, M. (2022). Evaluation of educational service quality of vocational high school (VHS) based on importance performance analysis (IPA) quadrant. Eurasian Journal of Educational Research, 97(97), 27–42.

- Ford, M. R., & Ihrke, D. M. (2016). Board conflict and public performance on urban and non-urban boards: Evidence from a national sample of school board members. Journal of Urban Affairs, 25(3), 1038–1052.

- Ganda, F. (2021). The impact of health expenditure on environmental quality: The case of BRICS. Development Studies Research, 8(1), 199–217. https://doi.org/10.1080/21665095.2021.1955720

- García Martín, C. J., & Herrero, B. (2020). Do board characteristics affect environmental performance? A study of EU firms. Corporate Social Responsibility and Environmental Management, 27(1), 74–94. https://doi.org/10.1002/csr.1775

- Genc, I. H. (2021). The impact of technology on regional price dispersion in the US. Technological and Economic Development of Economy, 27(6), 1281–1300. https://doi.org/10.3846/tede.2021.15238

- Gil-Cordero, E., Rondan-Cataluna, F. J., & Rey-Moreno, M. (2021). Premium private label strategies: Social networks and traditional perspectives. Journal of Innovation & Knowledge, 6(2), 78–91. https://doi.org/10.1016/j.jik.2020.06.003

- Halkos, G. E., & Paizanos, E. A. (2017). The channels of the effect of government expenditure on the environment: Evidence using dynamic panel data. Journal of Environmental Planning and Management, 60(1), 135–157. https://doi.org/10.1080/09640568.2016.1145107

- Handoyo, E., Mukhibad, H., Tusyanah, T., & Ekaningsih, L. (2021). Lecturers’ performance in pandemic era based on online pedagogical practices in Universitas Negeri Semarang (UNNES), Indonesia: A cluster analysis-based approach. Educational Sciences: Theory & Practice, 21(4), 138–154.

- Harimbawa, G., Sumaryadi, I. N., Djohan, D., Mulyati, D., & Achmad, M. (2022). The collaborative governance with focus on controlling the illegal mining in Indonesia. Croatian International Relations Review, 28(89), 209–224.

- Hereth, B. (2022). Queer advice to Christian philosophers. European Journal for Philosophy of Religion, 14(1), 49–75. https://doi.org/10.24204/ejpr.2022.3291

- Hernández-Lara, A. B., & Gonzales-Bustos, J. P. (2020). The influence of family businesses and women directors on innovation. Applied Economics, 52(1), 36–51. https://doi.org/10.1080/00036846.2019.1638496

- Hershatter, A., & Epstein, M. (2010). Millennials and the world of work: An organization and management perspective. Journal of Business and Psychology, 25(2), 211–223. https://doi.org/10.1007/s10869-010-9160-y

- Hlongwane, N. W., & Daw, O. D. (2022). Monetary policy in South Africa: A VECM approach. International Journal of Economics and Finance Studies, 14(1), 1–28.

- Homroy, S., & Slechten, A. (2019). Do board expertise and networked boards affect environmental performance? Journal of Business Ethics, 158(1), 269–292. https://doi.org/10.1007/s10551-017-3769-y

- Huang, W., & Boateng, A. (2017). Executive shareholding, compensation, and analyst forecast of Chinese firms. Applied Economics, 49(15), 1459–1472. https://doi.org/10.1080/00036846.2016.1218432

- Huo, H., Zhang, D., & Wang, H. (2022). Measurement of tourist experience satisfaction of sports tourism based on psychological capacity analysis. Revista de Psicología del Deporte (Journal of Sport Psychology), 31(1), 98–106.

- Ismail, A. M., & Latiff, I. H. M. (2019). Board diversity and corporate sustainability practices: Evidence on environmental, social and governance (ESG) reporting. International Journal of Financial Research, 10(3), 31–50. https://doi.org/10.5430/ijfr.v10n3p31

- Jeffrey, A. (2021). Varieties of theism and explanations of moral realism. European Journal for Philosophy of Religion, 13(1), 25–50. https://doi.org/10.24204/ejpr.v13i1.2884

- Jermsittiparsert, K. (2021). Linkage between energy consumption, natural environment pollution, and public health dynamics in asean. International Journal of Economics and Finance Studies, 13(2), 1–21.

- Jin, G. (2021). Psychological factors and training methods affecting Chinese college students' confrontational training in football teaching. Revista de Psicología del Deporte (Journal of Sport Psychology), 30(4), 62–68.

- Josaiman, S. K., Faisal, M. N., & Talib, F. (2021). Social sustainability adoption barriers in supply chains: A middle east perspective using interpretive structural modeling. International Journal of Operations and Quantitative Management, 27(1), 61–80. https://doi.org/10.46970/2021.27.1.4

- Khan, A., Hussain, J., Bano, S., & Chenggang, Y. (2020). The repercussions of foreign direct investment, renewable energy and health expenditure on environmental decay? An econometric analysis of B&RI countries. Journal of Environmental Planning and Management, 63(11), 1965–1986. https://doi.org/10.1080/09640568.2019.1692796

- Khoma, N., & Vdovychyn, I. (2021). Universal basic income as a form of social contract: Assessment of the prospects of institutionalisation. Socialspacejournal. eu, 97

- Lee, J. W., & Brahmasrene, T. (2020). Exchange rate movements and structural break on China FDI inflows. Contemporary Economics, 14(2), 112–127. https://doi.org/10.5709/ce.1897-9254.335

- Li, Y., Zhong, Z., Guan, J., Zhou, J., & Li, J. (2020). Firm size affecting efficiency of production and commercialization of knowledge: Embedded in cluster development. Asian Journal of Technology Innovation, 28(1), 94–118. https://doi.org/10.1080/19761597.2020.1713831

- Lipińska, E. J. (2021). Koncepcja ekozarządzania miastami w kontekście zrównoważonego rozwoju i odpowiedzialności społecznej. Socialspacejournal. eu, 21, 117–135.

- Lu, J., & Herremans, I. M. (2019). Board gender diversity and environmental performance: An industries perspective. Business Strategy and the Environment, 28(7), 1449–1464. https://doi.org/10.1002/bse.2326

- Macheridis, N. (2022). Control mechanisms towards project success. The Journal of Modern Project Management, 9(3), 87–101.

- MacMillan, K., Money, K., Downing, S., & Hillenbrand, C. (2004). Giving your organisation SPIRIT: An overview and call to action for directors on issues of corporate governance, corporate reputation and corporate responsibility. Journal of General Management, 30(2), 15–42. https://doi.org/10.1177/030630700403000203

- Makhitha, K. M. (2022). The motivation factors affecting shopper behaviour in South Africa: The demographic influence. International Journal of eBusiness and eGovernment Studies, 14(1), 106–133. https://doi.org/10.34109/ijebeg.202214106

- Mamghaderi, M., Khamooshi, H., & Kwak, Y. H. (2021). Project duration forecasting: A simulation-based comparative assessment of earned schedule method and earned duration management. The Journal of Modern Project Management, 9(2), 7–19.

- Martínez‐Ferrero, J., Lozano, M. B., & Vivas, M. (2021). The impact of board cultural diversity on a firm's commitment toward the sustainability issues of emerging countries: The mediating effect of a CSR committee. Corporate Social Responsibility and Environmental Management, 28(2), 675–685. https://doi.org/10.1002/csr.2080

- Mattayaphutron, S., Tam, B., & Jariyapan, P. (2021). Macroeconomic Impact of Mandatory Retirement Age Policy to Population Aging in Thailand. Cuadernos de Economía, 44(126), 34–44.

- Méndez, M.-T., Picazo, M., & G.-M.-S.-M, A. (2021). Effects of sociocultural and economic factors on social entrepreneurship and sustainable development. Journal of Innovation & Knowledge, 6(2), 69–77.

- Ocampo, L. (2018). A probabilistic fuzzy analytic network process approach (PROFUZANP) in formulating sustainable manufacturing strategy infrastructural decisions under firm size influence. International Journal of Management Science and Engineering Management, 13(3), 158–174. https://doi.org/10.1080/17509653.2017.1345334

- Olaleye, B. R., Ali-Momoh, B. O., Herzallah, A., Sibanda, N., & Fa, A. (2021). Dimensional context of total quality management practices and organizational performance of SMEs in Nigeria: Evidence from mediating role of entrepreneurial orientation. International Journal of Operations and Quantitative Management, 21(4), 399–415. https://doi.org/10.46970/2021.27.4.6

- Oradi, J., & E-Vahdati, S. (2021). Female directors on audit committees, the gender of financial experts, and internal control weaknesses: Evidence from Iran. Accounting Forum, 45(3), 273–306. https://doi.org/10.1080/01559982.2021.1920127

- Orozco, L. A., Vargas, J., & Galindo-Dorado, R. (2018). Trends on the relationship between board size and financial and reputational corporate performance: The Colombian case. European Journal of Management and Business Economics, 27(2), 183–193. https://doi.org/10.1108/EJMBE-02-2018-0029

- Paltanavičiūtė, J. (2022). Creativity as social critique: A case study of the opera Have a Good Day!. Creativity Studies, 15(1), 233–245. https://doi.org/10.3846/cs.2022.15026

- Papenfuß, U., van Genugten, M., de Kruijf, J., & van Thiel, S. (2018). Implementation of EU initiatives on gender diversity and executive directors’ pay in municipally-owned enterprises in Germany and The Netherlands. Public Money & Management, 38(2), 87–96. https://doi.org/10.1080/09540962.2018.1407133

- Paraschiv, D.-M., Manea, D.-I., Țițan, E., & Mihai, M. (2021). Development of an aggregated social inclusion indicator. Disparities in the European Union on inclusion/exclusion social determined with social inclusion index. Technological and Economic Development of Economy, 27(6), 1301–1324. https://doi.org/10.3846/tede.2021.15103

- Peternel, I., & Grešš, M. (2021). Economic diplomacy: Concept for economic prosperity in Croatia. Economic Research-Ekonomska Istraživanja, 34(1), 109–121. https://doi.org/10.1080/1331677X.2020.1774788

- Que, N. D., Van Song, N., Mai, T. T. H., Phuong, N. T. M., Huong, N. T. X., Tiep, N. C., & Uan, T. B. (2022). Rice farmers’ perception and determinants of climate change adaptation measures: A case study in Vietnam. AgBioForum, 24(1), 13–22.

- Qureshi, M. A., Kirkerud, S., Theresa, K., & Ahsan, T. (2020). The impact of sustainability (environmental, social, and governance) disclosure and board diversity on firm value: The moderating role of industry sensitivity. Business Strategy and the Environment, 29(3), 1199–1214. https://doi.org/10.1002/bse.2427

- Rehman, S., Orij, R., & Khan, H. (2020). The search for alignment of board gender diversity, the adoption of environmental management systems, and the association with firm performance in Asian firms. Corporate Social Responsibility and Environmental Management, 27(5), 2161–2175. https://doi.org/10.1002/csr.1955

- Saeidi, P., Saeidi, S. P., Gutierrez, L., Streimikiene, D., Alrasheedi, M., Saeidi, S. P., & Mardani, A. (2021). The influence of enterprise risk management on firm performance with the moderating effect of intellectual capital dimensions. Economic Research-Ekonomska Istraživanja, 34(1), 122–151. https://doi.org/10.1080/1331677X.2020.1776140

- Saifan, S., Shibli, R., Ariffin, I. A., Ab Yajid, M. S., & Tham, J. (2021). Climate change and extension services' effects on farm level income in Malaysia: A time series analysis. AgBioForum, 23(2), 72–81.

- Salas-Rueda, R.-A., & Alvarado-Zamorano, C. (2022). Design of creative virtual spaces through the use of a web application during the educational process about bank savings. Creativity Studies, 15(2), 299–315. https://doi.org/10.3846/cs.2022.12304

- Saleem, A., Cheema, A. R., Rahman, A., Ali, Z., & Parkash, R. (2021). Do health infrastructure and services, aging, and environmental quality influence public health expenditures? Empirical evidence from Pakistan. Social Work in Public Health, 36(6), 688–706. https://doi.org/10.1080/19371918.2021.1920540

- Tamayo-Torres, I., Gutierrez-Gutierrez, L., & Ruiz-Moreno, A. (2019). Boosting sustainability and financial performance: The role of supply chain controversies. International Journal of Production Research, 57(11), 3719–3734. https://doi.org/10.1080/00207543.2018.1562248

- Türegün, N. (2018). Effects of borrowing costs, firm size, and characteristics of board of directors on earnings management types: A study at Borsa Istanbul. Asia-Pacific Journal of Accounting & Economics, 25(1–2), 42–56. https://doi.org/10.1080/16081625.2016.1246192

- Udeh, D., Abiahu, M.-F C., & Tambou, L. (2017). Impact of corporate governance on firms financial performance: A study of quoted banks in Nigeria. Udeh, FN, Abiahu, MC, & Tambou, LE (2017). Impact of Corporate Governance on Firms Financial Performance: A Study of Quoted Banks in Nigeria. The Nigerian Accountant,(50), 2(1), 54–62.

- Yang, W., Yang, J., & Gao, Z. (2019). Do female board directors promote corporate social responsibility? An empirical study based on the critical mass theory. Emerging Markets Finance and Trade, 55(15), 3452–3471. https://doi.org/10.1080/1540496X.2019.1657402

- Yousaf, Z., Radulescu, M., Nassani, A., Aldakhil, A. M., & Jianu, E. (2021). Environmental management system towards environmental performance of hotel industry: Does corporate social responsibility authenticity really matter? Engineering Economics, 32(5), 484–498. https://doi.org/10.5755/j01.ee.32.5.28619

- Zaid, M. A., Wang, M., Adib, M., Sahyouni, A., & Abuhijleh, S. T. (2020). Boardroom nationality and gender diversity: Implications for corporate sustainability performance. Journal of Cleaner Production, 251(1), 119–128. https://doi.org/10.1016/j.jclepro.2019.119652

- Zhu, X., Shang, H., Dai, Z., & Liu, B. (2021). The impact of E-commerce sales on capacity utilization. Engineering Economics, 32(5), 499–516. https://doi.org/10.5755/j01.ee.32.5.28508