?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

To achieve sustainable development, companies are aware that they need to move from the ‘take-make-consume-throw away’ pattern toward an economic model based on sharing, re-use, repair, refurbishing, and recycling. Implementing the circular economy concept into a company’s business model is not an easy process, given that some eco-innovations have higher costs with direct effects on financial performance. Hence, this study aims to determine the relationship between corporate financial performance and the performance measures of the circular economy through multivariate econometric estimations. The observations considered in our sample reflect the financial and circular economy performance for 411 companies with headquarters in the European G7 members disclosed in the period 2014-2020. The EU was chosen to carry out the study because the member states subscribe to a general reporting framework and the European Green Deal agreement, making it the most active in implementing the circular economy model. The findings are based on the econometric models related to the nature and amplitude of the association relation between firms’ financial performance and circular economy in connection with firms’ performance. The results show that the performance of the circular economy has a relatively small influence on the firms’ financial performance.

1. Introduction

The concept of productivity has been a driving force for economic growth (Solow, Citation1967). Still, it has also been a source for a massive waste of natural resources and serious long-term effects on the natural environment (Gibbs & Longhurst, Citation1995). A priority for the entire world became finding solutions for economic activity's negative effects. As a result, a paradigm shift has arisen: the sustainable development concept (Johnson & Wilson, Citation1999) is used to avoid depletion (UN, Citation2015).

Thus, through the UN Sustainable Development Goals, the UN seeks to involve stakeholders in the supply chain with environmentally friendly practices. Mostly, firms operate with constrained resources, so this is a challenging transition for economic entities (Rodríguez-Espíndola et al., Citation2022). To operate in a circular economy, firms need to develop a business model and base their entire activity on the pursuit of innovation (van Renswoude et al., Citation2015).

However, with all these benefits of the circular economy, one question remains: Does the circularity of a business model positively impacts a firm’s financial performance? This study aims to determine the relationship between corporate financial performance and the performance measures of the circular economy through multivariate econometric estimations. Therefore, it contributes to the circularity assessment process in companies by describing how circularity of business models impacts a firm’s financial performance. Our analysis examines 411 companies with headquarters in the European G7 members, considering that EU member states subscribe to a common reporting framework and the European Green Deal agreement, making it the most active region in the implementation of the circular economy. First, relevant research results about the relation between the circular economy concept and the business models are found and the theoretical concepts involved are described. Then, based on the framework for circular economy business model innovation, an exploratory analysis was performed that involved three levels of analysis. The first level is based on different financial performance measures that firms disclose through annual financial statements and is referred to both investors’ expectations and firms’ operations profitability. The next level is related to the measures reflecting some essential dimensions of the circular economy on a firm level. In contrast, the last level of analysis concerns the management factor, which is seen as a basic premise for the effective implementation of circular economy initiatives.

Our paper emphasizes that it is necessary to promote circular economy-oriented corporate strategic thinking, corporate circular economy policies, and effective governance mechanisms and monitoring tools addressing the risks derived from circular economy requirements. Starting from a top-down approach, we highlight that the authorities are responsible for ensuring the compliance of companies' business models with the European Directives in the field of circular economy, by outlining a more robust monitoring and control framework. Therefore, accountability must be addressed through effective and efficient processes and tools (Di Vaio et al., Citation2022). This approach includes a harmonized non-financial reporting framework, as described by the 2014/95/EU directive and a common model of evaluation of corporate circular economy performance, which should be the basis for macroeconomic benchmarking analysis and public policies in transition toward a circular economy. In those circumstances, process management, human capital, and alignment to new advanced technologies become essential success factors for the transition to a circular economy (Awan & Sroufe, Citation2022; Khan et al., Citation2020). This way, firms can become more agile in coping with shocks to the economy and the exponential increase on demand, by transforming into a factor of change of paradigm, increasing public awareness regarding the opportunity of circular economy strategies such as the use of regenerable resources, increase of resources productivity, reduction of waste, sharing resources, supporting supplier loops, etc., with implications on consumers’ demand and producers’ offerings (Lewandowski, Citation2016).

However, a firm’s direction toward circular economy is mainly driven by management discretionary choice, who must be incentivized either through internal bonus payments or forced by capital markets’ pressure and governments’ non-compliance costs to align its business model to the principles of circular economy. Instead, it is expected the institutional factor should be present to promote and support circular economy initiatives. Otherwise, the initial investment costs required are unlikely to be covered by firms, either because of lack of resources or simply because of lack of opportunity from a management perspective. Therefore, for the current study also considers country fixed effects and industry fixed effects, to understand if there is a coordinated approach on the transition towards a circular economy or a high degree of heterogeneity in practice that describes few effects of a circular economy.

This paper fills the gap in the literature by analyzing the impact of a circular economy-based business model on firms’ financial performance for companies with headquarters in the European G7 members, limiting the study to the weighted cost of capital and return of assets. Corporate financial performance indicators were selected to reflect both management choice, driven mainly by the return on assets, and the shareholders’ expectations, reflected by the return premium expected to assume the risk of transition to a circular economy.

The proposed research is structured in six sections. This first section highlights the preliminary aspects of the undertaken scientific approach, while the second section provides a literature review. The next two sections present the research methodology, the results obtained, and a discussion. Finally, the fifth section concludes our research.

2. Literature Review

Sustainable development adoption involved numerous conceptual changes regarding the need for economic development to consider not only economic but also social and environmental goals. In recent years, a shift involving the involvement of resources in the production process occurred. As a result, the traditional linear economy model evolved into the circular economy model, bringing many benefits, not only in terms of money savings but also in the business model innovation (Lewandowski, Citation2016). In such a model, corporations take the leading role, and the innovation of the business model becomes the main action.

As resources are limited, the circular economy is perceived as a production and consumption model needed to ensure economic growth and sustainability (Benz, Citation2022; Di Vaio et al., Citation2022; Walker et al., Citation2021), promoted as an alternative way to the traditional and currently dominant linear business model (Uhrenholt et al., Citation2022). A circular economy extends the traditional cycle of the resources involved in the production through an extension of their life, and so obtain results not only in reducing resources consumption and waste disposal but also in emissions and pollution with a positive impact on financial, environmental, and social performance (Rodríguez-Espíndola et al., Citation2022).

Hence, as the awareness of the impact of economic activities on the environment increased, the circular economy became a desirable model necessary to be adopted by companies. However, moving to this business model is not an easy process (Horbach & Rammer, Citation2019), as real industry barriers and institutional challenges have been identified (Aloini et al., Citation2020; Khan et al., Citation2020; Tan et al., Citation2022). For instance, some eco-innovations have higher costs and need longer periods to produce effects on different indicators of firm performance (Soltmann et al., Citation2015).

Nevertheless, some studies show that reducing costs by optimizing the use of resources such as waste and water leads to increased profits and a consolidated position in the market, gaining a competitive advantage from a long-term perspective (Moric et al., Citation2020). Also, improving resource efficiency is conducive to positive returns and profitability (Rexhäuser & Rammer, Citation2014). In the long run, researchers state that a mix of factors, including country, sector of activity, size, the importance of R&D activities, and more importantly, the share of turnover invested in the circular economy, influence the relationship between financial performance of companies and that a circular economy-based business model can be implemented to fight against climate change, waste generation, pollution, and resource depletion challenges (Moric et al., Citation2020; Svensson & Funck, Citation2019; Zamfir et al., Citation2017). A proactive eco-innovation in product, process, and technology also directly affects firms’ financial performance (Johl & Toha, Citation2021). Nonetheless, Blasi et al. (Citation2021) highlight that SMEs that fall into the lower-medium-performing range might benefit from intensively signaling their circularity into the market.

However, there are a wide variety of circular economy indicators used to assess waste management and resources recovery systems that may be included in the unclear and diverse understanding of the concept and the links between the circular economy business model and financial performance (Corona et al., Citation2019). It seems that, currently, there is a lack of empirical evidence on a more comprehensive approach regarding the costs and benefits of implementation of a circular economy-based business model on firms’ financial performance level (De Angelis, Citation2018; Lahti et al., Citation2018). The previous research is oriented toward the theoretical universe of strategies, policies, and business model redesign, or mainly directed toward the area of the more general objective of sustainable growth (Hansen & Revellio, Citation2020; Kalmykova et al., Citation2018). Most of the existing papers are address a theoretical framework and the macroeconomic landscape of the circular economy (Barros et al., Citation2021; Martinho & Mourão, Citation2020). Therefore, our study attempts to fill the literature gap concerning the circularity assessment in companies, more specifically, how the circularity of a business model impacts a firm’s financial performance.

Smol (Citation2021) stated that the state of art of monitoring progress on transition to sustainable business models and circular economy-oriented business models lacks coherent monitoring platforms and tools. Moreover, a limited number of jurisdictions have adopted regulations that ask for mandatory disclosure of such non-financial information (Christensen et al., Citation2021; Monciardini et al., Citation2020). Nonetheless, an essential criterion for transparency concerning circular economy and sustainability-related information is strongly connected to the preparers’ subjective rationale on information materiality (Christensen et al., Citation2021). Also, it seems that penalties and incentives and the responsibility for product recovery are the prominent external practices advocated for a successful circular economy implementation (Sudusinghe & Seuring, Citation2021). However, the crisis generated by COVID-19 has caused major disruptions to supply chains. It has put all factors of aggregate demand (namely, consumption, capital spending, and exports) in exceptional decline (Hassan et. al., 2021) and highlighted the need to reduce dependences and diversify supplies for enhanced resilience, a strong commitment to a more circular economy, and to achieve financial performance.

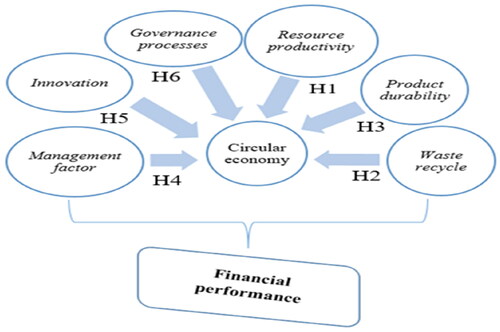

With these aspects under consideration, this research study proposes the following main hypotheses, depicted in :

Figure 1. Hypotheses development.

Source: authors' projection.

H1: Resource productivity influences firm performance.

H2: Waste recycle ratio influences firm performance.

H3: Product durability influences firm performance.

H4: Management is a mediating factor of the circular economy with an impact on firm performance.

H5: Innovation in the environmental area is a moderating factor for resource productivity with an impact on firm performance.

H6: Governance processes moderate the impact of sustainability strategy on firm performance.

3. Methodology

The study is designed to analyze the relationship between financial performance disclosed by firms and several performance measures of the circular economy. For this purpose, we proceed to multivariate econometric estimations using data extracted from the Refinitiv database.

3.1. Data collection

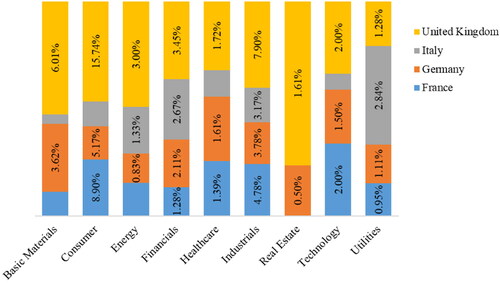

Econometric models are estimated starting from data collected from the Refinitiv database. Starting from a database of 25564 observations describing 2014-2020 financial and non-financial information disclosed by 3652 companies with headquarters in the European G7 members, we have reached a final sample of 1768 observations. The observations considered in our sample reflect financial and circular economy performance for 411 companies disclosed in the period 2014-2020. Most of the sample is covered by British companies (41.98%), followed by French companies (21.97%), German companies (20.34%), and Italian companies (15.7%).

In , we represent the composition of our sample by country and by area of activity, which indicates that the sample is relatively balanced with the highest proportion covered by companies operating in the Consumer domain (33.97%), followed by manufacturing companies (19.57%).

Figure 2. Sample size distribution by area of activity.

Source: authors’ projection

We have resumed our analysis of the G7 European members, considering two main reasons. First, it was noted in the literature that the EU community may have made the biggest progress towards a circular economy and a sustainable economic growth model (Mazur-Wierzbicka, Citation2021). Second, empirical evidence suggests that developed economies are more interested and have sufficient resources to initiate conversion programs for their national economies (OECD, 2021). EU countries are subject to a similar legal framework and better cooperation and regional monitoring of key circular economy indicators (Mhatre et al., Citation2021; Smol, Citation2021).

3.2. Variable definitions

The estimated model look for interaction effects that reveal the conditionality of financial performance based on firms’ governance effectiveness, management commitment to sustainability strategies, and respectively implementation of firm policy concerning executives’ compensation for performance in the sustainability area. However, currently, there is a lack of a coherent measurement framework designed to measure circular economy at the microeconomic level (Roos Lindgreen et al., Citation2020), with some progress on the design and implementation of circular economy monitoring on the macroeconomic level (Smol, Citation2021).

We have resumed our analysis of three essential directions of action toward circular economy business models, respectively measures that relate to progress on the productivity of resources affected on firms’ operations, the level of waste recycling, the degree of CO2 and other emissions, and the measure of the maturity of quality management systems.

In , we briefly describe the study's variables: dependent, independent, and control variables. The independent variables considered in the model represent scores calculated and reported on the Refinitiv database. Those variables ensure scale uniformity for our model estimation, as they are calculated based on a percentile-based score methodology that suggests a ranking score for each company within the ESG universe of companies included in the Refinitiv database. Score-based variables considered in the analysis are collected directly from the Refinitiv database. Variables such as resource used, waste recycled, management systems, emissions, governance, management, innovation, and strategy represent score-based values calculated on the Refinitiv database using a percentile-based ranking methodology that uses more than 630 measures of ESG dimensions. This percentile rank scoring methodology is complex, revealing information for each firm about its position on the industry benchmarking, considering weights for each measure specific to each industry group, based on a materiality matrix.

Table 1. Variable definition and source of information.

Resource productivity: As highlighted by De Angelis (Citation2018), circular economy-based business models look more for pollution prevention, product stewardship, and sustainable development. Firms can gain a competitive advantage from a long-term perspective when rationalizing the use of resources and the design of their products and processes because of the actual context of constrained resources. Therefore, we expect higher involvement in activities to reduce material consumption, increase resource productivity, and continuously improve operational processes. This leads to a decrease in cost-based performance measures.

Waste materials recycling: With this study, we plan to highlight the role of firms’ initiatives in reducing the waste materials through dedicated projects of continuous improvement and consolidation of an internal culture of circular economy widely spread along the supply chains (Bertassini et al., Citation2021; Kwarteng et al., Citation2021; Scipioni et al., Citation2021). All those efforts are expected to correlate between firms participating in the supply chains. Therefore, knowledge transfers and strong cooperation along the supply chain are required, with coordination ensured by governmental agencies and professional organizations.

Quality management systems: As noted by Adam et al. (Citation2017), waste material cannot be avoided, but rather can be substantially reduced. This objective must identify the best solutions in process redesign to ensure a transition from a linear economy to a circular economy. Moreover, it is unanimously confirmed in the literature that the redesign of business models towards the philosophy of circular economy must take into account the specific of each industry, local market, and firm’s operations particularities (Adam et al., Citation2017; Hansen & Revellio, Citation2020), with particular focus on circular-oriented innovations and global best practice (Chioatto et al., Citation2020). Instead, any change determined by process redesign must ensure high product quality, effective and cost-optimized industrial processes, and proper continuous control and monitoring tools. For this objective, firms should assess their quality systems, continuous improvement processes, and TQM-related processes to adjust them to the new circular economy requirements. Therefore, we expect an effective quality management system oriented toward circular-economy requirements to increase fixed costs. The dynamics of the economic environment and the pressure firms currently face with constraints on resources ask for a smooth and controllable adjustment to shocks in the economy, including those related to circular economy requirements. Through a robust and mature quality management systems framework, firms can cope with those fast changes, supported by processes, tools, and people involved in change management concerning product quality (Santa-Maria et al., Citation2021).

3.3. Econometric model design

Models planned to be estimated in the study are designed considering four main objectives. First, econometric models estimate the relationship between the primary dependent variable, the weighted cost of capital, and the measures of circular economy performance disclosed by firms included in the sample. Second, we look for the robustness of results, reviewing this time association between operational profitability and the measures of circular economy performance disclosed by firms included in the sample. Third, we analyze the changes determined on econometric model estimates if we control each country and industry's fixed effects. Forth and the last level of analysis assume a mixed approach of all the above econometric models incorporated to understand how much of the financial performance disclosed by firms can be explained by circular economy percentile-based scores calculated by Refinitiv.

Panel data econometric approach is considered in the study, revealing the country fixed effects and industry-specific fixed effects. Models tested are described in relations below:

models (1) to (6) that address circular economy measures influence on financial performance, respectively weighted cost of capital and operations profitability:

models (7) to (10) that address, besides the circular economy measures influence on financial performance, moderating effect of governance, strategy, and management factors:

Where represent the company, whereas

represent either the country or the industry dummy variable, depending on the model, each of those models is estimated, considering no fixed effects (models (1) and (4)), country fixed effects (models (2), (5), (7) and (9)), and industry fixed effects (models (3), (6), (8) and (10)). Therefore, the intercept of pooled OLS regression model

is decomposed into two elements, a component indicating the unobserved differences between countries and a constant term.

Decision made concerning the choice of fixed effects versus random effects econometric models is made based on the Hausman test. In case the -value of the test is under the significance level before being established, the model with fixed effects econometric model is considered a better model fit than the pooled econometric regression model (Lee et al., Citation2019). Otherwise, we chose between the random effects econometric model and pooled OLS econometric model. For this decision, we look for the

-value of the Breusch-Pagan test.

Nonetheless, we check for the hypothesis of heteroskedasticity, performing the Modified Breusch-Pagan cross-sectional test to check if our estimates are consistent but inefficient as the estimates' variance is not minimized. As long the -value of the test exceeds the significance level selected prior, the model is heteroskedastic, and we estimate the standard errors of our regression coefficient using the White cross-section covariance method.

4. Results and discussion

In the exploratory analysis, we performed three levels of analysis. The first level looks for different financial performance measures firms disclose through annual financial statements, addressing investors’ expectations and profitability. The next level is related to the measures reflecting some essential dimensions of the circular economy on a firm level. In contrast, the last level of analysis concerns the management factor, which is seen as a basic premise for the flawless implementation of circular economy initiatives.

In , we first provide basic descriptive statistics to draw up an overall image of our sample in terms of financial performance, circular economy performance, and management commitment to the circular economy direction of firms’ development.

Table 2. Descriptive statistics

4.1. Corporate financial performance analysis

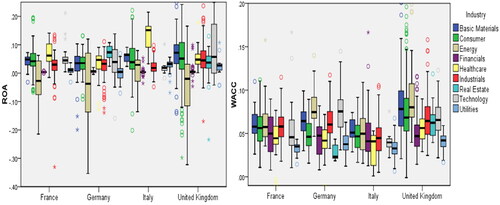

We observed that firms’ financial performance is relatively heterogeneous in terms of financial performance, as it depends on financing, investment, and operations decisions. However, the firms included in our sample are relatively profitable (0.038), with approximately 15.85% reporting negative values, while most of them reporting slight positive values. Instead, the measure of WACC, which incorporates investors’ expectations in terms of risk aversion, is more homogenous along with the sample, as more than 50% of the firms have reported a weighted cost of capital in the range of 0.041 to 0.074. In contrast, five companies have reported negative cost of capital only, of which four operate in the healthcare area of activity. As noted in , we observe the significant impact of industry-specific performance disclosed by financial statements.

Figure 3. Differences in financial performance reported.

Source: authors’ projection

Regarding Refinitiv percentile methodology scoring, the circular performance measures reported by firms seem to be moderate, as they are on the average of the interval of 0 to 100 scale. The higher score in the case of the productivity resources was 72.44. In contrast, high value is also found in the case of CO2 emissions (75.03), which suggests that despite the efforts companies make to reduce material consumption, industrial processes continue to grow faster than savings made through increased materials productivity.

Firms vary significantly through the specific of their business model, which is significantly different across areas of activity and conditioned by macroeconomic conditions on a national level.

Looking at , we observe that industry-specific determine substantial differences in firms’ financial performance, especially in manufacturing and services areas of activity which are better covered in our sample. Those differences are expected as investors’ expectations differ based on substantially different risk exposure specific for each activity area. Additionally, the representation shows that the macroeconomic context of each economy brings differences in the mean level of weighted cost of capital, as significant differences can be found in the structure of the national economies.

4.2. Corporate circular economy performance analysis

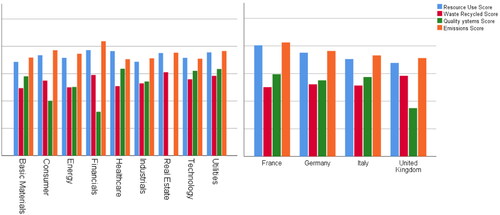

In , we have represented the mean score of our metrics reflecting firms’ dimensions of circular economy, as calculated and reported on the Refinitiv database, based on the random selection made for our study.

Figure 4. Differences in circular economy performance reported.

Source: authors’ projection

On the one hand, the results suggest that firms, no matter the area they operate in, look for optimization of the use of resources (Heshmati, Citation2015). Additionally, we observe that firms pay attention to the quality management systems implemented and the initiatives of continuous improvement operationalized through Six Sigma projects. Those dimensions represent fundamental premises for circular economy initiatives to generate expected outcomes. In the current Industry 5.0, the symbiosis between management systems, operational processes, disruptive technologies, and human factors is essential (Domil et al., Citation2022).

On the other hand, firms with operations in the construction area seem to have the lowest waste recycling score, as waste material in this area involves high costs of recycling and reuse, with additional exposure to non-compliance issues (EEA, Citation2020). However, those scores must be carefully evaluated. For instance, a higher level of the score for firms in the services area, compared with those operating in construction, indicates that the waste generated is recycled in a higher proportion but does not refer to the fact that the volume is significantly lower than in the construction area.

4.3. Management and governance profile analysis

We find similar results concerning the scores addressing the effectiveness and commitment of the management team to a sustainable growth strategy and implementation of innovative technologies in environment conservation, with moderate mean values related to the 0 to 100 scale. However, a higher value is reported in the case of CSR strategy (62.91), suggesting that companies became aware of the need to orient their vision and strategies more towards sustainable growth. Our sample seems relatively homogenous when referring to management commitment and corporate governance measures, which ensure the organization of formal processes to implement strategies and policies in sustainability and circular economics on the firm level.

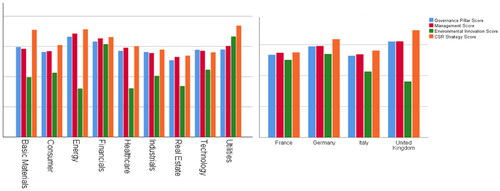

Industry-specific determines significant differences in the complexity of the operational process and the key activities, the effectiveness of governance mechanisms, and the management team committed to sustainable development. Based on information from , we emphasize higher differences, across both industries and countries, on the score of environmental innovation, which shows reluctance for using emerging technologies in environmental protection, primarily associated with high acquisition and implementation costs.

Figure 5. Differences on the organizational profile level.

Source: authors’ projection

Instead, management commitment seems to differ within firms operating in the commerce area, as the level of management score is lower than in the case of the other areas of activity included in our analysis. We observed similar findings in the firms’ governance scores, which shows an even more systemic issue related to how processes and decision structures are combined besides lower alignment of the management team to firms’ strategies. They seem to generate lower synergy effects, including in firms’ circular economy and sustainable development.

Unfortunately, firms operating in construction still face problems in terms of developing towards a circular economy and sustainable development. The innovation score is lower than the other areas, as waste material from this area implies extremely high recycling costs or high exposure to non-compliance to sensitive legal requirements (EEA, Citation2020).

All those elements represent fundamental directions of action for firms to successfully implement redesigned circular economy-based business models (Heshmati, Citation2015; Mhatre et al., Citation2021). Management attitude towards sustainability, circular economy (including exposure to risks related), firms’ infrastructure (including waste management processes and equipment), firms’ governance mechanisms (including controls on compliance with legal, industry standards, and corporate requirements) or strategies and policies implementation and compliance are just a few of the multiple factors from this management and organizational perspective that might affect the success of the transition to the circular economy business model (Kalmykova et al., Citation2018).

4.4. Correlation analysis

In , we provide the Pearson correlation matrix to show the associations between the dependent variables in our study and the factors considered. The results suggest that statistically significant correlations exist only between a few variables considered in the analysis.

Table 3. Pearson correlation matrix.

The highest positive correlations are indicated by the relationship between the resource productivity score and the score concerning gas emissions (0.633). This suggests that the transition to more sustainable resource consumption is not always translated into less pollution, especially when choosing to continue using old technologies.

The lowest negative association appears between the productivity percentile score for the use of resources and the weighted cost of capital (-0.131), followed by the negative association with the score concerning the interest in environmental technologies (-0.101). Those relationships indicate that the cost implied by the transition of firms’ business model to a circular economy is one of the essential reasons for firms’ management reluctance (Camilleri, Citation2020). First, a higher volume of waste materials involves higher costs of handling, recycling, and re-use, directly impacting the firms’ financial results through the cost structure, leading to an increase in indirect production cost. Second, engagement in an initiative to recycle, reuse, raw material communization, or process optimization involves prior feasibility studies that consist of the cost of R&D, including costs of tooling, testing, and certification according to legal requirements, industry standards, customer-specific requirements.

A statistically significant association exists between ROA and the score reflecting the quality of the strategic framework companies have adopted for sustainable growth (-0.101). This result indicates a trade-off between sustainability objectives and financial objectives companies have set up. Despite the small value of the negative correlation, we would like to emphasize that such conflicting situations between strategic objectives have become a reality. The trend is that synergy effects expected from sustainability projects initiated by companies will decrease, in favor of more visible trade-off effects, with negative short-term on financial performance.

In these circumstances, management commitment to such direction is highly conditioned by authorities’ position towards a circular economy. Many main barriers to the transition towards a circular economy are sufficiently addressed (Khan et al., Citation2020). We remind here that the quality of regulation on the circular economy area is not sufficiently clear all the time. After all, firms willing to adopt a green business model are generally interested in the existence of incentives offered through national or regional strategic programs that grant financing resources and facilitate knowledge transfer, especially in the context of available Industry 4.0 enabling technologies (Alhawari et al., Citation2021).

4.5. Effects of circular economy on corporate financial performance

In , we synthesize the econometric models’ estimation results that help us identify the nature and amplitude of the association relation between firms’ financial performance and circular economy-related firms’ performance. Starting from three main pillars of what circular economy-based business models mean, we check through those models how efforts made by firms affect their equity profitability and liquidity and how investors’ expectations are influenced by green economy projects' implementation. For this purpose, we have looked for the influence of product quality, the proportion of waste materials recycled, and the initiatives to reduce material used along the entire supply chain.

Table 4. Marginal econometric effects of circular economy measures.

On the one hand, the results show a significantly negative marginal effect of the resource use score on the weighted cost of capital (), which is robust even when controlling for country fixed effects (

) and industry fixed effects (

). A higher score on resource productivity suggests a lower cost of capital. The results align with Masi et al. (Citation2018), who have emphasized that firms focus mainly on resource and energy utilization efficiency rather than investment recovery, green purchasing, and customer cooperation.

In the circular economy context, the transformation of the business models relates to ensuring circular supplies, resources recovery, product life extension, sharing platforms, or products perceived as services by the firms (Mhatre et al., Citation2021). The increase in resource productivity is essential for a successful circular economy on a firm level. Subsequently, value creation is expected in the long-term through gaining competitive advantage, with direct implications on the future cost structure, increase in capital profitability, and consolidation of investors’ trust in management's strategic vision and actions (Lahti et al., Citation2018). Those objectives ensure the premises for future financing and generate multiplier effects of current investments through a close relationship with financial institutions, but with an effective corporate governance landscape on the firms’ level (Aranda-Usón et al., Citation2019).

On the other hand, results show significant marginal effects of waste recycle score on the cost of capital, even after controlling for country fixed effects (), and the lower level of industry fixed effects (

). The negative association suggests that capital markets react positively to information disclosed by firms concerning actions of waste materials recycling.

Over the last decade, at least in the European Union, there have been started multiple regulatory initiatives in the circular economy (Barros et al., Citation2021; Reim et al., Citation2019). Relevant in this direction is the recent release EU Commission Action Plan for Circular Economy, integrated as a block within the so-called EU Green Deal, which is aimed to bring more coordination of national jurisdictions' efforts toward a national model of the circular economy. Consequently, capital markets have realized the need to transition towards circular-economy-based business models, as capital markets are significantly sensitive to the interest national authorities pay to changes in these directions. Moreover, in a highly competitive market environment, benchmarking against industry performers is essential to survive, especially in areas of activity that have already been oriented towards a circular economy, such as logistics, textiles, packaging, or agricultural domains. In those circumstances, performers in some critical areas become promoters for circular economy practice, with indirect implications on investors’ interest in companies subject to the benchmarking analysis.

The business model redesign represents basic strategic directions for management, aiming to create a significant competitive advantage in the long term and generate value along the supply chain by following the sustainable growth model (Hansen & Revellio, Citation2020). In those circumstances, management systems play a leading role in ensuring management control on the changes determined by external shocks or even requested by internal customers through consolidating a robust and mature change management system and strategies for reducing business model complexity. Adopting lean manufacturing, running Six Sigma projects, or simply adhering to Industry 5.0 principles and technologies is expected to facilitate management mission by giving them tools for business resilience to any external shocks. Essential in the circular economy context is that those changes are first controllable by the management team and second align to firms’ circular economy-based strategies (Mhatre et al., Citation2021).

We observe a statistically significant negative association between management systems scores and firms’ operations profitability (), with even a higher marginal effect when controlling for country fixed effects (

), or industry fixed effects (

). Unfortunately, the results suggest the importance of the horizon of time managers and shareholders focus on, as the management team looks mainly for high financial performance obtained on short-term, while investors search for a more long-term oriented strategic decision making. Suppose WACC can be perceived as a financial performance measure incorporating strategic investors' long-term perspective on the risk they assume. In that case, the rate of profitability is a short-term-based financial metric, whereas the WACC is related to a long-run perspective. Therefore, the costs to have organized robust and mature quality management systems within the company are reflected negatively on the ROA, with implications on the discussion on the trade-off between long-term oriented management action plans and short-term ones.

All models estimated are statistically significant, with a -value under the 1% significance level. However, the

adjusted is small, which suggests performance in a circular economy has a relatively small influence on the financial performance compared with other factors not included in our models, such as firm size, financial leverage, business model complexity, or even stock market liquidity.

4.6. Moderating and mediating effects of organizational factor

Bär et al. (Citation2021) emphasize the essential role of circular support models: managing and coordinating networks and resource flows, providing incentives for the transition to the circular economy, and other supporting activities. Those models refer mainly to governments' actions towards implementing the macroeconomic level of circular economy-based business models. Those actions should also promote and finance programs for entrepreneurial initiatives around the circular economy.

However, similar directions should be followed on firms’ levels as well. From this perspective, we underline the essential role of management team capabilities and commitment, doubled by developing an effective and transparent framework of corporate governance mechanisms, processes, and policies (Di Vaio et al., Citation2021). Nonetheless, the moderating effect of internal resource capabilities ensures optimal allocation of resources and leads to achieving circular economy targets set up at the firm level (Kristoffersen et al., Citation2021).

In , we provide the results that emphasize the interaction effects of organizational and management commitment on financial performance. Those interaction terms are aimed to allow us to analyze the impact of management commitment and ESG innovation capabilities on corporate financial performance (Suchek et al., Citation2021).

Table 5. Marginal effect of innovation and management factor.

The results show statistically significant effects of some interaction terms on firms' cost of capital. Therefore, the cost of capital is negatively influenced by firms’ ESG innovation capabilities (). These results suggest that managers would get positive economic benefits in the long term, as results related to those sustainability initiatives are generally expected to be obtained on longer time horizons. The results give management a solid base for decisions favoring circular economy-based business models. In the context of pressure on increasing resource productivity, ESG innovation determines a decrease in the cost of capital. This interaction term shows that firms could achieve potential cost savings if management could gain synergy by adopting Industry 4.0 and a circular economy. It also indicates potential indirect savings that could be obtained through digitalization and certification on relevant quality standards, which provide the company a robust framework for monitoring and controlling for alignment to actual best practices in the circular economy, which focuses mainly on resource and energy utilization efficiency, rather than investment recovery, green purchasing, and customer cooperation (Abdullah et al., Citation2018; Masi et al., Citation2018; Shah et al., Citation2019).

The results show an isolated marginal effect of the policy executives' compensation score and the score describing management commitment (Coef.= −0.000002, sig.<0.1), but only in the case of the models that control for country fixed effects. The results indicate shareholders' positive perception regarding the degree of management commitment to the company’s sustainable growth strategies, as the agency's costs are significantly reduced, with implications on the risk investors assume. Those effects are more visible in the case of firms that implemented a specific policy that describes management accountability and remuneration schemes (Di Vaio et al., Citation2022).

Instead, the ROA is negatively influenced, both in the case of the model controlling for country fixed effects ( and industry fixed effects (

). As mentioned already in previous sections, this negative effect is more related to the short-term horizon managers follow. As long managers are compensated for performance in the circular economy, they will have to trade off with the short-term financial profitability (Eccles et al., Citation2014). After all, no matter the business model design, leadership is essential. The only problem is how much managers contribute to the transition towards a circular economy, especially since they are also main facilitators of strategic thinking, promoters of optimal knowledge management, and supporters of attractive organizational culture and strong cooperation (Santa-Maria et al., Citation2021).

These results suggest how important is the role of governance mechanisms at the entity level on the degree of implementation of the sustainability strategies (). As we already underlined, governments' efforts in drafting guidance to support companies to transition to a circular economy, and financing initiatives on sustainability at the microeconomic level, ensure the premises for sufficient knowledge and best practice sharing. (Heshmati, Citation2015). However, the results show that the mediating role of the effectiveness of governance mechanisms is negative on firms’ financial performance, as they lead to an increase in the cost of capital, primarily because of insufficient investors' trust in how governance processes work.

4.7. Moderating effects of institutional factors

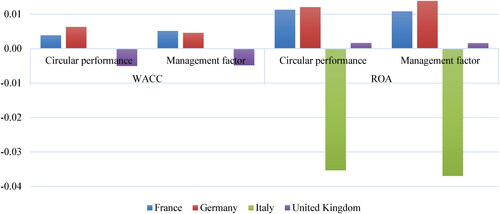

Based on Hausman tests, we decided that models including fixed effects provide the best fit as the value is less than the threshold of 0.05 (Lee et al., Citation2019). Therefore, systematic effects on the country and industry levels are confirmed when analyzing the marginal effects of performance measures of the circular economy on both the cost of capital and the operation's profitability. The exception is made in the case of model 6, assessing the relationship between the performance of the circular economy on firms’ profitability, looking for industry random fixed effects. Therefore, the random effects confirm the relation between ROA and the circular economy's performance measures, which vary significantly across countries. Evolution is mainly driven by structural differences in the cost structure, which is affected differently based on macroeconomic and local factors and economic context.

Differences between models estimated and presented in concerning the effect of circular economy performance on the weighted cost of capital are relatively small. When controlling for country and industry fixed effects, we observe small differences in the marginal effect of the resource use score on the WACC. Those results suggest that industry-specific and country macroeconomic context does not significantly impact firms’ circularity performance. Those results suggest that neither industry-specific associations nor governments haven’t yet found practical solutions to support effectively corporate circular economy initiatives, or at least the expected outcome is not yet visible. However, those results could be affected by the different involvement of countries in efforts to transition to a circular economy. They vary significantly because such decisions are highly subjective and depend on political decisions that do not always consider the information provided by specialists. In , we observe significant differences across countries only when analyzing firms’ profitability. Instead, a significantly higher negative impact on firms’ profitability is observed in Italian firms (-0.0354). In other words, the cost of capital is higher for Italian companies, while for British companies, the cost is lower. Integrating the factor concerning management commitment, governance processes, and adherence to emerging technologies in environmental protection, fixed effects in the model do not change. Those results indirectly suggest governmental support for circular economy provided on the firm level, either through regulation and enforcement or by grants and facilities provided for entrepreneurial circular economy-based initiatives (Heshmati, Citation2015).

Figure 6. Country fixed effects.

Source: authors’ projection

All countries included in our sample are classified as role model countries from the perspective of circular economy implementation over the last decade. Despite the lower ranking, Italy ensures the premises for a better cost of capital for firms. These results again underline how vital the coordination and promoting activities expected to be performed by governments are and the structure of the national economy, which might have as predominant domains the more critical ones in terms of a circular economy or not. However, the transition to a circular economy differs significantly on an industry base and even regionally. Differences are mainly related to three institutional factors mediating the transition of circular economy, this time in a regional context, respectively: the proximity of physical flows and assets, the maturation and diversity of market networks, and the inherent values and patterns of cooperation (Henrysson & Nuur, Citation2021).

Smol (Citation2021) stated that Italy has decided to implement integrated strategies to steer public opinion toward the circular economy concept. In contrast, the United Kingdom has chosen a more limited approach to implementing the circular economy. They have focused their attention on a limited number of sectors of the economy and a limited number of stakeholders involved.

Germany is classified as the best performer in the circular economy in the EU region (Mazur-Wierzbicka, Citation2021). These results suggest no significant systemic effects of the circular economy on firms’ financial performance. Despite the significant insights on circular economy regulation, waste material volumes still increase, which means the actual framework for waste recycling is not sufficiently developed to process all waste (Kruse & Wedemeier, Citation2022). Therefore, at the microeconomic level, we expect this association is rather influenced by local market and industry-specific.

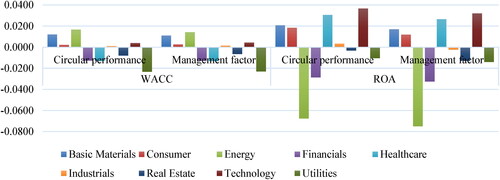

represents the fixed effects obtained, estimating the econometric relation between weighted cost of capital and firms’ circular economy performance, controlling for industry fixed effects. On the one hand, we observe highest fixed effects are obtained in the case of utilities and energy domains, which means a systemic increase in capital cost in firms operating in those sectors.

Figure 7. Sector fixed effects.

Source: authors’ projection

On the other hand, we observe negative systemic fixed effects on the weighted cost of capital in healthcare and technology companies. Those results are expected, as companies operating in those areas do not generate high volumes of waste materials. The exception would make the companies operating in the healthcare area manage dangerous materials. There is a low chance of waste recycling or re-use in those domains. However, proper maintenance plans can extend product lifetime, especially equipment, which is positively perceived by strategic investors. The lower complexity of business models and operational processes has allowed those companies to implement circular economy-based business models much more easily.

To sum-up our findings related to country and industry fixed effects, we note that the marginal effect of different circular economy metrics on the corporate financial performance is not significantly conditioned by institutional factors or challenges driven by industry-specific challenges.

5. Discussion

Our results reveal several insights concerning corporate financial performance and corporate circular economy performance. There are various circular economy business models that combine different strategies that refer to specific criteria concerning: characteristics of resources regeneration (e.g., use of renewable energy, waste recycling), possibility to share products and services (e.g., product lease, collaborative use of services), increase of resources productivity (e.g., waste reduction, make-to-order production models), focus on the circular flow of materials (e.g., remanufacture, recycle, resource recovery, upcycling), dematerialization (e.g., shift physical products, processes or services to virtual), and open innovation and knowledge exchange (e.g., 3 D printing, best practice sharing) (Lewandowski, Citation2016). These types of circular economy-oriented strategies have significant implications on corporate financial performance through impact on various business areas, such as strategic planning, cost management, supply chain management, quality management, environmental management, process management, logistics and reverse logistics, service management, and research and development (Barros et al., Citation2021; Shehzad et al., Citation2020). The main impact on those areas is translated to cost savings. However, there is an impact as well on the selling model, especially in supply chain management and R&D capabilities. On the one hand, both effects impact the short-term corporate financial performance, including asset profitability. On the other hand, there is an indirect effect apparent in the long term that is determined by the pressure of the capital markets and the effect of institutional factors on promoting and supporting transition of business models to a circular economy.

The results in this study focus on the increase on resources productivity, the effectiveness of waste management, and the impact of integrated quality management systems on corporate financial performance. Based on the econometric analysis, we partially confirm the hypotheses H1 and H2 that underline an increase in resource productivity and improvement on waste management, leading to lower costs of capital, which ensure higher economic value add and sustainable corporate growth. Therefore, the transition to a circular economy can generate benefits for firms only in the long term (Moric et al., Citation2020) and with the condition that shareholders’ expectations are met (Maitre-Ekern, Citation2017; Naseem et al., Citation2021).

Shareholders are not concerned with how managers achieve their expectations, including those related to sustainability, which is why implementing and consolidating an integrated quality management system is at managers’ discretion. Therefore, the cost of capital, incorporating investors’ expectations through the measure of risk premium, is less affected. However, our results show that such a quality management system affects corporate financial performance negatively, regarding assets profitability, mainly driven by the short-term impact of initial investment costs (Shah et al., Citation2019; Svensson & Funck, Citation2019) required by changes planned to gain new dynamic capabilities in terms of new advanced production technology, knowledge management, intellectual capital, or process optimization (Awan & Sroufe, Citation2022). Therefore, an increase in product durability, continuous improvements on the design of the processes, or active efforts on running value stream mapping and implementing lean strategic thinking initiatives represent a way towards a circular economy. However, the decision on this direction is mainly dependent on management discretionary choice and less on capital markets pressure, or national regulation requirements.

Management’s commitment to the firm’s objectives is essential and can be partially ensured through a bonus payment policy promoting the transition to a circular economy. However, firms’ objectives should be clearly stated concerning the path towards a circular economy business model, which is why it is essential that firms devise a transparent and viable long-term strategy, because the strategy is the most important dimension (Di Vaio et al., Citation2022). Our results indicate that a CSR strategy implemented with the support of governance processes leads to a slight increase in the weighted cost of capital. However, those results show just the short-term perspective of the transformation process of the business model towards a circular economy. Additionally, the results demonstrate how important it is that a firm’s strategy does not address its social and environmental risks in an isolated manner but instead consider the financial impact properly as well. Otherwise, the synergy effects when implementing a circular economy reduce drastically. That is why integrated strategic thinking about the transition toward a circular economy is necessary, involving not only changes in the product design, changes to the manufacturing process design by focusing on supply loops, or strengthening the strategic sourcing operations, but also changes to the sales model and cost structure objectives, or changes to governance mechanisms and tools ensuring a proper monitoring of progress towards a circular economy business model (Lewandowski, Citation2016). Therefore, firms should search for comprehensive reporting frameworks meant to ensure proper accountability regarding sustainability and circular economy objectives (Di Vaio et al., Citation2022), which can give firms a starting point for future benchmarking analysis if the corporate circular economy dashboard harmonizes on the firm level, at least limited to industry groups and regional clusters. It is only in this way that firms can transform its dynamic capabilities that ensure pollution prevention, product stewardship, material use standardization, processes optimization, and sustainable development in general, into a competitive advantage.

These potential benefits can be obtained through management commitment to corporate circular economy objectives via the more coordinated direction of governments and capital markets as well. The pressure of the capital markets on firms to move toward a circular economy business model is highly conditioned by the incentives provided through public policies, meaning that the state should become more involved in firms’ circular economy initiatives, by providing different forms of financial support and ensuring platforms of communication and cooperation that build up networks of long-term collaboration within the same industry (Goyal et al., Citation2022; Maitre-Ekern, Citation2017).

It must be recognized that the transition to a circular economy is not just a national objective emphasized by countries commitments to SDGs but much more. Limited resources, in parallel with an exponential demographic increase, requires drastic decisions that should be aimed toward ensuring sustainable consumption and production. This means that firms, supported by governments, become factors of change among consumers, influencing their consumption behaviour and preferences.

Generally, the voluntary transformation towards circular economy is expected to be more beneficial in the longterm, compared with the transformation determined through mandatory changes directed by regulations and non-compliance costs. As such, firms and governments should work together to be more transparent and cooperate on increasing public awareness concerning the need to move toward a circular economy. Afterall, implementation of a circular economy should be perceived as a potential source of self-financing resources in the long term, if management, shareholders, and the other stakeholders prove their commitment to the principles of circular economy (Aranda-Usón et al., Citation2019; Gonçalves et al., Citation2022).

This study has some limitations, which relate to the small sample of countries considered in the analysis, and as such further research is planned that is focused on emerging economies. This study highlights the need to study the link between corporate financial performance and corporate circular economy performance, considering the moderating effect of the capital markets as well. Nonetheless, this analysis could be extended to the regional level, to consider the macroeconomic measures of circular economy performance, to gain a better understanding of the lack of harmonized and coordinated efforts to implement circular economy initiatives.

6. Conclusion

Our study aimed to assess the relationship between corporate financial performance and the performance measures of the circular economy through multivariate econometric estimations using data extracted from the Refinitiv database. Therefore, our aim was to fill in a gap in the literature concerning the link between corporate financial performance and corporate circular performance (Aranda-Usón et al., Citation2019; Gonçalves et al., Citation2022). Consequently, managers are less likely to choose to transition toward the circular economy business model if they do not perceive long-term benefits that exceed the initial investment costs.

The results demonstrate that firms are trying to optimize the use of their resources by adopting different strategies toward the circular economy that look for an increase in resource productivity and the use of more renewable resources. For example, agile production processes aim to lead to sustainable consumption and production (Goyal et al., Citation2022; Lewandowski, Citation2016). The results show that corporate financial performance is sensitive to shareholders’ expectations, including expectations regarding sustainability and circular economy-based objectives because the weighted cost of capital is negatively affected by adapting business models to align with circular economy principles.

However, efforts made by firms in their attempts to transform their business model to align with circular economy principles become effective only with the support of the institutional factor that must promote and support corporate circular economy initiatives (Di Vaio et al., Citation2022; Walker et al., Citation2021).

Disclosure statement

No potential conflict of interest was reported by the author.

References

- Abdullah, M. I., Sarfraz, M., Qun, W., & Javaid, N. (2018). Drivers of green supply chain management. LogForum, 14(4), 437–447. https://doi.org/10.17270/J.LOG.2018.297

- Adam, S., Bucker, C., Desguin, S., Vaage, N., & Saebi, T. (2017). Taking part in the circular economy: four ways to designing circular business models. Available at SSRN 2908107

- Alhawari, O., Awan, U., Bhutta, M. K. S., & Ülkü, M. A. (2021). Insights from circular economy literature: A review of extant definitions and unravelling paths to future research. Sustainability, 13(2), 859. https://doi.org/10.3390/su13020859

- Aloini, D., Dulmin, R., Mininno, V., Stefanini, A., & Zerbino, P. (2020). Driving the transition to a circular economic model: A systematic review on drivers and critical success factors in circular economy. Sustainability, 12(24), 10672. https://doi.org/10.3390/su122410672

- Aranda-Usón, A., Portillo-Tarragona, P., Marín-Vinuesa, L. M., & Scarpellini, S. (2019). Financial resources for the circular economy: A perspective from businesses. Sustainability, 11(3), 888. https://doi.org/10.3390/su11030888

- Awan, U., & Sroufe, R. (2022). Sustainability in the circular economy: Insights and dynamics of designing circular business models. Applied Sciences, 12(3), 1521. https://doi.org/10.3390/app12031521

- Bär, H., Schenuit, C., & Runkel, M. Klimaneutralität, A. F. H., inkonsistenter Politik, I. I. I. B., einer Klima-Finanzpolitik, B. Z. S., Umfang, I., von ökologischen Steuern, L., & öffentlicher Ausgaben, I. I. I. U. (2021). Öffentliche Finanzen und die ökologische Transformation: Ansatzpunkte für mehr Konsistenz. Jahrbuch Für Öffentliche Finanzen 2-2021, 1–336.

- Barros, M. V., Salvador, R., do Prado, G. F., de Francisco, A. C., & Piekarski, C. M. (2021). Circular economy as a driver to sustainable businesses. Cleaner Environmental Systems, 2, 100006. https://doi.org/10.1016/j.cesys.2020.100006

- Benz, L. A. (2022). Critical success factors for circular business model innovation from the perspective of the sustainable development goals. Sustainability, 14(10), 5816. https://doi.org/10.3390/su14105816

- Bertassini, A. C., Ometto, A. R., Severengiz, S., & Gerolamo, M. C. (2021). Circular economy and sustainability: The role of organizational behaviour in the transition journey. Business Strategy and the Environment, 30(7), 3160–3193. https://doi.org/10.1002/bse.2796

- Blasi, S., Crisafulli, B., & Sedita, S. R. (2021). Selling circularity: Understanding the relationship between circularity promotion and the performance of manufacturing SMEs in Italy. Journal of Cleaner Production, 303, 127035. https://doi.org/10.1016/j.jclepro.2021.127035

- Camilleri, M. A. (2020). European environment policy for the circular economy: Implications for business and industry stakeholders. Sustainable Development, 28(6), 1804–1812. https://doi.org/10.1002/sd.2113

- Chioatto, E., Zecca, E., & D’Amato, A. (2020). Which Innovations for a Circular Business Model? A Product Life-Cycle Approach

- Christensen, H. B., Hail, L., & Leuz, C. (2021). Mandatory CSR and sustainability reporting: economic analysis and literature review. Review of Accounting Studies, 26(3), 1176–1248. https://doi.org/10.1007/s11142-021-09609-5

- Corona, B., Shen, L., Reike, D., Carreón, J. R., & Worrell, E. (2019). Towards sustainable development through the circular economy—A review and critical assessment on current circularity metrics. Resources, Conservation and Recycling, 151, 104498. https://doi.org/10.1016/j.resconrec.2019.104498

- De Angelis, R. (2018). Business models in the circular economy: Concepts, examples and theory. Springer.

- Di Vaio, A., Hasan, S., Palladino, R., & Hassan, R. (2022). The transition towards circular economy and waste within accounting and accountability models: A systematic literature review and conceptual framework. Environment, Development and Sustainability, 1–77.

- Di Vaio, A., Hasan, S., Palladino, R., Profita, F., & Mejri, I. (2021). Understanding knowledge hiding in business organizations: A bibliometric analysis of research trends, 1988–2020. Journal of Business Research, 134, 560–573. https://doi.org/10.1016/j.jbusres.2021.05.040

- Domil, A., Burca, V., & Bogdan, O. (2022). Assessment of economic impact generated by industry 5.0, from a readiness index approach perspective. A cross-country empirical analysis. In Sustainability and innovation in manufacturing enterprises (pp. 233–256). Springer.

- Eccles, R. G., Ioannou, I., & Serafeim, G. (2014). The impact of corporate sustainability on organizational processes and performance. Management Science, 60(11), 2835–2857. https://doi.org/10.1287/mnsc.2014.1984

- EEA. (2020). Improving circular economy practices in the construction sector key to increasing material reuse, high quality recycling. Retrieved December 13, 2021. https://www.eea.europa.eu/highlights/improving-circulareconomy-practices-in

- Gibbs, D., & Longhurst, J. (1995). Sustainable development and environmental technology: A comparison of policy in Japan and the European Union. The Environmentalist, 15(3), 196–201. https://doi.org/10.1007/BF01901575

- Gonçalves, B. d S. M., Carvalho, F. L. d., & Fiorini, P. d C. (2022). Circular economy and financial aspects: A systematic review of the literature. Sustainability, 14(5), 3023. https://doi.org/10.3390/su14053023

- Goyal, S., Garg, D., & Luthra, S. (2022). Analyzing critical success factors to adopt sustainable consumption and production linked with circular economy. Environment, Development and Sustainability, 24(4), 5195–5224.

- Hansen, E. G., & Revellio, F. (2020). Circular value creation architectures: Make, ally, buy, or laissez‐faire. Journal of Industrial Ecology, 24(6), 1250–1273. https://doi.org/10.1111/jiec.13016

- Henrysson, M., & Nuur, C. (2021). The role of institutions in creating circular economy pathways for regional development. The Journal of Environment & Development, 30(2), 149–171. https://doi.org/10.1177/1070496521991876

- Heshmati, A. (2015). A review of the circular economy and its implementation, IZA Discussion Papers, No. 9611. Institute for the Study of Labor (IZA), Bonn. https://www.Econstor.Eu/Bitstream/10419/130297/1/Dp9611.Pdf.

- Horbach, J., & Rammer, C. (2019). Employment and performance effects of circular economy innovations. ZEW-Centre for European Economic Research Discussion Paper, 19–016.

- Johl, S. K., & Toha, M. A. (2021). The nexus between proactive eco-innovation and firm financial performance: A circular economy perspective. Sustainability, 13(11), 6253. https://doi.org/10.3390/su13116253

- Johnson, H., & Wilson, G. (1999). Institutional sustainability as learning. Development in Practice, 9(1-2), 43–55. https://doi.org/10.1080/09614529953205

- Kalmykova, Y., Sadagopan, M., & Rosado, L. (2018). Circular economy–From review of theories and practices to development of implementation tools. Resources, Conservation and Recycling, 135, 190–201. https://doi.org/10.1016/j.resconrec.2017.10.034

- Khan, S., Maqbool, A., Haleem, A., & Khan, M. I. (2020). Analyzing critical success factors for a successful transition towards circular economy through DANP approach. Management of Environmental Quality: An International Journal, 31(3), 505–529. https://doi.org/10.1108/MEQ-09-2019-0191

- Kristoffersen, E., Mikalef, P., Blomsma, F., & Li, J. (2021). The effects of business analytics capability on circular economy implementation, resource orchestration capability, and firm performance. International Journal of Production Economics, 239, 108205. https://doi.org/10.1016/j.ijpe.2021.108205

- Kruse, M., & Wedemeier, J. (2022). Circular economy in Germany: A methodology to assess the circular economy performance of NUTS3 regions. HWWI Research Paper.

- Kwarteng, A., Simpson, S. N. Y., & Agyenim-Boateng, C. (2021). The effects of circular economy initiative implementation on business performance: The moderating role of organizational culture. Social Responsibility Journal, 1–11. https://doi.org/10.1108/SRJ-01-2021-0045

- Lahti, T., Wincent, J., & Parida, V. (2018). A definition and theoretical review of the circular economy, value creation, and sustainable business models: Where are we now and where should research move in the future? Sustainability, 10(8), 2799. https://doi.org/10.3390/su10082799

- Lee, C.-F., Chen, H.-Y., & Lee, J. (2019). Financial econometrics, mathematics and statistics. Springer.

- Lewandowski, M. (2016). Designing the business models for circular economy—Towards the conceptual framework. Sustainability, 8(1), 43. https://doi.org/10.3390/su8010043

- Maitre-Ekern, E. (2017). The Choice of Regulatory Instruments for a Circular Economy. In Environmental law and economics (pp. 305–334). Springer.

- Martinho, V. D., & Mourão, P. R. (2020). Circular economy and economic development in the European Union: A review and bibliometric analysis. Sustainability, 12(18), 7767. https://doi.org/10.3390/su12187767

- Masi, D., Kumar, V., Garza-Reyes, J. A., & Godsell, J. (2018). Towards a more circular economy: Exploring the awareness, practices, and barriers from a focal firm perspective. Production Planning & Control, 29(6), 539–550. https://doi.org/10.1080/09537287.2018.1449246

- Mazur-Wierzbicka, E. (2021). Towards circular economy—A comparative analysis of the countries of the European Union. Resources, 10(5), 49. https://doi.org/10.3390/resources10050049

- Mhatre, P., Panchal, R., Singh, A., & Bibyan, S. (2021). A systematic literature review on the circular economy initiatives in the European Union. Sustainable Production and Consumption, 26, 187–202. https://doi.org/10.1016/j.spc.2020.09.008

- Monciardini, D., Mähönen, J. T., & Tsagas, G. (2020). Rethinking non-financial reporting: A blueprint for structural regulatory changes. Accounting, Economics, and Law: A Convivium, 10(2), 1–43.

- Moric, I., Jovanović, J. Š., Đoković, R., Peković, S., & Perović, Đ. (2020). The effect of phases of the adoption of the circular economy on firm performance: Evidence from 28 EU countries. Sustainability, 12(6), 2557. https://doi.org/10.3390/su12062557

- Naseem, S., Mohsin, M., Zia-UR-Rehman, M., Baig, S. A., & Sarfraz, M. (2021). The influence of energy consumption and economic growth on environmental degradation in BRICS countries: An application of the ARDL model and decoupling index. Environmental Science and Pollution Research, 29(9), 13042–13055.

- Reim, W., Parida, V., & Sjödin, D. R. (2019). Circular business models for the bio-economy: A review and new directions for future research. Sustainability, 11(9), 2558. https://doi.org/10.3390/su11092558

- Rexhäuser, S., & Rammer, C. (2014). Environmental innovations and firm profitability: unmasking the Porter hypothesis. Environmental and Resource Economics, 57(1), 145–167. https://doi.org/10.1007/s10640-013-9671-x

- Rodríguez-Espíndola, O., Cuevas-Romo, A., Chowdhury, S., Díaz-Acevedo, N., Albores, P., Despoudi, S., Malesios, C., & Dey, P. (2022). The role of circular economy principles and sustainable-oriented innovation to enhance social, economic and environmental performance: Evidence from Mexican SMEs. International Journal of Production Economics, 248, 108495. https://doi.org/10.1016/j.ijpe.2022.108495

- Roos Lindgreen, E., Salomone, R., & Reyes, T. (2020). A critical review of academic approaches, methods and tools to assess circular economy at the micro level. Sustainability, 12(12), 4973. https://doi.org/10.3390/su12124973

- Santa-Maria, T., Vermeulen, W. J. V., & Baumgartner, R. J. (2021). Framing and assessing the emergent field of business model innovation for the circular economy: A combined literature review and multiple case study approach. Sustainable Production and Consumption, 26, 872–891. https://doi.org/10.1016/j.spc.2020.12.037

- Scipioni, S., Russ, M., & Niccolini, F. (2021). From barriers to enablers: The role of organizational learning in transitioning SMEs into the Circular economy. Sustainability, 13(3), 1021. https://doi.org/10.3390/su13031021

- Shah, S. G. M., Sarfraz, M., Fareed, Z., Rehman, M. A. u., Maqbool, A., & Qureshi, M. A. A. (2019). Whether CEO succession via hierarchical jumps is detrimental or blessing in disguise? Evidence from Chinese listed firms. Zagreb International Review of Economics and Business, 22(2), 23–41. https://doi.org/10.2478/zireb-2019-0018

- Shah, S. G. M., Tang, M., Sarfraz, M., & Fareed, Z. (2019). The aftermath of CEO succession via hierarchical jumps on firm performance and agency cost: Evidence from Chinese firms. Applied Economics Letters, 26(21), 1744–1748. https://doi.org/10.1080/13504851.2019.1593932

- Shehzad, K., Xiaoxing, L., Sarfraz, M., & Zulfiqar, M. (2020). Signifying the imperative nexus between climate change and information and communication technology development: A case from Pakistan. Environmental Science and Pollution Research International, 27(24), 30502–30517.

- Smol, M. (2021). Inventory and comparison of performance indicators in circular economy roadmaps of the European countries. Circular Economy and Sustainability, 1–28. https://doi.org/10.1007/s43615-021-00127-9

- Solow, R. M. (1967). Some recent developments in the theory of production. In The theory and empirical analysis of production (pp. 25–53). USA: National Bureau of Economic Research.

- Soltmann, C., Stucki, T., & Woerter, M. (2015). The impact of environmentally friendly innovations on value added. Environmental and Resource Economics, 62(3), 457–479. https://doi.org/10.1007/s10640-014-9824-6

- Suchek, N., Fernandes, C. I., Kraus, S., Filser, M., & Sjögrén, H. (2021). Innovation and the circular economy: A systematic literature review. Business Strategy and the Environment, 30(8), 3686–3702. https://doi.org/10.1002/bse.2834

- Sudusinghe, J. I., & Seuring, S. (2021). Supply chain collaboration and sustainability performance in circular economy: A systematic literature review. International Journal of Production Economics, 245, 108402.

- Svensson, N., & Funck, E. K. (2019). Management control in circular economy. Exploring and theorizing the adaptation of management control to circular business models. Journal of Cleaner Production, 233, 390–398. https://doi.org/10.1016/j.jclepro.2019.06.089

- Tan, J., Tan, F. J., & Ramakrishna, S. (2022). Transitioning to a circular economy: A systematic review of its drivers and barriers. Sustainability, 14(3), 1757. https://doi.org/10.3390/su14031757

- Uhrenholt, J. N., Kristensen, J. H., Gil, M. C. R., Jensen, S. F., & Waehrens, B. V. (2022). Circular economy: Factors affecting the financial performance of product take-back systems. Journal of Cleaner Production, 130319

- UN. (2015). Resolution adopted by the General Assembly on September 25, 2015

- van Renswoude, K., ten Wolde, A., & Joustra, D. J. (2015). Circular business models–Part 1: An introduction to IMSA’s circular business model scan. IMSA Amsterdam, April

- Walker, A. M., Opferkuch, K., Roos Lindgreen, E., Raggi, A., Simboli, A., Vermeulen, W. J. V., Caeiro, S., & Salomone, R. (2021). What is the relation between circular economy and sustainability? Answers from frontrunner companies engaged with circular economy practices. Circular Economy and Sustainability, 9(9), 1–28.

- Zamfir, A.-M., Mocanu, C., & Grigorescu, A. (2017). Circular economy and decision models among European SMEs. Sustainability, 9(9), 1507. https://doi.org/10.3390/su9091507