?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study examines the effects of gender and cultural diversity of boards on the corporate governance and social performance of 373 companies listed in 24 emerging country markets over the period of 2010–2019 using panel data analysis. A two-step system GMM model is also applied to test the endogeneity problem. The results indicate that gender and cultural diversity positively affect corporate governance performance. While we note that social performance is positively associated with both gender and cultural diversity, this relationship is insignificant. The findings offer multidimensional insights for companies, policy makers, and stakeholders to promote the association between gender and cultural diversity initiatives and corporate sustainability dimensions in emerging markets.

JEL CODES:

1. Introduction

Recent developments in technology and the business environment have forced companies to generate more value for stakeholders. They have also created distinct challenges that can have a profound effect on decision-making and corporate performance. The increasing complexity of business life has forced companies to employ dedicated board members equipped with creative toolkits and different backgrounds to reflect their contribution to operational and financial performance. In this spirit, the diversity of board members has drawn the attention of many companies, policymakers, and other related parties with its role in formulating and implementing business strategies.

The corporate board is a vital internal governance mechanism, playing a critical role in mitigating agency problems and enhancing corporate performance (Borlea et al., Citation2017; Ciftci et al., Citation2019). It is composed of team members with different backgrounds that help companies reach their goals. In this frame, the diversity of board members allows a greater range of views to shape the business by perceiving stakeholders' interests and offering creative solutions to challenging problems. As a valuable attribute, this ability also plays a complementary role in corporate performance (Fatemi et al., Citation2018; Friede et al., Citation2015; Luo et al., Citation2015). Companies show more interest in social activities, customer satisfaction, ties with local communities, and human capital when there is greater stakeholder pressure (Dodd et al., Citation2019; Rajesh, Citation2020). Kemp (Citation2011) claimed that corporate boards have an important role in ensuring that companies pursue economic value creation objectives by observing values consistent with social responsibility and keeping a balance between financial and non-financial goals. In this context, new social and environmental standards complete business performance (Achim et al., Citation2015).

Although numerous studies have examined the impact of board diversity on corporate performance, relatively few, mostly in developed countries, have predominantly investigated the effects of gender and cultural diversity on corporate governance and social performance. Female board members with prior experience in other companies offer diverse opinions and network ties, contributing to improved cohesion and corporate governance (Wagn, Citation2020). Therefore, the inclusion of more female members may calm difficulties in achieving consensus and increasing team decision-making effectiveness. Most of the studies on gender diversity have revealed that gender-diverse boards may enhance corporate performance (Fakoya & Nakeng, Citation2019; Gupta et al., Citation2014; Kagzi & Guha, Citation2018a; Kyaw et al., Citation2017; Li & Chen, Citation2018; Siciliano, Citation1996; Velte, Citation2016). Hafsi and Turgut (Citation2013) found that firms with more female directors tend to show greater interest in a broader range of stakeholders and positively impact the firm’s corporate governance and social responsibility performance. Similarly, Zhang (Citation2012) notes that gender-diverse boards positively increase institutional and social performance.

Cultural diversity is also an essential but relatively overlooked board attribute. Although more companies are reporting on gender diversity, the data shows that the actual membership of boards is more culturally diverse than gender diverse. According to the Refinitiv report (Citation2019), women accounted for about 18% of board memberships, while culturally diverse directors made up nearly 29% in 2017. Cultural diversity engenders information elaboration, bringing a diverse range of perspectives from the home countries of board members (Nederveen et al., Citation2013). It also leads to creative teamwork and effective leadership in companies and affects decision-making quality, benefiting from the different cultural backgrounds of board members (Maznevski, Citation1994; Schneider & De Meyer, Citation1991). Although cultural diversity plays a vital role in the contemporary business world, its effect on corporate governance and social performance has been undermined compared with its impact on firm performance. Thus, the literature on cultural diversity and social and governance performance is still in its infancy and is emerging as a sensitive topic, particularly in emerging markets (Zaid et al., Citation2020).

Given the limited evidence between the rising level of board diversity and corporate governance and social performance in emerging markets, the present study makes contributions to the literature by examining the effects of board gender and cultural diversity on two key dimensions of sustainability, i.e., corporate governance and social performance, rather than on financial angle, for a sample of non-financial companies listed in emerging markets. Focusing on emerging markets is essential because the implementation of governance and social practices is less relevant in these countries due to weak investor protection, gender discrimination, geographically proximate cultures, and institutional voids (Claessens & Yurtoglu, Citation2013). Companies in these markets also face more external and internal pressure and environmental challenges to increase their social and governance commitment, thus meeting stakeholders' expectations and improving corporate reputation (Geng et al., Citation2010). Thus, this study extends the discussion above for emerging markets by deepening the way to capturing the level of diversity and further assessing the nexus between board diversity and different dimensions of corporate sustainability to provide valuable insights for different interest groups. The research also aims to raise a flag about whether firms in emerging markets are forward-looking and committed to meeting corporate governance and social concerns by getting women and cultural-diverse board members to ensure expert guidance and oversight on sustainability matters. Thus, it becomes essential to understand whether conclusions drawn from experience in developed countries can be extended to emerging markets (Disli et al., Citation2022; Radhakrishnan et al., Citation2018). Finally, a deeper understanding of women directors’ role and cultural diversity in improving corporate governance and social performance will help companies and policymakers to ultimately improve corporate sustainable growth.

Drawing on a sample of 373 companies listed in 24 emerging markets from the Thomson Reuters database for the period 2010-2019, we carried out a multivariate panel data analysis and used governance and social pillar scores that are widely accepted in performance measurement (Ahi et al., Citation2018; Rajesh & Rajendran, Citation2020). Since the findings may often be influenced by the endogeneity problem, we also provided a profound analysis by performing a two-step system dynamic panel generalized method of moments (GMM). The results show that gender and cultural diversity positively influence corporate governance performance. We also note that social performance is positively associated with gender and cultural diversity, but this relationship is insignificant.

The remainder of the study is organized as follows. Section 2 reviews the literature and sets out the hypotheses. Section 3 presents the data and methodology. Section 4 discusses the results, and Section 5 concludes.

2. Literature review and hypotheses

2.1. Theoretical background

While a considerable number of studies have assessed the effect of board diversity on financial performance, relatively few have focused on the influence of board diversity on sustainability attributes. This work was based on the premises of several theoretical perspectives, ranging from agency theory (Jensen & Meckling, Citation1976; Mitnick, Citation1975; Ross, Citation1973), institutional theory (Mitnick, Citation1973), and cognitive diversity theory (Miller, Citation1990; Miller et al., Citation1998) to the stakeholder theory (Freeman, Citation1984; Freeman, Citation1999), resource-dependency theory (Penrose, Citation1959), and the resource-based view (Barney, Citation1991; Galbreath, Citation2016).

Among these theories, the most prominent is the stakeholder theory, which argues that a company's performance depends not only on the contributions of shareholders but also on the vital role played by government, consumers, community, environment, employees, media, and financial institutions. Thus, value creation is an outcome of the relationship between board members, shareholders, managers, and stakeholders (Freeman et al., Citation2004; Ranängen, Citation2017). Board members should balance each stakeholder’s expectations without compromising the needs of others (Haniffa & Cooke, Citation2002; Liao et al., Citation2015; Velte, Citation2016).

In a social framework, diversity refers to the various characteristics of complex communities based on the biological, cultural, and cognitive differences between individuals (Goodman, Citation1975; Miller, Citation1990; Miller et al., Citation1998; Nehring & Puppe, Citation2002), while in an organizational context, diversity is associated with the cultural and demographic characteristics of the board, managers, and workforce (Bernile et al., Citation2018; Coffey & Wang, Citation1998; Fakoya & Nakeng, Citation2019; Harjoto et al., Citation2018; Harjoto et al., Citation2019; Kagzi & Guha, Citation2018b; Li & Chen, Citation2018; Lin et al., Citation2018; Siciliano, Citation1996). Board members with different characteristics and backgrounds enable greater independence in decision-making, leading to an improvement in management quality (Adusei, Citation2019; Aggarwal et al., Citation2019; Harjoto et al., Citation2018; Ye et al., Citation2019). The resource-based view argues that board diversity creates synergies and helps solve complex problems (Galbreath, Citation2005), while resource dependence theory underlines the role that corporate boards play in managing uncertainty in the external environment and gaining access to critical resources (Hillman et al., Citation2009; Pfeffer & Salancik, Citation2003).

Diversity-based studies use two formal classifications: demographic (observable) and cognitive (non-observable). Gender, age, race, ethnicity, and language are observable, while knowledge, experience, culture, values, beliefs, and attitudes are cognitive attributes of diversity (Erdelyi, Citation1985; Jensen & Meckling, Citation1976; Lau & Murnighan, Citation1998; Miller et al., Citation1998; Pelled, Citation1996; Riordan, Citation2000; Riordan & Shore, Citation1997; Timmerman, Citation2000; Williams et al., Citation1988). Managing this heterogeneity is a complex task because such attributes can be connected, particularly the non-observable ones (Brush et al., Citation1987; Clark & Summers, Citation1981; Lau & Murnighan, Citation1998; Tsui & Gutek, Citation1999).

The academic debate on board diversity has generated different views. While some scholars treat diversity from a negative perspective, others assign a decisive role to it. The former base their arguments on potential conflict among team members, poor communication, and a lack of shared values (Abubakar, Citation2017; Buckley et al., Citation1978; Chapple & Humphrey, Citation2014; Churchill & Valenzuela, Citation2019; Churchill et al., Citation2017; Delis et al., Citation2017; Ferreira & Adams, Citation2007; Frijns et al., Citation2016; Kilic, Citation2015; Khaoula & Moez, Citation2019; Tarigan et al., Citation2018; Wellalage & Locke, Citation2013), while the latter argue that it makes a positive contribution to high financial performance (Alvarado et al., Citation2017; Campbell & Mínguez-Vera, Citation2008; Erhardt et al., Citation2003; Gupta et al., Citation2014; Miller & del Carmen Triana, Citation2009). The following section discusses both views and clarifies the role of diversity in non-financial performance. Appendix 1 provides a summary of selected studies linking board diversity with various firm-level outcomes.

2.2. Board diversity and non-financial performance

The institutional theory argues that society sways firm behavior (DiMaggio & Powell, Citation1983; Meyer & Rowan, Citation1977). According to Frynas and Yamahaki (Citation2016), a company’s institutional environment encompasses the social environment, the array of its activities, and its network of social relationships. Furthermore, the institutional theory asserts that a company's survival is contingent on its legitimacy derived from societal norms. Here, legitimacy is supported by resource dependence and the stakeholder theories that highlight the importance of resources (Milne & Patten, Citation2002; Sonpar et al., Citation2010). In this frame, cultural diversity plays a resource provisioning role and encourages companies to fulfill their social and governance obligations in ensuring their long-term commitment to internal and external stakeholders.

Pfeffer and Salancik (Citation1978) emphasize four benefits of boards to an organization: (i) advising and counseling; (ii) legitimacy and good reputation; (iii) communication channels between stakeholders and firm; and (iv) privileged access to or support from third parties. From this perspective, more diversified boards may positively affect corporate performance by contributing to decision-making (Buckley et al., Citation1978; Campbell & Mínguez-Vera, Citation2008; Carter et al., Citation2003; Churchill, Citation2019; Fidanoski et al., Citation2014; Low et al., Citation2015). Board members also use their social skills to interact directly with external sources. This may also lead to a competitive advantage in achieving prosperity and thus, increasing strategic flexibility (Adusei, Citation2019; Aggarwal et al., Citation2019; Harjoto et al., Citation2018; Wright, Citation1995; Ye et al., Citation2019).

Some studies have drawn attention to the potential nexus between board diversity and non-financial performance by concentrating on the cultivation of attitudes and beliefs and their positive effects on corporate governance and social performance (Al-Musali & Ku Ismail, Citation2015; Anderson et al., Citation2011; Ferreira, Citation2010; Ferreira & Adams, Citation2007; Frijns et al., Citation2016; Kim et al., Citation2013; Nederveen et al., Citation2013; Tarus & Aime, Citation2014). Zhang (Citation2012) highlights the point that board gender diversity is partially linked to social performance. In a recent study, Kagzi and Guha (Citation2018b) indicate that the board demographic diversity index positively influences corporate performance. Cook and Glass (Citation2015) argue that firms with more board diversity are more likely to implement non-discriminatory policies, leading to a more satisfied workforce.

From the standpoint of emerging markets, by examining a sample of Palestine companies from 2013 to 2018, Zaid et al. (Citation2020) noted that gender diversity and nationality had a positive but insignificant effect on corporate sustainability practices. Likewise, Naciti (Citation2019) assessed the effects of board diversity on social and environmental performance for 362 companies in 46 different countries by relying on the agency theory and stakeholder theory and found that both dimensions of sustainability performance are positively influenced by nationality and gender diversity. Khan et al. (Citation2019) revealed similar results for a sample of 86 Pakistani companies over the period of 2010–2017, concluding that nationality and gender diversity on board improves the quality of the CSR disclosure.

Hence, companies are expected to be more concerned with shaping the cognitive thinking of boards by diversifying them, thereby enhancing governance quality and promoting beneficial social practices.

2.2.1. Linking board cultural diversity with corporate governance and social performance

In contemporary management, cultural diversity is a key element of a supportive business environment for multinational enterprises. It reflects the presence of directors from different cultures on the board. As a form of comparatively unobservable social diversity, it can be a fundamental source of exclusive business practices blended with cultural differences. It may also facilitate effective policies. According to Dodd et al. (Citation2019), cultural diversity promotes individual achievement through the implementation of effective business practices. Ferrero-Ferrero et al. (Citation2015) claimed that a higher proportion of board members from different nationalities bring different perspectives and ideas due to their international experience, knowledge, diverse culture, professional background, language, religion, and life experiences. A similar approach is proposed by Lau et al. (Citation2016) on the relationship between nationality diversity and CSR for a sample of Chinese companies. Hence, culturally diverse board members and managers execute business strategies effectively with a clearer understanding of stakeholders’ expectations by reflecting different values and beliefs in the decision-making process and have a positive impact on engaging corporate sustainability activities (El-Bassiouny & El-Bassiouny, Citation2019; Maznevski, Citation1994; Nederveen et al., Citation2013; Schneider & De Meyer, Citation1991).

Board cultural diversity is also essential for creative teamwork. McLeod et al. (Citation1996) argue that groups, including members with different cultural fractions, produce more creative and feasible ideas than stereotypical groups with similar backgrounds. Butler (Citation2012) states that culturally diverse boards process information from different perspectives and encourage more inspiring group discussions. Similarly, in a recent study held on the US firms, Harjoto et al. (Citation2019) document that improving board nationality diversity may enrich CSR. Thus, from the perspectives of stakeholder and resource dependency theories, board cultural diversity may lead to more rational thinking and stimulate to take high-quality decisions (Zaid et al., Citation2020).

Cultural diversity is also associated with institutional theory (García, Citation1994; Kottak, Citation2015; Parekh, Citation2001) and the resource-based view (Barney, Citation1991; Galbreath, Citation2005). Culturally diverse boards generate more ideas and experiences using their members’ different resources (Shukeri et al., Citation2012). Thus, they guide the way employees behave in their responses to events in the surrounding environment and play an essential role in getting the required resources from external parties, i.e., suppliers, customers, and communities (Frijns et al., Citation2016). Hence, they offer heterogeneous human and social capital in the form of expertise, reputation, and experience (Hillman & Dalziel, Citation2003). Cai et al. (Citation2016) noted that country-level factors of the institutional framework and national culture rather than firm characteristics explain the variation in corporate social performance across firms. Similarly, Kang et al. (Citation2019) claimed that culturally diverse boards lead to different outcomes regarding a firm’s CSR involvement.

However, cultural diversity is a ‘double-edged sword’ (Milliken & Martins, Citation1996). Cognitive dissonance can arise between board members because they have different cultural characteristics, creating conflict, confusion, and a lack of understanding. It may then damage corporate performance (Anderson et al., Citation2011; Doney et al., Citation1998). Bjørnskov (Citation2008) claims that cultural diversity can also lead to a lower level of intragroup trust due to differences in norms and values. Despite these conflicting views, we adopt a positive stance toward the impact of board cultural diversity on corporate governance and social performance and propose the following two-part hypothesis:

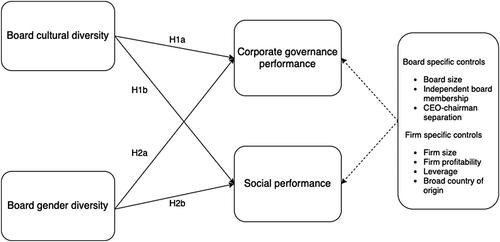

H1a: There is a positive association between board cultural diversity and corporate governance performance.

H1b: There is a positive association between board cultural diversity and social performance.

2.2.2. Linking board gender diversity with corporate governance and social performance

Gender diversity has become the most frequently used dimension of corporate governance in many countries because of the increasing global awareness of gender issues in terms of gender equality and diversity. Companies have recently made rapid progress in accomplishing higher gender presence on boards (Yarram & Adapa, Citation2021). Ashforth and Mael (Citation1989) demonstrate that gender-diverse boards facilitate social activities and pay closer attention than male-dominated ones to healthy working environments. Similarly, Siciliano (Citation1996) and Bear et al. (Citation2010) argued that a firm’s social performance is positively affected by gender diversity. This may be because women have distinct characteristics, i.e., they are cooperative, polite, and empathetic. Thus, in the framework of stakeholder theory, a greater female presence on a board facilitates discussions of a wider range of perspectives in meetings and leads to improved board performance. It also enhances monitoring and mitigates agency conflicts due to their socio-psychological and cognitive features (Adams & Ferreira, Citation2009).

Some scholars have postulated that the wider the gender diversity on board, the better the corporate performance (Adams & Ferreira, Citation2009; Hassan et al., Citation2016; Nguyen et al., Citation2015; Ruigrok et al., Citation2007). Arayssi et al. (Citation2016) suggest that female presence on board improves corporate performance and encourages investment in social engagement. Similarly, female directors also facilitate tasks that are qualitative in nature. In line with this, Ibrahim and Angelidis (Citation2011) find that female directors are more oriented toward CSR matters. They offer more contribution to decision-making on CSR issues (Burgess & Tharenou, Citation2002).

Kyaw et al. (Citation2017) observed the impact of board gender diversity on corporate social performance among 589 firms in Europe from 2002 to 2013. They concluded that gender diversity had a positive influence on environmental and social performance. Yarram and Adapa (Citation2021) investigated the link between gender diversity and CSR from the ethical and social dimensions for a sample of companies listed on the Australian Stock Exchange 300 Index by employing systems GMM. They indicated that companies with enhanced gender balance engage in more positive CSR activities and reduce controversial activities that hinder CSR. Lin et al. (Citation2018) investigated the association between gender diversity and charitable donations among 370 electronics companies in Taiwan between 2011 and 2013. They discovered that gender diversity was positively related to donations and corporate reputation. Velte (Citation2016) studied women's participation in management by using 1019 observations for the years 2010-2014 and concluded that female presence on board had a positive impact on sustainability performance. Hence, gender diversity plays an influential role in inducing managers to adhere to social and corporate governance norms. Thus, we propose the following two-part hypothesis:

H2a. There is a positive association between board gender diversity and corporate governance performance.

H2b. There is a positive association between board gender diversity and social performance.

Figure 1. Research framework.

Source: Authors.

3. Data and methodology

3.1. Sample selection

Our sample comprised non-financial companies listed in 24 emerging countries. We selected the countries according to the classification of the International Monetary Fund (www.imf.org). The sample covers panel data for a ten-year period (2010–2019). This was a decade characterized by stable economic conditions in the wake of the 2008–2009 global financial crisis. We obtained the data from Thomson Reuters DataStream. Thomson Reuters provides environmental, social, and governance (ESG) scores for three main categories and multiple associated sub-categories: environment (resource use, emission, and innovation), social (community, human rights, product responsibility, and workforce), and governance (management, shareholders, and corporate social responsibility strategy). We conducted an unbalanced panel data analysis. The sample covers 3281 observations from 373 companies.

3.2. Measurement of variables

We provide the measurements of the variables in the following subsections.

3.2.1. Dependent variables

We used two dependent variables, namely corporate governance and social performance. Corporate governance performance was measured by the governance pillar score (GPS), while social performance was measured by the social pillar score (SPS). Both GPS and SPS evaluate a company’s relative corporate governance and social performance, commitment, and effectiveness (Thomson Reuters, Citation2019).

According to Thomson Reuters’ definition (2019), GPS is an important measurement that shows the quality of a company’s systems and processes. It also reflects a firm’s capability, through best management practices, to control its rights and responsibilities by creating incentives to create enduring shareholder value.

The social pillar score measures a firm’s capability to maintain a supportive business culture based on trust and loyalty and best management practices for its workforce, customers, and society. It also highlights the importance of reputation and operational capacity in sustaining a firm’s ability to generate long-term shareholder value.

3.2.2. Independent variables

The independent variables are the board cultural diversity and board gender diversity. Board cultural diversity (BCD) is measured by the proportion of board members having a culturally diverse background from the location of the corporate headquarters. Board gender diversity (BGD) is measured by the ratio of females on the board.

3.2.3. Control variables

Consistent with previous studies, we used two sets of control variables, including board-specific (Aksoy et al., Citation2020; Ciftci et al., Citation2019; Disli et al., Citation2022; Kouaib et al., Citation2020; Naciti, Citation2019; Pathan & Faff, Citation2013) and firm-specific controls (Aksoy et al., Citation2020; Artiach et al., Citation2010; Ciftci et al., Citation2019; Disli et al., Citation2022; Gani & Jermias, Citation2006). The former included board size, independent board membership, and CEO − chairman separation, while the latter consisted of firm profitability, firm size, leverage, and broad country of origin. Board size, independent board membership, and firm size were normalized/scaled using natural logarithms suggested by Harjoto and Rossi (Citation2019), so they could be compared.

Board-specific controls

Board size (BS) was measured by the total number of board members at the end of the fiscal year. Independent board membership (IBM) was computed by the ratio of independent board members. CEO-chairman separation (CCS) was measured using a binary variable, where ‘1’ denoted whether the CEO also serves as a chairperson and ‘0’ otherwise.

Firm-specific controls

Firm profitability (ROA) was measured using the return on assets, i.e., net profits to total assets.

Firm size (SIZE) was computed as the natural logarithm of the total assets of the company.

Leverage (LEV) was computed by total liabilities divided by total assets.

Broad country of origin (ClusterID) is a categorical variable showing the country cluster groups for our sample companies based on their cultural similarities. Relying on the country clusters of the ‘Global Leadership and Organizational Behavior Effectiveness’ (GLOBE) project (House et al., Citation2004), we classified the companies in our sample into six clusters: Anglo, Latin America, Eastern Europe, Middle East, Confucian Asia, and Southern Asia. In recent years, the GLOBE project has provided new opportunities for studying the influence of culture on firms’ performance (Neculaesei et al., Citation2019, p. 44). displays the country of origin of the sample companies along with their corresponding broad country of origin based on the GLOBE country clusters. presents the definitions and measurements of all the variables used in this study.

Table 1. The sample.

Table 2. Definitions and measurement of the variables.

3.3. Data analysis and research models

To assess the effect of board cultural diversity and gender diversity on GPS and SPS, we conducted a panel regression analysis using Stata 15. We estimated the following models by using panel data techniques.

(1)

(1)

(2)

(2)

where GPS and SPS measure corporate governance and social performance, respectively; subscript i denotes ith firm (i = 1…373), and subscript t denotes tth year. To test the year effect, we inserted the level 1 variable year into the analysis. We also added the level 3 variable ClusterID to test the broad country of origin effect.

4. Empirical results

4.1. Descriptive analysis

shows the summary of descriptive statistics and correlation matrix. None of the pairwise correlations have coefficients above 0.48, suggesting no severe multicollinearity problems for our regression models. It should be noted that while some researchers use correlation coefficient cutoffs of 0.5 and above (Donath et al., Citation2012), the most typical cutoff is 0.80 (Berry & Feldman, Citation1985) for multicollinearity diagnostic. The variance inflation factor (VIF) test was also carried out to confirm the non-existence of multicollinearity. displays the VIF scores. The VIF scores were far less than the threshold value of 10, indicating that multicollinearity was not a severe issue.

Table 3. Descriptive statistics and correlation matrix.

Table 4. Variance inflation factors (VIF).

Normality tests were also conducted using the Skewness/Kurtosis test. The test results, presented in Appendix 2, reveal the non-normality of the variables (p < 0.05). However, it should be noted that our data set is relatively large, including more than 3,000 observations. Thus, non-normality does not pose a severe threat (McClave, Citation2008).

4.2. Estimation results

Prior to testing our hypotheses via panel data analysis, we first conducted the fixed effects model and F-test to check if there were any firm-specific characteristics. We rejected the null hypothesis and determined that the fixed effect model was better than the other models. Then, we ran the Hausman test and concluded that the fixed effects model was superior to the random effects model. Thus, there was evidence of significant differences across the sample companies.

We then tested whether the assumptions of the regression model were violated. The modified Wald test was used for heteroscedasticity, while Durbin-Watson (DW) and the Baltagi-Wu (LBI) tests were applied for autocorrelation. Pesaran’s (Citation2004) cross-sectional dependence test was also used. The results indicated that the panel exhibited cross-sectional dependence and heteroscedasticity. Therefore, we also estimated a model with Driscoll-Kraay standard errors (Driscoll & Kraay, Citation1998).

presents the results of the panel data regression model with fixed effects (standard and Driscoll-Kraay methods) and mixed effects (REML model). The sign on the coefficient of BCD was positive and significant (p < 0.05) for GPS but not significant on SPS, which provided support for H1a, confirming that board cultural diversity was positively related to corporate governance performance. A culturally diverse board may help a company better understand other groups’ sentiments, as suggested by Raineri (Citation2018). However, no support was found for H1b, as there was no significant relationship between BCD and SPS (p > 0.05) within the context of emerging markets. In this regard, board cultural diversity does not have enough power in improving social performance. The finding (which is in line with Kotmom et al. [Citation2019]) may be explained partly by the fact that multiculturalism is still at a nascent stage in emerging markets; this, in turn, is due to the relatively slow pace of globalization and the low scale of immigration compared with developed countries. Thus, it will take time for board members from different cultures to work effectively in these markets.

Table 5. Results of panel data analysis.

The sign on the coefficient of BGD was positive on both GPS and SPS but significant only on GPS (p < 0.01), considering both fixed and mixed effects. This finding provides support for H2a. In other words, the greater the board gender diversity, the better the corporate governance. These results support resource dependence theory and align with previous studies (Arayssi et al., Citation2016; Bruna et al., Citation2020; Hafsi & Turgut, Citation2013; Low et al., Citation2015; Wasiuzzaman & Wan Mohammad, Citation2020; Yarram & Adapa, Citation2021; Yasser et al., Citation2017). They corroborate the view that female board members tend to introduce novel perspectives on how corporate governance quality can be improved. No support was found for H2b, as the BGD has a positive but insignificant effect on SPS. This finding is not particularly surprising. Female presence on board is a relatively recent phenomenon in many emerging markets. Thus, female board membership may not send a strong signal to stakeholders that the firm pays attention to social activities (Carpes Dani et al., Citation2019).

Of the board-specific control variables, we found a positive effect of IBM on both GPS and SPS but significant only on GPS (p < 0.01), considering both fixed and mixed effects. There is obviously an increasing tendency among companies in emerging markets to appoint independent board members who may contribute to the decision-making process, particularly on sustainability-related matters. The positive influence of IBM on corporate governance and social performance was consistent with prior studies (Arayssi et al., Citation2020; Beji et al., Citation2021; Husted & de Sousa-Filho, Citation2017; Ortas et al., Citation2017). Contrary to the widely held assumption, we found negative and significant (p < 0.05) effects of BS on GPS, which is in line with previous studies (de Andres et al., Citation2005; Ghosh, Citation2006; Mak & Yuanto, 2001).

Of the firm-specific control variables, ROA, SIZE, and LEV were found to be significant (p < 0.05). ROA was negatively, and SIZE was positively associated with GPS and SPS. The finding that LEV was positively associated with GPS, though negatively related to SPS, was interesting. These results imply that high-performing companies prefer to focus on improving financial performance at the expense of social performance (Beji et al., Citation2021; Siregar & Bachtiar, Citation2010). Also, large companies have better corporate governance and social performance since they are more visible and more exposed to pressure from other social groups.

Finally, we also attempted to explore the broad country of origin and the year effects by running hierarchical linear modeling (HLM). Since the number of country clusters was relatively small, we used the restricted maximum likelihood (REML) approach consistent with the earlier studies (e.g., Hair & Fávero, Citation2019; Hayes, Citation2006; McNeish & Stapleton, Citation2016). The model’s highest level included a broad country of origin, which consisted of a total of six country clusters. Hence, a three levels model was adequate. This included country clusters at level 3, companies at level 2, and years at level 1. The results of the multivariate HLM analyses are provided in .

shows the intraclass correlation (ICC) values. These denote the extent of variation unexplained by any predictors in the model that can be attributed to the grouping variable compared with the overall unexplained variance (within and between variance). The correlation between GPSs was equal to 3.58 percent (rhocluster) for the same cluster. In comparison, the correlation between GPSs was equal to 87.34 percent (rhofirm|cluster) for the same firm of a particular cluster. The correlation between SPSs was equal to 14.55 percent (rhocluster) for the same cluster, while the correlation between SPSs was equal to 93.65 percent (rhofirm|cluster) for the same firm of a particular cluster. These correlation values, in general, tended to indicate that GPS was associated more with the broad country of origin than was SPS. In addition, the results of the mixed model in tend to confirm the results of the fixed-effect models.

Table 6. Tests of strict exogeneity.

4.3. Addressing the endogeneity problem

The static fixed effect model may not have been strong enough in the presence of a dynamic relationship between BCD or BGD and GPS or SPS. Therefore, we re-examine the relationships between board attributes and GPS and SPS using the GMM estimator. Following Wintoki et al. (Citation2012), two diagnostic tests were employed before using GMM estimation.

First, a test of strict exogeneity suggested by Wooldridge (Citation2010) was applied to identify the exogeneity among the variables, which is given in the following equation:

(3)

(3)

Where ‘Zit+1’ represents the future values (the values of the next year) of the independent variables (BCD, BGD) and ‘Ωit+1’ are the subset of future values of control variables (BS, IBM, ROA, SIZE, and LEV).

shows the Wooldridge strict exogeneity test results. The coefficient estimates for the future values of IBMt+1 and ROAt+1 is significantly different from zero for GPS. The coefficient estimates for the future values of BGDt+1, IBMt+1, ROAt+1, and SIZEt+1 is also significantly different from zero for SPS. This suggests that neither of these variables is strictly exogenous. An F-test of the joint influence of the coefficient estimates of all the future values is also significant. The Wooldridge strict exogeneity test results show high endogeneity in the models by denying Wooldridge’s null hypothesis.

Second, static and dynamic OLS models are given in EquationEquations (4)(4)

(4) and Equation(5)

(5)

(5) , respectively.

(4)

(4)

(5)

(5)

Where ‘i’ indicates the company under observation and ‘t’ denotes time, ‘Xit’ shows the independent variables (BCD and BGD), Ωit is a vector of control variables (BS, IBM, CCS, ROA, SIZE, and LEV), uit’ indicates the time-invariant unobserved effect of an individual firm and ‘eit’ shows random error term.

The dynamic model in EquationEquation (5)(5)

(5) is formulated by including the lagged dependent variable (GPSit-1, SPSit-1) as an independent variable to EquationEquation (4)

(4)

(4) to identify if the lagged dependent variable also acts as a regressor.

When the dynamic OLS model is employed, the adjusted R2 increases significantly (see ), reflecting the existence of reverse causality in the model (Wintoki et al., Citation2012). Moreover, indicates that the estimated coefficient (0.847) of lagged GPS is statistically significant (p < 0.01), specifying that past GPS significantly explains variations in current GPS. Similarly, the estimated coefficient (0.928) of lagged SPS is statistically significant (p < 0.01), indicating that past SPS may explain variations in current SPS. These results tend to confirm the existence of dynamic relationships between the independent (BCD and BGD) and dependent variables (GPS and SPS).

Table 7. Results of GMM modeling.

Thus, regression results for dynamic models may be subject to endogeneity biases, and a simple fixed effect model may not be suitable for this kind of relationship, leading to biased results (Nguyen et al., Citation2014). After attesting the endogeneity and the dynamic nature of the relationships among the variables, the following GMM EquationEquations (6(6)

(6) and Equation7)

(7)

(7) are employed.

(6)

(6)

(7)

(7)

Where ‘u’ denotes un-observed firm-specific effects and ‘e’ represents the error term in the dynamic model.

Blundell and Bond (Citation1998) two-step system (generalized method of moment [GMM]) is adopted as the most suitable method for coping with the endogeneity problems which may have been caused by the dynamic nature of our model (see Antoniou et al., Citation2008; Nadeem et al., Citation2017; Nguyen et al., Citation2014). Moreover, the GMM system is particularly developed to handle panel data, including large numbers of companies and shorter time periods (as was the case herein; Nadeem et al., Citation2017: 880). We applied the two-step GMM system with Windmeijer's (Citation2005) correction. In line with Wintoki et al. (Citation2012), year dummies and cluster dummies were assumed to be exogenous. The other independent and control variables were treated as endogenous.

We then conducted several tests for GMM instrument validation. These tests involved (i) the Arellano-Bond test for autocorrelation and (ii) the Hansen test of over identifying restrictions. displays the results of the GMM model (Hansen et al., Citation1982). The GMM specifications were well specified and based on the Hansen test of overidentifying restrictions (p > 0.1) and the Arellano-Bond test (Arellano-Bond AR(1) p < 0.01, Arellano-Bond AR(2) p > 0.1) of autocorrelation.

As shown in , the one- and two-year lagged GPS, and one-year lagged SPS coefficients were found to be positive and significant (p < 0.01). This implies that the preceding GPS and SPS values had significant effects on current GPS and SPS values. The signs on the coefficients of BCD, BGD, and IBM were positive and significant (p < 0.05) in Model 1 but not significant in Model 2.

The GMM coefficient estimates of BCD and BGD for GPS fully corroborate the estimates of both fixed and mixed effects in . On the other hand, the GMM results fail to confirm the existence of the significant relationships between the firm-specific controls of ROA, SIZE, LEV, and the dependent variables of GPS and SPS. This finding is not particularly surprising, as the dynamic endogeneity and/or simultaneity can produce a bias in the parameter estimates of fixed-effects panel models (Garcia-Castro et al., Citation2010; Li et al., Citation2021; Schultz et al., Citation2010; Surroca et al., Citation2010; Wagner & Blom, Citation2011). The presence of a dynamic relationship may also cause any fixed effects estimator to overestimate the key coefficient (Li et al., Citation2021). Hence, we suggest that the relationship between BGD and SPS or the relationship between GPS or SPS and control variables (ROA, SIZE, and LEV) may simply be spurious.

presents the summary of the hypotheses, along with the level of support for each.

Table 8. Summary of the hypotheses.

5. Discussions and implications

Companies often attempt to integrate global governance and social standards into their operations and decision-making processes to foster sustainable practices and improve corporate performance. In this respect, policy makers, managers, and investors increasingly demand accurate evaluations for sustainability pillars scores.

The present study offers several insights at the emerging country level by focusing on companies’ corporate governance and social engagement and showing how they were impacted by board diversity. We particularly focused on the effects of cultural and gender diversity on corporate governance and social performance among 373 companies across 24 countries during the period 2010-2019. The results indicated that board gender and cultural diversity were positively and significantly associated with corporate governance performance. In contrast, no significant relationship was identified with respect to the effect on social performance in emerging markets. Female presence on board improves corporate governance performance. Female directors bring different leadership skills to the table, and they are more flexible in their views. This facilitates more open discussion, reduces groupthink, and improves relations between board members and employees. The workforce is then more productive, and the company’s reputation is enhanced. Women directors also mitigate agency problems and boost the board’s monitoring abilities; thus, the firm’s sustainable growth is also enhanced, supporting agency theory and resource dependence theory. Hence, companies should consider increasing gender diversity voluntarily rather than waiting for a mandate from regulators. These results corroborate the findings of the previous studies (Disli et al., Citation2022; Lenard et al., Citation2014; Wahid, Citation2019), confirming that female directors promote high-quality governance practice.

Similarly, board cultural diversity is equally important. It allows different voices to be heard and contrasting insights to be integrated, and corporate governance becomes less subject to tokenism. Thus, board cultural diversity boosts a company’s ability to satisfy the needs of broader groups of stakeholders and improve its competitiveness, holding up the stakeholder and resource dependence theory. However, the positive effect of cultural diversity on corporate governance is not straightforward. The relevance of cultural-diverse directors' knowledge and experience to the firms' needs is the key to making cultural diversity an asset for companies. Further, using the potential of cultural diversity may require dealing with its disruptive consequences and incorporating initiatives that improve communication and promote group integration on boards. This finding is in line with the previous studies on the relationship between culture and corporate sustainability performance (Jian et al., Citation2017; Ringov & Zollo, Citation2007). Companies operating in emerging countries should wisely design cultural diversity on board to enhance governance performance.

To sum up, the enhanced gender and cultural diversity lead to improved behavioral incorporation of the various interests on board. Thus, a critical mass of female directors and culturally diversified board members is recommended for companies in emerging markets to positively influence corporate governance performance. Although firms in developed countries show, on average, a better governance performance than firms located in emerging countries (Martinez et al., Citation2022), given the differences in economic development, cultural background, legal and institutional environment, it is important to note that conclusions drawn from experience in developed countries will carry over to emerging markets in the long run.

5.1. Implications of the study

The present study offers a greater understanding of the management of companies in emerging markets related to the functioning of boards and the resource view perspective in optimizing corporate governance and social performance. The results show the presence of sustainable behavior in corporate governance but not in social performance in most of the emerging countries. Though the companies in different country clusters may have been dissimilar in terms of governance and social practices, they invariably carried out policies to create a healthy corporate governance environment to meet their goals. However, companies should further concentrate on the role of cultural diversity in corporate governance and social performance since improvements, particularly in board cultural diversity, may have greater positive influence on sustainability performance.

The study also suggests that improved corporate performance in emerging markets is closely correlated to the presence of females and members from different cultural backgrounds on company boards. Thus, owners, managers, and boards of directors can use this information in practice to enhance their companies’ reputation and competitiveness by improving the gender balance and cultural diversity on board. Furthermore, companies should accommodate independent board members as part of the governance framework. Such actions will help to improve corporate governance and social performance, leading to high levels of sustainability and better financial performance. Board members are responsible for the smooth running of companies and are usually held accountable for corporate performance, so their composition is a matter of paramount importance.

Finally, regulatory authorities and policymakers in emerging markets may use the findings of this study to revise their policies in improving diversity and equality on board. They should introduce more female members and encourage parties from around the world to join the boards.

5.2. Limitations and future research

We recognize that the present study has some limitations. We did not account for every aspect of diversity (e.g., education, age, and international affiliation). Future researchers could introduce additional variables to address this shortcoming. We also employed only two out of the thirteen Thomson Reuter’s ESG scores to run our analysis. The remaining scores could also be incorporated to show their interaction with cultural and gender diversity. Although we obtained some partial evidence regarding the effect of a broad country of origin on corporate governance performance, a new research framework with new data is definitely required to investigate the distinctions between emerging and developed countries by incorporating some country-level characteristics, including legal differences.

Disclosure statement

No potential conflict of interest was reported by the authors.

References

- Abubakar, A. (2017). Corporate board diversity and financial performance: Evidence from quoted deposit money banks in Nigeria, Al-Muqaddimah. Journal of Humanities, Law, Social & Management Sciences, 1(1), 20–47.

- Achim, M. V., Borlea, S. N., & Mare, C. (2015). Corporate governance and business performance: Evidence for the Romanian economy. Journal of Business Economics and Management, 17(3), 458–474. https://doi.org/10.3846/16111699.2013.834841

- Adams, R. B., & Ferreira, D. (2009). Women in the boardroom and their impact on governance and performance. Journal of Financial Economics, 94(2), 291–309. https://doi.org/10.1016/j.jfineco.2008.10.007

- Adusei, M. (2019). Board gender diversity and the technical efficiency of microfinance institutions: Does size matter? International Review of Economics & Finance, 64, 393–411. https://doi.org/10.1016/j.iref.2019.07.008

- Aggarwal, R., Jindal, V., & Seth, R. (2019). Board diversity and firm performance: The role of business group affiliation. International Business Review, 28(6), 101600–101617. https://doi.org/10.1016/j.ibusrev.2019.101600

- Ahi, P., Searcy, C., & Jaber, M. Y. (2018). A probabilistic weighting model for setting priorities in assessing sustainability performance. Sustainable Production and Consumption, 13, 80–92. https://doi.org/10.1016/j.spc.2017.07.007

- Aksoy, M., Yilmaz, M. K., Tatoglu, E., & Basar, M. (2020). Antecedents of corporate sustainability performance in Turkey: The effects of ownership structure and board attributes on non-financial companies. Journal of Cleaner Production, 276, 124284.

- Al-Musali, M., & Ku Ismail, K. N. I. (2015). Board diversity and intellectual capital performance: The moderating role of the effectiveness of board meetings. Accounting Research Journal, 28(3), 268–283. https://doi.org/10.1108/ARJ-01-2014-0006

- Alvarado, N. R., Fuentes, P., & Laffarga, J. (2017). Does board gender diversity influence financial performance? Evidence from Spain. Journal of Business Ethics, 141(2), 337–350. https://doi.org/10.1007/s10551-015-2735-9

- Anderson, R. C., Reeb, D. M., Upadhyay, A., & Zhao, W. (2011). The economics of director heterogeneity. Financial Management, 40(1), 5–38. https://doi.org/10.1111/j.1755-053X.2010.01133.x

- Antoniou, A., Guney, Y., & Paudyal, K. (2008). The determinants of capital structure: Capital market-oriented versus bank-oriented institutions. Journal of Financial and Quantitative Analysis, 43(1), 59–92. https://doi.org/10.1017/S0022109000002751

- Arayssi, M., Dah, M., & Jizi, M. (2016). Women on boards, sustainability reporting and firm performance. Sustainability Accounting, Management and Policy Journal, 7(3), 376–401. https://doi.org/10.1108/SAMPJ-07-2015-0055

- Arayssi, M., Jizi, M., & Tabaja, H. H. (2020). The impact of board composition on the level of ESG disclosures in GCC countries. Sustainability Accounting, Management and Policy Journal, 11(1), 137–161. https://doi.org/10.1108/SAMPJ-05-2018-0136

- Arellano, M., & Bond, S. (1991). Some tests of specification for panel data: Monte Carlo evidence and an application to employment equations. The Review of Economic Studies, 58(2), 277–297. https://doi.org/10.2307/2297968

- Artiach, T., Lee, D., Nelson, D., & Walker, J. (2010). The determinants of corporate sustainability performance. Accounting & Finance, 50(1), 31–51. https://doi.org/10.1111/j.1467-629X.2009.00315.x

- Ashforth, B. E., & Mael, F. (1989). Social identity theory and the organization. Academy of Management Review, 14(1), 20–39. https://doi.org/10.5465/amr.1989.4278999

- Barney, J. (1991). Firm resources and sustained competitive advantage. Journal of Management, 17(1), 99–120. https://doi.org/10.1177/014920639101700108

- Bear, S., Rahman, N., & Post, C. (2010). The impact of board diversity and gender composition on corporate social responsibility and firm reputation. Journal of Business Ethics, 97(2), 207–221. https://doi.org/10.1007/s10551-010-0505-2

- Beji, R., Yousfi, O., Loukil, N., & Omri, A. (2021). Board diversity and corporate social responsibility: Empirical evidence from France. Journal of Business Ethics, 173(1), 133–155. https://doi.org/10.1007/s10551-020-04522-4

- Bernile, G., Bhagwat, V., & Yonker, S. (2018). Board diversity, firm risk, and corporate policies. Journal of Financial Economics, 127(3), 588–612. https://doi.org/10.1016/j.jfineco.2017.12.009

- Berry, W. D., & Feldman, S. (1985). Multiple regression in practice (quantitative applications in the social sciences). SAGE Publications.

- Bjørnskov, C. (2008). Social trust and fractionalization: A possible reinterpretation. European Sociological Review, 24(3), 271–283.

- Blundell, R., & Bond, S. (1998). Initial conditions and moment restrictions in dynamic panel data models. Journal of Econometrics, 87(1), 115–143. https://doi.org/10.1016/S0304-4076(98)00009-8

- Borlea, S. N., Achim, M. V., & Mare, C. (2017). Board characteristics and firm performances in emerging economies. Lessons from Romania. Economic Research-Ekonomska Istraživanja, 30(1), 55–75. https://doi.org/10.1080/1331677X.2017.1291359

- Bruna, M. G., Đặng, R., Ammari, A., & Houanti, L. (2020). The effect of board gender diversity on corporate social performance: An instrumental variable quantile regression approach. Financial Research Letters, 40, 101734.

- Brush, D. H., Moch, M. K., & Pooyan, A. (1987). Individual demographic differences and job satisfaction. Journal of Organizational Behavior, 8(2), 139–155. https://doi.org/10.1002/job.4030080205

- Buckley, P. J., Dunning, J. H., & Pearce, R. D. (1978). The influence of firm size, industry, nationality, and degree of multinationality on the growth and profitability of the World’s largest firms, 1962-1972. Review of World Economics, 114(2), 243–257. https://doi.org/10.1007/BF02696473

- Burgess, Z., & Tharenou, P. (2002). Women board directors: Characteristics of the few. Journal of Business Ethics, 37(1), 39–49. https://doi.org/10.1023/A:1014726001155

- Butler, S. R. (2012). All on board! Strategies for constructing diverse boards of directors. Virginia Law & Business Review, 7, 61–96.

- Cai, Y., Pan, C. H., & Statman, M. (2016). Why do countries matter so much in corporate social performance? Journal of Corporate Finance, 41, 591–609. https://doi.org/10.1016/j.jcorpfin.2016.09.004

- Campbell, K., & Mínguez-Vera, A. (2008). Gender diversity in the boardroom and firm financial performance. Journal of Business Ethics, 83(3), 435–451. https://doi.org/10.1007/s10551-007-9630-y

- Carter, D. A., Simkins, B. J., & Simpson, W. G. (2003). Corporate governance, board diversity, and firm value. The Financial Review, 38(1), 33–53. https://doi.org/10.1111/1540-6288.00034

- Chapple, L., & Humphrey, J. E. (2014). Does board gender diversity have a financial impact? Evidence using stock portfolio performance. Journal of Business Ethics, 122(4), 709–723. https://doi.org/10.1007/s10551-013-1785-0

- Churchill, A. S., Valenzuela, M. R., & Sablah, W. (2017). Ethnic diversity and firm performance: Evidence from China’s materials and industrial sectors. Empirical Economics, 53(4), 1711–1731. https://doi.org/10.1007/s00181-016-1174-5

- Churchill, S. A. (2019). Firm financial performance in Sub-Saharan Africa: The role of ethnic diversity. Empirical Economics, 57(3), 957–970.

- Churchill, S. A., & Valenzuela, M. R. (2019). Determinants of firm performance: Does ethnic diversity matter? Empirical Economics, 57(6), 2079–2105.

- Ciftci, I., Tatoglu, E., Wood, G., Demirbag, M., & Zaim, S. (2019). Corporate governance and firm performance in emerging markets: Evidence from Turkey. International Business Review, 28(1), 90–103. https://doi.org/10.1016/j.ibusrev.2018.08.004

- Claessens, S., & Yurtoglu, B. B. (2013). Corporate governance in emerging markets: A survey. Emerging Markets Review, 15, 1–33. https://doi.org/10.1016/j.ememar.2012.03.002

- Clark, K. B., & Summers, L. H. (1981). Demographic differences in cyclical employment variation. The Journal of Human Resources, 16(1), 61–69. https://doi.org/10.2307/145219

- Coffey, B. S., & Wang, J. (1998). Board diversity and managerial control as predictors of corporate social performance. Journal of Business Ethics, 17(14), 1595–1603. https://doi.org/10.1023/A:1005748230228

- Cook, A., & Glass, C. (2015). The power of one or power in numbers? Analyzing the effect of minority leaders on diversity policy and practice. Work and Occupations, 42(2), 183–215. https://doi.org/10.1177/0730888414557292

- Carpes Dani, A. C., Picolo, J. D., & Klann, R. C. (2019). Gender influence, social responsibility and governance in performance. RAUSP Management Journal, 54(2), 154–177. https://doi.org/10.1108/RAUSP-07-2018-0041

- de Andres, P. A., Azofra, V., & Lopez, F. (2005). Corporate boards in some OECD countries: Size, composition, functioning and effectiveness. Corporate Governance, 13(2), 197–210. https://doi.org/10.1111/j.1467-8683.2005.00418.x

- Delis, M. D., Gaganis, C., Hasan, I., & Pasiouras, F. (2017). The effect of board directors from countries with different genetic diversity levels on corporate performance. Management Science, 63(1), 231–249. https://doi.org/10.1287/mnsc.2015.2299

- DiMaggio, P. J., & Powell, W. W. (1983). The iron cage revisited: Institutional isomorphism and collective rationality in organizational fields. American Sociological Review, 48(2), 147–160. https://doi.org/10.2307/2095101

- Disli, M., Yilmaz, M. K., & Mohamed, F. F. M. (2022). Board characteristics and sustainability performance: Empirical evidence from emerging markets. Sustainability Accounting, Management and Policy Journal, 13(4), 929–952. https://doi.org/10.1108/SAMPJ-09-2020-0313

- Dodd, O., Frijns, B., & Garel, A. (2019). Cultural diversity in the boardroom and corporate social performance. Available at SSRN: https://ssrn.com/abstract=3389707

- Donath, C., Gräßel, E., Baier, D., Pfeiffer, C., Bleich, S., & Hillemacher, T. (2012). Predictors of binge drinking in adolescents: Ultimate and distal factors – a representative study. BMC Public Health, 12(1), 263. https://doi.org/10.1186/1471-2458-12-263

- Doney, P. M., Cannon, J. P., & Mullen, M. R. (1998). Understanding the influence of national culture on the development of trust. Academy of Management Review, 23(3), 601–620. https://doi.org/10.5465/amr.1998.926629

- Driscoll, J., & Kraay, A. (1998). Consistent covariance matrix estimation with spatially dependent panel data. Review of Economics and Statistics, 80(4), 549–560. https://doi.org/10.1162/003465398557825

- El-Bassiouny, D., & El-Bassiouny, N. (2019). Diversity, corporate governance and CSR reporting: A comparative analysis between top-listed firms in Egypt, Germany and the USA. Management of Environmental Quality: An International Journal, 30(1), 116–136. https://doi.org/10.1108/MEQ-12-2017-0150

- Erdelyi, M. H. (1985). Psychoanalysis: Freud's cognitive psychology. WH Freeman/Times Books/Henry Holt & Co.

- Erhardt, N. L., Werbel, J. D., & Shrader, C. B. (2003). Board of director diversity and firm financial performance. Corporate Governance: An International Review, 11(2), 102–111. https://doi.org/10.1111/1467-8683.00011

- Fakoya, M. B., & Nakeng, M. V. (2019). Board characteristics and sustainable energy performance of selected companies in South Africa. Sustainable Production and Consumption, 18, 190–199. https://doi.org/10.1016/j.spc.2019.02.003

- Fatemi, A., Glaum, M., & Kaiser, S. (2018). ESG performance and firm value: The moderating role of disclosure. Global Finance Journal, 38(1), 45–64. https://doi.org/10.1016/j.gfj.2017.03.001

- Ferreira, D. (2010). Board diversity. In Anderson, R., Baker, H.K. (Eds.), Corporate governance: A synthesis of theory research, and practice, (pp. 225–242). John Wiley & Sons.

- Ferreira, D., & Adams, R. B. (2007). A theory of friendly boards. The Journal of Finance, 62(1), 217–250. https://doi.org/10.1111/j.1540-6261.2007.01206.x

- Ferrero-Ferrero, I., Fernández-Izquierdo, M. Á., & Muñoz-Torres, M. J. (2015). Integrating sustainability into corporate governance: An empirical study on board diversity. Corporate Social Responsibility and Environmental Management, 22(4), 193–207. https://doi.org/10.1002/csr.1333

- Fidanoski, F., Simeonovski, K., & Mateska, V. (2014). The impact of board diversity on corporate performance: New evidence from Southeast Europe. In Corporate governance in the US and global settings, (Advances in Financial Economics, Vol. 17, pp. 81–123). Bingley: Emerald Group Publishing Limited. https://doi.org/10.1108/S1569-373220140000017003

- Freeman, R. E. (1984). Strategic management: A stakeholder approach. Cambridge University Press.

- Freeman, R. E. (1999). Divergent stakeholder theory. Academy of Management Review, 24(2), 233–236.

- Freeman, R. E., Wicks, A. C., & Parmar, B. (2004). Stakeholder theory and the corporate objective revisited. Organization Science, 15(3), 364–369. https://doi.org/10.1287/orsc.1040.0066

- Friede, G., Busch, T., & Bassen, A. (2015). ESG and financial performance: Aggregated evidence from more than 2000 empirical studies. Journal of Sustainable Finance & Investment, 5(4), 210–233. https://doi.org/10.1080/20430795.2015.1118917

- Frijns, B., Dodd, O., & Cimerova, H. (2016). The impact of cultural diversity in corporate boards on firm performance. Journal of Corporate Finance, 41, 521–541. https://doi.org/10.1016/j.jcorpfin.2016.07.014

- Frynas, G., & Yamahaki, C. (2016). Corporate social responsibility: Review and roadmap of theoretical perspectives. Business Ethics: A European Review, 25(3), 258–285. https://doi.org/10.1111/beer.12115

- Galbreath, J. (2005). Which resources matter the most to firm success? An exploratory study of resource-based theory. Technovation, 25(9), 979–987. https://doi.org/10.1016/j.technovation.2004.02.008

- Galbreath, J. (2016). When do board and management resources complement each other? A study of effects on corporate social responsibility. Journal of Business Ethics, 136(2), 281–292. https://doi.org/10.1007/s10551-014-2519-7

- Gani, L., & Jermias, J. (2006). Investigating the effect of board independence on performance across different strategies. The International Journal of Accounting, 41(3), 295–314. https://doi.org/10.1016/j.intacc.2006.07.009

- Garcia-Castro, R., Ariño, M. A., & Canela, M. A. (2010). Does social performance really lead to financial performance? Accounting for endogeneity. Journal of Business Ethics, 92(1), 107–126. https://doi.org/10.1007/s10551-009-0143-8

- García, E. E. (1994). Understanding and meeting the challenge of student cultural diversity. Houghton Mifflin.

- Geng, Y., Xinbei, W., Qinghua, Z., & Hengxin, Z. (2010). Regional initiatives on promoting cleaner production in China: A case of Liaoning. Journal of Cleaner Production, 15, 1502–1508.

- Ghosh, S. (2006). Do board characteristics affect corporate performance? Firm-level evidence for India. Applied Economics Letters, 13(7), 435–443. https://doi.org/10.1080/13504850500398617

- GLOBE. (2020). Global leadership and organizational behavior effectiveness. https://globeproject.com/.

- Goodman, D. (1975). The theory of diversity-stability relationships in ecology. The Quarterly Review of Biology, 50(3), 237–266. https://doi.org/10.1086/408563

- Griffin, D., Li, K., & Xu, T. (2021). Board gender diversity and corporate innovation: International evidence. Journal of Financial and Quantitative Analysis, 56(1), 123–154. https://doi.org/10.1017/S002210901900098X

- Gupta, P. P., Lam, K. C., Sami, H., & Zhou, H. (2014). Board diversity and its long-term effect on firm financial and non-financial performance. SSRN Electronic Journal. http://dx.doi.org/10.2139/ssrn.2531212

- Hafsi, T., & Turgut, G. (2013). Boardroom diversity and its effect on social performance: Conceptualization and empirical evidence. Journal of Business Ethics, 112(3), 463–479. https://doi.org/10.1007/s10551-012-1272-z

- Hair, J. F., Jr,., & Fávero, L. P. (2019). Multilevel modeling for longitudinal data: Concepts and applications. RAUSP Management Journal, 54(4), 459–489. https://doi.org/10.1108/RAUSP-04-2019-0059

- Haniffa, R. M., & Cooke, T. E. (2002). Culture, corporate governance and disclosure in Malaysian corporations. Abacus, 38(3), 317–349. https://doi.org/10.1111/1467-6281.00112

- Hansen, L. P. (1982). Large sample properties of the generalized methods of moments. Econometrica, 50(4), 1029–1054. https://doi.org/10.2307/1912775

- Harjoto, M. A., & Rossi, F. (2019). Religiosity, female directors, and corporate social responsibility for Italian listed companies. Journal of Business Research, 95, 338–346. https://doi.org/10.1016/j.jbusres.2018.08.013

- Harjoto, M. A., Laksmana, I., & Yang, Y. W. (2018). Board diversity and corporate investment oversight. Journal of Business Research, 90, 40–47. https://doi.org/10.1016/j.jbusres.2018.04.033

- Harjoto, M. A., Laksmana, I., & Yang, Y. W. (2019). Board nationality and educational background diversity and corporate social performance. Corporate Governance: The International Journal of Business in Society, 19(2), 217–239. https://doi.org/10.1108/CG-04-2018-0138

- Hassan, R., Marimuthu, M., & Kaur Johl, S. (2016). Women on boards and market performance: An exploratory study on the listed companies. International Business Management, 10(2), 84–91.

- Hayes, A. F. (2006). A primer on multilevel modeling. Human Communication Research, 32(4), 385–410. https://doi.org/10.1111/j.1468-2958.2006.00281.x

- Hillman, A. J., & Dalziel, T. (2003). Boards of directors and firm performance: Integrating agency and resource dependence perspectives. The Academy of Management Review, 28(3), 383–396. https://doi.org/10.2307/30040728

- Hillman, A. J., Withers, M. C., & Collins, B. J. (2009). Resource dependence theory: A review. Journal of Management, 35(6), 1404–1427. https://doi.org/10.1177/0149206309343469

- House, R. J., Hanges, P., Javidan, M., Dorfman, P. W., & Gupta, V. (2004). Culture, leadership and organizations: The GLOBE study of 62 societies. Sage Publications.

- Husted, B. W., & de Sousa-Filho, J. M. (2017). The impact of sustainability governance, country stakeholder orientation, and country risk on environmental, social, and governance performance. Journal of Cleaner Production, 155, 93–102. https://doi.org/10.1016/j.jclepro.2016.10.025

- Ibrahim, N. A., & Angelidis, J. P. (2011). Effect of board members gender on corporate social responsiveness orientation. Journal of Applied Business Research (JABR), 10(1), 35–40. https://doi.org/10.19030/jabr.v10i1.5961

- International Monetary Fund. (2021). World economic outlook: Managing divergent recoveries. International Monetary Fund. https://www.imf.org

- Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4), 305–360. https://doi.org/10.1016/0304-405X(76)90026-X

- Jian, W. Z., Jaaffar, A. H., Ooi, S. K., & Amran, A. (2017). The effects of national culture, corporate governance, and CSR governance on CSR disclosure quality. Global Business and Management Research, 9(4), 298–314.

- Jiang, L., Cherian, J., Sial, M. S., Wan, P., Filipe, J. A., Mata, M. N., & Chen, X. (2021). The moderating role of CSR in board gender diversity and firm financial performance: Empirical evidence from an emerging economy. Economic Research-Ekonomska Istraživanja, 34(1), 2354–2373. https://doi.org/10.1080/1331677X.2020.1863829

- Jouber, H. (2021). Is the effect of board diversity on CSR diverse? New insights from one-tier vs two-tier corporate board models. Corporate Governance: The International Journal of Business in Society, 21(1), 23–61. https://doi.org/10.1108/CG-07-2020-0277

- Kagzi, M., & Guha, M. (2018a). Board demographic diversity: A review of literature. Journal of Strategy and Management, 11(1), 33–51. https://doi.org/10.1108/JSMA-01-2017-0002

- Kagzi, M., & Guha, M. (2018b). Does board demographic diversity influence firm performance? Evidence from Indian-knowledge intensive firms. Benchmarking: An International Journal, 25(3), 1028–1058. https://doi.org/10.1108/BIJ-07-2017-0203

- Kang, Y. S., Huh, E., & Lim, M.-H. (2019). Effects of foreign directors’ nationalities and director types on corporate philanthropic behavior: Evidence from Korean firms. Sustainability, 11(11), 3132. https://doi.org/10.3390/su11113132

- Katmon, N., Mohamad, Z. Z., Norwani, N. M., & Farooque, O. (2019). Comprehensive board diversity and quality of corporate social responsibility disclosure: Evidence from an emerging market. Journal of Business Ethics, 157(2), 447–481. https://doi.org/10.1007/s10551-017-3672-6

- Kemp, S. (2011). Corporate governance and corporate social responsibility: Lessons from the land of OZ. Journal of Management & Governance, 15(4), 539–556. https://doi.org/10.1007/s10997-010-9133-6

- Khan, I., Khan, I., & Saeed, B. B. (2019). Does board diversity affect quality of corporate social responsibility disclosure? Evidence from Pakistan. Corporate Social Responsibility and Environmental Management, 26(6), 1371–1381. https://doi.org/10.1002/csr.1753

- Khaoula, F., & Moez, D. (2019). The moderating effect of the board of directors on firm value and tax planning: Evidence from European listed firms. Borsa Istanbul Review, 19(4), 331–343. https://doi.org/10.1016/j.bir.2019.07.005

- Kilic, M. (2015). The effect of board diversity on the performance of banks: Evidence from Turkey. International Journal of Business and Management, 10(9), 182–192. https://doi.org/10.5539/ijbm.v10n9p182

- Kilic, M., & Kuzey, C. (2016). The effect of board gender diversity on firm performance: Evidence from Turkey. Gender in Management: An International Journal, 31(7), 434–455. https://doi.org/10.1108/GM-10-2015-0088

- Kim, I., Pantzalis, C., & Park, J. C. (2013). Corporate boards' political ideology diversity and firm performance. Journal of Empirical Finance, 21, 223–240. https://doi.org/10.1016/j.jempfin.2013.02.002

- Kottak, C. P. (2015). Cultural anthropology: Appreciating cultural diversity. McGraw-Hill Education.

- Kouaib, A., Mhiri, S., & Jarboui, A. (2020). Board of directors’ effectiveness and sustainable performance: The triple bottom line. The Journal of High Technology Management Research, 31(2), 100390. https://doi.org/10.1016/j.hitech.2020.100390

- Kyaw, K., Olugbode, M., & Petracci, B. (2017). Can board gender diversity promote corporate social performance? Corporate Governance. The International Journal of Business in Society, 17(5), 789–802.

- Latif, R. A., Yahya, N. H., Mohd, K. N. T., Kamardin, H., & Ariffin, A. H. M. (2020). The influence of board diversity on environmental disclosures and sustainability performance in Malaysia. International Journal of Energy Economics and Policy, 10(5), 287–296. https://doi.org/10.32479/ijeep.9508

- Lau, C., Lu, Y., & Liang, Q. (2016). Corporate social responsibility in China: A corporate governance approach. Journal of Business Ethics, 136(1), 73–87. https://doi.org/10.1007/s10551-014-2513-0

- Lau, D. C., & Murnighan, J. K. (1998). Demographic diversity and fault lines: The compositional dynamics of organizational groups. The Academy of Management Review, 23(2), 325–340. https://doi.org/10.2307/259377

- Lenard, M. J., Yu, B., York, E. A., & Wu, S. (2014). Impact of board gender diversity on firm risk. Managerial Finance, 40(8), 787–803. https://doi.org/10.1108/MF-06-2013-0164

- Li, H., & Chen, P. (2018). Board gender diversity and firm performance: The moderating role of firm size. Business Ethics: A European Review, 27(4), 294–308. https://doi.org/10.1111/beer.12188

- Li, J., Ding, H., Hu, Y., & Wan, G. (2021). Dealing with dynamic endogeneity in international business research. Journal of International Business Studies, 52(3), 339–362. https://doi.org/10.1057/s41267-020-00398-8

- Liao, L., Luo, L., & Tang, Q. (2015). Gender diversity, board independence, environmental committee, and greenhouse gas disclosure. The British Accounting Review, 47(4), 409–424. https://doi.org/10.1016/j.bar.2014.01.002

- Lin, T. L., Liu, H. Y., Huang, C. J., & Chen, Y. C. (2018). Ownership structure, board gender diversity and charitable donation. Corporate Governance: The International Journal of Business in Society, 18(4), 655–670. https://doi.org/10.1108/CG-12-2016-0229

- Low, D. C., Roberts, H., & Whiting, R. H. (2015). Board gender diversity and firm performance: Empirical evidence from Hong Kong. South Korea, Malaysia and Singapore. Pacific-Basin Finance Journal, 35, 381–401. https://doi.org/10.1016/j.pacfin.2015.02.008

- Luo, X., Wang, H., Raithel, S., & Zheng, Q. (2015). Corporate social performance, analyst stock recommendations, and mainly future returns. Strategic Management Journal, 36(1), 123–136. https://doi.org/10.1002/smj.2219

- McClave, J. B. (2008). Statistics for Business and Economics. (8th ed.). Prentice Hall International.

- Mak, Y. T., & Yuanto, K. (2005). Size really matters: Further evidence on the negative relationship between board size and firm value. Pacific-Basin Finance Journal, 13(3), 301–318. https://doi.org/10.1016/j.pacfin.2004.09.002

- Martinez, M. C. V., Martin-Cervantes, P. A., & Miralles-Quiros, M. M. (2022). Sustainable development and the limits of gender policies on corporate boards in Europe. A comparative analysis between developed and emerging markets. European Research on Management and Business Economics, 28(1), 100168.

- Maznevski, M. L. (1994). Understanding our differences: Performance in decision-making groups with diverse members. Human Relations, 47(5), 531–552. https://doi.org/10.1177/001872679404700504

- McLeod, P. L., Lobel, S. A., & Cox, T. H. Jr.(1996). Ethnic diversity and creativity in small groups. Small Group Research, 27(2), 248–264. https://doi.org/10.1177/1046496496272003

- McNeish, D. M., & Stapleton, L. M. (2016). The effect of small sample size on two-level model estimates: A review and illustration. Educational Psychology Review, 28(2), 295–314. https://doi.org/10.1007/s10648-014-9287-x

- Meyer, J. W., & Rowan, B. (1977). Institutionalized organizations: Formal structure as myth and ceremony. American Journal of Sociology, 83(2), 340–363. https://doi.org/10.1086/226550

- Miller, C. (1990). Cognitive diversity within management teams: Implications for strategic decision processes and organizational performance. Unpublished doctoral dissertation. Graduate School of Business, University of Texas.

- Miller, C., Burke, L., & Glick, W. (1998). Cognitive diversity among upper-echelon executives: Implications for strategic decision processes. Strategic Management Journal, 19(1), 39–58. https://doi.org/10.1002/(SICI)1097-0266(199801)19:1<39::AID-SMJ932>3.0.CO;2-A

- Miller, T., & del Carmen Triana, M. (2009). Demographic diversity in the boardroom: Mediators of the board diversity–firm performance relationship. Journal of Management Studies, 46(5), 755–786. https://doi.org/10.1111/j.1467-6486.2009.00839.x

- Milliken, F. J., & Martins, L. L. (1996). Searching for common threads: Understanding the multiple effects of diversity in organizational groups. Academy of Management Review, 21(2), 402–433. https://doi.org/10.5465/amr.1996.9605060217

- Milne, M. J., & Patten, D. M. (2002). Securing organizational legitimacy: An experimental decision case examining the impact of environmental disclosures. Accounting, Auditing & Accountability Journal, 15(3), 372–405. https://doi.org/10.1108/09513570210435889