?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Hot money is generally associated with economic and financial turmoil in emerging economies. In this backdrop, a number of studies document the causal links between hot money and financial markets. Accordingly, the study examines the causal relationship among hot money, equities, and real estate assets in the small-scale economy of Pakistan. For this purpose, we employ various time series techniques such as the JJ Co-integration test, Granger causality tests, Impulse Response Functions (IRF), and Variance Decomposition Analysis (VDC). The findings validate the long-term association between speculative funds and underlying investment markets. The results uncover unidirectional causality from investment markets to hot money in Pakistan. However, the lack of a bi-directional relationship among the underlying variables indicates that hot money is not a major driver of soaring prices in equities and real estate assets. Alternatively, developing the underlying markets attracts speculative cash inflows into the economy. The findings of the study highlight some useful implications for investors and regulators. For instance, the study's findings present valuable insights for international investors seeking diversification opportunities in small-scale economies such as Pakistan. Also, the regulators in the underlying economy can utilize the study findings to formulate an optimal model to manage international capital flows.

1. Introduction

Due to economic globalisation and financial liberalisation, huge amounts of speculative funds flow worldwide to chase short-term profits. The term hot money is generally employed to describe such speculative funds. Hot money is generally defined as a flow of capital or funds from one country to another mainly to earn a short-term profit due to anticipated exchange rate shifts or differences in interest rates. Typically, the flow of speculative funds is driven by investors who actively seek short-term investment and arbitrage opportunities. Such investors pursue short-term investment opportunities with a high-interest rate, increasing volatility in the underlying financial markets.

Consequently, asset prices are significantly influenced due to liquidity shocks generated by hot money rather than firms’ fundamental financial changes (Ferreira & Matos, Citation2008). The previous evidence also suggests that hot money can fuel inflation and drive stock prices (Zhang & Fung, Citation2006). The surge in hot money can cause market instability (Martin & Morrison, Citation2008). In this backdrop, Chari and Kehoe (Citation2003) argue that booms and crises in emerging economies are associated with the inflow of speculative funds, wherein a large influx of funds causes a boom in the financial markets. Nevertheless, the sudden outflow of hot money bursts the financial bubble created by the inflow of sizeable speculative capital, and the consequences can be devastating (Sarno & Taylor, Citation1999).

The speculative funds dramatically increased after the 1990s around the globe; many believed that they led to various economic and financial crises, such as Asian financial crisis 1997 (Kaminsky, Citation1999; Kaminsky & Reinhart, Citation1998). Conventionally, the restrictions on capital movement are believed to promote economic development and better allocation of resources (McKinnon, Citation2010; Shaw, Citation1973). On the contrary, the statistic unveils exponential growth of speculative funds around the world, the flow of speculative funds rose from USD82 billion in the 1970s to a staggering USD1,680 billion in 2008. In light of this, a thread of literature has documented the impact of hot money on major financial markets (Filer, Citation2004; Zhang et al., Citation2019). In particular, many studies have examined the influence of hot money on financial markets in emerging economies (e.g., Fuertes et al., Citation2016; Wei et al., Citation2018), wherein the surge in hot money is generally suggested as a destabilising factor and trigger of regulations. In this regard, examples of such circumstances are cited, including Brazil, Argentina, Taiwan, Thailand, Indonesia, etc. (Korinek, Citation2011; McCauley, Citation2010; Ostry et al., Citation2010). In addition, it is also suggested that the flow of speculative funds in emerging markets is highly sensitive to the expected return of assets, currency valuations, and anticipated exchange rate movements (Han Kim & Singal, Citation2000). In particular, the increase in trade liberalisation causes the inflow of hot money in emerging economies, giving rise to stock prices (Domowitz et al., Citation1997). Studies also show that hot money is among the main drivers of herd behaviour in emerging markets. After all, herding may not be linked to economic fundamentals (Kim & Wei, Citation2002). Herding behaviour caused by hot money is often linked to financial turmoil and volatility in emerging markets (Calvo, Citation1998; Domowitz et al., Citation1997).

In general, speculative funds in emerging economies are viewed through a dual lens of benefits and costs. This is also true for a small-scale economy like Pakistan since anecdotal evidence associates hot money with extreme volatility in the financial and real sector due to its extreme size and short-term nature. In the early days, the exposure of Pakistan’s economy to global economic conditions was not as significant as other similar emerging economies. In contrast, the country has recently attracted a large inflow of speculative cash inflows. Many suggest that trade liberalisation, flexible exchange rate regime, and growing opportunities to invest in the financial sector drive the surge in speculative cash inflows. Others argue that the decrease in FDI and exports have stimulated policymakers in the country to use hot money as an instrumental tool to attract an inflow of USD into the economy (Adil et al., Citation2021). In this backdrop, the country has experienced many episodes where hot money flew in and out of its financial markets. Nevertheless, they are concerned that the economy might be exposed to colossal risks of speculative cash flows, which were previously encountered by many other emerging economies (e, g., the Mexico peso crisis in 1994, the Asian crisis in 1997, and the great crisis in Argentina 2001). Hence, it is crucial for policymakers in the country to accurately estimate hot money and its influence on financial markets for suitable policy design.

In general, the real estate sector and stock markets around the world offer promising investment opportunities to individual and institutional investors. In this regard, the underlying investment markets in Pakistan have also presented significant positive returns to local and foreign investors, especially in the last decade. First, Pakistan’s real estate industry is among the country’s most growing sectors. According to the statistics of the federal board of revenue of Pakistan, the real estate sector is worth USD 700 billion. While in the last decade, a rise in Pakistan’s foreign exchange reserves has resulted in the protracted ‘Bull Run’ in the real estate sector. This upward trend in the real estate sector has attracted significant foreign investment. In fact, under the China-Pakistan Economic Corridor (CPEC) initiative, infrastructure and transportation projects worth USD 11.63 billion are initiated in the economy. Also, the domestic investors in the country prefer the real estate sector over financial markets for investmentsFootnote1. Nevertheless, on the other side continuous rise of house prices in the last decade has prompted regulations to cool down the market. Consequently, recently, regulations have been enforced to impose taxes on the capital gain from the sale of real estate assets. Other measures such as increased minimum down payment ratios and swelling mortgage rates have also been introduced into the economy. In the same way, the capital market in Pakistan has drawn considerable attention from foreign and local investors. In the year 2016, Pakistan Stock Exchange (PSX) was included in Morgan Stanley’s emerging market index when the market recorded 47% annual growth. Consequently, there is a large influx of foreign investment in the stock market due to opportunities for realising high returns and portfolio diversification. In this spirit, the regulators in the country have taken many serious measures to ensure higher transparency in the market to attract foreign investors. Also, many reforms, including tax incentives and the commitment to treating foreign and local investors equally, have stimulated foreign investment in the stock market. Resultantly, the share of foreign investment has increased in PSX.

In the global context, many studies have contributed a great deal to the literature on the relationship between hot money and financial markets. Still, there is little known about the influence of hot money on the real estate sector and the stock market in Pakistan. In this regard, several research problems are yet to be addressed, and there is a dearth of empirical evidence to formulate prudent policies regarding international capital flows and market stability. To fill this theoretical void, the study focuses on exploring the impact of hot money on major investment markets such as the stock market and real estate sector in a small-scale economy. In this way, the findings of the study will hold functional insights for policymakers and investors. In addition, the study extends the existing literature as we argue that the effect of hot money on investment markets varies across large- and small-scale economies. In contrast, the major share of the previous literature on the topic has focussed on large and developed economies. In this way, the study contributes to scarce literature that documents the role of hot money in shaping up investment markets in the small-size economies. In fact, the findings ascertained from the study could effectively be used in similar economies and markets to make better policy and investment choices.

In the local context, few studies have attempted to document the association between the stock market and the real estate sector in the economy. For instance, Yousaf and Ali (Citation2020) suggest bi-directional linkages between the real estate sector and the stock market in Pakistan. Adil et al. (Citation2021) illustrate the impact of the COVID-19 pandemic and policy rate on the inflow of speculative funds into the economy. However, there is a lack of empirical research examining the impact of hot money on the stock market and real estate sector in the economy. Since the underlying investment markets offer profitable investments and arbitrage opportunities to foreign investors, the research question of whether hot money can influence real estate and stock prices in Pakistan remains unaddressed. Therefore, this study investigates this crucial topic by exploring the dynamic association between hot money, the stock market, and the real estate sector in Pakistan. The study’s findings hold important implications for various stakeholders, especially the regulators of the financial and real estate sector in Pakistan and investors (local and foreign). In fact, from the policy perspective, the topic becomes crucial because the convenient nature of entertaining speculative funds exposes the economy to various risks such as inflation risk, exchange rate risk, and interest rate risk. In addition, the study also provides functional information to investors seeking prudent portfolio investment decisions to maximise their profits and diversify risks.

In order to examine the desired nexus among hot money and major investment markets, we use various robust time series techniques such as the JJ Co-integration test, Granger causality tests, Impulse Response Functions (IRF), and Variance Decomposition Analysis (VDC) in a multivariate vector autoregressive (VAR) environment. The study’s findings unveil some interesting facts about the association of hot money with the real estate sector and the stock market in Pakistan. The findings uncover a unidirectional relationship between hot money, Pakistan’s real estate sector, and the stock market. Moreover, the findings show that hot money does not drive up prices in Pakistan’s real estate sector and the stock market. In contrast, the development of the underlying investment markets attracts speculative cash inflows into the economy.

The rest of the paper is organised as follows: Section 2 describes the related literature. Section 3 explains the data and methodology of the study. The discussion on the results is presented in Section 4. The last section concludes the study with implications.

2. Literature review

The study is related to two strands in literature. The first strand of literature describes the influence of interest rate fluctuations on international capital flows. The second strand covers the impact of international capital flows on financial markets.

2.1. Interest rate fluctuations and international capital flows

Under the Purchasing Power Parity (PPP) theory, interest rate differential is termed as the main driver of short-term international capital flows. Theoretically, the speculative cash flows move towards economies with high-interest rates. In financial markets, the term hot money indicates the flow of capital (or funds) from one country to another to obtain short-term profit from differences in the interest rate or predicated exchange rate shifts. Such speculative flows of capital are also known as ‘hot money’ because they can move in and out of the markets in a concise time span; therefore, they can cause instability in the market (Martin & Morrison, Citation2008). In addition, flow of speculative funds creates a bubble in asset prices and can even cause a serious economic crisis (Zhang et al., Citation2019). Also, increased money supply due to excessive inflows of hot money can cause inflation in the domestic economy (Su et al., Citation2018). Since speculative funds are controlled by investors who are actively seeking short-term returns, Fleming (Citation1962) found that speculative cash inflows are more responsive to the floating interest rates than fixed interest rates. In contrast, Mundell (Citation1963) suggests that capital flows are more sensitive to interest rate differentials.

Another literature thread indicates that international capital flows depend on exchange rate fluctuations and the balance of imports and exports (Branson, Citation1968). Han Kim and Singal (Citation2000) assert that speculative funds are highly sensitive to interest rate differentials in emerging economies, expected return from assets, and currency revaluations. In addition, Chari and Kehoe (Citation2003) suggest that economic booms and financial crises are closely linked with movements of speculative funds in emerging economies. Sarno and Taylor (Citation1999) show that one of the major reasons behind the 1997 East Asian financial crisis was the sudden reversal of capital flows.

A line of studies also documents that international capital flows depend on the country and industry-specific factors. In this regard, Reinhardt et al. (Citation2013) claim that emerging economies experience net capital inflows. Alternatively, developed economies observe net outflows. Similarly, Jin (Citation2012) argues that capital flows towards economies with developed capital-intensive sectors. In addition, Wurgler (Citation2000) advocates that financial markets improve the allocation of such capital flows by increasing the capital for growing sectors and decreasing capital for poor-performing industries.

2.2. International capital flows and financial markets

A large body of literature examines the relationship between international capital flows and financial markets, especially equities, bonds, and real estate. In this regard, many authors suggest a positive impact of international capital flows on stock prices in emerging markets (e.g., Ni & Huang, Citation2014; Sohinger & Horvatin, Citation2006; CitationTabak, 2003). For instance, CitationTabak (2003) argues that international capital flows improve stock market efficiency. Sohinger and Horvatin (Citation2006) and Gharghori et al. (Citation2009) propose a positive impact of international capital flows on stock markets in Australia and Croatia. In addition, Law et al. (Citation2014) suggest a positive causal impact of economic liberalisation on stock market development.

In contrast, studies highlight the negative consequences of international capital flows on stock market development. Neumann et al. (Citation2009) suggest that international capital flows should be analysed from a dual lens of costs and benefits. Domowitz et al. (Citation1997) demonstrate the strong influence of hot money flows on stock market development in Mexico, but the authors also describe the major role of such capital flows in causing the 1994 economic crisis in Mexico. Some studies also suggest that the rise in short-term international capital flows in emerging economies is one of the major reasons for destabilising and activating the regulations in emerging economies, of which recent examples include Taiwan, Indonesia, Thailand, Brazil, and other many other emerging economies (Habermeier et al., Citation2011; McCauley, Citation2010; Ostry et al., Citation2010). Wei et al. (Citation2018) the notion of hot money also showcases a sudden rise in stock prices due to excessive capital inflow, generating worrisome asset price bubbles. As a result, this might cause significant uncertainty and instability in the underlying market. Nevertheless, speculative funds have grown around the globe, especially in emerging markets, due to the notion of trade liberalisation and globalisation (Fuertes et al., Citation2016; Kim & Iwasawa, Citation2017).

A growing thread of literature also documents the impact of hot money on the real estate sector. Ferreira and Matos (Citation2008) suggest that speculative funds in hot markets tend to chase assets with recent positive returns. The bull rally begins when the hot market offers whooping profits to investors and speculators. Consequently, the demand for securities in such a market soars, driving up prices, market capitalisation, and returns. In the same way, short-term international capital flows are also considered the cause of worrisome real estate market price bubbles (Zhang & Fung, Citation2006). Yongqiang and Tien (Citation2004) indicate that the Chinese real estate market’s rapid growth is mainly because of the significant incursion of speculative capital inflows into the Chinese market. Martin and Morrison (Citation2008) assert that the flow of hot money in emerging markets significantly influences investment. The authors suggest that a large inflow of speculative cash inflows in Chinese real estate is alarming since it can cause major economic destabilisation.

In this backdrop, Guo and Huang (Citation2010) use the multivariate Vector Auto Regressive model (VAR) to examine the influence of hot money in the Chinese stock market and real estate sector. The findings recognise speculative cash flows as a major reason to drive up property prices and accelerate instability in both markets because of their massive size and short-term investing nature. The results also indicate that speculative cash inflows are the second largest contributor to fluctuations in both the underlying markets. Several studies have also shown wealth impact on Chinese housing and stock markets. In this light, the evidence indicates that monetary politics or ‘hot money’ can simultaneously affect the prices of both types of assets, stocks and property (Chiang & Tsai, Citation2020).

Further, Wei et al. (Citation2018) conducted a study using the nonlinear Granger causality test and the new model ‘GARCH – MIDAS’. The findings revealed that hot money has a significant positive impact on the long-term volatility of the Chinese stock market. However, there is no linear and nonlinear causality between hot money, growth rate, and the Chinese stock market. Similarly, Zhao et al. (Citation2013) also show the intensive effect of hot money on China’s real estate, foreign exchange, and capital markets. Lu and Dong (Citation2016) also find that entry of short-term international capital flows drives the high prices in the real estate market. Zhang (Citation2018) evaluates the association between hot money, the stock market, and the real estate sector from the perspective of the co-selling effect.

As cited, the previous literature largely covers the impact of hot money on stocks and real estate sectors in developed and large economies. Still, there is little known about the influence of hot money on the underlying investment markets in the case of small-open economies. Accordingly, we aim to uncover the relationship between hot money and financial markets such as the stock market and the real estate sector in Pakistan. In this way, the study extends the previous literature by offering new insights on the association between hot money and investment markets, which are more pertinent to medium or small-size economies and markets. In light of this, we have formulated two main hypotheses:

H1: Hot money causes an increase in the stock prices in Pakistan.

H2: Hot money causes an increase in the real estate prices in Pakistan.

3. Methodology

3.1. Data and empirical approach

The study uses monthly data collected from January 2011 to December 2017. The period selection is based on the data available as there are limited sources for real estate data in Pakistan. In this backdrop, we employ a unique dataset to examine the relationship between hot money and investment markets. Utilising monthly data series for empirical analysis allows us to determine robust results as compared to annual, quarterly, or annual data as both underlying are associated with extensive size distortion (Zhang & Fung, Citation2006). In our proposed framework, hot money is the dependent variable and is calculated as the difference between foreign exchange reserves, trade and services balance, and foreign direct investments. The data for hot money is extracted from the monthly statistical bulletin of the State Bank of Pakistan (SBP). KSE-100 is used as proxy of the stock market, and the data of the index is obtained from data portal of PSX. The housing price index (HPI) data is obtained from Zameen.com (Pakistan’s largest property web portal). It is considered a major source of real estate price data in Pakistan as currently, no other real estate price index is maintained in the country. In addition, two control variables such as policy rate and Sharpe ratio, are introduced in the model. The policy rate is the benchmark rate determined by SBP, and the data is extracted from the website of SBP. Sharpe ratio is a widely utilised indicator to evaluate the stock market performance as it shows the risk-adjusted performance of the stock market. It is measured as monthly excess returns of the index divided by the standard deviation of index returns, wherein excess returns are the difference between the return on the market and risk-free rate (the 3 month treasury bills yield rate is taken as the risk-free rate).Due to data unavailability, the empirical configuration lacks a control variable from the real estate sector variable. The variable definitions are provided in .

Table 1. Definition of the variables.

In order to investigate the nexus among hot money, the stock market, and the real estate sector, the study employs robust time series methods based on the unrestricted multivariate vector autoregressive (VAR) model. Firstly, the ADF (Augmented Dickey-Fuller) unit root test is applied to determine the stationarity of the variables in the model. Secondly, AIC (Akaike Information Criteria) is employed to estimate the appropriate lag length for the execution of the JJ co-integration test to evaluate long-term equilibrium conditions. Thirdly, the unrestricted multivariate VAR model is executed. Fourthly, IRF is executed to determine the effects of shocks in various endogenous variables in the model. Fifthly, VDC is employed to analyse the variance decomposition of forecast errors. Finally, since the relationships among financial markets are often complex and non-linear, we also estimate results through nonlinear Granger causality tests to serve as robustness for our main analysis.

3.2. The VAR model

The VAR model holds various advantages over single equation regression. The single-equation regression model only finds the association of economic variables but not the causes of such variations. VAR model extends the multi-period dynamics by permitting both lagged and instantaneous effects of all economic variables. Opposite to estimating each regression independently, it is better to employ VAR to estimate individual regression within a system, where all economic variables are endogenously resolute. According to Zivot and Wang (Citation2006) VAR model has been widely employed for multivariate time series analysis as it is considered the most flexible and easily understood model. Also, it is also well known that the VAR model is beneficial for forecasting and describing the dynamic behaviour of economic and financial time series. In addition, it also recognised that the VAR approach makes forecasting quite flexible, and therefore, it specifies potential future paths of the variables in the model. The basic VAR model equation setup employed in the study is explained in Equation (1).

+

(1)

In the model [ ……….

] represent the vectors of economic variables. It contains (

L) 5 × 5 matrix of polynomials in the lag operator. In model [

……

] is a vector of corresponding innovation processes with a non-diagonal variance-covariance matrix of σ2Ω and a mean zero. The model contains five variables, and each endogenous variable depends on its own lagged values.

3.3. Co-integration test

If the time series of respective variables have long-term associations, the two variables are said to be co-integrated, irrespective of the fact that individual time series could be non-stationary. In fact, the stationary series can still predict invalid outcomes even though ADF statistics have confirmed the stationarity. Co-integration indicates that if the residual is stationary then the variables tend to have co-movement implying a long-term equilibrium between the variables. Multivariate co-integration test by Johansen and Juselius (Citation1990) has been used in this study to examine the long-term association among study variables. The approach allows several co-integrating vectors to be tested in the model; therefore, it is possible to explore several associations between the variables. The co-integration test statistics are formulated as:

(2)

(2)

(3)

(3)

3.4. Granger causality test

Following the study of Torres and Vela (Citation2003) we use Granger causality test to examine the causal relationship among hot money, stock market and real estate sector in Pakistan. According to Granger (Citation1969) causality test, if a variable Y1 causes a variable Y2, then in time series the past values of Y1 must contain significant information that helps to predict Y2 above and beyond the information contained in the time series of Y2. The following two equations are considered for a bi-variate VAR model of two variables Y1 and Y2.

(4)

(4)

(5)

(5)

In the above equations, and

are the optimum numbers of lag length, whereas the random error terms are

and

3.5. IRF and VDC analysis

Impulse responses explain the effect of one standard deviation shock or the innovation of one variable on the current and future values of another variable. According to Sims (Citation1980) for dynamic VAR (vector autoregressive) model orthogonalised impulse responses are commonly employed. The underlying shocks in the VAR model are based on Cholesky decomposition before the computation of impulse responses and forecast error variance decompositions. Pesaran and Shin (Citation1998) introduced newly developed G-IRF and G-VDC (Generalised VAR). This model overcomes the shortcoming of orthogonalised impulse responses and forecast error variance decompositions. It has the advantage that the ordering of the variables is invariant. Dekker et al. (Citation2001) compare the generalised VAR with traditional VAR by investigating the linkages of the Asia-Pacific stock markets. The results uncovered that the generalised approach is more realistic and significant. In light of this, we employ generalised impulse response analysis in our study.

In the same way, VDC analysis is employed to describe the error forecast variance in a particular variable due to shocks in other variables. Moreover, it explains the change arising in a specific variable due to its past innovations and changes in other variables at a given period. Given this we utilise VDC analysis to explain the short-term and long-term variations in investment markets due to hot money.

4. Empirical results and findings

4.1. Stationarity results

Commonly the time series are regarded as non-stationary, therefore, the first assumption that needs to be satisfied for such analysis is to check the stationarity of the variables in the model. Tuaneh and Essi (Citation2017) indicate that the stationarity of the series can strongly impact its behavior, whereas the use of non-stationary data can lead to invalid regression results. Hence, in order to carry out a significant joint test on lags of the variables, the time series of the underlying variables must be stationary. As per Gujarati (Citation2013), to test the stationarity of the data, there are multiple approaches available such as Augmented-Dickey-Fuller (ADF), the graphical method, and the Philip-Person (PP) test. In light of this, the study uses Augmented-Dickey-Fuller (ADF) unit root test to check the stationarity of the variables in the model (). The results show that all of the variables in our model are stationary at first order except HPI. Further, the Phillip-Perron test is also applied to check the stationarity of the variables in our model. The results confirm that all the variables are stationary at first order (results are not reported for the Phillip-Perron test).

Table 2. Results of Augmented-Dickey-Fuller (ADF) unit root tests.

4.2. Co-integration results

Two standard approaches are commonly employed, such as Johansen–Juselius (JJ) approach and Eagle–Granger (E.G.) approach, to test the co-integration among time series. In this study we utilise the approach introduced by Johansen (Citation1988) and Johansen and Juselius (Citation1990) to test the long-term relationship among variables in our model. The co-integration test uses two statistics to evaluate the number of co-integrating vectors. The two statistics include maximum Eigen-value and trace statistic to determine the long-run association among the variables. In a co-integration test the objective is to examine the stationarity of the residual in the model. If the residual of the model is stationarity, then the variables are considered to have a long-term co-movement. Hence, it indicates an equilibrium relationship in the long run. We follow the step-down procedure to identify the lag length criteria. The optimal lag length for th JJ co-integration is selected from the optimal lag length selection criteria. The lag selection criteria results indicate that standard indicators for selecting optimal lag order such as Final Prediction Error (FPE), Sequential Modified LR test statistic, and Akaike Information Criteria (AIC) propose two lags criteria to identify the number of co-integrating vectors the equation. shows the summary results obtained from the JJ co-integration test models. The results for different models show 1-2 co-integration equations for our model. Our multivariate co-integration test results confirm a long-term association between the variables in our model. Here, the findings confirm the earlier evidence suggesting a long-term association between Pakistan’s stock and real estate markets (Yousaf & Ali, Citation2020). However, more importantly, our findings suggest that speculative funds have a long-term association with Pakistan’s stock market and the real estate sector. Also, the degree of association between speculative cash flows and both markets is moderate.

Table 3. JJ co-integration test results.

4.3. Causality results

In order to determine the causal relationship between hot money, stocks, and the real estate sector in Pakistan, we utilise the Granger Causality test in an unrestricted VAR environment. The results are exhibited in (only relevant results are reported). The results of causality tests display a lack of bid-directional relationship among Pakistan’s hot money and investment markets. First, the results uncover that housing prices cause inflow of speculative funds. The results imply that a rise in house prices in the real sector attracts an inflow of hot money into the economy.

Table 4. Granger causality results.

In contrast, we find no evidence of hot money driving the prices in the real estate sector of Pakistan. In light of the findings, it can be inferred from the findings that speculative funds do significantly influence the prices of real estate assets and volatility in the real estate market. In the same way, we also find unidirectional causality running from the stock market to hot money in Pakistan. Once again, the findings suggest that an increase in equity prices attracts foreign speculative funds into the stock market in Pakistan. The evidence also clearly shows that hot money does not stimulate soaring prices and volatilities in PSX. The evidence somewhat indicates the weak role of speculative capital in building asset price bubbles in investment markets in Pakistan. The findings are the same as Huang (Citation2010), who also suggests a small role of hot money in driving prices in the stock market and real estate sector in the Chinese economy. The findings contradict the conventional view that suggests hot money drives stocks and real estate prices.

In contrast, our results support a weak role of speculative cash flows in accelerating the prices of stocks and real estate assets in Pakistan. The findings have crucial implications for similar medium or small-scale economies. In addition, the other findings also illustrate unidirectional causality from the real estate sector to the stock market in Pakistan. The findings are the same as Yousaf and Ali (Citation2020); they also findings the real estate market leads the stock market in Pakistan. Alternatively, we recognise the nonlinearities that might exist in the time series to fairly reflect the causal relationship among hot money and investment markets. Therefore, we calculate our results through non-linear causality tests. The robustness findings validate our main findings (results are not reported for the non-linear tests).

4.4. Impulse response analysis

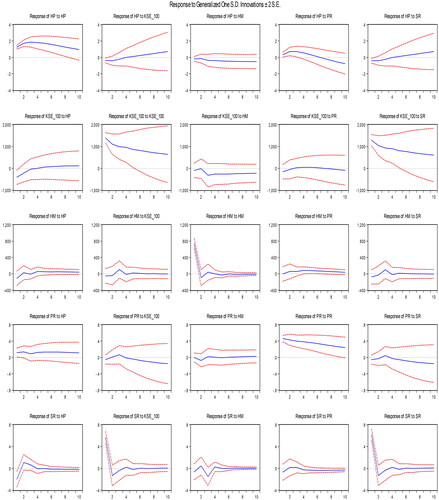

After the unrestricted VAR execution, we determine the time path effects of various endogenous shocks in our model. IRF determines the path of different economic variables when they return to their equilibrium position after injecting the shock into the system. We use the Generalised Impulse Response Functions (GIRF) introduced by Pesaran and Shin (Citation1998), creating a set of innovations that are not dependent on VAR ordering. illustrates the IRF results.

Figure 1. Impulse response functions.

Source: Authors estimations.

The results show that one standard deviation shock in hot money and equity prices negatively influences real estate prices in Pakistan. The negative shock persists in the system for five months and then housing prices begin to rebound. The results indicate that changes in speculative funds and the equity market adversely affect the prices in the real estate sector. The findings are in line with the notion that the volatility of speculative cash flows can negatively affect the real sector in an economy. The negative association between the real estate sector and the stock market is explained by the fact that market participants perceive the underlying markets as substitute investment opportunities. Moreover, the findings also suggest that shock in one market leads to an augmented level of uncertainty in the other, ultimately inflicting the investment decisions of market participants in both markets.

In the same way, the results also exhibit the negative impact of one standard deviation shock in hot money on the stock market. Once again, the findings imply that changes in hot money increase the uncertainty in the equity market. The obtained evidence again implies that swelling speculative funds does not fuel the prices in stock market and real estate sector in Pakistan. The findings reinforce a thread of literature that documents the weak role of speculative inflows in rising returns and volatilities in equities and real estate assets. For instance, Liang and Cao (Citation2007), Huang (Citation2010), and Chen et al. (Citation2011) argue that short-term speculative funds are not a major driver of soaring volatilities in stock and real estate markets in emerging economies. The findings clearly show that one standard deviation shock in housing and equity prices positively influences the inflow of speculative funds. The findings confirm our earlier presented evidence that growth of the underlying investment markets attracts foreign speculative funds into the country. Finally, the findings also show that one standard deviation shock in the KSE-100 index positively affects real estate prices in the economy. This implies that volatility in the stock market is perceived as a negative signal by investors as they start to divert their capital flows towards the real estate sector during the shock period. In such times investors reckon real estate sector as a more secure and less volatile investment opportunity in Pakistan.

4.5. Variance decomposition analysis (VDC)

display the results of VDC analysis.

Table 5. Variance decomposition analysis of Housing prices VDC of HP.

Table 6. Variance decomposition analysis of stock prices.

Table 7. Variance decomposition analysis of Hot money.

First, the VDC of the housing price index uncovers that none of the variables in our model explain any changes in the underlying index in the short run. In contrast, the findings show that stock prices explain around 16% changes in the real estate assets in the short run. The findings again confirm the equity market’s crucial role in deterring market outcomes in the real estate sector in Pakistan. Also, the results again display the weak role of hot money in explaining the changes in the real estate sector in Pakistan. The findings imply hot money plays a limited role in shaping prices in the real estate sector. In addition, the results show that the policy rate explains around 9% of the changes in real estate sector in the long run. The findings uncover the influence of policy rates on mortgage financing costs and the subsequent impact on the prices and growth of the real estate sector in Pakistan.

The results of the VDC analysis of the stock market index unveil an interesting association between the stock market and the real estate sector. The results show that the prices of real estate assets explain 8% of changes in the stock prices. The results suggest that seeking short-term gains carefully examine the environment in the real estate sector before deciding to invest in the stock market. In contrast, the influence decreases to 3% in the long run as the investment decisions are influenced by factors other than the price level of alternative investment markets. Once again we note weak contribution of hot money in explaining the changes in the stock market. The results indicate a weak association between hot money and stock market prices and volatility in Pakistan.

Finally, the VDC analysis of hot money depicts that stock prices and real estate prices only explain 2% each of the variations in the speculative funds in the short run. In addition, we note a small increment in explanation proportion in the long run. However, the findings stress the weak association between hot money, the stock market, and the real estate sector in Pakistan. Our findings are in line with Guo and Huang (Citation2010), who indicate that influence of hot money in driving business cycle volatility is infinitesimal. Similarly, Wheaton and Nechayev (Citation2008) support the same argument that short-term speculative inflows do not predominantly cause a rise in the real estate sector of the US. On the contrary, the changes in the real estate sector are explained by employment, an increase in demand, and rural-urban migration.

5. Conclusions and policy implications

The study examines the impact of hot money (speculative funds) on stock market and real estate markets in a small-scale economy such as Pakistan. The study investigates the role of hot money in driving the prices of equities and real estate assets. For this purpose, various variables from the underlying markets are employed to determine the causal association. Afterward, various robust time series methods are utilised to model the relationship between hot money and the underlying investment markets. The study’s findings show essential insights into the association between hot money inflow and prices of financial and real assets in Pakistan.

The study’s findings unveil a long-term association between the inflow of hot money and housing and equities prices. However, still, the findings demonstrate a lack of bi-directional linkages among speculative funds and major investment markets in Pakistan. Interestingly, the findings unveil that hot money does not drive up prices in Pakistan’s stock market and real estate sector. In contrast, the growth of the underlying markets attracts foreign speculative funds into the economy. The non-linear causality results also confirm these main findings. In addition, the findings also highlight that investors and speculators consider both the underlying markets as alternative investment avenues. Overall, the findings imply that hot money is not a major driver of prices and volatilities in major investment markets in Pakistan instead, other indigenous factors (e.g., political instability, terrorism, institutional quality, remittances, ownership structure, and rural-urban migration) are a better predictor of stock prices and housing prices in Pakistan. The findings hold functional policy implications regarding regulations related to currency and international capital flows because no existing research has highlighted the impact of speculative funds on the stock market and real estate sector in Pakistan. The study findings have crucial implications for international investors seeking diversification opportunities in a small-scale economy like Pakistan. In addition, the regulators can equally benefit from these findings by utilising them to design the optimal framework for managing international capital flows.

Although the findings of the study contribute some valuable insights to the literature, there are a few limitations of the current analysis that should be considered for future research. First, the study uses limited variables from the real estate sector due to data unavailability. Therefore, future research should focus on adding more meaningful variables from real estate sectors to better present the relationship between speculative funds and the real estate sector in Pakistan or similar small-scale economies. Second, although many studies exist that model the relationship between hot money and investment markets in different economies, there is a lack of cross-section research on this topic. Third, a large thread of literature has documented the influence of the COVID-19 pandemic on financial markets around the world. In this backdrop, there is a need to revisit the association between hot money and investment markets during the pandemic period.

Disclosure statement

No potential conflict of interest was reported by the authors.

Data availability statement

The data that support the findings of this study are available from the corresponding author upon reasonable request.

Additional information

Funding

Notes

1 In this spirit, Government of Pakistan has started a low cost housing scheme termed as “Naya” Pakistan Housing Scheme” to meet the shortage of 10 million houses in the country.

References

- Adil, F., Fiaz, A., & Ahmad, N. (2021). Hot money cools on pakistan amid COVID-19: Evidence from nonlinear ARDL. Working paper # 92, Sustainable Development Policy Institute.

- Branson, W. H. (1968). Financial capital flows in the US balance of payments (Vol. 56). North-Holland Publishing.

- Calvo, G. A. (1998). Capital flows and capital-market crises: The simple economics of sudden stops. Journal of Applied Economics, 1(1), 35–54. https://doi.org/10.1080/15140326.1998.12040516

- Chari, V. V., & Kehoe, P. J. (2003). Hot money. Journal of Political Economy, 111(6), 1262–1292. https://doi.org/10.1086/378525

- Chen, J., Guo, F., & Wu, Y. (2011). One decade of urban housing reform in China: Urban housing price dynamics and the role of migration and urbanization, 1995–2005. Habitat International, 35(1), 1–8. https://doi.org/10.1016/j.habitatint.2010.02.003

- Chiang, M.-C., & Tsai, I. (2020). Importance of proper monetary liquidity: Sustainable development of the housing and stock markets. Sustainability, 12(21), 8989. https://doi.org/10.3390/su12218989

- Dekker, A., Sen, K., & Young, M. R. (2001). Equity market linkages in the Asia Pacific region: A comparison of the orthogonalised and generalized VAR approaches. Global Finance Journal, 12(1), 1–33. https://doi.org/10.1016/S1044-0283(01)00025-4

- Domowitz, I., Glen, J., & Madhavan, A. (1997). Market segmentation and stock prices: Evidence from an emerging market. Journal of Finance, 52(3), 1059–1085. https://doi.org/10.1111/j.1540-6261.1997.tb02725.x

- Ferreira, M. A., & Matos, P. (2008). The colors of investors’ money: The role of institutional investors around the world. Journal of Financial Economics, 88(3), 499–533. https://doi.org/10.1016/j.jfineco.2007.07.003

- Filer, L. H. II, (2004). Large capital inflows to Korea: The traditional developing economy story? Journal of Asian Economics, 15(1), 99–110. https://doi.org/10.1016/j.asieco.2003.11.002

- Fleming, J. M. (1962). Domestic financial policies under fixed and under floating exchange rates. Staff Papers - International Monetary Fund, 9(3), 369–380. https://doi.org/10.2307/3866091

- Fuertes, A. M., Phylaktis, K., & Yan, C. (2016). Hot money in bank credit flows to emerging markets during the banking globalization era. Journal of International Money and Finance, 60, 29–52. https://doi.org/10.1016/j.jimonfin.2014.10.002

- Gharghori, P., Lee, R., & Veeraraghavan, M. (2009). Anomalies and stock returns: Australian evidence. Accounting & Finance, 49(3), 555–576. https://doi.org/10.1111/j.1467-629X.2009.00298.x

- Granger, C. W. (1969). Investigating causal relations by econometric models and cross-spectral methods. Econometrica: Journal of the Econometric Society, 37(3), 424–438. https://doi.org/10.2307/1912791

- Gujarati, D. N. (2013). Basic econometrics. McGraw Hills.

- Guo, F., & Huang, Y. (2010). Hot money and business cycle volatility: Evidence from China. China & World Economy, 18(6), 73–89. https://doi.org/10.1111/j.1749-124X.2010.01221.x

- Habermeier, M. K. F., Kokenyne, A., & Baba, C. (2011). The effectiveness of capital controls and prudential policies in managing large inflows (No. 2011/014). International Monetary Fund. https://doi.org/10.5089/9781463902896.006

- Han Kim, E., & Singal, V. (2000). Stock market openings: Experience of emerging economies. The Journal of Business, 73(1), 25–66. https://doi.org/10.1086/209631

- Huang, Y. S. (2010). What causes speculative fund inflow to China? The Chinese Economy, 43(5), 50–61. https://doi.org/10.2753/CES1097-1475430504

- Jin, K. (2012). Industrial structure and capital flows. American Economic Review, 102(5), 2111–2146. https://doi.org/10.1257/aer.102.5.2111

- Johansen, S. (1988). Statistical analysis of cointegration vectors. Journal of Economic Dynamics and Control, 12(2–3), 231–254. https://doi.org/10.1016/0165-1889(88)90041-3

- Johansen, S., & Juselius, K. (1990). Maximum likelihood estimation and inference on cointegration—with appucations to the demand for money. Oxford Bulletin of Economics and Statistics, 52(2), 169–210. https://doi.org/10.1111/j.1468-0084.1990.mp52002003.x

- Kaminsky, G. L. (1999). Currency and banking crises: The early warnings of distress. IMF Working Papers, 99/178. https://doi.org/10.5089/9781451858938.001

- Kaminsky, G. L., & Reinhart, C. M. (1998). Financial crises in Asia and Latin America: Then and now. The American Economic Review, 88(2), 444–448.

- Kim, D., & Iwasawa, S. (2017). Hot money and cross-section of stock returns during the global financial crisis. International Review of Economics & Finance, 50, 8–22. https://doi.org/10.1016/j.iref.2017.03.022

- Kim, W., & Wei, S. J. (2002). Foreign portfolio investors before and during a crisis. Journal of international economics, 56(1), 77–96.

- Korinek, A. (2011). Hot money and serial financial crises. IMF Economic Review, 59(2), 306–339. https://doi.org/10.1057/imfer.2011.10

- Law, S. H., Azman-Saini, W. N. W., & Tan, H. B. (2014). Economic globalization and financial development in East Asia: A panel cointegration and causality analysis. Emerging Markets Finance and Trade, 50(1), 210–225. https://doi.org/10.2753/REE1540-496X500112

- Liang, Q., & Cao, H. (2007). Property prices and bank lending in China. Journal of Asian Economics, 18(1), 63–75. https://doi.org/10.1016/j.asieco.2006.12.013

- Lu, X., & Dong, Z. (2016). Dynamic correlations between real estate prices and international speculative capital flows: An empirical study based on DCC-MGARCH method. Procedia Computer Science, 91, 422–431. https://doi.org/10.1016/j.procs.2016.07.114

- Martin, M. F., & Morrison, W. M. (2008). China’s “hot money” problems. Congressional Research Service Reports. No. RS22921. Asian Development Bank.

- McCauley, R. N. (2010). Managing recent hot money inflows in Asia. Managing Capital Flows The Search for a Framework (pp. 129–159). ADBI and Edward Elgar Publishing.

- McKinnon, R. I. (2010). Money and capital in economic development. Brookings Institution Press.

- MacKinnon, J. G., Haug, A. A., & Michelis, L. (1999). Numerical distribution functions of likelihood ratio tests for cointegration. Journal of applied Econometrics, 14(5), 563–577.

- Mundell, R. (1963). Inflation and real interest. Journal of Political Economy, 71(3), 280–283. https://doi.org/10.1086/258771

- Neumann, R. M., Penl, R., & Tanku, A. (2009). Volatility of capital flows and financial liberalization: Do specific flows respond differently? International Review of Economics & Finance, 18(3), 488–501. https://doi.org/10.1016/j.iref.2008.04.005

- Ni, Y. S., & Huang, P. Y. (2014). Are investors’ portfolios enhanced by incorporating CTA index funds? Applied Economics Letters, 21(1), 43–46. https://doi.org/10.1080/13504851.2013.837571

- Ostry, J. D., Ghosh, A. R., Habermeier, K., Chamon, M., Qureshi, M. S., & Reinhardt, D. (2010). Capital inflows: The role of controls. Revista de Economia Institucional, 12(23), 135–164.

- Pesaran, H. H., & Shin, Y. (1998). Generalized impulse response analysis in linear multivariate models. Economics Letters, 58(1), 17–29. https://doi.org/10.1016/S0165-1765(97)00214-0

- Reinhardt, D., Ricci, L. A., & Tressel, T. (2013). International capital flows and development: Financial openness matters. Journal of International Economics, 91(2), 235–251. https://doi.org/10.1016/j.jinteco.2013.07.006

- Sarno, L., & Taylor, M. P. (1999). Hot money, accounting labels and the permanence of capital flows to developing countries: An empirical investigation. Journal of Development Economics, 59(2), 337–364. https://doi.org/10.1016/S0304-3878(99)00016-4

- Shaw, E. S. (1973). Financial deepening in economic development. Washington, DC: Brookings.

- Sims, C. A. (1980). Macroeconomics and reality. Econometrica: Journal of the Econometric Society, 48(1), 1–48. https://doi.org/10.2307/1912017

- Sohinger, J., & Horvatin, D. (2006). International capital flows and financial marketsin transition economies: the case of Croatia. Working Paper Series No. 154067, Institute of European Studies, UC Berkeley.

- Su, C., Yin, X., Tao, R., Lobonţ, O.-R., & Moldovan, N.-C. (2018). Are there significant linkages between two series of housing prices, money supply and short-term international capital?–Evidence from China. Digital Signal Processing, 83, 148–156. https://doi.org/10.1016/j.dsp.2018.08.017

- Tabak, B. M. (2003). The random walk hypothesis and the behaviour of foreign capital portfolio flows: the Brazilian stock market case. Applied Financial Economics, 13(5), 369–378.

- Torres, A., & Vela, O. (2003). Trade integration and synchronization between the business cycles of Mexico and the United States. The North American Journal of Economics and Finance, 14(3), 319–342. https://doi.org/10.1016/S1062-9408(03)00025-1

- Tuaneh, G. L., & Essi, I. D. (2017). Simultaneous equation modeling and estimation of consumption and investment functions in Nigeria. International Journal of Economics and Business Management, 3(8), 53–71.

- Wei, Y., Yu, Q., Liu, J., & Cao, Y. (2018). Hot money and China’s stock market volatility: Further evidence using the GARCH–MIDAS model. Physica A: Statistical Mechanics and Its Applications, 492, 923–930. https://doi.org/10.1016/j.physa.2017.11.022

- Wheaton, W., & Nechayev, G. (2008). The 1998-2005 housing “Bubble” and the current “Correction”: What’s different this time? Journal of Real Estate Research, 30(1), 1–26. https://doi.org/10.1080/10835547.2008.12091212

- Wurgler, J. (2000). Financial markets and the allocation of capital. Journal of Financial Economics, 58(1-2), 187–214. https://doi.org/10.1016/S0304-405X(00)00070-2

- Yongqiang, C., & Tien, S. (2004). Inflation hedging characteristics of the Chinese real estate market. Journal of Real Estate Portfolio Management, 10(2), 145–154. https://doi.org/10.1080/10835547.2004.12089697

- Yousaf, I., & Ali, S. (2020). Integration between real estate and stock markets: New evidence from Pakistan. International Journal of Housing Markets and Analysis, 13(5), 887–900. https://doi.org/10.1108/IJHMA-01-2020-0001

- Zhang, G., & Fung, H.-G. (2006). On the imbalance between the real estate market and the stock markets in China. The Chinese Economy, 39(2), 26–39. https://doi.org/10.2753/CES1097-1475390203

- Zhang, Y. (2018). Impact of short-term international capital flows on interactivity of stock market and real estate market in Chinese first-tier cities: A viewpoint of “co-selling effect”. Journal of Financial Risk Management, 7(1), 1–11. https://doi.org/10.4236/jfrm.2018.71001

- Zhang, Y., Chen, F., Huang, J., & Shenoy, C. (2019). Hot money flows and production uncertainty: Evidence from China. Pacific-Basin Finance Journal, 57, 101070. https://doi.org/10.1016/j.pacfin.2018.09.006

- Zhao, Y., de Haan, J., Scholtens, B., & Yang, H. (2013). The dynamics of hot money in China. In BOFIT and CityU HK Conference on Renminbi and the Global Economy, 23–24 May 2013, City University of Hong Kong.

- Zivot, E., & Wang, J. (2006). Vector autoregressive models for multivariate time series. Modeling Financial Time Series with S-PLUS® (pp. 385–429). Springer. https://doi.org/10.1007/978-0-387-32348-0_11.