?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Environmental degradation has become a severe concern for the globe; therefore, policymakers in emerging economies are trying to meet the environmental standards. Nowadays, economies have shifted their energy pattern from non-renewable to renewable energy (R.E.U.), but its cost is too high. Undoubtedly, the financial sector also performs well in facilitating such green activities. Therefore, the current study investigates the role of R.E.U. and green finance in environmental quality and collects the data for B.R.I.C.S. economies from 2000 to 2018. The study uses quantile regressions and other advanced techniques to deal with the problems of cross-sectional dependence (C.S.D.) and heterogeneity. The estimated outcomes show that green finance, R.E.U. consumption, and technical innovations perform well in securing the environment by reducing carbon emissions. Likewise, the environmental quality in selected economies is deteriorating due to the rise in non-R.E.U. consumption, economic progress, F.D.I., and trade openness. Therefore, it is time to reshape the local, national and regional growth policies concerning a green investment that can secure our environment. Also, this study proposes future pathways for green finance and other factors relevant to a sustainable environment.

1. Introduction

The rising trend in economic progress (G.D.P.) and human activities is responsible for deteriorating the environmental quality (Lee et al., Citation2022). The global economies have non-serious behaviour toward the sustainable environment because they try to make economic progress regardless of environmental damage (Ye et al., Citation2022). The energy sector cannot be neglected in such activities because all economic and human activities are highly dependent on energy use (E.n.U.; Sarma & Roy, Citation2021). Therefore, the massive use of non-renewable energy (R.E.U.) such as fossil fuels increases environmental damage and reduce green economic growth (E.C.G.; Nawaz et al., Citation2021). However, numerous researchers have studied the variation in climate change and its harmful impact on biodiversity in recent decades (Rasoulinezhad & Taghizadeh-Hesary, Citation2022). Carbon emissions are the key sources contributing to greenhouse gas emissions and environmental damage. Numerous studies have tried to elaborate on the alarming situation of climate change. Therefore, according to Yu et al. (Citation2021), ‘if serious steps are not taken, the continuous increase in environmental pollution could double by 2035’. In December 1997, the Koyoto protocol agreement was signed to fight against global warming. Later on, as global warming increased, the Paris Agreement Conference set a target that the temperature would remain under 2 °C (Dong et al., Citation2022).

Furthermore, the rising temperature may harm global biodiversity (Zhang et al., Citation2022). As the environment and an objective target of human survival practices, nature is the bearer of all human activities in the process of human conquest and transformation. In terms of alienation, nature has also manifested itself in the strongest state (Zheng et al., Citation2021). This reduces air, water, health, and food. Therefore, mankind seeks to achieve a subject position, integrate nature into humanity’s economic and social development, and eliminate the confrontation and conflict brought about by the subject’s activities to the environment (Khan et al., Citation2021; Z. Liu, Vu et al., Citation2022). Climate change mainly causes CO2, nitrous oxide and methane gas increases. Most research falls short of providing adequate information on climate change challenges (Lei et al., Citation2021; Lv, Chen et al., Citation2021). Academics and researchers believe that implementing new environmental regulations and policies can increase environmental quality, but preserving energy reduces E.C.G. Decision-makers must strike a balance between E.C.G. and environmental protection, reducing CO2 emissions while ensuring that reliable and affordable energy is available to everyone (Huang et al., Citation2021; Quan et al., Citation2022).

As the green finance market has grown, governments have played an important role in promoting it (Deng & Zhao, Citation2022). Environmental considerations are becoming increasingly important in financial and investment planning, resulting in a rise in the green economy that consumes more resources and provides environmental and ecological benefits (Zhou et al., Citation2022). Banking and government entities have taken various steps to foster the expansion of green finance principles (Wang & Luo, Citation2022). So, financing for green product research and development must be secure and substantial, and this cannot be done without the backing of the capital market (Cline et al., Citation2020). Angel investors or venture capitalists are reluctant to participate in G.T.I. because of its high risk, high investment features, and maturity mismatch (Wu et al., Citation2022). To overcome the drawbacks of conventional finance, we need a new funding model that is both efficient and long-term. Incorporating artificial intelligence (A.I.) algorithms, big data, cloud technology, blockchains, and standard accounting services has resulted in formidable teaching tool banking (Chen et al., Citation2021; Ji et al., Citation2021). Green technology R&D would be more accessible for businesses, the investment would be more straightforward, and a wider group of investors might benefit from payment systems hypothetically. G.T.I.'s financial problem may be solved with digital finance, which complements and enhances green E.C.G. (Hanafiah et al., Citation2017). The organic growth in digital financing with environmental sustainability to boost the CO2 economy is of critical significance for Korea’s decarburisation objectives and sustained E.C.G. This study aims to give more specific research data knowledge and scope for future studies on virtual currencies and Intelligence in the E.C.C. at the provincial capital compared to earlier material (Mohsin et al., Citation2022). There is also a geographical spillage impact of C.E.E. in multiple cities, and the estimate procedure may be skewed if a value obtained is ignored (Zimon et al., Citation2020).

Green finance and technology innovation allows industries to modify and promote E.C.G. However, Green finance and technology innovation comprehensively enhance the capacity of green E.C.G. and strive to modernise the environmental governance system. It also promotes capital to be shifted from carbon-intensive and polluting industries to those that use innovative technology. According to Zhang, Mohsin et al. (Citation2021), green finance improves ecological sustainability and management and acts as a treatment for environmental damage. A major benefit of green financing (G.F.N.) is that it allows underdeveloped and developed countries to battle pollution jointly. Significant investments and funding for environmentally friendly initiatives are being made under the green finance concept (Muganyi et al., Citation2021).

The impact of these policies on CO2 emissions is particularly complicated in mitigating climate change because of the various new financial laws established by B.R.I.C.S. nations over the previous decades (for a review, see the ‘Data’ section). The link between green finance and CO2 emissions is under-investigated, despite its importance in determining the climate-related financial environment (van Veelen, Citation2021).

With this background, this study makes a triple contribution to the literature. To begin, no empirical analysis of the factors influencing CO2 emissions has considered climate-related financial policies. Our research focuses on this topic for the first time and significantly adds to the study of environmental quality (proxied by CO2 emissions). Footnote. It also uses a P.Q.R. technique to investigate the impact of climate-related financial policies, financial development (F.D.), and E.C.G. on CO2 emissions. Our results will be more detailed than those obtained using the ordinary least squares (O.L.S.) approach if we use the P.Q.R. approach. We will be able to discuss the heterogeneity of countries’ experiences. Because B.R.I.C.S. countries represent the world’s most developed and developing economies, the study’s focus on these countries is critical. In addition, they account for most of the world’s total carbon dioxide emissions. As a result, we think it is important to look at climate-related finance policies from the B.R.I.C.S. nation’s point of view.

The rest of the article is structured as follows. Our research is placed in context in the ‘Literature review’ section. Methods and data are discussed separately. We present the empirical results and discussions, and finally the ‘Conclusions and policy implications’ offer our final remarks and examines the investigation’s policy implications.

2. Literature review

The 2030 Sustainable Creation Goals (S.D.G.s) have received significant attention in the academic literature since their development. To some extent, the findings of this research show that the practices of corporate organisations and industries with sustainable development are largely determined by green finance, clean energy, and the green economy (Pyka & Nocoń, Citation2021). We have covered both theoretical and empirical approaches in this section. Green funding and sustainable development in Asia have been addressed by Taghizadeh-Hesary et al. (Citation2022), for example. Asian economies are said to need a major change in investment from fossil fuel, greenhouse gas, and natural resource-intensive technologies to more efficient ones in order to achieve sustainable growth (Chen et al., Citation2021). In this context, a finance sector green transformation would be critical (Lv, Bian et al., Citation2021). They also looked closely at the main obstacles to green investment for long-term growth. H. Liu, Tang et al. (Citation2022) considered the importance of G.F. and energy security for the S.D.G.s. This is one of the most important statistics presented by these authors: the global investment in R.E.U. and energy efficiency declined by 3% in 2017. Financial institutions favour fossil fuel projects over green ones because of the higher risk associated with, the newer technologies and the consequently lower rate of return. Therefore, it has been suggested by writers that in order to fulfill the S.D.G.s, new files for environmentally beneficial green projects and investment vistas, including green bonds and carbon market instruments, should be opened. They will be referred to as ‘green finance’ when put together.

Arif et al. (Citation2021) claim that green finance is a form of monetary assistance for environmentally friendly development that aids in advancing long-term, environmentally friendly activities. Promoting green structures, securities, and other green activities is critical to establishing it as a necessary component of business and environmental concerns (Mngumi et al., Citation2022). Environmental protection and the advancement of a green economy have both been considered when developing green finance, according to Dong et al. (Citation2021). The researchers used provincial data from 2007 to 2016 to examine the 30 Chinese enterprises’ cooperation between green finance and the green economy. In terms of sustainable development and the green economy, green funding has been found to have a substantial impact.

There has also been a significant amount of research into the link between green energy and sustainable development. One of the first contributions in this respect came from Wang, Li, Wen et al. (Citation2021), who presented various green energy solutions for long-term growth. The writers considered the green energy effect ratio, sustainability ratio and green energy usage when they came up with different green energy techniques. Increased technological, sectoral and effect ratios have been linked to green energy-based sustainability ratios. R.E.U. solutions, such as solar, wind, tidal, and biomass, are cited as having an essential role in economies with abundant green energy sources. A study of the prospects for sustainable development, R.E.U., and E.C.G. in Africa by Z. Liu, Vu et al. (Citation2022) has been published.

In addition, new B.R.I.C.S. policy initiatives urge a more rapid approach to R.E.U. investment for long-term development. Guo et al. (Citation2022) examine R.E.U. and economic activity in sustainable development in 17 G20 countries between 1980 and 2012. The study results show that the variables have a long-term equilibrium connection. In addition, R.E.U. consumption’s significant and positive role in economic activity ensures low carbon emissions and long-term economic development in the selected member countries. The use of R.E.U. in Africa is examined by Streimikiene and Kaftan (Citation2021), who examine alternative energy policies while keeping an eye on the situation. The study’s overall results confirm that tackling Africa’s energy dilemma, which produces greater environmental problems due to its excessive fuel use, is the key to successful sustainable development in that continent’s economies. However, a long-term output can be achieved with the help of the country’s support for R.E.U. sources. The environmental sustainability of O.E.C.D. economies from 1990 to 2018 was examined by Purnamawati (Citation2022). According to the study’s conclusions, decentralisation has been shown to improve environmental quality by reducing carbon emissions. They look at the Chinese economy and the relationship between carbon dioxide emissions, environmental taxes, investment in new technologies, and innovation in 2021. Slope heterogeneity and other panel data difficulties are being addressed when it is discovered that the rapid growth of China’s province economies has resulted in increased carbon emissions, posing a serious threat to the country’s ecology. In addition, Sharma and Choubey (Citation2022) have considered the pre- and post-COVID-19 economic performance. One of the most important findings of their study is that it investigates the link between commodity prices and China’s E.C.G. During the COVID-19 period, the prices of natural resources appear to be more sensitive to economic performance than they were in the past. Some more research, such as those by Akomea-Frimpong et al. (Citation2021), Hou et al. (Citation2022) and Ning et al. (Citation2021), are also focusing on R.E.U. and sustainable practices.

Despite the importance of a green economy and sustainable practices in the literature, there is still a large gap to be filled under diverse regional contexts. As a recent contribution, a green economy and sustainable development are closely linked, as demonstrated by Saeed Meo and Karim (Citation2021), a recent contribution. It was decided to focus on green economy investment and its function in promoting firm-level jobs from an environmental perspective. Hence two key research topics were devised by the authors. In addition, they looked at the role of information diffusion in the ecological setting. The conclusions of their research focus on the impact of environmental spill over on employment. According to Zhang, Wu et al. (Citation2021), the green economy and long-term E.C.G. face numerous policy problems. The authors argue that world policymakers are focusing on green growth through clean energy technology and sustainable development at the same time. They have claimed that green growth cannot guarantee long-term economic prosperity if environmental degradation continues. While evaluating the current academic research on sustainable development under the shadow of S.D.G.s, Yu et al. (Citation2021) have made an important contribution to the literature. They concentrated on four areas: the circular economy, green growth, degrowth and S.D.G. research. The United Nations’ 17 S.D.G.s are directly linked to green growth, the circular economy and degrowth (M. Wang, Li & Wang, Citation2021). Ning et al. (Citation2022) argue that green economy growth techniques are needed since conventional economic models have a negative impact on the natural environment. According to their research, Ghana has yet to reach substantial goals in the green economy, so they are focusing on the country’s procedures and policies. Three main obstacles to developing the green economy are rising costs of green technologies, an increasing threat from climate change, and corruption. However, it is recommended that policymakers prioritise technology and scientific education in order to encourage the development of the green economy (F. Wang, Wang et al., Citation2021).

3. Theoretical framework and empirical modelling

3.1. Theoretical framework

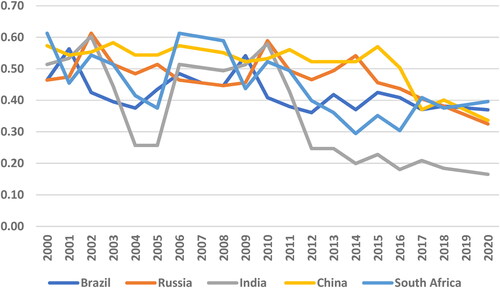

When there is an increase in E.C.G. in a given location (Vinet & Zhedanov, Citation2011) created the E.K.C. hypothesis, which states that the quality of the environment decreases. The green finance is a critical part of the equation regarding the long-term viability of a country’s economy. We suggest that G.F. ideas be regarded as acceptable strategies to reduce ecological deterioration as a conceptual complement to environmental quality. Green credit is defined as loans (project loans, mortgage loans) that banks provide to businesses to generate environmentally friendly goods, as seen in . The importance of G.F. is shown by the rise of E.V.P. in B.R.I.C.S. economic systems. G.F. is predicted to have an inverse correlation with E.V.P. if ENIit is more significant than zero.

Figure 1. Green finance index.

Source: Authors calculation.

One of the most important factors in improving innovation and green technology utilisation in the manufacturing operations of businesses has recently been recognised as E.N.I. Ecologists thus propose E.N.I. as a strategy for improving ecological quality. According to Muhammad (Johnes, Citation2006), E.N.I. enhances environmental quality in the workplace. As a result, ENIit > 0 is predicted to have an inverse relationship with E.V.P. in this investigation. The ecological consequences of over N.R.R. are dire (Solarin et al., Citation2017). There is a growing need for natural resources, and N.R.R. is considered a greener form of energy. E.C.G. forces many nations to utilise their N.R.R. resources inefficiently, resulting in land destruction and E.V.P., which harms the environment. Because of this, our research contends that increased use of N.R.R. in M.I.N.T. countries without sufficient management may favour E.V.P. levels. With NRRit less than 0, we predict a direct and beneficial relationship between N.R.R. and E.V.P. Trade openness may exacerbate toxic pollution from transportation, residential, and E.n.U. Using E.K.C. and earlier literature (Caballero-Morales, Citation2021), EquationEquation (2)(2)

(2) mathematically expresses the econometric technique used in this study

(2)

(2)

All chosen factors were changed to the natural logarithm to improve the allocation and brightness of the data series. Heteroskedasticity and autocorrelation problems may be alleviated with series adjustment in natural logarithmic (Kapoor et al., Citation2021). The E.V.P.'s logarithmic form is stated in the following EquationEquation (3)(3)

(3)

(3)

(3)

Such that, in terms of E.G.C., the utilisation of R.E.U., G.F.N., the rent from natural resources, E.N.I., and urbanisation (U.R.B.).

3.1.1. Green finance index

To calculate green credit, this study examined the data from six high-energy-consumption businesses and the interest expense to total industrial interest expense ratio. The remedy of pollutants in the environment is promoted by green investment. In order to gauge green investment, this study used the G.D.P.-to-environmental pollution expense ratio. Long-term capital like insurance funds is better suited to green projects’ long-term financing and investment requirements than short-term capital like bank loans. However, farming significantly contributes to global warming pollution (Lee et al., Citation2021). The depth of green insurance was therefore measured using the agricultural insurance scale and loss ratio in this article. The market value of environmentally friendly enterprises can be used to gauge green securities to some extent since green securities can measure the scale of environmentally friendly companies. displays the index system for green finance development, calculated using the entropy method.

3.1.2. Data and descriptive statistics

To investigate the proposed study objectives, this study uses the annual data from 2000 to 2018 for B.R.I.C.S. economies. This specified time period is based on data availability; therefore, the data for the selected variable has been collected from the World Development Indicators (W.D.I.). In other words, E.V.P. is taken as the proxy of CO2 and the data for carbon emissions is collected in Mt from the W.D.I. Similarly, the data for research and development (R&D) expenditures are collected in a million US$. Moreover, the data for trade as a % of G.D.P., E.n.U. in Mt, R.E.U. consumption in % of total energy consumption, F.D. in % of G.D.P., and G.D.P. per capita in US$ are collected from the W.D.I.s. Likewise, the descriptive statistics outcomes are present in .

Table 1. Summary statistics.

According to , CO2 emissions, as well as the contribution of R.E.U. consumption, British units of thermal energy per person, total G.D.P. percentage, foreign direct investment, and trade openness in trillions of dollars in present value, are presented in this table. As shown in , the green finance index value triples from 0.02214 in 2000 to 0.06321 in 2018, regardless of fluctuations in the B.R.I.C.S. countries’ overall development trends. Emissions from non-polluting sources have nearly doubled, from 10,669.87 Mt in 2000 to 67,933.13 Mt in 2012.

Table 2. Cross-sectional dependence tests results.

3.2. Model specification

3.2.1. Cross-sectional dependency test

The numerous macroeconomic methodologies used for actual research are described in this research portion. The first step is to examine the cross-sectional dependence (C.S.D.) between the panel data estimations. The fact that C.S.D. exists raises the spectre of measurement inefficiencies and volatility. Due to a wide range of factors, such as common disruptions, regional impacts, and unforeseen country-specific features, several issues may occur. C.S.D. was used in this study since it is mathematically defined in EquationEquation (4)(4)

(4) .

(4)

(4)

3.2.2. Unit root tests

First generation panel root tests (C.A.D.F. and C.I.P.S.) were used in this research, which focused on the chosen variable in the second stage panel root test. The C.A.D.F. and the C.I.P.S. test aid in resolving C.S.D.-related concerns and identifying and removing erroneous regression analysis findings. Furthermore, the researchers could assess the robustness and correctness of the series variance using both stationarity tests. EquationEquation (5)(5)

(5) provides the following description of the C.A.D.F. test’s mathematical expression:

(5)

(5)

As a result, xit displays the factors investigated in the research, indicates the variation in factors, and shows the white error term.

(6)

(6)

Such that the parameter φi(N, T) indicates C.A.D.F. regression test statistics.

3.2.3. Panel co-integration test

Assessing whether the residue element of the equation is stable (Yigitcanlar et al., Citation2019) co-integration technique helps to investigate the co. Integration relationship among these two series. This method’s null hypothesis (H0) states that there is no series co-integration. EquationEquation (6)(6)

(6) expresses the co-integration test physically

This equation is equivalent to: Y it=(n = 0)

(7)

(7)

So that n reflects the causative factors, I denote the specific-individual impact. It represents the series trend. In addition to the co-integration technique, the C.S.D. and series heterogeneity were examined in this work. For this approach, the null hypothesis states that the error-correction term does not co-integrate among the series. EquationEquation (7)(7)

(7) is a mathematical representation of the model:

(8)

(8)

In this way _ (′_i)

are the sensitivity predictions for the series trend. The constant term for all nations series is ′, and the CSD and research period are all indicated by I and t. Statistical test statistics are described quantitatively in equations in this manner.

It is possible to calculate the panel co. Integration approach statistics as follows mathematically:

(9)

(9)

(10)

(10)

(11)

(11)

(12)

(12)

According to the group mean statistics, Gτ and Gτ, and P and Pa exhibit the panel statistics. This marks the shift from short-term stability in terms of speed to long-term stability.

3.2.4. Causality analysis

The researchers used the (Bostian et al., Citation2016) contemporary granger correlation test to analyse the causation link between the series. This method lets us identify whether our model has any slope fluctuation, which helps us handle the likelihood of C.S.D. The null hypothesis of the D–H Granger causality test is that there is no causal link between the variables. It is hypothesised that the model’s cause-and-effect connection may be explained. In EquationEquation (15)(15)

(15) , the D–H non-causality test is formally expressed: Y it = α i+∑ (m = 1) Mathematical formula: i = m + y = t + M

The model’s autoregressive variables are shown in where m is the lag length.

(15)

(15)

3.2.5. Robustness test

As recommended by Kumar and Agarwala (Citation2013), the A.M.G. and C.C.-M.G. were utilised in this research to examine the robustness of our short- and long-term forecasts. A.M.G. and C.C.-M.G. models are used in this study because they are reliable and aid in obtaining predictions free of bias. The data were analysed using the Statistical Package for the Social Sciences E-views (Version 12) program.

4. Empirical analysis

4.1. Cointegration, unit root and C.D. tests

Several recent studies have focused their analysis on detecting their samples’ C.S.D. Because, if it exists, it produces biased results and conclusions if researchers do not use estimators that take this property into account in the data (Lee et al., Citation2021; Ning et al., Citation2022; F. Wang, Wang et al., Citation2021; M. Wang, Li, & Wang, Citation2021; Yu et al., Citation2021; S. Zhang, Wu et al., Citation2021). Using the tests listed in , we could determine if C.S.D. was present. At the 1% level of statistical significance, the findings demonstrate a high C.S.D.

The C.I.P.S. and C.A.D.F. tests were used to determine if the series were stationary. shows that the integration order for all variables is I(1).

Table 3. The results of the CIPS and CADF unit root testing.

According to , the findings of the co-integration test address structural fractures, allowing co-integration test results to be obtained through trials. The results in reveal a strong correlation between carbon dioxide emissions and non-R.E.U. use, green finance, open trade, energy consumption, foreign direct investment, E.C.G., and technological innovation.

Table 4. Co-integration test results.

Table 6. Results of fixed effects quantile regression.

4.2. Random and fixed effect model comparison

The model is first calculated using pooled and fixed effects O.L.S. regression estimations. , columns 1 and 2, show the pooled O.L.S. and fixed effect regression estimates. Pedroni (Citation2001) used the F.M.O.L.S. method presented in his research to estimate long-run elasticities. Pedroni (Citation2001) noted that common time dummies capture various sorts of cross-sectional dependency. It is in Column 1 that the F.M.O.L.S. findings are summarised. Control for all time-specific and spatially invariant factors that could affect the results of a typical study using time-period fixed effects, according to Baltagi (Citation2008), are employed to control for all time-period random effects. Since we are interested in the results of a model with fixed effects in both ways, we prefer models with random effects in either direction. Results from the two-way fixed-effects analysis are shown in column 1. There is only one component of trade that can be said to be consistent across all specifications: the effect of trade.

Table 5. Comparison of fixed and pooled OLS model.

4.3. Quantile regression on a panel

Koenker’s (Citation2004) fixed-effects quantile regression is utilised to account for the distributional variation. In an average time series investigation, removing time-period fixed effects could skew the estimations, which is the power source for our focus on two-way fixed effect quantile regression analysis. Results of the panel quantile regression estimation are shown in . For each of the five percentiles of the emission distribution, the findings are presented in the following order: 5th, 10th, 20th, 30th, 40th, 50%, 60%, 70%, 80% and 90%. All in all, empirical findings show substantial heterogeneity in the effects of numerous factors on carbon emissions

The study results reveal that green finance and carbon emissions have a negative correlation. The intermediate and upper quantiles of green funding and carbon emissions have a particularly detrimental effect. However, the lower and higher quantiles of G.F.N. have a negative correlation (from 5th to 40th and 60th to 95th). To put it another way, according to these data, G.F.N. in the B.R.I.C.S. countries cut CO2. Demand for green investments rises in tandem with increases in CO2 emissions, even if the relationship is not linear. The core focus of the term ‘green credit’ is the green payment and credit business, which includes house mortgages and project financing. Although China’s banks began publishing social responsibility reports in 2006, according to the United Nations Environment Programme (Citation2017), the country only began to properly unify statistical standards and improve the quality of green finance data in 2014. China has accumulated data on green credits, but there are a few drawbacks, such as incomplete disclosure and short-term disclosure, as well as inconsistencies in the statistical criteria.

Furthermore, technological advancement has a detrimental impact on CO2 emissions. Technological innovation requires promoting energy conservation, reducing CO2 emissions, and replacing fossil fuels with R.E.U. sources. As Lemieux et al. (Citation2021) noted, technology innovation is critical to the growth of the R.E.U. sector. Aside from boosting energy efficiency and cutting down on consumption, technological advancements are essential for increasing energy efficiency and cutting down on consumption. Technology innovation has a significant negative impact on CO2 emissions in nations with higher CO2 emissions than in countries with lower CO2 emissions. Growth in the economies of high-emissions countries consumes more energy than growth in the economies of low-emissions countries, implying that energy technology needs to be improved further in order to enhance energy efficiency and raise the number of renewables. Much money has been spent on cutting-edge energy technology in these high-emission countries. Technology is the driving force behind a reduction in carbon emissions. R.E.U. technology investments in the power sector will rise from $270 billion in 2015 to $400 billion in 2030, according to the IEA (Citation2020). Chinese investments in R.E.U. totalled $83.3 billion in 2014, a 39% increase over 2013. In addition, Russian investments totalled $38.3 billion, an increase of 7% in a single year alone. Third place went to India, with a gain of 10% over 2013s $35.7 billion. For this reason, countries with high emissions should boost investment in energy-saving equipment and foster technological innovation to reduce carbon emissions.

The use of R.E.U. in B.R.I.C.S. negatively impacts CO2 emissions. Empirical findings for E.U. nations (Council of the European Union, Citation2020), for 27 advanced countries (Calvo-Gallardo et al., Citation2021), O.E.C.D. countries (Careri et al., Citation2022), for Turkey and Kenya are consistent with this conclusion. However, E.U. nations (Pejović et al., Citation2021), M.E.N.A. Region, and 19 developed and developing countries indicated a positive association between R.E.U. usage and CO2 emissions. According to Mngumi et al. (Citation2022), using R.E.U. in the United States fails to reduce CO2 emissions. R.E.U. usage’s influence on carbon dioxide emissions is also heterogeneous: the lower quantiles of R.E.U. consumption are more likely to reduce CO2 emissions than the upper quantiles. The countries with high carbon emissions, non-R.E.U. consumption regulates carbon emissions, whereas the role of R.E.U. consumption is restricted when it comes to reducing carbon emissions. This is mainly because fossil fuels are still the primary energy source in these high-emissions countries, and the use and proportion of R.E.U. are insufficient.

In addition, the other control variables included in the model are helpful. At all quantile levels, the findings show that the coefficient of F.D. is significant and positive, implying that as E.C.G. improves, so will carbon dioxide emissions. Changes in people’s attitudes toward consumption may be to blame for this, as F.D. frequently occurs alongside economic expansion and higher wealth, which may lead to a rise in people’s desire for more goods and services, which may contribute to an increase in carbon emissions.

Another critical control variable is E.n.U., which considerably impacts CO2 emissions at all quantile levels and has a large coefficient value. E.n.U. in both low- and high-emission countries will significantly impact carbon emissions. This result is in line with Yu et al. (Citation2022). It is a well-known fact that rising levels of carbon dioxide emissions are due to increased global energy consumption. We may argue that the impact of trade on CO2 is modest because the trade coefficient is insignificant in most quantile levels and only significant in the 5th and 20th quantiles. Let’s look at how much income per person affects carbon emissions. We can see from these data that the G.D.P. per capita coefficient is positive, but the G.D.P. quadratic term coefficient is negative, proving the E.K.C. hypothesis exists. The impacts of G.D.P. per capita and its quadratic term on CO2 emissions are distinct from those of F.D. and energy usage, which are both homogeneous. There is no statistical significance in the coefficients of G.D.P. per capita at higher quantile levels. Its quadratic term is also insignificant at higher quantile levels (i.e., 80th and 90th), implying that E.C.G. will significantly increase carbon emissions in low- and high-emission countries.

4.4. Granger causality test

The Granger causality test is used to enhance our analysis after fixed-effects panel quantile regression. There are findings in . The data reveal that the dependent and independent variables are causally linked in both directions. Trade openness and carbon emissions also exhibit a feedback link at the 1% and 5% significance levels, and at the 1% significance level, CO2 emissions are affected by E.C.G. In response, the relationship between CO2 emissions and E.C.G. is one-way in the granger sense. R&D has an effect on CO2, and CO2 has an effect on R&D. R&D also has an impact on E.C.G., and E.C.G. impacts R&D.

Table 7. Causality test.

4.5. Results of Cup-F.M. and Cup-B.C. test

The test results are shown in . The results show that the green finance index has a negative and significant correlation with CO2 emissions. In both scenarios, a 1% increase in G.F.N. reduces carbon emissions by 2.5% and 2.3%, respectively. While environmental pollution is rising in the B.R.I.C.S. countries, green finance is helping to lower it by increasing awareness of environmental issues and spreading cutting-edge technology. The negative green finance coefficient reveals U.S. financial institutions’ distribution of environmental protection capitals. Ecologically friendly practices benefit businesses and production facilities alike as a result. For M. Wang, Li, and Wang (Citation2021), free trade and financial transparency would bring in foreign investment and new R&D initiatives. As a result, green investments and financial obligations boost energy efficiency, reducing environmental pollution. The findings show strong negative association among R.E.U. consumption and environmental pollution. E.n.U. from renewable sources climbed by 1%, and environmental pollution decreased by 0.118% in the survey results. This decrease demonstrates that the use of non-fossil fuels has a negative correlation with CO2 emissions and that reducing CO2 emissions protects environmentally favourable quality. According to Ning et al. (Citation2022) for China, our findings align with their findings.

Table 8. Panel long run test using Cup-BC test and Cup-FM test results.

Carbon emissions fall by 0.302% for every 1% increase in R&D, according to the findings at a 1% significance level. The money spent on R&D contributes to the growth of new technologies. Furthermore, the B.R.I.C.S. countries’ environmental policies and technological advancements help to fuel industrial development by developing advanced environmentally friendly technologies. Technology advancements also lead to an increase in domestic revenue, which implies sustainable growth, while the coefficient of economic development is higher and positive when compared to other variables. This reflects the reliance on fossil fuels in the economy of the B.R.I.C.S. countries. Fossil fuels are bad for the environment and bad for the economy at the same time. A favourable correlation between G.D.P. and emissions has been discovered in the studies of Saeed Meo and Karim (Citation2021) and Hou et al. (Citation2022).

4.6. Robustness check

Several robustness tests are performed on the estimated results, including Canal’s fixed quantile regression technique and a substitute proxy indicator for the G.F.I., which investigates the disparity in the significant results. Substitute metrics for the G.F.I. are used to assess this research’s findings that employ three prime variables as G.F. benchmarks: green investment, green securities, and green credit. shows three prime variables, green investment, green credit, and green securities, and all had a significant and negative effect on carbon emissions, similar to the G.F.I. In conclusion, various G.F. measures have significantly influenced CO2 emissions. By reducing carbon dioxide emissions, G.F. improves the environment. As a result, we may be confident in our findings and draw the same conclusions as before.

Table 9. Robust analysis using original variables.

5. Conclusions and policy implications

The B.R.I.C.S. countries’ G.F.N. and climate change mitigation were examined in this study from 2000 to 2018. We used the quantile regression approach to determine whether these countries’ commitments to G.F.N. and climate change strategies differed between the two periods. We did so by providing a counterfactual hypothesis and then proving it by treating these countries differ in time periods. As a result, these countries formed the control and treatment groups. The assumption may collapse if there are unobserved time-varying factors. We used matching approaches such as the kernel, the radius matching, and the closest neighbour approach to determine the effects of the treatment on the countries in this case.

We have discovered that B.R.I.C.S. needs to address the systemic risks of climate change by mobilising the necessary financing to minimise these threats and repercussions. Because there is no correlation between green money and climate risk in B.R.I.C.S. nations, different approaches yielded different outcomes. Particularly in rising and developing economies, the problem of sustainability is of paramount importance (E.M.D.E.).

This one is of tremendous importance as a theoretical and empirical inquiry because it accomplishes both simultaneously. As a theoretical contribution to environmental protection literature, it must be discussed on its whole. This study investigates the growth of green finance in B.R.I.C.S. countries and its impact on environmentally friendly ventures, such as R.E.U. firms. The launch of various environmental initiatives due to the introduction of eco-friendly practices in credit, investment, and financial securities policies (both equity and debt securities) initiates the R.E.U. businesses in the economy. According to the report, the government’s investment in environmental protection technologies and procedures leads to the formation of R.E.U. firms by financially supporting them. Environmentally friendly economic and financial policies and their impact on the economy are the subjects of numerous previous research. But this research is a start because it looks at the same sections of the economy endangered by the COVID-19 outbreak. It focuses light on COVID-19's widespread use, its negative influence on the economy, and its issues, and finally proposes a remedy. Green finance and R.E.U. use and investment policies can be developed with the help of this study, which is beneficial for newcomers and regulators alike.

Eco-friendly adjustments to fiscal policies or financial regulations such as credit, securities, and investment policies lead them to boost environmentally-friendly enterprises like R.E.U. projects. It is possible to sustain environmental preservation by increasing E.C.G. and putting pressure on companies to release a corporate social report regularly. Additionally, this study serves as a theoretical guide for economists looking for ways to save the earth and people for future E.C.G. while simultaneously boosting R.E.U. investment. Furthermore, economists and policymakers can benefit from this research since it guides how to minimise the health-damaging effects of COVID-19 while maintaining the economy in light of the rise in green finances.

For these countries, access to G.F.N. and climate change initiatives would be supported by a number of variables. These countries’ G.D.P. per capita is critical to their efforts to mitigate the dangers of change. The B.R.I.C.S. countries’ E.C.G. and the success of their efforts to combat climate change and implement environmentally friendly macroeconomic policies are critical. Physical damage to infrastructure and degradation of the environment are just two examples of these dangers. According to regression results, G.F.N. and climate change mitigation measures in these countries are anticipated to be influenced by CO2, F.D.I., U.R.B. and investments in the energy sector. Emerging markets will likely be affected by the need to transition to a low-carbon future when creating and executing policies to cope with CO2 externalities. In addition, F.D.I. is a major driver of green funding, with the B.R.I.C.S. attracting a disproportionate amount of F.D.I. in the R.E.U. sector. The Human Development Index (H.D.I.) has become a criterion for countries obtaining green funding from multilateral development banks (M.D.B.s) or blended financing. Therefore, countries with high H.D.I.s are more likely to receive G.F.N. One of the most important outcome variables in attracting G.F.N. is the proxy for renewables usage in final energy demand. A significant amount of CO2 is emitted as a result of the high levels of energy intensity found in the B.R.I.C.S. countries. As a result, some of them have begun initiatives aimed at shifting their economy to one that relies heavily on R.E.U. sources. For example, the country’s low-carbon development effort was established by B.R.I.C.S (L.C.D.I.). Based on the findings, it’s recommended that you do as follows:

The B.R.I.C.S. countries must work together to establish an environment that encourages F.D.I. into G.F.N.

Governments must aid efforts to increase the market for bonds.

Green bonds should also be issued by non-corporate organisations such as pension funds in emerging and developing nations.

Finally, green bonds must be set up in accordance with the Green Bond Principles (G.B.P.). This would ensure full disclosure and the allocation of funds to initiatives and assets that positively impact the environment.

5.1. Limitations and future directions

There are also a number of limitations to this investigation. These constraints inspire future researchers and academics to provide insight into their field and take particular actions to eradicate them. To back up the findings, the researchers drew upon data from a single source. As a result, future researchers may have to address the issue of data sufficiency and correctness by compiling information from various sources. Also investigated in B.R.I.C.S. nations, emerging and low-middle-income economies is how implementing and executing green practices in finance contribute to investment in renewable projects. There may be discrepancies between these results in B.R.I.C.S. nations and industrialised economies. When COVID-19 prevails in an economy where green investment and securities are introduced, there is a tendency toward establishing and developing R.E.U. firms that may be traced to these findings. As a result, future researchers should be unable to draw the same conclusions from this study because of its lack of generalisability. Next-generation research should examine green development in financial fields and the impact of R.E.U. firms’ financial sources on a typical economy rather than an economy during a pandemic.

Disclosure statement

No potential conflict of interest was reported by the authors.

References

- Akomea-Frimpong, I., Adeabah, D., Ofosu, D., & Tenakwah, E. J. (2021). A review of studies on green finance of banks, research gaps and future directions. Journal of Sustainable Finance & Investment, 1–24. https://doi.org/10.1080/20430795.2020.1870202

- Arif, M., Hasan, M., Alawi, S. M., & Naeem, M. A. (2021). COVID-19 and time-frequency connectedness between green and conventional financial markets. Global Finance Journal, 49, 100650. https://doi.org/10.1016/j.gfj.2021.100650

- Baltagi, B. H. (2008). Forecasting with panel data. Journal of Forecasting, 27(2), 153–173. https://doi.org/10.1002/for.1047

- Bostian, M., Fare, R., Grosskopf, S., & Lundgren, T. (2016). Environmental investment and firm performance: A network approach. Energy Economics, 57, 243–255. https://doi.org/10.1016/j.eneco.2016.05.013

- Caballero-Morales, S. O. (2021). Innovation as recovery strategy for SMEs in emerging economies during the COVID-19 pandemic. Research in International Business and Finance, 57, 101396. https://doi.org/10.1016/j.ribaf.2021.101396

- Calvo-Gallardo, E., Arranz, N., & Fernandez de Arroyabe, J. C. (2021). Analysis of the European energy innovation system: Contribution of the framework programmes to the EU policy objectives. Journal of Cleaner Production, 298, 126690. https://doi.org/10.1016/j.jclepro.2021.126690

- Careri, F., Efthimiadis, T., & Masera, M. (2022). 2020–2022: Pivotal years for European energy infrastructure. Energies, 15(6), 1999. https://doi.org/10.3390/en15061999

- Chen, Q., Ning, B., Pan, Y., & Xiao, J. (2021). Green finance and outward foreign direct investment: Evidence from a quasi-natural experiment of green insurance in China. Asia Pacific Journal of Management, 1–26. https://doi.org/10.1007/s10490-020-09750-w

- Chen, X., Huang, C., Wang, H., Wang, W., Ni, X., & Li, Y. (2021). Negative emotion arousal and altruism promoting of online public stigmatization on COVID-19 pandemic. Frontiers in Psychology, 12, 652140. https://doi.org/10.3389/FPSYG.2021.652140/FULL

- Cline, B. N., Fu, X., & Tang, T. (2020). Shareholder investment horizons and bank debt financing. Journal of Banking & Finance, 110, 105656. https://doi.org/10.1016/j.jbankfin.2019.105656

- Council of the European Union. (2020). Volume 18 • Issue 1 • January 2020 ***EXCERPT*** 2.

- Deng, L., & Zhao, Y. (2022). Investment lag, financially constraints and company value – Evidence from China. Emerging Markets Finance and Trade. https://doi.org/10.1080/1540496X.2021.2025047

- Dong, F., Zhu, J., Li, Y., Chen, Y., Gao, Y., Hu, M., Qin, C., & Sun, J. (2022). How green technology innovation affects carbon emission efficiency: Evidence from developed countries proposing carbon neutrality targets. Environmental Science and Pollution Research International, 29(24), 35780–35799. https://doi.org/10.1007/s11356-022-18581-9

- Dong, S., Xu, L., & McIver, R. (2021). China’s financial sector sustainability and “green finance” disclosures. Sustainability Accounting, Management and Policy Journal, 12(2), 353–384. https://doi.org/10.1108/SAMPJ-10-2018-0273

- Guo, L., Zhao, S., Song, Y., Tang, M., & Li, H. (2022). Green finance, chemical fertilizer use and carbon emissions from agricultural production. Agriculture, 12(3), 313. https://doi.org/10.3390/agriculture12030313

- Hanafiah, M., Abdullah, R., Azrifah, M., Murad, A., Din, J., & Wahid, N. (2017). Infrastructure requirements for experience based factory model in software development process in a collaborative environment. Acta Informatica Malaysia, 1, 9–10.

- Hou, D., Chan, K. C., Dong, M., & Yao, Q. (2022). The impact of economic policy uncertainty on a firm’s green behavior: Evidence from China. Research in International Business and Finance, 59, 101544. https://doi.org/10.1016/j.ribaf.2021.101544

- Huang, C., Wu, X., Wang, X., He, T., Jiang, F., & Yu, J. (2021). Exploring the relationships between achievement goals, community identification and online collaborative reflection: A deep learning and Bayesian approach. Educational Technology & Society, 24, 210–223.

- IEA. (2020). Global Commission for urgent action on energy efficiency recommendations of the global.

- Ji, X., Cheng, Y., Tian, J., Zhang, S., Jing, Y., & Shi, M. (2021). Structural characterization of polysaccharide from jujube (Ziziphus jujuba Mill.) fruit. Chemical and Biological Technologies in Agriculture, 8(1), 1–7. https://doi.org/10.1186/S40538-021-00255-2/TABLES/2

- Johnes, J. (2006). Measuring teaching efficiency in higher education: An application of data envelopment analysis to economics graduates from UK universities. European Journal of Operational Research, 1993. https://doi.org/10.1016/j.ejor.2005.02.044

- Kapoor, A., Fraser, G. S., Carter, A. V., & Brooks, D. (2021). Overcoming divisive strategic environmental assessments for offshore oil and gas in Nova Scotia, Canada. Journal of Environmental Assessment Policy and Management, 23, 2250012. https://doi.org/10.1142/S1464333222500120

- Khan, M. A., Riaz, H., Ahmed, M., & Saeed, A. (2021). Does green finance really deliver what is expected? An empirical perspective. Borsa İstanbul Review. https://doi.org/10.1016/j.bir.2021.07.006

- Koenker, R. (2004). Quantile regression for longitudinal data. Journal of Multivariate Analysis, 91(1), 74–89. https://doi.org/10.1016/j.jmva.2004.05.006

- Kumar, R., & Agarwala, A. (2013). Energy certificates REC and PAT sustenance to energy model for India. Renewable and Sustainable Energy Reviews. https://doi.org/10.1016/j.rser.2013.01.003

- Lee, C., Chuan, L., & Chien, C. (2022). How does green finance affect green total factor productivity? Evidence from China. Energy Economics, 107, 105863. https://doi.org/10.1016/j.eneco.2022.105863

- Lee, C., Chuan, L., Chien, C., & Li, Y. Y. (2021). Oil price shocks, geopolitical risks, and green bond market dynamics. The North American Journal of Economics and Finance, 55, 101309. https://doi.org/10.1016/j.najef.2020.101309

- Lei, X.-t., Xu, Q.-y., & Jin, C.-z (2021). Nature of property right and the motives for holding cash: Empirical evidence from Chinese listed companies. Managerial and Decision Economics. https://doi.org/10.1002/MDE.3469

- Lemieux, V. L., Mashatan, A., Safavi-Naini, R., & Clark, J. (2021). A cross-pollination of ideas about distributed ledger technological innovation through a multidisciplinary and multisectoral lens: Insights from the Blockchain Technology Symposium ’21. Technology Innovation Management Review, 11, 58–66. https://doi.org/10.22215/timreview/1445

- Liu, H., Tang, Y. M., Iqbal, W., & Raza, H. (2022). Assessing the role of energy finance, green policies, and investment towards green economic recovery. Environmental Science and Pollution Research International, 29(15), 21275–21288. https://doi.org/10.1007/s11356-021-17160-8

- Liu, Z., Vu, T. L., Phan, T. T. H., Ngo, T. Q., Anh, N. H. V., & Putra, A. R. S. (2022). Financial inclusion and green economic performance for energy efficiency finance. Economic Change and Restructuring, 1–31. https://doi.org/10.1007/s10644-022-09393-5

- Lv, C., Bian, B., Lee, C. C., & He, Z. (2021). Regional gap and the trend of green finance development in China. Energy Economics, 102, 105476. https://doi.org/10.1016/j.eneco.2021.105476

- Lv, Z., Chen, D., & Lv, H. (2021). Smart city construction and management by digital twins and BIM big data in COVID-19 scenario. ACM Transactions on Multimedia Computing, Communications, and Applications. https://doi.org/10.1145/3529395

- Mngumi, F., Shaorong, S., Shair, F., & Waqas, M. (2022). Does green finance mitigate the effects of climate variability: Role of renewable energy investment and infrastructure. Environmental Science and Pollution Research, 1, 1–13. https://doi.org/10.1007/s11356-022-19839-y

- Mohsin, M., Taghizadeh-Hesary, F., Iqbal, N., & Saydaliev, H. B. (2022). The role of technological progress and renewable energy deployment in green economic growth. Renewable Energy, 190, 777–787. https://doi.org/10.1016/j.renene.2022.03.076

- Muganyi, T., Yan, L., & Sun, H. p (2021). Green finance, Fintech and environmental protection: Evidence from China. Environmental Science & Ecotechnology, 7, 100107. https://doi.org/10.1016/j.ese.2021.100107

- Nawaz, M. A., Seshadri, U., Kumar, P., Aqdas, R., Patwary, A. K., & Riaz, M. (2021). Nexus between green finance and climate change mitigation in N-11 and BRICS countries: Empirical estimation through difference in differences (DID) approach. Environmental Science and Pollution Research International, 28(6), 6504–6519. https://doi.org/10.1007/s11356-020-10920-y

- Ning, Q. Q., Guo, S. L., & Chang, X. C. (2021). Nexus between green financing, economic risk, political risk and environment: Evidence from China. Economic Research-Ekonomska Istraživanja, 1–25. https://doi.org/10.1080/1331677X.2021.2012710

- Ning, Y., Cherian, J., Sial, M. S., Álvarez-Otero, S., Comite, U., & Zia-Ud-Din, M. (2022). Green bond as a new determinant of sustainable green financing, energy efficiency investment, and economic growth: A global perspective. Environmental Science and Pollution Research, 1, 1–16. https://doi.org/10.1007/S11356-021-18454-7/TABLES/10

- Pedroni, P. (2001). Purchasing power parity tests in cointegrated panels. Review of Economics and Statistics, 83(4), 727–731. https://doi.org/10.1162/003465301753237803

- Pejović, B., Karadžić, V., Dragašević, Z., & Backović, T. (2021). Economic growth, energy consumption and CO2 emissions in the countries of the European Union and the Western Balkans. Energy Reports, 7, 2775–2783. https://doi.org/10.1016/j.egyr.2021.05.011

- Purnamawati, I. G. A. (2022). Sustainable finance for promoting inclusive growth. Jurnal Ilmiah Akuntansi, 6(2), 435. https://doi.org/10.23887/jia.v6i2.39208

- Pyka, I., & Nocoń, A. (2021). Banks’ capital requirements in terms of implementation of the concept of sustainable finance. Sustainability, 13(6), 3499. https://doi.org/10.3390/su13063499

- Quan, Q., Liang, W., Yan, D., & Lei, J. (2022). Influences of joint action of natural and social factors on atmospheric process of hydrological cycle in Inner Mongolia, China. Urban Climate, 41, 101043. https://doi.org/10.1016/j.uclim.2021.101043

- Rasoulinezhad, E., & Taghizadeh-Hesary, F. (2022). Role of green finance in improving energy efficiency and renewable energy development. Energy Efficiency, 15(2), 1–12. https://doi.org/10.1007/S12053-022-10021-4/TABLES/11

- Saeed Meo, M., & Karim, M. Z. A. (2021). The role of green finance in reducing CO2 emissions: An empirical analysis. Borsa İstanbul Review. https://doi.org/10.1016/j.bir.2021.03.002

- Sarma, P., & Roy, A. (2021). A scientometric analysis of literature on green banking (1995-March 2019). Journal of Sustainable Finance & Investment, 11(2), 143–162. https://doi.org/10.1080/20430795.2020.1711500

- Sharma, M., & Choubey, A. (2022). Green banking initiatives: A qualitative study on Indian banking sector. Environment, Development and Sustainability, 24(1), 293–319. https://doi.org/10.1007/s10668-021-01426-9

- Solarin, S. A., Al-Mulali, U., Musah, I., & Ozturk, I. (2017). Investigating the pollution haven hypothesis in Ghana: An empirical investigation. Energy, 124, 706–719. https://doi.org/10.1016/j.energy.2017.02.089

- Streimikiene, D., & Kaftan, V. (2021). Green finance and the economic threats during COVID-19 pandemic. Terra Economicus, 19(2), 105–113. https://doi.org/10.18522/2073-6606-2021-19-2-105-113

- Taghizadeh-Hesary, F., Zakari, A., Alvarado, R., & Tawiah, V. (2022). The green bond market and its use for energy efficiency finance in Africa. China Finance Review International, 12(2), 241–260. https://doi.org/10.1108/CFRI-12-2021-0225

- United Nations Environment Programme. (2017). On the role of Central Banks in enhancing green finance (pp. 1–27). United Nations Environment Programme.

- van Veelen, B. (2021). Cash cows? Assembling low-carbon agriculture through green finance. Geoforum, 118, 130–139. https://doi.org/10.1016/j.geoforum.2020.12.008

- Vinet, L., & Zhedanov, A. (2011). A “missing” family of classical orthogonal polynomials. Journal of Physics A: Mathematical and Theoretical, 44(8), 085201. https://doi.org/10.1088/1751-8113/44/8/085201

- Wang, C., Li, X.-w., Wen, H.-x., & Nie, P.-y. (2021). Order financing for promoting green transition. Journal of Cleaner Production, 283, 125415. https://doi.org/10.1016/j.jclepro.2020.125415

- Wang, F., Wang, R., & He, Z. (2021). The impact of environmental pollution and green finance on the high-quality development of energy based on spatial Dubin model. Resources Policy, 74, 102451. https://doi.org/10.1016/j.resourpol.2021.102451

- Wang, H., & Luo, Q. (2022). Can a colonial legacy explain the pollution haven hypothesis? A city-level panel analysis. Structural Change and Economic Dynamics, 60, 482–495. https://doi.org/10.1016/j.strueco.2022.01.004

- Wang, M., Li, X., & Wang, S. (2021). Discovering research trends and opportunities of green finance and energy policy: A data-driven scientometric analysis. Energy Policy, 154, 112295. https://doi.org/10.1016/j.enpol.2021.112295

- Wu, B., Monfort, A., Jin, C., & Shen, X. (2022). Substantial response or impression management? Compliance strategies for sustainable development responsibility in family firms. Technological Forecasting and Social Change, 174, 121214. https://doi.org/10.1016/j.techfore.2021.121214

- Ye, J., Al-Fadly, A., Huy, P. Q., Ngo, T. Q., Hung, D. D. P., & Tien, N. H. (2022). The nexus among green financial development and renewable energy: Investment in the wake of the Covid-19 pandemic. Economic Research-Ekonomska Istraživanja, 1–26.http://www.tandfonline.com/action/authorSubmission?journalCode=rero20&page=instructions. https://doi.org/10.1080/1331677X.2022.2035241

- Yigitcanlar, T., Kamruzzaman, M., Foth, M., Sabatini-Marques, J., da Costa, E., & Ioppolo, G. (2019). Can cities become smart without being sustainable? A systematic review of the literature. Sustainable Cities and Society, 45, 348–365. https://doi.org/10.1016/j.scs.2018.11.033

- Yu, C. H., Wu, X., Zhang, D., Chen, S., & Zhao, J. (2021). Demand for green finance: Resolving financing constraints on green innovation in China. Energy Policy, 153, 112255. https://doi.org/10.1016/j.enpol.2021.112255

- Yu, J., Tang, Y. M., Chau, K. Y., Nazar, R., Ali, S., & Iqbal, W. (2022). Role of solar-based renewable energy in mitigating CO2 emissions: Evidence from quantile-on-quantile estimation. Renewable Energy, 182, 216–226. https://doi.org/10.1016/j.renene.2021.10.002

- Zhang, D., Mohsin, M., Rasheed, A. K., Chang, Y., & Taghizadeh-Hesary, F. (2021). Public spending and green economic growth in BRI region: Mediating role of green finance. Energy Policy, 153, 112256. https://doi.org/10.1016/j.enpol.2021.112256

- Zhang, H., Geng, C., & Wei, J. (2022). Coordinated development between green finance and environmental performance in China: The spatial-temporal difference and driving factors. Journal of Cleaner Production, 346, 131150. https://doi.org/10.1016/j.jclepro.2022.131150

- Zhang, S., Wu, Z., Wang, Y., & Hao, Y. (2021). Fostering green development with green finance: An empirical study on the environmental effect of green credit policy in China. Journal of Environmental Management, 296, 113159. https://doi.org/10.1016/j.jenvman.2021.113159

- Zheng, G. W., Siddik, A. B., Masukujjaman, M., & Fatema, N. (2021). Factors affecting the sustainability performance of financial institutions in Bangladesh: The role of green finance. Sustainability, 13(18), 10165. https://doi.org/10.3390/su131810165

- Zhou, G., Zhu, J., & Luo, S. (2022). The impact of Fintech innovation on green growth in China: Mediating effect of green finance. Ecological Economics, 193, 107308. https://doi.org/10.1016/j.ecolecon.2021.107308

- Zimon, G., Sobolewski, M., & Lew, G. (2020). An influence of group purchasing organizations on financial security of SMEs operating in the renewable energy sector-case for Poland. Energies, 13(11), 2926. https://doi.org/10.3390/en13112926