Abstract

The objective of the article is twofold. Firstly, it evaluates the importance and significance of true and fair view (TFV)/fair presentation (FP) in European jurisdictions using IFRS standards. Secondly, it examines the potential role of TFV/FP for sustainability accounting and for aligning with the moral code of Islamic accounting. We assess whether we are at an important juncture in time where a common understanding of TFV/FP and the TFO could pave the way for increased understanding and harmonisation across all three frameworks.

Conventional accounting is examined in the context of TFV/FP. A survey shows significant acceptance of TFV in European jurisdictions using IFRS, but gaps exist, and reclarification of the concepts could be timely. Experts’ opinions on TFV in ‘conventional accounting’ can illuminate sustainability accounting, which could benefit from the application of these concepts. The introduction of sustainability accounting in IFRS is an opportunity to develop a unified understanding of the TFV/FP concepts across all three frameworks and conclude in stronger and connected base frameworks.

This is the first time that sustainability accounting development is considered as an opportunity to strengthen and unify the frameworks of conventional, Islamic and sustainability accounting through the common acceptance of principles-based concepts TFV/FP.

1. Introduction

This study examines the harmonisation of the ‘True and Fair View’ concept in European jurisdictions using IFRS standards. The study also examines the potential role of TFV/FP for sustainability accounting and for aligning with the moral code of Islamic accounting. The objective is to explore whether the TFV/FP concept could act as a harmonisation tool for sustainability, Islamic and conventional accounting to build a stronger support structure for the three frameworks.

The TFV has a long tradition in EU jurisdictions and has long been a cornerstone objective of financial statements. Preparers of financial statements are required to show a TFV in the financial statements to comply with the requirement of accounting standard setters and auditors are required to give an opinion as to whether the financial statements have succeeded in giving a TFV. In 1997, International Financial Reporting Standards (IFRS) moved from the term TFV to ‘Fair Presentation’ in order to coincide with references included by the Financial Accounting Standards Board (FASB). The International Accounting Standards Board (IASB) considers that TFV and FP are identical (IASB, Citation2008). Therefore, although IFRS changed the term from TFV to FP to align with the FASB references, the TFV still continues to be an objective for financial information. Both EU legislation and IFRS contemplate the override provision (departure from accounting standards in order to present a true and fair view), the former in exceptional circumstances and the latter in extremely rare circumstances.

IFRS and EU accounting standards rely on principles-based methods, developed from a principles-based Conceptual Framework (CF), and are subject to an override provision to depart from a standard, in extremely rare or exceptional cases respectively, in order to reach the objective of TFV. The true and fair view override (TFO) is a critical distinguishing feature between rule-based and principle-based accounting. For principles-based accounting to truly prevail, preparers and auditors need to recognise the need for, use and apply the TFO concept when necessary to arrive to TFV/FP. Strict compliance with standards does not always mean fulfilling the requirement of giving a TFV and faithfully representing the reality of the company (Aisbitt & Nobes, Citation2001; Alexander, Citation1993; Alexander & Eberhartinger, Citation2009; Garvey et al., Citation2021). Indeed, substance over form should be the genesis when financial statements follow the accounting rules but do not report its economic substance (Fischer et al., Citation2021).

Our primary focus is on gaining a better understanding of the TFV/FP concepts in European jurisdictions using IFRS standards. The evidence provides insights about TFV/FP concepts—are they aligned to a true principles-based approach or they are cornerstone concepts with limited and problematic application in practice. Using a survey from accounting experts in the context of IFRS, we gather their opinions and reflections around these cornerstone concepts in an IFRS context. The responses from accounting experts confirm the importance of TFV/FP for EU and IFRS financial reporting, but a lack of harmonisation in the understanding of the terms is noted. We believe that it is timely to go a step further. Firstly, TFV/FP, as a cornerstone concept in conventional accounting, should be clarified in order to mitigate potential bias in its practical application in EU jurisdictions. Secondly, TFV/FP creates an opportunity to build accounting standards on a similar base and unify accounting areas. Essentially, TFV/FP can act as an anchor concept between three accounting frameworks, ‘conventional’, ‘Islamic’ and ‘sustainability’. Therefore, as a second step we explore the role of TFV/FP as a harmonisation tool for sustainability, Islamic and conventional accounting to build a stronger support structure for the three frameworks.

Islamic accounting is an accounting framework which furnishes data empowering organisations to be managed according to the moral and ethical code of Islamic law. Sharia law supports the register of transactions with fairness, justice, and benevolence (Hassan et al., Citation2019). Therefore, it is built on two basic principles of justice and benevolence and one of the underlying principles behind Islamic reporting is transparency and completeness and clarity of reporting. Our study examines the role of TFV/FP in Islamic accounting, driven by the actual debate to facilitate the harmonisation of ‘Islamic accounting’ with what we call ‘conventional accounting’. In this context, the override provision, or the potential situations when standards could be overridden to reach a TFV is an important issue to advance a step further in this important research area. The TFO has also been explored in the context of Islamic accounting. The evidence reveals that TFV and TFO are applicable in Islamic accounting and not contradictory to the Shari’ah (Salihin et al., Citation2014, Citation2015).

Sustainability is currently recognised as an essential part of reporting to stakeholders due to its growing global importance. It extends the role of financial information to recognising the social and environmental impact of certain activities. Sustainability accounting is predicated on the principle of transparency, developed and anchored on a principles-based approach with the proposal for a CF base. Indeed, the final report published in March 2021 mentions faithful information as one of the qualitative characteristics (European Financial Reporting Advisory Group (EFRAG), Citation2021a, Citation2021b). Consequently, the TFV/FP and the TFO could have an important role in sustainability accounting and non-financial reporting. At this early stage, we consider it important to correctly define the role of TFV/FP to establish guarantee mechanisms for sustainability and non-financial information to comply with the objectives pursued and intended by the regulators. Otherwise, all the current efforts to regulate sustainability and non-financial information can be doomed to fail because they separate rather than unite the frameworks. The use of the TFV/FP for sustainability accounting from the preparers and audit perspective could improve the quality of sustainability reporting by preparers and auditors. Indeed, it would be ideal to use the advances in sustainability accounting to achieve consensus in the understanding of the TFV/FP concepts across all three accounting frameworks, becoming a basis for increased mutual acceptance of all three frameworks into the future.

This paper contributes to accounting research by recognising that the principle of TFV/FP has been and is a base pillar in accounting and guarantees the capacity of obtaining high quality financial information, even when accounting standards fail to do so. TFV/FP invites the use of professional judgement in the preparation of financial statements. It also allows company directors to assume full responsibility for the information content in the financial report. From the above, the auditor gives an opinion as to whether the content of the report reaches the objective of TFV/FP. Both Islamic and sustainability accounting are compatible with TFV/FP and there is an opportunity for TFV/FP to become the base for harmonising concepts for conventional, sustainability and Islamic accounting.

We believe the study can be useful for academia and standard-setters in developing a common language across all three accounting frameworks and also to assist preparers and academics who can compare and meditate the differences between countries and take measures to change education material for future professionals.

The remainder of the study proceeds as follows. The second section reviews TFV/FP in IFRS (conventional accounting). The third section explores the TFV/FP in other contexts (Islamic accounting and sustainability accounting). The fourth section introduces the empirical work (survey and participants), the fifth section explains and discusses the results, and the final section provides the conclusions.

2. True and fair view/fair presentation in conventional accounting

The TFV concept was introduced into EU legislation in 1978 through the IV Directive. It has its origin in the UK with different words from 1844 and was incorporated into the UK Companies Act in 1944. The term was originally included in IASC accounting standards as TFV but was replaced with FP in IFRS in the reform of the accounting standards in the 1990s. According to IAS 1 (IASB, Citation2019), financial statements shall present fairly the financial position, financial performance and cash flows of an entity. The standard also mentions that FP requires the faithful representation of the effects of transactions, other events and conditions in accordance with the definitions and recognition criteria for assets, liabilities, income and expenses set out in the Framework. The standard adds that the application of IFRSs, with additional disclosure when necessary, is presumed to result in financial statements that achieve a FP. IAS 1 contemplates the accounting standard departure in extremely rare circumstances.

Although IFRS replaced TFV with FP to align with the FASB references, TFV still continues to be an objective for financial information and has a long tradition. The IASB indicated that TFV/FP were the same (IASB, Citation2008). The EU Directive (Directive 2013/34/EU, OJEU, 2013) used the term TFV but the sentiment is similar to FP in IFRS and is applicable in the national legislation of EU member countries for non-quoted companies. EU legislation envisages overriding in exceptional circumstances, while IFRS indicates that it will only be appropriate in extremely rare circumstances.

IFRS are principle-based standards. According to the prestigious philosopher Dworkin (1977); a “policy” refers to a kind of standard that sets out a goal to be reached, generally an improvement in some economic, political, or social feature of the community “(…)”, while a “principle” refers to a standard, not because it will advance or secure an economic, political, or social situation deemed desirable, but because it is a requirement of justice or fairness or some other dimension of morality.

In the TFV literature, Garvey (Citation2012) states that the TFV should always be the objective when financial statements are prepared. In case of conflict, both the Directive and IFRS, with different approaches, recognise the possible departure from a rule or standard by the preparers of the financial information in order to arrive at a TFV. Respecting this degree of priority, Garvey (Citation2012) considers that from a European legislation point of view the TFV principle must take precedence over the rules. Van Hulle (Citation1997) mentions that the final answer on the meaning of this concept and its implications lies with the European Court of Justice.

If IFRS and EU standards rely on principles-based methods, developed from a principles-based CF and are subject to an overriding provision to depart from a standard or part of a standard which does not allow the financial statements to be presented according to the underlying accounting principles, then the TFO is accordingly a critical distinguishing feature between rules-based and principles-based accounting. For principles-based accounting to truly prevail, there must be clarity of understanding of the TFO concept and respect for and adherence to, its appropriate application.

There was considerable debate on the Principles versus Rules based approaches when FASB (US) and IASB formalised the Norwalk Agreement, a Memorandum of Understanding in 2002. Alexander and Jermakowicz (Citation2006) comment that the principles-based method tries to indicate what needs to be done, and in essence it is an attempt to help the preparer and the auditor not what to do, but how to decide what needs doing. Garvey (Citation2012) supports the importance of principles when it comes to preparing the financial information. Stuebs and Thomas (Citation2011) refer to the need to build judgement skills by practitioners under principles-based methods and the incentives for preparers to fulfil the judgement process. In an excellent paper published by Fischer et al. (Citation2021), which explains how the substance over form philosophy has lost importance in the FASB conceptual framework and reflects on the consequences for accountants, preparers and auditors. Hence, under the new umbrella it is not clear if accountants and auditors have ‘a right’ and ‘responsibility’ to look for the substance over form.

3. The role of TFV/FP in other contexts

3.1. True and fair view/fair presentation in Islamic accounting

In recent years, there has been debate about the use of IFRS for Islamic-based operations in order to improve and harmonise global financial information. According to CitationAnsari and Tabrazi (2018), accounting does not have a religion but may be faith driven, which is the case in Islamic accounting. Indeed, Bakr and Napier (Citation2022) interview 15 SMEs in Saudi Arabia and note that the majority of the participants reasoned that the religion logic could easily be accommodated rather than posing a challenge. Also, Franzoni and Ait Allali (Citation2018) focus on the convergence of religious principles of Islamic finance and the principles of Corporate Social Responsibility (CSR) proposed for conventional companies and find that the only element of divergence encountered regarding the conventional concept of CSR is the obligation for Islamic financial institutions to respect the principles and obligations established by Islam and apply them in their operations. However, it is not considered a stumbling block to the development of Islamic finance in conventional contexts, because of the mutual and intrinsic convergence of principles and concepts.

The IASB opened doors by considering that the underlying understanding of the contract is fundamental for the classification of the operation, but it closes them when it warns of the risks of the primacy of substance over form, based on the CF of financial information. In short, ‘substance over form’ is not considered a separate component of the principle of TFV/FP, among other things because it could be redundant. Indeed, faithful representation indicates that financial information represents the essence of a transaction and not only its legal form, in other words it is inbuilt in the qualitative characteristic of faithful representation. In reality, the substance over form issue is relevant for Islamic accounting, El-Gamal (Citation2006) explains how the form over substance juristic approach squanders the prudential regulatory content of premodern Islamic jurisprudence. Divergences from substance over form have been reorientated by standard setters where possible to comply with IFRS. The Accounting and Auditing Organisation for Islamic Financial Institutions (AAOIFI) guidance is a step in the right direction according to Maurer (Citation2010).

The AAOIFI refers to true and fair financial statements in its content on the General Presentation and Disclosure in the Financial Statements and Auditing Standards for Islamic Financial Institutions (Salihin et al., Citation2014). However, as Salihin et al. (Citation2014) explains the concept of TFV is merely mentioned but does not include a clarification or discussion. There are interesting academic constructions that try to facilitate the harmonisation of ‘Islamic accounting’ with what we call ‘conventional accounting’. It has been postulated to approve a provision that allows those entities to ‘override’ the accounting regulations in order to achieve a (or ‘their’) TFV. It has been investigated whether the principle-based and the override technique are compatible with Islamic law and the result has been positive (Salihin et al., Citation2014, Citation2015). The TFO could take two forms, instead of its usual singular form: (a) It could be applicable when IFRS make it difficult to comply with the requirements of Islam; (b) could be applicable (as a general rule) when the regulation or standard damages the TFV. In each case it would be necessary to explain if (a) or (b) applies, justify the option chosen and state the effect it could have on the financial statements. Proposals such as the one set forth would allow Islamic countries to ‘essentially’ comply with the IASB regulations without breaching the requirements of its legality.

Nowadays, applying the override according to the first classification (a) would mean that Islamic entities could not state that they conform to the IASB rules, which require compliance with all its regulations to guarantee their use. However, it is an important option, or at least a starting point, to solving the convergence issues between IFRS and Islamic accounting. From here, it is obvious that a third option, such as negotiating with the IASB the standards to which the override would apply to in order to comply with Islamic law must be considered. However, making exceptions is not the norm for the IASB (it was created for the opposite). Nonetheless, we must think that the third possibility presented, without guaranteeing accounting harmonisation, could be a stepping stone to reaching it without jeopardising essential issues and could be contemplated. This third option is similar to the possibility given by the UE member states to comply with TFV. More specifically it consists of developing a list of situations when standards could be overridden to reach a TFV. Although member states largely ignored this possibility it may be more appropriate for Islamic accounting because the differences between IFRS and Islamic accounting are now well focussed, and a list of these items have been identified.

The TFV concept and the override provision have been examined in Islamic accounting in order to understand the main consensus and divergences with conventional accounting and IFRS (Salihin et al., Citation2014, Citation2015). The override provision is not contrary to Shari’ah rules and can be applied in Islamic accounting and auditing. According to Salihin et al. (Citation2014), the requirement of including a TFV and TFO as a mechanism to improve accounting quality, requires greater responsibility by preparers and auditors but overall it is beneficial to financial reporting. CitationAnsari and Tabrazi (2018) point out that there are only a few minor differences between ‘conventional accounting’ and ‘Islamic accounting’ or more precisely there are a few additional considerations for Islamic accounting and Islamic finance accounting. According to the authors, one of the needs of Shari’ah based accounting is that the TFV is paramount for Shari’ah conscious users.

The substance over form debate is also important in Islamic accounting and further research is necessary here as Islamic financial contracts have very specific technical differences to conventional contracts and may not always comply to the substance over form requirement by IFRS. At the same time, the AAOIFI Accounting Board (AAB) identified possible problems with some contracts which may not comply with the substance over form philosophy and has implemented mechanisms so that they coincide and are applicable from 1 January 2020 under FAS 33 using the business model classification approach. However, it was stressed by experts in the discussions on standards relating to sukak contracts that issuers and investors should fully comply with Shari’ah rules and principles (AAOIFI, Citation2016). The case of sukak contracts has led to questions on whether they comply with the substance over form rule. According to Hanif (Citation2016), who examined five of the most widely used contracts in Islamic finance found that they complied in legal form with Islamic finance and were not very different to conventional products regarding their economic substance. More recently, Razak et al. (Citation2019) analyses the pricing of various sukuk contracts as important technical elements of sukuk and consider it essential to differentiate sukuk from conventional bonds and appreciate the spirit of Islamic finance. They also call for more research in the area of Islamic finance because there are important differences with conventional contracts and Islamic based contracts and that education and training is important to understand these products better. Although, this article does not focus on these specific types of contract, we consider it essential to go a step further in order to guarantee a convergence between Shari’ah rules and conventional accounting.

Assuming the importance of facilitating this complicated but possible convergence, the benefits are easily identifiable. Firstly, the growing importance of Islamic entities in the world is a fact and we must work so that their financial information is of quality and useful for decision-making. Secondly, we must reflect on the contribution of such entities to the global world and reflect on the lessons we can extract from the moral principles of Islamic society. The application of TFV/FP and the override provision could offer a solution to the convergence process of Islamic accounting to IFRS.

3.2. Sustainability accounting and principles based methods

The area of sustainability is currently recognised as an essential part of the information to be reported on to stakeholders due to its growing global importance and as a consequence many international organisations are examining their own involvement in the area. Schaltegger and Burritt (Citation2010) explain sustainability accounting as dealing with activities, methods and systems to record, analyse and report: First, environmentally and socially induced financial impacts; second, ecological and social impacts of a defined economic system (e.g., the company, production site, nation, etc.); and third, and perhaps most importantly, the interactions and linkages between social, environmental and economic issues constituting the three dimensions of sustainability.

Sustainable policies are explained from different frameworks such as legitimacy theory, stakeholder theory, agency theory (see e.g. Lassala et al., Citation2021). The empirical evaluation of sustainable reports shows confronting results in different settings. For example, Schiehll and Kolahgar (Citation2021) find that environmental, social and governance disclosure is value-relevant for investors and increasing financial materiality in reports helps to provide more informative stock prices.

However, this involvement has advanced in recent years and organisations have become involved due to global demand. In September 2020, the IASB issued a Consultation document on Sustainability Reporting (IFRS Foundation, Citation2020) to open up the discussion on several issues, including the possibility of creating a Sustainability Standards Board (SSB), the interaction with other institutions and initiatives, the possible scope of the SSB (IFRS Foundation, Citation2020). A total of 576 comment letters were received (IFRS Foundation, Citation2021), showing the interest in this theme and also the growing and urgent demand to improve the global consistency and comparability in sustainability reporting. A Trustee Steering Committee was set up to oversee the next phases of work, and the area of climate is to be given priority (IFRS Foundation, Citation2021).

Sustainability standards on climate would be given priority and then other standards would be progressively introduced. This new standards board will operate under a principles-based approach to coincide with the IASB. Initially, a specific Conceptual Framework (CF) for sustainability standards will be prepared. Zyznarska-Dworczak (Citation2020) point out that a CF for sustainability accounting is important as part of a principles-based accounting method, although it would contain similar areas as the IASB CF, for example the materiality principle which is especially important in the area of climate due to the risks involved. It seems that an independent CF would be necessary. The existing frameworks include the Task Force on Climate-related Financial Disclosures (TCFD), the Sustainability Accounting Standards Board (SASB), the International Integrated Reporting Council (IIRC) and the Sustainable Development Goals Disclosure recommendations (SDGD).

We consider that relevance and faithful representation should be included in the fundamental characteristics of sustainability information. Gonzalo-Angulo and Garvey (Citation2015) explain that sustainability information should respect the principles related to sincerity and obtain a balance between the quantity and relevance of the information. They also refer to the importance of an independent audit to ensure the credibility of this sustainability information. Grey (Citation2019) points out that in the area of sustainable accounting information, the quality and reliability of the accounts is the most important part, more than who prepares it. Bebbington and Unerman (Citation2020) find that accounting practices are seemingly unable to account for the interconnections and interdependencies taking place within the natural system in which organisations operate. Accounting practices therefore need to find a way to disclose these interconnections and interdependencies, and TFV/FP could be the key to reaching the solution while methods and models are being developed but at the same time securing useful and quality financial information.

The European Financial Reporting Advisory Group (EFRAG) is also involved in sustainability accounting. It is responsible for the technical preparation of the development, adaptation, and implementation of European standards for non-financial reporting. The progress report calls for more homogeneous and clear definitions and principles. Again, we can see the development of the non-financial information using a principles-based approach. There is no reference to TFV and TFO which we would again expect to play an important part in the overall objective of non-financial information coinciding with the objective of EU financial information. Based on almost 100 initiatives, the report reveals important conceptual differences, and some require clarification such as materiality and the scope of the information (qualitative and quantitative). The most widely used sustainability standards are those issued by the Global Reporting Initiative (GRI) that support and offer help to the EU initiative for separate non-financial reporting standards (GRI, Citation2021). The final report issued in March 2021 (EFRAG, Citation2020, Citation2021), is similar to the progress report in terms of principles-based methods, also includes a reference to faithful information but not to TFV. A tentative roadmap is also included for the development and application of the new sustainability standards. The ‘core’ standards should be ready for application for reports published in 2024 and for ‘advanced’ topical standards for reports published in 2025.

At this early stage, the sustainability scenario offers an ideal opportunity for studying more policy-relevant research, specifically about the current sustainability reporting standard-setting process, the connection between the potential adoption of ISSB (International Sustainability Standards Board) standards and the proposals issued by different accounting bodies (IFRS Foundation and EC/EFRAG) and the role played by different actors, including consultancy and assurance services, in disseminating the ideas and developing the practices proposed by accounting bodies (Giner & Luque-Vílchez, Citation2022).

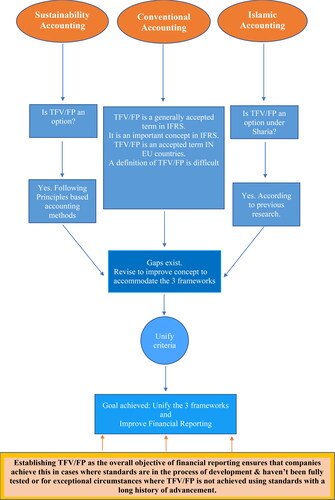

In sum, sustainability is a growing area of interest. The advances are anchored on a principles-based approach with the proposal for the incorporation of a CF. We expect this CF to include similar objectives and qualitative characteristics to those of IFRS with some special attention to sustainability. We also expect similarities in the presentation of sustainability information to coincide with IAS 1 and therefore give importance to the TFV/FP and TFO aspects of the information. In fact, we consider that the TFO is much more important where standards are not fully developed and applied in practice to obtain a TFV of the information. This is especially true in the critical area of materiality, where models are being introduced slowly and are highly subjective. The TFV/TFO can be a fundamental principle for confiding in the information disclosed. summarises the study framework.

Figure 1. Study framework.

Source: Own.

4. Method: participants and survey

The perceptions of TFV/FP are tested using an online survey through a panel of 29 accounting experts representing 24 European countries. The participants were chosen from the authors (or substitute experts) of the articles published in Accounting in Europe (AIE) for a special volume dedicated to examining the current Status of IFRS in European jurisdiction.Footnote1 The AIE journal selected an expert in the field in each jurisdiction.Footnote2 The survey was administrated during the first semester 2019 and the response rate was 66%. The participants received a cover letter, which outlined the objectives of the project and assured participants of confidentiality.

The countries represented are Austria, Belgium, Croatia, Cyprus, Czech Republic, Denmark, Finland, France, Germany, Greece, Ireland, Italy, Malta, Netherlands, Norway, Poland, Portugal, Romania, Slovenia, Spain, Sweden, Switzerland, Turkey and UK. In 2005, the EU adopted IFRS for the consolidated financial statements of listed companies. The exception is Malta that adopted IFRS in 1998. Norway, Switzerland and Turkey are non-EU member states; however, they comply with IFRS. The UK forms part of the group of EU members because UK was a member at the time of the study. The countries represented belong to this which follow common law and civil law regimes.

The survey is designed to capture the perceptions of TFV/FP through seven closed-form questions organised in two subsections: FP in IFRS and local GAAP (questions 1–5), and definition of TFV/FP concepts (questions 6–7). The respondents rated the participants´ opinions on a five-point Likert scale (from 1 ‘strongly disagree’ to 5 ‘strongly agree’) but there is also a space to express personal opinions in each question. The survey also includes some questions relating to the participants´ characteristics. We examine the frequencies of each item, the mean and the standard deviation. We also examine the expert’s comments manually one by one due to the quality of the responses. We classify the comments according to the expert’s opinion.

5. Results

5.1. Descriptive statistics

shows the participants’ characteristics. The number of participants is 29. In terms of gender, 12 participants are females, and 17 participants are males. The mean number of years of academic experience is 22.07. There are also 12 participants that belong to a Professional Organisation. The mean number of years of affiliation is 27.50, this indicates a high level of expertise and experience in the field. It is also noted that 25 participants have professional experience, mainly in Audit and Accounting but also in the Banking and Insurance industry and in Regulation and Compliance. The mean number of years of professional experience is 12.78.

Table 1. Descriptive statistic.

5.2. Question analysis per section

Section 1. FP in IFRS and in local GAAP

Q1. In your opinion Fair Presentation (FP) is an accepted and generally applied term in IFRS (IASB).

Q2. In your opinion TFV/FP have lost importance for IFRS.

Q3. Under IFRS, the ‘Fair Presentation’ notion is identical to the notion of ‘True and Fair View’ which was used previously.

Q4. In your opinion, TFV should be replaced by FP in order for the terminology to coincide with IFRS.

Q5. The true and fair view (TFV) is a consolidated term in your country’s GAAP.

shows that over 75% consider that FP is an accepted and generally applied term in IFRS (IASB); however, there are some participants that disagree with this question (Q1). A much higher percentage would have been expected in this case. We find some interesting opinions:

Table 2. Results of FP in IFRS and in local GAAP.

Comments in disagreement category

Fair presentation seems weaker by omitting Truth.

The IASB explicitly uses different terms, such as relevance and faithful representation, to define quality in financial statements

Comments in agreement category

I think and hope that it is the generally aim of the presentation rules.

I don’t see how anyone could disagree with this.

From the disagreement perspective, the experts justified their opinions based on reference to faithful representation. It is important to clarify that the terms of relevance and faithful representation are included in the CF dealing with the quality of Financial Information rather than the requirements for Presenting Financial Statements which are included in IAS 1. Definitely, these terms should be taken into account when taking fundamental decisions, but the CF does not override the requirement of IAS 1 to show a TFV/FP. From the agreement perspective, the answers are clear, and in some cases the expert’ argument is strong (see last comment).

exhibits that there was a 65% disagreement to Q2 referring to the loss of importance of TFV/FP in IFRS, so experts consider that IFRS continues to give importance to this term. If experts consider the principle to be important, we would have considered a much higher agreement to this question. Some clarifications are obtained:

Comments in disagreement category

It’s important that fair values (FV) have conceptual underpinnings in IFRS.

The de-emphasis if it has occurred, must be a contributing factor to market indiscipline and inefficiencies.

Comments in agreement category

Standard setting has become rules driven

From the disagreement opinion, some experts mention the importance of conceptual terms when dealing with FV and the market inefficiencies and indiscipline as being a guilty factor if the de-emphasis occurred showing here that the expert is uncertain that a change in the importance of the concept actually occurred. An interesting comment in the agreement category is the fact that standard setting has become rules driven which might explain a disinterest for open concepts such as TFV/FP.

Q3 examines whether the FP notion and the TFV (previously used by IASB) were identical. In this case, the agreement is around 50% and the disagreement is around 31%. It is also noted that experts responding from common law countries are in disagreement with a percentage of 75% while no experts agreed with the question and 25% answered indifferently supporting the stand-alone position of this concept in these countries. Q4 reveals that over 41% were undecided, 34.48% were in disagreement and 24.14% agreed with the question ().

Table 3. Results of the need for a definition of TFV/FP.

In general, the comments renew the interest of the translation of TFV, the terminology used in the IFRS context and its interpretation. As local GAAPs differ in certain aspects from IFRS translations and terminology, it could create bias and misinterpretation. As mentioned before, the debate started some decades ago and is still open (Aisbitt & Nobes, Citation2001; Alexander, Citation1993; Alexander & Eberhartinger, Citation2009; Gonzalo-Angulo et al., Citation2018).

Q5 shows that 20 experts (71.43%) consider that TFV is a consolidated term in their country’s GAAP. Interestingly, no participants answered that they strongly disagree with the question and only six participants disagree with the question (). Some experts’ comments are:

Comments in disagreement category

The TFV holds a very specific meaning in Germany, the actual translation would more like "a presentation of assets, finance and profitability’s that corresponds to the actual current status"

Included in the law, but without definition

Comments in agreement category

It is for accounting standard setters and auditors and enforcers. It is not in the legal field

TFV in Belgium is very much coloured by fiscal considerations

It is a concept that was introduced with the adaptation of the Portuguese accounting plan to the EU accounting directives

Faithful Image in its Spanish version

It is an overarching or capstone concept.

The experts’ comments in the disagreement section show the fact that it does not come with a definition and the expert from Germany shows that the country has never really been able to consolidate this term into its local legislation as required by EU legislation. The comments in the neutral and agreement categories expose some interesting clarifications referring mainly to their specific country or jurisdiction (not reported due to limited space). The responses raise concerns again about the translation and terminology used in the IFRS context and its rooted concepts in many jurisdictions that impede a complete integration.

Considering participants´ characteristics (professional experience outside academia and whether they are members of a Professional Organisation or Standard Setting Body or other) and country origin (common law vs civil law legal regimes), we find some interesting results.

In Q4, TFV should be replaced by FP, 75% of experts responding from common law countries answered negatively to this question, no experts agreed with the question and 25% answered indifferently supporting the stand-alone position of this concept in these countries. In Q2, TFV/FP have lost importance for IFRS, 68% of experts with professional experience disagreed with this question as against 16% in agreement. Those with no professional experience were 50% in disagreement and 25% in agreement with this question. The results show that being a member of a Professional Organisation or Standard Setting Body or other is important in the survey. For example, in Q2, TFV/FP have lost importance for IFRS, shows that members of PO have a higher level of disagreement to this question (more than 83%) and only one expert agrees with the question. In contrast, the percentage of disagreement from non-PO members is nearly 53%. In Q4, TFV should be replaced by FP, more than 58% of experts who are members of a professional body disagreed with this question. In Q5, TFV is a consolidated term in your country’s GAAP, almost 91% of experts that are members of PO answered in agreement with this question.

We could conclude from the above results that experts consider that FP/TFV is important in IFRS and that in general the terms are integrated in their countries GAAP and they do not seem to give too much importance to the terms used. However, we find some differences between countries, which opens an opportunity for revising and unifying concepts and understanding for the future.

Section 2. The need for a definition of TFV/FP

Q6. In your opinion the creation of a definition of TFV/FP in relation to the annual accounts is a very difficult task.

Q7. In your opinion, it is not necessary to have a definition of TFV/FP.

(Q6) shows that almost 70% agreed that it is difficult to define this concept. There was complete agreement to the question from experts from Common law countries. Some clarifications are obtained:

Comments in disagreement category

Use the conceptual framework

The definition is not a problem (something like 'presentation of financial performance and financial position that allow users to make adequate judgements regarding the entity’), the application is a challenge.

Comments in agreement category

Yes, it is a very difficult task but this is what accounting is supposed to do.

The whole point is that it should not be defined.

I'm not sure that such a definition would improve it

Very difficult but still worthwhile. It is a term of art, a philosophical construct as well as a rubric of professional practice. This is the nature of judgement as opposed to a programmable algorithm.

Professional accountants are remunerated to make such judgements, and hold themselves out as capable of doing so to clients, to markets and to wider society.

(Q7) shows that almost 50% disagree with this question and 38% agree showing that there is more desire to have a definition of the term. There was 50% agreement from experts from common law countries.

The segmentation of the participants according to whether they are members of a Professional Organisation or Standard Setting Body or other, and country origin (common law vs civil law legal regimes), reveals interesting results.

In Q6, the creation of a definition of TFV/FP in relation to the annual accounts is a very difficult task, there was complete agreement to this question from experts from common law countries. In Q7, it is not necessary to have a definition of TFV/FP, there was 50% agreement from experts from common law countries, but the highest level of agreement (57%) came from mature experts. Also, in Q7, the highest level of disagreement came from experts who were not members of a professional body.

There is clearly a difference of opinion, some experts consider that a definition of TFV is necessary and strict indications need to be provided on how to reach a TFV. Other experts consider that precisely due to its nature a definition is not necessary and furthermore, would not be appropriate. This latter opinion is in line with IAS 1.

5.3. Discussion

The responses show that TFV/FP is important in IFRS and in general it is integrated into the GAAP of the different countries being represented in the survey. However, it is noted that there are different approaches to comprehend how TFV/FP should be applied which question its harmonisation.

There continues to be tax implications in accounting terms which could have been smoothed out at this point. Some experts bring up the issue of preference for the reference to truth in the term and on a more positive note some refer to TFV/FP as the overall objective of financial information. Other experts comment that TFV has been forgotten in order to concentrate on tax areas in accounting. Experts brought up issues about accounting becoming more rules based and some argued as to the choice of words used to describe the principle.

Some experts also mention the desire for a definition of the terms and find it difficult to deal with open terms involving flexibility as those under analysis. Indeed, some experts mentioned that a definition was not necessary for several reasons and others expressed the difficulty in creating one but that it was worthwhile having one. Considering the necessity to have a definition of TFV/FP almost 50% confirmed this need, and the comments justified the possibility of having a definition of some sort. Carnegie et al. (Citation2021) reflect that accounting definitions have evolved but they do not adequately reflect accounting as a social and moral practice but rather continue to position accounting as a technical practice. We add to this debate by incorporating TFV/FP to be revised so as to be correctly harmonised in Islamic and sustainability accounting.

This paper complements previous studies in the field. Most of them find a lack of harmonisation in the application of the TFV in their jurisdictions previous to the incorporation of IFRS. Nobes and Parker (Citation1991) find that most of the directors of large UK firms did not take specific action to make operational the TFV concept, relying on auditors for compliance with standards and less attention is paid to the requirement to achieve a TFV. Hence, they observe that few directors depart from standards to give a TFV. Garvey et al. (Citation2017) detect different cognitive structures between academics and students when several aspects of TFV are tested. Gonzalo-Angulo et al. (Citation2018) find that auditors in public practice and Spanish students are more in favour of following the accounting standards than applying the TFO provision. They also note differences due to participant’s professional status and maturity.

The experience of the sample participants in the accounting and regulation field creates an opportunity to fully understand the role of TFV/FP which is valuable as a base for analysis. Indeed, the accounting experts consider that TFV/FP is important in IFRS and the terms are integrated in their jurisdictions. In this context, if ‘conventional accounting’ has been able to provide solutions to complex problems during the last 200 years, then, we can learn some lessons from the past. We consider that it is important to take advantage of the accounting experts’ opinions and include similar concepts in sustainability accounting. This can help to provide the mechanisms to comply with the objectives pursued by the regulators in the area of sustainability and non-financial information. Otherwise, the current efforts to regulate sustainability and non-financial information can be subject to divergence, rather than a harmonisation, from other accounting frameworks.

Actually, a crucial question is the importance of TFV/FP in sustainability accounting. We consider a standard similar to IAS 1 on the Presentation of Sustainability Information and its overall objective to give a TFV/FP including TFO where necessary is appropriate and necessary. Hence, a principles-based accounting method for sustainability accounting with a CF is appropriate for sustainability accounting to achieve a similar accounting process and avoid disconnecting it as an entirely separate accounting area. Assuming that the final objective of financial reporting is to achieve a TFV/FP, and sustainability accounting is an area very sensitive to risk, the role and importance of TFV/TFO could be enhanced in order to improve decision making by users.

Also, the experts’ opinions from ‘conventional accounting’ have implications for Islamic accounting where the TFV/FP and override provision are not incompatible with the legislation. As renowned Islamic academics (CitationAnsari & Tabrazi, 2018; Salihin et al., Citation2015) have pointed out, it is desirable to continue making progress in this important research area due to the benefits for the quality of financial information. Sustainability accounting offers the opportunity to revisit the concept, to unify criteria in ‘conventional accounting’, to incorporate Islamic accounting and harmonise the three frameworks.

If convergence is achieved between IFRS and Islamic accounting, then convergence on sustainability accounting should be more straightforward for Islamic accounting. From an Islamic perspective, investment must comply with the principles of the Shari’ah by funding environmental-friendly projects that encourage economic growth and protect the environment. Starting with this base and complying with the TFV for more disclosures or using the override provision should be an advantage to more harmonised standards. These premises could offer inspiration to standard setters around the world in relation to sustainability accounting. Franzoni and Ait Allali (Citation2018) state that CSR may be the element of convergence for ‘conventional’ and Islamic accounting.

So, bringing together the issues, where are we at this point? The authors believe that the TFV/FP can play an important role in developing a common framework across conventional Islamic and sustainability accounting. The opinions of experts on TFV/FP in ‘conventional accounting’ can illuminate progress in these two areas offering valuable solutions using over 200 years of experience. The concept is not incompatible with Islamic accounting and is in line with its underlying philosophy. Therefore, this concept could help to bring Islamic accounting closer to IFRS standards. Also, the concept and its overriding provision is an important aspect of principles-based accounting methods and could help to achieve the objectives of sustainability accounting. The conclusions from the experts can be extrapolated to the other two areas which would benefit from the accumulated experience of ‘conventional accounting’. The current developments in sustainability accounting are an opportunity to review the concepts by the IASB to ensure unification of the three frameworks. Next steps should be the coming together of policymakers and practitioners of all three frameworks to explore and develop a common understanding around these concepts.

Finally, we believe this research can be useful for academia and standard setters in considering the current status of the concepts, and also to preparers and academics who can compare and meditate the differences between countries and take measures to change education material for future professionals.

6. Conclusions

The main conclusion of the study is that TFV/FP are still important in financial accounting, but a full harmonisation has never been achieved. In this respect we consider our research timely to propose a harmonisation of the understanding and applicability of the concepts, a process which could foster alignment of IFRS and Islamic accounting rules and provide a stronger base for developing new standards for sustainability accounting. This harmonisation incorporating Islamic accounting will undoubtedly have advantages for global financial reporting. There is little previous research dealing with the unification of frameworks in accounting and this is a limitation to our study, and feedback from all experts contacted in IFRS would have added to this study. However, the fact that they have a high level of expertise justifies this small sample size, indeed experts have also observed that given the novelty of the sustainability reporting standard-setting process, even purely conceptual works and studies based on limited empirical evidence—for which the EU offers a unique scenario to explore the usefulness of a broad approach to sustainability reporting—would be welcome additions to the literature (Giner & Luque-Vílchez, Citation2022).

As sustainability accounting grows and researchers develop fundamental views, we consider that effort should be made to achieve a harmonised understanding of these requirements and not have them dealt with in an ‘a la carte’ fashion (Garvey et al., Citation2021). This consensus has to be from an educational point of view on how to reach the overall objective. TFV/TFO can assist preparers and auditors for sustainability accounting to reflect a company’s true situation to improve the overall quality of financial information.

The TFO provision is even more important for areas in early development as the standards are not perfected and the need to abandon them to show a TFV/FP may be more necessary than in more refined and widely applied areas. This is especially true in areas of high risk and where materiality is important.

Our analysis concludes that a consensus definition or a revision of the guidelines for showing TFV/FP financial statements would bring much needed clarity for users of IFRS. We contend that this consensus definition/guidelines could also have a role in both Islamic accounting and sustainability accounting and could serve to forge a greater level of understanding across all three frameworks. Using a common framework to account for Islamic and conventional products and transactions would enhance the transparency and international comparability of financial reporting for Islamic finance. The principles nature of IFRS should make it possible to recognise, measure, and disclose the economic substance of Islamic finance without compromising Shari’ah principles. There cannot however be ambiguity around the key principles. Likewise, as sustainability accounting develops, the TFV/FP, which is a universal principle linked to transparency in commercial law, can firstly fill loopholes in sustainability standards; secondly, allow the interpretation of the standards focussing on an objective of transparency; and thirdly, given its flexibility it allows for the harmonisation and unification of diverse systems. Let it be built on rock solid principle-based foundations and not on sandy soil which can cause instability. We recognise that there may be a long road ahead but it is important to take the first steps.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

Notes

1 The Role and Current Status of IFRS in the Completion of National Accounting Rules – Evidence from European Countries.

2 These authors have articles published in first-tier journals, and they were specifically invited by the journal to write on IFRS in their country. They are also associated with (or have occupied) relevant positions in accounting institutions.

References

- Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI). (2016). Exposure Draft Financial Accounting Standard No. 29 Sukuk Issuance. Retrieved 10 November, 2022, from http://aaoifi.com/wp-content/uploads/2017/03/Sukuk-standard-with-BOC-v5-.pdf

- Aisbitt, S., & Nobes, C. (2001). The true and fair view requirement in recent national implementations. Accounting and Business Research, 31(2), 83–90. https://doi.org/10.1080/00014788.2001.9729603

- Alexander, D. (1993). A European true and fair view? European Accounting Review, 2(1), 59–80. https://doi.org/10.1080/09638189300000004

- Alexander, D., & Eberhartinger, E. (2009). The True and Fair View in the European Union. European Accounting Review, 18(3), 571–594. https://doi.org/10.1080/09638180902784405

- Alexander, D., & Jermakowicz, E. (2006). A true and fair view of the principles/rules debate. Abacus, 42(2), 132–164. https://doi.org/10.1111/j.1467-6281.2006.00195.x

- Ansari, O. M., & Tabrazi, H. (2018). IFRS and the Shari’ah Based Reporting: A Conceptual Study. AAOIFI, Manama, Kingdom of Bahrain. https://lnkd.in/eX7EUbD.

- Bakr, S. A., & Napier, C. J. (2022). Adopting the international financial reporting standard for small and medium-sized entities in Saudi Arabia. Journal of Economic and Administrative Sciences, 38(1), 18–40. https://doi.org/10.1108/JEAS-08-2018-0094

- Bebbington, J., & Unerman, J. (2020). Advancing research into accounting and the UN sustainable development goals. Accounting, Auditing & Accountability Journal, 33(7), 1657–1670. https://doi.org/10.1108/AAAJ-05-2020-4556

- Carnegie, G., Parker, L., & Tsahuridu, E. (2021). It’s 2020: What is accounting today? Australian Accounting Review, 31(1), 65–73. https://doi.org/10.1111/auar.12325

- Dworkin, R. (1977). Taking rights seriously. Cambridge, Mass: Harvard University Press.

- El-Gamal, M. A. (2006). Islamic finance: Law, economics, and practice. Cambridge University Press.

- European Financial Reporting Advisory Group (EFRAG). (2021). Proposals for a relevant and dynamic EU sustainability reporting standard setting. https://www.efrag.org/Assets/Download?assetUrl=%2Fsites%2Fwebpublishing%2FSiteAssets%2FEFRAG%2520PTF-NFRS_MAIN_REPORT.pdf.

- European Financial Reporting Advisory Group (EFRAG). (2020). European Lab PTF-NFRS Progress Report (up to 31 October 2020). https://www.efrag.org/Assets/Download?assetUrl=/sites/webpublishing/SiteAssets/PTF-NFRS%20Progress%20Report%20Final.pdf.

- Fischer, D., Ellman, O., & Schochet, S. (2021). The Decline of Substance over Form in Accounting. Accounting, Economics-A Convivium, 1–18. https://doi.org/10.1515/ael-2019-0052

- Franzoni, S., & Ait Allali, A. (2018). Principles of Islamic finance and principles of corporate social responsibility: What convergence? Sustainability, 10(3), 637. https://doi.org/10.3390/su10030637

- Garvey, A. (2012). Los antecedentes de la imagen fiel y su aplicación en España [The origins of True and Fair View and its application in Spain]. Dykinson.

- Garvey, A., Gonzalo Angulo, J. A., & Parte, L. (2017). Cognitive Load Theory: Limiting the gap between academics and students in accounting and auditing. Revista de Ciências Empresariais e Jurídicas (RCEJ), 28, 5–28. https://doi.org/10.26537/rebules.v0i28.1024

- Garvey, A. M., Parte, L., McNally, B., & Gonzalo-Angulo, J. A. (2021). True and fair override: Accounting expert opinions, explanations from behavioural theories, and discussions for sustainability accounting. Sustainability, 13(4), 1928. https://doi.org/10.3390/su13041928

- Giner, B., & Luque-Vílchez, M. (2022). A commentary on the “new” institutional actors in sustainability reporting standard-setting: a European perspective. Sustainability Accounting, Management and Policy Journal, 13(6), 1284–1309. https://doi.org/10.1108/SAMPJ-06-2021-0222

- Global Reporting Initiative (GRI). (2021). GRI Backs EU Proposal for Separate Pillar on Non-Financial Reporting. https://www.globalreporting.org/about-gri/news-center/2021-01-15-gri-backs-eu-proposal-for-separate-pillar-on-non-financial-reporting/.

- Gonzalo-Angulo, J. A., & Garvey, A. M. (2015). El informe de Gestión: Validez y perspectivas. Revista de Contabilidad y Dirección, 1, 34–39.

- Gonzalo-Angulo, J. A., Garvey, A., & Parte, L. (2018). Perceptions of true and fair view: Effects of professional status and maturity. In A. Pinto, & D. Zilberman (Eds.), Modelling, dynamics, optimisation and bioeconomics III (vol. 224, pp. 159–186). Springer. https://doi.org/10.1007/978-3-319-74086-7_8

- Grey, R. (2019). Towards an ecological accounting: Tensions and possibilities in social and environmental accounting. In F. Birkin, & T. Polesie (Eds.) Intrinsic capability. University of St Andrews. https://doi.org/10.1142/9789813225589_0005

- Hanif, M. (2016). Economic substance or legal form: An evaluation of Islamic Finance Practice. International Journal of Islamic and Middle Eastern Finance and Management, 9(2), 277–295. https://doi.org/10.1108/IMEFM-07-2014-0078

- Hassan, M. K., Aliyu, S., Huda, M., & Rashid, M. (2019). A survey on Islamic Finance and accounting standards. Borsa Istanbul Review, 19(S1), S1–S13. http://www.elsevier.com/journals/borsa-istanbul-review/2214-8450 https://doi.org/10.1016/j.bir.2019.07.006

- IASB. (2008). Exposure Draft Conceptual Framework for Financial Reporting: The Objective of Financial Reporting and Qualitative Characteristics and Constraints of Decision-Useful Financial Reporting Information, on May, 29.

- IASB. (2019). IAS 1: Presentation of Financial Statements. International Accounting Standards Board. http://eifrs.ifrs.org/eifrs/ViewContent?num=1&fn=IAS01_TI0002.html&collection=2019_Issued_Standards.

- IFRS Foundation. (2020). Consultation paper on Sustainability Reporting. https://cdn.ifrs.org/-/media/project/sustainability-reporting/consultation-paper-on-sustainability-reporting.pdf.

- IFRS Foundation. (2021). Consultation on Sustainability Reporting, IFRS Advisory Council February. https://cdn.ifrs.org/-/media/feature/meetings/2021/february/advisory-council/ap-02-sustainability-feb-2021.pdf.

- Lassala, C., Orero-Blat, M., & Ribeiro-Navarrete, S. (2021). The financial performance of listed companies in pursuit of the Sustainable Development Goals (SDG). Economic Research-Ekonomska Istraživanja, 34(1), 427–449. https://doi.org/10.1080/1331677X.2021.1877167

- Maurer, B. (2010). Form Versus Substance: AAOIFI Projects and Islamic Fundamentals in the Case of Sukuk. Journal of Islamic Accounting and Business Research, 1(1), 32–41. https://doi.org/10.1108/17590811011033398

- Nobes, C. W., & Parker, R. H. (1991). True and fair: A survey of UK Financial Directors. Journal of Business Finance & Accounting, 18(3), 359–375. https://doi.org/10.1111/j.1468-5957.1991.tb00600.x

- Official Journal of the European Union (OJEU). (2013). Directive 2013/34/EU of the European Parliament and of the Council of 26 June 2013 on the annual financial statements, consolidated financial statements and related reports of certain types of undertakings. https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A32013L0034

- Razak, S. S., Saiti, B., & Dinç, Y. (2019). The contracts, structures and pricing mechanisms of Sukuk: A critical assessment. Borsa Istanbul Review, 19, S21–S33. https://doi.org/10.1016/j.bir.2018.10.001

- Salihin, A., Fatima, A. H., & Ousama, A. A. (2014). An Islamic perspective on the true and fair view override principle. Journal of Islamic Accounting and Business Research, 5(2), 142–157. https://doi.org/10.1108/JIABR-12-2011-0005

- Salihin, A., Fatima, A. H., & Ousama, A. A. (2015). Analysis of the true and fair view concept: An Islamic perspective. International Journal of Managerial and Financial Accounting, 7(1), 38–61. DOI https://doi.org/10.1504/IJMFA.2015.067499

- Schaltegger, S., & Burritt, R. L. (2010). Sustainability accounting for companies: Catch-phrase or decision support for business leaders? Journal of World Business, 45(4), 375–384. https://doi.org/10.1007/978-1-4020-4974-3_2

- Schiehll, E., & Kolahgar, S. (2021). Financial materiality in the informativeness of sustainability reporting. Business Strategy and the Environment, 30(2), 840–855. https://doi.org/10.1002/bse.2657

- Stuebs, M. T., & Thomas, C. W. (2011). Principles-based accounting: The case for principled judgement. In C. Jeffrey (Ed.), Research on professional responsibility and ethics in accounting (vol. 15, pp. 47–73). Emerald Group Publishing Limited. https://doi.org/10.1108/S1574-0765(2011)0000015005

- Van Hulle, K. (1997). The true and fair view override in the European Accounting Directives. European Accounting Review, 6(4), 711–720. https://doi.org/10.1080/09638189700000012

- Zyznarska-Dworczak, B. (2020). Sustainability accounting—Cognitive and conceptual approach. Sustainability, 12(23), 9936. https://doi.org/10.3390/su12239936