Abstract

Recently, the financial performance of the steel industry has faced several challenges due to a lack of focus on corporate social responsibilities (CSR), green finance, and information communication technology (ICT). Hence, this study investigates the impact of CSR, green finance, and ICT on the financial performance of the steel industry in China. The present research also investigates the moderating role of organizational support among CSR and firm performance and ICT and firm performance. We applied structural equation modeling to analyze the primary data of 290 employees collected from the employees of the steel industry in China. The findings indicated that CSR, green finance, and ICT have a positive and significant impact on the financial performance of this industry. The results also showed that organizational support significantly and positively moderates the interaction between CSR, ICT, and financial performance. These findings suggest that Chinese steel industries should adopt CSR practices and implement an ICT adoption strategy for better financial performance.

1. Introduction

Rapid industrialization and globalization have harmed the environment in the recent decade, contributing to issues including air and water pollution, global warming, and deadly chemical explosions. In response to rising environmental awareness, the concept of sustainable financial performance has gained attention among researchers and practitioners. Firm performance ensures its existence, administration of many business areas, operational effectiveness, and long-term development. The sustainable improvement in the financial performance increases its financial position, alleviates financial distress, aids in future planning, reduces the likelihood of risks, helps in risk management, helps benefit from competitive opportunities, and achieves the firm’s goals (Bayraktaroglu et al., Citation2019).Because sustainable financial performance ensures the payment of amore significant amount of dividends on equity and debt from lenders by providing reasonable interest payments, the firm can make more investments from public or other business firms within the country or abroad. Furthermore, if the firm’s financial performance is higher, it can set aside more money in cash reserves even after making payments (Alkhazali et al., Citation2020; Ibhagui & Olokoyo, Citation2018). As a result, the company has more financial resources, and its decision-making is faster, more responsive, and more successful since it can afford high-quality raw materials, innovation-based resources, technology, and tools and recruit more efficient workers.

Firms must establish sustainability in their performance, which means attaining financial performance along with improving social and environmental performance (Shahzad et al., Citation2019). It continually increases financial performance or profitability, which ensures the firm’s performance is sustainable in terms of social, ecological, and economic performance (Bennouri et al., Citation2018). ICT, green finance, and CSR determine the firms’ performance. ICT is an extension of information technology with the stress on communication, information management, and telecommunication. It integrates telecommunications, computers, software, and apps to access, store, transfer, understand, process, and manipulate information. With an effectively managed ICT system, the firms can benefit from quality information and communication with the stakeholders. Quality information and contacts can be used to improve the business resources, processes, and advertisement, improving marketing and profitability. Hence, effective ICTs enhance firm performance (Abu-Rumman et al., Citation2021; Erkmen et al., Citation2020).

Green financing flows financial resources from financial institutions like banking, micro-credit, insurance, and investment firms, from the private, public, and not-for-profit sectors to encourage environment-friendly activities. When the trend of green financing increases within a region, the business firms that indicate the human source of GHG, can acquire extra funds to invest in mitigating adverse environmental impacts. This improves the business operations and its production quality and triggers the firm reputation among the general public and the market. In this situation, the firms can broaden the business scope and accelerate financial performance (Al Shraah et al., Citation2021; Gilchrist et al., Citation2021).CSR refers to the firm’s self-regulation. It requires that the firms be accountable to themselves, the stakeholders, and the general public. With employing CSR, the firms must be aware of the nature of their influences on all aspects of the people and other stakeholders, including social, economic, and environmental. With the effective implementation of CSR, firms can improve their business processes and well-being; thus, they can have competitive advantages and improve their performance (Ciftci et al., Citation2019; Hameed Al-Ali et al., Citation2019).

The present article aims to investigate the impacts of ICTs, green finance, and CSR on a firm sustainable financial performance in the steel industry of the Chinese economy. China is an emerging upper-middle-income country with a newly industrialized economy (Ding et al., Citation2020). It is the 2nd largest economy globally in terms of nominal gross domestic product (GDP), which accounts for $19.91 trillion estimated for 2022. It is the 1st largest economy in the world in terms of GDP; purchasing par parity accounts for $30.18 trillion, estimated for 2022. The steel industry is one of the biggest industries in China. The country produced 1054 million tons of steel in 2020, accounting for more than half of the global output (Tee et al., Citation2021).This shows a 5.6 percent gain over the previous year, despite a 0.9 percent drop in world steel production. The country’s global crude steel output share grew to 56 percent in 2020, up from 53 percent in 2019(Ding et al., Citation2020). In the early 1990s, iron ore output maintained up with steel production, but in the early 2000s, iron ore that was imported and other metals overtook it. Steel output climbed from 140 million tons in 2001 to 419 million tons in 2006 and produced 928 million tons in 2018. Many small and medium-scale production hubs, including Anshan in Liaoning, produce much of the state’s steel (Gao et al., Citation2019).China is the world’s top steel exporter, as per the statistics of 2018, with an export volume of 66.9 million tons, down 9 percent from the previous year. The drop halted China’s decade-long steel export expansion. Due to significant anti-dumping levies, steel exports had not recovered to pre-2008 levels as of 2012. China’s steel exports, on the other hand, hit a new high of 110 million metric tons in 2015(Zhu et al., Citation2019). Domestic steel demand remained consistent, especially in the growing west, where Xinjiang’s steel production was increasing.

The steel industry in China posted a profitability of CNY 470 billion ($70 billion) in 2018, up 39 percent from the previous year. Twenty-one of the world’s 45 top steel producers is Chinese, including the world’s largest, Sino steel (Sun et al., Citation2019). China’s steel industry is growing and significantly contributes to the country’s GDP, but the rate of progress is getting slow. So, it is severely necessary to pay attention to this industry in the Chinese economy so that the growth rate can be accelerated and sustained. The present study addresses individual firms’ performance, which contributes to the industry’s growth within the economy. The study examines the impacts of ICTs, green finance, and CSR on firm performance by analyzing the moderating role of perceived organizational support in the relation of ICTs and CSR impacts on sustainable firm performance.

Thus, the research questions are: What impacts green finance, ICT, and CSR on sustainable financial performance? What is the role of perceived organizational support in CSR, ICT, and sustainable financial performance? The following is a list of the particular objectives of the study: In the first place, the purpose of this research is to analyze how information and communications technology (ICT), green finance, and corporate social responsibility (CSR) affect the long-term financial performance of the steel sector in China. The second objective is to investigate the essential moderating role that perceived organizational support plays in the context of these relationships. The data were analyzed using structural equation modeling (SEM), which was collected specifically for this project.

Though sustainable financial performance is not a new subject to be addressed by authors, there are many literary gaps that the authors fill. First, the ICTs is a technological business concept, green finance is an ecological business concept, and CSR is linked to business regulation. These three concepts differ, and their relation to sustainable financial performance has been analyzed individually in prior literature. This study confiscates this literary gap with equal attention to the role of ICTs, green finance, and CSR in sustainable financial performance. Second, in past literature, perceived organizational support influences ICTs, CSR, and sustainable financial performance in some previously conducted studies. But, in very few studies, the moderating effects of perceived organizational support on the association of ICTs, and CSR, with sustainable financial performance have been examined. This literary gap removes the present study, which analyzes the moderating role of perceived organizational support between ICTs, CSR, and sustainable financial performance. Third, the decrease in the rate of progress in China’s steel industry has been there for several years. Still, very few studies have discussed the role of ICTs, green finance, CSR, and perceived organizational support in sustainable financial performance in the context of the steel industry of China. The present study distinguishes the impacts of ICTs, green finance, and CSR on sustainable financial performance in the Chinese steel industry.

The structure of the study includes the introduction as the first part. After the introduction, the second part deals with the past views of the authors regarding the relationship between ICTs, green finance, CSR, and perceived organizational support and sustainable financial performance. The third part describes the applied methodology for information collection and analysis of the variables and the validity of their relationship. After the data analysis, the results are extracted. Through a proper discussion, the validity of the results is approved by previous literature outcomes. Finally, the study implications, conclusions, and limitations are given in the final chapter of the study.

2. Literature review

The acceleration and sustainability of performance are significant to a business firm. Firm performance determines the business’s survival, management works, the efficiency of operational activities, and long-term progress. The financial position can be sustained with consistent improvement in firm performance. Financial distress can be reduced, future planning can be effective, risks and the potential of damages on risks exposures can be overcome, and competitive advantages and business goals can be achieved (Maroufkhani et al., Citation2019). Moreover, when adequately disclosed or shared, increasing firm performance improves the firm’s reputation in the sales market, equity market, and general public. Firms with a good reputation can enjoy support from stakeholders, large investments, and improved marketing (Chen et al., Citation2021). But firm performance is influenced by firm decisions and actions like arrangement for ICTs, benefit from green finance (green loans, green securities, or green investment), and CSR implementation. In the existing literature, the relationship between ICTs, green finance, CSR, perceived organizational support, and firm performance is dominant. Different authors have presented different views about the relationships between ICTs, green finance, CSR, and perceived organizational support and firm performance (Ding et al., Citation2021). The present article throws light on these past literary arguments for establishing hypotheses regarding the relationship among of ICTs, green finance, CSR, and perceived organizational support and firm performance.

The empirical investigation by DeStefano et al. (Citation2018)checked the influences of infrastructure and ICT use on firm performance. UK firms served as the study sample so that the relationship between infrastructure and ICT use to firm performance could be analyzed empirically. The data about the variables were collected from the Ci Technology Database (CiTDB), with the help of which an annual survey for 1999–2005 was made. The impacts of heterogeneous ICT capital like various types of computers, different sorts of software, and the number of employed IT specialists. The study results showed a positive impact of ICT on firm performance. The study implies that with an increased number of computers having high efficiency and work capacity, effective and updated software, and skilled IT experts, the firms can acquire, process, and share information and, thus, protect the business from financial risks. So, the improved ICT ensures superior firm performance with higher profitability. The study by article, Anser et al. (Citation2020), examine the ICT role in firm performance. This study proclaims that up-to-date, relevant, and accurate information is acquired from an effective ICT system. Quality information benefits all aspects of a company’s operations, such as developing efficient business resources, improving infrastructure, improving labor-force abilities and skills, strengthening relationships, increasing productivity, and ensuring sustainability in the ever-increasing marketing of goods and services (Rehman et al., Citation2020).

As a result, organizations’ financial performance improves due to increased profitability. Chege et al. (Citation2020) investigated ICT innovation on firm performance. The authors analyze the nexus between innovation in ICT and firm performance with a sample of 240 firms in Kenya. For the analysis purpose, structural equation modeling was applied. The results showed a positive contribution of ICT innovation to firm performance. The study posits that when entrepreneurs adopt innovative behavior and have the policies to implement Innovative ICTs, they have competitive advantages in information and communication systems. In this way, they can develop abilities to compete against their rivals in the market and retain the total profits. Hence, ICT innovation improves the firms’ performance. Based on the above discussions, we put the following hypothesis:

Hypotheses (H1). There is a significant and positive impact of ICT on financial performance.

The study of Sadiq et al. (Citation2021) investigated the relationship between green finance, sustainable management, CSR, and firm performance during Covid-19. The data for the research investigation were acquired from commercial banks and corporate in both private and public economic sectors in Southeast Asia. The ARDL analytical technique and Pooled mean group (PMG) method were implied to analyze the variables green finance, sustainable management, CSR, and firm performance and their relationship. The results revealed that during some crises, especially the health-related crisis in an economy, businesses become challenging to be carried on a sustainable basis because of weak control of pollution. But in areas where the firms have green finance facilities, the firms can be sustainably administered, and CSR implementation maintains the firm’s marketing and profitability. Based on the above discussions, the following hypothesis can be put:

Hypotheses (H2). There is a significant and positive impact of green finance on financial performance.

The successful application of CSR practices, and hence the execution of business policies, improve the company’s performance. The research was carried out by Yang et al. (Citation2019) o gauge the impacts of CSR on firm performance. In this research, the five dimensions of CSR such as responsibilities towards shareholders, customers and suppliers, employees, environmental quality, and society, and three indicators of the firm’s financial performance like return on equity (ROE), return on assets (ROA), and earnings per share (EPS) ratios were analyzed. The data were acquired from 125 Chinese Pharmaceuticals from 2010 to 2016 to analyze individual dimensions of CSR influences on firm financial performance. The study claims that all dimensions of CSR positively impact firm financial performance. With the increase in the efficiency with which CSR practices are fulfilled, the financial performance of firms increases as well, for the stakeholders play a significant role in operational processes. The above discussions help to put the following hypothesis:

Hypotheses (H3). There is a significant and positive impact of CSR on financial performance.

Hence, perceived organizational support improves the relationship between ICTs and firm performance. Kim et al. (Citation2018) investigated the relationship between perceived organizational support, CSR, and firm performance. The study posits that when firms provide support to their employees, they win the employees’ hearts and their willingness to follow social and environmental regulations while performing business operations. Thus, it becomes easy for the firm to implement CSR, and sustainable financial performance can be achieved by fulfilling CSR responsibilities intended for social well-being. Similarly, Aldabbas et al. (Citation2021) show that perceived organizational support is helpful in CSR execution and improving firm performance. In this case, CSR can better contribute to sustainability in firm performance. Based on the above discussions, we put the following hypotheses:

Hypotheses (H4). Perceived organizational support has significantly moderated the relationship between ICTs and financial performance.

Hypotheses (H5). Perceived organizational support has significantly moderatedthe relationship betweenCSR and financial performance.

3. Research methods

The article investigates the impact of CSR, green finance, and ICT on financial performance and the moderating role of organizational support among CSR and firm performance and ICT and firm performance. The present study has employed the primary data collection methods and used questionnaires to gather the data from selected respondents. The questionnaires are adopted from past studies, such as financial performance has five items scale extracted from Nor Rifhan (Citation2017). The measurement scale and source for financial performance are given in .

Table 1. Measurement scale for financial performance.

In addition, the scale related to information communication technology is adopted from Ul-Hameed et al. (Citation2019), which also has five items. The measurement scale and source for information communication technology are given in .

Table 2. Measurement scale for ICT.

Moreover, the scale related to green financiers has six items, adapted from Zheng et al. (Citation2021). The measurement scale and source for green finance are given in .

Table 3. Measurement scale for green finance.

In addition, corporate social responsibilities have sixteen item scale extracted from Manzoor et al. (Citation2019). The measurement scale and source for corporate social responsibilities are given in .

Table 4. Measurement scale for CSR.

Finally, the scale related to perceived organizational support is adopted from Iqbal & Hashmi,(Citation2015), which has eight items. The measurement scale and source for perceived organizational support are given in .

Table 5. Measurement scale for perceived organizational support.

The steel industry employees in Beijing, China, are the respondents. Thus, the unit of the analysis is individual employees of the steel industry. The respondents were selected using simple random sampling. The researchers sent around 510 surveys to the selected employees but received only 290, showing a 56.86 percent response rate. The valid responses should be greater than 100 and considered appropriate for this study (Natori & Iio, Citation2021), and the current study has 290 valid responses. The researchers control the common method bias by providing clear and easier items to the respondents and separate items of predictors and predictive constructs. In addition, to avoid social desirability bias, the researchers convinced the respondents that their information should not be disclosed and used indirect questioning. In addition, the respondents include 189 males and 101 females, while 55 have graduation qualifications, 179 have master’s qualifications, and 56 have Ph.D. qualifications. Moreover, the 77 respondents have 1 to 5 years of experience, while 186 have 6 to 10 years of experience, and 27 have more than ten years of experience. Finally, 65 respondents are subordinates, 117are managers, and108 have other natures of employment. This information is given in .

Table 6. Demographic information of respondents.

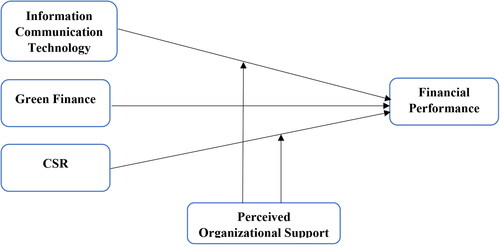

The current article has assessed measurement and structural models. The study assesses the measurement and structural models because the purpose of the study is to examine the key variables’ impact on predictive variables. It is an effective tool that provides the best results even though the researchers have used complex models and large sample sizes (Hair et al., Citation2021). This tool examines the measurement model to check the validity and reliability of the constructs while also investigating the structural model to test the study’s hypotheses (Hair et al., Citation2019). Finally, shows the theoretical framework for three predictors as ICT, CSR, and green finance (GF) were used while perceived organizational support (POS) was taken as the moderating variable, and financial performance (FP) was taken as the predictive variable. The study has taken the legitimacy theory that states that organizations continuously try to ensure that they carry out activities such as CSR practices adopting new technologies, and finance following the financial performance. Similarly, the current study also investigates the role of CSR, Green finance, and ICT on financial performance.

Figure 1. Theoretical Model.

Source: Author's source.

4. Research findings

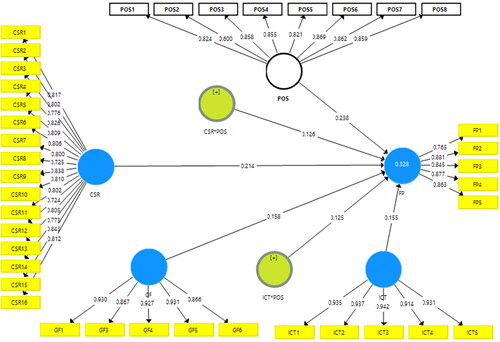

The findings section exposed the content validity using factor loadings, and the figures indicated that the values are larger than 0.50 and exposed valid content validity. In addition, the results also revealed the convergent validity using average variance extracted (AVE), and the figures indicated that the values are larger than 0.50 and exposed valid convergent validity. Finally, the results also exposed the reliability using composite reliability (CR) and Alpha, and the figures indicated that the values are larger than 0.70 and exposed significant reliability. given below, shows these figures.

The present study has examined the discriminant validity using Fornell &Larcker (Fornell & Larcker, Citation1981). The results indicated that the first value in the column is larger than the rest of the values. These results indicated that the relationship among variables themselves is stronger than the other constructs and proved discriminant validity as valid. shows these outcomes.

Table 7. Convergent validity.

Table 8. Fornell &Larcker.

The study has also examined the discriminant validity using cross-loadings. The results indicated that the values that indicated the relationship among variables were larger than the values that indicated the association with other variables and proved discriminant validity as valid. shows these outcomes.

Table 9. Cross-loadings.

The findings section also exposed the discriminant validity using Heterotrait Monotrait (HTMT) ratio, and the figures indicated that the values are lower than 0.90 and exposed valid discriminant validity (Henseler et al., Citation2015). , given below, shows these figures ().

Figure 2. Measurement model assessment.

Source: Author's source.

Table 10. Discriminant validity.

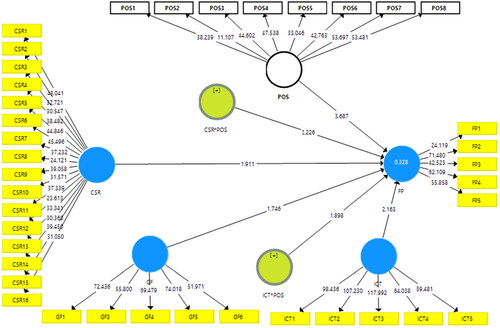

The path analysis results revealed that CSR, green finance, and ICT positively affect the steel industry’s financial performance in China and accept H1, H2 and H3. The findings also indicated that the organizational support significantly moderates CSR, ICT, and financial performance of the steel industry in China and accepts H4 and H5. The same results can be observed in and , respectively. and given below show these figures.

Figure 3. Structural model assessment.

Source: Author's source.

Table 11. Path analysis.

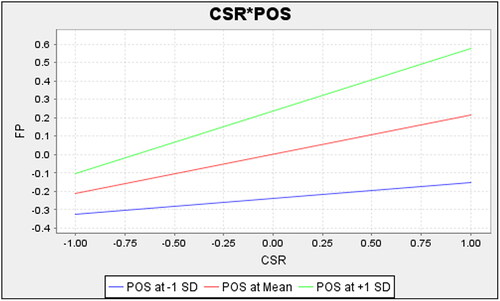

The findings also indicated that the organizational support significantly and positively moderates CSR and financial performance of the steel industry in China and accepts H4. , given below, shows these figures.

Figure 4. CSR*POS.

Source: Author's source.

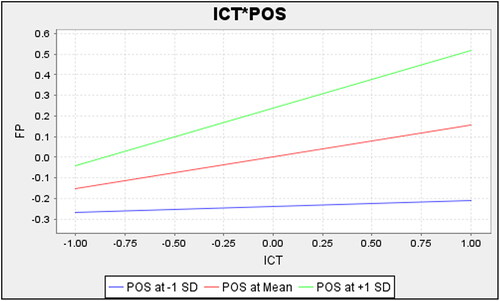

Finally, the findings also indicated that the organizational support significantly and positively moderates the ICT and financial performance of the steel industry in China and accepts H5. report these outcomes.

Figure 5. ICT*POS.

Source: Author's source.

5. Discussions

The results indicated that ICT has a positive impact on firm performance. These results align with Viete and Erdsiek (Citation2020), which show that using ICT tools and instruments within an organization improves the communication network between the management and the internal and external stakeholders. This communication network assists managers in sharing their thoughts with the stakeholders and having a look at their ideas. This information transfer makes it easy for managers to modify their strategies to achieve business goals, and this flexibility creates responsiveness and agility in business operations. So, the operational and marketing performance of the firm gets improved by employing ICTs. These results are supported by Cuevas-Vargas et al. (Citation2022), which highlight that up-to-date, relevant, and accurate information is helpful in all the business areas of a firm it helps to acquire efficient business resources, improve infrastructure, improve the abilities and skills of labor-force, strengthens the relations, improves productivity, and creates sustainability in the increasing level of marketing of goods and services.

Hence, higher profitability determines the firm’s higher financial performance. These results are also in line with Loukis et al. (Citation2019), which post that the firms have employed high-potential ICT tools the firms have an awareness of the business shifts like the change in the equity market conditions, which affect their investment and financial position, the change in the customers’ requirements which determine sales, and market trends. This awareness helps make the right decisions at the right time and achieve higher financial performance.

The results showed that green finance has a positive impact on firm performance. These results match Wu et al. (Citation2021), research on the role of green finance in the sustainability of firm performance.

The research found that the firm’s overall performance is the combination of the firm’s environmental, social, and economic performance. Environmental performance also influences social and economic performance, and the firms which enjoy green finance from financial institutions can improve their environmental performance by reducing pollution emissions. So, in the presence of green finance, the firms can make higher performance. These results are also supported by Zhang et al. (Citation2021), which show that in the areas where the financial institutions follow the policy to grant finance for the undertaking of green practices and they have easy requirements from candidates. The firms operating there can carry on the green programs along with the performance of business operations to remove the negative environmental impacts. These firms improve their operational and financial performance with a quality work environment, good quality resources, and retained marketing.

The study results also showed that CSR positively impacts firm performance. These results agree with Saha et al. (Citation2020), which examines the integration of CSR and its contribution to firm performance. The study implies that when firms undertake the CSR practices like philanthropic activities, ecologically friendly programs, and social welfare activities, they can build solid relations with the stakeholders such as the government, suppliers, employees, and customers. These relations help the firms implement their policies with the cooperation of the stakeholders. Effectively implementing CSR practices and, thereby, business policies’ execution enhances the firm’s overall performance. These results are supported by Kong et al. (Citation2020), which highlight that under CSR integration, the firms feel their accountability towards the environment and are engaged in green practices like waste management, recycling, water management, renewable energy consumption, reusable materials, green supply chains, and adopting ecological friendly infrastructure. These firms provide a healthy and clean work environment to the firm employees. In such a high-quality environment, the employees have high motivation towards their job functions. The responsible undertaking of these functions helps to have maximum productivity, improve quality goods and services, and enhance marketing efficiency. So, there are more chances of higher profitability and the financial performance of the firms is higher.

The results revealed that perceived organizational support moderates’ ICTs and firm performance. These results are supported by Liu and Lu (Citation2021), which indicate that the employee’s perception of the behavior of the organizational management or the owners affects their thinking and actions. When the organizational personnel have the perception that the organization shows supportive behavior towards the employees while making policies, they try to have information about the ICTs advancements and develop the skills to run ICT technologies, tools, and instruments. The perceived organizational support also improves the employees’ work efficiency and their contribution to firms’ outcomes. So, when there is high perceived organizational support, ICTs’ contribution to firm financial performance increases. These results are also in line with Amoako et al. (Citation2020), which highlight that when a business organization provides supportive behavior or assurance to have support, by improving the employees’ skills and organizational commitment, it can better benefit from ICTs and improve the firm financial performance. The results indicated that perceived organizational support moderates CSR and firm performance. These results are supported by Pham and Tran (Citation2020), which indicate that when an organization shows supportive behavior through its representatives towards the employees who offer their services for management, operations, production practices, and marketing of the products and services, it successfully develops an emotional attachment of employees with the organization. These employees are committed to the organization and work to achieve its goals; thus, it never lets its profitability lower.

5.1. Theoretical contribution

The present article carries theoretical as well as empirical implications. This study has considerable theoretical significance for its great contribution to economic literature. The study contributes to the literature on ICT and financial performance, CSR and financial performance, green finance, and financial performance. In the prior literature, ICTs, green finance, and CSR impacts on firm performance have been discussed separately and with minor detail. The present study adds to the literature for it simultaneously examines the relationship of ICTs, green finance, and CSR to firm performance. In the existing literature, the relationship between perceived organizational support to ICTs, CSR, and its role in improving firm performance has simply been checked without considering the moderating role of perceived organizational support between ICTs, CSR, and firm performance. The study contributes to the extant literature by examining moderating the impacts of perceived organizational support on the relationship of ICTs and CSR with firm performance. In past articles, China is the largest country, having a growing economy, but to our disappointment, the economic growth at the firm level is still weak, and it requires attention. In previous literature, only a few studies have discussed this need. The present study, with the analysis of firm performance and influences of perceived organizational support, ICTs, green finance, and CSR on firm performance in the Chinese economy, extends the literature.

5.2. Practical implications

The current study also has great empirical significance in any emerging economy, for it discusses firms’ financial performance. Individual business firms contribute to the country’s GDP, so their financial performance is significant. This study guides individual business firms on how they can accelerate their performance. This article guides future researchers while examining this area in the future and guides policymakers in developing policies related to the improvement of financial performance. The study guides that government and economists must encourage green finance issuance and use within the economy to improve firm performance. The study suggests that policymakers must motivate firms to implement CSR effectively so that the firm performance can be improved. Moreover, it also indicates that in an economy, ICTs must be developed and adopted in order to improve firms’ performance. Authors, through this research, convey that business firms must adopt supportive behavior while forming business policies to implement CSR and enhance business performance effectively. So, with the improvement in perceived organizational behavior, CSR's role in firm performance must be improved. In addition, the firms must show organizational and employees must have good perceptions about the supportive behavior of firms so that ICTs can be effectively implemented.

6. Conclusion

The study aimed to analyze the impacts of ICTs, green finance, and CSR on firm performance and also to analyze how perceived organizational support moderates between ICTs and CSR and firm performance. An empirical survey was conducted on firms in China’s steel industry and quantitative information regarding ICTs, green finance, CSR, perceived organizational support, and their contribution to the firm performance was collected with the help of questionnaires. These findings from the empirical research survey showed a positive relation between ICTs, green finance, and CSR with firm performance and perceived organizational support as a moderator between ICTs and CSR and firm performance. The results indicated that when business firms apply ICTs thoroughly and effectively, they can have up-to-date, relevant, and reliable information regarding any object, event, or phenomenon and build good and cooperative relations through an effective communication system. The quality of information and sound contribute to the firm’s operational and financial performance. The results indicated that the business firms’ green finance on the part of financial institutions improves their financial resources and prepares them to overcome environmental risks, ultimately improving the firm’s financial performance. Similarly, integrating CSR into the firm policies and strategies brings ecologically friendly and social improvement in all business areas. So, the firm performance goes high. The study also suggests that the enhanced perceived organizational support enhances the contribution of ICTs and CSR to firm performance.

7. Limitations and future directions

The present article also has some limitations, which may cause objections to the application of this study in the practical field. Future authors are expected to remove these limitations and improve the study’s validity. The study examines the impacts of ICTs, green finance, and CSR on firm performance without giving much detail to these concepts and their dimensions. In the future, the authors may throw light on the concepts and dimensions of ICTs, green finance, and CSR, analyzing their impacts on firm performance to broaden the scope of the study. The study outcomes are based on information from the Chinese business world. China has particular economic conditions, specific technological advancements, and environmentally friendly practices. So, a study based on one economy cannot be a suitable guideline for the readers. Researchers must conduct a survey of multiple economies for information about the concerned nexus in the future.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

References

- Abu-Rumman, A., Al Shraah, A., Al-Madi, F., & Alfalah, T. (2021). The impact of quality framework application on patients’ satisfaction. International Journal of Human Rights in Healthcare, 15(2), 151–165. https://doi.org/10.1108/IJHRH-01-2021-0006

- Al Shraah, A., Abu-Rumman, A., Al Madi, F., Alhammad, F. A. F., & AlJboor, A. A. (2021). The impact of quality management practices on knowledge management processes: A study of a social security corporation in Jordan. The TQM Journal, 34(4), 605–626. https://doi.org/10.1108/TQM-08-2020-0183

- Aldabbas, H., Pinnington, A., & Lahrech, A. (2021). The influence of perceived organizational support on employee creativity: The mediating role of work engagement. Current Psychology, 8, 1–15. https://doi.org/10.1007/s12144-021-01992-1

- Alkhazali, Z., Abu-Rumman, A., Khdour, N., & Al-Daoud, K. (2020). Empowerment, HRM practices and organizational performance: A case study of. Entrepreneurship and Sustainability Issues, 7(4), 2991–3000. https://doi.org/10.9770/jesi.2020.7.4(28)

- Amoako, T., Sheng, Z. H., Dogbe, C. S. K., & Pomegbe, W. W. K. (2020). Effect of internal integration on SMEs’ performance: The role of external integration and ICT. International Journal of Productivity and Performance Management, 71(2), 643–665. https://doi.org/10.1108/IJPPM-03-2020-0120

- Anser, M. K., Yousaf, Z., Usman, M., & Yousaf, S. (2020). Towards strategic business performance of the hospitality sector: Nexus of ICT, E-marketing and organizational readiness. Sustainability, 12(4), 1346–1358. https://doi.org/10.3390/su12041346

- Bayraktaroglu, A. E., Calisir, F., & Baskak, M. (2019). Intellectual capital and firm performance: An extended VAIC model. Journal of Intellectual Capital, 20(3), 406–425. https://doi.org/10.1108/JIC-12-2017-0184

- Bennouri, M., Chtioui, T., Nagati, H., & Nekhili, M. (2018). Female board directorship and firm performance: What really matters? Journal of Banking & Finance, 88, 267–291. https://doi.org/10.1016/j.jbankfin.2017.12.010

- Chege, S. M., Wang, D., & Suntu, S. L. (2020). Impact of information technology innovation on firm performance in Kenya. Information Technology for Development, 26(2), 316–345. https://doi.org/10.1080/02681102.2019.1573717

- Chen, L., Jia, F., Li, T., & Zhang, T. (2021). Supply chain leadership and firm performance: A meta-analysis. International Journal of Production Economics, 235, 1080–1096. https://doi.org/10.1016/j.ijpe.2021.108082

- Ciftci, I., Tatoglu, E., Wood, G., Demirbag, M., & Zaim, S. (2019). Corporate governance and firm performance in emerging markets: Evidence from Turkey. International Business Review, 28(1), 90–103. https://doi.org/10.1016/j.ibusrev.2018.08.004

- Cuevas-Vargas, H., Aguirre, J., & Parga-Montoya, N. (2022). Impact of ICT adoption on absorptive capacity and open innovation for greater firm performance. The mediating role of ACAP. Journal of Business Research, 140, 11–24. https://doi.org/10.1016/j.jbusres.2021.11.058

- DeStefano, T., Kneller, R., & Timmis, J. (2018). Broadband infrastructure, ICT use and firm performance: Evidence for UK firms. Journal of Economic Behavior & Organization, 155, 110–139. https://doi.org/10.1016/j.jebo.2018.08.020

- Ding, X., Appolloni, A., & Shahzad, M. (2021). Environmental administrative penalty, corporate environmental disclosures and the cost of debt. Journal of Cleaner Production, 332, 129919. https://doi.org/10.1016/j.jclepro.2021.129919

- Ding, X., Li, Q., Wu, D., Huo, Y., Liang, Y., Wang, H., Zhang, J., Wang, S., Wang, T., Ye, X., & Chen, J. (2020). Gaseous and particulate chlorine emissions from typical iron and steel industry in China. Journal of Geophysical Research: Atmospheres, 125(15), 15–31. https://doi.org/10.1029/2020JD032729

- Erkmen, T., Günsel, A., & Altındağ, E. (2020). The role of innovative climate in the relationship between sustainable IT capability and firm performance. Sustainability, 12(10), 4058–4074. https://doi.org/10.3390/su12104058

- Fornell, C., & Larcker, D. F. (1981). Evaluating structural equation models with unobservablevariables and measurements error. Journal of Marketing Research, 18(1), 39–50. https://doi.org/10.1177/002224378101800104

- Gao, C., Gao, W., Song, K., Na, H., Tian, F., & Zhang, S. (2019). Spatial and temporal dynamics of air-pollutant emission inventory of steel industry in China: A bottom-up approach. Resources, Conservation and Recycling, 143, 184–200. https://doi.org/10.1016/j.resconrec.2018.12.032

- Gilchrist, D., Yu, J., & Zhong, R. (2021). The limits of green finance: A survey of literature in the context of green bonds and green loans. Sustainability, 13(2), 478–494. https://doi.org/10.3390/su13020478

- Hair, J. F., Astrachan, C. B., Moisescu, O. I., Radomir, L., Sarstedt, M., Vaithilingam, S., & Ringle, C. M. (2021). Executing and interpreting applications of PLS-SEM: Updates for family business researchers. Journal of Family Business Strategy, 12(3), 1–12. https://doi.org/10.1016/j.jfbs.2020.100392

- Hair, J. F., Risher, J. J., Sarstedt, M., & Ringle, C. M. (2019). When to use and how to report the results of PLS-SEM. European Business Review, 31(1), 2–24. https://doi.org/10.1108/EBR-11-2018-0203

- Hameed Al-Ali, A., Khalid Qalaja, L., & Abu-Rumman, A. (2019). Justice in organizations and its impact on Organizational Citizenship Behaviors: A multidimensional approach. Cogent Business & Management, 6(1), 1–18. https://doi.org/10.1080/23311975.2019.1698792

- Henseler, J., Ringle, C. M., & Sarstedt, M. (2015). A new criterion for assessing discriminant validity in variance-based structural equation modeling. Journal of the Academy of Marketing Science, 43(1), 115–135. https://doi.org/10.1007/s11747-014-0403-8

- Ibhagui, O. W., & Olokoyo, F. O. (2018). Leverage and firm performance: New evidence on the role of firm size. The North American Journal of Economics and Finance, 45, 57–82. https://doi.org/10.1016/j.najef.2018.02.002

- Ikram, M., Sroufe, R., Mohsin, M., Solangi, Y. A., Shah, S. Z. A., & Shahzad, F. (2019). Does CSR influence firm performance? A longitudinal study of SME sectors of Pakistan. Journal of Global Responsibility, 11(1), 27–53. https://doi.org/10.1108/JGR-12-2018-0088

- Iqbal, S., & Hashmi, M. S. (2015). Impact of perceived organizational support on employee retention with mediating role of psychological empowerment. Pakistan Journal of Commerce and Social Sciences (PJCSS), 9(1), 18–34.

- Jia, X. (2020). Corporate social responsibility activities and firm performance: The moderating role of strategic emphasis and industry competition. Corporate Social Responsibility and Environmental Management, 27(1), 65–73. https://doi.org/10.1002/csr.1774

- Kim, B.-J., Nurunnabi, M., Kim, T.-H., & Jung, S.-Y. (2018). The influence of corporate social responsibility on organizational commitment: The sequential mediating effect of meaningfulness of work and perceived organizational support. Sustainability, 10(7), 2208–2219. https://doi.org/10.3390/su10072208

- Kong, Y., Antwi‐Adjei, A., & Bawuah, J. (2020). A systematic review of the business case for corporate social responsibility and firm performance. Corporate Social Responsibility and Environmental Management, 27(2), 444–454. https://doi.org/10.1002/csr.1838

- Lee, C.-C., & Lee, C.-C. (2022). How does green finance affect green total factor productivity? Evidence from China. Energy Economics, 107, 1058–1073. https://doi.org/10.1016/j.eneco.2022.105863

- Liu, M., & Lu, W. (2021). Corporate social responsibility, firm performance, and firm risk: The role of firm reputation. Asia-Pacific Journal of Accounting & Economics, 28(5), 525–545. https://doi.org/10.1080/16081625.2019.1601022

- Loukis, E., Janssen, M., & Mintchev, I. (2019). Determinants of software-as-a-service benefits and impact on firm performance. Decision Support Systems, 117, 38–47. https://doi.org/10.1016/j.dss.2018.12.005

- Manzoor, F., Wei, L., Nurunnabi, M., Subhan, Q. A., Shah, S. I. A., & Fallatah, S. (2019). The impact of transformational leadership on job performance and CSR as mediator in SMEs. Sustainability, 11(2), 1–14. https://doi.org/10.3390/su11020436

- Maroufkhani, P., Wagner, R., Wan Ismail, W. K., Baroto, M. B., & Nourani, M. (2019). Big data analytics and firm performance: A systematic review. Information, 10(7), 226–238. https://doi.org/10.3390/info10070226

- Muganyi, T., Yan, L., & Sun, H-p (2021). Green finance, Fintech and environmental protection: Evidence from China. Environmental Science and Ecotechnology, 7, 100107–100118. https://doi.org/10.1016/j.ese.2021.100107

- Natori, T., & Iio, T. (2021). An empirical study of how much a social robot increases the rate of valid responses in a questionnaire survey [Paper presentation].Paper Presented at the 2021 30th IEEE International Conference on Robot & Human Interactive Communication (RO-MAN),. https://doi.org/10.1109/RO-MAN50785.2021.9515364

- Nor Rifhan, H. (2017). The effect of lean manufacturing towards financial performance at Hicom Automotive Manufacturers, Pekan, Pahang. Universiti Utara Malaysia.

- Pham, H. S. T., & Tran, H. T. (2020). CSR disclosure and firm performance: The mediating role of corporate reputation and moderating role of CEO integrity. Journal of Business Research, 120, 127–136. https://doi.org/10.1016/j.jbusres.2020.08.002

- Phong, L. B., Hui, L., & Son, T. T. (2018). How leadership and trust in leaders foster employees’ behavior toward knowledge sharing. Social Behavior and Personality: An International Journal, 46(5), 705–720. https://doi.org/10.1080/14778238.2018.1445426

- Rehman, S. U., Shahzad, M., Farooq, M. S., & Javaid, M. U. (2020). Impact of leadershipbehavior of a project manager on his/her subordinate’s job-attitudes and job-outcomes. Asia Pacific Management Review, 25(1), 38–47. https://doi.org/10.1016/j.apmrv.2019.06.004

- Sadiq, M., Nonthapot, S., Mohamad, S., Chee Keong, O., Ehsanullah, S., & Iqbal, N. (2021). Does green finance matter for sustainable entrepreneurship and environmental corporate social responsibility during COVID-19? China Finance Review International, 12(2), 317–333. https://doi.org/10.1108/CFRI-02-2021-0038

- Saha, R., Cerchione, R., Singh, R., & Dahiya, R. (2020). Effect of ethical leadership and corporate social responsibility on firm performance: A systematic review. Corporate Social Responsibility and Environmental Management, 27(2), 409–429., https://doi.org/10.1002/csr.1824

- Sepúlveda-Rivillas, C.-I., Alegre, J., & Oltra, V. (2021). Impact of knowledge-based organizational support on organizational performance through project management. Journal of Knowledge Management, 26(4), 993–1013. https://doi.org/10.1108/JKM-12-2020-0887

- Shahzad, M., Qu, Y., Rehman, S., Zafar, A., Ding, X., & Abbas, J. (2019). Impact of knowledge absorptive capacity on corporate sustainability with mediating role of CSR: Analysis from the Asian context. Journal of Environmental Planning and Management, 63(2), 148–174. https://doi.org/10.1080/09640568.2019.1575799

- Sun, W., Zhou, Y., Lv, J., & Wu, J. (2019). Assessment of multi-air emissions: Case of particulate matter (dust), SO2, NOx and CO2 from iron and steel industry of China. Journal of Cleaner Production, 232, 350–358. https://doi.org/10.1016/j.jclepro.2019.05.400

- Tee, M., Wang, C., Tee, C., Pan, R., Reyes, P. W., Wan, X., Anlacan, J., Tan, Y., Xu, L., Harijanto, C., Kuruchittham, V., Ho, C., & Ho, R. (2021). Impact of the COVID-19 pandemic on physical and mental health in lower and upper middle-income Asian countries: A comparison between the Philippines and China. Frontiers in Psychiatry, 11, 1–11. https://doi.org/10.3389/fpsyt.2020.568929

- Ul-Hameed, W., Shabbir, M., Imran, M., Raza, A., & Salman, R. (2019). Remedies of low performance among Pakistani e-logistic companies: The role of firm’s IT capability and information communication technology (ICT). Uncertain Supply Chain Management, 7(2), 369–380.

- Viete, S., & Erdsiek, D. (2020). Mobile information technologies and firm performance: The role of employee autonomy. Information Economics and Policy, 51, 100–125. https://doi.org/10.1016/j.infoecopol.2020.100863

- Wu, X., Sadiq, M., Chien, F., Ngo, Q.-T., Nguyen, A.-T., & Trinh, T.-T. (2021). Testing role of green financing on climate change mitigation: Evidences from G7 and E7 countries. Environmental Science and Pollution Research International, 28(47), 66736–66750. https://doi.org/10.1007/s11356-021-15023-w

- Yang, M., Bento, P., & Akbar, A. (2019). Does CSR influence firm performance indicators? Evidence from Chinese pharmaceutical enterprises. Sustainability, 11(20), 5656–5667. https://doi.org/10.3390/su11205656

- Zhang, D., Mohsin, M., Rasheed, A. K., Chang, Y., & Taghizadeh-Hesary, F. (2021). Public spending and green economic growth in BRI region: Mediating role of green finance. Energy Policy, 153, 1122–1137. https://doi.org/10.1016/j.enpol.2021.112256

- Zheng, G.-W., Siddik, A. B., Masukujjaman, M., Fatema, N., & Alam, S. S. (2021). Green finance development in Bangladesh: The role of private commercial banks (PCBs). Sustainability, 13(2), 1–17.

- Zhu, X., Zeng, A., Zhong, M., Huang, J., & Qu, H. (2019). Multiple impacts of environmental regulation on the steel industry in China: A recursive dynamic steel industry chain CGE analysis. Journal of Cleaner Production, 210, 490–504. https://doi.org/10.1016/j.jclepro.2018.10.350