?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Finance plays an important role in China’s new development pattern, and the financial industry is also a crucial part of the country’s economic growth. This paper selects the four financial index data of 76 listed companies in the financial profile of Hithink RoyalFlush stocks and the consolidated balance sheet and consolidated income statement in the China Stock Market Accounting Research (CSMAR) database, empirically studies the impact of tax reduction and fee reduction on the financial industry through the Panel Vector Autoregression (PVAR) model, and gives relevant suggestions. The results show that: (1) The implementation of tax reduction and fee reduction policy makes the net profit available to the financial industry increase in the short term, but the long-term effect is not obvious. (2) The reduction of the tax burden will significantly increase the net sales interest rate of the financial industry within one year, and then the fluctuation in the impact tends to 0. (3) The reduction of the tax burden will lead to the reduction of financial enterprises’ sense of hardship in a certain period of time, which will lead to the reduction of the total asset turnover rate. (4) The reduction of the tax burden will increase the debt-to-asset ratio of financial enterprises within two years, thus increasing financial risk. The research not only provides a theoretical analysis and policy basis for the analysis of the impact of tax reduction on the financial industry but also provides decision support for tax reduction policies to revitalize industry development, stimulate financial market activities, ensure direct access to financial resources to enterprises, and further increase the market activities of the whole society.

1. Introduction

Finance is an important core competitiveness of the country. With the rapid development of globalization and the domestic economy, the financial industry is increasingly related to people’s lives and has become the main force in maintaining economic security and promoting social development (Stiglitz, Citation1998; Benjamin, 2020). In addition, the development of the financial industry can promote the flow of capital in the market and add vitality to national economic development (Gourinchas & Obstfeld, Citation2012). Therefore, a complete financial system is an inevitable condition to ensure the development of China’s economic globalization. In recent years, the treatment of employees and the added value of the financial industry have improved substantially. According to the data of the National Bureau of Statistics, the financial industry ranks among the top three industries in the country in terms of annual income, after the computer service industry and the science and technology research service industry. The annual average wage of financial employees rose from 114885.34 yuan in 2015 to 131405.68 yuan in 2019, and the gross domestic product (GDP) increased from 5.6 trillion yuan in 2015 to 8.4 trillion yuan in 2020, which increased by nearly 2.8 trillion yuan in just six years.

Following the promulgation of financial prudential regulations to curb the real estate bubble, such as the three red lines, concentration management of banks, Asset-Backed Medium-term Notes (ABN), and house purchase balance, the Chinese government has taken practical action to uphold the principle of ‘no speculation for housing’ (Jie, Citation2017). On November 8, 2021, the Sixth Plenary Session of the 19th Central Committee further emphasized the important position of the financial industry.Footnote1 In order to further develop the real economy, support the innovation and development of small and medium-sized enterprises and promote the efficient operation of funds, the Beijing Stock Exchange officially started trading on November 15, 2021. The establishment of the Beijing Stock Exchange reflects the firm determination of China to actively promote the high-quality development of capital markets and deepen financial reform. As an exclusively listed market for small and medium-sized enterprises, the opening of the Beijing Stock Exchange will solve the problems of financing difficulties and high financing for small and medium-sized enterprises, effectively promote their independent research and development as well as innovation, and achieve high-speed and high-quality development (Zhou, 2021). In addition, in order to support the financial industry’s high-quality development, deepen its supply-side reform, and promote its deep integration of standardization and key areas, the People’s Bank of China, together with the Bureau of Market Supervision, the China Banking and Insurance Regulatory Commission (CBIRC), and the China Securities Regulatory Commission (CSRC) jointly issued the ‘14th Five-Year Development Plan for Financial Standardization’ on January 23, 2022 (Song, 2022). The content of the document is committed to improving the financial market system, assisting modern financial management, consolidating the foundation of financial standardization development, and promoting financial standardization reform and innovation.

The tax reform of ‘replacing business tax with value-added tax (VAT)’ avoids the drawbacks of repeated taxation during the business tax period (Zhang et al., Citation2018) and realizes the VAT deduction link of the whole industry in China. On the basis of replacing business tax with VAT, a package of tax reduction and fee reduction policies achieves the goal that the tax burden of all industries is reduced (Group, Citation2022) but not increased to sustain economic growth (Nobilis, Citation2021). However, since implementing a human-oriented and asset-lighted model in the financial sector (Nejad, Citation2022) is more dependent on information technology (Wang, Citation2021), and the system is more complex, the implementation of tax reduction policies may not be in place. Therefore, the study of tax reduction policies in the financial sector can not only test the tax reduction effect but also revitalize the development of banks, stimulate the vitality of financial markets, ensure that financial resources reach enterprises, and further increase social market activities.

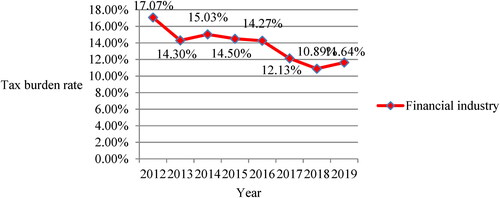

Since replacing business tax with VAT across the board in May 2016, the financial industry has experienced a large tax reduction from 2016 to 2018; thus it has gained room for rapid development, and its GDP has increased more than before; although the tax expenditure of the financial industry rose to Chinese yuan renminbi (CNY) 887.57 billion in 2019, its overall tax burden rate was only 11.64%. Compared with the tax burden rate after replacing business tax with VAT, it was lower than the tax burden rate in other years, except 0.75% more than that in 2018, and was much lower than the tax burden rate of nearly 15% before replacing business tax with VAT (see ). However, with the rapid development of the financial industry, its problems, including urbanization development (Zhang, Citation2022), Internet of Things finance (Li et al., Citation2022), and digital financial risks (Chen, Citation2021), and many contradictions and shortcomings have also been revealed. On February 22, 2019, the Political Bureau of the Central Committee of the Communist Party of China (CPC) carried out its thirteenth collective study on the financial industry. President Xi Jinping pointed out that many factors in China’s financial industry have not yet reached the level required by high-quality economic development, and there are still many outstanding contradictions and problems. Therefore, for the development of the financial industry, it is necessary to analyze the impact of tax cuts on it and give targeted fiscal and taxation policy recommendations.

Figure 1. Tax burden rate of the financial industry.Footnote2

Source: National Bureau of Statistics of the People’s Republic of China from the collated statistical yearbooks of the past years.

China, as the world’s second-largest economy, needs to do a good job in financial risk prevention in order to achieve the goal of common prosperity for a hundred years, promote the healthy and stable development of the real estate industry, and recover rapidly from the novel coronavirus epidemic repeatedly hit the real economy, which is also the reason why this paper selects China as the research object and the financial industry as the research industry. In recent years, China has implemented a package of tax reduction and fee reduction, tax rebate, and tax slowdown policies, which have effectively played a role in helping enterprises rescue and stabilize the macro economy. Therefore, the ultimate goal is to provide a theoretical and policy basis for the country to adopt discretionary taxation policies and promote the development of the financial industry. The contributions and innovations of this paper are as follows: (1) To explore whether the tax cut and fee reduction policy implemented in China in recent years has had a positive effect on the financial industry. (2) From the perspective of measurement, this paper tries to use the Panel Vector Autoregression (PVAR) model to study the specific impact and short-term evaluation of tax cuts on financial industry enterprises from the micro level.

Based on the data provided by Hithink RoyalFlush and China Stock Market Accounting Research (CSMAR) databases, this paper uses the PVAR model to analyze the financial data of 76 listed companies in the financial industry. The study finds that: (1) The reduction of the tax burden has a short-term positive effect on the net profit of financial enterprises, but the long-term effect is not obvious. (2) The reduction of the tax burden will make the net sales interest rate of financial enterprises rise in the short term, but this promotion effect is not obvious in the later period. (3) A lower tax burden will result in a lower total asset turnover rate and a longer-term nature, which will also make financial enterprises reduce their own sense of urgency. (4) The reduction of the tax burden will increase the asset-liability index of financial enterprises and has a certain long-term nature. With the decrease in tax burden, the long-term solvency of financial enterprises decreases, and then the financial risks increase.

The practical significance of the impact of tax cuts on the financial industry is reflected in the following four aspects: First, it promotes the development of the financial industry. At the macro level, tax cuts promote economic growth (Dahlby & Ferede, Citation2012), and the implementation of more preferential tax policies for the financial industry can give the financial industry better development space. As an important part of national development, the financial industry has a positive impact on the business environment and the advancement of the whole society when its financial risk is reduced, and it is dynamic and digital. (Allen et al., Citation2017; Niemand et al., Citation2021). Second, it promotes regional economic development. If the financial industry gets rapid development due to tax reduction and fee reduction policies, the financial industry can better serve the real economy and promote its development of the real economy (Cărăușu, Citation2018). Regional development is more dependent on the real economy; the development of the real economy will greatly promote regional development (Wang & Tan, Citation2021). Third, it promotes financial risk control. Financial risks are transmitted and divergent. Financial risk management helps to prevent financial risks (Wang et al., Citation2022), which can not only reasonably avoid the disadvantages caused by financial risks in the financial industry but also maintain the stability of the entire market economy. Fourth, a higher income-tax rate reduces the after-tax wage income that individuals receive, adversely affecting their work incentives (Ferede, Citation2021).

2. Literature review and research hypothesis

2.1. Literature review

As an important part of economic development, the financial industry plays an extremely important role in promoting the development of the real economy. At the macro level, the promotion of the development of the real economy is reflected in many aspects. With the promotion of national policies, green financial investment is becoming more and more important to prevent economic and political risks (Ning et al., Citation2022). Ye et al. (Citation2022) obtained through sparse support vector quantile regression that the development of financial technology can effectively reduce poverty and promote regional economic development. Wang et al. (Citation2022) found through dynamic effect analysis that sustainable financing can promote the green development of China’s economy. In the process of economic development, government intervention should be strengthened to promote the development of green productivity at the macro level. The results of that study indicated that policymakers should give priority to promoting the development of the financial industry. Some scholars found that the benign development of finance is conducive to the growth of employment through generalized method of moments (GMM) estimation (Wen et al., Citation2022). However, the sound development of the financial industry is inseparable from the adjustment of its own structure and the government’s policy intervention. In terms of structural adjustment of financial institutions themselves, some scholars believe that financial institutions should combine financial services with technology, labor and other factors to improve the performance level of enterprises (Yi et al., Citation2022). In addition, the new financial services provided by the financial industry have made great contributions to promoting national economic development. The development of traditional finance can improve the inclusiveness of digital finance, help narrow the income gap between urban and rural areas, and promote the development of digital technology (Li et al., Citation2022). Filippidis and Katrakilidis (Citation2015) studied the impact of the economic system and human development on financial development through the data of 52 developing economies from 1985 to 2008. The research results show that the economic system and human development play an important role in the development of financial institutions. By building a spatial econometric model, scholars found that the adjustment of monetary policy is conducive to digital finance to promote economic growth and believed that the intervention of monetary policy in the development of digital finance should be strengthened (Jiang et al., Citation2022). Scholars found that digital inclusive finance can significantly promote export upgrading (Pan et al., Citation2022) through Chinese customs data and the digital financial inclusion index of Peking University in China.

At the micro level, as a representative sub-industry of the financial industry, the banking sectors are very important in serving the development of the real economy. Effiom and Edet (Citation2022) found that the financial innovation tools used by the Bank of Nigeria have a significant role in promoting the productivity of Nigerian small and mid-size enterprises (SMEs) through the study of the autoregressive distributed lag method. The biggest problem faced in the development of SMEs is the limited financing channels, and financial institutions will greatly facilitate SMEs’ access to capital (Rao et al., Citation2021). Yuan and Zongxian (2019) found through the evolutionary game that under a stable business strategy, commercial banks will provide different loan strategies after comprehensively judging the repayment ability of enterprises to solve the financing problems of SMEs and promote the development of SMEs. Ipek (2019) studied 492 samples of Turkish SMEs through the logistic regression method and found that the banking industry was willing to lend to innovative, service-oriented SMEs with frequent business activities. As the main factor affecting the efficiency of resource allocation, government intervention can adjust the efficiency of resource allocation in financial sectors to promote national economic growth (Li et al., Citation2022).

Since the reform of replacing business tax with VAT, China has adopted a series of tax and fee reduction policies to further strengthen macroeconomic regulation (Xing, Citation2020), stimulate the vitality of microeconomic entities, and maintain local financial operations. At present, due to the repeated impact of the epidemic, the global economic recovery is slow, and there is a negative effect on the Gig economy (Umar et al., Citation2021), and the pressure on government revenue and expenditure is increasing (Chen, Citation2017). In order to boost the economy, major economies in the world have implemented policies to cut taxes and fees. As the world’s second-largest economy, China has also implemented tax reduction and fee reduction policies in line with its own economic development. Academic circles have extensively studied the differential effects of tax and fee reduction policies among industries by using different methods and perspectives. Their research consensus is that China has made remarkable achievements in reducing taxes and fees. However, some studies also found that the effects of tax and fee reduction in different industries are quite different. Wang et al. (2021) empirically studied the effectiveness of tax and fee reduction policies through a time-varying parameter (TVP) model. The study found that the effect of tax and fee reduction policies on economic growth is obvious, but there is significant variation in the effectiveness of tax reduction measures in industry structure. Zhang and Gao (2022) empirically studied the policy effect of tax and fee reduction in China through a multiple regression model. The study found that tax and fee reduction improved the confidence of real enterprises in future economic development. Among them, the effect on the manufacturing industry is more significant (Ying, 2020), while the existence of the real estate industry, the financial industry, and the industry tax burden outliers will hinder the sustainable development of the regional economy (Shen et al., Citation2021, Suzuki, Citation2022). Internationally, Isik et al. (Citation2020) used the differences-in-differences (DID) method to examine the impact of agricultural input costs on food prices in Turkey. The analysis results provide some hints that consumers received benefits from the tax reduction decisions. In terms of research methods, Lee (Citation2022) advocated the process and comprehensive method of establishing the causal relationship between ESG behavior and financial performance variables and put forward the method of analyzing the model. Gordon and Sarada (Citation2018) found that the tax reduction policy can ease the pressure on enterprise access, which has a positive impact on enterprise access. Therefore, scholars have increased the research on the tax reduction effect in the financial industry.

2.2. Hypotheses development

Some scholars believe that tax and fee reduction policies have positive promotion significance for enterprise profitability, enterprise innovation, and debt financing cost reduction. Tax and fee reduction policies can effectively promote the development of enterprises, especially small and medium-sized enterprises, but have a small and insignificant impact on GDP (Ekmekjian et al., Citation2022). In terms of enterprise R&D investment, Hossain and Rahman (Citation2021) found that corporate tax cuts do not affect R&D expenditures by all publicly traded firms in the U.S., while an increase in the tax rate leads to a decrease in R&D spending. Scholars have conducted an empirical study on the effect of tax reduction and fee reduction policies on promoting innovation development through DID methods, and the results show that tax reduction and fee reduction policies can significantly increase enterprises’ investment in R&D, enhance entrepreneurs’ confidence, and promote enterprises’ innovation output (Zheng and Zhang, 2020, Cao et al., Citation2022). Tax benefits are also granted to companies to improve current corporate performance, which directly increases current corporate performance, such as return on assets (ROA) (Fotiou et al., Citation2020). Furthermore, Hussain (2014) used VAR estimates to show that permanent and exogenous tax increases have strong, permanent, and negative effects on total factor productivity (TFP), which represents about 80% of the change in output following the tax increase. Based on this, this paper proposes the following hypothesis:

Hypothesis 1: Tax cuts can effectively promote the development of the financial sectors in the short term but not in the long term.

Hypothesis 2: The tax cut and fee reduction policy will improve the profitability of the financial industry but will not be sustainable in the long run.

Further studies by some scholars found that the financial industry is special, and the existing tax policy is unscientific (Савић, Citation2016; Yu et al., 2020). They also concluded that the tax policy implemented after replacing business tax with VAT has significantly reduced the tax burden of the downstream tertiary industry in the financial industry. The current tax policy and system are not perfect, and there are loopholes in tax collection and management. However, large financial firms are now strictly compliant with tax laws, while small financial firms are likely to evade taxes to earn more profits (Guo, Citation2020). The defects of tax policy will also lead to more short-term idle investment in the financial industry and strong volatility in the securities market. At the same time, an excessive tax burden reduces the enthusiasm of financial institutions to participate, which seriously affects the development of the financial industry (Zhang, 2019). Richardson (Citation2018) believed that tax policy played a positive role in stabilizing and reducing the tax burden of the financial industry. Based on this, this paper proposes the following hypothesis:

Hypothesis 3: Tax cuts reduce the tax burden of the financial industry.

3. Variable description and model design

3.1. Data sources

The data comes from the four financial indicators that have been calculated in the financial situation of Hithink RoyalFlush stock. The consolidated balance sheet and consolidated profit statement of listed financial companies (including banking, insurance, securities, and non-banking finance) are in the CSMAR database. In order to reflect the representativeness and ensure the balance of the data, the ST-listed companies and the listed companies after the first quarter of 2016 were excluded, and 76 listed companies were finally selected. The sample time span is 21 data from the second quarter of 2016 to the second quarter of 2021.

3.2. Index selection and variable setting

The selection of indicators in this paper is mainly based on the following three reasons: (1) Through the collection of enterprise tax-related data and financial statements (balance sheet and profit statement), the selection of indicators is based on the representative indicators of financial stability, including indicators that comprehensively consider the tax burden of enterprises (including tax burden rate, input and output tax ratio); enterprise profitability indicators (including net profit margin on sales, net profit growth rate, returns on total assets (ROTA), main business profit rate, main business cost rate, total revenue growth rate, return on equity (ROE), etc.); enterprise operational capability indicators (including inventory turn over (ITO), accounts receivable turnover, total asset turnover rate, cost and expense ratios, and current asset turnover);enterprise growth capacity indicators (including main business income growth rate, net profit growth rate, net asset growth rate and total asset growth rate);corporate solvency indicators(including operating cash flow ratio, debt to asset ratio, current ratio (CR), quick ratio (QR), etc.). (2) Taking into account the availability and convenience of data, this paper refers to the data information that can be obtained from the financial profile of Hithink RoyalFlush stock information, and directly uses the relevant indicators commonly used in the above four financial indicators displayed by Hithink RoyalFlush software. Although each financial index in Hithink RoyalFlush stock software contains more specific indicators, excessive selection of indicators will lead to dimension disaster. At the same time, in order to avoid repeated selection of indicators, indicators with similar meanings will have to be selected. For example, only the current ratio (CR) is taken for both the current ratio and quick ratio (QR), and only the net profit margin on sales is taken for both the net profit margin on sales and gross profit margin. The indicators selected from the Hithink RoyalFlush data are net profit growth rate, total revenue growth rate, net profit margin on sales, ROE, inventory turnover (ITO), current ratio (CR), and debt to asset ratio. Calculation of cost and expense ratios, accounts receivable turnover, total asset turnover, and comprehensive tax burden from consolidated balance sheets and consolidated income statements (in this paper, it equals the sum of tax and additional and income tax costs divided by the total operating income, which is relatively reasonable to use this indicator without VAT). It is particularly important to note that the relevant data in the income statement (such as operating costs, total operating income, income tax costs, etc.) that need to be calculated through the financial statements of the indicators in the calculation process should be calculated as current data. Since the banking, insurance, and securities industries do not involve ITO and CR, these two indicators are deleted. And since many banks have not disclosed accounts receivable in recent years, the data on accounts receivable turnover is incomplete, so this indicator is deleted, and it eventually covers four major capacity indicators and tax burdens, with a total of eight indicators, namely net profit growth rate year on year, total operating income growth rate year on year, the net profit margin on sales, ROE, cost and expense ratios, total asset turnover rate, debt to asset ratio, and comprehensive tax burden, respectively recorded as (Refer to for details).

Table 1. Description of related data variables.

3.3. Model design

The panel data of 76 listed financial companies contain more time dimension data, and the amount of information is large. Therefore, the possibility of deviation may also be large and easily affect the analysis results. The PVAR model can regard the variables studied as endogenous variables, and each endogenous variable is regarded as a function of the lag value of all endogenous variables in the system. Therefore, the model can provide rich structures and capture more features of the data studied. In addition, the advantage of the PVAR model is that it allows individual effects and heteroscedasticity in the data. Therefore, the PVAR model using panel data can effectively solve the problem of individual heterogeneity and fully consider the individual and time effects.

This empirical analysis uses the following PVAR model:

(1)

(1)

Where represents the individual,

represents the quarter,

is the column vector of endogenous variables including the four capacity indicators of financial analysis and tax burden,

is the lag order,

is the disturbance column,

is the individual effect,

is the time effect, and is estimated by the generalized moment method (GMM) (see Holtz-Eakin et al., Citation1988).

4. The empirical results

4.1. Stationarity test

Before the PVAR model analysis of the data, it is necessary to test the unit root of the relevant index data to ensure the stability of the data. This paper adopts the IPS and LLC tests, and the results (see ) show that all indicators do not reject the stationary test at the 1% significance level. In order to avoid the trouble of dimensionality caused by excessive dependent variables in the process of model estimation, among the four financial indicators, only one representative is selected for each indicator. In other words, Select in

and

due to the correlation of multiple collinearities of

and

is eliminated; select

in

and

five indicators are finally selected, namely, net profit growth rate year on year, net profit margin on sales, total asset turnover rate, debt to asset ratio, and comprehensive tax burden.

Table 2. Stability test results of each index.

4.2. Pvar model result

This paper draws on the research results of Lian Yujun and uses Stata software to fit. shows that the optimal lag order of the Akaike information criterion (AIC), bayesian information criterion (BIC), and HQIC (Hannan-Quinn information criterion) values of the model is 5; that is, the PVAR model has better estimation results than the five-quarter lag periods. Therefore, the five-variable PVAR model is established and estimated by the GMM method, and the impulse response shocks in are obtained for the comprehensive tax burden.

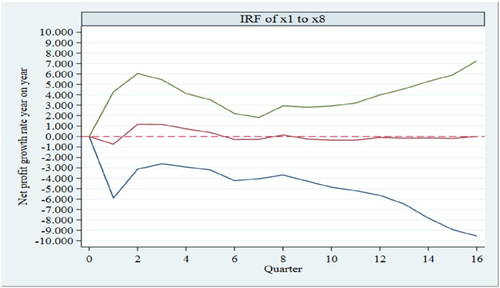

Figure 2. Response of net profit growth rate year on year to the comprehensive tax burden.

Source: results of impulse response operation of the sorted data by stata software.

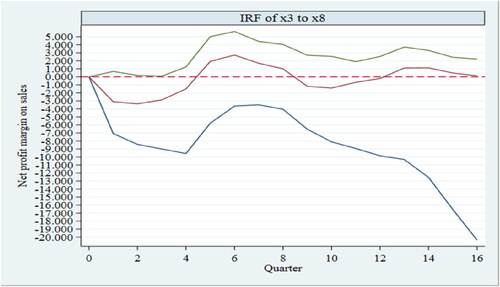

Figure 3. Response of net profit margin on sales to the comprehensive tax burden.

Source: results of impulse response operation of the sorted data by stata software.

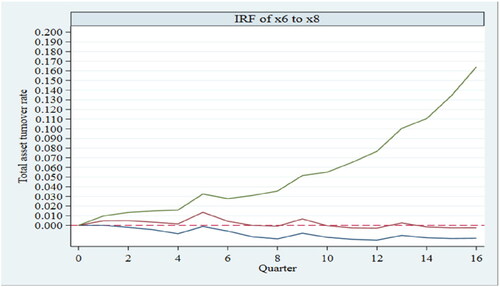

Figure 4. Response of total asset turnover rate to the comprehensive tax burden.

Source: results of impulse response operation of the sorted data by stata software.

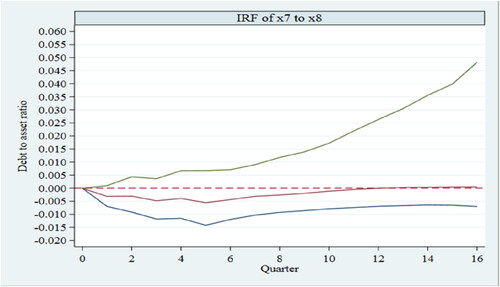

Figure 5. Response of debt to asset ratio to the comprehensive tax burden.

Source: results of impulse response operation of the sorted data by stata software.

Table 3. Optimal lag order selection results.

As can be seen from , when the comprehensive tax burden is positively impacted by 1 unit, the net profit growth rate year on year will decrease first, and this negative effect will reach the maximum-0.8 after a quarter. After one quarter, the negative effect gradually decreases and gradually transforms into a positive effect until it reaches a maximum value of 1.1 in two quarters. After two quarters, this positive effect gradually weakens and approaches 0, until it reaches a stable state after five quarters. This shows that the increase in the current comprehensive tax burden will reduce net profit growth over the next quarter; and make net profit growth rate year on year increase in the next two to five quarters. It can be seen from that when the tax burden rate is positively impacted by one unit, it will also have a negative effect on the net profit margin in the first four periods (one year), and this negative effect will reach the maximum value of −3.2 after two quarters. After five quarters, it turns into a positive effect. After eight quarters, the above fluctuation impact is repeated, but the impact is significantly weakened. This shows that the increase of the comprehensive tax burden will first reduce the net profit margin of the financial industry and will start to promote the growth of the net profit margin of enterprises in one year, but this promotion will gradually weaken in the second year. The data trend in shows that when the tax burden is positively impacted by 1 unit, the impact on the total asset turnover rate is close to 0, which is obvious, but it will still have a positive role in promotion. shows that when the tax burden is positively impacted by 1 unit, it will have a relatively long-term negative effect on the debt-to-asset ratio, but this negative effect is close to 0 and not obvious.

5. Conclusion

This paper selects the four financial index data of 76 listed companies in the financial profile of Hithink RoyalFlush stocks and the consolidated balance sheet and consolidated income statement in the CSMAR database, empirically studies the impact of tax reduction and fee reduction on the financial industry through the PVAR model, and gives relevant suggestions. The implementation of a tax reduction policy has led to a relative reduction in the tax burden of the financial industry. According to the impact of the tax burden rate on the net profit growth rate in the impulse response diagram, when the tax burden is relatively low, the net profit that the financial industry can obtain will be relatively increased in the short term, which will promote the short-term development of the financial industry. However, since there are relatively few preferential tax policies related to the financial industry in the tax reduction policy, this will lead to the fact that the year-on-year growth rate of net profit in the financial industry cannot increase with the decrease of the tax burden rate for a long time, and the year-on-year growth of net profit in the financial industry will gradually slow down in the later period, which confirms Hypothesis 1.

The net profit margin on sales in the financial industry has been significantly improved in one year when the tax burden is reduced; that is, the profitability of enterprises is enhanced, and more profits are obtained, which also confirms hypothesis 2 of this paper. The net profit margin on sales in the financial industry will also be relatively low for a long time because of the lack of support from tax reduction policy, and the growth of sales income in the financial industry will also be relatively slow, indicating that over time, tax incentives should also keep pace with the times, so as to adapt to and help the development of the industry.

Under the tax cut and fee reduction policy, the reduction of the tax burden rate of the financial industry has no obvious effect on its total asset turnover in the short term, but there is a tendency to reduce the total asset turnover in the long term. It shows that the decrease in tax burden decreases the operating efficiency of the financial industry’s own funds, and the decrease in the sales ability of the financial industry will lead to a decrease in the utilization efficiency of private funds.

A lower tax burden increases the debt-to-asset ratio of the financial industry, and the impact lasts for a long time. It shows that with the implementation of tax cuts, the financial sector is more inclined to borrow money to maintain its own operations, but this leads to relatively higher financial risks in the financial sector. When the financial risk of the financial industry increases, it may lead to insufficient cash flow for the financial industry to pay its debts promptly, and it will also affect the timely collection of taxes.

This paper attempts to add 36 listed companies covering the New Third Board to the above samples and then subdivide them into banking, insurance, and securities industries for analysis. However, due to the small sample size of each industry after subdividing, it has not obtained good results. The method of this paper is also applicable to other industries or sub-regions and scales to examine the heterogeneous impact of tax cuts on other industries or different scales in different regions and then propose more targeted tax policies for different industries and different scales in different regions. This is also the practical significance of this paper.

5.1. Policy implications

In order to promote the healthy and sustainable development of the economy, ensure stable economic operation, and continue to bring into play the long-term and short-term effects of tax reduction and fee reduction, it is necessary to accurately implement policies for the industry in the future. Based on the results of this study, the following three aspects of tax policy recommendations for the financial industry are proposed:

Tax reduction policies adapted to the development of the financial industry should be stable, long-term, and keep pace with the times.

At present, the preferential tax policy of tax reduction and fee reduction basically stipulates the applicable time of the policy. Because of the short duration of the policy, financial enterprises often find it difficult to adjust their business methods in time to better enjoy the tax benefits brought by the tax reduction policy. For example, the notice on the VAT exemption policy for the loan interest income of small and micro enterprises in financial institutions has continued this policy to stimulate the development of both sides. Therefore, according to the current situation of the development of the financial industry, the state should relatively extend the implementation time of tax reduction and fee reduction policy for the financial industry, so that the financial industry has more time to enjoy the tax reduction and fee reduction policy. At the same time, according to the characteristics of the development of the industry, the state should continuously introduce new preferential tax policies in line with the development of the industry.

2. Enhancing the pertinence of tax reduction and fee reduction policies in the financial industry

Among the tax and fee reduction policies, there are relatively few preferential policies for the financial industry, which leads to the inconspicuous effect of tax reduction and fee reduction in the financial industry. The state should introduce some specific tax reduction and fee reduction policies for the financial industry to further strengthen the role of finance in promoting national economic development. The manufacturing industry is the ‘ballast stone’ of the great power economy. In order to encourage financial institutions to increase financial credit support for manufacturing enterprises, industry loan interest income should be included in the exemption category. In view of the income of securities companies and local state-owned platforms to support the listing of ‘specialized new’ small and medium-sized enterprises, it is suggested that certain tax incentives should be given. At the same time, in order to retain local taxes, certain tax incentives should be given to the personal income tax reduced after the listing so as to achieve the precision of the policy.

3. Improving the precise service level of tax authorities

To speed up the implementation time of tax policy, without disturbing the enterprises, the tax authorities should push them to the relevant enterprises in the jurisdiction through the electronic tax bureau, WeChat, or SMS after the relevant tax reduction and fee reduction policies begin to pilot in some areas. Provide sufficient time for financial industry enterprises to adjust their business model and strategic planning in order to better enjoy the tax incentives brought by tax reduction and fee reduction policy. When the new policy is formally implemented, the tax authorities should communicate with relevant beneficiary enterprises for the first time to achieve precise service. This not only helps to reduce the tax cost of enterprises but also improves the tax collection efficiency of tax authorities.

Disclosure statement

The authors report there are no competing interests to declare.

Additional information

Funding

Notes

1 China economic situation report network: http://www.china-cer.com.cn/guwen/2021111815703.html

2 Data sources: National Bureau of statistics of China

References

- Allen, F., Qian, J. Q., & Gu, X. (2017). An overview of China’s financial system. Annual Review of Financial Economics, 9(1), 191–231. https://doi.org/10.1146/annurev-financial-112116-025652

- Babar, D. (2020). A Macro analysis of Corporate Tax Cuts: A Strategy to improve India’s Competitiveness. Buettner, Thiess, and Katharina Erbe. “Revenue and welfare effects of financial sector VAT exemption. International Tax and Public Finance, 21(6)2014):, 1028–1050. https://ssrn.com/abstract=3630106

- Braun, B. (2020). Central banking and the infrastructural power of finance: The case of ECB support for repo and securitization markets. Socio-Economic Review, 18(2), 395–418. https://doi.org/10.1093/ser/mwy008

- Cao, Q., Wang, H., & Cao, L. (2022). “Business Tax to Value-added Tax” and Enterprise Innovation Output: Evidence from Listed Companies in China. Emerging Markets Finance and Trade, 58(2), 301–310. https://doi.org/10.1080/1540496X.2021.1939671

- Cărăușu, D. N. (2018). The Relationship Between Finance and Economic Growth. Journal of Public Administration, Finance and Law, (13), 37–48. https://www.ceeol.com/search/article-detail?id=744250

- Савић, С. (2016). Tax calculation account method as a potential method of taxing financial services. Acta Economica, 14(25), 111–130. https://doi.org/10.7251/ACE1625111S[Mismatch

- Chen, S. X. (2017). The effect of a fiscal squeeze on tax enforcement: Evidence from a natural experiment in China. Journal of Public Economics, 147, 62–76. https://doi.org/10.1016/j.jpubeco.2017.01.001

- Chen, Y., Kumara, E. K., & Sivakumar, V. (2021). Invesitigation of finance industry on risk awareness model and digital economic growth. Annals of Operations Research, 1–22. https://doi.org/10.1007/s10479-021-04287-7

- Dahlby, B., & Ferede, E. (2012). The effects of tax rate changes on tax bases and the marginal cost of public funds for Canadian provincial governments. International Tax and Public Finance, 19(6), 844–883. https://doi.org/10.1007/s10797-012-9210-7

- Dharmapala, D., & Riedel, N. (2013). Earnings shocks and tax-motivated income-shifting: Evidence from European multinationals. Journal of Public Economics, 97, 95–107. https://doi.org/10.1016/j.jpubeco.2012.08.004

- Effiom, L., & Edet, S. E. (2022). Financial innovation and the performance of small and medium scale enterprises in Nigeria. Journal of Small Business & Entrepreneurship, 34(2), 141–174. https://doi.org/10.1080/08276331.2020.1779559

- Ekmekjian, E. C., & Snyder, T. C. (2022). How Did the Tax Cuts and Jobs Act Impact Stock Prices, Business Investment, Economic Growth and Unemployment in the United States? International Journal of Economics & Business Administration (IJEBA), 10(1), 3–14. https://www.ijeba.com/journal/745/download

- Ferede, E. (2021). Will Cutting Income Tax Rates Create Jobs for Canadians?. https://policycommons.net/artifacts/1501824/will-cutting-income-tax-rates-create-jobs-for-canadians/2160801/

- Feng, X. (2020). An Empirical Study on the Relationship between Financial Taxation and Economic Growth Based on Provincial Panel Data. Tax Research, 1, 34–38. https://kns.cnki.net/kcms/detail/detail.aspx?dbcode=CJFD&dbname=CJFDLAST2020&filename=SWXH202001006&uniplatform=NZKPT&v=6v0UIFrQaJjhvL-TN96dsrxLpDIgpT6dwGGQV06kvi3KfKcgyKeg91KpFu7wZTaM

- Filippidis, I., & Katrakilidis, C. (2015). Finance, institutions and human development: Evidence from developing countries. Economic Research-Ekonomska Istraživanja, 28(1), 1018–1033. https://doi.org/10.1080/1331677X.2015.1100839

- Fotiou, A., Shen, W., & Yang, S. C. S. (2020). The fiscal state-dependent effects of capital income tax cuts. Journal of Economic Dynamics and Control, 117, 103860. https://doi.org/10.1016/j.jedc.2020.103860

- Giaretta, E., & Chesini, G. (2021). The determinants of debt financing: The case of fintech start-ups. Journal of Innovation & Knowledge, 6(4), 268–279. https://doi.org/10.1016/j.jik.2021.10.001

- Gordon, RSarada. (2018). How should taxes be designed to encourage entrepreneurship? Journal of Public Economics, 166, 1–11., https://doi.org/10.1016/j.jpubeco.2018.08.003

- Gourinchas, P. O., & Obstfeld, M. (2012). Stories of the twentieth century for the twenty-first. American Economic Journal: Macroeconomics, 4(1), 226–265. https://doi.org/10.3386/w17252

- Group, W. R. B. D. (2022). Turkey’s botas in financial squeeze due to rising energy prices. Worldwide Refining Business Digest: The Fast-read Comprehensive Newaletter for Busy Professionals Working in the Refining Industry(May.). https://xueshu.baidu.com/usercenter/paper/show?paperid=1b490js0vw1804e05j6r0pd0n8120752&site=xueshu_se

- Guo, J. T., & Hung, F. S. (2020). Tax evasion and financial development under asymmetric information in credit markets. Journal of Development Economics, 145, 102463. https://doi.org/10.1016/j.jdeveco.2020.102463

- Holtz-Eakin, D., Newey, W., & Rosen, H. S. (1988). Estimating vector autoregressions with panel data. Econometrica, 56(6), 1371–1395. https://doi.org/10.2307/1913103

- Hossain, R., & Rahman, A. (2021). Is There Anything Good About Corporate Tax Cut? Economics Bulletin, 41(3), 896–910. https://econpapers.repec.org/RePEc:ebl:ecbull:eb-20-00265

- Hussain, S. M. (2015). The contractionary effects of tax shocks on productivity: An empirical and theoretical analysis. Journal of Macroeconomics, 43, 93–107. https://doi.org/10.1016/j.jmacro.2014.09.006

- Ipek Erdogan, A. (2019). Determinants of perceived bank financing accessibility for SMEs: evidence from an emerging market. Economic Research-Ekonomska Istraživanja, 32(1), 690–716. https://doi.org/10.1080/1331677X.2019.1578678

- Isik, S., & Özbuğday, F. C. (2020). The role of tax cuts on agricultural input prices in Turkey. Studies in Agricultural Economics, 122(3), 167–171. https://doi.org/10.7896/j.2070

- Jack, W. (2000). The treatment of financial services under a broad-based consumption tax. National Tax Journal, 53(4.1), 841–851. https://doi.org/10.17310/ntj.2000.4.03

- Jiang, S., Qiu, S., & Zhou, H. (2022). Will digital financial development affect the effectiveness of monetary policy in emerging market countries? Economic Research-Ekonomska Istraživanja, 35(1), 3437–3472. https://doi.org/10.1080/1331677X.2021.1997619

- Jie, C. H. E. N. (2017). Promote” Housing is not for Speculation” Housing System Construction through Supply Side Reform. China Development. https://kns.cnki.net/kcms/detail/detail.aspx?dbcode=CJFD&dbname=CJFDLAST2018&filename=ZGFZ201705004&uniplatform=NZKPT&v=YYS2TfWXPSDgGlD00L1bhROPJj8UaCxa6SvRRlZI4Vkc18Z-1JFCjnWlKS6D0yPe

- Lee, M. T., & Suh, I. (2022). Understanding the effects of Environment, Social, and Governance conduct on financial performance: Arguments for a process and integrated modelling approach. Sustainable Technology and Entrepreneurship, 1(1), 100004. https://doi.org/10.1016/j.stae.2022.100004

- Legwaila, T. (2018). An exposé of the value-added tax muddle in financial services in South Africa. Journal of South African Law/Tydskrif Vir Die Suid-Afrikaanse Reg, 2018(3), 587–600. https://doi.org/10.10520/EJC-f520ef488

- Lencho, T. (2011). To Tax or Not To Tax: Is that Really the Question?–VAT, Bank Foreclosure Sales, and the Scope of Exemptions for. Mizan Law Review, 5(2), 264–310. https://doi.org/10.4314/mlr.v5i2.4

- Li, M. C., Feng, S. X., & Xie, X. (2022). Spatial effect of digital financial inclusion on the urban–rural income gap in China—analysis based on path dependence. Economic Research-Ekonomska Istraživanja, 1–22. https://doi.org/10.1080/1331677X.2022.2106279

- Li, Y. (2022). Security and Risk Analysis of Financial Industry Based on the Internet of Things. Wireless Communications and Mobile Computing, 2022, 1–13. https://doi.org/10.1155/2022/6343468

- Li, Z. (2022). The influence of economic institution on finance sector credit allocation in China. Economic Research-Ekonomska Istraživanja, 35(1), 728–745. https://doi.org/10.1080/1331677X.2021.1931915

- Muthitacharoen, A. (2021). Tax rate cut and firm investment: evidence from Thailand. Applied Economics Letters, 28(3), 220–224. https://doi.org/10.1080/13504851.2020.1743813

- Nejad, M. G. (2022). Research on financial innovations: an interdisciplinary review. International Journal of Bank Marketing, 40(3), 578–612. https://doi.org/10.1108/IJBM-07-2021-0305

- Ning, Q. Q., Guo, S. L., & Chang, X. C. (2022). Nexus between green financing, economic risk, political risk and environment: evidence from China. Economic Research-Ekonomska Istraživanja, 35(1), 4195–4219. https://doi.org/10.1080/1331677X.2021.2012710

- Niemand, T., Rigtering, J. C., Kallmünzer, A., Kraus, S., & Maalaoui, A. (2021). Digitalization in the financial industry: A contingency approach of entrepreneurial orientation and strategic vision on digitalization. European Management Journal, 39(3), 317–326. https://doi.org/10.1016/j.emj.2020.04.008

- Nobilis, B. (2021). On the road towards a competitive tax system:hungarian perspective. Belt and Road Taxation (English), 2(6), 43–48. https://xueshu.baidu.com/usercenter/paper/show?paperid=1m4f00m0ws5x0px06y730440r3683073&site=xueshu_se

- Pan, Y., Ma, L., & Wang, Y. (2022). How and what kind of cities benefit from the development of digital inclusive finance? Evidence from the upgrading of export in Chinese cities. Economic Research-Ekonomska Istraživanja, 35(1), 3979–4007. https://doi.org/10.1080/1331677X.2021.2007414

- People’ s Bank of China Chongqing Business Management Department of Accounting and Finance Research Group. (2021). Research on the impact of financial industry tax on regional financial development—empirical analysis based on spatial econometric model. Financial Accounting, (2), 64–70. https://kns.cnki.net/kcms/detail/detail.aspx?dbcode=CJFD&dbname=CJFDLAST2021&filename=JRKJ202102012&uniplatform=NZKPT&v=jqQ1e0xAq0ZWsOfOwWiDX5KR6y_mbwPtFW9dqkyd9jppai6b5XYRYbezIOf6mUvk

- Rao, P., Kumar, S., Chavan, M., & Lim, W. M. (2021). A systematic literature review on SME financing: Trends and future directions. Journal of Small Business Management, 1–31. https://doi.org/10.1080/00472778.2021.1955123

- Richardson, D. (2018). Company tax changes and the big four banks. https://australiainstitute.org.au/wp-content/uploads/2020/12/P485-Company-tax-changes-benefits-for-the-big-four-banks.pdf

- Shen, Z., Miao, J., & Li, L. (2021). Study on tax burden calculation and risk allocation for industries in free trade zones. Economic Research-Ekonomska Istraživanja, 34(1), 880–901. https://doi.org/10.1080/1331677X.2020.1805346

- Yan, S. (2022). The Central People’s Government of the People’s Republic of China, Four departments printed and distributed the 14th five year development plan for financial standardization: http://english.www.gov.cn/policies/policywatch/202202/10/content_WS62046362c6d09c94e48a4e3f.html

- Stiglitz, J. (1998). JuneThe role of the financial system in development. In Presentation at the Fourth Annual Bank Conference on Development in Latin America and the Caribbean (Vol. 29, p. 17). http://www.kleinteilige-loesungen.de/globalisierte_finanzmaerkte/texte_abc/s/stiglitz_financial_system_in_development.pdf

- Suzuki, K. (2022). Corporate tax cuts in a Schumpeterian growth model with an endogenous market structure. Journal of Public Economic Theory, 24(2), 324–347. https://doi.org/10.1111/jpet.12545

- Umar, M., Xu, Y., & Mirza, S. S. (2021). The impact of Covid-19 on Gig economy. Economic Research-Ekonomska Istraživanja, 34(1), 2284–2296. https://doi.org/10.1080/1331677X.2020.1862688

- Wang, R., & Tan, J. (2021). Exploring the coupling and forecasting of financial development, technological innovation, and economic growth. Technological Forecasting and Social Change, 163, 120466. https://doi.org/10.1016/j.techfore.2020.120466

- Wang, X., Wu, Z., & Shen, S. (2022). Financial Technology Risk Management and Control in the Big Data Era. In International Conference on Cognitive based Information Processing and Applications (CIPA 2021). (pp. 368–374) Springer. https://doi.org/10.1007/978-981-16-5854-9_46

- Wang, X., Sun, L., Razzaq, H. K., Abdul-Samad, Z., & The Cong, P. (2022). The dynamic role of ecological innovation and sustainable finance in improving green productivity: evidence from China. Economic Research-Ekonomska Istraživanja, 1–18. https://doi.org/10.1080/1331677X.2022.2103840

- Xiaoping, W., Bing, J., & Yongfu, C. (2021). Research on the effect evaluation and optimization path of China’s tax and fee reduction policies - empirical analysis based on TVP model. Local Finance Research, 3, 58–66 + 85. https://kns.cnki.net/kcms/detail/detail.aspx?dbcode=CJFD&dbname=CJFDLAST2021&filename=DFCZ202103010&uniplatform=NZKPT&v=Oi0BgkyK0cwaemmWzce4aRNfiqf1GxS5SNlgcFjJzqut6Yr4ePmWsRr7le6VNCLZ

- Wang, Y. (2021). Prevention of Internet Financial Risks in the Era of Digital Economy. Proceedings of Business and Economic Studies, 4(5), 38–44. https://doi.org/10.26689/pbes.v4i5.2649

- Wen, J., Mahmood, H., Khalid, S., & Zakaria, M. (2022). The impact of financial development on economic indicators: A dynamic panel data analysis. Economic Research-Ekonomska Istraživanja, 35(1), 2930–2942. https://doi.org/10.1080/1331677X.2021.1985570

- Liyun, W. (2020). Research on the development status and countermeasures of financial service industry in Zhejiang Province. Rural Economy and Science and Technology, 31, 146–148. https://kns.cnki.net/kcms/detail/detail.aspx?dbcode=CJFD&dbname=CJFDLAST2020&filename=NCJI202009055&uniplatform=NZKPT&v=zGatHsY6GiCjp41MEVOYuTbVGSfbI68bMl4KUc4k_dELnOMhsL2WQojW_xLT1K8V

- Xing, K. (2020). Economic High-quality Development Research Based on Tax Cut and Fee Reduction. https://www.researchgate.net/publication/342659950_Economic_High-quality_Development_Research_Based_on_Tax_Cut_and_Fee_Reduction

- Ye, Y., Chen, S., & Li, C. (2022). Financial technology as a driver of poverty alleviation in China: Evidence from an innovative regression approach. Journal of Innovation & Knowledge, 7(1), 100164. https://doi.org/10.1016/j.jik.2022.100164

- Yi, H., Meng, X., Linghu, Y., & Zhang, Z. (2022). Can financial capability improve entrepreneurial performance? Evidence from rural China. Economic Research-Ekonomska Istraživanja, 1–20. https://doi.org/10.1080/1331677X.2022.2091631

- Yuanyuan, H., & Zongxian, F. (2019). Is collective financing feasible for small and micro-sized enterprises? An evolutionary game analysis of the credit market in China. Economic Research-Ekonomska Istraživanja, 32(1), 2959–2977. https://doi.org/10.1080/1331677X.2019.1658531

- Zhang, F., & Wu, F. (2022). Financialised urban development: Chinese and (South-) East Asian observations. Land Use Policy, 112, 105813. https://doi.org/10.1016/j.landusepol.2021.105813

- Zhang, L., Chen, Y., & He, Z. (2018). The effect of investment tax incentives: Evidence from China’s value-added tax reform. International Tax and Public Finance, 25(4), 913–945. https://doi.org/10.1007/s10797-017-9475-y

- Shijing, Z., & Wenliang, G. (2022). Research on the Effect of Tax and Fee Reduction Policies on the Confidence of Real Enterprises–Based on the perspective of corporate cash decision-making behavior. Macroeconomic Research, 7, 53–64. https://kns.cnki.net/kcms/detail/detail.aspx?dbcode=CJFD&dbname=CJFDLAST2022&filename=JJGA202207003&uniplatform=NZKPT&v=JQnDAoaEiRa7pptgF8GIbuGIHXqPgf96Ftkt8Kw-l7ZJxTsOzKUn1fceBQ764DqY