?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

We investigate the influence of environmental subsidies on enterprise environmental performance based on 257 heavily polluting A-share listed companies in Shanghai and Shenzhen stock exchange from 2010 to 2017. We also discuss the mechanism of how these environmental subsidies influence enterprise environmental performance further. The study employs OLS and PSM methods to evaluate the association between environmental subsidies and enterprise environmental performance. The study finds that environmental subsidies have a positive incentive effect on the environmental performance of heavily polluting enterprises. Its positive incentive effect mainly contributes through three channels: promoting green technology innovation, increasing government environmental supervision and enhancing executives’ environmental awareness. Further research shows that environmental subsidies significantly promote environmental performance in non-state-owned enterprises, with a high degree of financing constraints and high levels of risk-taking. This study contributes to prior works by revealing the black box of the government’s macro policies affecting enterprise micro behaviour and exploring how environmental subsidies influence firm-specific behaviours.

1. Introduction

In just over 40 years since the start of reform and opening up, China has made remarkable progress in economic growth. This rapid development of China’s economy is largely attributed to various industrial policies launched by the government (Han & Hong, Citation2014). With China’s economic development into a ‘new normal’, the traditional extensive economic growth pattern of the accumulated contradictions has been increasingly prominent. Problems such as excessive consumption of resources and ecological destruction gradually become the bottleneck of economic development, making it pay a heavy price in terms of resources and the environment (Su, Yuan, Tao, et al., Citation2022). However, the ‘Jinshan silver’, ‘green mountains and clear waters’ gradually disappear. According to Yale University’s global Environmental Performance rankings, China ranked 94th out of 133 countries in the 2006 Environmental Performance Index and 128th in air quality (sixth from the bottom worldwide). China’s environmental performance index ranked 120th out of 180 countries in 2018, and the air quality index ranked 177th (4th from the bottom worldwide). These data show that China’s environmental quality is still far behind the world’s, in stark contrast to its current position as the world’s second-largest economy. Coordinating the conflict between environmental protection and economic growth has become the most critical challenge faced by the government in environmental governance. As an important source of environmental pollution, industrial enterprises, especially heavily polluting ones, pose a major threat to the living environment of human beings (Walls et al., Citation2012; Tao et al., Citation2022). Therefore, effectively controlling the environmental pollution of heavily polluting enterprises and improving environmental quality and their performance will contribute to the sustained (Xu et al., Citation2022), healthy development of China’s national economy.

As an important government macro control, environmental protection subsidy policy reflects a country’s or region’s industrial policy in a certain period. To correct market failure, governments of various countries generally use industrial policies to transform and upgrade related industries, especially the environmental protection industry. The governments of various countries adopt the environmental protection subsidy policy to optimise the industrial structure mainly because the ecological environment is characteristic of public goods, which leads to excessive consumption and environmental protection market failure. It is difficult to effectively solve the environmental pollution problem with market-based behaviour using carbon markets and carbon bonds. Therefore, the government contributes to resource allocation (Qin, Wu, et al., Citation2022). Implementing the environmental protection subsidy policy helps enterprises reduce environmental governance costs and compensates for the loss of profit caused by the positive externalities of environmental governance activities. As the new structural economics emphasises, economic development requires efficient markets and an effective government (Su, Yuan, Umar, et al., Citation2022). Therefore, implementing the environmental protection subsidy policy is the main form of government intervention. Whether the environmental protection subsidy policy can achieve the win-win goal of reducing pollution and increasing efficiency has become the criterion to measure the success of the environmental protection industrial policy worldwide. The key to the effectiveness of environmental protection policies lies in whether the design intention of the government’s macro policies can be effectively implemented at the micro-enterprise level. As China’s economic development enters the new normal, ecological and environmental problems become increasingly prominent and gradually become the bottleneck for China’s economic development. In the economic development framework, China’s framework for economic development is prominent. To alleviate the dual pressure of ‘pollution reduction’ and ‘efficiency increase’, the government has invested in a large number of environmental subsidies to promote environmental governance in heavily polluting industries. These subsidies have attracted much attention. Environmental protection subsidies improve the environmental performance of heavily polluting enterprises. If so, what are the possible channels of action?

However, different kinds of enterprises with different characteristics have dissimilar resource endowments and risk bearing levels due to different property rights. Therefore, environmental protection subsidies have dissimilar incentive effects on the environmental performance of different enterprises. In addition, environmental protection subsidies are usually dominated by industrial policies and independent of the aided units. In contrast, the heterogeneity of enterprises is endogenous and embedded in the organizational structure and corporate culture. Thus, coordination of the enterprises’ heterogeneity and policy resources can effectively implement targeted adjustment and take appropriate measures if the related environmental subsidy policy is based on different enterprise characteristics to differentiate environmental subsidies. This will significantly improve the environmental performance and production efficiency of environmental subsidies.

In recent years, research on the economic consequences of environmental subsidy policies has shifted from the macro and industry level to the micro firm level. It has yielded fruitful results, focusing mainly on the following.

The first is the influence of environmental subsidies on firm investment. Academic studies on the relationship between environmental subsidies and firms’ investment decisions have the following competing views: first, environmental subsidies enhance firms’ investment efficiency (Aghion et al., Citation2015; Bu et al., Citation2019; Xie et al., Citation2022); second, environmental subsidies harm firms’ investment efficiency (Chen et al., Citation2013).

The second is the effect of environmental subsidies on enterprise financing. Existing studies show that implementing environmental protection subsidy policies positively and negatively influence enterprise financing. However, some scholars believe that environmental protection subsidies positively affect enterprise financing (Chen et al., Citation2017; Yang et al., Citation2020). Conversely, some scholars believe environmental protection subsidies negatively affect enterprise financing (Huang et al., Citation2022).

The third is the influence of environmental subsidies on firm innovation. The discussion on the effect of environmental subsidies’ incentives on corporate innovation has been controversial and has three main views: (i) the promotion effect, focusing on technological innovation and new energy development (Hojnik & Ruzzier, Citation2016; Huang & Chen, Citation2022; Yuan et al., Citation2022; (ii) the suppression effect, specifically showing that environmental subsidies have a more limited effect on corporate innovation or even inhibit or hinder innovation (Blazenko & Yeung, Citation2015); (iii) uncertainty (Desmarchelier et al., Citation2013; Hsu et al., Citation2014; Liao, Citation2018). In addition, some scholars have argued that environmental subsidies influence firms’ investment in environmental governance (Wang et al., Citation2012).

The above literature review shows that the existing literature examines the impact of government environmental subsidies on enterprise investment, financing and innovation. However, these studies do not discuss the impact of environmental subsidies on the ecological environment. Wang et al. (Citation2012) studied the impact of environmental subsidies on corporate environmental governance investment. These are indirect factors in terms of their influence. However, minimal literature has focused on corporate environmental performance, a factor more directly related to ecological quality. Therefore, they have not explored the role of environmental subsidies on corporate environmental performance, providing a research opportunity.

Our primary contributions can be summarised as follows. First, based on the environmental performance of micro-enterprises, we provide direct evidence for the implementation effect of environmental protection subsidies at the micro level and expand on the effectiveness of these subsidies. Second, this study explores the mechanism of the impact of environmental subsidies on enterprise environmental performance. The existing literature focuses on the relationship between environmental subsidies and enterprise investment and financing decisions and the relationship between environmental subsidies and innovation. Based on the relationship between government environmental subsidies and firms’ environmental performance, this study analyses the mechanism of environmental subsidies affecting environmental performance from three aspects: government environmental supervision, enterprise green technology innovation and senior executives’ environmental awareness (Chen, Xiao, et al., Citation2022). Thus, we investigate the deep-rooted causes of the consequences of the environmental protection subsidy policy, which provides a reference for the government’s targeted regulation and precise policy implementation.

This study examines the mechanism of environmental subsidies and their impact on enterprise environmental performance. It finds that environmental subsidies positively incentivise the environmental performance of heavily polluting enterprises. This effect works through three channels: promoting green technology innovation, increasing government environmental supervision and enhancing executives’ environmental awareness. Moreover, the impact of environmental subsidies on environmental performance is more obvious in non-state-owned enterprises with high financing constraints and risk-taking levels. Based on the environmental benefits of micro-enterprises, this study provides direct evidence for the implementation effect of environmental subsidies at the micro level. Therefore, it provides a reference for the government to improve the specific implementation path of environmental subsidies. Moreover, it also provides a reference for the government to implement directional regulations and accurate policies according to the particularity of enterprises with different characteristics. ()

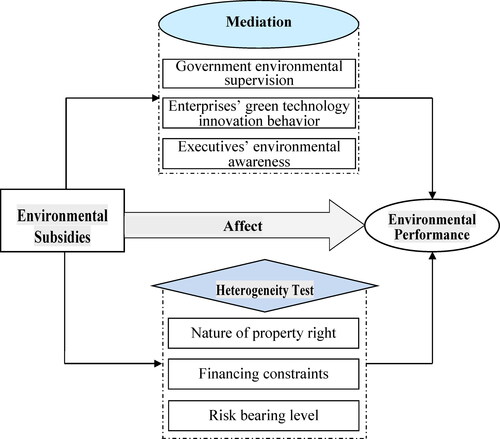

Figure 1. Concept framework.

Source: Author’s drawing.

The concept framework of this study is shown in .

2. Theoretical analysis and research hypothesis

According to the theory of public goods, environmental pollution has negative externalities. In contrast, environmental governance has the positive externalities of private costs being greater than social costs and private benefits being less than social benefits, leading to less enthusiasm for environmental governance. In addition, environmental governance has the characteristics of a long cycle and high cost. Therefore, enterprises lack the enthusiasm for environmental management, leading to the failure of the environmental protection market, which urgently needs the government’s active intervention. Environmental protection subsidies are specific industrial policies to intervene in economic operations. Implementing environmental protection subsidies reduces environmental governance costs. It compensates for the loss of profits caused by the positive externalities of environmental governance activities, encouraging enterprises to carry out environmental protection technology innovation and strengthen environmental governance.

The government environmental protection subsidies promote enterprises’ environmental performance, as reflected in the incentive and pressure effects of the system. According to national environmental policies, such as ‘several provisions on strengthening the management of environmental protection subsidy funds’, ‘the environmental protection tax law of the People’s Republic of China’, and other relevant provisions, enterprises encouraged by environmental protection subsidy policies are more likely to obtain government support on the one hand and release good signals to the outside world on the other hand, which helps to boost investor confidence, reduce financing costs and encourage enterprise participation in environmental governance. It has a good system incentive effect.

As an important means of government macro-control, the environmental protection subsidy reflects the industrial policy of a country or region in a certain period. To correct the influence of market failures on the national economy, governments generally use fiscal subsidies and other policy tools to drive the transformation and upgrade related industries, especially environmental protection industries. Some scholars believe China’s energy conservation and environmental protection industry contributes to alleviating environmental externalities. The capital-intensive environmental protection industry needs government subsidies because of its high risk, high level of uncertainty, and the need for sustained capital investment as support during the emerging period of innovation (Zhang et al., Citation2017; Xu et al., 2021b). Some studies believe that environmental subsidies promote environmental management innovation but do not affect environmental technology innovation (Shi, Citation2021). Therefore, whether environmental protection subsidies can achieve effective results lies in whether the government’s macro policy design intention is effectively implemented at the micro-enterprise level. Although ecological environment governance requires several long-term resource investments, the ecological environment has the characteristics of a public product. However, private corporations have no strong motivation to participate in environmental governance; lack of resource incentives and constraints beset environmental management (Grossman & Helpman, Citation2018). According to the theory of public goods, the ecological environment is not privately owned but is a public resource. The governance of the ecological environment will occupy other productive investments used initially by enterprises, which is an extra cost. Thus, enterprises will lose the original motivation for green governance of their pollution behaviours. Many enterprises in the environmental governance ‘free ride’ phenomenon lead to environmental market failure. The environmental protection subsidy policy alleviates the lack of funds required for environmental governance, helps enterprises expand reproduction and forms economies of scale to reduce environmental governance costs and compensate for the profit loss caused by the positive externalities. However, encouraged and constrained by the environmental protection subsidy policy, heavier pollution enterprises seek to maximise their profits and show a willingness to adopt green and new energy technologies in daily production and operation, to eliminate polluting and backward production capacity. This improves the efficiency of enterprise resource allocation and achieves the double benefits of ‘reducing pollution emissions’ and ‘increasing economic efficiency’ (Hojnik al., 2019; Li et al., Citation2018; Qin, Su, et al., Citation2022).

Meanwhile, as one of the important dimensions of the formal system, the environmental protection subsidy policy focuses on coal, steel, chemical, electric power and nonferrous heavy pollution industries, emphasizing ‘green’, ‘clean’ production, which theoretically, has an important effect on enterprises’ participation in environmental governance and improvement of environmental performance: institutional pressure exists (Huang & Chen, 2022). The environmental protection subsidies have the resource compensation effect. However, an enterprise enjoying environmental protection subsidies is subject to stringent environmental supervision by government departments, mainly supervising and evaluating the direction and efficiency of special environmental protection funds (Stoever & Weche, Citation2018). Therefore, this institutional pressure on the ecological supervision of environmental subsidies restricts non-green production and environmental violations, improving enterprises’ environmental performance.

Based on the theory of signal transmission, companies that receive environmental subsidies from the government send an important signal to the world. These companies support the government as a recessive guarantee, enhancing the company’s financing gravity (Zhou & Zhao, Citation2022). They help raise funds through the capital market and boost stakeholder confidence in green enterprise development. They reduce financing costs, encourage enterprise participation in environmental governance and reduce stakeholders’ negative expectations of non-green environmental protection behaviours (Buysse & Verbeke, Citation2003). Therefore, it has a positive influence on reducing the financing difficulties of enterprises, increasing investments in green technology innovation and improving environmental governance efficiency. The environmental management of enterprises with heavy environmental pollution is characterised by large investments in special equipment, long investment cycle span, high risk and slow effect (Rabeloo & de Azevedo Meloa, Citation2019), which cannot be separated from the support of sufficient cash flow. Moreover, enterprises that receive government environmental protection subsidies send a favourable signal to external stakeholders. The implicit government guarantee behind the enterprises facilitates raising funds from the bond and stock markets. An enterprise’s active participation in green environmental governance signals its legitimate operation to the outside world. This promotes the good image of fulfilling social responsibilities. It provides psychological guarantees for investors to make decisions, raises good expectations, reduces financing costs and provides financial security to improve environmental performance (Martin & Moser, Citation2016). The government supports heavily polluting enterprises participating in environmental governance through measures such as environmental protection subsidies, helping them expand reproduction and reduce the uncertainty and irreversibility of their environmental governance investment. Then, they promote the adoption of green environmental protection equipment and technologies (Hamamoto, Citation2006), improving environmental performance. Based on the above incentive and pressure effects, the environmental subsidy policy encourages enterprises to improve environmental performance. Therefore, the following assumptions are proposed as follows:

Hypothesis 1: Government environmental protection subsidies positively influence the improvement of the environmental performance of heavily polluting enterprises.

First, according to the technological innovation theory, green technological innovation can improve resource utilisation efficiency, reduce energy consumption per unit product and eliminate the backward polluting capacity to promote enterprises realise green production (Chen, Zhu, et al., Citation2022). However, technological innovation is highly risky and uncertain and needs sustained capital investments as support. Moreover, financing difficulties and lack of motivation have always troubled enterprises’ green technology innovation (Hsu et al., 2014; Su, Pang, et al., Citation2022). However, environmental protection subsidies provide financial support for enterprises’ green technology innovation. They reduce the financing constraints, the high risk and uncertainty of innovation activities (Stiglitz, Citation2015), and green innovation costs, encouraging enterprises to carry out green innovation. Shapiro and Walker (Citation2018) also showed that green environmental protection subsidies promote enterprises’ green technology innovation.

Second, based on the externality theory, once innovation appears, the owner usually is unable to or struggles to exclude others from using green technology innovation or cannot fully control its spread. Therefore, in innovation, the private income is less than the social benefits of the enterprise, showing the spillover effects of green technology innovation (Fiorillo et al., Citation2022). Government environmental protection subsidies can effectively overcome the cost-benefit asymmetry caused by the spillover effect of green technology innovation. This improves their enthusiasm for green technology innovation and alleviates the problem of insufficient investment. More importantly, enterprises use innovative green technologies and intelligent equipment in production (Su, Chen, et al., Citation2022). On the one hand, it is conducive to accelerating the greening of the enterprise’s production process, reducing the dependence on the original production methods that damage the environment, reducing environmental supervision costs and improving environmental performance (Shapiro & Walker, 2018; Pirtea et al., 2021). On the other hand, through the green technology innovation chain, enterprises produce differentiated products to create new market demand and enhance green competitiveness, maintaining existing markets and expanding new markets (Huang & Chen, 2022). Therefore, environmental protection subsidies stimulate enterprise investments in green technology innovation because they can relieve resource constraints.

Moreover, these subsidies may encourage heavily polluting enterprises to invest in green technology innovations because their capability to carry out green technology innovation depends on whether the threshold conditions of innovation are met, especially with continuous cash flow support. Therefore, environmental protection subsidies help an enterprise cross the threshold conditions and reduce the uncertainty and irreversibility of its green technology innovation. Thus, enterprises can make green technology innovation decisions (Hamamoto, 2006). Furthermore, green technology innovation helps enterprises eliminate polluting and backward production capacity and improve production efficiency and environmental performance (Porter & Linde, Citation1995; Hu et al., Citation2020). Based on the above analysis, the following assumptions are proposed as follows:

Hypothesis 2: Environmental protection subsidies can encourage enterprises to innovate in green technology, thus helping improve their environmental performance.

As a special government subsidy, the environmental protection subsidy funds should comply with the ‘Provisions on Strengthening the Management of Environmental Protection Subsidy Funds’. According to this regulation, environmental protection subsidies should be used exclusively for ‘comprehensive environmental treatment, key pollution source treatment’ and special funds. Therefore, enterprises enjoying the special environmental protection subsidy funds become the government’s key supervision targets. The government mainly supervises the use, direction and efficiency of special environmental protection funds. Therefore, the government’s supervision restricts enterprises’ non-green production and illegal environmental behaviours to improve environmental performance.

With increasingly severe resource and environmental constraints, promoting green production and improving the environmental performance of enterprises are imperative. As the core content of the environmental protection system, the effectiveness of environmental law enforcement supervision is directly related to environmental protection policies. It is an important factor that determines the production and emission behaviour of individual enterprises and even the environmental quality of the whole region. Environmental protection law enforcement and supervision is the main driving force leading the change in green technology choice of enterprises (Wang et al., Citation2018). Zhang (Citation2022) showed that strengthening the environmental protection law enforcement improves access to polluting, energy-intensive industries and survival threshold, encouraging enterprises to carry out green technology innovation and application. Thus, it enhances enterprise energy conservation, emission reduction and green production and realises the ‘win-win’ and environmental performance. Recent studies also show that stringent administrative regulation is the primary driver for companies to reduce pollution emissions (Shapiro & Walker, 2018). Therefore, the government should regulate enterprises that obtain financial subsidies based on the stakeholders proposed by experts and scholars represented by Freeman. In modern economic society, the government as a stakeholder is irreplaceable mainly because on the one hand, it provides financial support, tax reduction and other preferential policies for developing enterprises. On the other hand, it supervises enterprises’ micro behaviours and their environmental responsibility. Environmental protection subsidies are financial support the government provides to encourage enterprises to carry out energy conservation and emission reduction and actively participate in environmental governance. They can transfer payments unilaterally and have specific objectives and related environmental performance requirements. The government strengthens production and operation activities regulations to optimise resource allocation and increase benefits from environmental subsidies. This ensures that the limited usage of special allowance incentives can implement specific economic, environmental and social objectives and the enterprise’s primary responsibility. This will restrict the enterprise sewage production behaviour, improving corporate environmental performance. Based on the above analysis, the following assumptions are proposed as follows:

Hypothesis 3: After implementing environmental protection subsidies, the government’s environmental supervision will be strengthened, which is conducive to improving enterprises’ environmental performance.

According to the upper echelons theory, senior executives are the core predictive variables that affect an enterprise’s strategic choice and performance level (Hambrick & Mason, Citation1984; Su, Liu, et al., Citation2022). Executives make bounded rational decisions based on their background characteristics, personal psychological traits and cognitive paradigm (Hambrick & Mason, 1984). Yang et al. (Citation2012) showed that executives’ cognition of the environment determines whether enterprises actively adopt green production behaviours. The environmental awareness of senior executives is a specific manifestation of their cognition.

The guiding effect of government environmental protection support is mainly reflected in the following aspects: on the one hand, it makes enterprise executives realise that government subsidy funds can reduce environmental protection investment risks and environmental governance costs (Henriques & Sadorsky, Citation1996; Yang et al., Citation2020); On the other hand, the greater the government’s support for environmental protection, the more it encourages executives to pay attention to environmental policies and regulations, information on government support policies and the latest trends of government’s punishment or reward based on the environmental performance of peer enterprises (Suk et al., Citation2013). Senior executives obtain more information about green environmental protection to be aware of the importance of environmental issues. They positively and optimistically interpret the guiding function of the policy guidance of environmental protection subsidies on the green production behaviour of enterprises (Gholami et al., Citation2013). Therefore, implementing positive environmental strategies will likely respond to the government’s environmental protection subsidy policies to achieve environmental protection, improving enterprises’ environmental performance. In addition, subsidies for green environmental protection have increased as the government has focussed on environmental issues in recent years. This eases financing constraints and reduces the risk of green environmental protection investment, leading to a stronger willingness of enterprises to participate in green innovation and thus enhancing the environmental responsibility awareness of executives (Pirtea et al., Citation2021). However, promoting executives’ awareness of environmental responsibility will encourage enterprises to carry out green environmental protection practices, improving environmental performance. Therefore, environmental subsidies improve environmental performance by improving the environmental awareness of executives.

Hypothesis 4: Government environmental protection subsidies can enhance the environmental awareness of senior executives, thus helping improve the environmental performance of enterprises.

3. Data

According to classification, heavy pollution industries were selected for investigation. This study measured environmental performance by the ecological benefit method. According to the Environmental Protection Law of the People’s Republic of China promulgated in 2017, the environmental protection tax was officially levied on 1 January 2018, and the standard for the discharge fee changed to some extent. Therefore, the data on the discharge fee in the ecological benefit law was available up to 2017. Thus, we selected 16 listed companies of heavy pollution industries in China’s A-share market from 2010 to 2017 as the research sample.

The environmental performance data of the dependent variables were obtained from the CSMAR database and the Great Tide Information network. Amongst them, the sewage fee data used in the ecological benefit method were obtained from the manual sorting of annual and corporate social responsibility reports.

Explanatory variables include environmental protection subsidy data obtained from the amount of government subsidy in the financial statements of the company’s annual report. By searching for keywords, such as ‘energy saving’, ‘emission reduction’, ‘pollution control’, ‘environmental protection’, ‘clean’ and ‘green’, the specific environmental protection subsidy projects and the amount were determined by manual screening and sorting.

The green technology innovation data of mediation variable enterprises were obtained from the R&D investment projects in the CSMAR database. By searching keywords such as ‘environmental protection’, ‘green’, ‘energy saving and emission reduction’, ‘clean’, ‘pollution control’, ‘garbage’, ‘wastewater’, ‘waste gas’, ‘three wastes’, ‘recycling’, manual screening or sorting was performed to determine the specific green nature of related R&D investments as innovation variables of the green technology. The data on the intensity of environmental supervision was obtained from the data centre of the government website of the Ministry of Environmental Protection. The data included in the national key monitoring enterprises list were sorted out by manual search. The data on senior executives’ awareness of environmental responsibility were obtained from detailed data in Hexun’s corporate social responsibility score profile.

Control variables included environmental management system certification data from the national Certification and Accreditation Administration official website through the website certification results link under the ‘national certification and accreditation information public service platform’ manual sorting sample enterprise environmental management system certification data. In addition, data regarding other control variables were obtained from the CSMAR database. According to the above 16 categories of heavy pollution industry screening, A stock listed companies, ST and *ST companies were eliminated, and abnormal samples of financial data were removed. However, the main continuous variables were treated with 1% Winsorise on both sides to eliminate the influence of outliers. After the above treatment, 257 listed companies with heavy pollution were obtained, with 1382 observed values.

4. Definition of variables and model design

4.1. Dependent variables

In this model, the dependent variable is the environmental performance of the enterprise. However, existing literature has not yet reached a unified conclusion on measuring environmental performance indicators. Moreover, because most enterprises in China do not disclose specific pollutant emission details, obtaining the emission data at the micro level is difficult. In addition, the environmental performance indicators in the domestic literature mainly include the ecological benefit, environmental responsibility scoring and environmental reward and honour scoring methods. This section focuses on the effect of environmental subsidies on the enterprise’s environmental performance, mainly focusing on environmental policy resources to reduce pollution emissions. Therefore, the ecological emulation method is used to measure environmental performance.

This study adopts the index framework of the World Council for Sustainable Development of Enterprises. It emulates Yu et al. (Citation2020), measuring the environmental performance of enterprises using the ecological benefit method. Its estimation formula is ecological benefit = value of products or services/environmental influence; the higher the index value is, the better the environmental performance. Amongst them, the environmental effect is expressed by the pollutant discharge fee paid by the enterprise, and the business income represents the product or service values. Therefore, based on Yu et al. (2020), the ratio of logarithmic operating revenue to logarithmic sewage charge is used as the ecological benefit method, which is the environmental performance.

4.2. Core explanatory variables

The environmental protection subsidy is the explanatory variable. Environmental protection subsidy is the government’s financial support for environmental protection to encourage enterprises to carry out energy conservation and emission reduction and actively participate in green environmental governance. The amount of environmental protection subsidy is the data related to environmental protection that are sorted manually according to the keywords ‘energy saving’, ‘emission reduction’, ‘pollution control’, ‘environmental protection’, ‘green’ and ‘clean’ in the government subsidy data. As for the measurement of the environmental protection subsidy of the explanatory variable, following Jiang et al. (Citation2022), the government environmental protection subsidy is measured by the ratio of the sum of the environmental protection subsidies received by the enterprise in the current year to the operating income.

4.3. Mediating variables

Green technology innovation is measured by the ratio of a firm’s green R&D expenditure to its revenue. Green R&D expenditure mainly refers to the technical transformation expenditure, the facility investment and maintenance expenditure related to environmental protection or green. In the R&D expenditure, the green-related R&D expenditure can be obtained by selecting keywords such as ‘environmental protection’, ‘energy saving’, ‘green’, ‘emission reduction’, ‘pollution’ and ‘clean’.

For government environmental supervision, environmental supervision intensity is measured by whether heavy-polluting enterprises are included in the list of national key monitoring enterprises. If listed, it is 1; otherwise, it is 0. The categories of government environmental supervision include wastewater, waste gas, hazardous waste and heavy metals.

Corporate executive environmental awareness is measured by the corporate environmental awareness score.

4.4. Control variables

In addition to the influence of environmental protection subsidies, environmental performance is affected by the control variables of enterprise characteristics. According to Shen & Zhou (Citation2017), control variables include company size, financial leverage, capital intensity, operating cash flow, listing age, ownership concentration and environmental management system certification. The model also controls for time and industry dummy variables. Specific variables are defined in .

Table 1. The specific definitions of variables.

4.5. Model design

First, the effect of environmental subsidies on the environmental performance of enterprises is revealed. Moreover, considering environmental protection subsidies and enterprise environmental performance may cause reverse causation problems. This section constructs the regression model (1) to ease its reverse cause and effect of endogenous problems. The explanatory variable lag issue of data regression is established to verify hypothesis H1, control the industry and year effects and use a robust standard to overcome heteroscedasticity and serial correlation problems. The model is constructed as follows:

(1)

(1)

r is the dependent variable, representing environmental performance;

is the explanatory variable, representing environmental subsidy;

is a series of control variables;

and

are annual and industry dummy variables, respectively. The specific variables are defined in . In model (1),

represents the enterprise individual, and

represents the year. If the coefficient

is significantly positive, the environmental protection subsidies positively affect enterprise environmental performance. Conversely, if coefficient

is significantly negative, the environmental protection subsidies negatively impact the environmental performance.

This section uses the mediation effect test principle to test the mediation mechanism to verify whether hypotheses H2, H3 and H4 are valid. The mediation mechanism test model is as follows:

(2)

(2)

(3)

(3)

Mediation effect test principle: first, whether the regression coefficient of the independent variable versus the dependent variable in model (1) is significant is tested. Second, if the coefficient of first step is significant, the second step is to test whether the regression coefficient

between the independent variable and the mediation variable of model (2) is significant. Finally, if the coefficient of

is significant in model (2), it directly goes to the third step. Then test model (3), the mediation variable on the dependent variable regression coefficient a2 is significant, and the independent variable on the dependent variable coefficient a1 is significant. If in step 3

is significant, and

is not significant, then the full mediating effect is established. If the independent variable coefficient a1 in the second step is significant, and the coefficient

in model (3) is significant, but a1 is significantly smaller than the

coefficient in model (1), then the partial mediation effect is valid. However, if the independent variable coefficient a1 in the second step is not significant, the Sobel test should be carried out. The above mediation effect holds if the Sobel test is statistically significant.

In the above model, represents the mediation variable: enterprise’s green technology innovation, government’s environmental supervision and senior executive’s environmental awareness, as defined in .

5. Empirical results and discussion

5.1. Descriptive statistics

presents the descriptive statistics of the main variables. The mean of environmental performance is 1.501, the median value is 1.453, the minimum value is 1.062, and the maximum is 2.895, indicating that nearly half the enterprises in the sample reach the mean level of environmental performance. Moreover, differences in environmental performance among enterprises exist. The sample’s mean value of environmental protection subsidies is 0.016, indicating that the government has supported heavily polluting enterprises in environmental governance in recent years. The minimum value of environmental protection subsidy is 0.000, and the maximum is 0.184, indicating a great difference in environmental protection subsidy among enterprises. The mean value of green technology innovation is 0.018; the median is 0.013, and the minimum and maximum values are 0 and 0.546, respectively, indicating that the green technology innovation of heavily polluting enterprises is different. The green technology innovation levels of the most heavy-polluting enterprises cannot reach the average industry level (0.013 < 0.018). Therefore, China’s heavy polluting enterprises’ overall expenditure on green technology innovation is low. The mean value of government environmental supervision intensity is 0.378, and the minimum and maximum values are 0.000 and 1.000, respectively, indicating that nearly 40% of the sample firms are included in the national essential monitoring enterprises list. The mean value of executives’ environmental awareness is 1.83, the median value is 2.000, and the minimum and maximum values are 0.000 and 4.000, respectively, indicating that most executives of heavily polluting enterprises have a good sense of environmental responsibility.

Table 2. Descriptive statistical results.

The variables of enterprise characteristics, size, growth, asset-liability ratio and other indicators are within a reasonable range, and other variables have little difference.

5.2. Basic regression analysis

shows the regression results of the influence and mechanism of environmental protection subsidies on enterprises’ environmental performance. Column (1) in shows that the effective coefficient of environmental protection subsidies on the environmental performance of enterprises is 0.048, significantly positive at the 1% level. A significant positive correlation is observed between environmental protection subsidies and environmental performance; environmental protection subsidies promote environmental performance. Hypothesis H1 is verified.

Table 3. The impact and mechanism of environmental subsidy on environmental performance.

Columns (1)–(3) in test the mediating role of green technology innovation in the relationship between environmental protection subsidies and environmental performance of enterprises. First, the effect of environmental subsidies on green technology innovation is investigated. Column (2) shows that the coefficient of environmental subsidies is significantly positive at the 1% level, indicating that the environmental subsidies promote green technology innovation. Second, the effect of green technology innovation on the environmental performance of enterprises is tested. Column (3) shows that the green technology innovation coefficients are all significantly positive at the 1% level, indicating that green technology innovation improves environmental performance. Third, by testing the change of the influence coefficient of environmental protection subsidies on environmental performance, the environmental protection subsidy coefficients in Column (1) are also significantly positive at the 1% level, indicating that the environmental protection subsidy significantly promotes environmental performance. The environmental protection subsidy coefficient in Column (3) is 0.031, smaller than that in Column (1), which is 0.048. Based on the above results, green technology innovation partially mediates the relationship between environmental protection subsidies and enterprise environmental performance. Hypothesis H2 is established.

In , Columns (1), (4) and (5) show the results of the mediation mechanism of government environmental regulations. In Column (4), the environmental subsidies coefficient is significantly positive under the 5% level, indicating that the subsidy strengthens the intensity of government environmental supervision. In Column (5), the intensity coefficient of government environmental regulation is significantly positive at the 5% level, indicating that the intensity of government environmental regulation improves environmental performance. The environmental protection subsidy coefficient in Column (5) is 0.027, significantly positive at the 1% level and smaller than the environmental protection subsidy coefficient (0.048) in Column (1). This indicates that government environmental regulation plays a significant and partial mediation role in the relationship between environmental protection subsidies and the environmental performance of enterprises. Hypothesis H3 is established.

In , Columns (1), (6) and (7) present the results of the mediation mechanism of executives’ environmental awareness. The coefficient of the environmental protection subsidy in Column (6) is significantly positive at the 1% level, indicating that the subsidy enhances the environmental protection awareness of senior executives. The coefficient of environmental protection awareness in Column (7) is significantly positive at the 5% level, indicating that the environmental protection awareness of senior executives promotes the environmental performance of enterprises. In addition, the coefficient of environmental protection subsidy in Column (7) is 0.033, smaller than that in Column (1), which is 0.048. The above results indicate that the environmental awareness of senior executives plays a significant partially mediating role in environmental protection subsidies promoting the environmental performance of enterprises.

In addition, the control variables in the model show that firm size and environmental performance are significantly negative. This indicates that the environmental performance does not improve with a larger firm size, possibly because the larger the firm size, the lower the environmental governance efficiency and the lower the environmental performance. A significant negative correlation is observed between operating cash flow and environmental performance, indicating that operating cash flow negatively affects environmental performance. The busier enterprises are with production and operation activities, the more likely they are to neglect environmental governance. Companies listed for a long time also have good environmental performance. Capital intensity is negatively correlated with environmental performance.

5.3. Robustness test

5.3.1. Propensity score matching PSM

Given the environmental subsidies and enterprise environmental performance among endogenous problems may be heavier, they need to be verified further through various robustness tests. Therefore, the PSM method is used for the robustness test. Suppose the OLS method or the firm’s fixed effects model is used for identification. Then, selectivity and mixed bias may occur because whether an enterprise receives environmental protection subsidies from the government may be non-random. The government may consider enterprises’ environmental governance capabilities when providing subsidies. However, government subsidies and enterprises’ environmental performance may also be influenced by other factors (such as enterprise size). The optimal identification method is used to compare the differences between the environmental performance of a heavily polluting enterprise that receives subsidies under the condition of ‘subsidy’ and ‘non-subsidy’ exclude the influence of other characteristics and then reveal the actual effect of government environmental protection subsidies on the environmental performance. The PSM method proposed by Heckman et al. (Citation1997) is an effective tool for estimating the relationship between environmental protection subsidies and the environmental performance of enterprises. First, data matching and the balance test are carried out. Then, the model is re-regressed with the matching samples.

First, matching variables are selected, and data matching is performed. The matching covariate is all the control variables in the previous model, including company size, profitability, growth, financial leverage, operating cash flow, equity structure, capital intensity, company age and ISO certification variables.

The Logit method is used to estimate the binary variables and calculate the propensity score of each enterprise. The calculation process is as follows:

(4)

(4)

where the binary dummy variable

when Dsub is 1, it means that the government environmental protection subsidy is enjoyed; when Dsub is 0, it means that the government environmental protection subsidy is not enjoyed, and

is the matching variable. The above scores reflect the probability of an enterprise enjoying government environmental protection subsidies. The probability value obtained by estimating the above equation is the probability predicted value of the treatment and control groups. ‘A pair of four is put back to neighbour matching’, and the balance test is carried out. It is expressed as follows:

(5)

(5)

represents the matching set from the control group enterprise corresponding to the processing group enterprise.

Second, shows the results of the test of balance. Before matching sample regression, the balance test is performed, and the results are shown in . The balance test shows that the standard deviation of relevant control variables after matching is less than 10%. Furthermore, the t-test results of control variables accept the null hypothesis that no significant difference exists between the treatment and the control groups. This indicates that the characteristic differences between enterprises receiving environmental protection subsidies and those without subsidies have been largely eliminated.

Table 4. Test of balance.

Finally, based on the samples from PSM, this study re-regressed models (1)–(3) to test the effect and mechanism of environmental protection subsidies on enterprises’ environmental performance (results shown in )

Table 5. The regression tests after propensity score matching.

The explanatory variable investigates the data with a one-period lag in model regression to alleviate the endogeneity problem caused by the reverse causality between environmental protection subsidies and enterprises’ environmental performance. Column (1) shows that the environmental subsidies coefficient is positive and significant under the 1% level. The regression results also verify that environmental subsidies help improve corporate environmental performance. Therefore, assuming H1 is proven, this result indicates that the previous conclusion is still robust. In Columns (1)–(3), the mediation mechanism of test results verified that green technology innovation in environmental subsidies and enterprise environmental performance relationship plays a significant mediation role. Columns (1), (4) and (5) shows that the government regulation plays a significant mediating role in the process of environmental protection subsidies improving the environmental performance.

Furthermore, Columns (1), (6) and (7) show that the environmental awareness of senior executives plays a significant mediating role in the positive correlation between environmental subsidies and environmental performance. In conclusion, further verifies H1, H2, H3 and H4.

5.3.2. Variable substitution

In order to test the robustness of the above conclusions, we refer to Lu et al. (Citation2017), measuring the environmental performance of enterprises using the environmental responsibility score (envir_sc). The results are shown in .

Table 6. Environmental performance indicators replacement.

Column (1) of show that the environmental subsidies coefficient is significantly positive at the 1% level, indicating that the environmental subsidies improve environmental performance, further verifying the previous conclusion is robust. The results of column (1), column (2) and column (3) show that green technology innovation plays a significant and partial mediation role in the relationship between environmental subsidies and corporate environmental performance. Similarly, the results of Column (1), Column (4) and Column (5) indicate that environmental regulation plays a significant and partial mediation role in the relationship between environmental subsidies and corporate environmental performance. The results of column (1), column (6) and column (7) indicate that senior executives’ environmental awareness plays a significant and partial mediation role in the relationship between environmental subsidies and corporate environmental performance. In conclusion, further verifies H1, H2, H3 and H4, showing that the previous findings are robust.

5.4. Further analysis: enterprise heterogeneity test

This study analyses the impact of environmental protection subsidies on enterprises’ environmental performance. It discusses the mechanism of environmental protection subsidies on firms’ environmental performance from three aspects: government environmental supervision, enterprises’ green technology innovation behaviour and executives’ environmental awareness. It is found that environmental protection subsidies positively affect the environmental performance of enterprises. The main reason is that environmental protection subsidies increase the environmental supervision of the government, stimulate the green technology innovation behaviour of enterprises, and strengthen the environmental awareness of executives, to significantly improve environmental performance. However, there is a big gap between the environmental protection subsidies obtained by enterprises under different property rights, and the efficiency of environmental protection subsidies is also very different. Moreover, enterprises with different financing constraints have different use values of environmental protection subsidies, and their impacts on environmental performance are also different. In addition, enterprises with risk levels have different willingness to invest in green technology innovation or environmental governance, and their impact on environmental performance is also different. Therefore, it is necessary to continue exploring the effects of different property rights, financing constraints, and levels of risk-taking on the relationship between environmental subsidies and environmental performance.

First, we test the impact of property heterogeneity on the relationship between environmental protection subsidies and environmental performance of enterprises. Column (1) in is the group of state-owned enterprises, and Column (2) represents non-state-owned enterprises. The environmental protection subsidy coefficient of Column (1) is significantly positive at the 10% level. The environmental protection subsidy coefficient of Column (2) is significantly positive at the 1% level. In addition, the results of the inter-group coefficient comparison show a significant difference between them. The promotion effect of environmental subsidies on environmental performance is more evident in non-state-owned enterprises than in state-owned.

Table 7. Analysis of heterogeneity.

Second, the heterogeneity of financing constraints tests the relationship between environmental subsidies and corporate environmental performance. As for the measurement of financing constraints, Hadlock and Pierce (2010) show that the sensitivity analyses (SA) index method can comprehensively reflect the degree of corporate financing constraints. Referencing Hadlock and Pierce (Citation2010), a financing constraint SA index is built to measure the financing constraint indicators. The formula is as follows:

(6)

(6)

The greater the absolute value of the lower the degree of corporate financing constraints; When testing the heterogeneity of financing constraints, they are grouped according to the median of the

index. When they are greater than or equal to the median, they are defined as low financing constraint groups, and when they are less than the median, they are defined as high financing constraint groups. Columns (3) and (4) of show the test results. In the high financing constraint group in Column (3), the regression coefficient of environmental subsidies on the environmental performance of enterprises is 0.084, significantly positive at the 1% level. However, in the low financing constraint group in Column (4), the regression coefficient of environmental protection subsidies on the environmental performance of enterprises is 0.023, which does not pass the significance test. The above results show that the promotion effect of environmental subsidies on the environmental performance of enterprises with low financing constraints is less significant than those with high financing constraints. In addition, the coefficient between the two groups showed significant differences. The above results show that environmental protection subsidies have a stronger promoting effect on the environmental performance of enterprises with high financing constraints. This indicates that government environmental protection subsidies have a better environmental governance effect on enterprises with high financing constraints.

Third, we test the impact of heterogeneity of risk-bearing level on the relationship between environmental protection subsidies and environmental performance of enterprises. This study uses the earnings volatility index() to measure the risk-bearing level. It estimates it by the three-year standard deviation of industry-adjusted return on assets of listed companies in the observation period. The specific calculation formula is as follows:

(7)

(7)

(8)

(8)

where

is the enterprise,

is 1–3, which represents the year of the observation period,

represents the total number of enterprises in the industry, and

is the KTH enterprise in an industry.

is the profit before interest and tax of the corresponding year,

is the total

at the end of the year, and the higher the

value, the higher the risk-bearing level. In the heterogeneity test of risk-bearing level, groups were also grouped according to the median. Those greater than or equal to the median were classified as the high-risk level group. However, those less than the median were classified as a low-risk level group. The test results are shown in Columns (5) and (6) of . Column (5) represents the group with a high-risk-bearing level; its environmental subsidy coefficient is 0.093, significantly positive at the 1% level. Column (6) represents the group with a low risk-bearing level, its environmental protection subsidy coefficient is 0.052, significantly positive at the 10% level, and the coefficient comparison between the two groups shows that there is a significant difference. Therefore, the above results indicate that the environmental protection subsidies of enterprises with high-risk levels have a more significant promotion effect on environmental performance than those with low-risk levels.

6. Conclusions and implications

This study takes 257 heavily polluted listed companies in Shenzhen and Shanghai Stock Exchanges in China from 2010 to 2017 as the research object. It empirically tests whether environmental subsidies affect enterprise environmental performance and the mechanism of environmental subsidies affecting enterprise environmental performance. The main conclusions are as follows: government environmental subsidies have a significant positive role in promoting enterprise environmental performance; the analysis of the mediation mechanism shows that environmental subsidies can improve the environmental performance of enterprises through three channels, namely, encouraging enterprises to carry out green technology innovation, strengthening government environmental supervision and enhancing enterprises’ environmental awareness.

The above analysis of the mediation mechanism helps understand the objective performance and deep-rooted reasons for the impact of government environmental protection subsidies on enterprises’ environmental performance. This provides supporting evidence for the micro effects of government environmental protection subsidies. In addition, further analysis shows significant differences in the incentive effects of environmental protection subsidies on the environmental performance of enterprises with different characteristics. Therefore, to improve the impact of macroeconomic policies, it is necessary to implement targeted regulations and policies, which provide direct evidence for the government to enhance the dynamic adjustment mechanism of environmental protection subsidy policies.

The findings of this study have some important policy implications. First, to give full play to the signalling function of government environmental protection subsidies and actively guide and cultivate corporate executives’ awareness of environmental responsibility. The government should strengthen the environmental protection subsidy policies for heavy-polluting enterprises, form institutional arrangements, give full play to the signal transmission function of environmental protection subsidy, disseminating policy-related economic and financial information (Xu, Yang, et al., Citation2021), and actively guide and cultivate the sense of environmental responsibility of corporate executives to improve the environmental governance efficiency of enterprises.

Second, policy support for enterprises’ green technology innovation activities should be increased. The government should increase the policy support for green technology innovation activities and effectively promote the green innovation transformation of heavily polluting enterprises rather than be limited to direct environmental protection investment to achieve the dual benefits of ‘emission reduction’ and ‘efficiency increase’. Environmental protection subsidies incentivise enterprises’ green technology innovation. These enterprises can enhance their competitive advantage through green technology innovation to reflect the long-term effect of environmental governance.

Third, the environmental information supervision platform must be built to improve the environmental information disclosure mechanism. Presently, the environmental awareness of senior executives in Chinese enterprises is generally not strong. Therefore, the government’s incentives and guidance should be strengthened. In addition, the environmental information supervision platform should be constructed, the environmental information disclosure mechanism should be further improved, the supervision and reward and punishment systems should be improved, and the media and the masses should accept the supervision under the ‘sunshine supervision’. Therefore, the government should build a scientific, transparent information management platform for environmental protection subsidies, including two sub-information systems: first, integrate environmental protection information, environmental performance and other information into the basic information system. Second, include green technology innovation input information, ‘blocklist’ performance of production responsibilities and other information in the credit information system to serve as the reference basis for heavy pollution enterprises to obtain environmental protection subsidies.

Finally, different environmental protection policies should be introduced according to the other characteristics of enterprises. For example, the efficiency of environmental protection subsidies in non-state-owned enterprises is higher than that in state-owned. The use efficiency of environmental protection subsidies in enterprises with strong financing constraints is higher than in those with low financing constraints. The use efficiency of environmental protection subsidies in enterprises with high-risk bearing is higher than that in enterprises with a low-risk approach. Therefore, the government should fully consider the heterogeneity and implement different subsidy policies for enterprises with different characteristics when issuing environmental protection subsidy policies. If the government’s macro-environmental protection subsidy policy adopts, the ‘one size fits all’ incentive mode, the implementation effect of the subsidy policy is not ideal. There may even be resistance against the design intention of the policy, which may lead to huge policy waste and delay the government’s timely regulation. Therefore, implementing macro regulation and control is necessary to improve the effectiveness of the macro-environmental protection subsidy policy. Furthermore, when stimulating enterprises, the heterogeneous characteristics should be considered, different for enterprises with different characteristics to improve the precision of policies.

The limitations and future prospects of this study are as follows. As for the selection of sample time, due to the continuous data generation limitation, this study only selects the heavily polluted enterprise samples from 2010 to 2017. It does not test the various research hypotheses proposed with the latest data. The sample started in 2010 because Hexun disclosed the environmental responsibility rating data in 2010. Although other networks have also disclosed the data for the first two years of 2010, the available data is small. In addition, the reason why the deadline was not the latest year in 2019 is that the environmental protection tax in 2018 replaced the collection of pollution charges. To avoid the inconsistency of data sources due to the differences in the collection calibre between the two collection systems, the deadline for the samples selected in this study is 2017. In future research, the effect of environmental protection tax policies after 2018 on corporate environmental performance can be considered. Other environmental protection industry policy tools can be supplemented and expanded to examine the effect of environmental protection industry policy tools more comprehensively on environmental performance. In addition, this study defines enterprise environmental performance from the perspective of economic resources, like most other scholars. However, due to the difficulty in obtaining pollution emission data, few studies have measured enterprise environmental performance through pollution emission indicators. In future research, we can consider using pollution emission indicators to define enterprise environmental performance.

Authors’ contributions

All the authors have contributed equally.

Disclosure statement

No conflict of interest exits in the submission of this manuscript.

Additional information

Funding

References

- Aghion, P., Cai, J., Dewatripont, M., Du, L., Harrison, A., & Legros, P. (2015). Industrial policy and competition. American Economic Journal: Macroeconomics, 7(4), 1–32. https://doi.org/10.1257/mac.20120103

- Blazenko, G., & Yeung, W. H. (2015). Does R&D create or resolve uncertainty? The Journal of Risk Finance, 16(5), 536–553. https://doi.org/10.1108/JRF-01-2015-0004

- Bu, D., Zhang, C., & Wang, X. (2019). Grant priming and allocation efficiency. Accounting Research, 7, 68–74. https://doi.org/10.3969/j.issn.1003-2886.2019.07.009

- Buysse, K., & Verbeke, A. (2003). Proactive environmental strategies: A stakeholder management perspective. Strategic Management Journal, 24, 453–470. https://doi.org/10.1002/smj.299

- Chen, D., Khan, S., Yu, X., & Zhou, Z. (2013). Government intervention and investment comovement: Chinese evidence. Journal of Business Finance & Accounting, 40(3–4), 564–587. https://doi.org/10.1111/jbfa.12022

- Chen, W., Zhu, Y. F., He, Z. H., & Yang, Y. (2022). The effect of local government debt on green innovation: Evidence from Chinese listed companies. Pacific-Basin Finance Journal, 73, 101760. https://doi.org/10.1016/j.pacfin.2022.101760

- Chen, Z., Poncet, S., & Xiong, R. (2017). Inter-industry relatedness and industrial-policy efficiency: Evidence from China’s export processing zones. Journal of Comparative Economics, 45(4), 809–826. https://doi.org/10.1016/j.jce.2016.01.003

- Chen, Z., Xiao, Y., & Jiang, K. (2022). Corporate green innovation and stock liquidity in China. Accounting & Finance, https://doi.org/10.1111/acfi.13027

- Desmarchelier, B., Djellal, F., & Gallouj, F. (2013). Environmental policies and eco-innovations by service firms: An agent-based model. Technological Forecasting and Social Change, 80, 1395–1408. https://doi.org/10.1016/j.techfore.2012.11.005

- Fiorillo, P., Meles, A., Mustilli, M., & Salerno, D. (2022). How does the financial market influence firms’ green innovation? The role of equity analysts. Journal of International Financial Management & Accounting, 33(3), 428–458. https://doi.org/10.1111/jifm.12152

- Gholami, R., Sulaiman, A. B., Ramayah, T., & Molla, A. (2013). Senior managers’ perception on green information systems (IS) adoption and environmental performance: Results from a field survey. Information and Management, 50, 431–438. https://doi.org/10.1016/j.im.2013.01.004

- Grossman, G. M., & Helpman, E. (2018). Growth, trade, and inequality. Econometrica, 86(1), 37–83. https://doi.org/10.3982/ECTA14518

- Hadlock, C. J., & Pierce, J. R. (2010). New evidence on measuring financial constraints: Moving beyond the KZ index. Review of Financial Studies, 23, 1909–1940. https://doi.org/10.1093/rfs/hhq009

- Hamamoto, M. (2006). Environmental regulation and the productivity of Japanese manufacturing industries. Resource and Energy Economics, 28(4), 299–312. https://doi.org/10.1016/j.reseneeco.2005.11.001

- Hambrick, D. C., & Mason, P. A. (1984). Upper echelons: Organization as a reflection of its managers. The Academy of Management Review, 9(2), 193–206. https://doi.org/10.5465/amr.1984.4277628

- Han, G., & Hong, Y. (2014). National industrial policy, asset price and investor behavior. Economic Research Journal, 49, 143–158. https://doi.org/cnki:sunjjyj.0.2014-12-012

- Heckman, J. J., Ichimura, H., & Todd P. E. (1997). Matching as an econometric evaluation estimator: Evidence from evaluating a job training programme. The Review of Economic Studies, 64, 605–654. https://doi.org/10.2307/2971733

- Henriques, I., & Sadorsky, P. (1996). The determinants of an environmentally responsive firm: An empirical approach. Journal of Environmental Economics and Management, 30, 381–395. https://doi.org/10.1006/jeem.1996.0026

- Hojnik, J., & Ruzzier, M. (2016). The driving forces of process eco-innovation and its impact on performance: Insights from Slovenia. Journal of Cleaner Production, 133, 812–825. https://doi.org/10.1016/j.jclepro.2016.06.002

- Hsu, P. H., Tian, X., & Xu, Y. (2014). Financial development and innovation: Cross-country evidence. Journal of Financial Economics, 112(1), 116–135. https://doi.org/10.1016/j.jfineco.2013.12.002

- Hu, J., Huang, N., & Shen, H. (2020). Can market incentive environmental regulation promote technological innovation: A natural experiment based on China’s carbon emission trading system. Financial Research, 1, 171. https://doi.org/cnki:sun:jryj.0.2020-01-010

- Huang, Y., & Chen, C. (2022). Exploring institutional pressures, firm green slack, green product innovation and green new product success: Evidence from Taiwan’s high-tech industries. Technological Forecasting and Social Change, 174, 121196. https://doi.org/10.1016/j.techfore.2021.121196

- Huang, Y., Zimmerman, J. L., Kothari, S. P., Lys, T. Z., & Watts, R. L. (2022). Government subsidies and corporate disclosure. Journal of Accounting and Economics, 74(1), 101480. https://doi.org/10.1016/j.jacceco.2022.101480

- Jiang, Z., Xu, C., & Zhou, J. (2022). Government environmental protection subsidies, environmental tax collection, and green innovation: Evidence from listed enterprises in China. Environmental Science and Pollution Research, 1–15. https://doi.org/10.1007/s11356-022-22538-3

- Li, J., Xia, J., & Zajac, E. J. (2018). On the duality of political and economic stakeholder influence on firm innovation performance: Theory and evidence from Chinese firms. Strategic Management Journal, 39(1), 193–216. https://doi.org/10.1002/smj.2697

- Liao, Z. (2018). Environmental policy instruments, environmental innovation and the reputation of enterprises. Journal of Cleaner Production, 171, 1111–1117. https://doi.org/10.1016/j.jclepro.2017.10.126

- Lu, H., Tang, F., & Xu, W. (2017). Can tax policy enhance corporate environmental responsibility? Evidence from Chinese listed companies. Research of Finance and Trade, 28(01), 86–91. https://doi.org/10.19337/j.cnki.34-1093/f.2017.01.009

- Martin, P. R., & Moser, D. V. (2016). Managers’ green investment disclosures and investors’ reaction. Journal of Accounting and Economics, 61(1), 239–254. https://doi.org/10.1016/j.jacceco.2015.08.004

- Pirtea, M. G., Noja, G. G., Cristea, M., & Panait, M. (2021). Interplay between environmental, social and governance coordinates and the financial performance of agricultural companies. Agricultural Economics, 67(12), 479–490. https://doi.org/10.17221/286/2021-AGRICECON

- Porter, M. E., & Linde, C. V. D. (1995). Toward a new conception of the environment competitiveness relationship. Journal of Economic Perspectives, 9(4), 97–118. https://doi.org/10.1257/jep.9.4.97

- Qin, M., Su, C. W., Zhong, Y., Song, Y., & Oana-Ramona, L. T. (2022). Sustainable finance and renewable energy: Promoters of carbon neutrality in the United States. Journal of Environmental Management, 324, 116390. https://doi.org/10.1016/j.jenvman.2022.116390

- Qin, M., Wu, T., Tao, R., Su, C. W., & Petru, S. (2022). The inevitable role of bilateral relation: A fresh insight into the bitcoin market. Economic Research-Ekonomska Istraživanja, 35(1), 4260–4279. https://doi.org/10.1080/1331677X.2021.2013269

- Rabeloo, O. d. S., & de Azevedo Meloa, A. S. S.. (2019). Drivers of multidimensional eco-innovation: Empirical evidence from the Brazilian industry. Environmental Technology, 40, 2556. https://doi.org/10.1080/09593330.2018.1447022

- Shapiro, J. S., & Walker, R. (2018). Why is pollution from US manufacturing declining? The roles of environmental regulation, productivity, and trade. American Economic Review, 108, 3814–3815. https://doi.org/10.1257/aer.20151272

- Shen, H., & Zhou, Y. (2017). Environmental law enforcement supervision and firm environmental performance: Evidence from quasi-natural experiments. Nankai Management Review, 20, 73–82. https://doi.org/10.3969/j.issn.1008-3448.2017.06.008

- Shi, J. (2021). Do government R&D subsidies improve the quality of corporate innovation? Empirical evidence from Chinese listed companies. Enterprise Economics, 40, 100–108. https://doi.org/10.13529/j.cnki.enterprise.economy.2021.11.011

- Stiglitz, J. E. (2015). Leaders and followers: Perspectives on the Nordic model and the economics of innovation. Journal of Public Economics, 127, 3–16. https://doi.org/10.1016/j.jpubeco.2014.09.005

- Stoever, J., & Weche, J. P. (2018). Environmental regulation and sustainable competitiveness: Evaluating the role of firm-level green investments in the context of the porter hypothesis. Environmental and Resource Economics, 70(2), 429–455. https://doi.org/10.1007/s10640-017-0128-5

- Su, C. W., Chen, Y., Hu, J., Chang, T., & Umar, M. (2022). Can the green bond market enter a new era under the fluctuation of oil price. Economic Research-Ekonomska Istraživanja, 36(1), 536–561. https://doi.org/10.1080/1331677X.2022.2077794

- Su, C. W., Liu, F., Qin, M., & Chnag, T. (2022). Is a consumer loan a catalyst for confidence? Economic Research-Ekonomska Istraživanja, 1–22. https://doi.org/10.1080/1331677X.2022.2142260

- Su, C. W., Pang, L. D., Tao, R., Shao, X., & Umar, M. (2022). Renewable energy and technological innovation: Which one is the winner in promoting net-zero emissions? Technological Forecasting and Social Change, 182, 121798. https://doi.org/10.1016/j.techfore.2022.121798

- Su, C. W., Yuan, X., Tao, R., & Shao, X. (2022). Time and frequency domain connectedness analysis of the energy transformation under climate policy. Technological Forecasting and Social Change, 184, 121978. https://doi.org/10.1016/j.techfore.2022.121978

- Su, C. W., Yuan, X., Umar, M., & Chang, T. (2022). Is presidential popularity a threat or encouragement for investors. Economic Research-Ekonomska Istraživanja, 1–24. https://doi.org/10.1080/1331677X.2022.2129409

- Suk, S., Liu, X., & Sudo, K. (2013). A survey study of energy saving activities of industrial companies in the republic of Korea. Journal of Cleaner Production, 41, 301–311. https://doi.org/10.1016/j.jclepro.2012.10.029

- Tao, R., Su, C. W., Naqvi, B., & Rizvi, S. K. A. (2022). Can Fintech development pave the way for a transition towards low-carbon economy: A global perspective. Technological Forecasting and Social Change, 174, 121278. https://doi.org/10.1016/j.techfore.2021.121278

- Walls, J. L., Berrone, P., & Phan, P. H. (2012). Corporate governance and environmental performance: Is there really a link? Strategic Management Journal, 33(8), 885–913. https://doi.org/10.1002/smj.1952

- Wang, C., Wu, J., & Zhang, B. (2018). Environmental regulation, emissions and productivity: Evidence from Chinese cod-emitting manufacturers. Journal of Environmental Economics and Management, 92, 54–73. https://doi.org/10.1016/j.jeem.2018.08.004