?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Green finance is a vital foundation for fundamental economic low-carbon transformation. Therefore, this study examines the effect of green finance on low-carbon economic development by applying various panel estimators including panel threshold model using data set of 30 provincial administrations in China during 2008–2020. The statistical results suggest that green finance significantly stimulates low-carbon economic development based on a carbon emission and emission intensity perspective. Green finance is more effective in promoting low-carbon economic development in the mid-western areas than in the eastern areas, while it is more effective in less economically developed areas than economically developed areas. Green finance is primarily responsible for driving low-carbon economic development, which is accomplished mainly by stimulating industrial structure upgrading and science and technology investment scale. The threshold outcome reveals that when green finance levels cross a certain threshold, their contribution to low-carbon economic development decreases. These findings offer valuable policy implications.

JEL CODES:

1. Introduction

Since the second industrial revolution, technological changes have contributed to significant developments in human society (Li et al., Citation2021). In particular, electricity has been generated from fossil energy sources such as coal, which is widely used in production and life, increasing productivity and enabling the rapid development of the world’s economies (Liu et al., Citation2022; Sims et al., Citation2003). Underlying economic prosperity is the long-term uncontrolled use of fossil energy and the release of large amounts of greenhouse gases into the environment, at the cost of which humankind has to face severe global warming (Yang et al., Citation2022; Chen & Chen, Citation2021). The truth of global warming and its far-reaching consequences for humanity’s present and future is increasingly receiving worldwide attention (Kumar et al., Citation2022a). The IPCC's Sixth Assessment Report (AR6) in 2022 shows that by 2040, scientists anticipate a global surface temperature increase of 1.5 °C.Footnote1 Consequently, reducing carbon emissions has been identified as an essential initiative to combat global warming by countries around the world, for which numerous agreements have been reached (Sun et al., Citation2022; Wu et al., Citation2021). The Paris Agreement, signed by 178 parties in 2015, creates unified global arrangements for climate change action. In line with this goal, countries worldwide would have to cooperate to significantly reduce carbon emissions over the next decade (2022–2033) (Nadeau et al., Citation2022). Therefore, curbing the global greenhouse effect at its source is still a long way off (Ramanathan & Feng, Citation2009). Faced with this daunting task and the possible damage to their interests in the implementation of this task, countries around the world are forced to consider how to ensure their economic development while maximizing carbon reduction to reduce environmental damage (Su et al., Citation2021). Establishing the low-carbon economic development mode has emerged as the consensus of all nations across the globe, even though they are all engaged in a multi-party game (Razzaq et al., Citation2022). Seeking new tipping paths to combat global warming and intensity and encourage low-carbon economic development is essential for green development (Fankhauser & Jotzo, Citation2018).

Huge investments are required during a real economy’s transition to a low-carbon economy. The expansion degree of the financial sector, which acts as both a funding source and a route for the financing of businesses and other organizations, will have a major influence on the economies as they make the shift to low carbonization (Liu et al., Citation2022; Tang et al., Citation2022). Along with the increasingly close connection between finance and environmental governance, green finance as a financial instrument has become a synonym and an essential medium for extending finance to environmental governance (Irfan et al., Citation2022). As green finance has become increasingly relevant in the economy, the G20 Green Finance Study Group, led by China during its presidency of the G20 Summit in 2016, has dramatically aroused the attention of green finance (He, Citation2019; Lee, Citation2020). As an advocate of green finance, through the release of the “Guidance on Building a Green Financial System,” China made it the first global nation to implement a comprehensive green finance policy framework. Therefore, realizing low-carbon economic development is an enormous social revolution, while green finance is the key to its realization (Li et al., Citation2022).

Green finance means the provision of financial services for green investments and policies, such as the promotion of environmentally sustainable products as well as the mitigation of carbon damage to the climate, with both the goal of fostering environmental improvement and addressing climate change (Kumar et al., Citation2022b; Zhang et al., Citation2022; Lee & Lee, Citation2022). Green finance relates to the segment of the financial sector concerned with environment-conscious investments, and it helps redirect funding away from polluting and energy-hungry sectors and toward those that rely on cutting-edge technology and have a little environmental impact (Hailiang et al., Citation2022; Kirikkaleli & Adebayo, Citation2022; Sharif et al., Citation2022). Green finance can make financial investments in sustainable projects and policies such as boosting energy efficiency, protecting water resources, controlling industrial pollution, controlling traffic pollution, and reducing deforestation and carbon emissions (Hemanand et al., Citation2022; Wang et al., Citation2022). Therefore, learning effective strategies for green finance is crucial to bringing about green transformation and creating a low-carbon economy (Wang & Wang, Citation2022). So, how does green finance contribute to low-carbon economic development? What, if any, role does green finance play in low-carbon economic development, and in what ways? Does the role of green finance in low-carbon economic development vary across economic development levels and geographic locations? What is the mechanism through which green financing influences low-carbon economic growth? Is there a non-linear link between the two at varying degrees of green finance? Based on the above issues, this study mines the impact of green finance on low-carbon economic development, which has significant implications, both conceptually and practically, for China’s efforts to achieve its twin carbon ambitions and generate high-quality economic growth.

The following four facets are where this research makes its most significant contributions: firstly, this study clarifies the impact of green finance on low-carbon economic development in light of Chinese practice, which animates the existing research. Second, given the geographical characteristics and economic differences among Chinese provinces, this study analyzes the heterogeneous effects of green finance on low-carbon economic development. Third, the role mechanism of green finance affecting low-carbon economic development is verified in terms of science and technology investment scale and industrial structure upgrading. Fourth, a comprehensive analysis of the non-linear features that may arise throughout the process of green finance on low-carbon economic development has been carried out to offer a reference for the design of the differentiated policy.

2. Literature review

Scholars have investigated the nexus between green finance and low-carbon economic development. Thus, this study mainly aims to conduct a literature analysis on the dimensions of green finance measurement, the impact of green finance on low-carbon economic development, and the role mechanism of green finance on low-carbon economic development. Green finance is also known as environmental finance or sustainable finance. According to Cai and Guo (Citation2021), green finance is a novel financial system that prioritizes financial stability and environmental sustainability. Sachs et al. (Citation2019) argues that green finance is innovative financing that amplifies funding for investments beneficial to the environment utilizing novel monetary tools and incentives. Like Sachs et al. (Citation2019) argue, green finance primarily involves green bonds, investments, insurance, and carbon finance. Therefore, green finance is not a specific business and not owned by one specialized sector but has multi-sectoral, multi-business, and multi-disciplinary intersections. It is only possible to determine the value of the green finance indicator with a single variable or dimension alone (Cui et al., Citation2020). Scholars in the field of green finance indicators have done considerable work on measuring it. For instance, Jiang et al. (Citation2020) employ an improved entropy technique to test green finance indicators regarding economic, financial, and socio-environmental aspects. Lv et al. (Citation2021) construct a green finance index from policy and market-oriented directions. Utilizing data on green credit extended in China between 2011 and 2019, Wang et al. (Citation2021) determined that indicators like new energy and green transportation projects have the most weight when gauging the extent of the country’s green financial system. Iqbal et al. (Citation2021) establish a green finance indicator capable of measuring the cumulative consequences of energy, environmental, and financial factors and reveal that green finance is essential for the shift in energy use to green energy.

Moreover, the association between green finance and low-carbon economic development is also an extensively negotiated topic among scholars. There are many discussions in academic circles, but a unified opinion has yet to be formed. Since scholars have recognized the low-carbon economic development from different aspects, many different perspectives may be mostly broken down into the areas listed below. First, in some cases, the association between green finance and green economic growth has been examined by scholars (Desalegn and Tang, 2022). Green finance is a crucial component of low-carbon economic development owing to fosters connections between the economy, improvements in environmental quality, and financial markets (Soundarrajan & Vivek, Citation2016). Singh and Mishra (Citation2021) find a positive impact of green finance on economic growth. Ngo et al. (Citation2021) and Sadiq et al. (Citation2022) conclude similarly by noting that evolving green finance is the optimum path to advance economies toward greening. Apart from arguing that green finance promotes new growth points and engines for green economic development, some scholars also argue that green finance and green growth have a high degree of coordination. Liu et al. (Citation2020), through constructing a model of linking synchronization between areas, reaches the opinion that the coupling coordination nexus green finance and green economy. Ma (Citation2022) reveals that green finance moves with higher education and green growth in an identical direction. Second, some scholars have explored the nexus between green finance and carbon emissions. The role of greenhouse gases in the creation of a low-carbon economy has been highlighted, and it has been argued that to facilitate a shift toward a low-carbon economy, it is necessary first to recognize that economic growth need not be incompatible with reducing carbon emissions (Jiang et al., Citation2018; Mohsin et al., Citation2019; Shen & Sun, Citation2016). Shen et al. (Citation2021) reveal that green investment is inversely related to levels of carbon emissions. Meo and Abd Karim (Citation2022) reveal that despite green finance’s negative influence on carbon emissions generally, variations are observed in different quartiles of these two variables. Feng et al. (Citation2022) discovers that an inverted U-shaped spatial association is demonstrated for green finance and carbon emissions. Cao (Citation2022) demonstrates that green financing decreases carbon emissions and supports green development.

The nexus between carbon emission intensity and green finance is also a topic that many scholars are investigating (Li & Fan, Citation2022). It has been pointed out that carbon intensity reflects the carbon emissions required to produce a unit of economy, which correlates carbon emission reduction and economic development well (Kretschmer et al., Citation2013; Rahim, Citation2014). Ren et al. (Citation2020) argues that the green finance industry developed rapidly using Chinese data from 2000–2018, and the improvements and decreases in carbon intensity have resulted from green finance. Wang et al. (Citation2021) points out that green finance is highly adaptive and can synergistically contribute to carbon emission reduction under different intensities of environmental regulation. Zhang and Ke (Citation2022) yield the intriguing result that green finance’s dampening role on carbon intensity relies on the capital stock per capita.

Some scholars have also investigated the nexus between green finance and productivity (TFP). They argue that promoting the low-carbon economy involves boosting carbon efficiency, contributing to the win-win objective of ecology and economy (Chen et al., Citation2021; Lin & Sai, Citation2022; Zhang et al., Citation2017). As carbon emission efficiency involves technological improvements, scholars often use green TFP to measure it in specific studies (Rusiawan et al., Citation2015; Yang et al., Citation2021; Zhang, Citation2015). Li et al. (Citation2022) points out that green finance, represented by green credit, exerts a favorable ameliorative effect on green TFP. Finally, some scholars have also studied the role mechanisms through which green finance shocks low-carbon economic development. Some scholars point out that energy consumption (Sun & Chen, Citation2022), green technological progress (Lin et al., Citation2022), industrial structure transformation and upgrading (Zhu et al., Citation2022), urbanization (Tsai, Citation2019), and unemployment rate (Cui et al., Citation2022) are fundamental reasons for green finance to influence changes in the low-carbon economy. Specifically, Wang et al. (Citation2019) analyzes that green finance exacerbates the financing constraints of polluting firms based on data from 192 listed firms, thus inhibiting investment in polluting enterprises. However, this phenomenon only occurs in private firms and has yet to manifest itself in state-owned enterprises. Chen et al. (Citation2021) find that green finance indirectly damps carbon emissions by boosting science and technology investment scale and facilitating green innovation.

Even after reviewing the available literature, scholars have yet to yield a clear consensus on the effects of green financing on the low-carbon economy. This may be due to the different research samples, time, and methods (Soundarrajan & Vivek, Citation2016; Singh & Mishra, Citation2021). Moreover, the impact of green finance on green economic growth, carbon emission, or carbon emission efficiency is generally analyzed only separately (Liu, 2021; Lin & Sai, Citation2022; Liu et al., Citation2020; Zhang & Ke, Citation2022). However, with the development of low-carbon economic theory, the connotation of the low-carbon economy is getting more affluent and prosperous (Sun & Chen, Citation2022). More and more scholars not only focus on low carbon economic development unilaterally from green growth, carbon emission, or emission efficiency but also consider low carbon economy comprehensively in many aspects (Desalegn & Tangl, Citation2022; Li & Fan, Citation2022). However, related research still needs to be further expanded.

Regarding the role mechanism of green finance on low-carbon economic development, the investigation perspectives also present diversification, among which science and technology investment scale and industrial structure upgrading are the actual contents that most scholars focus on (Chen et al., Citation2021; Zhu et al., Citation2022). The research still needs to be improved. Therefore, this study quantifies the impact of green finance on the low-carbon economic development in China in terms of carbon emissions and emission intensity. Meanwhile, the roles of science and technology investment scale and industrial structure upgrading in the impact of green finance on low-carbon economic development are investigated. Finally, this study also elaborates on green finance’s non-linear and heterogeneous characteristics influencing low-carbon economic development.

3. Research design

3.1. Model settings

Following Wang et al. (Citation2021), this study tests the impact of green finance on low-carbon economic development by constructing the OLS model. Given data fluctuations of different magnitudes, this study applies the logarithmic process to some variables to remedy the issue of biased model estimation brought on by heteroskedasticity. The baseline model is set as follows:

(1)

(1)

(2)

(2)

where low-carbon economic development is the dependent variable, including carbon emissions

and carbon emission intensity

is green finance level of each province.

signifies the control variables, namely population

environmental regulation

foreign direct investment

urbanization level

and government intervention

and

are each region and year fixed effects.

is a disturbance term.

and

are the evaluated parameters.

3.2. Variables selection

3.2.1. Dependent variable

Low-carbon economic development. Referring to Wang et al. (Citation2022), carbon emission intensity (CI) and carbon emission levels (C) are jointly applied to measure low carbon economic development levels. The existing literature needs to contain a uniform standard for measuring carbon emissions. Currently, there are two main types of carbon emission measurement techniques, namely sectoral accounting technique and episodic emission accounting technique. This study uses the epistatic technique to measure carbon emissions based on the consumption-side data of disposable energy sources (Coal, coke, crude oil, gasoline, kerosene, diesel, fuel oil, and natural gas), to estimate the carbon emissions. The carbon emissions are calculated as follows:

(3)

(3)

where

denotes carbon emissions.

is the carbon dioxide to carbon molecule weight ratio.

is the consumption of fossil fuels in category

Carbon emission intensity (CI). The following formula could be employed to determine the carbon emission intensity, which is determined based on creating the carbon emission index C.

(4)

(4)

Among them, C signifies carbon emissions, and GDP is gross domestic product.

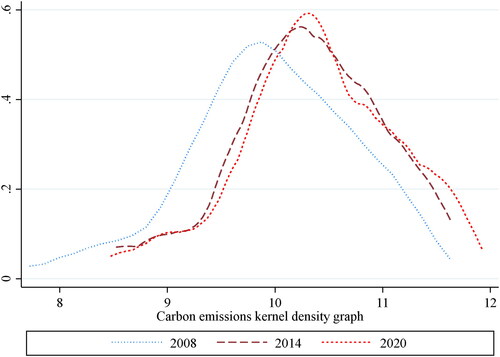

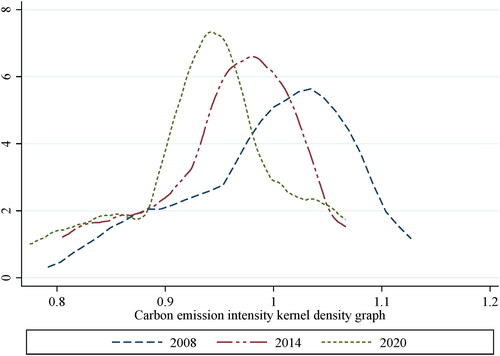

illustrates the changing trend of carbon emission intensity. The kernel density curve shows a noticeable shift to the left, indicating a clear trend of decreasing carbon intensity. The crest of the kernel density curve gradually becomes steeper and flatter, indicating that the carbon intensity of each area becomes more concentrated from more even distribution. The kernel density estimation graph in depicts the carbon emissions trend. The kernel density curve has moved leftover time, which is consistent with a declining trend in carbon emissions in China. However, the leftward shift of the kernel density curve is slight, indicating a slow downward trend of carbon emissions. The wave of the kernel density curve gradually becomes flat from high to steep, indicating that carbon emissions in each area become even more concentrated.

Figure 1. Carbon emission intensity kernel density graph.

Source: drawn by all authors.

Figure 2. Carbon emissions kernel density graph.

Source: drawn by all authors.

3.2.2. Core explanatory variables

Green finance (GF). Some scholars argue that green finance is the cross between environmental economics and finance, aiming to counter the financing of ecological and environmental protection (Cowan, Citation1999). Certain scholars have considered green finance a financial innovation and a link between the financial industry and environmental conservation (Salazar, Citation1998). Different countries or regions often interpret green finance in different manners. Developed countries prefer to concentrate on climate change and the innovation and application of green technologies at the environmental protection level. Developing countries, however, concentrate more on financial investments to reduce energy consumption. The best way to quantify green finance is by establishing green finance development indicators. Therefore, the field is still very much in its exploratory phase. Referring to Song (Citation2022), this study sets a green finance indicator system and systematically measures the regional green finance status from various perspectives, such as development trends, development variability, and spatial distribution level (See ).

Table 1. Green finance indicator system.

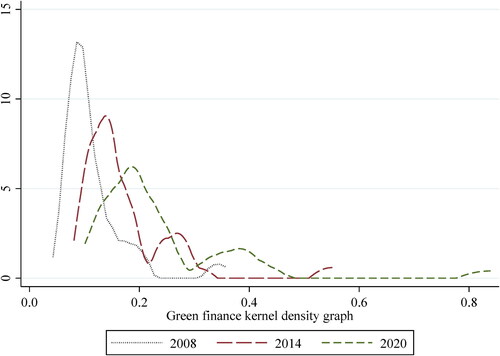

depicts green finance’ changing trend in the kernel density estimation graph. On the one hand, the kernel density curve shows a clear rightward shift over time, implying that China’s green finance is on a growth trend. On the other hand, the crest of the kernel density curve is slowing down over time, indicating that green finance is becoming relatively more balanced across regions, and the overall gap is shrinking.

Figure 3. Green finance kernel density map.

Source: drawn by all authors.

3.2.3. Control variables

To reduce the impact of the endogeneity issue brought on by the additional values, the relevant control variables have been included, including population (POP), environmental regulation (ER), foreign direct investment (FDI), urbanization level (URBAN), and government intervention (GOV). The population at the end of the year is used to calculate the total population (POP). Typically, the larger the population, the more people are engaged in production and consumption. Therefore, higher energy is used, which results in more carbon being released, and more money and technology are invested in combating the climate and environmental issues caused by excessive carbon emissions. Environmental regulation (ER) is measured by the amount of investment in pollution control. In order to meet the environmental regulation policy, companies must meet the requirements by saving energy and reducing emissions or face the option of relocation. However, some studies have shown that environmental regulations do not affect firms in the short term and, thus, do not affect carbon emissions. Foreign direct investment (FDI) is measured by the amount of foreign investment in China. High pollution and energy consumption have long been hallmarks of most foreign-invested firms entering China, and neither of these factors is helpful in the effort to reduce carbon emissions. Whether they are currently transformed into environmentally friendly enterprises is still open to debate. The percentage of the total population residing in urban areas at the end of the year is used to determine the urbanization level (URBAN). Urbanization is often driven by industrialization, which implies many waste emissions. Considering that as the quality of urbanization becomes higher, there may be a turning point in its effect on carbon emissions, a quadratic term of urbanization level is included in the regression. Government intervention (GOV) measures government intervention in terms of government fiscal spending as a share of GDP. Government intervention affects the direction of green finance policy and shapes low-carbon economic development.

3.3. Data sources

Thirty Chinese province-level administrative areas are the focus of this study, covering the years 2008–2020. The indicators are built using information culled from the China EPS and CNKI databases during the time under consideration. This research uses the interpolation method to make up for individual missing values in the statistical data. provides descriptive statistics.

Table 2. Descriptive statistical results.

4. Results and discussion

4.1. Baseline regression results and discussion

reveals the impact of green finance on low-carbon economic development. Columns (1) and (2) of report that green finance has a track record and substantial potential for lowering carbon emissions. In the case of introducing control variables, the coefficient is −1.740, implying that for every 1 unit increase in green finance, carbon emissions will decrease by 1.74 units. Columns (3) and (4) of reveal that green finance significantly reduces carbon intensity, with a regression coefficient of 0.214. For every 1 unit increase in green finance, carbon intensity will decrease by 0.214 units. Our study is comparable to the arguments of Soundarrajan and Vivek (Citation2016), Sharif et al. (Citation2022), and Zhang et al. (Citation2022). Zhang et al. (Citation2022) that green finance eliminates the adverse effects of climate change after using G20 economies as a study subject. Green finance helps reduce carbon emissions while reaping economic benefits (Lee, Citation2020). Green finance is not simply about reducing carbon emissions but, more importantly, about achieving low-carbon economic development targets primarily by reducing carbon emission intensity (Kumar et al., Citation2022; Liu et al., Citation2020). This is because financial resources are essential in low-carbon economic development and control floodgates. Green finance is a vivid practice of the new low-carbon development model in the financial field and is an innovative financial product for achieving environmental protection, economic development, and resource conservation (Kirikkaleli & Adebayo, Citation2022; Sun, Citation2022). Overall, green finance deepens traditional finance functions, controls the intensity and total amount of carbon emissions through financial means, strengthens the effectiveness of constraints on emission reduction, and ultimately promotes low-carbon economic development.

Table 3. Baseline regression result.

Table 4. Economic development level heterogeneity results.

4.2. Heterogeneity regression results and discussion

Influenced by economic and geographical environmental factors, green finance and low-carbon economic development levels among different parts of China may vary in somewhat different forms, which makes such impact may have significant heterogeneity. Whether green finance can effectively contribute to low-carbon economic development is strongly associated with the local economic development level. Areas with higher economic development levels have more available sources, which effectively absorb the initial capital and innovation deployment required for low-carbon economic development. For this purpose, this study uses each province’s per capita GDP indicator to evaluate the economic development level of the areas strictly. It divides the 30 provincial administrative areas in the sample data into economically developed and less developed areas (See ). This study classifies the dataset into eastern and mid-western areas following the locational characteristics. Comparatively, the eastern areas benefit from superior infrastructure (in terms of both accessibility and the sophistication of their respective processing trades) and green finance access. Moreover, the eastern areas are primed for brisk growth for green finance, but the crucial majority of traditional, labor-intensive, incredibly energy-intensive processing trade industries are concentrated in the mid-western areas. There is still a need to explore how the structural mismatch between supply and demand of industrial growth may affect green finance for low-carbon economic development in various sectors (See ).

Table 5. Regional heterogeneity results.

Columns (1) and (2) of reveal that the coefficients of green finance on carbon emissions (-1.267) and carbon emission intensity (-0.151) in economically developed areas are significantly negative. Columns (3) and (4) in reveal that the coefficients of green finance on carbon emissions (-3.487) and carbon emission intensity (-0.546) in less economically developed areas are significantly negative. In terms of carbon emissions and carbon intensity, green finance is more effective for low-carbon economic development in less-developed areas (Zhao et al., Citation2022). Because of the urgent desire to develop the economy and realize jumping ahead, the less developed economic areas favor high energy consumption industries with high output. However, green finance will essentially inhibit investment in high-energy consumption industries in less developed areas, curbing their development and thus achieving low-carbon economic development (Huang, Citation2022). Moreover, economically developed areas have achieved economic development advantages and pay more attention to ecological protection (Bai et al., Citation2022). Governments at the municipal level sometimes outright ban high-energy-use enterprises, and green financing seldom gets a shot (Wang et al., Citation2022). Therefore, green finance is relatively weak in influencing low-carbon economic development.

Columns (1) and (2) of reveal that the regression coefficients of green finance on carbon emissions (-1.158) and carbon intensity (-0.115) in the eastern area are significantly negative. Columns (3) and (4) of reveal that the coefficients of green finance on carbon emissions (-3.026) and carbon intensity (-0.415) are significantly negative in the mid-western area. Comparative analysis suggests that although the overall impact of green finance on carbon emissions and carbon emission intensity is significantly negative, the impact of green finance is more prominent in the mid-western areas from both carbon emission and carbon emission intensity perspectives. On the one hand, the mid-western area of China is where China’s labor-intensive, and high-polluting industries are transferred (Li et al., Citation2022). The green transformation of these sectors will be “reversed” by green finance to meet the main prerequisites of green finance supply, allowing for the attainment of regional low-carbon economic development (Sun & Chen, Citation2022). On the other hand, green finance enjoys tremendous benefits in the eastern areas due to its developed financial base, human resources, and digital infrastructure (Zhou & Xu, Citation2022). However, the excessive financialization of green finance may also lead to a “de-realization” of the economy, thus affecting local industries and low-carbon economic development.

4.3. Robustness check results and discussion

To check the empirical results reliability, this study also tries to conduct robustness checks from the following aspects. First of all, the measurement technique is changed. This study not only adopts a fixed-effects model to test the impact of green finance on the low-carbon economy but also opts for a random-effects model to test for it (see , columns (1) and (2)). Second, potential omitted variables are controlled for. Energy consumption significantly shocks local low-carbon economic development. Green finance also restrains the development of overly energy-dependent related industries to a certain extent. Therefore, this study further controls for local energy consumption, using total local energy consumption taken as a logarithm to measure. In addition, the degree of regional technology level

is crucial when using green financing to advance low-carbon economic growth. Regional technology-level development relies on green finance to help. Low-carbon economic transformation requires specific technical support. Therefore, this paper also further controls for regional technology level, which is measured by taking the logarithm of the total number of local invention patents (see columns (3) and (4) of ).

Table 6. Robustness check results.

Finally, the sample of municipalities directly under the central government is excluded. Considering that Chinese municipalities are different from ordinary prefecture-level cities and provincial capitals in terms of economic and political aspects, the sample of municipalities is excluded (see columns (5) and (6) of ). reveals that the primary explanatory variables’ regression coefficients show no discernible sign or significance change from the above findings.

4.4. Role mechanism results discussion

Furthermore, green finance controls carbon emissions and emission intensity through financial instruments and strengthens the effectiveness of constraints on emission reduction, ultimately promoting low-carbon economic development. Its inherent realization path is mainly through guiding industrial structures and boosting technology progress. From the perspective of guiding industrial structure development, established research has shown that green finance promotes industrial structure in provincial nations by creating diversified green financial instruments. For example, through various ways, such as green funds and green credits, capital flows are guided to green industries to achieve optimal industrial restructuring and ultimately promote regional low-carbon economic development (Qi & Qi, Citation2020).

In terms of advancing technology level, green technology innovation is the intrinsic driving force of regional low-carbon economic development. Whereas technology level promotion often relies on a large amount of financial investment. The key to green finance for technology-level development is to boost the science and technology investment scale. Green finance can provide more efficient, lower cost, and larger scale financial support for enterprise green technology innovation, which is conducive to solving the fund’s shortage and enhancing the willingness and ability of enterprises to engage in green technology innovation. Second, green innovation projects often have high-risk characteristics. A developed green financial market and abundant green financial products can provide investors with more efficient and diversified investment products and risk-averse tools, enhance the investment enthusiasm of risk capital, and thus stimulate the core momentum of regional low-carbon economic development.

To test whether green finance can promote low-carbon economic development through industrial structure upgrading (Upg) and science and technology investment scale (kjtr). Further, this study analyzes the potential role mechanism of green finance on low-carbon economic development in terms of science and technology investment scale and industrial structure upgrading

The specific setting form is as follows.

(3)

(3)

(4)

(4)

(5)

(5)

where

includes both science and technology investment scale

and industrial structure upgrading

During the process of industrial structure upgrading, the proportion of primary industry to the entire industrial sector falls, while the proportions of intermediate and tertiary sectors grow (Gao et al., Citation2022). The most sophisticated tertiary industry is the most appropriate term to use when discussing modernizing manufacturing. So, the ratio of the tertiary sector’s added value to GDP is a good indicator of progress in modernizing the industrial structure

The science and technology investment scale (Kjtr) is an essential factor limiting enterprises’ implementation of technological innovation. The high level of science and technology investment is directly reflected in the sufficient investment in enterprises and related industries, which will not only limit the development of green transformation of enterprises but also restrict the iteration of a green technology update. Considering that boosting science and technology investment will directly shock innovation input, this study uses regional science and technology investment to characterize the ability to increase science and technology investment scale. Local science and technology investment funds represent the indicators of science and technology investment scale (Kjtr).

and

are the evaluated parameters. The remaining parameters are the same as in EquationEquations 1

(1)

(1) and Equation2

(2)

(2) .

Columns (1)–(3) of reveal the role mechanism of industrial structure upgrading in green finance influencing low-carbon economic development. Column (1) of reveals that the effect of green finance on industrial structure upgrading is significantly positive, which is consistent with the analysis results above. Columns (2) and (3) in reveal that green finance promotes low-carbon economic development mainly by mitigating carbon emission intensity through industrial structure. Still, the effect on carbon emission is paradoxically presented as a promotion effect.

Table 7. Role mechanism results.

One potential explanation is that green finance eliminates backward and energy-intensive industries in promoting industrial structure upgrading and further expansion of the green industry scale (Yu et al., Citation2021; Wang and Wang, 2022). However, carbon emissions still show an increasing trend due to the limitation of low-carbon technology levels (Ren et al., Citation2021). The continued low carbon emission intensity also means that the positive effect of overall economic enhancement brought by green finance is more prominent. Columns (4)–(6) of demonstrate how boosting science and technology investment scale under green finance influences low-carbon economic development. Column (4) of reveals that the effect of green finance on boosting science and technology investment scale shows a significant positive correlation, implying that green finance development will significantly boost the science and technology investment scale, which is consistent with the logical discussion above. Columns (5) and (6) of confirm that green finance reduces carbon emission intensity to achieve low-carbon economic development by boosting science and technology investment scale, but the impact on carbon emissions is insignificant. Green finance removes a significant barrier to innovation and technological advancement by making investing in and implementing green practices easier (Irfan et al., Citation2022). It not only improves the “quality” of the technical level of industrial production development but also promotes the “quantity” of green attribute industries and enterprises (Jiakui et al., Citation2023). Although the influence of science and technology investment scale on carbon emissions is not significantly inhibitive, the carbon emission intensity, which is more indicative of the low-carbon economic development indicator.

4.5. Threshold effect results and discussion

The above results indicate that green finance is disturbed by regional and economic development level heterogeneity when it contributes to low-carbon economic development. To analyze the possible non-linear evolutionary pattern of green finance contributing to low-carbon economic development, referring to Hansen (1999), this study mines the effect of green finance on low-carbon economic development under different green finance levels by using green finance as a threshold variable. This study constructs a model with a single threshold as an example.

(6)

(6)

(7)

(7)

EquationEquations (6)(6)

(6) and Equation(7)

(7)

(7) in

and

and for the threshold value, the rest of the variables with the same EquationEquations (1)

(1)

(1) and Equation(2)

(2)

(2) , more details will not be elaborated.

4.5.1. Threshold effect test and threshold value determination

Testing the threshold effect and establishing a threshold value are prerequisites to evaluating the potential non-linear properties of green finance (see ). Green financing has a threshold influence on low-carbon economic development, as shown in . The threshold values and confidence intervals for each sample size are reported in and , respectively.

Table 8. Threshold test results.

Table 9. Threshold value results.

4.5.2. Threshold estimation results

reveals that green finance presents significant non-linear characteristics in promoting regional low-carbon economic development. After comparing the threshold coefficients of green finance on carbon emission and carbon emission intensity, one finds that when green finance is below the first threshold, both carbon emission and carbon emission intensity perspectives, green finance passes the significance test for low-carbon economic development. As green finance steadily increases, green finance will significantly drive low-carbon economic development. When the green finance level keeps rising across the threshold, the driving effect of green finance on low-carbon economic development is still significant, but the driving effect decreases slightly when comparing the influence coefficients before and after the green finance threshold. One possible reason is that financial development’s fundamental purpose is to serve the real economy (Zhao et al., Citation2022). However, the profit-oriented nature of finance also means that excessive financial development may lead to a “de-realization” of finance to the financial industry with more lucrative returns, thus squeezing out the capital demand for industrial development and ultimately inhibiting industrial development (Bai et al., Citation2022). Therefore, green finance must be completely unleashed while driving green finance to enable low-carbon economic development and avoid catastrophic financial risks.

Table 10. Threshold regression results.

5. Conclusion and policy implications

This study discusses the effects of green finance on low-carbon economic development by developing OLS, mediating effect, and threshold effect models with the dataset of 30 provincial administrations in China during 2008–2020. The significant study findings reveal that green finance significantly stimulates low-carbon economic development based on carbon emission or emission intensity perspective. Green finance is more effective in promoting low-carbon economic development in the mid-western areas than in the eastern areas, while it is more effective in less economically developed areas than economically developed areas. Green finance promotes low-carbon economic development mainly by mitigating carbon emission intensity through industrial structure, but the effect on carbon emission is paradoxically presented as a promotion effect. Green finance reduces carbon emission intensity to achieve low-carbon economic development by boosting the science and technology investment scale, but the impact on carbon emissions is insignificant. Lastly, when green finance levels cross the threshold, their contribution to low-carbon economic development decreases.

As such, this study proposes the following countermeasures.

Policymakers shall continuously drive the deepening of green finance levels in each area. To fully realize green finance’s potential for stimulating the low-carbon economy, it is essential to move quickly toward establishing a cutting-edge green financial system and supporting the robust growth of green finance. Differentiated strategies should be implemented. Policymakers should consider the regional imbalances and inadequacies during the low-carbon economic transition at all levels of administration. For example, green finance construction in the central-western and less developed areas should be supported to improve the financial infrastructure. Then, information on green finance should be widely distributed so that individuals and organizations can better understand how to use green financial instruments and more easily identify and embrace green finance.

Efforts must be made to increase the creation of technological infrastructure and continually expand the popularity and depth of usage of environmentally friendly financing throughout the nation. Policymakers should utilize green finance’s industrial structure upgrading shock and guide the green transformation. Policymakers should utilize the effect of green finance in boosting science and technology investment scale, guiding the flow of funds into environmental protection and green industries, and providing diversified financing channels for the low-carbon economy to mobilize all sectors of society in the growth of green finance, so that green finance can more fully support low-carbon economy by offering a variety of funding channels for the low-carbon economy. Policymakers should selectively make relevant policies so that green finance in each area can reach the threshold of the main push for low-carbon economic development. While promoting green finance, attention should also be paid to preventing systemic financial risks and avoiding financial “de-realization to deficiency” caused by the excessive development of green finance.

Although this study thoroughly investigates the impact of green finance on low-carbon economic development, some significant aspects still deserve attention. This study, for example, only employs provincial-level data to examine the nexus between green finance and low-carbon economic development without analyzing it from a more microscopic perspective. As data analysis and acquisition techniques continue to advance, scholars can conduct a deeper discussion of the nexus between the two from the perspective of micro-enterprises. Furthermore, this study mines the role mechanisms of green finance on low-carbon economic development from both pathways science and technology investment scale and industrial structure upgrading. However, resource misallocation and marketization are also potentially significant mechanisms. Future scholars can take resource misallocation and marketization views to analyze the role mechanism of green finance on low-carbon economic development.

Disclosure statement

The authors declare that the research was conducted without any commercial or financial relationships that could be construed as a potential conflict of interest.

Additional information

Funding

Notes

References list

- Bai, J., Chen, Z., Yan, X., & Zhang, Y. (2022). Research on the impact of green finance on carbon emissions: Evidence from China. Economic Research-Ekonomska Istraživanja, 35(1), 6965–6984.

- Cai, R., & Guo, J. (2021). Finance for the environment: A scientometrics analysis of green finance. Mathematics, 9(13), 1537.

- Cao, L. (2022). How green finance reduces CO2 emissions for green economic recovery: Empirical evidence from E7 economies. Environmental Science and Pollution Research, 30, 3307–3320.

- Chen, H., Guo, W., Feng, X., Wei, W., Liu, H., Feng, Y., & Gong, W. (2021). The impact of low-carbon city pilot policy on the total factor productivity of listed enterprises in China. Resources, Conservation and Recycling, 169, 105457.

- Chen, X., & Chen, Z. (2021). Can green finance development reduce carbon emissions? Empirical evidence from 30 Chinese provinces. Sustainability, 13(21), 12137.

- Cowan, E. (1999). Topical issues in environmental finance. Research Paper Was Commissioned by the Asia Branch of the Canadian International Development Agency (CIDA), 1, 1–20.

- Cui, H., Wang, R., & Wang, H. (2020). An evolutionary analysis of green finance sustainability based on multi-agent game. Journal of Cleaner Production, 269, 121799.

- Cui, Y., Wang, G., Irfan, M., Wu, D., & Cao, J. (2022). The effect of green finance and unemployment rate on carbon emissions in china. Frontiers in Environmental Science, 10, 887341. https://doi.org/10.3389/fenvs.2022.887341

- Desalegn, G., & Tangl, A. (2022). Enhancing green finance for inclusive green growth: A systematic approach. Sustainability, 14(12), 7416.

- Fankhauser, S., & Jotzo, F. (2018). Economic growth and development with low‐carbon energy. Wiley Interdisciplinary Reviews: Climate Change, 9(1), e495.

- Feng, L., Shang, S., An, S., & Yang, W. (2022). The spatial heterogeneity effect of green finance development on carbon emissions. Entropy, 24(8), 1042.

- Gao, P., Wang, Y., Zou, Y., Su, X., Che, X., & Yang, X. (2022). Green technology innovation and carbon emissions nexus in China: Does industrial structure upgrading matter? Frontiers in Psychology, 13, 951172. https://doi.org/10.3389/fpsyg.2022.951172

- Hailiang, Z., Iqbal, W., Chau, K. Y., Raza Shah, S. A., Ahmad, W., & Hua, H. (2022). Green finance, renewable energy investment, and environmental protection: Empirical evidence from BRICS countries. Economic Research-Ekonomska Istraživanja, 1–23. https://doi.org/10.1080/1331677X.2022.2125032

- He, A. (2019). Interaction between the G20 agenda and members’ national-level policy: A theoretical model for increasing G20 effectiveness. South African Journal of International Affairs, 26(4), 601–620.

- Hemanand, D., Mishra, N., Premalatha, G., Mavaluru, D., Vajpayee, A., Kushwaha, S., & Sahile, K. (2022). Applications of intelligent model to analyze the green finance for environmental development in the context of artificial intelligence. Computational Intelligence and Neuroscience, 2022. https://doi.org/10.1155/2022/2977824

- Huang, D. (2022). Green finance, environmental regulation, and regional economic growth: From the perspective of low-carbon technological progress. Environmental Science and Pollution Research, 29(22), 33698–33712.

- Iqbal, S., Taghizadeh-Hesary, F., Mohsin, M., & Iqbal, W. (2021). Assessing the role of the green finance index in environmental pollution reduction. Studies of Applied Economics, 39(3). https://doi.org/10.25115/eea.v39i3.4140

- Irfan, M., Razzaq, A., Sharif, A., & Yang, X. (2022). Influence mechanism between green finance and green innovation: Exploring regional policy intervention effects in China. Technological Forecasting and Social Change, 182, 121882.

- Jiakui, C., Abbas, J., Najam, H., Liu, J., & Abbas, J. (2023). Green technological innovation, green finance, and financial development and their role in green total factor productivity: Empirical insights from China. Journal of Cleaner Production, 382, 135131.

- Jiang, L., Wang, H., Tong, A., Hu, Z., Duan, H., Zhang, X., & Wang, Y. (2020). The measurement of green finance development index and its poverty reduction effect: dynamic panel analysis based on improved entropy method. Discrete Dynamics in Nature and Society, 2020, 1–13. https://doi.org/10.1155/2020/8851684

- Jiang, R., Zhou, Y., & Li, R. (2018). Moving to a low-carbon economy in China: Decoupling and decomposition analysis of emission and economy from a sector perspective. Sustainability, 10(4), 978.

- Kirikkaleli, D., & Adebayo, T. S. (2022). Political risk and environmental quality in Brazil: Role of green finance and green innovation. International Journal of Finance & Economics. https://doi.org/10.1002/ijfe.2732

- Kretschmer, B., Hübler, M., & Nunnenkamp, P. (2013). Does foreign aid reduce energy and carbon intensities of developing economies? Journal of International Development, 25(1), 67–91.

- Kumar, A., Singh, P., Raizada, P., & Hussain, C. M. (2022). Impact of COVID-19 on greenhouse gases emissions: A critical review. The Science of the Total Environment, 806, 150349.

- Kumar, L., Nadeem, F., Sloan, M., Restle-Steinert, J., Deitch, M. J., Ali Naqvi, S., … Sassanelli, C. (2022). Fostering green finance for sustainable development: A focus on textile and leather small medium enterprises in Pakistan. Sustainability, 14(19), 11908.

- Lee, C. C., & Lee, C. C. (2022). How does green finance affect green total factor productivity? Evidence from China. Energy Economics, 107, 105863.

- Lee, J. W. (2020). Green finance and sustainable development goals: The case of China. Journal of Asian Finance Economics and Business, 7(7), 577–586.

- Li, B., Zhang, J., Shen, Y., & Du, Q. (2022). Can green credit policy promote green total factor productivity? Evidence from China. Environmental Science and Pollution Research, 30(3), 6891–6905. https://doi.org/10.1007/s11356-022-22695-5

- Li, W., & Fan, Y. (2022). Influence of green finance on carbon emission intensity: Empirical evidence from China based on spatial metrology. Environmental Science and Pollution Research, 30, 20310–20326. https://doi.org/10.1007/s11356-022-23523-6

- Li, W., Fan, J., & Zhao, J. (2022). Has green finance facilitated China’s low-carbon economic transition? Environmental Science and Pollution Research, 29(38), 57502–57515. https://doi.org/10.1007/s11356-022-19891-8

- Li, Y., Yang, X., Ran, Q., Wu, H., Irfan, M., & Ahmad, M. (2021). Energy structure, digital economy, and carbon emissions: Evidence from China. Environmental Science and Pollution Research, 28(45), 64606–64629.

- Lin, B., & Sai, R. (2022). Towards low carbon economy: Performance of electricity generation and emission reduction potential in Africa. Energy, 251, 123952.

- Lin, Z., Liao, X., & Jia, H. (2022). Could green finance facilitate low-carbon transformation of power generation? Some evidence from China. International Journal of Climate Change Strategies and Management, (ahead-of-print). https://doi.org/10.1108/IJCCSM-03-2022-0039

- Liu, N., Liu, C., Xia, Y., Ren, Y., & Liang, J. (2020). Examining the coordination between green finance and green economy aiming for sustainable development: A case study of China. Sustainability, 12(9), 3717.

- Liu, X., Razzaq, A., Shahzad, M., & Irfan, M. (2022). Technological changes, financial development and ecological consequences: A comparative study of developed and developing economies. Technological Forecasting and Social Change, 184, 122004.

- Liu, Z., Deng, Z., He, G., Wang, H., Zhang, X., Lin, J., … Liang, X. (2022). Challenges and opportunities for carbon neutrality in China. Nature Reviews Earth & Environment, 3(2), 141–155.

- Lv, C., Bian, B., Lee, C. C., & He, Z. (2021). Regional gap and the trend of green finance development in China. Energy Economics, 102, 105476.

- Ma, W. (2022). Research on the coupling and coordination of green finance, higher education, and green economic growth. Environmental Science and Pollution Research, 29(39), 59145–59158. https://doi.org/10.1007/s11356-022-20026-2

- Meo, M. S., & Abd Karim, M. Z. (2022). The role of green finance in reducing CO2 emissions: An empirical analysis. Borsa Istanbul Review, 22(1), 169–178.

- Mohsin, M., Rasheed, A. K., Sun, H., Zhang, J., Iram, R., Iqbal, N., & Abbas, Q. (2019). Developing low carbon economies: An aggregated composite index based on carbon emissions. Sustainable Energy Technologies and Assessments, 35, 365–374.

- Nadeau, K. C., Agache, I., Jutel, M., Annesi Maesano, I., Akdis, M., Sampath, V., … Akdis, C. A. (2022). Climate change: A call to action for the United Nations. Allergy, 77(4), 1087–1090.

- Ngo, Q. T., Tran, H. A., & Tran, H. T. T. (2021). The impact of green finance and COVID-19 on economic development: Capital formation and educational expenditure of ASEAN economies. China Finance Review International, 12(2), 261–279. https://doi.org/10.1108/CFRI-05-2021-0087

- Qi, R., & Qi, L. (2020). Can synergy effect exist between green finance and industrial structure upgrade in China? Open Journal of Social Sciences, 8(08), 215.

- Rahim, K. A. (2014). Towards low carbon economy via carbon intensity reduction in Malaysia. Journal of Economics & Sustainable Development, 5, 123–132.

- Ramanathan, V., & Feng, Y. (2009). Air pollution, greenhouse gases and climate change: Global and regional perspectives. Atmospheric Environment, 43(1), 37–50.

- Razzaq, A., Sharif, A., An, H., & Aloui, C. (2022). Testing the directional predictability between carbon trading and sectoral stocks in China: New insights using cross-quantilogram and rolling window causality approaches. Technological Forecasting and Social Change, 182, 121846.

- Ren, L., Zhou, S., Peng, T., & Ou, X. (2021). A review of CO2 emissions reduction technologies and low-carbon development in the iron and steel industry focusing on China. Renewable and Sustainable Energy Reviews, 143, 110846.

- Ren, X., Shao, Q., & Zhong, R. (2020). Nexus between green finance, non-fossil energy use, and carbon intensity: Empirical evidence from China based on a vector error correction model. Journal of Cleaner Production, 277, 122844.

- Rusiawan, W., Tjiptoherijanto, P., Suganda, E., & Darmajanti, L. (2015). Assessment of green total factor productivity impact on sustainable Indonesia productivity growth. Procedia Environmental Sciences, 28, 493–501.

- Sachs, J. D., Woo, W. T., Yoshino, N., & Taghizadeh-Hesary, F. (2019). Why is green finance important?

- Sadiq, M., Amayri, M. A., Paramaiah, C., Mai, N. H., Ngo, T. Q., & Phan, T. T. H. (2022). How green finance and financial development promote green economic growth: Deployment of clean energy sources in South Asia. Environmental Science and Pollution Research, 29(43), 65521–65534. https://doi.org/10.1007/s11356-022-19947-9

- Salazar, J. (1998). Environmental finance: Linking two world. In a workshop on financial innovations for biodiversity Bratislava. (Vol. 1, pp.2–18). Bratislava.

- Sharif, A., Saqib, N., Dong, K., & Khan, S. A. R. (2022). Nexus between green technology innovation, green financing, and CO2 emissions in the G7 countries: The moderating role of social globalisation. Sustainable Development. https://doi.org/10.1002/sd.2360

- Shen, L., & Sun, Y. (2016). Review on carbon emissions, energy consumption and low-carbon economy in China from a perspective of global climate change. Journal of Geographical Sciences, 26(7), 855–870.

- Shen, Y., Su, Z. W., Malik, M. Y., Umar, M., Khan, Z., & Khan, M. (2021). Does green investment, financial development and natural resources rent limit carbon emissions? A provincial panel analysis of China. The Science of the Total Environment, 755, 142538.

- Sims, R. E., Rogner, H. H., & Gregory, K. (2003). Carbon emission and mitigation cost comparisons between fossil fuel, nuclear and renewable energy resources for electricity generation. Energy Policy, 31(13), 1315–1326.

- Singh, V., & Mishra, N. (2021). Impact of green finance on national economic growth during the COVID-19 pandemic. Energy RESEARCH LETTERS, 3(3), 29975.

- Song, Y. R. (2022). The measurement of China’s green financial development index and its distribution characteristics analysis. Western Finance, (04), 29–36. https://doi.org/10.16395/j.cnki.61-1462/f.2022.04.009

- Soundarrajan, P., & Vivek, N. (2016). Green finance for sustainable green economic growth in India. Agricultural Economics, 62(1), 35–44.

- Su, X., Yang, X., Zhang, J., Yan, J., Zhao, J., Shen, J., & Ran, Q. (2021). Analysis of the impacts of economic growth targets and marketization on energy efficiency: Evidence from China. Sustainability, 13(8), 4393.

- Sun, C. (2022). The correlation between green finance and carbon emissions based on improved neural network. Neural Computing and Applications, 34(15), 12399–12413.

- Sun, H., & Chen, F. (2022). The impact of green finance on China’s regional energy consumption structure based on system GMM. Resources Policy, 76, 102588.

- Sun, Y., Razzaq, A., Sun, H., & Irfan, M. (2022). The asymmetric influence of renewable energy and green innovation on carbon neutrality in China: Analysis from non-linear ARDL model. Renewable Energy. 193, 334–343.

- Tang, C., Irfan, M., Razzaq, A., & Dagar, V. (2022). Natural resources and financial development: Role of business regulations in testing the resource-curse hypothesis in ASEAN countries. Resources Policy, 76, 102612.

- Tsai, S. F. (2019). Urbanization, public finance and carbon intensity – Based on panel data and error correction model.

- Wang, Y. L., Hou, L. Q., & Zhu, J. H. (2022). Can urban innovation contribute to the development of low-carbon economy – An assessment of the impact of innovative city pilot policies on carbon intensity and mechanism analysis[J/OL]. Science and Technology Progress and Countermeasures, 39(18), 39–49. http://kns.cnki.net/kcms/detail/42.1224.G3.20220120.1810.010.html

- Wang, F., Cai, W., & Elahi, E. (2021). Do green finance and environmental regulation play a crucial role in the reduction of CO2 emissions? An empirical analysis of 126 Chinese cities. Sustainability, 13(23), 13014.

- Wang, K., Sun, X., & Wang, F. (2019). Green Finance, Financing Constrains and the Investment of Polluting Enterprise.

- Wang, K. H., Zhao, Y. X., Jiang, C. F., & Li, Z. Z. (2022). Does green finance inspire sustainable development? Evidence from a global perspective. Economic Analysis and Policy, 75, 412–426.

- Wang, X., & Wang, Q. (2022). Research on the impact of green finance on the upgrading of China’s regional industrial structure from the perspective of sustainable development. Resources Policy, 74, 102436.

- Wang, X., Sun, X., Zhang, H., & Xue, C. (2022). Does green financial reform pilot policy promote green technology innovation? Empirical evidence from China. Environmental Science and Pollution Research, 29(51), 77283–77299. https://doi.org/10.1007/s11356-022-21291-x

- Wang, X., Zhao, H., & Bi, K. (2021). The measurement of green finance index and the development forecast of green finance in China. Environmental and Ecological Statistics, 28(2), 263–285.

- Wu, H., Hao, Y., Ren, S., Yang, X., & Xie, G. (2021). Does internet development improve green total factor energy efficiency? Evidence from China. Energy Policy, 153, 112247.

- Xu, S., & Gao, K. (2022). Green finance and high-quality development of marine economy. Marine Economics and Management, 5(2), 213–227. https://doi.org/10.1108/MAEM-01-2022-0001

- Yang, X., Su, X., Ran, Q., Ren, S., Chen, B., Wang, W., & Wang, J. (2022). Assessing the impact of energy internet and energy misallocation on carbon emissions: New insights from. China. Environmental Science and Pollution Research, 29(16), 23436–23460.

- Yang, X., Wang, W., Wu, H., Wang, J., Ran, Q., & Ren, S. (2021). The impact of the new energy demonstration city policy on the green total factor productivity of resource-based cities: Empirical evidence from a quasi-natural experiment in China. Journal of Environmental Planning and Management, 66(2), 293–326. https://doi.org/10.1080/09640568.2021.1988529

- Yu, C. H., Wu, X., Zhang, D., Chen, S., & Zhao, J. (2021). Demand for green finance: Resolving financing constraints on green innovation in China. Energy Policy, 153, 112255.

- Zhang, D., Mohsin, M., & Taghizadeh-Hesary, F. (2022). Does green finance counteract the climate change mitigation: Asymmetric effect of renewable energy investment and R&D. Energy Economics, 113, 106183.

- Zhang, J., & Ke, H. (2022). The moderating effect and threshold effect of green finance on carbon intensity: From the perspective of capital accumulation. Complexity, 2022. https://doi.org/10.1155/2022/4273691

- Zhang, J., Zeng, W., Wang, J., Yang, F., & Jiang, H. (2017). Regional low-carbon economy efficiency in China: Analysis based on the super-SBM model with CO2 emissions. Journal of Cleaner Production, 163, 202–211.

- Zhang, S. (2015). Evaluating the method of total factor productivity growth and analysis of its influencing factors during the economic transitional period in China. Journal of Cleaner Production, 107, 438–444.

- Zhao, C., Taghizadeh-Hesary, F., Dong, K., & Dong, X. (2022). Breaking carbon lock-in: The role of green financial inclusion for China. Journal of Environmental Planning and Management, 1–30. https://doi.org/10.1080/09640568.2022.2125368

- Zhou, H., & Xu, G. (2022). Research on the impact of green finance on China’s regional ecological development based on system GMM model. Resources Policy, 75, 102454.

- Zhu, Y., Zhang, J., & Duan, C. (2022). How does green finance affect the low-carbon economy? Capital allocation, green technology innovation and industry structure perspectives. Economic Research-Ekonomska Istraživanja, 1–23. https://doi.org/10.1080/1331677X.2022.2110138