?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

We examine the relationship between firm leverage and firm-level labour shares by using the panel threshold effect model. Based on the sample of Chinese firms listed in the Shanghai Stock Exchange (SHSE) and the Shenzhen Stock Exchange (SZSE) from 2010 to 2019, we find that leverage has a significant threshold effect on the labour share of firms, and on average, firm leverage is positively associated with the labour share when the debt per labour is less than 640,000 CNY (approximate 89,600 USD). When the firm leverage exceeds the threshold, firm leverage is negatively associated with labour share. We also find significant heterogeneity over state-owned enterprises (SOEs) and non-state-owned enterprises (non-SOEs), capital-intensive firms and labour-intensive firms, firms with different levels of financial constraints and firms in different life cycles. We contribute to prior literature by revealing the nonlinear association between leverage and firm-level labour share. Therefore, various policies (e.g. made credit policy to restrict lending to firms without sustainable profitability) must be implemented to increase the labour share of enterprises as well as achieve the higher-quality development of the economy in the long term.

1. Introduction

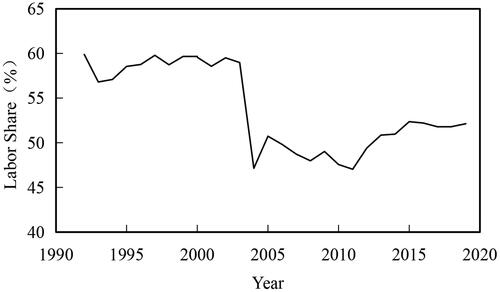

Labour share is defined as the share of gross value-added paid to labour, with broad implications for shaping production function, social justice and macroeconomic dynamicFootnote1 (Autor et al., Citation2017; Hu et al., Citation2020; Karabarbounis & Neiman, Citation2014). The labour share has significantly declined in the large majority of countries along with great advances in information technology and the computer age, and this puzzle has aroused growing concern for scholars and policy-makers in discussing the causes and consequences of labour share dynamic in macro- and micro-levels (Brooks et al., Citation2021). As can be seen in , China’s labour share, as well as its decline, may lead to a widening income gap and a decrease in residents’ disposable income, which is detrimental to long-term economic growth and socio-political stability. Before joining the WTO (i.e. before 2001), the Chinese capital market was underdeveloped, and the operating profits of enterprises were generally low. Moreover, the number of employees was large. Thus, the labour share accounted for a large proportion. Beyond 2001, after China’s accession to the WTO, the degree of economic openness was improved. Chinese firms further increased their capital returns by introducing advanced technologies, and the labour share declined rapidly. Since 2012, to achieve the development goal of common prosperity for all people, China implemented the minimum wage system, which has led to the continuous increase in China’s labour share (Zhan et al., Citation2020).

Graph 1. The trend of labour share in China.

Given the strong desire of researchers to understand the foundations of labour share dynamics, there is an active stream of literature on the causes of its decline from different perspectives. Various explanations have been offered at the macro- level, such as the stage of economic development (Hur, Citation2021), industrial structure evolution (Dong et al., Citation2021), globalization or foreign trade (Hu et al., Citation2020), minimum wage regulation (Zhan et al., Citation2020), and fiscal policy (Bing Li et al., Citation2021). Another stem of works discusses the determinations of labour share from micro- perspectives, such as technological progress bias or capital deepening (Karabarbounis & Neiman, Citation2014; Kehrig & Vincent, Citation2021), labour-management bargaining power (Brooks et al., Citation2021), financial constraints (Harrison & McMillan, Citation2003), and enterprise informatization (Dong et al., Citation2021) are linked with labour share dynamics.

Studies have discussed the linear relationship between firm-specific contexts. For instance, Dong et al. (Citation2021) find that labour share is negatively associated with firm debt. Highly leveraged firms are more likely to default and experience stock price crash, thus leading to a disruption in the financial market. Moreover, Kini et al. (Citation2017) argued that high leverage leads to a lack of investment in product quality. However, some studies have shown that appropriate corporate debt is beneficial for maintaining sufficient liquidity to improve corporate performance (Sinaga et al., Citation2019). Bartoloni (Citation2011) argued that debt financing is required when internal resources are not sufficient to cover long-term projects. Choi et al. (Citation2016) proposed that debt becomes a vital instrument in directing innovation along the optimal trajectory while preventing the balance from shifting too far towards suboptimal investments. They highlight the positive role of debt in the long-term development of the firms in greater depth. In this regard, firm leverage acts as a double-edged sword in promoting firm growth (Tao et al., Citation2017). However, the threshold effects of leverage on the specific behaviour of firms have received limited attention. As such, this matter will be discussed in the current study.

Our work fills this gap in the literature by providing evidence that an inverted U-shaped nonlinear relationship exists between firm leverage and labour share. Given that leverage can stimulate firm investment and capital accumulation (Campello, Citation2006), a reduction in the leverage ratio could stimulate capital deepening (Tao et al., Citation2017), thus leading to dynamics in the labour share. The primary purpose of this article is to estimate empirically the non-linear relationships between firm leverage and labour share and put forward a dimension of understanding the causes of labour share dynamics at the firm level. Based on the sample of Chinese firms listed in the Shanghai Stock Exchange (SHSE) and the Shenzhen Stock Exchange (SZSE) from 2010 to 2019, we find that firm leverage is positively associated to the labour share when the debt per labour is less than 640,000 CNY (approximate 100,000 USD). When the firm leverage exceeds the threshold, firm leverage is negatively associated with labour share. We also find significant heterogeneity over non-state-owned and state-owned firms, capital-intensive firms and labour-intensive firms, firms with different levels of financial constraints and firms in different life cycles.

The contributions of this study are as follows. Firstly, to the best of our knowledge, ours is the first empirical study to examine the relationship between leverage and labour share at the firm level. Despite the academic and policy importance of the subject, few empirical works have used data at the firm level to discuss the association between micro-level factors and the dynamics of labour share. Prior works have examined the determinations of labour share at the macro- or meso-level. For instance, Brooks et al. (Citation2021) found that market power lowers labour’s share of income. Furthermore, Bing Li et al. (Citation2021) revealed that falling corporate income taxes could have contributed to the global decline in the labour share. Hence, we systematically explain the basic mechanism of leverage affecting labour share from the perspective of overall and enterprise heterogeneity and provide theoretical support for deleveraging and stabilising leverage to optimise income distribution and increase labour share.

Secondly, we contribute to the literature on firm leverage. Although a rich body of literature has examined the effects of firm leverage on investment, innovation, CSR, employment and risk-taking (Choi et al., Citation2016; Demirhan & Aldan, Citation2021; Tao et al., Citation2017), the threshold effects of leverage on the specific behaviour of the firms have received limited attention. Literature on corporate finance also suggests that firms use debt strategically to affect the decisions of competitors, clients and suppliers (Campello, Citation2006; Choi et al., Citation2016; Harris & Bromiley, Citation2007; Kini et al., Citation2017). Most of the findings involve the linear effects of leverage on firm decisions. While debt financing can help to meet urgent development needs, such as infrastructure, much of the current debt wave is taking riskier forms (de Jong et al., Citation2011). To make the debt sustainable and affordable, maintaining productivity growth, which drives economic growth in the long run, has become increasingly important for all economies (Song & Zhou, Citation2020). We contribute to this literature by drawing attention to an understudied yet important outcome—labour share. This distinction is notable, as changes in labour share can have a disparate trajectory than wages (Karabarbounis & Neiman, Citation2014). The findings of this study have several implications for implementing stable leverage and structural deleveraging policies in the context of deleveraging and provide important references for optimising the income distribution pattern in the same context (Dong et al., Citation2021).

Thirdly, we focus on the threshold effect of leverage on firm-level labour share in Chinese listed firms by establishing a panel threshold model. Rather than examining the linear relationship between specific factors and labour share (Dong et al., Citation2021; Young & Lawson, Citation2014; Young & Zuleta, Citation2017), we find a nonlinear association between leverage and firm-level labour share, which significantly contributes to research on labour share. We determine the threshold for the impact of leverage on labour share of the firms. Furthermore, we examine the different impacts of leverage on firm-level labour under different property rights, factor intensity, financial constraints and life cycle to shed more light on the mechanisms of the influence of firm leverage on labour share. Our work explores the reasonable range of firm leverage and provides empirical evidence for the government to formulate differentiated industrial and monetary policies. In this regard, structural deleveraging policies should be adopted to realise social justice and economic recovery.

2. Literature review and hypothesis

2.1. Theoretical foundations of labour share dynamics

Early literature under the assumptions of perfect market competition and the absence of technological change reveals that the capital-output ratio remains constant, as does labour share within the neoclassical framework. In the Cobb–Douglas production function, the labour share is equal to the output elasticity of labour; even considering self-employed income, no difference is observed in the labour share varying across time and countries (Gollin, Citation2002). As long as the technological improvement and human resource are upgrading, the labour share will remain constant (i.e. so-called ‘stylised facts’ of balanced economic growth). However, the significant decline in the labour share in recent years evidently contradicts the so-called stylised fact that the capital-output ratio remains constant in equilibrium, as does labour share (Barkai, Citation2020). As changes in relative factor prices tend to be similar across firms, lower elasticity, i.e. below unity and lower relative equipment prices, should lead to greater capital adoption and falling labour shares in all firms. Some research shows that rising trade (e.g. OFDI) is associated with labour share dynamics in emerging countries (Hu et al., Citation2020). While other research also reveals that labour shares have significantly declined in most domestic industries (i.e. non-traded sectors), such as retail, utilities and wholesale, we cannot simply link the dynamics of labour share with the global economy (Autor et al., Citation2017).

To explain the decline of labour share, recent studies have focused on some micro evidence such as the influences of tax reform on the dynamics of labour share (Bing Li et al., Citation2021). Firms promote investing in physical assets and bank borrowing while keeping their employment unchanged in response to the tax cut. In explaining the effect of firm size on the reallocation of activity, Van Reenen et al. (Citation2020) emphasise the role of firm heterogeneity in labour share dynamics. Brooks et al. (Citation2021) find that monopsony power significantly lowers labour’s share of income. Meanwhile, technology advancement may also strengthen the network effects of firms with specific intellectual property capital and bargaining power in adopting and exploiting new production, which in turn influences labour share dynamics (Koh et al., Citation2020). In addition, unions may play an essential role in the distribution of income and affect labour share in the US (Young & Zuleta, Citation2017). Above all, we should reconsider the role of firm heterogeneity in the dynamics of the aggregate labour share.

2.2. Research on firm leverage

Prior literature has effectively documented three theories that are relevant to the discussion of the leverage (or capital structure) of firms: agency theory, pecking order theory and trade-off theory (Chen et al., Citation2012; Tan et al., Citation2021; Tong, Citation2011). These arguments are built on diversified hypotheses in relation to which research positions itself and specific contexts.

Agency theory is premised on the idea that an agent-type relationship exists between managers and shareholders—managers are required to behave in the interest of the shareholders (Jensen & Meckling, Citation1976). However, managers may seek a range of personal benefits (e.g. managerial entrenchment, higher compensation and luxury offices) and secure assets or cash flow (Chen et al., Citation2012), and the perfect monitoring mechanism remains an unattainable goal. Recent research within the framework of the principal-agent conflict shows that managers will also deter firm value or transfer assets through some mechanism, such as affecting cash holding and overinvestment (Zhang et al., Citation2021).

Based on trade-off theory, firms make decisions on the optimal capital structure by balancing the benefits (e.g. tax-deductibility) and costs of taking on additional debt (e.g. interest expense or borrowing costs) (Abel, Citation2018). Borrowing costs are associated with the optimal marginal gain, which balances the cost of debt of bankruptcy costs and conflict of interest between shareholders and bondholders (Brogaard et al., Citation2017). Further research on targeted leverage also reveals that firms can maximise their value by considering the static trade-off phase (during which firm theory operates under the assumptions of the theory mentioned above for a specific period, for example, one year) and the dynamic trade-off phase (which allows successive adjustment steps by which a firm seeks to achieve the target debt level gradually) (Tao et al., Citation2017). Above all, firms will borrow up to the point where the marginal value of the tax advantage of debt is balanced by the increase in the present value of bankruptcy costs.

Pecking order theory posits that the order of resources prevails over their size (Myers & Majluf, Citation1984). Given the information asymmetry and costs of issuing new securities, firms prefer self-financing to external funds; even when outside finance is necessary, firms prefer debt to equity (Frank & Goyal, Citation2003). The preference expressed by companies for financing their projects is characterised by a reassessment of the preference: retained earnings, equity and, finally, long-term debt. de Jong et al. (Citation2011) also revealed that the pecking order yields debt issuance until the debt capacity is reached, which is a better predictor of firms’ issue decisions.

2.3. Leverage and labour share

The limited financial resources can subsequently be allocated to businesses with sustained profitability, thereby facilitating their transformation, upgrading and high-quality development. In turn, structural deleveraging will enhance China’s sustainable economic development by laying the groundwork and providing assistance for financial risk avoidance and reduction. In discussing how to implement structural deleveraging policies, Xie (Citation2019) contended that creditors (e.g. commercial banks and other financial institutions) will rationally select enterprises with sustainable profitability to stabilise or even raise leverage when their risk is under control. Additionally, they will opt to reduce the leverage of firms without sustainable profitability.

At the micro-level, high leverage refers to the asset allocation problem caused by the high proportion of debt funds, which increases enterprises’ financial cost and debt risk, weakens the investment capacity and reduces the efficiency of enterprise capital use. Higher leverage at the macro-level (e.g. high proportion of total debt to GDP) could also trigger systematic risk. According to China National Balance Sheet 2020 published by the Chinese Academy of Social Sciences, as of the end of 2019, the leverage ratio of China’s non-financial corporate sector was as high as 151.3%, higher than that of the financial sector, the residential sector and the government sector. Moreover, high leverage has become a potential threat to the sustainable and benign development of the Chinese economy. Therefore, structural deleveraging based on market-based principle has been one of the core duties of regulators.

However, prior studies also show that the relationship between leverage and economic impact is mixed (Campello, Citation2006; Croce et al., Citation2019; Dong et al., Citation2021). The influence of leverage on the labour income may differ at diversified contexts and institutional environment. According to trade-off theory, a moderate leverage ratio can increase corporate capital flows and bring tax benefits to firms (Abel, Citation2018). As the leverage ratio increases, the risk of corporate bankruptcy increases. Hence, an optimal leverage ratio that maximises corporate efficiency exists. As such, does an optimal leverage ratio or leverage interval that maximises the labour share of the firm exist?

Moderate leverage can increase the labour income share of firms through several paths. Financial deepening theory suggests that credit growth and external debt financing can positively affect economic development through investment and income effects (Levine, Citation2005). Firstly, a moderate leverage ratio can exert a financial leverage amplification effect. Usually, the marginal cost of capital of debt financing is lower than that of equity financing. Thus, debt financing becomes the primary way of temporary financing for enterprises. Debt financing can increase the short-term cash flow of enterprises, relieve the pressure of enterprise financing constraints, optimise investment decisions and increase the enthusiasm of enterprise fixed asset investment and R&D investment. The increase in enterprise investment helps expand production scale, which, on the one hand, can improve profitability by improving an enterprise’s business performance, which in turn improves labour compensation (Dong et al., Citation2021). On the other hand, the increase in investment can drive employment and increase labour force hiring, thus causing the share of labour income to rise rapidly. Secondly, moderate leverage has a signalling effect. Given the information asymmetry between managers and external investors, companies can send positive signals to the outside world through good financial information, which in turn can obtain more investments from creditors and help to improve employee welfare while enhancing business conditions (Bergh et al., Citation2018; Colombo, Citation2021; Connelly et al., Citation2010). Thirdly, moderate leverage increases the share of corporate labour income by optimising the allocation of financial assets. Moderate corporate indebtedness will weaken the incentive to invest in financial assets and use more funds for real operations, such as purchasing advanced machinery and equipment, which will further drive the demand for labour and increase the share of corporate labour income (Brooks et al., Citation2021; Kehrig & Vincent, Citation2021).

However, excessive leverage will also reduce the labour share of firms. Firstly, high leverage increases the reinforcing effect of financial capital on tangible capital, thus making firms adopt more capital-intensive production methods. The direct result of the shift in production methods is that capital replaces labour, wage income decreases and the share of corporate labour income decreases. Karabarbounis and Neiman (Citation2014) noted that technological progress during economic transformation tends to show a ‘capital bias’ against resource endowment, which leads to an increase in the capital income share and a decrease in the labour income share. Secondly, high leverage can depress firms’ labour income share by weakening bargaining power. High leverage implies that firms have more investment and more elastic labour demand (Brooks et al., Citation2021) and higher cost markups in the Kaleckian framework, both of which can reduce labour income shares by reducing workers’ bargaining power. In addition, when firms’ debt levels are too high and liquidity tightens, firms are under pressure to cut costs, which can increase the bargaining power of firms in bargaining with labour, by actively lowering labour wages and thus reducing firms’ labour income share (Campello, Citation2006). Thirdly, high leverage increases firms’ risk and thus reduces the share of labour income. When a firm has too much debt, the uncertainty faced by the firm increases, and the level of firm risk rises, which will reduce the level of labour effort; furthermore, both output levels and wages will fall, thus negatively affecting the labour income share (Dong et al., Citation2021). Xie (Citation2019) argued that the proper implementation of the market-based structural deleveraging will promote the transformation and upgrading of China’s companies and economy towards higher-quality development. Therefore, we propose:

Hypothesis 1: Firm leverage is associated with labour share.

2.4. Firm heterogeneity

Prior research always adopts a conservative view that firms should reduce financial risks by restraining the scale of bank loans and adjusting capital structure (Dong et al., Citation2021). However, deleveraging may lead to more serious financing constraints for specific firms, which causes some negative impact on economic growth. As discussed above, when risk is under control, companies with sustainable profitability should be permitted to stabilise or even increase their leverage, whereas companies without sustainable profitability and growth abilities (e.g. zombie companies) should be required to reduce their leverage, undergo reorganisation or even be liquidated. The limited financial resources may subsequently be allocated to businesses with sustained profitability, thereby facilitating their high-quality development and the adjustment of the labour share. We argue that standardising corporate financing and reducing the leverage ratio should be adopted by considering the heterogeneity of firms, which further extends the non-linear relationship between leverage and labour share of the firms.

Compared with non-SOEs, SOEs generally suffer from high operating risks, overcapacity and excessive inventories, thus leading to low operating efficiency and severe efficiency losses (Nee, Citation1992; Sun et al., Citation2021). As long as ownership and management are separated in SOEs, agency problems arise because managers of SOEs may take advantage of their positions as agents and exploit personal gain at the expense of principals’ interests, thus leading to over-debt among SOEs (Zhou et al., Citation2017). SOEs are influenced by the implicit government guarantee and have easy access for the allocation of capital (Tsafack et al., Citation2021). Thus, their overall debt level is relatively higher, and their optimal leverage ratio will be higher than that of non-SOEs. Conversely, facing the same leverage level within a reasonable range of liabilities, non-SOEs have more efficient use of capital and a more reasonable capital structure. Thus, the contribution to labour share is more substantial than that of SOEs. Moreover, compared with SOEs that run with state socialism logics (e.g. contribute to social welfare), non-SOEs are driven by market logics and economic efficiency (Greve & Zhang, Citation2017). Hence, easier access to external resource (e.g. credit support) can increase their labour income share more quickly.

Apart from the heterogeneity of property rights (L. H. Fang et al., Citation2017), we also discuss the other aspects of firm chrematistics in influencing the association between the leverage and labour share of firms. Unlike labour-intensive firms, capital-intensive firms have a higher share of capital. Within a reasonable range of leverage, firms with substantial capital reserves are more inclined to expand investment and production to obtain returns to scale. In addition, their demand for labour is more vital, thus allowing them to increase their labour income share more quickly. In general, capital-intensive firms have higher capital-to-labour ratios, require more significant financing to maintain normal operations and thus have higher optimal leverage to promote the labour income distribution than labour-intensive firms. Compared with firms with high financing constraints, firms with low financing constraints are more likely to obtain bank loans to form working capital, which can increase labour hiring or raise employee wages and, subsequently, labour income shares. In addition, low financing constraint firms have more guaranteed employee benefits, which make them more attractive to workers, and the increase in labour income share is relatively more significant. Growing enterprises will face difficulties in financing, and promoting the increase of labour income share through moderate debt is not vital. In the maturity period, the performance of enterprises continues to improve, and the financing channels are diversified. To expand the scale of enterprises to obtain scale payoffs further, enterprises will increase investment in fixed assets and hire more human capital, which will, in turn, lead to a higher labour income share. In the recession period, although the financial situation of enterprises is poor, they have more stable financing sources by relying on the scale advantage. Thus, they have a stronger incentive to retain talents by raising the wages of employees through debt, and the labour income share will increase. Through the comprehensive analysis of the above, this study puts forward the following hypotheses.

In summary, we argue that there is the heterogeneity in the relationship between leverage and labour share of the firms—property rights, factor intensity, financial constraints, and life cycle—to shed more light on the standardizing corporate financing and reducing the leverage ratio.

3. Research design

3.1. Sample

This study developed a unique panel dataset of Chinese firms listed in the A-share of the Shanghai Stock Exchange (SHSE) and the Shenzhen Stock Exchange (SZSE) from 2010 to 2019. Since 2010, the China Securities Regulatory Commission (CSRC) has obligated listed firms to disclose salary and other labour information in detail, which provides a basis for our study. Hence, our sample starts from 2010. The data are obtained from the China Securities Markets and Accounting Research Database (CSMAR) and the RESET database (RESSET). Following prior studies (Dong et al., Citation2021; H. Fang et al., Citation2017; Wang et al., Citation2021), we excluded samples with incomplete data, abnormal value (e.g. labour share is above 1)Footnote2, ST/ST* companies and financial firms. We winsorized all continuous variables at the 1% and 99% levels.

3.2. Model setting

This paper first empirically tests the threshold effect of firm leverage on labour share. According to Hansen (Citation1999), we set model as follows:

(1)

(1)

Or it can be presented as another functions as follows:

(2)

(2)

where i is the individual, t is the time, εit is a random disturbance term. We assume that εit obeys a finite independent identical distribution with mean zero and variance σ2 (i.e.

). The variable LS it is labour share of the firms. Lev it is the firm leverage (i.e. threshold variable). Xit refers to sets of control variables and βi is coefficient. λ is the threshold value of firm leverage (

). I is the indicative function, when

I = 1, otherwise, I = 0. Obviously, when Lev it is less than the threshold value λ, the influence of firm leverage on labour share is

On the contrary, when the Lev it is greater than λ, the influence of firm leverage on labour share is

Based on the determination of the existence of threshold effects, we further discuss the existence of two or more thresholds. In this paper, a two-threshold model is used as an example (as Equationequation (3)(3)

(3) , and other models can be set up as follows:

(3)

(3)

3.3. Variables

3.3.1. Dependent variable

Labour share is defined as the share of gross value-added paid to labour, while it is always calculated by the proposition of total wage in value-added (Karabarbounis & Neiman, Citation2014). In our paper, labour share (LS_1) is measured by employees’ total compensation divided by the value-added by GDP method, where value-added is the sum of: (1) employees’ total compensation, (2) operating surplus, (3) depreciation of fixed assets, and (4) net production tax (Bing Li et al., Citation2021).

Specifically, employees’ total compensation refers to the income of the employees. We adopt ‘cash paid to and for employees’ in the cash flow statement of listed companies to calculate employees’ compensation, including actual wages, bonuses, various allowances and subsidies paid to employees in the current period, as well as pension insurance, unemployment insurance, supplementary insurance, housing fund, housing hardship allowance paid to employees, and expenses paid to retirees. When calculating value-added, operating surplus is the total profit of the firms. Depreciation of fixed assets can be obtained from ‘Fixed assets, accumulated depreciation, and provision for impairment’ in the financial statements of listed firms. The net amount of production tax is calculated as ‘business tax and surcharge’ pluses ‘value-added tax’, and subtracts ‘government subsidies’. We also use another four alternative ways to measure labour share in robustness tests.

3.3.2. Independent variable

Firm leverage (Lev) is calculated by debt per worker—the ratio of a firm’s total debt to the number of employees (unit: billion CNY/person) (Autor et al., Citation2017; Dong et al., Citation2021). Debt per worker eliminates the effect of firm size on debt, reflecting the essential power balance between owner and workers, which is an important channel through which firm debt can affect the share of labour income (Dong et al., Citation2021). In addition, this paper also uses interest expense per worker to measure it in robustness tests (Autor et al., Citation2017).

3.3.3. Control variable

We also included some control variables. Size was measured by the natural logarithm of total assets (Zhou et al., Citation2017). Age was measured by the number of years since the firm’s incorporation (Yang et al., Citation2020). Roa was measured by dividing the net profit by the total return on total assets of the firm (Wang et al., Citation2021). Rfa is measured by the ratio of the fixed asset to total assets (He & Tian, Citation2013; Zhang, Citation2017). Ca is measured by liquid assets scaled by total assets (Hu et al., Citation2019; Lyandres & Palazzo, Citation2016). Total factor productivity (Tfp) is calculated using the LP method (Li et al., Citation2018; Yi et al., Citation2017). Financial constraint (Sa) is measured by using the SA index (Hyytinen & Toivanen, Citation2005). Firm ownership (Own) is a dummy variable while it is equal to 1 for state-owned enterprises, otherwise 0 (Xie et al., Citation2022).

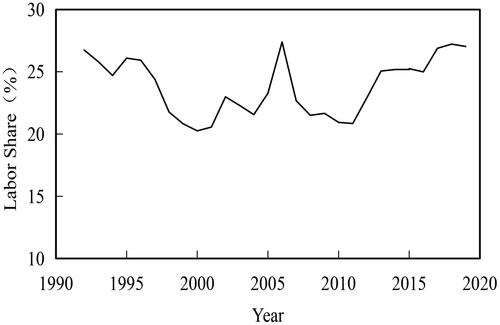

shows the results of descriptive statistics. The mean values of the labour share of listed firms measured by GDP method and factor method are 22.60% and 26.22%, respectively, which is very close to the share of labour compensation in GDP of non-financial enterprise sector of 24.63%, as shown in . The mean value of enterprise leverage is 0.0243, which means that the average labour debt of listed enterprises is 2.43 million CNY, and the maximum and minimum values are 50,000 CNY and 40.44 million CNY, respectively, with large differences in leverage among enterprises.

Graph 2. Labour share in non-financial sectors.

Table 1. Descriptive statistics.

4 Results

4.1. Threshold-effect test

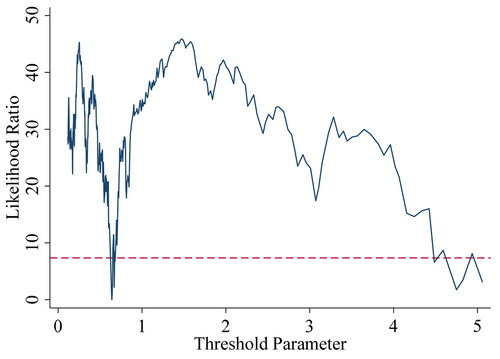

If there are multiple thresholds (that is, multiple regimes), we fit the models sequentially (Wang, Citation2015). First, we directly fit a triple-threshold model, then the double-threshold. Finally, we fit a single-threshold model while testing for a threshold effect is the same as testing for whether the coefficients are the same in each regime (Wang, Citation2015). reports the results of the threshold tests. It can be found that both of the coefficients of triple and double threshold models are insignificant, and the coefficients of single threshold model is significant at 1% level, so single threshold model can be used in our analysis. represents the plot of the single-threshold effect model.

Graph 3. Threshold parameter graph.

Table 2. Threshold tests (bootstrap = 300).

4.2. Benchmark regression

presents the results of our main regression. The coefficient of the firm leverage (Lev(th ≤ λ = 0.0064)) is 1.9347, thus suggesting that a 10,000 CNY (approximate 1,400 USD) rise in the firm leverage per worker leads to a decrease of approximately 2 percentage points in labour share when firm leverage (debt per worker) is less than 640,000 CNY (approximate 89,600 USD). This value is statistically significant at the 1% level, thus indicating that firm leverage is positively associated with labour share when the firm leverage is less than the threshold value. When firm leverage (debt per worker) is more than 640,000 CNY (approximate 89,600 USD), the coefficient value of firm leverage (Lev(th > λ = 0.0064)) is negative and significant at the 1% level, thus indicating that when the firm leverage exceeds the threshold value, firm leverage is negatively associated with labour share. The results suggest an inverted U-shaped correlation between firm leverage and labour share.

Table 3. Analysis of leverage and labour share of the firms.

Meanwhile, firm size (Size) and firm age (Age) are both positively linked with labour share, which means that with the increase of production efficiency and profitability, the income of employees increases significantly, and the labour share rises steadily. Profitability (i.e. Return on Assets, Roa), fixed asset ratios (Rfa), current assets ratio(Ca), total factor productivity (Tfp) and financial constraint (Sa) are negatively associated with labour share. The estimated coefficient of Roa is significantly negative, thus indicating that the stronger the profitability of the enterprise is, the more unfavourable the increase of the labour income share will be, which reflects that the current capital factor owners have stronger control power and influence of the firms, weaken labour bargaining power and can obtain more remuneration from the growth of the enterprise. A significant negative correlation exists between the Rfa and labour share, thus indicating that the increase of fixed assets, such as machinery and equipment, may crowd out labour input, thus leading to a decline in the labour share. A significant negative link also exists between Tfp and labour share, thus indicating that capital gains obtained by enterprises relying on technological innovation will significantly increase. Meanwhile, labour share will decrease. The higher degree of financing constraint (Sa) will lead to the reduction of cash flow, and the enterprise may reduce employee wages or labour employment, which will lead to the decline of labour share. The estimated coefficient of firm ownership (Own) is negative but insignificant. However, firm heterogeneity on firm ownership (SOE vs. non-SOE) will be analysed later.

4.3. Robustness test

We opt for several tests to check the robustness of the results. Firstly, we redefined the dependent variable (labour share) while using four alternative ways to measure labour share. Specifically, LS_2 is measured by the employees’ total compensation divided by the sum of employees’ total compensation, operating surplus and depreciation of fixed assets (i.e. income method). The net production tax is removed from the value-added tax because this indicator is just a government share of national income but not linked with GDP. LS_3 is measured by the amount of employee compensation payable divided by the total operating income. LS_4 is measured by the sum of the cash payments to and on behalf of employees and employee compensation payable divided by the total operating income. LS_5 is measured by cash payments to and on behalf of employees at the end of the year. The regression results in Model 1 to Model 4 of show that the key results remain qualitatively unchanged, thus supporting our hypothesis above.

Table 4. Robustness tests.

Secondly, we redefined the independent variable while using interest expense per worker (Interest_Exp) as a proxy to measure firm leverage (Autor et al., Citation2017). Interest expense (i.e. interest payable) includes the interest accrued by the enterprise on long-term loans, bonds payable and other long-term liabilities that pay interest on schedule and repay the principal on schedule. The regression results in Model 5 of show that the coefficient is significantly positive at the 1% level when the average labour interest expense is less than 328 CNY (approximate 45.92 USD), thereby indicating that the labour income share increases as the average labour interest expense increases. When the interest expense per worker is greater than this threshold, the estimated coefficient is negative but insignificant, which may be due to the loss of sample size and supports our benchmark regression.

Thirdly, considering that the simultaneity issue (i.e. reverse causality) may also influence our findings (Hill et al., Citation2020; Xu et al., Citation2021), we used a lagged version of the endogenous variable and re-estimated the main models. The regression results in Model 6 of show that the lagging form of firm leverage (L.Lev) is still significant and consistent with our benchmark regression.

Fourthly, given that the excluded samples for firms’ labour share are above 1 due to abnormal value (i.e. due to negative operating surplus, we use a full sample, which includes firms’ labour share with a value above 1. The results of Model 7 of remain robust.

Finally, we also use alternative models and re-estimate our sample. Firstly, we divide our sample into low leverage and high leverage groups based on the median leverage (Lev) in the initial year of the sample (i.e. firm leverage in 2010) and re-run the fixed effect model for analysis. Although artificially dividing the intervals has some drawbacks, it is an appropriate aid to test the robustness of the regression results. As shown in column (1) of , the coefficient of firm leverage (Lev) in the low leverage group is 0.0597 and significant at the 1% level, thus indicating that moderate leverage can promote the labour share of the firm. In column (2) of , the coefficient of firm leverage (Lev) in the high leverage group is −0.1282 and significant at the 1% level, thus indicating that excessive leverage has a suppressive effect on the firm’s labour income share. Secondly, considering the potential inverted U-shaped relationship between firm leverage and labour share, we regress the dependent variable (LS_1) on the independent variable (i.e. Lev) and its square (i.e. Lev2) in our model (Haans et al., Citation2016). In column (3) of , the coefficient of the squared term of firm leverage (Lev2) is negative and significant at the 5% level, thus suggesting the inverted U-shaped relationship between firm leverage and labour share. Thirdly, we also use one-year lagged firm leverage variable (Lev) as instrumental variables (IVs) based on the view that the events and decisions related to these variables occurred in the past and are not correlated with the error term in the present. The two-stage least squares (2SLS) empirical test in column (4) of shows that the coefficient of the squared term of firm leverage (Lev2) remains significantly negative, which further supports the inverted U-shaped relationship between firm leverage and labour share. Moreover, this relationship is highly robust. The results of these tests support the findings of the benchmark regressions.

Table 5. Analyses for dividing samples and including the squared term of the independent variables.

5. Further analysis

In this section, we explore the potential heterogeneity in four critical dimensions of firm characteristics—property rights, factor intensity, financial constraints and life cycle—to shed more light on the mechanisms of the influence of firm leverage on labour share.

5.1. Heterogeneity of property rights

We expect firm leverage to have different impacts on labour share in SOEs and non-SOEs (Arocena & Oliveros, Citation2012; Chen, Citation2020; Kong et al., Citation2020; Zhou et al., Citation2017). This study divides the sample firms into state-owned and non-state-owned enterprise groups according to the nature of their property rights for separate regressions (Bin Li et al., Citation2021). The estimation results in column (1) of show that the coefficient of firm leverage is significantly positive at the 5% level when the firm leverage is less than 650,000 CNY (approximate 91,000 USD). When the firm leverage is greater than the threshold, the coefficient of firm leverage is negative and significant at the 1% level, thus indicating that the excessive debt of SOEs has a suppressive effect on the labour share, which is consistent with the basic regression.

Table 6. Heterogeneity analyses.

Comparing the magnitude of the thresholds, the threshold value of the firm leverage of SOEs is higher than that of non-SOEs and the full sample (0.0065 > 0.0064). These findings may due to the larger size of SOEs and their greater propensity to raise debt. In addition, SOEs usually have government backing and are more likely to have access to large-scale financing, which leads to a higher stationing point for the effect of corporate leverage on labour share.

In column (2) of , the estimated coefficient of firm leverage is positive and significant at the 1% level when the firm leverage is less than the threshold, and the contribution of moderate debt raising to labour share is stronger for non-SOEs compared with SOEs (2.3981 > 1.5871), which reflects a possible efficiency loss problem for SOEs. The estimated coefficient of firm leverage is negative but insignificant when firms’ leverage is greater than the threshold. These findings may be due to stronger demand for labour and capital investment contracts of non-SOEs when their debt levels become higher. In turn, this outcome leads to an insignificant decline in the labour share.

5.2. Heterogeneity of factor intensity

Secondly, we test for differences in factor intensity. This study uses the logarithm of the ratio of employee compensation to gross operating income to measure labour intensity (Serfling, Citation2016). Firms are classified as a labour-intensive firm group when their labour intensity in 2010 is greater than the median labour intensity of all firms in the sample in that year. Otherwise, they are classified as a capital-intensive firm group.

For labour-intensive firms (column (3) of ), leverage will promote the labour share when their leverage is less than the threshold. However, when the firm leverage is greater than the threshold, the coefficient of firm leverage is positive but insignificant. The possible reason is that capital and labour are complementary for labour-intensive firms. Firms can boost employment and, subsequently, labour share while raising debt financing to expand capital investment. For capital-intensive firms (column (4) of ), the results are consistent with the benchmark regression.

Comparing the results of two groups of coefficients, we find that the coefficient of the firm leverage of capital-intensive firms is bigger and more significant than that of capital-intensive firms (2.8151 > 1.7046). Capital-intensive firms can increase labour hiring and raise employee income levels through investment effects and income effects under the moderate firm leverage. In addition, in terms of the size of the threshold, the optimal leverage of capital-intensive firms is greater than that of labour-intensive firms (0.0067 > 0.0065), which is more consistent with prior works (Autor et al., Citation2017; Kehrig & Vincent, Citation2021).

5.3. Heterogeneity of financial constraints

Considering the differences in financing costs for firms with various financing constraints, this study further examines the impact of differences in financing constraints on the income distribution effect of leverage. This research uses the absolute value of the credit financing constraint index as a proxy for the cost of capital used to group sample firms, and a larger absolute value of this index indicates a higher cost of capital used for the firm. When the financing constraint index of a firm is greater than the median of the financing constraint index of the sample firms, it is classified as a high financing constraint group (column (6) of ). Otherwise, it will be classified as a low financing constraint group (column (5) of ).

Comparing the coefficients of the two groups, when the firm leverage is less than the threshold, the positive influence of leverage on the labour share is weaker in the high financing constrained firms than in the low financing constrained firms (1.9238 < 2.1055). Financing constraint will affect the firm’s labour hiring policy and human resource strategies, either by cutting the use of labour or by compressing the wage level of the existing labour force. In turn, this action will have a certain hindering effect on the labour share.

When leverage exceeds the threshold, excessive indebtedness reduces labour income share for both firms. The threshold is higher for firms with high financing constraints than those with low financing constraints (0.0068 > 0.0064). High financing constrained firms tend to be private SMEs, which have limited access to financing and thus maintain sufficient cash flow to cope with uncertainty. As their debt levels are more tolerant, they can still contribute to the labour income share when corporate debt increases.

5.4. Enterprise life cycle heterogeneity

Firms at different life cycle stages may have some differences due to their various business strategies and resource endowments (Dickinson, Citation2011). As shown in , we divide the sample firms into three groups, namely, growth, maturity and decline, based on the combination of net flows () of operating, investment and financing cash (Dickinson, Citation2011). From the regression results in columns (7)-(9) of , the estimated coefficients are 2.4717, 6.0515, and 6.0705, respectively, when the average labour debt of firms is less than the threshold. The values are all significantly positive at the 5% level, thus indicating that moderate leverage is beneficial to boosting the labour income share of the three types of firms.

Maturing firms will increase investment in fixed assets and hire more human capital, and recessionary firms will retain talent by raising corporate employee wages through debt, both of which will lead to higher labour income shares. Maturing-period firms have fewer employees and are generally faced with the problems of difficult and expensive financing. Thus, the role of promoting labour income share increase through moderate debt is weaker than the previous two. When the firm leverage is greater than the threshold, excessive debt harms all three types of firms, with the estimated coefficients for the growth and recession periods failing the significance level test. The possible reason is that the stronger demand for capital in the growth period offsets the negative effect of high debt on labour share to a certain extent. In the recession period, the firms themselves have higher debt levels. When their employees’ income is at a high level, further leverage may be used by the firms for non-production projects. Thus, the effect on labour share becomes insignificant.

6. Conclusion and implications

This research uses a panel threshold effect model to analyse the relationship between firm leverage and labour share. We find that leverage has a threshold effect on the labour share of firms. On average, firm leverage increases the labour share when the debt per labour is less than 640,000 CNY (approximate 89,600 USD), thus suggesting that moderate firm leverage promotes the labour share. Meanwhile, excessive indebtedness reduces the labour share of firms when the leverage is larger than a specific threshold. We also find significant heterogeneity over non-SOEs and SOEs, capital-intensive firms and labour-intensive firms, firms with different levels of financial constraints and firms in different life cycles. Further investigation suggests that the effects of the moderate leverage (i.e. leverage is lower than threshold) on labour share are more pronounced in non-SOEs, capital-intensive enterprises, low financing-constrained firms and mature and recessionary firms.

Although our findings are derived from the Chinese context, they can be generalised to other countries. Promising avenues for future research include more in-depth investigations into the underlying mechanisms of the leverage on labour share and exploration of evidence from other contexts. In the context of efforts to achieve high-quality economic development, economic growth achieved by relying on financial leverage is unsustainable and prone to systemic financial risks. Our results show that maintaining the leverage ratio at a reasonable range is conducive to improving the income distribution. This outcome implies that the situation is not just a matter of deleveraging (Dong et al., Citation2021) but also that moderate stabilising leverage can help retain liquidity within a reasonable range, ease corporate financing constraints and improve corporate performance.

Meanwhile, differentiated policies should be adopted for various types of enterprises to play the vital role of deleveraging in improving the labour share of firms. In addition to reducing the corporate leverage ratio, the government should also formulate other policies to increase labour share, such as lowering the payroll tax, raising the capital tax or strengthening subsidies to workers. In the context of the progress of information regulation technology and the improvement of social security collection and management ability, we can consider the further reduction of the legal contribution rate of social insurance to make up for the lack of enterprises’ perception of tax and fee reduction policies and their sense of gain to stabilise market expectations and give full play to the redistribution function of social insurance.

Structural deleveraging is an important tool and an institutional arrangement for promoting the transformation and upgrading of firms and economy towards higher-quality development not just for the Chinese background (Xie, Citation2019). Credit policies related to the goal of structural deleveraging should be a market-oriented screening mechanism that leverages entry barriers and loan threshold of specific sectors and encourages incompetent enterprises (e.g. firms without sustainable profitability) that are seeking strategic changes or even diversification. The limited financial resources can then be allocated to firms with sustainable profitability or competitive advantage (e.g. high-tech enterprises), which help the adjustment of labour share, transformation and high-quality development of these companies.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

Notes

1 Serval studies on macroeconomics (e.g., national-level research) also used the term “labour income share” in study this issue.

2 We excluded the firm samples with negative operating surplus (i.e., labour share is more than 1). In prior works, labour share should be among 0 and 1. According to the calculation formula of labour income share, labour share = employees’ total compensation / (employees’ total compensation + operating surplus + depreciation of fixed assets + net production tax). However, if the labour share is above 1 (e.g., due to negative operating surplus), it means that the sample data is abnormal, so it should be deleted. Moreover, we also run robustness test while including firms which labour share is above 1, and results are still robust.

References

- Abel, A. B. (2018). Optimal debt and profitability in the trade-off theory. The Journal of Finance, 73(1), 95–143. https://doi.org/10.1111/jofi.12590

- Arocena, P., & Oliveros, D. (2012). The efficiency of state-owned and privatized firms: Does ownership make a difference? International Journal of Production Economics, 140(1), 457–465. https://doi.org/10.1016/j.ijpe.2012.06.029

- Autor, D., Dorn, D., Katz, L. F., Patterson, C., & Reenen, J. V. (2017). Concentrating on the fall of the labor share. American Economic Review, 107(5), 180–185. https://doi.org/10.1257/aer.p20171102

- Barkai, S. (2020). Declining labor and capital shares. The Journal of Finance, 75(5), 2421–2463. https://doi.org/10.1111/jofi.12909

- Bartoloni, E. (2011). Capital structure and innovation: Causality and determinants. Empirica, 40(1), 111–151. https://doi.org/10.1007/s10663-011-9179-y

- Bergh, D. D., Ketchen, D. J., Orlandi, I., Heugens, P. P. M. A. R., & Boyd, B. K. (2018). Information asymmetry in management research: Past accomplishments and future opportunities. Journal of Management, 45(1), 122–158. https://doi.org/10.1177/0149206318798026

- Brogaard, J., Li, D., & Xia, Y. (2017). Stock liquidity and default risk. Journal of Financial Economics, 124(3), 486–502. https://doi.org/10.1016/j.jfineco.2017.03.003

- Brooks, W. J., Kaboski, J. P., Li, Y. A., & Qian, W. (2021). Exploitation of labor? Classical monopsony power and labor’s share. Journal of Development Economics, 150, 102627. https://doi.org/10.1016/j.jdeveco.2021.102627

- Campello, M. (2006). Debt financing: Does it boost or hurt firm performance in product markets? Journal of Financial Economics, 82(1), 135–172. https://doi.org/10.1016/j.jfineco.2005.04.001

- Chen, X. (2020). The state-owned enterprise as an identity: The influence of institutional logics on guanxi behavior. Management and Organization Review, 16(3), 543–568. https://doi.org/10.1017/mor.2020.14

- Chen, Q., Chen, X., Schipper, K., Xu, Y., & Xue, J. (2012). The sensitivity of corporate cash holdings to corporate governance. Review of Financial Studies, 25(12), 3610–3644. https://doi.org/10.1093/rfs/hhs099

- Choi, B., Kumar, M. V. S., & Zambuto, F. (2016). Capital structure and innovation trajectory: The role of debt in balancing exploration and exploitation. Organization Science, 27(5), 1183–1201. https://doi.org/10.1287/orsc.2016.1089

- Colombo, O. (2021). The use of signals in new-venture financing: A review and research agenda. Journal of Management, 47(1), 237–259. https://doi.org/10.1177/0149206320911090

- Connelly, B. L., Certo, S. T., Ireland, R. D., & Reutzel, C. R. (2010). Signaling theory: A review and assessment. Journal of Management, 37(1), 39–67. https://doi.org/10.1177/0149206310388419

- Croce, M. M., Nguyen, T. T., Raymond, S., & Schmid, L. (2019). Government debt and the returns to innovation. Journal of Financial Economics, 132(3), 205–225. https://doi.org/10.1016/j.jfineco.2018.11.010

- de Jong, A., Verbeek, M., & Verwijmeren, P. (2011). Firms’ debt–equity decisions when the static tradeoff theory and the pecking order theory disagree. Journal of Banking & Finance, 35(5), 1303–1314. https://doi.org/10.1016/j.jbankfin.2010.10.006

- Demirhan, A. A., & Aldan, A. (2021). Financial constraints and firm employment: Evidence from Turkey. Borsa Istanbul Review, 21(1), 69–79. https://doi.org/10.1016/j.bir.2020.07.003

- Dickinson, V. (2011). Cash flow patterns as a proxy for firm life cycle. The Accounting Review, 86(6), 1969–1994. https://doi.org/10.2308/accr-10130

- Dong, F., Shen, G., & Jiao, Y. (2021). Firm debt and labor share: The distribution effect of de-leverage. China Economic Quarterly International, 1(1), 59–71. https://doi.org/10.1016/j.ceqi.2021.01.003

- Fang, H., Bao, Y., & Zhang, J. (2017). Asymmetric reform bonus: The impact of VAT pilot expansion on China’s corporate total tax burden. China Economic Review, 46, S17–S34. https://doi.org/10.1016/j.chieco.2017.02.003

- Fang, L. H., Lerner, J., & Wu, C. (2017). Intellectual property rights protection, ownership, and innovation: Evidence from China. The Review of Financial Studies, 30(7), 2446–2477. https://doi.org/10.1093/rfs/hhx023

- Frank, M. Z., & Goyal, V. K. (2003). Testing the pecking order theory of capital structure. Journal of Financial Economics, 67(2), 217–248. https://doi.org/10.1016/S0304-405X(02)00252-0

- Gollin, D. (2002). Getting income shares right. Journal of Political Economy, 110(2), 458–474. https://doi.org/10.1086/338747

- Greve, H. R., & Zhang, M. C. (2017). Institutional logics and power sources: Merger and acquisition decisions. Academy of Management Journal, 60(2), 671–694. https://doi.org/10.5465/amj.2015.0698

- Haans, R. F. J., Pieters, C., & He, Z.-L. (2016). Thinking about U: Theorizing and testing U- and inverted U-shaped relationships in strategy research. Strategic Management Journal, 37(7), 1177–1195. https://doi.org/10.1002/smj.2399

- Hansen, B. E. (1999). Threshold effects in non-dynamic panels: Estimation, testing, and inference. Journal of Econometrics, 93(2), 345–368. https://doi.org/10.1016/S0304-4076(99)00025-1

- Harris, J., & Bromiley, P. (2007). Incentives to cheat: The influence of executive compensation and firm performance on financial misrepresentation. Organization Science, 18(3), 350–367. https://doi.org/10.1287/orsc.1060.0241

- Harrison, A. E., & McMillan, M. S. (2003). Does direct foreign investment affect domestic credit constraints? Journal of International Economics, 61(1), 73–100. https://doi.org/10.1016/S0022-1996(02)00078-8

- He, J., & Tian, X. (2013). The dark side of analyst coverage: The case of innovation. Journal of Financial Economics, 109(3), 856–878. https://doi.org/10.1016/j.jfineco.2013.04.001

- Hill, A. D., Johnson, S. G., Greco, L. M., O’Boyle, E. H., & Walter, S. L. (2020). Endogeneity: A review and agenda for the methodology-practice divide affecting micro and macro research. Journal of Management, 47(1), 105–143. https://doi.org/10.1177/0149206320960533

- Hu, J., Li, A. T., & Luo, Y. G. (2019). CEO early life experiences and cash holding: Evidence from China’s great famine. Pacific-Basin Finance Journal, 57, 101184. https://doi.org/10.1016/j.pacfin.2019.101184

- Hur, J. (2021). Labor income share and economic fluctuations: A sign-restricted VAR approach. Economic Modelling, 102, 105546. https://doi.org/10.1016/j.econmod.2021.105546

- Hu, X., Wan, G., & Wang, J. (2020). The impacts of globalization on the labor share: Evidence from Asia. The Singapore Economic Review, 65(supp01), 57–73. https://doi.org/10.1142/S0217590820440038

- Hyytinen, A., & Toivanen, O. (2005). Do financial constraints hold back innovation and growth? Research Policy, 34(9), 1385–1403. https://doi.org/10.1016/j.respol.2005.06.004

- Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4), 305–360. https://doi.org/10.1016/0304-405X(76)90026-X

- Karabarbounis, L., & Neiman, B. (2014). The global decline of the labor share. The Quarterly Journal of Economics, 129(1), 61–103. https://doi.org/10.1093/qje/qjt032

- Kehrig, M., & Vincent, N. (2021). The micro-level anatomy of the labor share decline. The Quarterly Journal of Economics, 136(2), 1031–1087. https://doi.org/10.1093/qje/qjab002

- Kini, O., Shenoy, J., & Subramaniam, V. (2017). Impact of financial leverage on the incidence and severity of product failures: Evidence from product recalls. The Review of Financial Studies, 30(5), 1790–1829. https://doi.org/10.1093/rfs/hhw092

- Koh, D., Santaeulàlia-Llopis, R., & Zheng, Y. (2020). Labor share decline and intellectual property products capital. Econometrica, 88(6), 2609–2628. https://doi.org/10.3982/ECTA17477

- Kong, D. M., Wang, Y. N., & Zhang, J. (2020). Efficiency wages as gift exchange: Evidence from corporate innovation in China. Journal of Corporate Finance, 65, 101725. https://doi.org/10.1016/j.jcorpfin.2020.101725

- Levine, R. (2005). Finance and growth: Theory and evidence. Handbook of Economic Growth. 1, 865–934. https://doi.org/10.1016/S1574-0684(05)01012-9

- Li, B., He, M., Gao, F., & Zeng, Y. (2021). The impact of air pollution on corporate cash holdings. Borsa Istanbul Review, 21, S90–S98. https://doi.org/10.1016/j.bir.2021.04.007

- Li, Y. A., Liao, W., & Zhao, C. C. (2018). Credit constraints and firm productivity: Microeconomic evidence from China. Research in International Business and Finance, 45, 134–149. https://doi.org/10.1016/j.ribaf.2017.07.142

- Li, B., Liu, C., & Sun, S. T. (2021). Do corporate income tax cuts decrease labor share? Regression discontinuity evidence from China. Journal of Development Economics, 150, 102646. https://doi.org/10.1016/j.jdeveco.2021.102624

- Lyandres, E., & Palazzo, B. (2016). Cash holdings, competition, and innovation. Journal of Financial and Quantitative Analysis, 51(6), 1823–1861. https://doi.org/10.1017/S0022109016000697

- Myers, S. C., & Majluf, N. S. (1984). Corporate financing and investment decisions when firms have information that investors do not have. Journal of Financial Economics, 13(2), 187–221. https://doi.org/10.1016/0304-405X(84)90023-0

- Nee, V. (1992). Organizational dynamics of market transition: Hybrid forms, property rights, and mixed economy in China. Administrative Science Quarterly, 37(1) https://doi.org/10.2307/2393531

- Serfling, M. (2016). Firing costs and capital structure decisions. The Journal of Finance, 71(5), 2239–2286. https://doi.org/10.1111/jofi.12403

- Sinaga, H. D. P., Samekto, F. X. A., & Emirzon, J. (2019). Ideal corporate criminal liability for the performance and accreditation of public accountant audit report in Indonesia. International Journal of Economics and Business Administration, 7(4), 451–463. https://doi.org/10.35808/ijeba/357

- Song, L., & Zhou, Y. (2020). The COVID‐19 pandemic and its impact on the global economy: What does it take to turn crisis into opportunity? China & World Economy, 28(4), 1–25. https://doi.org/10.1111/cwe.12349

- Sun, P., Deng, Z. L., & Wright, M. (2021). Partnering with Leviathan: The politics of innovation in foreign-host-state joint ventures. Journal of International Business Studies, 52, 595–620. https://doi.org/10.1057/s41267-020-00340-y

- Tan, J., Tan, Z., & Chan, K. C. (2021). Does air pollution affect a firm’s cash holdings? Pacific-Basin Finance Journal, 67, 101549. https://doi.org/10.1016/j.pacfin.2021.101549

- Tao, Q., Sun, W., Zhu, Y., & Zhang, T. (2017). Do firms have leverage targets? New evidence from mergers and acquisitions in China. The North American Journal of Economics and Finance, 40, 41–54. https://doi.org/10.1016/j.najef.2017.01.004

- Tong, Z. (2011). Firm diversification and the value of corporate cash holdings. Journal of Corporate Finance, 17(3), 741–758. https://doi.org/10.1016/j.jcorpfin.2009.05.001

- Tsafack, G., Li, Y., & Beliaeva, N. (2021). Too-big-to-fail: The value of government guarantee. Pacific-Basin Finance Journal, 68, 101313.https://doi.org/10.1016/j.pacfin.2020.101313

- Van Reenen, J., Patterson, C., Katz, L. F., Dorn, D., & Autor, D. (2020). The fall of the labor share and the rise of superstar firms. The Quarterly Journal of Economics, 135(2), 645–709. https://doi.org/10.1093/qje/qjaa004

- Wang, Q. (2015). Fixed-effect panel threshold model using stata. The Stata Journal: Promoting Communications on Statistics and Stata, 15(1), 121–134. https://doi.org/10.1177/1536867x1501500108

- Wang, B. Y., Duan, M., & Liu, G. (2021). Does the power gap between a chairman and CEO matter? Evidence from corporate debt financing in China. Pacific-Basin Finance Journal, 65, 101495. https://doi.org/10.1016/j.pacfin.2021.101495

- Xie, D. (2019). Structural deleveraging for preventing and resolving systematic financial risk. China Economic Transition, 2(1), 17–25. https://doi.org/10.3868/s060-009-019-0002-1

- Xie, H., Yang, Z., & Xu, S. (2022). Benefit synergy or “fishing in troubled waters?” Economic policy uncertainty and executive perquisite consumption. Kybernetes, https://doi.org/10.1108/k-04-2022-0626

- Xu, S., Yang, Z., Tong, Z., & Li, Y. (2021). Knowledge changes fate: Can financial literacy advance poverty reduction in rural households? The Singapore Economic Review, 1–36. https://doi.org/10.1142/s0217590821440057

- Yang, Z., Ali, S. T., Ali, F., Sarwar, Z., & Khan, M. A. (2020). Outward foreign direct investment and corporate green innovation: An institutional pressure perspective. South African Journal of Business Management, 51(1), 91–102. https://doi.org/10.4102/sajbm.v51i1.1883

- Yi, J. T., Hong, J. J., Hsu, W. C., & Wang, C. Q. (2017). The role of state ownership and institutions in the innovation performance of emerging market enterprises: Evidence from China. Technovation, 62–63, 4–13. https://doi.org/10.1016/j.technovation.2017.04.002

- Young, A. T., & Lawson, R. A. (2014). Capitalism and labor shares: A cross-country panel study. European Journal of Political Economy, 33, 20–36. https://doi.org/10.1016/j.ejpoleco.2013.11.006

- Young, A. T., & Zuleta, H. (2017). Do unions increase labor shares? Evidence from US industry-level data. Eastern Economic Journal, 44(4), 558–575. https://doi.org/10.1057/s41302-016-0086-6

- Zhan, Q., Zeng, X., Wang, Z.-A., & Mu, X. (2020). The influence of minimum wage regulation on labor income share and overwork: Evidence from China. Economic Research-Ekonomska Istraživanja, 33(1), 1729–1749. https://doi.org/10.1080/1331677x.2020.1762104

- Zhang, L. (2017). CEOs’ early-life experiences and corporate policy: Evidence from China’s great famine. Pacific-Basin Finance Journal, 46, 57–77. https://doi.org/10.1016/j.pacfin.2017.08.004

- Zhang, L., Liang, B., Bi, D., Zhou, Y., & Yu, X. (2021). Relationships among CEO narcissism, debt financing and firm innovation performance: Emotion recognition using advanced artificial intelligence. Frontiers in Psychology, 12, 734777. https://doi.org/10.3389/fpsyg.2021.734777

- Zhou, K. Z., Gao, G. Y., & Zhao, H. X. (2017). State ownership and firm innovation in China: An integrated view of institutional and efficiency logics. Administrative Science Quarterly, 62(2), 375–404. https://doi.org/10.1177/0001839216674457

Appendix

Table A1. Variable definition.

Table A2. Characteristics of cash flows in different enterprise life cycles.