?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The aim of this research is to inspect whether Corporate Governance (CG) attributes such as Audit Meeting Frequency, Ownership Concentration, Board Meeting Frequency, Foreign Ownership, Institutional Ownership, Board Gender Diversity, Audit Committee Size, Board Size, Audit Reputation and CEO Compensation affect firms’ performance in Pakistan. This research employed the pooled least square method to estimate the association among attributed of CG and firm performance measures (Return on Asset and Tobin’s Q) by selecting the Cement Sector and Energy sector companies listed in Pakistan Stock Exchange (PSX) during 2009–2022. A substantial result is that the energy sector’s CG system does not differ from the cement sector. Tobin’s Q is lesser than ROA, suggesting the same condition as companies in the cement sector. On average, firms in the energy sector are older than the firms in the cement sector. It contradicts the result of profitability proxies of the energy sector. Being older firms, the profitability proxies show lower returns as compared to cement sector firms. Pakistan needs a uniform CG code and the need for good CG practices for specific approaches of firms. This study enhances the literature in CG domain by investigating the impact of CG processes in Pakistani firm’s performance. In Pakistan, there are studies available on the topic but the comparison between the selected two industries with such a large data set are the unique elements of the current research. In prior studies, the time interval was also short, only five years. Further, the firm performance was measured by an accounting-based tool and did not include a market-based tool for performance, as well as variables for CG were also limited.

JEL CLASSIFICATION:

1. Introduction

Local firms can compete with global firms if effective corporate governance (CG) (Tsai & Mcgill, Citation2011) system is in force as it carries out a pivotal role in giving strength to a firm (Bhatt & Bhatt, Citation2017). Hopt (Citation2011) and Wondem and Batra (Citation2019) stated that CG had got wide attention in academic research as well as in practice as good CG practices are an indicator that shows how companies are controlled and directed in a better way. Firm performance and CG mechanisms perform a crucial role in an organization. In most research, CG has an extensive emphasis on organizational and other fields (Alabdullah, Citation2018). CG is an emerging area associated with firm performance and has got an extensive range of topics (Alabdullah, Citation2018). The principle-agent problem, which is the partition of ownership and control, can be lessened by CG practices (Ciftci et al., Citation2019). The company’s competitive advantage, effectiveness, and efficiency can be improved due to a capable CG (Darko et al., Citation2016). The providers of finance to corporations console themselves that they will get the profit on their investment due to a proficient CG system (Jiang et al., Citation2021).

Alabdullah (Citation2018) admits that better firm performance can be derived from good CG. Firms which have better CG practice, perform in a better way than those having poor CG practices. Singh and Pillai (Citation2022) examined the role of CG in SMEs in India. They found that CG can provide long-run financial results as well as sustainable growth. Erena et al. (Citation2022) also found the same results in Ethiopia in case of SMEs. In the matter of accounting fraud, CG plays a vital role. Those firms with inadequate CG mechanisms have a high chance of being involved in accounting fraud (Arora & Sharma, Citation2016). The prior researches have observed that strong bonding within firm performance and CG exists. Alabdullah (Citation2018) and Kren and Kerr (Citation1997) stated that managerial ownership is an instrument (Muhammad et al., Citation2016). If the firm increases the share of mangers, then the performance of the firm becomes better. A suitable CG mechanism gives the advantage of lower cost of capital, better performance, more access to financing, and a supportive environment for all stakeholders. Weak CG is a cause of sensitive financing patterns and inferior performance (Mubarik et al., Citation2021). A growing body of corporate finance studies admits the correlation within the firm performance and CG. Specifically, in Asia and the USA, many studies show positive relationships between them (Saidat et al., Citation2019). Other studies show that no positive relationship exists between firm performance and CG (Ali, Aqil, et al., Citation2021). The influence of CG on developing country’s firm performance is an important issue, and researchers are paying more attention to it (Khan et al., Citation2023; Mardnly et al., Citation2018).

Ahmed Sheikh et al. (Citation2013) stated that in most previous research, data was collected on firm performance and CG from developed countries, which shows that developed countries have many institutional similarities, yet, in some researches, evidence shows conflicting results. However, in developing countries firms have different institutional structures as well as inconsistent results.

1.1. Conflicting empirical findings

There was not much of a correlation between CG procedures and financial performance at Pakistani corporations between 2011 and 2014, which may be attributable to a lack of early adoption of the amended CG code 2012 across businesses in the country. Multivariate regression methods, such as a fixed effects model and two-stage least squares, are employed by Wang et al. (Citation2019) to establish this connection between CG and FP.

In their analysis of the impact of CG procedures on business performance, Farooq et al. (Citation2022) use the two-stage least squares (2SLS) method for data from 201 non-financial companies during the years 2010–2018 and consider the impact of firm size. Their research lends credence to resource dependency theory and agency theory by showing that bigger enterprises in Pakistan gain more from a robust governance framework, whereas medium- and small-sized businesses in the country need to improve their governance practices to get optimal results.

Looking at 152 non-financial enterprises listed on the Pakistan Stock Exchange between 2003 and 2017, Younas et al. (Citation2021) use the absolute value of the financial distress indicator (Z-Score) to determine the PAKCGI's correlation with company performance. Good corporate practices are shown to operate as a catalyst in this study, protecting businesses from financial difficulties.

Mehmood et al. (Citation2019) classify corporate diversification as product and regional diversity in order to study its influence on the financial performance of the manufacturing enterprises in South Asian Countries. Managers choose a diversification strategy for its own benefits, which is counter to agency theory and has a negative impact on the firm’s success. According to the resource dependency theory, CG techniques such as board size and CEO duality have no effect on performance, however the size of the audit committee does.

Using the four-step model developed by Baron and Kenny (Citation1986), Rashid (Citation2020) examines the mediating function of corporate board characteristics connected to capital structure and business performance in the context of Bangladesh. The findings reveal that institutional ownership has a beneficial influence on accounting-based performance but not on market-based performance, whereas foreign ownership and director ownership have a positive effect on both. This study examines the role of board independence and board size in mediating the association between ownership structure and firm performance for a sample of 527 company years (168 from 2015, 183 from 2016, and 176 from 2017).

Bashir et al. (Citation2020) attempt to analyse how capital structure mediates CG systems and financial performance by using Baron and Kenny’s four-step process to 113 non-financial enterprises listed at PSX between 2013 and 2018. The findings show that the size of the audit committee has a favourable effect on performance, whereas the size of the board has a negative effect. Research shows that companies benefit from having CEOs who hold several roles by a factor of 20%. Companies with a larger proportion of independent CEOs use more debt, and the link between CG and financial success is not mediated by capital structure, according to this article.

The research by Lu et al. (Citation2021) used organizational and management, agency, and stakeholder theories to look at the basics of internal CG. CEO authority, board size, board independence, ownership concentration, management ownership, and audit quality are the independent variables used by the authors. The study’s dependent variable is the performance of participating firms, and it is measured by economic value added and sustainable growth rate. The authors used factors including the number of employees, the quantity of the company’s assets, the rate at which they are turned over, and environmental awareness as controls. In order to better understand the reasons for the positive, negative, or null correlation between internal CG factors and organizational performance with the goal of increasing firm profitability, the researchers used Corporate Social Responsibility (CSR) as a moderating factor. From 2010 to 2019, 339 Pakistani businesses were chosen for this study, yielding a total of 3,950 observations. In order to compile this information, they scoured a variety of websites belonging to the Pakistan Stock Exchange (PSX), the State Bank of Pakistan (SBP), the Securities and Exchange Commission of Pakistan (SECP), sustainability reports, and annual reports issued by local businesses. Ordinary Least Squares (OLS), Fixed Effects (FE), Two-Stage Least Squares (2SLS), Generalized Method of Moments (GMM), and Feasible Generalized Least Squares (FGLS) are only few of the statistical methods that have been used by the researchers, with varying results. Several criteria were shown to have a positive and substantial relationship with firm performance: a strong CEO, independent board, large board, management ownership, ownership concentration, high-quality audits, and corporate social responsibility programs. Internal CG has been found to have a positive correlation with business performance, while CSR has been found to have a moderating role in this relationship. The concepts of management and organization offered backing for the CEO's influence. The board of directors, the ownership structure, and the audit committee can all take comfort from the agency theory approach. According to the stakeholder theory, the link between a firm performance and its internal CG is mediated by its commitment to social responsibility.

Chief Executive Officers’ (CEOs’) influence on Corporate Social Responsibility (CSR) in publicly listed Chinese enterprises was investigated by Cherian et al. (Citation2020). Non-financial enterprises listed on the Shanghai Stock Exchange between 2010 and 2019 were the subject of this research. The CSMAR database was mined for information on financial performance and CG. Corporate social responsibility (CSR) information was compiled from various reports, statements, and comments included with audited financial statements, as well as from the director’s remarks, the chairman’s declarations, and other public sources. In order to further understand the connection between CSR disclosure and CEO authority, a regression analysis was performed. Company size, age, board independence, return on assets, and debt-to-equity ratio are among the control variables included in this analysis. According to the data, there is an inverse relationship between a CEO's authority and the transparency of their CSR practices. In particular, the results imply that the quality of CSR disclosure tends to diminish as a CEO's degree of power grows. The principles of agency theory support this claim. According to the principles of agency theory, the separation of the CEO and chairman roles can reduce agency conflicts and increase the depth of CSR disclosure.

In order to analyse the connection between business performance and governance features such board leadership structure, Duru et al. (Citation2016) used generalized method of moments (GMM) to generate a dynamic model. ExecuComp, ISS (previously Risk Metrics), and Compustat datasets were combined to create a sample of 17,282 firm-year observations that covered the years 1997–2011. There were a total of 950 distinct businesses included in the final sample of 6848 firm-year data. The author has considered CEO duality as an independent variable. The success of the company is the dependent variable the author has used. The study found that having two CEOs had a significant negative impact on a company’s overall performance when compared to a single CEO. The authors suggest that the effect in issue is moderated in a favourable way by an independent board of directors. Although the presence of duality may contribute to executive entrenchment and a reduction in company performance, the results are consistent with the views expressed by agency theorists and certain management researchers who indicate that duality can offer benefits to the firm when board oversight is present. The claim made in agency theory lends credence to the notion.

Thus, conflicting research on firm performance motivates the need to do more research. In prior studies, the time interval was also short, only five years (Muhammad et al., Citation2016). Further, the firm performance was measured by an accounting-based tool and did not include a market-based tool for performance, as well as variables for CG were also limited (Akbar, Citation2015; Akbar et al., Citation2020; Ibrahim et al., Citation2010; Latif et al., Citation2013; Ullah et al., Citation2017; Yasser et al., Citation2011; Zabri et al., Citation2016; Zaman et al., Citation2014). The current study contributes to the existing literature in a manner that (1) in Pakistan, there are studies available on the topic but the comparison between the selected two industries with such a large data set are the unique elements of the current research (2) we have selected two proxies of firm performance. One is accounting based and the other is market based which helps understand the true impact of CG on the firm performance (3) we have selected two economic sector of Pakistan with highest contribution to the GDP of Pakistan.

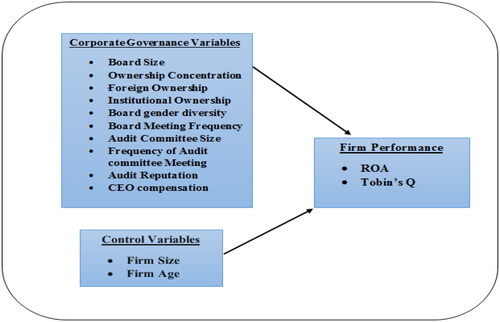

The objective of this research is to inspect whether CG affects firm performance in Pakistan. In the present study, companies from Energy and Cement Sector are selected that are listed in Pakistan Stock Exchange (PSX) during 2009–2022. Both the sectors show the highest year-to-year growth in the overall GDP of the country. The contribution of cement sector to the country’s GDP was 7.5% (SBP, Citation2018). The fiscal year 2017–18, has witnessed a 13-year high growth of 5.78% of the sector as percentage of overall GDP (Finance Division, Citation2018). The variables used are Audit Meeting Frequency (AMF), Ownership Concentration (OC), Board Meeting Frequency (BMF), Foreign Ownership (FO), Institutional Ownership (IO), Board Gender Diversity (BGD), Audit Committee Size (ACS), Board Size (BS), Audit Reputation (AR), and CEO Compensation (CEOC). For Firm Performance measurement, two proxies are used. One is an accounting-based tool (ROA), and second is Tobin’s Q as substitutes for market-based measurement.

1.2. Background

There is a strong link between good CG and a flourishing economy. Growth of a country’s economy is dependent on a number of variables, including the availability of external capital and the success of individual businesses. The most widely held view is that it refers to dynamics among top management, the board of directors, shareholders, and other interested parties. Several firm- and market-level factors provide light on the nature of CG. According to the facts at hand, there is a link between good CG and a company’s financial stability. Other researchers have defined the corporate governance in the country in terms of shareholder rights. The World Economic Forum using indicators that are unique to businesses and economies measures it.

There are several CG models and systems to choose from. Many academics in the field of CG find it vital to evaluate the relative merits of the market model and the relationship-based model, two approaches to the same problem that display different levels of efficiency (John & Senbet, Citation1998). When emerging markets decide to adopt good CG structures, the concept becomes more appealing. In general, traditional governance methods are ineffective and developing countries have different market structures than mature ones. Majumdar and Chhibber (Citation1999) research focused on the issue of CG in India. The writers argued that the current system of governmental control over the financial sector should be rethought.

Ownership is extremely concentrated in Pakistan, distorting otherwise good CG norms in the country. When borrowing money is necessary, banks are frequently looked to as a viable option, even if their loans come with a somewhat high rate of interest. CG based on personal connections appears to be the norm in Pakistan. Managers, historically, have used their good standing with financial institutions to get loans for the express purpose of increasing their companies’ market value. However, such actions might eventually cause financial ruin. Managers want just more perks for themselves and give little thought to the company’s future. More businesses rely on internal governance methods of control than on external ones. The current stage of growth in the capital market is marked by a lack of activity in the market for corporate control and a relatively weak stock market. Pakistan is a country with a relatively simple legal system and set of regulations. Anomalies and wrongdoing in the market also reduce the effectiveness of incentives. In the absence of market-based control mechanisms, ownership-based control has been developed as a key governance tool.

There are many different corporate models in the West due to the diversity of board duties within the framework of CG and the wide range of board structures and compositions. Two main approaches exist for organizing corporate boards. Countries like the USA, UK, and Canada have embraced the Anglo-Saxon one-tier board model. Several countries on the European continent use a two-tiered board structure, such as Germany, Finland, and the Netherlands.

Businesses in Pakistan are often controlled and influenced by the families or groups of families that founded them. One family, for instance, may own several businesses, some of which compete with one another within the same industry, while others may operate in other fields. This suggests that they are a dominant force in more than one economic sector. Many people’s choices are informed by the idea of ownership, which is why it’s such a hot topic of conversation. Oman et al. (Citation2004) argue that in countries experiencing transition, development, and emerging markets, potential conflicts of interest are more likely to arise between dominant shareholders and minority shareholders than between managers and shareholders. This is in contrast to the situation in the United States and the United Kingdom.

Government agencies and private companies called Independent Power Producers (IPPs) make up Pakistan’s energy industry. There are differences between the two types of businesses in terms of their underlying organizational structure. Poor CG is more common in government enterprises than in IPPs, especially when the latter are under a prolonged cash crunch. A company’s management might enrich itself at the expense of their external shareholders.

2. Literature review and hypotheses development

2.1. Corporate governance (CG) in Pakistan

The distribution of the SECP CG code 2002 for freely recorded associations has created a basic scope of analysis for company division in Pakistan. It includes laws related to financial disclosure and associations of accounting models and practices; all these are different sections of the CG system. It communicates the standards related to the return of money allocated among shareholders, different partners, executives, delegates, and individuals who take the firm’s guarantees, and all the things are described by the CG rules (Rashid et al., Citation2017). Younas et al. (Citation2021) investigated the impact of corporate governance index on firms’ financial distress in case of Pakistani firms and found that risk is reduced if corporate governance practices are adopted. SECP launched the code of CG in 2000, as the first step towards reforms. Suggestions for improving businesses, such as the firm will be bound to disclose data to the general public, the director’s board will be responsible to shareholders, improve board size, internal and external audits, and board composition are included in the codes. The main goal is to secure the control and separation of ownership, which becomes the cause for principal-agent issues (Raza et al., Citation2020).

According to the literature, a board’s primary duty is to keep an eye on management in order to cut down the agency costs that result from the separation of ownership and control (Hillman & Dalziel, Citation2003). Strategies, performance, executive appointments, and salary structures may all be approved as part of the monitoring process. Alhossini et al. (Citation2021) combined publications on the issue of corporate board and its performance to undertake a theoretical analysis. The research found that recurring proxies are a common feature of CG. Gender, status in society, and political philosophy were all mentioned as potential areas of further research into CG. In this analysis, we use gender diversity as a proxy for good CG.

2.2. Influence of agency theory

Agency cost rises due to preference issues among shareholders and managers of the firm. Kyereboah-Coleman and Biekpe (Citation2006) and Jensen and Meckling (Citation1976) further described the connection between agency and identified agency costs. In an agency contract, they assign the authority to the agent who is authorized and responsible for the decision-making and hiring of another person on their behalf to perform services. Mostly it is agreed that whenever there is any change which separates control of an organization from its legal owners, it may cause preference issues or interest conflicts between management and shareholders as management does not want to bear the risk of any loss (Safieddine, Citation2009). Agency theory argues that challenges and agency conflicts can be reduced due to effective corporate governance, and also firm’s ability can be improved to deal with such types of problems (Hussain et al., Citation2018). de Barros et al. (Citation2021) investigated the impact of corporate governance characteristics on market performance of firms from the perspective of agency theory and found positive relationship. The agency theory also argues that a firm’s validity can be enhanced due to effective CG (Hussain et al., Citation2018), and financial performance also becomes better (Hussain et al., Citation2018).

2.3. Hypothesis formulation

2.3.1. Board size (BS)

A company can be effectively controlled and directed due to members on the board (Maztoul, Citation2014). The agency theory argues that a leader’s authority and control can be encouraged by large size, and due to this, conflicts can rise (Ahmadi et al., Citation2018). Some researchers stated that better decision-making and effective monitoring are formed by the large size of the board (Arora & Sharma, Citation2016). Large Board Size (BS) is less operative than small BS, and as in larger boards, some administrators can take advantage of others’ effort. Therefore, firm value is increased due to a small board size (Ahmed Sheikh et al., Citation2013). Tran (Citation2021) proved that independent directors in the board have a positive influence on firm performance with CSR interaction in case of 20 Asia, America and Europe Countries. Huynh et al. (Citation2022) found a positive impact of board size on firm performance in case of Pakistan. Kijkasiwat et al. (Citation2022) investigated the relationship between corporate governance and firm performance with the mediating role of financial leverage in case of Pakistan, Taiwan and Turkey. The study found that large board size can improve the firm performance subject to low leverage levels. Some researchers stated that firm performance and board size are negatively connected with each other (Ahmadi et al., Citation2018). Likewise, other researchers stated that BS is positively interconnected with firm performance (Hassan et al., Citation2016). Ntim et al. (Citation2015) investigated the impact of CG practices on firm value in the South Africa. The study found that larger board size affects the firm value positively. The research of Huynh et al. (Citation2022) is followed to develop the hypothesis below as the current study is also based on Pakistan.

H1: There exists a positive association between firm performance and board size.

2.3.2. Ownership concentration (OC)

Agency theory argued that effective monitoring of a company is the result of concentrated ownership. The preferences or conflicts between managers and firms can be lowered due to ownership concentration (Detthamrong et al., Citation2017). Venture-innovative activities can be increased due to strongly concentrated ownership structures benefiting companies (Wu, Citation2019). The organizations that are mainly controlled by a few owners might face financial problems as these organizations depend on finances provided by these few owners and investment in new projects. They can also obtain other financing but in strict conditions due to the control of these few shareholders (Wang & Shailer, Citation2015). Some past literature contends that firm performance association with ownership concentration is positive but is not substantial (Al-Ghamdi & Rhodes, Citation2015), others reported that firm performance association with OC is negative (Iwasaki & Mizobata, Citation2020; Wang & Shailer, Citation2015). By reviewing the work of Iwasaki and Mizobata (Citation2020), to make this hypothesis:

H2: There exists a negative association between firm performance and ownership concentration.

2.3.3. Foreign ownership (FO)

Foreign owners have more exposure and more experience to deal with systematic changes related to different national contexts. Foreign owners adopt the best practices from abroad if they observe that the existing structure is weak (Ciftci et al., Citation2019). Some researchers stated that the connection between firm performance and FO is positive. Foreign directors and foreign owners have strong networks to manage investment opportunities and valuable resources. Foreign ownership results in companies spending more money on research and development activities and have more finance than their domestic counterparts, which results in improved performance (Mardnly et al., Citation2018). In comparison, some researchers stated that a firm’s performance and investment policy is positively affected by foreign ownership (Mardnly et al., Citation2018). Alodat et al. (Citation2022) investigated the relationship between Foreign Ownership and firm performance in case of Jordan and found significant and positive impact between these variables. In Korea, it was observed that a firm’s performance is insignificantly influenced by foreign ownership (Mardnly et al., Citation2018). The study of Alodat et al. (Citation2022) is observed to formulate the subsequent hypothesis:

H3: There exists a positive association between firm performance and foreign ownership.

2.3.4. Institutional ownership (IO)

Several vital roles are carried out by institutional ownership. First, a firm’s performance is positively influenced by an active monitoring role. Second, incentives are reduced by short-term passive roles, which affects firm performance positively. Third, for taking advantage of the expense of minority shareholders, institutional owners collaborate with the firm’s managers (Guo & Platikanov, Citation2019). Influence is exerted as passive institutional owners raise the voice by using their voting rights, like reducing management proposals’ support. Moreover, a firm’s value is positively affected by changes in governance. Long-term performance can be improved by passive mutual fund engagement (Bajo et al., Citation2020). A positive impact was found between Institutional Ownership and firm performance in case of Jordan (Alodat et al., Citation2022). Past studies suggest that the link between a firm’s stock price and institutional ownership is positive (Michel et al., Citation2020). Simultaneously, some researchers stated that no link was found between institutional owners and company performance (Michel et al., Citation2020). After reviewing the study of Alodat et al. (Citation2022), the below hypothesis is formed:

H4: The positive association between institutional ownership and firm performance exists.

2.3.5. Board gender diversity (BGD)

BGD is known as diversity within the structure of a board of administrators (Song et al., Citation2020). It is one of the serious matters related to the capability of directors of their effects on corporate performance (Song et al., Citation2020). Improving performance, more access to a broader talent pool, providing strength to corporate governance, and increasing market response are the four criteria’s female directors representation relies upon (Song et al., Citation2020). The theoretical as well as empirical literature illustrates mixed results of the female inclusion in the corporate board and its impact on firms’ performance. Nguyen et al. (Citation2020) studied 634 past studies on this topic and concluded that (i) theoretically, women board members add more value to firm’s performance (ii) but empirical literature is unable to conclude as there are positive as well as negative results exist globally.

Leyva-Townsend et al. (Citation2021) revealed that presence of at least one woman on corporate board has a positive impact on Colombian firms’ performance i.e. ROE and Tobin’s Q. Some researchers argue that various benefits are delivered from gender diversity due to various reasons. Members of the female board have more capacity to circulate useful information. They focus on harmony in a group. They use cognitive styles, etc. (Song et al., Citation2020). Ahsan et al. (Citation2021) found a positive mediation of Board Gender Diversity (BGD) between economic policy uncertainty (EPU) and sustainable growth (SG) in Chinese firms while without corporate governance, this effect becomes negative. Ali, Wang, et al. (Citation2021) argued, on the basis of Tobin regression and two-step GMM approach that diversity on corporate board positively influences on firms’ efficiency. Some researchers discovered that the influence of BGD on company performance is either negative, positive, or has no impact on performance (Kirsch, Citation2018). Chatjuthamard et al. (Citation2021) went on another aspect to check the impact of takeover market on board characteristics, especially board gender diversity which showed that more active takeover market will lead to lower board gender diversity. Karim (Citation2021) found that BGD negatively mediates the relationship of CEO remuneration-CSR. On the contrary, Amin et al. (Citation2022) found positive impact of female presence in the corporate board on firms’ financial performance in case of Pakistan. Since the current study is also based on Pakistan, we developed the following hypothesis:

H5: There exists a positive and significant association between firm performance and board gender diversity.

2.3.6. Board meeting frequency (BMF)

Board meetings reveal monitoring the success of board efforts. Board meetings help monitor and assess CEOs and corporate proposals (Ji et al., Citation2020). Some researchers believe that there is always a need to take meetings on a time-to-time basis, hence the management evaluation and strategy setting functions are fulfilled effectively by board members (Eluyela et al., Citation2018). Other researchers stated that firm performance could not become better due to board meetings as managerial time is wasted, and it also increases the firm’s expenses like traveling and relaxing allowance (Eluyela et al., Citation2018). Firm performance and board meetings are positively and significantly connected to each other (Wondem & Batra, Citation2019). Naz et al. (Citation2022) confirmed this positive relationship in their study, mentioning that increasing the board meeting may enhance the performance of firms. The study of Naz et al. (Citation2022) is followed to develop this particular hypothesis:

H6: There exists a positive association between firm performance and board meeting frequency.

2.3.7. Audit committee size (ACS)

An audit committee monitors the activities of management as well as decreases the manipulated information problem. The audit committee gives extra security against misrepresentation as well as assurance that they meet the needed standards and best practices. Associate audit members ought to perform their duties while having the necessary qualifications (Detthamrong et al., Citation2017). Past studies argue that large committee size has a broader knowledge, more authority, and excellent organizational status (Darko et al., Citation2016). In the global financial crisis, the firm performance was positively influenced by audit committee size as smaller size firms have more experience and financial proficiency (Detthamrong et al., Citation2017). Farooq et al. (Citation2022) developed a corporate governance index, including Audit Committee Size and revealed that there is positive impact of audit committee on accounting return and Tobin’s Q but nominal impact on ROE of Pakistani firms. Huynh et al. (Citation2022) found a positive impact of audit committee size on firm performance in case of Pakistan. While other researches state, that firm performance is negatively influenced by audit committee size because large size increases the expenses and leads to inefficient governance (Al-Ahdal & Hashim, Citation2022). The work of Huynh et al. (Citation2022) is followed to develop the following hypothesis:

H7: There exists a positive association between firm performance and audit committee size.

2.3.8. Audit meeting frequency (AMF)

Effectiveness of audit meetings is measured by audit meeting frequency, as noted in prior researches. An inoperative audit committee cannot monitor management effectively (Darko et al., Citation2016). Audit nomination committee and executives influence the corporate activities greatly (Vance, Citation1983). The audit committee is less likely to maintain a useful monitoring role because of fewer meetings (Darko et al., Citation2016). Shrivastav (Citation2022) examined the relationship between Audit Meeting Frequency and firm performance. The study found a positive impact in case of Indian firms. Some researchers have found positive, while others found no association between firm performance and AMF (Darko et al., Citation2016). The research of Shrivastav (Citation2022) assists in preparing the below hypothesis:

H8: There exists a positive association between the audit meeting frequency and firm performance.

2.3.9. Audit reputation (AR)

High audit quality is supported by a critical factor that is the auditor’s reputation (Chang & Chen, Citation2020). The one question that is always linked with a financial statement is the accuracy and quality of information whenever the market participants see the financial statements. Al-Ahdal and Hashim (Citation2022) found positive impact of audit reputation on firm performance in case of Indian non-financial firms. In reducing the cost of capital and information risk, auditor reputation plays an important role (Detthamrong et al., Citation2017). According to researchers, big auditors are those firms that are large in size and deal with foreign operations. They are not only performing better than domestic and small companies but also than other auditors (Detthamrong et al., Citation2017). Reviewing the research work of Al-Ahdal and Hashim (Citation2022), the below hypothesis is constructed:

H9: There exists a positive association between firm performance and audit reputation.

2.3.10. CEO compensation (CEOC)

The informativeness principle in agency theory states that compensation contracts should embody the performance results that give progressive information regarding the actions shareholders need to energize managers to carry out activities (Gan et al., Citation2020). Regulators emphasize that in the remuneration committee of directors, the presence of directors assures feasible CEO compensation (Malik & Makhdoom, Citation2016). Equity-based elements of compensation structure are expected to inspire managers to focus on additional long-term value (Gan et al., Citation2020). Chen and Hassan (Citation2022) examined the relationship between executives’ compensation and firm performance in case of China and found positive impact of equity – based compensation on firm performance. Many types of researches stated that the risk of stock crashes and stock overvaluation is increased by the manager’s involvement in short-term decisions induced by equity-based compensation (Gan et al., Citation2020). Saleem et al. (Citation2021) examined the impact of corporate governance index, including compensation committee, on firm performance on firms listed on New York Stock Exchange and found that firms deviation from standard corporate governance practices influence on firm’s performance. Hazami-Ammar and Gafsi (Citation2021) examined the impact of corporate governance variables, including remuneration structure of directors on financial distress risk of the French companies. This study revealed that distress is negatively affected by the remuneration of directors. Sarhan et al. (Citation2019) examined the impact of board diversity in terms of gender on corporate performance and executive compensation. The findings revealed that existence of female director enhances not only firm performance but also directors’ remunerations. This study follows Chen and Hassan (Citation2022) to develop the following hypothesis is prepared:

H10: There exists a positive association between firm performance and CEO compensation.

2.4. Control variables

2.4.1. Firm size (FS)

In the investigation of Saidat et al. (Citation2019), firm size has been used as a control variable. Agency cost of larger firms increases because of their larger board size (Ciftci et al., Citation2019). Large firms have more opportunities to increase their value and have more access to external funds at a cheap cost than smaller firms (Saidat et al., Citation2019). On the contrary, large firms have a negative relationship with corporate governance (Kijkasiwat et al., Citation2022). While other researchers Agrawal and Knoeber (Citation1996) and Saidat et al. (Citation2019), stated that chances of a small firm’s growth opportunities are high compared to large firms. The study of Kijkasiwat et al. (Citation2022) aids in drafting the subsequent hypothesis:

H11: There exists an association between firm performance and firm size.

2.4.2. Firm age (FA)

New firms have new assets that help the firms to perform better as compared to old firms. However, old firms have a large market share compared to new firms (Ciftci et al., Citation2019). Thompson and Manu (Citation2021) investigated the impact of corporate governance composition along with firms’ age on dividend policy of US firms. They found that there is a strong positive impact on firms’ age on the dividend policy of US firms. Capital structure and financial growth of firms are associated with age (Ahmed & Hamdan, Citation2015). Focusing on the work of Ciftci et al. (Citation2019), the below hypothesis is developed:

H12: There exists an association between firm performance and firm age.

2.5. Literature roundup and contribution

After reviewing the literature, Gender Diversity in Board, Ownership Concentration, Audit meeting frequency, Foreign Ownership, Audit Committee Size, Reputation of Audit, Board Meeting Frequency, CEO Compensation, Board Size, and Institutional Ownership variables are used by various researchers in their studies in different situations. However, all these variables are not used in one research paper previously. In the context of Pakistan, the research that is conducted on this topic is minimal. In prior studies, limited variables were used as well as a short time frame was used. In this study, the authors work on the energy sector and cement sector of Pakistan by including a more significant number of variables and cover 14 years of time frame starting from 2009 till 2022 to consolidate the research.

3. Research design

This study aims to find the influence of CG attributes on the performance of firms operating in cement and energy sector of Pakistan. These data were composed of the annual reports of companies listed on the Stock Exchange of Pakistan from 2009 to 2022. The criteria of exclusion of firms related to the data are as follows: First, if any of the independent variables were not available in annual reports of the companies, they were excluded from the sample. Second, during the period of 2009 to 2022, if any company did not survive on KSE, it was excluded from the sample (Kok et al., Citation2013).

3.1. Variables

In this study, the firm performance was measured by the ROA, this variable was used as the accounting-based tool, and another variable used for the firm performance measurement is Tobin’s Q, which was used as a market-based tool. In prior studies, the Tobin’s Q and ROA were used as substitutes for firm performance (Anderson & Reeb, Citation2003). Corporate governance variables are AR, AMF, BS, BGD, OC, IO, FO, BMF, ACS, and CEOC. Control variables in which FA and FS are included. The descriptions of the variables are given in (see ).

Figure 1. Conceptual framework. Source: Authors own work.

Table 1. Description of variables.

3.2. Statistical model

For the linear panel regression model, researchers mostly use an econometric model. Hence as to know the relationship and impact of CG on firm performance, panel data analysis is suitable. Similarly, for handling econometric data, the preferable analytical method utilized is the panel data model. The pooled linear panel econometric model is as below:

3.3. The Hausman test

Hausman test is used for deciding between the fixed-effects or random-effects model. Ahn and Moon (Citation2001) stated that Hausman statistics identify the difference between the fixed and random-effects models. In this test, we test H0, which represents consistent and efficient results in the context of random effects. Although, H1 showed that random effect is inconsistent (as a result in the fixed-effect context will always be consistent). The Hausman test uses the below statistics:

If the statistic value is greater, differences between results showed significant, so the null hypothesis is rejected and showed consistent results for random effect, therefore we used a fixed-effect model. The random effect model is more suitable if the Hausman static value is smaller.

3.4. Selection between random effect and fixed effect model

For assessing a model, another alternative used is the random effect model. For testing panel data models, the best two possible ways are fixed and random effect models. The fixed-effect model states that each country is different in the sense of intercept term, while the random effect model states that each country is different from each other in terms of error. Usually, the fixed-effect model is superior to the random-effect model when panel data is balanced. In other scenarios, the random effect model is more effective if the sample has a limited number of observations.

For the selection between ‘random and fixed effect’ the Hausman test is used. There are two models in which Model 1 represents ROA, and Model 2 represents Tobin’s Q. For Model 1, the pvalue is 0.5402, which is > 0.05, so we may accept the H0 of the random effect model. For Model 2, the p value is 0.2352, which is > 0.05, so we may accept the H0 of the random effect model, consequently, we used the random effect model in this study (Asteriou & Hall, Citation2011) (as shown in ).

Table 2. Hausman tests.

4. Empirical results and discussion

The analysis begins with the descriptive statistics for both of the economic sectors separately. and describe it for the period of 2009 to 2022. The results from the Cement Sector are self-explanatory and do not require an in-depth analysis. Ownership Concentration (OC) is a dominating factor followed by Institutional Ownership (IO) and Foreign Ownership (FO). It shows a weak corporate governance system in the cement sector. On average, Tobin’s Q is lesser than ROA, which depicts that companies’ market capitalization in the cement sector is lesser than their book values.

Table 3. Descriptive statistics – cement sectors from 2009 to 2022.

Table 4. Descriptive statistics – energy sectors from 2009 to 2022.

illustrates the results of the descriptive analysis of the energy sector from 2009 to 2022. Ownership Concentration (OC) is more distinct in the energy sector as opposed to the cement sector. Institutional Ownership (IO) dominates over Foreign Ownership (FO). The corporate governance system of the energy sector does not differ from the cement sector. Tobin’s Q is lesser than ROA, suggesting the same condition as companies in the cement sector. On average, firms in the energy sector are older than the firms in the cement sector. It contradicts the result of profitability proxies of the energy sector. Being older firms, the profitability proxies show lower returns as compare to cement sector firms.

4.1. Estimation of firm performance

shows the impact on corporate governance due to the cement sector’s firm performance through the random effect regression model.

Table 5. Random effects regression – cement sector from 2009 to 2022.

4.2. Estimation of ROA

Model 1 shows that FO and ROA are positively and significantly related to each other and also indicate consistency with the previous study of Saidat et al. (Citation2019). It has a 5% significance level, which means if FO rises, the firm performance also rises. It gives logical reasoning to understand that more board members with diverse business experience can provide a firm competitive edge in terms of performance. The BGD has a positive and insignificant connection with ROA, which is opposite to the results shown in Wondem and Batra (Citation2019). The CEOC coefficient’s magnitude is almost zero, showing a relationship with ROA with a significant impact at a 10% level. AR and ROA are positively and significantly related to each other at a 1% significance level. FA is positively and significantly interlinked with ROA at a 1% level of significance, which means that a firm can grow in terms of its performance with time. There is a positive and statistically significant relationship between FS and ROA, and the previous study of Saidat et al. (Citation2019) also has similar results. It has a 10% significance level, which indicates that if FS increases, the firm performance also increases. Out of 12 variables in this model, 7 variables are statistically significant at different significance levels with all significant t statistics.

4.3. Estimation of Tobin’s Q

Model 2 shows that Tobin’s Q is positively but statistically insignificant association with BS. The result shows opposite the study of Ciftci et al. (Citation2019). It means if BS increases, the firm performance also increases. The result is also consistent with agency theory, which recommends monitoring managers’ activity by the large size of the board. The results show the negative and significant interconnection between OC and Tobin’s Q, and this result is similar to the result of Saidat et al. (Citation2019), while it has a 5% significance level and t-statistics value is significant, which means if the firm performance increases the OC decreases. FO and Tobin’s Q are positively and significantly linked with each other, which is the same as Saidat et al. (Citation2019) result. The results show that a 5% significance level and t-statistics value is significant, which means if FO increases, the firm performance also increases. IO is positively and significantly related to Tobin’s Q. These results support the previous study of Arora and Sharma (Citation2016). It has a 10% significance level, and t-statistics value is significant indicates that as the institutional ownership increases, the firm performance also increases. ACS has a negative and significant relationship with Tobin’s Q at a 5% significance level, and the t-statistics value is significant. However, according to the previous study of Darko et al. (Citation2016), results show a negative but insignificant relationship with Tobin’s Q. The study results reveal that if ACS increases, the firm performance decreases. A negative and statistically insignificant relationship exists between AR and Tobin’s Q and which means if AR increases, the performance decreases but statistically insignificant. In model 2 out of 12 variables only three variables are statistically significant.

The impact of CG on firm performance is shown in the following equation:

In the equations above, i represents the firm (i = 1…26) in cement sector, t represents the year (t = 2009 to 2022). ROA and Tobin’s Q variables are considered as financial performance measures.

shows the impact of corporate governance on the energy sector’s firm performance through the random effect regression model.

Table 6. Random effects regression of selected companies of energy sector from 2009 to 2022.

4.4. Estimation of ROA

Model 1 shows that ACS has a negative and significant relationship with ROA, but our results show dissimilarity with the result of Darko et al. (Citation2016) because their study shows a positive and insignificant relationship. Our results show that a 5% significance level and t-statistics value is significant, which reveals that if the audit committee size increases, the firm performance decreases. There is a negative and significant relationship between FA and ROA, and our results do not support the results of the previous study of Ciftci et al. (Citation2019) as it shows a positive and insignificant relationship. Our result also indicated at 1% significance level, and the t-statistics value is significant, which means if FA increases, the firm performance decreases. Our result shows a positive and statistically significant relationship between FS and ROA, which is consistent with the previous study of Saidat et al. (Citation2019), and it also indicated 5% significance level, and t-statistics value is significant, which indicates that if FS increases the firm performance also increases. In model 1, out of 12 variables, three variables are statistically significant.

4.5. Estimation of Tobin’s Q

Model 2 defines that FO and Tobin’s Q are positively and significantly related to each other as the result of Saidat et al. (Citation2019). This result shows a 10% significance level, and the t-statistics value is significant, which means if FO increases, the fire performance also increases. A positive and significant relationship exists between AR and Tobin’s Q at a 1% level, and the t-statistics value is significant, which means if AR increases the performance, also increases. There is a positive and significant relationship between FS and Tobin’s Q, and our result is not the same as the results of previous study Darko et al. (Citation2016), as their results show a negative and significant relationship between firm size and Tobin’s Q. Our results show a 1% significance level and t-statistics value is significant, which indicates that if FS increases the firm performance also increases.

The following equation shows the impact of CG on firm performance.

In the equations above, i represents the firm (i = 1…11) in the energy sector, t represents the year (t = 2009 to 2022). ROA and Tobin’s Q variables are considered as financial performance measures (as shown in ).

Table 7. Random effects regression of selected companies of energy sector from 2009 to 2022.

4.6. Model 1

Model 1 shows that the BS of both sectors is positive and insignificant, while in both sector’s OC is negative and insignificant. Although the cement sector’s FO is positive and shows a 5% significance, the FO is negative and insignificant for the energy sector. The IO for both sectors represented an insignificant and positive relation. For the cement sector, the BGD is positive and shows a 5% significance, but BGD is insignificant and positive for the energy sector. ACS of the cement sector is positive and insignificant, while for the energy sector, it shows a negative relationship at a 5% significance level. For both sectors, CEOC is positive, but it shows a 5% significance level for the cement sector. For the energy sector, it is insignificant. AR of the cement sector is significant at 1% and positive, but it shows the insignificant and positive for the energy sector. FA of both sectors shows significance at a level of 1%, but it shows a positive relationship for the cement sector, and for the energy sector, it shows a negative relationship. For the cement sector, the FS represented a 10% significance level and positive correlation, while for the energy sector, it shows 5% of significance. The adjusted R-Squared of the energy sector is better than the cement sector, but the cement sector’s regression error is less than the energy sector.

4.7. Model 2

Model 2 shows that the BS of cement sectors is positive and significant at 5%, but it represents a negative and insignificant relationship for the energy sector. Both sector’s OC is negative, but the cement sector OC shows 5% significance. FO of both sectors shows positive and significant relationships, the cement sector showed 5% significance, and the energy sector showed 10% significance. IO of the cement sector represents a significant and positive relationship at 5%, but it shows insignificance for the energy sector. BGD of both sectors represented a negative and insignificant relationship. ACS of the energy sector is positive and insignificant, while for the cement sector, it shows a negative relationship at a 5% significance level. For both sectors, CEOC is positive and insignificant. AR of the cement sector is significant at 5% and shows a negative association, but it shows a 1% significance and a positive association for the energy sector. FA of both sectors shows insignificance and also shows a positive relationship. For the cement sector, the FS represented insignificance and negative correlation, while for the energy sector, it shows 1% significance and positive correlation. The adjusted R- Squared of the energy sector is better than the cement sector, the regression error of the energy sector is less than the cement sector.

4.8. Robustness check

We also check the robustness by applying 2SLS on the same data. The 2SLS help validate the regression results. After observing all the values on the 2SLS table, we found that there is no difference in the magnitude of coefficient as well as the Adj R2. Besides, there are some minor differences in the values of standard errors. The (2SLS for Cement Sector), (2SLS for Energy Sector) and (2SLS for both sectors for comparison) are placed in the Appendix.

5. Summary and conclusion

This study examined CG's impact on firm performance in the energy and cement sector from 2009 to 2022. The study found that the results of the cement sector are represented in . The performance indicator of ROA shows that six variables are statistically significant out of 12 variables, and these variables are FO, BGD, CEOC, AR, FA, and FS, and have a positive and significant relationship. In contrast, BS, IO, AMF, ACS have a positive but insignificant correlation with ROA.OC and BMF have negatively and insignificantly correlated with ROA. The performance indicator Tobin’s Q is used in Model 2, and it is indicated that out of 12 variables, six variables are statistically significant. BS, FO, IO are positively and significantly correlated with Tobin’s Q, while OC, ACS, and AR have a negative and significant relationship with Tobin’s Q. For the cement sector, the best performance indicator is Tobin’s Q because its standard error of the regression is small than the other two indicators. The descriptive statistics result of the cement sector for the period of 2009 to 2022 shows that, by comparing the variations of ROA and Tobin’s Q, Tobin’s Q's standard deviation is the minimum shows that Tobin’s Q is a better performance indicator for our sample.

The energy sector results are indicated in . Three variables are statistically significant in which FS has a positive and ACS and FA have a negative relationship with ROA. BS, IO, BGD, BMF, CEOC, AR are positively associated with ROA, while OC, FO, is negatively related to ROA. Model 2 results indicated that three variables are statistically significant, and all three have a positive relationship with Tobin’s’ Q, which is FO, AR, and FS. BS, OC, BGD, and FA are negatively and insignificantly associated with Tobin’s Q, while others IO, BMF, AMF, ACS, CEOC are positively and insignificantly correlated with Tobin’s Q. For the Energy sector, the best performance indicator is Tobin’s Q because its standard error of the regression is small than the other two indicators. The descriptive statistics result of the energy sector for the period of 2009 to 2018 shows that by comparing the variations of ROA and Tobin’s Q, Tobin’s Q's standard deviation is minimal, representing that Tobin’s Q is a better performance indicator for our sample. The paper successfully achieved to cover the research gap identified in the paper and contributes to the existing literature with new empirical evidences as explained.

5.1. Implications

The results indicate that BOD needs more competencies like diversification strategy, which relates to attracting new market possibilities, to a larger BS, to use technological and financial facilities more proficiently.

The higher management of a cement sector firm must focus on ownership structure to improve the firm’s financial performance, especially the Foreign Ownership (FO) which is significant not only with accounting based (ROA) but also with market-based measure (Tobins’Q). This implies that firms should focus on FO to develop the ownership structure more efficiently. This result may be a breakthrough for most of the firms in the cement sector where the FO is on the lowest level. Managers and executive directors must ponder this point to improve the financial performance of their firms.

The market-based performance (Tobins’Q) in case of ACS deteriorates in the cement sector while improving in accounting-based measure (ROA). The energy sector does not show any significance in this regard. This assumes that governance structure of energy sector might be different from that of cement sector and managers and other decision makers in this sector must focus on different variables of corporate governance to improve their financial performance.

The results board gender diversity is not much pronounced as it is negatively significant only in case of ROA in the Energy Sector. Market reaction towards the inclusion of female director is of no concern for both cement as well as energy sector firms. CEOC and AR both illustrate a positive and significant relationship with ROA only in cement sector.

We come to this point that firms working in the emerging market have different corporate governance practices due to which their financial performance mismatch with other firms. This may be resolved if we develop a uniform CG code and perform good CG practices. Our outcomes are in favour of supporting the impact of good CG on firm performance.

5.2. Recommendation for future research

The corporate governance is a broad area of research which requires special attention and interest. This area has already been explored many times but still has conflicting empirical evidences. Time-varying results is the biggest challenge in this area. Future research can capitalize this opportunity to capture this area of challenge. Secondly, there are multiple proxies of corporate governance as well as index, which are being used in research. Future studies can develop a unified CG index, which may be applicable to all researches. Additionally, efficiency of corporate governance differs of the developed counties from that of developing nations. This area needs the full attention of researchers to find the solution. In the area of corporate governance, control variables play a significant role. Besides leverage and firm size that were frequently used, other variables like cost of capital, fixed assets and dividend policy need further evidence in this regard.

5.3. Limitations

We make our efforts to incorporate important factors of corporate governance (CG) to check their impact on firm performance. There are still some proxies of CG, which are not part of the study. Future researchers may take this opportunity to capitalize it. Secondly, this study only considered Pakistan due to difficulty of collecting data of firms outside the country. Foreign researchers may take it as a future research gap. An opportunity exists to employ a corporate governance index as a proxy of CG and check the impact of exogenous variables. Corporate governance quality is another area of research where future studies can be carried out.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Data availability statement

Data is openly available in a public repository that does not issue DOIs.

References

- Agrawal, A., & Knoeber, C. R. (1996). Firm performance and mechanisms to control agency problems between managers and shareholders. The Journal of Financial and Quantitative Analysis, 31(3), 377–397. https://doi.org/10.2307/2331397

- Ahmadi, A., Nakaa, N., & Bouri, A. (2018). Chief Executive Officer attributes, board structures, gender diversity and firm performance among French CAC 40 listed firms. Research in International Business and Finance, 44, 218–226. https://doi.org/10.1016/j.ribaf.2017.07.083

- Ahmed, E., & Hamdan, A. (2015). The impact of corporate governance on firm performance: Evidence from Bahrain Bourse. International Management Review, 11, 21.

- Ahmed Sheikh, N., Wang, Z., & Khan, S. (2013). The impact of internal attributes of corporate governance on firm performance: Evidence from Pakistan. International Journal of Commerce and Management, 23(1), 38–55. https://doi.org/10.1108/10569211311301420

- Ahn, S., & Moon, H. (2001). Large-N and large-T properties of panel data estimators and the Hausman test (USC CLEO Research Paper, No. C01-20).

- Ahsan, T., Mirza, S. S., Al-Gamrh, B., Bin-Feng, C., & Rao, Z.-U.-R. (2021). How to deal with policy uncertainty to attain sustainable growth: The role of corporate governance. Corporate Governance: The International Journal of Business in Society, 21(1), 78–91. https://doi.org/10.1108/CG-04-2020-0121

- Akbar, A. (2015). The role of corporate governance mechanism in optimizing firm performance: A conceptual model for corporate sector of Pakistan. Journal of Asian Business Strategy, 5(6), 109–115. https://doi.org/10.18488/journal.1006/2015.5.6/1006.6.109.115

- Akbar, M., Hussain, S., Ahmad, T., & Hassan, S. (2020). Corporate governance and firm performance in Pakistan: Dynamic panel estimation. Abasyn Journal of Social Sciences, 12, 213–230.

- Al-Ahdal, W. M., & Hashim, H. A. (2022). Impact of audit committee characteristics and external audit quality on firm performance: Evidence from India. Corporate Governance: The International Journal of Business in Society, 22(2), 424–445. https://doi.org/10.1108/CG-09-2020-0420

- Al-Ghamdi, M., & Rhodes, M. (2015). Family ownership, corporate governance and performance: Evidence from Saudi Arabia. International Journal of Economics and Finance, 7(2), 78–89. https://doi.org/10.5539/ijef.v7n2p78

- Alabdullah, T. T. Y. (2018). The relationship between ownership structure and firm financial performance: Evidence from Jordan. Benchmarking: An International Journal, 25(1), 319–333. https://doi.org/10.1108/BIJ-04-2016-0051

- Alhossini, M. A., Ntim, C. G., & Zalata, A. M. (2021). Corporate board committees and corporate outcomes: An international systematic literature review and agenda for future research. The International Journal of Accounting, 56(01), 2150001. https://doi.org/10.1142/S1094406021500013

- Ali, F., Wang, M., Jebran, K., & Ali, S. T. (2021). Board diversity and firm efficiency: Evidence from China. Corporate Governance: The International Journal of Business in Society, 21(4), 587–607. https://doi.org/10.1108/CG-10-2019-0312

- Ali, M. A., Aqil, M., Alam Kazmi, S. H., & Zaman, S. I. (2021). Evaluation of risk adjusted performance of mutual funds in an emerging market. International Journal of Finance & Economics, 28(2), 1436–1449. https://doi.org/10.1002/ijfe.2486

- Alodat, A. Y., Salleh, Z., Hashim, H. A., & Sulong, F. (2022). Corporate governance and firm performance: Empirical evidence from Jordan. Journal of Financial Reporting and Accounting, 20(5), 866–896. https://doi.org/10.1108/JFRA-12-2020-0361

- Amin, A., Ali, R., Rehman, R. u., Naseem, M. A., & Ahmad, M. I. (2022). Female presence in corporate governance, firm performance, and the moderating role of family ownership. Economic Research-Ekonomska Istraživanja, 35(1), 929–948. https://doi.org/10.1080/1331677X.2021.1952086

- Anderson, R. C., & Reeb, D. M. (2003). Founding‐family ownership and firm performance: Evidence from the S&P 500. The Journal of Finance, 58(3), 1301–1328. https://doi.org/10.1111/1540-6261.00567

- Arora, A., & Sharma, C. (2016). Corporate governance and firm performance in developing countries: Evidence from India. Corporate Governance, 16(2), 420–436. https://doi.org/10.1108/CG-01-2016-0018

- Asteriou, D., & Hall, S. G. (2011). Applied econometrics (2nd ed.). Palgrave Macmillan.

- Bajo, E., Croci, E., & Marinelli, N. (2020). Institutional investor networks and firm value. Journal of Business Research, 112, 65–80. https://doi.org/10.1016/j.jbusres.2020.02.041

- Baron, R. M., & Kenny, D. A. (1986). The moderator–mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. Journal of Personality and Social Psychology, 51(6), 1173–1182. https://doi.org/10.1037//0022-3514.51.6.1173

- Bashir, Z., Bhatti, G. A., & Javed, A. (2020). Corporate governance and capital structure as driving force for financial performance: Evidence from non-financial listed companies in Pakistan. IBA Business Review, 15(1), 108–133.

- Bhatt, P. R., & Bhatt, R. R. (2017). Corporate governance and firm performance in Malaysia. Corporate Governance: The International Journal of Business in Society, 17(5), 896–912. https://doi.org/10.1108/CG-03-2016-0054

- Chang, W.-C., & Chen, J.-P. (2020). Auditor sanction and reputation damage: Evidence from changes in non-client-company directorships. The British Accounting Review, 52(3), 100894. https://doi.org/10.1016/j.bar.2020.100894

- Chatjuthamard, P., Jiraporn, P., Lee, S. M., Uyar, A., & Kilic, M. (2021). Does board gender diversity matter? Evidence from hostile takeover vulnerability. Corporate Governance: The International Journal of Business in Society, 21(5), 845–864. https://doi.org/10.1108/CG-08-2020-0353

- Chen, C., & Hassan, A. (2022). Management gender diversity, executives compensation and firm performance. International Journal of Accounting & Information Management, 30(1), 115–142. https://doi.org/10.1108/IJAIM-05-2021-0109

- Cherian, J., Safdar Sial, M., Tran, D. K., Hwang, J., Khanh, T. H. T., & Ahmed, M. (2020). The strength of CEOs’ influence on CSR in Chinese listed companies. New insights from an agency theory perspective. Sustainability, 12(6), 2190. https://doi.org/10.3390/su12062190

- Ciftci, I., Tatoglu, E., Wood, G., Demirbag, M., & Zaim, S. (2019). Corporate governance and firm performance in emerging markets: Evidence from Turkey. International Business Review, 28(1), 90–103. https://doi.org/10.1016/j.ibusrev.2018.08.004

- Darko, J., Aribi, Z. A., & Uzonwanne, G. C. (2016). Corporate governance: The impact of director and board structure, ownership structure and corporate control on the performance of listed companies on the Ghana stock exchange. Corporate Governance, 16(2), 259–277. https://doi.org/10.1108/CG-11-2014-0133

- de Barros, F. E. E., dos Santos, R. C., Orso, L. E., & Sousa, A. M. R. (2021). The evolution of corporate governance and agency control: The effectiveness of mechanisms in creating value for companies with IPO on the Brazilian stock Exchange. Corporate Governance: The International Journal of Business in Society, 21(5), 775–814. https://doi.org/10.1108/CG-11-2019-0355

- Detthamrong, U., Chancharat, N., & Vithessonthi, C. (2017). Corporate governance, capital structure and firm performance: Evidence from Thailand. Research in International Business and Finance, 42, 689–709. https://doi.org/10.1016/j.ribaf.2017.07.011

- Duru, A., Iyengar, R. J., & Zampelli, E. M. (2016). The dynamic relationship between CEO duality and firm performance: The moderating role of board independence. Journal of Business Research, 69(10), 4269–4277. https://doi.org/10.1016/j.jbusres.2016.04.001

- Eluyela, D. F., Akintimehin, O. O., Okere, W., Ozordi, E., Osuma, G. O., Ilogho, S. O., & Oladipo, O. A. (2018). Board meeting frequency and firm performance: Examining the nexus in Nigerian deposit money banks. Heliyon, 4(10), e00850. https://doi.org/10.1016/j.heliyon.2018.e00850

- Erena, O. T., Kalko, M. M., & Debele, S. A. (2022). Corporate governance mechanisms and firm performance: Empirical evidence from medium and large-scale manufacturing firms in Ethiopia. Corporate Governance: The International Journal of Business in Society, 22(2), 213–242. https://doi.org/10.1108/CG-11-2020-0527

- Farooq, M., Noor, A., & Ali, S. (2022). Corporate governance and firm performance: Empirical evidence from Pakistan. Corporate Governance: The International Journal of Business in Society, 22(1), 42–66. https://doi.org/10.1108/CG-07-2020-0286

- Finance Division. (2018). Pakistan Economic Survey 2017-18. Government of Pakistan.

- Gan, H., Park, M. S., & Suh, S. (2020). Non-financial performance measures, CEO compensation, and firms’ future value. Journal of Business Research, 110, 213–227. https://doi.org/10.1016/j.jbusres.2020.01.002

- Guo, L., & Platikanov, S. (2019). Institutional ownership and corporate governance of public companies in China. Pacific-Basin Finance Journal, 57, 101180. https://doi.org/10.1016/j.pacfin.2019.101180

- Hassan, Y. M., Naser, K., & Hijazi, R. H. (2016). The influence of corporate governance on corporate performance: Evidence from Palestine. Afro-Asian J. of Finance and Accounting, 6(3), 269–287. https://doi.org/10.1504/AAJFA.2016.079296

- Hazami-Ammar, S., & Gafsi, A. (2021). Governance failure and its impact on financial distress. Corporate Governance: The International Journal of Business in Society, 21(7), 1416–1439. https://doi.org/10.1108/CG-08-2020-0347

- Hillman, A. J., & Dalziel, T. (2003). Boards of directors and firm performance: Integrating agency and resource dependence perspectives. Academy of Management Review, 28(3), 383–396. https://doi.org/10.2307/30040728

- Hopt, K. J. (2011). Comparative corporate governance: The state of the art and international regulation. American Journal of Comparative Law, 59(1), 1–73. https://doi.org/10.5131/AJCL.2010.0025

- Hussain, N., Rigoni, U., & Orij, R. P. (2018). Corporate governance and sustainability performance: Analysis of triple bottom line performance. Journal of Business Ethics, 149(2), 411–432. https://doi.org/10.1007/s10551-016-3099-5

- Huynh, Q. L., Hoque, M. E., Susanto, P., Watto, W. A., & Ashraf, M. (2022). Does financial leverage mediates corporate governance and firm performance? Sustainability, 14(20), 13545. https://doi.org/10.3390/su142013545

- Ibrahim, Q., Rehman, R., & Raoof, A. (2010). Role of corporate governance in firm performance: A comparative study between chemical and pharmaceutical sectors of Pakistan. International Research Journal of Finance and Economics, 50, 7–16.

- Iwasaki, I., & Mizobata, S. (2020). Ownership concentration and firm performance in European emerging economies: A meta-analysis. Emerging Markets Finance and Trade, 56(1), 32–67. https://doi.org/10.1080/1540496X.2018.1530107

- Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4), 305–360. https://doi.org/10.1016/0304-405X(76)90026-X

- Ji, J., Talavera, O., & Yin, S. (2020). Frequencies of board meetings on various topics and corporate governance: Evidence from China. Review of Quantitative Finance and Accounting, 54(1), 69–110. https://doi.org/10.1007/s11156-018-00784-2

- Jiang, Y., Khan, M. I., Zaman, S. I., & Iqbal, A. (2021). Financial development and trade in services: Perspective from emerging markets of Asia, South and Central America and Africa. International Journal of Finance & Economics, 26(3), 3306–3320. https://doi.org/10.1002/ijfe.1963

- John, K., & Senbet, L. W. (1998). Corporate governance and board effectiveness. Journal of Banking & Finance, 22(4), 371–403. https://doi.org/10.1016/S0378-4266(98)00005-3

- Karim, S. (2021). An investigation into the remuneration – CSR nexus and if it can be affected by board gender diversity. Corporate Governance: The International Journal of Business in Society, 21(4), 608–625.

- Khan, B., Aqil, M., Alam Kazmi, S. H., & Zaman, S. I. (2023). Day‐of‐the‐week effect and market liquidity: A comparative study from emerging stock markets of Asia. International Journal of Finance & Economics, 28(1), 544–561. https://doi.org/10.1002/ijfe.2435

- Kijkasiwat, P., Hussain, A., & Mumtaz, A. (2022). Corporate governance, firm performance and financial leverage across developed and emerging economies. Risks, 10(10), 185. https://doi.org/10.3390/risks10100185

- Kirsch, A. (2018). The gender composition of corporate boards: A review and research agenda. The Leadership Quarterly, 29(2), 346–364. https://doi.org/10.1016/j.leaqua.2017.06.001

- Kok, B. E., Coffey, K. A., Cohn, M. A., Catalino, L. I., Vacharkulksemsuk, T., Algoe, S. B., Brantley, M., & Fredrickson, B. L. (2013). How positive emotions build physical health. Psychological Science, 24(7), 1123–1132. https://doi.org/10.1177/0956797612470827

- Kren, L., & Kerr, J. L. (1997). The effects of outside directors and board shareholdings on the relation between chief executive compensation and firm performance. Accounting and Business Research, 27(4), 297–309. https://doi.org/10.1080/00014788.1997.9729556

- Kyereboah-Coleman, A., & Biekpe, N. (2006). The link between corporate governance and performance of the non-traditional export sector: Evidence from Ghana. Corporate Governance: The International Journal of Business in Society, 6(5), 609–623. https://doi.org/10.1108/14720700610706090

- Latif, B., Shahid, M. N., Haq, M., Waqas, H. M., & Arshad, A. (2013). Impact of corporate governance on firm performance: Evidence from sugar mills of Pakistan. European Journal of Business and Management, 5, 51–59.

- Leyva-Townsend, P., Rodriguez, W., Idrovo, S., & Pulga, F. (2021). Female board participation and firm’s financial performance: A panel study from a Latin American economy. Corporate Governance: The International Journal of Business in Society, 21(5), 920–938. https://doi.org/10.1108/CG-07-2019-0235

- Lu, J., Javeed, S. A., Latief, R., Jiang, T., & Ong, T. S. (2021). The moderating role of corporate social responsibility in the association of internal corporate governance and profitability; evidence from Pakistan. International Journal of Environmental Research and Public Health, 18(11), 5830. https://doi.org/10.3390/ijerph18115830

- Majumdar, S. K., & Chhibber, P. (1999). Capital structure and performance: Evidence from a transition economy on an aspect of corporate governance. Public Choice, 98(3/4), 287–305. https://doi.org/10.1023/A:1018355127454

- Malik, M. S., & Makhdoom, D. D. (2016). Does corporate governance beget firm performance in fortune global 500 companies? Corporate Governance, 16(4), 747–764. https://doi.org/10.1108/CG-12-2015-0156

- Mardnly, Z., Mouselli, S., & Abdulraouf, R. (2018). Corporate governance and firm performance: An empirical evidence from Syria. International Journal of Islamic and Middle Eastern Finance and Management, 11(4), 591–607. https://doi.org/10.1108/IMEFM-05-2017-0107

- Maztoul, S. B. M. (2014). Does corporate governance matter in meeting and beating analysts’ forecasts. International Journal of Business and Management, 9(2), 276. https://doi.org/10.5539/ijbm.v9n2p276

- Mehmood, R., Hunjra, A. I., & Chani, M. I. (2019). The impact of corporate diversification and financial structure on firm performance: Evidence from South Asian countries. Journal of Risk and Financial Management, 12(1), 49. https://doi.org/10.3390/jrfm12010049

- Michel, A., Oded, J., & Shaked, I. (2020). Institutional investors and firm performance: Evidence from IPOs. The North American Journal of Economics and Finance, 51, 101099. https://doi.org/10.1016/j.najef.2019.101099

- Mubarik, M. S., Miao, M., Mubarak, M. F., Zaman, S. I., Kazmi, S. H. A., & Naghavi, N. (2021). Host country corruption and headquarters-subsidiary relationships in emerging economies. International Journal of Emerging Markets. https://doi.org/10.1108/IJOEM-10-2019-0882