?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.ABSTRACT

The zero lower bound (ZLB) may restrict the responsiveness of exchange rates to news. A proxy for central bank communication is added as a determinant in a model of exchange rate movements. Two reserve currencies, the British pound and euro, and two currencies of small open economies, the Canadian dollar and Swedish krona, are examined. Reserve currencies are more vulnerable to the ZLB constraint, while the currencies of small open economies become more responsive to foreign central bank announcements. Certain unconventional monetary policy announcements were found to significantly impact exchange rates at the ZLB.

I. Introduction

A large literature exists linking news events to exchange rate fluctuations. Since the global financial crisis of 2008–2009, however, we now have data to analyse whether the zero lower bound (ZLB) for interest rates restricts movements of exchange rates. Even if policy rates can enter negative territory, central bankers typically acknowledge that there are limits to how far interest rates can go below zero.

In economies with exchange rates that move freely, any indication that the effectiveness of monetary policy is hampered by the ZLB may have implications for the ability of exchange rates to absorb external shocks. The purpose of this research is to identify whether approaching the ZLB constraint on the monetary policy interest rate restricts the responsiveness of exchange rates to news events. Other than Swanson and Williams (Citation2014), we are not aware of any empirical attempt to investigate the issue.

This article makes two additional contributions. As many central bankers have recently pointed out, monetary policy communication becomes more important as policy rates approach the ZLB and, near this threshold, communication of policy may be even more important than actual policy changes (e.g., Bernanke Citation2015; Carney Citation2012; Draghi Citation2014; Yellen Citation2013). Accordingly, we include a quantitative measure of the ‘tone’ of central bank communication as an additional determinant of exchange rate movements.

Second, we consider a broader set of economies than Swanson and Williams (Citation2014), and a longer sample. We examine data for Canada, the Eurozone, Sweden and the UK since the central banks of these countries come closest to adhering to a monetary policy strategy that includes a pure-floating exchange rate regime. The sample consists of two reserve currencies and the currencies of two small open economies that target inflation.

II. The ZLB and exchange rate movements

The workhorse model linking exchange rate movements to the ZLB constraint is uncovered interest rate parity. Define as the (log) nominal exchange rate at time t, in terms of domestic currency units vis-à-vis the US dollar,

is a one period nominal interest rate,

is the expectations operator and * denotes foreign equivalents. For two sovereign bonds, we can writeFootnote1

As seen from Equation 1, exchange rate and interest rate movements are restricted if exchange rate expectations are themselves constrained. Swanson and Williams (Citation2014) also show that Equation 1 can be linked to the yield differential on longer-term bonds if the real exchange rateFootnote2 returns to some steady state, consistent with purchasing power parity. Therefore, even if short-term interest rates are constrained, short-term exchange rate movements need not be restricted at the ZLB.

The standard econometric specification links a change in asset prices to ‘news’ ordinarily defined as unexpected movements in a vector of macroeconomic announcements. We expand the definition to include news content from central bank communications. Moreover, the ZLB effectively introduces nonlinearity in the relationship between news and exchange rate movements.Footnote3 The estimated specification then is written as follows:

where denotes a function to capture sensitivity to news and other factors. More precisely,

Equations 2 and 3 are estimated jointly. is a vector consisting of the first principal component of the available domestic yields at various terms to maturity, and the (10-day) rolling SD of the first principal component of both domestic and foreign yields. The first principal component extracts common movements in yields. It is included because, as identified by Swanson and Williams (Citation2014), the sensitivity of exchange rates may depend on yield levels. The volatility of the first principal component is assumed to proxy financial market uncertainty both domestically and in the corresponding foreign country (i.e., the US).

is a vector of news components of macroeconomic data releases defined as the observed data less the consensus forecast. We extend standard specifications with a vector capturing the ‘tone’ of central bank announcements (

). We employ the DICTION algorithm (see Hart, Childers, and Lind Citation2013). Tone is interpreted on the basis of a dictionary of (financial) words that convey meaning along various dimensions. We group expressions and terms into two categories: positive and negative. A ‘positive tone’ variable captures sentiments that indicate accomplishment, predictability or agreement; this signals a proactive stance, or signals positive outcomes. Hence, an appreciation of the domestic currency is expected. The ‘negative tone’ variable includes words that describe hardship and stagnation; this combination signals unfavourable conditions and, therefore, a depreciation of the currency. The tone variable cannot capture actual policy changes such as the announcement of a quantitative easing (QE) policy. Hence, we also add a vector of dummy variables,

, that capture unconventional monetary policy (UMP) announcements.

III. Data and evidence

The sample period is from January 2003 to March 2015. Data consists of currencies from four economies that reduced their monetary policy interest rate to the effective ZLB during this period: Canada, the Eurozone, Sweden and the UK.Footnote4

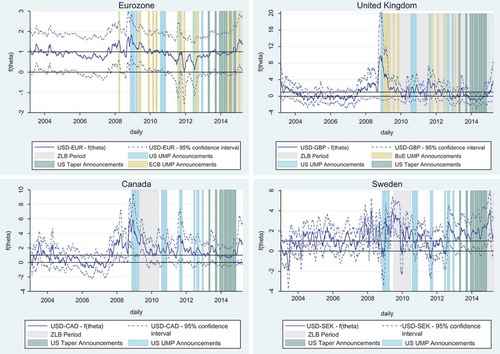

plots the estimates of , which is intended to capture the responsiveness of foreign exchange rates to news against a benchmark period where interest rates are not constrained by the ZLB and, therefore, are expected to respond ‘normally’ to news; the benchmark period was standardized to an average value of one.

Figure 1. Foreign exchange rates sensitivity to news.

Notes: 52-business day (2 months) moving average of the fitted values of Equation 3. The foreign uncertainty variable included in the regression on the British pound is the Eurozone uncertainty variable because domestic and US uncertainty were highly correlated, and the EMU uncertainty variable can capture some relevant ‘international’ volatility. The highlighted policy announcement dates capture a 22-business day window. is set to an average value of one during the benchmark sample, which includes the period where domestic policy rates are at or above 2%.

The most striking observation from these graphs is the difference between the responsiveness of the reserve currencies and the currencies of the small open economies. The exchange rates of the euro and pound generally behaved normally during the crisis, but are constrained in some periods (around 2011–2013 for the euro, and 2013–2014 for the pound). The Canadian dollar and Swedish krona, however, are more sensitive to news events through most of 2008 to 2015.

The responsiveness of exchange rates during the ZLB period varies by economy.Footnote5 In Canada and Sweden, the responsiveness of the exchange rate to news during the ZLB began to fall, but it still remained more responsive than in the benchmark period where exchange rates are considered to respond ‘normally’ to news. In the UK, a similar trend occurs but the exchange rate eventually becomes constrained. There is also evidence that the exchange rate became more sensitive near the beginning of 2015 as it was unclear whether the Fed or the Bank of England would be the first to raise interest rates.

The Eurozone is a special case because, once the European Central Bank (ECB) lowered its policy rate to what it had then deemed the ZLB,Footnote6 the exchange rate became more responsive to news. This may be owing to the fact that the ECB finally broke the imaginary wall between ‘nonstandard’ policies it had implemented since the crisis into more unconventional policies, including QE. Our sample, however, only reaches to the beginning of the ECB’s UMP package; therefore, the results are not conclusive. A final interesting observation is that the exchange rates of the small open economies become more responsive around an announcement of UMPs by the US Fed. This is less prevalent in the UK and the Eurozone.

The analysis also sheds light on the impact of UMP announcements and monetary policy communications on the exchange rate when policy rates approach the ZLB.Footnote7 In Canada and Sweden, the magnitude and significance of the coefficients on the tone of the US Fed monetary policy announcements increased during the ZLB period. In the UK and the Eurozone, however, it is the macroeconomic developments on both sides of the Atlantic that become more important.

While the coefficient on the US Fed UMP announcements dummy suggests that these policies contribute to an appreciation for foreign currencies relative to the US dollar, the results are only statistically significant for the euro and krona. We performed a separate analysis to identify the specific events that had the largest impact on exchange rates by taking the difference in the coefficient when a specific observation is included and excluded from the regression. The results reveal that the announcements concerning the first round of the US Fed’s QE programme and its extension in early 2009 had the largest impact on the coefficient. The announcements of the second and third QE programmes, however, had a sizeable impact only on the Canadian dollar. This took place as the Bank of Canada raised its policy rate twice in 2010 while the Fed funds rate remained at the ZLB. Similarly, announcements concerning the introduction of QE in the UK were generally associated with a depreciation of the currency, while the impacts of additional announcements were more muted. In this regard, the ECB’s UMP policy announcements stand apart because they remained relatively effective over time. In particular, the Securities Markets Programme and the policy package introduced from late 2014 to early 2015 were associated with a depreciation of the euro. Interestingly, the announcements regarding the Outright Monetary Transactions programme were associated with an appreciation of the euro, perhaps owing to greater confidence in the monetary union.

IV. Conclusion

Analysis reveals that the exchange rate responsiveness to news and central bank communication near the ZLB differ significantly depending on whether the domestic currency is a reserve currency or the currency of a small open economy. Exchange rates in the small open economies considered remain highly responsive to news when facing this constraint, and may become more responsive to monetary policy announcements of central banks in countries that host a reserve currency. Exchange rates between reserve currencies for the most part respond normally to news, especially in macroeconomic developments, but they appear to be more vulnerable to the ZLB constraint. Importantly, the announcement of UMPs can affect exchange rates after the ZLB has been reached; however, the impact of these policy announcements only appear to be significant if they are extraordinary, such as when QE1 was introduced in the US, and QE in the UK and the Eurozone.

RAEL_A_1181827_Supplementary_data.docx

Download MS Word (28.5 KB)Acknowledgement

Siklos is grateful to the BIS and the Hoover Institution at Stanford University where parts of this article were written and to CIGI for financing and supporting this research.

Disclosure statement

No potential conflict of interest was reported by the authors.

Supplemental Material

Supplemental data for this article can be accessed here.

Additional information

Funding

Notes

1 A risk premium term could be added; for simplicity this is set to zero.

2 Defined as , where

is the (log) of the price levels.

3 The derivation (not shown) requires that exchange rates satisfy some steady state in equilibrium.

4 The term effective zero lower bound (ZLB) refers to a boundary that was, at some point, deemed the lowest policy interest rate that the domestic central bank was willing to tolerate. Several years into the crisis, several central banks have acknowledged that the effective ZLB may be below zero and some have even introduced negative rates.

5 The US policy interest rate was constrained by the ZLB from December 2008 to the end of the sample period.

6 Dates are provided in the online appendix.

7 The results can be found in an online appendix.

References

- Bernanke, B. S. 2015. The Courage to Act: A Memoir of a Crisis and Its Aftermath. New York: W.W. Norton & Company.

- Carney, M. 2012. “Guidance.” Speech delivered at the CFA Society Toronto, Toronto, December 11.

- Draghi, M. 2014. “Monetary Policy Communication in Turbulent Times.” Speech delivered at the Conference De Nederlandsche Bank 200 years: Central banking in the next two decades, Amsterdam, April 24.

- Hart, R. P., J. P. Childers, and C. J. Lind. 2013. Political Tone: How Leaders Talk and Why. Chicago: University of Chicago Press.

- Swanson, E., and C. Williams. 2014. “Measuring the Effect of the Zero Lower Bound on Yields and Exchange Rates in the U.K. and Germany”, Journal of International Economics, v. 92 (April, Suppl. 1), pp. S2-S21.

- Yellen, J. 2013. “Communication in Monetary Policy.” Speech delivered at the Society of American Business Editors and Writers 50th Anniversary Conference, Washington, DC, April 4.