?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.ABSTRACT

This study investigates the effects of four types of terrorist attacks on three types of capital flow. We extend the literature by introducing a new measure of terrorist attacks, namely ‘attacks in big cities’ and empirically investigate its impact on capital flow. Drawing from a sample of seven South Asian countries over a time period of 27 years spanning 1990–2016, we found that terrorist attacks in big cities and capital flows are negatively related. In particular, the results show that terrorist attacks in big cities, in comparison to the other terrorist attacks forms, have the highest negative impact on the three types of capital flow.

I. Introduction

Investigating the macroeconomic consequences of terrorism remains a challenging task for policymakers, international institutions and scholars (Enders, Sandler, and Parise Citation1992; Enders and Sandler Citation2002; Feridun and Sezgin Citation2008; Abadie and Gardeazabal Citation2008; Polyxeni and Theodore Citation2019). Needless to say, there is a growing consensus among researchers and international institutions that terrorism will continue to be a major threat to global economic development (GTI Citation2017; Radic´ Nikši Citation2018). Theoretically speaking, terrorism is known to damage a country’s infrastructure and negatively affect its production activities, financial strength and stability (Blomberg, Hess, and Orphanides Citation2004; Fielding Citation2003), foreign trade (Nitsch and Schumacher Citation2004), tourism sector (Enders and Sandler Citation1991; Charfeddine and Goaied Citation2019), and inherently its capital flows (Enders and Sandler Citation1996). Furthermore, the obvious increased security costs and insurance premium ultimately result in a raise in uncertainty, instability as well as the cost of doing business (Gupta et al. Citation2004; Hotchkiss and Pavlova Citation2009). From an empirical standpoint, accumulated evidence shows that terrorist attacks have drastic effects on the performance of several economic indicators (Blomberg, Hess, and Orphanides Citation2004; Bandyopadhyay, Sandler, and Younas Citation2014).

Although recent research offers answers to some important questions related to the macroeconomic consequences of terrorism, other questions remain unanswered (Bagchi and Paul Citation2018). In particular, the question of whether or not different types of terrorism have the same impact on macroeconomic indicators is still yet to be addressed. In this paper, we focus on this very research question by investigating the effects of different types of terrorist attacks on distinct types of capital flow. More precisely, in addition to the existing types of terrorist attacks, we adopt a new approach by introducing a new measure, namely terrorism in big cities. The story line of the current research is to demonstrate that this newly introduced type of terrorist attacks will outperform the existing measures (i.e., global, domestic and transnational terrorism) in capturing the effect of terrorism on capital flows.

Terrorism is expected to disrupt production and commercial activities more severely in big cities than in small cites. This is mainly due to the fact that the majority of industrial and services organizations are logcated in big cities where it is easy to get access to talent and skilled labour as well as to plentiful resources and materials (Huang and Wei Citation2014). Of course, as suggested by the location theory, accessibility to various forms of resources is the key determinant of industrial location and capital flows (Huang and Wei Citation2014). In the same vein, Glaeser and Shapiro (Citation2002) support the view that big cities, historically, were the target of terrorist attacks inasmuch as terrorists expect that the damage will be of large scale in urban areas, especially in big cities. In fact, ‘cities are more susceptible to this form of political violence (terrorism) than rural areas because of the likelihood of greater impact and visibility’ (Beall Citation2006?). It goes without saying that foreign investors will become more reluctant and cautious to invest in countries where big cities are often targeted by terrorism (Glaeser and Shapiro 2002; Beall Citation2006).

Although the adverse effects of terrorist attacks in big cities have been alluded to in the literature, there are no empirical attempts that investigated its relative economic impact in comparison to other kinds of terrorist attacks. The current research pursues this line by empirically testing the following proposition:

Proposition: “Terrorist attacks in metropolitan and big cities might affect economic conditions more severely than terrorist attacks in small cities or in the borders of the country”.

Particularly, we believe that the South Asian region is a good case in point. Despite its high ranking in regional trends of terrorism, the South Asian region has rarely been investigated in the terrorism literature. In fact, this region was ranked second in 2017 (GTI Citation2017).Footnote1 The South Asian countries have spent millions of dollars on counter-terrorism and military expenditures. However, these countries are still unable to foster a stable economic environment. In worldwide terrorism, the majority of terrorist attacks happened in Afghanistan (23%), India (9%) and Pakistan (7%). As a result, South Asia is associated with an economic environment of insecurity, high risk and instability (Shahzad et al. Citation2020). One particularity of the South Asia region is that capital flows are the main driver of the economic development of this region (Filer and Stanišić Citation2016). In this regard, the high terrorism-related risks hinder the expansion of capital flows and investment decisions in South Asia (Abadie and Gardeazabal Citation2008; Filer and Stanišić Citation2016). As such, the South Asia region represents a plausible context to empirically investigate the link between terrorist attacks in big cities and capital flows.

II. Data and materials

Data and description of the variables

The dataset used in this study covers a time period of 27 years (from 1990 to 2016). It includes a sample of seven South Asian countries: Afghanistan, Bangladesh, India, Indonesia, Nepal, Pakistan and Sri Lanka.Footnote2 The data on the capital flow types (foreign direct investment (FDI), portfolio investments and external debt), the real GDP per capita, military expenditure as a percentage of GDP, terms of trade and exchange rates were drawn from the 2017’s World Development Indicators. The financial openness data were gathered from financial openness indexFootnote3 developed by Chinn and Ito (Citation2016). Finally, the terrorist attack data were extracted from the Global Terrorism Database (https://www.start.umd.edu/gtd/).

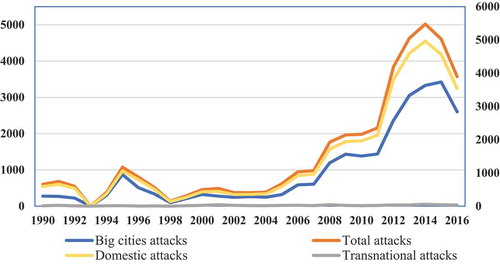

shows the evolution of the number of terrorist attacks by type (total, domestic, transnational and attacks in big cities). It shows that transnational attacks are small in number compared to the three other types of terrorist attacks. This is confirmed by the results reported in , which depicts the number of total, domestic, transnational, and big city attacks as a percentage for each country over the period 1990–2016.

Figure 1. Terrorist attacks by types over the period 1990–2016

Table 1. Number and percentage of terrorist attacks per country (1990–2016)

shows evidence of a negative correlation between the different types of terrorist attacks (total, domestic and big city attacks) and the three variables of capital flow (FDI, portfolio investments and debt stocks) for 10 out of 12 cases. In particular, big city terrorist attacks have the highest negative correlation with portfolio investments and debt stocks, and the lowest correlation with FDI.

Table 2. Descriptive statistics and correlation analysis

Materials and methods

We use a dynamic panel data model, which takes the general form given by:

where, denotes time-invariant country fixed effects,

are year fixed effects that account for time-varying common shocks,

refers to the type of capital inflow (FDI, portfolio investments or external debt) expressed as a share of GDP for country

in time

,

denotes the type of terrorist attack (total, domestic, transnational and big city attacks) measured per 100,000 persons and

is a vector of control variables (GDP per capita, military expenditure, trade openness, financial openness, exchange rate and terms of trade). In all the considered equations, the real GDP per capita and military expenditure were used as control variables. Military expenditure was used to control for peace, stability and lowering the risk in that country, expressed as percentage of GDP (Enders and Sandler Citation1993; Feridun and Shahbaz Citation2010). Moreover, other specific control variables were used for each type of capital flow. For instance, we have included trade and financial openness in the FDI equation. In addition, exchange rate and terms of trade were used as control variables for the portfolio investment and external debt stock equations. We expect that depreciation in the local currency will attract more capital inflow, as this makes the country’s exports more competitive internationally. Similarly, terms of trade, depicting the level of uncertainty in the balance of payments and fiscal positions, are expected to have a significant impact on external debts and portfolio investments.

For the sake of the results’ robustness, we use different econometric techniques including fixed effect models (where the lagged dependent variable is dropped from EquationEquation 1)(1)

(1) and dynamic models estimated using different techniques such as the feasible generalized least squares, the difference generalized method of moments, and the system of generalized methods of moments estimation techniques.Footnote4

III. Results and discussion

A summary of the results is reported in where only the estimated coefficients associated with the four variables (total, domestic, transnational and big city attacks) are reported.Footnote5 Except for the transnational type of terrorist attack, the results show that for all the other three types of terrorist attacks, the coefficients are in the expected direction (i.e., negative sign) and most of them are significant at conventional levels (5%). Interestingly, big city terrorist attacks have the greatest magnitude of effect on foreign investments, implying that the geographical location of the terrorist attack is a key determinant of FDI flows. This suggests that, as opposed to the earlier literature, domestic and transnational attacks might not be very relevant variables for accessing economic disruption. In fact, the study’s results show that when countries experience terrorist attacks in big cities, the amount of FDI in these countries decreases significantly in comparison to the other types of terrorist attacks.

Table 3. Results estimations of the terrorist attacks impact on capital flows by component

The results for the portfolio investments equation reveal evidence of a negative impact for all types of terrorist attacks (again with transnational attacks being reported as an exception). Similar to the FDI equation, the impact of terrorist attacks in big cities is much higher than those of the two other types. Also, the results show that the domestic, total, and big city terrorist attacks have significant negative effects on external debt. In particular, the results show that attacks in big cities and urban areas have a greater adverse impact on external debt stocks and government borrowings than total and domestic terrorist attacks. This result is consistent with the findings of Hotchkiss and Pavlova (Citation2009), who conclude that the 9/11 attacks reduced labour force participation during working hours because of an increased risk.

Regarding the control variables, we find that GDP, financial openness, trade and terms of trade have a positive significant impact on the three capital flow types. This result is consistent with previous studies (Bandyopadhyay, Sandler, and Younas Citation2014; Polyxeni and Theodore Citation2019). The trade and financial openness findings imply that economic openness and low restrictions on capital transactions play a positive role in attracting investment flows. Military expenditure has a significant negative impact on all types of capital flows, which is in line with some prior studies (e.g., Polyxeni and Theodore Citation2019). Also, we find that currency depreciation has a negative impact on capital flows.

IV. Concluding remarks

We introduced a new measure of terrorist attacks, namely terrorism in big cities to investigate the effect of different types of terrorism on capital flows for a sample of seven South Asian economies. The results show that terrorism in big cities or metropolitan areas, in comparison to other terrorist attacks types, has the highest adverse effects on all the three forms of capital flows. The results indicate that terrorist attacks in big cities are a key hindrance for capital flows in South Asian countries. Consequently, more attention should be paid to this type of terrorism.

Acknowledgments

Open Access funding provided by the Qatar National Library.

We are grateful to the anonymous reviewers’ for their valuable input and helpful suggestions.

Disclosure statement

No potential conflict of interest was reported by the authors.

Notes

1 The South Asian region has witnessed 3430 terrorist attacks with 7664 causalities (GTI Citation2017).

2 Major attacks in South Asia: Mumbai attacks (2008) known as 26/11 in India, APS Peshawar attacks (2014) in Pakistan, Church attacks in Indonesia in 2016 to 2018.

3 See the International Monetary Fund’s Annual Report on Exchange Agreements and Exchange Restrictions at

4 The main reason behind the use of these different estimation techniques is that each method has some advantages as solving the endogeneity problem (see Baltagi, Demetriades, and Law Citation2009; Shahzad et al. Citation2020).

5 The detailed results based on all the estimated methods are reported in the Appendix .

References

- Abadie, A., and J. Gardeazabal. 2008. “Terrorism and the World Economy.” European Economic Review 52 (1): 1–27. doi:https://doi.org/10.1016/j.euroecorev.2007.08.005.

- Bagchi, A., and J. A. Paul. 2018. “Youth Unemployment and Terrorism in the MENAP (Middle East, North Africa, Afghanistan, and Pakistan) Region.” Socio-Economic Planning Sciences 64 (December 2017): 9–20. doi:https://doi.org/10.1016/j.seps.2017.12.003.

- Baltagi, B., P. Demetriades, and S. H. Law. 2009. “Financial Development and Openness: Evidence from Panel Data.” Journal of Development Economics 89 (2): 285–296. doi:https://doi.org/10.1016/j.jdeveco.2008.06.006.

- Bandyopadhyay, S., T. Sandler, and J. Younas. 2014. “Foreign Direct Investment, Aid, and Terrorism.” Oxford Economic Papers 66 (1): 25–50. doi:https://doi.org/10.1093/oep/gpt026.

- Beall, J. (2006), Cities, terrorism and development. Journal of International Development, 18: 105–120.

- Blomberg, S. B., G. D. O. Hess, and A. Orphanides. 2004. “The Macroeconomic Consequences of Terrorism.” Journal of Monetary Economics 51 (5): 1007–1032. doi:https://doi.org/10.1016/j.jmoneco.2004.04.001.

- Charfeddine, L., and M. Goaied. 2019. “Tourism, Terrorism and Political Violence in Tunisia: Evidence from Markov-switching Models.” Tourism Management 70: 404–418. doi:https://doi.org/10.1016/j.tourman.2018.09.002.

- Chinn, M., and H. Ito. 2016. “Finan-open-chinn-ito-index, Financial Openness Index.” http://www.cesifo-group.de/ifoHome/facts/DICE.html

- Enders, W., and T. Sandler. 1991. “Causality between Transnational Terrorism and Tourism: The Case of Spain.” Terrorism 14 (1): 49–58. doi:https://doi.org/10.1080/10576109108435856.

- Enders, W., and T. Sandler. 1993. “The Effectiveness of Anti-terrorism Policies: A Vector-autoregression-intervention Analysis.” American Political Science Review 87 (4): 829–844. doi:https://doi.org/10.2307/2938817.

- Enders, W., and T. Sandler. 1996. “Terrorism and Foreign Direct Investment in Spain and Greece.” Kyklos 49 (3): 331–352. doi:https://doi.org/10.1111/j.1467-6435.1996.tb01400.x.

- Enders, W., and T. Sandler. 2002. “Patterns of Transnational Terrorism, 1970–1999: Alternative Time-series Estimates.” International Studies Quarterly 46 (2): 145–165. doi:https://doi.org/10.1111/1468-2478.00227.

- Enders, W., T. Sandler, and G. F. Parise. 1992. “An Econometric Analysis of the Impact of Terrorism on Tourism.” Kyklos 45 (4): 531–554. doi:https://doi.org/10.1111/j.1467-6435.1992.tb02758.x.

- Feridun, M., and M. Shahbaz. 2010. “Fighting Terrorism: Are Military Measures Effective? Empirical Evidence from Turkey.” Defence and Peace Economics 21 (2): 193–205. doi:https://doi.org/10.1080/10242690903568884.

- Feridun, M., and S. Sezgin. 2008. “Regional Underdevelopment and Terrorism: The Case of South Eastern Turkey.” Defence and Peace Economics 19 (3): 225–233. doi:https://doi.org/10.1080/10242690801972196.

- Fielding, D. 2003. “Counting the Cost of the Intifada: Consumption, Saving and Political Instability in Israel.” Public Choice 116 (3/4): 297–312. doi:https://doi.org/10.1023/A:1024831518541.

- Filer, R. K., and D. Stanišić. 2016. “The Effect of Terrorist Incidents on Capital Flows.” Review of Development Economics 20 (2): 502–513. doi:https://doi.org/10.1111/rode.12246.

- Glaeser, E. L., and J. M. Shapiro. (2002). Cities and Warfare: The Impact of Terrorism on Urban Form. Journal of Urban Economics, 51(2): 205–224.

- GTI. 2017. Measuring and Understanding the Impact of Terrorism. Institute for Economics and Peace.

- Gupta, S., B. Clements, R. Bhattacharya, and S. Chakravarti. 2004. “Fiscal Consequences of Armed Conflict and Terrorism in Low- and Middle-income Countries.” European Journal of Political Economy 20 (2): 403–421. doi:https://doi.org/10.1016/j.ejpoleco.2003.12.001.

- Hotchkiss, J., and O. Pavlova. 2009. “The Impact of 9/11 on Hours of Work and Labour Force Participation in the US.” Applied Economics Letters 16 (10): 999–1003. doi:https://doi.org/10.1080/13504850701250252.

- Huang, H., and Y. D. Wei. 2014. “Intra-metropolitan Location of Foreign Direct Investment in Wuhan, China: Institution, Urban Structure, and Accessibility.” Applied Geography 47: 78–88. doi:https://doi.org/10.1016/j.apgeog.2013.11.012.

- Nitsch, V., and D. Schumacher. 2004. “Terrorism and International Trade: An Empirical Investigation.” European Journal of Political Economy 20 (2): 423–433. doi:https://doi.org/10.1016/j.ejpoleco.2003.12.009.

- Polyxeni, K., and M. Theodore. 2019. “An Empirical Investigation of FDI Inflows in Developing Economies: Terrorism as a Determinant Factor.” The Journal of Economic Asymmetries 20(e00125. doi:https://doi.org/10.1016/j.jeca.2019.e00125.

- Radic´ Nikši, M. 2018. “Terrorism as a Determinant of Attracting FDI in Tourism : Panel Analysis.” Sustainability 10 (4553): 1–17. doi:https://doi.org/10.3390/su10124553.

- Shahzad, U., S. Sarwar, M. U. Farooq, and F. Qin. 2020. “USAID, Official Development Assistance and Counter Terrorism Efforts: Pre and Post 9/11 Analysis for South Asia.” Socio-Economic Planning Sciences 69 (January): 100716. doi:https://doi.org/10.1016/j.seps.2019.06.001.

Appendix

Table A1. Empirical results of fixed effects, FGLS, DGMM and SGMM (dependent variable: FDI)

Table A2. Empirical results of fixed effects, FGLS, DGMM and SGMM (dependent variable: Portfolio stocks)

Table A3. Empirical results of fixed effects, FGLS, DGMM and SGMM (dependent variable: External debts)