?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.ABSTRACT

This paper investigates trends in intangibles investment since the onset of the COVID-19 pandemic in the United Kingdom. Responses from an online survey show that investment in R&D has dropped substantially for many firms but that over 40% of firms increased their ICT investment, which is likely to reflect the need to facilitate remote working and customer engagement. Industry is a major predictor of the change in intangibles investment. This is consistent with expectations in light of the different effect that measures to contain the pandemic have had across industries.

KEYWORDS:

I. Introduction

The COVID-19 pandemic has had profound effects on the world economy (International Monetary Fund Citation2021). In the United Kingdom (UK), Bank of England figures suggest that it has led to the largest fall in GDP since 1709 (Hills, Thomas, and Dimsdale Citation2010; Office for Budget Responsibility Citation2021). While the short-run effects of the early stages of the pandemic are now well understood, less is known about its implications for growth in the medium to long-term. This paper aims to address this by analysing, firstly, trends in intangibles investment since March 2020 when the UK entered its first ‘lockdown’ and, secondly, changes in the distribution of intangibles investment across firms. Intangibles investment is measured by research and development (R&D) spending and investment in information and communications technology (ICT), which previous literature has shown are significant determinants of productivity and growth (Dal Borgo et al., Citation2013).

The effect of recessions on intangibles investment is theoretically ambiguous. A pro-cyclical relationship is expected if recessions lower the potential returns from or decrease the resources available for intangibles investment but the lower opportunity cost of investing when demand is lower suggests a counter-cyclical relationship (Geroski and Walters Citation1995). However, because intangible capital is often scalable, intangible investment has the characteristics of a fixed cost (De Ridder Citation2019), which suggests that it will be less cyclical than other forms of investment. Moreover, the knowledge embedded in the human capital of R&D workers and the length of time of R&D projects creates a disincentive for firms to make R&D workers redundant. Since their wages account for a high proportion of R&D investment, this also suggests that R&D investment may be less responsive to the business cycle (Hall and Lerner Citation2010). The empirical evidence is generally supportive of a pro-cyclical relationship (Barlevy Citation2007; Filippetti and Archibugi Citation2011; Fabrizio and Tsolmon Citation2013) and cross-country data shows that intangibles investment declined more than tangibles investment in Europe during the Great Recession (Roth Citation2020). But since the recession caused by COVID-19 is unique, both in its origins and policy response from government, the conclusions from previous studies may not apply.

The next section discusses the data and methodology. The third section presents the results. The final section concludes.

II. Data and methodology

The data was collected from an online survey of UK firms conducted by the authors (further information is available in the Supplementary Material). The target population was active companies in the UK with a minimum of seven employees in the Orbis database (Bureau van Dijk Citation2020). This yielded 4,529 responses between October and November 2020. Firms that invested in R&D or ICT in the year to March 2020 (22.9% or 23.7%, respectively, of the total) were asked to answer, on a slider scale from −100 to 100, with step sizes of 10, by what percentage their investment had changed compared to the year to March 2020.Footnote1 Information was also obtained on a range of variables that are described in . Comparison of the characteristics of respondents with those in the wider population show that the respondents represent a broad range of UK firms (see Table S1 in the Supplementary Material) but the results below are nevertheless weighted to ensure representativeness (unweighted results are provided in the Supplementary Material).

Table 1. Variable descriptions

To test whether intangibles investment has declined, a one-tailed t-test is conducted of the null hypothesis that the mean of the change in intangibles investment is greater than or equal to zero. To analyse which firms experienced the largest changes in their intangibles investment the following model is estimated:

where is the percentage change in investment in R&D or ICT. and

are the natural logarithms of employment and age respectively.

,

, and

are binary variables indicating whether the firm is family owned, operates in more than one location and has workplaces in other countries, respectively. Also included in the model are industry dummies, region dummies, source of input dummies and main market dummies.

Because the dependent variable is top-coded at 100, we experimented with the use of a Tobit model (the results are provided in Table S4 in the Supplementary Material). A Heckman model was also estimated to address any selection bias arising from the non-random selection of firms into R&D (Table S5). In addition, probit and logit models were estimated using a binary variable indicating whether was greater than or equal to zero as the dependent variable (Tables S6 and S7). The use of these alternative specifications did not change the main conclusions from the analysis.

III. Results

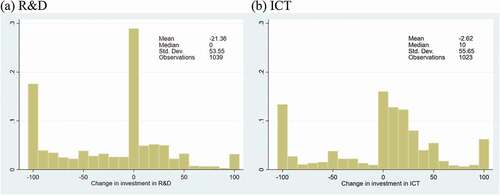

Histograms of responses to the questions on the change in R&D and ICT investments are provided in . In the case of R&D investment ()), many firms (29%) reported no change to their R&D investments since the onset of the pandemic. However, a larger proportion (45%) stated that they had reduced rather than increased their investment in R&D (26%) and almost 18% reported that they had stopped R&D investment altogether. A t-test of the null hypothesis that the mean change in R&D investment is greater than or equal to zero leads to rejection of the null at the 1% level. There is therefore strong evidence that R&D investment has decreased during the pandemic, which is likely to have serious repercussions for productivity growth in the medium to longer-term.

Figure 1. Histogram of change in investment in

A different pattern emerges for ICT investment ()). While 13% of firms stopped investing in ICT, over 40% of firms increased their ICT investment. The null that the mean change in ICT investment is non-negative is not rejected at the 5% level. This finding is likely to be the result of firms having to invest in ICT to facilitate working from home and remote engagement with customers. Whether such investment will enhance growth in the medium to long-term depends upon the extent to which employers continue to allow their employees to work from home and how productively people can work from home. The relatively small literature on the latter question suggests that remote working may have positive effects on productivity (Bloom et al. Citation2015; Choudhury, Foroughi, and Larson Citation2021) and therefore that this type of investment is likely to be growth enhancing.

The remainder of the analysis aims to explain the heterogeneity in responses observed in and hence to understand how the pandemic has changed the distribution of intangibles investment across firms. The results in (Table S8 provides standard errors) show that industry is a strong predictor of the change in intangibles investment. For R&D, relative to the baseline industry (manufacturing), significant negative associations are obtained for seven of 10 service industries and the industry dummies are jointly significant. The importance of industry is expected since the effect of the measures taken by the government to contain the pandemic differed across sectors, with several industries being unable to operate for significant periods.Footnote2 Region plays less of a role: compared to the South East of England, R&D investment declined less in only Yorkshire/Humberside, the East Midlands and Wales. While the main source of inputs (reflecting backward supply-chains) does not predict changes in R&D, there is some evidence that selling the largest share of output to the rest of the UK and, especially, to the rest of the world is positively associated with the change in R&D. One implication of our results is therefore that more internationally-oriented manufacturing firms experienced relatively small reductions in R&D.

Table 2. Results from OLS estimation of EquationEquation (1)(1)

(1)

For ICT, industry also played an important role with eight sectors having significantly higher investment than manufacturing. There is less evidence of regional heterogeneity in the change in ICT investment than for R&D investment but having multiple workplaces in the UK was positively associated with the change in ICT investment. Firms for which their main market was overseas (but not the EU) experienced, ceteris paribus, a smaller decline in ICT investment.

IV. Conclusion

This paper investigates the effect of the COVID-19 pandemic on intangibles investment. Responses from a survey of UK firms shows that investment in R&D had fallen substantially. This suggests that the COVID-19 pandemic will have long-lasting negative effects on productivity and hence growth. For ICT, the fall in investment was far smaller, which is likely to reflect the need for firms to facilitate remote working and customer engagement. The fall in intangibles investment is distributed unevenly across firms, with industry playing a major role in predicting the change in investment and internationally-oriented firms experiencing smaller declines in the early stages of the pandemic.

Supplemental Material

Download MS Word (399 KB)Disclosure statement

No potential conflict of interest was reported by the author(s).

Supplementary material

Supplemental data for this article can be accessed here.

Additional information

Funding

Notes

1 For R&D, the question was: ‘How has your organisation’s spending on R&D (research & development) in the UK changed compared to the year up to March 2020?’

2 For example, hotels and restaurants in England were closed from the 23rd March to the 4th July and belonging to the accommodation and food services sector is associated with a decline of 38 percentage points in R&D investment.

References

- Barlevy, G. 2007. “On the Cyclicality of Research and Development.” American Economic Review 97 (4): 1131–1164. doi:https://doi.org/10.1257/aer.97.4.1131.

- Bloom, N., J. Liang, J. Roberts, and Z. J. Ying. 2015. “Does Working from Home Work? Evidence from a Chinese Experiment.” The Quarterly Journal of Economics 130 (1): 165–218. doi:https://doi.org/10.1093/qje/qju032.

- Bureau van Dijk. 2020. “Orbis.” https://orbis.bvdinfo.com/

- Choudhury, P., C. Foroughi, and B. Larson. 2021. “Work-from-Anywhere: The Productivity Effects of Geographic Flexibility.” Strategic Management Journal 42 (4): 655–683. doi:https://doi.org/10.1002/smj.3251.

- Dal Borgo, M., P. Goodridge, J. Haskel, and A. Pesole. 2013. “Productivity and Growth in UK Industries: An Intangible Investment Approach.” Oxford Bulletin of Economics and Statistics 75 (6): 806–834. doi:https://doi.org/10.1111/j.1468-0084.2012.00718.x.

- De Ridder, M. 2019. “Market Power and Innovation in the Intangible Economy.” Cambridge Working Papers in Economics No. 1931.

- Fabrizio, K., and U. Tsolmon. 2013. “An Empirical Examination of the Procyclicality of R&D Investment and Innovation.” Review of Economics and Statistics 96 (4): 662–675. doi:https://doi.org/10.1162/REST_a_00412.

- Filippetti, A., and D. Archibugi. 2011. “Innovation in Times of Crisis: National Systems of Innovation, Structure, and Demand.” Research Policy 40 (2): 179–192. doi:https://doi.org/10.1016/j.respol.2010.09.001.

- Geroski, P., and C. Walters. 1995. “Innovative Activity over the Business Cycle.” The Economic Journal 105 (431): 916–928. doi:https://doi.org/10.2307/2235158.

- Hall, B., and J. Lerner. 2010. “The Financing of R&D and Innovation.” In Handbook of the Economics of Innovation, edited by B. Hall and N. Rosenberg, 609–639, Amsterdam: North-Holland.

- Hills, S., R. Thomas, and N. Dimsdale. 2010. “The UK Recession in Context — What Do Three Centuries of Data Tell Us?” Bank of England Quarterly Bulletin 50 (4): 277–291.

- International Monetary Fund. 2021. “World Economic Outlook Update.” https://www.imf.org/en/Publications/WEO/Issues/2021/01/26/2021-world-economic-outlook-update

- Office for Budget Responsibility. 2021. “Welfare Trends Report.” https://obr.uk/wtr/welfare-trends-report-march-2021/

- Roth, F. 2020. “Revisiting Intangible Capital and Labour Productivity Growth, 2000–2015.” Journal of Intellectual Capital 21 (5): 671–690. doi:https://doi.org/10.1108/JIC-05-2019-0119.