?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This research analyses high-frequency data of the cryptocurrency market in regards to intraday trading patterns related to algorithmic trading and its impact on the European cryptocurrency market. We study trading quantitatives such as returns, traded volumes, volatility periodicity, and provide summary statistics of return correlations to CRIX (CRyptocurrency IndeX), as well as respective overall high-frequency based market statistics with respect to temporal aspects. Our results provide mandatory insight into a market, where the grand scale employment of automated trading algorithms and the extremely rapid execution of trades might seem to be a standard based on media reports. Our findings on intraday momentum of trading patterns lead to a new quantitative view on approaching the predictability of economic value in this new digital market.

1. Motivation

High-frequency trading takes advantage of the incredible rise of computing power provided by the steady development of ever more capable structures. Algorithms are already major players in a variety of financial applications and have proven to be more efficient than their human counterparts. By employing these so-called ‘algos’, positive effects can be exploited to their maximum and market inefficiencies can potentially be eliminated (Härdle, Harvey, and Reule Citation2020). However, just like for every coin, there is a flipside, such as the negative impact on capital markets caused by technological inefficiencies (Emem Citation2018). One of the most noted events of an early point of attack for these algorithms was the Flash Crash of 2010.

No matter what, the machines are here to stay and their influence, possibly powered by ‘learning’ algorithms, will certainly increase even more with time – especially in regards to new emerging markets such as cryptocurrencies. The rising popularity and acceptance of this alternative asset, as it has yet to be understood as an alternative to fiat currency, requires for specialized strategies to maximize the potential return of investments (Akhtaruzzaman, Sensoy, and Corbet Citation2019; Platanakis and Urquhart Citation2019; Trimborn et al. Citation2018; Petukhina et al. Citation2020).

Yet, did the quantlets or algorithms really venture in the realm of autonomous machines, the digital world, or are they still with the world of the humans, the world of manual labor oil and baby nutrition companies?

This is especially of interest since the cryptocurrency market has significantly matured in recent years and has attracted enormous investments, not only by major players but especially by individuals. Especially FinTech Startups are of high interest, as absurd amounts of financial backing was (and is still to some extent) being generated by just presenting a briefly written Whitepaper-PDF marketing outlet (Zetzsche et al. Citation2019). The early cryptocurrency market kick-off starting in late 2017 is evidently presenting such happenings. The discrepancy between sentiment and tone generated by marketing versus the delivered performance is fascinating (with further references (Härdle, Harvey, and Reule Citation2020; Chen et al., “What makes cryptocurrencies special,” Citation2019; Qian, Tu, and Härdle Citation2019).

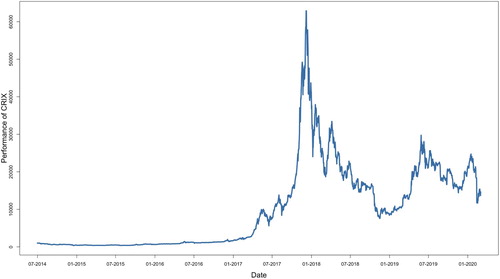

In this research, we are analyzing high-frequency data (5-minute intervals) gained from the cryptocurrency market and see, if there is really 24/7 algorithmic trading, or if there are still people sitting behind their computers creating and executing orders by hand after they have returned from their daily jobs (Figure ).

Figure 1. CRIX time series (https://github.com/QuantLet/CrixToDate/tree/master/CTD_CRIX_Full_24h/Full).

Previous research outputs on this theme, such as Zhang et al. (Citation2019), have used time spans ranging from 1 hour to 12 hours. Their methods yielded results, which lead to different conclusions, yet opened up further thoughts towards factors such as trading patterns, variations in returns, volatility and trading volume. Zhang et al. (Citation2018) are also looking at the same aspects as the previous research, with the additional finding of a power-law correlation between price and volume. Röschli et al. (Citation2017), respectively, build a uni- and multivariate analysis of quantitative facts to show off stylized facts of cryptocurrencies. Schnaubelt, Rende, and Krauss (Citation2019) analyzed limit order data from cryptocurrency exchanges. Besides their recovery of common qualitative facts, they find that these data exhibit many of the properties found for classic limit order exchanges, such as a symmetric average limit order book, the autocorrelation of returns only at the tick level and the timing of large trades. Yet they find that cryptocurrency exchanges exhibit a relatively shallow limit order book with quickly rising liquidity costs for larger volumes, many small trades and an extended distribution of limit order volume far beyond the current mid-price.

Given the search for the most efficient trading strategies, Caporale and Plastun (Citation2019) provide a range of historic scientific works on the time of day effects to reap abnormal profits. In contrast to their work, we aim at identifying the market drivers, which are responsible for how this new emerging market, which is still full of conundrums for many, behaves – i.e. do market movements fit into human activity patterns or are these independent from time.

Preliminary research has therefore not touched the highly topical question of human impact in the wake of digital systems. There are many papers with interesting approaches and solutions, but only for problems that are already known and have been rebrewn for some time now. Yet, with the advent and popular discussion of the employment of Long Short Term Memory Neural Networks (LSTM) and hence deep learning for finance, AI advisory, essentially based on the human factor of sentiment in the realm of cryptocurrencies (Chen et al., “What makes cryptocurrencies special,” Citation2019), will play a major role in especially this completely digital market. This, as a circular argument, brings us once again to the fundamental idea of enforcing the understanding of market behavior based on the time of the day and the agents acting in these markets that are predestined to be ruled by the machines.

As a polemic term, we are using (PoH; derived from

,

et cetera consensus algorithms) to underline the hypotheses that not algorithms are the major players in this market, but humans. Humans do not act as programmed like algorithms – they act based on biological and psychological input, such as hunger or fatigue. The majority of humans will have certain times at which they are active, and at which they rest and are therefore inactive. Alternatively spoken, algorithms need humans to start and then exacerbate a price trend – the question is, therefore if the cryptocurrency market is dominated by human or algorithmic behavior. Eventually, we can differentiate algorithmic and human trading patterns expressed within the market (with further references Caporale et al. Citation2016).

The paper is structured by giving a brief general introduction and data source disclosure and methodology section, followed by a respective intraday data analysis, which is concluded by a section on Time-Of-Day effects and the Proof-Of-Human.

All presented graphical and numerical examples shown are reproducible and can be found on www.quantlet.de (Borke and Härdle Citation2018) and are indicated as CCID.

2. High-frequency cryptocurrency data

To understand the dynamics of this new high-frequency market, it is mandatory to investigate the statistical properties of various high-frequency variables, for example, trading volume or volatility, to find respective answers to questions like option pricing and forecasting. Preliminary research to visualize the cryptocurrency market was done by Trimborn and Härdle (Citation2018) with the CRyptocurrency IndeX, CRIX (crix.berlin), in order to represent the performance of the cryptocurrency market with the help of the most mature and accepted cryptocurrencies, such as Bitcoin (BTC), Ethereum (ETH), or Ripple (XRP) – see appendix A.1 for further used abbreviations. As the CRIX index family covers a range of cryptocurrencies based on different liquidity rules and various model selection criteria, we have chosen this as the main data source. CRIX represents the cryptocurrency market, but by its very nature is dominated by a few main players with BTC being the absolute market driver over time.

Furthermore, we used data provided by dyos solutions GmbH (dyos.io) compiled from various exchanges' data, to ensure that our findings are coherent with other data available. It is important to keep in mind, that the 5-minute data analyzed in this research is gained from sources located in the European markets (+1h GMT) and therefore the time-of-day effects may look different for markets from the Americas or Asia. We will make an exegesis on this important point in Section 3.3.

In addition, the analyzed data sample belongs to the time period after the cryptocurrency market heated up immensely around the end of 2017, followed by a sharp cooldown at the beginning of 2018. By that time a plethora of euphoric media outlets was praising the endless possibilities which the blockchain technology may provide – and what eventually also lead to quite a lot of ICO scams (Zetzsche et al. Citation2019). At that time, algorithmic trading in cryptocurrency markets was not seen as being a mere idea, but reality by more or less promising FinTech startups. These emerging enterprises are offering a wide variety of blockchain-related services, such as trading, asset management, or technical support. Especially FinTech startups related to the financial sector, in contrast to for example supply chain oriented ventures, are heavily interested in ArtificialIntelligence (‘learning’ algorithms) and are marketing their individual related products as groundbreaking and ready-to-use. Given the chosen typical vacation period, July and August, one should hence expect a less pronounced human, but algorithmic-driven market behavior to contradict the hypotheses of the PoH concept – more on that as well in Section 3.3.

Regarding data handling, we are coherent with previous research on high-frequency data based on traditional data sources, such as the NYSE, which has underlined data preparation issues and the specific statistical properties of various high-frequency variables (Hautsch Citation2011). As we are dealing with a subject, where individuals can act directly with the market without involving a middle-man, the characteristics of our data observed on transaction level, therefore, are especially irregularly spaced in time and without interruption – see Section 3.

3. Intraday data analysis

In the following chapter, we provide an overview of the methods employed to analyze our high-frequency data at hand with further statistical intraday cryptocurrency market observations.

3.1. Methodology

This paper undertakes a fresh empirical investigation of key financial variables of cryptocurrency market, such as volatility, returns and trading volume. Following, for example, Hussein (Citation2011), intraday return volatility is calculated as absolute log-returns as defined in (Equation2(2)

(2) ). As we are looking at high-frequency data, there is no need to use measures like, for example, the compounded annual growth rate (CAGR) instead of absolute returns, which is used to get the per-annum returns and does not support the analysis in this case.

The simple return is defined as

(1)

(1) where

und

are prices of coins at time points t and t−1, respectively. The log return

is defined as

(2)

(2) In order to expressively visualize some features of our high dimensional and nonstationary time series gained from our large high-frequency dataset of the specifically chosen period of time, a Generalized Additive Model (GAM) is best suited. A GAM is a generalized linear model (GLM), where the nonlinear predictor is given by a specified sum of smooth functions of the covariates, as well as a conventional parametric component of the linear predictor (Härdle Citation1990). The basic advantage of GAM is the possibility to model highly complex nonlinear relationships given a large number of potential predictors. In particular, recent computational developments in GAM fitting methods, such as Wood, Goude, and Shaw (Citation2015), Wand (Citation2017), and Wood (Citation2017), have made it possible to use these models to explore very large datasets. Moreover, in the last two decades, GAM methods have intensively developed in terms of the range of models that can be fitted. All these advantages make GAMs a feasible tool to investigate intraday seasonality patterns with high-frequency trading data. In general, the model has a structure something like:

(3)

(3) where

observation of a response variable Y, g is a link function (identical, logarithmic or inverse, etc.),

are independent variables,

is an intercept,

are unknown nonparametric smooth functions, and

is an i.i.d. random error. In our application we use the identity link function, since the LHS of our equations are features/variables observed or measured on a continuous scale, to fit the following statistical model:

(4)

(4) Here

will be a trading volume, volatility, or returns as defined in (Equation2

(2)

(2) ),

will be the daily and weekly effects. The nonlinear function

is a smooth function, composed by sum of basis functions

(for example B-splines, P-splines or cubic splines) and their corresponding regression coefficients

. Thus, each function

is expressed as:

(5)

(5) where

is the dimension of the spline basis.

The smooth function is estimated by penalized regression:

(6)

(6) where the penalty parameter

is a smoothing parameter controlling the fit-smoothness trade-off for

and can be selected by minimization of the Generalized Cross Validation (GCV) score, see Wood (Citation2004, Citation2011). Denoting B the matrix formed by concatenation of the

, one has to solve the following problem:

(7)

(7) where

is the vector of the unknown regression parameters,

is a matrix of known coefficients (a smoothing matrix) and depends on the spline basis. Thus, given λ, expression (Equation7

(7)

(7) ) may readily be minimized to yield the coefficient estimates

. The method of obtaining the estimate of the β is called Penalized Iteratively Re-weighted Least Squares (P-IRLS) which is implemented in the mgcv R package, see Wood (Citation2019).

3.2. Summary statistics

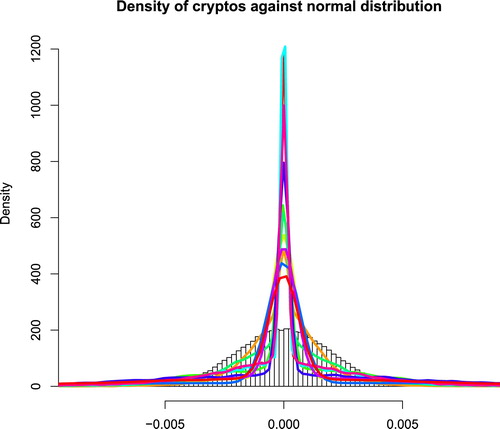

As an introduction to the data analyzed in this brief research, we are providing summary statistics regarding its statistical properties to form a basic understanding of the market at hand. Firstly, the trading data density of cryptocurrencies against the normal distribution of BTC is far from normally distributed, see Figure . Hence the behavior of agents in this market is far from what we would see in classic markets. This implies that new rules are being employed, and therefore we have to rethink our common way on how to approach the quantitative analysis of markets in general. We will start our discussion on the specific research question by first providing a general overview of the cryptocurrency market with increasingly narrowed focus and attention to detail regarding specific timeframes and parameters for individual crypto-assets.

Figure 2. Density of intraday CCs returns. 01 July 2018–31 August 2018. The probability density functions of the distributions of daily returns for the analyzed cryptocurrencies with the following color code: BCH, BTC, DASH, ETC, ETH, LTC, REP, STR, XMR, XRP, ZEC. A normal distribution with the same mean and standard deviation as the returns on BTC is displayed as a histogram in the background. (https://github.com/QuantLet/CCID/tree/master/CCIDHistReturnsDensity)

Secondly, using GAM, we gain interesting insights into the trading activities in this 24/7 market. Cryptocurrencies are being traded without any forced break, as we know it from classic markets, for example, if the stock exchange closes for the night or especially for weekends. In addition to this fact, we have to consider, that there is no centralized trading in the act, but a plethora of service providers, so-called cryptocurrency exchanges. As we disclose the origin of our data, we underline, that caused by this very decentralized nature of cryptocurrency genesis and their respective trading, partially greatly diverging price data is available for each individual cryptocurrency. Again, this is caused by the decentralized root of individual, unsupervised and unregulated, places for exchange. There is no fixed price for BTC contrary to, for example, for exchange rates of USD-EUR.

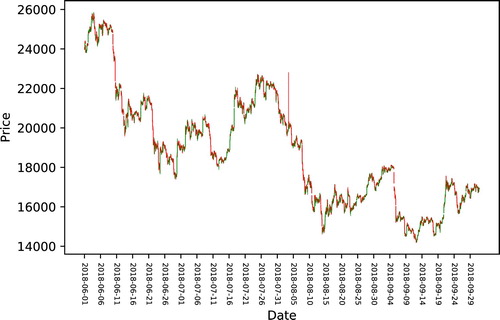

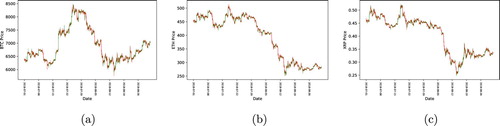

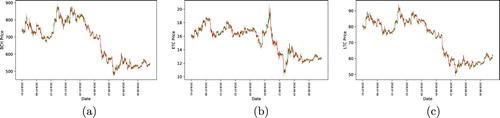

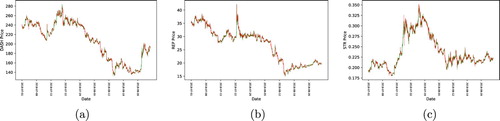

In contrast to the CRIX candlestick chart presented in Figure , where five minute high-frequency data is aggregated to 60 minutes, we present respective individual plots for each examined cryptocurrency, as shown in Figure to give an easier entry to understand this volatile market. Consistency between Figures , , and can be seen in the context of the findings in Chen et al., “What makes cryptocurrencies special,” (Citation2019), where the impact of sentiment on cryptocurrency prices is evident (with further references (Chen et al., “SONIC” Citation2019; Qian, Tu, and Härdle Citation2019). Furthermore, when recurring to the observable price structure of the Flash Crash of 2010 as well, we can see quite many jumps in these figures – a phenomenon also described in Chen et al., “Risk of Bitcoin Market,” (Citation2019) and Qian, Tu, and Härdle (Citation2019).

Figure 3. Candlestick chart of CRIX. 01 July 2018–29 September 2018. (https://github.com/QuantLet/CCID/tree/master/CCIDCandles)

Figure 4. Chandlestick charts for individual price movements. 01 July 2018–31 August 2018. (https://github.com/QuantLet/CCID/tree/master/CCIDCandles)

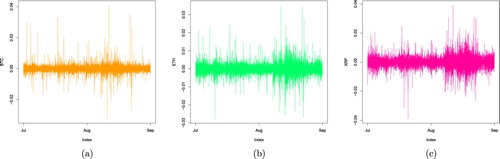

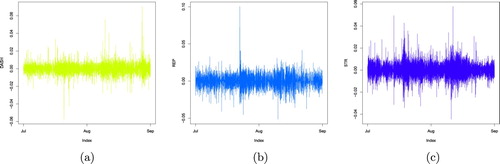

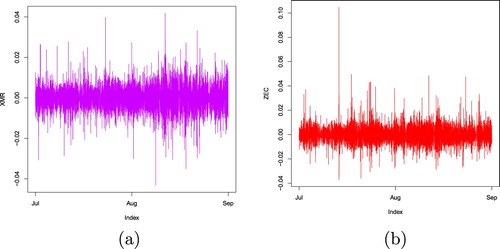

Figure , shows the intraday 5-minutes returns for the period from the 01 July 2018 to the 31 August 2018. As indicated, overall returns across the board are very extreme – a phenomenon generally unknown to classic financial markets. In addition, we can observe an extreme activity cluster around the second half of August. We can link this activity to increased media outlets regarding cryptocurrencies: the more investors flooded into this market, the higher the trading activity, fueled by sentiment, became – leading to partially absurd returns; positive as well as negative.

Figure 5. Intraday returns (5 min). 01 July 2018–31 August 2018. (https://github.com/QuantLet/CCID/tree/master/CCIDHistRet). (a) BTC, (b) ETH, (c) XRP.

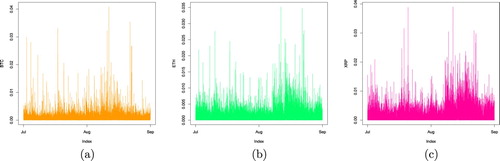

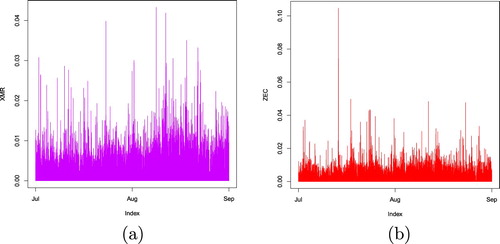

Figure adds to this finding, presenting the overall volatility from the beforehand stated period. As we can see, the return activity cluster in August from Figure is mirrored in the volatility activity cluster in Figure . Hence, we proof the beforehand stated claim of cryptocurrency activity being fueled by media outlets as well as sentiment, as being attested.

Figure 6. Intraday volatility. 01 July 2018–31. August 2018. (https://github.com/QuantLet/CCID/tree/master/CCIDHistVola). (a) BTC, (b) ETH, (c) XRP.

Table displays the estimated values of selected parameters for the cryptocurrency intraday trading for the given period of the 01 July 2018 to the 31 August 2018. The largest autocorrelation is for DASH (0.01), the smallest autocorrelation is for STR (−0.09).

Table 1. Estimated first-order autocorrelation of the returns,  , the squared returns, , and the absolute returns, , as well as the estimated skewness, , the estimated excess kurtosis, , and the Jarque-Bera test statistic, JB, with the respective, obviously very small, p-value for the overall summed intraday high-frequency data from the 01 July 2018 to the 31 August 2018. (https://github.com/QuantLet/CCID/tree/master/CCIDReturns).

, the squared returns, , and the absolute returns, , as well as the estimated skewness, , the estimated excess kurtosis, , and the Jarque-Bera test statistic, JB, with the respective, obviously very small, p-value for the overall summed intraday high-frequency data from the 01 July 2018 to the 31 August 2018. (https://github.com/QuantLet/CCID/tree/master/CCIDReturns).

While the first-order autocorrelation of the returns of all cryptocurrencies is all close to zero and mostly negative, the autocorrelations of the squared and absolute returns of all cryptocurrencies are positive and significantly larger than zero. Obviously, there is a linear relationship in the absolute and squared values of the chronologically sequential returns. Since the autocorrelation is positive, it can be concluded, that small absolute returns are followed sequentially by small absolute returns and large absolute returns are followed by large ones again. This means, that there are quiet periods with small price changes and dynamic periods with large oscillations.

Furthermore, whereas the estimate for skewness is mostly close to zero, except for BTC and ZEC, the estimate for excess kurtosis is in every case significantly larger than 3. The smallest estimated excess kurtosis is by STR (yet with an expressive of 8.12), and the largest by BTC (

). These values show, that the tested constituents are far from normally distributed. Negative skewness signals about increasing the downside risk and is a consequence of asymmetric volatility models. Positively skewed distributions have a longer right tail, meaning for investors a greater chance of extremely positive outcomes. A well-known stylized fact about returns distributions highlights their leptokurtic nature: they have more mass around the center and in the tails than a normal distribution. For example, Hussein (Citation2011) reports relatively high levels of kurtosis in stock data from the United States of America. This phenomenon is known as kurtosis risk.

The combined test of the normal distribution from Jarque and Bera (JB) can be derived as asymptotically distribution with two degrees of freedom. The last column in Table shows, that in all cases the normal distribution hypothesis is clearly rejected. This is above all caused by the value of kurtosis, which is significantly larger than 3, caused by a very frequent appearance of outliers in this new market. The higher kurtosis, compared to a normal distribution, proves that these extreme points result in leptokurtic distributions and are evidence of fat tails relative to the normal distribution's tail. However, as this asymmetry is common to financial markets, it is especially strong in the cryptocurrency markets with potentially extreme returns and a very pronounced volatility.

The following tables, respectively, show the individual correlation to CRIX, if the market is acting positively, Table , or negatively, Table . Extensive care should be put on our main actors – BTC, ETH and XRP – when studying these. As these enjoy a large market acceptance and hence are long-term drivers of the cryptocurrency market, we can once again, underline our findings given beforehand.

Table 2. Pairwise cryptocurrency correlations of returns for positive market-movement days, as defined by returns on CRIX. 01 July 2018–31 August 2018 (https://github.com/QuantLet/CCID/tree/master/CCIDcorr).

Table 3. Pairwise cryptocurrency correlations of returns for negative market-movement days, as defined by returns on CRIX. 01 July 2018–31 August 2018 (https://github.com/QuantLet/CCID/tree/master/CCIDcorr).

On a side note, Tables and show that among the top 11 cryptocurrencies, most pairs exhibit low return correlations, what suggest strong diversification benefits in a portfolio, especially outside the major cryptocurrencies presented, see also Petukhina et al. (Citation2020).

We can observe, that the correlation to CRIX in both tables presents itself as clustered around well-known cryptocurrencies, namely BTC, ETH, XRP, as well as BCH, and ETC. Therefore, this activity can be interpreted in a way, which indicates these constituents as the market drivers. This finding also correlates with the long-term trading activity registered on many online sources for these coins. We should note, without going into detail, that LTC and BCH are closely related to BTC, and that ETC is closely tied to the history of ETH. XRP itself was able to carve out its very specific niche early enough for certain applications, especially in the banking sector – in contrast, BTC can be seen as the genesis of digital currency without any intrinsic value, whereas the ETH system enables many different applications, majorly through so-called ‘smart contracts’.

3.3. Time-of-day effects and proof-of-human

To support our hypothesis of mostly dealing with human agent initiated trades, which we coin as PoH, we present our findings regarding the time-of-day trading in this section. Additional material on information arrival, news sentiment, volatilities and jumps of intraday returns can also be taken from Qian, Tu, and Härdle (Citation2019).

Cryptocurrency exchanges, as introduced in Section 2, are often designed to serve a certain target group, for example by emphasizing compliance with national regulatory frameworks. By plotting the trade volume against the timestamps, we can also observe certain properties of market activity and draw coherent conclusions to the origin of the market participants: are these mostly human, who are doing trades by hand, or are we looking at a well oiled automatic machinery full of algorithms – just as commonly portrayed. Keep in mind, as mentioned in Section 2, that our data are gained from Europe-based sources, and taken from periods that are overwhelmingly identifiable by corporate staff vacations. One should hence expect a less pronounced human, but algorithmic-driven market behavior to contradict our hypotheses.

To underline this argument, it is useful to imagine a transitional system, whereas human interference is completely removed or not relevant to a market system (e.g. Caporale et al. Citation2016), and where the trading pattern will, therefore, be independent of the time-of-day effects:

With increasing market participation of algorithms, we expect, for example, nighttime to have a negligible impact on the market activity. In contrast, we expect nighttime to have an impact on market activity if the market is dominated by human interaction.

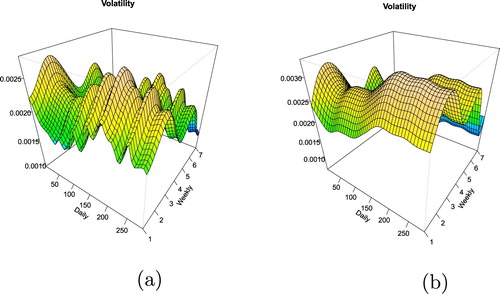

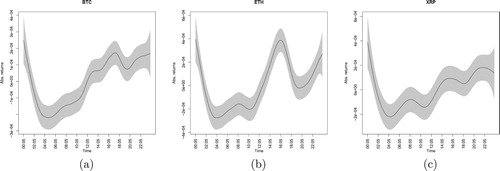

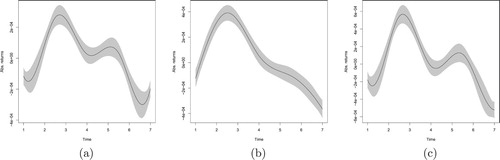

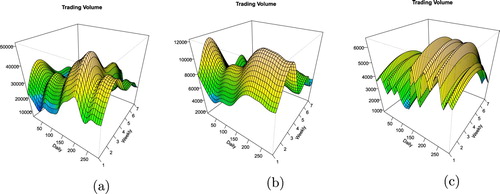

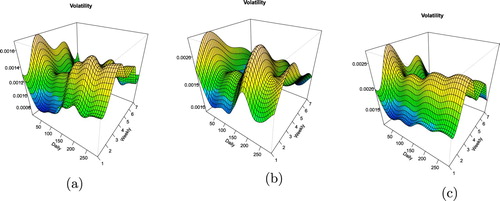

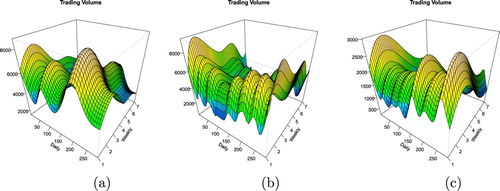

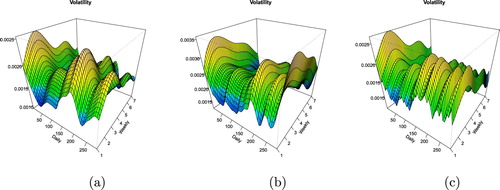

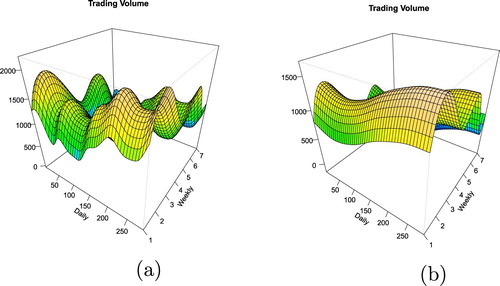

The following figures employ GAM to observe daily and weekly patterns for intraday volatility and trading volume. For daily seasonality cubic regression splines, for weekly seasonality P-splines are used, and a number of knots are logically set to the number of unique values, i.e 62 for daily patterns and 7 for weekly. The summary statistics of GAM for all cryptocurrencies demonstrate a high significance of smooth terms combined with a quite low explanatory power (coefficients of determination are around 1%). Nevertheless, we can observe distinct intraday seasonality patterns.

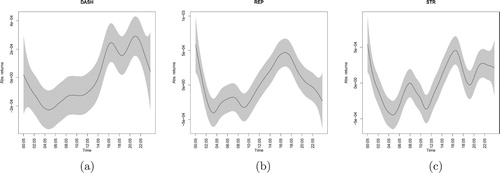

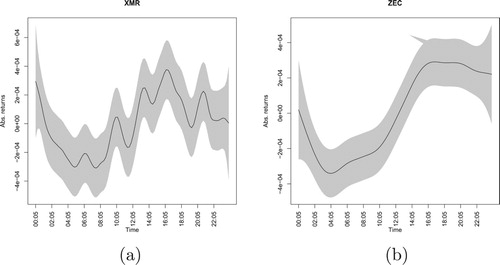

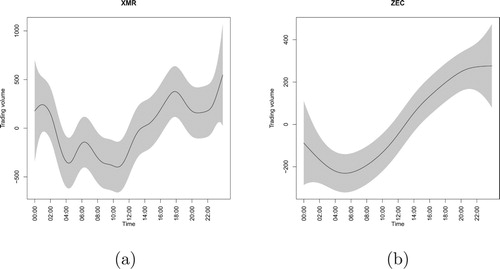

Assuming that the majority of employed persons do work from 09:00 to 17:00 o'clock in Europe, Figures and (data time is +1 GMT) present us with a very clear picture of returns and volume. Characteristic human activity curves are presented by Figure showing the daily seasonality – a curve driven by algorithms as the main actor, or Artificial Intelligence in a FinTech startup buzzword context, should not present such a comparatively extreme low around a typical time for the majority of humans to be asleep. Following that point, the curves expresse a significant growth, only to flat out again around lunch break time. Most figures present a peak between 17:00 and 20:00 o'clock, just when most people finish their daily routine jobs, followed by an expressive decline of the curves. This is surprising, as media outlets and startup marketing generally praise the non-stop availability and easy access to cryptocurrency exchanges, and hence we would presume to see a curve different to that of a ‘routine’-job. Further adding to this argument of trading being mostly done by humans organized in cooperations (regarding Figure with the seven numbers indicating the days of the week), is research on anomalies such as the ‘Monday Effect’ applied to our findings (e.g. Cross Citation1973; Basher and Sadorsky Citation2006). By applying both parametric and nonparametric methods, Caporale and Plastun (Citation2019) find abnormal returns for no other cryptocurrency than BTC, and that only on Mondays – yet, in Figure we can observe that weekly absolute returns across cryptocurrencies reach their peak only in the period from Tuesdays to around Thursdays, with a steep decline in activity during the weekends.

Figure 7. Daily seasonality: fit of Generalized Additive Model (5 min nodes) with cubic regression splines for absolute returns of cryptocurrencies (shaded regions represent confidence bands for smooths), 01 July 2018–31 August 2018. (https://github.com/QuantLet/CCID/tree/master/CCIDvolaGAM). (a) BTC, (b) ETH, (c) XRP.

Figure 8. Weekly seasonality: fit of Generalized Additive Model with p-splines for absolute returns of cryptocurrencies (shaded regions represent confidence bands for smooths), 01 July 2018–31 August 2018. (https://github.com/QuantLet/CCID/tree/master/CCIDvolaGAM). (a) BTC, (b) ETH, (c) XRP.

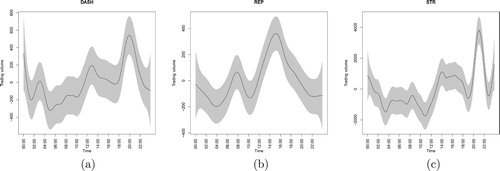

Figure presents us a respective lower trading volume during the weekends, compared to for example Thursdays or especially Fridays. Similar results can be seen in Figure , presenting us with low volatility on the cryptocurrency market at said times – one assumption from this could be taken from the immense influx of financially potent startups organized as cooperations in this emerging market (c.f. Benedetti and Kostovetsky Citation2018). Yet, we can see that human interaction is shaping how the market behaves during the given time frames. Trade limited to regular working hours and days in Europe leads to the conclusion, that the majority of trades are not done by algorithms, which are active 24/7, but by human agents themselves making transactions and orders individually and by hand. This is especially obvious through Figure , which is presenting a much lower activity pattern observable during the weekends. Should algorithms really be the drivers in this, technically predestined, fully digitized market, then this curve should not drop off as observable on Saturdays and Sundays. These findings are similar across the board (see appendix A.2–A.4). While there is a plethora of well working, open-source trading bots available for these markets, for example via Github (Nevskii Citation2019), as well as an abundance of commercially available trading bots (Norry Citation2020), the trust in these – or the knowledge of how to employ them in this emerging market – is certainly low. This is especially surprising, as the possibility for arbitrage or mean reversion is obvious with multiple exchanges trading the same assets each with individually different prices, see Section 3. The inherent possibility to take advantage of this inefficiency of the distributed trading, with near-simultaneous transactions, leads to great opportunities for traders unseen in most traditional markets for most assets. Hence we can assume, as algorithms need humans to get deployed and take action, like reacting to price changes, that the overall impact of these is not significant, if not negligible at all.

Figure 9. Daily and weekly seasonality: fit of Generalized Additive Model with cubic and p-splines for trading volume of cryptocurrencies (5 min nodes), 01 July 2018–31 August 2018. (https://github.com/QuantLet/CCID/tree/master/CCIDvolumeGAM). (a) BTC, (b) ETH, (c) XRP.

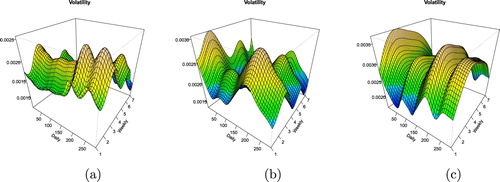

Figure 10. Daily and weekly seasonality: fit of Generalized Additive Model with cubic and p-splines for volatility of cryptocurrencies (5 min nodes), 01 July 2018–31 August 2018. (https://github.com/QuantLet/CCID/tree/master/CCIDvolaGAM). (a) BTC, (b) ETH, (c) XRP.

In total we can observe, that the activity patterns displayed in this market not only tend to express human interaction but also corporate structures as well, as most trading is done Mondays to Fridays, with the weekends expressing a low intensity of trades taking place. The previously mentioned immense increase of financially potent FinTech entities have attracted absurd amounts of financial backing compared to the output delivered via initial coin offerings, ICOs for short (c.f. Benedetti and Kostovetsky Citation2018; Zetzsche et al. Citation2019). To enable new industries using the blockchain technology, startups and commercial companies have been launching ICOs, similar to the initial public offerings (IPOs) of companies, to sell tokens in a transparent and decentralized manner and therefore creating a new method of raising funds without intermediaries, like traditional financial institutes. Some of these tokens are pegged to other (monetary) systems or even cryptocurrency constructions directly, as these have already gained a high market acceptance – especially the Ethereum ecosystem is facilitating this by providing excessive tools and documentaries, paired with a focused and growing community of developers, to create what they coined as ‘coloured coins’ in order to expand the utility of the existing blockchain (Walters Citation2018). Besides the fact, that the legality of ICOs is disputed and potential responses from regulatory agencies are growing to be imminent, ICOs enable anyone within the community to participate in the investment, providing opportunities for small-scale investors. Hence the assumption would be, that especially these specialized corporate startups are working on their backend and maintain their ecosystem, whilst being active drivers of trading in this market – yet predominantly human ones.

Coming back to the 2010 Flash Crash mentioned in the introduction of this paper, one could argue, that such a flash crash is not possible due to the delay that is inherent to blockchains – the so-called blocktime (Härdle, Harvey, and Reule Citation2020). However, as research has shown, it is easily possible to derive sentiment and therefore market reactions from Twitter, Facebook, Stocktwits, or similar public forums. As most activity can be seen on the respective cryptocurrency exchanges, where the order books are not handled on-chain, but necessarily off-chain to quickly process the exchange users trading requests (Chen et al., “What makes cryptocurrencies special,” Citation2019; Chen et al., “SONIC” Citation2019; Qian, Tu, and Härdle Citation2019). Therefore a crash related to certain cryptocurrency prices may be seen only after the respective information has been seeded into the network and accepted as new information to the individual blockchain. This is creating an inherent risk, as market behavior can not be seen by only relying on-chain data to predict certain price movements. The previously mentioned ‘learning’ algorithms could therefore be, if they are employed in this manner, be dangerous if a ‘false-postive’ is identified and results in a respective process leading to dumping a certain asset, which in turn could then generate a waterfall when other algorithms, that respond to blockchain price data, reply to this movement (Zinovyeva, Härdle, and Lessmann Citation2019). Hence, a grand scale application of algorithms needs to be finely tuned in order to avoid any humanely unforeseeable, but technically feasible, consequences.

With the cryptocurrency market being easy to join and to actively participate in, financial traders are becoming redundant – unless they provide specialized services. Making many transactions does not cost time to interact with a trader and money to pay this person, as one can do that by hand at home with very low transaction costs. This said, there is a big competition going on between the exchanges, who themselves may act as traders or brokers. The future has to tell if through this competition the rise of the machines and the respective mass employment of algorithmic trading in this digital realm will become reality.

4. Closing remarks

We have shown, that meanwhile there are certainly grand-scale employers of algorithmic trading around in this new emerging market of cryptocurrencies, yet, based on the time-of-day effects and the evidence gained, we can conclude, that the impact of 24/7 algorithmic trading is rather negligible given the empirical facts we have at hand. This leads us to the conclusion, that even though this new digital market appears predestined to be ruled by algorithms and specialized AI advisors, the digital realm of cryptocurrencies has yet to be conquered by the machines and is still firmly in the hands of humans or generally driven by respective startup's.

Further research should certainly step into this breach, that we have proven to be existent, and create means on how to best exploit this open ground on a market-oriented basis, as well as on an individual level, say in regards to the exchanges. Necessarily, such research not only needs to be of quantitative or technical origin but also needs to include a regulatory point of view, as especially this field on blockchain research is more and more characterized by its evident interdisciplinary nature.

Acknowledgement

We acknowledge support by the Open Access Publication Fund of Humboldt-Universität zu Berlin.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Related Research Data

References

- Akhtaruzzaman, Md., A. Sensoy, and S. Corbet. 2019. “The Influence of Bitcoin on Portfolio Diversification and Design.” Finance Research Letters. doi:10.1016/j.frl.2019.101344.

- Basher, S. A., and P. Sadorsky. 2006. “Day-of-the-week Effects in Emerging Stock Markets.” Applied Economics Letters 13 (10): 621–628.

- Benedetti, H., and L. Kostovetsky. 2018. “Digital Tulips? Returns to Investors in Initial Coin Offerings.” SSRN. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3182169 (Retrieved 12 February 2020).

- Borke, L., and W. Härdle. 2018. “Q3-D3-LSA: D3.js and Generalized Vector Space Models for Statistical Computing.” In Handbook of Big Data Analytics, edited by H. Lu, X. Shen, and W. Härdle, 377–424. Berlin, HL; Springer-Verlag. ISBN 978-3-319-18284-1, doi:10.1007/978-3-319-18284-1.

- Caporale, G. M., and A. Plastun. 2019. “The Day of the Week Effect in the Cryptocurrency Market.” Finance Research Letters 31.

- Caporale, G. M., A. Plastun, L. Gil-Alana, A. Plastun, and I. Makarenko. 2016. “Intraday Anomalies and Market Efficiency: A Trading Robot Analysis.” Computational Economics 47: 275–295.

- Chen, C. Y., R. Despres, L. Guo, and T. Renault. 2019. “What makes cryptocurrencies special? Investor sentiment and return predictability during the bubble.” IRTG 1792 Discussion Paper. ISSN: 2568-5619. Forthcoming. https://www.wiwi.hu-berlin.de/de/forschung/irtg/results/discussion-papers/discussion-papers-2017-1/irtg1792dp2019-016.pdf.

- Chen, C. Y., R. Despres, L. Guo, T. Renault, W. K. Härdle, and Y. Klochkov. 2019. “SONIC: SOcial Network with Influencers and Communities.” IRTG 1792 Discussion Paper. ISSN: 2568-5619. Forthcoming. https://www.wiwi.hu-berlin.de/de/forschung/irtg/results/discussion-papers/discussion-papers-2017-1/irtg1792dp2019-025.pdf.

- Chen, C. Y., R. Despres, L. Guo, T. Renault, W. Kuo, L. Guo, and W. K. Härdle. 2019. “Risk of Bitcoin Market: Volatility, Jumps, and Forecasts.” IRTG 1792 Discussion Paper. ISSN: 2568-5619. Forthcoming. https://www.wiwi.hu-berlin.de/de/forschung/irtg/results/discussion-papers/discussion-papers-2017-1/irtg1792dp2019-024.pdf.

- Cross, F. 1973. “The Behavior of Stock Prices on Fridays and Mondays.” Financial Analysts Journal 29 (6): 67–69

- Emem, M. 2018. “Wall Street Shenanigans: Rampant Trading Bots are Exploiting Crypto Exchanges.” CNN. Retrieved on the 28.06.2019 from https://www.ccn.com/trading-bots-exploit-crypto-exchanges-dex/.

- Härdle, W. 1990. Applied Nonparametric Regression. Cambridge, New York, Melbourne: Cambridge University Press.

- Härdle, W. K., C. R. Harvey, and R. C. G. Reule. 2020. “Understanding Cryptocurrencies.” Journal of Financial Econometrics 18 (2): 181–208. doi:10.1093/jjfinec/nbz033.

- Hautsch, N. 2011. Econometrics of Financial High-Frequency Data. Springer.

- Hussein, S. 2011. “The Intraday Behaviour of Bid-Ask Spreads, Trading Volume and Return Volatility: Evidence from DAX30.” International Journal of Economics and Finance 3 (1): 23–34. http://www.ccsenet.org/journal/index.php/ijef/article/download/7973/6606.

- Nevskii. 2019. “Crypto trading bots review 2019.” Medium. https://medium.com/@vladnevskii/crypto-trading-bots-review-2018-312cf3e8145c (Retrieved 25 June 2019).

- Norry, A. 2020. “Beginner's Guide to Bitcoin & Crypto Trading Bots.” Blockonomi. Retrieved on the 12.02.2020 from https://blockonomi.com/bitcoin-trading-bots/.

- Petukhina, A., S. Trimborn, W. Härdle, and H. Elendner. 2020. “Investing With Cryptocurrencies – Evaluating the Potential of Portfolio Allocation Strategies.” Quantitative Finance, submitted, RR 20200320.

- Platanakis, E., and A. Urquhart. 2019. “Should Investors Include Bitcoin in Their Portfolios? a Portfolio Theory Approach.” The British Accounting Review. doi:10.2139/ssrn.3215321.

- Qian, Y., J. Tu, and W. Härdle. 2019. “Information Arrival, News Sentiment, Volatilities and Jumps of Intraday Returns.” IRTG 1792 Discussion Paper. ISSN: 2568-5619. Forthcoming. https://www.wiwi.hu-berlin.de/de/forschung/irtg/results/discussion-papers/discussion-papers-2017-1/irtg1792dp2019-002.pdf.

- Röschli, K., L. Vetter, W. Breymann, J. Osterrieder, J. Chu, S. Nadarajah, and S. Chan. 2017. Stylized Facts of Cryptourrencies. Technical Report, Zurich University of Applied Sciences/ZHAW.

- Schnaubelt, M., J. Rende, and C. Krauss. 2019. “Testing Stylized Facts of Bitcoin Limit Order Books.” Journal of Risk and Financial Management 12 (1): 25. doi: 10.3390/jrfm12010025.

- Trimborn, S., and W. Härdle. 2018. “CRIX An Index for Cryptocurrencies.” Journal of Empirical Finance 49 (December): 107–122. doi:10.1016/j.jempfin.2018.08.004.

- Trimborn, S., W. Härdle, M. Li, and W. K. Härdle. 2018. “Investing with Cryptocurrencies – A Liquidity Constrained Investment Approach.” Published version: Trimborn, S., M. Li, and W. K. Härdle. 2019. “Investing with Cryptocurrencies – A Liquidity Constrained Investment Approach.” Journal of Financial Econometrics. doi:10.1093/jjfinec/nbz016.

- Walters, S. 2018. “What are Colored Coins? The Ultimate Guide.” Unblock. https://unblock.net/what-are-colored-coins/ (Retrieved 13 February 2020).

- Wand, Matt P. 2017. “Fast Approximate Inference for Arbitrarily Large Semiparametric Regression Models Via Message Passing.” Journal of the American Statistical Association 112 (517): 137–168.

- Wood, S. 2004. “Stable and Efficient Multiple Smoothing Parameter Estimation for Generalized Additive Models.” Journal of the American Statistical Association 99 (467): 673–686.

- Wood, S. 2011. “Fast Stable Restricted Maximum Likelihood and Marginal Likelihood Estimation of Semiparametric Generalized Linear Models.” Journal of the Royal Statistical Society: Series B (Statistical Methodology) 73 (1): 3–36.

- Wood, Simon N. 2017. Generalized Additive Models: An Introduction with R, Second Edition. CRC Press. https://www.routledge.com/Generalized-Additive-Models-An-Introduction-with-R-Second-Edition/Wood/p/book/9781498728331.

- Wood, S. 2019. “gam.models.” RDocumentation. https://www.rdocumentation.org/packages/mgcv/versions/1.8-31/topics/gam.models (Retrieved 17 February 2020).

- Wood, Simon N., Yannig Goude, and Simon Shaw. 2015. “Generalized Additive Models for Large Data Sets.” Journal of the Royal Statistical Society: Series C (Applied Statistics) 64 (1): 139–155.

- Zetzsche, D. A., R. P. Buckley, D. Arner, and L. Föhr. 2019. “The ICO Gold Rush: It's a Scam, It's a Bubble, It's a Super Challenge for Regulators.” Harvard International Law Journal 63 (2): 275–295.

- Zhang, Y., S. Chan, J. Chu, and S. Nadarajah. 2019. “Stylised Facts for High Frequency Cryptocurrency Data.” Physica A 513 (C): 598–612.

- Zhang, W., P. Wang, X. Li, and D. Shen. 2018. “Some Stylized Facts of the Cryptocurrency Market.” Applied Economics 50 (55): 5950–5965.

- Zinovyeva, E., W. K. Härdle, and S. Lessmann. 2019. “Antisocial Online Behavior Detection Using Deep Learning.” IRTG 1792 Discussion Paper. ISSN: 2568-5619. Forthcoming. https://www.wiwi.hu-berlin.de/de/forschung/irtg/results/discussion-papers/discussion-papers-2017-1/irtg1792dp2019-029.pdf.

Appendix

A.1. List of cryptocurrencies in this research

A.2. Statistics for BCH, ETC and LTC

Figure A.1. Candlestick charts for individual price movements. 01 July 2018–31 August 2018. (https://github.com/QuantLet/CCID/tree/master/CCIDCandles). (a) BCH, (b) ETC, (c) LTC.

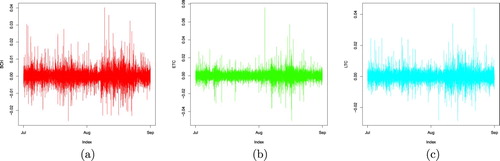

Figure A.2. Intraday 5-minutes log-returns. 01 July 2018–31 August 2018. (http://github.com/QuantLet/CCID). (a) BCH, (b) ETC, (c) LTC.

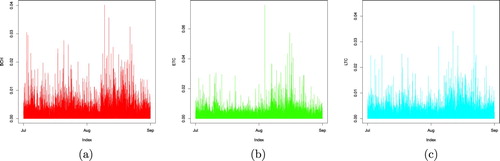

Figure A.3. Intraday volatility (absolute values of 5-minutes log-returns). 01 July 2018–31 August 2018. (https://github.com/QuantLet/CCID/tree/master/CCIDHistRet). (a) BCH, (b) ETC, (c) LTC.

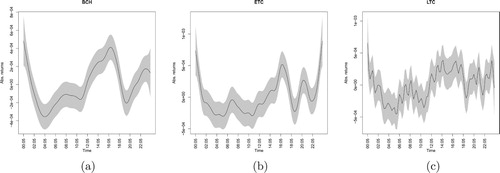

Figure A.4. Generalized additive model of volatility. 01 July 2018–31 August 2018. (https://github.com/QuantLet/CCID/tree/master/CCIDvolaGAM). (a) BCH, (b) ETC, (c) LTC.

Figure A.5. Generalized Additive Model of trading volume of cryptocurrencies. 01 July 2018–31. August 2018. (https://github.com/QuantLet/CCID/tree/master/CCIDvolumeGAM). (a) BCH, (b) ETC, (c) LTC.

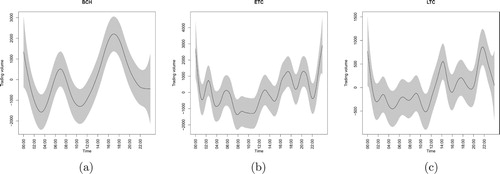

Figure A.6. Daily and weekly seasonality: fit of Generalized Additive Model with cubic and p-splines for trading volume of cryptocurrencies (5 min nodes), 01 July 2018–31 August 2018. (https://github.com/QuantLet/CCID/tree/master/CCIDvolumeGAM). (a) BCH, (b) ETC, (c) LTC.

Figure A.7. Daily and weekly seasonality: fit of Generalized Additive Model with cubic and p-splines for volatility of cryptocurrencies (5 min nodes), 01 July 2018–31 August 2018. (https://github.com/QuantLet/CCID/tree/master/CCIDvolaGAM). (a) BCH, (b) ETC, (c) LTC.

A.3. Statistics for DASH, REP and STR

Figure A.8. Candlestick charts for individual price movements (60-minutes intervals). 01 July 2018–31 August 2018. (https://github.com/QuantLet/CCID/tree/master/CCIDCandles). (a) DASH, (b) REP, (c) STR.

Figure A.9. Intraday log-returns (5-minutes). 01 July 2018–31 August 2018. (https://github.com/QuantLet/CCID/tree/master/CCIDHistRet). (a) DASH, (b) REP, (c) STR.

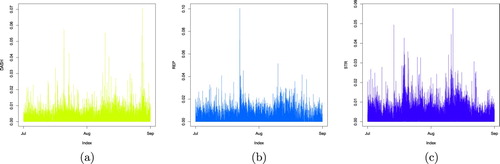

Figure A.10. Intraday volatility (absolute 5-minutes log-returns). 01 July 2018–31 August 2018. (https://github.com/QuantLet/CCID/tree/master/CCIDHistVola). (a) DASH, (b) REP, (c) STR.

Figure A.11. Generalized Additive Model of volatility of cryptocurrencies. 01 July 2018–31 August 2018. (https://github.com/QuantLet/CCID/tree/master/CCIDvolaGAM). (a) DASH, (b) REP, (c) STR.

Figure A.12. Generalized Additive Model of intraday trading volume of cryptocurrencies. 01 July 2018–31 August 2018. (https://github.com/QuantLet/CCID/tree/master/CCIDvolumeGAM). (a) DASH, (b) REP, (c) STR.

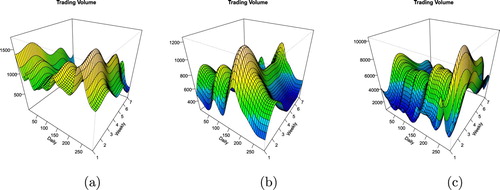

Figure A.13. Daily and weekly seasonality: fit of Generalized Additive Model with cubic and p-splines for trading volume of cryptocurrencies (5 min nodes), 01 July 2018–31 August 2018. (https://github.com/QuantLet/CCID/tree/master/CCIDvolumeGAM). (a) DASH, (b) REP, (c) STR.

Figure A.14. Daily and weekly seasonality: fit of Generalized Additive Model with cubic and p-splines for volatility of cryptocurrencies (5 min nodes), 01 July 2018–31 August 2018. (https://github.com/QuantLet/CCID/tree/master/CCIDvolaGAM). (a) DASH, (b) REP, (c) STR.

A.4. Statistics for XMR and ZEC

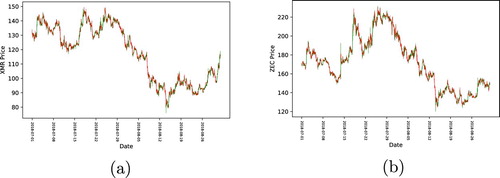

Figure A.15. Chandlestick charts for individual price movements. 01 July 2018–31 August 2018. (https://github.com/QuantLet/CCID/tree/master/CCIDCandles). (a) XMR, (b) ZEC.

Figure A.16. Intraday 5-minutes log-returns. 01 July 2018–31 August 2018. (https://github.com/QuantLet/CCID/tree/master/CCIDHistRet). (a) XMR, (b) ZEC.

Figure A.17. Intraday volatility. 01 July 2018–31 August 2018. (https://github.com/QuantLet/CCID/tree/master/CCIDHistRet). (a) XMR, (b) ZEC.

Figure A.18. Generalized Additive Model of volatility of cryptocurrencies. 01 July 2018–31 August 2018. (https://github.com/QuantLet/CCID/tree/master/CCIDvolaGAM). (a) XMR, (b) ZEC.

Figure A.19. Generalized Additive Model of the 62 intraday trading volume of cryptocurrencies. 01 July 2018–31 August 2018. (https://github.com/QuantLet/CCID/tree/master/CCIDvolumeGAM). (a) XMR, (b) ZEC.

Figure A.20. Daily and weekly seasonality: fit of Generalized Additive Model with cubic and p-splines for trading volume of cryptocurrencies (5 min nodes), 01 July 2018–31 August 2018. (https://github.com/QuantLet/CCID/tree/master/CCIDvolumeGAM). (a) XMR, (b) ZEC.

Figure A.21. Daily and weekly seasonality: fit of Generalized Additive Model with cubic and p-splines for volatility of cryptocurrencies (5 min nodes), 01 July 2018–31 August 2018. (https://github.com/QuantLet/CCID/tree/master/CCIDvolaGAM). (a) XMR, (b) ZEC.